Embed Size (px)

Citation preview

Protecting the Family Home & Will Trusts

The Family HomeThe most valuable asset which most people have worked hardest to obtain is the family home. It is also the asset they most want to pass on to their children on death. Unfortunately with the current rules on paying for long term care and Inheritance Tax (IHT) there is no certainty that this will happen. Unless steps are taken to legally protect the family home there is every possibility that children will not benefit as much as their parents might wish.

Home OwnershipA family home is most usually owned jointly by couples whether married/Civil Partners or not and held by them as ‘joint tenants’. They both own the home such that on death of either partner, the property automatically becomes solely owned by the survivor. This means that they are unable to leave their interest in the house to anyone else. Less frequently, home buyers have been and can be advised to own the house jointly as ‘tenants in common’. As tenants in common they each own a separate share in the property and, importantly, have the right to dispose of that share in their Will to whom they wish.

A Will can deal only with assets which are solely in the deceased’s estate and a house, held by joint tenancy, cannot be part of this. See diagram A.

A - Joint Tenants

On Mr Jones’s death the property becomes solely owned by Mrs Jones. The entire value of the property is therefore exposed to and can be attacked by various threats. Amongst these are:- Mrs Jones being taken into care, claims due to future breakdown of relationships, re-marriage, creditors and Inheritance Tax.

11

Mr Jones &

Mrs Joneseach own

100%

Step 1. By transferring ownership of their property to a ‘tenancy in common’, joint owners own their own share - normally half of the property each. Now, on the first death, half of the home is in the deceased’s estate and can be disposed of in his or her Will. See diagram B.

B - Tenants in Common

Mr & Mrs Jones are now ready to take Step 2 in the planning process

If the Will of the first to die leaves the deceased’s half share in the house to the survivor then he or she has the whole house in their name and nothing has been achieved to mitigate against the main threats to the family’s assets (see our notes ‘Threats to the Family Wealth & Home’). To take advantage of the tenancy in common, the share of the first to die must be left to someone else. If it is left to the children directly it is in their estate and the right of the surviving spouse or partner to live in the house could be affected. The way round this is to set up a trust within the Wills.

Decisions about setting up a trust will depend on family circumstances, relationships and on the wealth and wishes of each person and couple.

Will TrustsThese paragraphs are a very short introduction to trusts and provide a summary only.

Trusts might be described as a ‘safe box’. You, for example, include in your Will a clause which sets up a Trust on your death. In your Will you say what assets are to pass into the Trust and you appoint others (trustees) to manage and distribute the assets to your chosen beneficiaries. In many cases you will be asked to write a Letter of Wishes which gives direction to the Trustees as to how the assets are to be used, for what purpose and for whom.

Trusts have the sole purpose of protecting assets and there are many reasons for setting them up:- to protect assets for minor children, for a disabled person (without adversely effecting the latter’s State disability benefits), to protect the value of the family home, to secure the home for a survivor after the first death, to secure life insurance, investment and pension policy proceeds and, when appropriate, to mitigate the impact of inheritance tax (IHT).

Depending on the value of the assets there may be a liability to Inheritance Tax.

The notes below highlight three types of Will Trust. The first a Property Protection Trust which can be used to protect a share in the family home; it is not suitable for IHT planning. The second and third, Discretionary Trusts can accept cash, the family home (or share in it) and other assets; they can be used for IHT planning if personal circumstances justify it.

22

Mr Jones

50%

Mrs Jones

50%

Mr Jones diesMrs Jones dies

Tenants in Common

So back to the Jones. Depending on their circumstances, they may now take Step 2 of the planning process. In considering how to protect their home they have three options – either setting up one of three Will Trusts as described below or a Lifetime Trust, see our paper on Asset Protection Trusts.

Step 2a. Either – a Property Protection Trust. (also known as a Life Interest of Property Trust)

Having adopted a Tenancy in Common, as described earlier, homeowners have, through their Wills, a tested method of protecting and directing their share of their home to their chosen beneficiaries. This is to set up a Property Protection Trust.

