Embed Size (px)

Citation preview

PROTRANSThe Role of Third Party Logistics Service Providers

and their Impact on Transport

Deliverable No 6

Final Public Report

Contract No.: 1999-RD.10795

ProjectCo-ordinator: Buck Consultants International

Partners: Cranfield University (UK)Zentrum für Logistik und Unternehmungsplanung GmbH (GE)Fraunhofer Institut Materialfluss und Logistik (GE)Ecorys Transport (NL)Stratec S.A. (BE)PTV Planung Transport Verkehr A.G. (DE)Linköping Universitet (SE)Technische Universität Berlin (DE)Environment, Transport & Planning (ES)Louis Berger S.A. (FR)

Work Package: 5

Work PackageLeader: Buck Consultants International

Status: Final public report

Date: August 2003

Project funded by the European Commission under the Competitive and SustainableGrowth Programme of the 5th Framework Programme

ContentsPage

Executive Summary 1

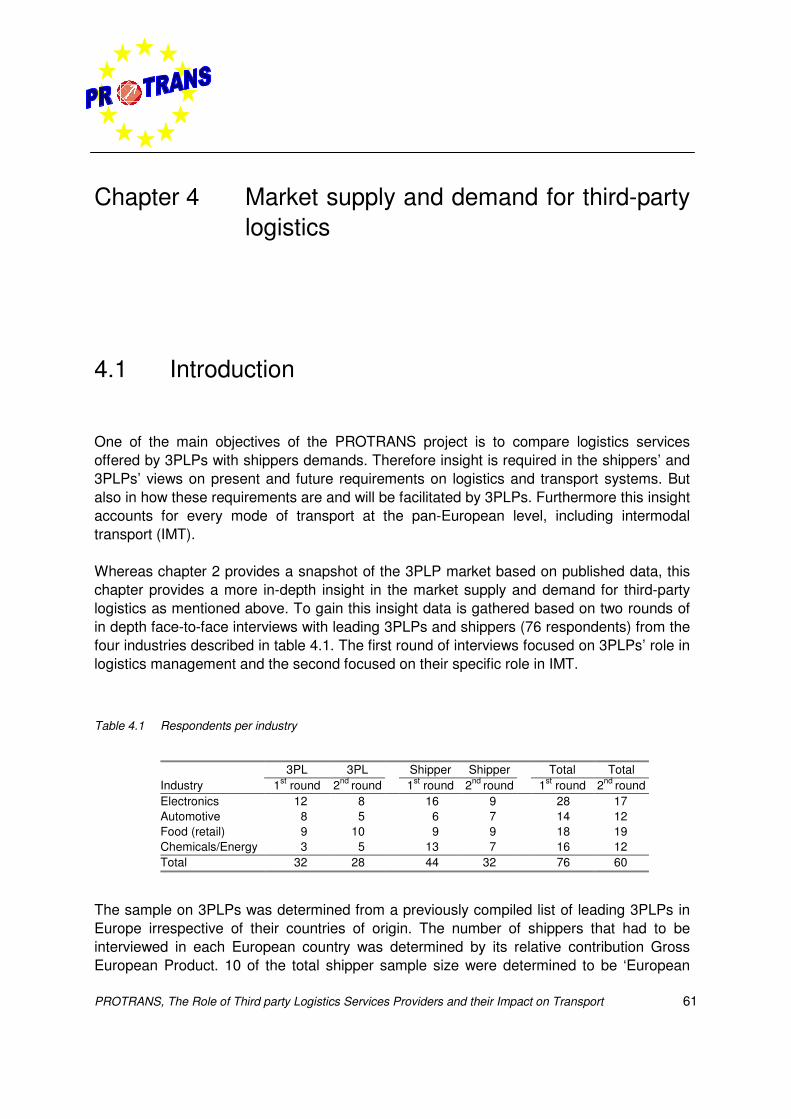

1 Introduction 12 Third-party logistics market overview 23 Regional perspective of third-party logistics 54 Market supply and demand for third-party logistics 105 Barriers and opportunities for third-party logistics 126 The potential for a modal shift 157 Conclusions and recommendations for policymakers 21

Chapter 1 Introduction 25

1.1 Background and definitions 251.2 Objectives of PROTRANS 261.3 Methodological approach 271.4 Report structure 29

Chapter 2 Third-party logistics market overview 31

2.1 Introduction and definitions 312.2 Typology of the logistics service provider 342.3 3PLP database development 392.4 Conclusions on the 3PLP market overview 40

Chapter 3 Regional perspective of third-party logistics 45

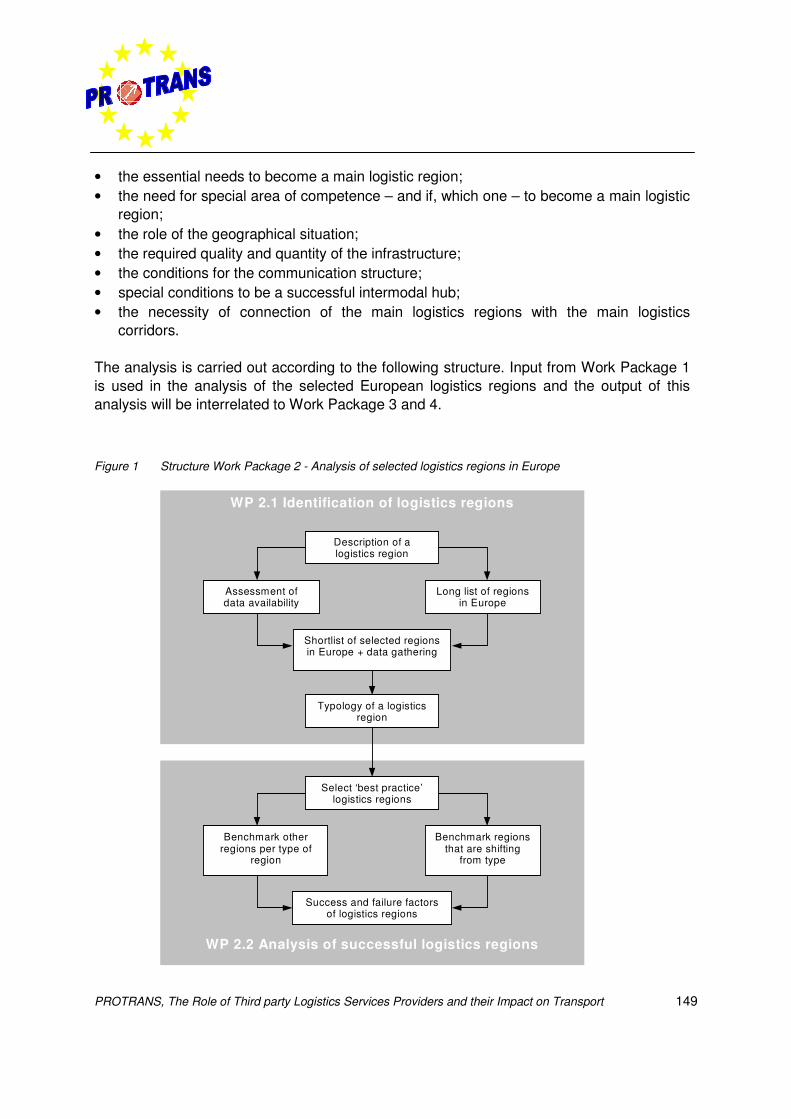

3.1 Introduction 453.2 Analysis of logistics regions in Europe 473.3 Typology of the logistics regions 543.4 Success and failure factors of logistics regions 563.5 Conclusions on the analysis of logistics regions 58

Page

Chapter 4 Market supply and demand for third-party logistics 61

4.1 Introduction 614.2 Conceptual framework and market conditions 624.3 Supply and demand of logistics services 654.4 Conclusions on supply and demand of logistics services 79

Chapter 5 Barriers and opportunities for third-party logistics 81

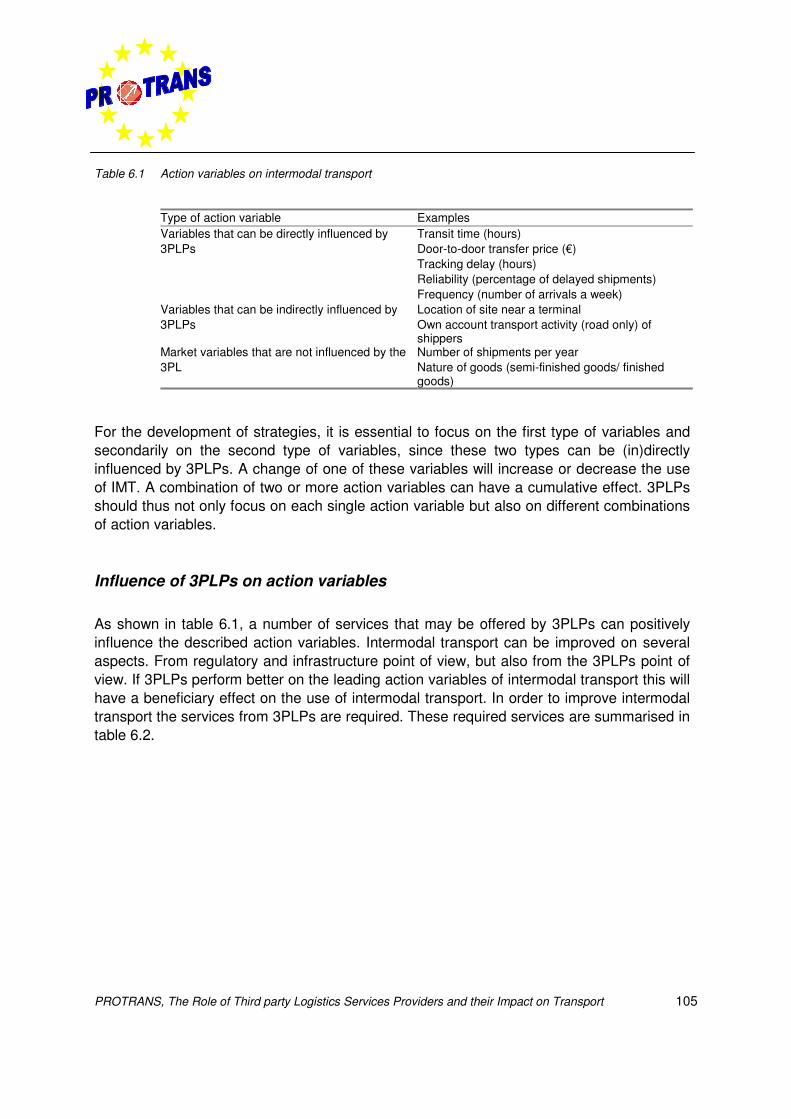

5.1 Introduction 815.2 Barriers and opportunities for further outsourcing 815.3 Barriers and opportunities to intermodal transport 895.4 Conclusions 97

Chapter 6 The potential for a modal shift 99

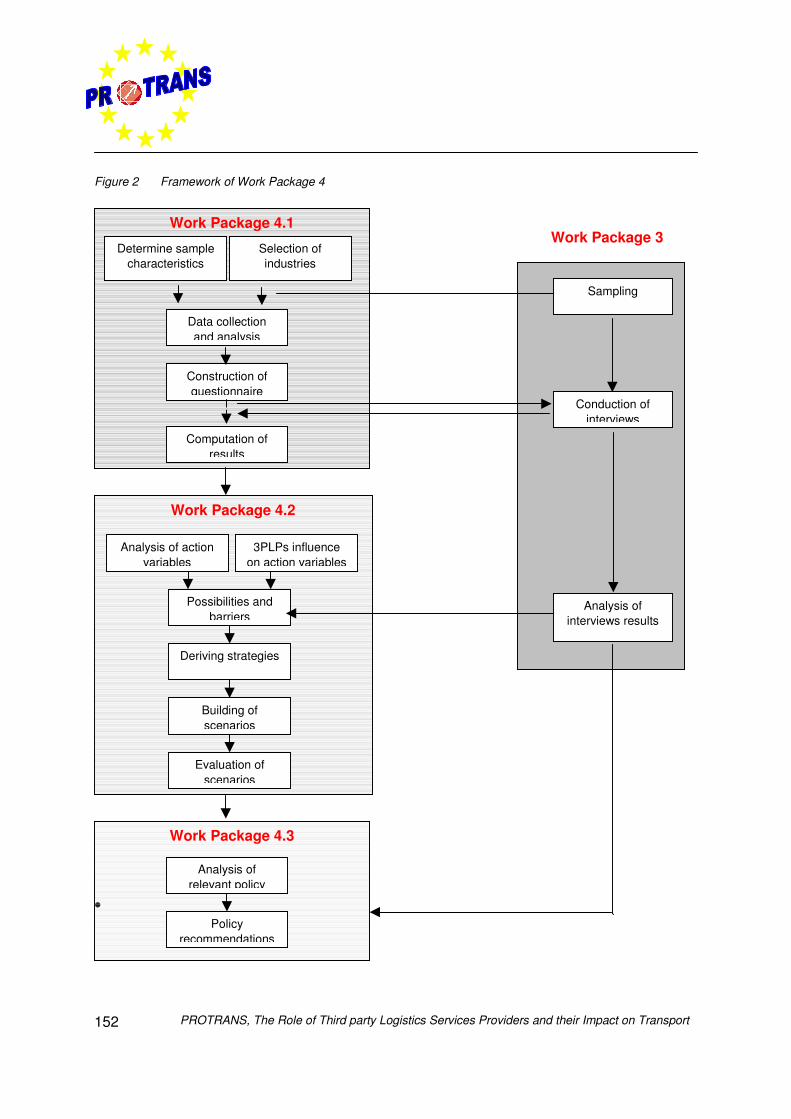

6.1 Introduction 996.2 Value of the services offered by 3PLPs 996.3 Strategies on intermodal transport 1046.4 Future scenario’s 1106.4 Conclusions 114

Chapter 7 Conclusions and recommendations for policymakers 117

7.1 Conclusions on the market position of 3PLP’s 1177.2 Conclusions on the regional perspective of 3PL 1187.3 Conclusions on the barriers and opportunities 1197.4 Conclusions on the intermodal potential 1217.5 Recommendations for policymakers 122

Page

Bibliography 133

Annexe 1 Description per work package 147

Annexe 2 Definitions of 3PL 157

Annexe 3 Type of clients 159

Annexe 4 Overview of sub-activities 161

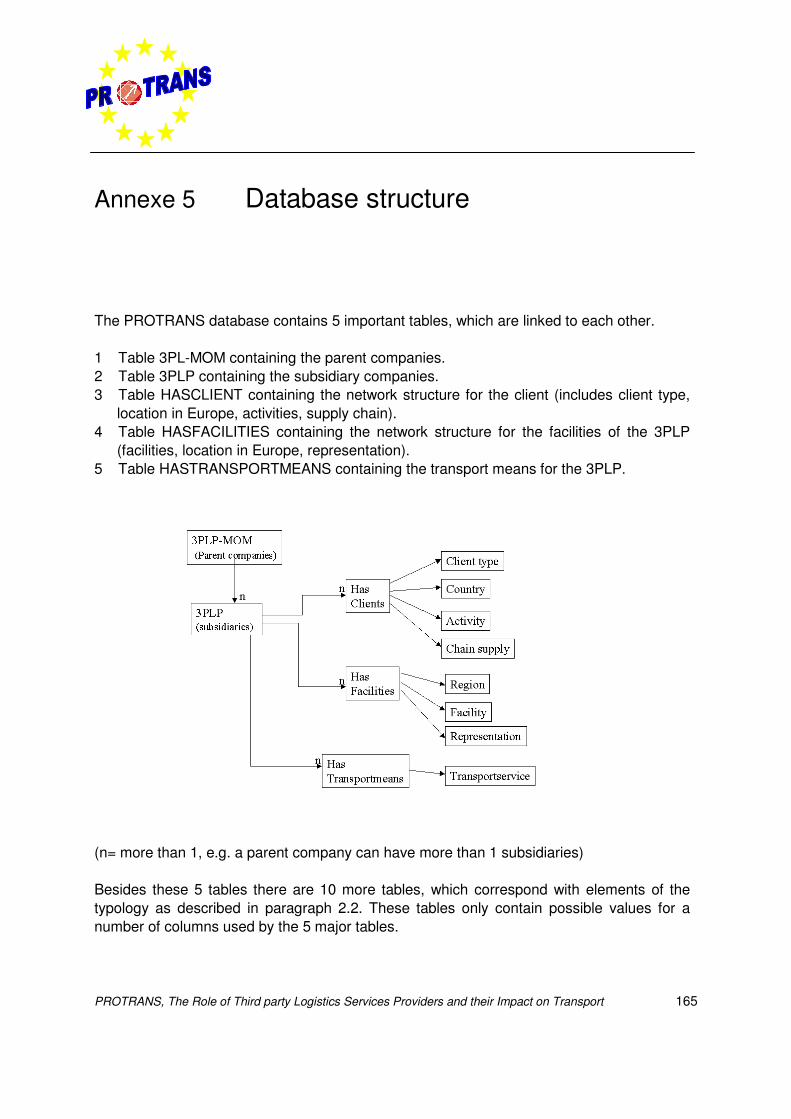

Annexe 5 Database structure 165

Annexe 6 Score per element of logistics regions 167

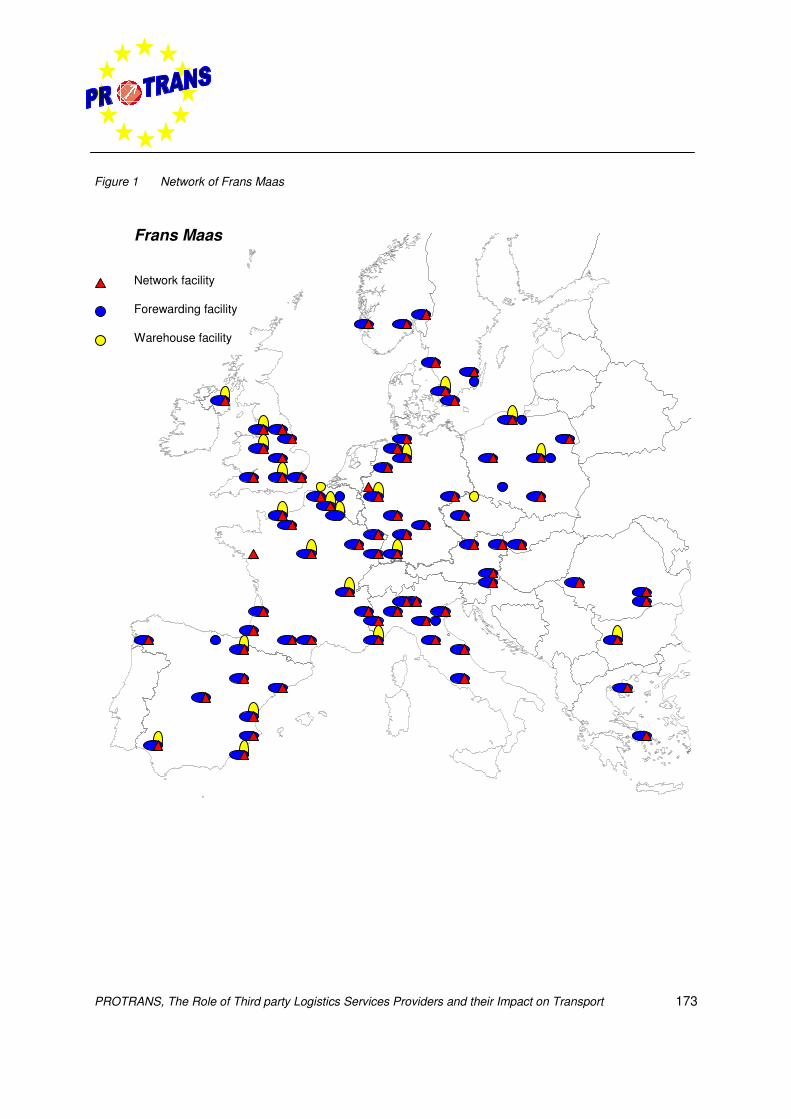

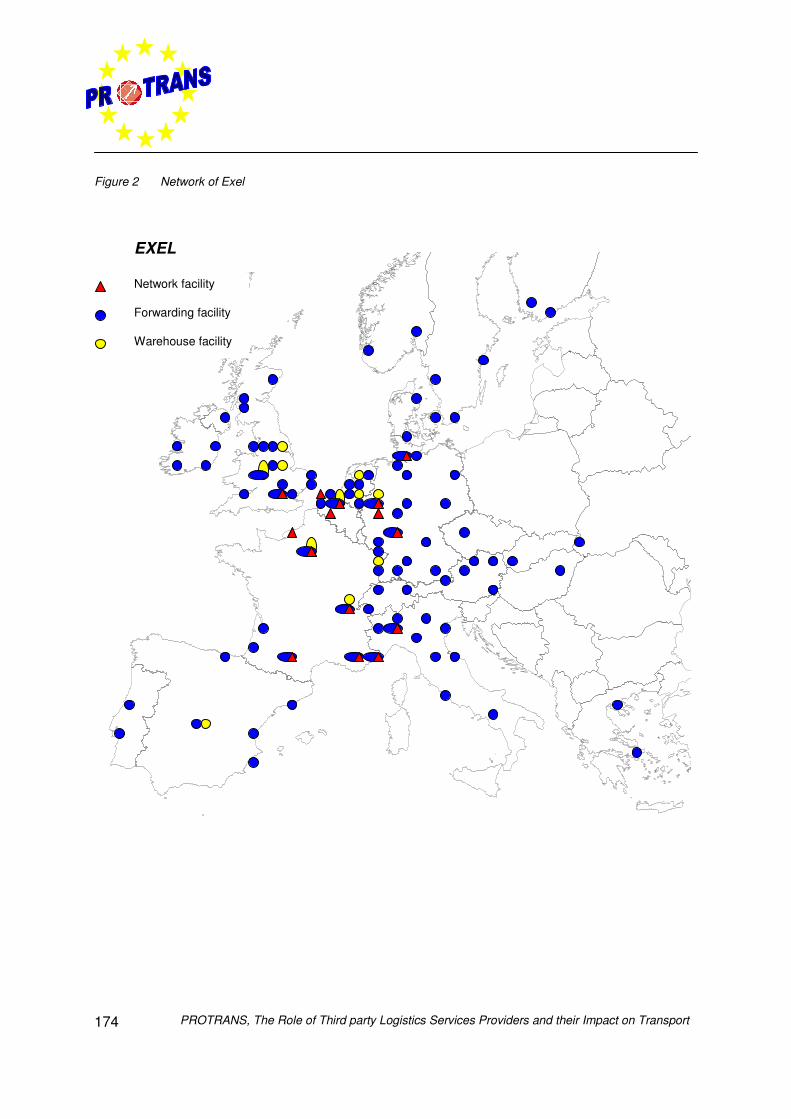

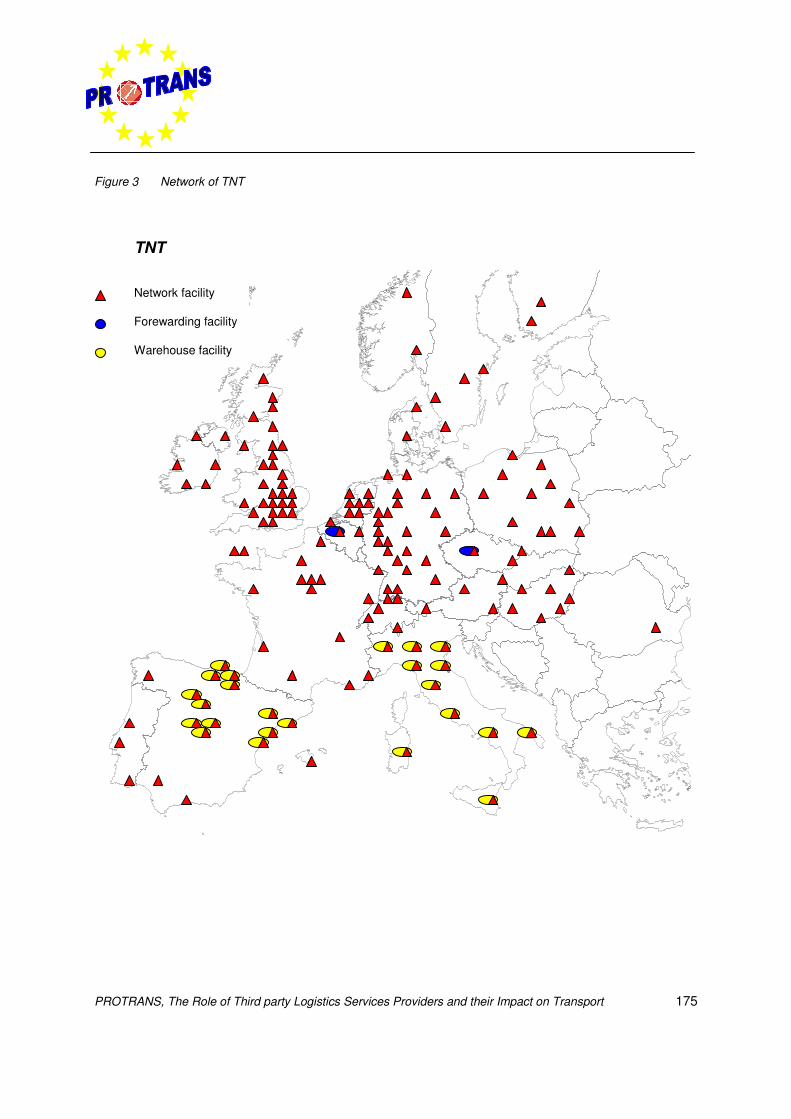

Annexe 7 Examples of 3PLP networks in Europe 171

Annexe 8 Typology of logistics regions 177

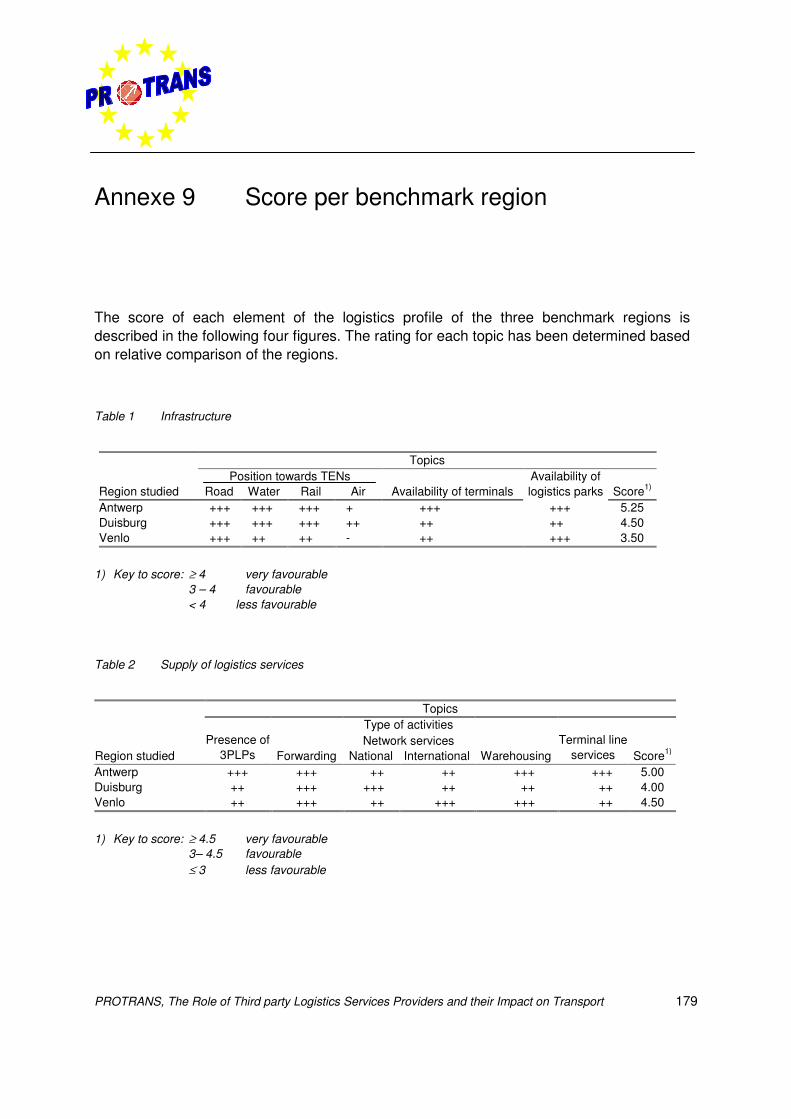

Annexe 9 Score per benchmark region 179

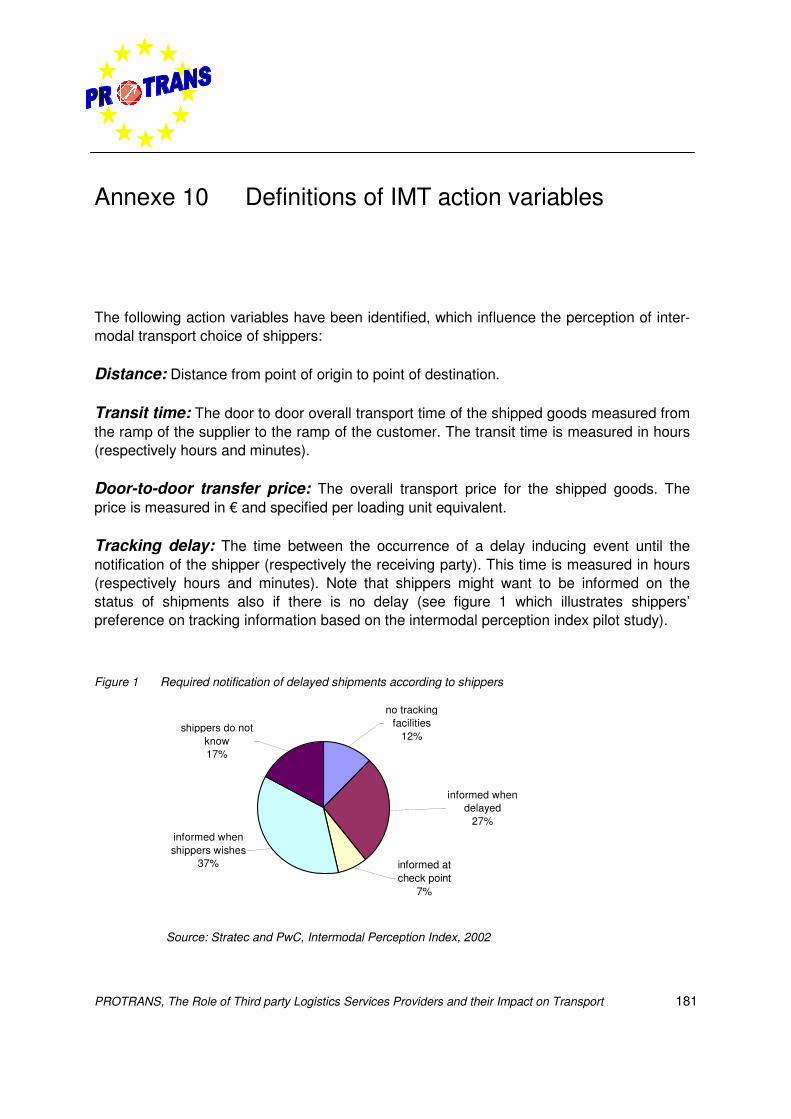

Annexe 10 Definitions of IMT action variables 181

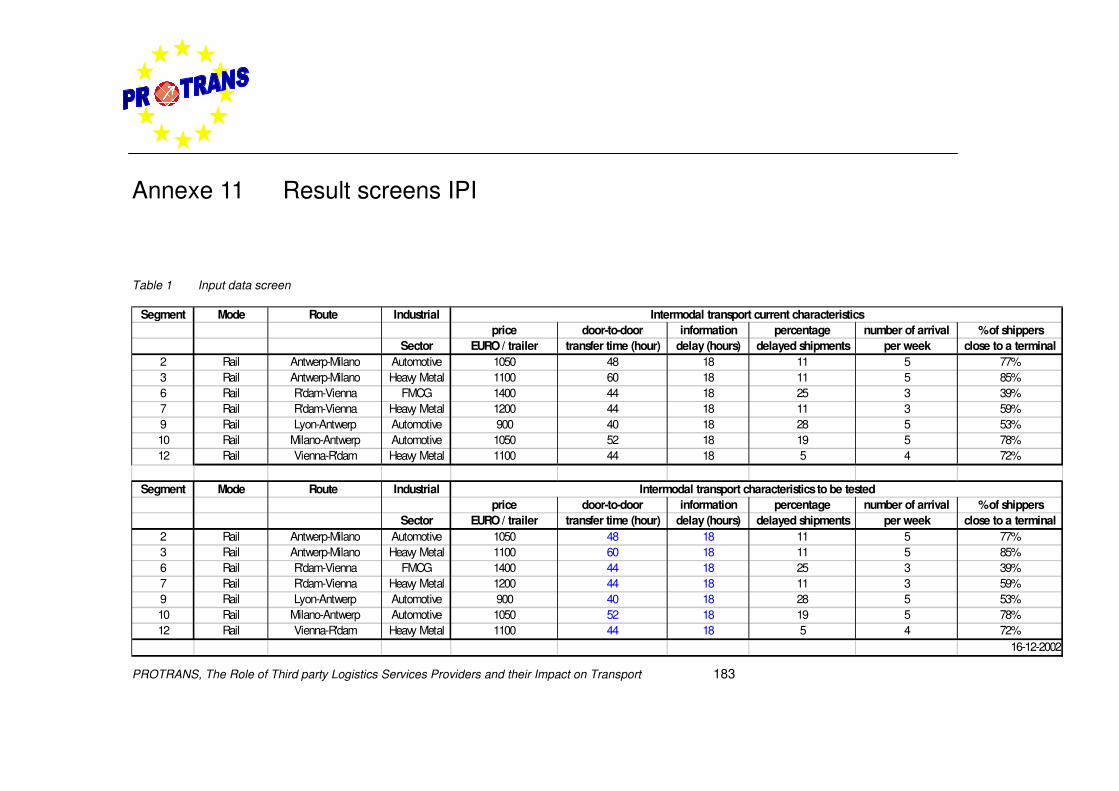

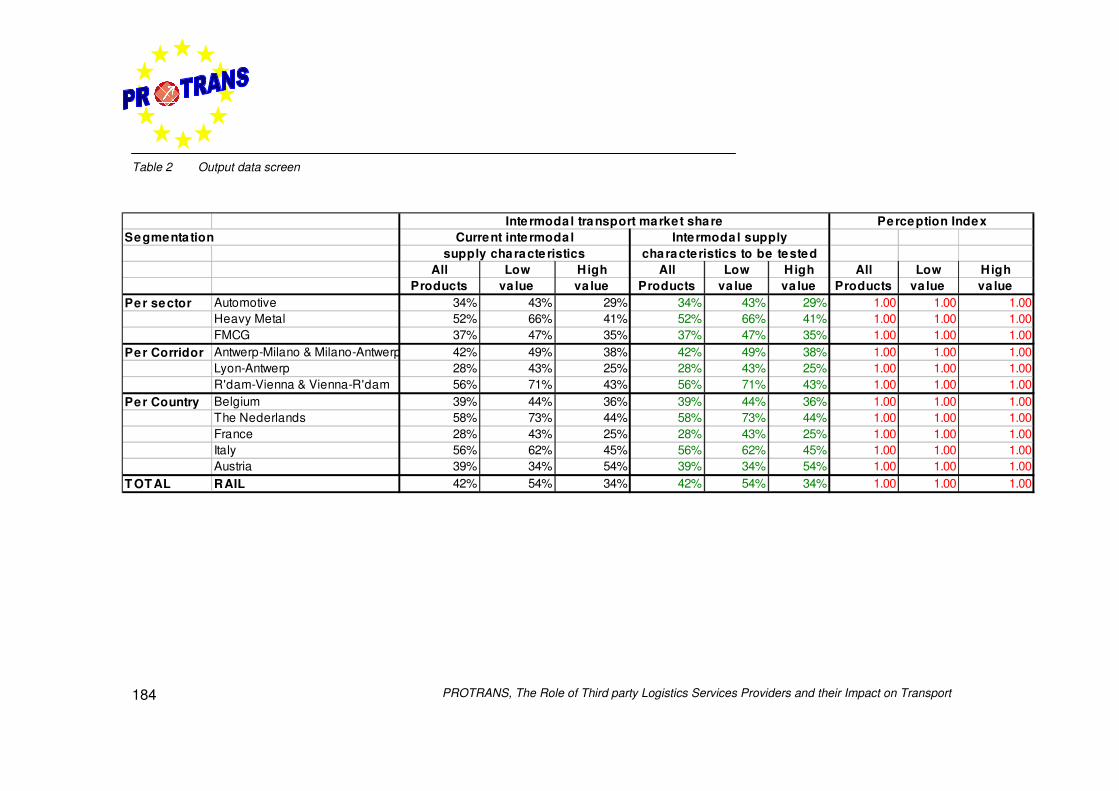

Annexe 11 Result screens IPI 183

List of figures

PageFigures of Executive Summary

Figure 1 Example input screen 2PLP facilities 4Figure 2 Four main elements of a logistics region 5Figure 3 Perceptions on current 3PLPs behaviour in the logistics system 13Figure 4 Influence of 3PLPs on leading action variables 17Figure 5 Evaluation of the first scenario regarding fast moving, high valued goods 20Figure 6 Evaluation of the second scenario regarding slow moving, low valued

