Embed Size (px)

Citation preview

Prospectus

for admission to trading on the

Regulated Market (Regulierter Markt) of the Frankfurt Stock Exchange (Frankfurter

Wertpapierbörse), sub-segment General Standard

of 35,000,000 ordinary bearer shares with no par value (Stückaktien)

- each with a pro-rata amount of EUR 1.00 in the share capital and with full dividend

rights for the financial year ending 31 December 2017, and for all subsequent financial

years -

of

De Raj Group AG Cologne

International Securities Identification Number: DE000A2GSWR1

German Securities Code (Wertpapier-Kenn-Nummer): A2GSWR

Trading Symbol: DRJ

Listing Agent

ACON Actienbank AG

15 November 2017

- 2 -

TABLE OF CONTENTS

1. SUMMARY OF THE PROSPECTUS ...................................................................................... 7

A - Introduction and Warnings ................................................................................................. 7

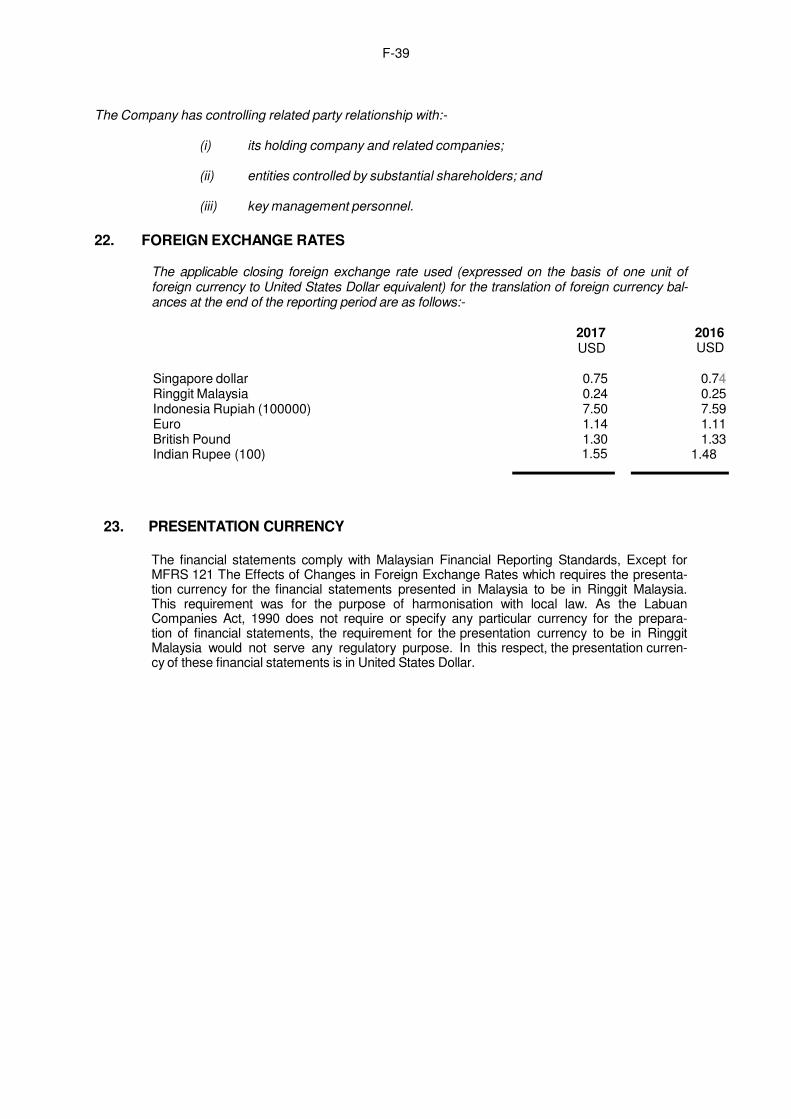

B - Issuer .................................................................................................................................. 7

C - Securities .......................................................................................................................... 26

D - Risks …………………………………………………………………………………………..…26

E - Offer ……………………………………………………………………………………………..28

2. GERMAN TRANSLATION OF THE SUMMARY OF THE PROSPECTUS -

ZUSAMMENFASSUNG DES PROSPEKTES....................................................................... 30

A - Einleitung und Warnhinweise ........................................................................................... 30

B - Emittent ............................................................................................................................ 30

C - Wertpapiere. ..................................................................................................................... 51

D - Risiken .............................................................................................................................. 52

E - Angebot ............................................................................................................................ 54

3. RISK FACTORS .................................................................................................................... 56

3.1 Market and Business Risks .................................................................................... 56

3.2 Legal and Regulatory Risks .................................................................................... 73

3.3 Risks related to the Listing and the Shareholder Structure .................................... 77

3.4 Tax Risks ................................................................................................................ 78

4. GENERAL INFORMATION ................................................................................................... 80

4.1 Responsibility for the Content of this Prospectus ................................................... 80

4.2. Purpose of this Prospectus ..................................................................................... 80

4.3. Forward-Looking Statements ................................................................................. 80

4.4. Note on Third-Party Information on Market Information and Technical Terms ...... 82

4.5. Auditor..................................................................................................................... 82

4.6. Note on Figures and Financial Information............................................................. 82

4.7. Documents Available for Inspection ....................................................................... 84

5. THE LISTING ......................................................................................................................... 85

5.1 Admission to Exchange Trading, Individual Share Certificates, Delivery and

Transferability ......................................................................................................... 85

5.2 ISIN, WKN, Trading symbol .................................................................................... 85

5.3 Form, Voting Rights ................................................................................................ 85

5.4 Dividend Entitlement and Participation in Liquidation Proceeds ............................ 85

5.5 Disposal Restrictions and Transferability ............................................................... 85

5.6 Timetable of the Listing........................................................................................... 86

5.7 Listing Agreement ................................................................................................... 86

5.8 Lock-up Agreement ................................................................................................ 87

6. REASONS FOR THE LISTING AND COST OF THE LISTING ............................................ 88

- 3 -

7. GENERAL INFORMATION ABOUT THE COMPANY ......................................................... 89

7.1 Name, Formation, Registration with the Commercial Register, Fiscal Year, Term

and Business Seat of De Raj .................................................................................. 89

7.2 Business Purpose of De Raj ................................................................................... 89

7.3 Formation and History of De Raj ............................................................................ 89

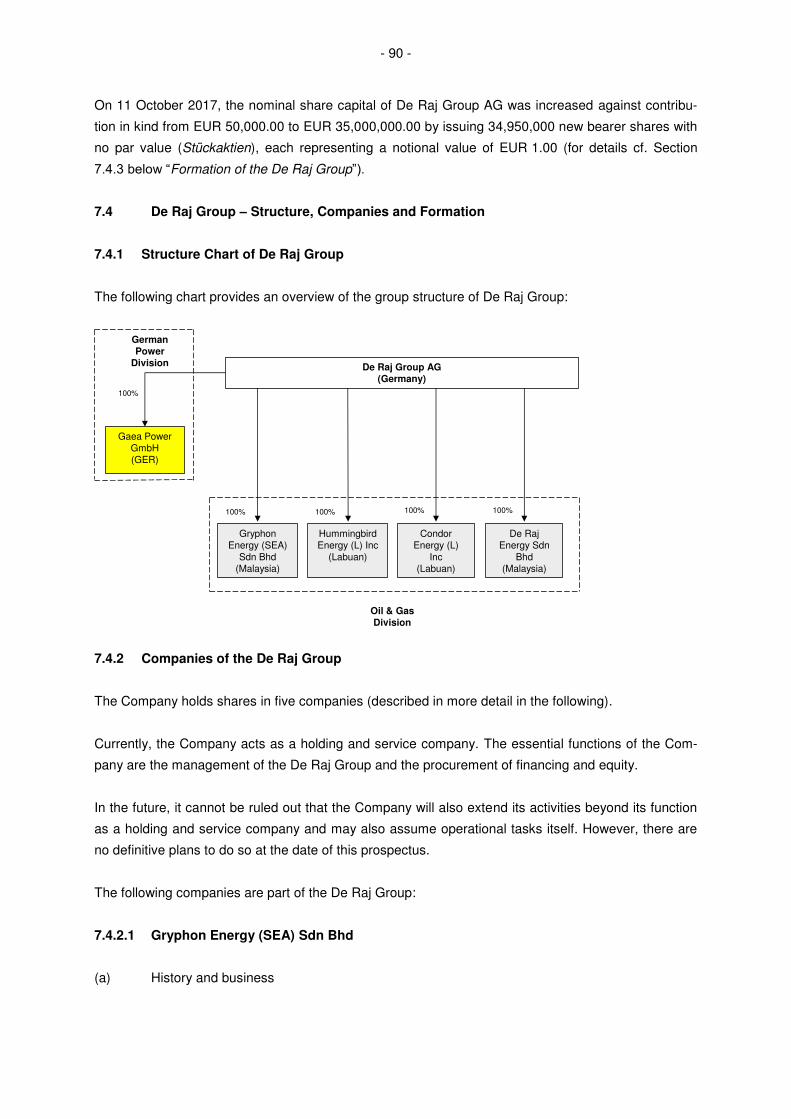

7.4 De Raj Group – Structure, Companies and Formation .......................................... 90

7.5 Tax status of De Raj ............................................................................................... 95

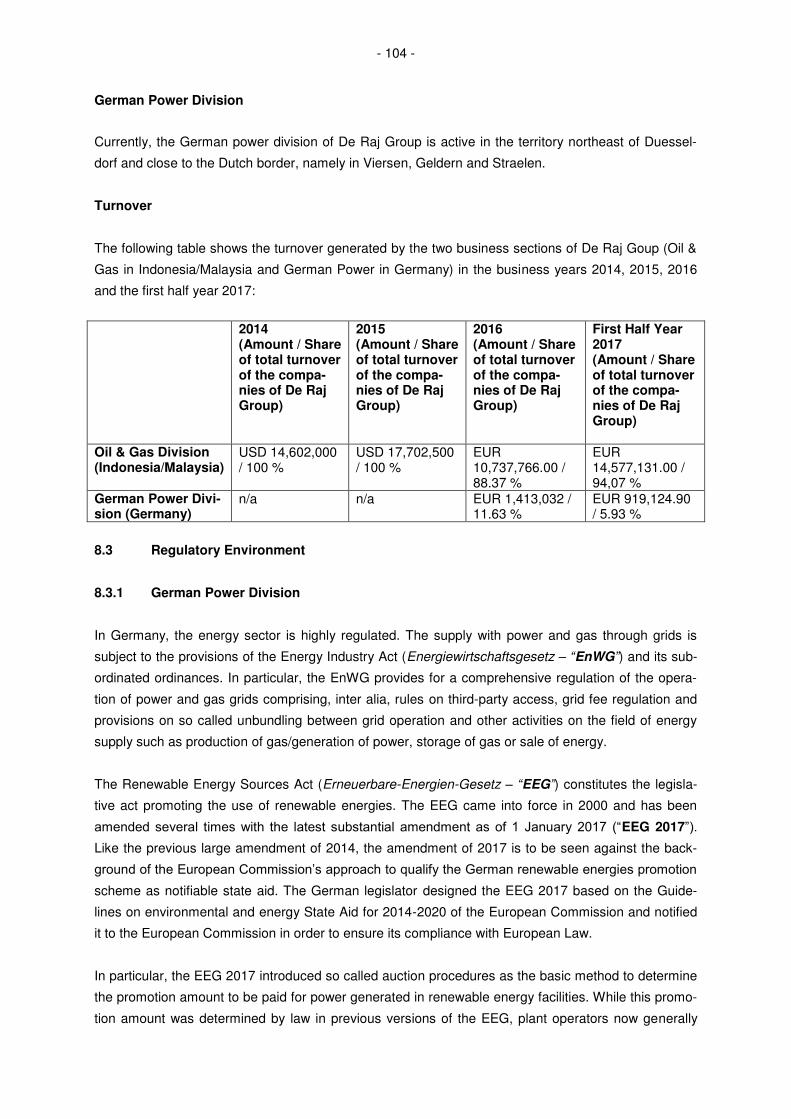

8. BUSINESS DESCRIPTION ................................................................................................... 96

8.1 Introduction and Overview ...................................................................................... 96

8.2 Market Overview ................................................................................................... 103

8.3 Regulatory Environment ....................................................................................... 104

8.4 Competitive Strengths and Competition ............................................................... 111

8.5 Strategy................................................................................................................. 116

8.6 Investment and Financing Requirements ............................................................. 117

8.7 Material Contracts ................................................................................................. 120

8.8 Insurance .............................................................................................................. 132

8.9 Litigation/ Administrative Proceedings .................................................................. 133

8.10 Research and Development ................................................................................. 133

8.11 Employees ............................................................................................................ 133

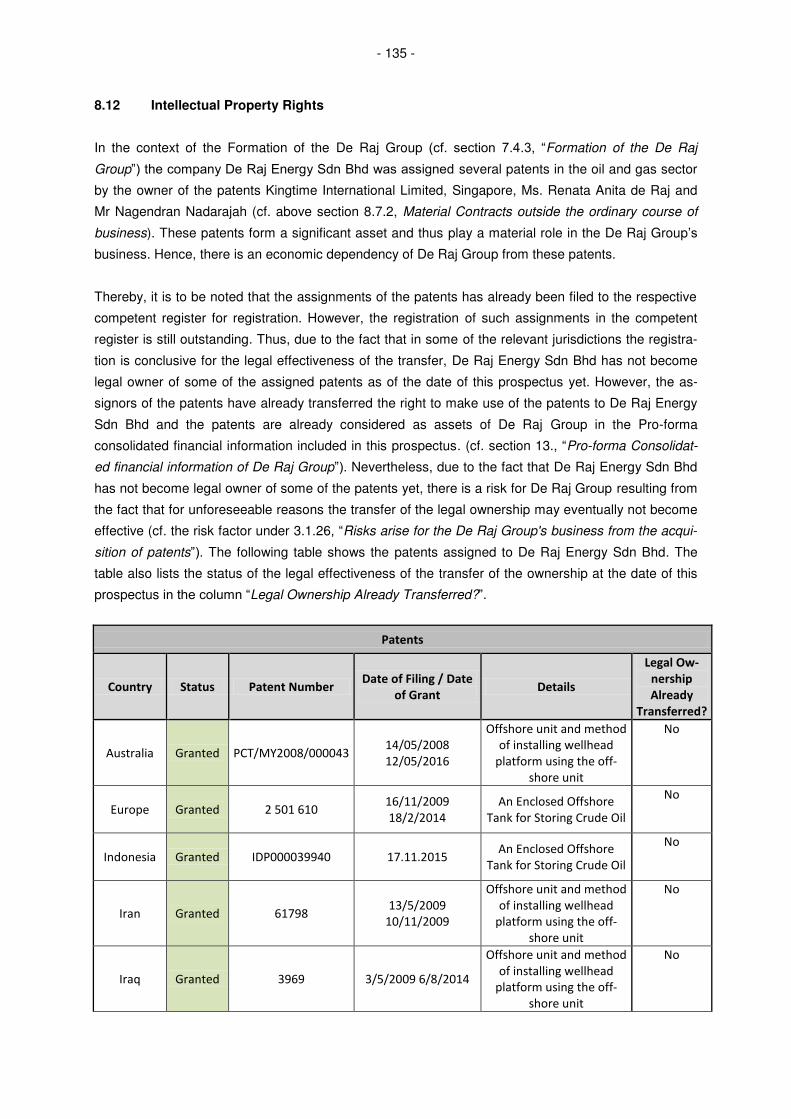

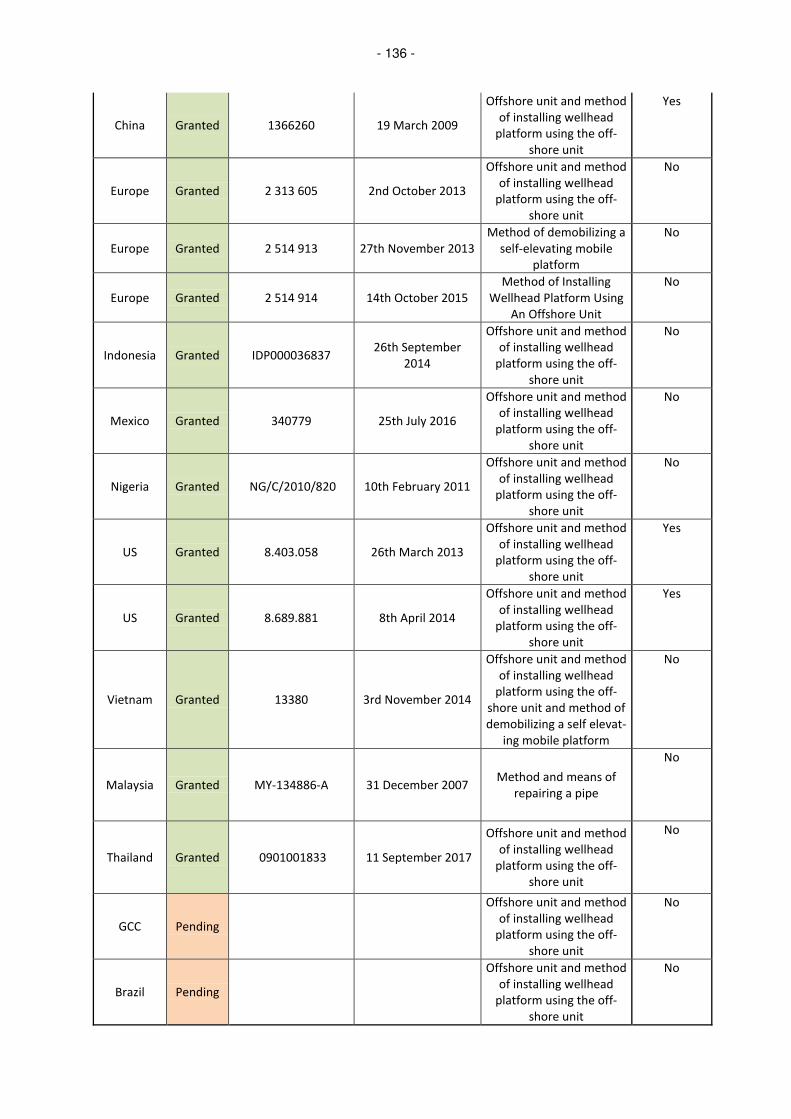

8.12 Intellectual Property Rights ................................................................................... 135

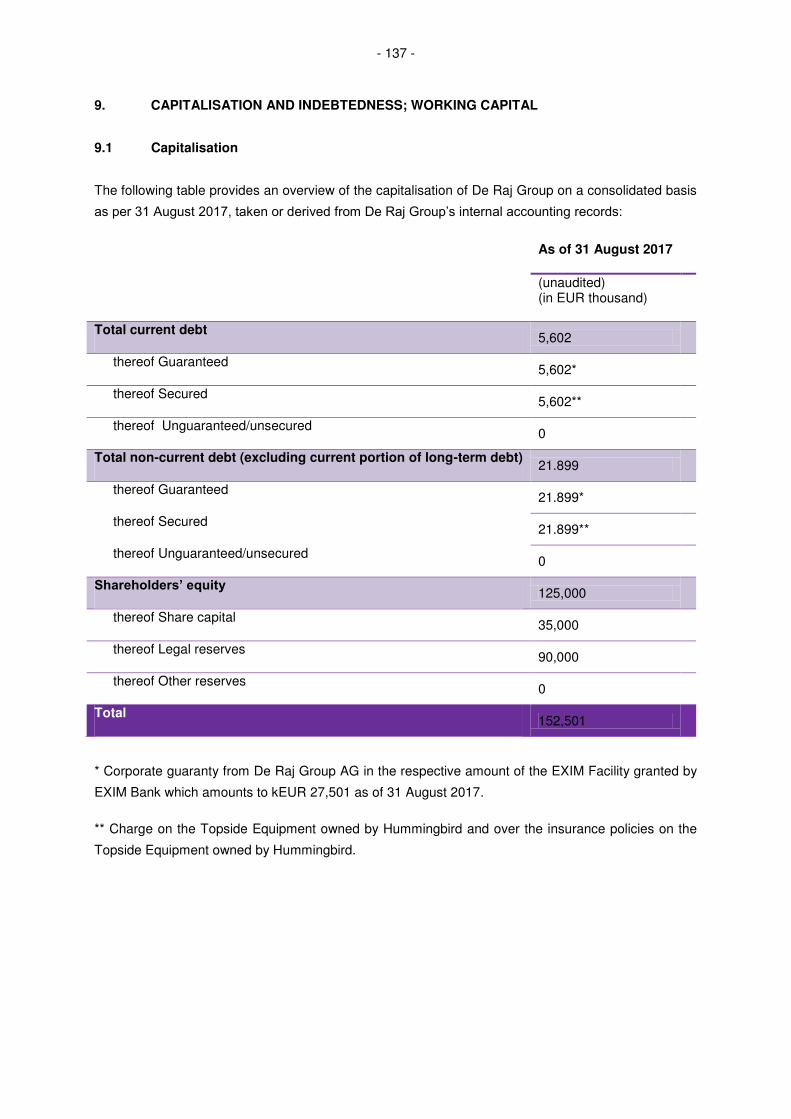

9. CAPITALISATION AND INDEBTEDNESS; WORKING CAPITAL .................................... 137

9.1 Capitalisation ........................................................................................................ 137

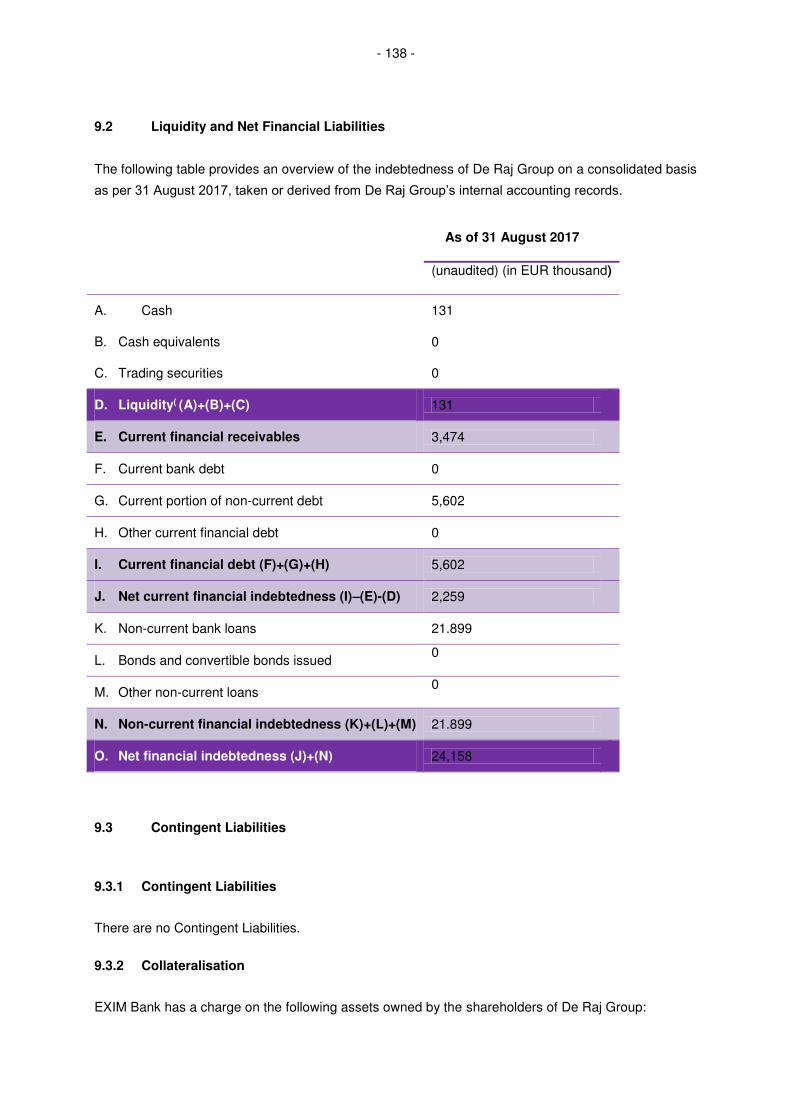

9.2 Liquidity and Net Financial Liabilities .................................................................... 138

9.3 Contingent Liabilities ............................................................................................. 138

