Embed Size (px)

Citation preview

PROXY PAPERJPMORGAN CHASE & CO.

NYSE: JPM ISIN: US46625H1005

MEETING DATE: 21 MAY 2013

RECORD DATE: 22 MARCH 2013

PUBLISH DATE: 06 MAY 2013

COMPANY DESCRIPTION

JPMorgan Chase & Co., a financial holding company,provides various financial services worldwide.

INDEX MEMBERSHIP:

DOW JONES COMPOSITE AVERAGE;DOW JONES GLOBAL TITANS 50; DOWJONES INDUSTRIAL AVERAGE; RUSSELL3000; S&P 500; RUSSELL 1000; S&P 100;S&P GLOBAL 100

SECTOR: FINANCIALS

INDUSTRY: DIVERSIFIED FINANCIAL SERVICES

COUNTRY OF TRADE: UNITED STATES

COUNTRY OF INCORPORATION: UNITED STATES

VOTING IMPEDIMENT: NONE

DISCLOSURES: THIS REPORT CONTAINS A DISCLOSURENOTE. TO VIEW, SEE APPENDIX

OWNERSHIP COMPANY PROFILE COMPENSATION PREVIOUS BOARD PEER COMPARISON VOTE RESULTS APPENDIX

2013 ANNUAL MEETING PROPOSAL ISSUE BOARD GLASS LEWIS CONCERNS

1.00 Election of Directors FOR SPLIT

1.01 Elect James A. Bell FOR AGAINST Restated financial statements

1.02 Elect Crandall C. Bowles FOR AGAINST Restated financial statementsAffiliate on a committee

1.03 Elect Stephen B. Burke FOR FOR

1.04 Elect David M. Cote FOR AGAINST Other governance issue

1.05 Elect James S. Crown FOR AGAINST Other governance issue

1.06 Elect James Dimon FOR FOR

1.07 Elect Timothy P. Flynn FOR FOR

1.08 Elect Ellen V. Futter FOR AGAINST Other unique issueOther governance issue

1.09 Elect Laban P. Jackson, Jr. FOR AGAINST Restated financial statements

1.10 Elect Lee R. Raymond FOR FOR

1.11 Elect William C. Weldon FOR FOR

2.00 Ratification of Auditor FOR FOR

3.00 Advisory Vote on Executive Compensation FOR FOR

4.00 Allow Shareholders to Act by Written Consent FOR FOR

5.00 Key Executive Performance Plan FOR FOR

6.00 Shareholder Proposal Regarding Independent BoardChairman

AGAINST FORAn independent chairman is betterable to oversee the executives of acompany and set a pro-shareholderagenda

7.00 Shareholder Proposal Regarding Retention of SharesUntil Retirement

AGAINST AGAINST

8.00 Shareholder Proposal Regarding Genocide-Free Investing AGAINST AGAINST

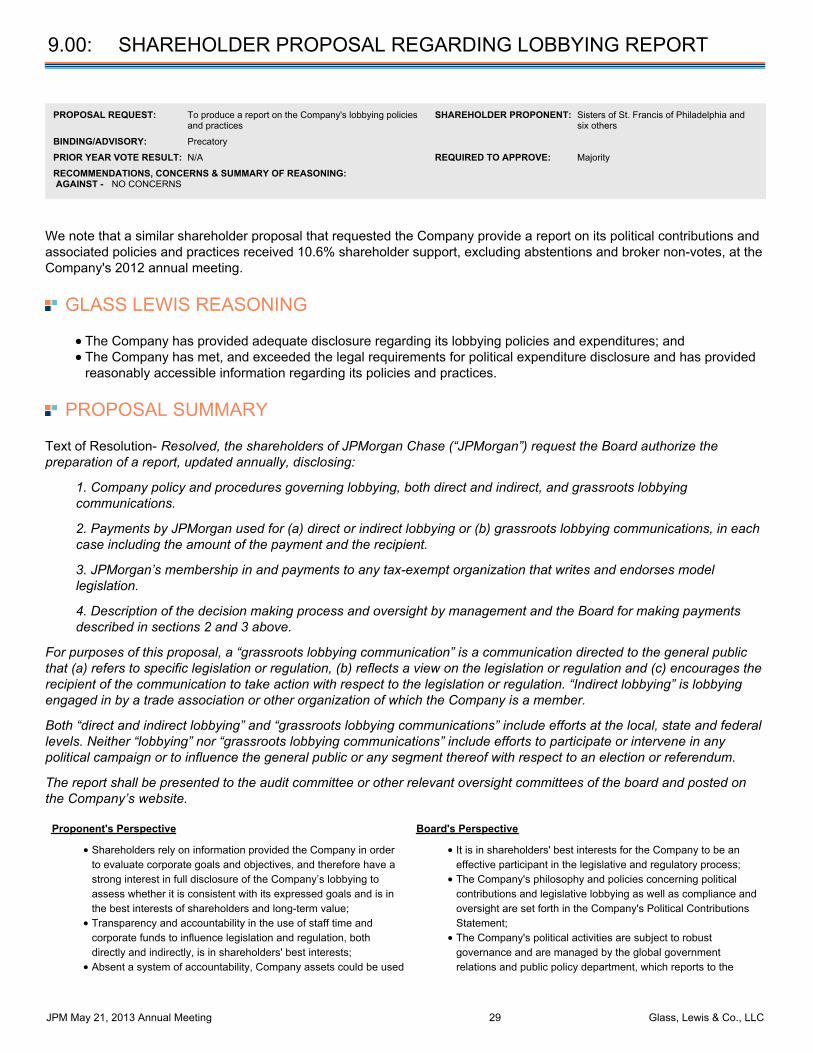

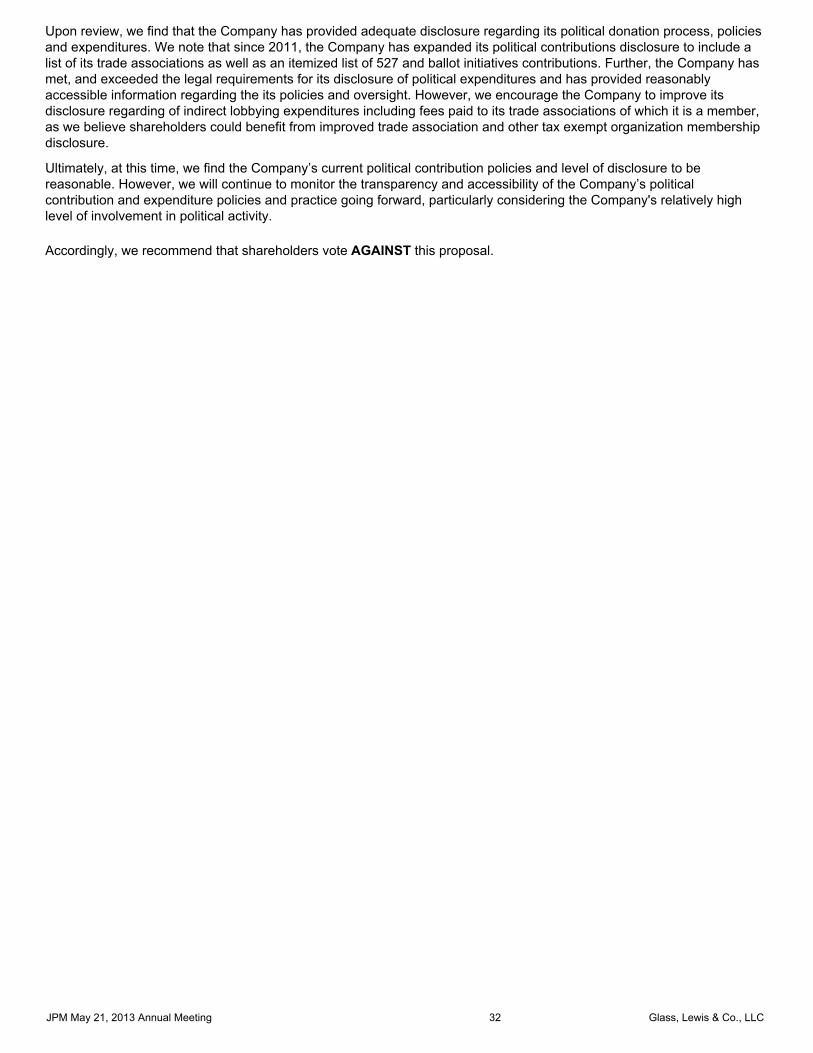

9.00 Shareholder Proposal Regarding Lobbying Report AGAINST AGAINST

JPM May 21, 2013 Annual Meeting 2 Glass, Lewis & Co., LLC

SHARE OWNERSHIP PROFILE

SHARE BREAKDOWN

1

SHARE CLASS Common Shares

SHARES OUTSTANDING 3,803.5 M

VOTES PER SHARE 1

INSIDE OWNERSHIP 0.53%

STRATEGIC OWNERS** 0.53%

FREE FLOAT 99.47%

SOURCE CAPITAL IQ AND GLASS LEWIS. AS OF 10-APR-2013

TOP 20 SHAREHOLDERS HOLDER OWNED* COUNTRY INVESTOR TYPE

1. BlackRock, Inc. 6.94% United States Traditional Investment Manager 2. The Vanguard Group, Inc. 4.46% United States Traditional Investment Manager 3. State Street Global Advisors, Inc. 4.34% United States Traditional Investment Manager 4. Wellington Management Company LLP 2.74% United States Traditional Investment Manager 5. Fidelity Investments 2.28% United States Traditional Investment Manager 6. T. Rowe Price Group, Inc. 1.92% United States Traditional Investment Manager 7. Capital Research and Management Company 1.72% United States Traditional Investment Manager 8. Northern Trust Global Investments 1.61% United States Traditional Investment Manager 9. MFS Investment Management, Inc. 1.33% United States Traditional Investment Manager 10. Invesco Ltd. 1.26% United States Traditional Investment Manager 11. Franklin Resources Inc. 1.26% United States Traditional Investment Manager 12. Columbia Management Investment Advisers, LLC 1.04% United States Traditional Investment Manager 13. BNY Mellon Asset Management 0.82% United States Traditional Investment Manager 14. Barrow, Hanley, Mewhinney & Strauss, Inc. 0.80% United States Traditional Investment Manager 15. Norges Bank Investment Management 0.77% Norway Traditional Investment Manager 16. UBS Global Asset Management 0.76% Switzerland Traditional Investment Manager 17. Teachers Insurance and Annuity Association College Retirement Equities Fund 0.73% United States Traditional Investment Manager 18. Merrill Lynch & Co. Inc., Asset Management Arm 0.68% United States Traditional Investment Manager 19. Harris Associates L.P. 0.66% United States Traditional Investment Manager 20. Geode Capital Management, LLC 0.66% United States Traditional Investment Manager

*COMMON STOCK EQUIVALENTS (AGGREGATE ECONOMIC INTEREST) SOURCE: CAPITAL IQ. AS OF 10-APR-2013 **CAPITAL IQ DEFINES STRATEGIC SHAREHOLDER AS A PUBLIC OR PRIVATE CORPORATION, INDIVIDUAL/INSIDER, COMPANY CONTROLLED FOUNDATION,ESOP OR STATE OWNED SHARES OR ANY HEDGE FUND MANAGERS, VC/PE FIRMS OR SOVEREIGN WEALTH FUNDS WITH A STAKE GREATER THAN 5%.

SHAREHOLDER RIGHTS MARKET THRESHOLD COMPANY THRESHOLD1

VOTING POWER REQUIRED TO CALL A SPECIAL MEETING N/A 20% VOTING POWER REQUIRED TO ADD AGENDA ITEM 1%2 1%2 VOTING POWER REQUIRED FOR WRITTEN CONSENT N/A 50%

1N/A INDICATES THAT THE COMPANY DOES NOT PROVIDE THE CORRESPONDING SHAREHOLDER RIGHT.2SHAREHOLDERS MUST OWN THE CORRESPONDING PERCENTAGE OR SHARES WITH MARKET VALUE OF AT LEAST $2,000 FOR AT LEAST ONE YEAR.