goods 21

Figures of Chapters 1 to 7

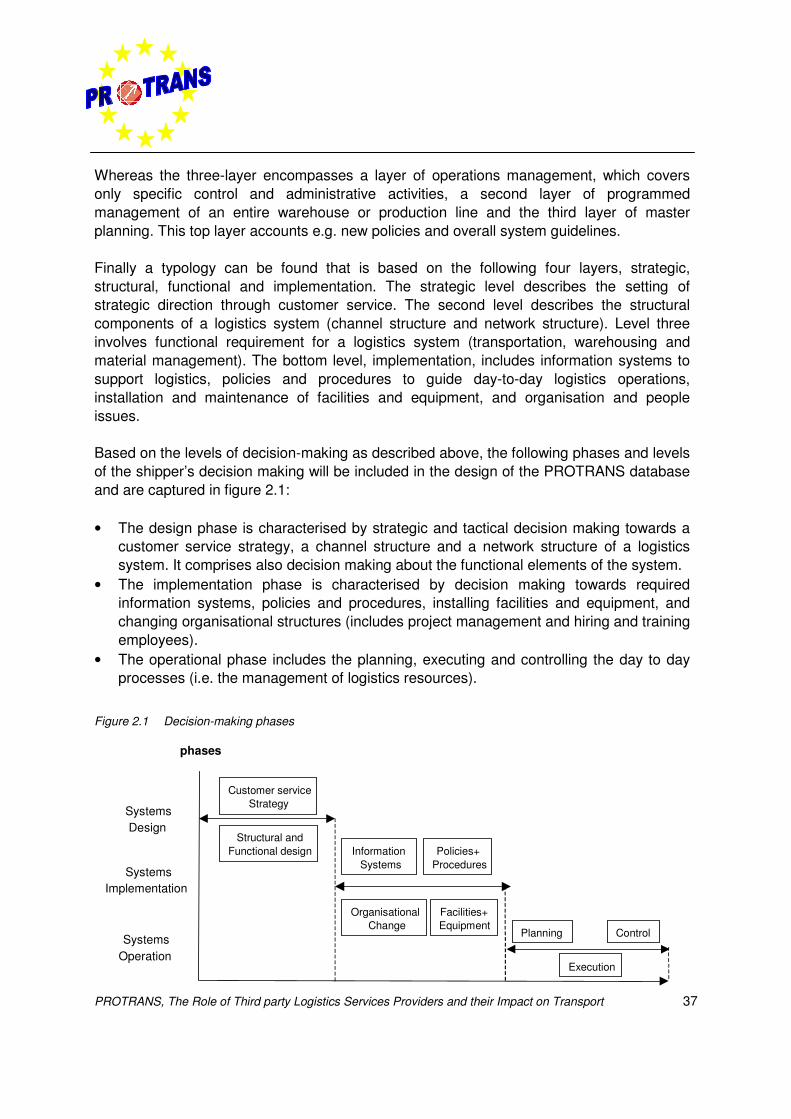

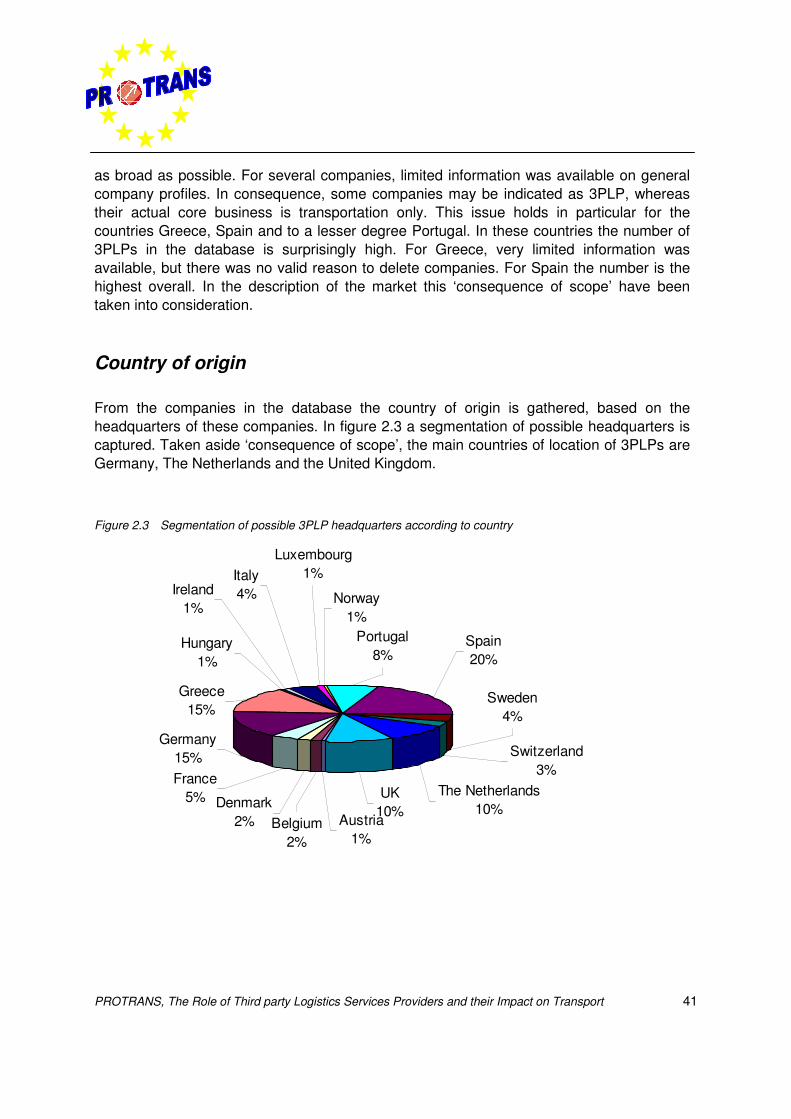

Figure 2.1 Decision-making phases 37Figure 2.2 Example input screen 3PLP facilities 40Figure 2.3 Segmentation of possible 3PLP headquarters according to country 41Figure 2.4 Segmentation of type of clients served by 3PLPs 42Figure 2.5 Segmentation of type of activities being offered by 3PLPs 43Figure 2.6 Segmentation of transport services offered by 3PLPs 43Figure 3.1 The four main elements of a logistics region 47Figure 3.2 Infrastructure 48Figure 3.3 Demand of logistics services 49Figure 3.4 Supply of logistics services 51Figure 3.5 External environment 52Figure 3.6 Profile of logistics regions 54Figure 4.1 Conceptual model 65Figure 4.2 Transport Management as part of a logistics systems 65Figure 4.3 Logistics services performed by logistics service providers 66Figure 4.4 3PLPs using IMT 68Figure 4.5 3PLPs level of involvement in different IMT related activities 69Figure 4.6 Proactive behaviour of 3PLPs per identified phase 70Figure 4.7 Proactive behaviour of 3PLPs per identified phase in IMT 71Figure 4.8 Sufficiency of critical resources 72Figure 4.9 Adequacy of skills 73Figure 4.10 3PLPs degree of experience and know-how in IMT 74

Page

Figure 4.11 The perception of the current transport effects caused by the use of3PLPs 76

Figure 4.12 Perceived factors of 3PLPs that effect current and future transportefficiency 77

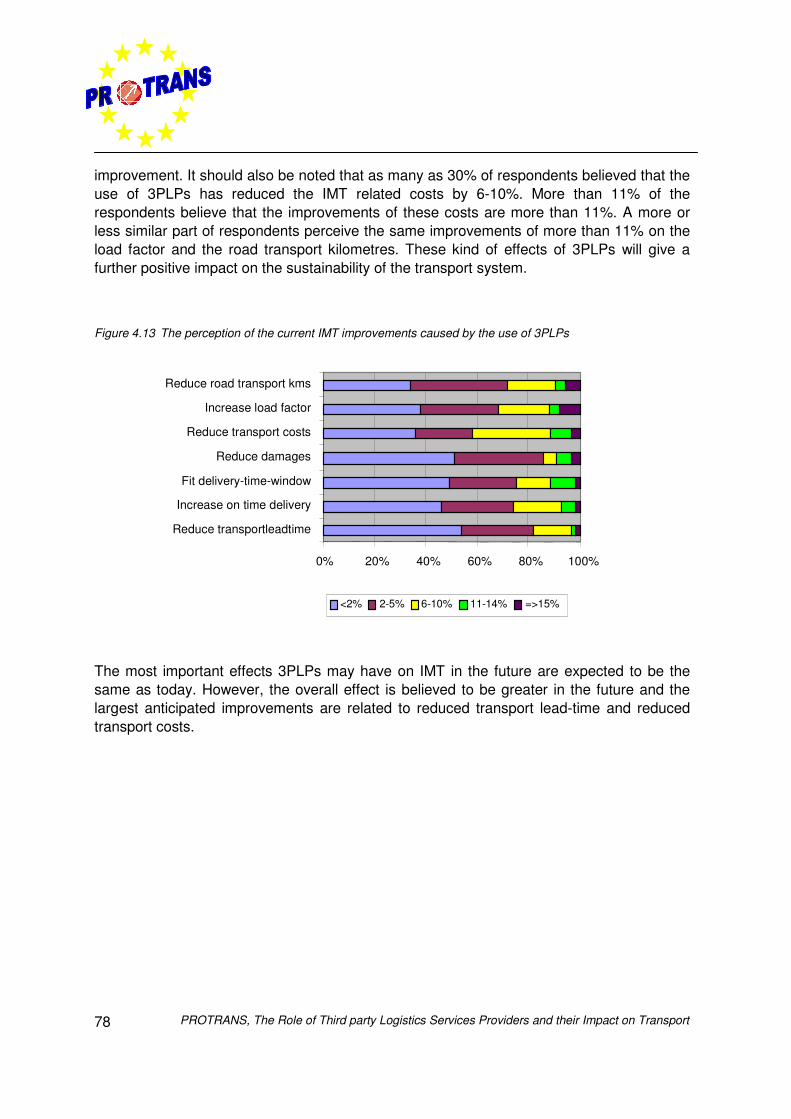

Figure 4.13 The perception of the current IMT improvements caused by the useof 3PLPs 78

Figure 5.1 Perceptions on current 3PLPs behaviour in the logistics system 83Figure 5.2 Deficiencies in critical design resources and skills - now and in future 84Figure 5.3 Deficiencies in critical implementation resources and skills - now and in

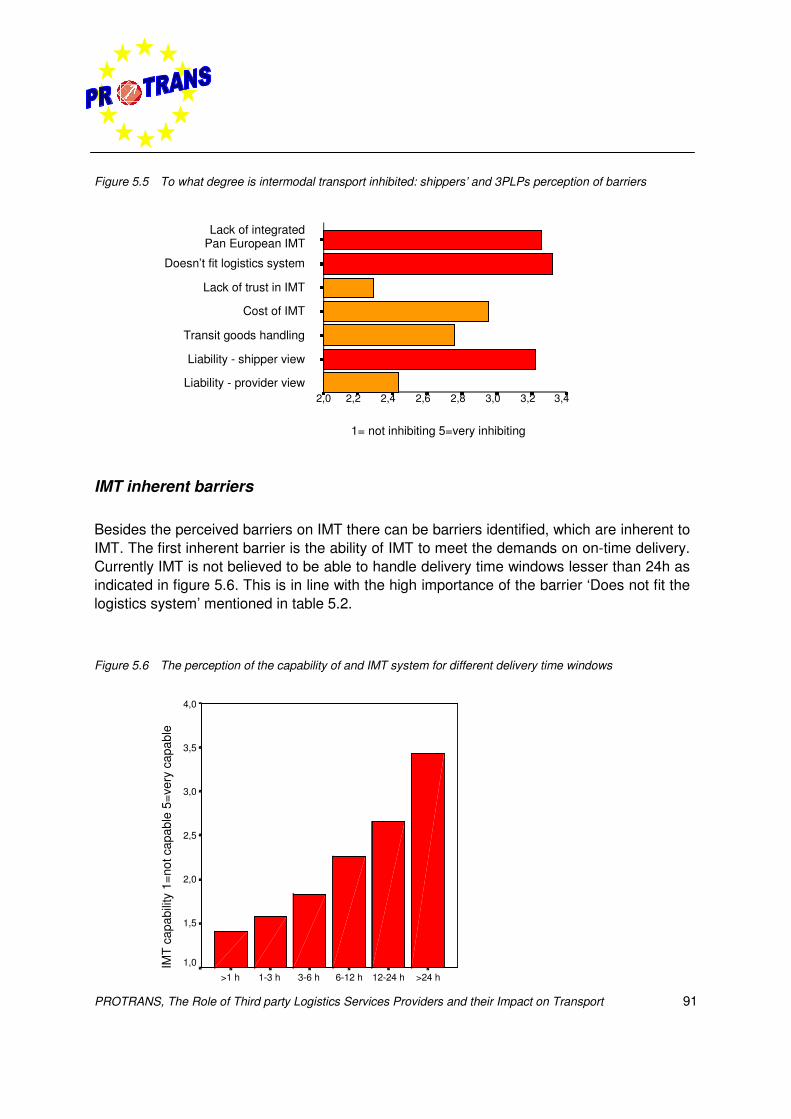

future 85Figure 5.4 Deficiencies in critical operational resources and skills - now and in future 86Figure 5.5 To what degree is intermodal transport inhibited: shippers’ and 3PLPs

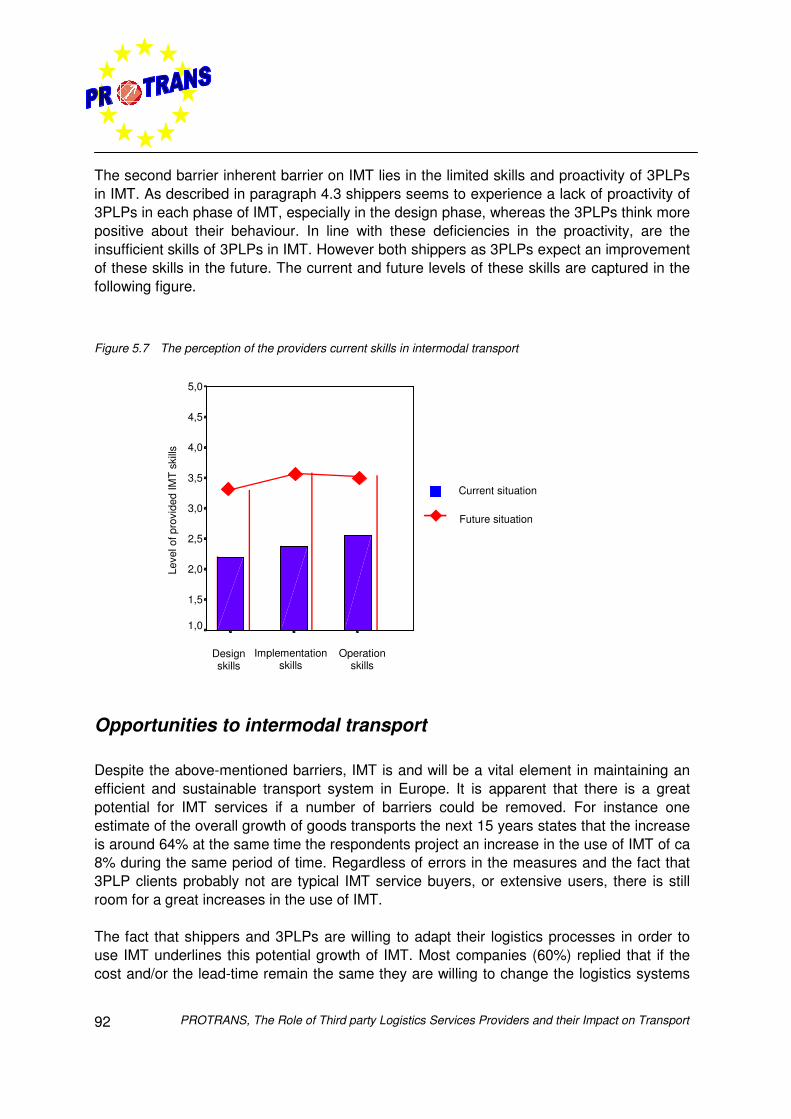

perception of barriers 91Figure 5.6 The perception of the capability of and IMT system for different delivery

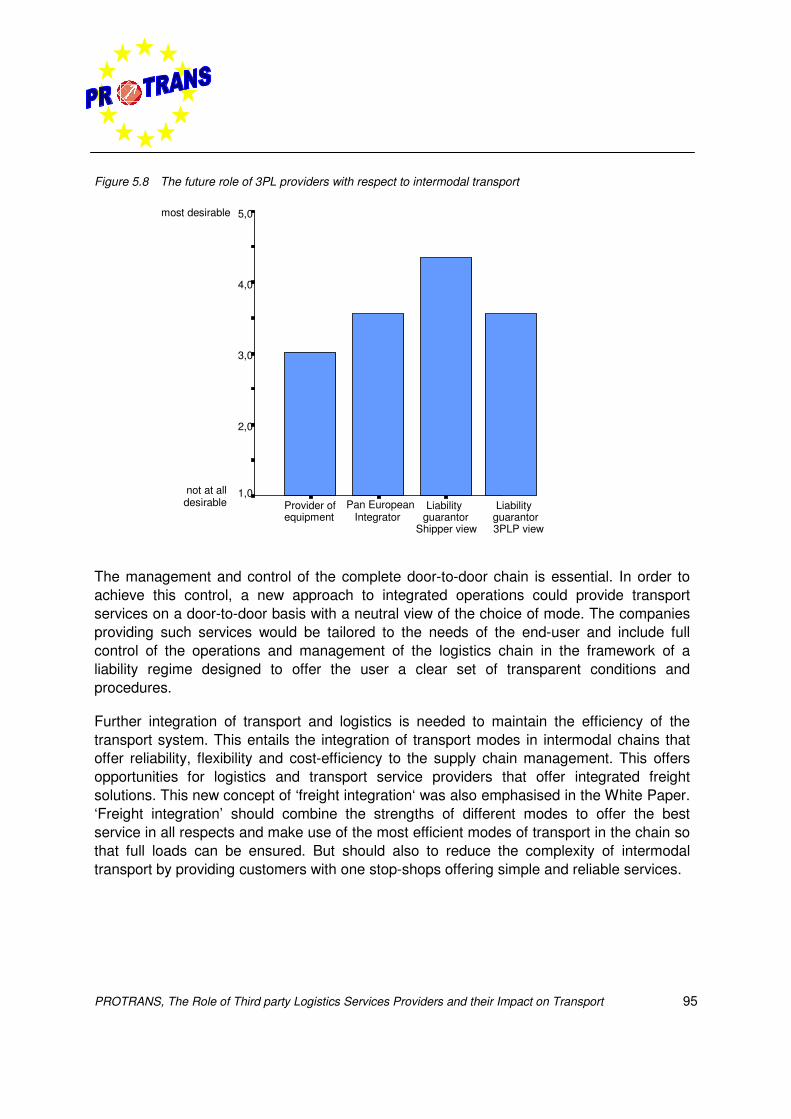

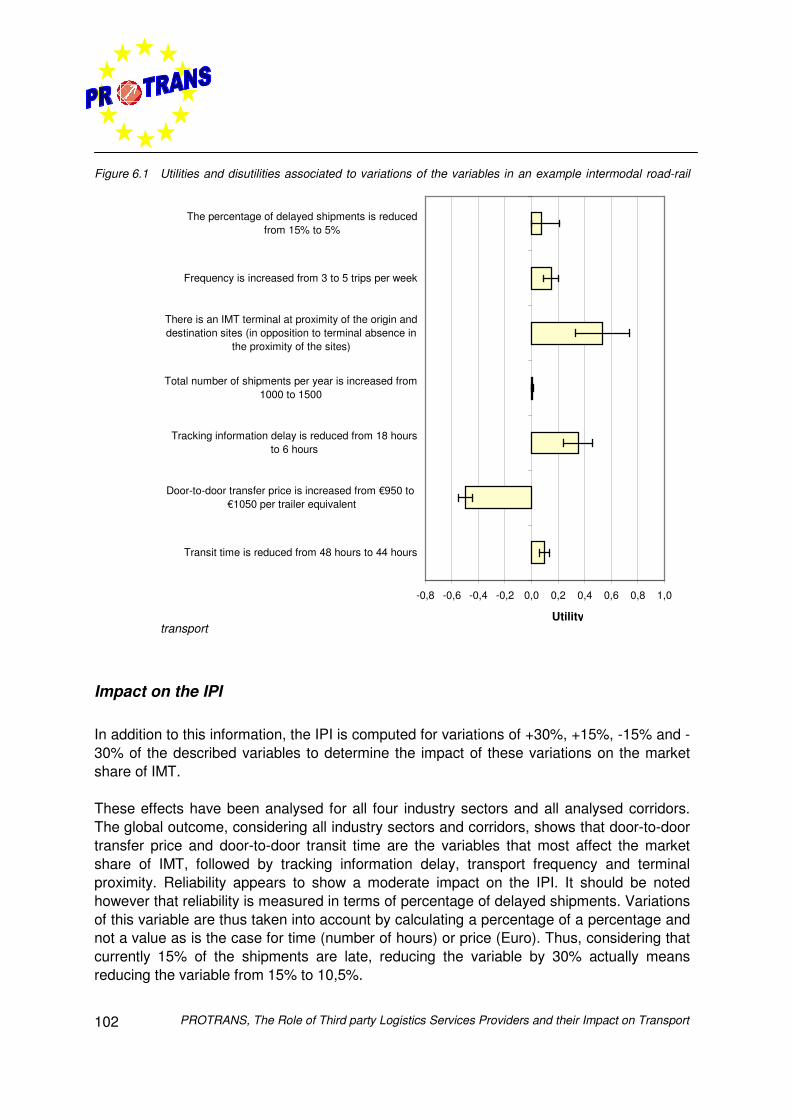

time windows 91Figure 5.7 The perception of the providers current skills in intermodal transport 92Figure 5.8 The future role of 3PL providers with respect to intermodal transport 95Figure 6.1 Utilities and disutilities associated to variations of the variables in an

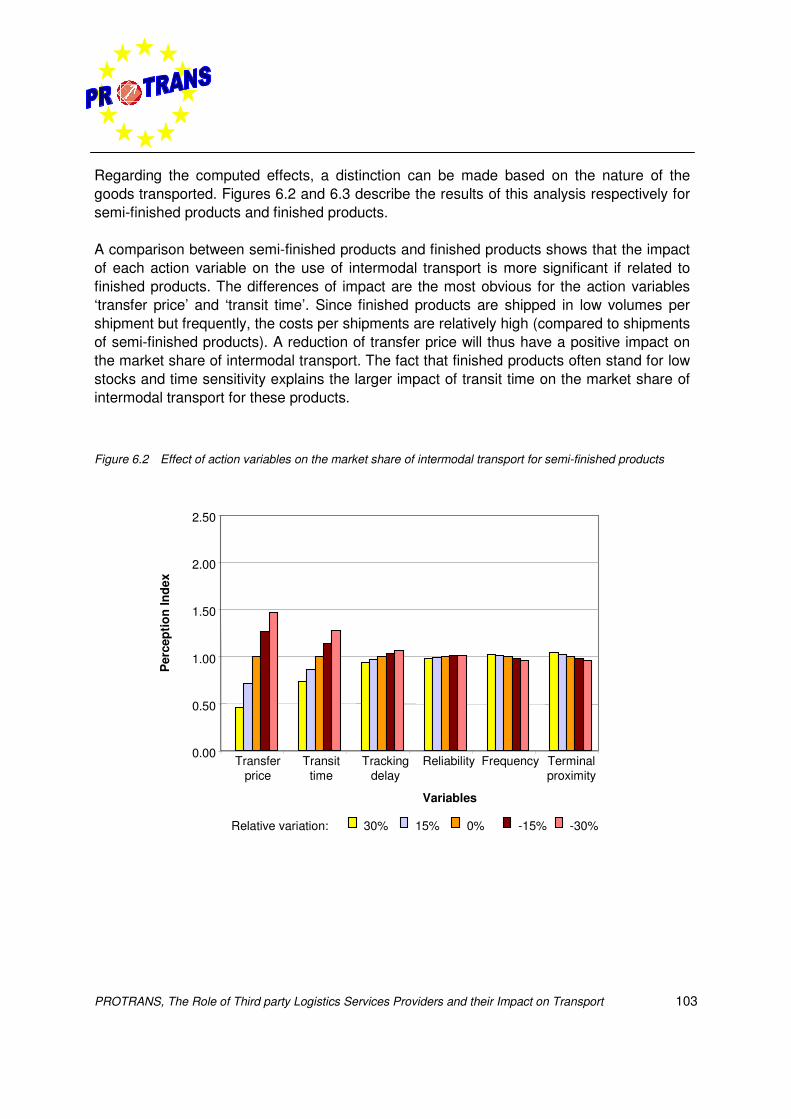

example intermodal road-rail transport 102Figure 6.2 Effect of action variables on the market share of intermodal transport for

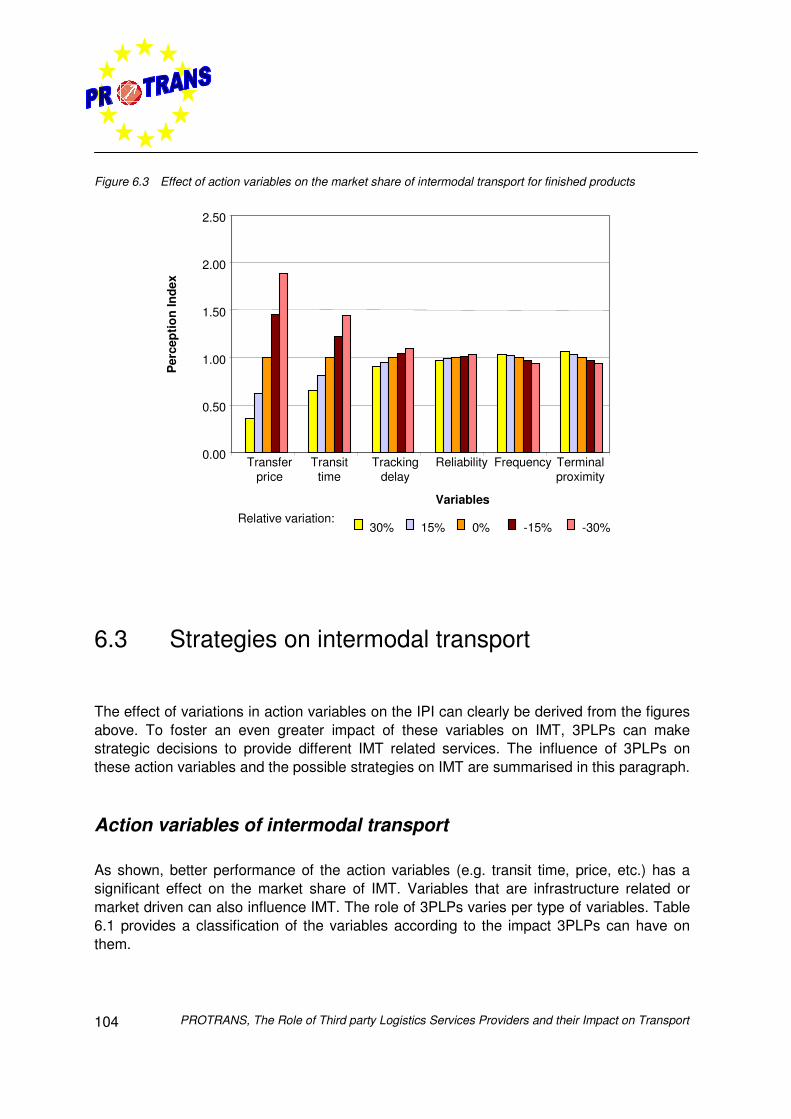

semi-finished products 103Figure 6.3 Effect of action variables on the market share of intermodal transport for

finished products 104Figure 6.4 Influence of 3PLPs on leading action variables 107Figure 6.5 Evaluation of the first scenario regarding fast moving, high valued goods 113Figure 6.6 Evaluation of the second scenario regarding slow moving, low valued

goods 114

Figures of Annexes

Figure 1 Structure Work Package 2 - Analysis of selected logistics regions inEurope 149

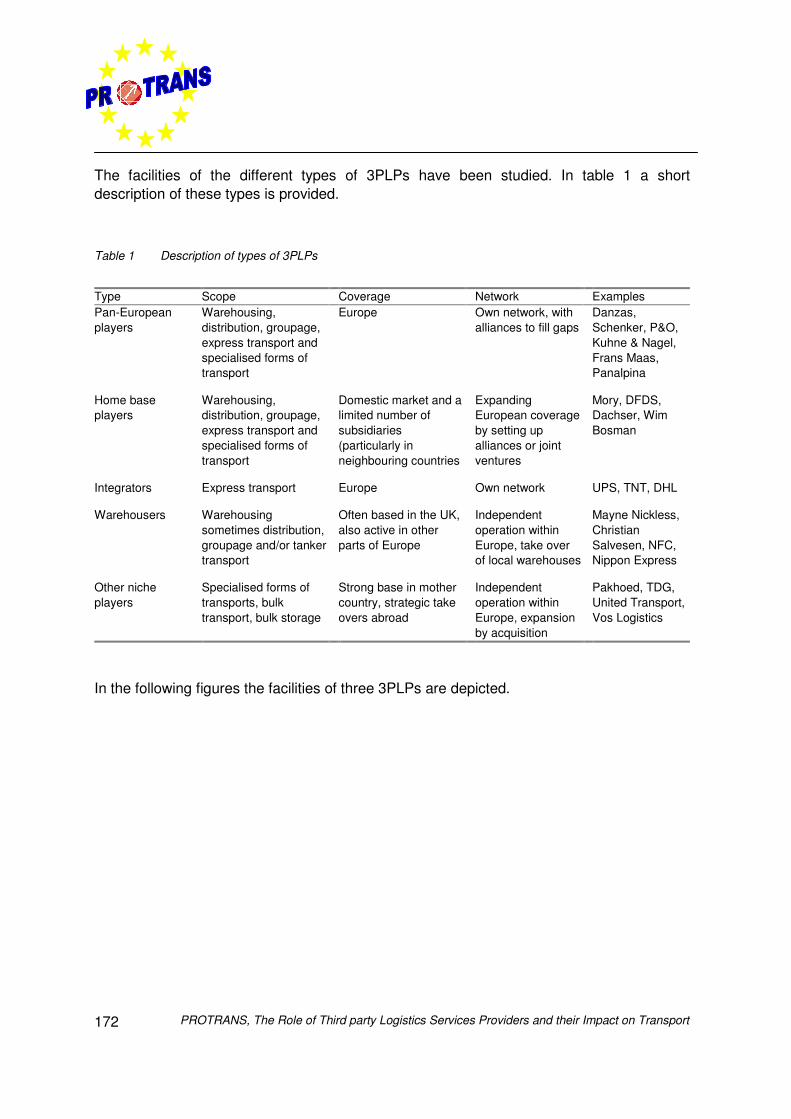

Figure 2 Framework of Work Package 4 152Figure 1 Network of Frans Maas 173Figure 2 Network of Exel 174Figure 3 Network of TNT 175Figure 1 Required notification of delayed shipments according to shippers 181

List of tablesPage

Tables of Executive Summary

Table 1 Scores of studied logistics regions 6Table 2 Classification of the sample regions studied according to the typology 7Table 3 Focus of logistics regions 9Table 4 Changes in logistics performance due to 3PLP influence 11Table 5 Impact of National and European laws on the use of intermodal transport 15Table 6 Required 3PLPs services on action variables 16Table 7 Importance of the leading action variables per industry 19Table 8 Estimated efficiency effects per action variable 20

