Embed Size (px)

Citation preview

J. Lauritzen A/S (A Danish company limited by shares organised under the laws of Denmark)

Business registration number 55 70 01 17

www.j-l.com

PROSPECTUS

Registration Document

Copenhagen, 15 January 2013

Managers:

NORDEA SEB

THIS REGISTRATION DOCUMENT, TOGETHER WITH A SECURITIES NOTE, SERVES AS A LISTING PROSPECTUS ONLY AS REQUIRED BY NORWEGIAN LAW AND REGULATIONS. THIS PROSPECTUS DOES NOT CONSTITUTE AN OFFER TO BUY, SUBSCRIBE OR SELL ANY OF THE SECURITIES DESCRIBED HEREIN, AND NO SECURITIES ARE BEING OFFERED OR SOLD PURSUANT TO IT.

2

Important information

This Registration Document has been prepared by J Lauritzen A/S in order to provide information about J. Lauritzen A/S and its business.

This Registration Document together with the Securities Note constitutes the Prospectus.

For the definitions of terms used throughout this Registration Document, see Section 2 “Definitions and Glossary of Terms”.

_______________________

The Issuer has furnished the information in this Registration Document and accepts responsibility for the information contained herein. The Managers make no representation or warranty, expressed or implied, as to the accuracy or completeness of such information, and nothing contained in this Registration Document is, nor shall be relied upon as, a promise or representation by the Managers. This Registration Document does not contain any offer to subscribe and/or purchase the securities issued by J. Lauritzen A/S. The Norwegian Financial Supervisory Authority (Nw.: Finanstilsynet) has reviewed and approved this Registration Document in accordance with Sections 7-7 and 7-8 of the Norwegian Securities Trading Act.

All inquiries relating to this Registration Document should be directed to the Issuer or the Managers. No other person has been authorised to give any information about, or make any representation on behalf of, the Issuer in connection with the Prospectus. If any such information is given or made, it must not be relied upon as having been authorised by the Issuer or the Managers or any of its affiliates or advisors.

The information contained herein is as of the date hereof and subject to change, completion or amendment without notice. There may have been changes affecting the Issuer or its subsidiaries subsequent to the date of this Registration Document. The delivery of this Registration Document at any time after the date hereof will not, under any circumstances, create any implication that there has been no change in the Issuer’s affairs since the date hereof or that the information set forth in this Registration Document is correct as of any time since its date. However, in accordance with Section 7-15 of the Norwegian Securities Trading Act, every new factor, material mistake or inaccuracy which may have significance for the assessment of the Issuer's securities and which is brought to light between the publication of this Prospectus and listing of the Issuer's securities, respectively, on Oslo Børs, will to the extent required be included in a supplement to this Prospectus.

The distribution of this Registration Document may in certain jurisdictions be restricted by law. Persons into whose possession this Registration Document may come are required by the Issuer and the Managers to inform themselves about, and to observe, any such restrictions. The Prospectus serves as a listing prospectus as required by applicable laws and regulations. The Prospectus does not constitute an offer to buy, subscribe or sell any of the securities described herein, and no securities are being offered or sold pursuant to it.

The contents of this Registration Document shall not be construed as legal, business or tax advice. Each reader of this Registration Document should consult its own legal, business or tax advisor as to legal, business or tax advice. If you are in any doubt about the contents of this Registration Document, you should consult your stockbroker, bank manager, lawyer, accountant or other professional adviser.

In the ordinary course of its business, the Managers and certain of its affiliates have engaged, and may continue to engage, in investment and commercial banking transactions with the Issuer and its subsidiaries.

Investing in the securities issued by the Issuer involves certain inherent risks. See Section 1 “Risk Factors” of this Registration Document.

Statistical and graphical information

Some of the statistical and graphical information contained in the Registration Document is supplied from the Clarkson Research Services Limited (“CRSL”) database and other sources. CRSL has advised that (i) some information in CRSL’s database is derived from estimates or subjective judgments, (ii) the information in the databases of other maritime data collection agencies may differ from the information in CRSL’s database, (iii) whilst CRSL has taken reasonable care in the compilation of the statistical and graphical information and believes it to be accurate and correct, data compilation is subject to limited audit and validation procedures and may accordingly contain errors, (iv) CRSL, its agents, officers and employees cannot accept liability for any loss suffered in consequence of reliance on such information or in any other manner, and (v) the provision of such information does not obviate any need to make appropriate further enquiries.

ANY USE OF SUCH DATA AND GRAPHICAL INFORMATION APPEAR WITH REFERENCE TO CLARKSON RESEARCH SERVICES LIMITED.

3

TABLE OF CONTENTS

1 RISK FACTORS ................................................................................................................................ 4 1.1 General .............................................................................................................................. 4 1.2 Industry risks ...................................................................................................................... 4 1.3 Operational risks ................................................................................................................. 5 1.4 Financial risks ..................................................................................................................... 7

2 DEFINITIONS AND GLOSSARY OF TERMS.......................................................................................... 10 2.1 Definitions ........................................................................................................................ 10 2.2 Glossary ........................................................................................................................... 10

3 RESPONSIBILITY FOR THE INFORMATION ......................................................................................... 11 3.1 Persons responsible for the information ................................................................................ 11 3.2 Declaration by persons responsible ...................................................................................... 11

4 NOTICE REGARDING FORWARD LOOKING STATEMENTS ..................................................................... 12 5 INFORMATION ABOUT THE ISSUER .................................................................................................. 13

5.1 History and development of the Issuer ................................................................................. 13 5.1.1 Legal and commercial name ................................................................................................ 13 5.1.2 Place of registration and registration number ........................................................................ 13 5.1.3 Date of incorporation ......................................................................................................... 13 5.1.4 Domicile and legal form ...................................................................................................... 13

6 BUSINESS OVERVIEW .................................................................................................................... 14 6.1 Bulk carriers ..................................................................................................................... 14 6.2 Gas carriers ...................................................................................................................... 15 6.3 Offshore support vessels .................................................................................................... 17 6.4 Product tankers ................................................................................................................. 19

7 ORGANISATIONAL STRUCTURE ....................................................................................................... 21 8 TREND INFORMATION .................................................................................................................... 23 9 PROFIT FORECASTS AND ESTIMATES ............................................................................................... 24 10 BOARD OF DIRECTORS AND MANAGEMENT OF THE ISSUER ................................................................ 25

10.1 Board of Directors ............................................................................................................. 25 10.2 Executive Management ...................................................................................................... 25 10.3 Corporate Governance ....................................................................................................... 26 10.4 Internal control ................................................................................................................. 26 10.5 Statement on conflict of interests ........................................................................................ 27

11 BOARD PRACTISES ........................................................................................................................ 28 11.1 Supervisory bodies ............................................................................................................ 28

12 MAJOR SHAREHOLDERS ................................................................................................................. 29 12.1 Information about major shareholders, etc. .......................................................................... 29 12.2 Arrangements regarding a change of control of the Issuer ...................................................... 29

13 FINANCIAL INFORMATION .............................................................................................................. 30 13.1 Capitalization, liquidity and capital resources ........................................................................ 30 13.2 Historical financial information ............................................................................................ 31 13.3 Financial statements .......................................................................................................... 32 13.4 Age of latest financial information ........................................................................................ 33 13.5 Governmental, legal and arbitration proceedings ................................................................... 34 13.6 Significant change in the Issuer’s financial or trading position ................................................. 34

14 MATERIAL CONTRACTS ................................................................................................................... 35 14.1 Material contracts .............................................................................................................. 35 14.2 Related Party Transactions.................................................................................................. 35

15 ADDITIONAL INFORMATION ............................................................................................................ 36 15.1 Third party information ...................................................................................................... 36 15.2 Documents on Display ........................................................................................................ 36 15.3 Statutory auditors ............................................................................................................. 36 15.4 Advisors ........................................................................................................................... 36

16 LIST OF DOCUMENTS INCORPORATED IN THIS REGISTRATION DOCUMENT BY REFERENCE.................... 37

APPENDICES: 1 Articles of Association for J. Lauritzen A/S

4

1 RISK FACTORS

1.1 General

An investment in securities issued by J. Lauritzen A/S involves a high degree of risk. This Section 1 “Risk factors” contains an overview of the risk factors that are known to the Issuer and considered material by it. Prospective investors should carefully consider all the information set out in the Prospectus and in particularly the risk factors set forth below before making an investment decision, and should consult his or her own expert advisors as to the suitability of an investment in securities issued by J. Lauritzen A/S.