JPM May 21, 2013 Annual Meeting 3 Glass, Lewis & Co., LLC

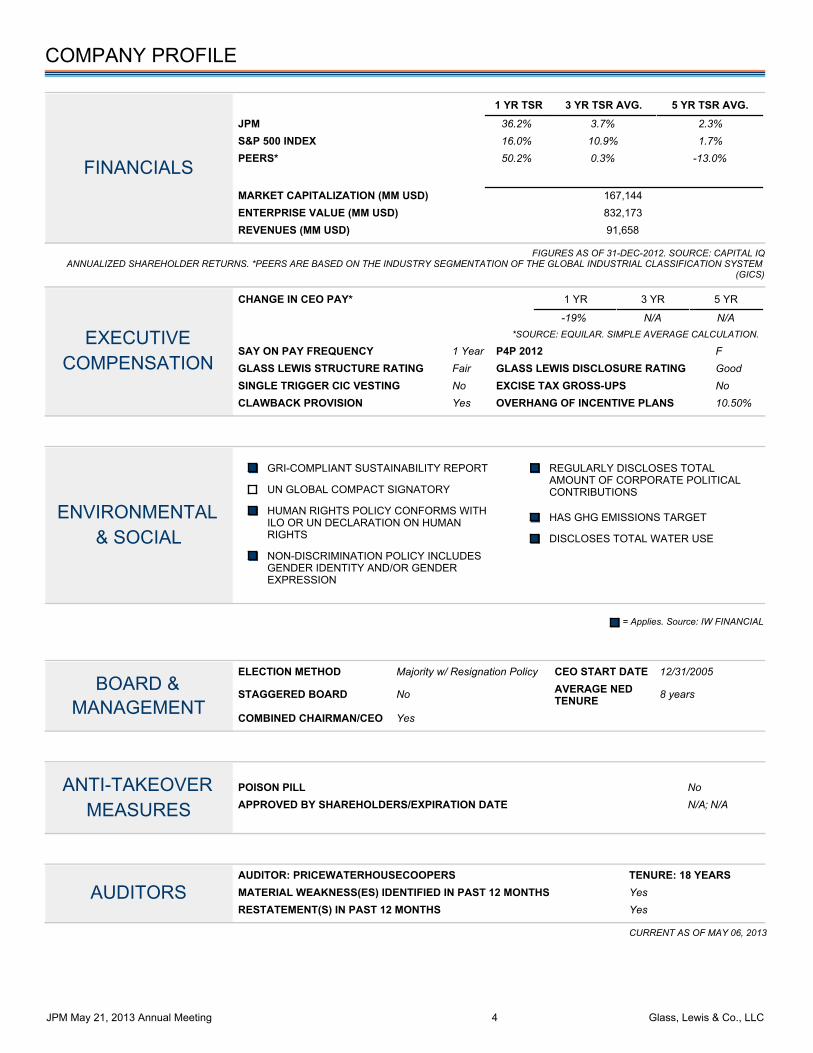

COMPANY PROFILE

FINANCIALS

1 YR TSR 3 YR TSR AVG. 5 YR TSR AVG.

JPM 36.2% 3.7% 2.3%S&P 500 INDEX 16.0% 10.9% 1.7%PEERS* 50.2% 0.3% -13.0%

MARKET CAPITALIZATION (MM USD) 167,144 ENTERPRISE VALUE (MM USD) 832,173 REVENUES (MM USD) 91,658

FIGURES AS OF 31-DEC-2012. SOURCE: CAPITAL IQANNUALIZED SHAREHOLDER RETURNS. *PEERS ARE BASED ON THE INDUSTRY SEGMENTATION OF THE GLOBAL INDUSTRIAL CLASSIFICATION SYSTEM

(GICS)

EXECUTIVECOMPENSATION

CHANGE IN CEO PAY* 1 YR 3 YR 5 YR

-19% N/A N/A *SOURCE: EQUILAR. SIMPLE AVERAGE CALCULATION.

SAY ON PAY FREQUENCY 1 Year P4P 2012 F GLASS LEWIS STRUCTURE RATING Fair GLASS LEWIS DISCLOSURE RATING Good SINGLE TRIGGER CIC VESTING No EXCISE TAX GROSS-UPS No CLAWBACK PROVISION Yes OVERHANG OF INCENTIVE PLANS 10.50%

ENVIRONMENTAL& SOCIAL

GRI-COMPLIANT SUSTAINABILITY REPORT

UN GLOBAL COMPACT SIGNATORY

HUMAN RIGHTS POLICY CONFORMS WITHILO OR UN DECLARATION ON HUMANRIGHTS

NON-DISCRIMINATION POLICY INCLUDESGENDER IDENTITY AND/OR GENDEREXPRESSION

REGULARLY DISCLOSES TOTALAMOUNT OF CORPORATE POLITICALCONTRIBUTIONS

HAS GHG EMISSIONS TARGET

DISCLOSES TOTAL WATER USE

= Applies. Source: IW FINANCIAL

BOARD &MANAGEMENT

ELECTION METHOD Majority w/ Resignation Policy CEO START DATE 12/31/2005

STAGGERED BOARD No AVERAGE NEDTENURE 8 years

COMBINED CHAIRMAN/CEO Yes

ANTI-TAKEOVERMEASURES

POISON PILL No APPROVED BY SHAREHOLDERS/EXPIRATION DATE N/A; N/A

AUDITORSAUDITOR: PRICEWATERHOUSECOOPERS TENURE: 18 YEARS MATERIAL WEAKNESS(ES) IDENTIFIED IN PAST 12 MONTHS Yes RESTATEMENT(S) IN PAST 12 MONTHS Yes

CURRENT AS OF MAY 06, 2013

JPM May 21, 2013 Annual Meeting 4 Glass, Lewis & Co., LLC

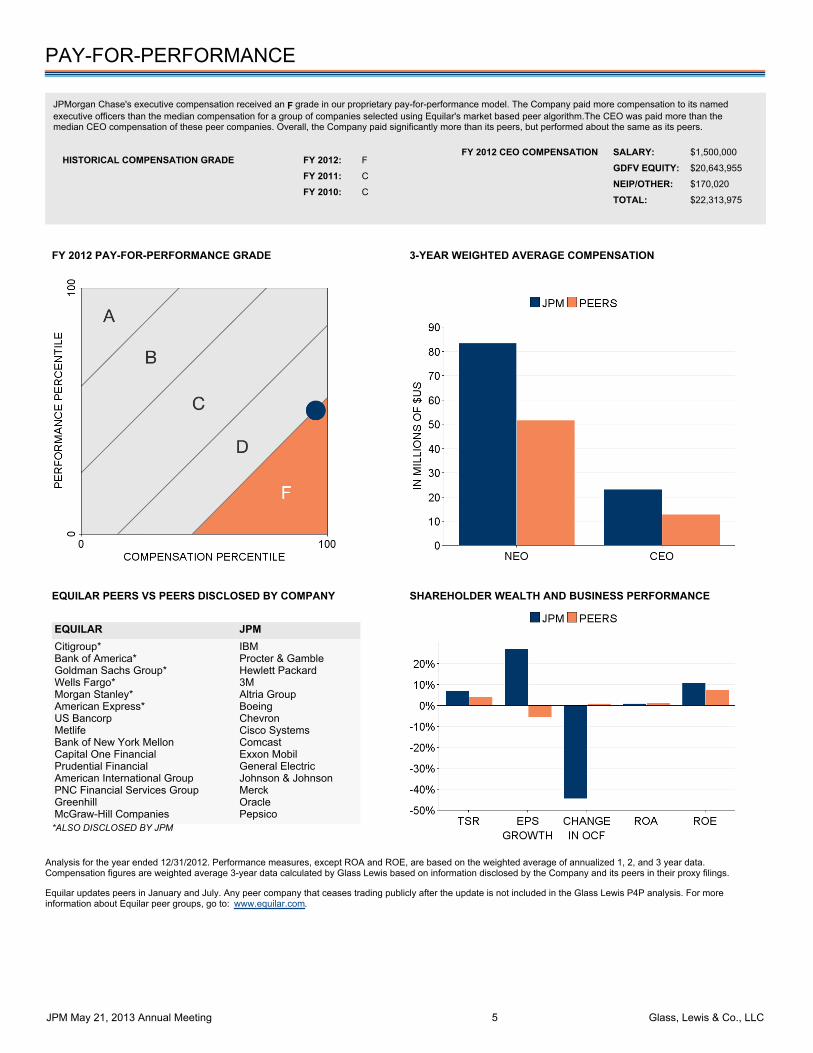

PAY-FOR-PERFORMANCE

JPMorgan Chase's executive compensation received an F grade in our proprietary pay-for-performance model. The Company paid more compensation to its namedexecutive officers than the median compensation for a group of companies selected using Equilar's market based peer algorithm.The CEO was paid more than themedian CEO compensation of these peer companies. Overall, the Company paid significantly more than its peers, but performed about the same as its peers.

HISTORICAL COMPENSATION GRADE FY 2012: F

FY 2011: C

FY 2010: C

FY 2012 CEO COMPENSATION SALARY: $1,500,000

GDFV EQUITY: $20,643,955

NEIP/OTHER: $170,020

TOTAL: $22,313,975

FY 2012 PAY-FOR-PERFORMANCE GRADE 3-YEAR WEIGHTED AVERAGE COMPENSATION

EQUILAR PEERS VS PEERS DISCLOSED BY COMPANY

EQUILAR JPMCitigroup* Bank of America* Goldman Sachs Group* Wells Fargo* Morgan Stanley* American Express* US Bancorp Metlife Bank of New York Mellon Capital One Financial Prudential Financial American International Group PNC Financial Services Group Greenhill McGraw-Hill Companies

IBM Procter & Gamble Hewlett Packard 3M Altria Group Boeing Chevron Cisco Systems Comcast Exxon Mobil General Electric Johnson & Johnson Merck Oracle Pepsico

*ALSO DISCLOSED BY JPM

SHAREHOLDER WEALTH AND BUSINESS PERFORMANCE

Analysis for the year ended 12/31/2012. Performance measures, except ROA and ROE, are based on the weighted average of annualized 1, 2, and 3 year data.Compensation figures are weighted average 3-year data calculated by Glass Lewis based on information disclosed by the Company and its peers in their proxy filings.

Equilar updates peers in January and July. Any peer company that ceases trading publicly after the update is not included in the Glass Lewis P4P analysis. For moreinformation about Equilar peer groups, go to: www.equilar.com.

JPM May 21, 2013 Annual Meeting 5 Glass, Lewis & Co., LLC

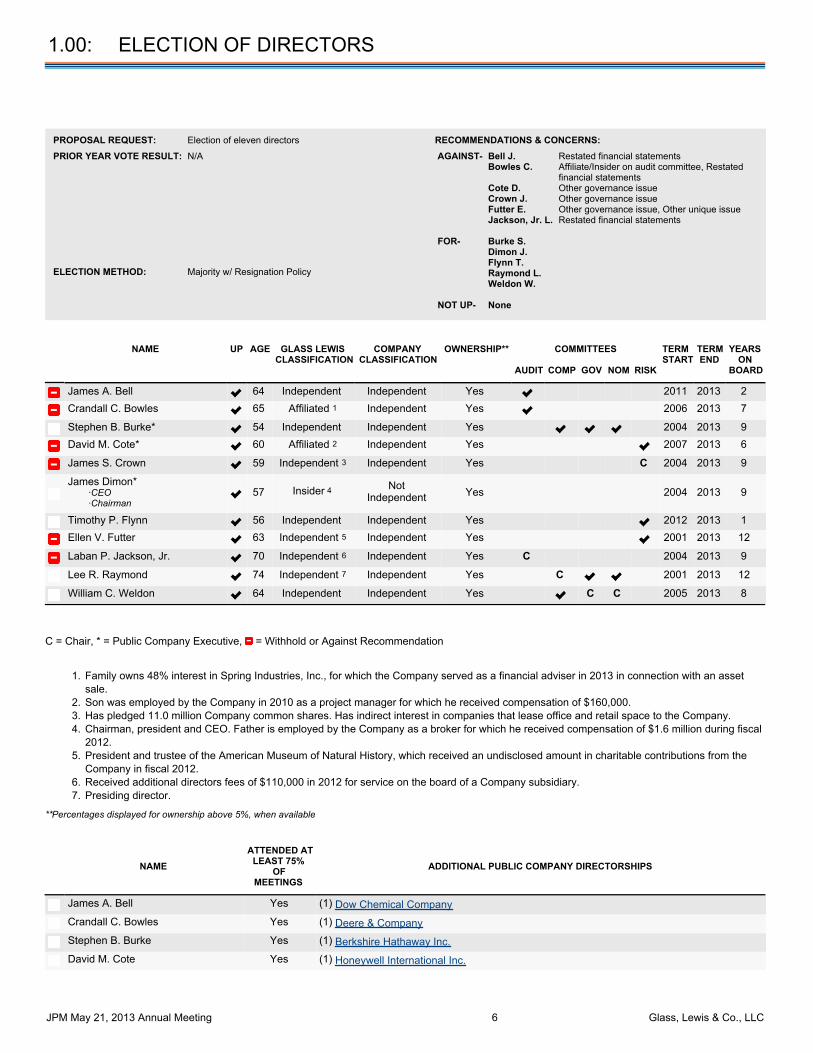

1.00: ELECTION OF DIRECTORS

PROPOSAL REQUEST: Election of eleven directors RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A AGAINST- Bell J. Restated financial statements

Bowles C. Affiliate/Insider on audit committee, Restatedfinancial statements

Cote D. Other governance issue Crown J. Other governance issue Futter E. Other governance issue, Other unique issue Jackson, Jr. L. Restated financial statements

FOR- Burke S.

Dimon J.Flynn T.Raymond L.Weldon W.

NOT UP- None

ELECTION METHOD: Majority w/ Resignation Policy

NAME UP AGE GLASS LEWISCLASSIFICATION

COMPANYCLASSIFICATION

OWNERSHIP** COMMITTEES TERMSTART

TERMEND

YEARSON

BOARDAUDIT COMP GOV NOM RISK

James A. Bell 64 Independent Independent Yes 2011 2013 2

Crandall C. Bowles 65 Affiliated 1 Independent Yes 2006 2013 7

Stephen B. Burke* 54 Independent Independent Yes 2004 2013 9

David M. Cote* 60 Affiliated 2 Independent Yes 2007 2013 6

James S. Crown 59 Independent 3 Independent Yes C 2004 2013 9

James Dimon*

·CEO·Chairman

57 Insider 4 NotIndependent Yes 2004 2013 9

Timothy P. Flynn 56 Independent Independent Yes 2012 2013 1

Ellen V. Futter 63 Independent 5 Independent Yes 2001 2013 12

Laban P. Jackson, Jr. 70 Independent 6 Independent Yes C 2004 2013 9

Lee R. Raymond 74 Independent 7 Independent Yes C 2001 2013 12

William C. Weldon 64 Independent Independent Yes C C 2005 2013 8

C = Chair, * = Public Company Executive, = Withhold or Against Recommendation

Family owns 48% interest in Spring Industries, Inc., for which the Company served as a financial adviser in 2013 in connection with an assetsale.