Tables of Chapters 1 to 7

Table 1.1 Activities per Work Package 27Table 2.1 Examples of relationships between 3PLPs 44Table 3.1 Short list selected regions 46Table 3.2 Scores of the 13 logistics regions studied 53Table 3.3 Classification of the regions studied in the proposed typology 55Table 3.4 Focus of logistics regions 57Table 4.1 Respondents per industry 61Table 4.2 Positive changes in logistics performance since 3 years 75Table 4.3 Changes in logistics performance due to 3PLP influence 76Table 5.1 Economic growth and logistics outsourcing 88Table 5.2 Perceived barriers to use IMT 90Table 5.3 Regulatory measures to foster intermodal transport 96Table 5.4 Impact of National and European laws on the use of intermodal transport 96Table 6.1 Action variables on intermodal transport 105Table 6.2 Required 3PLPs services on action variables 106Table 6.3 Logistics characteristics per industry 108Table 6.4 Intermodal transport related strategies and their impact on the action

variables 110Table 6.5 Importance of the leading action variables per industry 111Table 6.6 Estimated efficiency effects per action variable 112Table 7.1 Recommended measures according to their scope 110

PageTables of Annexes

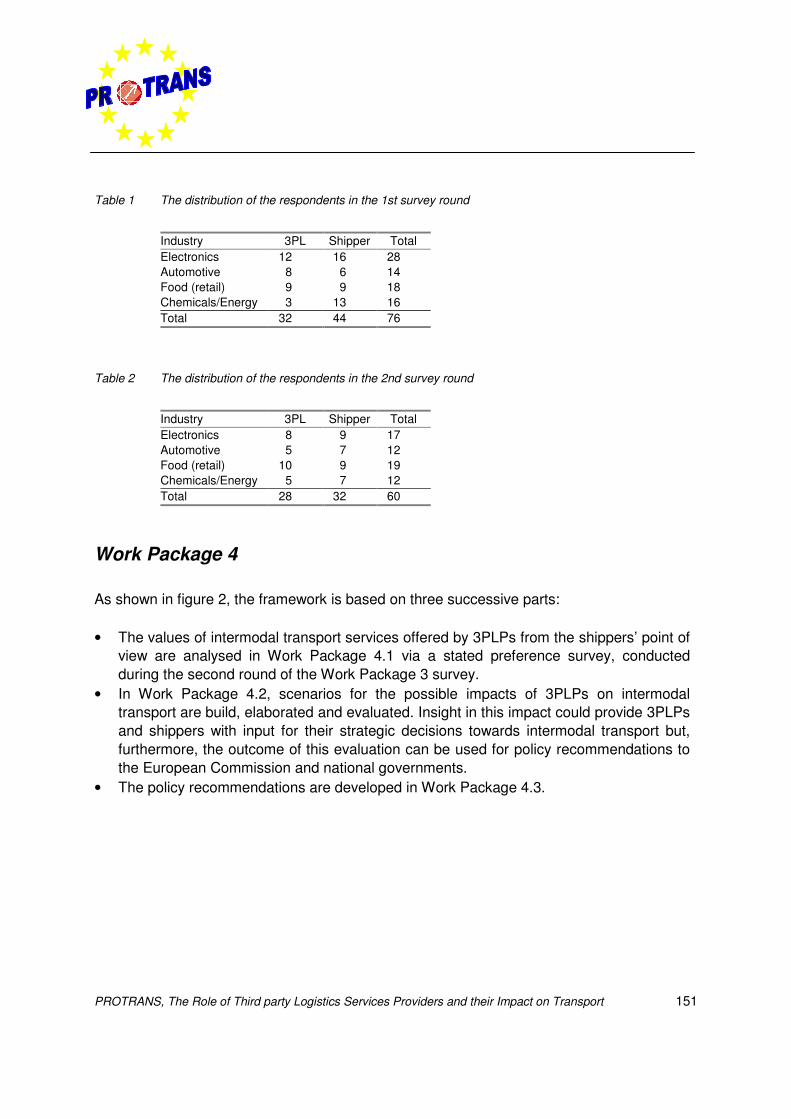

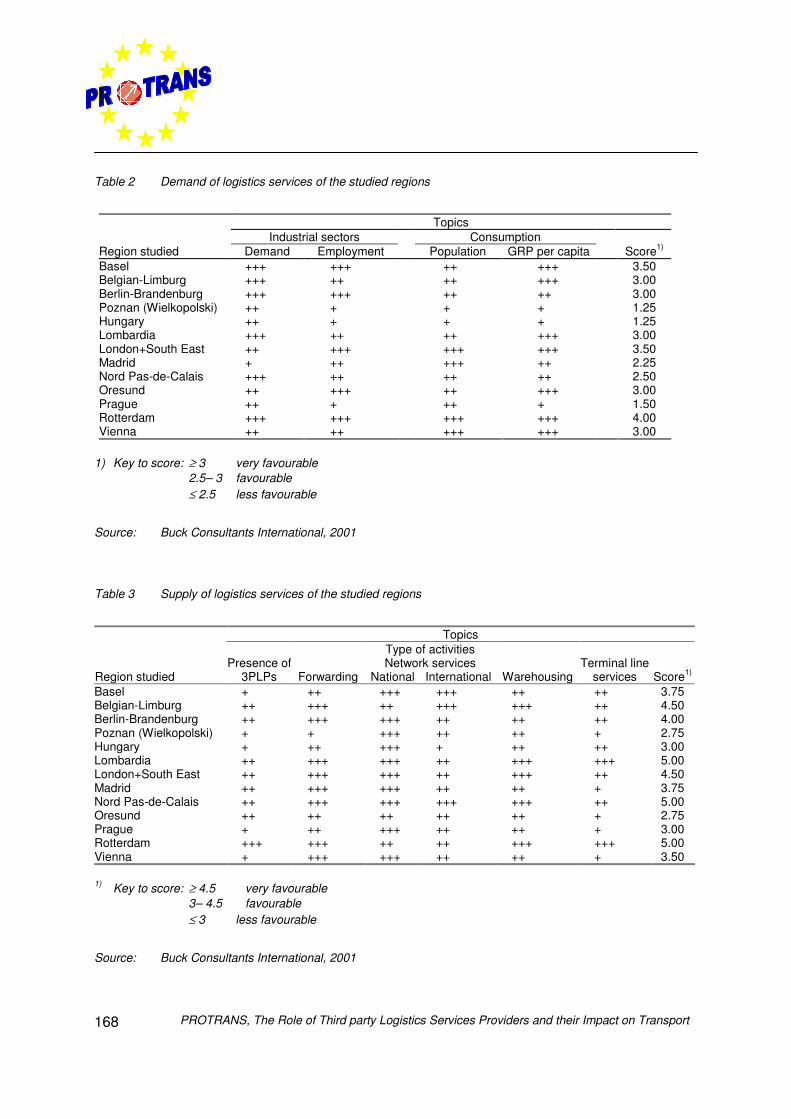

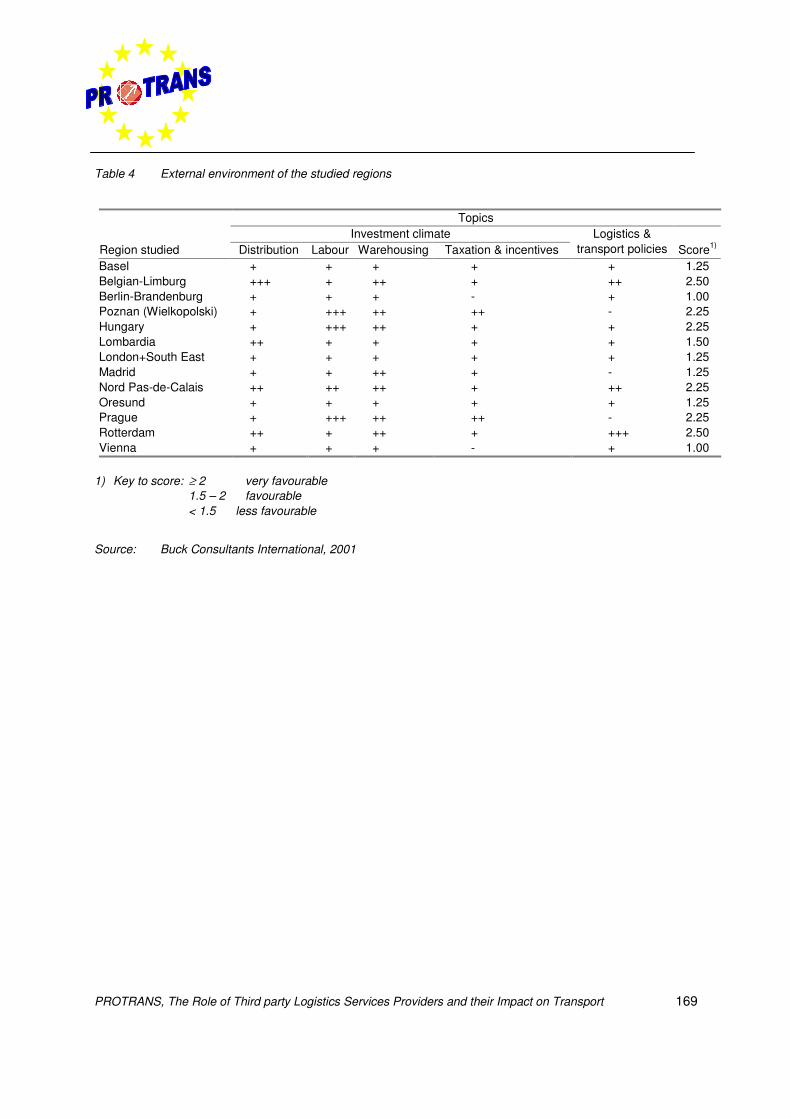

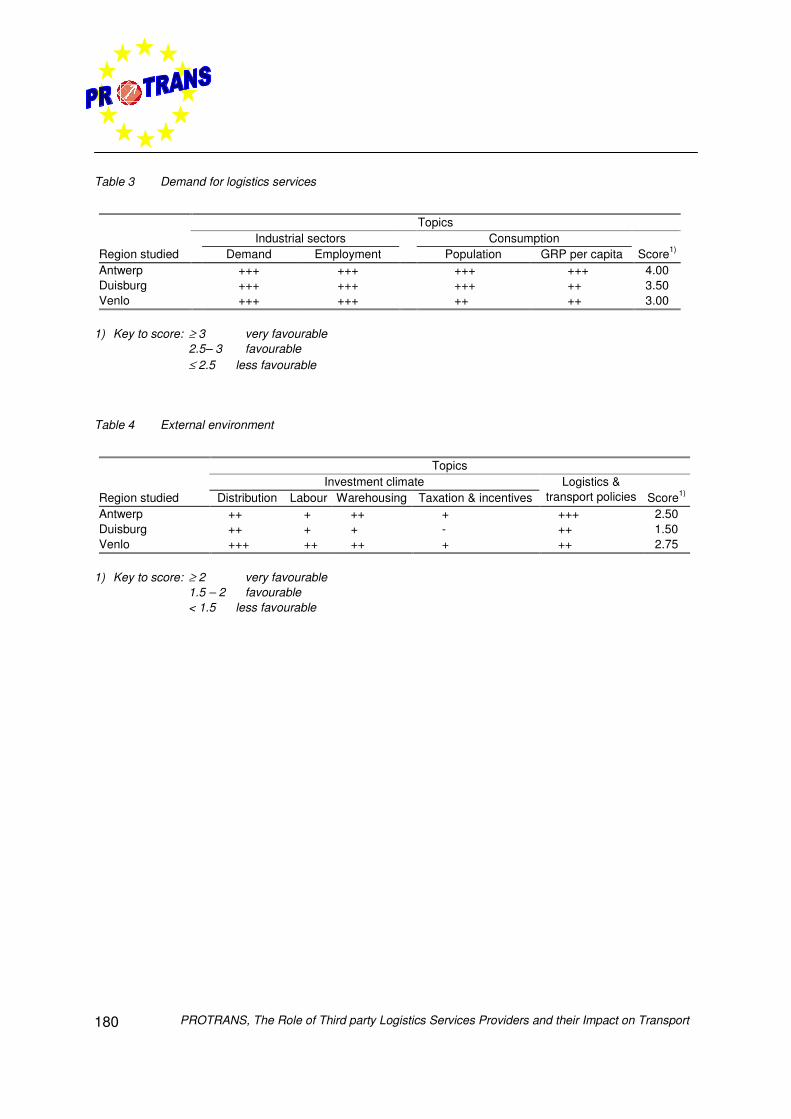

Table 1 The distribution of the respondents in the 1st survey round 151Table 2 The distribution of the respondents in the 2nd survey round 151Table 1 Infrastructure of the studied regions 167Table 2 Demand of logistics services of the studied regions 168Table 3 Supply of logistics services of the studied regions 168Table 4 External environment of the studied regions 169Table 1 Description of types of 3PLPs 172Table 1 Infrastructure 179Table 2 Supply of logistics services 179Table 3 Demand for logistics services 180Table 4 External environment 180Table 1 Input data screen 183Table 2 Output data screen 184

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 1

Executive Summary

1 Introduction

The international competitiveness of European industry will increasingly depend on itsability to deliver customer-adapted products all over the world quickly and in time. Such acompetitive image places a number of demands on the logistics system and management'sattitude to how important logistics is as a competitive parameter. In the 1990s, focus haschanged from internal efficiency in the logistics function to external relations between theparties in the total supply chain. The largest potential for improvements is not found insidean individual company, but in the interfaces between independent companies in the supplychain. Outsourcing logistics activities has become a relative common principle forcompanies. Since Third Party Logistics Providers (3PLPs) provide this service for multipleclients, 3PLPs play a significant and increasing role in overall optimised logistics networks.

In order to gain insight in the role of 3PLPs in transport a consortium of 11 companies(consulting firms, research organisations and universities) designed the PROTRANSproject. The companies that participate in the PROTRANS project are:

• Buck Consultants International (BCI, NL)• Cranfield University (CU, UK)• Zentrum für Logistik und Unternehmungsplanung GmbH (ZLU, D)• Fraunhofer Institut Materialfluss und Logistik (IML, D)• Ecorys Transport (NEI, NL)• Stratec S.A. (B)• PTV Planung Transport Verkehr A.G. (PTV, D)• Linköping Universitet (LiU, SE)• Technische Universität Berlin (TU-B, D)• Environment, Transport & Planning (CH2Mhill/ET&P, ES)• Louis Berger S.A. (LB, F)

The project is co-ordinated by Buck Consultants International.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport2

This project, which is conducted within the Vth Framework Programme of the, EuropeanCommission, started in January 2000 and has been finalised in December 2002. The maingoal of the PROTRANS project is to identify the most important challenges (for whom/what),to determine barriers, success and failure factors and to assess the future importance ofintermodal transport forthis the strategies of 3PLPs on a European level. In the PROTRANSproject Third-party Logistics has been defined as:

”…activities carried out by an external company on behalf of a shipper and consisting of atleast the provision of management of multiple logistics services. These activities are offeredin an integrated way, not on a stand- alone basis. The co-operation between the shipperand the external company is an intended continuous relationship”.

In order to achieve this main goal, the work of the project has been divided into 5 tasks(Work Packages):

Work Package 1 Analysis of the 3PL marketWork Package 2 Analysis of European logistics regionsWork Package 3 Market demands and services offered by 3PLPsWork Package 4 Intermodality as an integral part of pan European strategiesWork Package 5 Conclusions, recommendations and dissemination

The results of these tasks are summarised in this executive summary of this Deliverable(No. 6), which summarises the total results of the PROTRANS project.

2 Third-party logistics market overview

The 3PLP market is a very dynamic one. Mergers, acquisitions and alliances are commonnews in this industry. Customer demands changes frequent, distribution channels emergeand new products are introduced on a daily basis. All these market developments requireadaptation of supply chains and a different role of 3PLPs in transport and logistics. In orderto gain insight in this role of 3PLPs, a ‘snapshot’ of the 3PLP market is taken in thePROTRANS project.

This snapshot is actually the stepping stone for further research within the PROTRANSproject, by providing a sound theoretical basis on the characteristics of a 3PLP and byproviding an extensive overview of possible 3PLP providers all over Europe. Thesecharacteristics consists of the following nine elements:• Origination (what was the original scope and activity of the 3PLP company).

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 3

• The type of clients that are served (which industrial sectors).• (Part of) the supply chain that is covered (upstream or downstream).• The network structure that is covered (location of clients and facilities).• The type of activities that are carried out for the client (types of services).• The level of decision making (strategic/structural/functional/implementation).• Transport means served (segmentation along transport means and service provided,

with a special focus on intermodal transport).• Size of the 3PLP (in turnover, number of employees, number of locations, etc.).• Region (segmentation along the regions of interest as specified in the second Work

Package, on European logistics regions).• Degree of interrelationship between 3PLPs (level of participation in logistic networks,

alliances).

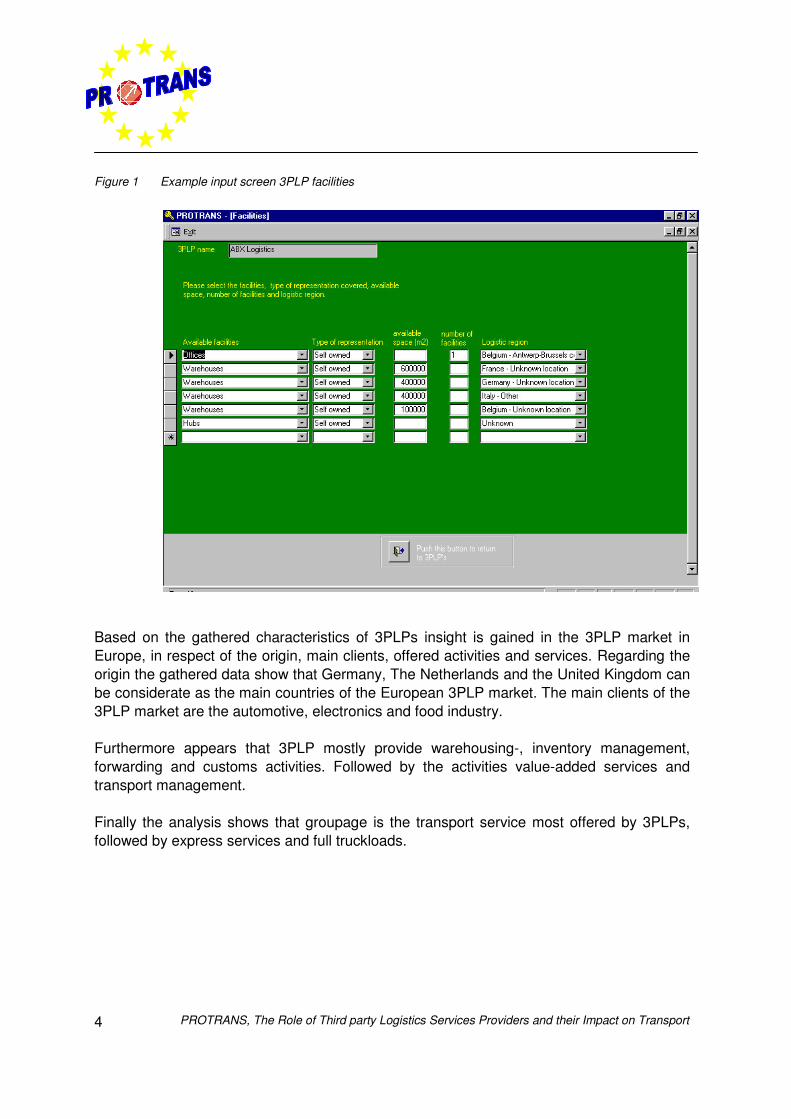

Based on these elements a database is designed in the PROTRANS project. The user-friendly database has been written in MS–Access and contains the structure for informationon 3PLPs, programmed in such a way that the information can be easily fed into thedatabase. The information filled in per 3PLP record is structured in five main input screens:

• Overview of parent companies• 3PLP general information• 3PLP facilities• 3PLP transport means• 3PLP client information

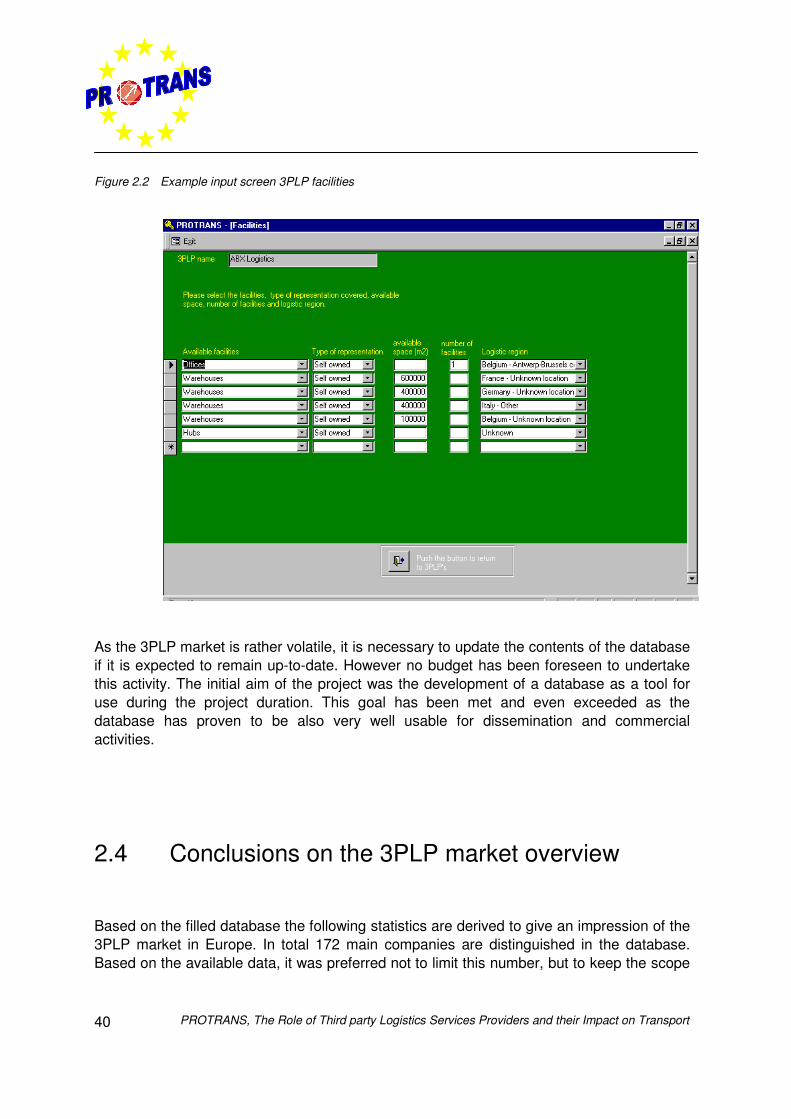

In figure 1 an example of the input screen of the 3PLP facilities is captured.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport4

Figure 1 Example input screen 3PLP facilities

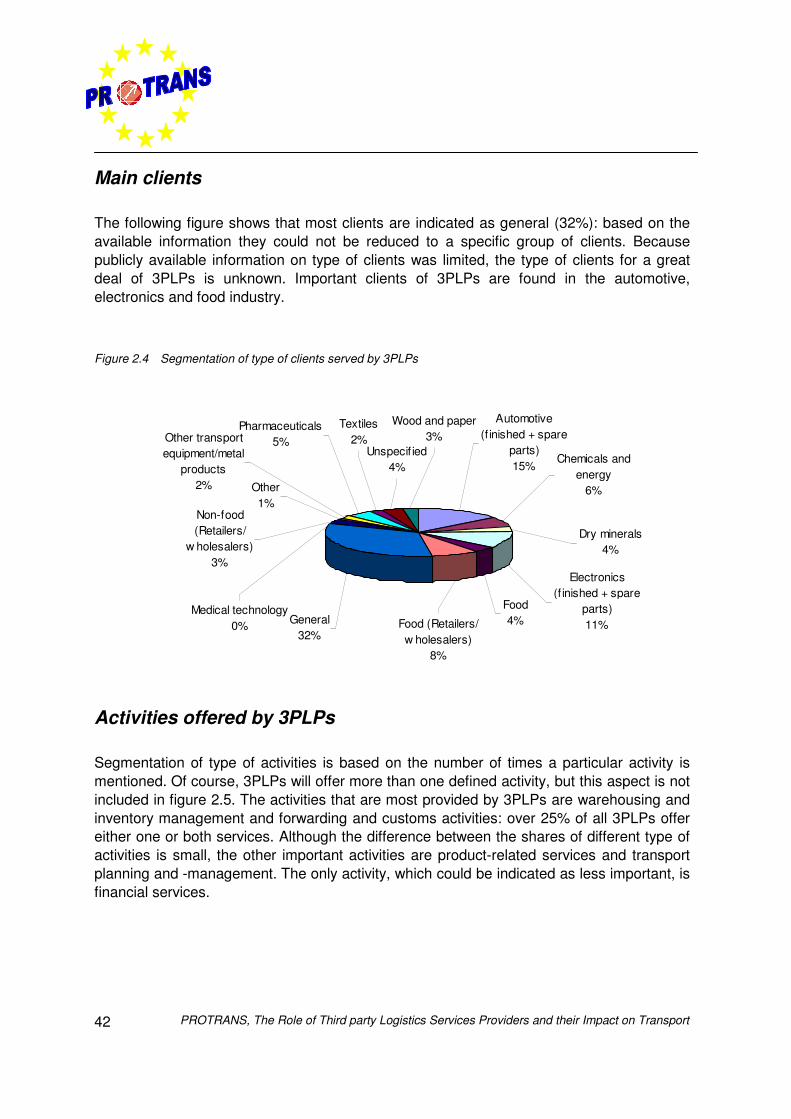

Based on the gathered characteristics of 3PLPs insight is gained in the 3PLP market inEurope, in respect of the origin, main clients, offered activities and services. Regarding theorigin the gathered data show that Germany, The Netherlands and the United Kingdom canbe considerate as the main countries of the European 3PLP market. The main clients of the3PLP market are the automotive, electronics and food industry.

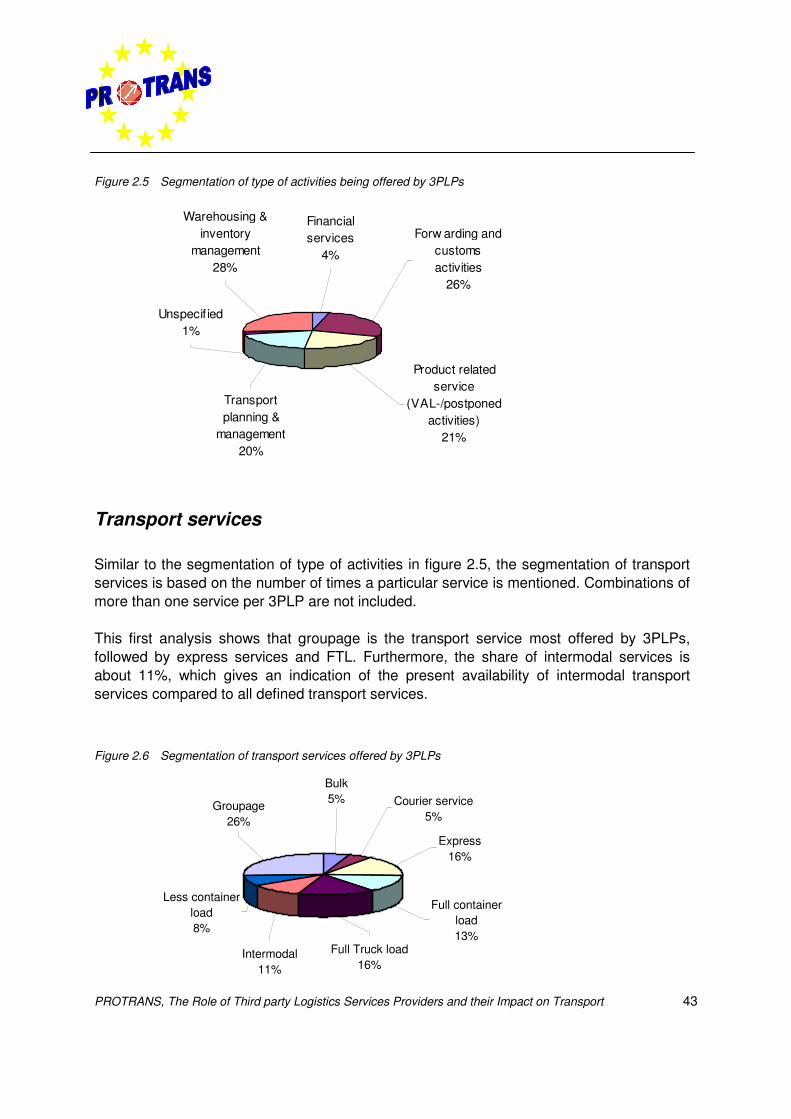

Furthermore appears that 3PLP mostly provide warehousing-, inventory management,forwarding and customs activities. Followed by the activities value-added services andtransport management.

Finally the analysis shows that groupage is the transport service most offered by 3PLPs,followed by express services and full truckloads.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 5

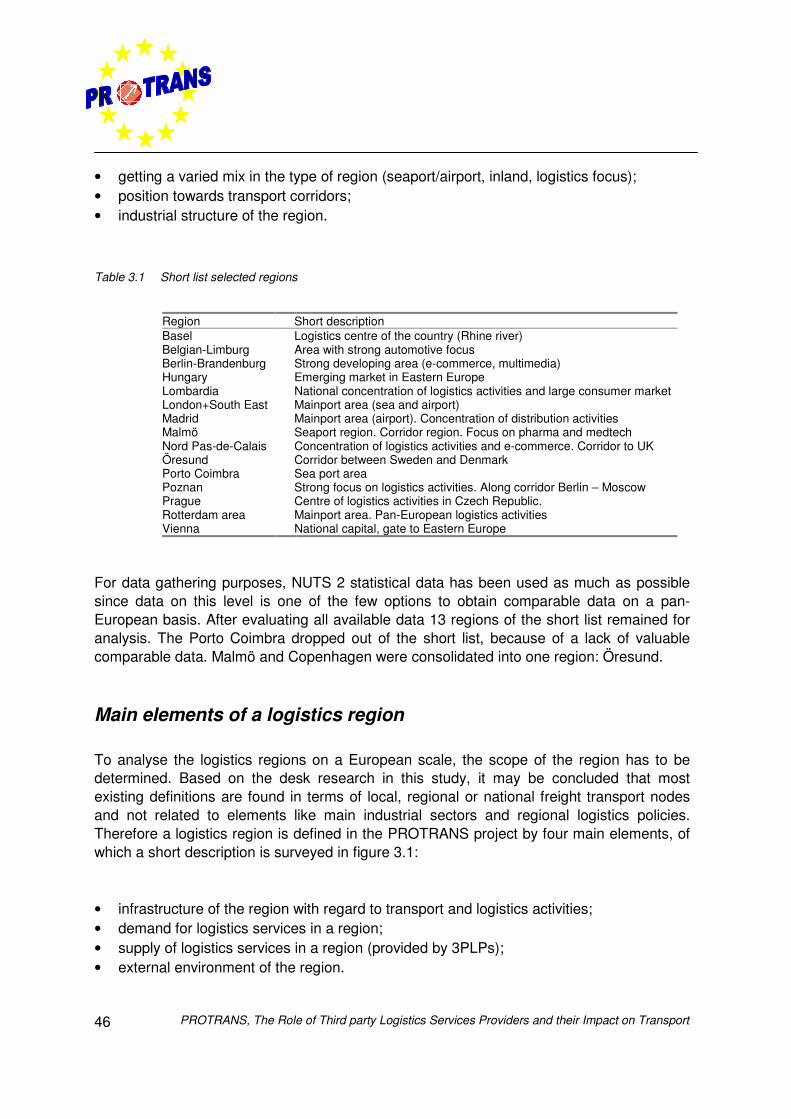

3 Regional perspective of third-party logistics

Profile of a logistics region

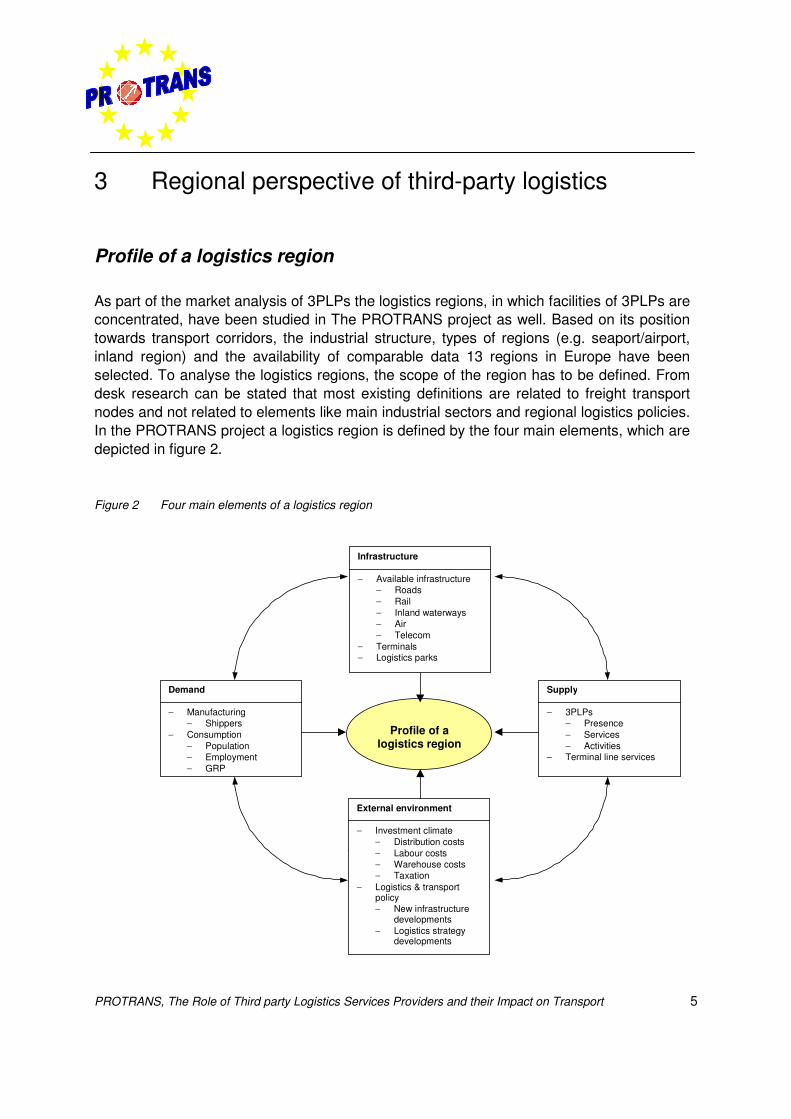

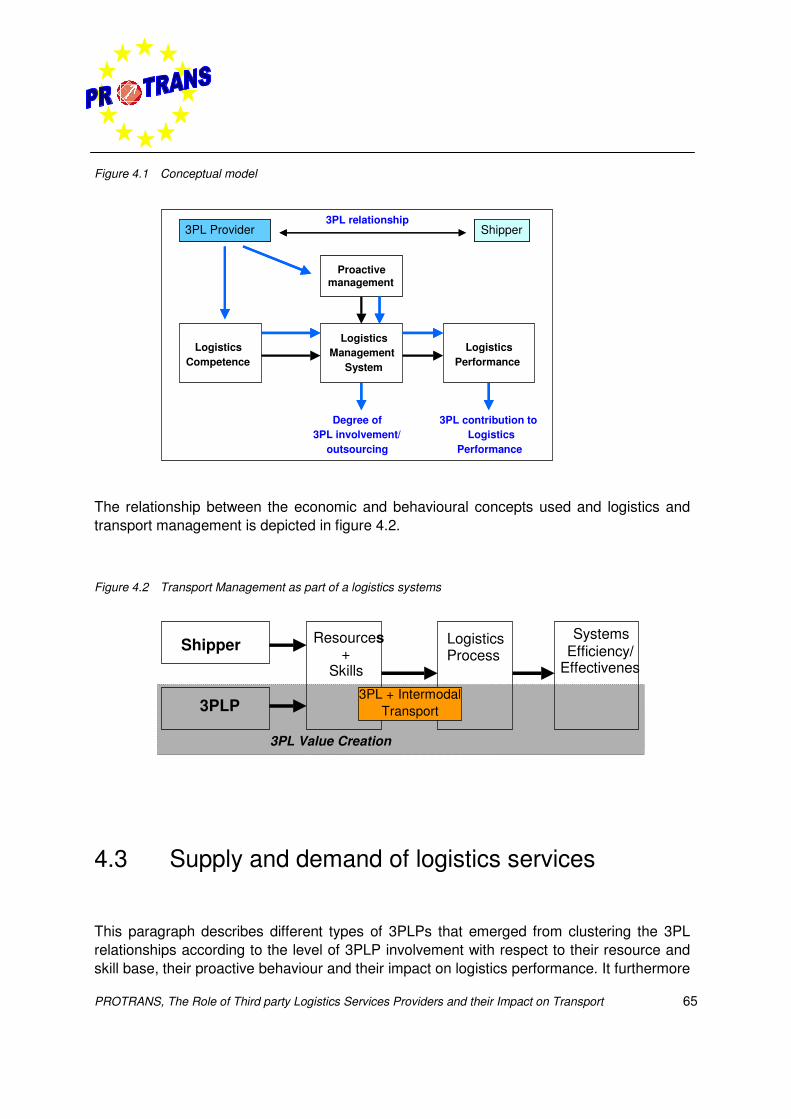

As part of the market analysis of 3PLPs the logistics regions, in which facilities of 3PLPs areconcentrated, have been studied in The PROTRANS project as well. Based on its positiontowards transport corridors, the industrial structure, types of regions (e.g. seaport/airport,inland region) and the availability of comparable data 13 regions in Europe have beenselected. To analyse the logistics regions, the scope of the region has to be defined. Fromdesk research can be stated that most existing definitions are related to freight transportnodes and not related to elements like main industrial sectors and regional logistics policies.In the PROTRANS project a logistics region is defined by the four main elements, which aredepicted in figure 2.