9.4 Statement on Working Capital .............................................................................. 139

10. DIVIDEND POLICY AND EARNINGS PER SHARE .......................................................... 140

11. SELECTED FINANCIAL INFORMATION ........................................................................... 142

11.1 Selected Financial Information for De Raj Group AG ........................................... 144

11.2 Selected Financial Information for Hummingbird Energy (L) Inc .......................... 151

11.3 Selected Financial Information for Gryphon Energy (SEA) Sdn Bhd ................... 156

11.4 Selected Financial Information for De Raj Group from the Pro-Forma Consolidated

Financial Statements ............................................................................................ 159

12. MANAGEMENT’S DISCUSSION AND ANALYSIS OF NET ASSETS, FINANCIAL

CONDITION AND RESULTS OF OPERATIONS ............................................................... 162

12.1 Business Overview ............................................................................................... 163

12.2 Significant Factors affecting De Raj’s Net Assets, Financial Condition and Results of Operations ........................................................................................................ 165

12.3 Significant Accounting and Valuation Methods .................................................... 167

12.4 Management Discussion and Analysis of Hummingbird Energy (L) Inc. ............. 168

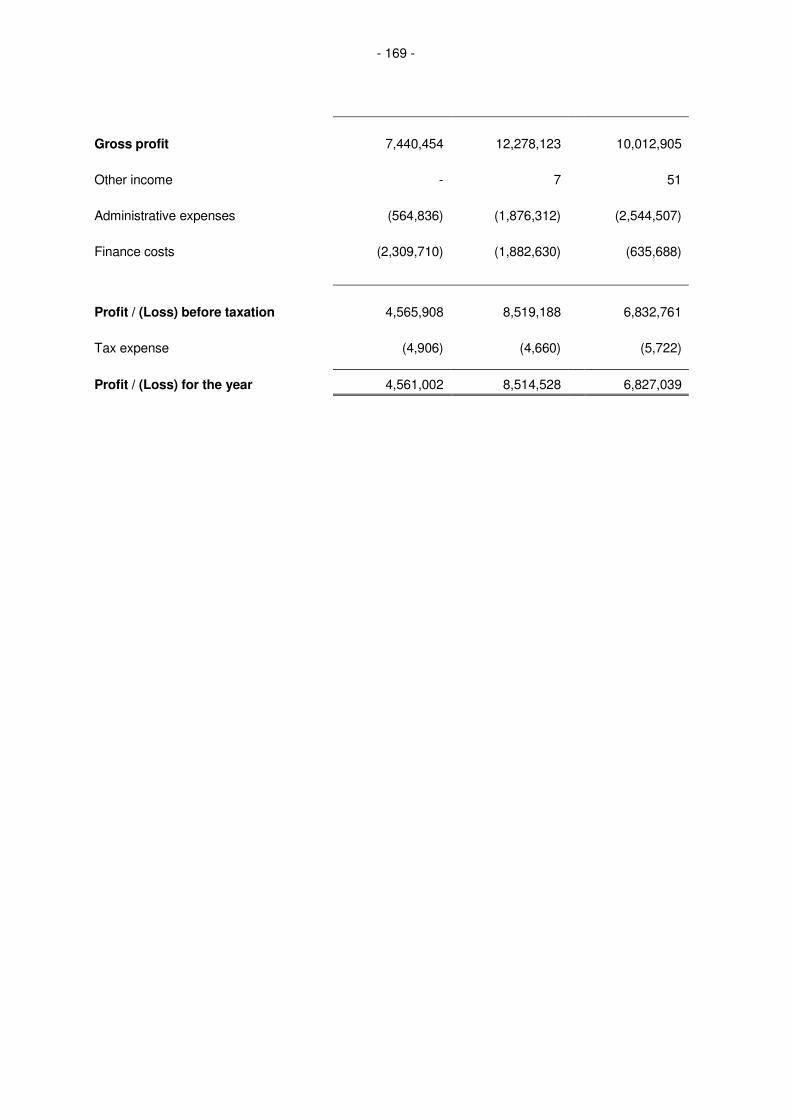

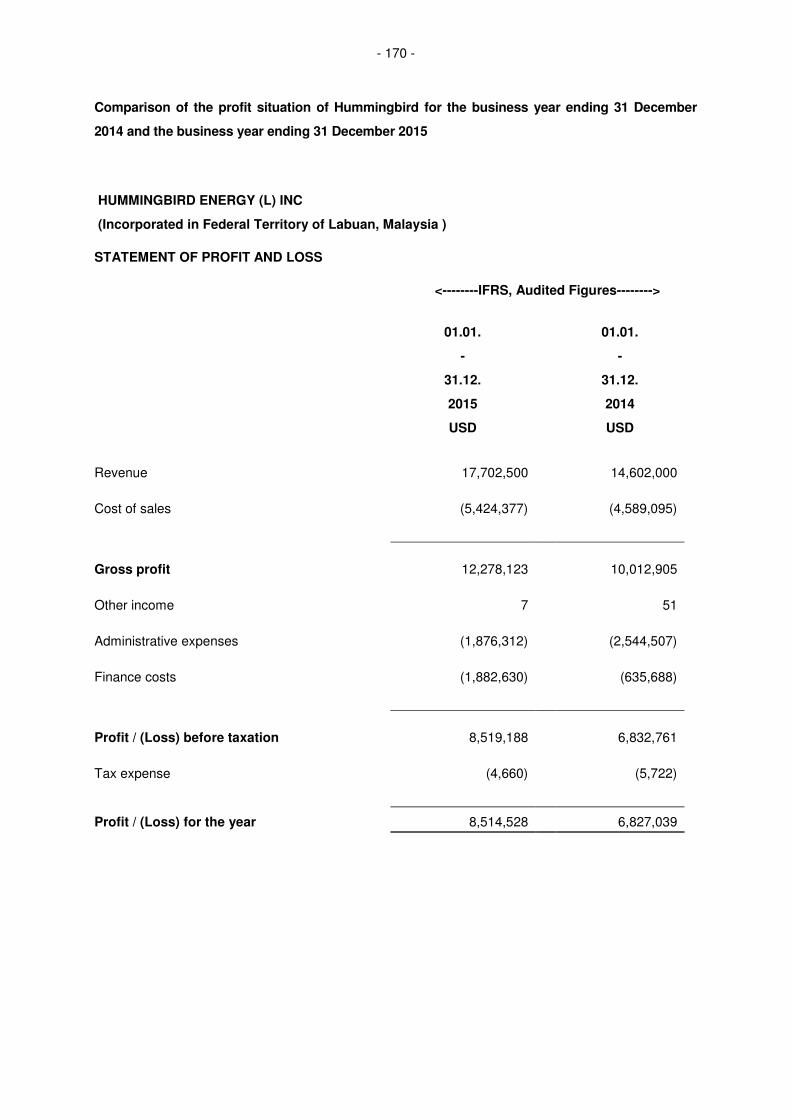

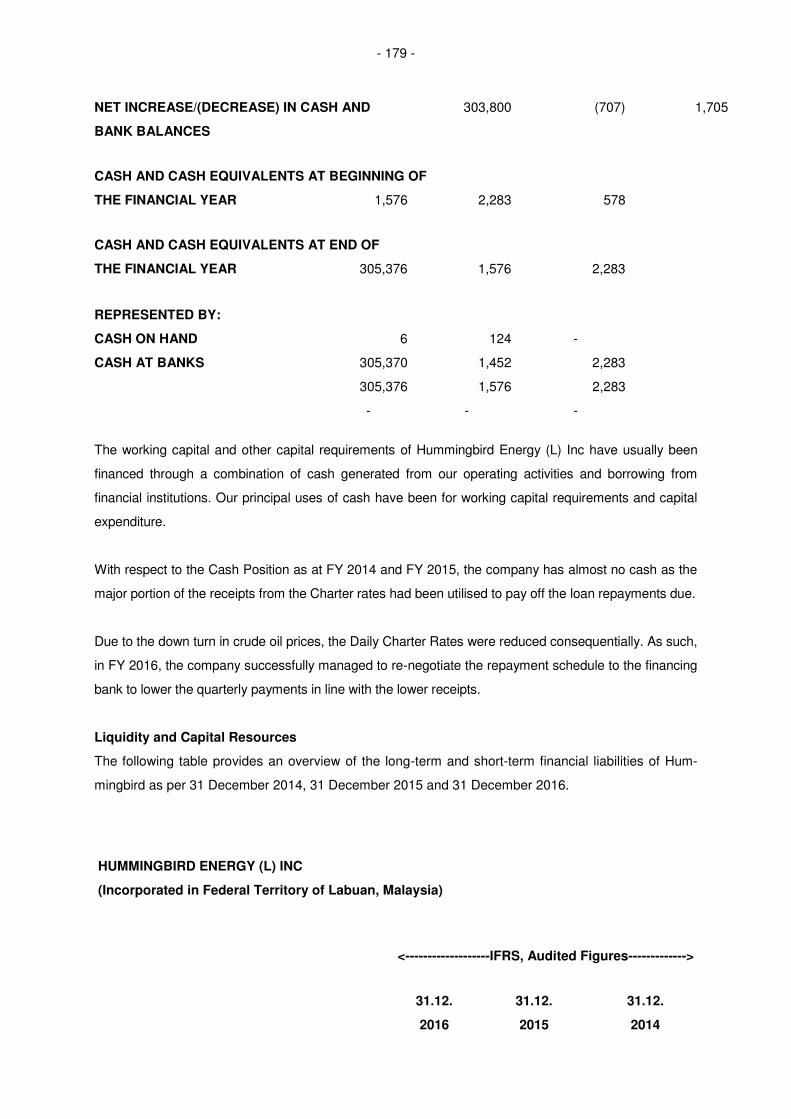

12.4.1 Results of Operation of Hummingbird Energy (L) Inc ........................................... 168

- 4 -

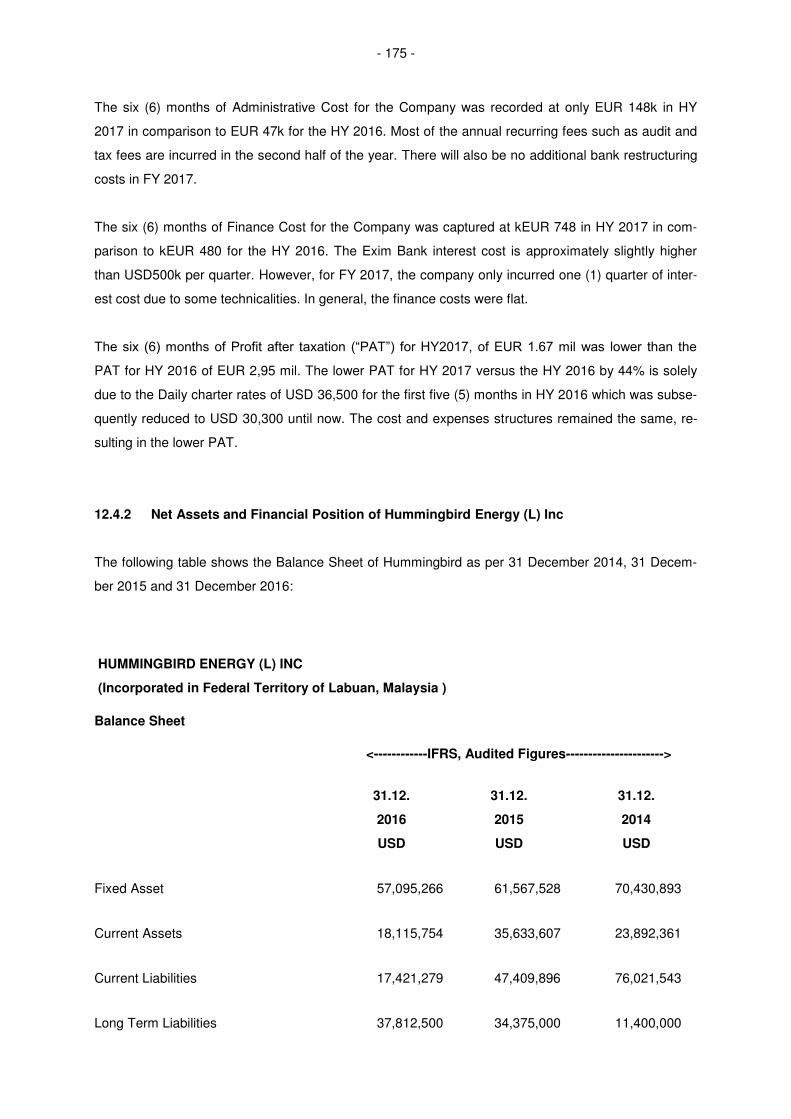

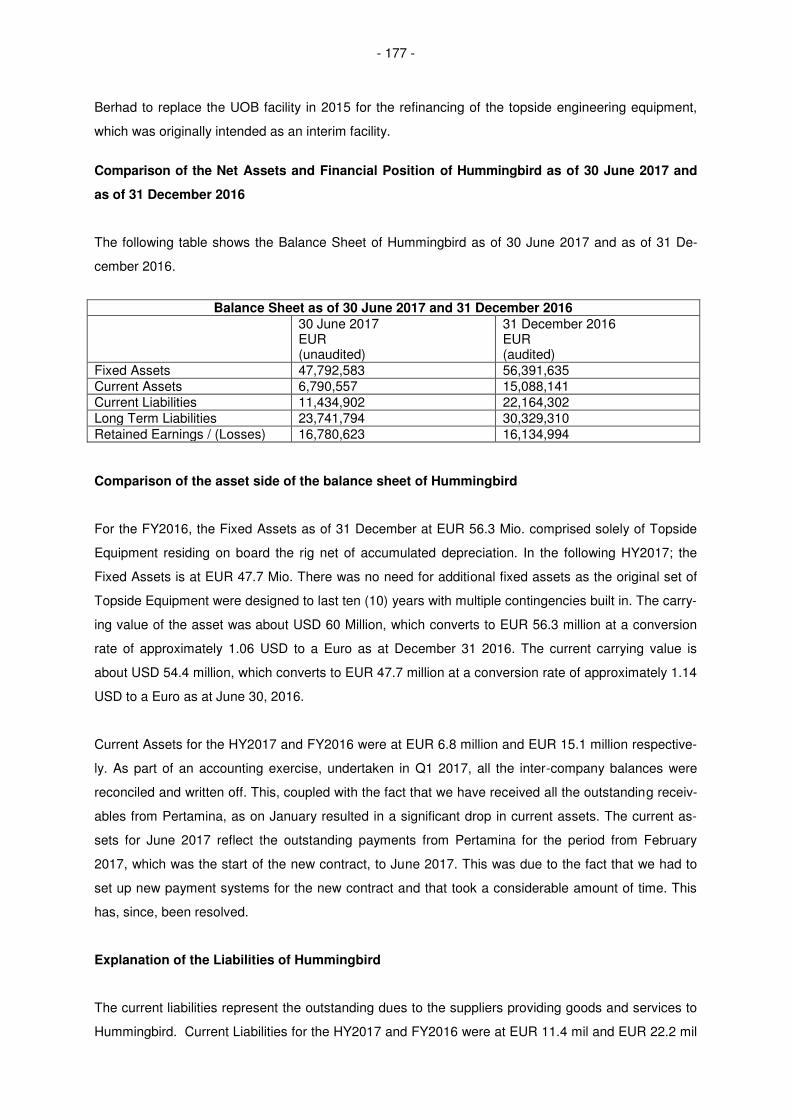