The occurrence of any of the events discussed below could harm the Issuer. If one or more of these events occur, J. Lauritzen A/S’ business, financial condition, results of operations and cash flow could be materially and adversely affected, and the trading prices of securities issued by J. Lauritzen A/S could decline. An investment in securities issued by J. Lauritzen A/S is thus suitable only for investors who understand the risk factors associated with such type of investment and who can afford a loss of all or part of the investment.

The order in which the risks are presented below is not intended to provide an indication of the likelihood of their occurrence nor of their severity or significance.

1.2 Industry risks

1.2.1 Global political, economic and market conditions could negatively impact the Issuer’s business

The Issuer is subject to industry risks. For the Issuer, industry risks relate primarily to market volatility and cyclicality, conditions which are affected by global political, economic and market conditions and which the Issuer cannot influence or can only do so to a very limited extent. The Issuer is sensitive to fluctuations in the global private and public spending, and slowdown of the world economy may, among other things, result in a reduced demand for the Issuer’s services.

The Issuer transports bulk commodities, liquefied gasses, crude and refined oil products and there is a close correlation between global economic trends, political interventions, the demand for such commodities and the associated requirement for ocean transportation. Similar factors create the business environment for the extraction of oil and gas which forms the basis for the Issuer’s offshore services. Changes in global demand affect revenues, costs, utilization of assets and subsequently asset values.

The geographical pattern of production and sales of the bulk commodities transported by the Issuer may change going forward as a consequence of, inter alia, restructuring in the industry, sanctions growing protectionism and currency concerns. A potential shift in the balance between locally produced cargo and exported cargo may impact the overall demand for ocean transportation, resulting in lower and less efficient utilisation of the Issuer’s fleet and may thus negatively affect the Issuer’s profitability as well as the Issuer’s ability to implement its strategies.

Shipping, including servicing the offshore industry, is a cyclical industry with shorter or longer market cycles that create freight rate volatilities. The Issuer seeks to manage such risks through a balanced portfolio of owned vessels, time-chartered tonnage and cargo contract coverage supplemented with fuel oil hedging and to some extent Forward Freight Agreements (FFAs).

1.2.2 Risks related to market volatility and supply/demand imbalances

The Issuer’s revenues are mainly determined by charter rates which are set in an open and competitive market that historically has experienced volatility and supply/demand imbalances outside the Issuer’s control. The Issuer cannot predict the future level of demand for its services or the future conditions in the industry it serves. The size of the global new building order book for vessels could put further pressure on the charter rates for the Issuer’s vessels.

Unfavorable market developments could have a material adverse affect on the Issuer’s revenues, profitability, cash flow and financial condition.

1.2.3 Competition

The Issuer operates in a volatile market characterised by competition between the various suppliers of carriers. Although the Issuer believes that its vessels are currently competitive with regard to standard and attractiveness in the market, no assurance can be given that the Issuer will be able to maintain its market position in relation to current and/or future competitors. If the Issuer fails to maintain its competitiveness through its current strategy, this may have a negative impact on the Issuer’s operations, results of operation and financial condition.

5

1.2.4 Employment of vessels

The Issuer may not be able to compete successfully against other ship-owners and operators for the employment of its vessels in the highly competitive international shipping market. Competition for the employment of vessels depends on price, location, size, age, condition and the acceptability of the vessels to the charterer. Competitors with sufficient resources could acquire and operate vessels through acquisitions, consolidations or new buildings, and may be able to offer a more competitive service than the Issuer, which could result in lower revenues and less profitability on the vessels for the Issuer.

1.2.5 Political risks

The Issuer cannot predict whether governments of the countries in which territories it operates, or the regulators of international shipping, will change the fiscal framework governing the shipping industry or enact new legislation that could restrict or impair the Issuer’s operations in such areas which for instance could be relevant for technical and safety requirements, for example age.

1.3 Operational risks

1.3.1 Key personnel risk

Managing the Issuer’s current portfolio and attracting new orders is dependent on its senior management. Although no single individual is instrumental in this, departure of several key members of senior management may jeopardize profitability.

1.3.2 Delivery of contracted newbuildings risk

Long delays in or failure to take delivery of the vessels ordered due to problems at yards may have a negative effect on the results of the Issuer. Higher costs of newbuildings may also affect the Issuer’s future profitability, although many changes are due to rising requirements from customers, which normally will be reflected in higher levels of rates. Each of the yards chosen for building vessels to the Issuer have a proven track record for timely delivery.

1.3.3 Execution risk

Ability to deliver vessels and equipment at the defined specification at the agreed time is important, and failure to do so may have a negative impact on the Issuer’s results as charterers may be in a position to refuse delivery of the vessel.

1.3.4 Partnership risk

Partnerships, being an important part of the sourcing of tonnage for the Issuer, create risk in case default or bankruptcy of the individual partner materialises, due to the withdrawal of tonnage in such case. The Issuer will in such circumstances do its utmost to obtain quiet enjoyment for sufficiently long period of time to ensure fulfilling obligations towards customers, alternatively through substitution.

1.3.5 Renewal risk

Renewal of existing contracts in the future at similarly rewarding levels or without period of off-hire cannot be guaranteed. New contracts or renewal of contracts might include investments in upgrading, however, normally compensated for in the rate achieved.

1.3.6 Acquisition and sale of vessels

Part of the Issuer’s strategy includes acquiring and selling vessels. There are various risks associated with such a strategy, including, but not limited to, identifying suitable vessels to acquire, procuring the financing necessary for acquisitions of vessels on favourable terms, and identifying suitable buyers for the Issuer’s vessels. Some or all of these factors may be beyond the Issuer’s control, and could adversely affect the Issuer’s ability to pursue this part of the Issuer’s strategy.

1.3.7 Aging fleet

The aging of the Issuer’s fleet may result in increased operating costs in the future, which may have a material adverse effect on revenues, profitability, cash flow and the financial condition of the Issuer. In general, the cost of maintaining a vessel in good operating condition increases with the age of the vessel. Older vessels are typically somewhat less fuel efficient and more costly to maintain than more recently built vessels. Cargo insurance rates taken out by the charterers may increase with the age of a vessel, which may reduce the competitiveness of older vessels. Governmental regulations and safety standards and/or other equipment standards related to the age of vessels may also require expenditures for alterations or new equipment for the Issuer’s vessels, and may restrict the type of activities in which the vessels may engage. In addition, some of the Issuer’s customers may set their own age restrictions for vessels they will agree to charter. No assurance can be given that general market conditions will justify those expenditures or enable Issuer to operate the older vessels of the fleet profitably during the remainder of their useful lives.

6

1.3.8 Terrorist risk

Any terrorist incident may adversely impact the Issuer’s profitability, and if sustained in a specific region of major importance to the business, it could potentially lead to the closing down of serving such area with loss of earnings opportunities for a period of time.

1.3.9 Potential conflict of interest with its owner

The owner of the Issuer, Lauritzen Fonden, is also involved in other shipping companies. There can be no assurance that future shipping business opportunities will not be allocated such other companies. Lack of business opportunities can adversely impact the Issuer’s operations and profitability.

1.3.10 Safety risk

The Issuer recognizes the risks and potential hazards involved in owning, operating and managing a large, diversified fleet of ships worldwide. These risks include vessel performance in accordance with statutory requirements and additional customer requirements for health and safety, security, quality and environmental issues.

Casualties and property and environmental damages from ship operations can have serious consequences and, hence, merchant shipping is one the most heavily regulated industries in the world. The industry was among the first to adopt international safety standards while the international oil majors have implemented even further additional requirements relating to safety, environmental protection, etc.

Any accident may have serious consequences for the Issuer’s financial position due to loss of income, repair costs, claims and damages and indirect loss relating to customer satisfaction.

The Issuer’s main effort with respect to handling safety risks is to ensure that all ships under its control comply with comprehensive internal management systems that are in line with or exceed the requirements of the International Safety Management (ISM) code. Management systems and reporting practices are regularly revised so as to communicate best practice across the fleet, thus avoiding or minimizing the risk of incidents, accidents and time loss.

In addition, ongoing training of members of the crews is the key to minimizing risks relating to ship and cargo handling operations.

1.3.11 Piracy

Unfortunately piracy and associated risks continues to be on at the top of the global shipping agenda, hence also for the Issuer.