1.

Son was employed by the Company in 2010 as a project manager for which he received compensation of $160,000. 2.Has pledged 11.0 million Company common shares. Has indirect interest in companies that lease office and retail space to the Company. 3.Chairman, president and CEO. Father is employed by the Company as a broker for which he received compensation of $1.6 million during fiscal2012.

4.

President and trustee of the American Museum of Natural History, which received an undisclosed amount in charitable contributions from theCompany in fiscal 2012.

5.

Received additional directors fees of $110,000 in 2012 for service on the board of a Company subsidiary. 6.Presiding director. 7.

**Percentages displayed for ownership above 5%, when available

NAME ATTENDED AT

LEAST 75%OF

MEETINGS ADDITIONAL PUBLIC COMPANY DIRECTORSHIPS

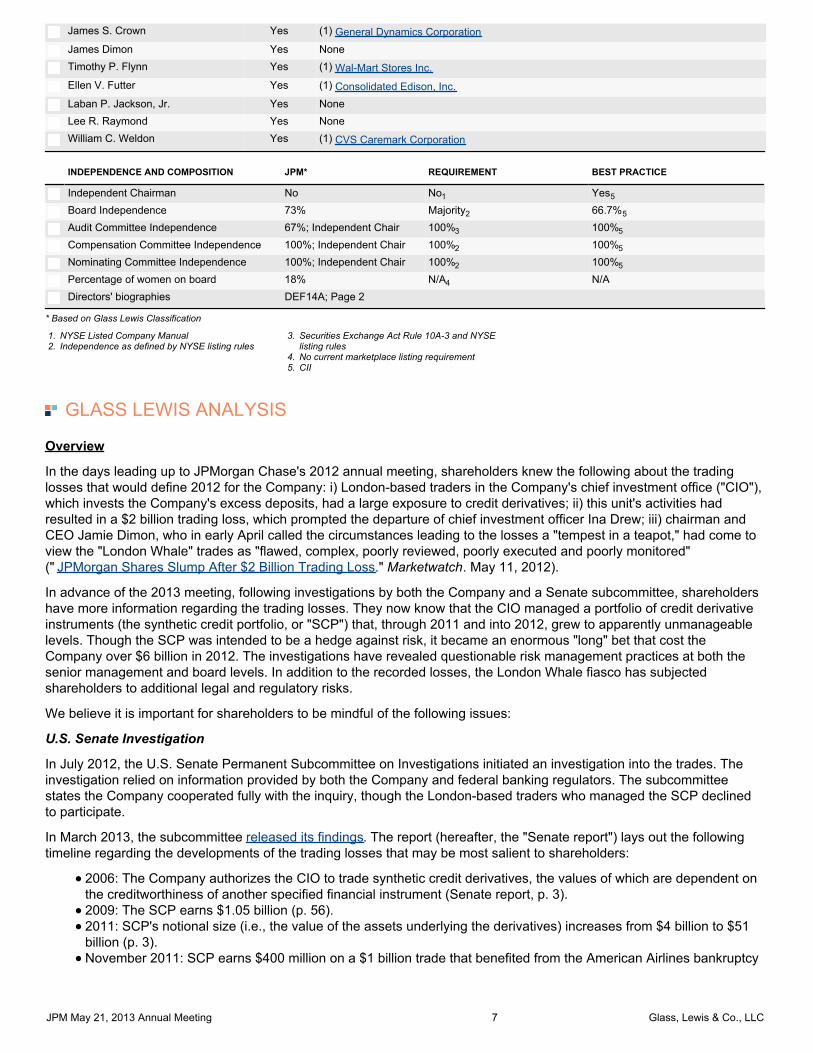

James A. Bell Yes (1) Dow Chemical Company

Crandall C. Bowles Yes (1) Deere & Company

Stephen B. Burke Yes (1) Berkshire Hathaway Inc.

David M. Cote Yes (1) Honeywell International Inc.

JPM May 21, 2013 Annual Meeting 6 Glass, Lewis & Co., LLC

James S. Crown Yes (1) General Dynamics Corporation

James Dimon Yes None

Timothy P. Flynn Yes (1) Wal-Mart Stores Inc.

Ellen V. Futter Yes (1) Consolidated Edison, Inc.

Laban P. Jackson, Jr. Yes None

Lee R. Raymond Yes None

William C. Weldon Yes (1) CVS Caremark Corporation

INDEPENDENCE AND COMPOSITION JPM* REQUIREMENT BEST PRACTICE

Independent Chairman No No1 Yes5

Board Independence 73% Majority2 66.7%5

Audit Committee Independence 67%; Independent Chair 100%3 100%5

Compensation Committee Independence 100%; Independent Chair 100%2 100%5

Nominating Committee Independence 100%; Independent Chair 100%2 100%5

Percentage of women on board 18% N/A4 N/A

Directors' biographies DEF14A; Page 2

* Based on Glass Lewis Classification

NYSE Listed Company Manual 1.Independence as defined by NYSE listing rules 2.

Securities Exchange Act Rule 10A-3 and NYSElisting rules

3.

No current marketplace listing requirement 4.CII 5.

GLASS LEWIS ANALYSIS

Overview

In the days leading up to JPMorgan Chase's 2012 annual meeting, shareholders knew the following about the tradinglosses that would define 2012 for the Company: i) London-based traders in the Company's chief investment office ("CIO"),which invests the Company's excess deposits, had a large exposure to credit derivatives; ii) this unit's activities hadresulted in a $2 billion trading loss, which prompted the departure of chief investment officer Ina Drew; iii) chairman andCEO Jamie Dimon, who in early April called the circumstances leading to the losses a "tempest in a teapot," had come toview the "London Whale" trades as "flawed, complex, poorly reviewed, poorly executed and poorly monitored"(" JPMorgan Shares Slump After $2 Billion Trading Loss." Marketwatch. May 11, 2012).

In advance of the 2013 meeting, following investigations by both the Company and a Senate subcommittee, shareholdershave more information regarding the trading losses. They now know that the CIO managed a portfolio of credit derivativeinstruments (the synthetic credit portfolio, or "SCP") that, through 2011 and into 2012, grew to apparently unmanageablelevels. Though the SCP was intended to be a hedge against risk, it became an enormous "long" bet that cost theCompany over $6 billion in 2012. The investigations have revealed questionable risk management practices at both thesenior management and board levels. In addition to the recorded losses, the London Whale fiasco has subjectedshareholders to additional legal and regulatory risks.

We believe it is important for shareholders to be mindful of the following issues:

U.S. Senate Investigation

In July 2012, the U.S. Senate Permanent Subcommittee on Investigations initiated an investigation into the trades. Theinvestigation relied on information provided by both the Company and federal banking regulators. The subcommitteestates the Company cooperated fully with the inquiry, though the London-based traders who managed the SCP declinedto participate.

In March 2013, the subcommittee released its findings. The report (hereafter, the "Senate report") lays out the followingtimeline regarding the developments of the trading losses that may be most salient to shareholders:

2006: The Company authorizes the CIO to trade synthetic credit derivatives, the values of which are dependent onthe creditworthiness of another specified financial instrument (Senate report, p. 3).2009: The SCP earns $1.05 billion (p. 56).2011: SCP's notional size (i.e., the value of the assets underlying the derivatives) increases from $4 billion to $51billion (p. 3).November 2011: SCP earns $400 million on a $1 billion trade that benefited from the American Airlines bankruptcy(p. 35).

JPM May 21, 2013 Annual Meeting 7 Glass, Lewis & Co., LLC

(p. 35).December 2011: Mr. Dimon orders the CIO to reduce risk weighted assets ("RWA"), such as credit derivatives (p.35).January 2012: SCP breaches its Value at Risk ("VaR") limit (p. 173); the Company implements a new VaR modelunder which the SCP does not breach risk limits (p. 179); CIO traders begin using non-standard valuations of SCPassets (p. 106).March 2012: The CIO acquires $40 billion more in notional size of "long" credit derivatives, even as values for suchinstruments declined (p. 82); CIO's valuation of SCP decreases loss estimate by $432 million (p. 5); SCP losses arenot discussed by management at a meeting of the board's risk policy committee (p. 162); Ina Drew orders SCPtraders to stop trading, as counterparties were trading to take advantage of the SCP's large position (p. 85).April 2012: Bloomberg and The Wall Street Journal publish stories regarding the SCP; on April 13, the bankreleases a Form 8-K that discloses first quarter VaR without disclosing the shift to a new VaR model (p. 13); duringan earnings call April 14, Mr. Dimon refers to the notoriety surrounding the issue as a "tempest in a teapot"; Mr.Dimon requests an analysis of SCP's effectiveness as a hedge but received no response from Ms. Drew or theCIO traders (p. 273).May 2012: The Company discloses that SCP lost $2 billion in the second quarter and that the VaR model had beenswitched; CIO traders are terminated; Ina Drew resigns.

The Senate report also criticizes Company management (including Mr. Dimon) for its statements describing the intent ofthe SCP as a hedge against losses rather than a bet seeking profits and the bank's disclosure of the its transparency withregulators.

Findings of Internal Review

In May 2012, the board formed the Board Review Committee to oversee an internal review of the losses, to assess theCompany’s risk management processes, and to report to the board its findings and recommendations. In January 2013,the findings of the internal review and the Board Review Committee were released. The internal review concluded that inthe first quarter of 2012 CIO’s risk management had been ineffective in dealing with the growth and complexity of theSCP.

The review drew the following conclusions regarding the bank's risk management:

The CIO lacked a robust risk committee structure;The CIO’s risk limits were insufficiently granular and should have been reassessed in light of the positions beingadded to the SCP in the first quarter of 2012;CIO risk management was insufficiently engaged in the approval and implementation during the first quarter of2012 of a new CIO Value-at-Risk (“VaR”) model related to the portfolio (before that model was discontinued andthe previous model was restored); andThere was inadequate reporting to management of risk issues relating to the portfolio.

In order to correct these deficiencies, the Company has appointed a new Chief Risk Officer for CIO/Treasury/Corporate(“CTC”), added resources in CIO risk management, created new risk committees to improve governance and controls,and introduced more specific risk limits for CIO.

Notably for shareholders, the report states on page 92 that the CIO participated in a bank-wide annual incentivecompensation plan overseen by the compensation committee. Awards under the plan are discretionary and non-formulaic,and compensation is dependent on multiple factors that can be adjusted and modified. The report concludes that theCIO's compensation structure did not unduly incentivize the trading activities that led to the losses.

Consent Orders with Federal Reserve and OCC

In January 2013, the Company entered into consent Orders with the Federal Reserve and with the Office of theComptroller of the Currency ("OCC") relating to their reviews of the trading losses. These orders relate to riskmanagement, model governance and other control functions related to trading activities. The Company states that manyof the actions required by the consent orders have already been implemented. The Senate report discloses that the OCCcriticized management's oversight of the CIO in a November 2012 letter, which stated: "[b]usiness management wasallowed to operate with little effective challenge from either the board or executive management." Further, The Wall StreetJournal has reported that in April 2013 the OCC stated to Mr. Dimon and the board that regulators don't trust Companymanagement ("For Dimon, Unfamiliar Heat." Wall Street Journal. May 4, 2013).

Current Status of Trading Losses

For 2012, the CIO reported over $6.2 billion of losses from the portfolio. In July 2012, the Company transferred a portionof the synthetic credit portfolio to CIB, which the Company states has the expertise, trading platforms and market franchise

JPM May 21, 2013 Annual Meeting 8 Glass, Lewis & Co., LLC

to manage the positions. The Company states the portfolio experienced modest losses following the transfer.

Material Weakness and Restatement

On July 13, 2012, the Company reported a material weakness in its internal control over financial reporting at March 31,2012. This weakness related to the valuation control function for the SCP during the first quarter of 2012. The Companyalso concluded that its disclosure controls and procedures were not effective for the same period. The Companyundertook remediation efforts, including enhancing management supervision of valuation matters, and states the controldeficiency was substantially remediated by June 30, 2012, and was fully remediated by September 30, 2012.

On August 9, 2012, the Company restated its financial statements for the quarter ended March 31, 2012. Therestatement related to valuations of positions in the synthetic credit portfolio. The restatement had the effect of reducingthe Company’s reported net income for the three months by $459 million.

In connection, the Company recouped up to two years of compensation from Ms. Drew and some of the tradersresponsible for managing the portfolio ("JPMorgan's Drew Forfeits Two Years' Pay as ManagersOusted." BloombergBusinessweek. July 13, 2012).

Fiscal 2012 Performance and 2013 Stress Test Results

Despite the trading losses, the Company reported increased income in 2012 of $21.3 billion ($5.20 per share) andrevenue of $97.0 billion. The Company's return on equity was 11%, level with 2011 performance. The Company endedthe year with a Basel I Tier 1 common ratio of 11%, up from 10.1% a year earlier, and its estimated Basel III Tier 1common ratio was approximately 8.7%.