12.4.2 Net Assets and Financial Position of Hummingbird Energy (L) Inc ...................... 175

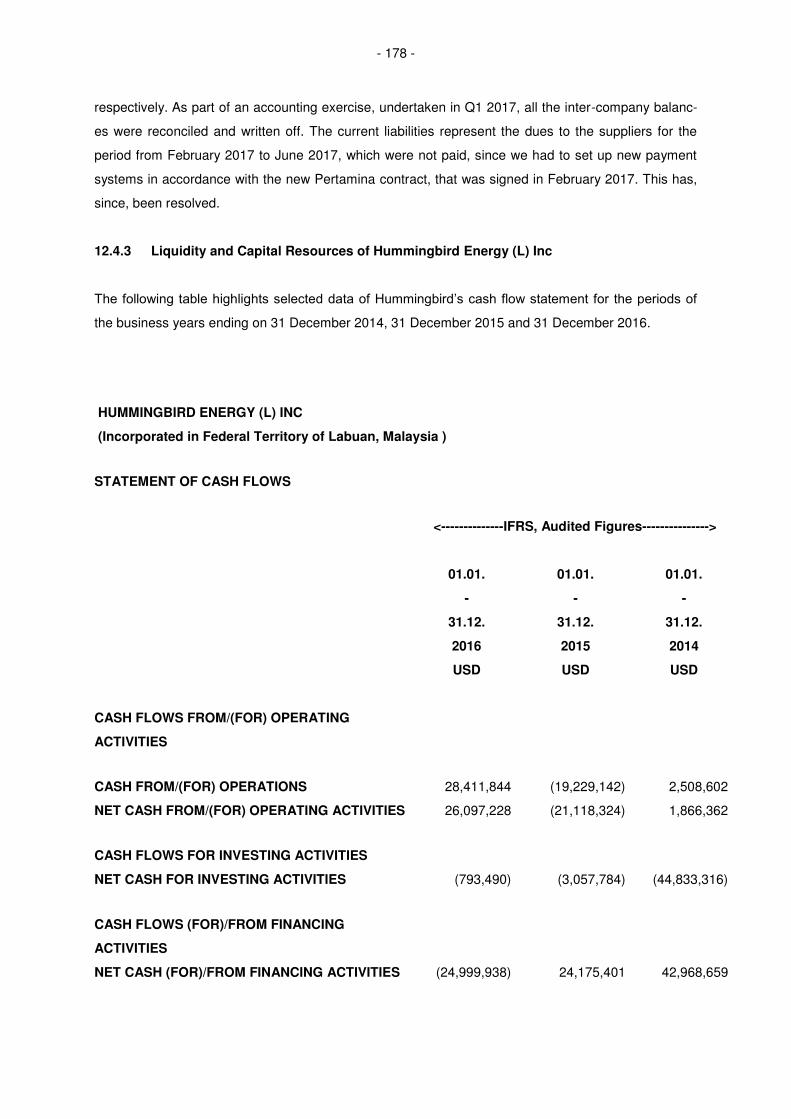

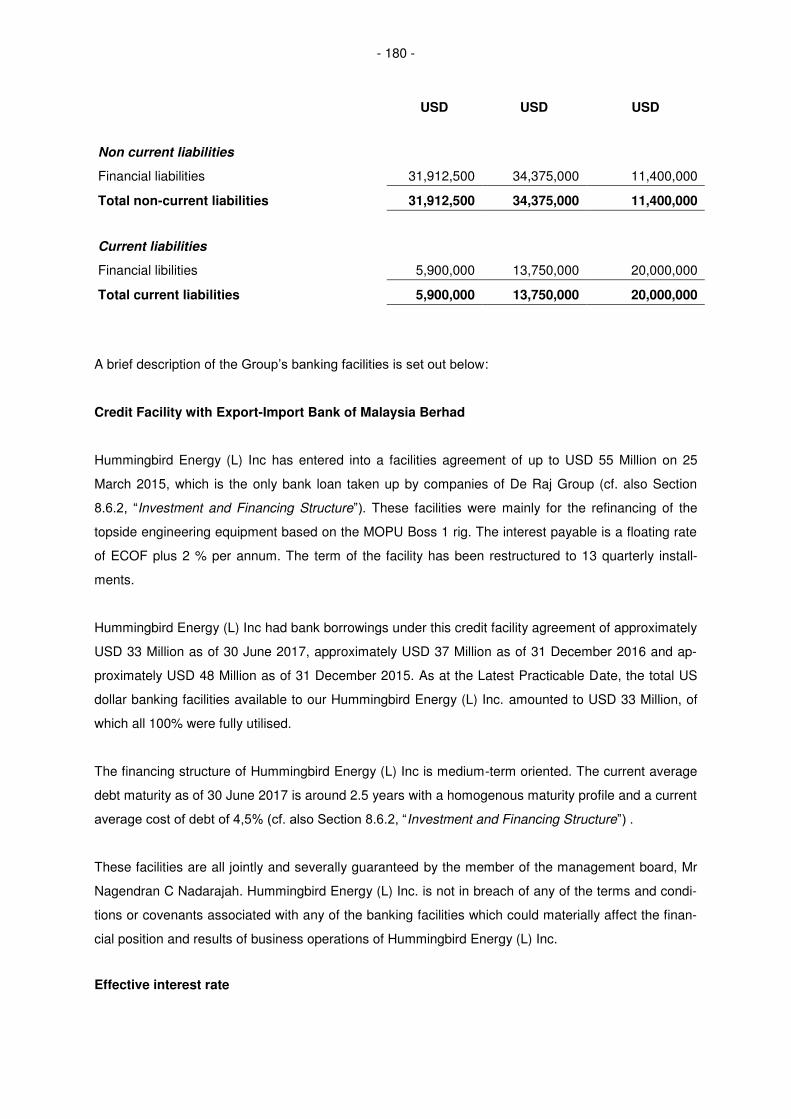

12.4.3 Liquidity and Capital Resources of Hummingbird Energy (L) Inc ......................... 178

12.5 Management Discussion and Analysis of Gryphon Energy (SEA) Sdn Bhd ........ 181

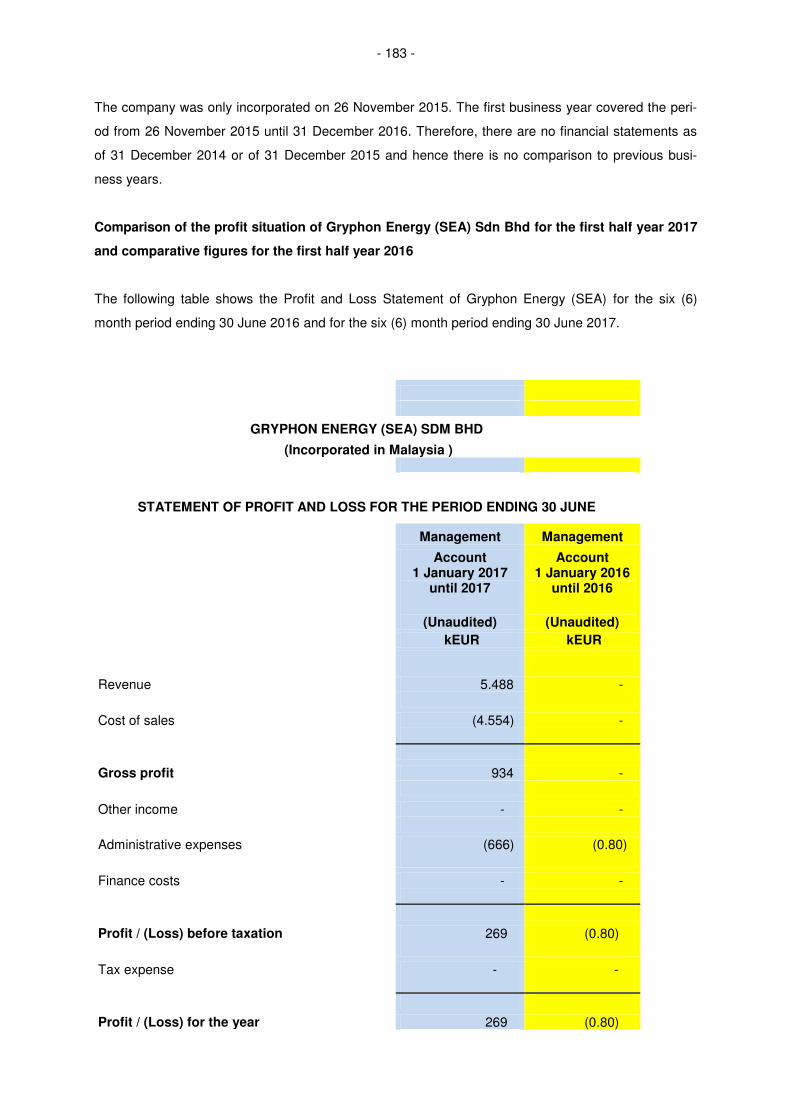

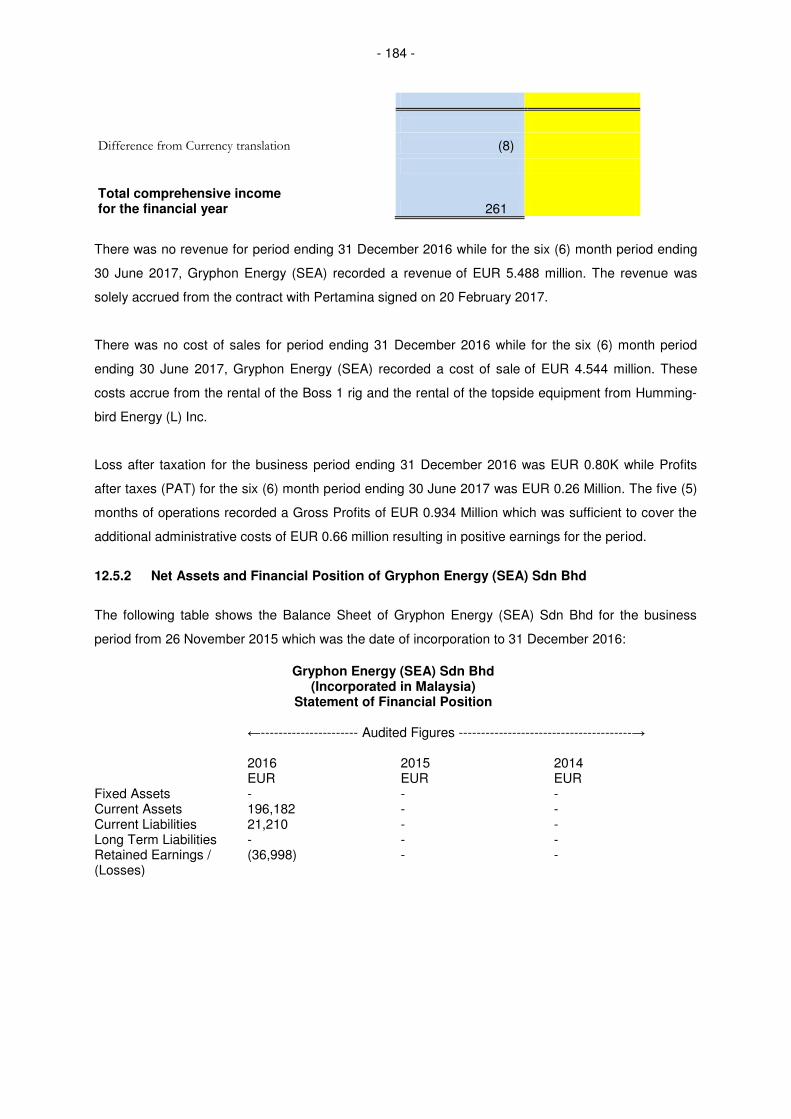

12.5.1 Results of Operation of Gryphon Energy (SEA) Sdn Bhd .................................... 181

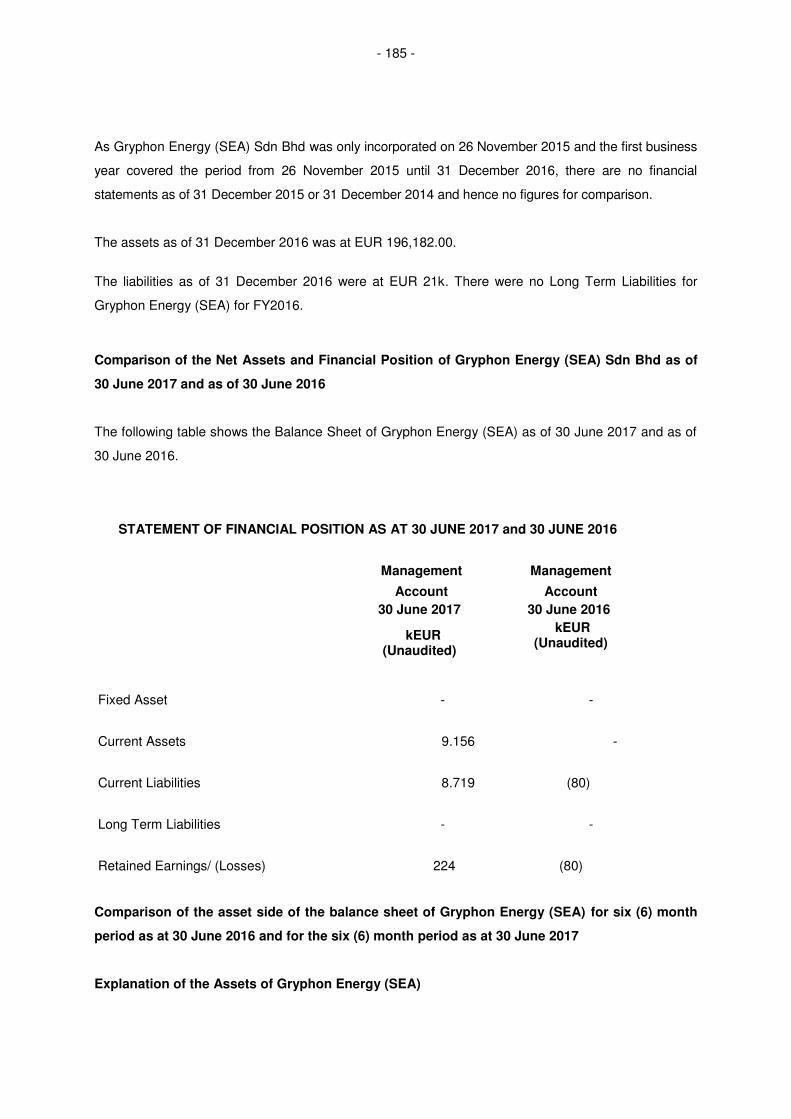

12.5.2 Net Assets and Financial Position of Gryphon Energy (SEA) Sdn Bhd ............... 184

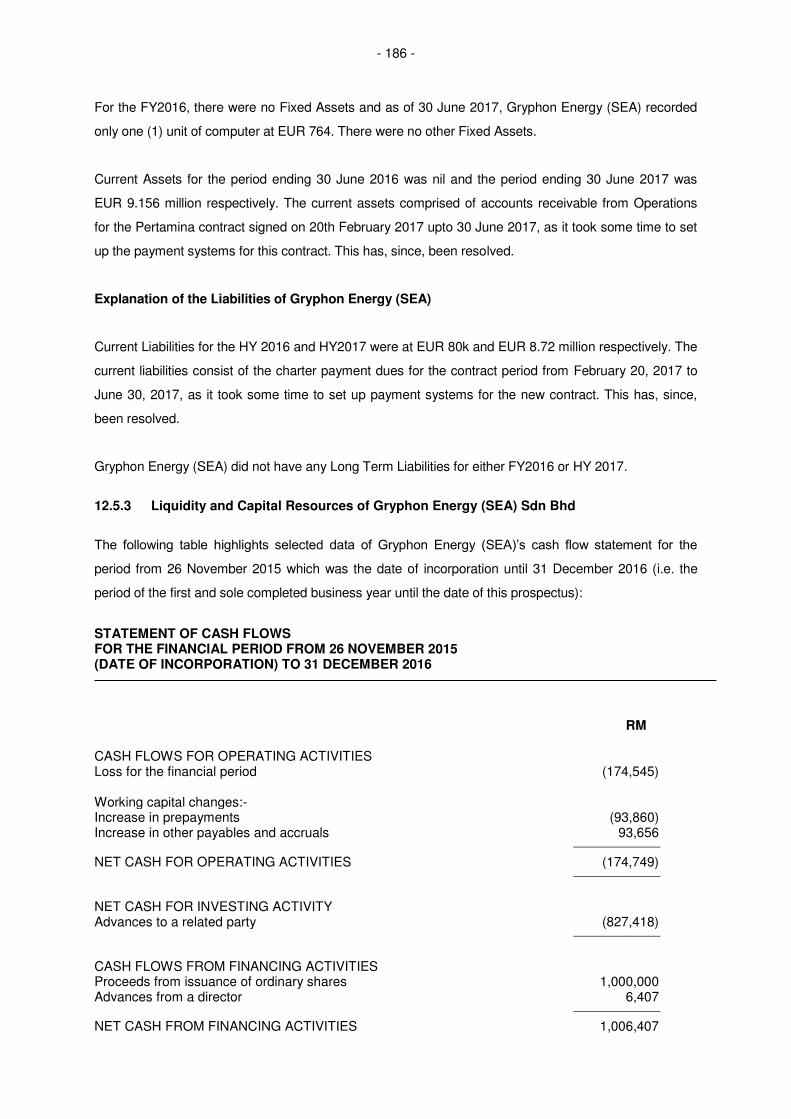

12.5.3 Liquidity and Capital Resources of Gryphon Energy (SEA) Sdn Bhd .................. 186

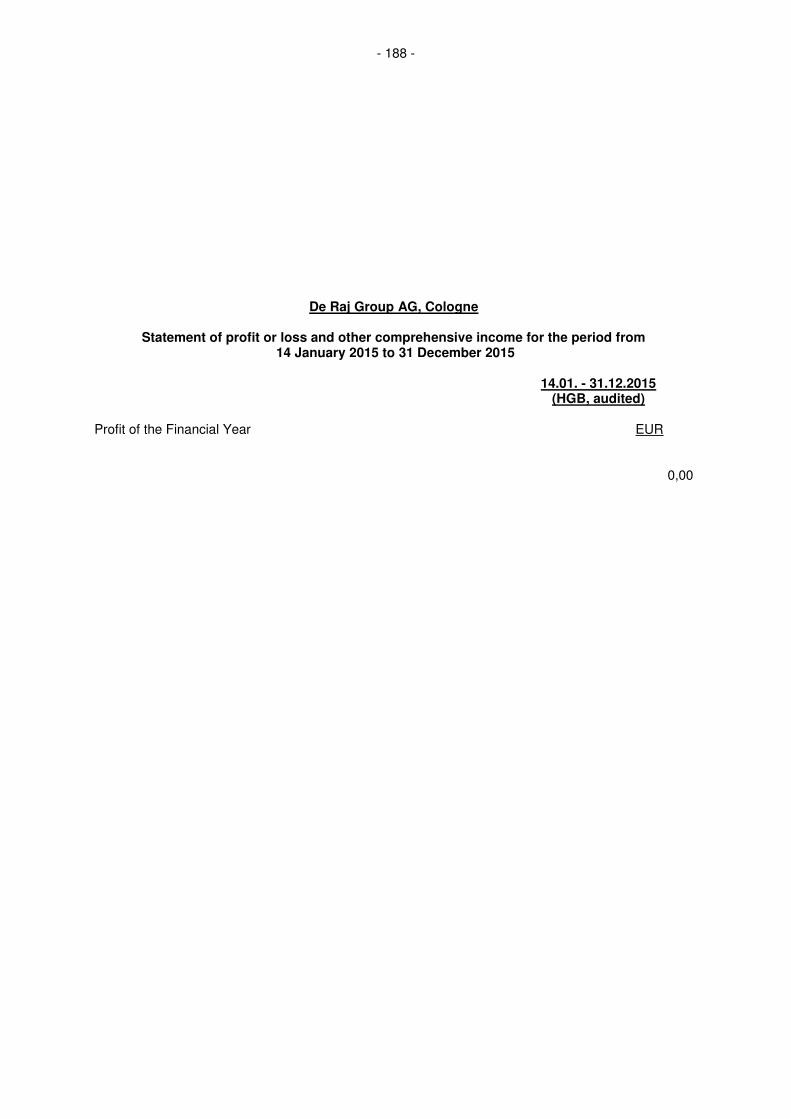

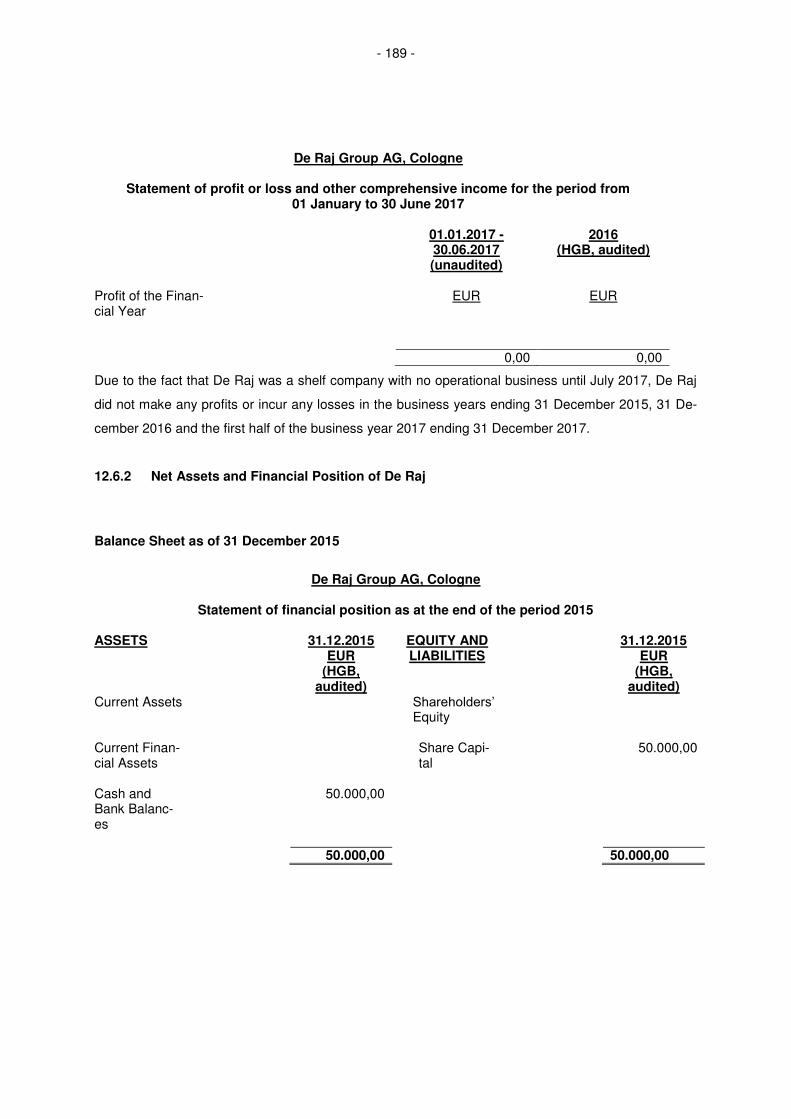

12.6 Management Discussion and Analysis of De Raj Group AG ............................... 187

12.6.1 Results of Operation of De Raj Group AG ............................................................ 187

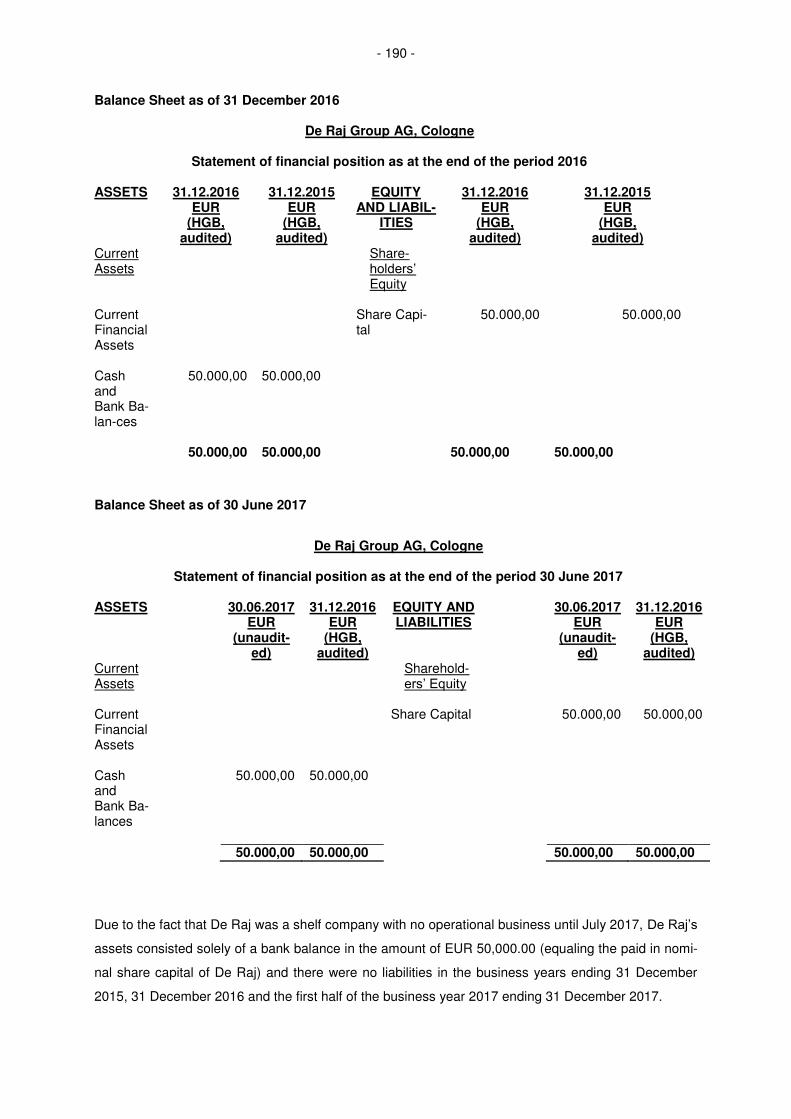

12.6.2 Net Assets and Financial Position of De Raj ........................................................ 189

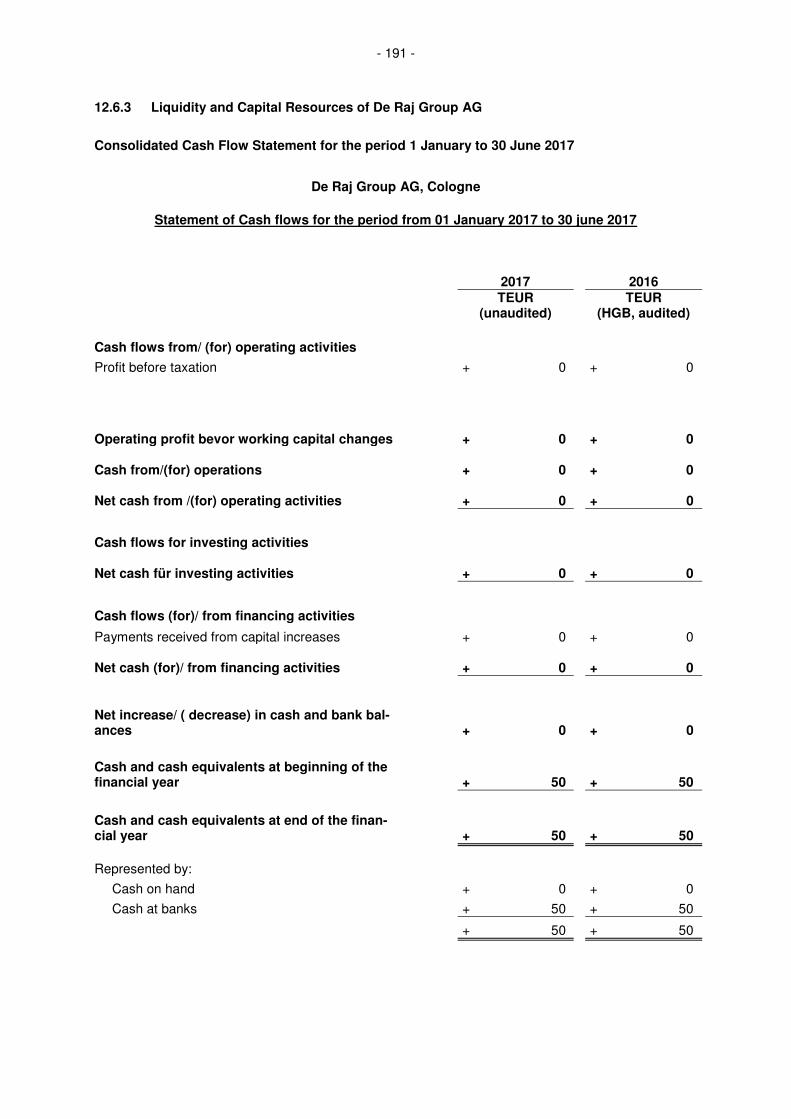

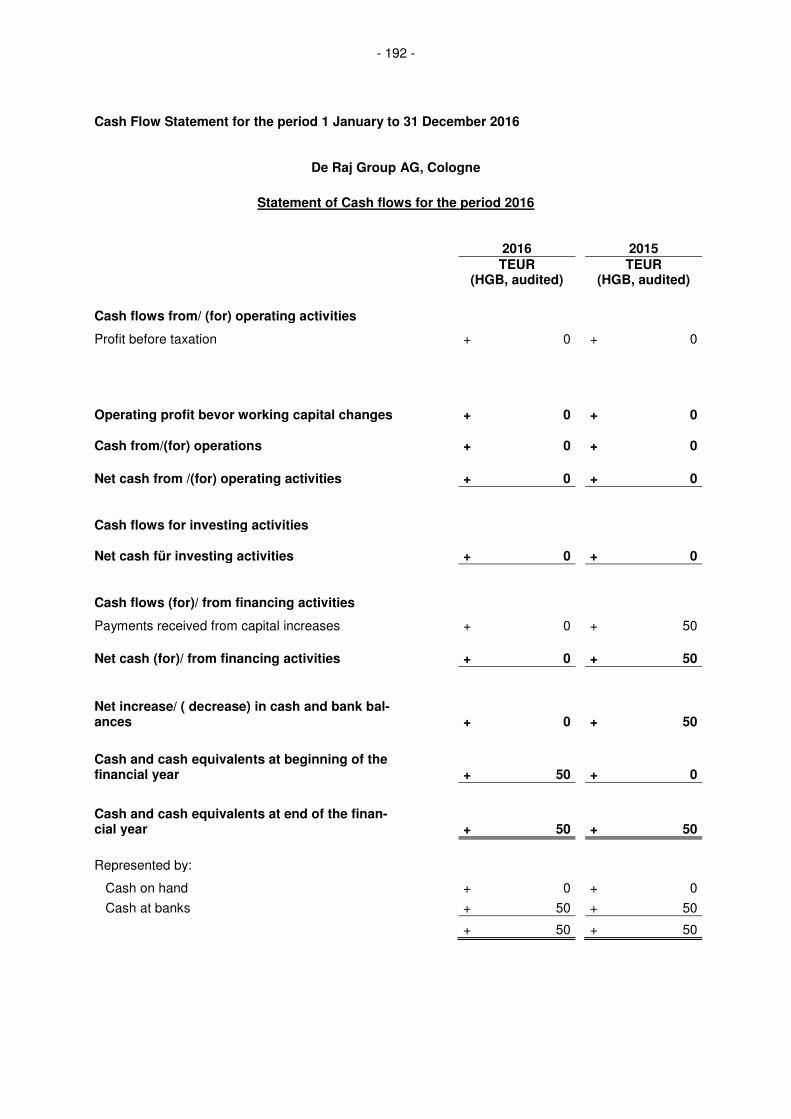

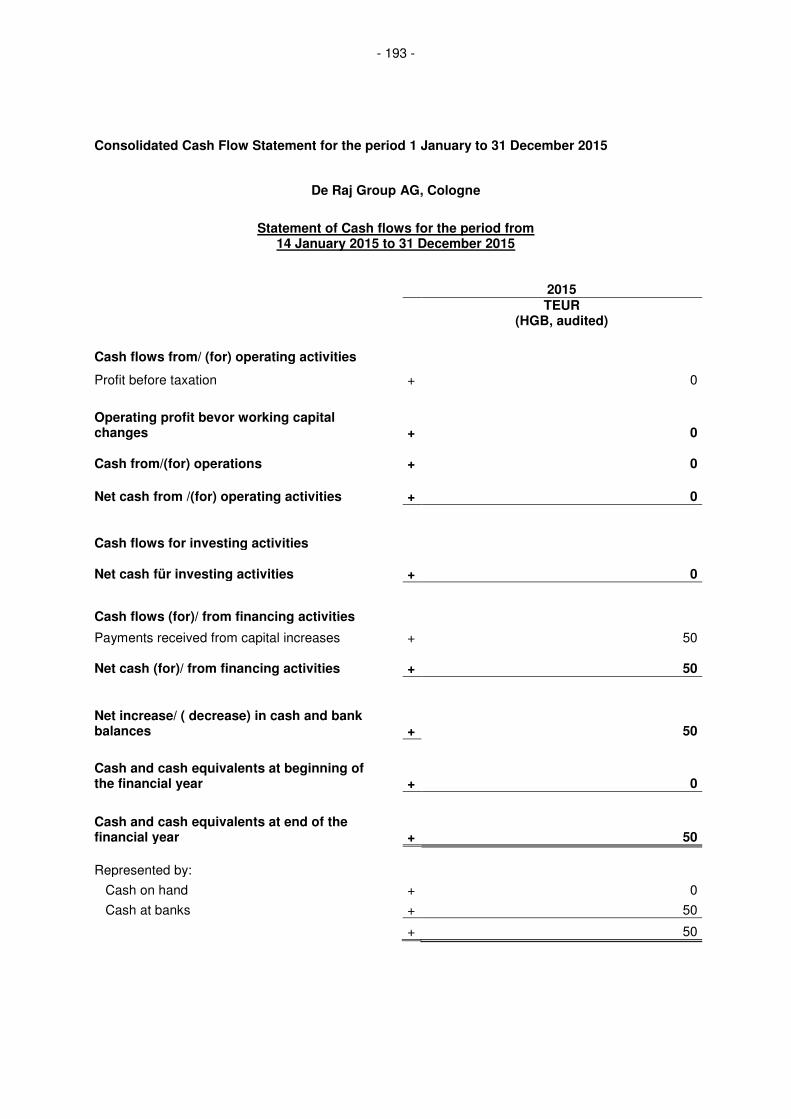

12.6.3 Liquidity and Capital Resources of De Raj Group AG .......................................... 191

12.7 Further Information on De Raj Group ................................................................... 194

12.7.1 Liquidity and Capital Resources of De Raj Group ................................................ 194

12.7.2 Profit participation rights, Mezzanine finance instruments and Corporate Bonds of

De Raj Group ........................................................................................................ 194