The risk to the Issuer’s crews and customers’ cargo due to piracy related activity in certain parts of the world has the Issuer’s strictest attention. The Issuer adheres to recommendations and best management practices from relevant national and international bodies as consolidated in the Issuer’s corporate security guidelines.

The Issuer supports the use and dispatch of private armed security teams on board our vessels. Based on voyage specific risk assessments the necessity is evaluated of engaging private armed security teams on vessels operating in the high risk regions. This is supported by anti-piracy measures installed on board and close monitoring by the technical management and NATO forces providing intelligence relevant to the vessels and military escorts.

The strong commitment for the Issuer is to ensure minimum risk for the Issuer’s crews’ wellbeing and the care for our customers’ cargo. The Issuer’s efforts are strengthened by close corporation with external anti-piracy professionals for assessment of current risk development. This corporation includes tests of new anti-piracy designs and measures to continue countering the development in the current risk.

1.3.12 Insurance risks

The Issuer’s insurance strategy has been adopted with the aim of reducing the financial risks of any incidents and casualties.

The Issuer’s insurances cover its assets, hired and operated fleet, cargo and non-marine risks. Insurance is taken out with top tier international insurance companies. As a general rule insurances are always taken out with a certain financial safety margin to avoid any serious consequential impact of an incident or casualty on the Issuer’s financial status. However, pollution and environmental risks are generally not fully insurable, and the Issuer’s insurance policies may not adequately cover all its losses, or may have exclusions of coverage for some losses. If a significant accident or other event occurs and is not fully covered by insurance, it could adversely affect the Issuer’s financial position, results of operations and cash flows.

7

1.3.13 Counterparty risks

Managing counterparty risk has become an increasingly important part of the shipping industry, particularly in view of the current economic environment and the substantial entry of new players into the market. The Issuer’s policy comprises both suppliers (e.g. critical IT systems) and customers (e.g. charterers).

Important counterparties are monitored and rated and limits to exposure have been established. Very large contracts and long-term commitments are reviewed and approved by the Executive Management and in some cases by the Board. Seeking the highest degree of guarantees from counterparties is part of the policy.

If a counterparty due to events beyond the control of the Issuer defaults its obligations this may affect results and cash flows of the Issuer. In case of default, the Issuer will do its utmost to secure fulfilment of the obligations of the counterparty, in case needed through indemnification, and to secure future cash flows through alternative employment or sale of assets.

The Issuer is constantly reviewing its policies with a view to extending the measures available to reduce counterparty risks.

1.3.14 Disputes

The Issuer may from time to time be involved in disputes and legal proceedings where the outcome is uncertain. Such disputes and legal proceedings may be expensive and time-consuming, and could divert management’s attention from the Issuer’s business. Furthermore, legal proceedings could result in rulings against the Issuer and the Issuer could be required to, inter alia, pay damages, which again could have a significant negative impact on the Issuer’s business, prospects, operating results or financial condition. In the event of a favorable ruling, no assurance can be given that the Issuer is able to enforce the judgment, due to the financial condition of the counterpart, the nature of the ruling or the enforcement options available under various jurisdictions.

1.3.15 IT systems risk

IT is critical for the conduct of the Issuer’s business. Systems for “vessels-online” are being implemented, adding even further to the requirements of the Issuer’s systems, platforms and infrastructure.

Both redundant systems and duplicate infrastructure are in place, and the Issuer frequently tests to see that restoring systems can be done within pre-defined time limits.

Breakdown of the IT systems can have a material adverse effect on the Issuer’s operations, and consequently, its profitability.

1.4 Financial risks

1.4.1 General

Financial risks relate to capital management risks (access to funding and liquidity) and in general to the financial markets (currency exchange rates and interest rates) as well as credit risks (loss arriving from counterparty’s failure to fulfil its contractual obligations towards the Issuer).

Financial risk management only applies to underlying financial risks and hedging contracts are entered into to reduce these risks. Risks primarily relate to non-USD currencies, net interest rate and credit risks and access to well-functioning financial markets.

1.4.2 Level of indebtedness

As of 30 June, 2012, the Issuer has a total debt of USD 1,340 million. The Issuer’s level of debt could have important consequences for investors of securities issued by the Issuer, including the following:

• The Issuer may have difficulty borrowing money in the future for acquisitions, capital expenditures or to meet its operating expenses or other general corporate obligations;

• The Issuer will need to use a substantial portion of its cash flows to pay interest on its debt, which will reduce the amount of money the Issuer has for operations, working capital, capital expenditures, expansion, acquisitions or general corporate or other business activities;

• The Issuer may have a higher level of debt than some of its competitors, which may put the Issuer at a competitive disadvantage;

• The Issuer may be more vulnerable to economic downturns and adverse developments in its industry or the economy in general; and

• The Issuer’s debt level, and the financial covenants in its various debt agreements, could limit its flexibility in planning for, or reacting to, changes in its business and the industry in which it operates.

8

1.4.3 Access to credit

The Issuer is exposed to the risk of limited availability of funding for future growth or for refinancing its existing debt. The Issuer may be unable to obtain sufficient funds to grow and develop its business or, if required, refinance its existing debt, and any additional financing may be on terms adverse to the interests of the Issuer and its shareholders. In the wake of the global financial and economic downturn, access to credit has become increasingly scarce. If the Issuer does not obtain additional financing when required, the Issuer may be unable to fund its operations and expansion or to successfully promote its business or take advantage of business or acquisition opportunities or refinance existing debt. Furthermore, no assurance can be given that the terms of financing obtained will be favorable or acceptable to the Issuer.

1.4.4 Financial covenants

The Issuer’s current credit facility requires, and the Issuer’s future credit facilities may require, the Issuer and certain of its subsidiaries to satisfy specified financial tests and maintain specified financial ratios and covenants.

The Issuer’s ability to comply with these ratios and to meet these tests may be affected by events beyond its control, and no assurance can be given that the Issuer will continue to meet these tests. The Issuer’s failure to comply with these obligations could lead to a default under these credit facilities unless it can obtain waivers or consents in respect of any breaches of these obligations under these credit facilities. No assurance can be given that that these waivers or consents will be granted. A breach of any of these covenants or the inability to comply with the required financial ratios could result in a default under these credit facilities. In the event of any default under these credit facilities, the lenders under these facilities will not be required to lend any additional amounts to the Issuer and could elect to declare all outstanding borrowings, together with accrued interest, fees and other amounts due thereunder, to be due and payable after any applicable grace periods in such existing credit facilities. If the debt under the Issuer’s credit facilities were to be accelerated, no assurance can be given that the Issuer’s assets would be sufficient to repay such debt in full.

1.4.5 Restrictions on the Issuer’s ability to operate its business in its indebtedness

Restrictions contained in the Issuer’s indebtedness may limit its ability to, among other things:

• incur additional indebtedness;

• create liens on its assets;

• pay dividends and make distributions or repurchase shares;

• carry on new businesses or make other investments;

• enter into certain types of transactions;

• merge, demerge, consolidate or transfer and sell substantially all of its assets;

• sell assets; and

• engage in transactions with affiliates.

Certain restrictions also apply in respect of changes in the ownership to the shares in the Issuer.

Therefore, the Issuer may need to seek permission from its lenders in order to engage in some corporate actions. The Issuer’s lenders’ interests may be different from the Issuer and the Issuer cannot guarantee that the Issuer will be able to obtain such permission when needed. This may prevent the Issuer from taking actions that it believes are in its best interest. The restrictions contained in the Issuer’s indebtedness may adversely affect the Issuer’s ability to finance its future operations or capital needs, or to engage in other business activities that may be in its interest.

1.4.6 The Issuer may be able to incur substantially more debt

1.4.7 The terms of the Issuer’s debt instruments permit it to incur additional indebtedness, including in connection with future acquisitions, some of which may also be secured. To the extent new debt is added to its currently anticipated debt levels, the substantial leverage related risks described above would be further exacerbated. Liquidity risk

Liquidity risk relates to the risk that the Issuer will not be able to fulfil its financial obligations as they fall due.

Failure to access necessary liquidity could require the Issuer to scale back its operations, postpone or cancel plans to acquire ships or could have other materially adverse consequences for its business and its ability to meet its obligations

9

1.4.8 Currency risk

The Issuer’s functional and reporting currency is USD and thus all amounts are recorded and reported in USD. By matching income and expenses and assets and liabilities the net currency risk is minimized leaving net positions to be focused on.

