Embed Size (px)

Citation preview

Report No. 1769-GH

Ghana FILEAgricultural Sector Review(In Three Volumes)

Volume III (Annexes VI-XI)

April 12, 1978Western Africa Country Programs I

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by iecipientsonly in the performance of their official duties. Its contents may nototherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

US$1 = ¢1.15

¢1 = US$0.87

ABBREVIATIONS

ADB Agricultural Development BankCDB Cotton Development BoardCMB Cocoa Marketing BoardCPD Cocoa'Production Division.CRI Crop Research InstituteCRIG Cocoa Research Institute of GhanaCSIR Council for Scientific and Industrial

ResearchFDC Food Distribution CorporationFLO Farm Loan OfficeFPC Food Production CorporationGDB Grains and Legumes Development BoardGFC Ghana Fertilizer CompanyGGADP Ghanaian-German Agricultural Development

ProjectGHA Ghana Highway AuthorityGHOC Ghana Industrial Holding CompanyGNPA Ghana National Procurement AgencyGWC Grains Warehousing CompanyICCO International Cocoa OrganizationMCA Ministry of Cocoa AffairsMOA Ministry of AgricultureNIB National Investment BankRMU Rice Mills UnitSFC State Farms CorporationSRI Soil Research Institute

This report is based on the findings of a mission which visitedGhana in February/March 1977. The mission comprised Messrs. Hendrik T.Koppen, Paul S. Zuckerman, Walter Kock (RMWA), Thakoor Persaud andMrs. Bruna Vitagliano of the Bank and Messrs. Peter Calkin and LawrenceCockcroft (consultants).

?

FOR OFFICIAL USE ONLY

LIST OF ANNEXES

ANNEX VI: AGRICULTURAL CREDIT

'\NNEX VII: PRICE AND SUBSIDY POLICIES

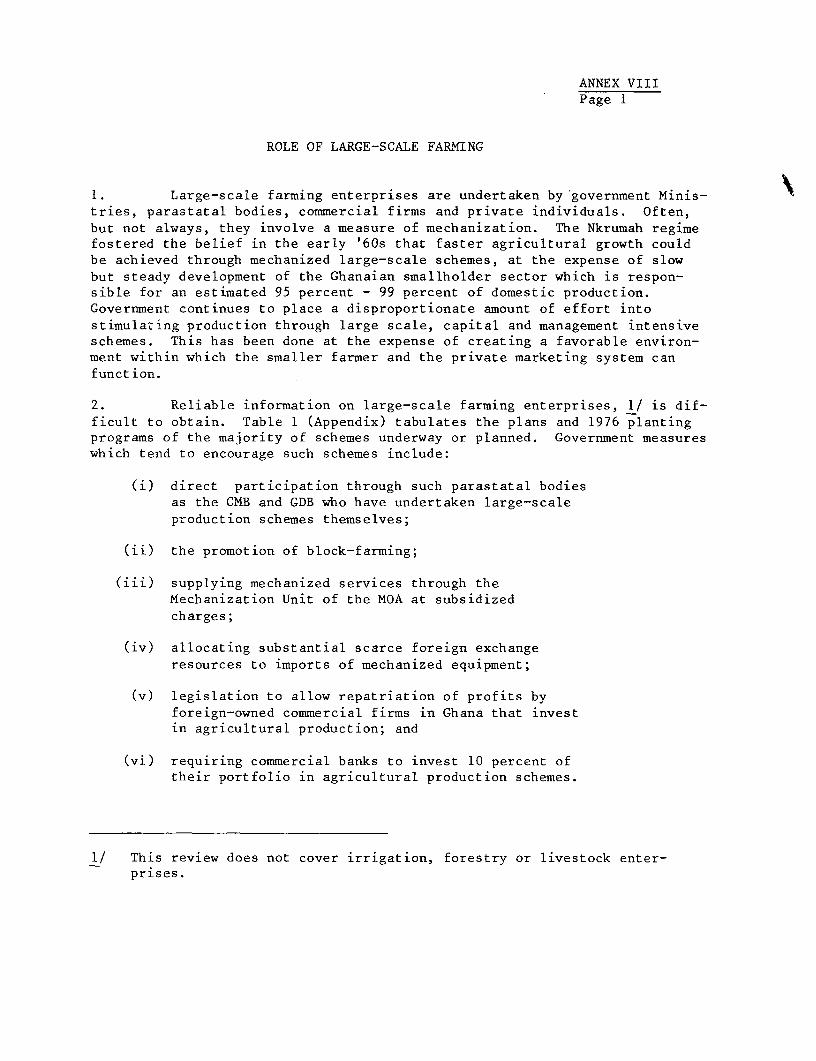

ANNI.X VIII: ROLE OF LARGE-SCALE FARMING

ANNEX IX: MANPOWER AND THE AGRICULTURAL LABOR FORCE

ANNEX X: AGRICULTURAL RESEARCH

ANNEX XI: AGRICULTURAL PROCESSING

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

I

I

ANNEX VIPage 1

AGRICULTURAL CREDIT

SUMMARY AND CONCLUSIONS

General

(i) Government's agricultural credit policy pursued so far reflects astrategy which emphasizes mechanization of large farms as a means of increas-ing agricultural production more rapidly, while tending to neglect the smallfarmer sector. As a result, the number of large farms has increased con-sistently in the last years. These farms have contributed little to growthof production, however, due to inefficient operation. To overcome the acutefood shortage the country is currently experiencing, additional output hasmainly to come from small farmers, who account for 80 percent of the nationalproduction of foodcrops.

(ii) Increasing small farmer output requires purchase of improved inputsand adoption of new technologies. Increased flows of production credit willtherefore be needed by the small farmers. It is, however, crucial that creditis integrated with other development services. Credit is only part of a pack-

age of inputs and services necessary to improve farmer productivity. Timelyprovision of inputs such as seeds, fertilizers, availability of storage facil-ities, market outlets, extension services, and a realistic price policy areall important prerequisites to credit operation.

Institutional Coverage

(iii) Agricultural credit is provided in Ghana by the Agricultural Devel-opment B.nk (ADB), the three major commercial banks, and the National In-vestment Bank. Total credit to agriculture outstanding in 1975 amounted to0112,799. Less than 10 percent of the estimated 850,000 farmers in Ghanareceive institutional credit. Around 700,000 farmers have farms of 10 acresor less. Only 20 percent of the available institutional credit goes to them.ADB, which is virtually the only institution currently providing credit to thesmall farmers, has 14 branches and 8 Farmers Loan Offices (FLO) spread aroundthe country to service them. A farmer must sometimes travel up to 100 milesto file a loan application with ADB. Limited outreach in rural areas, inade-quacy of services offered, shortage of trained staff and limited resourcesare the main constraints of the current institutional set-up.

(iv) The local authorities are aware of the need to provide betteraccess to credit for small farmers and are beginning to experiment with newways to tackle the situation (enlargement of ADB's network and streamliningof its operations, rural banks, etc.). While experimentation is welcome,the importance of close coordination between the various institutions con-cerned in planning and implementing the various programs cannot be over-emphasized. It appears, instead, that little coordination exists in theeffort currently undertaken to expand the existing institutional networkand there is a risk of overlapping of activities in the field of credit andinput supply. A clear strategy for the development of agricultural creditthat takes into account the needs, potentials of its beneficiaries, and thelimitations of the available resources in terms of funds, staff, etc., is

ANNEX VIPage 2

an essential prerequisite for the success of any credit policy. Because ofits active involvement in the promotion of credit to agriculture and its

more qualified staff, Bank of Ghana appears to be today the institutionwhich could best perform this task, in coordination with Government depart-ments and credit agencies.

Staff

(v) An expansion of the credit institutions will increase the demandfor qualified and trained staff, thus making more acute the existing short-age in this field. Solving the staff problem is first priority in Ghana.Some arrangements are being made to overcome the problem -- ADB's trainingschool set up at the Tema branch, BOG's training to commercial banks staffenvisaged under the Fondo Scheme -- but there is still need for more train-ing programs. The Bank has provided technical assistance to ADB under sev-eral agricultural projects. Strengthening of ADB regional branches throughthe provision of an experienced loan officer is also included in the UpperRegion Agricultural Development Project and in the preparation report forthe Volta Region Agricultural Development Project. The Bank should intensifyits efforts to strengthen ADB for the following reasons: (a) ADB is the mostimportant source of institutional credit to agriculture in Ghana; (b) theGovernment is fully committed to the concept of an Agricultural DevelopmentBank. This is evident from Government financial support and from ADB's in-volvement in several large development schemes. Loan processing and train-ing of project staff are the areas in which the Bank could provide a valuableassistance to ADB.

Funds

(vi) Limited availability of funds is another constraint to the exten-sion of credit institutions. ADB depends greatly on the capital made avail-able by the Government. Given the present stringent monetary situation, ADBcannot count on substantial increases in the provision of government funds.The Bank might consider establishing a line of credit with ADB for on lendingto farmers. Besides alleviating the institution's financial constraints itwould help strengthen its credit management practices. Before consideringthe provision of an agricultural credit to ADB the Bank would, however, needto make sure that arrears have been reduced to an acceptable level. Therecently established rural banks could play an important role in the mobil-ization of savings and capital formation in the rural areas.

Interest Rate

(vii) Interest rates in agriculture range from 8.5 percent to 12.5 percentaccording to the type of credit (Table 15). 1/ ADB's loans for food andindustrial crops (except sugarcane), as well as livestock and commercial banksloans under the credit guarantee scheme bear a mandatory interest rate of 8.5

1/ 12.5 percent is the ceiling for general lending in Ghana.

ANNEX VIPage 3

percent. Both these types of loans represent the bulk of lending to the

agriculture sector. The low interest rate, originally set to help the smallfarmers, in practice benefits mostly the larger ones who have easier accessto credit facilities and receive larger loans. It also encourages capitalintensive investment. The low interest rate policy contrasts with the higheradministrative cost of lending to small farmers. In addition, repaymentperformance of Ghanaian farmers (large and small) is typically poor and this

adds to the cost of lending.

(viii) The fact that non-institutional money lenders, who still representa substantial source of small farmer financing,are able to charge interestrates as high as 50 percent and in some cases even 100 percent, indicates thatthe borrowers are willing to pay higher interest rates in exchange of promptavailability of credit. Another consideration in favor of the increaseof interest rate is that it represents in any case a small proportion offarm expenditures. There are, however, several problems related to an in-crease of lending rates in agriculture. Lending conditions as a whole arequite unrealistic in the high inflationary situation currently prevailing inGhana (with inflation running higher than 60 percent, on a yearly basis). Acorrection of the interest rate for agriculture alone can have distortingeffects on the economy. The problem for agriculture has, therefore, to besolved in the context of a policy aimed at restructuring total lending condi-tions.