Following the annual test by the Federal Reserve of the 19 largest banks' financial strength under hypothetical scenarios,the Company was authorized to repurchase an additional $6 billion in common shares over the next twelve months. TheCompany halted its share repurchases in May 2012. Also, the Fed authorized an increase in the quarterly dividend to$0.38 per share.

However, the Fed has required the Company to submit an additional capital plan by the end of the third quarteraddressing perceived weaknesses in the Company’s capital planning processes. The Company was one of five banksthat did not receive unconditional support of their planned capital actions. The Fed reportedly had concerns about theCompany’s forecasts for losses and revenues in a crisis scenario ("Fed Rebukes Goldman Sachs and JPMorgan ChaseOver Capital Plans." The New York Times. March 14, 2013). Following its review, the Fed can require the Company tomodify its dividend and buyback plans distributions.

Concerns have also arisen regarding the Company's creditworthiness. In 2012, Moody’s and Fitch downgraded theCompany's debt ratings and at year-end Moody’s and S&P had the Company on “negative” outlook. The rating agencieshave indicated that further control failures or a significant increase in risk taking could cause a downgrade in rating.

Legal and Regulatory Risk: Medium

In its most recent Form 10-K, the Company states the maximum aggregate of reasonably possible losses from its legalcontingencies is $6.1 billion, up from $5.1 billion the previous year. The Company has reported litigation expenses of $5.0billion, $4.9 billion and $7.4 billion for 2012, 2011 and 2010, respectively.

In addition to the matters discussed below, the Company continues to face risks from lawsuits and regulatory mattersstemming from the following matters: the Company's mortgage assets and practices; mortgage repurchase claims byFannie Mae and similar entities; past sales of asset-backed securities; bond issues by the cities of Milan, Italy andJefferson, Alabama; its management of investments by Ambac Guaranty and others; the LIBOR-rigging scandal; theBernie Madoff fraud; the MF Global bankruptcy; and the Lehman Brothers bankruptcy.

Shareholder Lawsuits and Government Investigations in Response to Trading Losses

The Company discloses a consolidated shareholder class action, a consolidated class action brought under the EmployeeRetirement Income Security Act (“ERISA”), shareholder derivative actions, and government investigations relating to theLondon Whale losses. The complaints alleges that current and former officers made false or misleading statementsconcerning CIO’s role, the Company's risk management practices and its financial results. Most of the matters arepending in federal court in New York.

In addition, the Company has received requests for information from Congress, the OCC, the Federal Reserve, the U.S.Department of Justice (the “DOJ”), the Securities and Exchange Commission (the “SEC”), the Commodity FuturesTrading Commission (the “CFTC”), the UK Financial Services Authority, the State of Massachusetts and othergovernment agencies.

JPM May 21, 2013 Annual Meeting 9 Glass, Lewis & Co., LLC

The Company states it is cooperating with these investigations and appears to be intent on repairing its relationships withregulators. Indeed, the Company has organized a town-hall style meeting in coming weeks in which Mr. Dimon willdiscuss risk management concerns with OCC examiners ("For Dimon, Unfamiliar Heat." Wall Street Journal. May 4,2013).

Volcker Rule

In the view of some (including Carl Levin, the chairman of the Senate subcommittee that conducted the review of thetrading losses), the London Whale losses served to justify the provisions of the Dodd-Frank Act prohibiting proprietarytrading and restricting the activities involving private equity and hedge funds (the “Volcker Rule”). ("Volcker Rule AuthorSays JPMorgan Loss Highlights Loophole."Los Angeles Times. May 11, 2012). During the April 2013 earnings call withanalysts in which the SCP losses were discussed, former CFO Doug Braunstein stated the bank believed the Whaletrades would be consistent with the Volcker Rule. In the Form 10-K, the Company states it ceased some prohibitedproprietary trading activities during 2010 and has since exited substantially all such activities. The provisions of theVolcker rule are expected to be finalized in 2013.

Independent Foreclosure Review

In January 2013, the Company and other financial institutions entered into a settlement agreement with the OCC and theFed which terminated a review of banks' foreclosure practices. Under this settlement, the Company will pay $753 millioninto a fund for qualified borrowers and also committed an additional $1.2 billion to foreclosure prevention actions (includingmodifications, short sales and other borrower relief).

Senate Legislation Targeting "Too Big to Fail" Banks

In April 2013, U.S. Senators Sherrod Brown (Democrat from Ohio) and David Vitter (Republican from Louisiana)introduced a bill that would require banks having more than $500 billion in assets (including the Company) to maintaincapital reserves of 15% (equity as a portion of assets) and limit the "risk-weighting" of assets. It is unclear whether thelegislation has significant support among other senators.

Bidding Practices in Power Markets

In March 2013, the Federal Energy regulation Commission told the Company that it had determined that Companytraders had manipulated electricity markets in California and Michigan in 2010 and 2011. The Company states it willdefend against the charges ("FERC Finds JPMorgan Manipulated Power Trading." Reuters. May 3, 2013).

Board Concerns

Change to Win "Vote No" Campaign

In March 2013, CtW Investment Group ("CtW") wrote to presiding director Lee Raymond to urge him not to re-nominatethree directors who served on the Company's risk policy committee during the development of the Whale losses (directorsCote, Crown and Futter; director Flynn joined the board later). CtW, which works with union pension funds on activistshareholder campaigns, argues that the risk committee lacks banking and trading experience, the board's review of thetrading losses failed to cite the committee for its poor oversight in the matter, and that recent assessments of theCompany's risk management by regulators suggest that the board's risk oversight framework is lacking.

Pledging of Stock by Director Crown

As in last year's proxy filing, the Company disclose this year that director Crown has pledged 11.0 million Companycommon shares as collateral. Based on the disclosure, it is unclear if the shares are held by brokers in margin loanaccounts or if the collateral has been posted on outstanding loans. Director Burke has also pledged 32,107 commonshares. The Company states that its directors have promised to retain all Company shares while they serve as a director.

Given the aggregate value of director Crown's pledged shares, we believe shareholders may benefit from moreinformation regarding the circumstances in which this collateral may be called.

Response to Shareholder Proposal

At last year’s annual meeting, a shareholder proposal asking the board to grant shareholders the ability to act by writtenconsent received the support of approximately 52% of the voted shares. This year, the Company has proposed anamendment to its certificate of incorporation (Proposal 4) that would grant shareholders the right to act by consent,subject to several advance notice requirements. While we believe the board could have provided shareholders with a lessrestrictive ability to take action without a meeting, we nonetheless believe that the board has responded adequately to thisshareholder initiative.

Shareholder Proposal Regarding Separation of Chairman and CEO

JPM May 21, 2013 Annual Meeting 10 Glass, Lewis & Co., LLC

Also at last year's meeting, when the full extent of the London Whale losses was unknown, a shareholder proposal askingthe board to adopt a policy that the chairman of the board be an independent director was defeated, receiving supportfrom about 40% of the voted shares. A similar proposal appears on this year's ballot and the board again opposes it. TheNew York Times has reported that some board members and shareholders think that, if the proposal is approved, Mr.Dimon might resign rather than accept a decreased role at the Company. The Times also reports that the board ismeeting with shareholders in advance of the meeting to assure them that it is in command of the issues discussed above("JPMorgan Works to Avert Split of Chief and Chairman Roles." The New York Times. April 5, 2013). Please refer toProposal 6 of this report for our analysis of this issue.

Vote Recommendation

We recommend that shareholders vote against the following nominees based on the following issues:

Audit Committee Oversight of Internal Controls

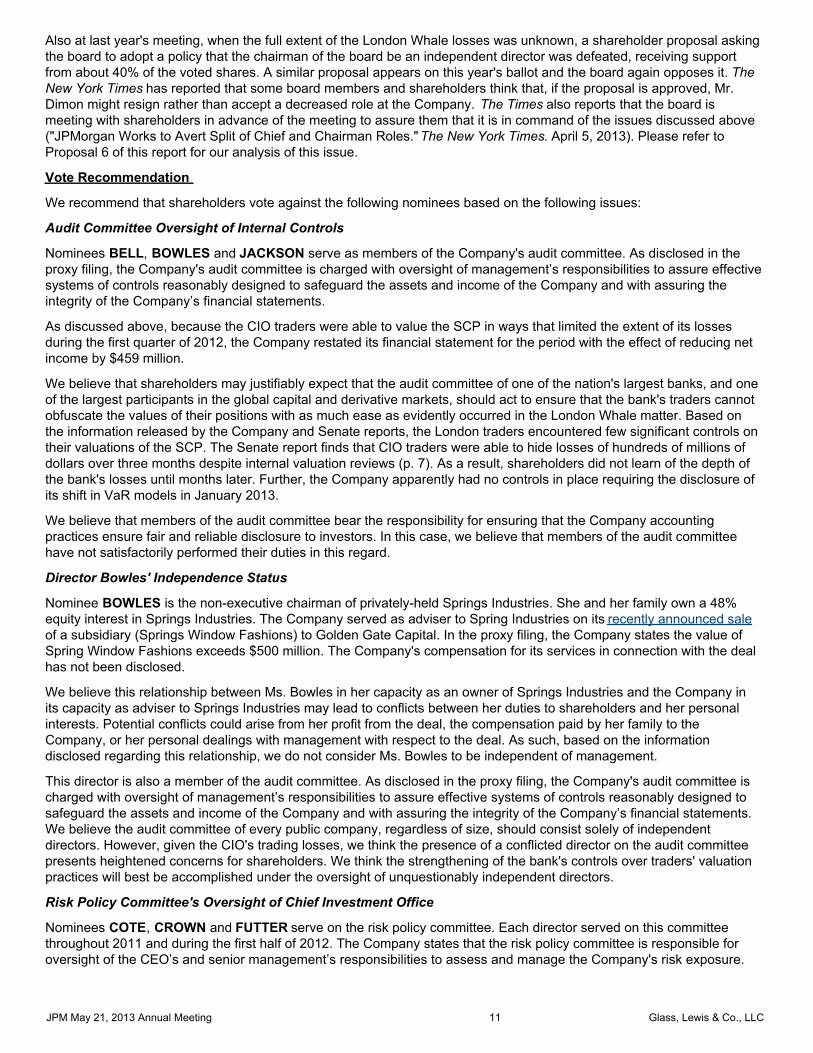

Nominees BELL, BOWLES and JACKSON serve as members of the Company's audit committee. As disclosed in theproxy filing, the Company's audit committee is charged with oversight of management’s responsibilities to assure effectivesystems of controls reasonably designed to safeguard the assets and income of the Company and with assuring theintegrity of the Company’s financial statements.

As discussed above, because the CIO traders were able to value the SCP in ways that limited the extent of its lossesduring the first quarter of 2012, the Company restated its financial statement for the period with the effect of reducing netincome by $459 million.

We believe that shareholders may justifiably expect that the audit committee of one of the nation's largest banks, and oneof the largest participants in the global capital and derivative markets, should act to ensure that the bank's traders cannotobfuscate the values of their positions with as much ease as evidently occurred in the London Whale matter. Based onthe information released by the Company and Senate reports, the London traders encountered few significant controls ontheir valuations of the SCP. The Senate report finds that CIO traders were able to hide losses of hundreds of millions ofdollars over three months despite internal valuation reviews (p. 7). As a result, shareholders did not learn of the depth ofthe bank's losses until months later. Further, the Company apparently had no controls in place requiring the disclosure ofits shift in VaR models in January 2013.

We believe that members of the audit committee bear the responsibility for ensuring that the Company accountingpractices ensure fair and reliable disclosure to investors. In this case, we believe that members of the audit committeehave not satisfactorily performed their duties in this regard.

Director Bowles' Independence Status

Nominee BOWLES is the non-executive chairman of privately-held Springs Industries. She and her family own a 48%equity interest in Springs Industries. The Company served as adviser to Spring Industries on its recently announced saleof a subsidiary (Springs Window Fashions) to Golden Gate Capital. In the proxy filing, the Company states the value ofSpring Window Fashions exceeds $500 million. The Company's compensation for its services in connection with the dealhas not been disclosed.

We believe this relationship between Ms. Bowles in her capacity as an owner of Springs Industries and the Company inits capacity as adviser to Springs Industries may lead to conflicts between her duties to shareholders and her personalinterests. Potential conflicts could arise from her profit from the deal, the compensation paid by her family to theCompany, or her personal dealings with management with respect to the deal. As such, based on the informationdisclosed regarding this relationship, we do not consider Ms. Bowles to be independent of management.

This director is also a member of the audit committee. As disclosed in the proxy filing, the Company's audit committee ischarged with oversight of management’s responsibilities to assure effective systems of controls reasonably designed tosafeguard the assets and income of the Company and with assuring the integrity of the Company’s financial statements.We believe the audit committee of every public company, regardless of size, should consist solely of independentdirectors. However, given the CIO's trading losses, we think the presence of a conflicted director on the audit committeepresents heightened concerns for shareholders. We think the strengthening of the bank's controls over traders' valuationpractices will best be accomplished under the oversight of unquestionably independent directors.

Risk Policy Committee's Oversight of Chief Investment Office

Nominees COTE, CROWN and FUTTER serve on the risk policy committee. Each director served on this committeethroughout 2011 and during the first half of 2012. The Company states that the risk policy committee is responsible foroversight of the CEO’s and senior management’s responsibilities to assess and manage the Company's risk exposure.