It is the policy of the Issuer to use derivative instruments to hedge the currency risks related to net non-USD cash flows from operating activities, investments and financing.

Operating cash inflows are mainly in USD and costs are also mainly in USD. The most important non-USD cost currency is DKK arising mainly from head office costs and Danish crew expenses, and EUR mainly related to the technical management of vessels. Currency risk related to non-USD investments in ships relates to JPY. Currency risk related on non-USD interest bearing debt relates to JPY, NOK and DKK.

1.4.9 Interest rate risks

Certain of the Issuer’s indebtedness are subject to floating interest rates. Consequently, the Issuer is exposed to fluctuations in interest rates.

It is the policy of the Issuer to hedge risks related to changes in interest rates to limit the negative financial effect of changes in interest rates by converting variable interest rates to fixed interest rates. USD credit facilities with a maturity longer than three years may be hedged up to 100%. The Issuer will cover the net interest rate risk via forward rate agreements, interest rate swaps and related instruments if assessed as advantageous. However, there can be no assurance that these measures will be effective in mitigating the risk.

1.4.10 Bunker oil price risk

Bunker oil is a significant cost element for the Issuer, though oil price risk only relates to contracted cargo volumes not covered by BAF (Bunker Adjustment Factor). At present, most of the fleet is contracted either in the spot market, re-let or on T/C (time charter), and hence bunker oil price risk is limited.

1.4.11 Credit risk

Credit risk is the risk of incurring a financial loss if a customer or counterparty fails to fulfil its contractual obligations.

The Issuer evaluates customers for creditworthiness based on historical trading and payment records as well as industry knowledge and customer reputation. Further, customers and counterparties are accepted only when fulfilling the general requirements. In certain cases contracts are guaranteed by parent companies or similar.

The risks relating to financial instruments, bonds and cash funds are minimized by trading only with financial institutions with a long term investment grade credit rating and by limiting the amount of exposure per counterparty.

1.4.12 Ability to service indebtedness is dependent on receipt of cash flows from subsidiaries

As a holding company, the Issuer’s principal assets consist of its direct and indirect shareholdings in its subsidiaries. Accordingly, the ability of the Issuer to make required payments of interest and principal on its indebtedness is effected by the ability of the Issuer’s subsidiaries, its principal source of cash flow, to transfer available cash resources to the Issuer. The transfer of funds to the Issuer by its subsidiaries (by way of dividends, inter-company loans or otherwise) may be restricted or prohibited by legal requirements applicable to the respective subsidiaries and their directors.

10

2 DEFINITIONS AND GLOSSARY OF TERMS

2.1 Definitions

Board of Directors or Board: The Board of Directors of the Issuer

Clearstream, Luxembourg Clearstream Banking, société anonyme

DKK: Danish Kroner, the legal currency of the Kingdom of Denmark

Euroclear: Euroclear Bank S.A./N.V.

IFRS: International Financial Reporting Standards

Issuer: J. Lauritzen A/S

Managers: Nordea Bank Danmark A/S and Skandinaviska Enskilda Banken AB (publ)

NOK: Norwegian Kroner, the legal currency of the Kingdom of Norway

Oslo Børs: Oslo Børs ASA

Trustee: Norsk Tillitsmann ASA

USD: United States Dollars, the legal currency of the United States of America

VPS: Verdipapirsentralen (the Norwegian Central Securities Depository)

2.2 Glossary

ASV: Accommodation and support vessel

Charterer: The customers to the Group’s operations

BAF: Bunker Adjustment Factor

cbm Cubic metre

CoA: Contract of Affreightment – an agreement with a customer to transport a quantity of cargo during a period of time between one or more loading and discharge ports

Dwt: Deadweight ton

ETH: Ethylene (gas carrier)

FFA Forward Freight Agreements

F/P: Fully-pressurized (gas carrier)

HSE: Health, Safety and Environment

MEG: Middle East Gulf

S/R: Semi-refrigerated (gas carrier)

T/C: Time charter (period charter)

11

3 RESPONSIBILITY FOR THE INFORMATION

3.1 Persons responsible for the information

Person responsible for the information given in this Registration Document is: J. Lauritzen A/S, 28 Sankt Annae Plads, Copenhagen, Denmark.

3.2 Declaration by persons responsible

Responsibility statement We confirm that, after having taken all reasonable care to ensure that such is the case, the information contained in this Registration Document is, to the best of our knowledge, in accordance with the facts and contains no omissions likely to affect its import.

Copenhagen, 15 January 2013

___________________________

Torben Janholt President & CEO, J. Lauritzen A/S

___________________________

Birgit Aagaard-Svendsen Executive Vice President & Group CFO, J. Lauritzen A/S

12

4 NOTICE REGARDING FORWARD LOOKING STATEMENTS

This Registration Document includes “forward-looking” statements, including, without limitation, projections and expectations regarding the Issuer’s future financial position, business strategy, plans and objectives. When used in this document, the words “anticipate”, “believe”, “estimate”, “expect”, “seek to” and similar expressions, as they relate to the Issuer, its subsidiaries or its management, are intended to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, performance or achievements of the Issuer and its subsidiaries, or, as the case may be, the industry, to materially differ from any future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Issuer’s present and future business strategies and the environment in which the Issuer and its subsidiaries operate. Factors that could cause the Issuer’s actual results, performance or achievements to materially differ from those in the forward-looking statements include but are not limited to:

• the competitive nature of the markets in which the Issuer operates,

• global and regional economic conditions,

• government regulations,

• changes in political events, and

• force majeure events.

Some important factors that could cause actual results to differ materially from those in the forward-looking statements are, in certain instances, included with such forward-looking statements and in the section entitled “Risk Factors” (Section 1) in this Registration Document.

13

5 INFORMATION ABOUT THE ISSUER

5.1 History and development of the Issuer

5.1.1 Legal and commercial name

The legal name of the Issuer is J. Lauritzen A/S.

5.1.2 Place of registration and registration number

The Issuer is registered with the Danish Commerce and Companies Agency (Erhvervs- og Selskabsstyrelsen) with business registration number 55 70 01 17 and is subject to the laws of Denmark.

5.1.3 Date of incorporation

The Issuer was founded on 15 April 1884 and incorporated in its current form on 4 January 1938.

5.1.4 Domicile and legal form

The Issuer is a private limited company with domicile in Denmark.

The Issuer’s registered office and main place of business is at 28, Sankt Annae Plads, Copenhagen, Denmark, telephone +45 3396 8000, telefax +45 3396 8001, web address www.j-l.com.

Overseas offices are located in China (Shanghai), Japan (Tokyo), the Philippines (Manila), Singapore, Spain (Bilbao) and USA (Stamford).

The Issuer has Denmark as its home state.

14

6 BUSINESS OVERVIEW

The Issuer is a shipping company engaged in worldwide operation of bulk carriers, gas carriers, product tankers, shuttle tankers and offshore service and accommodation units.

6.1 Bulk carriers

The bulk carrier market Dry bulks are traded worldwide and the main commodities are iron ore and coking coal (i.e. raw materials for steel production), steam coal (used for power generation) and grain. The key long-term driver of demand for maritime transports of dry bulks is industrialization and the subsequent increase in steel and power consumption. In addition, demand for bulk carriers is fairly closely correlated with the general business cycle, due to importance of fixed investments in creating business cycles. Besides these major commodities, a variety of other commodities is transported in bulk carriers, e.g. fertilizers, minerals and cement.

Bulk carriers, being specialized vessels for the carriage of dry bulks with distinct economies of scale characteristics, vary in size from 10,000 dwt to 400,000 dwt or more, numbering approximately 9,500 units according to Clarkson Research Services Limited1 as of beginning of November 2012. The dry bulk carrier market is fragmented with a large number of suppliers and customers. Cost of entry is relatively low and the complexity of managing bulk carriers is also comparatively low. Technical as well as commercial management outsourcing is common.

Major competitors in the handysize and handymax segments comprise Pacific Basin Group, D/S Norden A/S, Clipper Group, Oldendorff Carriers, Western Bulk Group, Cosco Group, NYK and MOSK among others.

Contracts are either spot (single voyage), trip charter, CoA (Contract of Affreightment), period charter (time charter) or bare boat charter. The spot market is very liquid and there is an active market for FFAs (Forward Freight Agreements) as well.

Bulk carriers are very liquid assets with a well-functioning sale and purchase market.