Figure 2 Four main elements of a logistics region

Demand

− Manufacturing− Shippers

− Consumption− Population− Employment− GRP

Supply

− 3PLPs− Presence− Services− Activities

− Terminal line services

Profile of alogistics region

Infrastructure

− Available infrastructure− Roads− Rail− Inland waterways− Air− Telecom

− Terminals− Logistics parks

External environment

− Investment climate− Distribution costs− Labour costs− Warehouse costs− Taxation

− Logistics & transportpolicy− New infrastructure

developments− Logistics strategy

developments

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport6

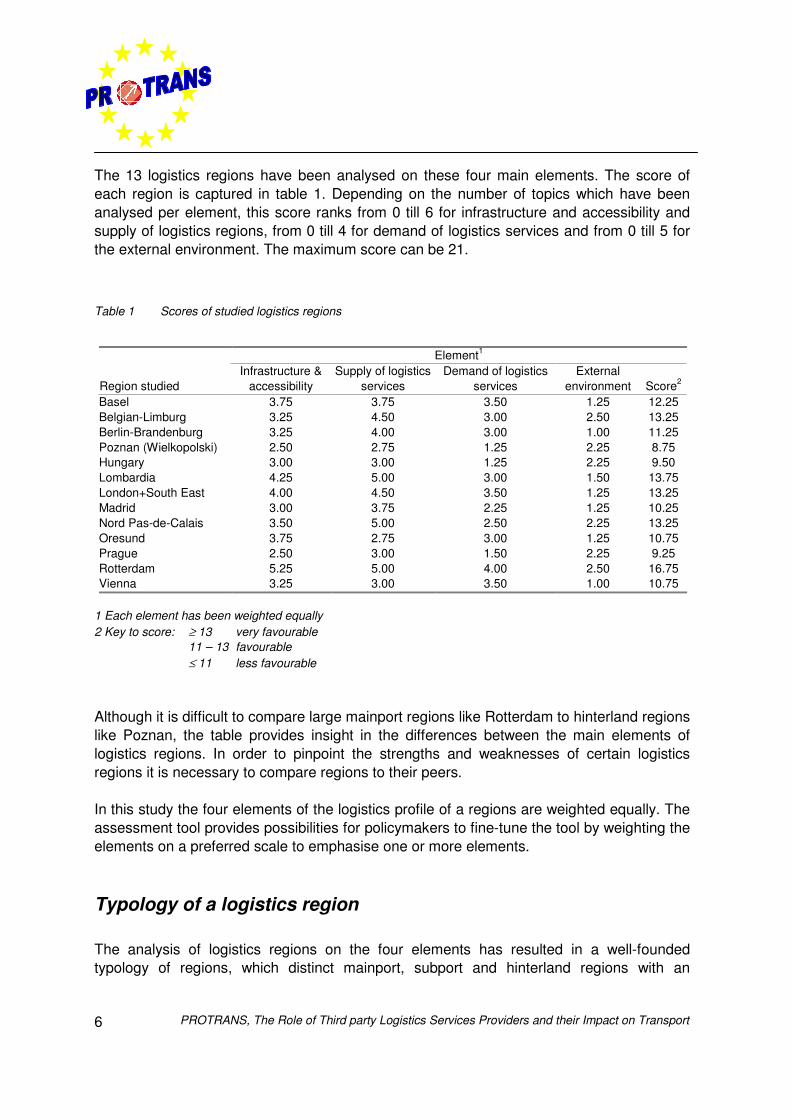

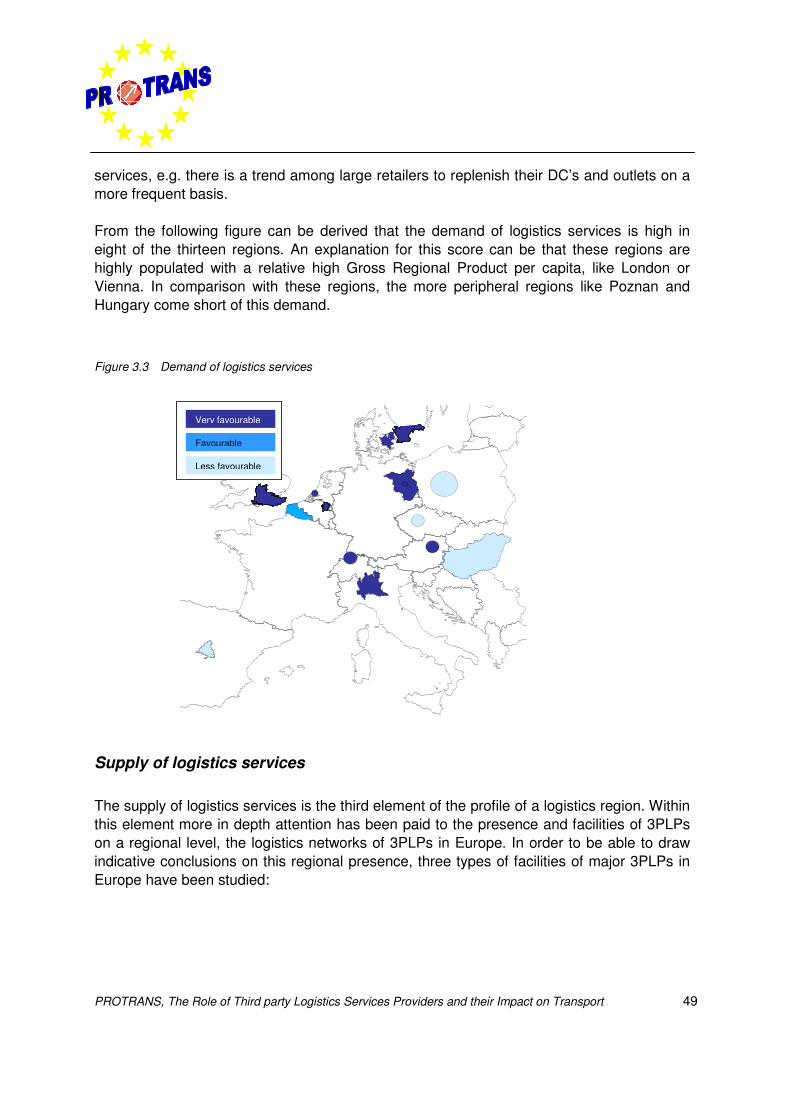

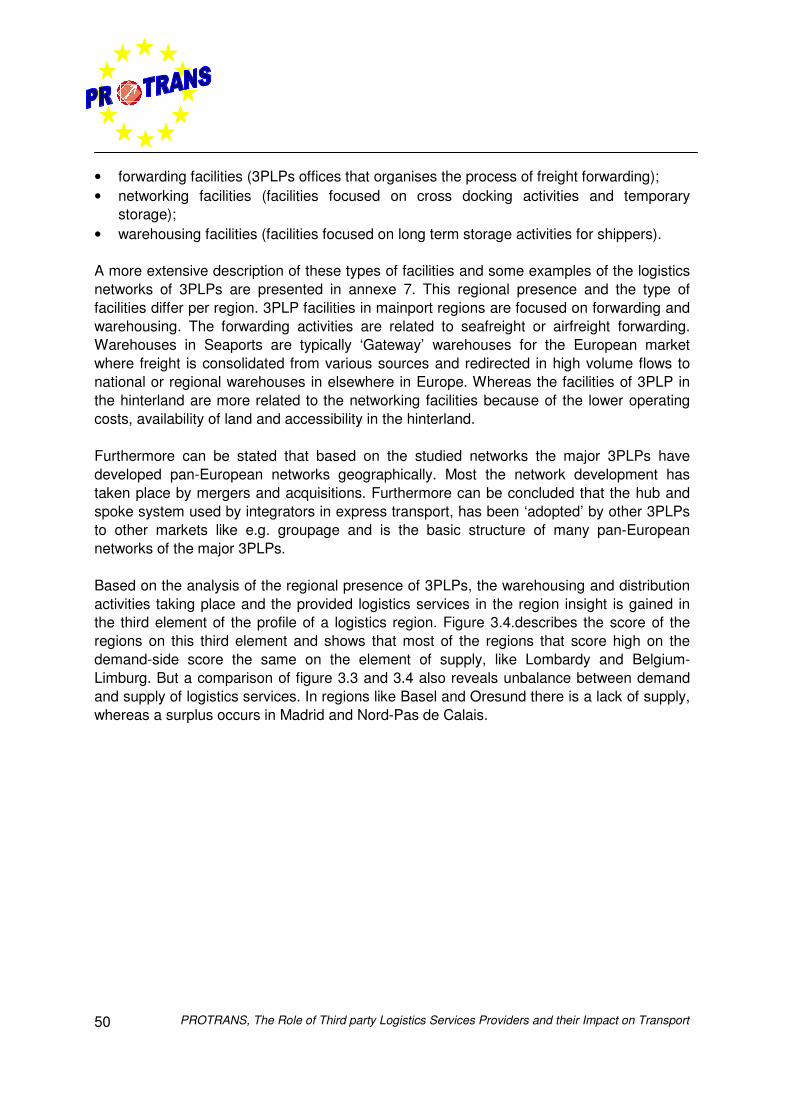

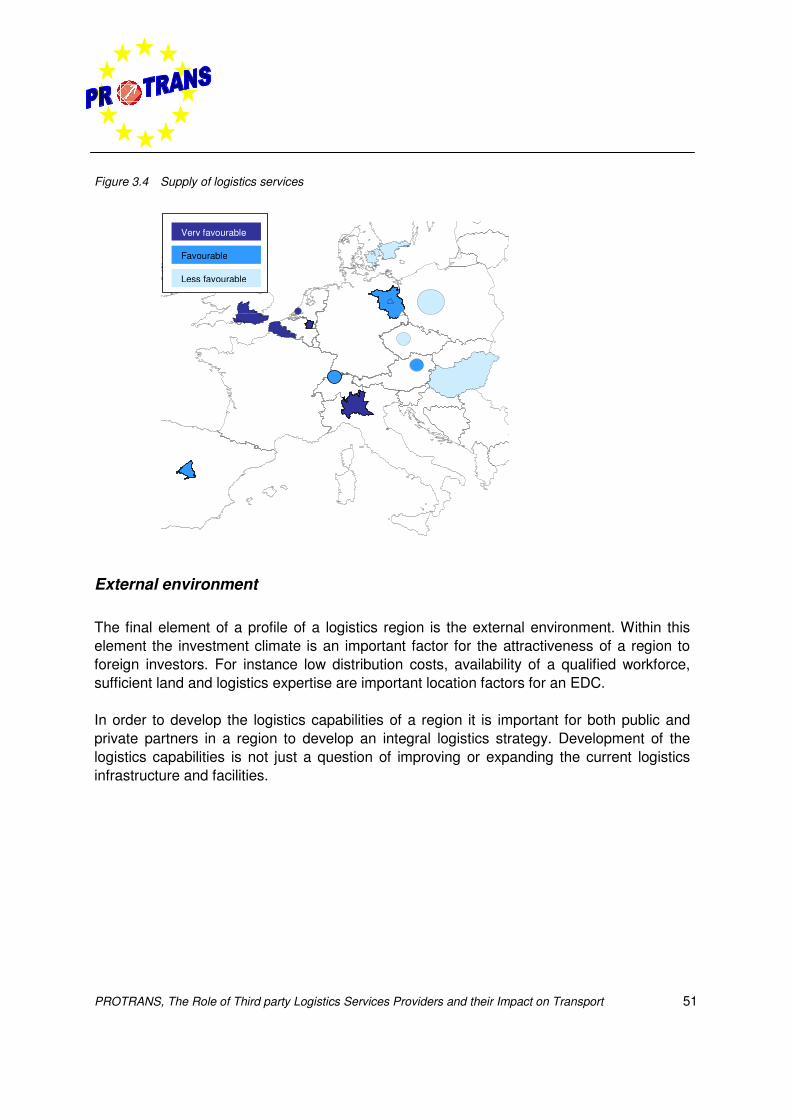

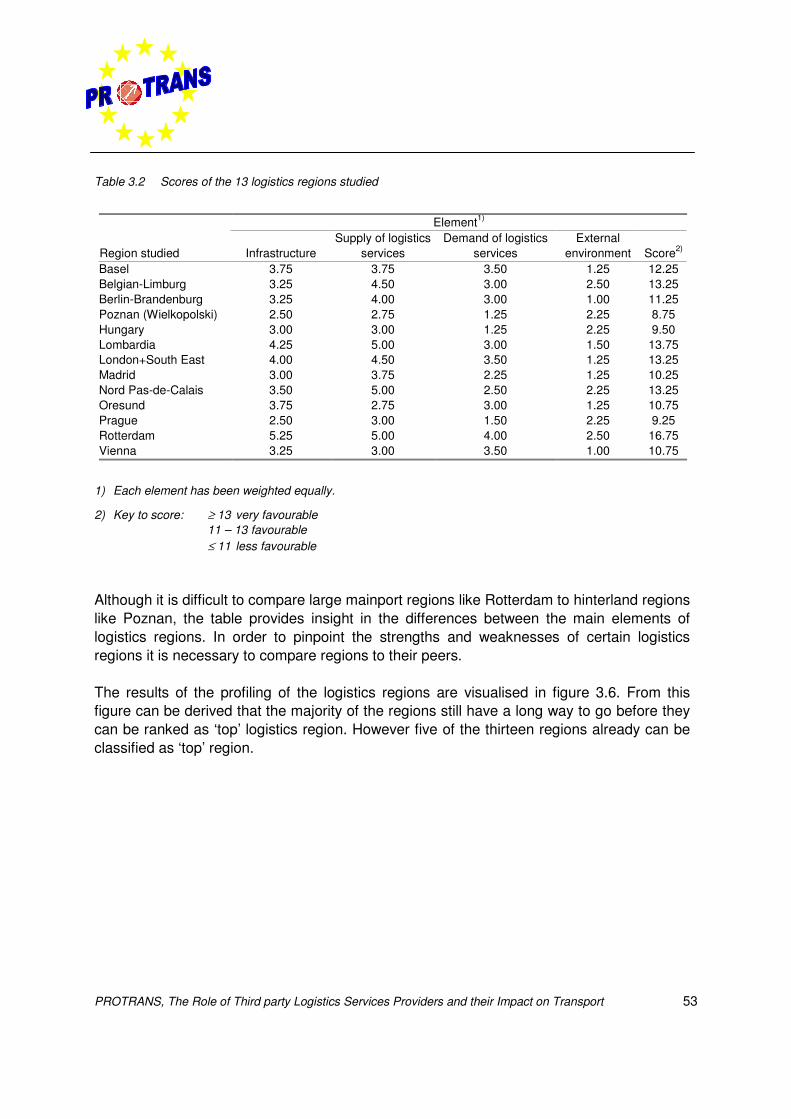

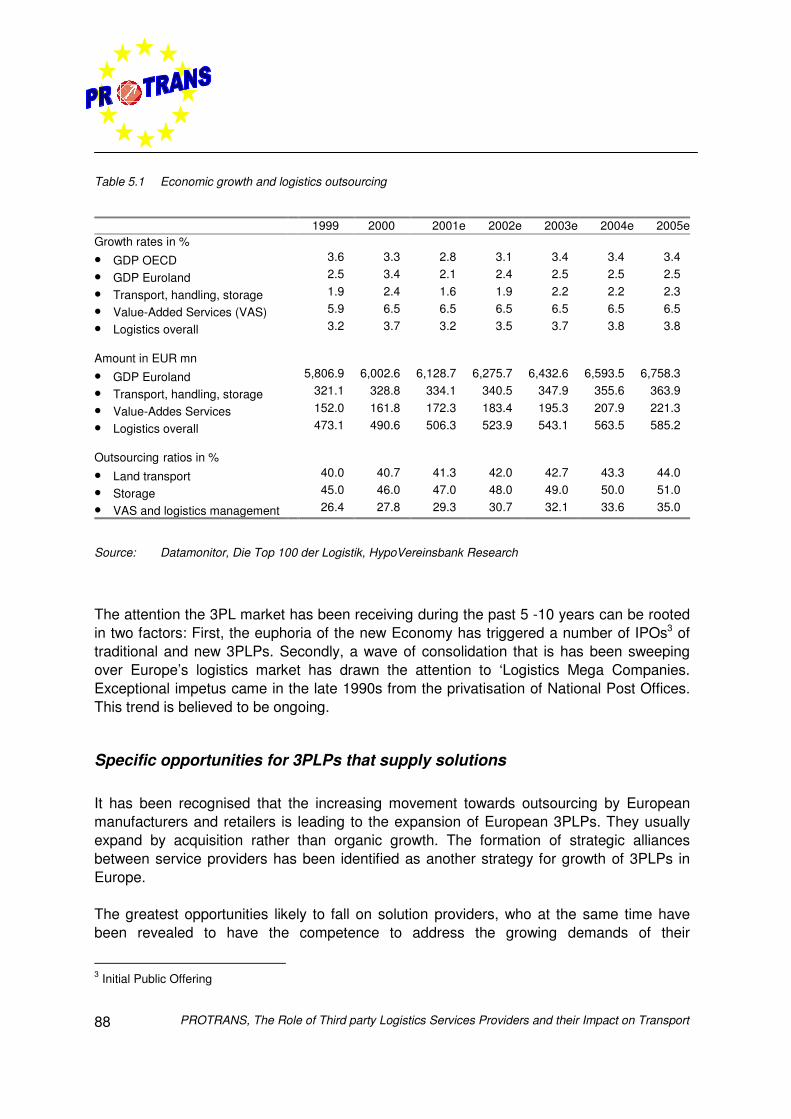

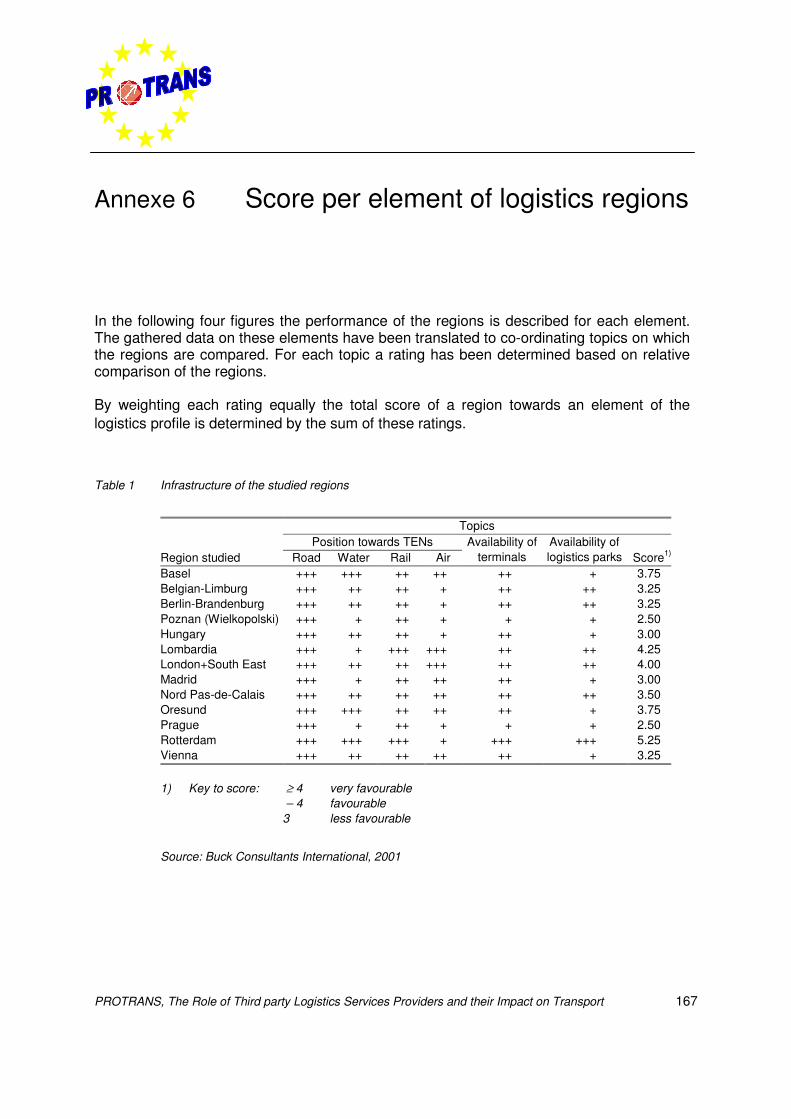

The 13 logistics regions have been analysed on these four main elements. The score ofeach region is captured in table 1. Depending on the number of topics which have beenanalysed per element, this score ranks from 0 till 6 for infrastructure and accessibility andsupply of logistics regions, from 0 till 4 for demand of logistics services and from 0 till 5 forthe external environment. The maximum score can be 21.

Table 1 Scores of studied logistics regions

Element1

Region studiedInfrastructure &

accessibilitySupply of logistics

servicesDemand of logistics

servicesExternal

environment Score2

Basel 3.75 3.75 3.50 1.25 12.25Belgian-Limburg 3.25 4.50 3.00 2.50 13.25Berlin-Brandenburg 3.25 4.00 3.00 1.00 11.25Poznan (Wielkopolski) 2.50 2.75 1.25 2.25 8.75Hungary 3.00 3.00 1.25 2.25 9.50Lombardia 4.25 5.00 3.00 1.50 13.75London+South East 4.00 4.50 3.50 1.25 13.25Madrid 3.00 3.75 2.25 1.25 10.25Nord Pas-de-Calais 3.50 5.00 2.50 2.25 13.25Oresund 3.75 2.75 3.00 1.25 10.75Prague 2.50 3.00 1.50 2.25 9.25Rotterdam 5.25 5.00 4.00 2.50 16.75Vienna 3.25 3.00 3.50 1.00 10.75

1 Each element has been weighted equally2 Key to score: ≥ 13 very favourable

11 – 13 favourable≤ 11 less favourable

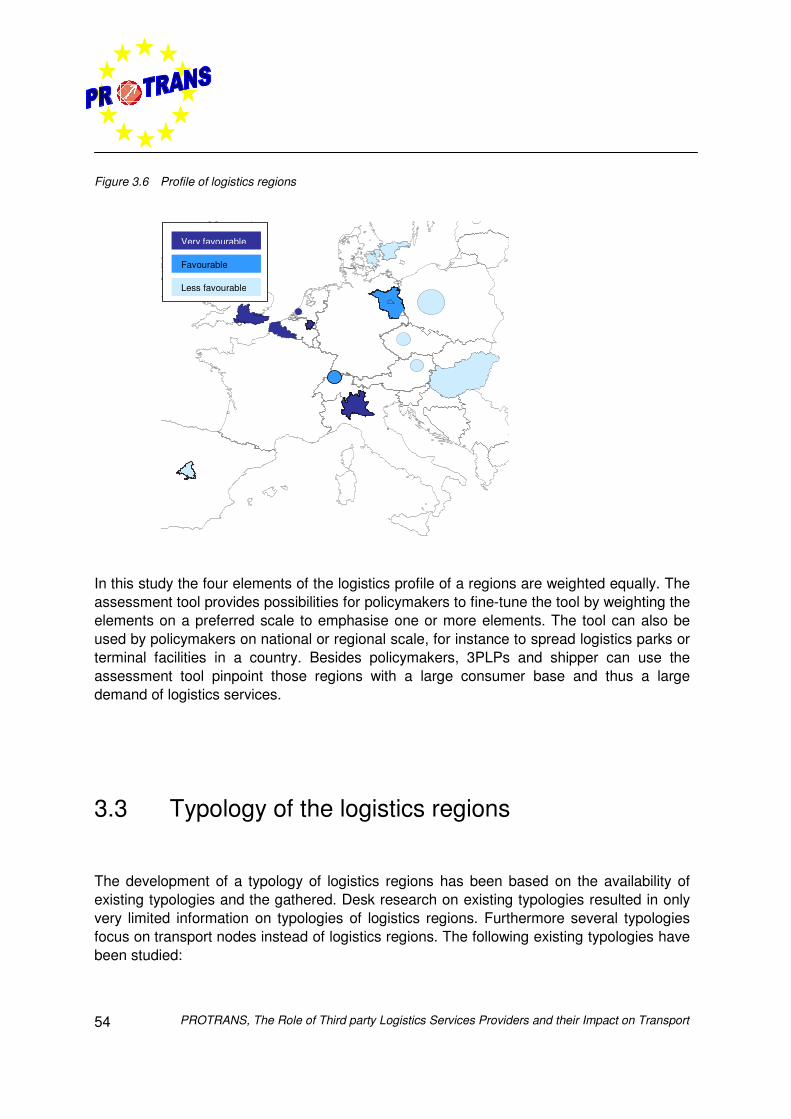

Although it is difficult to compare large mainport regions like Rotterdam to hinterland regionslike Poznan, the table provides insight in the differences between the main elements oflogistics regions. In order to pinpoint the strengths and weaknesses of certain logisticsregions it is necessary to compare regions to their peers.

In this study the four elements of the logistics profile of a regions are weighted equally. Theassessment tool provides possibilities for policymakers to fine-tune the tool by weighting theelements on a preferred scale to emphasise one or more elements.

Typology of a logistics region

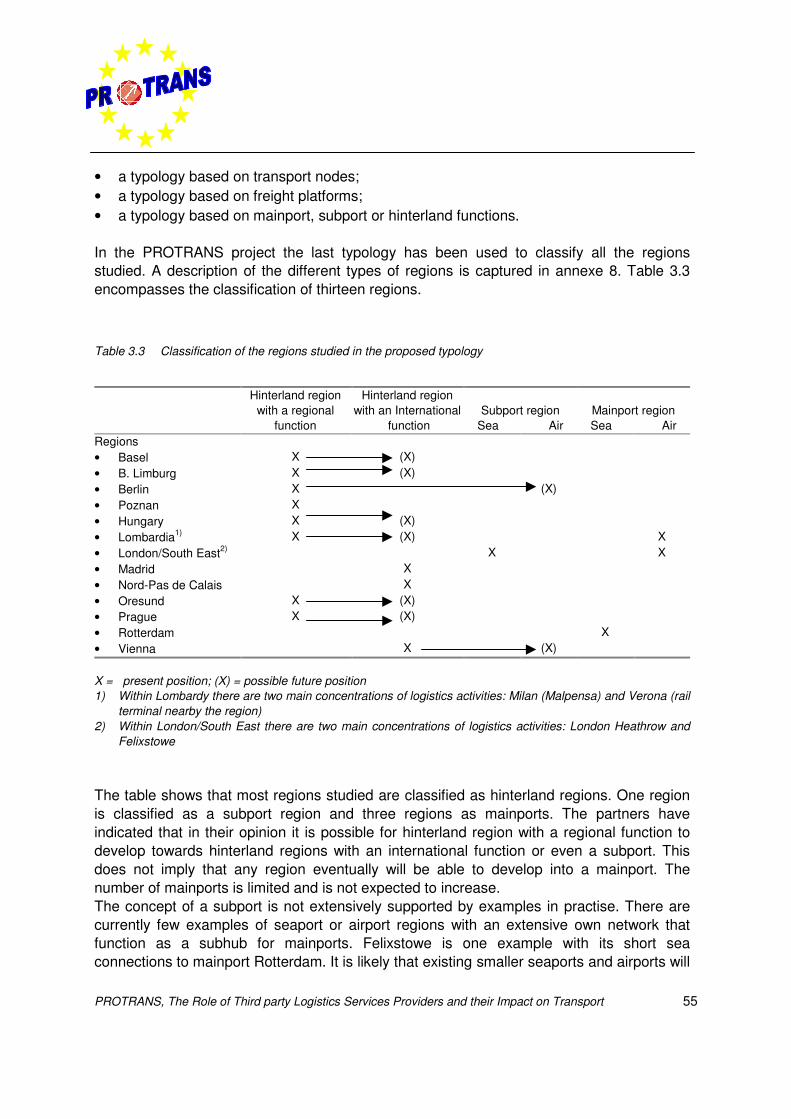

The analysis of logistics regions on the four elements has resulted in a well-foundedtypology of regions, which distinct mainport, subport and hinterland regions with an

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 7

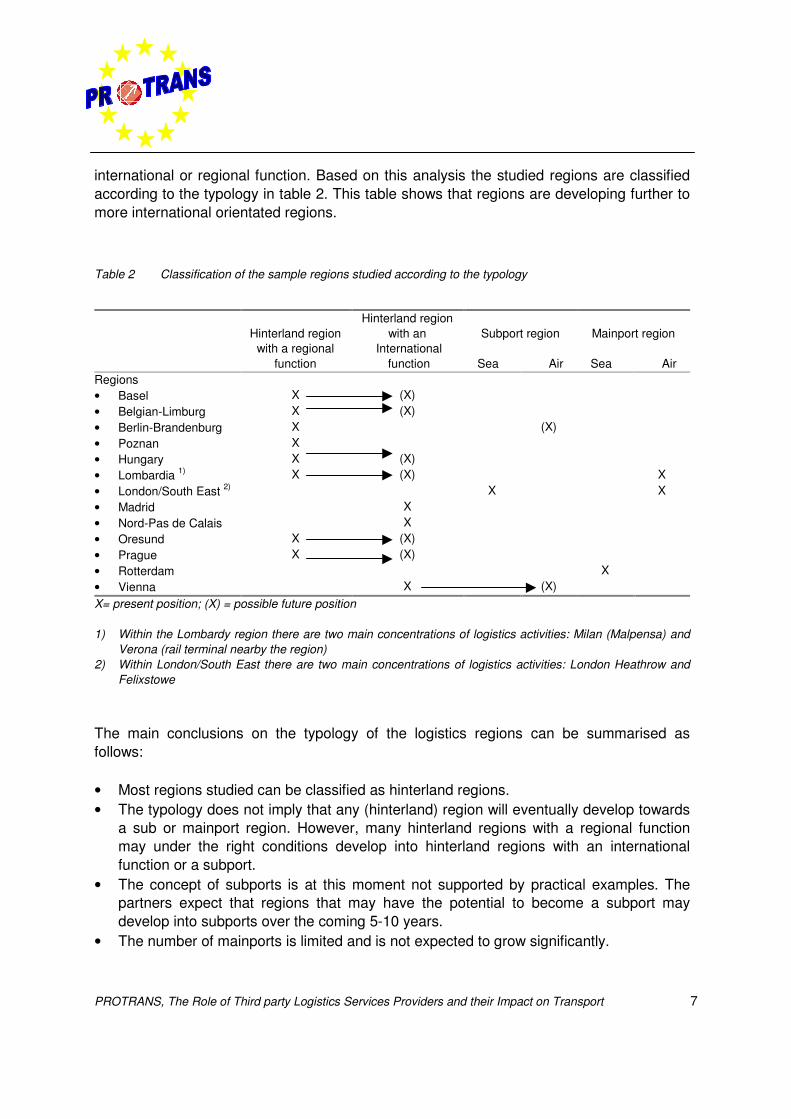

international or regional function. Based on this analysis the studied regions are classifiedaccording to the typology in table 2. This table shows that regions are developing further tomore international orientated regions.

