Embed Size (px)

Citation preview

1

Provisions of section 195- Certification and documentation

CA N. C. Hegde

January 2017

JB Nagar Study

Circle of WIRCIssues in ICDS, Disclosure in TAX Audit and Returns

J.B.Nagar CPE Study Circle

CA Jhankhana M. Thakkar

5 August 2017

.

Contents

2

Section Page

ICDS Overview 3 – 11

Issues 12

ICDS I – Accounting Policies 13 - 20

ICDS II - Valuation of Inventories 21 - 33

ICDS III - Construction Contracts 34 - 49

ICDS IV - Revenue Recognition 50 - 59

ICDS V - Tangible Fixed Assets 60- 72

ICDS VI - Effect of Changes in Foreign

Exchange Rates

73 - 85

ICDS VIII - Securities 86 - 91

ICDS IX - Borrowing Costs 92 - 104

Impact on Computation of total income 105 - 107

Disclosure in Tax audit report 108 – 110

Disclosure in Income-tax return forms 111 – 113

Questions & Answers 114

ICDS Overview

3

Background

March 2017

• CBDT has issued

Circular No. 10/2017 on 23 March 2017

to clarify specific issues

1995

S.145 of the

Act amended

to notify AS for

Taxpayer and income

Jan 1996

CG notified 2AS –

S.145(2) of the

Act

September 2016

Revised ICDS were notified on

29 Sept 2016 and the same is

effective from 1 April 2016

i.e.FY 2016-17

• Form 3CD amended

January 2015

• CBDT issued draft of 12 ICDS

• Draft ICDS kept open for comments and

suggestions

March 2015

CG notified 10 ICDS for taxpayers

following mercantile method of

accounting, w.e.f FY2015-16

4

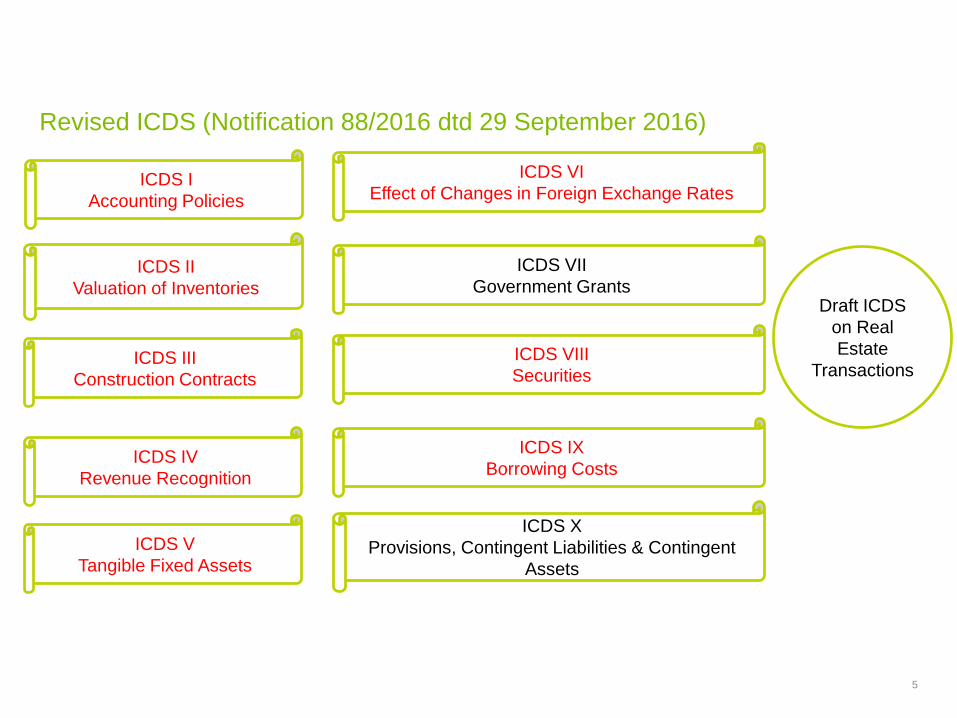

Revised ICDS (Notification 88/2016 dtd 29 September 2016)

5

ICDS II

Valuation of Inventories

ICDS I

Accounting Policies

ICDS III

Construction Contracts

ICDS IV

Revenue Recognition

ICDS V

Tangible Fixed Assets

ICDS VII

Government Grants

ICDS VI

Effect of Changes in Foreign Exchange Rates

ICDS VIII

Securities

ICDS IX

Borrowing Costs

ICDS X

Provisions, Contingent Liabilities & Contingent

Assets

Draft ICDS

on Real

Estate

Transactions

Back ground

6

ICDS

• The Income Computation and Disclosure

Standards (ICDS) are applicable for

computation of taxable income under the

heads ‘Income from Business or Profession’

and ‘Income from Other Sources’ (and not for

the purpose of maintenance of books of

accounts)

• 10 ICDS have been notified to be effective

from 1 April 2016

• Takes legal force from section 145(1) of the Act.

• Non-compliance with ICDS could result into

best judgement assessment – Section 145(3)

of the Act

• ICDS is not for the purpose of maintenance of

books of accounts

AS / IndAS

• The Ministry of Corporate Affairs (MCA) has

officially notified the Companies (Indian

Accounting Standards) Rules, 2015 (‘the Rules’)

in the Gazette of (Ind AS) applicable to certain

class of companies and set out the dates of

applicability.

• The Ind AS will be mandatorily applicable in

phases for following companies (including their

holding, subsidiary, joint venture or associate

companies)

- w.e.f financial year 2016-17 : companies net

worth > INR 500 crore

- w.e.f financial year 2017-18: companies with

listed debts/equity (listed in/outside India) with

net worth< INR 500 Crore and other companies

with net worth exceeding INR 250 Crore

• For the financial year 2015-16, the current

Accounting Standards will continue

Changes in accounting as well as income computation standards in FY 2016-17 –

Combined impact to be understood for harmonious implementation of new norms

Key Features of ICDS

7

• Effective Date of ICDS is 1 April 2016 i.e. FY 2016-17 & AY 2017-18

• ICDS applicable to all Assesses (other than an individual or an HUF to whom

tax audit u/s. 44AB is not applicable)following mercantile system of accounting

• No Net Worth or Turnover or any other criteria prescribed for applicability.

• Entity need not to maintain separate Books of accounts for ICDS.

• ICDS are only for computation of Income under the head “Profit and gains of

business or profession” or “Income from other sources”.

• ICDS is meant for normal computation of income not for Minimum Alternate Tax

(MAT)

• In the case of conflict between the provisions of the Income-tax Act, 1961(‘the

Act’) and ICDS, the provisions of the Act shall prevail to that extent.

• It is to be noted that non-compliance of ICDS gives power to the Tax Authority

to assess income on “best judgement” basis as per section 145(3) of the Act. It

may have potential penalty implications too.

Applicability

8

Circular No. 10/2017 dated 23 March 2017 clarifies that ICDS will apply to:

• Assessees under presumptive tax schemes – FAQ 3

• Companies adopting Ind-AS – FAQ 5

• AMT computation, but will not apply to MAT computation – FAQ 6

• Assessees in Finance, Insurance & Power sectors – FAQ 7

• Real estate developers, Build-Operate-Transfer projects, Leases – FAQ 12

Applies to all assessees following the

mercantile system of accounting, except

for individuals, HUF who are not covered

under the tax audit provisions

ICDS and AS/IndAS (Accounting Standards)

Can accounting taxation principles be harmonised ?

9

ICDS Accounting Standards

Disallow certain losses

Recognize revenue earlier

Recognises all possible

Losses

Recognise revenue only

when certain

Principles of “Prudence

and “Materiality” absent

in ICDS

ICDS and Accounting Standards harmonization – to be a factor of Industry and

government experience in implementation of these standards

ICDS and corresponding Accounting Standards

10

No. ICDS Accounting

Standard

(AS)

Ind AS

I Accounting policies AS 1 & 5 IND AS 8

II Valuation of Inventories AS – 2 IND AS 2

III Construction Contracts AS – 7 IND AS 115

IV Revenue Recognition AS – 9 IND AS 115

V Tangible fixed assets AS – 10 IND AS 16

VI Effects of changes in foreign exchange rates AS – 11 IND AS 21

VII Recognition of Government Grants AS – 12 IND AS 20

VIII Securities AS – 13/AS - 30 IND AS 109

IX Borrowing costs AS – 16 IND AS 23

X Provisions, Contingent Liabilities & Contingent

Assets

AS – 29 IND AS 37

Where no specific treatment of an element of income/expense/asset/liability is prescribed under the

Act or ICDS, the existing accounting framework (including guidance notes and other authoritative

pronouncements of ICAI) applicable to the entity will apply

General Clarifications vide Circular No. 10/2017 dated 23 March 2017

11

FAQ Clarification

1 ICDS do not apply to maintenance of books of account and for

preparation of financial statements

(the above is also clarified in the Preamble of each ICDS)

2 W.e.f AY 2017-18, ICDS shall prevail over judicial precedents on the

issues dealt therein

14 Specific provisions of Income-tax Rules, 1962 shall prevail over ICDS

25 Disclosures required under ICDS are to be made in the ITR Form and

Form 3CD, no separate disclosure requirement for persons not liable

to tax audit

ICDS - Issues

12

ICDS – I - Accounting

Policies

13

• ICDS recognizes three accounting concepts

− going concern

− consistency

− Accrual

• Accounting policies must be chosen to represent true and fair view of state of

affairs and income

• Treatment of transactions will be governed by their substance and not legal

form

• Accounting policy can be changed if there is reasonable cause to do so

• Mark-to-market or expected loss shall not be recognized unless provided by

other ICDS

ICDS I – Accounting policies

14

• This ICDS is not merely a disclosure standard but it requires income

computation standard to factor in elements of this standard viz accrual, going

concern and consistency. Therefore, the term accounting policies should be

read as “computation policies”

• The definition of “accrual” under a standard should not alter the understanding

of accrual under Section 5.The principle laid down by the Hyderabad Tribunal in

case of DCIT v Nagarajuna Investment Trust Limited (1998) 65 ITD 17 has

been affirmed by the Andhra Pradesh High Court in case of DCIT vs Chakra

Financial Services (350 ITR 396) that the provisions of Section 145 cannot

override Section 5 of the Act. Section 145 determines mode of computing the

taxable income, it does not affect the scope of taxable income.