Supply and demand last 4-6 years During 2006-2008, high economic growth rates and industrialization in the resource poor emerging Asian countries secured high demand growth rates for maritime transports of dry bulks and as deliveries of new vessels from shipyards were not able to keep up with the high demand growth rates the dry bulk industry experienced the most profitable cycle ever. A main contributing factor was China’s enormous appetite for iron ore and coal to support steel production for the construction sector.

During the present economic crisis, global steel production has been severely affected, although China’s steel production growth has remained high. Furthermore, China’s domestic iron ore resources lost competitiveness due to falling iron ore prices, which caused Chinese iron ore imports to increase significantly and thus supported demand for dry bulk maritime transport in 2009 and 2012.

During the boom, a substantial order book was build up for delivery during 2009-2013. In 2011 the bulk carrier fleet increased by app 15% according to Clarkson Research Services Limited2

Due to this order book the dry bulk fleet is likely to experience double digit growths rates again in 2012, and together with increased uncertainty in financial markets and a relatively weak recovery of the world economy this has put pressure on earnings in the dry bulk segment in 2011 and particularly 2012. Low earnings have put pressure on companies exposed to the dry bulk market causing renegotiations of long term contracts and even defaults which have affected the industry significantly.

1 Source: Shipping Intelligence Weekly, Issue No. 1045, 02 Nov 2012 (not public source) 2 Source: Shipping Intelligence Weekly, Issue No. 1045, 02 Nov 2012 (not public source)

15

Chart 1 Baltic Dry Index 2000-2012 (1 November 1999 = 1,334)

Source: Clarkson Research Services Limited. Data extracted by the Issuer from www.clarksons.net (SIN-05). Subscription required for access.

Lauritzen Bulkers A/S Lauritzen Bulkers A/S (“Lauritzen Bulkers”) operated a total of 111 Handysize, Handymax, Panamax and Capesize bulk carriers as per 30 June 2012.

Lauritzen Bulkers aims to secure high forward coverage for larger bulk carriers, which are characterized by large order books relative to fleet size, relatively young fleet age and large volatility in the spot market. For Handysize and Handymax bulk carriers, where Lauritzen Bulkers has a long time presence, the exposure to the spot market is kept higher. Thus, high contract coverage has been secured in the Capesize and Panamax segments, whereas contract coverage for Handysize and Handymax is limited, albeit at a higher level than in the past few years.

A strong market reputation and a modern fleet contribute to securing Lauritzen Bulkers a high fleet utilization.

Lauritzen Bulkers manages one of the top five Handysize pools worldwide which secures economies of scale and a competitive edge.

Lauritzen Bulkers’ fleet of Handysize bulk carriers, including owned, part-owned, time-chartered and partner tonnage, stood at 78 vessels by 30 June 2012, with Island View Shipping as the major pool partner. At the same time, the Handymax fleet comprised 20 vessels, with a further 4 Panamax vessels, and 9 Capesize vessels.

Lauritzen Bulkers’ fully-owned fleet comprised 27 vessels (17 Handysize, 4 Handymax and 6 Capesize vessels) having an average age of 2.3 years (numbers as of 30 June 2012). Of the mentioned 6 Capesize vessels, one Capesize vessel was sold but not delivered to her new owners as per 30 June 2012. Subsequently one more Capesize vessel has been sold and delivered to new owners.

Lauritzen Bulkers’ newbuilding portfolio comprised 10 vessels as per 30 June 2012, hereof 1 fully-owned vessel scheduled to be delivered in 2013 and 9 time-chartered newbuildings scheduled to be delivered in 2013 and 2014.

Fleet management Technical management, including crewing for Lauritzen Bulkers’ fleet of own bulk carriers, is undertaken by New Century Overseas Management Inc., Manila (NCO), a subsidiary of Good Hope Overseas Management Inc., Fleet Management Ltd., Hong Kong and by Synergy Marine Pte Ltd, Singapore.

6.2 Gas carriers

The small gas carrier market (3,000 - 20,000 cbm) Gas carriers are specialised tankers, designed for the carriage of petroleum gases, petrochemical gases and ammonia, using pressure, refrigeration or a combination of refrigeration and pressure to liquefy the gas

0

2000

4000

6000

8000

10000

12000

14000

16

cargoes. Small gas carriers, comprising some 550 units3, serve the market for regional distribution as well as interregional transportation, with carriage of petrochemical gases being the main product category.

Liquefied petroleum gases (LPG) are used for domestic heating, transportation, power production, and as feedstock to the petrochemical industry. Particularly usage of LPG for domestic purposes is growing rapidly in industrializing countries. Petrochemical gases, including ethylene, enter into the production of plastics, fibres, films for packaging, adhesives etc., implying a strong correlation with income level per capita and the business cycle in their consumption.

Demand for modern gas carriers is created by deficits of either liquefied petroleum or petrochemical gases due to structural features (demand exceeds local output) and/or seasonal features (demand for liquefied petroleum gases jumps during the winter season in the Northern Hemisphere), necessitating imports of products from other locations. The build-up of a large cost-effective cluster of steam crackers (production facilities for petrochemical gases) in recent years in the Middle East Gulf (MEG) has created a large increase in export material, thereby creating more long haul business.

The market is characterized by a limited number of vessel operators (sufficiently large and sophisticated in terms of fleet to serve customers’ wish for CoAs) and customers (oil companies, petrochemical companies, and commodity traders).

Competitors comprise Unigas, GasChem/Gasmare Pool, Evergas Solvang Ethylene, Norgas (I.M. Skaugen) and A. Veder.

Contracts are either spot (single voyage), CoA (Contract of Affreightment), period charter (time charter) or bare boat charter. The spot market is liquid. Although CoAs normally have a duration of one year, rate of retention is high in the market.

Cost of entry is medium to high, depending on the sophistication of the vessels. Complexity of managing small gas carriers is increasing due to both regulation and customer requirements.

Gas carriers are liquid assets with a well-functioning sale and purchase market.

Supply and demand last 4-6 years Although a dip was encountered in 2009, the medium-term demand trend for smaller gas carriers has been solidly upwards, driven by rising demand for plastic products particularly in emerging markets. Over time steam crackers get bigger in order to achieve economies of scale and high sophistication in terms of meeting product specifications at ever higher standards. The cost of equipping newbuildings with advanced cooling systems has been reduced in the past five to ten years, thereby lowering the cost of transporting gases. In combination with the emergence of very cost-effective steam crackers in MEG, this has increased competition in world markets for petrochemical gases, opening up for a rise in seaborne demand for small gas carriers with a rise in average haul.

Up to and including 2007, demand growth outpaced supply growth. 2008 and 2009, an erosion of the market balance occurred. Since 2010 though, a strengthening of the market balance has taken place primarily due to very strong demand growth for small gas carriers. However, the weakening of economic activity has weighed against demand growth, and a deterioration of the market balance has taken place during the past few quarters. Spot and period rates (time charter rates) have recovered from their 2010 lows, cf. Chart 2 below, although levelling out during the past year save for the S/R types that have experienced a slight decline. During the past couple of years, the order book of small gas tankers has declined in relative terms, as deliveries have outpaced new ordering and the fleet has grown.

3 Source: Data extract by the Issuer from Clarkson Ship Register (CD rom), October 2012, provided by Clarkson Research Services Limited. (not public source)

17

Chart 2 Spot market rates for small gas carriers 2008-2012

Source: The Issuer, based on data extract from Fearnleys Weekly, various issues Lauritzen Kosan A/S Lauritzen Kosan A/S (“Lauritzen Kosan”) operates a fleet of modern semi-refrigerated, ethylene and fully-pressurized gas carriers. The fleet which totals 45 vessels (number as per 30 June 2012) comprises a portfolio of fully-owned, part-owned, time-chartered vessels, bare boat chartered vessels and vessels committed by partners. Active fleet portfolio management via cargo contracts and the sale and purchase of vessels is an important element of the business model.

Lauritzen Kosan operates the fleet with a high forward coverage, primarily with cargo contracts with major oil and petrochemical companies. A number of vessels are employed on longer term time charter.

The operated fleet consisted as per 30 June 2012 of 33 semi-refrigerated/ethylene gas carriers and 12 fully-pressurized gas carriers.

Lauritzen Kosan’s owned fleet comprised 25 vessels (7 semi refrigerated, 12 fully-pressurized and 6 ethylene carriers) having an average age of 8.8 years (S/R and F/P fleet average age 10.3 years and ETH fleet average age 4.0 years) (numbers as per 30 June 2012). As of 30 June 2012 Lauritzen Kosan did not have orders for newbuildings.

