Embed Size (px)

Citation preview

Protection of the “particular” contractual vulnerability of the microinsurance consumerAndrea CamargoPhD Candidate (Law)Paris Dauphine UniversityFrance

1

Motivation

The “poor” are increasingly seen as new insurance consumers:

“The number of people covered by microinsurance rose from 78 million in 2007 to 135 million in 2009, reaching nearly 500 million today” (Press Release 10th April 2012, ILO and Munich Re Foundation)

By 2016, it is projected that there will be 100 million new microinsurance consumers in Brazil (Gertulio Vargas Foundation)

… nevertheless, the deprivations suffered by the “poor” could have an impact on contractualtransactions

2

Research Questions

1. Does poverty amplify the contractual vulnerability of microinsurance consumers?

2. Are the techniques designed to address the contractual vulnerability of the traditional insurance consumer, appropriate to protect the “particular” contractual vulnerability of the microinsurance consumer?

3. How can we restore the appropriateness of these techniques and protect the microinsurance consumer? 3

1. The “particular” contractual vulnerability of the microinsurance

consumer• Contractual vulnerability results from:• Asymmetry of information, and• Inequality of power,

Between contracting parties

• This is usually reflected when one of the contracting parties cannot provide an “informed” and “free” consent in respect of their contractual obligations

• The traditional insurance consumer is in a contractually vulnerable situation when dealing with insurance professionals

4

1. The “particular” contractual vulnerability of the microinsurance

consumer• Nonetheless…the contractual vulnerability of

microinsurance consumers exceeds that “standard” contractual vulnerability because of the deprivations linked with poverty, mainly:Lack of educationExclusion from participating in the economic, social and

political processes, leading to lack of: Commercial, financial and contractual experience Awareness of their rights and how to enforce them

• Such experience and awareness are prerequisites for entering into contracts in the formal economy in order to: Understand the scope of engagements and act

accordingly Defend rights, seek remedies from competent

authorities

5

1. The “particular” contractual vulnerability of the microinsurance

consumer..

• Australian Aboriginals: insurance companies via their distribution channels “cashed in” on the contractual vulnerability of the aboriginals. They took advantage of:

Social factors (poorly educated, illiterate, not aware of their rights or how to enforce them)

Economic factors (no commercial experience, limited exposure to financial transactions, lack of awareness of insurance, low and irregular incomes)

Geographic factors (remoteness and no access to independent financial or legal advice)

Historical factors (discrimination and social exclusion)

Cultural factors (“gratuitous concurrence”)