ICDS I – Accounting policies

15

ICDS I – Accounting policies

16

ICAI Accounting Standards

(AS)

ICDS

Change in

accounting

policy

should be made only if it is

required by statute,

accounting standard or if

such change will result in

more appropriate

presentation of financial

statements

shall not be changed without any

reasonable cause

Prudence profits are recognized only

when realized. Provision is

made for all known

liabilities and losses even

though the amount cannot

be determined with

certainty

"marked to market loss" or an

"expected loss" shall not be

recognized unless the recognition

of such loss is in accordance with

the provisions of any other ICDS

Materiality should disclose all

"material“ items

-

ICDS I – Accounting policies

17

This standard mandates the principle of substance over form. The financial

information should represent the substance of an economic phenomenon

rather than merely its legal form

• In case of Finance lease, the asset and depreciation is recorded in the

books of lessee. The Supreme Court in case of ICDS Ltd vs CIT(2013)

350 ITR 627 held that the owner of the asset had used it for its business

and was thus entitled to depreciation under Section 32 of the Act. Having

regard to this decision, the lease rent would be taxable as income and

lessor will be entitled for depreciation.

Key considerations

ICDS I : Accounting Policies

An accounting policy shall not be changed without reasonable cause

What does ‘reasonable cause’ mean in this regard?

Analysis:

• There are no judicial precedents on ‘reasonable cause’ in relation to change in accounting policy

• Normally, AO can change method of accounting:

− when he has ascertained the method of accounting followed by the assessee in the past is erroneous and

− when change in method of accounting is warranted on the ground that profit is being underestimated under the impugned method of accounting

− Based on below judicial precedents, assessee can change accounting policy if the same is bonafide and is followed in subsequent years as well

• Gujarat HC case of Atul Products Ltd. [125 TAXMAN 727]

• Andhra Pradesh HC case of Mopeds (India) [38 TAXMAN 123]

• Calcutta HC case of Snow White Food Products Co. Ltd. [141 ITR 847]

• Calcutta HC case of Reform Flour Mills (P.) Ltd. [114 ITR 227]

18

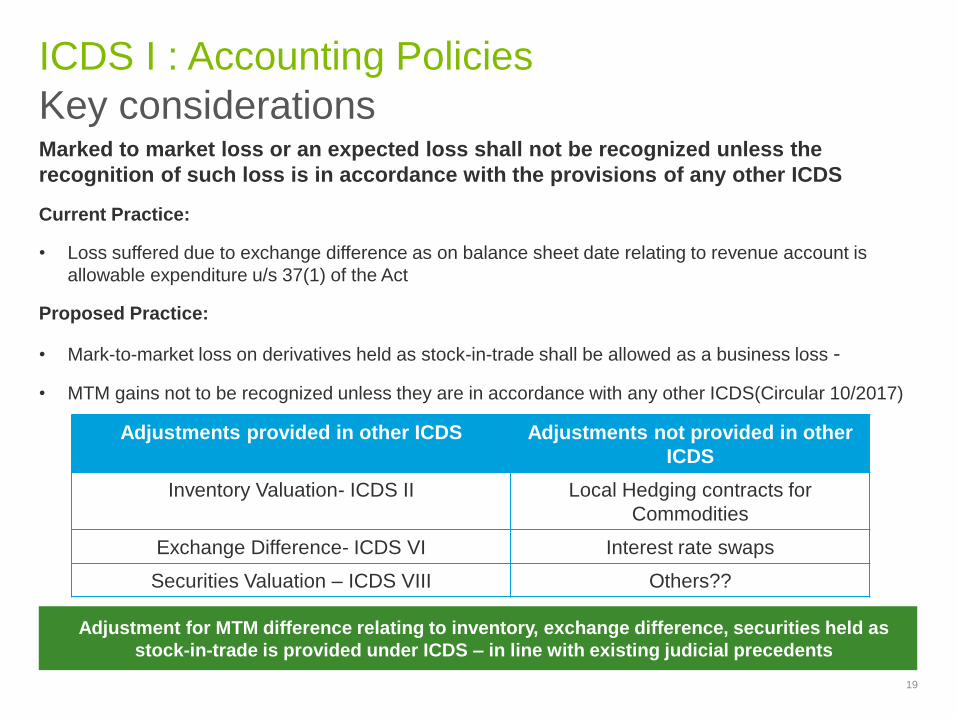

Key considerations

ICDS I : Accounting Policies

Marked to market loss or an expected loss shall not be recognized unless the

recognition of such loss is in accordance with the provisions of any other ICDS

Current Practice:

• Loss suffered due to exchange difference as on balance sheet date relating to revenue account is

allowable expenditure u/s 37(1) of the Act

Proposed Practice:

• Mark-to-market loss on derivatives held as stock-in-trade shall be allowed as a business loss -

• MTM gains not to be recognized unless they are in accordance with any other ICDS(Circular 10/2017)

19

Adjustments provided in other ICDS Adjustments not provided in other

ICDS

Inventory Valuation- ICDS II Local Hedging contracts for

Commodities

Exchange Difference- ICDS VI Interest rate swaps

Securities Valuation – ICDS VIII Others??

Adjustment for MTM difference relating to inventory, exchange difference, securities held as

stock-in-trade is provided under ICDS – in line with existing judicial precedents

Disclosure requirements

ICDS I : Accounting Policies

• Any change in accounting policy which has material impact shall be disclosed

• Amount should be quantified to the extent ascertainable

• Where the amount is not ascertainable, wholly or in part, such fact shall be

indicated

• Change having material effect on later previous years also to be disclosed.

20

ICDS II – Valuation of

Inventories

21

ICDS is applicable to valuation of inventories except:-

• WIP arising from construction contracts

• WIP dealt by other ICDS

• Shares, debentures and other financial instruments held as stock in trade and

dealt by other ICDS

• Inventories of livestock, agriculture and forest products, mineral oil, ores and

gases to the extent that they are measured at NRV

• Machinery spares used in connection with tangible fixed assets

22

ICDS II : Valuation of Inventories

Scope

ICDS II – Inventories

23

ICAI Accounting

Standards (AS)

ICDS

Techniques for the

measurement of the

cost of the inventories

techniques such as the

standard cost method or

retail method may be used if

the results approximate to the

actual cost

Standard Cost method or retail method is

allowed provided the results approximate

the actual cost

Change in method of

valuation

may be changed if it is

considered that the change

would result in a more

appropriate presentation

shall not be changed without a reasonable

cause

Dissolution of

partnership firm or AOP

or BOI

- Inventory on the date of dissolution of

partnership firm or AOP or BOI shall be valued

at the net realizable value [ALA Firm vs CIT

189 ITR 285(SC) v Sakthi Trading Co vs CIT

250 ITR 871 (SC)]

Inventory – Costs of

services ,

service providers

work-in-progress of service

provider excluded

Work in progress of service provider excluded

however, cost of service utilized in

manufacture, production or processing of

goods shall form part of the inventory

Highlights

ICDS II : Valuation of Inventories

• Inventories shall be valued at cost or net realizable value (NRV), whichever is lower*

• Following valuation methods have been identified –

− First-in First-out,

− weighted average cost and

− retail method ‘

− Standard costing

As per AS 2 Standard costing and retail method may be used for convenience if results approximate the actual cost

• Specific identification of cost is required for goods that are not interchangeable

• Method of valuation of inventory, once adopted in any tax year, cannot be changed without a reasonable cause

• Interest and other borrowing cost shall not be included in the cost of inventories, unless they meet the criteria for recognition of interest as a component of the cost as specified in the ICDS on borrowing costs i.e. direct / indirect attribution basis

• Value of opening inventory shall be the value of inventory as on the close of the immediately preceding previous year

Inventory shall be valued at NRV on the date of dissolution of partnership firm / AOP/ BOI, whether business is discontinued or not 24

Key Considerations

ICDS II : Valuation of inventories

25

As

pe

cts

• Standard costing method and retail costing is allowed – provided the results approximate the actual cost

• No change in valuation allowed without reasonable cause

Valuation method

• Inventory to be recorded at Net Realizable Value

Dissolution of partnership

• Opening inventory to be same as closing inventory of previous year

Valuation of opening stock

• Purchase price includes duties and taxes whether or not subsequently recoverable.

• In line with 145A of the Act

Cost of Purchases

Recording of Inventory- Goods and Services

ICDS II : Valuation of Inventories

26

Profit and Loss account shall reflect closing inventory of services

for all business and impact Profits

Topic ICDS AS

Inventories –

Valuation

ICDS II relating to valuation of

inventories

AS 2 – Valuation of Inventories

Of goods Cost of purchase

Add: Cost of services

Add: Costs of conversion

and other costs

XXX

XXX

XXX

_______

XXX

Costs of purchase

Add: Costs of

conversion and

other costs

XXX

XXX

______

XXX

Of Services Cost of Labour

Add: Other costs of

personnel directly

engaged in providing

the service

Add: Attributable

overheads.

XXX

XXX

XXX

_____

XXX

Not prescribed

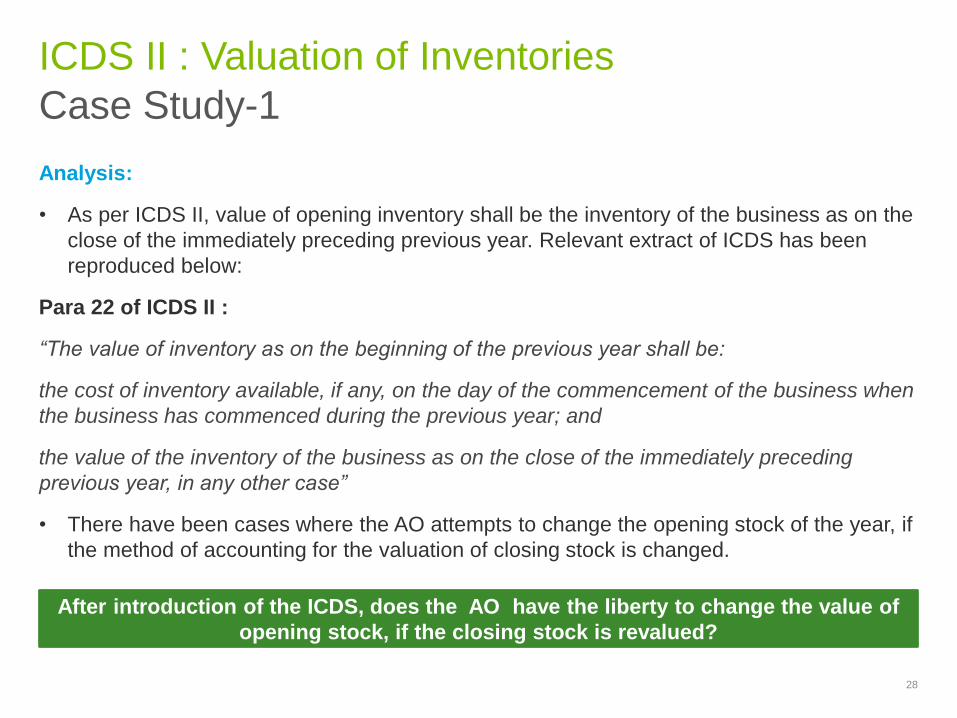

Case Study-1

ICDS II : Valuation of Inventories

Valuation of opening inventory vis-a-vis closing inventory of preceding financial year:

• For financial year 2015-16, closing stock of A Ltd. has been valued using Standard Costing Method.