Fleet Management Lauritzen Kosan handles the technical management for ethylene and semi-refrigerated gas carriers. Part-owned Star Management Associates, Tokyo, handles the technical management for the fully pressurized vessels.

Technical fleet management is based on health, safety, security, environmental and technical policies to ensure efficient vessel operations in order to comply with the rules and regulations as well as stringent customer expectations. The crews of the vessels play a crucial part in delivering the service expected by customers.

HSSEQ Health, safety and security as well as protection of the environment and high quality standards (HSSEQ) are imperatives for Lauritzen Kosan.

Security for crews, vessels and cargoes is also important for Lauritzen Kosan Fleet Management. Thorough monitoring and risk assessment of current intelligence were used to prepare operations at sea and ashore for vessels transiting high-risk areas such as the Gulf of Aden. Using naval convoys, on board anti-piracy measures, best practice and anti-piracy networks are all risk mitigation factors aimed of keeping crews, vessels and cargoes safe.

6.3 Offshore support vessels

Production of offshore oil and gas is on a strongly rising trend, as onshore fields are depleting. Further, the market for deepwater exploration, development, and production is growing even more strongly, as existing fields in shallow waters are reaching maturity. The overriding driver of this trend is oil and gas consumption

0

100

200

300

400

500

600

700U

SD

/mon

th

6500 S/R 8200 ETH East (F/P) coaster

18

which is growing, mainly in emerging markets. As a result, demand for the support of installation, maintenance, servicing etc. on deepwater oil and gas installations is growing.

Many specialized vessels are involved in this, among them shuttle tankers and accommodation support vessels.

Shuttletankers Shuttletankers are specialized ships designed to transport crude oil and condensates from offshore oil field installations to onshore terminals and refineries.

Shuttletankers are equipped with sophisticated bow loading systems and dynamic positioning systems that allow vessels to load cargo safely and reliably from oil field installations. Parts of the fleet of shuttletankers are converted crude oil or product tankers. Shuttletankers face competition from subsea pipelines, however, only in shallow waters, on oil fields close to shore, and where sea bed conditions are of no concern.

The main markets comprise the North Sea, Brazil, and Canada, but shuttletankers are also employed in Russian and African waters. The Mexican Gulf is a relatively new area for shuttletankers.

Customers are major oil companies or contractors running offshore installations. Competitors include Teekay, Knutsen NYK and American Eagle Tankers.

Shuttletankers are typically employed on long-term time charter or bare boat charterparties at fixed rates or escalating rates, catering for a specific offshore field or operation of several fields by a single operator, such as Petrobras.

Accommodation and Support Vessels Accommodation and Support Vessels (ASVs) are specialized ships designed to function as accommodation and work station in connection with above-sea construction as well as maintenance and repair of offshore installations.

High class ASVs are equipped with sophisticated gangways and dynamic positioning systems that allow vessels vessels to stay in position safely and reliably close to oil field installations.

Mono-hull ASVs are self-propelled structures which enable fast and flexible transfer and repositioning between more installation units without support from anchor-handling and platform supply vessels. Mono-hull ASVs compete with large semi-submersible accommodation units in deepwater areas of oil and gas installations. In more shallow waters, mono-hulls compete with barges and jack-ups.

The main markets comprise Brazil, North Sea, Australia, the Mexican Gulf and West Africa. Customers are major oil companies or contractors running offshore installations.

Competitors include Prosafe, Flotel International and Østensjø. Only a few units are competing for the highly specialized projects on the deep water.

High-end ASVs are both employed on short and long-term time-charter as well as bare boat charter parties at fixed rates, catering for a specific offshore field.

Lauritzen Offshore Pte. Ltd. Lauritzen Offshore Pte. Ltd. (“Lauritzen Offshore”) currently has three shuttletankers on contract to the Petrobras group. One mono-hull ASV, Dan Swift, now part-owned via the joint-venture Axis Offshore Pte. Ltd., is chartered on a long-term contract to Petrobras in Brazil.

Dan Swift was until 4 July 2012 a fully-owned vessel of Lauritzen Offshore. On 4 July 2012, The Issuer and HitechVision, a Norwegian private equity investor, announced the formation of a 50/50 joint venture, subsequently named Axis Offshore Pte. Ltd., based on Dan Swift and with a focus on ordering high-end semi-submersible ASVs capable of also servicing customers in the North Sea.

As of 30 June 2012, Lauritzen Offshore did not have orders for newbuildings.

On 10 September 2012, Axis Offshore Pte. Ltd. announced that it had ordered a Harsh Environment Semi-submersible Accommodation Rig for delivery in the 1st quarter of 2015 with options for a two more units.

Fleet management Lauritzen Offshore Services A/S performs in-house ship management functions for the shuttletankers.

19

Health, Safety and Environment Lauritzen Offshore Services A/S has implemented high Health, Safety and Environment (HSE) standards as required by the offshore oil & gas industry. Its HSE philosophy is based on a ZERO mindset in which it commits itself to the active prevention of all incidents and accidents. HSE is always at the forefront of its approach and forms an integral part of its operations.

6.4 Product tankers

Medium range – 30,000 - 60,000 dwt product tanker market The product tanker is a specialized tanker, designed for the carriage of liquid petroleum products, vegetable oils, and, if certified, also some types of chemicals. Product tankers vary in size from less than 10,000 dwt to about 120,000 dwt, with medium range product tankers (fleet of product tankers including chemical/oil tankers), comprising some 1,700 units being the largest segment according to Clarkson Research Services Limited4.

Demand for refined products is among other things determined by the demand for energy which is correlated with income per capita and energy prices. Consumption of some of the products like gasoil is more closely correlated with the business cycle than e.g. gasoline. There is a growing demand for refined oil products, mainly in emerging markets as a result of the rising energy consumption.

Demand for product tankers is created by refineries being unable to satisfy local demand either due to structural features (demand exceeds local output) and/or seasonal features (demand for gasoline and/or diesel jumps during the summer season in the Northern Hemisphere) necessitating imports of products from other locations. Location of refineries in relation to consumer markets is an important driver of demand.

The market is fragmented with many customers (oil companies and commodity traders) and many suppliers (individual operators, owners or pools).

Some of the major players in the MR segment comprise the Norient Pool, Navig8, OSG, Scorpio Tankers, D’Amico and Handytankers Pool.

Contracts are either spot (single voyage), trip charter, CoA, period charter (time charter) or bare boat charter. The spot market is very liquid and volatile, and there is an active market for FFAs as well.

Cost of entry is relatively low and the complexity of managing product tankers is relatively low, but has risen strongly due to increasing environmentally based and/or politically driven customer requirements.

Product tankers are very liquid assets with a well-functioning sale and purchase market for vessels.

Supply and demand last 4-6 years The medium-term demand trend for product tankers has been solidly upwards, driven by rising demand for refined products, both in advanced economies and in emerging economies. Over time refineries get bigger in order to achieve economies of scale and high sophistication in terms of meeting refined product specifications at even higher standards, e.g. products with low sulphur content. This has created more demand for product tankers, the more so as refineries increasingly are located closer to the oil production rather than close to the end consumer, with a rise in average haul as a result.

Up to and including 2005, demand growth outpaced supply growth, thereafter matching supply growth for more than 2½ years. Mid 2008 rates started sliding and after the collapse in financial market in the autumn 2008, earnings dropped rapidly hitting lay-up levels by 2nd quarter 2009, cf. Chart 3 below. Since then the spot market has been volatile around a fairly low level, having led to re-structuring of the market – a process not finished yet.

The phase-out of single hull tankers by end 2010 accelerated scrapping of tankers, including product tankers. Thus, the average age of the products tanker fleet is low today. Due to this in combination with low earnings ordering has been very constrained in recent years, and the fleet of MR product tankers is set for a very low growth in the medium term. With demand growth accelerating the market is working towards balance in coming years.

4 Source: Data extract by the Issuer from Clarkson Ship Register (CD rom), October 2012, provided by Clarkson Research Services Limited. (not public source)

20

Chart 3 Average earnings for medium range product tankers of selected routes 2008-2012

Source: Clarkson Research Services Limited data extract by the Issuer from www.clarksons.net (SIN-2010). Subscription required for access.