ANNEX VIPage 4

INTRODUCTION

Financial Environment

1. Ghana's Banking System is dominated by the Central Bank (Bank ofGhana) and three major commercial banks -- the state-owned Ghana CommercialBank and two private banks, Barclay's Bank of Ghana and Standard Bank ofGhana. In addition, the following operate in Ghana, some of which openedin the last few years: The National Finance and Merchant Bank, the Bankfor Housing and Reconstruction, the Post Office Savings Bank, the GhanaCooperative Bank, and the Social Security Bank. These banks so far haveoperated on a small scale but they have provided substantial demand depositservices. Non-bank financial institutions include the Agriculture DevelopmentBank (ADB), the National Investment Bank (NIB), the State Insurance Corpora-tion, the First Ghana Building Society and a new institution in the UpperRegion -- Farmers Services Company Ltd. (FSC).

Bank of Ghana (BOG)

2. The BOG acts as a banker to the Government and to the commercialbanks, in addition to its functions as a currency - issuing bank and cus-todian of foreign reserves. It was established in 1957 with an authorizedcapital of ¢2 million, which was later increased to ¢20 million (of which ¢1Omillion is paid up). Its Board of Directors is appointed by the Government.To regulate the volume and distribution of credit extended by the commercialbanks, BOG relies primarily on the following instruments: reserve require-ment, credit guidelines, advance import deposit requirement, and interestrates. Credit guidelines are currently BOG's main instrument for controllingcredit. As an anti-inflationary measure a new set of guidelines was issuedin mid-1975 which provides for a ceiling on credit expansion for most sectorsof the economy. The agriculture and export sectors continue to occupy prior-ity positions and banks were requested to expand credit to these sectorsby 50 percent and 25 percent respectively over the June 1975 level. Inpractice, however, credit development through January 1976 in these twosectors was far below the recommended guidelines. Credit to agriculturedeclined by 3.2 percent and credit to export increased by only 2.6 percent.Credit to other sectors, on the contrary, far exceeded the ceiling set forthem.

3. Interest Rate Structure: Interest rates were last increased inJuly 1975. The ceiling on general lending rose from 10 percent to 12.5percent, while the interest rate on export credit remained unchanged at 9percent. ADB's loans for food and industrial crops (except sugarcane), aswell as livestock to agriculture and commercial banks lending under the creditguarantee scheme (para. 11) bear an interest rate of 8.5 percent. Interestpaid on deposits was raised from 6 percent to 7.5 percent. BOG's discountrate increased from 6 percent to 8 percent.

ANNEX VIPage 5

Agricultural Credit

4. Availability of Institutional Credit -- Institutional credit foragriculture is currently provided by ADB, the three major commercial banksand the National Investment Bank (NIB). Together they provided in 1975about 98 percent of the institutional credit to agriculture (Table 1).Farmers' actual access to credit is still very limited. Less than 10 percentof the estimated 850,000 farmers in Ghana receive institutional credit.Around 80 percent of institutional credit for agriculture goes at present tothe medium and large farmers, while the small farmers (those with farms of 10acres or less) who represent 82 percent of farmers in Ghana and produce thebulk of domestic food still largely depend on non-institutional mdney lenders.The limited access of small farmers to credit is partly due to loan securityrequirements but also to lack of an adequate credit organization geared tothese farmers' needs. ADB provides about 47 percent of the institutionalcredit to agriculture and is today the only institution extending credit tosmall farmers, thrcugh a group lending program (para. 19). Although ADB'sinvolvement in sma.l farmers credit has steadily increased since the programwas introduced in 1969, only about 7 percent of the estimated 700,000 smallfarmers have access to ADB's group lending program. More than 50 percent ofthe Bank's financing goes to larger farmers.

5. Commercial Banks' involvement in agricultural credit is very lim-ited and is directed only to the larger, mostly mechanized farmers. Thesubsidized interest rate of 8.5 percent imposed by the government on mostagricultural lending has, in fact, led the commercial banks to focus theirinvestment in the less risky and more remunerative sectors of industry andtrade. Commercial banks provide about 40 percent of the institutional creditfor agriculture. NIB's contribution to the agricultural development islimited, as it finances only projects with a minimum capital requirement of010,000. NIB's share in total credit to agriculture is around 13.0 percent.Additional credit will be provided to farmers under the Upper Region Agricul-tural project approved by the Bank in June 1976 and become effective on April11, 1977. US$2.2 million will be onlent to ADB for on-lending to farmers andranchers for medium and long-term loans at 12 percent, while a new companyestablished under the project, the Farmers Service Company Ltd, will providefarm input supplies on deferred payment (up to 1 year) at a 12 percent interestrate.

Credit Policy

6. The Five-Year Development Plan for the period 1975/76 - 1979/80acknowledges the fact that most small farmers in Ghana are denied credit andfosters policies aimed at extending to them the services of modern creditinstitutions. However, the government has not as yet elaborated a clearstrategy to develop agricultural credit, encompassing all those concernedin the use and supply of credit. As can be seen from the following descrip-tion, the government is currently taking a fragmentary approach, creatingnew institutions to compensate for the inability of the existing ones to

ANNEX VIPage 6

cope satisfactorily with the situation. To allow credit to reach a largernumber of small farmers, the BOG is now experimenting with a system of ruralbanks, after a Filipino experience (para. 27). Five rural banks have so farbeen opened and seem to have a certain success in mobilizing rural savings.The BOG also plans to set up an Agricultural Trust Fund (FONDO) to providerediscount facilities to banks for loans made to the agricultural sector(para. 13). BOG is furthermore reorganizing the Cooperative Bank which hasresumed its operations in 1974 (para. 26). This institution is also intendedto provide a further credit channel for small farmers.

7. The Government, on its part, is negotiating with USAID a US$30 mil-lion loan (to be disbursed in three different stages) for the MIDAS project(Managed Inputs and Delivery of Agricultural Services). Credit expansion,specifically to small farmers, is one of the project's main components.Funds will be channelled through ADB, which plans to establish in six yearsa total number of 59 new Farm Loan Offices (FLO), in addition to the existing14 branches and 8 FLOs.

8. At this stage, it is difficult to assess the best way to reach alarge number of small farmers; perhaps it would be useful to experiment withdifferent approaches to find out which system best suits the social and eco-nomic conditions of the country and is capable to service, at reasonablecosts, the productive small farmers. Because of its centralized organiza-tion and its limited outreach in rural areas, ADB is better suited for cater-ing to the needs of large farmers. To maintain an adequate service to allfarmers ADB should have branches within their easy reach. Even after fullimplementation of the MIDAS project only around 20 percent of the small farmerswill be serviced by ADB. Ghana has a relatively large network of coopera-tives and a cooperative bank. However, their performance is very poor. Thisis partly due to the serious setback the cooperative movement suffered duringthe Nkrumah period. Cooperatives need to be strengthened and reorganized.Financially, they are too weak to provide an adequate credit channel to smallfarmers. Rural banks which are in Ghana still at the experimental stage,might provide an effective channel for reaching a large number of smallholders.Introduced by BOG in late 1976, rural banks are private commercial institutionswith Government support. Their function is to meet current local creditrequirements using savings mobilized in the rural areas. Rural banks have theadvantage of close contact with farmers and ability to adjust to local require-ments. Direct knowledge of the farmers lessens supervisory need. Defaultrisk is reduced by group responsibility for repayment and equity participation.Five rural banks are currently operating in Ghana. Judging from the experi-ence of the first two opened in 1976, these banks seem quite effective inmobilizing rural savings. If the rural bank experiment proves successful, aclose collaboration of ADB with a rural bank network providing a link with thevillages, might provide an effective way of reaching large numbers of farmers.Rural banks could operate as ADB agents for short and medium term credit.

9. A different approach for the provision of credit to small farmersis used by the Bank under the Upper Region Agricultural Development Project.Here, credit is channelled to the farmers directly by the project through

ANNEX VIPage 7

the Farmers Services Company. This approach was justified by the unsuitabil-ity of the existing local credit agencies of handling credit under the proj-ect. Because it is combined with technical assistance to ADB's branch inBolga,anga, it has the advantage of making project implementation possible,

while improving the operation on an existing institution. This approachcan therefore be effectively used in other agricultural development proj-ects, provided that emphasis be placed on ADB's strengthening.

Bank of Ghana (BOG)

10. The BOG's involvement in agricultural credit has expanded inrecent years. In addition to lending considerable amounts of money in theform of long-term loans to ADB, NIB (in which it also holds equityinvestment portfolio 1/) for their agricultural operations and onlending tofarmers, BOG has participated either jointly or on its own in various agri-cultural projects involving production of food and industrial crops, live-stock, etc. To stimulate flows of additional funds from the local commercialbanks, to the agricultural sector, BOG has introduced a Credit GuaranteeScheme for Small Borrowers and a Special Credit Facility for AgriculturalProduce Marketing.

I1. The Credit Guarantee Scheme was introduced in November 1969 andcovers commercial banks lending to small enterprises. Small enterprisesare defined as: agricultural operations not exceeding 200 acres per crop;manufacturing and servicing enterprises with original investments not ex-ceeding ¢100,000 and trade operations with annual sales volumes not exceed-ing ¢300,000. The guarantee covers 2/3 of the loan. The commercial banksare charged a 1 percent guarantee fee. Commercial bank lending to agriculturehas increased since the implementation of the scheme in late 1969, from 6million to 42 million cedis. The scheme, however, is not very popular withcommercial banks because of BOG's considerable delay in processing recov-ery claims.

12. The Credit Facility for Agricultural Produce Marketing operateson similar lines as the Cocoa Bill Discounting. It provides financing forthe marketing of agricultural commodities, particularly rice and maize, topublic and private agencies which are responsible for the purchase and stor-age of these goods. Since the introduction of the scheme in 1974 untilDecember 31, 1975, BOG had underwritten bills totalling approximately ¢25million. The breakdown is as follows:

1/ BOG holds also equity participation in the Upper Region's FSC.