From financial year 2016-17 onwards, A Ltd. changed its method for valuation of closing stock to First-

in-First-out method at the time of valuation of closing stock.

27

FY 2015-16

Opening Stock

Closing Stock

FY 2016-17

15 Lakh10 Lakh

A Ltd.

15 Lakh 25 Lakh

Issue:

Can the AO adjust the opening stock of the year?

Case Study-1

ICDS II : Valuation of Inventories

Analysis:

• As per ICDS II, value of opening inventory shall be the inventory of the business as on the

close of the immediately preceding previous year. Relevant extract of ICDS has been

reproduced below:

Para 22 of ICDS II :

“The value of inventory as on the beginning of the previous year shall be:

the cost of inventory available, if any, on the day of the commencement of the business when

the business has commenced during the previous year; and

the value of the inventory of the business as on the close of the immediately preceding

previous year, in any other case”

• There have been cases where the AO attempts to change the opening stock of the year, if

the method of accounting for the valuation of closing stock is changed.

28

After introduction of the ICDS, does the AO have the liberty to change the value of

opening stock, if the closing stock is revalued?

Case Study-2

ICDS II : Valuation of Inventories

Valuation of inventory at the time of dissolution of partnership firm / AOP/ BOI,

whether business discontinued or not

• For financial year 2016-17, M/s A & Co is in the process of dissolution. Details of inventory

at the time of dissolution is mentioned below:

Issue:

• Can inventory be valued at cost at the time of dissolution?

29

FY 2016-17

Cost of Inventory = 10 crore

Net Realizable Value of Inventory = 20 crore

Case Study-2

ICDS II : Valuation of Inventories

Analysis:

• As per ICDS II, Inventory shall be valued at NRV on the date of dissolution of partnership

firm / AOP/ BOI, whether business discontinued or not

30

Post adoption of the ICDS, does the assessee have the option of valuing inventory

at cost at the time of dissolution of partnership firm / AOP/ BOI, whether business

discontinued or not?

Case Study-3

ICDS II : Valuation of Inventories

Valuation of inventory in case of conversion of capital asset into Stock in trade

Issue:

• If an assessee converts capital asset into stock-in-trade and commences his

business during the year . How will the inventory be valued

31

Case Study-3

ICDS II : Valuation of Inventories

Analysis:

• Under Section 2(47)(iv) of the Act such conversion is to be treated as transfer and under

Section 45(2) of the Act capital gain is computed taking the fair value of the asset on the

date of conversion as full value of the consideration. The Supreme Court in case of CIT vs

Bai Shirnbai K. Kooka 46 ITR 86(SC) held that for computing the trading profit the fair

market value of the asset on the date of conversion into stock-in-trade is cost to the

business. Considering the decision of Supreme court ,the fair market value of the asset on

the date of conversion shall be regarded as cost of the invemtory, although ICDS I

provides that the cost of inventory available has to be taken as the value of the inventory

as on the beginning

32

• The accounting policies adopted in measuring inventories including the cost

formulae used and

• The carrying amount of inventories and its classification

33

ICDS II : Valuation of Inventories

Disclosure requirements

ICDS III – Construction

Contracts

34

• Revenue (including retentions) and costs (i.e. direct cost, allocated cost,

borrowing cost as per specific ICDS and other cost specifically chargeable to

customer) from construction contracts shall be recognized by reference to the

stage of completion of the contract

• The Delhi High Court in Tirath Ram Ahuja (P.) Ltd vs CIT (1976)[103 ITR 15]

(affirmed by Supreme Court (1990) [186 ITR 428] has affirmed that in the case

of contract, the profits can be estimated on the basis of receipts in each year

and need not wait till the completion of contract. AS 7 issued by the ICAI

mentions that revenue should be recognized only on Percentage Completion

Method(POCM). However, ICDS specifically mentions Percentage of

Completion Method(POCM)

• During the early stages of a contract, where the outcome of the contract cannot

be estimated reliably, contract revenue must be recognized only to the extent of

costs incurred. The early stage of a contract shall not extend beyond 25% of the

stage of completion

• Contract revenue to be recognized only when there is reasonable certainty of

its ultimate collection. Contract revenue once recognized cannot be reversed

but needs to be written off as expenses

ICDS III– Construction contracts

35

Significant deviations

• Retention money to be included in the sales turnover

• Interest/ dividend and capital gains need to be recognized as income separately

and cannot be reduced from contract costs

• Does not allow provision for foreseeable losses for tax purposes which is in line

with non-allowability of expected losses as provided in ICDS-1

ICDS III– Construction contracts

36

Where a contract covers a number of assets, the construction of each asset

should be treated as separate construction:

- Separate proposals have been submitted for each asset

- Each asset has been subject to separate negotiation

- Cost and revenues of each asset can be identified

A number of contracts whether with a single customer or with several customers

shall be treated as a single construction contract when:

- The group of contracts is negotiated as a single package

- The contracts are so closely interrelated that they are in fact part of a single

project

- The contracts are performed concurrently or in a continuous sequence

ICDS III – Construction ContractsCombining and Segmenting Construction Contracts

37

ICDS III– Construction contracts

38

ICAI Accounting Standards

(AS)

ICDS

Retention money - shall be recognized on basis

of percentage of completion

method

Pre-construction

interest income,

dividend income &

capital gains

Any income earned on the

temporary investment of

those borrowings is

deducted from the

borrowing costs incurred

(AS-16 borrowing cost)

shall not be reduced from the

contract costs but shall be

treated and taxed as income in

accordance with the applicable

provisions of the Act

Recognition of

losses including

probable/expected

losses

fully and not in proportion to

the percentage of

completion

shall not be allowed unless

such losses are actually

incurred. The losses incurred

shall be allowed only in

proportion to the stage of

completion

ICDS III – Construction Contract

Impact

Can upfront provision of expected loss be made based on following Supreme Court cases?

• Metal Box Co. of India Ltd. V. Their Workmen

• Rotork Controls India (P.) Ltd. [180 TAXMAN 422]

Year 1 Books ICDS

Revenue 100 x 30% 30 30

Less: Cost incurred during the year (40) (40)

Less: Provision for expected loss on construction contracts (30) NIL

Net profit (40) (10)

Year 2 Books ICDS

Revenue 100 x 70% 70 70

Less: Cost incurred during the year (60) (90)

Net profit 10 (20)

Recognition of taxable income at an earlier point in time as compared to book profits

Illustration: disallowance of expected loss• Contract revenue – 100

• Contract cost originally estimated – 80

• Revised probable estimated contract cost – 130

• Cost incurred during year 1 – 40

• Percentage of completion at end of year 1 – ~30% (40 of 130)

• Cost incurred during year 2 – 90

• Percentage of completion at end of year 2 – 100%

39

Key Considerations

ICDS III - Construction contracts

40

Retention money

ICDS possibly

militates against

the basic principle

that revenue

accrues only when

assesse gets the

right to receive /

amount becomes

payable

Early stage of

contract

• Revenue only to

the extent of

costs

recognized

• Early stage of

contract cannot

be > 25% of the

contract

completion

stage in order to

prohibit

deferment of

revenue

recognition

Expected loss

Recognized in

proportion of work

completed

Asp

ects

Adjustment of

contract revenue

Contract variations,

claims and

incentives included

in the contract

revenue only to the

extent it is

probable that they

will result in

revenue

ICDS III – Construction Contracts

41

Contract Revenue

• Contract Revenue = Initial amount of agreed revenue + retentions + (variations in contract work + claims + incentive payments)*

*only if capable of being reliably measured and only to the extent that will result in revenue

• If contract revenue recognized in earlier years is subsequently written off – the same shall be recorded as an expense

Contract Costs

• Contract Costs = Direct expenses + attributable to the contract + costsspecifically chargeable to the customer + allocated borrowings in termswith ICDS IX - Borrowing Costs

• Costs incurred from the date of securing the contract till the finalcompletion of the contract

• Costs incurred in advance – to be recorded as an asset as recoverablefrom customers

ICDS III – Construction Contracts

42

Borrowing costs allocable in terms of ICDS IX – Borrowing Costs

Clarifications vide Circular dated 23 March 2017

If there are specific provisions in the Act for disallowance of a portion of theborrowing costs, e.g. 14A, 43B, etc., only that portion of the borrowing cost shall becapitalized which is otherwise allowable as a deduction under the Act

Particulars Cost to be capitalized

If funds are specifically borrowed Actual borrowing cost incurred

If general borrowings are utilized Borrowing costs on general borrowings

x

(Average cost of qualifying asset /

Average of total assets excluding assets

funded out of specific borrowings)

Case Study-1

ICDS III : Construction Contracts

Retention money

• A Ltd. entered into a contract with B Ltd at an agreed contract revenue of INR 100 crore. As per the

terms of the contract, an amount of INR 10 crore is to be retained by B Ltd. and would be paid after

fulfillment of certain conditions mentioned in the contract.

Issue:

ICDS provides that contract revenue shall include retention money

Is retention money required to be included in the value of Contract Revenue?

43

FY 2015-16

Contract Revenue = INR 100 crore

Retention Money = INR 10 crore

Case Study-1

ICDS III : Construction Contracts

Analysis:

• Income can be held to accrue only when assessee acquires right to receive that income(Section

5 of the Act)

• Retention money may not accrue to the assessee if assessee had certain obligations which

were linked to the retention payment and right to receive crystalises only on the performance of

the obligation.