Lauritzen Tankers A/S Lauritzen Tankers A/S (“Lauritzen Tankers”) controls a fleet of 18 modern MR product tankers (as per 30 June 2012). The fleet is a mix of owned, part-owned, and time-chartered vessels as well as vessels committed by partners. Active fleet portfolio management via sale and purchase of vessels constitutes part of the business model.

Vessels not covered by long-term contracts are commercially and operationally managed by Hafnia Management in their MR pool. Partners include Marinvest, Sweden, Gotlandsbolaget, Sweden, Kirk Shipping, Denmark and LGR di Navigazione, Italy.

Lauritzen Tankers’ fully-owned fleet comprised 7 MR product tankers having an average age of 2.0 years (numbers as per 30 June 2012).

Lauritzen Tankers’ newbuilding portfolio comprised 6 vessels as per 30 June 2012, hereof 3 fully-owned vessels scheduled to be delivered in 2013 and 3 time-charted vessels, also scheduled to be delivered in 2013.

Fleet management Technical management is performed by Wallem Shipmanagement, Hong Kong/Bergen and MMS, Tokyo. Ship management practices remain in line with the high standards demanded for all JL vessels.

0

5

10

15

20

25

30

35'0

00 U

SD

/day

21

7 ORGANISATIONAL STRUCTURE

J. Lauritzen A/S is a holding company and all business operations of the Issuer are carried out by the Issuer’s subsidiaries. The Issuer is thus dependent upon contributions from its subsidiaries in order to meet its financial obligations and to pay dividends.

The below Chart 4 sets out the Issuer’s main group structure, while Table 1 below sets out the name and country of incorporation of each subsidiary and affiliated company of the Issuer.

Chart 4 Main group structure

Table 1 List of group companies

Company name Country Ownership % J. Lauritzen A/S Denmark - Segetrans Argentina S.A. Argentina 100 Greden Limited Bahamas 100 Labas (Bahamas) Ltd. Bahamas 100 Shoreoff Invest Bermuda Ltd. Bermuda 100 J. Lauritzen Invest (Chile) Ltda. Chile 100 East Gate Shipping Ltd. China 100 J.Lauritzen Shanghai Co. Ltd China 100 Owneast Shipping Limited China 100 De Forenede Sejlskibe I/S * Denmark 43 Freja Polaris A/S * Denmark 49 KRK 4 ApS Denmark 100 K/S Bulkinvest 30 * Denmark 18 K/S Danred I * Denmark 43.5 K/S Danred II * Denmark 40 K/S Danred III * Denmark 35 K/S Danred V * Denmark 50 K/S Danskib 30 * Denmark 10 K/S Danskib 34 * Denmark 20 K/S Danskib 63 * Denmark 14 K/S Danskib 72 * Denmark 20 K/S Danskib 77 * Denmark 20 K/S Handybulk * Denmark 26 Lauritzen Bulkers A/S Denmark 100 Lauritzen Kosan A/S Denmark 100 Lauritzen Offshore Services A/S Denmark 100 Lauritzen Reefers A/S Denmark 100 Lauritzen Ship Owner A/S Denmark 100 Lauritzen Tankers A/S Denmark 100 LB Ship Owner II A/S Denmark 100 Quantum Tankers A/S *** Denmark 50 Tankers Inc. Holdings A/S Denmark 10.1 Hafnia Managment A/S Denmark 12 J. Lauritzen (Japan) K.K. Japan 100 Star Management Associates ** Japan 30 Lauritzen Shuttletankers Netherlands B.V. The Netherlands 100

J. Lauritzen A/S

Lauritzen Bulkers A/S

Lauritzen Kosan A/S

Lauritzen Tankers A/S

J. Lauritzen Singapore Pte.

Ltd.

Lauritzen Offshore Pte.

Ltd.

Lauritzen Kosan Singapore Pte.

Ltd.

22

Axis Offshore Pte. Ltd. Singapore 50 Handyventure Singapore Pte. Ltd. * Singapore 50 J. Lauritzen Singapore Pte. Ltd. Singapore 100 Lauritzen Kosan Singapore Pte. Ltd. Singapore 100 Lauritzen Offshore Pte. Ltd. Singapore 100 Lauritzen Shuttletankers Singapore Pte. Ltd. Singapore 100 LBS Shipowner Pte. Ltd. Singapore 100 LKT Gas Carriers Pte. Ltd. * Singapore 50 Milau Pte. Ltd. * Singapore 50 Gasnaval S.A. Spain 100 J. Lauritzen (USA) Inc. USA 100 * Joint venture ** Associated company *** Treated as subsidiary as JL has more than 50% of the voting rights

23

8 TREND INFORMATION

The Issuer has not experienced any material adverse changes in its prospects since the date of its last published audited financial statements and to the date of this Registration Document.

24

9 PROFIT FORECASTS AND ESTIMATES

The Issuer has not included a profit forecast or a profit estimate in this Registration Document.

25

10 BOARD OF DIRECTORS AND MANAGEMENT OF THE ISSUER

10.1 Board of Directors

The Issuer’s Board of Directors are as follows:

Name Position Business address

Bent Østergaard Chairman Lauritzen Fonden & LF Investment ApS, Sankt Annae Plads 28, DK-1291 København K, Denmark

Ingar Skaug Vice chairman Mariesvei 18B, N-1363 Høvik, Norge

Peter Poul Lauritzen Bay Board member Accenture, Arne Jacobsens Allé 15, Ørestad City, DK-2300 København S, Denmark

Niels T. Heering Board member Gorrissen Federspiel, H. C. Andersens Boulevard 12, DK-1553 København V, Denmark

Marianne Wiinholt Board member Dong Energy A/S, Nesa Allé 1, DK-2820 Gentofte, Denmark

Søren Berg Board member (employee representative)

J. Lauritzen A/S, Sankt Annae Plads 28, DK-1291 København K, Denmark

Ulrik Danstrøm Board member (employee representative)

J. Lauritzen A/S, Sankt Annae Plads 28, DK-1291 København K, Denmark

Per Gommesen Board member (employee representative)

J. Lauritzen A/S, Sankt Annae Plads 28, DK-1291 København K, Denmark

Bent Østergaard (born 1944) – Chairman and member of the board since 2003. Mr. Østergaard is President of LF Investment ApS and of Lauritzen Fonden. Chairman of the Board of Directors of DFDS A/S, Kayxo A/S, Frederikshavn Maritime Erhvervspark, NanoNord A/S, Cantion A/S. Mr. Østergaard is member of the Board of Directors of Comenxa A/S, Mama Mia Holding A/S, Meabco Holding A/S, Meabco A/S, Royal Artic Line A/S, With Fonden and Durisol UK.

Ingar Skaug (born 1946) – Vice chairman and member of the board since 1998. Mr. Skaug is former CEO of Wilh. Wilhelsen ASA. Chairman of the Board of Directors of Bery Maritime A/S, Ragni Invest A/S and Center for Creative Leadership. Member of the Board of Directors of Berg-Hasen Reisebureau AS, DFDS A/S Miros, Petroleum Geo-Services and Performance Leadership AS.

Peter Poul Lauritzen Bay (born 1974) – Board member since 2003. Mr. Bay is Management Consultant at Accenture and descendant of the founder of the Lauritzen Group.

Niels T. Heering (born 1955) – Board member since 2001. Mr. Heering is Chairman of the Board and partner of Gorrisen Federspiel. Chairman of the Board of Directors of Jeudan A/S, NTR Holding A/S (incl. subsidiary company), Ellos A/S, EQT Partners, Helgstrand Dressage A/S, Nesdu A/S, Stæhr Holding A/S (incl. subsidiary company), Stæhr Invest II A/S and Civ. Ing N.T. Rasmussens Fond. Member of the Board of Directors of Scandinavian Private Equity Partners A/S, Ole Mathiesen A/S, 15. juni Fonden (Vice Chairman), Lise og Valdemar Kählers Familiefond and CCKN Holding ApS (incl. subsidiaries).

Marianne Wiinholt (born 1965) – Board member since 2011. Mrs. Wiinholt is Senior Vice President, Head of Corporate Finance, Dong Energy A/S. Member of the Board of Directors of KNI A/S, DK-3911 Sisimiut, Greenland.

Søren Berg (born 1957) – Board member since 2005 (employee representative). Mr. Berg is Project Manager, Lauritzen Kosan A/S.

Ulrik Danstrøm (born 1955) – Board member since 2009 (employee representative). Mr. Danstrøm is Vice President, Lauritzen Bulkers.