12.7.3 Maturity Analysis of De Raj Group and effective interest rate of De Raj Group ... 194

12.7.4 Shareholders’ Equity of De Raj Group ................................................................. 194

12.7.5 Contingent Liabilities and Other Financial Obligations of De Raj Group .............. 194

12.7.6 Investments of De Raj Group ............................................................................... 194

12.7.7 Pensions and Retirement Payments of De Raj Group ......................................... 195

12.7.8 Qualitative and quantitative information on market risks of De Raj Group ........... 195

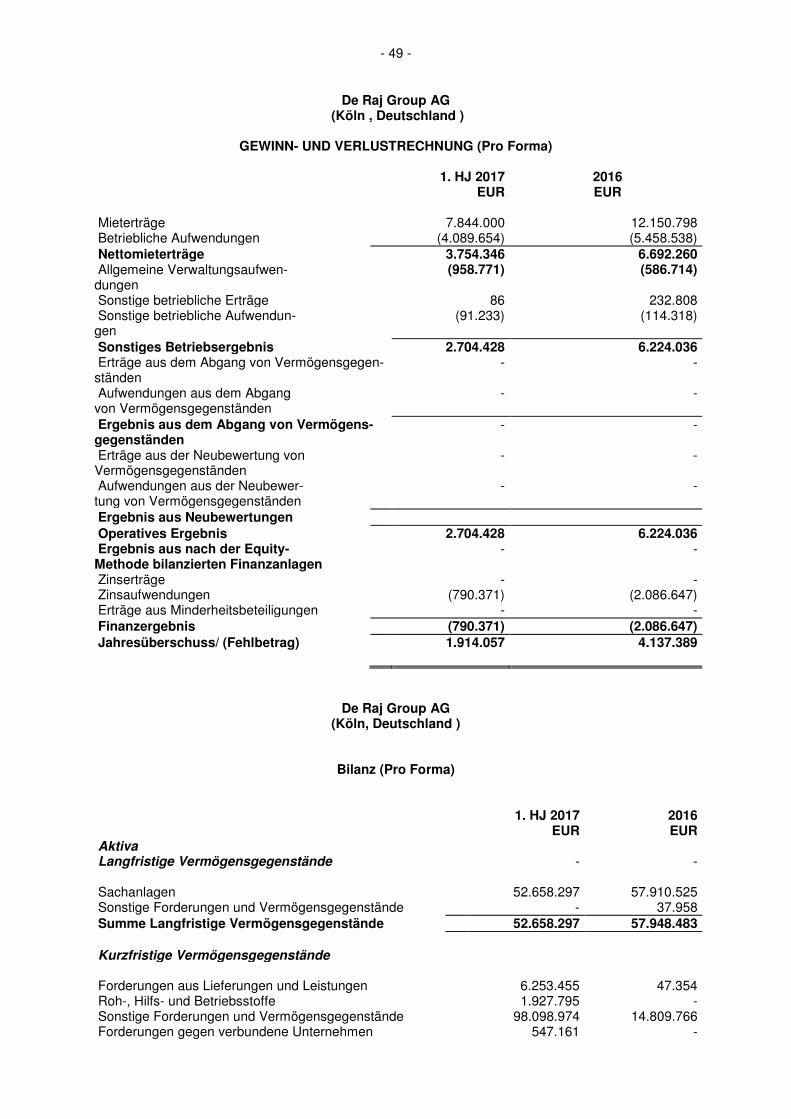

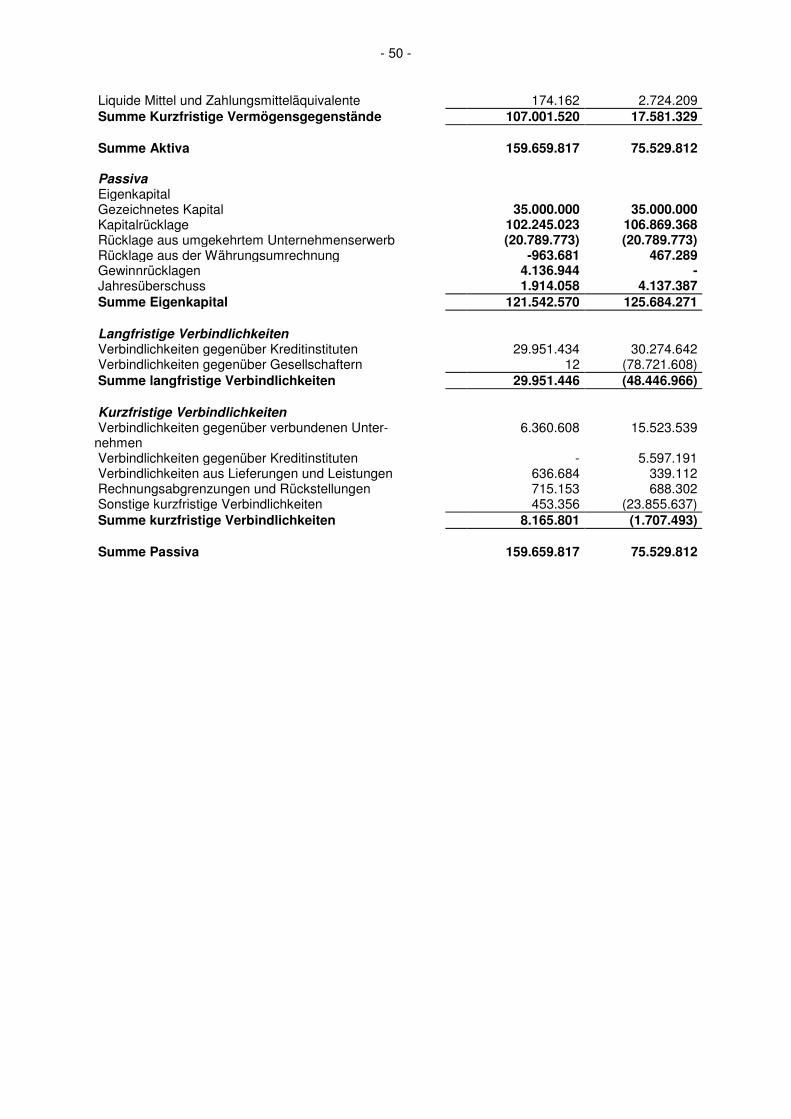

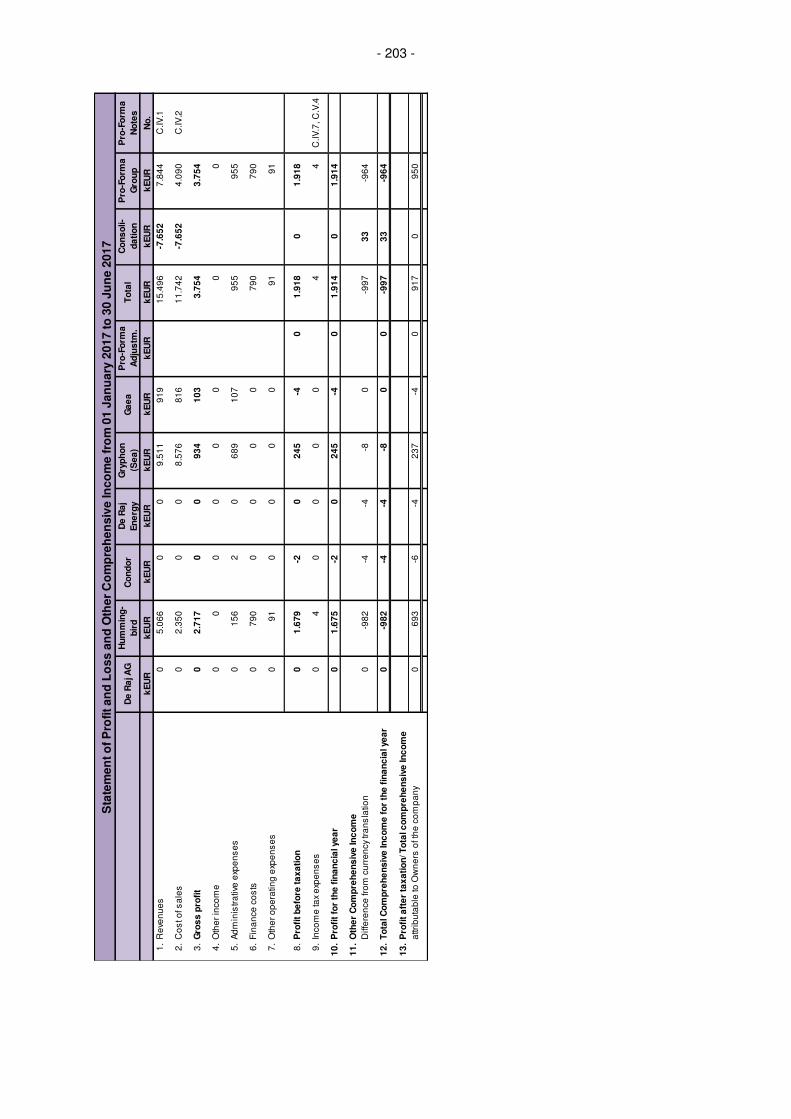

13. PRO-FORMA CONSOLIDATED FINANCIAL INFORMATION OF DE RAJ GROUP ....... 196

13.1 Introduction ........................................................................................................... 196

13.2 Pro-forma consolidated accounts and notes ........................................................ 197

13.3 Auditor’s Report to the Pro-forma consolidated financial information .................. 215

14. EXPLANATORY REMARKS ON THE PRO-FORMA FINANCIAL INFORMATION OF DE

RAJ GROUP ........................................................................................................................ 217

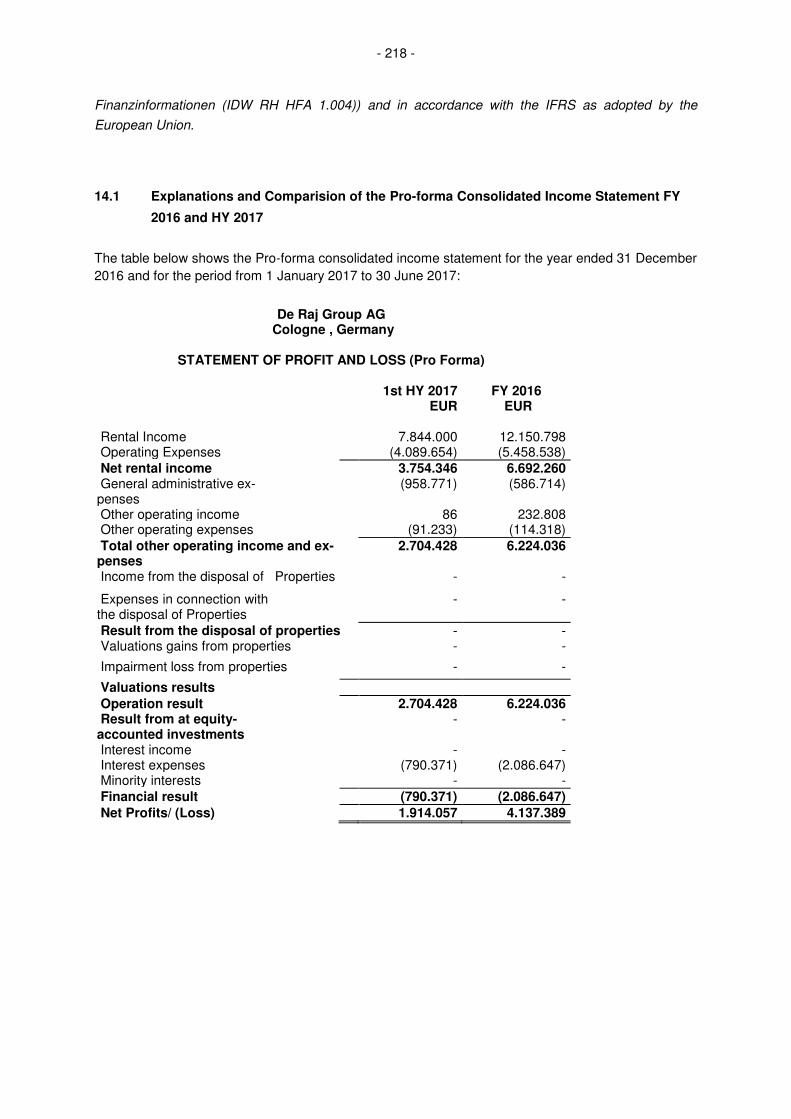

14.1 Explanations and Comparision of the Pro-forma Consolidated Income Statement

FY 2016 and HY 2017 .......................................................................................... 218

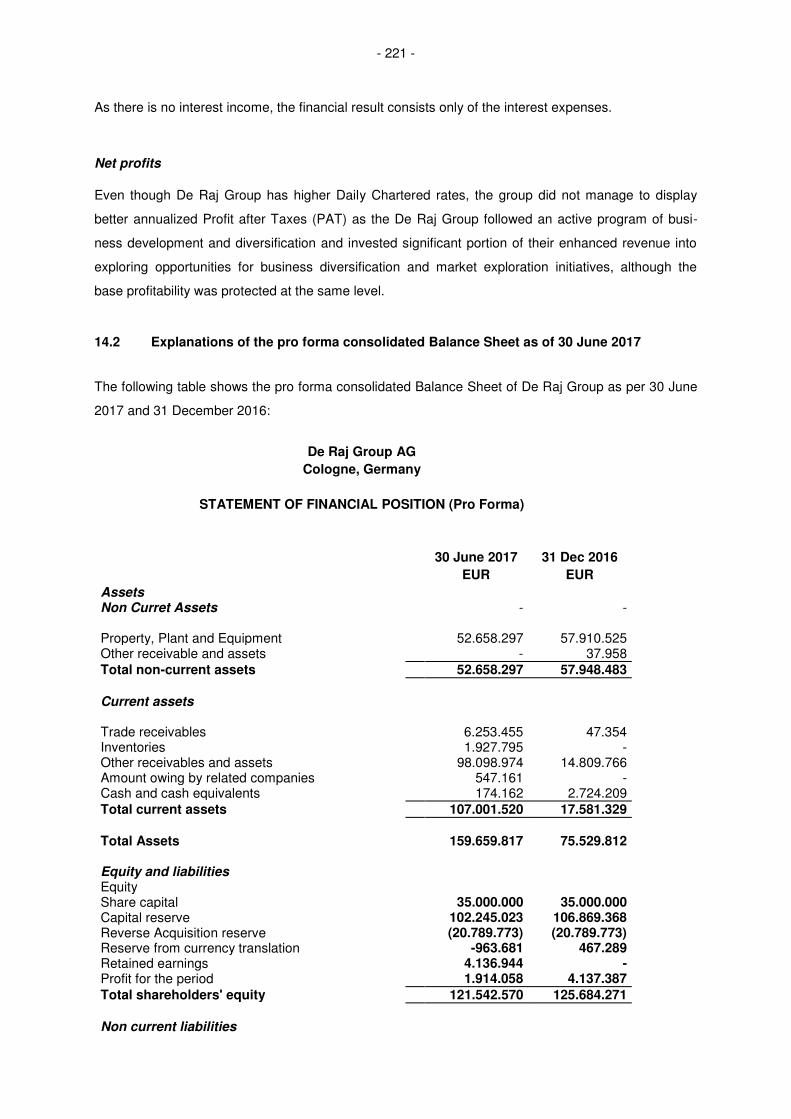

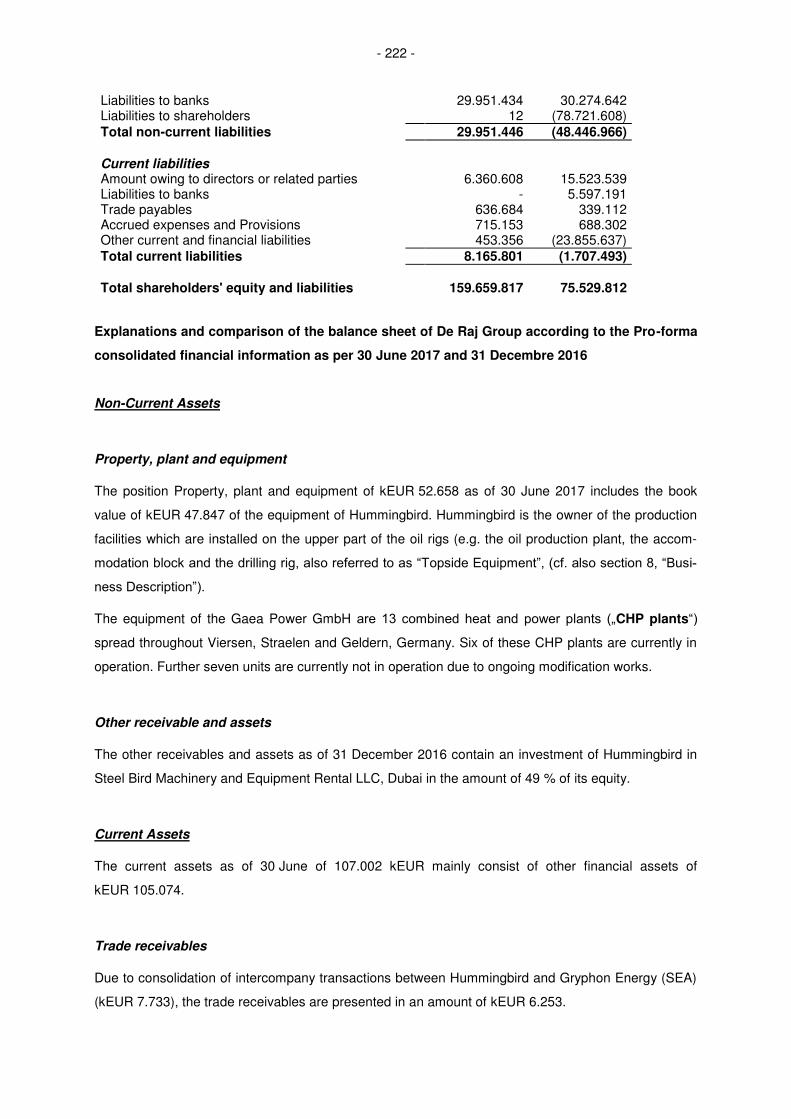

14.2 Explanations of the pro forma consolidated Balance Sheet as of 30 June 2017 . 221

15. CORPORATE BODIES ....................................................................................................... 227