• ICDS provides that contract revenue shall include retention money.

• ICDS also states that revenue shall be recognised when there is reasonable certainty of its

ultimate collection

• Income can be held to accrue only when assessee acquires right to receive that income – SC

cases of Ashokbhai [56 ITR 42], Shrivastava [57 ITR 624] ,Excel Industries(2013)(358 ITR 259)

• Retention money could not be said to be accrued to the assesse if assessee had no right to

receive the same till the completion of work or does not become payable as per the terms of the

contract.

• The following decisions also support this contention:

⁻ Calcutta HC case of Simplex Concrete Piles India (P) Ltd [79 CTR 71]

⁻ Madras HC case of P & C Constructions (P.) Ltd. [318 ITR 113]

44

When it can be said that there is reasonable certainty of ultimate collection ?

Case Study-2

ICDS III : Construction Contracts

Allowability of Expected Loss:

• A Ltd. entered into a contract with B Ltd at a agreed contract revenue of INR 100 crore. At

the end of the financial year, 60% of the contract was complete and an expected loss of

INR 5 crore was determined by A Ltd.

Issue:

• How is the expected loss on contract required to be recognized in the books of accounts?

45

FY 2015-16

Contract Revenue = INR 100 crore

% Completion of Contract = 60%

Expected Loss = INR 5 crore

Case Study-2

ICDS III : Construction Contracts

Analysis

Expected loss on Contract – ICDS and Accounting Standards

‒ Para 17 of ICDS III:

“The recognition of revenue and expenses by reference to the stage of completion of a contract is referred to as the percentage of completion method. Under this method, contract revenue is matched with the contract costs incurred in reaching the stage of completion, resulting in the reporting of revenue, expenses and profit which can be attributed to the proportion of work completed”

‒ AS-7 on ‘Construction Contracts:

“When it is probable that total contract costs will exceed total contract revenue, the expected loss should be recognized as an expense immediately”.

Current Practice‒ AS-7 provides that expected loss be recognized immediately as an expense, if it is probable

that the total contract costs would exceed total contract revenue

Practice under the ICDS regime:

‒ Expected losses from the contract has to be recognized in proportion to percentage completion

46

Whether expected loss can be claimed as an expense, post introduction of the ICDS?

Case study-3

ICDS III : Construction Contracts

Early stage of a contract:

• For financial year 2016-17, A Ltd. entered into a contract with B Ltd at a agreed contract

revenue of Rs. 100 crore. At the end of the financial year, assuming contract has been

completed as per the following percentages:

• 25%

• 30%

Issue:

• At what stage, is revenue to be recognised?

47

Case study-3

ICDS III : Construction Contracts

Analysis:

• AS does not specify a percentage at which early stage of the contract can be considered

to have reached.

• Generally, industry practice is to record profits post 25% stage of completion.

• Certain companies may not record profits up to 30%

• Para 20 of ICDS III:

“During the early stages of a contract, where the outcome of the contract cannot be

estimated reliably contract revenue is recognised only to the extent of costs incurred. The

early stage of a contract shall not extend beyond 25% of the stage of completion.”

• ICDS has specifically provided that early stage of a contract shall not extend beyond 25%

of the stage of completion and profits of a contract are required to be booked, once the

contract reaches the stage of 25%.

48

Is it mandatory to book profits post completion of 25%?

Does reasonable certainty of completion of the contract need to be examined?

Disclosure requirements

ICDS III : Construction Contracts

• Contract revenue recognized and method used to determine the stage of

completion

• In case of contracts in progress:-

‒ amount of cost incurred and recognized profits less recognized losses upto

the reporting date

‒ amount of advance received

‒ amount of retention

Further, as per revised ICDS

“ The transitional provisions in revised ICDS- III provide that the contract

revenue and contract costs, with respect to construction contracts which

commenced but were not completed on or before 31 March 2016, shall be

continued to be recognized in accordance with the method regularly

followed for such contracts before 1 April 2016.

49

ICDS IV – Revenue

Recognition

50

• Revenue from sale of goods shall be recognized when all significant risks and

rewards of ownership are transferred and when there is a reasonable certainty of

collection. Claims for escalation of price and export incentives can be postponed

to the extent of uncertainty involved

• Revenue from service transactions –

Revenue from service transactions will be recognized as per percentage

completion method and ICDS on ‘Construction contracts’ will apply except

‘Completed service contract method’, permissible under AS-9 (current Indian

accounting standard followed for maintaining books of accounts), is not

available to a taxpayer.

Exceptions to the above are:

‒ Where services are provided by an indeterminate number of acts over a

specific period of time, revenue may be recognized on a straight line basis

over the specific period.

- Where service contracts have duration of not more than 90 days, revenue

may be recognized when the rendering of services under that contract is

completed or substantially completed

ICDS IV– Revenue Recognition

51

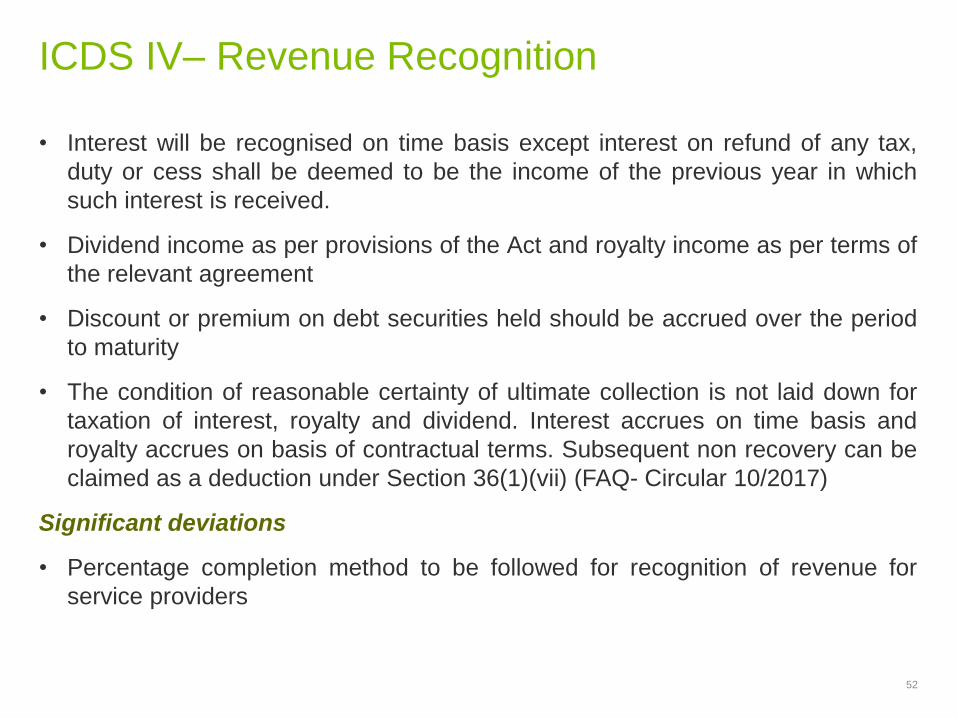

• Interest will be recognised on time basis except interest on refund of any tax,

duty or cess shall be deemed to be the income of the previous year in which

such interest is received.

• Dividend income as per provisions of the Act and royalty income as per terms of

the relevant agreement

• Discount or premium on debt securities held should be accrued over the period

to maturity

• The condition of reasonable certainty of ultimate collection is not laid down for

taxation of interest, royalty and dividend. Interest accrues on time basis and

royalty accrues on basis of contractual terms. Subsequent non recovery can be

claimed as a deduction under Section 36(1)(vii) (FAQ- Circular 10/2017)

Significant deviations

• Percentage completion method to be followed for recognition of revenue for

service providers

ICDS IV– Revenue Recognition

52

ICDS IV– Revenue Recognition

53

ICAI Accounting

Standards (AS)

ICDS

Revenue

recognition

from service

contracts

both the "proportionate

completion method" and

"completed service

contract method" for

recognition of revenue

from service

transactions

shall only be recognized by

following the "percentage

completion method".

Requirements of TAS for

Construction Contracts to apply

mutatis mutandis for recognition of

revenue and associated expenses

for a service transaction

exceptions are as per slide no. 52

Key Considerations

ICDS IV - Revenue recognition

54

Sale of goods /

services

Revenue

recognition on

transfer of

significant risks and

rewards of

ownership to the

buyer for sale of

goods

Revenue

recognition in cases

of obligation of free

/ discounted goods

/ services – ICDS

IV silent – ought to

be governed by

IndAS 18

Price escalations

and export

incentives

Postponement on

account of inability

to assess ultimate

collection in context

of escalations and

export incentives is

specifically

provided for

Discount /

premium on debt

securities

Recognized over

the period to

maturity rather than

receipt

Asp

ects

Royalty

Recognized based

on agreement

subject to

‘substance over

form’

Key considerations

ICDS IV : Revenue Recognition

Sale of goods:

Para 3 of ICDS IV :

“In a transaction involving the sale of goods, the revenue shall be recognized when the

seller of goods has [transferred to the buyer the property in the goods for a price] or

[all significant risks and rewards of ownership have been transferred to the buyer] and

[the seller retains no effective control of the goods] transferred to a degree usually associated

with ownership. In a situation, where transfer of property in goods does not coincide with the

transfer of significant risks and rewards of ownership, revenue in such a situation shall be

recognized at the time of transfer of significant risks and rewards of ownership to the buyer”

55

When the date of transfer of significant risks and rewards are different from the date of the

transfer of title to the goods, can revenue from sale of goods be recognized?

Key considerations

ICDS IV : Revenue Recognition

Royalty – Substance over Form?

Para 3 of ICDS IV :

“Royalties shall accrue in accordance with the terms of the relevant agreement and shall be

recognised on that basis unless, having regard to the substance of the transaction, it is more

appropriate to recognise revenue on some other systematic and rational basis”

56

Can authorities alter recognition of royalty based on substance of agreement and not

the terms of agreement?

Key considerations

ICDS IV : Revenue Recognition

Discount / premium on debt securities

Para 7 of ICDS IV :

Interest shall accrue on the time basis determined by the amount outstanding and the rate

applicable. Discount or premium on debt securities held is treated as though it were accruing

over the period to maturity

57

Can discount or premium on all debt securities be chargeable as interest over period

of maturity?