Table 2 Classification of the sample regions studied according to the typology

Hinterland regionwith a regional

function

Hinterland regionwith an

International function

Subport region

Sea Air

Mainport region

Sea AirRegions• Basel X (X)• Belgian-Limburg X (X)• Berlin-Brandenburg X (X)• Poznan X• Hungary X (X)• Lombardia 1) X (X) X• London/South East 2) X X• Madrid X• Nord-Pas de Calais X• Oresund X (X)• Prague X (X)• Rotterdam X• Vienna X (X)X= present position; (X) = possible future position

1) Within the Lombardy region there are two main concentrations of logistics activities: Milan (Malpensa) andVerona (rail terminal nearby the region)

2) Within London/South East there are two main concentrations of logistics activities: London Heathrow andFelixstowe

The main conclusions on the typology of the logistics regions can be summarised asfollows:

• Most regions studied can be classified as hinterland regions.• The typology does not imply that any (hinterland) region will eventually develop towards

a sub or mainport region. However, many hinterland regions with a regional functionmay under the right conditions develop into hinterland regions with an internationalfunction or a subport.

• The concept of subports is at this moment not supported by practical examples. Thepartners expect that regions that may have the potential to become a subport maydevelop into subports over the coming 5-10 years.

• The number of mainports is limited and is not expected to grow significantly.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport8

Policymakers, transport professionals and scientist in Europe have more and moreaccepted the typology of logistics regions as used in the PROTRANS project. This indicatesthat the logistics market needs a clear typology to identify and compare logistics regions.The exception of this typology also subscribes the innovative character of the projectexamined depend on the type of region.

Furthermore can be concluded that the presence of 3PLPs in the above-described types ofregions differ. 3PLPs in mainport regions are mainly focused on forwarding andwarehousing since these activities are related to locations where freight is consolidatedfrom various sources and redirected in high volume flows to national or regionalwarehouses in elsewhere in Europe. Since hinterland regions in general have loweroperating costs and more land available more presence of networking facilities is seen inthis type of logistics region.

Success and failure factors

A benchmark has been developed in PROTRANS, in order to define best practice regionsand to derive success and failure factors. This assessment tool can furthermore be used byregional, national or European policy makers to development of their logistics, but also byshippers and 3PLPs to gain insight in the regional variances, strengths and weaknesses ofregions. This information that can be of great value for decisions on for instance locationchoice and network development. The degree of success of a logistics region will even begreater if public and private partners like 3PLPs and shippers co-operated in thedevelopment of an integral strategic logistics vision of a region.

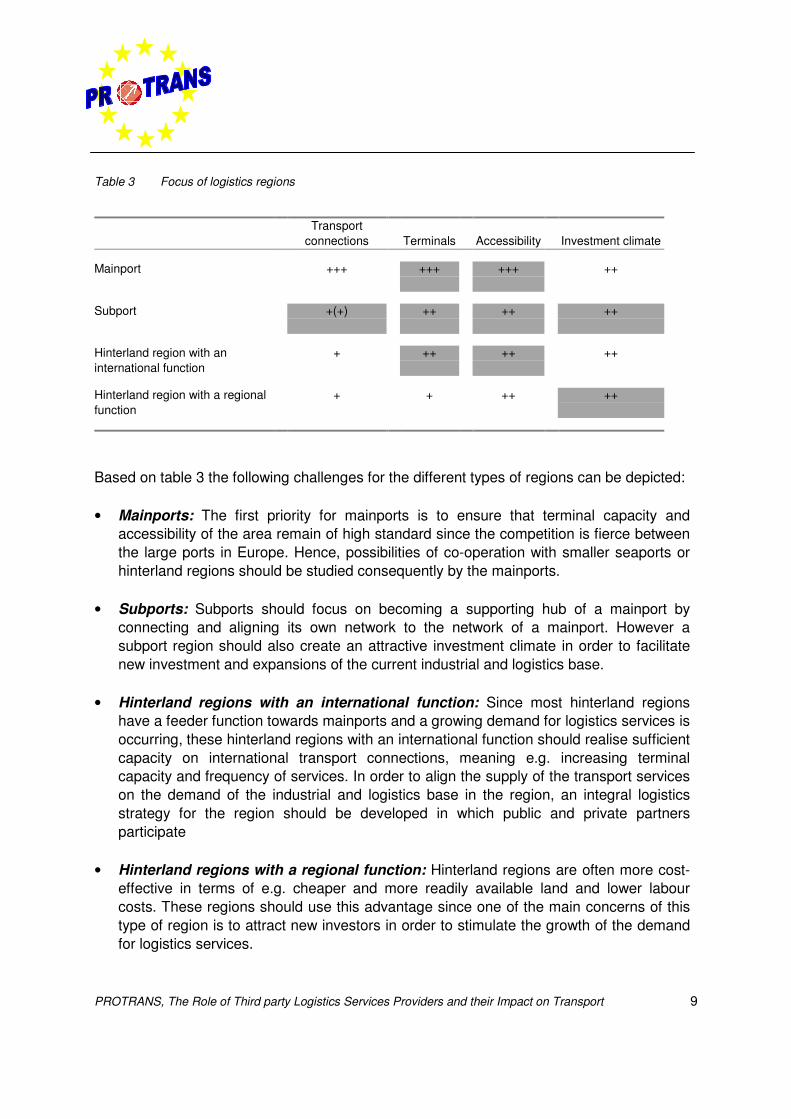

Looking at the success and failure factors of the various types of logistics regions and at thebenchmark of the best-practise regions in the PROTRANS project, the focus of each type ofregion in order to improve its logistics capabilities is summarised in table 3 the focus. Themain areas of focus are shaded in grey. The number of ‘plusses’ presents the success of aregion.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 9

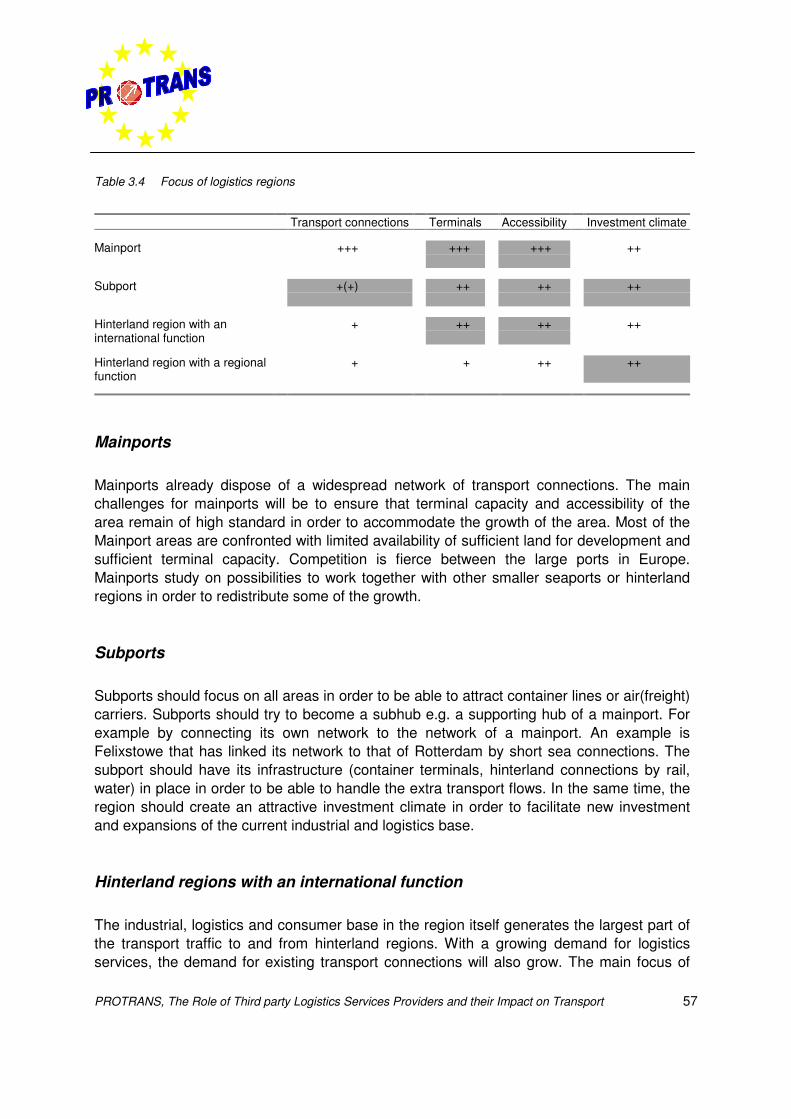

Table 3 Focus of logistics regions

Transportconnections Terminals Accessibility Investment climate

Mainport +++ +++ +++ ++

Subport +(+) ++ ++ ++

Hinterland region with aninternational function

+ ++ ++ ++

Hinterland region with a regionalfunction

+ + ++ ++

Based on table 3 the following challenges for the different types of regions can be depicted:

• Mainports: The first priority for mainports is to ensure that terminal capacity andaccessibility of the area remain of high standard since the competition is fierce betweenthe large ports in Europe. Hence, possibilities of co-operation with smaller seaports orhinterland regions should be studied consequently by the mainports.

• Subports: Subports should focus on becoming a supporting hub of a mainport byconnecting and aligning its own network to the network of a mainport. However asubport region should also create an attractive investment climate in order to facilitatenew investment and expansions of the current industrial and logistics base.

• Hinterland regions with an international function: Since most hinterland regionshave a feeder function towards mainports and a growing demand for logistics services isoccurring, these hinterland regions with an international function should realise sufficientcapacity on international transport connections, meaning e.g. increasing terminalcapacity and frequency of services. In order to align the supply of the transport serviceson the demand of the industrial and logistics base in the region, an integral logisticsstrategy for the region should be developed in which public and private partnersparticipate

• Hinterland regions with a regional function: Hinterland regions are often more cost-effective in terms of e.g. cheaper and more readily available land and lower labourcosts. These regions should use this advantage since one of the main concerns of thistype of region is to attract new investors in order to stimulate the growth of the demandfor logistics services.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport10

4 Market supply and demand for third-party logistics

3PLPs involvement

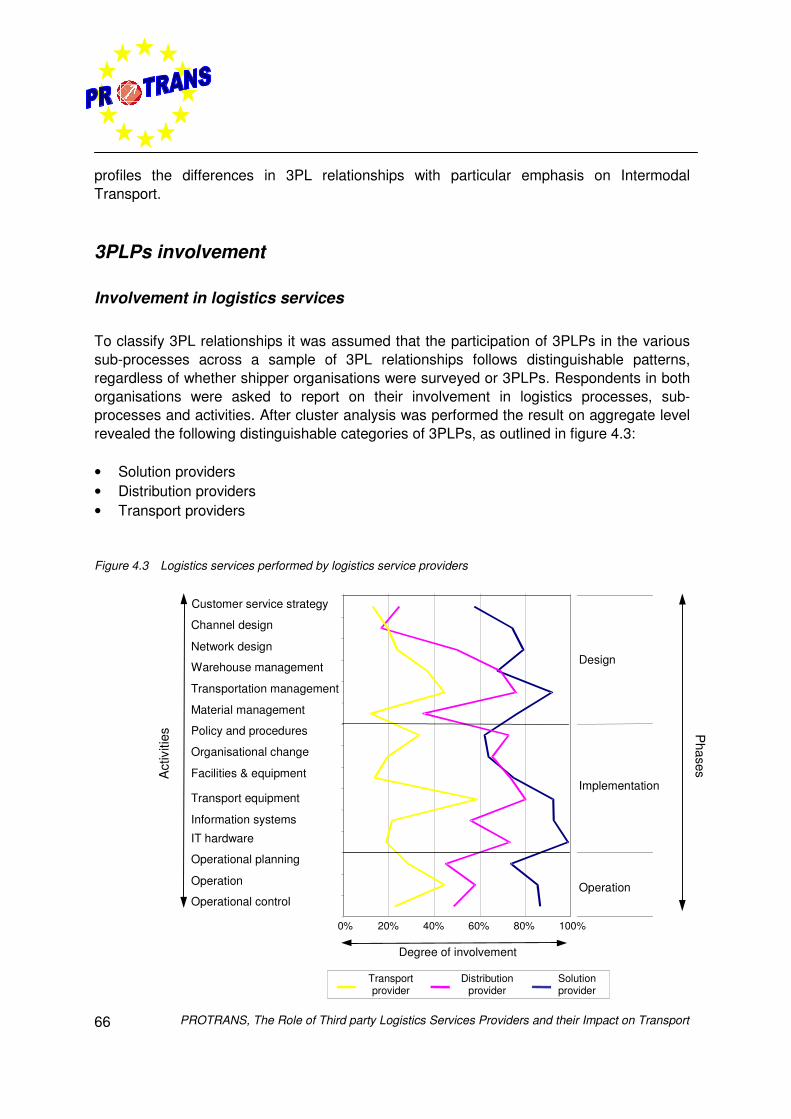

The last few years, there has been a significant change in shipper-3PLP relationships. Theprimary driving forces previously used to be reduction of costs and release capital toalternative purposes. Whereas today the driving forces have a more strategic trust likeincreasing the market coverage, improvement of service levels or increasing flexibilitytowards the changing requirements of customers. These changes result in different types of3PLPs. The segmentation in the logistics market revealed 3 clearly distinguishablecategories of 3PL provision:

• solution providers;• distribution providers;• transport providers.

The most advanced form of 3PL provision was labelled ‘solution provider’. These providershave successfully developed capabilities that exceed the traditional domain of transport andwarehousing in logistics. They emphasise additionally their strategic management skills andexpertise information systems. Distribution providers are mainly involved in design andimplementation activities in warehousing as well as transportation. Transport providers areaccordingly mainly involved in transport related design and implementation activities as wellas involvement in operations.

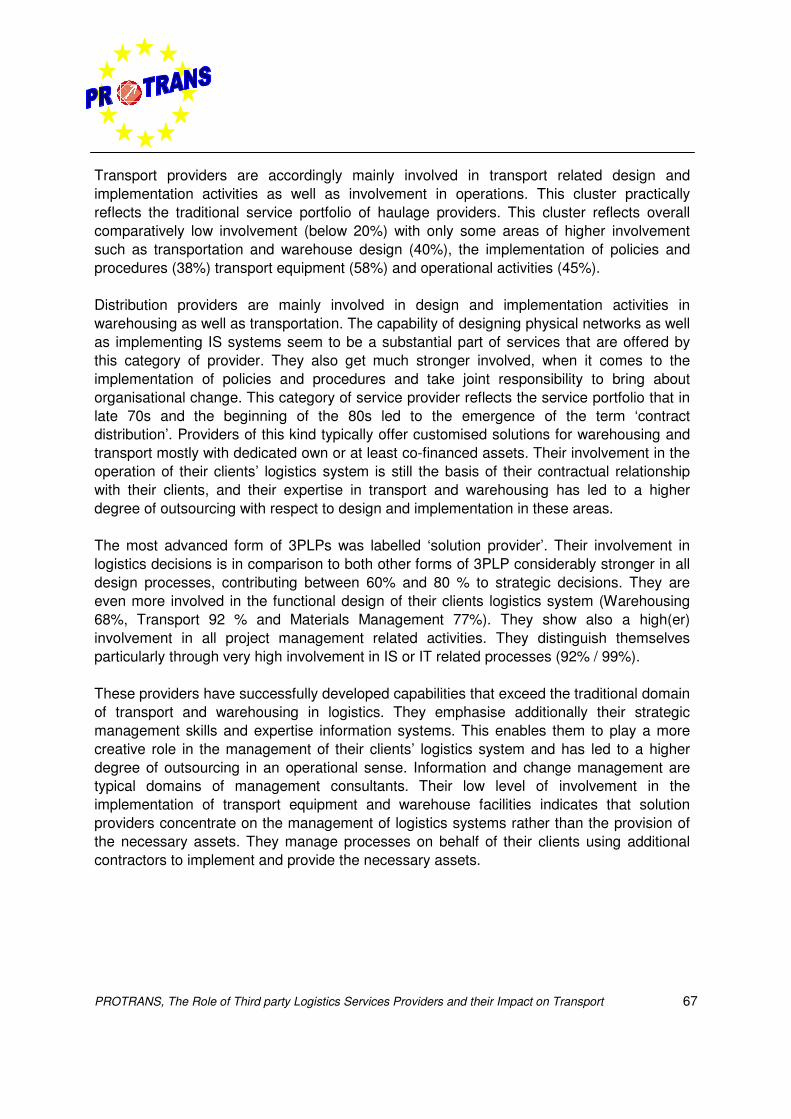

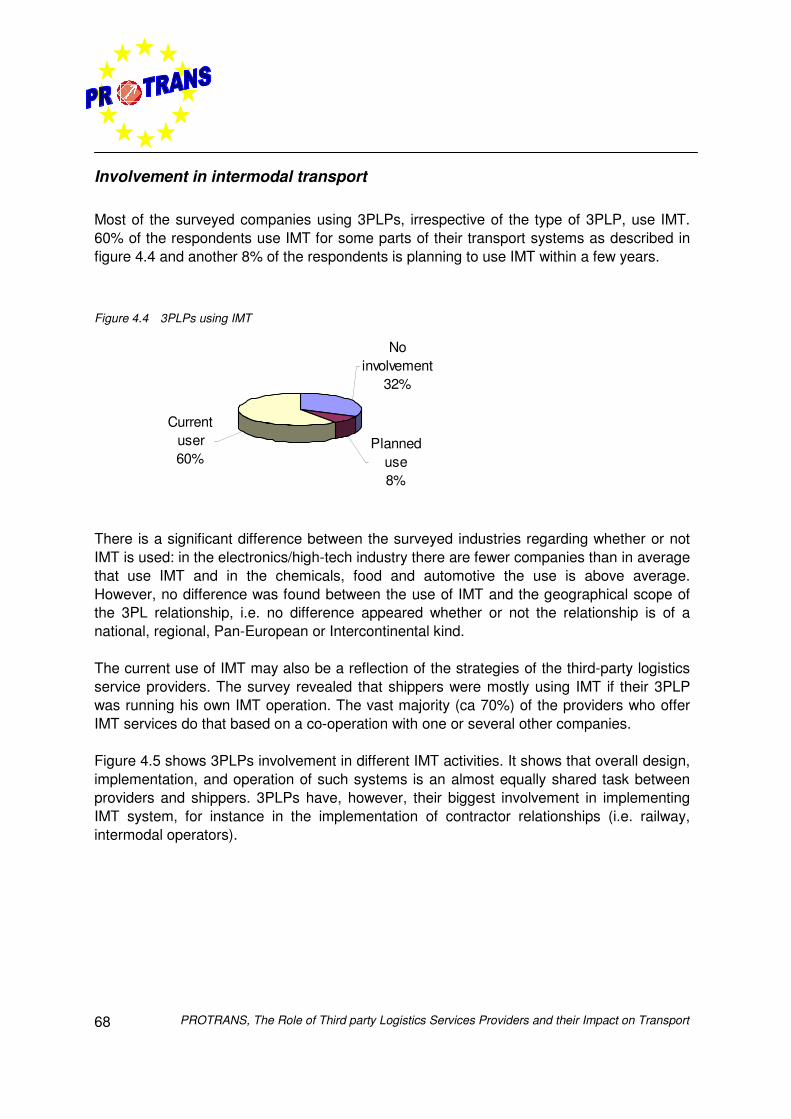

The current use of intermodal transport (IMT) may also be a reflection of the strategies ofthe third-party logistics service providers. There is a significant difference in the involvementof 3PLPs in IMT depending on what kind of IMT strategy the provider has.

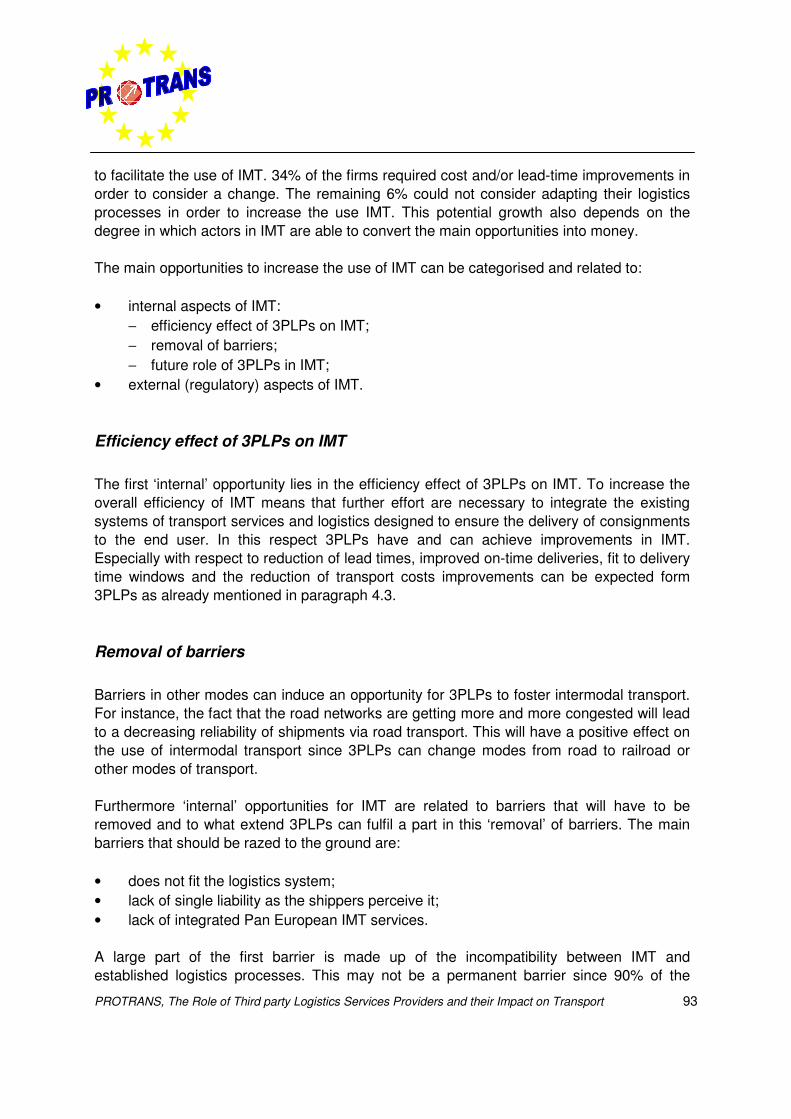

Proactivity of 3PLPs

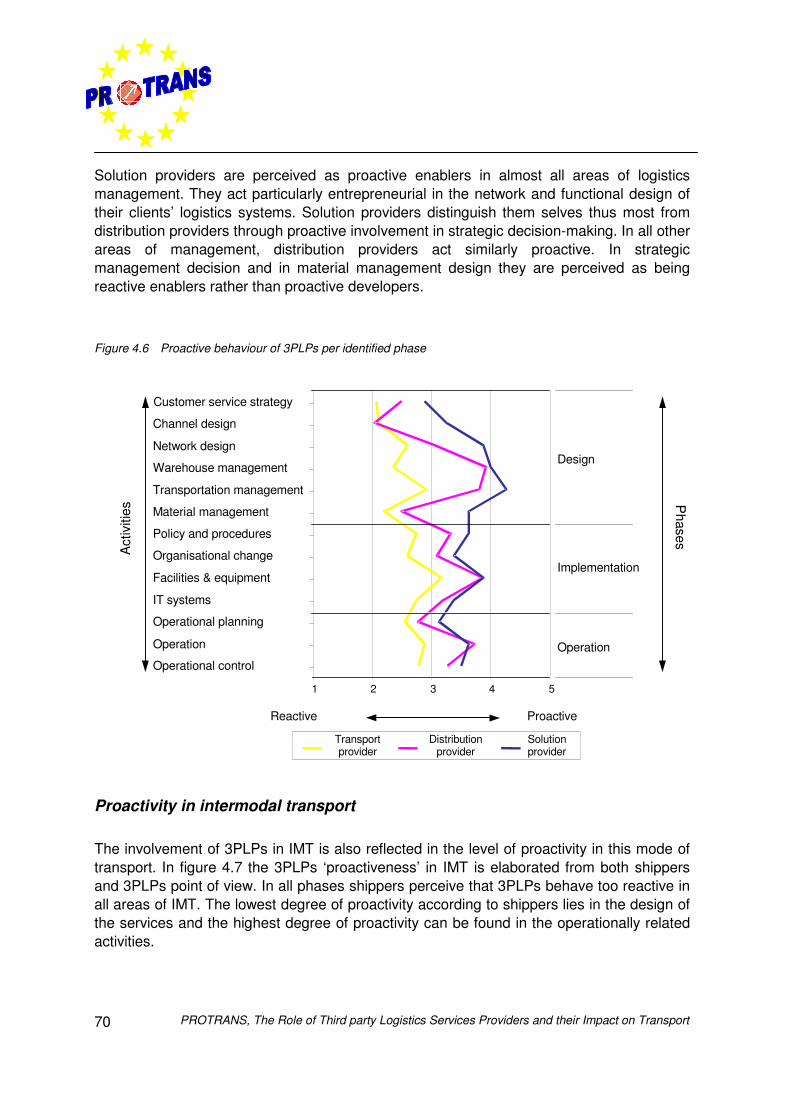

Solution providers are perceived as proactive enablers in almost all areas of logisticsmanagement. These providers are most heavily involved in all aspects of the shipperslogistics systems (level of involvement is 60-90%). They distinguish themselves most fromdistribution providers (level of involvement is 40-80% except strategic design activities werethey are much less involved) and finally the transport providers are the least involved (20-40%) and transport providers through proactive involvement in strategic decision-making.

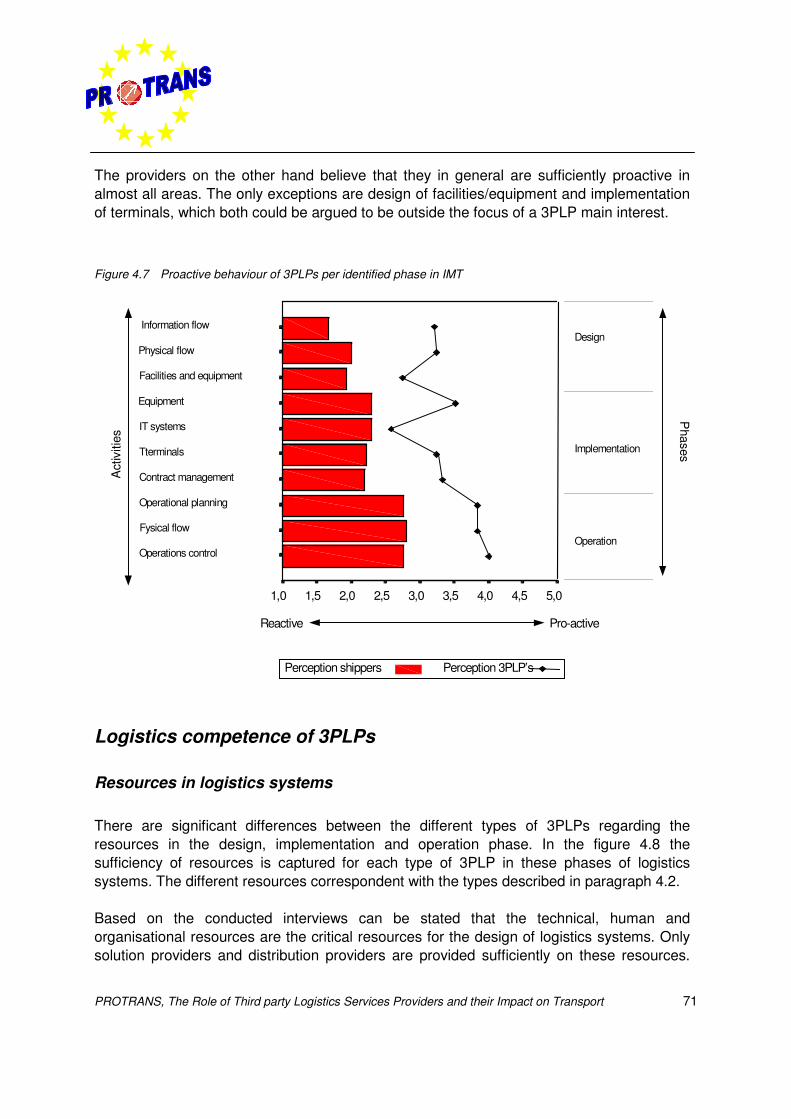

The limited involvement of 3PLPs in IMT is also reflected in the level of pro-activity in IMT.In all phases shippers perceive that 3PLPs behave too reactive in all areas of IMT. The

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 11

lowest degree of pro-activity according to shippers lies in the design of the services and thehighest can be found in the operationally related activities.

Competence of 3PLPs

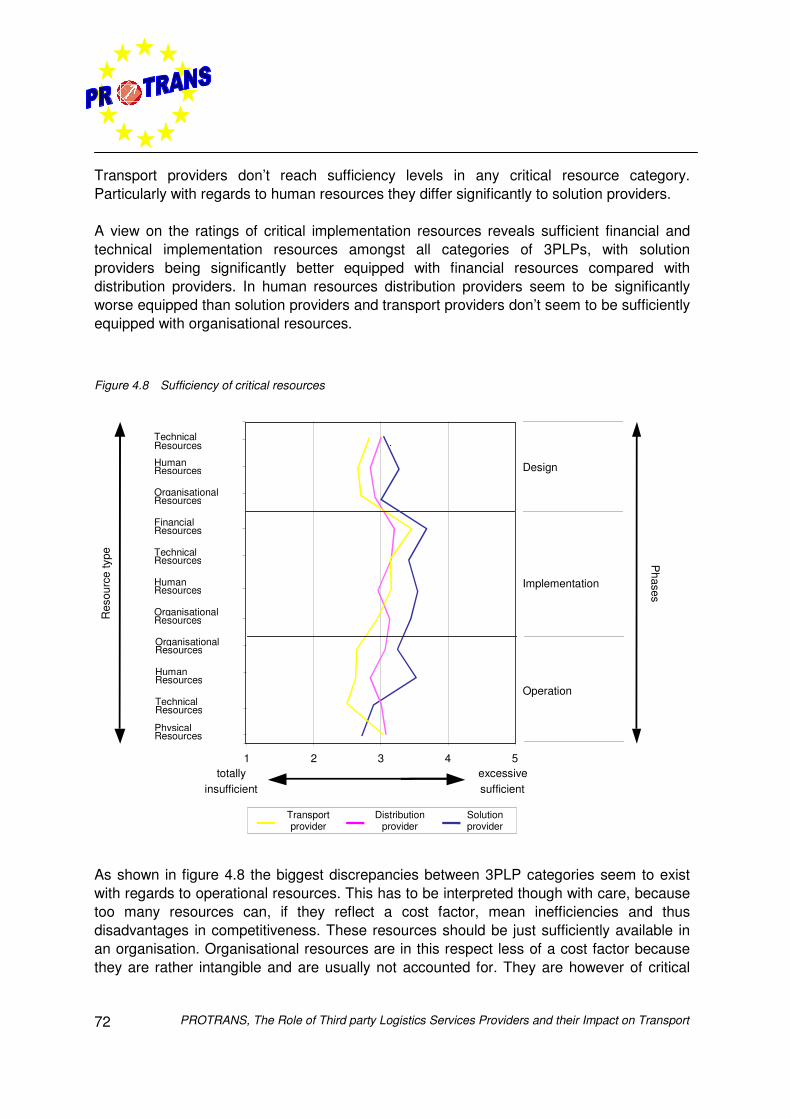

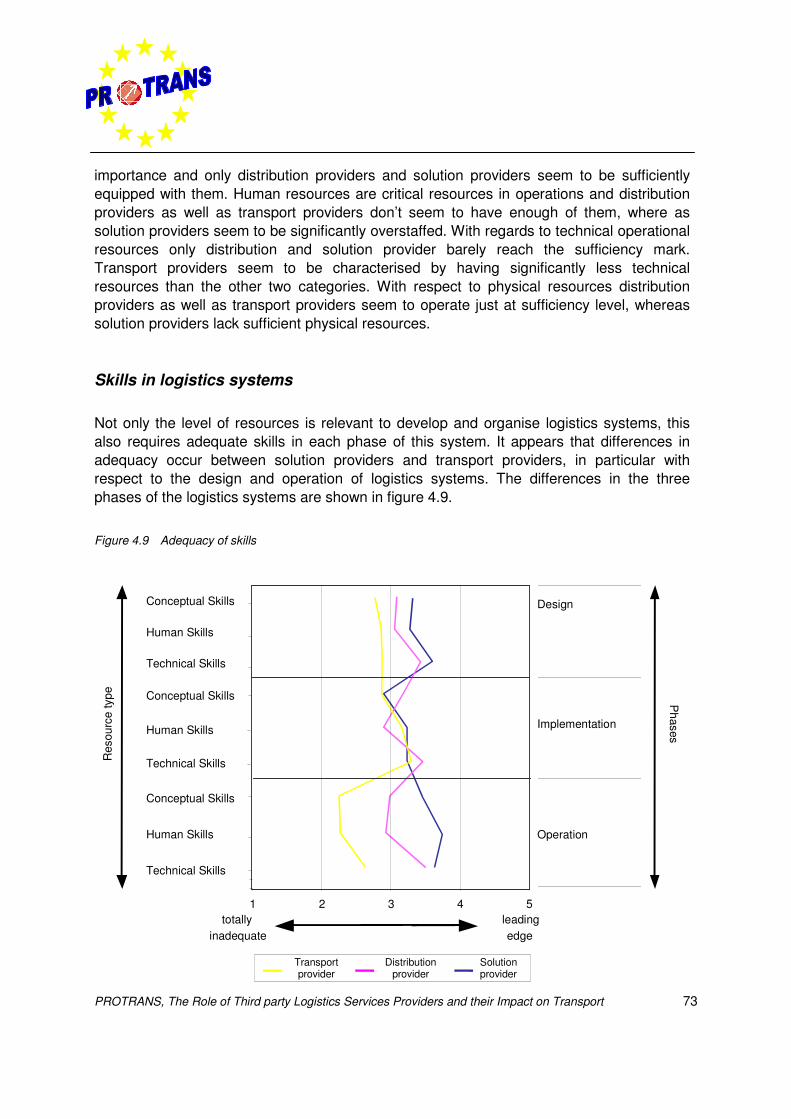

The difference between the categories of 3PLPs is additionally underlined by significantdifferences in their resource and skill base. Particularly sufficient human resources andconceptual skills distinguish solution providers from distribution or transport providers. Itappears that differences in adequacy of skills occur between solution providers andtransport providers, in particular with respect to the design and operation of logisticssystems.

