Embed Size (px)

Citation preview

8/3/2019 PS1 Forward Contract Pricing 2011

http://slidepdf.com/reader/full/ps1-forward-contract-pricing-2011 1/3

FIN 5207, Advanced Derivative Securities Fall 2011 Professor FengHW1, Forwards and SwapsPost Date: 9/17/11Due Date: 9/26/11 at 9AM EST

Please send your homework to our course GA Dan Martin at [email protected] .

Formalities

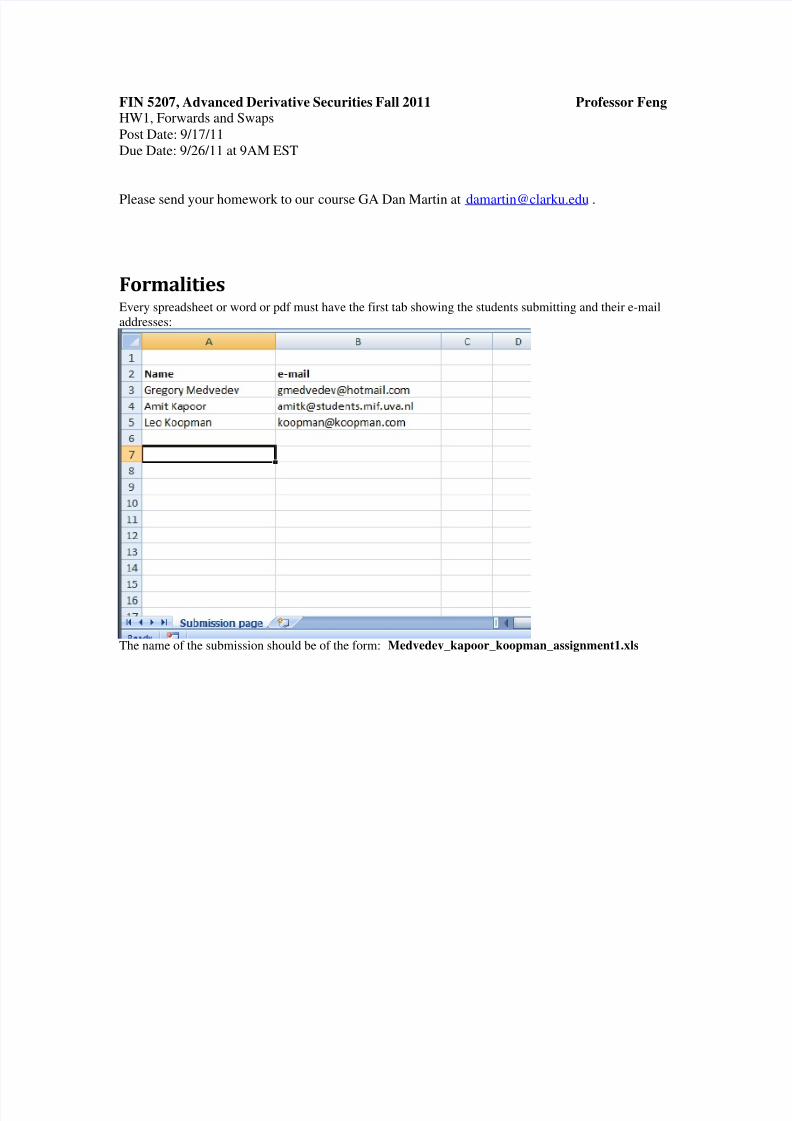

Every spreadsheet or word or pdf must have the first tab showing the students submitting and their e-mailaddresses:

The name of the submission should be of the form: Medvedev_kapoor_koopman_assignment1.xls