Case Study

ICDS IV : Revenue Recognition

Recognition of revenue from service transactions

• For financial year 2016-17, A Ltd. entered into an agreement with B Ltd. for rendering of

services at an agreed contract price of 100 Cr.. At the end of the financial year, 70% of the

services have been duly rendered to B Ltd. and the balance services would be rendered

in the next financial year.

Issue:

• How is the revenue from service transaction to be recognized

58

FY 2015-16

Contract Revenue = 100 crore

% of services rendered = 70%

Disclosure requirements

ICDS IV : Revenue Recognition

Following disclosures shall be made in respect of revenue recognition:

a) In a transaction involving sale of good, total amount of claim raised for escalation of price

and export incentives not recognised as revenue during the previous year along with

nature of uncertainty about such claims

b) the amount of revenue from service transactions recognised as revenue during the

previous year; and

c) the methods used to determine the stage of completion of service transactions in

progress

d) for service transactions in progress at the end of previous year:

i. amount of costs incurred and recognized profits (less recognized losses) upto end of

previous year;

ii. the amount of advances received; and

iii. the amount of retentions

59

ICDS V – Tangible Fixed

Assets

60

• Scope

- ICDS V deals with the treatment of tangible fixed assets

• Definitions

- “Tangible fixed asset” is an asset being land, building, machinery, plant or

furniture held with the intention of being used for the purpose of producing or

providing goods or services and is not held for sale in the normal course of

business.

−“Fair value” of an asset is the amount for which that asset could be exchanged

between knowledgeable, willing parties in an arm’s length transaction.

ICDS V– Tangible Fixed Assets

Scope and definitions

61

• Any tangible asset which is covered by the definition

• Stand-by equipment and servicing equipment are to be capitalized

• Generally, machinery spares are charged to revenue as and when consumed;

however, such spares are capitalised in the following cases:

- they are used only in connection with an item of tangible fixed asset; and

- their use is expected to be irregular

ICDS V– Tangible Fixed Assets

Identification of tangible fixed assets

62

• Tangible fixed asset shall be recorded at actual cost including purchase price,

taxes (excluding those that are recoverable) and other directly attributable

expenditure for making the asset ready for its intended use. Trade discounts and

rebates shall be deducted.

• The cost of the asset may undergo changes subsequent to its acquisition or

construction on account of:

- Price adjustments of the asset, changes in duties or similar factors

- Foreign exchange fluctuation –this will be governed by ICDS VI (effects of

changes of foreign exchange rates)

• Administration and general overheads shall be excluded from actual cost if not

relating to specific asset; however, expenses which are specifically attributable to

construction of a project or acquisition of a fixed asset or bringing it to its working

condition should be included as part of the cost of the project or the asset

• Expenditure on start-up and commissioning of a project shall be capitalized, while

expenditure post commencement of commercial production shall be expensed.

Expenditure incurred on test runs and experimental production should be

capitalised

ICDS V– Tangible Fixed Assets

Components of actual cost of fixed assets

63

• Actual cost of Self-constructed assets

− Same principles discussed for acquired assets would apply to compute actual

cost of self-constructed assets; costs attributable to construction activity in

general and can be allocated to the specific tangible fixed asset can also be

included in the actual cost

− Internal profits shall be eliminated in arriving at such costs

• Non-monetary consideration

- Tangible asset shall be recorded at its fair value if acquired for non-monetary

consideration i.e. in exchange for another asset or shares or other securities

• Valuation of tangible fixed assets in special cases

- The proportion in the actual cost, accumulated depreciation and written down

value of jointly owned tangible fixed assets should be grouped together with

other similar fully owned tangible fixed assets

- Consolidated price for acquiring group of assets shall be apportioned on fair

basis

ICDS V– Tangible Fixed Assets

Actual cost of fixed assets in different scenarios

64

• Improvements and repairs

- An expenditure that increases the future benefits from the existing asset

beyond its previously assessed standard of performance is added to its actual

cost; for example, an expenditure that results in an increase in the capacity of

a machine would be capitalized

- If an addition or extension to an existing asset is capital in nature and

becomes an integral part of the existing asset, it should be added to the actual

cost of the asset; however, if it has a separate identity and is capable of being

used after the existing asset is disposed it, it shall be treated as a separate

asset

• Depreciation

- Depreciation will be as per the Act

• Transfers

- Income on transfer of the tangible fixed asset should be computed as per the

Act i.e. the sections governing capital gains

ICDS V– Tangible Fixed AssetsImprovements and repairs, depreciation and transfers

65

• If the acquisition or construction of a tangible fixed asset commenced before 31

March 2016 but was not completed by that date, its actual cost will be recorded

in accordance with ICDS V

• With respect to assets for which actual cost was recognised for the previous

year commencing on or before 1 April 2015 (i.e. FY 2015-16 and earlier), the

same actual cost will be considered for FY 2016-17 and later as well

ICDS V– Tangible Fixed AssetsTransitional Provisions

66

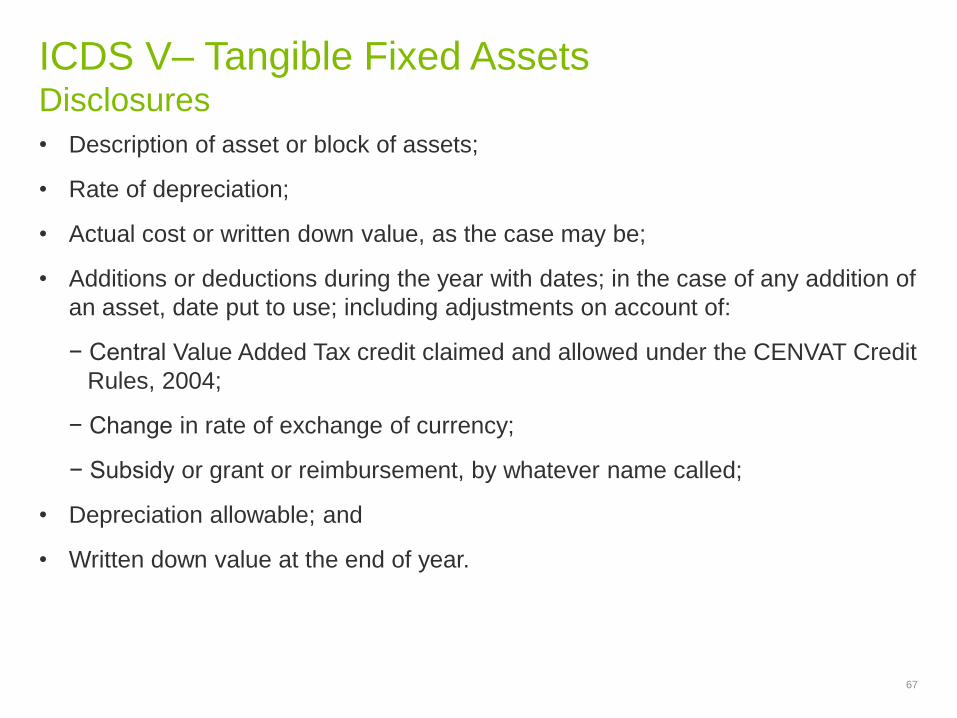

• Description of asset or block of assets;

• Rate of depreciation;

• Actual cost or written down value, as the case may be;

• Additions or deductions during the year with dates; in the case of any addition of

an asset, date put to use; including adjustments on account of:

− Central Value Added Tax credit claimed and allowed under the CENVAT Credit

Rules, 2004;

− Change in rate of exchange of currency;

− Subsidy or grant or reimbursement, by whatever name called;

• Depreciation allowable; and

• Written down value at the end of year.

ICDS V– Tangible Fixed AssetsDisclosures

67

Question no. 15

Para 8 of ICDS-V states expenditure incurred in commissioning of project,

including expenditure incurred on test runs and experimental production shall be

capitalised. It also stated that expenditure incurred after the plant has begun

commercial production i.e., production intended for sale or captive consumption

shall be treated as revenue expenditure. What shall be the treatment of expense

incurred after the conduct of test runs and experimental production but before

commencement of commercial production?

Answer: As clarified in Para 8 of ICDS-V, the expenditure incurred till the plant has

begun commercial production, that is, production intended for sale or captive

consumption, shall be treated as capital expenditure

ICDS V– Tangible Fixed AssetsRelevant FAQs as per CBDT’s circular no. 10 of 2017

68

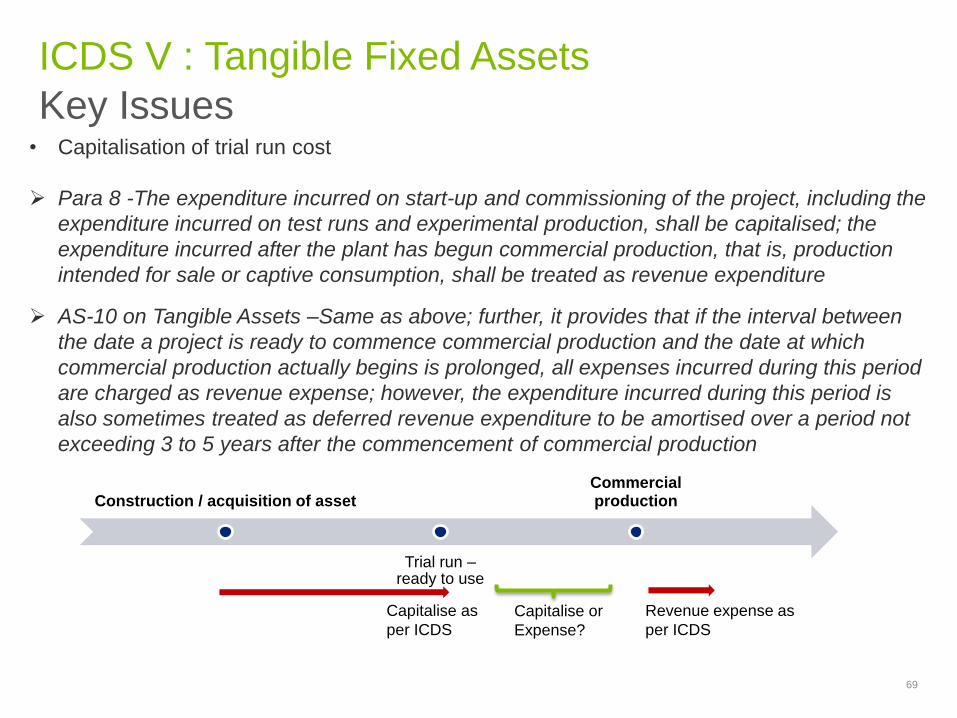

Key Issues

ICDS V : Tangible Fixed Assets

• Capitalisation of trial run cost

Para 8 -The expenditure incurred on start-up and commissioning of the project, including the

expenditure incurred on test runs and experimental production, shall be capitalised; the

expenditure incurred after the plant has begun commercial production, that is, production

intended for sale or captive consumption, shall be treated as revenue expenditure

AS-10 on Tangible Assets –Same as above; further, it provides that if the interval between

the date a project is ready to commence commercial production and the date at which

commercial production actually begins is prolonged, all expenses incurred during this period

are charged as revenue expense; however, the expenditure incurred during this period is

also sometimes treated as deferred revenue expenditure to be amortised over a period not

exceeding 3 to 5 years after the commencement of commercial production

69

Construction / acquisition of asset

Trial run –ready to use

Commercial production

Capitalise as

per ICDS

Revenue expense as

per ICDS

Capitalise or

Expense?