Per Gommesen (born 1957) – Board member since 2009 (employee representative). Mr. Gommesen is Captain, Lauritzen Offshore.

10.2 Executive Management

The Issuer’s executive management comprises the following:

26

Name Position Business address

Torben Janholt President and CEO J. Lauritzen A/S, 28, Sankt Annae Plads, DK-1291 Copenhagen K, Denmark

Birgit Aagaard-Svendsen EVP and CFO J. Lauritzen A/S, 28, Sankt Annae Plads, DK-1291 Copenhagen K, Denmark

Jan Kastrup-Nielsen EVP and COO J. Lauritzen A/S, 28, Sankt Annae Plads, DK-1291 Copenhagen K, Denmark

The Issuer’s business unit management comprises the following: Name Position Business address

Torben Janholt President Lauritzen Bulkers A/S, 28, Sankt Annae Plads, DK-1291 Copenhagen K, Denmark

Thomas Wøidemann President Lauritzen Kosan A/S, 28, Sankt Annae Plads, DK-1291 Copenhagen K, Denmark

Erik Donner President Lauritzen Tankers A/S and Lauritzen Offshore Services A/S, 28, Sankt Annae Plads, DK-1291 Copenhagen K, Denmark

Martin Sato Managing Director J. Lauritzen Singapore Pte. Ltd., 1 Harbourfront Avenue, #13-01/02 Keppel Bay Tower, Singapore 098632

The Issuer’s shared services management comprises the following: Name Position Business address

Tove Elisabeth Nielsen Senior Vice President, Corporate Human Resources

J. Lauritzen A/S, 28, Sankt Annae Plads, PO Box 2147, DK-1291 Copenhagen K, Denmark

Erik Bierre Senior vice President, Business Control

J. Lauritzen A/S, 28, Sankt Annae Plads, PO Box 2147, DK-1291 Copenhagen K, Denmark

John Jørgensen Senior Vice President, Treasury

J. Lauritzen A/S, 28, Sankt Annae Plads, PO Box 2147, DK-1291 Copenhagen K, Denmark

The Issuer’s Management Committee comprises the members of the executive management, the members of business unit management and the management of the shared services. The Issuer announced in announcement no. 7/2012 on 14 November 2012 that President and CEO of J. Lauritzen A/S Torben Janholt will retire in connection with the release of the Issuer’s Annual Report 2012 and will be replaced by Jan Kastrup-Nielsen. Further it was stated that after Torben Janholt’s retirement, J. Lauritzen’s executive management will consist of Jan Kastrup-Nielsen as President and CEO and Birgit Aagaard-Svendsen as Executive Vice President and CFO.

10.3 Corporate Governance

The Issuer included in its Annual Report 2011 a section which reports on its principles and practice in respect of corporate governance which is incorporated in the Registration Document by reference. For a list of cross-references, see section 16 (page 37).

10.4 Internal control

The Issuer’s financial management comprises long-term financial projections and annual budgets followed up by quarterly and monthly reporting. Internal quarterly reports include profit forecasts for the full year. Annual profit forecasts are also drawn up twice a year for following years.

Effective, credible reporting requires well-defined levels of authorisation, segregation of duties and transparent reporting structures. The Issuer’s IT systems promote the requisite knowledge-sharing and transparency.

Statutory reporting and internal management reporting are based on common policies, common databases and a common reporting system. These reporting policies apply to the entire group of the Issuer, its business units, JL as parent company as well as subsidiaries.

Executive Management of the Issuer routinely defines and controls policies and procedures to support its business, risk management and reporting and to benchmark these against generally accepted international practice.

27

An anti-fraud policy has operated since 2006 and was supplemented with an anti-bribery policy in early 2011 to include guidelines on whistleblower reporting and protection.

10.5 Statement on conflict of interests

There are no potential conflicts of interests between any duties to the Issuer of the persons referred to in Sections 10.1 and 10.2 and their private interests or other duties.

28

11 BOARD PRACTISES

11.1 Supervisory bodies

The Board of Directors of the Issuer has appointed the following as members of the Issuer’s Audit Committee: • Niels Heering (Chairman) • Ingar Skaug • Peter Poul Lauritzen Bay

The Board of Directors of the Issuer has appointed the following as members of the Issuer’s Nomination and Remuneration Committee:

• Bent Østergaard (Chairman) • Ingar Skaug • Niels Heering

29

12 MAJOR SHAREHOLDERS

12.1 Information about major shareholders, etc.

The Issuer is wholly owned by Lauritzen Fonden (the Lauritzen Foundation). Lauritzen Fonden is a commercial foundation and as such is a self-governing institution under Danish law. Lauritzen Fonden is regulated by the Danish Foundation Act, and the Danish Ministry of Justice as well as the Danish Ministry of Economic and Business Affairs oversee the Foundation.

According to the Foundation’s charter, one major aim of Lauritzen Fonden is to improve Denmark’s reputation by promoting and developing the Danish Shipping industry.

Lauritzen Fonden’s charter also lays down how it should exercise its role as owner of its affiliated companies and its core policies are to:

• Operate a prudent dividend policy, taking account of the continued existence and development of the affiliated enterprises.

• Pay special attention to its shipping business. • Ensure the independence of affiliated enterprises from the Foundation. • Take an open-minded approach towards capital increases in affiliated enterprises.

12.2 Arrangements regarding a change of control of the Issuer

There are no arrangements, known to the Issuer, the operation of which may at a subsequent date result in a change in the control of the Issuer.

30

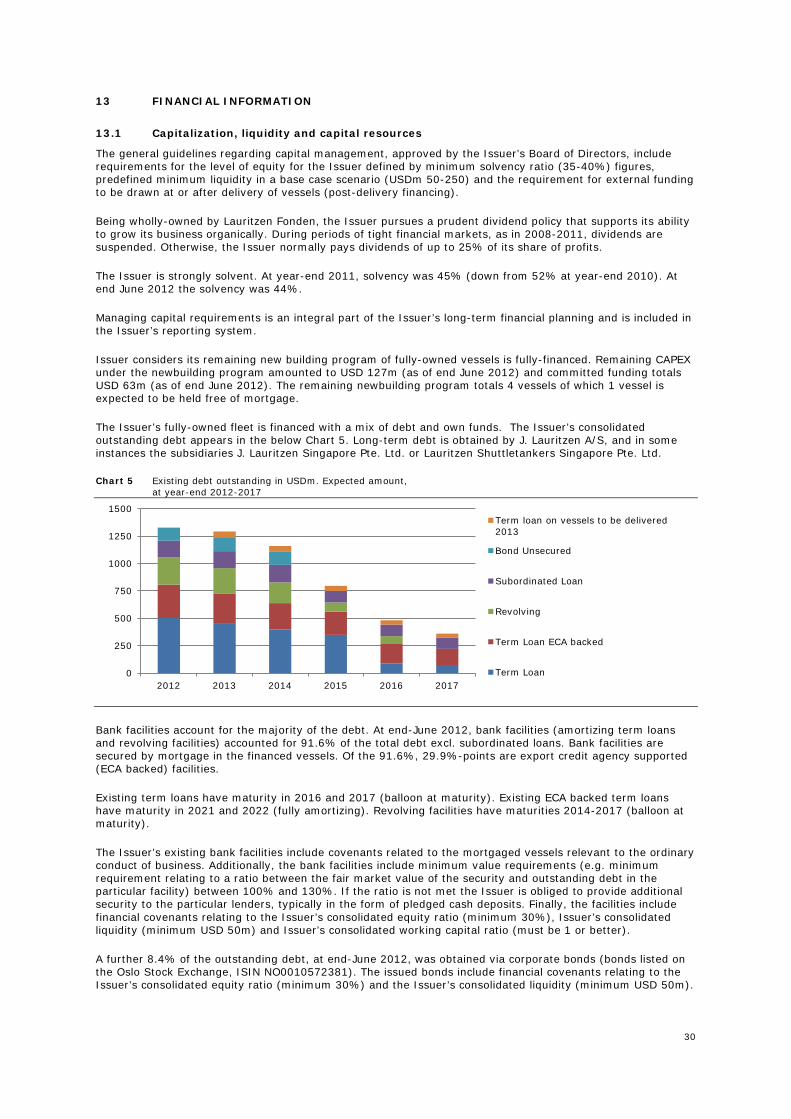

13 FINANCIAL INFORMATION

13.1 Capitalization, liquidity and capital resources