ANNEX VIPage 8

July 1974 - December 1975(¢ million)

Rice 12.37

Maize 5.53

Other Agri. Produce 7.18

Total 25.18

13. Other measures recently planned by the BOG to stimulate growth inthe agricultural sect are: (a) the setting up of a special fund to assistRegional Development Corporations to meet the cost of preparing feasibilitystudies; (b) the opening of rural banks; (c) the establishment of an Agri-cultural Trust Fund (FONDO). The FONDO scheme, modelled on the Mexicanexperience, is aimed at tapping idle funds from the commercial banks anddirecting them to the agricultural sector. Resources of the FONDO will bemade up of:

(a) Shortfalls under the credit guidelines - Under thecredit control regulations commercial banks arerequired to lend to agriculture an amount equiv-alent to a variable percentage of their depositsregulated by the BOG credit control policy (cur-rently 10 percent). If within a specified period acommercial bank invests in agriculture less than therequired share, the balance will have to be depositedwith the Bank of Ghana, which will pay no intereston this amount;

(b) Mandatory cash contribution (currently 5 percent of bank'sdeposits) - The BOG will pay a small interest rateon this amount.

The resources would be made available to a trust institution to be set upby the BOG to provide rediscount facilities to banks for loans made to theagricultural sector. By providing a combination of credit and technicalassistance to the banks (orientation courses are planned for banks staffin methods of project appraisal and supervisions), BOG hopes that the FONDOwill contribute significantly to growth in the volume of credit to agricul-ture and to its qualitative improvement in terms of better appraisal andsupervision practices. Furthermore, the participation of bank staff in theFONDO training courses will help establish a link of communication and co-operation between the FONDO and the banks, especially at the regional anddistrict level. Partly also because of MOA's deficiencies, BOG is currentlyplaying a major role in agricultural development. It appears to be todaythe best institution to coordinate the various institutions concerned inplanning and implementing the various credit programs and design a strategyfor the development of agricultural credit that takes into account thecountry's needs and resource constraints (in terms of funds, staff, etc.).

ANNEX VIPage 9

Agricultural Development Ba nk (ADB)

14. This Bank is the main channel of credit to agriculture in Ghanaand today virtually the only source of lending to the small farmers. ADBwas founded in August 1965, when it took over the assets of the Bank ofGhana's rural credit department. As of December 31, 1975 ADB's authorizedcapital was 030 million. The paid up capital was 019,9 million, of which014.5 million was subscribed by the Government and 05.4 million by the Bankof Ghana. In addition, the Bank of Ghana has made available to ADB, from1970 to 1976, 048.5 million in the form of long-term lending on concessionaryterms. The ADB is administered by a Board of seven members, representing theMinistries of Finance and Agriculture, the Bank of Ghana and the Departmentof Cooperatives, all named by the Government. The central office is locatedin Accra. In addition, there are 13 branches and 8 Farm Loan Offices (FLOs)located around the country. FLOs don't provide credit. Their services con-sist mostly of assisting the farmers in completing their loan applications,inspecting the farms, preparing field reports, supervising loans and pro-viding technical advice in cooperation with the Ministry of Agriculture'sextension officers. ADB staff on December 31, 1975 totalled 581, out ofwhich 237 were located at the head office in Accra. Although many of theprofessionals have graduated in agriculture, they generally lack adequatepractical experience and, consequently, the technical appraisal of loanapplications has not been entirely satisfactory. Senior staff have beentrained in the USA under the sponsorship of USAID or have received degreeseither in UK, USSR, USA, Germany, or Italy. The World Bank has providedtechnical assistance to ADB under several projects (Sugar I, Upper RegionAgricultural Development and Oil Palm). Under the Sugar Project, consultantswere appointed to review and improve credit management and financial control.Their recommendations (mechanization of loan accounts, establishment of adebt recovery division, and setting up of a training school) were imple-mented in 1974, resulting in increased efficiency of the lending operationand improved loan recovery performance.

Lending Operation

15. ADB's function is to assist in the development of agriculture andagricultural industries by making loans to farmers, cooperative societies,private companies and public bodies. Furthermore, the Bank undertakes largescale agricultural projects, either jointly with other organizations or byitself. Since 1970 ADB has participated in almost twenty such large projectsthroughout the country. ADB has increased more than ten times its lendingactivity in the years 1969-1976. The breakdown of loans by sector is detailedin Table 6. ADB has a variety of lending programs to both the small and thelarge-scale farm sectors. About 58 percent of the amount of loans made in 1976went to larger farmers, agro-industries and special large projects and 33percent to the small farmers under a "group loan" scheme (para. 19). ADB'scentralized organization and locational limitation makes it more suitable forcatering to the needs of large farmers. The recent growth in lending forfarm machinery and the increase in the average size of individual loans madefor food crops and livestock, as indicated in the following tables, reflectthe current trend in favor of large scale farmers supported by Government.

ANNEX VIPage 10

ADB Lending for Farm Machinery

1974 1975 1976-----------(in Cedis)-------

Amount 333,400 2,527,036 2,669,692 1/

% of TotalLending 2.3 12.0 8.3 1/

Average Size of ADB's Individual Loans

1971 1972 1973 1974 1975 1976…-----__-…---- (d 'OOO)…

Food Crops 4.79 5.08 5.74 3.61 6.23 7.23

Livestock 4.46 2.67 4.01 5.08 7.60 10.50

Industrial Crops 16.79 8.84 2.38 2.16 6.46 10.21

Fishing 20.70 19.24 17.70 14.30 15.43 13.48

Agrobusiness 9.38 8.74 5.98 4.z4 4.39 6.76

1/ Unavailability of import licenses for farm machinery and equipmenthas slowed down ADB's lending for mechanization.

16. ADB's financial position has been and still is precarious. Theunsatisfactory repayment performance and the low interest charges in rela-tion to the high level of inflation are to a great extent responsible forthis situation, which so far has been covered by consistent inflows ofequity funds from Government and the Bank of Ghana. Since 1972, Govern-ment and Bank of Ghana contributions to ADB have been mainly in the formsof loans, mostly long-term. Only by consistently improving its recoveryperformance will ADB be able to repay these loans. As shown in the follow-ing table private savings mobilization, although steadily increasing sinceits introduction in 1968, does not represent a sufficient source of fundsfor ADB.

1968 1969 1970 1971 1972 1973 1974 1975…( ------------- ~--- (i million)---------------------

Savings depositsand currentaccounts 0.06 0.19 0.37 0.46 3.10 4.48 7.99 13.62

For 1977 ADB has projected to lend ¢31.2 million. 019 million are expectedto come from loan repayment, ¢10 million from equity subscription and 2.2million from USAID/Ghana Government funds.

ANNEX VI

Page 11

17. 40.8 percent of ADB staff is located at the Accra office. This highconcentration at the headoffice underlines the centralization of lending oper-ations. Only limited autonomy is now given to the branch managers and variesaccordingly to branch performance. The most efficient branches are allowedto grant credit up to ¢5,000 without headoffice approval. A loan applicationmust otherwise be approved on all three organizational levels - the FLO, theBranch Office and the Headoffice - a process which may take well over threemonths. Under the MIDAS project, ADB plans to establish in six years 59 newFLOs. ADB's target is to reach in the ninth year of the program operation118,000 small 'armers in addition Lo the approximately 44,000 currentlyserviced. A little over 20 percent of all small farmers would thus be reachedby ADB. Lending procedures will be streamlined and decentralized. FLOs,under the project, would be authorized to make over-the-counter loans.

18. Terms of loans are based on the type of activity and vary between6 months (for maize, cotton, groundnuts) to 7 years for livestock and up to15 years for tree crops such as palm oil. Credit is secured, except forgroup loans, by land or through mortgages on farm equipment and machinery.The following breakdown of loans by terms of maturity shows a growing emphasison short-term loans (partly due to increased lending to small farmers).

1973 1974 1975

Short-term loans 38.0 40.0 58.2

Medium-term loans 47.0 46.0 28.7

Long-term loans 15.0 14.0 13.1

Total 100.0 100.0 100.0

Interest rates range between 8.5 percent and 12.5 percent (Table 15). PerGovernment degree, ADB food crop, livestock and industrial crop (exceptsugarcane) loans are charged an interest rate of 8.5 percent. The rate was 6percent until August 1975.

19. Group Loans - ADB lends to small farmers under a group loan scheme(also called Commodity Credit Scheme), a special credit program to providecredit to small farmers without collateral. Loans under this scheme aremade for a particular crop on a group basis. Groups are formed with theassistance of MOA's extension officers who help ADB in selecting reliableparticipants using their direct knowledge of the farmer and the nature ofhis operation. Once formed, the group selects a leader and a few executivemembers who will represent them. Credit is provided by either advancing thefarmer cash (to finance labor) or providing a voucher or chits with whichto purchase required items. Experience has shown that group loans, besidesreducing the cost of loan servicing by raising the average size of the loan,insure that credit is properly used. Furthermore, group joint responsibilityfor the repayment of members' loans has an important influence in ensuring

ANNEX VIPage 12

repayment. Loan recovery under the group scheme reaches in fact 80-90 percentof the outstanding loan. In 1975, 43,878 small farmers were reached byADB under the scheme (94 percent of all farmers reached by the institution),they represent an increase of 25 percent over the number of small farmersreached in 1974 (32,951). Each farmer received in 1975 an average loan of0187.5. Loans are seasonal (from the time of land preparation to harvesting).ADB increases gradually each year the acreage financed according to thefarmer's performance, up to a maximum of 15 - 20 acres. Tables 9 and 10provide a breakdown by sector and Regions of the group loans. In spite of thesteady expansion in the group lending program, only a relatively small frac-tion of small farmers is actually benefitting from it. The small farmersreached in 1975 by the scheme represent only 6.6 percent of the total numberof small farmers in the country. Insufficient capital resources, inadequatecoverage of branches serving the rural area, lack of trained staff and cumber-some bureaucratic procedures (most of the loans have to be approved by Accraoffice) limit ADB's servicing of small-scale farmers.