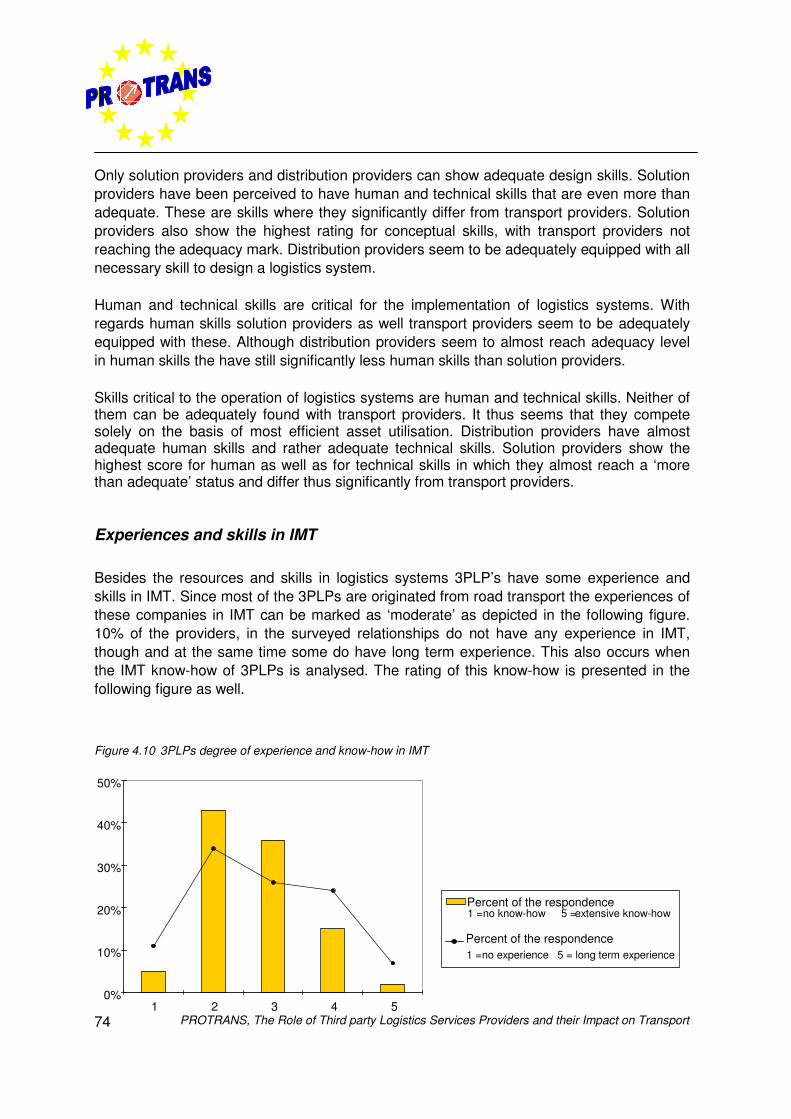

Regarding IMT the experience and know how can be marked as ‘moderate’ since most ofthe 3PLPs are originated from road transport.

Logistics performances

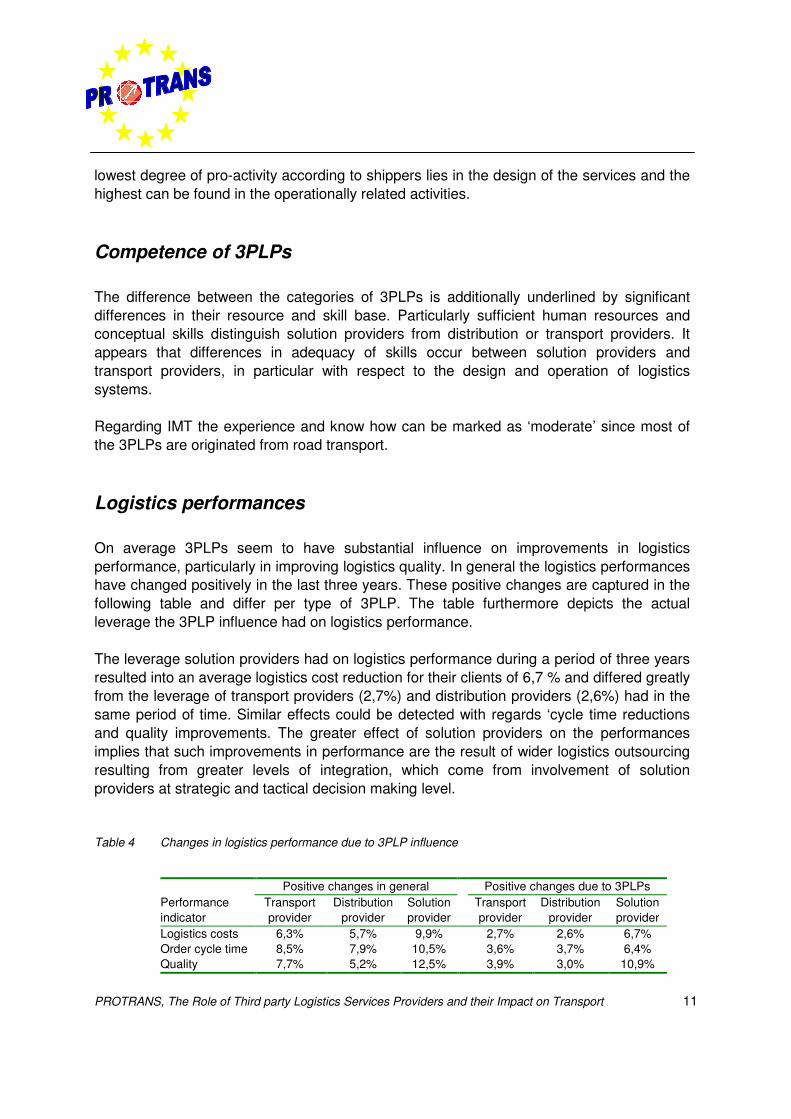

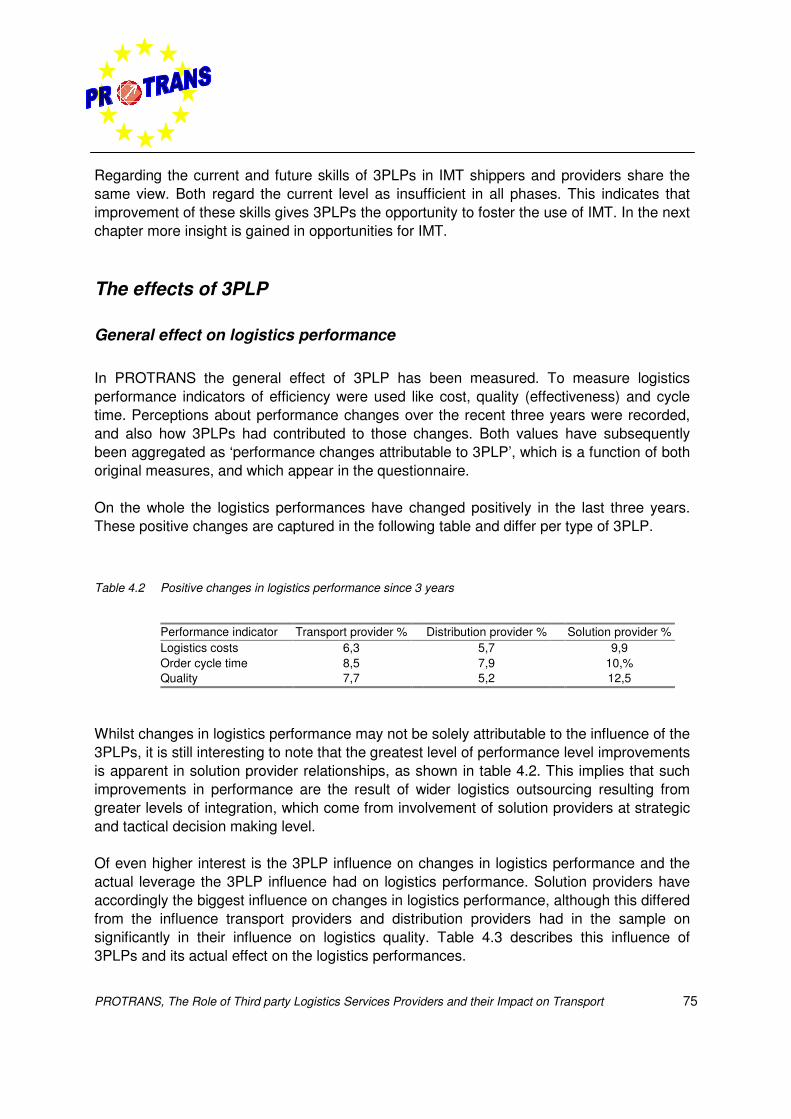

On average 3PLPs seem to have substantial influence on improvements in logisticsperformance, particularly in improving logistics quality. In general the logistics performanceshave changed positively in the last three years. These positive changes are captured in thefollowing table and differ per type of 3PLP. The table furthermore depicts the actualleverage the 3PLP influence had on logistics performance.

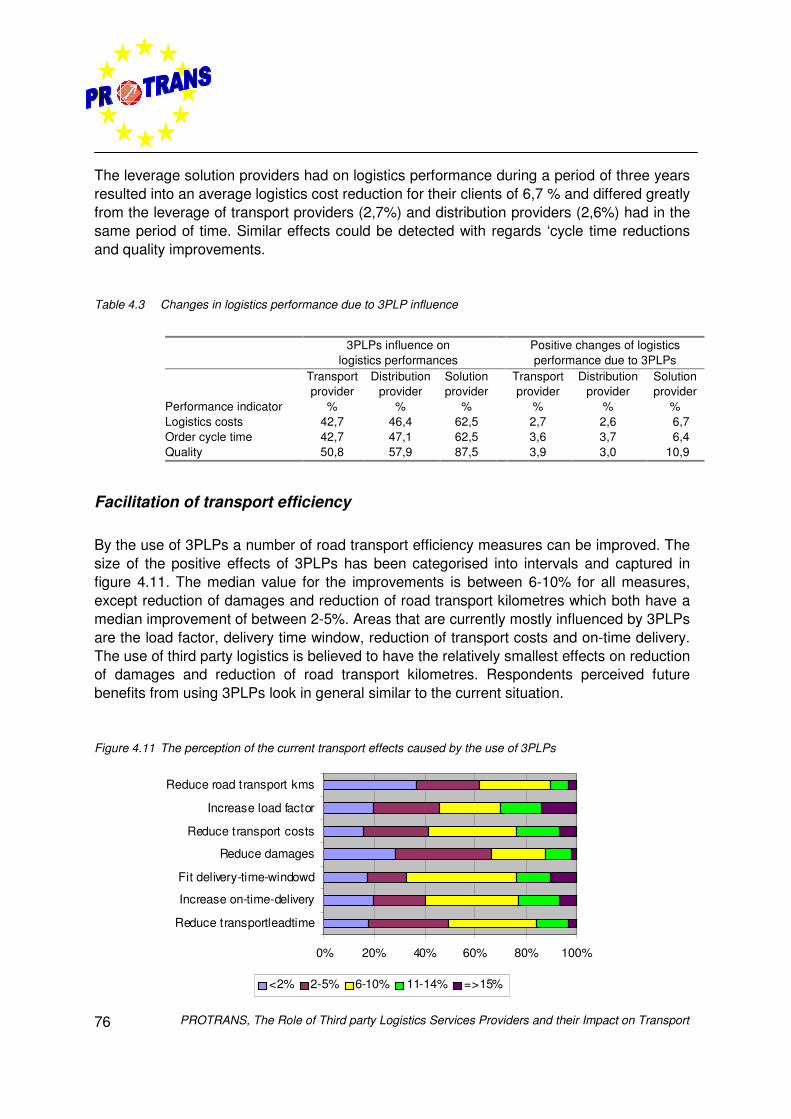

The leverage solution providers had on logistics performance during a period of three yearsresulted into an average logistics cost reduction for their clients of 6,7 % and differed greatlyfrom the leverage of transport providers (2,7%) and distribution providers (2,6%) had in thesame period of time. Similar effects could be detected with regards ‘cycle time reductionsand quality improvements. The greater effect of solution providers on the performancesimplies that such improvements in performance are the result of wider logistics outsourcingresulting from greater levels of integration, which come from involvement of solutionproviders at strategic and tactical decision making level.

Table 4 Changes in logistics performance due to 3PLP influence

Positive changes in general Positive changes due to 3PLPsPerformanceindicator

Transportprovider

Distributionprovider

Solutionprovider

Transportprovider

Distributionprovider

Solutionprovider

Logistics costs 6,3% 5,7% 9,9% 2,7% 2,6% 6,7%Order cycle time 8,5% 7,9% 10,5% 3,6% 3,7% 6,4%Quality 7,7% 5,2% 12,5% 3,9% 3,0% 10,9%

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport12

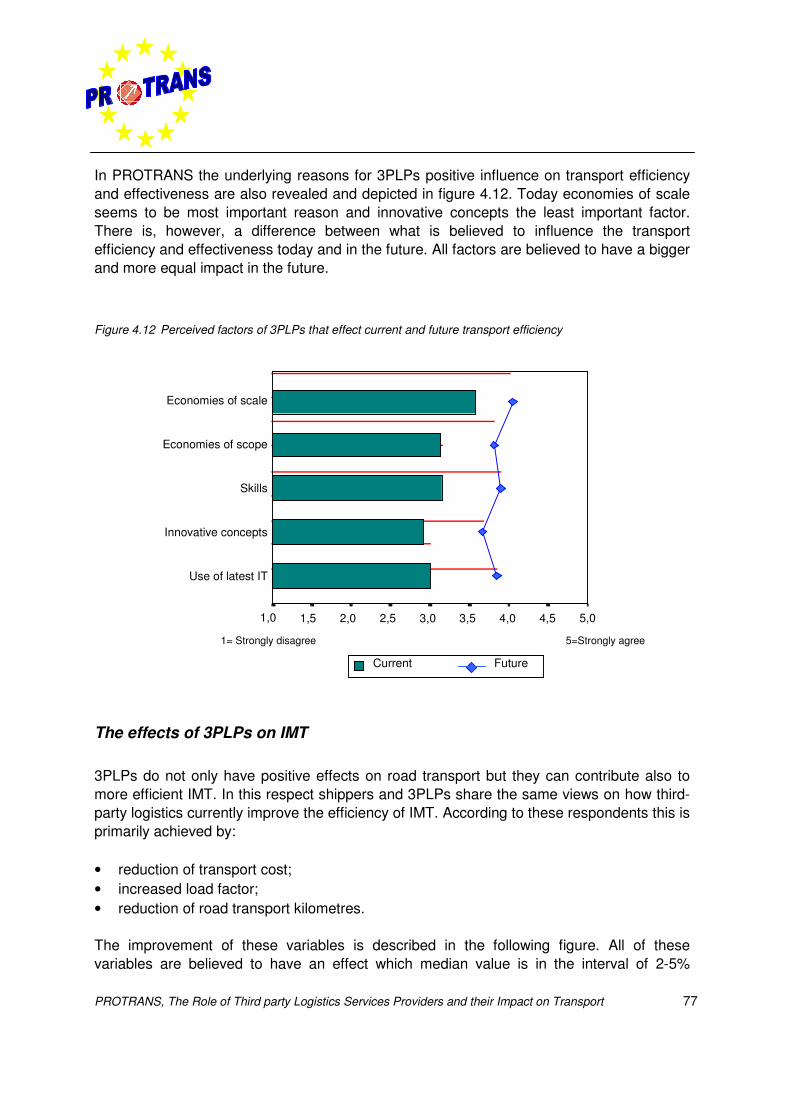

The use of 3PLPs is believed to currently improve road transport efficiency and to a lesserdegree IMT efficiency. The most important factor behind the fact that the 3PLPs achievebetter transport efficiency and effectiveness today is economies of scale. Because of theeconomies of scale and scope, 3PLPs are able for instance to consolidate physical flowsand optimise information flows.

Towards IMT shippers and 3PLPs share the same views on how third-party logisticscurrently improve the efficiency of IMT. They do that by:

• reducing transport cost;• increasing load factor;• reducing road transport kilometres for pre- and end haulage.

5 Barriers and opportunities for third-party logistics

The role of 3PLPs in the supply chain in general and in the provision of logistics and IMTservices in specific is increasing. Changes in the way logistics are managed and inparticular transport are a matter of designing or redesigning logistics and transport systems.Modal choice is a strategic decision that is determined at a very early stage of designing anew transport system. The degree of success in designing or redesigning logistics andtransport systems largely depends on the shipper-3PLP relationship and the ability toovercome the barriers in logistics and IMT and to effectuate the opportunities in the logisticsmarket.

Barriers for further outsourcing and IMT

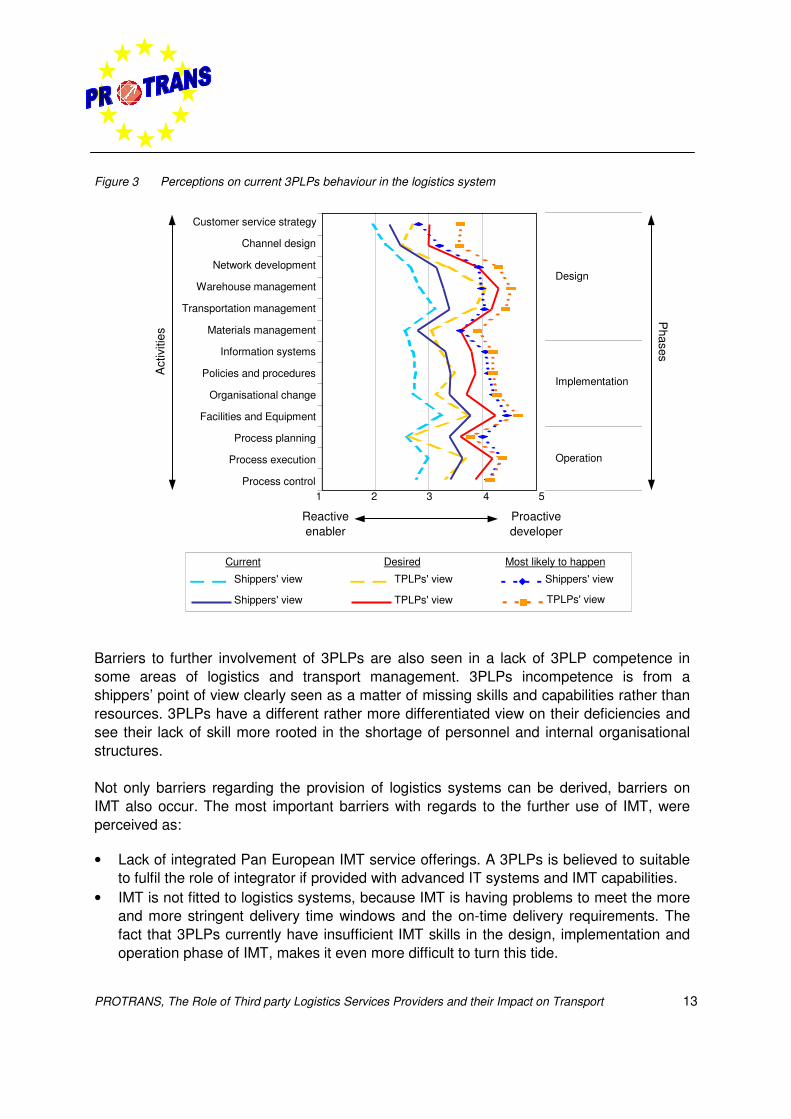

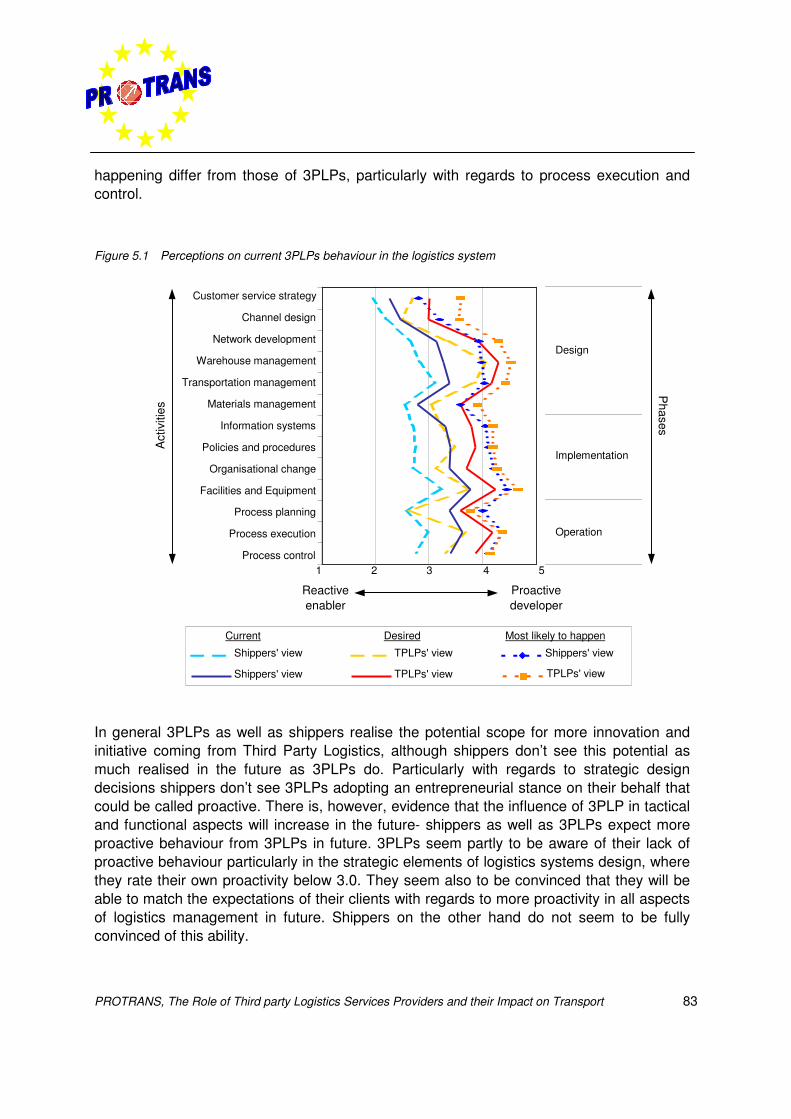

Shippers generally believe that 3PLPs are lacking a proactive entrepreneurial approach tologistics management and are thus failing to offer innovative concepts. Where shipperdesire more proactiveness from 3PLPs, they do not believe that these will improve much inthe future. The following figure reveals a difference between shippers’ and 3PLPs’perceptions of current, desired and ‘most likely to happen’ developments in 3PLPs proactivebehaviour. This appears today with regards to design and operation of a logistics systemand is expected to remain for the design phase.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 13

Figure 3 Perceptions on current 3PLPs behaviour in the logistics system

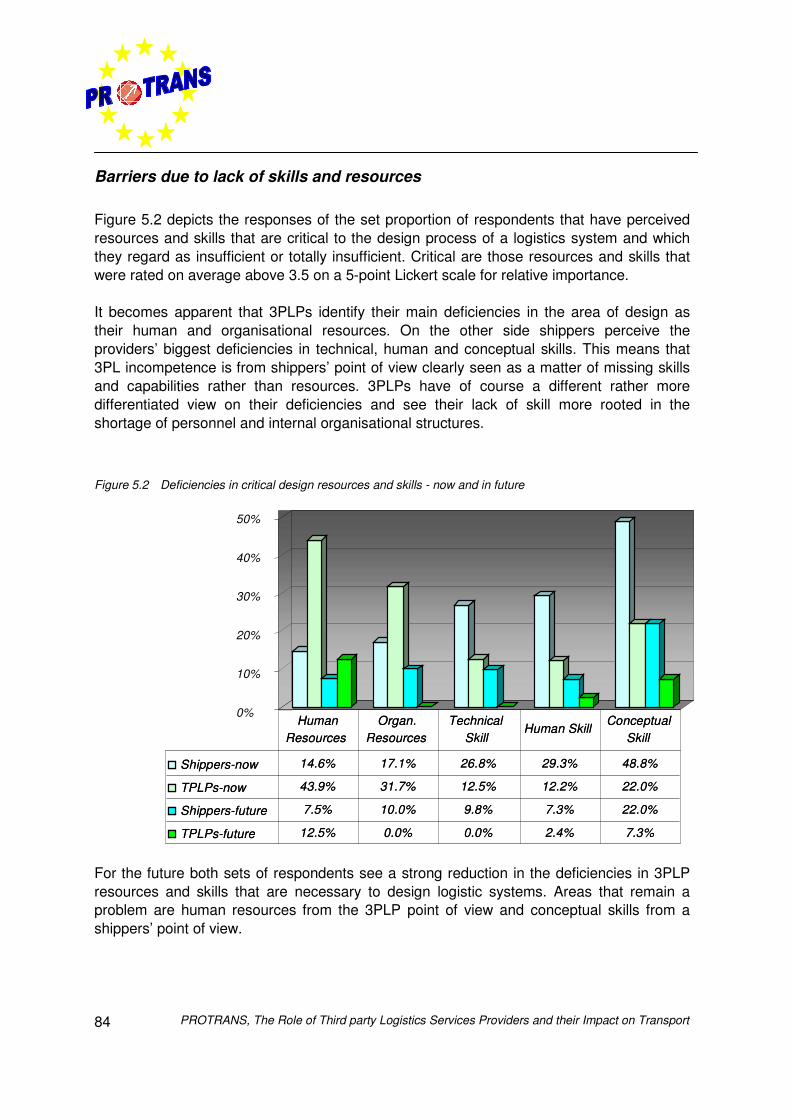

Barriers to further involvement of 3PLPs are also seen in a lack of 3PLP competence insome areas of logistics and transport management. 3PLPs incompetence is from ashippers’ point of view clearly seen as a matter of missing skills and capabilities rather thanresources. 3PLPs have a different rather more differentiated view on their deficiencies andsee their lack of skill more rooted in the shortage of personnel and internal organisationalstructures.

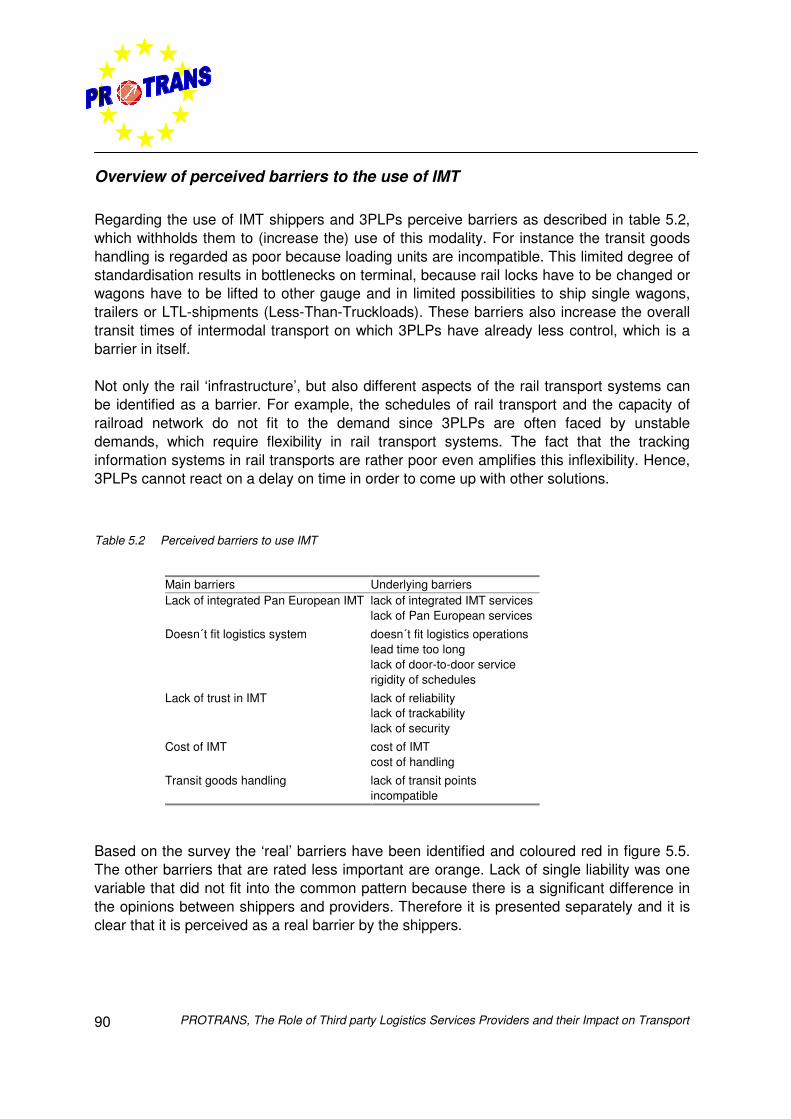

Not only barriers regarding the provision of logistics systems can be derived, barriers onIMT also occur. The most important barriers with regards to the further use of IMT, wereperceived as:

• Lack of integrated Pan European IMT service offerings. A 3PLPs is believed to suitableto fulfil the role of integrator if provided with advanced IT systems and IMT capabilities.

• IMT is not fitted to logistics systems, because IMT is having problems to meet the moreand more stringent delivery time windows and the on-time delivery requirements. Thefact that 3PLPs currently have insufficient IMT skills in the design, implementation andoperation phase of IMT, makes it even more difficult to turn this tide.

Customer service strategy

Channel design

Network development

Warehouse management

Transportation management

Materials management

Information systems

Policies and procedures

Organisational change

Facilities and Equipment

Process planning

Process execution

Process control

Shippers' view TPLPs' view Shippers' view

TPLPs' viewShippers' view TPLPs' view

Current Desired

1 2 3 4 5

Most likely to happen

Design

Implementation

Operation

Phases

Act

iviti

es

Reactiveenabler

Proactivedeveloper

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport14

• Lack of single liability of IMT according to the shippers, because of changes in laws andregulations on IMT and different actors involved in IMT.

With regards to the further use of intermodal transport there are barriers that are inherent toIMT and barrier that are rooted in the missing service offerings for IMT.

Opportunities for 3PLPs

In general opportunities for 3PLPs arise from the fact that shippers are more and moreturning to outsourcing strategies, not only in traditional operational areas, but also in areasof information and knowledge based logistics management. The 3PL industry in Europe isof a substantial size and is experiencing fast growth. The total expenditure, outsourced ornot outsourced, on logistics in Europe will grow annually between 3.5 and 3.8 % until 2005.This offers particular opportunities for solution providers that are capable of offeringservices at the high end of designing and implementing logistics systems. In general theuse of 3PLPs, especially in case of solution providers, has resulted in positive effects on thelogistics systems and there are several opportunities for 3PLPs to realise furtherimprovements. The main opportunities are:

• More proactive behaviour of 3PLPs in the optimisation of transport systems and furtherintegration of different transport modes. The solution providers can be seen as anexample since they show their capabilities in the strategic and tactical design of logisticssystems and are able to subcontract the daily operations to preferred subcontractors.

• Increase involvement of 3PLPs in the design phases of logistics systems.• Sustainable logistics by 3PLPs via consolidation of goods, mode selection, and carrier

selection. 3PLPs presently mainly contribute to the performances in IMT, theconsolidation and to the management of the carriers in the IMT. A 3PLP can furthermoreimprove the tracking information to improve the liability of intermodal transport since thisis not well developed in intermodal transport.

• 3PLPs are seen as potential facilitators of intermodal transport who will remove existingbarriers and hence make IMT more attractive. Potential future roles for 3PLPs are to actas Pan-European integrators and liability guarantors. The ‘Freight Integrator’ initiative asoutlined in the White Paper is in this respect a step in the right direction.