15.1 Overview ............................................................................................................... 227

15.2 The Management Board ....................................................................................... 228

15.3 The Supervisory Board ......................................................................................... 235

15.4 Shareholders’ Meeting .......................................................................................... 241

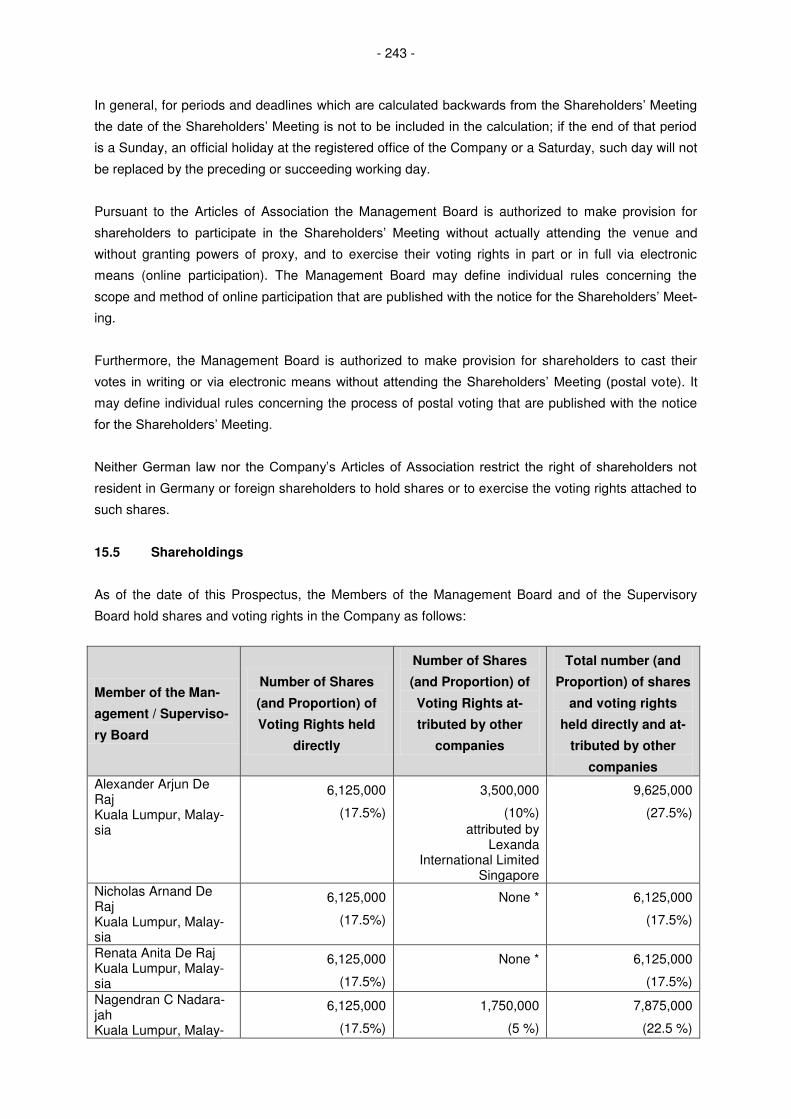

15.5 Shareholdings ....................................................................................................... 243

15.6 Corporate Governance ......................................................................................... 244

16. MAJOR SHAREHOLDERS AND LEGAL RELATIONSHIPS WITH RELATED PARTIES 246

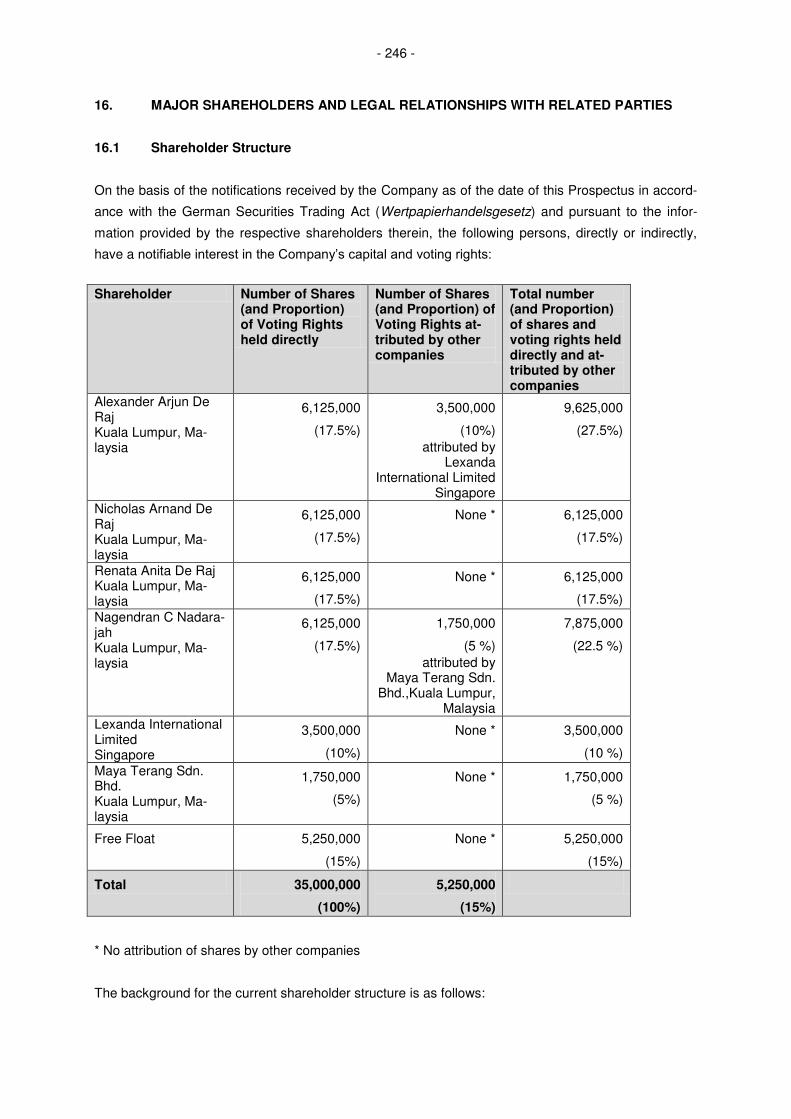

16.1 Shareholder Structure ........................................................................................... 246

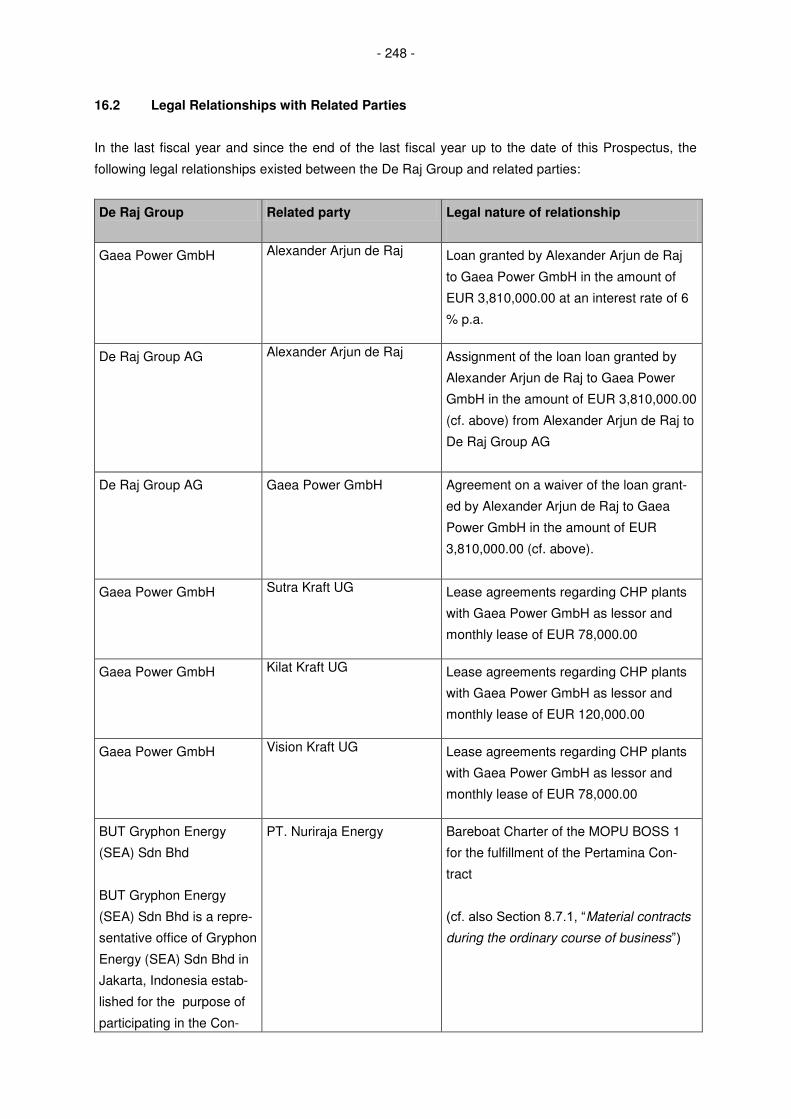

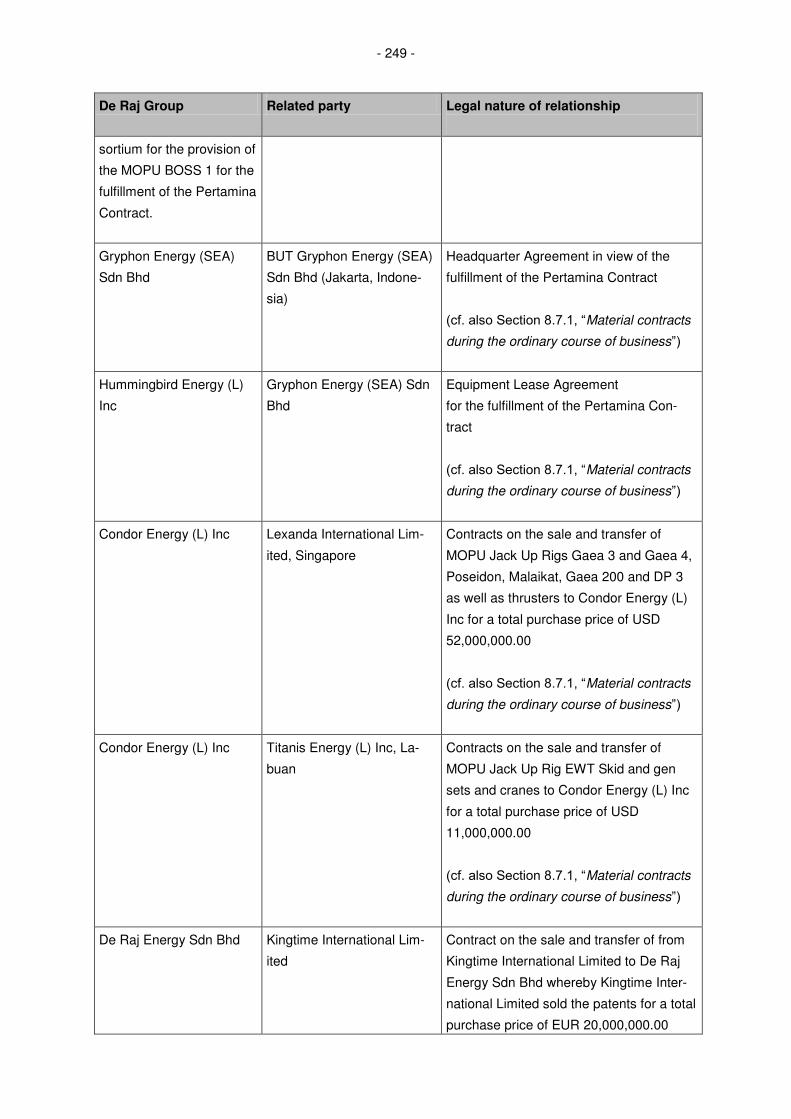

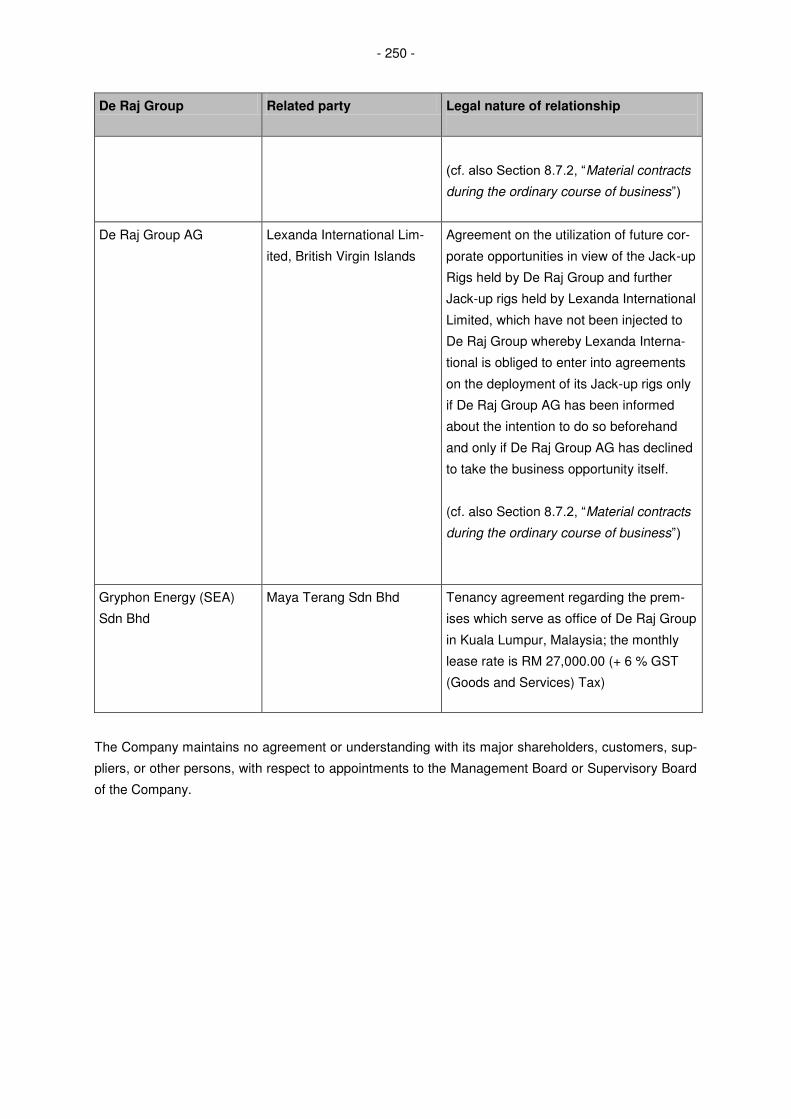

16.2 Legal Relationships with Related Parties ............................................................. 248

17. INFORMATION ON THE CAPITAL OF THE COMPANY ................................................... 251

- 5 -

17.1 Issued Share Capital and Shares ......................................................................... 251

17.2 Authorized Capital ................................................................................................ 251

17.3 Contingent Capital ................................................................................................ 253

17.4 General Provisions on Changes in the Share Capital .......................................... 256

17.5 General Provisions Governing Subscription Rights ............................................. 257

17.6 Treasury Shares ................................................................................................... 258

17.7 Shareholding Notification and Disclosure Requirements ..................................... 258

17.8 Duty to Submit a Public Offer ............................................................................... 259

17.9 Exclusion of Minority Shareholders ...................................................................... 259

17.10 Disclosure of Directors’ Dealings .......................................................................... 261

18. THIRD PARTY INTERESTS ................................................................................................ 262

19. TAXATION IN THE FEDERAL REPUBLIC OF GERMANY ............................................... 263

19.1 Taxation of the Company...................................................................................... 263

19.2 Taxation of Shareholders...................................................................................... 265

19.3 Taxation of Capital Gains ..................................................................................... 269

19.4 Special Treatment of Companies in the Financial and Insurance Sectors and

Pension Funds ...................................................................................................... 273

19.5 Inheritance and Gift Tax ....................................................................................... 274

19.6 Other Taxes .......................................................................................................... 274

- 6 -

FINANCIAL INFORMATION.………………………………………………………………………....……F-1

• Unaudited Interim Financial Information of De Raj Group AG for the six-months-period ended

June 30, 2017 (HGB) ............................................................................................................ F-4

• Audited Financial Statements of De Raj Group AG for the financial year ended

31 December 2016 (HGB) .................................................................................................. F-10

• Audited Financial Statements of De Raj Group AG for the abbreviated financial year ended

31 December 2015 (HGB) .................................................................................................. F-17

• Unaudited Interim Financial Information of Hummingbird Energy (L) Inc. for the six-months-

period ended June 30, 2017 (IFRS) .................................................................................... F-24

• Audited Financial Statements of Hummingbird Energy Inc. for the financial year ended

31 December 2016 (IFRS) .................................................................................................. F-40

• Audited Financial Statements of Hummingbird Energy Inc. for the financial year ended

31 December 2015 (IFRS) .................................................................................................. F-71

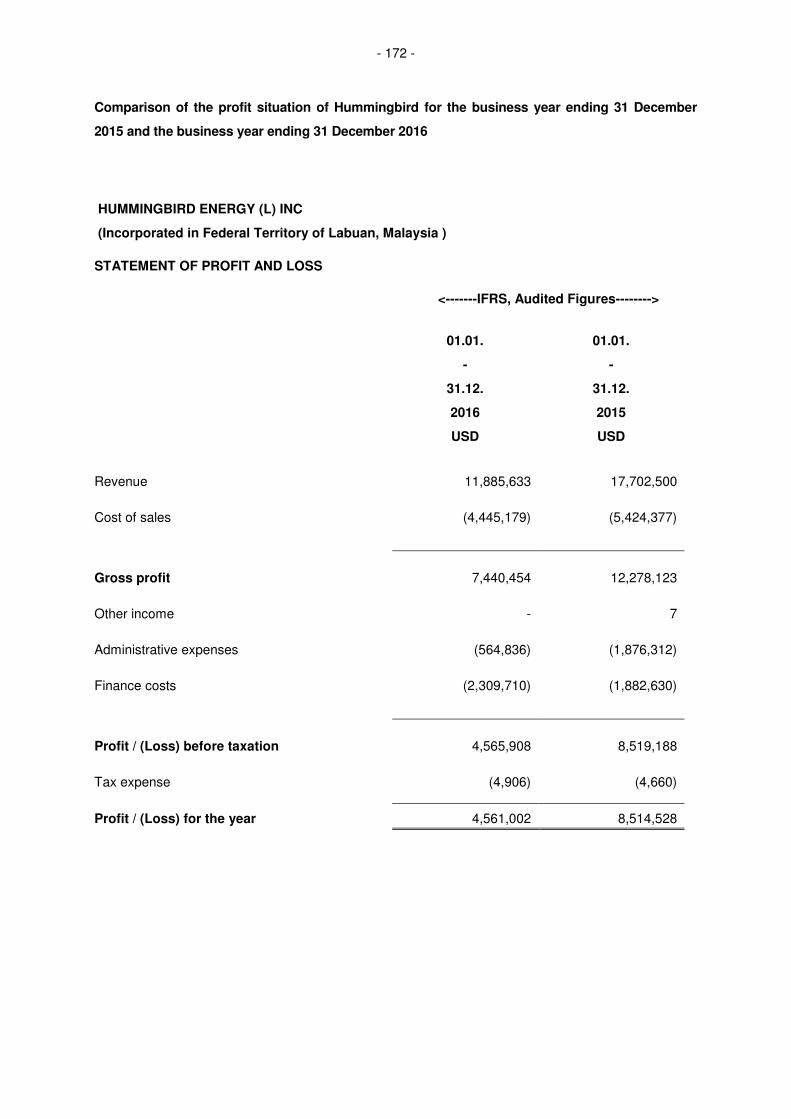

• Audited Financial Statements of Hummingbird Energy Inc. for the financial year ended 31

December 2014 (IFRS) ....................................................................................................... F-99

• Unaudited Interim Financial Information of Gryphon Energy (SEA) Sdn Bhd for the six-

months-period ended June 30, 2017 (IFRS) .................................................................... F-126

• Audited Financial Statements of Gryphon Energy (SEA) Sdn Bhd for the financial year start-

ed from 26 November 2015 and ended on 31 December 2016 (IFRS) ............................ F-131

RECENT DEVELOPMENTS AND OUTLOOK ....................................................................................O-1

- 7 -

1. SUMMARY OF THE PROSPECTUS Summaries to Securities Prospectuses are made up of disclosure requirements known as elements (“El-ements”). These Elements are numbered in sections A – E (A.1 – E.7). This summary contains all the Elements required to be included in a summary of this type of securities and issuer. Because some Ele-ments are not required to be addressed, there may be gaps in the numbering sequence of the Elements. Even though an Element may be required to be inserted in the summary because of the type of securities and issuer, it is possible that no relevant information can be given regarding the Element. In this case, a short description of the Element is included in the summary with the mention of “not applicable”.

A - Introduction and Warnings

A.1 Warnings. This summary should be read as an introduction to this prospectus (the “Prospec-tus”). Any decision to invest in the securities should be based on consideration of this Prospectus as a whole by the investor.

If any claims are asserted before a court of law based on the information contained in this Prospectus, the investor appearing as plaintiff may have to bear the costs of translating this Prospectus prior to the commencement of the court proceedings pursuant to the national legislation of the member states of the European Econom-ic Area.

De Raj Group AG (the “Company”, “De Raj”, or the “Issuer”), together with ACON Actienbank, Munich, Germany (“ACON” or the “Listing Agent”) have assumed responsibility for the contents of this summary and any translation thereof pursuant to Section 5 paragraph 2b no. 4 of the German Securities Prospectus Act (Wertpa-pierprospektgesetz, “WpPG”). The persons responsible for the summary, including any translation thereof or for the issuing (Veranlassung), can be held liable but only if this summary is misleading, inaccurate or inconsistent when read together with the other parts of this Prospectus or it does not provide, when read together with the other parts of this Prospectus, all necessary key information.

A.2 Information regarding the subse-quent use of the Pro-spectus.

Not applicable. Consent regarding the use of this Prospectus for a subsequent resale or placement of the shares has not been granted.

B - Issuer B.1 Legal and

commercial name.

The Company’s legal and commercial name is De Raj Group AG.

B.2 Domicile, legal form, legislation under which the issuer operates, country of incorpora-tion.