JPM May 21, 2013 Annual Meeting 11 Glass, Lewis & Co., LLC

Shareholders who have read the management and Senate reports are no doubt concerned at the minor role the risk policycommittee played as the CIO built its large risk exposure in 2011 and 2012. The Senate report states that on March 20,2012, Ina Drew and CIO Chief Risk Officer Irvin Goldman participated in a meeting of the risk policy committee regardingthe CIO, and gave a presentation on the CIO’s investment portfolios and risk profile. The presentation did not disclose theSCP’s ongoing losses, risk limit breaches, increased portfolio size, or increased RWA (p. 83). The same day, thecommittee met with Company chief risk officer John Hogan; again, the SCP was not discussed, likely because Mr. Hoganapparently was unaware of the SCP's risks prior to April 2012 (p. 265).

While it seems clear that CIO management failed to disclose the risks of the SCP to the committee, shareholders shouldnote that neither the Company's internal reviews nor the Senate investigation suggest that the committee sought outinformation regarding the CIO's activities (even following the initial breach of the Company's VaR limits in January 2012)or that it asked sufficiently probing questions of management at committee meetings. This indicates to us that the riskpolicy committee was likely too willing to trust senior management's risk oversight and did not have meaningful reviewprocesses in place to cover instances of risk limit breaches or significant deviations in portfolio valuation.

We are concerned by the risk policy committee's evident failure to ensure that the Company's risk management processescould not be overridden by short-term profit interests. We are also troubled by the committee's failure to implementreporting processes that would notify the board of any unwarranted risks to shareholders. Shares can reasonably expectthat the risk committee of a bank should better monitor an issue as significant as the London Whale loss.

Director Futter's Prior Service at AIG

Nominee FUTTER served on the board of directors of American International Group, Inc. ("AIG") from 1999 to 2008.Specifically, Ms. Futter served on AIG's nominating and corporate governance committee in 2007 and 2008, and as amember of the finance committee, which was responsible for overseeing AIG's financial affairs and investment activities,in 2004. During her tenure, AIG built a massive and largely unhedged derivative exposure to mortgage-backed securities,culminating in $99 billion in reported losses for 2008, a $180 billion government rescue and an evisceration of shareholdervalue. Shortly after Ms. Futter joined AIG, the firm gave $36.5 million to the Museum of Natural History where, as notedabove, Ms. Futter served as President (Diane Brady and Marcia Vickers." AIG: What WentWrong." BloombergBusinessweek. April 11, 2005). Ms. Futter continues to serve as President of the Museum which hasreceived undisclosed donations from the Company for several years.

We have consistently recommended that Company shareholders vote to remove Ms. Futter based on her inability toeffectively monitor risk exposure during her tenure at AIG. Following the events of the past year, our opinion is unchanged.

Summary

Shareholders should be concerned that Company management was allowed to build a massive exposure to creditderivatives, switch VaR models following a breach of risk limits, and value its positions so to minimize losses, and that itwas able to do each of these things without triggering a board-level review or a mandatory containment of risk. For thereasons stated above, we think shareholders should hold the members of the audit and risk policy committees for theselapses of oversight.

Accordingly, we recommend that shareholders vote:

AGAINST: Bell; Bowles; Cote; Crown; Futter; Jackson, Jr.

FOR: Burke; Dimon; Flynn; Raymond; Weldon

JPM May 21, 2013 Annual Meeting 12 Glass, Lewis & Co., LLC

2.00: RATIFICATION OF AUDITOR

PROPOSAL REQUEST: Ratification of PricewaterhouseCoopers RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Advisory

REQUIRED TO APPROVE: Majority

AUDITOR OPINION: Unqualified

AUDITOR FEES 2012 2011 2010

Audit Fees: $59,500,000 $52,900,000 $50,400,000 Audit-RelatedFees:

$24,100,000 $25,700,000 $23,400,000

Tax Fees: $8,900,000 $7,500,000 $5,700,000 All OtherFees:

$ 0 $400,000 $2,700,000

Total Fees: $92,500,000 $86,500,000 $82,200,000

Auditor: PricewaterhouseCoopers

PricewaterhouseCoopers

PricewaterhouseCoopers

Years Serving Company: 18 Auditor Responsible forRestatement:

No

Alternate Dispute Resolution: No Auditor Liability Caps: No

GLASS LEWIS ANALYSIS

The fees paid for non-audit-related services are reasonable and the Company discloses appropriate information aboutthese services in its filings.

Accordingly, we recommend that shareholders vote FOR the ratification of the appointment of PricewaterhouseCoopersas the Company's auditor for fiscal year 2013.

JPM May 21, 2013 Annual Meeting 13 Glass, Lewis & Co., LLC

3.00: ADVISORY VOTE ON EXECUTIVE COMPENSATION

PROPOSAL REQUEST: Approval of Executive Pay Package PAY FOR PERFORMANCEGRADES:

FY 2012 FFY 2011 CFY 2010 C

PRIOR YEAR VOTE RESULT: 90.1%; Approved RECOMMENDATION: FOR

STRUCTURE: Fair

DISCLOSURE: Good

PROGRAM FEATURES 1

POSITIVE

STI-LTI payout balanceNo single-trigger CIC benefitsAnti-Hedging PolicyClawback policy for NEOsExecutive stock ownership guidelines for NEOs

NEGATIVE

Significant disconnect between pay andperformanceNo performance-vesting LTI awardsSTIP awards are discretionary

1 Both positive and negative compensation features are ranked according to Glass Lewis' view of their importance or severity

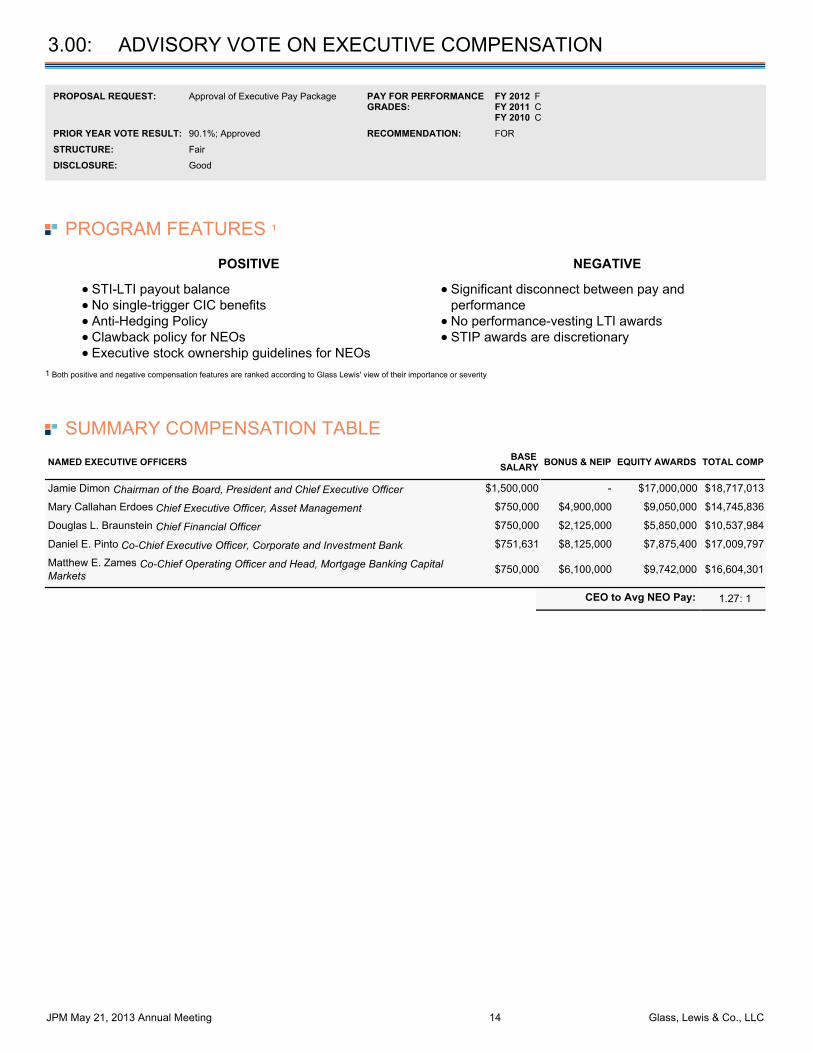

SUMMARY COMPENSATION TABLENAMED EXECUTIVE OFFICERS BASE

SALARY BONUS & NEIP EQUITY AWARDS TOTAL COMP

Jamie Dimon Chairman of the Board, President and Chief Executive Officer $1,500,000 - $17,000,000 $18,717,013

Mary Callahan Erdoes Chief Executive Officer, Asset Management $750,000 $4,900,000 $9,050,000 $14,745,836

Douglas L. Braunstein Chief Financial Officer $750,000 $2,125,000 $5,850,000 $10,537,984

Daniel E. Pinto Co-Chief Executive Officer, Corporate and Investment Bank $751,631 $8,125,000 $7,875,400 $17,009,797

Matthew E. Zames Co-Chief Operating Officer and Head, Mortgage Banking CapitalMarkets $750,000 $6,100,000 $9,742,000 $16,604,301

CEO to Avg NEO Pay: 1.27: 1

JPM May 21, 2013 Annual Meeting 14 Glass, Lewis & Co., LLC

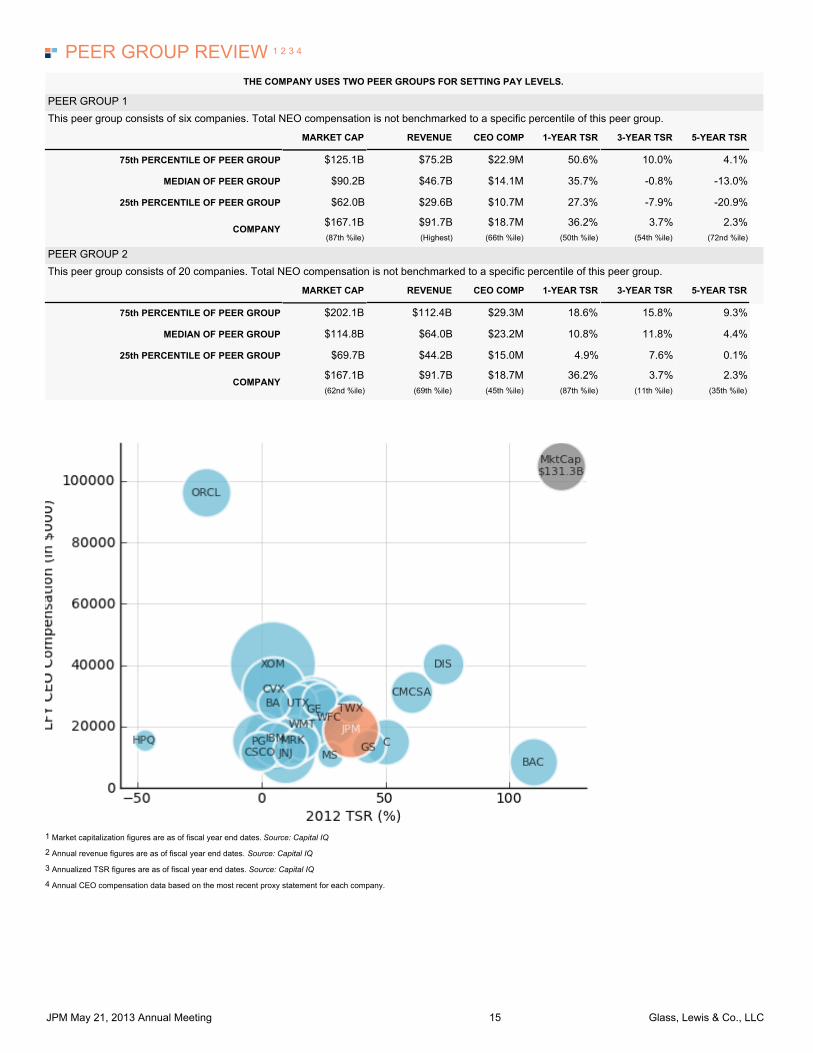

PEER GROUP REVIEW 1 2 3 4

THE COMPANY USES TWO PEER GROUPS FOR SETTING PAY LEVELS.

PEER GROUP 1This peer group consists of six companies. Total NEO compensation is not benchmarked to a specific percentile of this peer group.

MARKET CAP REVENUE CEO COMP 1-YEAR TSR 3-YEAR TSR 5-YEAR TSR

75th PERCENTILE OF PEER GROUP $125.1B $75.2B $22.9M 50.6% 10.0% 4.1%

MEDIAN OF PEER GROUP $90.2B $46.7B $14.1M 35.7% -0.8% -13.0%

25th PERCENTILE OF PEER GROUP $62.0B $29.6B $10.7M 27.3% -7.9% -20.9%

COMPANY$167.1B $91.7B $18.7M 36.2% 3.7% 2.3%(87th %ile) (Highest) (66th %ile) (50th %ile) (54th %ile) (72nd %ile)

PEER GROUP 2This peer group consists of 20 companies. Total NEO compensation is not benchmarked to a specific percentile of this peer group.