• Whether capitalisation of trial run expenditure is in line with current practice?

- Expenditure incurred on trial runs should be capitalised -Gujarat HC case of

Saurashtra Cement [127 ITR 47], Delhi HC case of Food Specialities[136 ITR

203], Bombay HC case of G T Industries (203 ITR 538)

- ICDS is in line with above decisions

• Question no. 15 of CBDT’s FAQs covers this issue with the question ‘what shall

be the treatment of expense incurred after the conduct of test runs and

experimental production but before commencement of commercial production?’

- According to the CBDT, the expenditure incurred till the plant has begun

commercial production, that is, production intended for sale or captive

consumption, shall be treated as capital expenditure; this would imply that

expense incurred after the conduct of test runs and experimental production

but before commencement of commercial production should be capitalised

ICDS V– Tangible Fixed AssetsCapitalisation of trial run cost

70

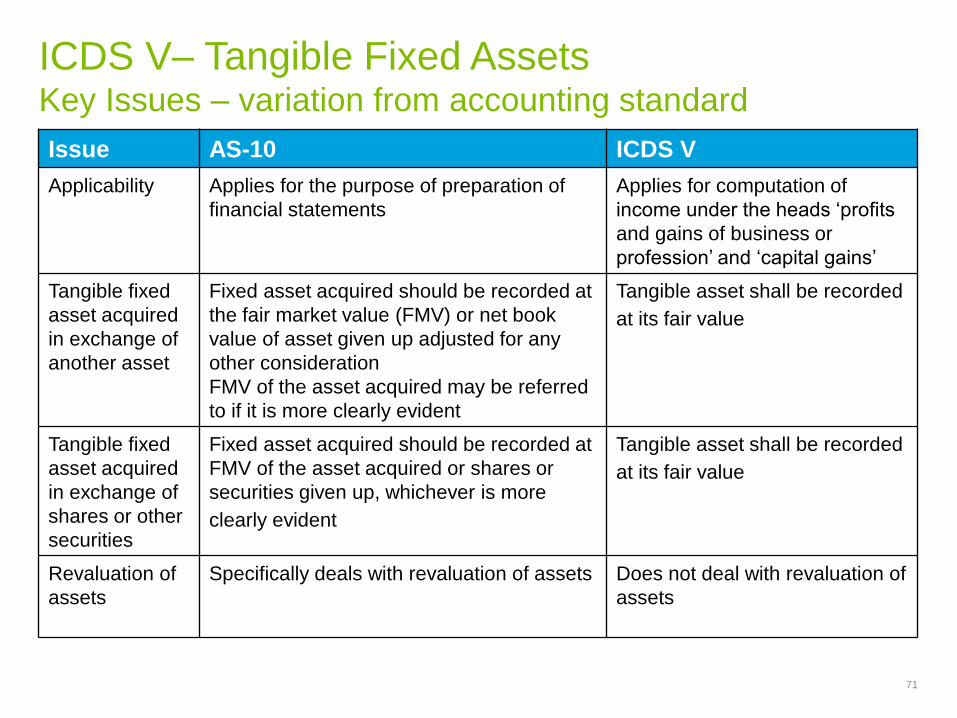

Issue AS-10 ICDS V

Applicability Applies for the purpose of preparation of

financial statements

Applies for computation of

income under the heads ‘profits

and gains of business or

profession’ and ‘capital gains’

Tangible fixed

asset acquired

in exchange of

another asset

Fixed asset acquired should be recorded at

the fair market value (FMV) or net book

value of asset given up adjusted for any

other consideration

FMV of the asset acquired may be referred

to if it is more clearly evident

Tangible asset shall be recorded

at its fair value

Tangible fixed

asset acquired

in exchange of

shares or other

securities

Fixed asset acquired should be recorded at

FMV of the asset acquired or shares or

securities given up, whichever is more

clearly evident

Tangible asset shall be recorded

at its fair value

Revaluation of

assets

Specifically deals with revaluation of assets Does not deal with revaluation of

assets

ICDS V– Tangible Fixed AssetsKey Issues – variation from accounting standard

71

• Proviso 2 to section 43(1) inserted by the Finance Act, 2017

− As per the above proviso, if any asset is acquired by a taxpayer by paying an

amount exceeding INR 10,000 to a person during a day by any mean other

than cheque or electronic clearing system of a bank, such payment will be

ignored for determining actual cost; accordingly, depreciation would not be

available under the Act

- This implies that even if a particular expense can be considered as actual cost

as per ICDS V, the above proviso would debar its inclusion in actual cost if it is

a cash payment exceeding INR 10,000 in a day to one person

ICDS V– Tangible Fixed AssetsInterplay between ICDS and Income-tax Act

72

ICDS VI:

Changes in Foreign

Exchange Rates

73

Scope

ICDS VI : Changes in Foreign Exchange Rates

ICDS VI deals with :-

a)treatment of transactions in foreign currencies;

b)translating the financial statements of foreign operations;

c)treatment of foreign currency transactions in the nature of forward exchange contracts

74

• Reporting Currency

- India Operations

- Overseas branch v. overseas JV/subsidiary

• Foreign currency

• Foreign currency transactions

- Denominated in foreign currency and settlement in foreign currency

• Monetary v. non-monetary items

Definitions

ICDS VI – Foreign exchange

75

AS - 11 ICDS IND AS 21

Foreign currency

transaction –

Initial Recognition

Record at

Spot Rate

As on the date of transaction or at a weekly / monthly

average rate (if rates do not fluctuate significantly from

actual)

Same as

AS

Conversion at last

day of the

Previous Year

All forex

differences

are

recognised

in P&L

Monetary Items –

Conversion at closing rate and recognize exchange

difference in P&L (subject to sec 43A read with Rule 115)

Non-monetary items (except inventory) –

Convert at rate as on date of transaction, exchange

difference shall not be recognised (subject to the

provisions of sec. 43A r.w.Rule 115)

Inventory – which is non-monetary item and is carried at

net realisable value denominated in a foreign currency,

shall be reported using the exchange rate that existed

when such value was determined.

Same as

AS

Q. 16 of FAQ – Taxability of opening Balance of Foreign Currency Translation Reserve (FCTR) relating to

Non-integral foreign operation as on 1 April 2016, if any, recognised as per Accounting Standards (AS) 11

?

Ans – FCTR balance as on 1 April 2016 pertaining to exchange difference on monetary items for

non-integral operations, shall be recognised in the previous year relevant for the assessment year

to the extent not recognised in the income computation in the past.

ICDS VI – Foreign exchange

76

AS - 11 ICDS IND AS 21

Forward contract -

not intended for

trading or

speculation and

entered to

establish reporting

currency on

settlement

Same as per ICDS Premium/discount is

amortized over the life of

contract.

Restated on MTM basis at

year end and difference is

recognized in P&L.

Profit/loss on cancellation or

renewal is also recognized in

P&L

Forward exchange contract

accounting treatment is similar to

Derivative accounting.

Derivatives are measured at fair

value with change in fair value

recognized in profit or loss

unless they qualify as hedging

instruments in a cash flow hedge

or in a net investment hedge.

Forward contract -

(trading,

speculation, firm

commitment,

highly probable

forecast)

Marked to market at

each balance sheet

date and the gain or

loss be recognized

in the P&L a/c.

No amortization of

premium/ discount.

Premium, discount or

exchange difference on

contracts be recognized at

the time of settlement only.

Forward exchange contract

accounting treatment is similar to

Derivative accounting.

Derivatives are measured at fair

value with change in fair value

recognized in profit or loss

unless they qualify as hedging

instruments in a cash flow hedge

or in a net investment hedge.

Q. 10 of FAQ – Which ICDS would govern derivative instruments ?

Ans – ICDS VI (subject to para 3 of ICDS-VIII) provides guidance on accounting for derivative contracts

such as forward contracts and other similar contracts. For derivatives, not within the scope of ICDS-VI,

provisions of ICDS-I would apply.

Revenue related

Foreign Exchange

77

Trade receivables,

payables, working

capital loans,

foreign currency

bank balances,

etc

Accounting

Income Tax

AS

Ind AS – P&L

IT Act, 1961 -

P& L

ICDS – P&L

If part of

borrowing cost,

cost, inventories

is part of

qualifying asset

Otherwise, P&L

Monetary Items-

Exchange

difference to be

recognised as

income /

expense

Capital related

Foreign Exchange

78

Fixed assets and

related payables

and borrowings

Accounting

Income Tax

AS

Ind AS – P&L

IT Act, 1961 -

P& L

ICDS – P&L

If part of

borrowing cost,

cost, capitalised

if part of

qualifying asset

Otherwise, P&L

In case of opting

for para 46A,

capitalised

Imported –

Capitalised on

settlement

Domestic - P&L

Derivatives – Fair value hedges

Foreign Exchange

79

Forwards and

options

Accounting

Income Tax

AS

Ind AS

IT Act, 1961 -

ICDS – P&L

Initial cost such

as premium, etc.

is amortised

over period of

contract

Exchange

difference –

P&L

Dept stand – On

settlement basis

Premium, discount is to

be amortised over the

period of the contract

Exchange Difference –

P&L

Derivatives – Cash flow hedges

Foreign Exchange

80

Forwards and

options

Accounting

Income Tax

AS

Ind AS

IT Act, 1961 -

ICDS – P&L

AS 30 –

Reserves

Otherwise –

Recognise MTM

losses as

incurred, gains

on settlement

Reserves

Recognise premium,

discount & exchange

difference on

settlement

Dept stand – On

settlement basis

Foreign Exchange

Derivatives – Speculative/Trading

81

Forwards and

options

Accounting

Income Tax

AS

Ind AS

IT Act, 1961 -

ICDS – P&L

Recognise MTM

gains as losses

as incurred

Recognise

gainson

settlement

Recognise

MTM

losses/gains as

incurred

Recognise premium,

discount & exchange

difference on

settlement

Dept stand – On

settlement basis

ICDS VI – Effects of Changes in Foreign

Exchange Rates

IMPACT

Can foreign exchange gain / loss on loan for purchase of capital assets in India be treated as

income / expense?