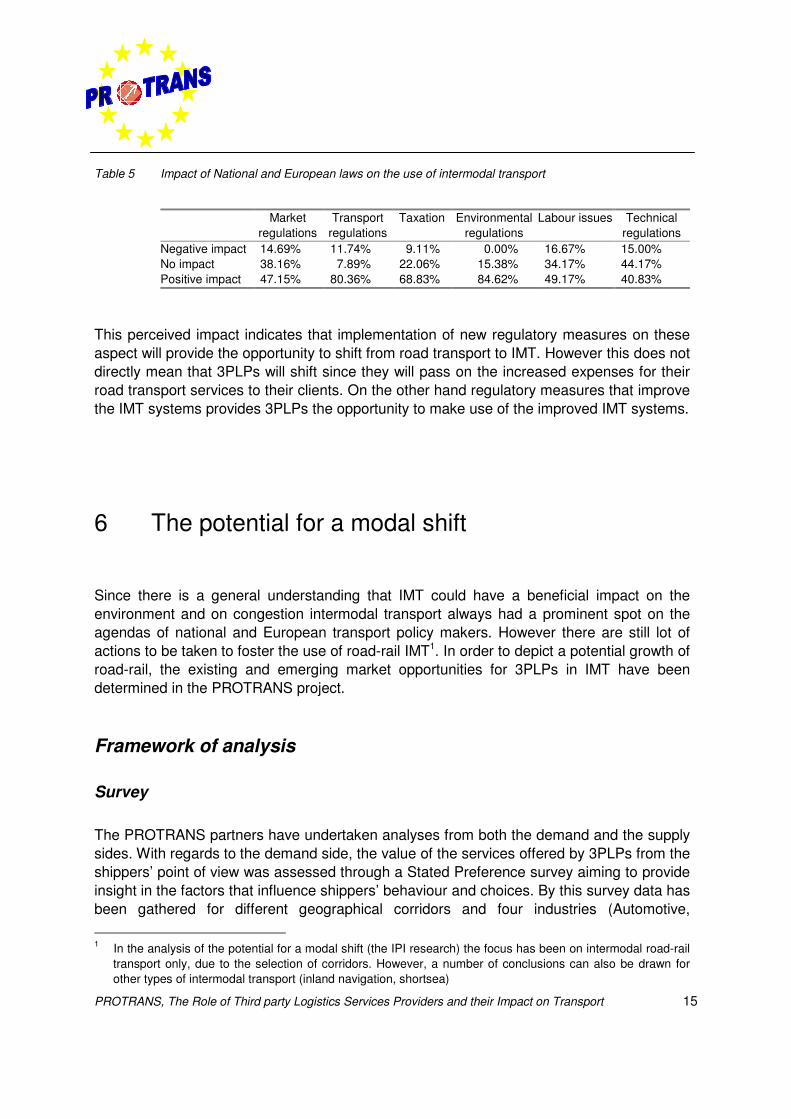

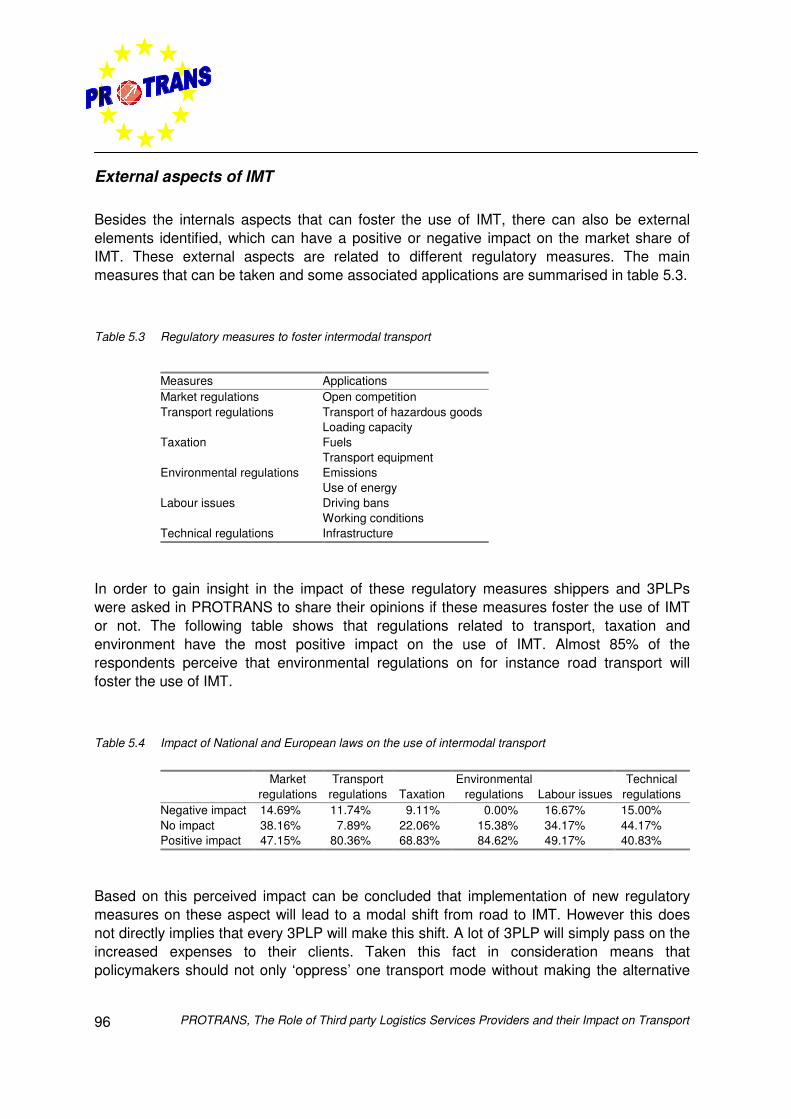

Finally the external aspects of IMT like regulatory measures provide opportunities that fosterthe use of IMT. Regulatory measures, like market regulations e.g. stimulation of opencompetition and transport regulations on for instance hazardous goods and loading capacityhave a positive effect on the use of IMT. This also applies for taxation, environmentalregulations and labour issues. Table 5 shows that regulations related to transport, taxationand environment have the most positive impact on the use of IMT. Almost 85% of therespondents perceive that environmental regulations on for instance road transport willfoster the use of IMT.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 15

Table 5 Impact of National and European laws on the use of intermodal transport

Marketregulations

Transportregulations

Taxation Environmentalregulations

Labour issues Technicalregulations

Negative impact 14.69% 11.74% 9.11% 0.00% 16.67% 15.00%No impact 38.16% 7.89% 22.06% 15.38% 34.17% 44.17%Positive impact 47.15% 80.36% 68.83% 84.62% 49.17% 40.83%

This perceived impact indicates that implementation of new regulatory measures on theseaspect will provide the opportunity to shift from road transport to IMT. However this does notdirectly mean that 3PLPs will shift since they will pass on the increased expenses for theirroad transport services to their clients. On the other hand regulatory measures that improvethe IMT systems provides 3PLPs the opportunity to make use of the improved IMT systems.

6 The potential for a modal shift

Since there is a general understanding that IMT could have a beneficial impact on theenvironment and on congestion intermodal transport always had a prominent spot on theagendas of national and European transport policy makers. However there are still lot ofactions to be taken to foster the use of road-rail IMT1. In order to depict a potential growth ofroad-rail, the existing and emerging market opportunities for 3PLPs in IMT have beendetermined in the PROTRANS project.

Framework of analysis

Survey

The PROTRANS partners have undertaken analyses from both the demand and the supplysides. With regards to the demand side, the value of the services offered by 3PLPs from theshippers’ point of view was assessed through a Stated Preference survey aiming to provideinsight in the factors that influence shippers’ behaviour and choices. By this survey data hasbeen gathered for different geographical corridors and four industries (Automotive, 1 In the analysis of the potential for a modal shift (the IPI research) the focus has been on intermodal road-rail

transport only, due to the selection of corridors. However, a number of conclusions can also be drawn forother types of intermodal transport (inland navigation, shortsea)

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport16

Chemicals, Fast Moving Consumer Goods and Steel). This data is related to transport offull-loads of non-hazardous and non-refrigerated goods. The Stated Preference surveyconsisted in 16 trade-offs between two alternatives (road-rail IMT and road transport).

Computation of the Intermodal Perception Index

Based on the gathered data for the industries, corridors and trade-offs of different actionvariables IMT, the potential market share of IMT can be computed via the IntermodalPerception Index (IPI). The IPI is the ratio of the potential market share of intermodaltransport (that can be reached by the application of a specific scenario), to the currentmarket share of intermodal transport.

Potential market share of Intermodal Transport IPI =

Current market share of Intermodal Transport

Strategies for 3PLPs on intermodal transport

Influence of 3PLPs on action variables

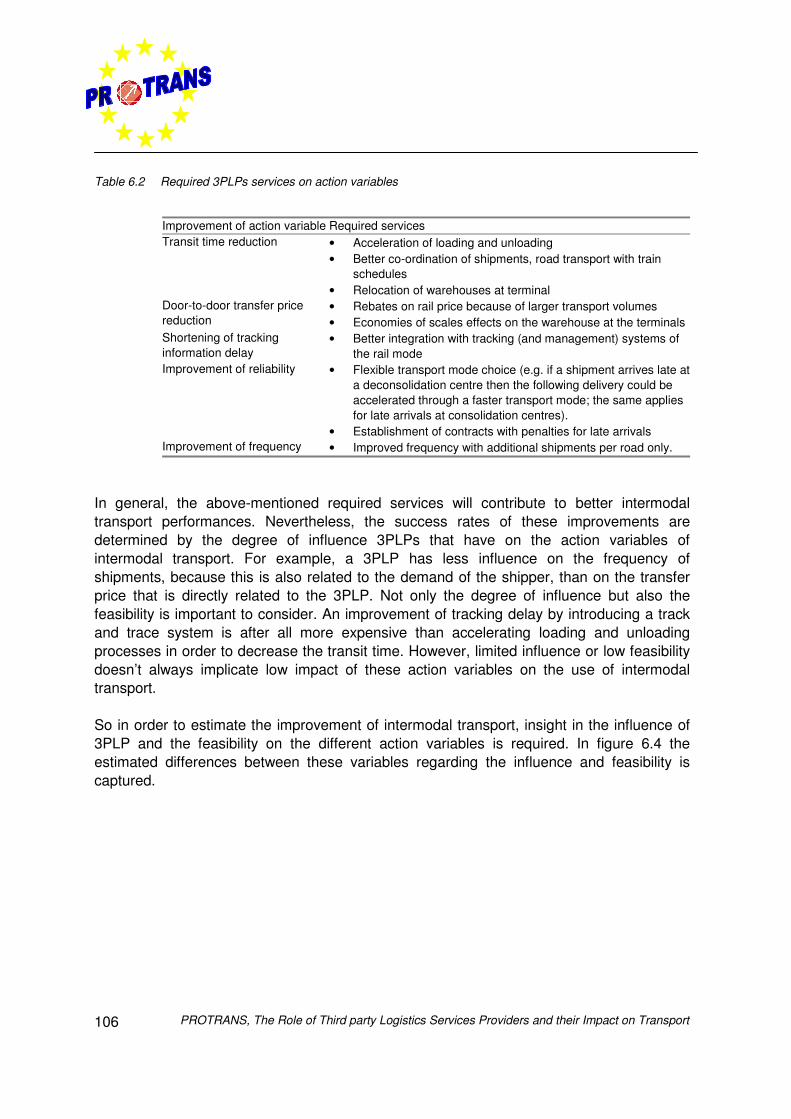

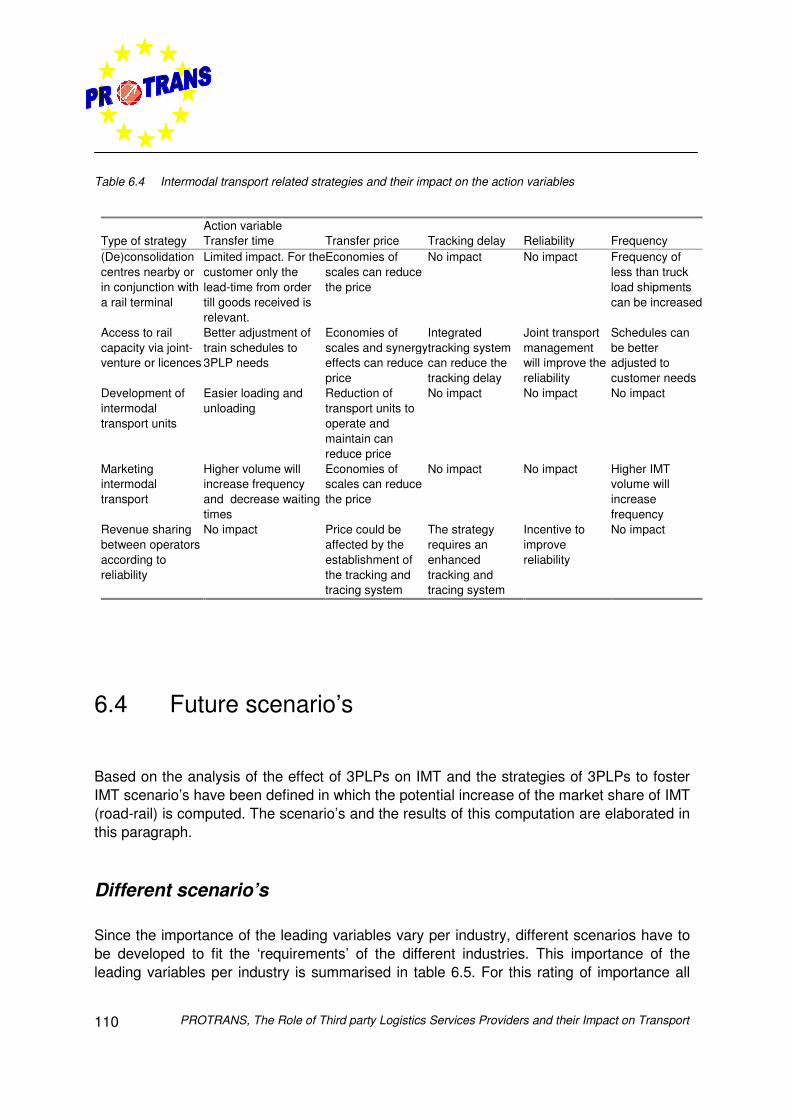

The potential growth of IMT depends on the degree in which action variables of IMT, liketransit time, transfer price or reliability is improved. This improvement is amongst othersdetermined by the influence of 3PLPs on these action variables. However 3PLPs can’tinfluence each action variable of IMT. For instance 3PLPs can’t impact the number ofshipments per year or the nature of goods (e.g. finished or semi-finished) since thesevariables are determined by the shipper. Hence, 3PLPs should develop strategies based onaction variables, which they can influence. In the following table a number of services arederived that can be offered by 3PLPs and which positively influence these action variables.

Table 6 Required 3PLPs services on action variables

Improvement of actionvariable Required servicesTransit time reduction • Acceleration of loading and unloading

• Better co-ordination of shipments, road transport with train schedules• Relocation of warehouses at terminal

Door-to-door transferprice reduction

• Rebates on rail price because of larger transport volumes• Economies of scales effects on the warehouse at the terminals

Shortening of trackinginformation delay

• Better integration with tracking (and management) systems of the rail mode

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 17

Improvement of actionvariable Required servicesImprovement ofreliability

• Flexible transport mode choice (e.g. if a shipment arrives late at a(de)consolidation centre then the following delivery could be accelerated througha faster transport mode)

• Establishment of contracts with penalties for late arrivalsImprovement offrequency

• Improved frequency with additional shipments per road only

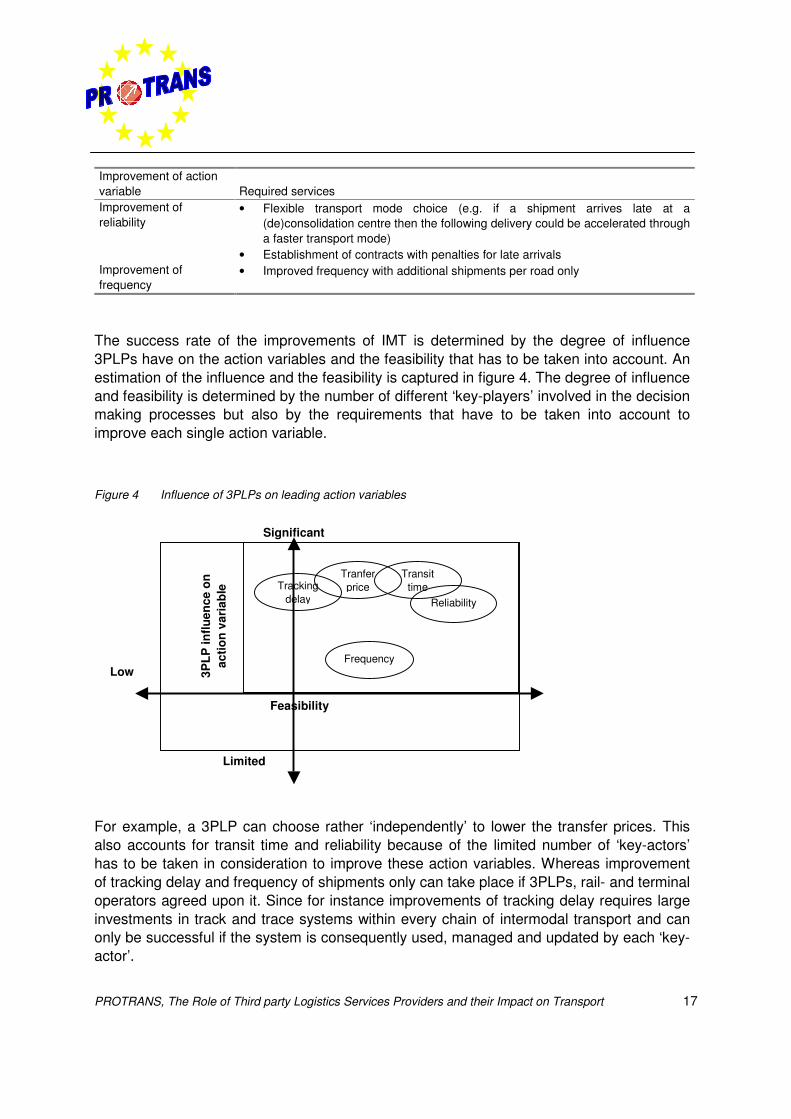

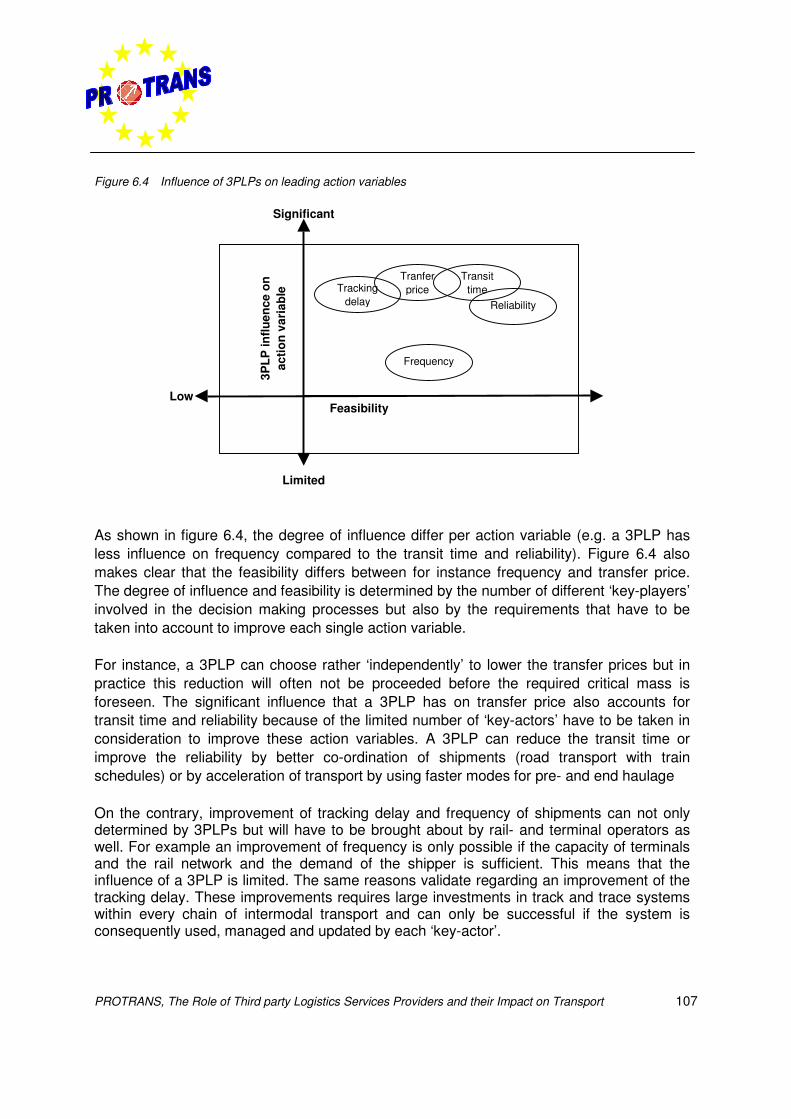

The success rate of the improvements of IMT is determined by the degree of influence3PLPs have on the action variables and the feasibility that has to be taken into account. Anestimation of the influence and the feasibility is captured in figure 4. The degree of influenceand feasibility is determined by the number of different ‘key-players’ involved in the decisionmaking processes but also by the requirements that have to be taken into account toimprove each single action variable.

Figure 4 Influence of 3PLPs on leading action variables

For example, a 3PLP can choose rather ‘independently’ to lower the transfer prices. Thisalso accounts for transit time and reliability because of the limited number of ‘key-actors’has to be taken in consideration to improve these action variables. Whereas improvementof tracking delay and frequency of shipments only can take place if 3PLPs, rail- and terminaloperators agreed upon it. Since for instance improvements of tracking delay requires largeinvestments in track and trace systems within every chain of intermodal transport and canonly be successful if the system is consequently used, managed and updated by each ‘key-actor’.

Significant

Limited

Transittime

TranferpriceTracking

delay Reliability

Frequency

Feasibility

3PLP

influ

ence

on

actio

n va

riab

le

Low

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport18

Strategies of 3PLPs on intermodal transport

In order to foster the use of road-rail 3PLPs can implement IMT related strategies. Thesestrategies have been derived from interviews with stakeholders in logistics and have beenvalidated through discussion with 3PLPs already performing intermodal transport. The mainstrategy or strategies, which a 3PLP can follow, are:

• Logistic centres for (de)consolidation nearby or in conjunction with a railterminal: Efficient rail transport requires that full truckloads are shipped. However, theshare of full truck on the overall transport volume is decreasing – especially for theautomotive sector – and thus a consolidation or deconsolidation of less than truckloadshipments is necessary. Hence, a 3PLP has to provide such services at a logisticcentre on the location or nearby a rail terminal. Furthermore, the 3PLP has to performadditional services like warehousing or light assembly on these logistic centres.

• Access to rail capacity: A 3PLP can undertake a joint venture with a rail operator inorder to offer better services for customers. Such a close co-operation can improve theoverall performance. Another option is to license 3PLPs and shippers for rail transport.

• Development of intermodal transport units: Intermodal transport requires thattransport units are easy to load and unload from road to rail and vice versa. Currently, avariety of transport units exists for this purpose. Standardisation and broad applicationof transport units suitable for IMT is necessary to improve the IMT market share.

• Marketing intermodal transport: Currently, the possibilities of intermodal transportare not well known by customers. IMT has often a negative image. Thus activemarketing is needed to increase the IMT share of the overall transport volume.

• Revenue sharing between operators according to reliability: Sharing the transportrevenues between rail operators according to the reliability of delivery services. Thesystem could be based on a monitoring system involving GPS transmitters embarkedon a sample of containers.

Scenarios on Intermodal transport

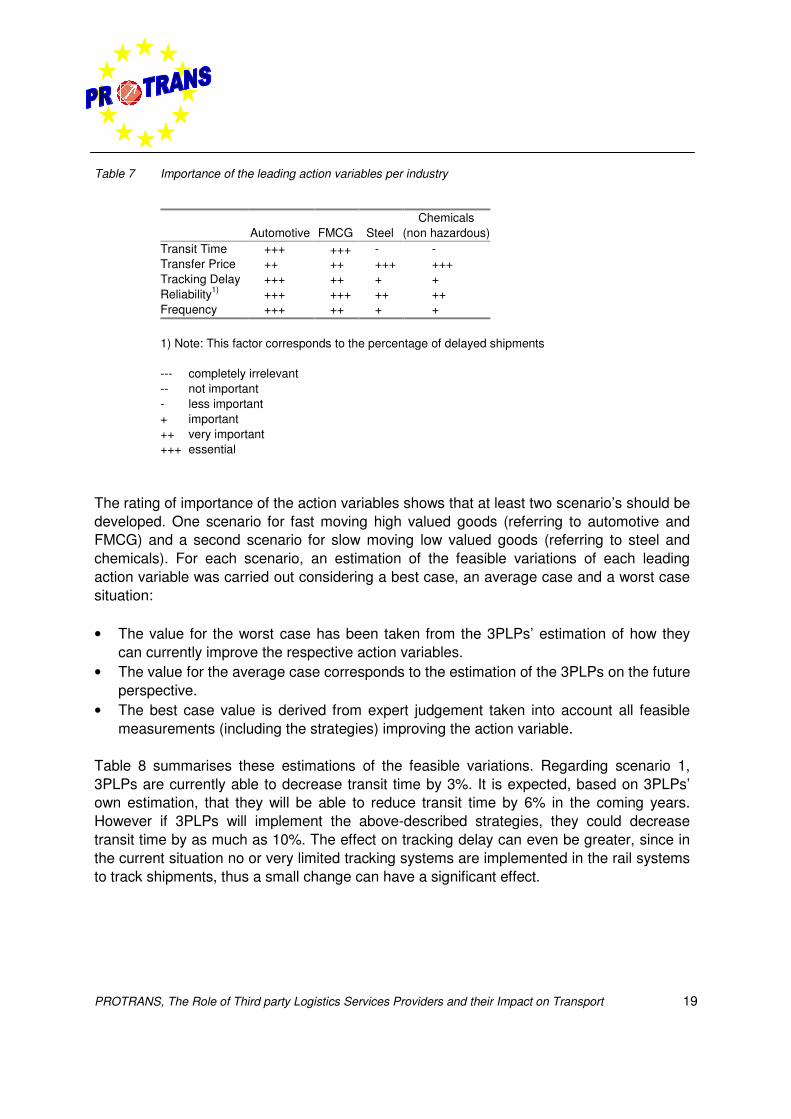

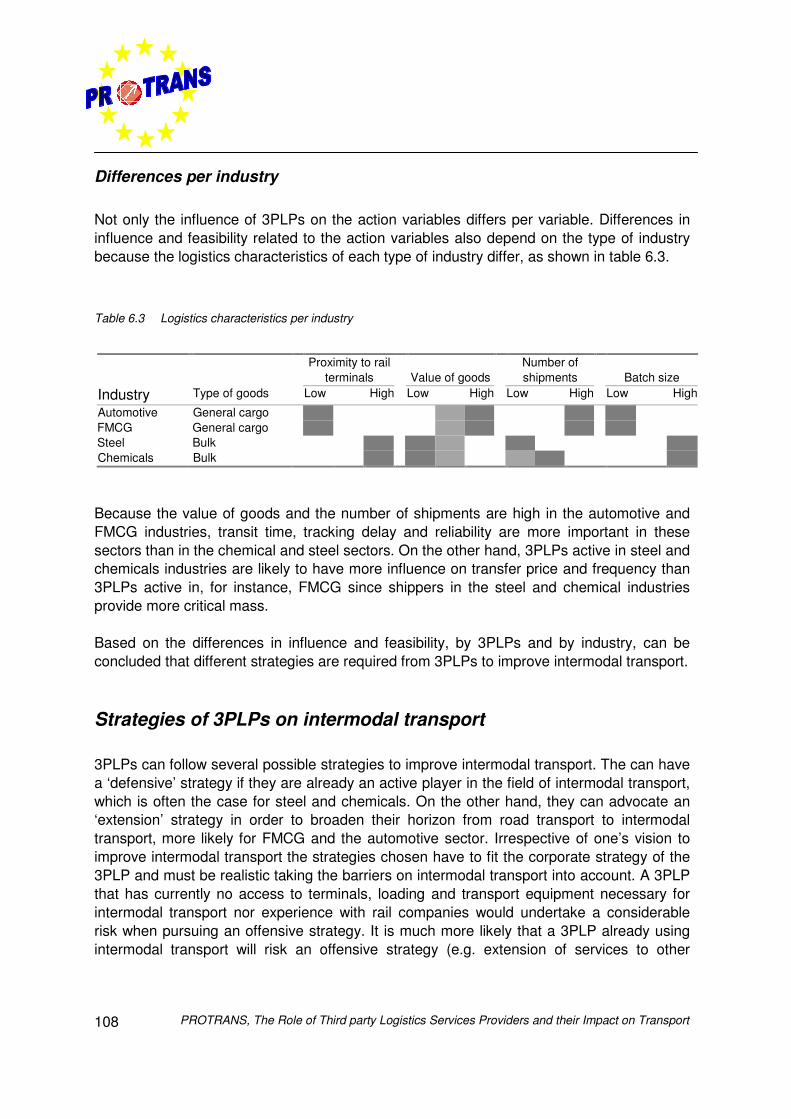

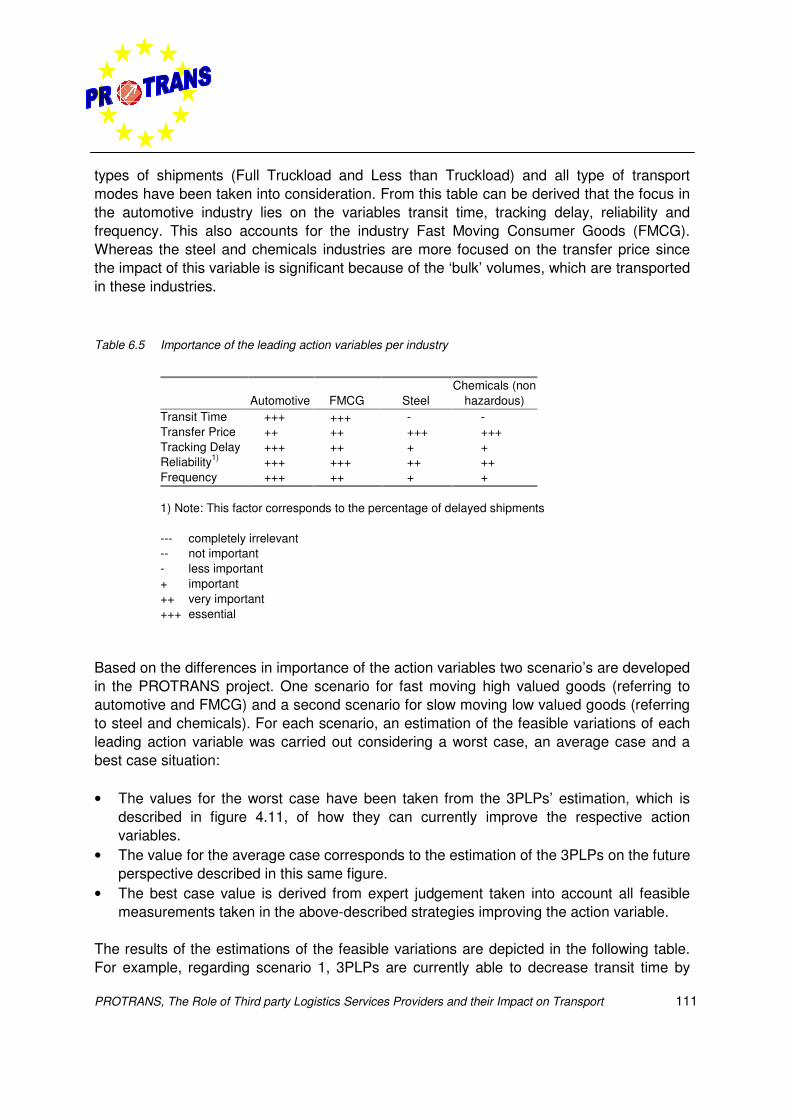

Since the value of goods and the number of shipments are high in the automotive andFMCG industries, transit time, tracking delay and reliability are more important in thesesectors than in the chemical and steel sectors. Whereas, 3PLPs active in steel andchemicals are likely to have more influence on transfer price and frequency since thesesectors are characterised by bulk because of the high batch sizes in production anddistribution. Hence, the importance of the leading variables varies per industry. Table 7depicts the rating of importance all types of shipments (Full Truckload and Less thanTruckload) and all type of transport modes per type of industry.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 19

Table 7 Importance of the leading action variables per industry

Automotive FMCG SteelChemicals

(non hazardous)Transit Time +++ +++ - -Transfer Price ++ ++ +++ +++Tracking Delay +++ ++ + +Reliability1) +++ +++ ++ ++Frequency +++ ++ + +

1) Note: This factor corresponds to the percentage of delayed shipments

--- completely irrelevant-- not important- less important+ important++ very important+++ essential

The rating of importance of the action variables shows that at least two scenario’s should bedeveloped. One scenario for fast moving high valued goods (referring to automotive andFMCG) and a second scenario for slow moving low valued goods (referring to steel andchemicals). For each scenario, an estimation of the feasible variations of each leadingaction variable was carried out considering a best case, an average case and a worst casesituation:

• The value for the worst case has been taken from the 3PLPs’ estimation of how theycan currently improve the respective action variables.

• The value for the average case corresponds to the estimation of the 3PLPs on the futureperspective.

• The best case value is derived from expert judgement taken into account all feasiblemeasurements (including the strategies) improving the action variable.