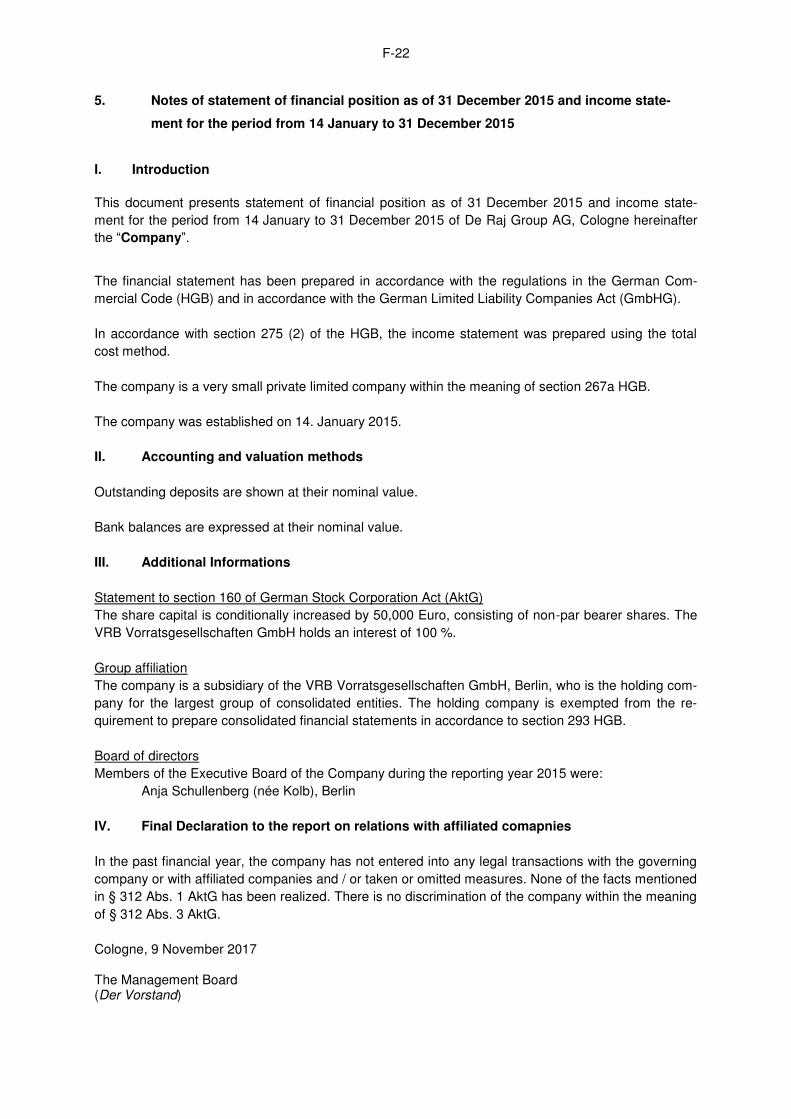

The Company has its registered seat in Cologne, Germany, (business address: c/o Heuking Kühn Lüer Wojtek, Magnusstr. 13, 50672 Cologne) and is registered with the commercial register of the local court (Amtsgericht) of Cologne, Germany, un-der the number HRB 92007. The Company is a German Stock Corporation (Ak-tiengesellschaft, AG) incorporated and existing in Germany and governed by the laws of the Federal Republic of Germany.

B.3 Current op-erations and principal business activities and princi-pal markets in which the issuer com-petes.

De Raj is the parent company of the companies Gryphon Energy (SEA) Sdn Bhd, Hummingbird Energy (L) Inc, Condor Energy (L) Inc, De Raj Energy Sdn Bhd and Gaea Power GmbH (“De Raj Group”). De Raj Group’s business is focussed on the oil and gas business in the South East Asian region and on the power business in Germany. Oil and Gas Division The oil and gas division of the De Raj Group is a service provider providing ser-vices encompassing the full spectrum of the offshore upstream oil and gas supply chain. The division is capable of being involved in (1) offshore exploration which involves the search for rock formations associated

with oil or natural gas deposits, and includes geophysical prospecting and/or exploratory drilling,

(2) well development, which occurs after exploration has located an economical-ly recoverable field, and involves the construction of one or more wells from the beginning (so-called “spudding”) to either abandonment if no hydrocar-

- 8 -

bons are found, or to well completion if hydrocarbons are found in sufficient quantities,

(3) production, which is the process of extracting the hydrocarbons and separat-ing the mixture of liquid hydrocarbons, gas, water, and solids, removing the constituents that are non-saleable, and selling the liquid hydrocarbons and gas

and, finally, (4) site abandonment which involves plugging the well(s) and restoring the site

when a recently-drilled well lacks the potential to produce economic quanti-ties of oil or gas, or when a production well is no longer economically viable for production.

The oil and gas division of De Raj Group provides a high quality, comprehensive and cost effective solution for the monetization of oil and gas fields. The clients of the oil and gas division of De Raj Group AG are National Oil Companies (“NOC’s”), companies having stakes in oil fields as well as other technological enterprises. The division is strategically placed with a full range of assets ranging from jack-up rigs (a type of mobile platform that consists of a buoyant hull fitted with a number of movable legs, capable of raising its hull over the surface of the sea (“Jack-up Rigs”)), drilling equipment, processing equipment and marine equipment which are capable of handling offshore oil and gas extraction and production for so called green fields (i.e. oil and gas fields that have not been developed yet and thus have no existing infrastructure), brown fields (i.e. oil and gas fields that have already been developed and thus have to be built around an existing infrastructure) and marginal fields (i.e. oil and gas fields located in remote locations with little or no infrastructure and of a size or nature that often makes it impossible to predict with certainty the amount or composition of recoverable hydrocarbons in place). The business concept of the oil and gas division of De Raj Group is to enter into agreements on the deployment of its oil rigs in oil and gas fields. Oil rigs consist of the platform, i.e. the jack-up rigs, and the topside construction on the jack-up rigs, i.e. the topside equipment: The buoyant hull of the Jack-up rigs enables transportation of the unit and all at-tached machinery to a desired location. Once on location the hull is raised to the required elevation above the sea surface supported by the sea bed. The legs of such units may be designed to penetrate the sea bed, may be fitted with enlarged sections or footings, or may be attached to a bottom mat. De Raj Group currently holds five Jack-up Rigs. Furthermore, De Raj Group holds and leases as lessor the production facilities which are installed on the upper part of the oil rigs, e.g. the oil production plant, the accommodation block and the drilling rig (also referred to as “Topside Equip-ment”). Moreover, the lease agreements entered into by De Raj Group may also contain not only the lease of the equipment but also the obligation to operate and maintain the oil rig during the term of its deployment (so called “wet lease”). To fulfill the obligations for the operation and maintenance, De Raj Group may employ its own employees but also assigns an agency employed work force with this task. The oil and gas division of De Raj Group AG comprises of four companies each having its own function: 1. Gryphon Energy (SEA) Sdn. Bhd employs the vast majority of the labour

workforce and functions as management arm of the oil and gas projects and general operations and enters into contracts with the clients, namely National Oil Companies (“NOC’s”).

2. Hummingbird Energy (L) Inc. owns and leases the Topside Equipment. 3. Condor Energy (L) Inc. owns the Jack-up Rigs while they are not deployed in

oil or gas fields. 4. De Raj Energy Sdn Bhd holds the patents of the oil and gas division of the

De Raj Group The main market catchment area for the oil and gas division of the De Raj Group comprises of South East Asia, Central Asia and the Middle East. However, the division has also participated in market surveys, expression of interests and pre-qualifications for NOC’s and stakeholders from Europe and West Africa. German Power Division

- 9 -

Gaea Power GmbH, a subsidiary of the Company, is the owner of 13 combined heat and power plants („CHP plants“) spread throughout Viersen, Straelen and Geldern, Germany. These CHP plants generate electricity, which is fed into the public power grid, and heat, which is delivered to nearby greenhouses. The CHP plants can be categorized into three groups based on their capacity of 330kW, 363kW and 400kW. The majority of the units owned by Gaea Power GmbH has a capacity of 400kW. However, only six CHP plants are currently in operation. Fur-ther seven units are currently not in operation due to ongoing modification works. The Group expects the recommissioning of three of these plants in fall 2017. Gaea Power GmbH does not operate the CHP plants itself, but leases them to five companies in the legal form of a German Unternehmergesellschaft (mit beschränk-ter Haftung), namely Rocky Kraft Unternehmergesellschaft (mit beschränkter Haf-tung), Freya Kraft Unternehmergesellschaft (mit beschränkter Haftung), Kilat Kraft Unternehmergesellschaft (mit beschränkter Haftung), Vision Kraft Unternehmerge-sellschaft (mit beschränkter Haftung) and Sutra Kraft Unternehmergesellschaft (mit beschränkter Haftung) which operate the plants and pay a monthly rent to Gaea. All CHP plants owned by Gaea Power GmbH are fired with palm oil and benefit from the promotion of renewables energies in Germany according to the Renewa-bles Energies Act (Erneuerbare-Energien-Gesetz – “EEG”). Currently, the German power division of De Raj Group is active in the territory northeast of Duesseldorf and close to the Dutch border, namely in Viersen, Geldern and Straelen.

B.4a Most signif-icant recent trends af-fecting the issuer and the industry in which it operates.

Since 31 December 2016, the effective date of the latest audited annual financial statement, the overall global economic outlook remains strong and the cyclical recovery continues. While there has been a better than expected growth rate in Malaysia, the growth in Indonesia has stalled in 2017. Oil prices have receded, reflecting strong inventory levels in the United States and a pickup in supply. However, Brent Crude Oil prices rose in recent weeks due to developments related to Hurricanes Harvey and Irma, as well as higher refinery demand in Europe and Asia. Since 31 December 2016, the following circumstances have occurred, which were of major relevance for the Company and De Raj Group: In February and June 2017, the companies of the oil and gas division of the De Raj Group entered into agreements for the deployment of an oil rig offshore Indonesia which constitute the main sources of revenue for De Raj Group at the moment. In April 2017, the loan facility granted for the financing of the business activities of the oil and gas division of De Raj Group was successfully restructured by way of a restructuring agreement with the bank granting the facility. In July 2017, the German power division of De Raj Group entered into several lease agreements on its combined heat and power plants. In October 2017, Alexander Arjun de Raj assigned a loan in the amount of EUR 3,810,000.00, which was granted to Gaea Power GmbH, to De Raj Group AG which was subsequently waived by De Raj Group AG. Finally, in October 2017 the shares in the other companies of the De Raj Group were contributed to the Company, partly by way of a capital increase against con-tribution in kind and partly by way of a contribution into the capital reserves of the Company, whereby the De Raj Group was formed. Furthermore, it is to be noted that some of the companies of De Raj Group acquired assets, i,e. Jack-up Rigs and patents, shortly before the contribution of their shares into the Company. One of the most significant developments for the De Raj Group since 31 December 2016, is the increase in the day-rates for the BOSS-1 oil rig, deployed in Indonesia and operated by De Raj Group from around USD 36,027 per day to USD 52,000 per day from 20 February 2017 on. This reflects the positive mood of the Oil & Gas industry in general and South East Asian prospects in particular. The Group had also undertaken significant cost saving measures, especially in the area of Operations and Maintenance of the assets, to cope with the negative price cycle, which are resulting in enhanced profitability now. De Raj Group is of the opinions that it has proven itself in the South East Asia re-gion to be a cost effective and an expedient contract partner. The next plan of ac-tion is to market these technologies to a wider global market. De Raj Group expects a serious upturn and to have at least four rigs in operations

- 10 -

by year 2019 whereby the time gap is caused by the current requirement for cus-tomisation and refurbishment of the oil rigs at qualified shipyards. De Raj Group aims to expand rapidly its power generation portfolio in Germany, based on a proven and cash flow positive business model by 2018. The German Power division will also opportunistically expand horizontally and ver-tically in Germany, i.e. into grid supportive and utility bankrolled large energy stor-age facilities and technologies. Besides expanding its existing business, De Raj Group generally also observes the markets to validate potential further business opportunities and worthwhile chances to extend its business to further business sectors in the future, namely investments in conventionally generated power in the Middle East markets and supportive infra-structure.

B.5 Description of the group and the is-suer’s posi-tion within the group.

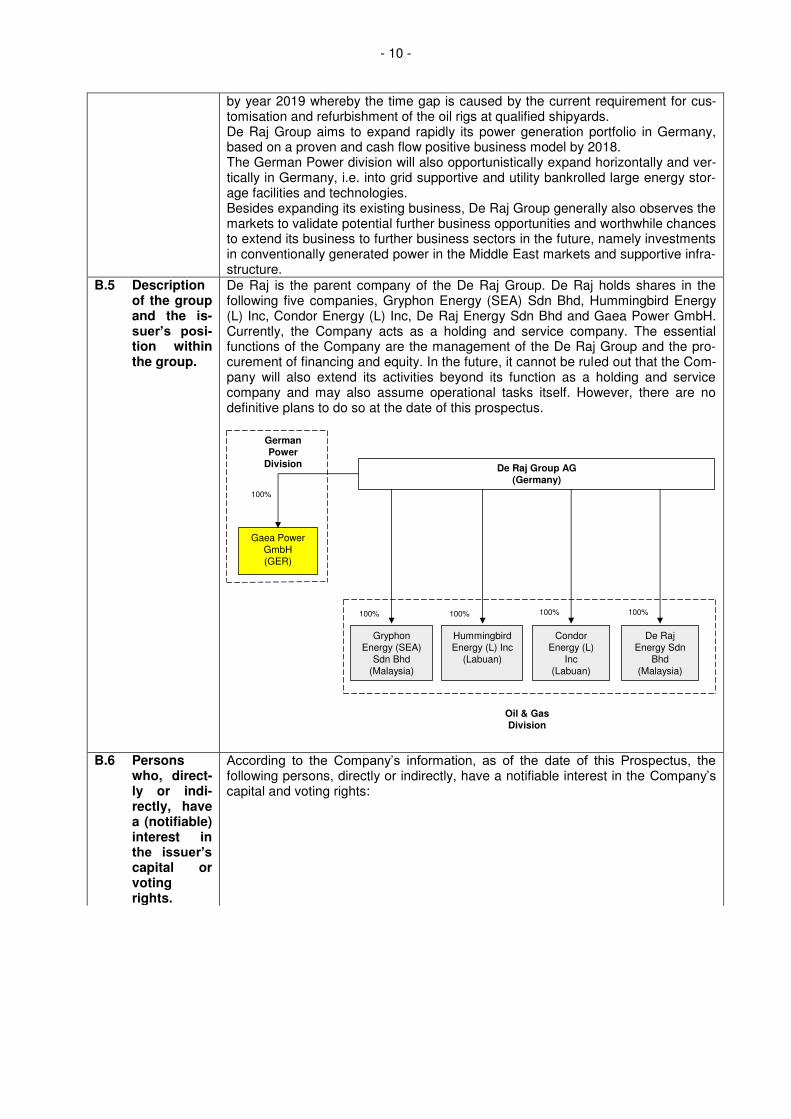

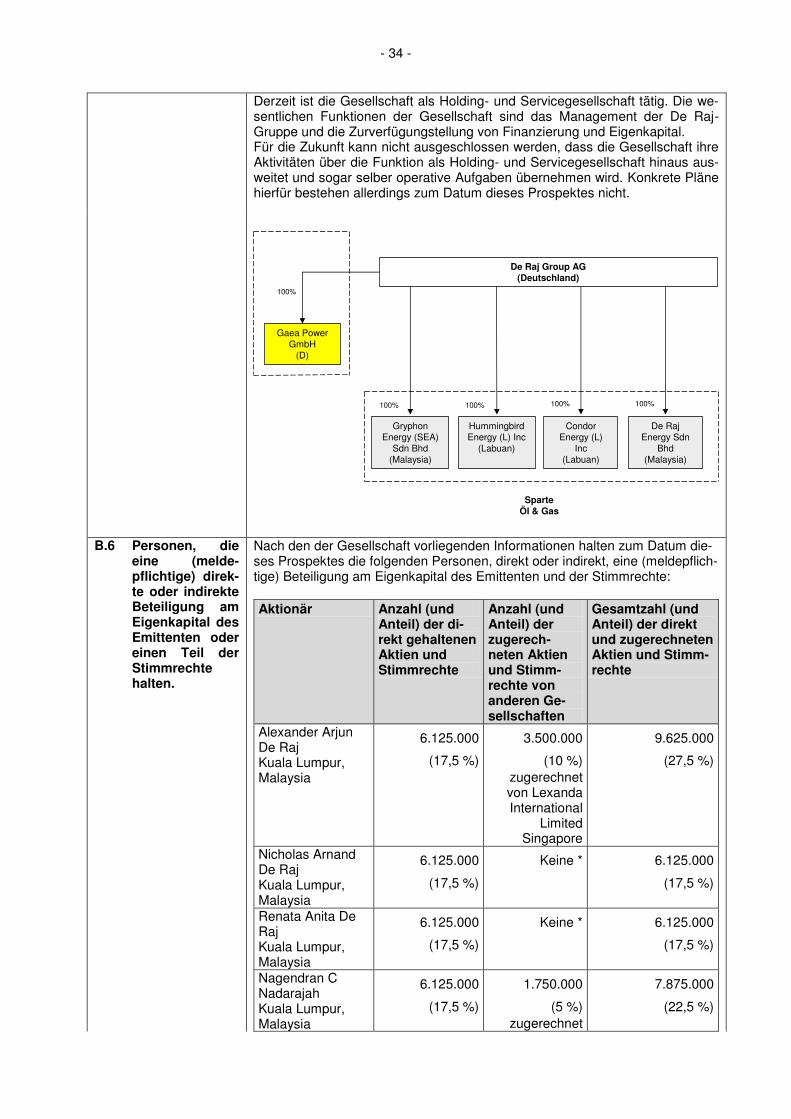

De Raj is the parent company of the De Raj Group. De Raj holds shares in the following five companies, Gryphon Energy (SEA) Sdn Bhd, Hummingbird Energy (L) Inc, Condor Energy (L) Inc, De Raj Energy Sdn Bhd and Gaea Power GmbH. Currently, the Company acts as a holding and service company. The essential functions of the Company are the management of the De Raj Group and the pro-curement of financing and equity. In the future, it cannot be ruled out that the Com-pany will also extend its activities beyond its function as a holding and service company and may also assume operational tasks itself. However, there are no definitive plans to do so at the date of this prospectus.

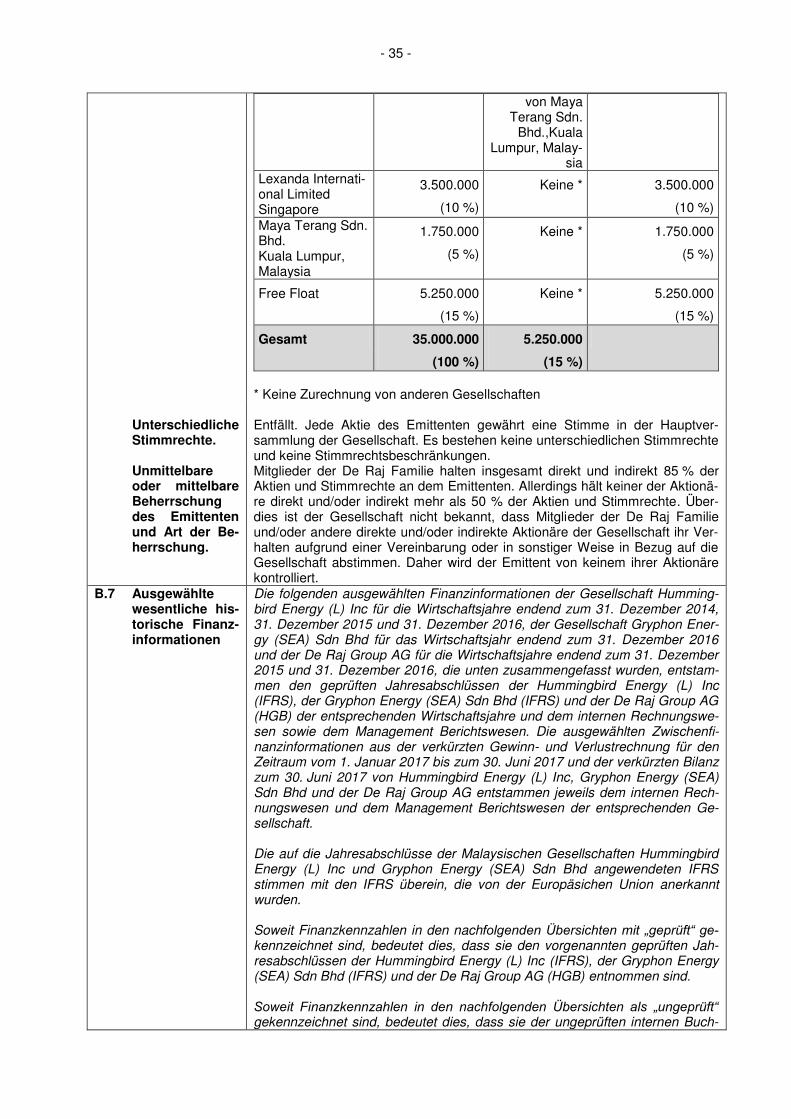

B.6 Persons who, direct-ly or indi-rectly, have a (notifiable) interest in the issuer’s capital or voting rights.