• ICDS only refers to section 43A

• As per section 43A, exchange difference relating to acquisition of a foreign asset is adjusted to

the cost of the asset at the time of payment

• Section 43A is silent on Indian assets

Illustration: Impact of ICDS on loan borrowed for purchase of capital assets in India

Overseas

India

Capital

asset

Exchange difference on loan –

adjust to asset cost as per

section 43A on settlement of

loan

Loan in foreign

currency for

purchase of

assets

Exchange difference on loan – ICDS treats

difference as revenue income / expense at

year end or settlement, whichever is earlier

Indian

company

Capital

asset

Overseas

lender

1 2

3

82

Case Study

ICDS VI : Changes in Foreign Exchange Rates

Treatment of exchange difference relating to borrowings taken for acquiring Indian

assets

A Ltd. purchased a machinery worth Rs 10 crore against the funds borrowed from a foreign

source at 1% p.m.

Issue:

• Can the exchange difference relating to borrowings taken for acquiring Indian assets be

treated as a revenue item?

83

FY 2016-17

Cost of Machinery = Rs. 10 crore

Interest incurred for the whole year in respect of foreign borrowings = Rs. 12 Lakh

Case Study

ICDS VI : Changes in Foreign Exchange Rates

Analysis

• Exchange difference on fixed assets

⁻ Para 6 of ICDS on ‘Tangible Fixed Assets’ :

The cost of a tangible fixed asset may undergo changes subsequent to its acquisition or

construction on account of (i) price adjustment, changes in duties or similar factors; or (ii)

exchange fluctuation as specified in ICDS on the effects of changes in foreign exchange rates

⁻ Para 5 of ICDS VI:

In respect of monetary items, exchange differences arising on the settlement thereof or on

conversion thereof at last day of the previous year shall be recognised as income or as

expense in that previous year.

⁻ Para 6 of ICDS VI

Initial recognition, conversion and recognition of exchange difference is subject to provisions of

section 43A or Rule 115 of the Act

• Current Practice

⁻ Amount payable due to foreign exchange difference on repayment of a loan is a capital

expenditure

84

Case Study

ICDS VI : Changes in Foreign Exchange Rates

Analysis

• As per section 43A, exchange difference relating to acquisition of a foreign asset is adjusted to

the cost of the asset at the time of payment

• Various HC judgements have held that higher amount payable due to foreign exchange

difference on repayment of a loan is a capital expenditure, not allowable as a deduction

• However, now ICDS permits exchange loss on monetary items to be recognised as an expense

and exchange gain as income

• Reliance can be place on recent decision of Pune Tribunal in case of Cooper Corporation Pvt

Ltd – 159 ITD 165 and Chennai Tribunal in case of Hyundai Motor India Limited – ITA

No.853/Chnny/2014 and 563/Chny/2015 wherein it has been held foreign exchange loss is

allowable under section 37(1) of the act.

• Further, ICDS on ‘Tangible Fixed Assets’ only states that adjustment to cost of tangible asset

may be adjusted for exchange difference but does not make the same mandatory.

85

Can the exchange difference relating to borrowings taken for

acquiring Indian assets be treated as a revenue item?

ICDS VIII: Securities

86

Scope

ICDS VIII: Securities

87

Scope

Securities held as stock in

trade

Part A

Securities held by a scheduled bank or

public financial institutions formed under

a Central or a State Act or so declared

under the Indian Companies Act

Part B

Securities shall be carried at actual cost (including purchase price, brokerage, cess, tax, etc.) or net

realizable value, whichever is lower at year-end. Unlisted / not regularly quoted securities will be

recognised at actual cost

88

• Comparison to be done category-wise and not on individual basis which has been also clarified in FAQ No. 19 – CBDT clarification dated 23 March 2017

• For this purpose, securities shall be classified as: shares, debt securities, convertible securities and any other

Comparison for cost vs Net realizable value

• Unpaid interest accrued before the acquisition of an interest-bearing security included in the price paid for the security – deducted from actual cost to the extent it pertains to pre-acquisition period

Pre-acquisition interest

ICDS VIII: SecuritiesSecurities held as stock-in-trade – Part A

•Where actual cost initially recognised cannot be ascertained by reference to specific identification, the cost of such security shall be determined as per First in First out method

First in First out method is permissible where actual cost is unascertainable

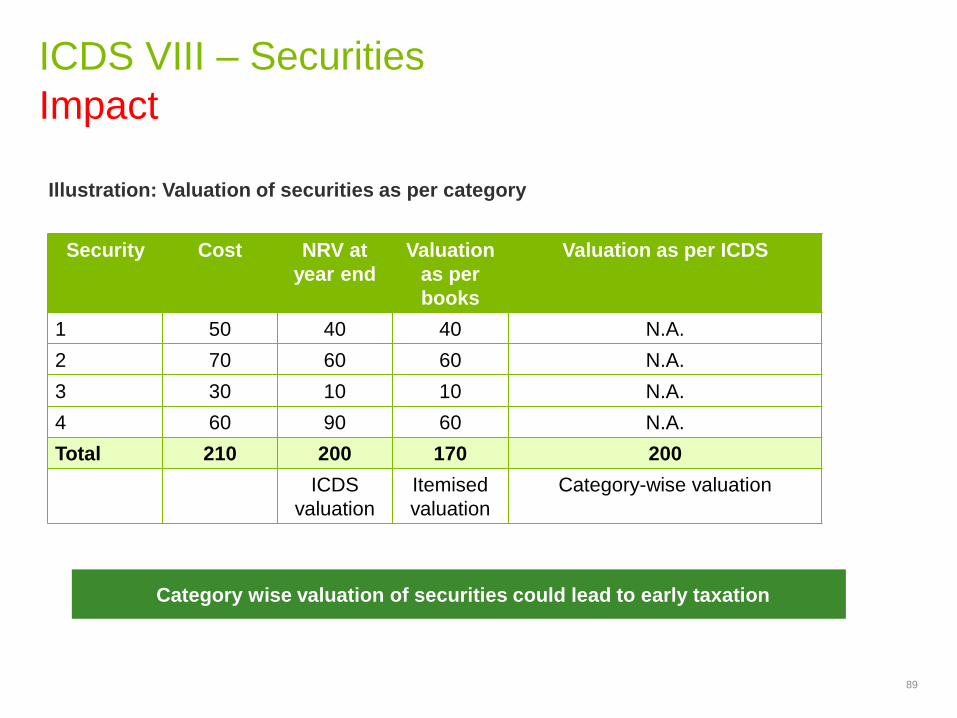

ICDS VIII – Securities

Impact

Security Cost NRV at

year end

Valuation

as per

books

Valuation as per ICDS

1 50 40 40 N.A.

2 70 60 60 N.A.

3 30 10 10 N.A.

4 60 90 60 N.A.

Total 210 200 170 200

ICDS

valuation

Itemised

valuation

Category-wise valuation

Category wise valuation of securities could lead to early taxation

Illustration: Valuation of securities as per category

89

Measurement of securities

90

ICDS VIII: SecuritiesCase Study - 1

Security Category Comments

Equities (listed) held as

stock in trade

Name of stock Actual cost NRV

ICDS VIII is applicable – Shares

will be valued at actual cost

initially recognized or net

realizable value, whichever is

lower, and the comparison shall

be done category-wise

Therefore, equities to be valued

at INR 3,250

ABC Co 500 1,050

XYZ Co 2,200 1,960

RNIP Co 350 350

BCD Co. 200 240

Total 3,250 3,600

Equities (unlisted) held

as stock in trade

Name of stock Actual cost NRV

ICDS VIII is applicable –

However, unlisted securities will

be valued at actual cost initially

recognized Therefore, equities

to be valued at INR 7,200

ABC Co 5,000 1,050

XYZ Co 2,200 1,960

Total 7,200 3,010

ICDS VIII: Securities

Securities held by Scheduled Bank or public financial institutions formed under a Central or a State Act or so declared under the Indian Companies ActDefinition –• Scheduled Bank shall have meaning assigned to it in clause (ii) of the Explanation to

section 36(1)(viia) of the Act• Securities shall have the meaning assigned to it in section 2(h) of the Securities Contract

(Regulation) Act, 1956 (42 of 1956) and shall include share of a company in which public are not substantially interested.

Classification, Recognition and Measurement – Para 3

• Securities shall be classified, recognised and measured in accordance with the extent

guidelines issued by the Reserve Bank of India in this regard and any claim for deduction

in excess of the said guidelines shall not be taken into account. To this extent, the

provisions of ICDS VI on the effect of changes in foreign exchange rates relating to

forward exchange contracts shall not apply

91

ICDS IX:

Borrowing Costs(Corresponds to AS 16 / IndAS 23)

It deals with treatment of borrowing costs however the actual or imputed

cost of owners‟ equity and preference share capital is not cover under ICDS

IX

92

ICDS IX- Borrowing Costs

Borrowing Costs are interest and other costs incurred by a person in connection with the borrowing

of funds

93

Includes

- Commitment charges

- Amortised amount of discounts or premiums

- Amortised amount of ancillary costs

- Finance charges in respect of assets acquired under finance lease

Excludes

- actual or imputed cost of owner’s equity and preference share capital

ICDS IX– Borrowing Costs

94

ICAI Accounting Standards (AS) ICDS

Qualifying asset Asset that necessarily takes a

substantial period of time to get

ready for its intended use or

sale (generally 12 months)

Assets that requires a period of 12months or more for its

acquisition, construction or production

- Land, building, machinery, plant or furniture, being

tangible assets

- Know-how, patents copyrights, trademarks, licenses,

franchises or any other business or commercial rights

of similar nature, being intangible assets;

- Inventories that require a period of 12months or more

to bring them to saleable condition

Capitalization of

specific

borrowing

Actual borrowing cost less any

income on the temporary

investment

Actual borrowing cost only. Investment income to offer for

tax.