Performance

20. ADB's operational efficiency has not been satisfactory as evidencedby debt recovery. At the end of September 1975, the amount in arrears ofthe loans for which accounts had been mechanized (76 percent of the total) was43.5 percent of the total of these loans. The absolute amount of arrears was012.2 million. Some of the reasons for poor debt collection record are beyondADB's control and stem from the social and legal structure of Ghanaian society.They include the absence of formal land ownership and the consequent impossi-bility of securing loans with land titles. Legislation on debt default iscomplicated and difficult to enforce. But to a large extent the arrearsproblem is attributable to inadequate loan appraisal and supervision on thepart of ADB's project officers. In an environment where borrowers histori-cally have been poor repayers to government financial institutions, ADB'sofficers have to display a special effort in pursuing defaulters. This firm-ness had seldom been forthcoming in the past. The situation has recentlyimproved following the establishment in 1974 of a Loan Recoveries Division.As of December 31, 1976 of total principal due 62.2 percent was repaid (Table11). This reduces the level of arrears to 37.8 percent against 43.5 percentas of September 30, 1975. Of the total amount of arrears almost 50 percentwas more than 1 year overdue (Table 12). Some branches still perform verybadly, the worst results being recorded in Hohoe (Volta Region with a recoveryrate of only 32.4 percent, Wa(Upper Region) with 35.6 percent, and Tema(Greater Accra) with 38.1 percent. Staffed only with three officers, theRecovery Division is very active; legal proceedings have been instituted inmany cases and, as a last resort, the army has been used in certain areas,with some success. The customers are beginning to realize that ADB intendsto use all the means at its disposal to recover the money and a small butsteadily growing number of defaulters are repaying. A limiting factor isstaff. Recovery, as well as legal staff, is currently overloaded and theirnumbers should be increased.

21. Staff quality, especially at the branches, still needs much im-provement. The training program recommended by the consultants Berenschot-Moret-Bosboom has now started and should be of great help to ADB in solving

ANNEX VIPage 13

the staff problem. There is a danger that the present food shortage mightcompel ADB to finance projects which are financially as well as economicallynot viable making it thus very difficult for it to operate as an efficientlending institution in spite of its willingness to do so.

Commercial Banks

22. Commercial banks provide almost 40 percent of the institutionalcredit to agricultural production. In January 1977, loans outstanding toagriculture totalled ¢51.6 million. This amount represents only a modestshare of total commercial bank lending. A breakdown of lending by end-use(Table 3) shows that more than 50 percent of commercial bank credit goes tothe manufacturing and trade sectors and only 10 percent to agriculture,forestry and fishing. However, lending to this sector has increased recently.While total bank lending shows an increase of 19.2 percent in January 1977 ascompared to January 1976, lending to agriculture increased 34.3 percent. Thisrise is a result of BOG's efforts to increase commercial banks' involvement inagriculture, by pre3cribing quotas for lending to the sector and partiallyguaranteeing loans to smaller farmers. In 1975 the three major commercialbanks approved agricultural loans for an estimated amount of ¢33 million.Almost 60 percent of these loans went into food and industrial crops with thebalance taken by cocoa production, logging, poultry, fishing, forestry, etc.Commercial banks finance predominantly large farmers. In the Northern Region,where commercial Lenders are mostly involved as far as agricultural credit isconcerned, 1/ the three major commercial banks lent in 1976 an estimatedamount of ¢12-13 million to about 450 farmers, whose farms have average sizeof about 200-250 acres. These farmers are predominantly involved in ricecultivation. Forty percent of the credit they received in 1976 financed thepurchase of agricultural machinery (tractors, combine harvesters, etc.).

23. Loans to farmers whose farms do not exceed 200 acres in size percrop are covered by the BOG credit guarantee scheme. The interest rate forthe loans under the scheme is 8.5 percent. On all other loans the interestcharged is 12.5 percent. Loans under the credit guarantee scheme representmore than half the commercial banks lending to agriculture. Recovery rates onagricultural loans are currently very low. The three leading commercial bankscomplain that in 1975 and 1976 less than 40 percent of the loans made in theNorthern Regions were repaid. This result is to a large extent attributed tothe drought that considerably reduced the

1/ Ninety percent of Barclay's Bank lending to agriculture in 1976 wentto the Northern Region, which also absorbed more than 50 percent ofStandard Bank's agricultural lending. Ghana Commercial Bank, althoughsubstantially involved in agricultural credit in the Northern Region,lends ample amounts in other Regions to finance livestock and poultryfarming (Volta, Brong Ahafo, Ashanti Regions) as well as forestry andlogging in the Western Region. In the Northern Region the Ghana Commer-cial Bank established its own wholly owned subsidiary, the DevelopmentLeasing Company. This Company provides mechanized services includingland clearing to large farmers.

ANNEX VIPage 14

expected crop yields. In 1974, when the harvest was good, the banks inthe Northern Region obtained recovery rates of 75-80 percent. Out of StandardBank's total bad debt of nearly ¢500,000 for the 1975-76 season, 86 percentwas agricultural. The bank estimated provision for agricultural bad debt for1976/77 in the Northern and Upper Region is close to ¢400,000. Because of therisks and the management costs involved in lending to agriculture and thesmall margin left to the banks due to the concessionary rate of interest fora large part of the agricultural loans (the ceiling on deposits is 7 percent),commercial banks are not eager to engage in agricultural lending programs,in spite of their excess liquidity position (Table 4). No major shift cantherefore be expected in their lending in the coming years.

24. In early 1975 Ghana Commercial Bank (GCB), the largest of the threecommercial banks 1/ introduced a special credit scheme for small farmers(whose farms do not exceed 5 acres in size). To be eligible, farmers haveto become member of the Ghana Commercial Bank Farmers' Association (CFA).Registration takes place through the Ministry of Agriculture extensionoffices. The basis for selecting the farmers is the direct knowledge theextension officer has on the individual farmer's productive capacity. Underthe credit scheme, the country has been divided in 11 zones. Loan applica-tions are examined at each branch by a visiting Area Manager. Loans aremade in small amounts to the individual farmers 2/ and no collateral isrequired. Once granted, the loan is credited to a farmer's CFA depositaccount. Withdrawals from this account are allowed onlv in accordance witha loan disbursement plan. Farmers are charged an interest rate of 10 percent.Loan supervision is performed by the branch staff. In addition to financialassistance, the GCB plans to provide the small farmers with supplies of otherinputs such as seedlings, fertilizers and farm equipment as well as transportand storage facilities. Through its scheme the Bank is planning to reach4,000 farmers in 1977 and 40,000 in the next 2-3 years. Emphasis is cur-rently given to the production of rice, maize, cotton, groundnuts and vege-tables.

National Investment Bank (NIB)

25. NIB, a public development finance company established in 1963 forfinancing and promoting public enterprises in all piroductive sectors, is themain Ghanaian institution for the term financing of industry. NIB's author-ized capital is ¢40.0 million. The paid up capital at December 31, 1976 was¢19 million. By the end of 1977 it is expected to go up to 025 million fol-lowing an additional contribution of ¢5 million from the Government and a

1/ In 1975 its deposits represented 79 percent of total commercial bank'sdeposits. The GCB operates a network of 128 between branches and sub-branches, the largest of any financial institution in Ghana.

2/ Loans are granted on the basis of 0125 per acre with the following break-down: ¢50 for land preparation, ¢5 for planting, 020 for first weeding,020 for second weeding, ¢20 for fertilizers, ¢10 for harvesting.

ANNEX VIPage 15

take up of 01.0 million of share capital by the DEG (Deutsche EntwicklungsGesellschaft) of Germany. In 1976 loans and equity investment amounted toO27 million, distributed as follows:

- Industry 017.2 million (of which 010.7 million in for-eign exchange);

- Agriculture 06.4 million (of which 01.8 million in for-eign exchange);

- Equity 03.4 million.

NIB lending to agriculture has expanded in recent years, partly in responseto the Government desire to expand domestic food production. In 1974 loansto agriculture totalled cedis 3.0 million (20.3 percent of total loans). In1975 and 1976 these loans amounted to cedis 8.1 and 6.4 million respectively(32 percent and 27 percent of total loans). Since 1970 BOG has made availableto NIB long term loans for a total amount of 018.7 million for its own agri-cultural operations and other lending to private farmers. Some agriculturaloperations are also being financed under the Bank first NIB Loan (Loan 1180-GH).Agricultural lending is the responsibility of the Agricultural Project Divi-sion, one of the three divisions of NIB's Development Service Institute (theother two being the Industrial Projects and the Investment Development Divi-sions). NIB's contribution to agriculture is limited to projects wiLh aminimum capital requirement of 010,000. Its financing goes therefore only tolarge-scale farmers in the form of medium and long term loans. Financingcovers land clearing, purchase of machinery and other farm equipment, purchaseof fertilizers, chemicals, processing equipment. Interest rate of agriculturalloans is 10.5 percent. In addition, NIB charges a 1 percent service charge.A commitment fee of 1 percent is due on undrawn balances. NIB has fiveoffices outside Accra, at Tamale, Kumasi, Takarady, Koforidua and Ha. Thearea offices are responsible for the appraisal of loans of less than 050,000,for projects supervision and recovery of arrears. Loan approvals are vir-tually centralized at the headoffice. This procedure causes delays in loanissuing that go from 6 up to 12 months. NIB is highly involved in financinglarge-scale rice farms in the Northern Region. In 1974 loans to that Regionrepresented 62 percent of total NIB lending to agriculture. The rate ofrecovery of agricultural loans is currently very low: 20-25 percent of theloan portfolio. Reasons for this include: poor project appraisals, deficientrecovery procedures, and difficulties experienced by clients (drought, short-age of raw materials and spare parts due to import restriction). Table 13provides a breakdown by sector of NIB's agricultural loeans.

The Cooperative Bank

26. This Bank was originally established in 1946 by the colonial govern-ment when cooperatives (especially cocoa marketing cooperatives) were flour-ishing throughout the country. The Bank provided funds to member societies,enabling them to extend less expensive credit to farmers. The cooperativemovement in Ghana was first promoted by the Department of Agriculture whichencouraged the formation of cooperatives by granting loans for scales and

ANNEX VIPage 16

other equipment. In 1956 the cooperatives came under the responsibility ofthe Department of Cooperatives. In 1961, the cooperative movement suffereda setback as a result of a change in cooperative policies followed by theNkrumah regime and the Cooperative Bank ceased its functions; it reappeared in1974. Since its reopening the Bank has encountered many difficulties becauseof poor management, inadequate funds and very poor repayment performance. 1/At the beginning of 1977 BOG took over the management of the Cooperative Bankwith the aim of correcting this situation. BOG has seconded staff to theBank, will provide training to its staff and will attempt to improve itsadministration, especially its financial management. The Bank's resourcescome from equity participation of the societies (which is very low: in 1976it totalled only 096,000); savings and current account from members, andlong-term loans by the Government. In 1975 the Bank received from the Govern-ment ¢1 million. A 02 million loan has been recently negotiated. The inter-est rate on this loan is 2.5 percent. In 1975 and 1976 the Cooperative Bankprovided loans and advances for a total amount of 02.3 mil lion, mostlyshort-term. Loans are made to groups or individuals who apply through theircooperative. No collateral is required because cooperatives are jointlyresponsible for the repayment of members' loans. Interest rate on all loansis 12.5%. The Cooperative Bank also provides an outlet for societies' fundsand members' savings. In 1976 deposits (demand, time, savings accounts)totalled 06.0 million. In 1975 the amount of deposits was ¢1.4 million. Thenumber of agricultural cooperatives is currently estimated at 1,600. At June1976 loans to the agriculture, forestry and fishing sectors amounted to0708,234 of which 0476,284 were for food crops. Loans to agricultural coopera-tives have so far been given in cash. The Cooperative Bank has 50 branchesthroughout the country and because of its closer contact with small farmers itcould play a significant role in the development of agricultural credit.However, is performance is currently too poor to play a significant impact onthe agricultural scene. The future of the Cooperative Bank is linked to thedevelopment of the cooperative movement.