Property Protection Trust

A Property Protection Trust is a valuable tool in protecting the value of property but it cannot accept other assets. It gives protection to half the property against third party threats and thus has limitations when being used to mitigate against care costs. See notes on Asset Protection Trusts.

Or Step 2b – a Discretionary Trust or a Nil Rate Band Discretionary TrustIn cases where there are complicated family relationships, minor or disabled children or in some cases exposure to IHT (where the value of an estate is above the tax free threshold of £325,000 (2010/1114) known as the Nil Rate Band (NRB)), there are advantages in setting up a Discretionary Trust. This type of trust can receive a share in the value of the family home, cash or other property and is used to direct those assets to beneficiaries of the trust e.g. children from an earlier relationship. This gives certainty to the first to die that their children will receive their proper due irrespective of what the surviving spouse or partner may do.

Assets put into discretionary trust are best kept to within or up to the value of the NRB which applies at the time of death. If the value exceeds the NRB on transfer, IHT at 40% will be charged on the excess. However the value of assets in Trust is not limited and can exceed the value of the NRB. If later, the value of the assets exceeds the NRB, there may be additional periodic exposure to IHT charges (every ten years) and when assets leave the trust.

With a Discretionary Trust, the executors of the deceased i.e. the trustees have the discretion (depending on circumstances, age, health of the beneficiaries) to direct the assets of the trust to the beneficiaries with the greatest need and in varying amounts. It is essential that a Letter of Wishes is written by the testator (person making the Will) to give them guidance, whilst not fettering their discretion, on how to manage and distribute the funds.

There are various issues and options to be considered when setting up a Discretionary Trust. For example a Discretionary Trust provides an element of control for the testator to direct affairs after death, it provides for the protection of assets and of the childrens’ interests and gives flexibility to the trustees to deal with the changing needs of the beneficiaries. Trust assets are distributed at the discretion of the trustees.

33

Mrs Jones 50%

On first Death50% of house

Property ProtectionTrust

Mrs Jones has the right to occupy the trusts’ half’ of the house free of charge during her lifetime or sell it with permission of the TrusteesThis also applies to any alternative home.

When she has no further use of it, the Trust’s half the house will revert to the Trust and, afterher creditors have been paid, the residue of Mrs Jones’s estate and her half of the house will pass to her beneficiaries.