(Tuticorin Alkali Chemicals and Fertilizers Ltd vs CIT 227

itr 172)

Capitalization of

general

borrowing

Apply capitalization rate to

expenditure on qualifying asset.

Capitalization rate = weighted

average cost of borrowing

Ratio of qualifying assets to total assets i.e. as per

prescribed formula in respect of general borrowings which

is other than specific borrowings

ICDS IX– Borrowing Costs

95

ICDS

Borrowing cost eligible

for capitalization

Specific borrowing – actual borrowing costs incurred

General borrowing – amount to be determined as per prescribed formula

Commencement of

capitalization

Specific borrowing – from the date on which funds were borrowed

General borrowing – from the date on which funds were utilised

Cessation of

capitalization

Tangible / intangible assets – when the asset is first put to use

Inventory – when substantially all activities necessary to prepare it for intended

sale are complete

ICDS IX : Borrowing Costs

Analysis

• Capitalization of general borrowings

Para 6 of ICDS - To the extent the funds are borrowed generally and utilised for the purposes of acquisition,

construction or production of a qualifying asset, the amount of borrowing costs to be capitalised shall be

computed in accordance with the following formula namely:

General borrowing cost X

• AS 16 on Borrowing Costs - To the extent that funds are borrowed generally and used for the purpose

of obtaining a qualifying asset, the amount of borrowing costs eligible for capitalisation should be

determined by applying a capitalisation rate to the expenditure on that asset. The capitalisation rate

should be the weighted average of the borrowing costs applicable to the borrowings of the enterprise that

are outstanding during the period, other than borrowings made specifically for the purpose of obtaining a

qualifying asset. The amount of borrowing costs capitalised during a period should not exceed the

amount of borrowing costs incurred during that period

96

average cost of qualifying asset as appearing in the balance sheet on first and last day of the previous year

average of total assets appearing in the balance sheet on first and last day of the previous year (other than

those assets which are directly funded out of specific borrowings)

Calculation of interest expense in respect of general borrowings (refer formula of earlier slide)

ICDS IX – Borrowing costs

Impact

Particulars Amount (Rs.)

Total assets appearing in balance

sheet as on 31.3.17*1,000

Total tangible assets acquired

during year 2016-2017700

General borrowings 500

Interest on general borrowings 50

Specific borrowings 200

Interest on specific borrowings 20

Cost of assets constructed using

general borrowings 450

Cost of assets constructed using

specific borrowings 200

Under – construction assets value 300

Particulars ICDS AS 16

Capitalizati

on of

general

borrowing

cost

= 22.73

Working:

50 X [(700 - 200) / 2]

[(300+1000-200) / 2]

= 45 (450 X 10%)

Working:

Weighted

average

borrowing cost is

10% i.e. (50/500)

Capitalization of general borrowing cost under ICDS and AS differs

• Does not consist of under-construction assets at beginning or end

of the year

97

Case Study-1

ICDS IX : Borrowing Costs

Interest expense to be claimed as revenue deduction u/s 36(1)(iii) , if not falling under

proviso to the said section.

A Ltd. constructed a building worth Rs. 10 crore against the funds borrowed from a bank at 1% p.m.

Issue:

• Whether the interest expense can be claimed as revenue deduction u/s 36(1)(iii), if not falling

under proviso to the said section?

98

FY 2016-17

Cost of Building = Rs. 10 crore

Interest incurred = Rs. 12 Lakh

Case Study-1

ICDS IX : Borrowing Costs

Analysis

• Section 36(1)(iii) of Act:

The deductions provided for in the following clauses shall be allowed in respect of the matters

dealt with therein, in computing the income referred to in section 28 - the amount of the interest

paid in respect of capital borrowed for the purposes of the business or profession

Provided that any amount of the interest paid, in respect of capital borrowed for acquisition of an

asset for extension of existing business or profession* (whether capitalised in the books of

account or not); for any period beginning from the date on which the capital was borrowed for

acquisition of the asset till the date on which such asset was first put to use, shall not be allowed

as deduction.

* Deleted by Finance act 2015 to remove the differential treatment for availability of interest in

case of capital borrowed for purchase of asset for existing business and for extension of existing

business

99

Case Study-1

ICDS IX : Borrowing Costs

Analysis

• Qualifying assets as per ICDS:

As per ICDS, Qualifying assets means

⁻ land, building, machinery, plant or furniture, being tangible assets;

⁻ know‐how, patents, copyrights, trade marks, licences, franchises or any other business or

commercial rights of similar nature, being intangible assets;

⁻ inventories that require a period of twelve months or more to bring them to a saleable

condition.

• Current Practice

⁻ Amount payable as interest and not falling under the proviso to Section 36(1)(iii) of Act is

claimed as revenue expense

100

ICDS IX : Borrowing Costs

Where qualifying asset as per AS 16 is not an asset for expansion of

business:

101

Particulars Profit and loss account

Tax claim under COI (Post

ICDS)

Borrowing cost Amount to be capitalised to the

cost of asset

Disallowed – amount to be

capitalised to the cost of asset

Income on temporary investment

of borrowed funds

To be netted off from borrowing

costs and capitalised

Will be taxed as income - No

netting off from the cost of asset

Depreciation Allowed on cost of asset which

includes borrowing cost

Allowed on cost of asset which

includes borrowing cost

ICDS IX – Borrowing costs

FAQs issued by CBDT on 23 March 2017

102

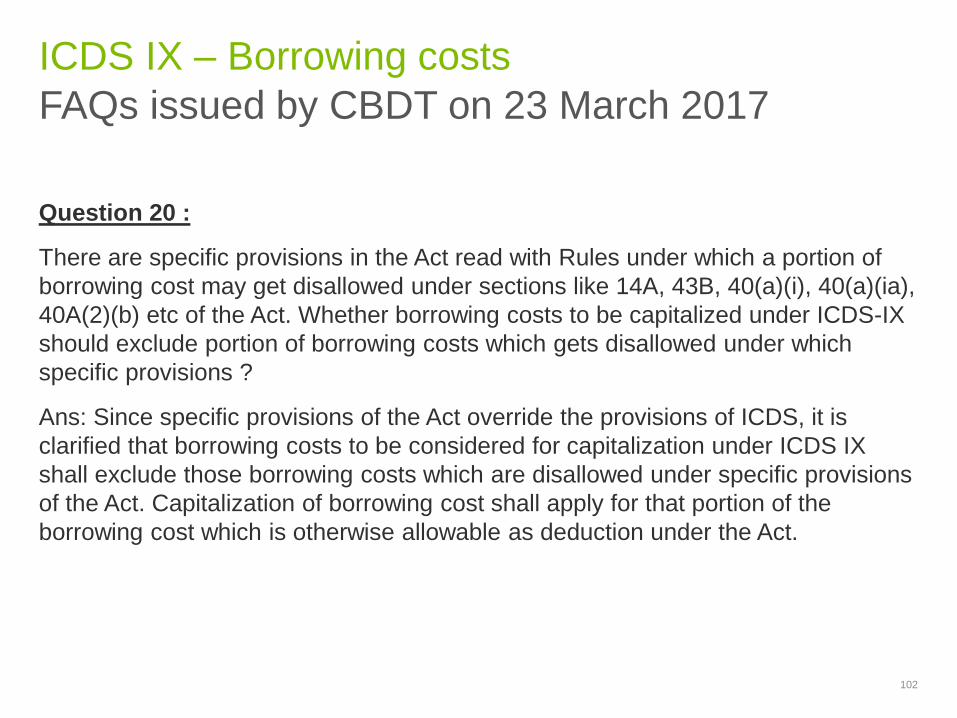

Question 20 :

There are specific provisions in the Act read with Rules under which a portion of

borrowing cost may get disallowed under sections like 14A, 43B, 40(a)(i), 40(a)(ia),

40A(2)(b) etc of the Act. Whether borrowing costs to be capitalized under ICDS-IX

should exclude portion of borrowing costs which gets disallowed under which

specific provisions ?

Ans: Since specific provisions of the Act override the provisions of ICDS, it is

clarified that borrowing costs to be considered for capitalization under ICDS IX

shall exclude those borrowing costs which are disallowed under specific provisions

of the Act. Capitalization of borrowing cost shall apply for that portion of the

borrowing cost which is otherwise allowable as deduction under the Act.

ICDS IX – Borrowing costs

FAQs issued by CBDT on 23 March 2017

103

Question 21 :

Whether bill discounting charges and other similar charges would fall under the definition of borrowing cost?

Ans: The definition of borrowing cost is an inclusive definition. Bill discounting charges and other similar charges are covered as borrowing cost.

Question 22 :

How to allocate borrowing costs relating to general borrowing as computed in accordance with formula provided under Para 6 of ICDS – IX to different qualifying assets?

Ans: The capitalization of general borrowing cost under ICDS-IX shall be done on asset-by-asset basis.

Disclosure requirements

ICDS IX : Borrowing Costs

The following disclosure shall be made in respect of borrowing costs:

a) the accounting policy adopted for borrowing costs;

b) the amount of borrowing costs capitalised during the previous year

104

ICDS – Impact on

Computation of Taxable

Income

105

Computation of taxable Income – Impact of ICDS

106

Profits and Gains from Business or Profession Pre ICDS Post ICDS

Net profit as per profit and loss account XXX XXX

Add: - Disallowance as per Act XXX XXX

Depreciation as per companies Act XXX XXX

Provision for gratuity XXX XXX

Less: Allowance as per Act (XXX) (XXX)

Depreciation as per Income tax Act (XXX) (XXX)

Allowance u/s 43B of the Income tax Act (XXX) (XXX)

Net profit before tax XXX XXX

Add / less : Adjustment on account of ICDS NA XXX

Valuation of Inventory (Standard Costing effect) NA XXX

Construction contract (Provision for expected loss) NA (XXX)

Foreign Exchange fluctuations (Premium of forward

contracts) NA XXX

Net Profit before after tax (after considering impact of

ICDS)XXX XXX

Computation of taxable Income – Impact of ICDS

107