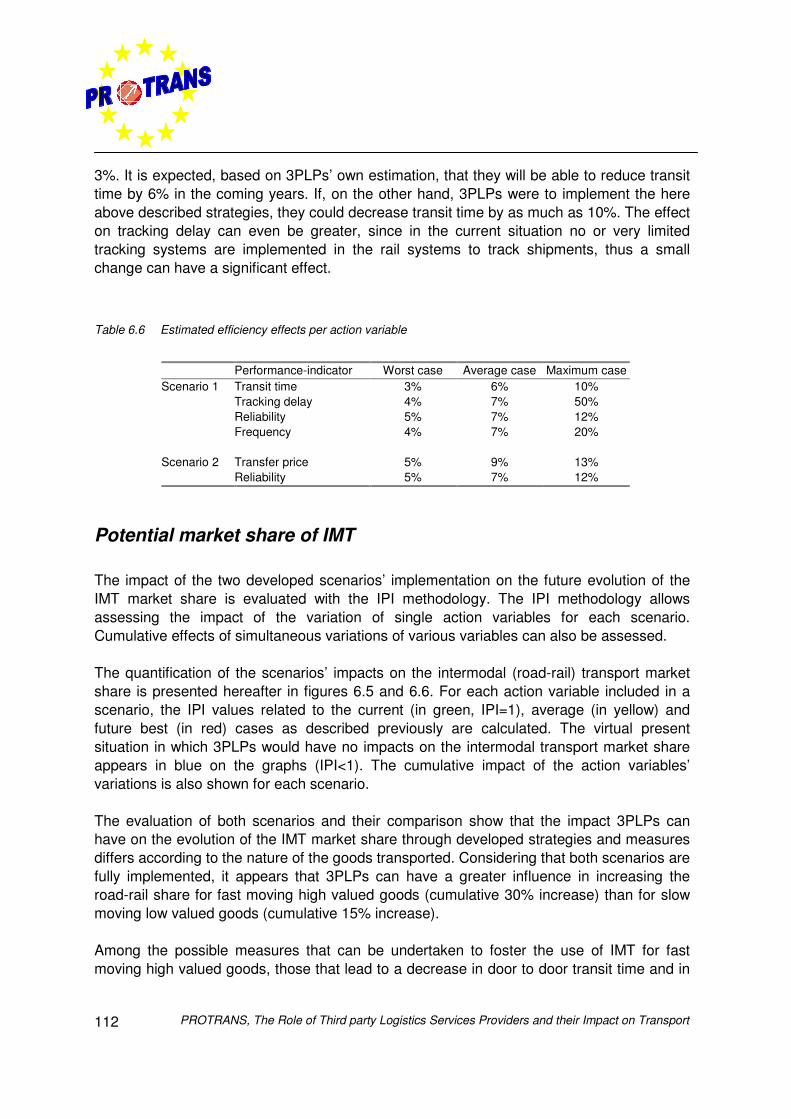

Table 8 summarises these estimations of the feasible variations. Regarding scenario 1,3PLPs are currently able to decrease transit time by 3%. It is expected, based on 3PLPs’own estimation, that they will be able to reduce transit time by 6% in the coming years.However if 3PLPs will implement the above-described strategies, they could decreasetransit time by as much as 10%. The effect on tracking delay can even be greater, since inthe current situation no or very limited tracking systems are implemented in the rail systemsto track shipments, thus a small change can have a significant effect.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport20

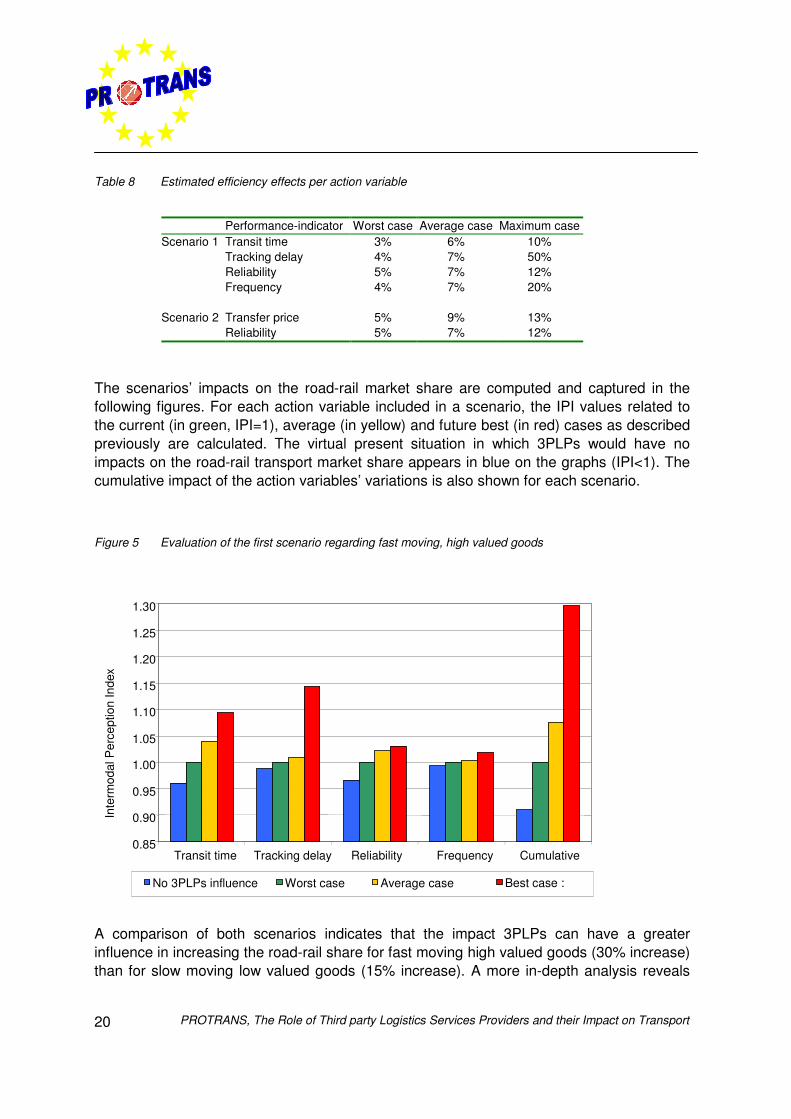

Table 8 Estimated efficiency effects per action variable

Performance-indicator Worst case Average case Maximum caseScenario 1 Transit time 3% 6% 10%

Tracking delay 4% 7% 50%Reliability 5% 7% 12%Frequency 4% 7% 20%

Scenario 2 Transfer price 5% 9% 13%Reliability 5% 7% 12%

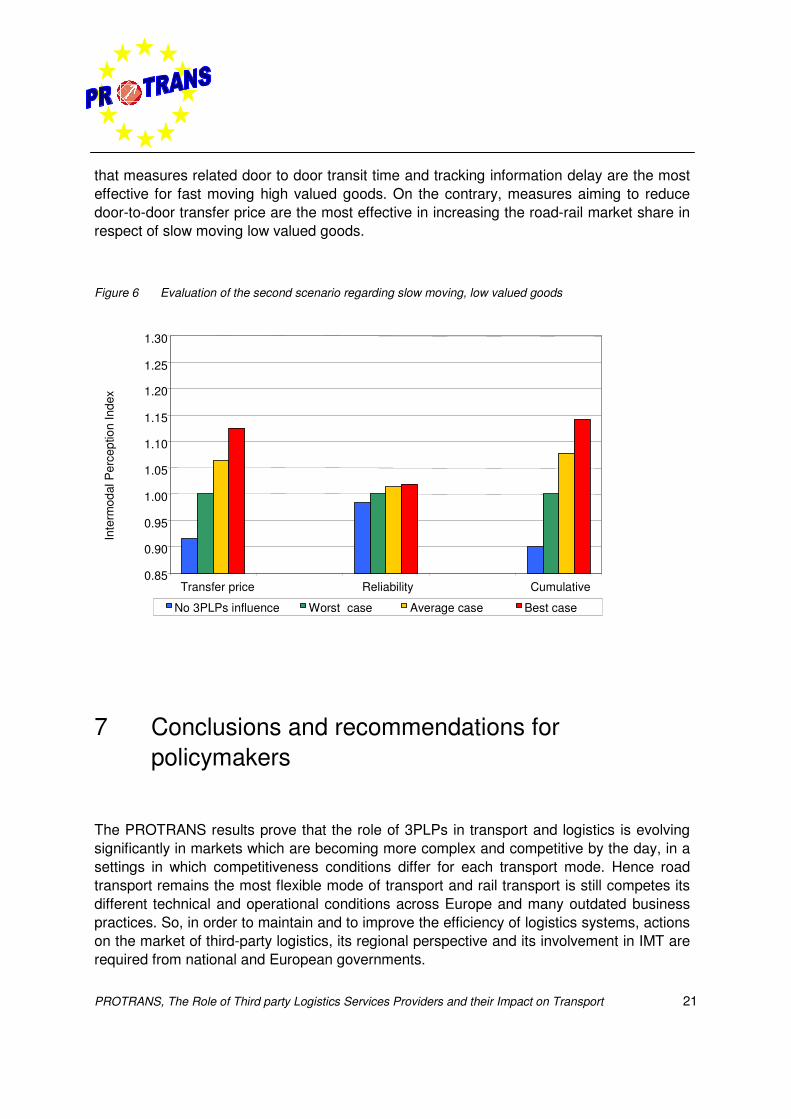

The scenarios’ impacts on the road-rail market share are computed and captured in thefollowing figures. For each action variable included in a scenario, the IPI values related tothe current (in green, IPI=1), average (in yellow) and future best (in red) cases as describedpreviously are calculated. The virtual present situation in which 3PLPs would have noimpacts on the road-rail transport market share appears in blue on the graphs (IPI<1). Thecumulative impact of the action variables’ variations is also shown for each scenario.

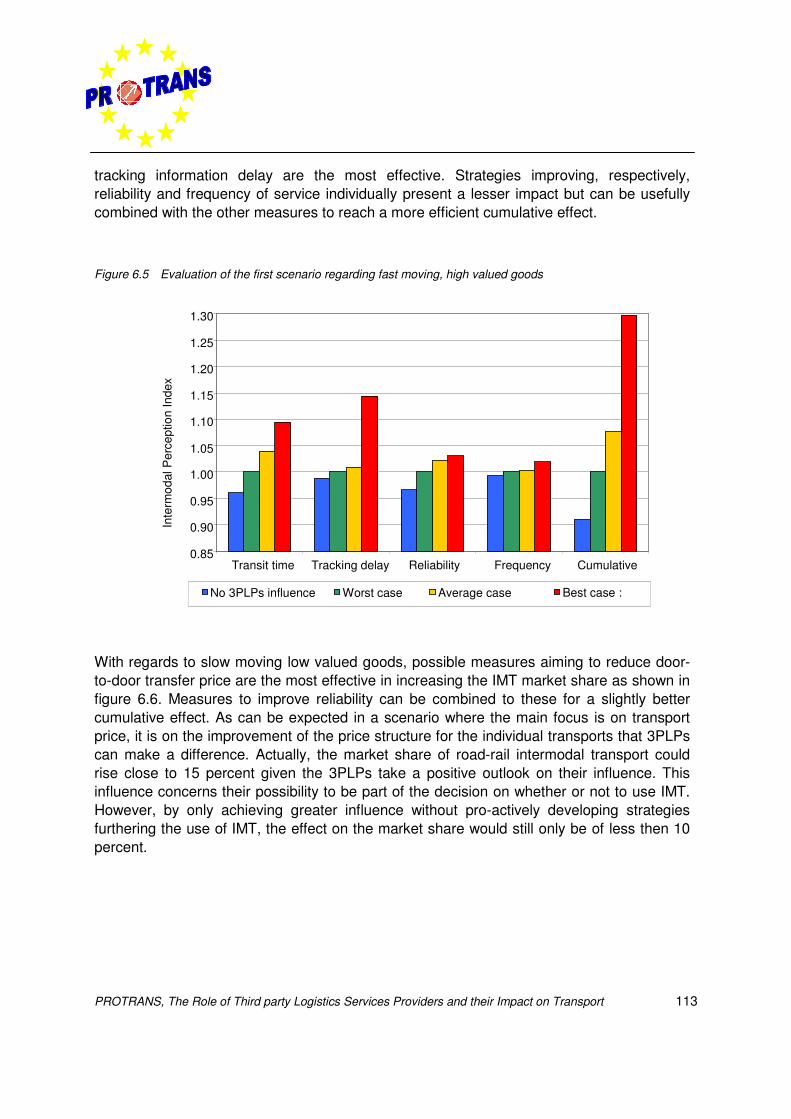

Figure 5 Evaluation of the first scenario regarding fast moving, high valued goods

A comparison of both scenarios indicates that the impact 3PLPs can have a greaterinfluence in increasing the road-rail share for fast moving high valued goods (30% increase)than for slow moving low valued goods (15% increase). A more in-depth analysis reveals

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Transit time Tracking delay Reliability Frequency Cumulative

Inte

rmod

al P

erce

ptio

n In

dex

No 3PLPs influence Worst case Average case Best case :

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 21

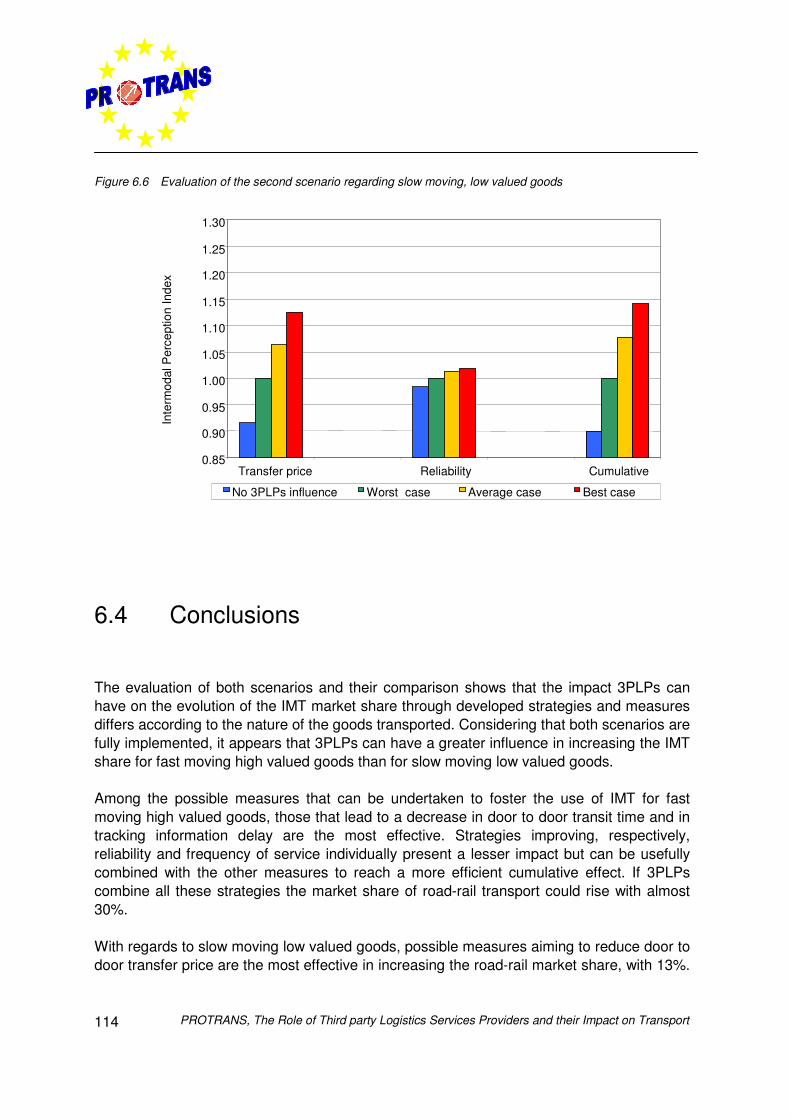

that measures related door to door transit time and tracking information delay are the mosteffective for fast moving high valued goods. On the contrary, measures aiming to reducedoor-to-door transfer price are the most effective in increasing the road-rail market share inrespect of slow moving low valued goods.

Figure 6 Evaluation of the second scenario regarding slow moving, low valued goods

7 Conclusions and recommendations forpolicymakers

The PROTRANS results prove that the role of 3PLPs in transport and logistics is evolvingsignificantly in markets which are becoming more complex and competitive by the day, in asettings in which competitiveness conditions differ for each transport mode. Hence roadtransport remains the most flexible mode of transport and rail transport is still competes itsdifferent technical and operational conditions across Europe and many outdated businesspractices. So, in order to maintain and to improve the efficiency of logistics systems, actionson the market of third-party logistics, its regional perspective and its involvement in IMT arerequired from national and European governments.

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Transfer price Reliability Cumulative

Inte

rmod

al P

erce

ptio

n In

dex

No 3PLPs influence Worst case Average case Best case

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport22

These actions are not only required from the 3PL market and policies point of few, butshould also be seen in the context of the EU-enlargement and the current economicdownturn. Since the enlargement will influence logistics and transport flows, the networks inthe new member countries should be assessed to ensure network uniformity in theEuropean Union. Furthermore the current economic downturn should be taken inconsideration as well because this downturn might lead to the postponement of necessaryinvestments in IMT by both 3PLPs and operators.

Summarised can be stated that the Commission should take the initiative where regulatoryor legal measures are concerned and where intermodality depends on co-ordination atEuropean level. In this respect the Commission already has set various policy objectivesacross the different policy areas, which are convergent in their goals towards thecommunity’s transport policy i.e. the sustainability of the entire transport system. Theseobjectives have been supported by political documents the most important ones being thehere above described Commission’s White and Green Papers and Directives.

Guiding principles

To facilitate the increasing role of 3PLPs in transport systems and to IMT, Europeanpolicymakers should take action in the next few years. These actions should be based onfour common principles:

• Logistics integration: Integration of logistics systems provides the opportunity tooptimise the intermodal chain management and enables to inform the shipper and3PLPs. Hence unified communication systems for data exchanges are required.

• Effective tariff integration: Integration of all tariffs of the different services in IMT toone single ticket that is provided by one single point of contact facilitates an easier useof the IMT system.

• Administrative integration: An effective administrative integration, by means of anintegrated intermodal Bill of Lading (B/L), allows to overcome problems derived fromdealing with a number of different transport modes and their correspondent cargodocuments.

• Physical integration: Providing seamless connection between two consecutive stagesof the trip enables to benefit from the advantages of each transport mode.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 23

Recommendations for policy actions

In the Commission’s White and Green Papers and Directives a lot of initiatives to facilitatethe increasing role of 3PLPs and to improve IMT are already depicted. However, based onthe PROTRANS project the following actions should be taken by the Europeanpolicymakers.

Improving logistics regions

Policymakers can and should align infrastructure plans on different levels, from European toregional level, in order to improve the transport connections, which makes efficientconsolidation of goods possible in and between regions. But they should also stimulateintegrated logistics strategies in regions, in which public and private partners participate.

Improving of railways

The greatest challenge is to liberalise the railway markets, allowing e/g the access forrailway operations to parties other than traditional railway companies, amongst others3PLPs, in order to develop a more efficient, competitive and reliable IMT system in Europe.

However policymakers should also improve the rail infrastructure. New infrastructureinvestments are required since duration of the trip, price, tracking and tracing and reliabilityare the key variables that have a strong impact on the potential market share of IMT.

In order to improve the railways, policymakers should furthermore develop an integratedinfrastructure pricing policy. An integrated infrastructure pricing policy across EU memberStates might rise the contributions of the different transport modes towards sustainabledevelopment and help 3PLPs choose the most suitable transport mode on a morerepresentative economic basis.

However, pricing policies do not imply a legacy that 3PLPs will shift from road to road-rail,since they will simply pass on the increased expenses to their clients. Hence policymakersshould not only ‘oppress’ road transport mode without making the alternative (IMT) morecompetitive. Policymakers could for instance increase the liability of IMT through stimulationof tracking systems or improve the integrated IMT services by ‘facilitating’ the logisticsmarket to realise the role of Pan European integrator.

Regarding railways, European policymakers should finally promote an independentcertification organisation, which is charged to certify the quality of service of intermodaloperators, in order to realise sharing the transport revenue between rail operators.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport24

Development of transfer points between modes

In order to develop transfer points between transport modes policymakers should promoteefficient transfer locations, by creating for instance investment incentives. But alsopromotion of freight villages will facilitate the development of transfer points. The advantageof these freight villages lies in the possibility to consolidate transport flows from differentorigins into bulk flows required for efficient use of IMT. At last the development of anIntegrated Logistic Master Plan should stimulate 3PLPs and shippers to locate on theselarge freight villages in order to consolidate flows.

Harmonisation of regulations

In order to foster the use of IMT by 3PLPs, EU Members States should harmonise theirregulations on intermodal transport units, carrier liability, labour and data processing. Firstof all standardisation of some characteristics of intermodal units (containers and swapbodies) is required to overcome delays in handling. A second aspect that needs to beharmonised is the carrier liability in order to be able to offer IMT clients a clear set ofcoherent, comprehensive and transparent liability conditions. Furthermore harmonisation oflabour conditions is an important rule of competition. Finally the Commission could providea legal framework on intermodal real-time electronic information systems to achieve dataprocessing systems and closer integration through the whole supply chain.

Marketing of intermodality

IMT should be marketed better. The European Commission and European organisationsand associations should facilitate information-related initiatives to improve overallawareness amongst shippers of IMT. The Commission should also promote educationinitiatives to expanding know-how and specialised skills on IMT amongst 3PLPs.

Evaluate intermodal processes

The last action that the European policy should take is the development of the criteria forassessing the impact of IMT on the environment, employment and social and regionaldevelopment. Hence further research should be encouraged to collect data on IMT on arevolving bases. This requires co-operation in data collection and data monitoring bydifferent Directorate Generals (e.g. DG Enterprise, DG Environment) and co-ordination byDG TREN.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 25

Chapter 1 Introduction

1.1 Background and definitions

Third party logistics service providers (3PLPs) become increasingly important because mostcompanies seek to outsource logistics tasks. However, 3PLPs perform their services formany different clients. Thus a simple outsourcing approach of the given structures (i.e.,operating existing warehouses and transport means for each customer separately) will notresult in overall optimised logistics networks. Hence, a 3PL must have a betterunderstanding how to organise their networks and on how to supply added value serviceswhich have greater complexity compared to the ‘traditional’ simple forwarding services.

The major 3PLPs are faced with a number of problems and challenges:

• They have to locate their scope in terms of services offered to shippers.• They have to extend their geographical coverage, offering a really pan-European

service.• They have to organise their network, combining the unique selling points of partners.• They have to offer a variety of transport options, including the use of intermodal

transport.• They have to optimise their transport processes with the aim of decoupling the rise of

economic growth from the rise of transport volume (reducing the negative effect on theenvironment).

• They have to supply additional services to their customers including the operation andmanagement of complex distribution/supply structures for their customers.

Although a lot of information has been gathered in the past couple of years, the impact androle of 3PLPs on transport, especially on intermodal transport on a European scale, still hasto be made. Also, a structured analysis of the main logistics regions and the reasons of theirsuccess hasn’t been carried out at a European level so far. In addition, there has beensome research on the perception of shippers regarding the use of intermodal transport, butnot from the 3PLP point of view.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport26

Within the 5th Framework Programme, a specific task has been dedicated to this role of3PLP and their impact on transport. Main objectives of this task are:

• map and analyse (SWOT-analysis) the European 3PLPs market;• detail the most important challenges and determine barriers, success and failure factors;• assess the future importance of intermodal transport for the strategies of 3PLPs

To meet this task and to fill-in these objectives a group of companies (consulting firms,research organisations and universities, have formed a consortium that has designed thePROTRANS proposal. The main goal of the PROTRANS project is to identify the mostimportant challenges, to determine barriers, success and failure factors and to assess thefuture importance of intermodal transport for the strategies of 3PLPs on a European level. Inother words to determine the role of 3PLPs and their impact on transport.

The PROTRANS project is carried out by order of the European Commission in the periodJanuary 2000 and December 2002, the following project partners participate:

• Buck Consultants International (BCI)• Cranfield University (CU)• Zentrum für Logistik und Unternehmungsplanung GmbH (ZLU)• Fraunhofer Institut Materialfluss und Logistik (IML)• Ecorys Transport (NEI)• Stratec S.A. (SC)• PTV Planung Transport Verkehr A.G. (PTV)• Linköping Universitet (LU)• Technische Universität Berlin (TUB)• Environment, Transport & Planning (ETP)• Louis Berger S.A. (LB)

The first project partner BCI is also the overall co-ordinator of the project.

1.2 Objectives of PROTRANS

As described above the main goal of the PROTRANS project is to determine the role of3PLPs and their impact on transport on a European level. Derived from this main goal, thefollowing research objectives of the PROTRANS project can be listed:

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 27

• Development of a theoretical framework for an analysis of the 3PLP market in Europe;• Description/mapping of scope (a/o. sector specialisation, business sectors of clients,

output volumes, geographical coverage network and transport options and important3PLPs in Europe, including a business profile;

• Identification of 15 main logistics regions in Europe, where a concentration of 3PLps canbe found, in conjunction with a node position in infrastructure networks and the mainEuropean networks;

• Analysis of the reasons why these regions have become successful as logistics hubs;• Analysis of present and future requirements (scope, course, network, transport options)

of 50 leading shippers operating on a European scale;• Review of the services offered by 3PLPs as an answer to the requirements posed;• Analysis of the existing barriers at leading 3PLPs to develop pan-European integrated

logistics serves;• Computation of the Intermodal Perception Index;• Integration of results on intermodal market demands, 3PLP perception and 3PLP future

strategies;• Defining of recommendations and actions;• Dissemination of project results.

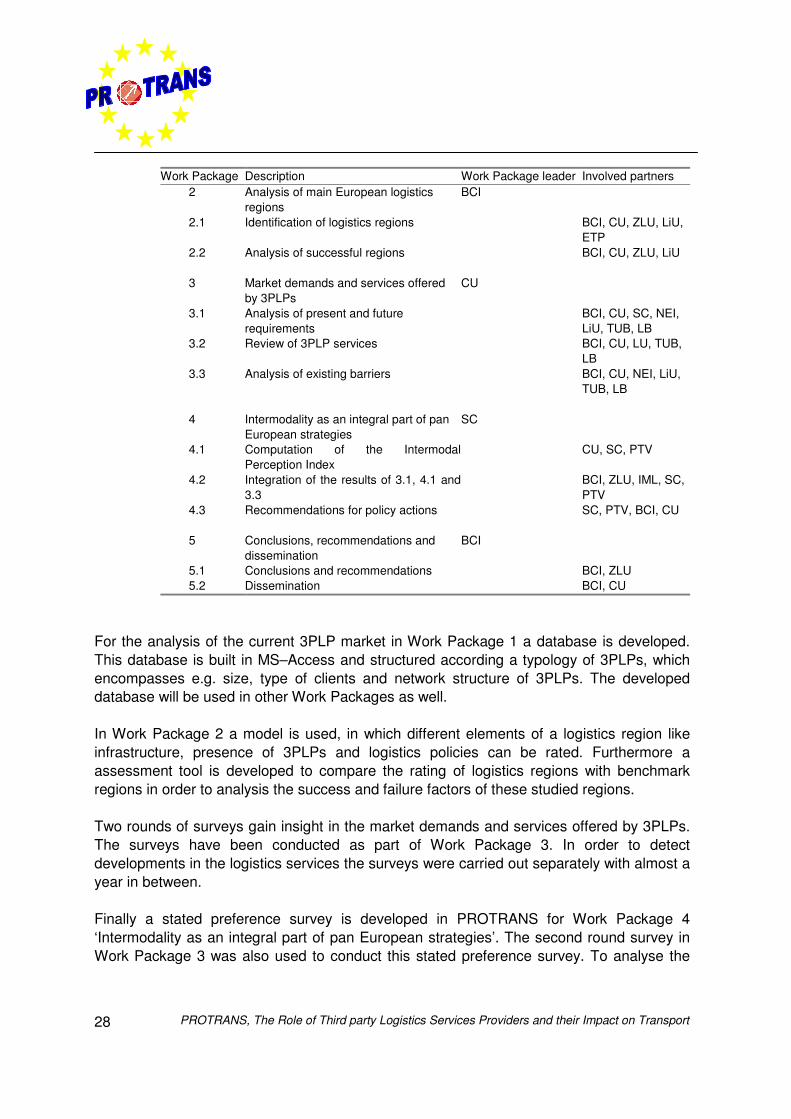

1.3 Methodological approach

In order to meet the objectives of the PROTRANS project five different Work Packageshave been defined with the following research activities, which are mentioned in table 1.1.In annexe 1 a description of each Work Package is provided. This table below alsodescribes the involved project partners.

Table 1.1 Activities per Work Package

Work Package Description Work Package leader Involved partners0 Project Management BCI All partners

1 Analysis of the 3PL market NEI1.1 Analysis of the 3PL market in Europe CU, IML, NEI, LiU,

ETP1.2 Mapping most important 3PLPs CU, IML, NEI, LiU,

ETP

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport28

Work Package Description Work Package leader Involved partners2 Analysis of main European logistics

regionsBCI

2.1 Identification of logistics regions BCI, CU, ZLU, LiU,ETP

2.2 Analysis of successful regions BCI, CU, ZLU, LiU

3 Market demands and services offeredby 3PLPs

CU

3.1 Analysis of present and futurerequirements

BCI, CU, SC, NEI,LiU, TUB, LB

3.2 Review of 3PLP services BCI, CU, LU, TUB,LB

3.3 Analysis of existing barriers BCI, CU, NEI, LiU,TUB, LB

4 Intermodality as an integral part of panEuropean strategies

SC

4.1 Computation of the IntermodalPerception Index

CU, SC, PTV

4.2 Integration of the results of 3.1, 4.1 and3.3

BCI, ZLU, IML, SC,PTV

4.3 Recommendations for policy actions SC, PTV, BCI, CU

5 Conclusions, recommendations anddissemination

BCI

5.1 Conclusions and recommendations BCI, ZLU5.2 Dissemination BCI, CU

For the analysis of the current 3PLP market in Work Package 1 a database is developed.This database is built in MS–Access and structured according a typology of 3PLPs, whichencompasses e.g. size, type of clients and network structure of 3PLPs. The developeddatabase will be used in other Work Packages as well.

In Work Package 2 a model is used, in which different elements of a logistics region likeinfrastructure, presence of 3PLPs and logistics policies can be rated. Furthermore aassessment tool is developed to compare the rating of logistics regions with benchmarkregions in order to analysis the success and failure factors of these studied regions.

Two rounds of surveys gain insight in the market demands and services offered by 3PLPs.The surveys have been conducted as part of Work Package 3. In order to detectdevelopments in the logistics services the surveys were carried out separately with almost ayear in between.

Finally a stated preference survey is developed in PROTRANS for Work Package 4‘Intermodality as an integral part of pan European strategies’. The second round survey inWork Package 3 was also used to conduct this stated preference survey. To analyse the

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 29

intermodality of 3PLPs the results of the stated preference survey have been used to ‘fill’ amodel that can calculate the potential market share of intermodal transport.

1.4 Report structure

The results of Work Packages 1 till 4 are captured in this final deliverable of thePROTRANS project. Since concepts like 3PLPs and supply chain management are relevantfor the total project, the main definitions are described in the following chapter, chapter 2.This chapter also provides a snapshot of the 3PLP market in Europe.In the third chapter 13 logistics regions are identified and analysed why some regionsbecome successful and why some others don’t.

Chapter 4 provides insight in the shippers’ and 3PLPs’ views on present and future marketdemands on logistics and transport systems in Europe. This accounts not only roadtransport but also intermodal transport. Furthermore this chapters describes how thesedemands are and will be facilitated by 3PLPs.

In the current situation of the market demands of logistics services barriers andopportunities for further outsourcing of logistics and intermodal transport can be identified.The fifth chapter of this deliverable describes these barriers and opportunities.

Not only the existing and emerging market opportunities for 3PLPs in intermodal transportare determined in the PROTRANS project. This deliverable also describes a potentialmarket share of intermodal transport. To realise this market share improvements strategiesin this mode of transport are required. In chapter 6 the analysis of the potential marketshare and its requirements are elaborated.

Finally the overall conclusions are captured in chapter 7. Based on these conclusionsrecommendations have been derived for policy actions on the 3PL market and onintermodal transport.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport30

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 31

Chapter 2 Third-party logistics marketoverview

2.1 Introduction and definitions

The third-party logistics market is becoming more complex. Success in this market isdetermined by the speed with which a supply chain adapts to changes in customerdemands, emerging distribution channels and new product introductions. In this chapter themarket of third-party logistics providers (3PLPs) in Europe is described. Before defining a3PLP in more detail, it is important to know what definitions of logistics and supply chainmanagement are taken into account in the PROTRANS project. For these definitions use ismade of the results of the TRILOG project (1999).

Definition of logistics

Based on the operational definition of logistics as used in the TRILOG project anddeveloped by the Council of Logistics Management, the definition of logistics used in thePROTRANS project is:

"Logistics is that part of the process that plans, implements, and controls theefficient, effective flow and storage of goods, services, and related information fromthe point of origin to the point of consumption in order to meet customers'requirements."

Regarding this definition the following remarks should be taken in consideration:

• The point of origin refers to a certain point in the supply chain from where the productsare transported. This point is not a fixed point when compared between different supplychains, but can be different according to the process that is analysed: a “movableorigin”.

• Financial activities, computing services and other activities that contribute to the supplychain, and have to be processed from origin to consumption, could enter the definition of

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport32

logistics. However, they are regarded as part of the term “services” in the definitionabove.

• Logistics can be applied to various scales (ranging from small production cells overlarge enterprises up to international domains).

• Implementing does not necessary imply physical action (such as transportation,warehousing, i.e.) but rather refers to the process of carrying out the defined plan.

Definition of supply chain management

Logistics management is an integrative process that seeks to optimise the flow of materialsand supplies through the organisation to the customer. If all firms involved in a particularsupply chain optimise their logistical systems independently of other firms in that chain themanagement of product flow across the whole chain, or ‘pipeline’, is likely to be sub-optimal.Attempts to overcome this problem have resulted in the creation of ‘supply chainmanagement’, in which the logistics activities are synchronised crossing geographical andorganisational boundaries. In PROTRANS the following definition of supply chainmanagement is used.

“Supply Chain Management (SCM) extends the principles of logistics acrossenterprise boundaries.”

Definition of Third-party logistics service provider (3PLP)

In the last decade many definitions of 3PL have been written. These definitions differ from‘outsourcing logistics functions’ to ‘strategic alliances in which shipper and provider bothwork on the best possible logistics solutions’. Several definitions that can be found in recentliterature are elaborated in annexe 2. Based on these definitions, for the PROTRANSproject the following definition of Third-party logistics has been selected:

Third-party logistics (3PL) are activities carried out by an external company on behalfof a shipper and consisting of at least the provision of management of multiplelogistics services. These activities are offered in an integrated way, not on a stand-alone basis. The co-operation between the shipper and the external company is anintended continuous relationship.

The shipper refers to the party that either sends or receives the goods; the source ordestination of the goods. External implies that the company is not being a subsidiarycompany in an exclusive unilateral relationship with the shipper (mother company). Basedon the above definition it can be stated that a 3PLP is a company who provides Third-partylogistics.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 33

Lately 4PL (Fourth-party logistics) have appeared in literature in connection to third partylogistics. This is originally a name for an Arthur Andersen consulting, which is starting to beused by different industry actors. Andersen define 4PL as: “a supply chain integrator thatassembles and manages the resources, capabilities, and technology of its ownorganisation with those of complementary service providers to deliver acomprehensive supply chain solution.” 4PL is normally connected to solution generatingand non-asset based providers or in more popular terms as a 3PL without an asset base.The 4PL term is not used in the 3PL typology as explained in this deliverable, as it is notlogically deductible from the construction of the term 3PL. However the focused issuesbehind 4PL are considered by the academically much more established positioningdimensions standardisation versus solution and asset based versus non-asset based.

Definition of intermodal transport

Since an element of the objective of the PROTRANS project is to point out the mostimportant challenges to intermodal transport (IMT) in relation to logistics and to assess theimportance of intermodal transport for the strategies of 3PLPs, it is important to know whichdefinition of intermodal transport is used in the PROTRANS project.

There are different definitions of intermodal transport and the related concepts of combinedtransport and multimodal transport. The ECMT (European Conference of Ministers ofTransport) and the European Committee for standardisation (CEN) use the followingdefinition for intermodal transport:

“Intermodal transport is the movement of goods in one and the same loading unit orvehicle, which uses successively several modes of transport without handling of thegoods themselves in changing modes.”

The ‘working definition’ used in the PROTRANS project is the same as the EC definition ofintermodal transport, which goes beyond the ECMT/CEN definition, and corresponds withthe ECMT/CEN definition of multimodal transport:

“Multimodal Transport is the movement of goods whereby at least two differentmodes are used in a door-to-door transport chain.”

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport34

2.2 Typology of the logistics service provider

With the main definitions being set, the next step is to develop a proper structure for 3PLPs.The purpose of the typology used in the PROTRANS project is to classify the 3PLPs for theanalysis of the 3PLP market in Europe, as well as for the development of the database,which will be used throughout the project. In this typology attention has also been paid toelements that have a relation to the application of intermodal transport by 3PLPs, since thisis part of the objective of the PROTRANS project and to more general elements, whichindicate for instance the size of a company.

The typology of 3PLPs used in the PROTRANS project contains the following mainelements:

• origination;• the type of clients that are served;• the network structure that is covered;• the type of activities that are carried out for the client;• the level of decision making;• transport means served;• size of the 3PLP;• regions of location;• degree of interrelationship between 3PLPs.

The above aspects will be further discussed in the following sub-paragraphs.

Origination of the 3PLP

In the 1980s, traditional logistics service providers entered the 3PL market. These providersare companies that have emerged from a traditionally strong position in either transportationor warehousing. In the 1990s, network players started as 3PLPs. These actors are mainlyparcel and express companies. In the late 1990s actors from non- traditional logistics areassuch as information technology, management consultancy and financial services, startedentering the market.

For the design of the database in the PROTRANS project, the following classification for theorigination of logistics service providers will be used:

• Carriers, i.e. road haulage companies, shipping companies, rail transport companies,and air freight companies.

• Forwarders and brokers.

PROTRANS, The Role of Third party Logistics Services Providers and their Impact on Transport 35

• Storage and warehousing companies.• Mail and express companies.• Shippers (manufacturer/wholesaler/retailer).• Actors from non-traditional logistics areas: Information technology providers, consultants

and financial service providers.

Type of clients

The 3PLP can offer its services to different types of industries. The following classification ofthe key clients of the 3PLP, based on the code used by Eurostat, is used for the typology.Annexe 3 describes the sub-categories of this classification.