MARKET CAP REVENUE CEO COMP 1-YEAR TSR 3-YEAR TSR 5-YEAR TSR

75th PERCENTILE OF PEER GROUP $202.1B $112.4B $29.3M 18.6% 15.8% 9.3%

MEDIAN OF PEER GROUP $114.8B $64.0B $23.2M 10.8% 11.8% 4.4%

25th PERCENTILE OF PEER GROUP $69.7B $44.2B $15.0M 4.9% 7.6% 0.1%

COMPANY$167.1B $91.7B $18.7M 36.2% 3.7% 2.3%(62nd %ile) (69th %ile) (45th %ile) (87th %ile) (11th %ile) (35th %ile)

1 Market capitalization figures are as of fiscal year end dates. Source: Capital IQ

2 Annual revenue figures are as of fiscal year end dates. Source: Capital IQ

3 Annualized TSR figures are as of fiscal year end dates. Source: Capital IQ

4 Annual CEO compensation data based on the most recent proxy statement for each company.

JPM May 21, 2013 Annual Meeting 15 Glass, Lewis & Co., LLC

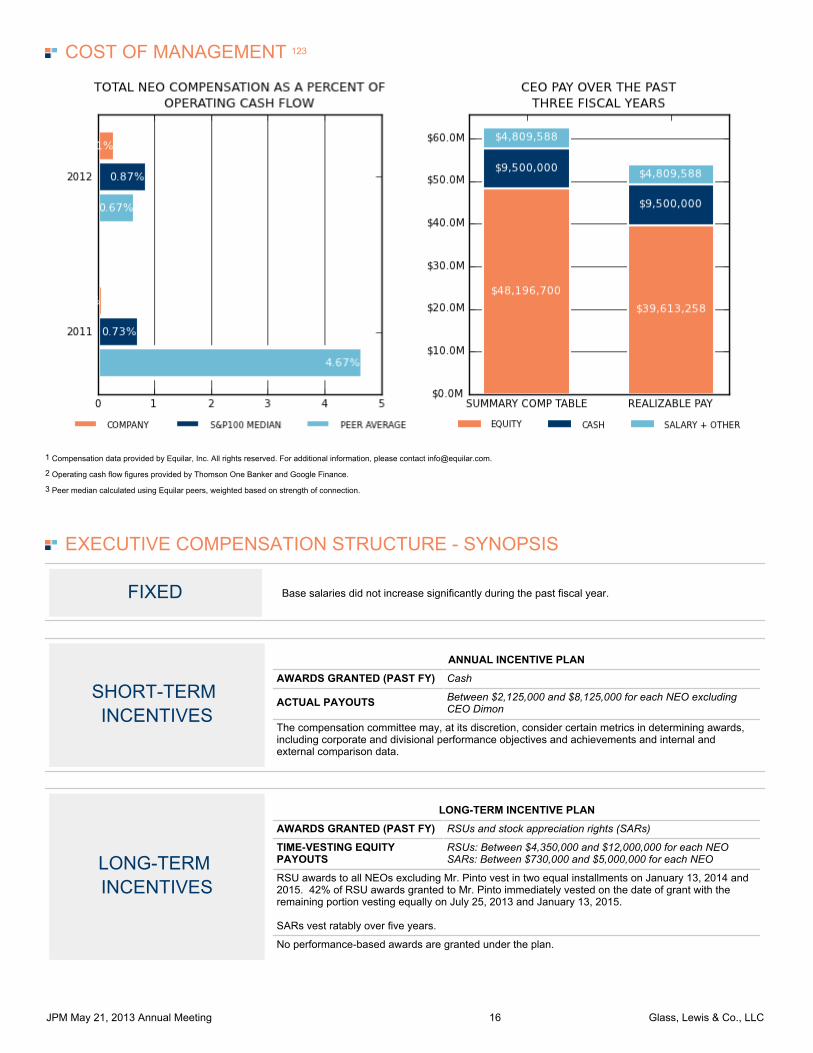

COST OF MANAGEMENT 123

1 Compensation data provided by Equilar, Inc. All rights reserved. For additional information, please contact [email protected].

2 Operating cash flow figures provided by Thomson One Banker and Google Finance.

3 Peer median calculated using Equilar peers, weighted based on strength of connection.

EXECUTIVE COMPENSATION STRUCTURE - SYNOPSIS

FIXED Base salaries did not increase significantly during the past fiscal year.

SHORT-TERMINCENTIVES

ANNUAL INCENTIVE PLAN

AWARDS GRANTED (PAST FY) Cash

ACTUAL PAYOUTS Between $2,125,000 and $8,125,000 for each NEO excludingCEO Dimon

The compensation committee may, at its discretion, consider certain metrics in determining awards,including corporate and divisional performance objectives and achievements and internal andexternal comparison data.

LONG-TERMINCENTIVES

LONG-TERM INCENTIVE PLAN

AWARDS GRANTED (PAST FY) RSUs and stock appreciation rights (SARs)

TIME-VESTING EQUITYPAYOUTS

RSUs: Between $4,350,000 and $12,000,000 for each NEO SARs: Between $730,000 and $5,000,000 for each NEO

RSU awards to all NEOs excluding Mr. Pinto vest in two equal installments on January 13, 2014 and2015. 42% of RSU awards granted to Mr. Pinto immediately vested on the date of grant with theremaining portion vesting equally on July 25, 2013 and January 13, 2015.

SARs vest ratably over five years.

No performance-based awards are granted under the plan.

JPM May 21, 2013 Annual Meeting 16 Glass, Lewis & Co., LLC

GLASS LEWIS ANALYSIS

This proposal seeks shareholder approval of a non-binding, advisory vote on the Company's executive compensation.Glass Lewis believes firms should fully disclose and explain all aspects of their executives' compensation in such a waythat shareholders can comprehend and analyze the company's policies and procedures. In completing our assessment,we consider, among other factors, the appropriateness of performance targets and metrics, how such goals and metricsare used to improve Company performance, the peer group against which the Company believes it is competing, whetherincentive schemes encourage prudent risk management and the board's adherence to market best practices.Furthermore, we also emphasize and evaluate the extent to which the Company links executive pay with performance.

OVERALL STRUCTURE : FAIR

We note the following concerns with the structure of the Company's compensation programs:

No Performance Formula The Company does not utilize an objective, formula-based approach to setting executive compensation levels. Rather, thecompensation committee determines LTI awards on a purely discretionary basis and considers the performancemeasures listed above to determine awards under the STI plan. We believe shareholders benefit when compensationlevels are based on metrics with pre-established goals and are thus demonstrably linked to the performance of thecompany, aligning the interests of management with those of shareholders. In this case, shareholders should be seriouslyconcerned with the Company's failure to implement formula-based incentive plans with objective metrics and goals.

Incentive Limits Executives are eligible to receive unlimited short-term compensation. We believe this runs contrary to best practices andshareholder interests, as management may receive excessive compensation that is not strictly tied to Companyperformance. We urge the Company to set and disclose individual caps on its short-term incentive plan so as to assureshareholders that executive pay will always be constrained by stated limits.

OVERALL DISCLOSURE : GOOD

Glass Lewis has thoroughly reviewed the Company's Compensation, Discussion & Analysis section of its most recentproxy statement, as well other relevant SEC filings. Upon review of the Company's complete executive compensationprogram, we find that the Company has provided good disclosure with regard to both its short-term and long-termincentive arrangements.

2012 PAY FOR PERFORMANCE : F

The Company has failed to link executive pay to corporate performance, as indicated by the "F" grade received by theCompany in Glass Lewis' pay-for-performance model. Shareholders should be concerned with this disconnect. A properlystructured pay program should motivate executives to drive corporate performance, thus aligning executive and long-termshareholder interests. In this case, as indicated by the failing grade, the Company has not done so. If we notice asustained failure in this area we may recommend that shareholders withhold votes from the compensation committeemembers as well.

SUMMARY

As noted earlier in our report, in April and May of 2012, the Company sustained enormous trading losses based ontransactions booked through its London branch, otherwise known as the "London Whale." The Company reported a $6.2million trading loss, and has restructured its executive compensation program around curbing and recouping payouts as aresult. The main features of its program include cutting CEO Dimon's compensation (2012 is about 50% less than 2011),along with the pay levels of now Vice Chairman (previously CFO) Braunstein, and extending its "protection-based vesting"provision.

JPM May 21, 2013 Annual Meeting 17 Glass, Lewis & Co., LLC

The above Summary Compensation Table, as well as that found in the proxy statement, reflect equity figures of 2012payouts for 2011 performance. To highlight cuts in executive pay, the Company provided the figures below (taken frompg. 23 of its proxy statement), showing equity payments made in 2013 for 2012 performance.

NAMED EXECUTIVE OFFICERS BASESALARY CASH rsus sars TOTAL COMP

Jamie Dimon Chairman of the Board, President and Chief Executive Officer $1,500,000 - $10,000,000 - $11,500,000

Mary Callahan Erdoes Chief Executive Officer, Asset Management $750,000 $4,900,000 $7,350,000 $2,000,000 $15,000,000

Douglas L. Braunstein Chief Financial Officer $750,000 $2,125,000 $2,125,000 - $5,000,000

Daniel E. Pinto Co-Chief Executive Officer, Corporate and Investment Bank $750,000 $8,125,000 $7,125,000 $1,000,000 $17,000,000

Matthew E. Zames Co-Chief Operating Officer and Head, Mortgage BankingCapital Markets $750,000 $6,100,000 $9,150,000 $1,000,000 $17,000,000

CEO Dimon, as seen publicly and in the proxy statement, has taken the ultimate responsibility of the London Whaleincident and took a pay cut by not participating in the cash program, not receiving SARs and receiving slightly fewer RSUsthan in previous years. Comparing his pay by looking at the peer review chart above, Mr. Dimon's pay in 2011 ($23million as reported on pg. 23 of the proxy) was around the 75th percentile of Peer Group 1 and the 50th percentile of PeerGroup 2, and his pay in 2012 ($11.5 million) is closer to the 25th percentile of Peer Group 1 and less than the 25thpercentile for Peer Group 2. In the very least, we believe shareholders should be somewhat encouraged that the spirit ofholding executives accountable for poor company financial performance is demonstrated through hefty paycuts.

Moreover, the Company has had a "long-standing recovery provision", which allows flexibility for the committee to recoupexecutive awards in the event of material restatements and even executive negligence. The recent proxy statement (aswell as past statements) states that the committee can "seek repayment if... the employee engages in conduct that causesmaterial financial or reputational harm... or with gross negligence fail to identify, raise or assess, in a timely manner risksand/or concerns" (Proxy, pg. 27). The Company also has a protection-based vesting provision, wherein RSU or SARsgrants can be cancelled or deferred for an executive if performance has been unsatisfactory or net income is negative forany fiscal year during the vesting period. During the past year, the Company invoked clawbacks of previous outstandingawards for employees who shouldered primary responsibilities, and discloses that it has recaptured over $100 million.Also, for 2013, the provision was extended for members of the operating committee, so that 100% of RSUs scheduled tovest at the end of three years are conditioned on 15% cumulative return on tangible common equity. The committee alsodeferred the vesting on prior SARs granted to the CEO in 2008 for 18 months.

We believe the presence of clawbacks at the Company was paramount in responding appropriately to events surroundingthe London Whale trading debacle. However, the Company should disclose from whom this $100 million was recouped.Shareholders should note that this "protection-based vesting" is not a far cry from a performance condition under along-term plan, where grants only vest if the Company is in a standard financial state at the end of a performance period.As noted in our past reports, the Company had not adopted any form of performance formula to govern cash or equitypayouts in the past. Shareholders benefit when short- and long-term compensation levels are based on objective andtransparent metrics and are thus demonstrably linked to the performance of the company; in this case, performanceconditions set for past awards could have served as a natural safeguard against executive receiving payouts if there arerisk oversight lapses and improper risk-taking.

Former executive Drew stepped down from the CIO position, and Messrs. Pinto and Zames took the positions of Co-ChiefExecutive Officer of CIB and CIO, respectively. We believe shareholders should be encouraged that this managementtransition has not been accompanied with egregious payments usually associated with poor succession planning.

Overall, we believe the board would best serve shareholders by adopting incentive arrangements that would improve thelink between pay and performance. Although pay and performance at the Company during the past year was not aligned(as seen in our pay-for-performance analysis on page 4), we note that decreases in compensation levels will be reflectedin our analysis until the next fiscal year. Moreover, we do not believe shareholders should be concerned with thecompensation decisions made at the Company during the past year, as we believe the response outlined abovedemonstrates considerable restraint and activism in responding to the financial condition of the Company. Ultimately, webelieve a vote against is not a proper response at this time, and believe shareholders can support this resolution.

Accordingly, we recommend that shareholders vote FOR this proposal.

JPM May 21, 2013 Annual Meeting 18 Glass, Lewis & Co., LLC

4.00: ALLOW SHAREHOLDERS TO ACT BY WRITTEN CONSENT

PROPOSAL REQUEST: Amend the Company's certificate of incorporation topermit action to be taken by the shareholders by less thanunanimous written consent

RECOMMENDATIONS & CONCERNS:

PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority

SUMMARY

The board proposes to amend the Company's certificate of incorporation to authorize shareholder action by writtenconsent. Specifically, the amendment will allow any action taken at any meeting of shareholders to be taken without ameeting if consents in writing are signed by shareholders having at least the minimum number of votes necessary to takesuch action at a meeting at which all shares entitled to vote were present and voted. This right will be subject to thefollowing procedural requirements:

In order to obtain a record date for a consent solicitation, shareholders must deliver to the Company requests forsuch record date signed by shareholders representing in the aggregate at least 20% of the outstanding commonshares. These shares must be “Net Long Shares” as defined in the By-Laws.The requests must describe the action proposed to be taken by written consent.Shareholders are not entitled to act by written consent if the request for a record date is delivered between 90 daysprior to the anniversary of of the notice of annual meeting for the last annual meeting and the date of the nextannual meeting (or 30 days after the anniversary of the last annual meeting).The desired action cannot be substantially similar (as determined by the board), other than the election or removalof directors, to an item presented at a shareholder meeting held during the 12 months before the request for arecord date.The desired action cannot be the election or removal of directors if a director nomination was presented at ashareholder meeting held not more than 90 days before the request for a record date.The desired action cannot be substantially similar to an item included in a Company notice of business to bebrought before a shareholder meeting that has been called before the request for a record date is delivered to theCompany.Consents must be solicited from all shareholders.No consents may be dated or delivered until 60 days after the delivery of a valid request to set a record date.