Rural Banks

27. Rural banks were established by the Bank of Ghana in November 1976.Based on the Filipino experience, rural banks are private banks organizedin rural communities for the purpose of specializing in the extension ofcredit to small farmers and other rural entrepreneurs using savings mobilizedin the rural areas. 2/ At the time of their establishment, the Bank of Ghanaassists rural banks by subscribing in the form of non-voting preferred stocksup to 50 percent of the paid-in capital, with the aim of gradually decreasingits participation. The Bank of Ghana provides free technical assistance, staff

1/ The Cooperative Bank's Manager was unable to provide information onloan recovery rate. He could only state that it is very low.

2/ "A Rural Banking System in Ghana," Bank of Ghana, Accra.

ANNEX VIPage 17

training facilities and funds through rediscounting facilities to guaranteethe liquidity of rural banks. It also supervises their operations. Individ-uals of Ghanaian citizenship or groups of persons, cooperatives and creditunions can establish a rural bank, provided that the subscribers are resi-dents of the community where the Bank is to be established. To this end,an application has to be sent to the Bank of Ghana, which will thereuponundertake an economic appraisal of the locality. No individual can own morethan 35 percent of the voting shares. Rural banks have an initial authorizedcapital of at least 0100,000 of which 50 percent in the form of ordinary sharesof 01 per share, and 50 percent in the form of preferred stocks. They aremanaged by a Board of Directors elected from among the stockholders withvoting power. The resources of the rural banks consist of their own capital,deposits from the public and borrowing from the central bank through re-discounting of notes. Eligible borrowers of rural banks are: (a) farmersowing or cultivating no more than 100 acres; (b) merchants whose capitalinvestment does not exceed 0100,000; (c) rural industries whose investmentin machinery and equipment does not exceed 0100,000; and (d) cooperatives ofsmall farmers, producers of livestock and poultry, fishermen and fishpondowners. The need for collateral is eliminated since, in their borrowing, therural banks rely heavily on their knowledge of local conditions and borrower'sreputation.

28. At the time the mission visited Ghana two rural banks were operating,both located in the central Region: one in Nyakrom started its operationsin November 1976, the second in Birwa, a fishing village, has been operatingsince February 1977. They seem rather effective in mobilizing local savings:the Bank of Nyakrom from November 1976, when it began operation, to February1977 collected 090,000 in savings and 040,000 in deposits; the Birwa Bankin one month of operation collected 070,000 in current and savings accounts.The bank in Nyakrom has already started lending to rice, maize, and sugarcane farmers, with the assistance of a MOA agricultural extension officerseconded to the bank. Credit is given to farmer groups (collectively respon-sible for repayment) in cash, for the time being, but in the future it willbe both in cash and kind (with the Ministry of Agriculture supplying therequired inputs). Loans, which currently average 0200 - 300 per individualfarmer, are seasonal (5-6 months for rice and maize, 11 months for sugarcane). Interest rate is 12 percent. No information was available at the timethat mission took place on repayment performance. Since then three morerural banks were opened: at Worawora (Volta Region), Esiama (Western Re-gion), and Nampong (Eastern Region). Rural bank's managers are mostly BOG'sretired officers. BOG's main objective behind the promotion of rural banksis to encourage that savings mobilized in rural areas are invested in thoseareas, instead of being transferred, as it is currently the case, to urbancenters and the cities for profitable investment in trading and other sec-tors.

29. The Bank of Ghana has not yet set a target for the number of ruralbanks to be established throughout the country in the coming years. Requestsfor the opening of these banks are coming from all regions and a survey iscurrently being undertaken by BOG in order to establish the most suitable

ANNEX VIPage 18

communities. However, BOG is proceeding very carefully with this experi-ment. Furthermore, BOG has no sufficient training and supervision staffto embark in a program of rapid expansion of rural banks. Advantages of arural bank system would be:

(a) easier access to credit and savings for small farmersbecause of their closer contact with them;

(b) simpified procedures as loan administration, super-vision and collection take place at the local level;greater familiarity with local conditions and thecharacteristics of individual farmers can, furthermore,be crucial for reducing administrative costs and delin-quency rate;

(c) use of rural savings for loans could encourage a moreresponsible use of borrowed funds as these come fromindividuals within the same community and not fromgovernment.

On the other hand, rural banks can be financially more vulnerable insti-tutions than development banks. They cannot afford weak recovery procedureswithout undermining their stability.

Farmers Services Company Ltd. (FSC)

30. The Company, established under the Upper Region AgriculturalDevelopment Project, was registered in June 1977. It has an authorizedcapital of ¢12.0 million. Initial shareholders are the Government, BOG,NIB and GCB. With a financial equity of ¢5.0 million, the Government isthe majority shareholder, followed by BOG (03.0 million); NIB and GCB havea financial equity of respectively ¢0.75 million and ¢0.25 million. Farmerswill obtain equity in the Company through a compulsory 2.5 percent mark-upon the C.I.F. store price of the goods purchased which will be credited totheir share accounts. It is intended that farmers should gradually takeover FSC's control. The FSC provides input supplies and mechanical hireservices to the Region's farmers through a network of 90 service centers.It also provides credit facilities by allowing farmers to purchase farminputs and other goods on a deferred payment basis, with a 12 percentmark-up on the price of the purchased good (which can be reduced in caseof early repayments). Farmers associations assist the FSC in identifyingcredit receipients. They are also collectively responsible for repayment.

Small Farmer Credit Channels

31. Various small farmers credit channels are currently being developedin Ghana. In addition to ADB's Commodity Credit Scheme, which started in1968, three more small farmer credit programs have been introduced in recentyears: GCB's Special Credit for Small Farmers (1975), BOG's Rural Bankexperiment (late 1976), and the Farmers Services Company, under the UpperRegion Agricultural Development Project (July 1977).

ANNEX VIPage 19

32. Under the four programs, all farmers have to be member either of acrop association (ADB's scheme) or a farmers' association (under the threeother schemes). With the exception of GCB's scheme, the association is alsoresponsible for the individual farmer's borrowing. This approach has proven tobe the most effective in ensuring loan repayment because of the strong senseof community in most rural areas. Group responsibility also reduces admini-strative costs as the group itself administers, supervises and collects theloan.

33. The Upper Region Project stimulates farmers' associations byproviding special incentives to them (a bulk discount system).

34. With the exception of the rural banks, for which BOG has not yetset a predetermined number for establishment in the coming years, the targetsof all other programs are known:

Institution Farmers Targeted to be Reached By Year

GCB 40,000 1980ADB/MIDAS 118,000 1/ 1986 2/Upper Region Project 125,000 1982-83

1/ In addition to the approx. 44, 000 small farmers currentlyserviced by ADB.

2/ If the USAID loan is signed in 1977.

Under the proposed Volta Region Agricultural Development Project 170,000farmers (most of which are small) should receive credit facilities. Ofcourse, all these credit channels will not be geographically exclusive.Farmers in certain areas will be able to choose among competing channels.However, if all the programs are implemented, by year 1985-86 more than50 percent of the small farmers (as opposed to the current 6.7 percent)will be reached by some form of institutional credit.

CREDIT OUTSTANDING TO AGRICULTURE 1970-1975(END OF YEAR)

(Cedis)

Other Financial

Commercial Banks ADB NIB Institutions a% of % of % of % of Total

Year Amount Total Credit Amount Total Credit Amount Total Credit Amount Total Credit Amount

1970 11,565 6.6 6,160 100 17,725

1971 14,327 5.6 11,031 100 25,358

1972 16,048 6.3 24,276 100 40,324

1973 21,673 7.6 35,881 100 7,534 24.8 2,488 35.7 67,576

1974 37,946 9.6 49,831 100 9,572 21.6 2,178 15.0 99,527

1975 42,244 10.5 53,283 100 15,065 25.0 2,207 16.5 112,799

Source: BOG

H t~

( M

ADVANCES GUARANTEED BY THE BANK OF GHANA TO COMMERCIALBANKS SINCE THE IMPLEMENTATION OF THE CREDIT GUARANTEE

SCHEME IN 1969, BY SECTOR

('000 cedis)

Nov. 1969 -

Sectors Dec. 1970 % 1971 % 1972 % 1973 % 1976 % 1975 %

Agricul-ture 170.4 2.8 254.8 2.3 ¢ 485.8 5.2. 1,353.3 8.2 2,795.2 9.7 4,909.1 11.7

Traiding 4,550.2 74.7 8,511.1 75.6 7,072.5 75.6 11,279.0 7.9 16,348.5 56.6 23,492.6 55.6

Others 1,370.7 22.5 2,493.2 22.1 1,796.8 19.2 3,968.7 23.9 9,743.9 33.7 13,829.2 32.7

TOTAL 6,091.3 100.0 11,259.1 100.0 9,353.1 100.0 16,601.0 100.0 28,887.6 100.0 42,230.9 100.0

SOURCE: Bank of Ghana. August 1976

N3Dlb Fd

(D !2:ti

r H

APPENDIXTable 3

COMMERCIAL BANKS' LCANS AND ADVANCES BY END-USE(IN M.ILLIONS OF CEDIS; END OF PERIOD)

June June June Dec. Jan. Feb. March June Sept. Dec. Jan.Sectors 1973 1974 1975 1976 1976 1976 1976 1976 1976 1976 1977