6

1. The “particular” contractual vulnerability of the microinsurance

consumer

7

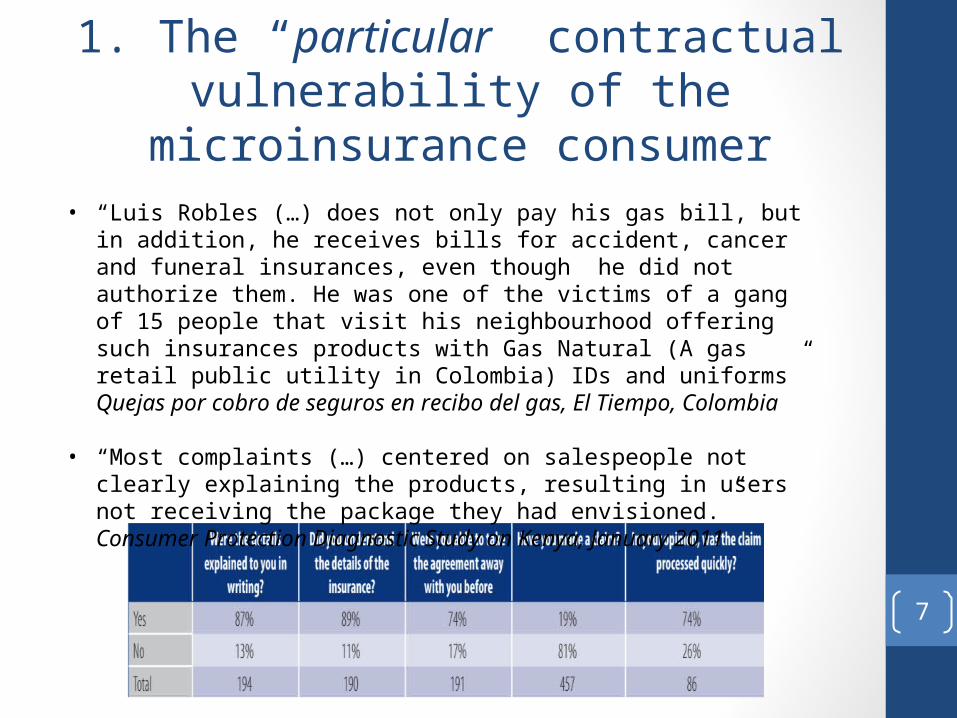

• “Luis Robles (…) does not only pay his gas bill, but in addition, he receives bills for accident, cancer and funeral insurances, even though he did not authorize them. He was one of the victims of a gang of 15 people that visit his neighbourhood offering such insurances products with Gas Natural (A gas retail public utility in Colombia) IDs and uniforms” Quejas por cobro de seguros en recibo del gas, El Tiempo, Colombia

• “Most complaints (…) centered on salespeople not clearly explaining the products, resulting in users not receiving the package they had envisioned.” Consumer Protection Diagnostic Study on Kenya, January 2011

2. The “inappropriateness” of techniques protecting traditional

insurance consumersI. Asymmetry of information

Contracts require free and informed consent, if not they are void - deceptive and unfair practices are prohibited and sanctioned

Imposition of disclosure obligations on insurers and intermediariesI. Information regarding (i) contractual conditions, (ii)

respective rights and obligations, (iii) mechanisms to exercise rights, must be disclosed at the time of entering into the contract in a transparent, clear, legible, simple, written, and appropriate manner, normally in the policy

II.Standard contracts must be registered with supervisory bodies

III.The contract and consumer consent are generally evidenced in writing

Financial education: In Colombia, financial education is recognized as a “right”

of the insurance consumer, therefore an “obligation” on the insurer. Consumer education in general is a right in Brazil

8

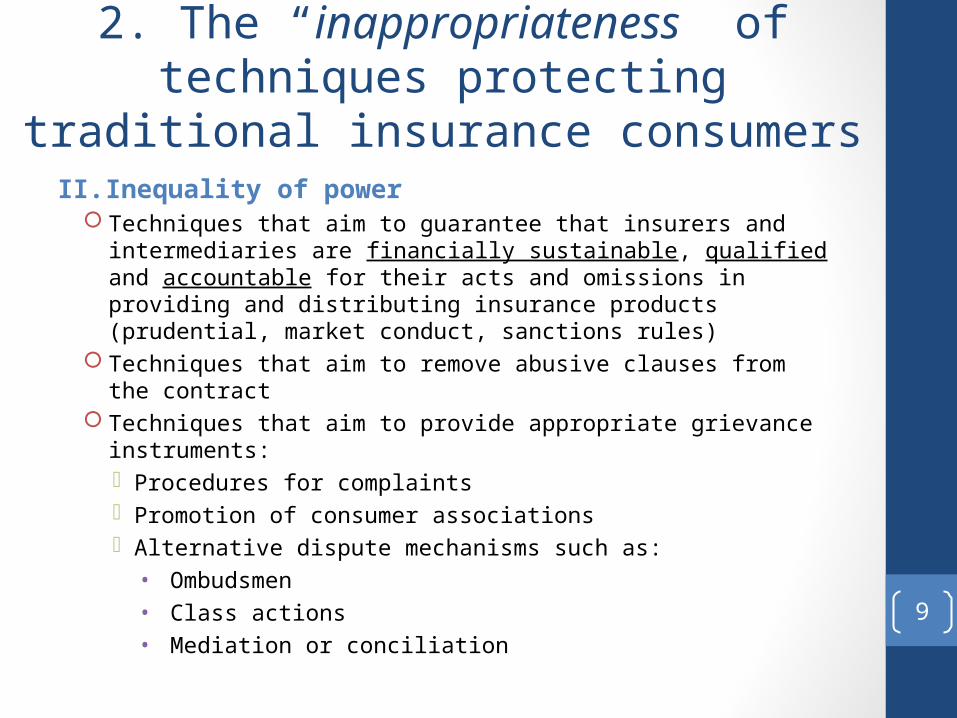

2. The “inappropriateness” of techniques protecting traditional

insurance consumersII. Inequality of power

Techniques that aim to guarantee that insurers and intermediaries are financially sustainable, qualified and accountable for their acts and omissions in providing and distributing insurance products (prudential, market conduct, sanctions rules)