BOARD'S PERSPECTIVE

At each of the past three annual meetings, the agenda included shareholder proposals seeking a right of action by writtenconsent. At two of these meetings the proposal received support from more than 50% of the voted shares. The boardnotes that at the 2010 annual meeting, a shareholder proposal seeking the right of action by written consent was approvedby 54.3% of the votes cast. The board opposed a similar proposal presented at the 2011 annual meeting because itbelieved that shareholders should have further time to adequately consider the merits and risks of the proposal. The 2011proposal was not approved.

At the 2012, the written consent proposal was approved by 52.3% of the votes cast (representing 38.1% of outstandingshares of common stock). The board states that it has discussed the proposal with institutional shareholders who havevoiced concerns about shareholder rights to act by written consent without adequate procedural safeguards.

In light of the results of the shareholder proposals and the noted investor concerns, the board has submitted anamendment permitting action by written consent, subject to certain procedural safeguards intended to protect the bestinterests of the Company and all shareholders. The safeguards are intended to assure that any action by written consentoccurs with adequate notice, transparency, information and timeframes.

GLASS LEWIS ANALYSIS

JPM May 21, 2013 Annual Meeting 19 Glass, Lewis & Co., LLC

Glass Lewis strongly supports the right of shareholders to act by written consent. We believe it protects shareholderinterests and makes boards more accountable. For these reasons, we recommended that shareholders vote for theshareholder proposals seeking this right at each of the past three annual meetings.

We recognize that the advance notice requirements the Company has attached to this right may impose added costs on aconsent solicitation and lessen the effectiveness of the right in responding to an immediate governance concern.However, the Company's shareholders currently have no right to act by written consent, so the proposal offersshareholders a discrete improvement in their ability to effect change at the Company.

Given these circumstances, and recognizing that some of the safeguards are reasonable to prevent abuse, we believeshareholders will benefit from the proposed amendments.

Accordingly, we recommend that shareholders vote FOR this proposal.

JPM May 21, 2013 Annual Meeting 20 Glass, Lewis & Co., LLC

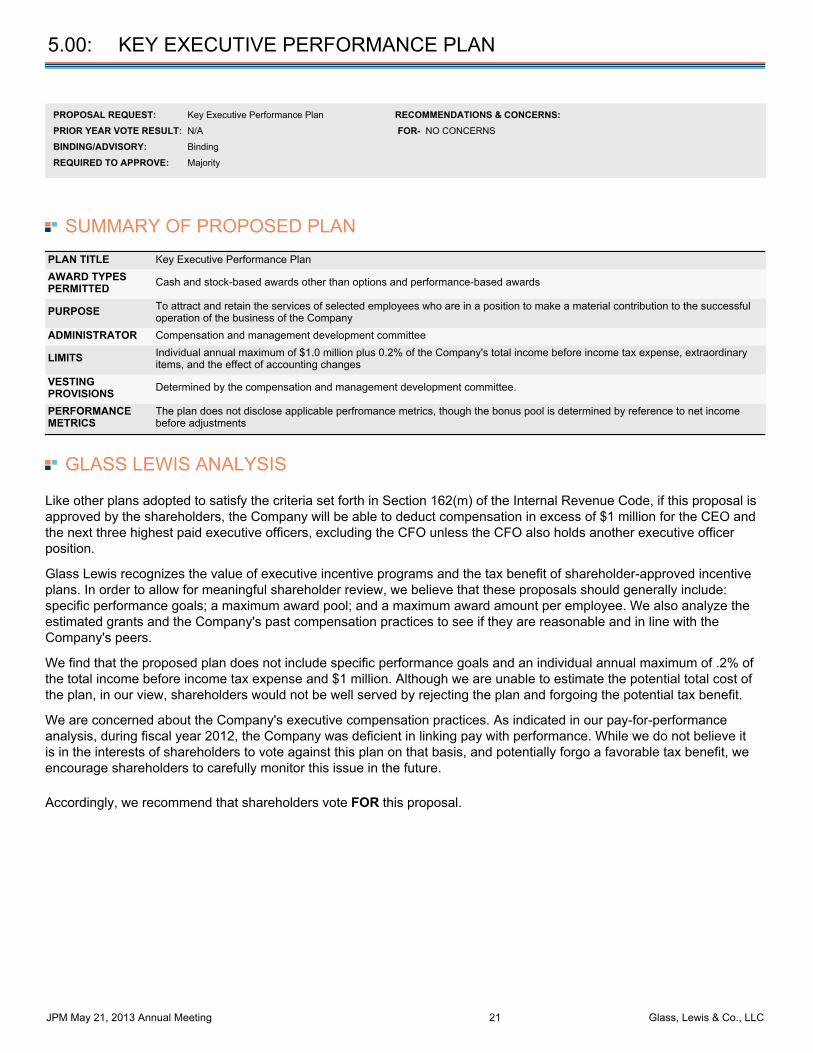

5.00: KEY EXECUTIVE PERFORMANCE PLAN

PROPOSAL REQUEST: Key Executive Performance Plan RECOMMENDATIONS & CONCERNS:PRIOR YEAR VOTE RESULT: N/A FOR- NO CONCERNS

BINDING/ADVISORY: Binding

REQUIRED TO APPROVE: Majority

SUMMARY OF PROPOSED PLANPLAN TITLE Key Executive Performance PlanAWARD TYPESPERMITTED Cash and stock-based awards other than options and performance-based awards

PURPOSE To attract and retain the services of selected employees who are in a position to make a material contribution to the successfuloperation of the business of the Company

ADMINISTRATOR Compensation and management development committee

LIMITS Individual annual maximum of $1.0 million plus 0.2% of the Company's total income before income tax expense, extraordinaryitems, and the effect of accounting changes

VESTINGPROVISIONS Determined by the compensation and management development committee.

PERFORMANCEMETRICS

The plan does not disclose applicable perfromance metrics, though the bonus pool is determined by reference to net incomebefore adjustments

GLASS LEWIS ANALYSIS

Like other plans adopted to satisfy the criteria set forth in Section 162(m) of the Internal Revenue Code, if this proposal isapproved by the shareholders, the Company will be able to deduct compensation in excess of $1 million for the CEO andthe next three highest paid executive officers, excluding the CFO unless the CFO also holds another executive officerposition.

Glass Lewis recognizes the value of executive incentive programs and the tax benefit of shareholder-approved incentiveplans. In order to allow for meaningful shareholder review, we believe that these proposals should generally include:specific performance goals; a maximum award pool; and a maximum award amount per employee. We also analyze theestimated grants and the Company's past compensation practices to see if they are reasonable and in line with theCompany's peers.

We find that the proposed plan does not include specific performance goals and an individual annual maximum of .2% ofthe total income before income tax expense and $1 million. Although we are unable to estimate the potential total cost ofthe plan, in our view, shareholders would not be well served by rejecting the plan and forgoing the potential tax benefit.

We are concerned about the Company's executive compensation practices. As indicated in our pay-for-performanceanalysis, during fiscal year 2012, the Company was deficient in linking pay with performance. While we do not believe itis in the interests of shareholders to vote against this plan on that basis, and potentially forgo a favorable tax benefit, weencourage shareholders to carefully monitor this issue in the future.

Accordingly, we recommend that shareholders vote FOR this proposal.

JPM May 21, 2013 Annual Meeting 21 Glass, Lewis & Co., LLC

6.00:

SHAREHOLDER PROPOSAL REGARDING INDEPENDENT BOARDCHAIRMAN

PROPOSAL REQUEST: That the chairman be an independent director SHAREHOLDER PROPONENT: AFSCME EmployeesPension Plan

BINDING/ADVISORY: Precatory

PRIOR YEAR VOTE RESULT: 40.2%; In favor REQUIRED TO APPROVE: Majority

RECOMMENDATIONS, CONCERNS & SUMMARY OF REASONING: FOR - An independent chairman is better able to oversee the executives of a company and set a pro-shareholder agenda

GLASS LEWIS REASONING

An independent chairman is better able to oversee the executives of a company and set a pro-shareholder agendawithout the management conflicts that a CEO or other executive insiders often face, leading to a more proactiveand effective board of directors;Some empirical evidence regarding this issue suggest that firms with separate CEO and chairman rolesconsistently outperform companies in which a single individual serves in both capacities;Separation of the roles of chair and CEO eliminates the conflict of interest that inevitably occurs when a CEO isresponsible for self-oversight; andThe presence of an independent chairman fosters the creation of a thoughtful and dynamic board that is notdominated by the views of senior management.

PROPOSAL SUMMARY

Text of Resolution- RESOLVED: The shareholders of JPMorgan Chase & Co. (“JPM”) request that the Board of Directorsadopt a policy, and amend the bylaws as necessary, to require the Chair of the Board of Directors to be an independentmember of the Board. This independence requirement shall apply prospectively so as not to violate any contractualobligation at the time this resolution is adopted. Compliance with this policy is waived if no independent director isavailable and willing to serve as Chair.

Proponent's Perspective

The combination of the roles of chairman and CEO weakens acorporation's governance, which can harm shareholder value; Shareholder value is enhanced by an independent board chairwho can provide a balance of power between the CEO and theboard and support strong board leadership; The primary duty of a board is oversee the management of acompany on behalf of shareholders, and a CEO who also servesas chair operates under a conflict of interest that can result inexcessive management influence on the board and weaken theboard's oversight of management; An independent board chairman has been found in academicstudies to improve the financial performance of public companies; Independent board leadership would be particularly constructiveat the Company, which recently faced a trading fiasco that costthe Company a recorded $5.8 billion; andThe Company has acknowledged that its "framework for managingrisks and risk management procedures and practices may not beeffective."

Board's Perspective

The fundamental objective of this proposal is to require that anindependent director lead the Company's board and overseemanagement; however, all but one director is independent; The board has adopted a presiding director role, which hasclearly defined responsibilities; Board and committee agendas are prepared based ondiscussions with all directors and recommendations ofmanagement; committee chairs, all of whom are independentapprove agendas and materials for committee meetings; and theindependent directors regularly meet in executive session; The Company has had strong financial performance under itscurrent board leadership; The board's actions following the Company's trading losses havebeen strong, including the appointment of a management taskforce to review the issue and assess the Company's riskmanagement processes;The Company's board review committee and management taskforce each released reports regarding the Company's tradinglosses and provided recommendations, some of which arealready being followed, regarding mitigating associated risksgoing forward; The board has determined to reduce the chairman and CEO'scompensation by 50% over the previous year; andThe board has no established policy on whether or not to have anon-executive chairman and believes that it should make that

JPM May 21, 2013 Annual Meeting 22 Glass, Lewis & Co., LLC

judgment based on circumstances and experiences.

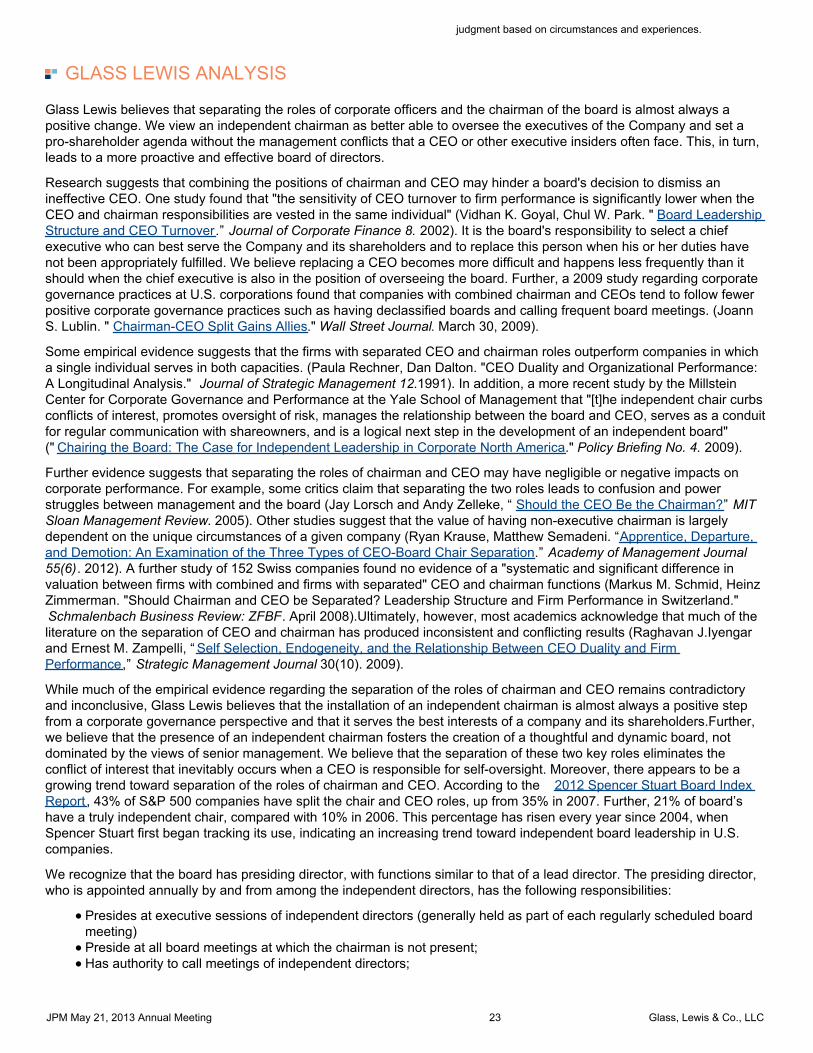

GLASS LEWIS ANALYSIS

Glass Lewis believes that separating the roles of corporate officers and the chairman of the board is almost always apositive change. We view an independent chairman as better able to oversee the executives of the Company and set apro-shareholder agenda without the management conflicts that a CEO or other executive insiders often face. This, in turn,leads to a more proactive and effective board of directors.