Agriculture, ForestryFishing 16.6 25.6 40.6 42.2 39.4 36.4 37.9 38.7 45.3 50.2 51.6

Mining, Quarrying 3.5 2.1 4.1 6.0 7.8 8.7 9.2 13.6 18.4 19.4 25.3

Mfanufacturing 80.5 91.7 119.1 101.5 109.5 111.0 110.5 118.8 120.1 128.6 123.7

Construction 27.7 34.2 34.9 44.5 46.2 47.6 47.9 48.3 55.8 58.2 60.1

Electricity, Gas,:.ater 1.5 0.9 1.2 1.5 1.5 1.5 1.4 1.8 1.8 1.8 2.0

Trace 80.7 124.7 112.4 128.1 133.2 138.8 143.1 137.0 149.1 146.5 147.2

Transport, StorageCommunications 17.8 33.2 45.7 42.9 42.4 42.4 42.2 43.1 51.8 50.2 49.6

Services 22.8 29.2 33.1 27.2 29.0 28.6 29.8 30.6 32.9 37.6 35.7

C.:er t1 ~ ~6.5 7.7 8.0 9.2 8.1 8.4 9.3 11.2 14.8 16.6 17.3

Tctals 257.6 349.3 399.1 403.1 417.1 423.4 431.3 443.1 490.0 509.1 512.50f which:

~.Irrde Sector 178.0 219.6 275.2 297.4 308.7 316.0 318.4 329.7 363.3 3.0.5 389.4

F'!"'c Sector 79.6 129.7 123.9 105.7 108.4 107.4 112.9 113.4 126.7 128.6 123.1Excladfns Cocoa'--ar ket fn g

'gricuiture in a

of total 6.4 7.3 10.2 10.5 9.4 8.6 8.8 8.7 9.2 9.9 10.1

ASSETS ANr} LIABILITIES OF COMMERCIAL BANKS

19/ 19/21 19 /3 19/49/5-Dr. !1 [1 m; j D Mardli June Srtpl. Dec.

ASSETS

1. Cash and aklance at the BRank of Glhana 79.0 113.9 1 /1.1 2 14.9 183.7 292.2 313.5 375.3

2. Foreign Currency Assets 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2

3. Balance (lue by other Bainiks, 1 2.9 9.1 20 4 19 3 1 0.9 13.0 16.6 12.9

4. Treasury Bills 26.0 6'i 0 42.8 40.8 43.3 43.3 42.8 42.8

5. Commercial Bills 60.7 37.5 56.4 61.4 18.3 26 7 13.0 104.6

6. Loans & Advances 253 4 255.2 283.6 396.8 408.8 399.4 391.5 403 5

7. Securities 27.5 49.4 65.6 7. 88.0 109.2 111.5 111.5

B. RCal Estates 1 9.4 21.0 21.2 23.1 23.9 22.8 23.8 26.3

9. Othier Assets 35.9 147.2 123.4 164.7 156.8 201.1 141.0 158.4

7'0 7 A 1. 514 9 - 699.0 /84.6 1,000.1 993.8 1,101.8 1,053.9 1,235.5

LIABILITIf S

1. Paidi up Capital 24.4 2A.4 32 2 35.0 34.1 35.5 36.2 39.9

2. Balance duLe to other Banks 5.8 15.3 4.1 19.8 14.0 10.8 5.6 8.7

3. Total Deposits: 399.9 414.8 563. 7 704.8 739.1 839.8 802.2 933.5

of which (a) DemanidJ Deposits 246.3 269.7 327.3 39/.1 400.7 48/.3 446.9 555.8

(b) Savings Deposits 89.6 123.0 158.5 194.3 212.7 230.4 237.9 263.6

(c) Time Deposits 64.( 62.1 77.9 113.4 125.7 122.0 117.4 114.1

4. Other Liabilities 84.9 16 0.3 184.6 240.5 206.5 221.7 209.9 253.4

_____. .__ ___I_ __ _ .. _.I- t71() 1 .4 1 5149 699.0 1B4.6 1,000.1 993.8 1,107.8 1,053.9 1,235.5

Source: &3nk of Ghana Qtia7rterly EcCnomic 3tillerin

AGRICULTURAL D)EVELOPMENT BANK

Balance Sheet(e '000)

ASSETS 1970 1971 1972 1973 1974 1975

Cash at bank and on hand 763.8 978.1 2,033.6 2,943.3 6,367.2 8,509.6Short term investment 1,321.5 4,765.7 8,038.4 4,832.1 1,857.5 4,000.0Loans and advances 5,888.3 10,650.9 23,662.3 37,507.0 52,837.8 59,302.7

(a) Private Sector 5,514.9 9,307.8 n.a. 21,126.6 26,921.6 41,475.8(b) Public Sector 373.4 1,343.1 n.a. 16,380.4 25,916.2 17,826.9

Other accounts 364.6 384.7 658.1 1,628.7 1,453.8 1,372.9Medium and long-term investments 5,282.0 922.0 652.0 990,0 3,628.5 4,017.4

Fixed assets (net of depreciation) 125.6 144.0 265.3 534.8 842.8 910.6Customers' liability on guarantees 9,129.1 9,154.8 7,393.0 25.0 69.5 231.8

Total Assets 22,874.9 27,000.2 42,702.7 48,460.9 67,057.1 78,345.0

LIABILITIES

Paid in capital 10,554.0 13,254.0 18,451.0 19,151.0 19,951.0 19,951.0General reserve fund 37.3 48.6 64.0 78.5 91.6 102,2Deposit and other accounts 3,154.5 4,542.8 16,794.6 29,206.4 46,945.0 58,060.0Liability on guarantees 9,129.1 9,154.8 7,393.1 25.0 69.5 231.8

Total Liabilities 22,874.9 27,000.2 42,702.7 48,460.9 67,057.1 78,345.0

Source: ADB Annual Reports |r

ADB: TOTAL LOANS TO AGRICULTURE APPROVED 1971-1976AND 1977 PROJECTIONS, BY SECTOR

Sector.s .====1971 1972 1973 1974 1975 1976 1977Amount No. Amount No. Amount No. Amount No. Amount No. Amount No. -Amount

Food Crops 1,351.0 282 2,591.8 510 2,999.0 522 1,876.8 519 4,475.7 712 6,410.3 886 4,251.0Livestock 558.1 125 502.3 188 577.3 144 584.2 115 828.0 109 1,488.5 142 2,055.0Industrial Crops 4,030.5 240 1,945.6 220 1,317.1 442 1,611.4 746 1,763.2 273 2,715.6 266 3,923.0Fishing 455.5 22 1,039.2 54 1,168.4 66 671.9 47 1,080.3 70 1,119.0 83 1,285.0Agrobusiness 703.8 75 1,197.5 137 1,352.1 226 1,272.3 300 1,272.8 255 3,449.6 510 2,612.0Cocoa Rehabilitation - - 606.7 3 1,191.9 7 1,104.5 1 1,468.5 1 1,965.7 1 -

Pineapple Project - - 312.0 50 _ _ - - - - -

9pecial Projects _ - 4,299.8 9 765.0 5 1,301.4 6 1,952.5 4 4,440.8 11 5,549.0"Groups" Scheme 1,523.5 8* 1,715.8 285 3,890.5 507 6,138.5 288 8,228.7 992 10,653.6 1208 11,325.0Corporations/O0Y Loans * _ _ 14,570.0 4 4,250.0 2 100.0 1 - - - - _TOTAL 8,622.4 752 28,.468.7 1310 17,823.4 1921 14,661.1 1504 21,069.7 2416 32,242.5 3107 31,000.0

1971=100 100 100 330 174 207 255 170 200 244 321 374 413 359

* 382 groups involved under the maize scheme, but each branch wasconsidered as one echeme.

** OFY = Operation Feed Yourselves

ADB: TOTAL AGRICULTURAL LOANS APPROVED 1970-1975, BY SIZE

(Cedis)

1970 1971 1972 1973 1974 1975Loan Size No. Amount No. Amount No. Amount No. Amount No. Amount No. Amount

Up to 500 20 6,52-. 49 16,033 158 48,480 347X x 173,743 108 38,570 121 62,252

501-1,000 22 17,574 102 77,897 141 94,719 117 107,660 511 350,933 152 134,135

1,001 - 2,000 108 186,683 155 244,128 154 220,084 343 561,831 363 687,458 274 474,590

2,001 - 3,000 - - - - 194 494,806 322 852,100 250 645,658 341 773,488

3,001 - 4,000 _ _ _ - 118 428,348 191 700,000 157 607,595 180 682,384

4,001 - 5,000 3 1X 117,872X 1 52 X 475,059 144 655,485 233 1,076,522 303 1,409,402 204 865,723

5,001 - 10,000 63 517,913 127 945,187 202 1,364,184 220 1,623,160 145 1,071,790 603 3,987,585

10,001 - 20,000 73 1,039,510 113 1,479,309 144 1,965,791 131 2,800,589 115 1,602,582 330 4,282,476

20,001 - 30,000 27 665,240 27 613,420 26 542,422 23 572,650 36 880,502 147 2,256,016

30,001 - 40,000 12 414,410 7 240,001 15 550,220 9 336,277 11 375,798 27 935,152

40,001 - 50,000 4 174,500 10 853,729 4 169,893 3 137,870 5 224,370 11 484,212

-50,0001 and above 8 1,389,499 10 3,677,6781 35 5,364,281 32 8,880,879 19 6,766,464 26 6,131,810

TOTAL 368 4,529,725 752 8,622,441 1,335x 11,898,713 1,971 17,823,281 2,023 14,661,122 2,416 21,069,824

x = Loan size 2,001-5,000xx = Excludes a loan of J16,570,000 approved for the State Corporations

xxxx = Mainly for cotton farmers in the Northern Region.

Source: ADB Annual Reports.