Techniques that aim to remove abusive clauses from the contract

Techniques that aim to provide appropriate grievance instruments: Procedures for complaints Promotion of consumer associations Alternative dispute mechanisms such as:• Ombudsmen• Class actions• Mediation or conciliation

9

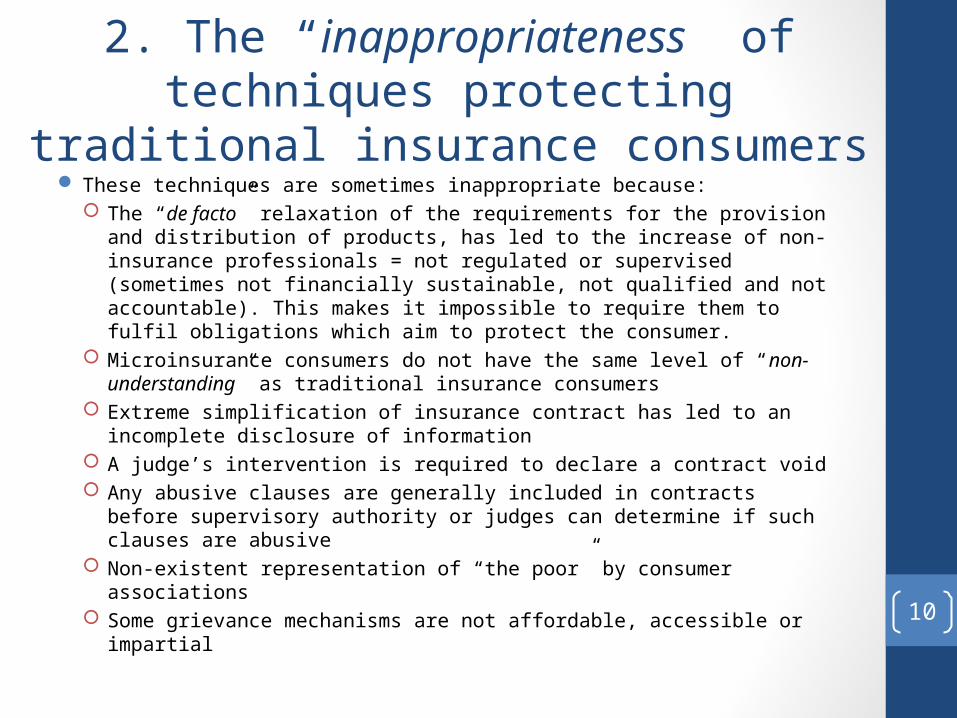

2. The “inappropriateness” of techniques protecting traditional

insurance consumers These techniques are sometimes inappropriate because:

The “de facto” relaxation of the requirements for the provision and distribution of products, has led to the increase of non-insurance professionals = not regulated or supervised (sometimes not financially sustainable, not qualified and not accountable). This makes it impossible to require them to fulfil obligations which aim to protect the consumer.

Microinsurance consumers do not have the same level of “non-understanding” as traditional insurance consumers

Extreme simplification of insurance contract has led to an incomplete disclosure of information

A judge’s intervention is required to declare a contract void Any abusive clauses are generally included in contracts before

supervisory authority or judges can determine if such clauses are abusive

Non-existent representation of “the poor” by consumer associations Some grievance mechanisms are not affordable, accessible or