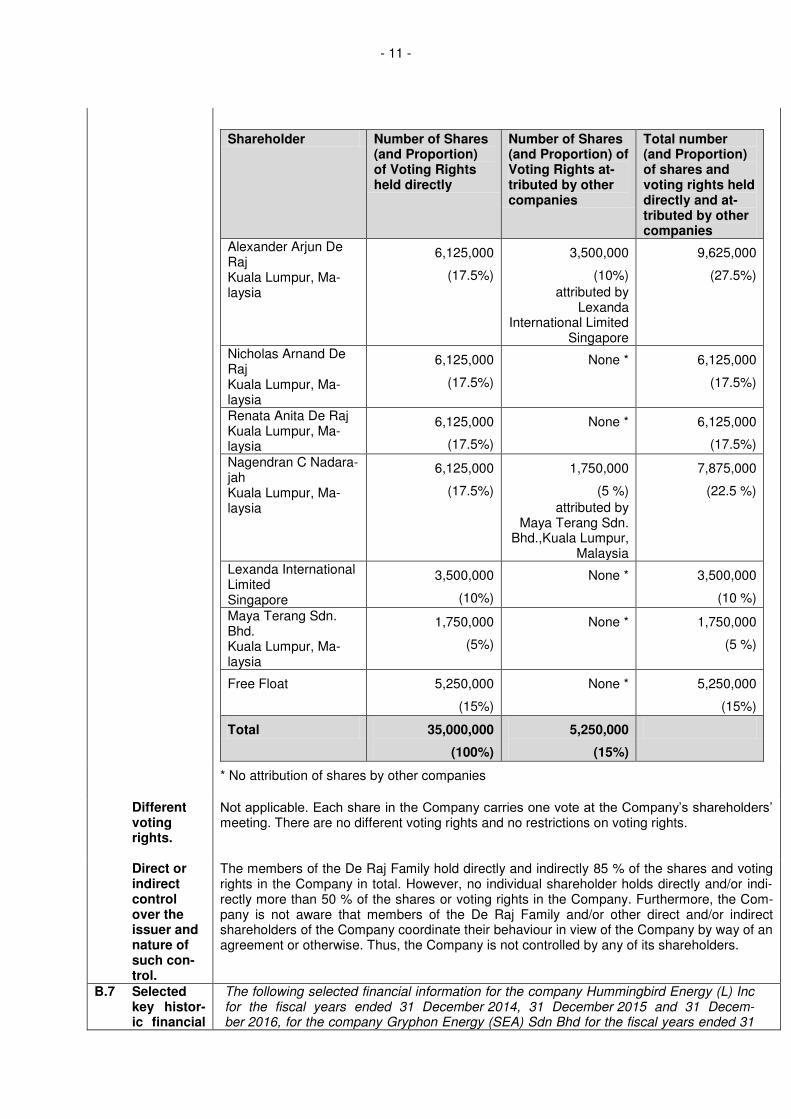

According to the Company’s information, as of the date of this Prospectus, the following persons, directly or indirectly, have a notifiable interest in the Company’s capital and voting rights:

De Raj Group AG (Germany)

Gaea Power GmbH(GER)

100%

German Power

Division

100%100%

HummingbirdEnergy (L) Inc

(Labuan)

GryphonEnergy (SEA)

Sdn Bhd(Malaysia)

CondorEnergy (L)

Inc(Labuan)

De Raj Energy Sdn

Bhd(Malaysia)

100%100%

Oil & GasDivision

- 11 -

Shareholder Number of Shares (and Proportion) of Voting Rights held directly

Number of Shares (and Proportion) of Voting Rights at-tributed by other companies

Total number (and Proportion) of shares and voting rights held directly and at-tributed by other companies

Alexander Arjun De Raj Kuala Lumpur, Ma-laysia

6,125,000

(17.5%)

3,500,000

(10%) attributed by

Lexanda International Limited

Singapore

9,625,000

(27.5%)

Nicholas Arnand De Raj Kuala Lumpur, Ma-laysia

6,125,000

(17.5%)

None * 6,125,000

(17.5%)

Renata Anita De Raj Kuala Lumpur, Ma-laysia

6,125,000

(17.5%)

None * 6,125,000

(17.5%) Nagendran C Nadara-jah Kuala Lumpur, Ma-laysia

6,125,000

(17.5%)

1,750,000

(5 %) attributed by

Maya Terang Sdn. Bhd.,Kuala Lumpur,

Malaysia

7,875,000

(22.5 %)

Lexanda International Limited Singapore

3,500,000

(10%)

None * 3,500,000

(10 %) Maya Terang Sdn. Bhd. Kuala Lumpur, Ma-laysia

1,750,000

(5%)

None * 1,750,000

(5 %)

Free Float 5,250,000

(15%)

None * 5,250,000

(15%)

Total 35,000,000

(100%)

5,250,000

(15%)

* No attribution of shares by other companies

Different voting rights.

Not applicable. Each share in the Company carries one vote at the Company’s shareholders’ meeting. There are no different voting rights and no restrictions on voting rights.

Direct or indirect control over the issuer and nature of such con-trol.

The members of the De Raj Family hold directly and indirectly 85 % of the shares and voting rights in the Company in total. However, no individual shareholder holds directly and/or indi-rectly more than 50 % of the shares or voting rights in the Company. Furthermore, the Com-pany is not aware that members of the De Raj Family and/or other direct and/or indirect shareholders of the Company coordinate their behaviour in view of the Company by way of an agreement or otherwise. Thus, the Company is not controlled by any of its shareholders.

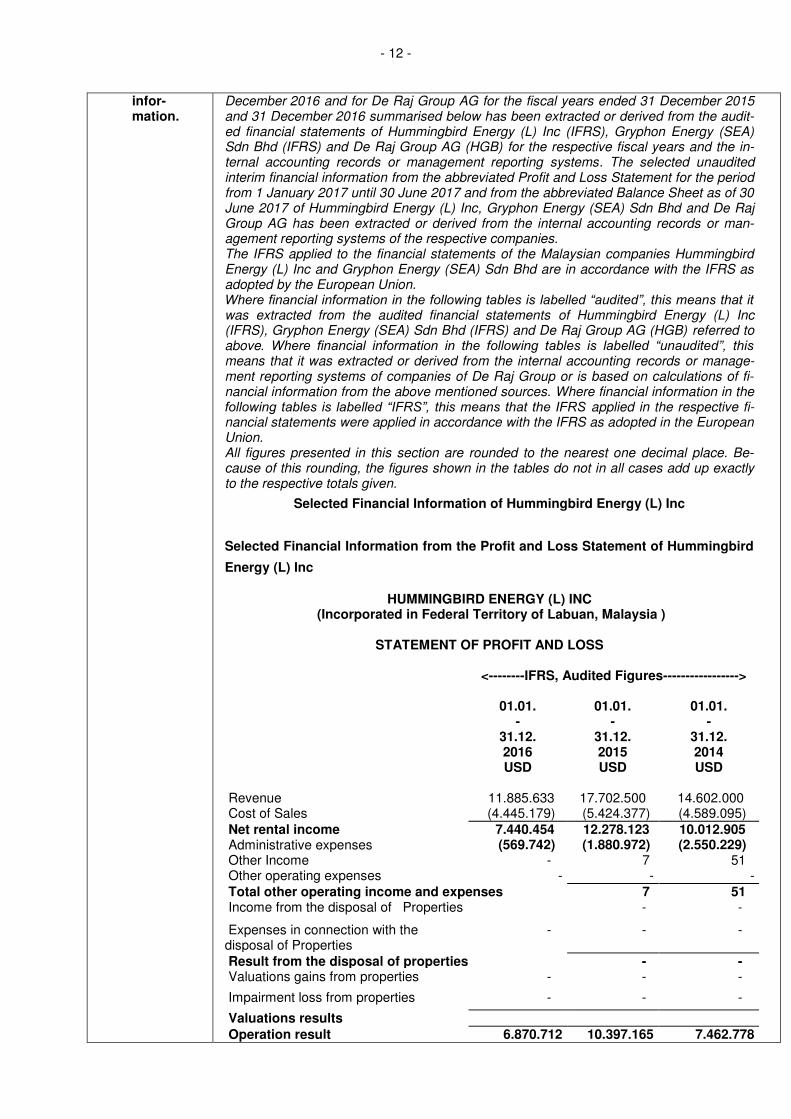

B.7 Selected key histor-ic financial

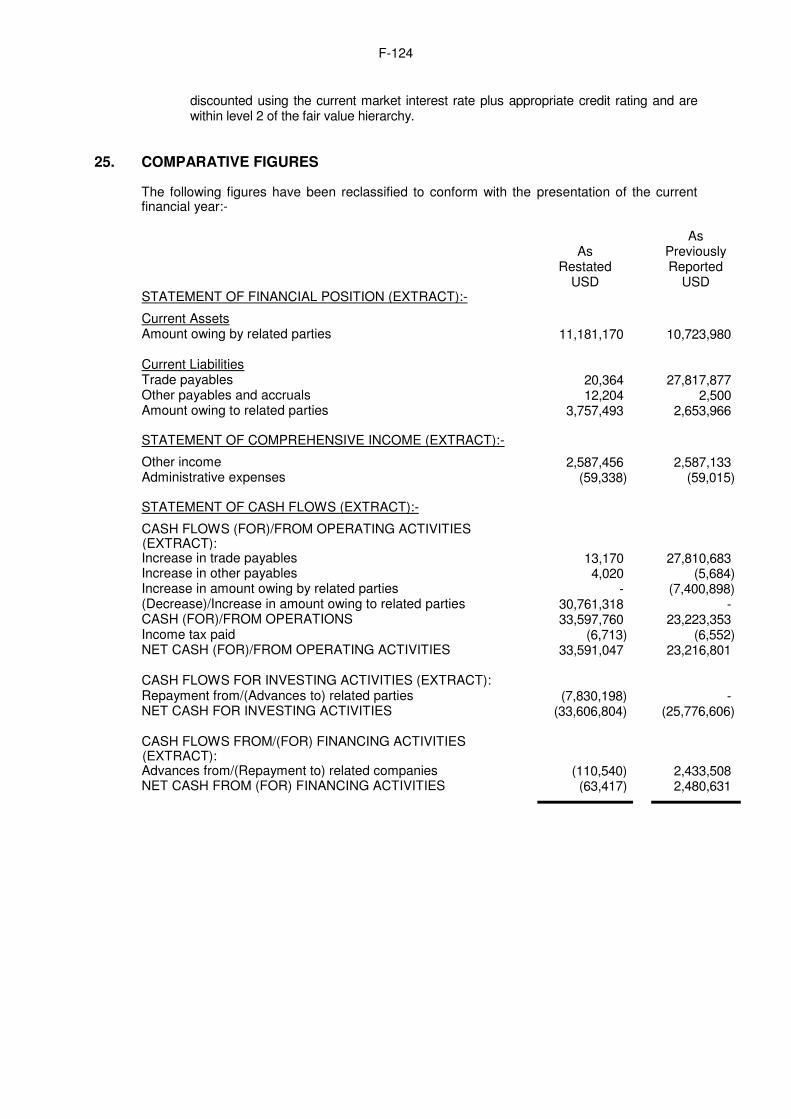

The following selected financial information for the company Hummingbird Energy (L) Inc for the fiscal years ended 31 December 2014, 31 December 2015 and 31 Decem-ber 2016, for the company Gryphon Energy (SEA) Sdn Bhd for the fiscal years ended 31

- 12 -

infor-mation.

December 2016 and for De Raj Group AG for the fiscal years ended 31 December 2015 and 31 December 2016 summarised below has been extracted or derived from the audit-ed financial statements of Hummingbird Energy (L) Inc (IFRS), Gryphon Energy (SEA) Sdn Bhd (IFRS) and De Raj Group AG (HGB) for the respective fiscal years and the in-ternal accounting records or management reporting systems. The selected unaudited interim financial information from the abbreviated Profit and Loss Statement for the period from 1 January 2017 until 30 June 2017 and from the abbreviated Balance Sheet as of 30 June 2017 of Hummingbird Energy (L) Inc, Gryphon Energy (SEA) Sdn Bhd and De Raj Group AG has been extracted or derived from the internal accounting records or man-agement reporting systems of the respective companies. The IFRS applied to the financial statements of the Malaysian companies Hummingbird Energy (L) Inc and Gryphon Energy (SEA) Sdn Bhd are in accordance with the IFRS as adopted by the European Union. Where financial information in the following tables is labelled “audited”, this means that it was extracted from the audited financial statements of Hummingbird Energy (L) Inc (IFRS), Gryphon Energy (SEA) Sdn Bhd (IFRS) and De Raj Group AG (HGB) referred to above. Where financial information in the following tables is labelled “unaudited”, this means that it was extracted or derived from the internal accounting records or manage-ment reporting systems of companies of De Raj Group or is based on calculations of fi-nancial information from the above mentioned sources. Where financial information in the following tables is labelled “IFRS”, this means that the IFRS applied in the respective fi-nancial statements were applied in accordance with the IFRS as adopted in the European Union. All figures presented in this section are rounded to the nearest one decimal place. Be-cause of this rounding, the figures shown in the tables do not in all cases add up exactly to the respective totals given.