8/3/2019 PS1 Forward Contract Pricing 2011

http://slidepdf.com/reader/full/ps1-forward-contract-pricing-2011 2/3

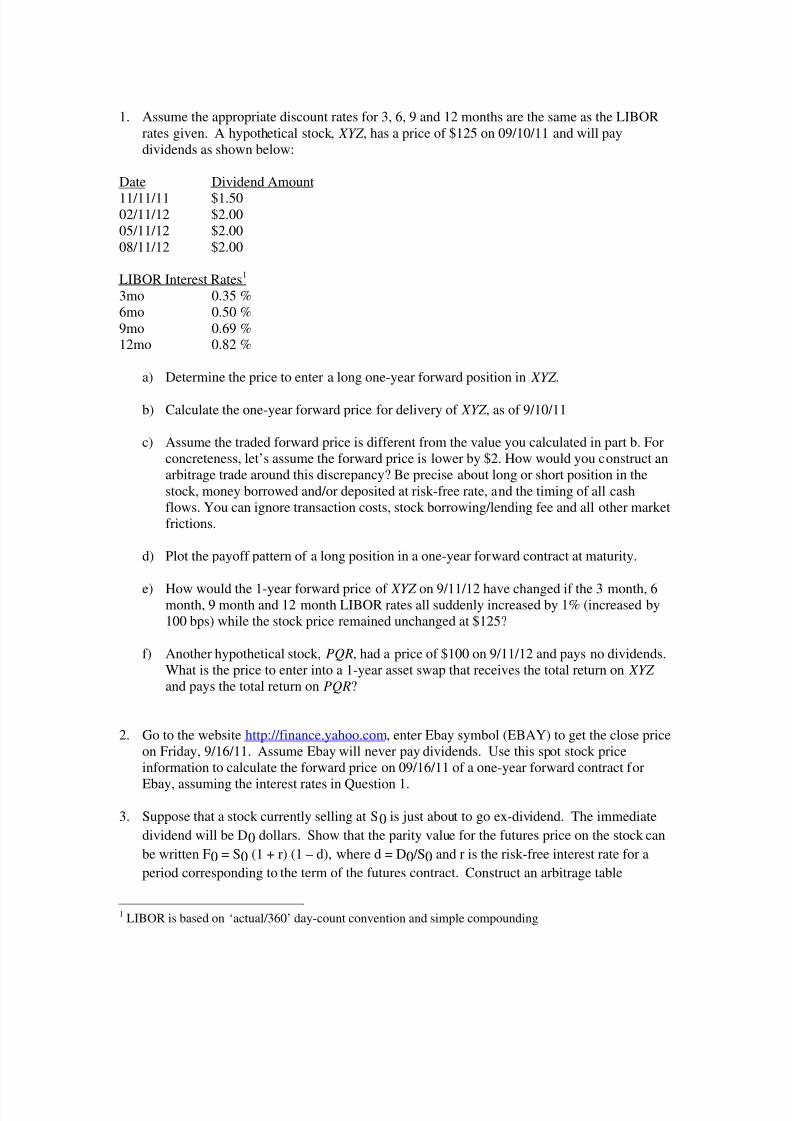

1. Assume the appropriate discount rates for 3, 6, 9 and 12 months are the same as the LIBOR

rates given. A hypothetical stock, XYZ , has a price of $125 on 09/10/11 and will paydividends as shown below:

Date Dividend Amount

11/11/11 $1.5002/11/12 $2.0005/11/12 $2.0008/11/12 $2.00

LIBOR Interest Rates1 3mo 0.35 %6mo 0.50 %9mo 0.69 %12mo 0.82 %

a) Determine the price to enter a long one-year forward position in XYZ .

b) Calculate the one-year forward price for delivery of XYZ , as of 9/10/11

c) Assume the traded forward price is different from the value you calculated in part b. Forconcreteness, let’s assume the forward price is lower by $2. How would you construct anarbitrage trade around this discrepancy? Be precise about long or short position in thestock, money borrowed and/or deposited at risk-free rate, and the timing of all cashflows. You can ignore transaction costs, stock borrowing/lending fee and all other marketfrictions.

d) Plot the payoff pattern of a long position in a one-year forward contract at maturity.

e) How would the 1-year forward price of XYZ on 9/11/12 have changed if the 3 month, 6month, 9 month and 12 month LIBOR rates all suddenly increased by 1% (increased by100 bps) while the stock price remained unchanged at $125?

f) Another hypothetical stock, PQR, had a price of $100 on 9/11/12 and pays no dividends.What is the price to enter into a 1-year asset swap that receives the total return on XYZ and pays the total return on PQR?

2. Go to the website http://finance.yahoo.com, enter Ebay symbol (EBAY) to get the close priceon Friday, 9/16/11. Assume Ebay will never pay dividends. Use this spot stock priceinformation to calculate the forward price on 09/16/11 of a one-year forward contract for

Ebay, assuming the interest rates in Question 1.