Research suggests that combining the positions of chairman and CEO may hinder a board's decision to dismiss anineffective CEO. One study found that "the sensitivity of CEO turnover to firm performance is significantly lower when theCEO and chairman responsibilities are vested in the same individual" (Vidhan K. Goyal, Chul W. Park. " Board LeadershipStructure and CEO Turnover.” Journal of Corporate Finance 8. 2002). It is the board's responsibility to select a chiefexecutive who can best serve the Company and its shareholders and to replace this person when his or her duties havenot been appropriately fulfilled. We believe replacing a CEO becomes more difficult and happens less frequently than itshould when the chief executive is also in the position of overseeing the board. Further, a 2009 study regarding corporategovernance practices at U.S. corporations found that companies with combined chairman and CEOs tend to follow fewerpositive corporate governance practices such as having declassified boards and calling frequent board meetings. (JoannS. Lublin. " Chairman-CEO Split Gains Allies." Wall Street Journal. March 30, 2009).

Some empirical evidence suggests that the firms with separated CEO and chairman roles outperform companies in whicha single individual serves in both capacities. (Paula Rechner, Dan Dalton. "CEO Duality and Organizational Performance:A Longitudinal Analysis." Journal of Strategic Management 12.1991). In addition, a more recent study by the MillsteinCenter for Corporate Governance and Performance at the Yale School of Management that "[t]he independent chair curbsconflicts of interest, promotes oversight of risk, manages the relationship between the board and CEO, serves as a conduitfor regular communication with shareowners, and is a logical next step in the development of an independent board"(" Chairing the Board: The Case for Independent Leadership in Corporate North America." Policy Briefing No. 4. 2009).

Further evidence suggests that separating the roles of chairman and CEO may have negligible or negative impacts oncorporate performance. For example, some critics claim that separating the two roles leads to confusion and powerstruggles between management and the board (Jay Lorsch and Andy Zelleke, “ Should the CEO Be the Chairman?” MITSloan Management Review. 2005). Other studies suggest that the value of having non-executive chairman is largelydependent on the unique circumstances of a given company (Ryan Krause, Matthew Semadeni. “Apprentice, Departure,and Demotion: An Examination of the Three Types of CEO-Board Chair Separation.” Academy of Management Journal55(6). 2012). A further study of 152 Swiss companies found no evidence of a "systematic and significant difference invaluation between firms with combined and firms with separated" CEO and chairman functions (Markus M. Schmid, HeinzZimmerman. "Should Chairman and CEO be Separated? Leadership Structure and Firm Performance in Switzerland."Schmalenbach Business Review: ZFBF. April 2008).Ultimately, however, most academics acknowledge that much of theliterature on the separation of CEO and chairman has produced inconsistent and conflicting results (Raghavan J.Iyengarand Ernest M. Zampelli, “ Self Selection, Endogeneity, and the Relationship Between CEO Duality and FirmPerformance,” Strategic Management Journal 30(10). 2009).

While much of the empirical evidence regarding the separation of the roles of chairman and CEO remains contradictoryand inconclusive, Glass Lewis believes that the installation of an independent chairman is almost always a positive stepfrom a corporate governance perspective and that it serves the best interests of a company and its shareholders.Further,we believe that the presence of an independent chairman fosters the creation of a thoughtful and dynamic board, notdominated by the views of senior management. We believe that the separation of these two key roles eliminates theconflict of interest that inevitably occurs when a CEO is responsible for self-oversight. Moreover, there appears to be agrowing trend toward separation of the roles of chairman and CEO. According to the 2012 Spencer Stuart Board IndexReport , 43% of S&P 500 companies have split the chair and CEO roles, up from 35% in 2007. Further, 21% of board’shave a truly independent chair, compared with 10% in 2006. This percentage has risen every year since 2004, whenSpencer Stuart first began tracking its use, indicating an increasing trend toward independent board leadership in U.S.companies.

We recognize that the board has presiding director, with functions similar to that of a lead director. The presiding director,who is appointed annually by and from among the independent directors, has the following responsibilities:

Presides at executive sessions of independent directors (generally held as part of each regularly scheduled boardmeeting)Preside at all board meetings at which the chairman is not present;Has authority to call meetings of independent directors;

JPM May 21, 2013 Annual Meeting 23 Glass, Lewis & Co., LLC

Approves board meeting agendas and schedules for each board meeting;May add agenda items at his or her discretion;Approves board meeting materials for distribution to and consideration by the board;Facilitates communication between the chairman and CEO and the independent directors, as appropriate;Is available for consultation and communication with major shareholders where appropriate, upon reasonablerequest; andPerforms such other functions as the board directs.

(2013 DEF 14A, p.8)

We recognize that the Company has appointed a presiding director and has listed the duties and responsibilities of theposition, providing some independent board leadership to balance the power of the combined chair and CEO. However,we ultimately we believe vesting a single person with both executive and board leadership concentrates too muchoversight in a single person and inhibits the independent oversight intended to be provided by the board on behalf ofshareholders. We believe adopting a policy requiring an independent chairman may serve to protect shareholder interestsand that it would ensure independent oversight of the Company. Further, given the massive trading losses at theCompany, we believe shareholders would benefit from independent board leadership to prevent such loss of shareholdervalue in the future. We believe that this proposal is reasonably crafted and that shareholders should support thisproposal.

Accordingly, we recommend that shareholders vote FOR this proposal.

JPM May 21, 2013 Annual Meeting 24 Glass, Lewis & Co., LLC

7.00:

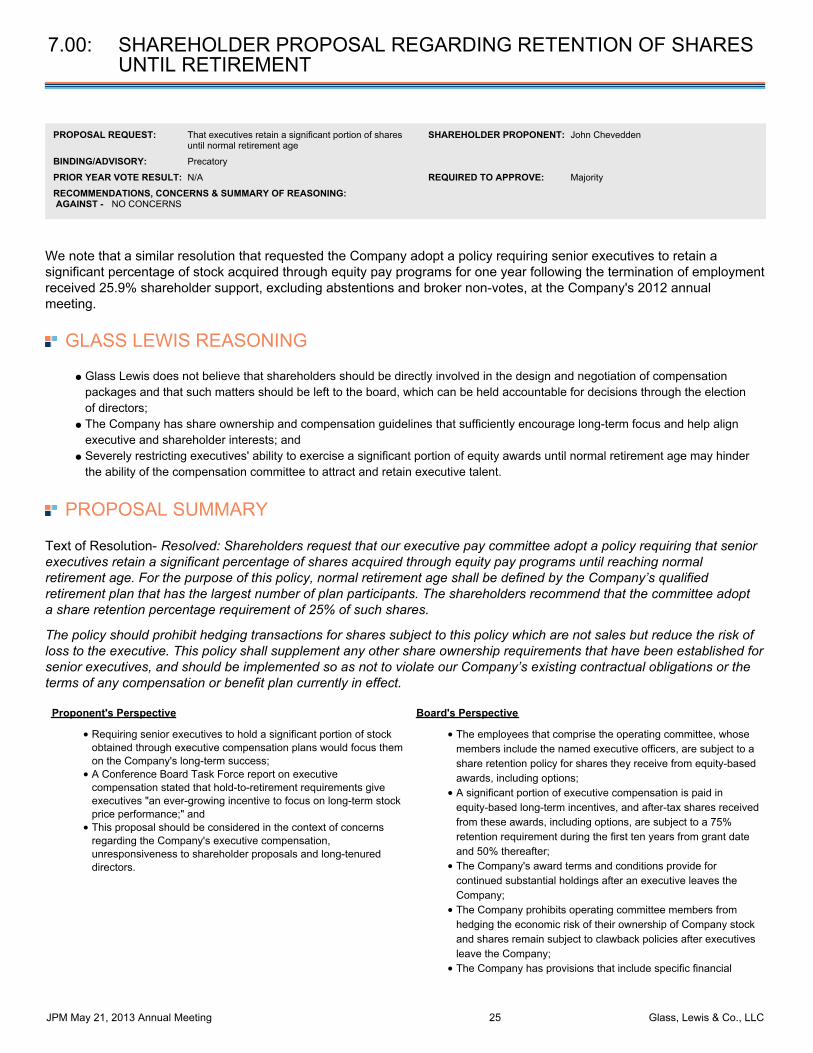

SHAREHOLDER PROPOSAL REGARDING RETENTION OF SHARESUNTIL RETIREMENT

PROPOSAL REQUEST: That executives retain a significant portion of sharesuntil normal retirement age

SHAREHOLDER PROPONENT: John Chevedden

BINDING/ADVISORY: Precatory

PRIOR YEAR VOTE RESULT: N/A REQUIRED TO APPROVE: Majority

RECOMMENDATIONS, CONCERNS & SUMMARY OF REASONING: AGAINST - NO CONCERNS

We note that a similar resolution that requested the Company adopt a policy requiring senior executives to retain asignificant percentage of stock acquired through equity pay programs for one year following the termination of employmentreceived 25.9% shareholder support, excluding abstentions and broker non-votes, at the Company's 2012 annualmeeting.

GLASS LEWIS REASONING

Glass Lewis does not believe that shareholders should be directly involved in the design and negotiation of compensationpackages and that such matters should be left to the board, which can be held accountable for decisions through the electionof directors;The Company has share ownership and compensation guidelines that sufficiently encourage long-term focus and help alignexecutive and shareholder interests; andSeverely restricting executives' ability to exercise a significant portion of equity awards until normal retirement age may hinderthe ability of the compensation committee to attract and retain executive talent.

PROPOSAL SUMMARY

Text of Resolution- Resolved: Shareholders request that our executive pay committee adopt a policy requiring that seniorexecutives retain a significant percentage of shares acquired through equity pay programs until reaching normalretirement age. For the purpose of this policy, normal retirement age shall be defined by the Company’s qualifiedretirement plan that has the largest number of plan participants. The shareholders recommend that the committee adopta share retention percentage requirement of 25% of such shares.

The policy should prohibit hedging transactions for shares subject to this policy which are not sales but reduce the risk ofloss to the executive. This policy shall supplement any other share ownership requirements that have been established forsenior executives, and should be implemented so as not to violate our Company’s existing contractual obligations or theterms of any compensation or benefit plan currently in effect.

Proponent's Perspective

Requiring senior executives to hold a significant portion of stockobtained through executive compensation plans would focus themon the Company's long-term success; A Conference Board Task Force report on executivecompensation stated that hold-to-retirement requirements giveexecutives "an ever-growing incentive to focus on long-term stockprice performance;" andThis proposal should be considered in the context of concernsregarding the Company's executive compensation,unresponsiveness to shareholder proposals and long-tenureddirectors.

Board's Perspective

The employees that comprise the operating committee, whosemembers include the named executive officers, are subject to ashare retention policy for shares they receive from equity-basedawards, including options; A significant portion of executive compensation is paid inequity-based long-term incentives, and after-tax shares receivedfrom these awards, including options, are subject to a 75%retention requirement during the first ten years from grant dateand 50% thereafter; The Company's award terms and conditions provide forcontinued substantial holdings after an executive leaves theCompany; The Company prohibits operating committee members fromhedging the economic risk of their ownership of Company stockand shares remain subject to clawback policies after executivesleave the Company; The Company has provisions that include specific financial

JPM May 21, 2013 Annual Meeting 25 Glass, Lewis & Co., LLC

thresholds that will result in formal compensation reviews todetermine the action to be undertaken under the appropriateclawback provisions; andThe Company's compensation, structure and approach, whichincludes equity-based compensation as a significantcomponents of total compensation, vesting periods of multipleyears, share retention requirements and prohibition of hedging,align the interests of executives with those of shareholders andencourage a focus on long-term price performance.

GLASS LEWIS ANALYSIS

Glass Lewis recognizes that the dramatic evaporation of shareholder value as a result of the global financial crisis hasprompted many shareholders to seek mechanisms through which executive compensation can be restricted and/or bemore closely tied to long-term sustainable value creation. However, Glass Lewis does not believe shareholders should bedirectly involved in the design and negotiation of compensation packages. Such matters should be left to the board'scompensation committee, which can be held accountable for its decisions through the election of directors. While webelieve shareholders should be afforded the opportunity to cast a nonbinding vote on executive compensation, wegenerally do not believe shareholders should support the implementation of specific compensation restrictions. Thisproposal seeks to grant shareholders a role in the setting of executive compensation policy, which we believe is a taskmore appropriately exercised by the board.