(D4

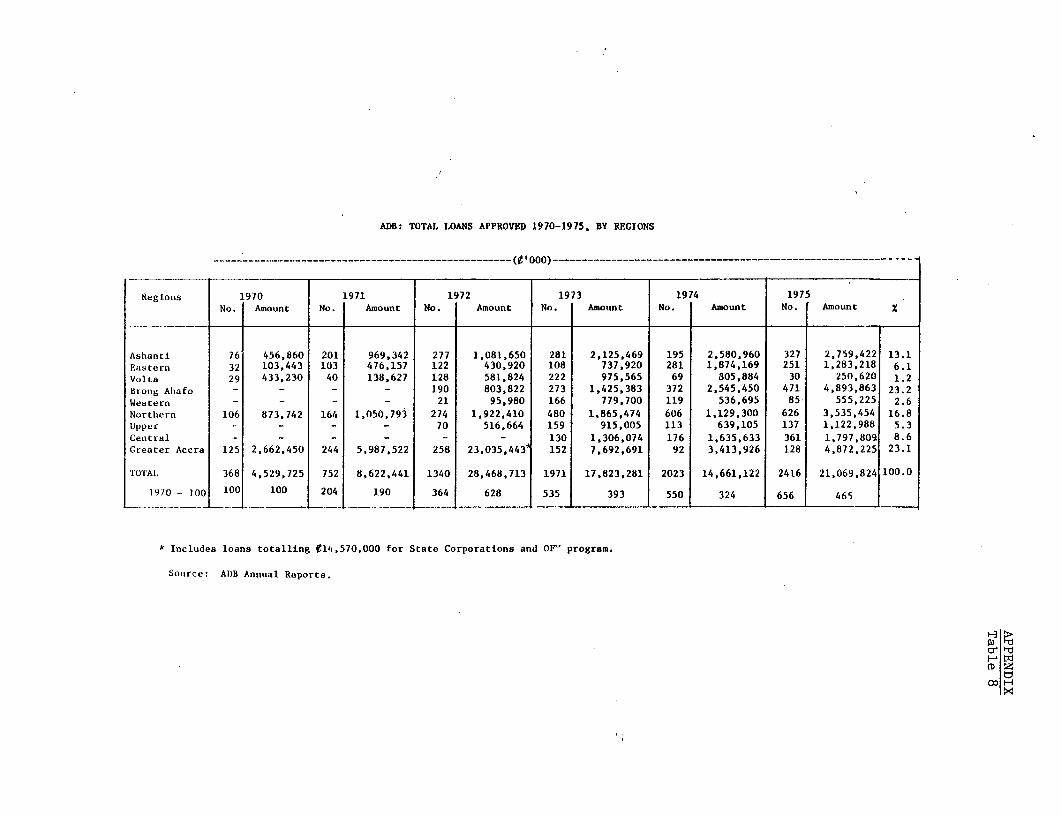

ADB: TOTAL LOANS APPROVED 1970-1975, BY REGIONS

…__________________________________________________(¢0 o o )…--------------------------------------------------------- --- _

Regions 1970 1971 1972 1973 1974 1975No. Amount No. Amount No. Amount No. Amount No.. Amount No. Amount Z

Ashantl 76 456,860 201 969,342 277 1,081,650 281 2,125,469 195 2,580.960 327 2,759,422 13.1Eastern 32 103,443 103 476,157 122 430,920 108 737,920 281 1,874,169 251 1,283,218 6.1Volta 29 433,230 40 138,627 128 581,824 222 975,565 69 805,884 30 250,620 1.2Brong Alhafo - - - - 190 803,822 273 1,425,383 372 2,545,450 471 4,893,863 23.2Western _ - _ 21 95,980 166 779,700 119 536,695 85 555,225 2.6Nortlhern 106 873,742 164 1,050,793 274 1,922,410 480 1,865,474 606 1,129,300 626 3,535,454 16.8Upper - - - _ 70 516,664 159 915,005 113 639,105 137 1,122,988 5.3Central - - - - - - 130 1,306,074 176 1,635,633 361 1,797,809 8.6Creater Accra 125 2,662,450 244 5,987,522 258 23,035,443 152 7,692,691 92 3,413,926 128 4,872,225 23.1

TOTAL 368 4,529,725 752 8,622,441 1340 28,468,713 1971 17,823,281 2023 14,661,122 2416 21,069,824 100.0

19-nO = ]100 100 100 204 190 364 628 535 393 550 324 656 465

* Includes loans totalling ¢14,570,000 for State Corporations and OFY program.

Source: ADB Annual Reports.

Fl e

(D ZwziCo H

ADB: SMALL FARMERS' GROUP LOANS APPROVED 1969-1976AND 1977 PROJECTIONS, BY SECTOR

(in Cedis)

Years Maize Yam Rice Cassav Cotton Shallo Ground Tomatoe Ginger Mixed Fiber TotalNuts Crops

1969 230,000 _ _ - _ _ _ _ _ _ _ 230,000

1970 373,350 - _ 45,000 _ _ _ _ _ _ - 418,350

1971 1,249,375 240,596 - 33,520 _- - - - - 1,523,4911972 939,642 630,700 31,500 47,360 21,780 9,990 - - 34,875 - - 1,715,847

1973 1,617,084 1,332,568 498,170 135,270 36,692 30,823 7,100 1,325 229,900 - 1,635 3,890,5671974 3,085,244 2,048,943 - 20,020 209,145 15,300 - 9,222 662,244 - - 6,05Q,118

1975 4,683,474 2,578,490 241,405 251,516 300,000 21,200 110,790 - - 41,820 - 8,228,6951976 4,535,614 3,909,786 435,395 147,625 800,000 118,450 476,680 20,000 64,030 145,060 - 10,653,6401977** 5,033,000 4,590,000 450,000 284,000 - * 220,000 440,000 100,000 120,000 88,000 - 11,325,000

TOTAL 21,746,743 15,331,083 1,656,470 964,311 1,367,617 415,763 1,034,570 130,547 ,112,04' 274,880 1,635 44,035,680

% 49.4 34.8 3.8 2.2 3.1 0.9 2.3 0.3 2.5 0.6 100.0

* Since 1976 funds are given to the Cotton Development Board for on lending to cotton farmers.

** 1977 ADB's projections.

Source: ADB's Annual Reports.

wzt?

ADB: SMALL FARMERS' GROUP LOANS APPROVED 1971-1976AND 1977 PROJECTIONS, BY REGIONS

.~~~~~~~~~~~~~

1971 1972 1973 1974 1975 1976 1977

Ashanti 530,315 493,050 1,432,575 1,884,500 1,890,822 2,789,999 2,563,000

Eastern 199,355 7,860 400,000 908,232 539,905 217,529 500,000

Volta 59,347 323,003 552,265 99,044 131,260 258,070 220,000

Brong Ahafo - 564,773 1,272,753 2,069,471 4,581,443 5,148,542 6,120,000

Western - - - 1,155 9,425 20,000 60,000

Northern - - 3,240 - 154,930 959,500 580,000

Upper - - - - - 75,000 175,000

Central - - 189,734 1,087,716 920,910 1,185,000 1,107,000

Greater Accra 734,474 327,161 40,000 - ** - ** - ** **

TOTAL 1,523,491 1,715,847 3,890,567 6,050,118 8,228,695 10,653,640 11,325,000

Source: ADB Annual Reports

* - ADB's projections

** - Following the opening of new branches no more small farmers loans wereprocessed by the head office.

I-. tI

cr Fd

o H

APPENDIXTable ll

ADB: RECOVERY RATE OF PRINCIPAL DUEAS OF DECEMBER 31, 1976

Principal Principal RecoveryBranch Due Repaid Rate

¢ ¢

Accra 9,883,068 4,845,262 49.0

Swedru 1,565,523 1,182,179 75.5

Koforidua 959,381 427,094 44.5

Hohoe 992,508 321,120 32.3

Tema 2,103,680 802.280 38.1

Somanya 3,821,800 1,768,872 46.3

Cape Coast 2,261,531 1,153,214 51.0

Takoradi 1,597,848 691,428 43.3

Kumasi 9,330,727 * 7,066,306 75.7

Sunyani 14,486,737 * 11,028,376 76.0

Bonla 1,920,633 * 1,077,033 56.0

Atebubu 1,609,341 * 1,307,703 81.3

Wa 283,184 * 100,761 35.6

Kwahu Tafo 349,939 * 32,325 9.2 **

Total: 51,165,900 31,803,953 62.2

* Branche A/c not mechanizedEstimated from Loans Outstanding

** Branch Office opened in latter part of the year. LoansOutstanding transferred from old Branch Office (Koforidua)to the new Office. This showed the least recovery rate.