3. Suppose that a stock currently selling at S0 is just about to go ex-dividend. The immediate

dividend will be D0 dollars. Show that the parity value for the futures price on the stock can

be written F0 = S0 (1 + r) (1 – d), where d = D0 /S0 and r is the risk-free interest rate for a

period corresponding to the term of the futures contract. Construct an arbitrage table

1 LIBOR is based on ‘actual/360’ day-count convention and simple compounding

8/3/2019 PS1 Forward Contract Pricing 2011

http://slidepdf.com/reader/full/ps1-forward-contract-pricing-2011 3/3

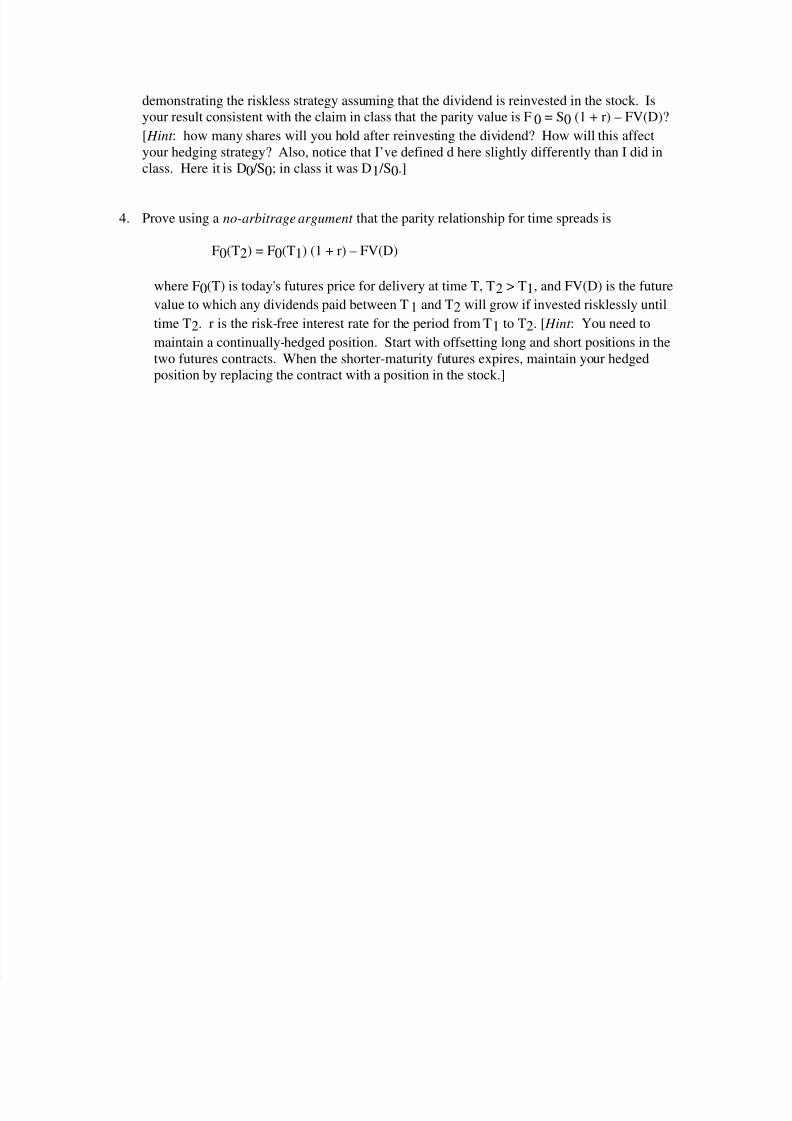

demonstrating the riskless strategy assuming that the dividend is reinvested in the stock. Isyour result consistent with the claim in class that the parity value is F0 = S0 (1 + r) – FV(D)?

[ Hint : how many shares will you hold after reinvesting the dividend? How will this affectyour hedging strategy? Also, notice that I’ve defined d here slightly differently than I did inclass. Here it is D0 /S0; in class it was D1 /S0.]

4. Prove using a no-arbitrage argument that the parity relationship for time spreads is

F0(T2) = F0(T1) (1 + r) – FV(D)

where F0(T) is today's futures price for delivery at time T, T2 > T1, and FV(D) is the future

value to which any dividends paid between T1 and T2 will grow if invested risklessly until

time T2. r is the risk-free interest rate for the period from T1 to T2. [ Hint : You need to

maintain a continually-hedged position. Start with offsetting long and short positions in thetwo futures contracts. When the shorter-maturity futures expires, maintain your hedgedposition by replacing the contract with a position in the stock.]