Discretionary Trust

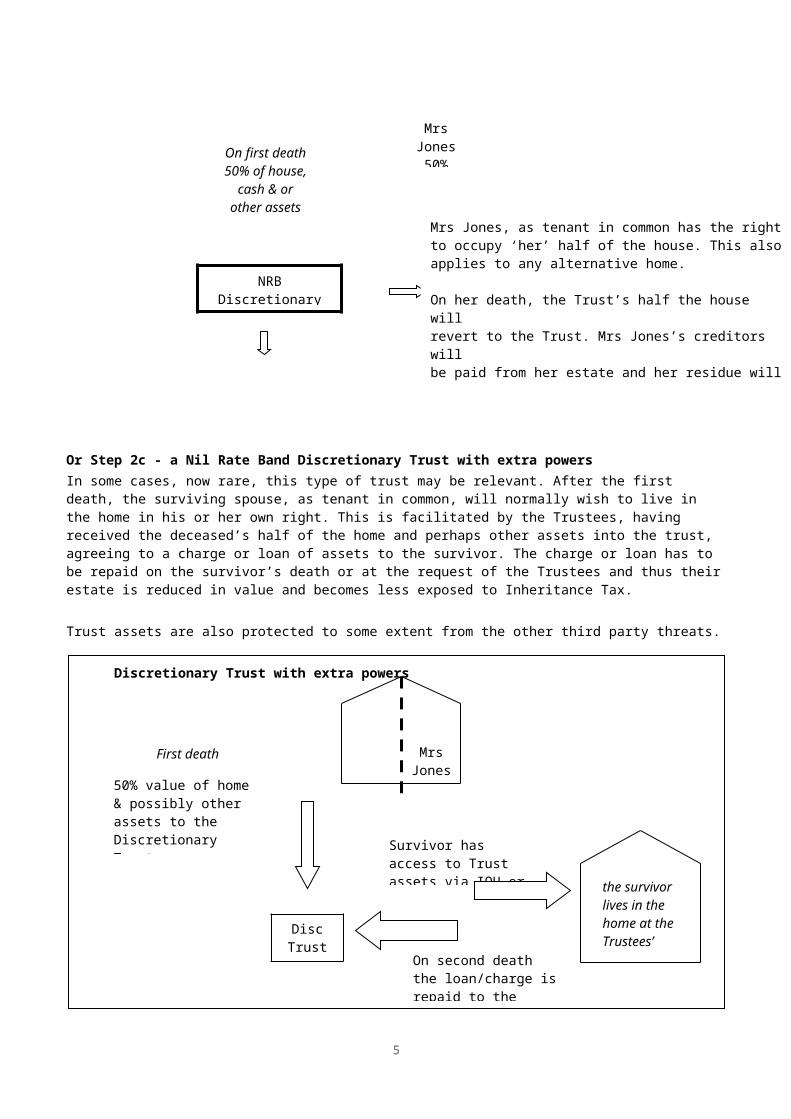

Or Step 2c - a Nil Rate Band Discretionary Trust with extra powersIn some cases, now rare, this type of trust may be relevant. After the first death, the surviving spouse, as tenant in common, will normally wish to live in the home in his or her own right. This is facilitated by the Trustees, having received the deceased’s half of the home and perhaps other assets into the trust, agreeing to a charge or loan of assets to the survivor. The charge or loan has to be repaid on the survivor’s death or at the request of the Trustees and thus their estate is reduced in value and becomes less exposed to Inheritance Tax.

Trust assets are also protected to some extent from the other third party threats.

Discretionary Trust with extra powers

The charge on or loan from the trust can be on any terms that the trustees consider to be appropriate.

44

First death

50% value of home & possibly other assets to the Discretionary Trust

the survivor lives in the home at the Trustees’ discretion

Mrs Jones

Disc Trust

Mrs Jones 50%

On first death50% of house,

cash & or other assets

NRB DiscretionaryTrust

for beneficiaries at discretion of the Trustees

Mrs Jones, as tenant in common has the rightto occupy ‘her’ half of the house. This also applies to any alternative home.

On her death, the Trust’s half the house will revert to the Trust. Mrs Jones’s creditors will be paid from her estate and her residue will go to her beneficiaries.

Survivor has access to Trust assets via IOU or charge

On second death the loan/charge is repaid to the Trust

Important – Tenancy in Common & Mortgage & Equity Release Plans lendersSevering a Joint Tenancy and establishing a Tenancy in Common of a jointly owned property is a simple and effective method to achieve greater flexibility in planning. There are no issues when there is a mortgage on a property. Lenders are best informed but they have no reason to prevent the severance.

It is important however to bear in mind the points below in relation to Equity Release Plans.1. Lenders will usually offer co-owners a loan on a property which is already held by them as Tenants in

Common. 2. A loan will almost certainly not be approved after the death of a co-owner. By this time half the value of the

house has passed into trust or to another beneficiary. 3. In all cases where there is an Equity Release Plan in place or where there is a probable need of one in the

future, advice should be sought from both our Associate and the proposed lender.

Please call us if you would like to learn more or have questions to ask about any of these issues. Tel: [xxxx]

On behalf of Simply Legal & Associates Ltd, White Hart Yard, Bridge Street, Worksop S80 1HR Simply Legal & Associates Ltd is a member of the Institute of Professional Will Writers

Simply Legal & Associates Ltd complies with the OFT approved IPW code of practice.

55