Source: ADB

APPENDIXTable 12

ADB: ARREARS POSITIONAS OF DECEMBER 31, 1976

3 Months 6 Months 1 YearBranch Overdue Overdue Overdue Total

Accra 27,591 374,765 1,308,944 1,711,299

Swedru - 45,535 89,257 131,792

Takoradi 39,935 62,610 220,840 323,384

Hohoe - 27,910 552,653 580,563

Somanya 28,674 91,318 1,748,013 1,868,005

Tema 55,105 8,875 546,983 610,963

Cape Coast 177,977 119,924 215,140 513,041

Koforidua 31,080 11,126 522,238 564,444

Kumasi 51,477 102,954 720,675 875,105

Sunyani 90,723 181,445 1,270,118 1,542,287

Tamale 99,085 198,170 1,387,188 1,684,443

Bolga 33,291 66,582 466,074 565,947

Atebubu 20,921 41,843 292,900 355,664

Wa 9,203 18,407 128,848 156,459

Kwahu Tafo 7,582 -15,164 106,148 128,894

Total 672,644 1,366,628 9,576,018 11,612,290

Source: ADB

APPENDIXTable 13

NIB LOANS TO AGRICULTURE ANDAGROBASED INDUSTRIES

1974 1975 1976----- …-----(cedis)-----------

Agriculture

Livestock 135,550 239,780 63,080

Poultry - 88,966 30,000

Foodcrcps 714,730 1,688,229 1,730,043

Industrial rawmaterials 2,126,377 5,629,900 972,176

Fishing - - 2,422,570

Agricultural services - 89,390 1,139,420

Other agriculture - 370,440 -

Total 2,976,657 8,106,705 6,357,289

AgrobasedIndustries 3,24,0775 1,199 363 802,370

NIB Equity Partici-pation-Agriculture- 180,000 262,810 250,000

AgrobasedIndustries 477.530 287,230 -

Total 657,530 550,040 250,000

Total financialassistance to theagricultural 6,874_962 9,856,108 7,409,659sector

Source: NIB

APPENDIXTableT14

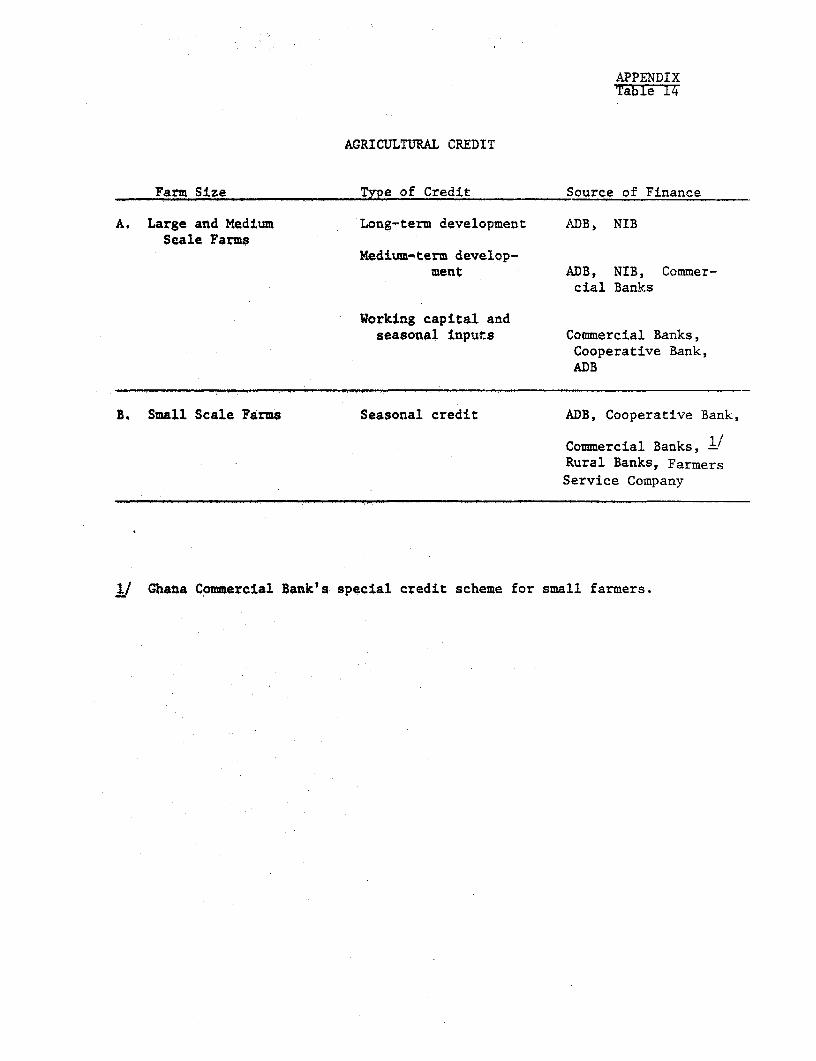

AGRICULTURAL CREDIT

Farm Size Type of Credit Source of Finance

A. Large and Medium Long-term development ADB, NIBScale Farms

Medium-term develop-ment ADB, NIB, Commer-

cial Banks

Working capital andseasonal inputs Commercial Banks,

Cooperative Bank,ADB

B. Small Scale Farms Seasonal credit ADB, Cooperative Bank,

Commercial Banks, 1-Rural Banks, FarmersService Company

1/ Ghana Commercial Bank's special credit scheme for small farmers.

APPENDIXTable 15

INTEREST RATES ON AGRICULTURAL CREDIT - MARCH 1977

Lending Institutions Lending Terms Interest Rate

Commercial banks Mostly short and 8.5 - 12.5%!'medium

Ghana Commercial Bank'sSpecial Credit Scheme for

small farmers seasonal 10%

Agriculture Development Short, mediumBank (ADB) and long

Agriculture (food andindustrial crops) 8.5%

Sugar 9.0%Agro-business 10 - 12.5%Fishing 8.5 - 9%Livestock 8.5%

National InvestmentBank (NIB) Medium and long 10.5%

Cooperatives Seasonal 12%Medium 12%

Rural Banks Seasonal 12.5%

Farmers Service Co. Seasonal 12%

1/ Same for short and medium, 8.5% interest rate on loans underthe credit guarantee scheme.

ANNEX VIIPage 1

PRICE AN'D SUBSIDY POLICIES

l. Successive governmen-s have set producer and retail prices, andsubsidized interest rates and inputs, to encourage agricultural production,to keep down food prices, in particular for the increasing urban population:,

or, in the case of cocoa, to raise fiscal revenue. Such nolicies have hadlimited effect, Retail prices have continued to rise rapidly, with theurban food index rising by 38 percent per annum 1970-1975, and more sharply

latterly (150 percent in 1976). Cocoa production is declining, largelybecause the price which the goverrment agency (CMB) pays for cocoa has beenheld down in real terms and consequently has successively reduced the attrac-tiveness of cocoa to the farmer. Subsidization of inputs has, in the absenceof an efficient distribution system, benefited larger and richer farmers withaccess tc Ministry officials, and there is little evidence that it has encour-aged smaller farmers, facing a riskier outlook, to adopt new technologies.Subsidized credit has also primarily benefited the larger farmer who hasgreater creditworthiness and ability to deal with official and commercialinstitutions. Further, the high level of subsidization has increased corrup-tion and contributed to the smuggling of inputs and produce across nationalboundaries. Except for cotton and bast fibres, where the Cotton DevelopmentBoard (CDB) and the Bast Fibres Development Board respectively are the solepurchasers, Government's intervention in the primary commodities market haslargely been ineffective, among other reasons because of lack of marketcoverage.

2. Cotton production was encouraged by the relatively high producerprice offered by CDB, which was increased in 1974 from ¢0.lO to ¢0.35 per lbseed cotton. It has been suggested that cotton expanded initially in certainareas at the expense of foodcrops, particularly yam, but this is difficultto substantiate. It is more likely that, where a proper rotation is used,cereals following cotton will benefit from the carry-over effect of the fer-tilizer applied to the cotton, and cereal production will increase.

Maximum Retail Consumer Prices

3. While efforts to dampen retail price rises help to lessen thedirect impact of inflation on the urban consumer, they tend to increase gov-ernment's budgetary deficit, distort demand levels and substitution betweendifferent commodities, encourage black marketing, and create expectationsthat cannot in the long run be satisfied. Where maximum price levels areset for commodities domestically produced, such as rice, and processingagencies are restricted or forced to sell at a financial loss, such pricesshould be recognized as support prices and the processing unit concernedshould receive a compensating subvention to allow it to operate on a finan-cially viable basis to encourage proper financial management. This is notthe case for the Rice Mills Unit which is forced to operate at a loss (seeAnnex XI). In most markets, but particularly those for oils, maize, beef,mutton and goat meat, official maximum prices are not effective in the faceof strong demand, shortages of supply and government's inability to eitherpolice markets or provide the necessary supplies from hold-over stocks tosatisfy demand.

ANNEX VIIPage 2

Interest Rates

4. In view of the high level of internal inflation (in excess of 60percent per annum) agricultural credit at 8.5 percent is very cheap and ratesshould be increased substantially if the present level of lending is to bemaintained as well as brought into line with lending rates to other sectors ofthe economy.

Minimum Producer Prices

5. During the 1976 season Government attempted to offer a minimumprice for cocoa, maize, rice, groundnuts, soyabeans, yam, sugar cane, plan-tain, cotton and kenaf, to guarantee producers a positive return to theirinvestment and to hold down retail prices. Apart from cocoa, cotton andkenaf where the respective government agency is the only buyer, governmentintervention, through the Food Distribution Corporation, was ineffectivein the other commodity markets. In the face of high and rising market pricesreturns to producers exceeded the minimum prices set, and government interven-tion was not required. However, apparently in an effort to halt the unpre-cedented maize price increases, Government entered the market, revising itsintervention price sharply upwards with the intention of reselling on theretail market. This temporarily exerted further upward pressure on prices.It is clear that government policy was not well formulated and that marketintelligence was poor.

6. Until there is adequate government or privately owned storagecapacity and Government has sufficient financial resources, there can beno long-term buffer stock of primary commodities, nor can Government holdshort-term stocks to even out seasonal fluctuations. When adequate financeand storage capacity does exist a far more sophisticated market intelligencesystem will be required to allow Government to operate in the market knowl-edgably (see proposals in Annex V), preferably without a minimum price schemewhich limits the flexibility of the intervening agency. Until such time Gov-ernment should limit its intervention to the cocoa, kenaf and cotton markets.

7. The minimum price at which the Rice Mills Unit is empowered to pur-chase rice is also the maximum price. During 1976, while prices rose drama-tically, the unit was not authorized to alter its maximum price, and wastherefore unable to buy sufficient rice for its needs. In order to protectits investment in milling capacity, the Rice Mills Unit should be allowed tocompete in the market, acting in a rational and financially prudent manner,using its storage capacity to buy cheaply at times of surplus. It should notbe constrained by a fixed price stipulation.

8. The present price of seed cotton was increased in 1974 to ¢.77/kg,from ¢.25/kg, an increase that made cotton more attractive than competingcrops as evidenced by the very considerable increase in area and productionsince 1974 (see Annex I). However, dramatic increases in the price of com-peting crops since 1974 have led to a decline in the relative attractivenessof cotton, on average by a factor of four:-

ANNEX VIIPage 3

Table 1: COTTON PRICE RATIOS WITH COMPETING CROPS (PER TON)

1974 1975 1976 1977 1/

Cotton: maize 3.9 3.1 1.5 .8Cotton: yam 4.1 2.9 2.1 .9Cotton: millet 2.8 2.7 1.2 .6

Source: Mrinistry of Agriculture.

1/ March 1.977 wholesale price.

9. The farm gate price for seed cotton is marginally higher than theimport substitution price calculated at the official rate of exchange, andconsiderably less (up to 60 percent) than that calculated at more realisticexchange rates.

Table 2: IMPORT SUBSTITUTION PRICE FOR COTTON

Official Price Import Substitution Prices

US$1 - ¢1.15 US$1 - 01.73 US$1 - 031977 1980 1977 1980 1977 1980

M/kg .77 .77 .66 1.13 1.05 1.97 1.81

10. A comparison of the Ghanaian producer price with that of her neigh-bors reveals that at the official rate of exchange their producers receivebetween 24 percent and 46 percent of the Ghanaian price. At an exchange rateof V3 to the dollar the Ivorian cotton farmer receives more than his Ghanaiancounterpart, as follows:-

Table 3: COTTON SEED PRICES

Comparison with Ghanaian Price 1/

Official Price US$1 - ¢1.15 US$1 - 03 US$1 - ¢5

Upper Volta CFA 38.6/kg 24% 61% 102%Togo CFA 52/kg 32% 83% 138%Ivory Coast CFA 75/kg 46% 119% 198%

1/ CFA 100 - ¢.4694.