impartial

10

3. Restoring the appropriateness of protection techniques

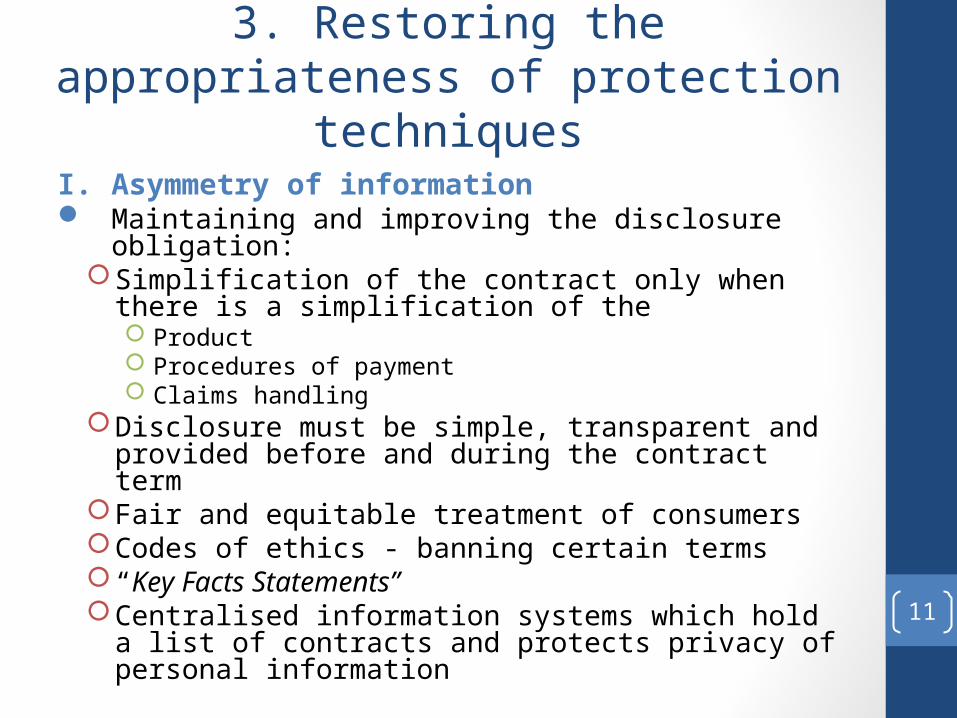

I. Asymmetry of information Maintaining and improving the disclosure

obligation:Simplification of the contract only when there is a

simplification of the Product Procedures of payment Claims handling

Disclosure must be simple, transparent and provided before and during the contract term

Fair and equitable treatment of consumersCodes of ethics - banning certain terms “Key Facts Statements” Centralised information systems which hold a list

of contracts and protects privacy of personal information

11

3. Restoring the appropriateness of protection techniques

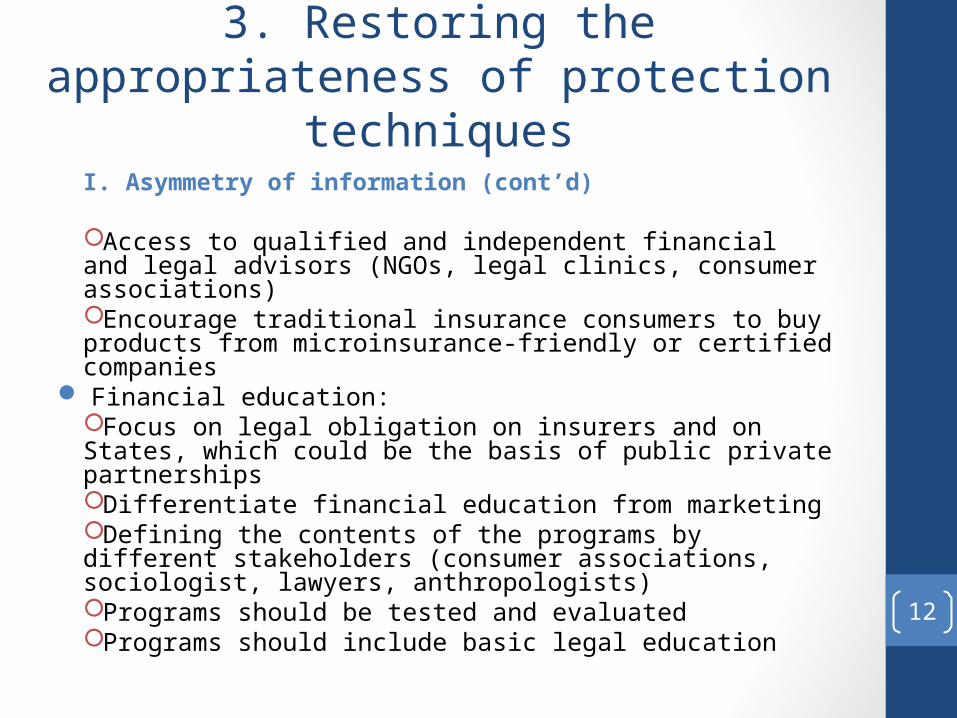

I. Asymmetry of information (cont’d)

Access to qualified and independent financial and legal advisors (NGOs, legal clinics, consumer associations)Encourage traditional insurance consumers to buy products from microinsurance-friendly or certified companies

Financial education:Focus on legal obligation on insurers and on States, which could be the basis of public private partnershipsDifferentiate financial education from marketingDefining the contents of the programs by different stakeholders (consumer associations, sociologist, lawyers, anthropologists) Programs should be tested and evaluated Programs should include basic legal education

12

3. Restoring the appropriateness of protection techniques

II. Inequality of power Real accountability of all stakeholders:

Progressive professionalization of non-regulated and non-supervised stakeholders

Compliance with requirements when they work with regulated and supervised stakeholders (codes of ethics as part of contractual arrangements between professionals and non-professionals with training and certification)

Insurance professionals must be liable for the acts and omissions of their distribution channels

It is essential to implement healthy practices such as: identifying with consumer associations and directly with the consumers banning abusive clauses, including cooling-off periods, promoting freedom to choose providers, protect personal data

13

3. Restoring the appropriateness of protection techniques

II. Inequality of power (cont’d)

Independent, affordable, fast, effective and accessible instruments to defend consumers:

Independent consumer associations Simple complaint procedures within one institutional

structure, in addition to the internal complaint departments. Submission of complaints should be easy and accessible (toll-free phone, email, post, in person). Statistics on consumer complaints must be published by supervisory authorities

Independent bodies competent to settle disputes with final and binding decisions. Should reconsider appointment of ombudsmen by insurers. Mediation, conciliation and class actions should be encouraged

Overarching principles of fairness and reasonableness

14

Conclusion

1. Does poverty amplify the contractual vulnerability of microinsurance consumers? YES

2. Are the techniques designed to address the contractual vulnerability of the traditional insurance consumer, appropriate to protect the “particular” contractual vulnerability of the microinsurance consumer? NOT ALWAYS

3. How can we restore the appropriateness of these techniques and protect the microinsurance consumer? 15

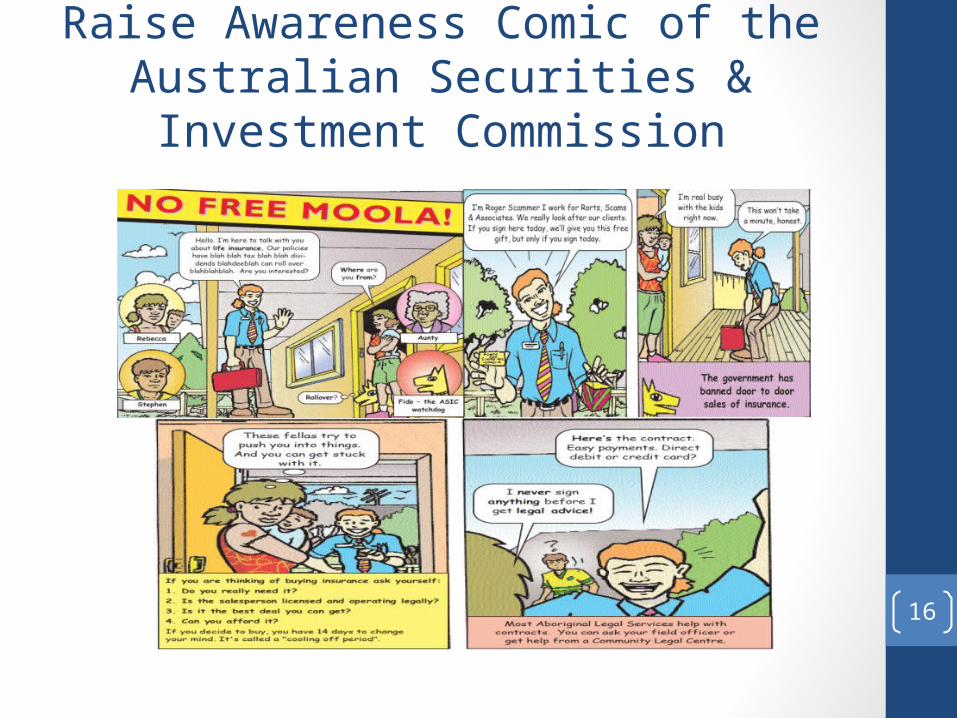

Raise Awareness Comic of the Australian Securities & Investment

Commission

16