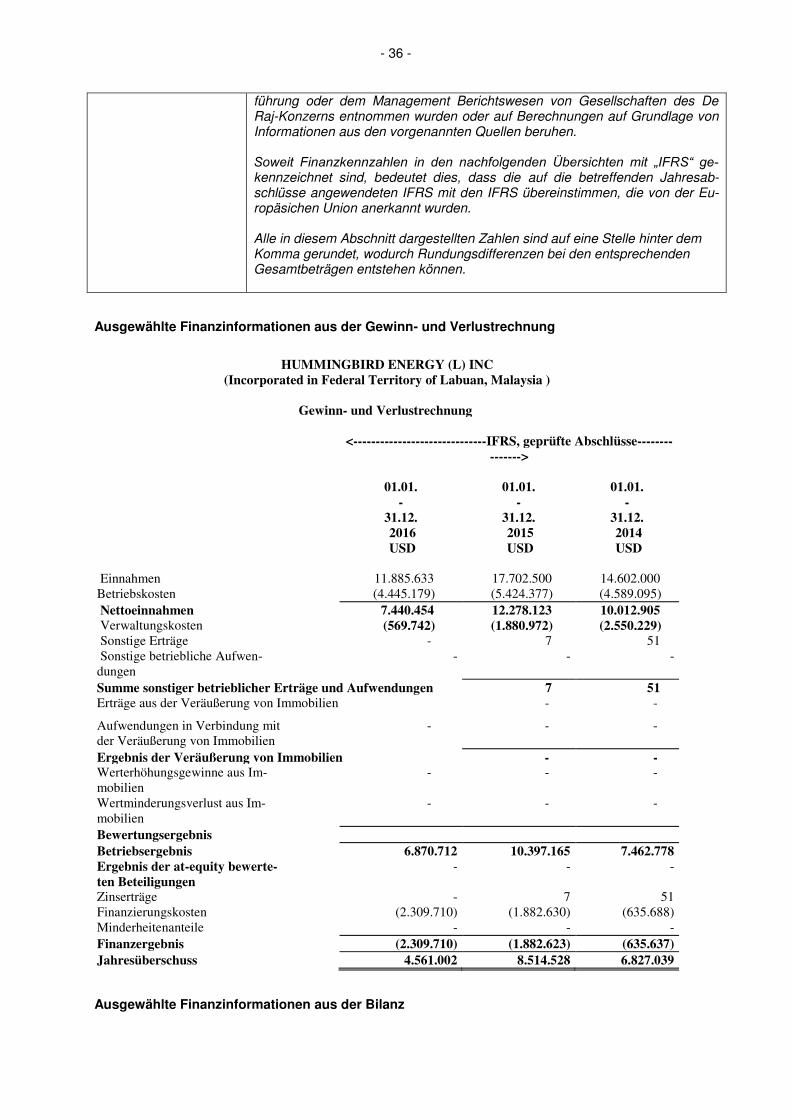

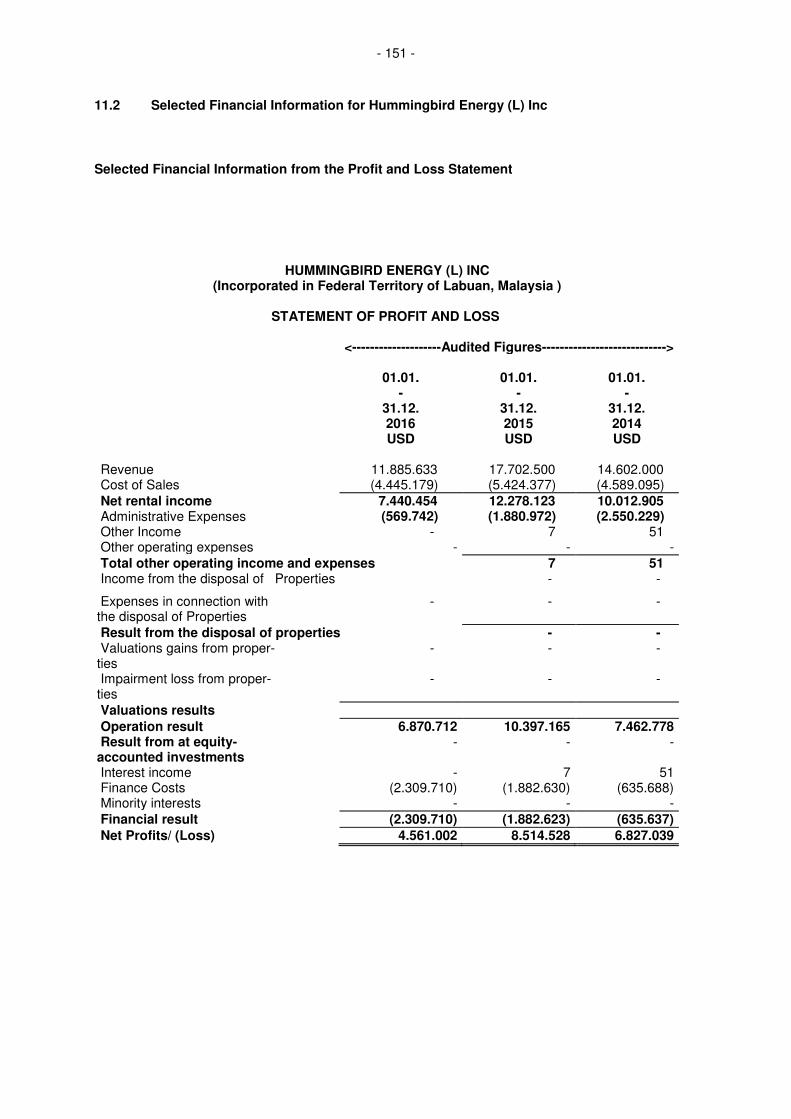

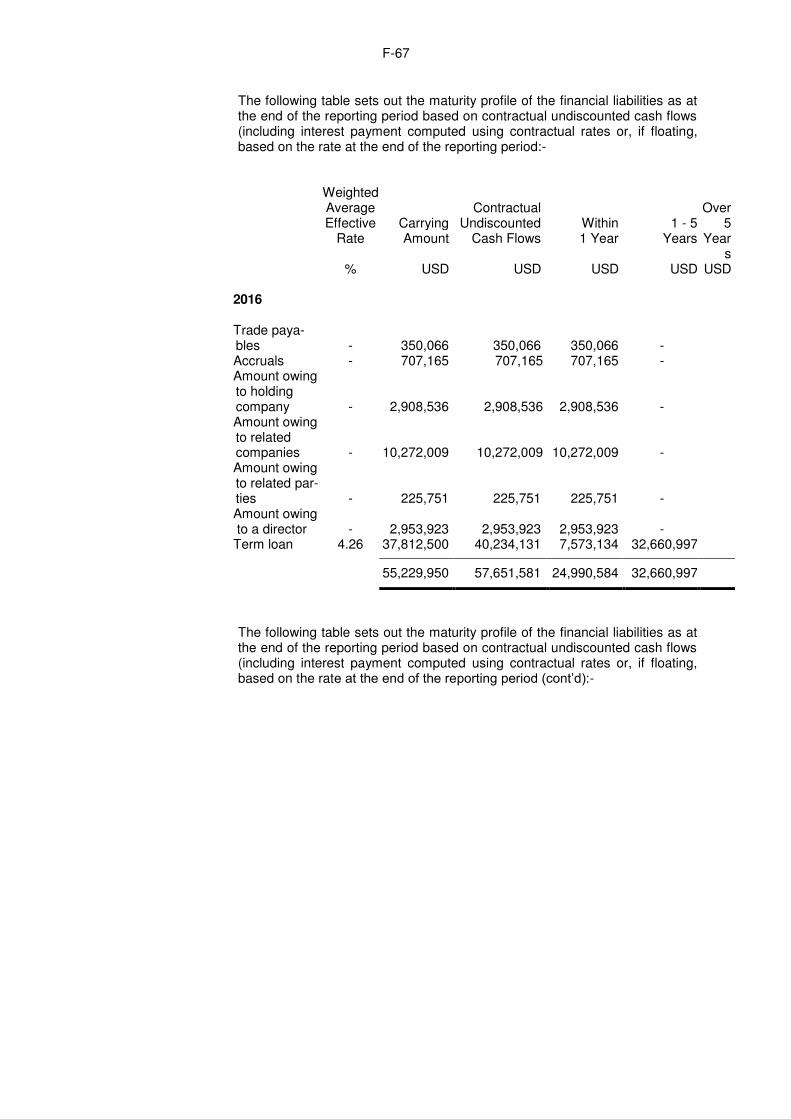

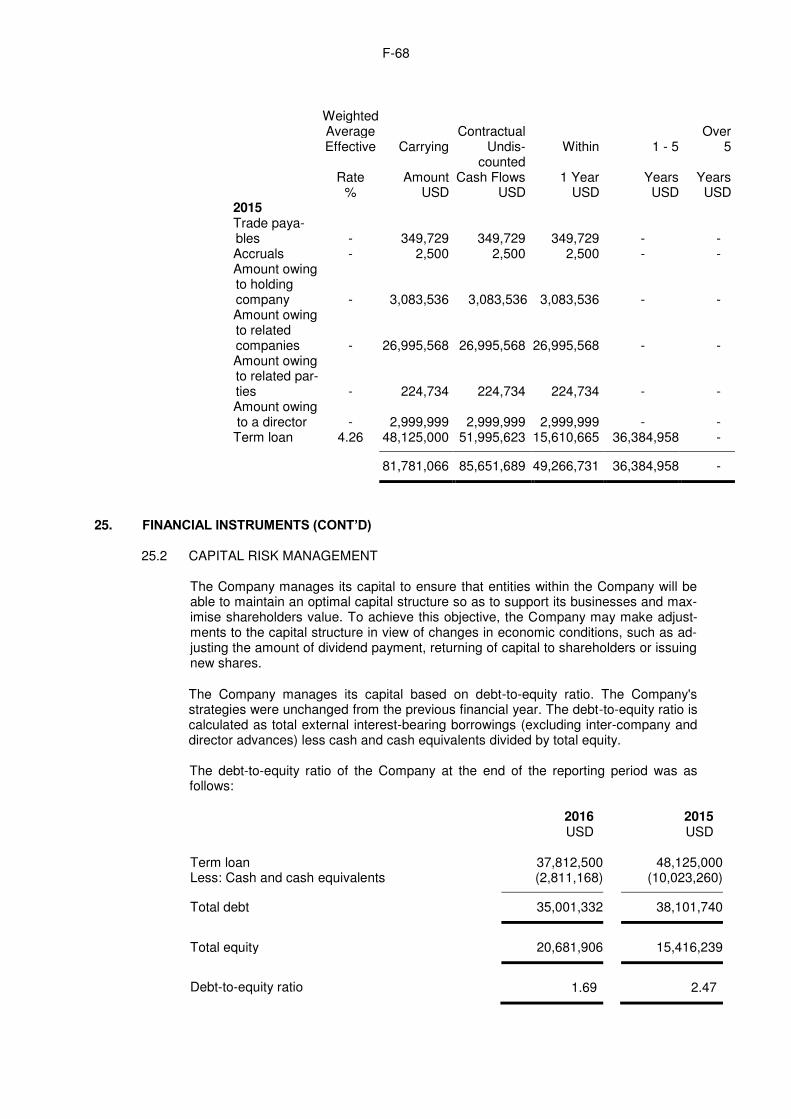

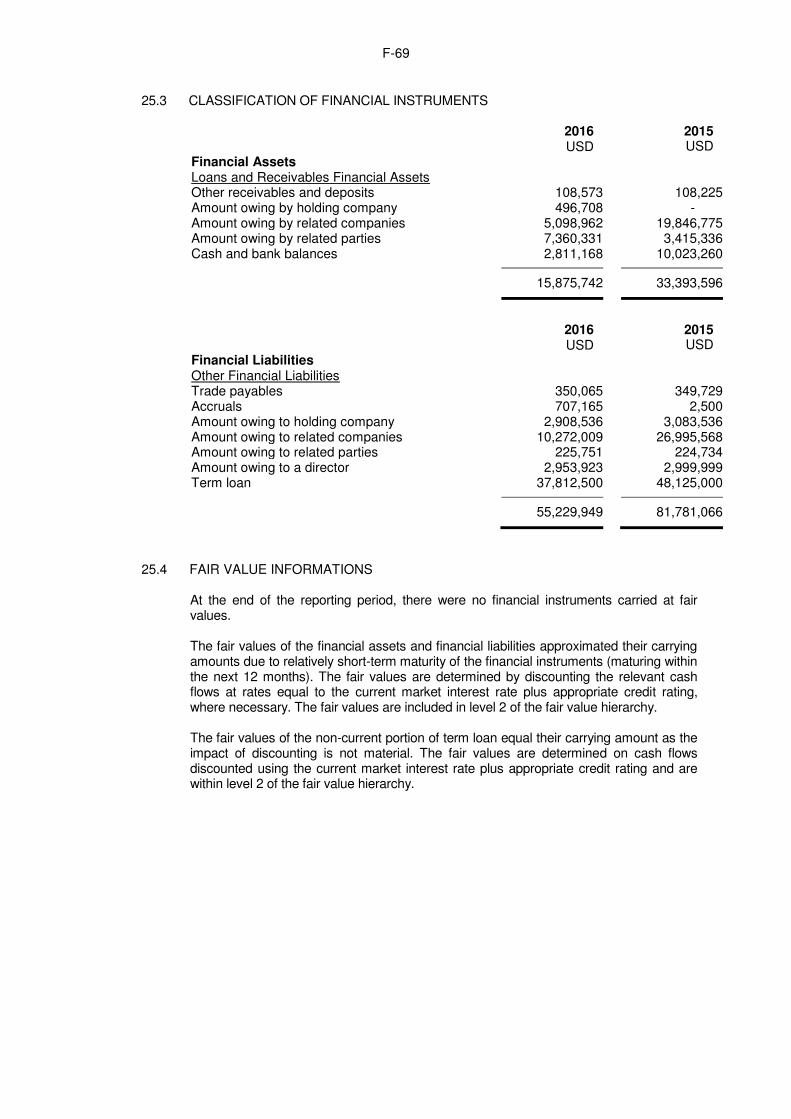

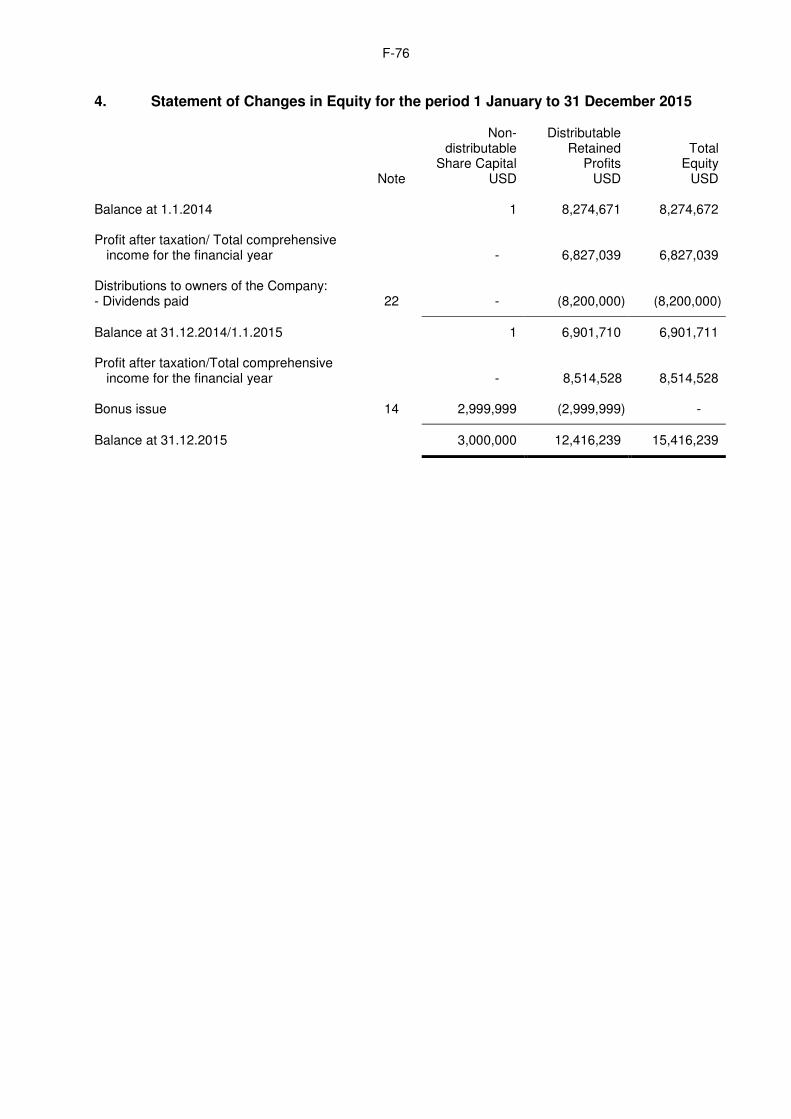

Selected Financial Information of Hummingbird Energy (L) Inc

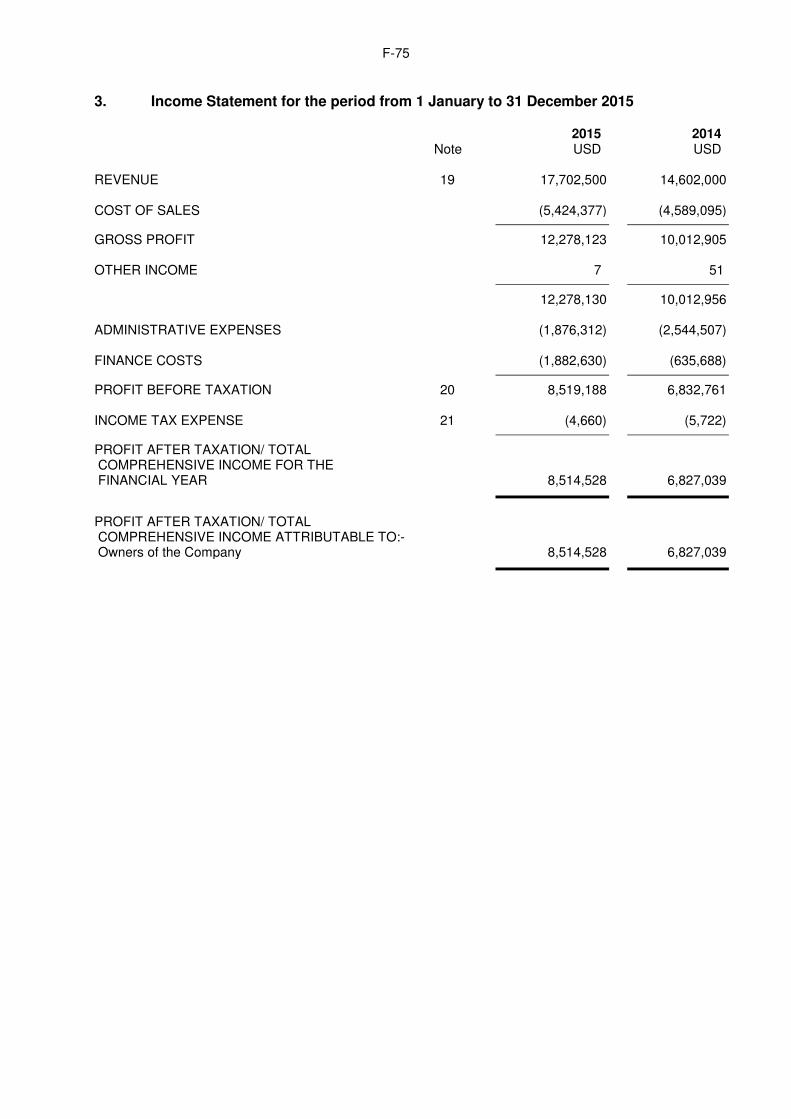

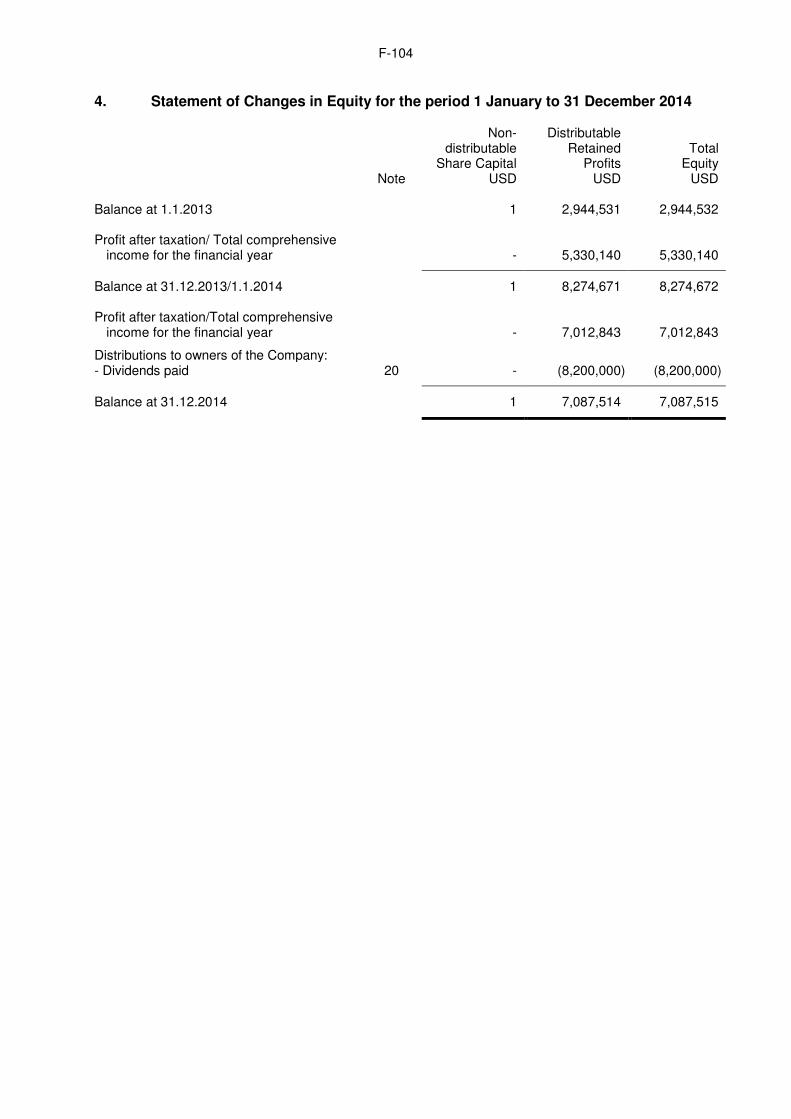

Selected Financial Information from the Profit and Loss Statement of Hummingbird

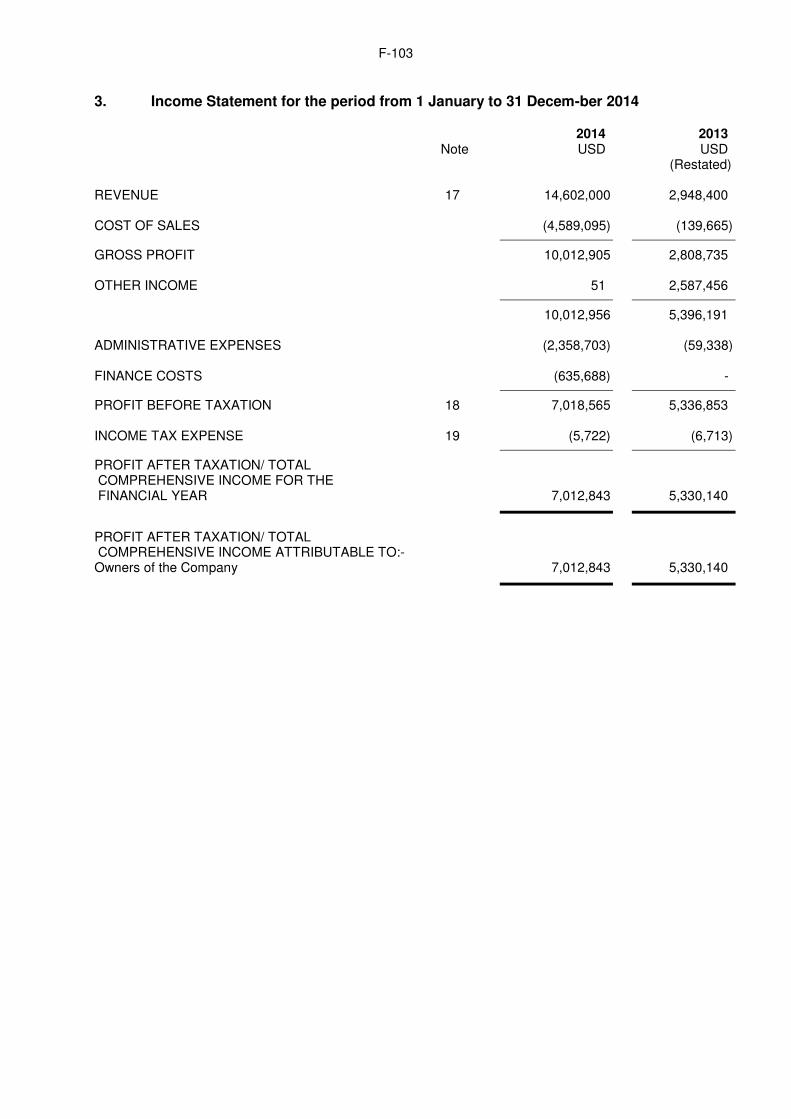

Energy (L) Inc

HUMMINGBIRD ENERGY (L) INC (Incorporated in Federal Territory of Labuan, Malaysia )

STATEMENT OF PROFIT AND LOSS

<--------IFRS, Audited Figures----------------->

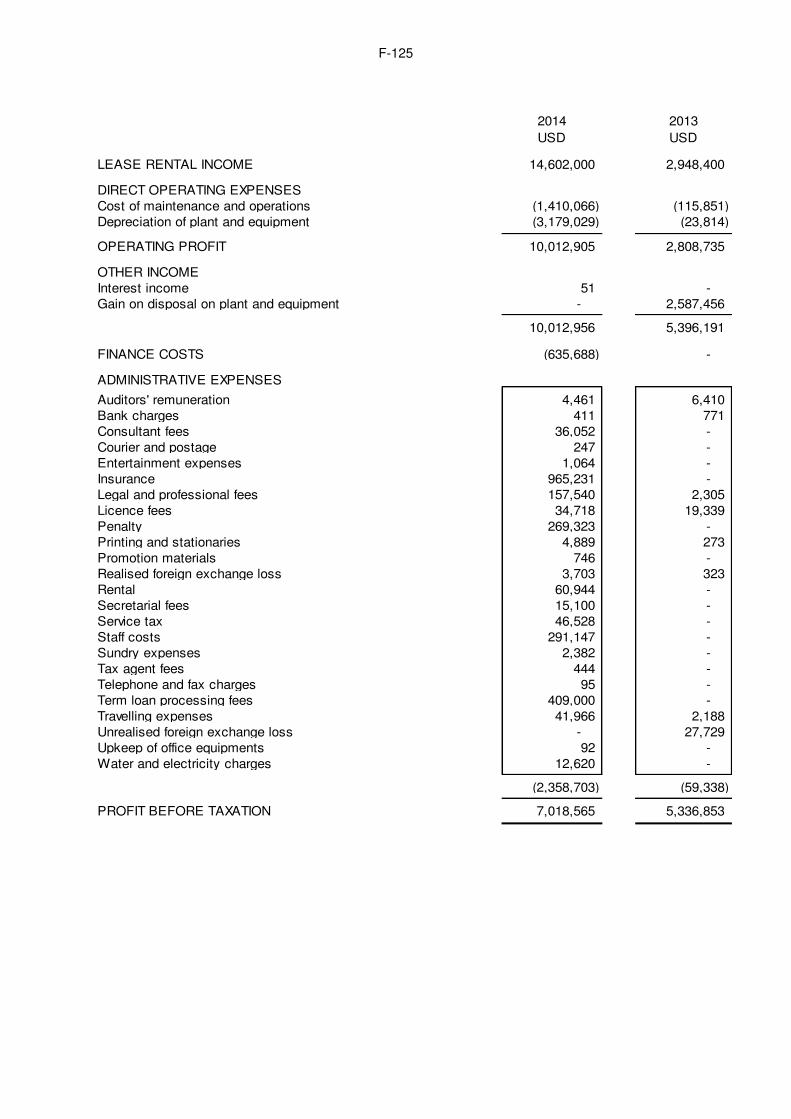

01.01. 01.01. 01.01. - - - 31.12. 31.12. 31.12. 2016 2015 2014 USD USD USD

Revenue 11.885.633 17.702.500 14.602.000 Cost of Sales (4.445.179) (5.424.377) (4.589.095) Net rental income 7.440.454 12.278.123 10.012.905 Administrative expenses (569.742) (1.880.972) (2.550.229) Other Income - 7 51 Other operating expenses - - - Total other operating income and expenses 7 51 Income from the disposal of Properties - -

Expenses in connection with the disposal of Properties

- - -

Result from the disposal of properties - - Valuations gains from properties - - -

Impairment loss from properties - - -

Valuations results Operation result 6.870.712 10.397.165 7.462.778

- 13 -

Result from at equity-accounted investments

- - -

Interest income - 7 51 Finance Costs (2.309.710) (1.882.630) (635.688) Minority interests - - - Financial result (2.309.710) (1.882.623) (635.637) Net Profits/ (Loss) 4.561.002 8.514.528 6.827.039

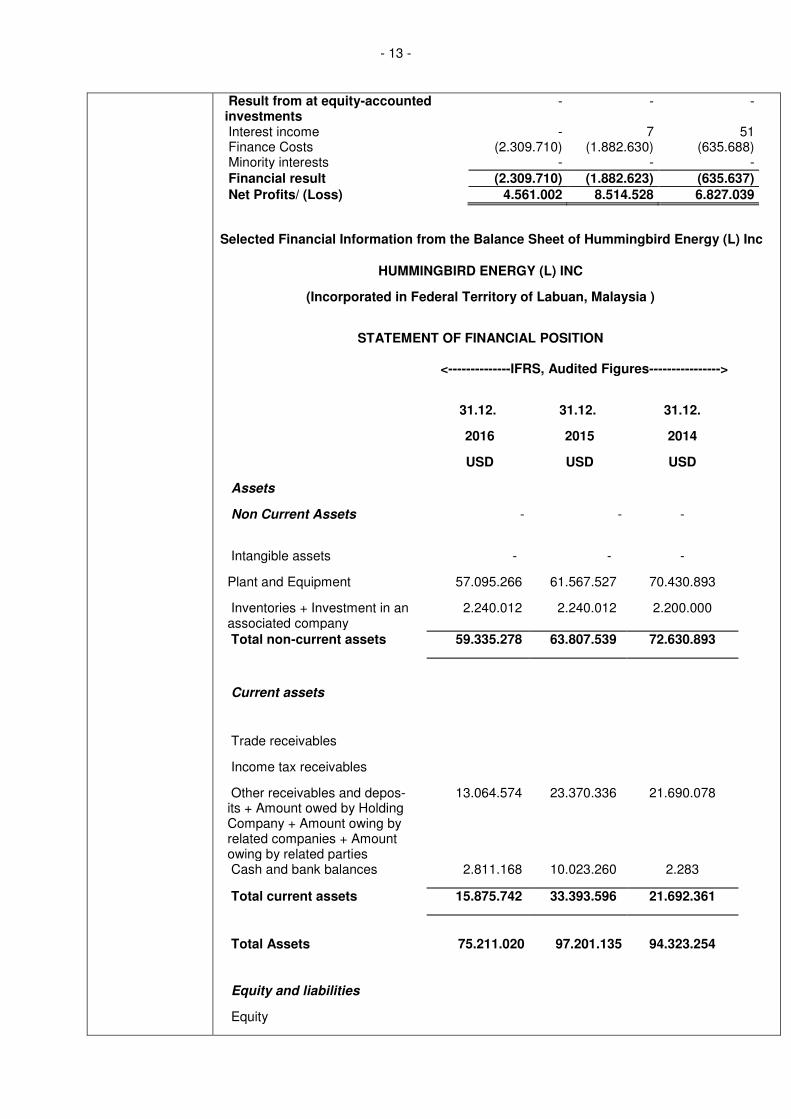

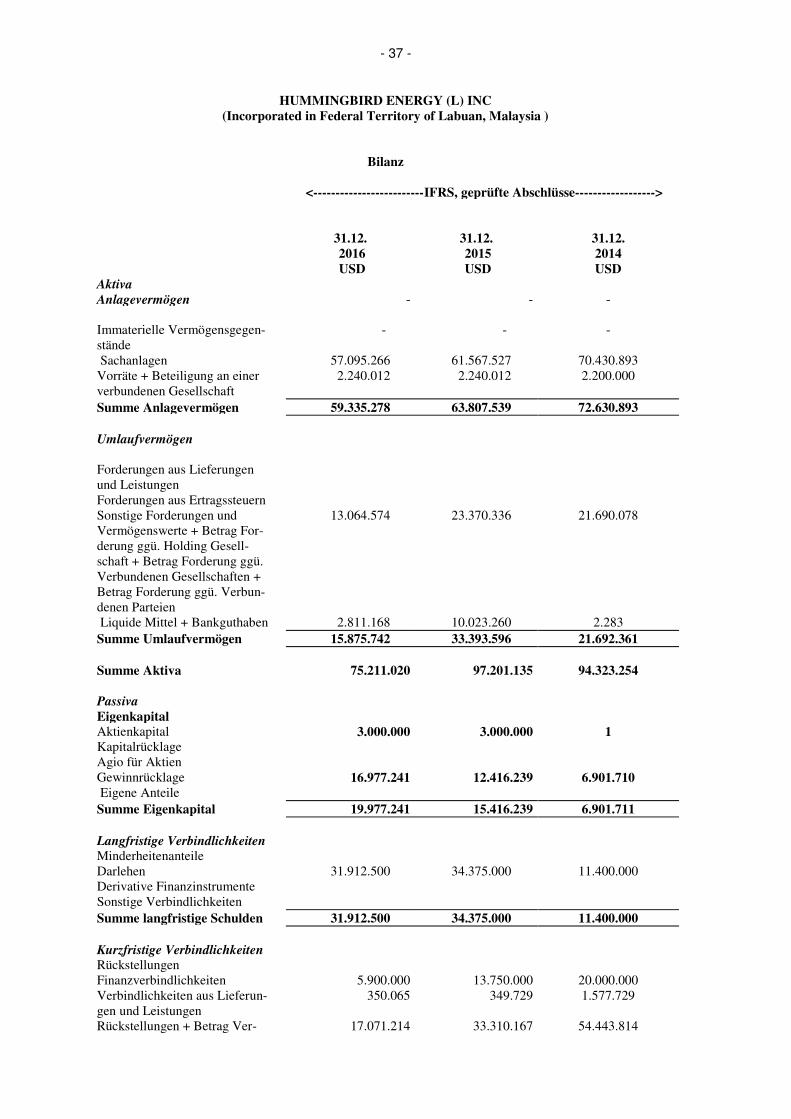

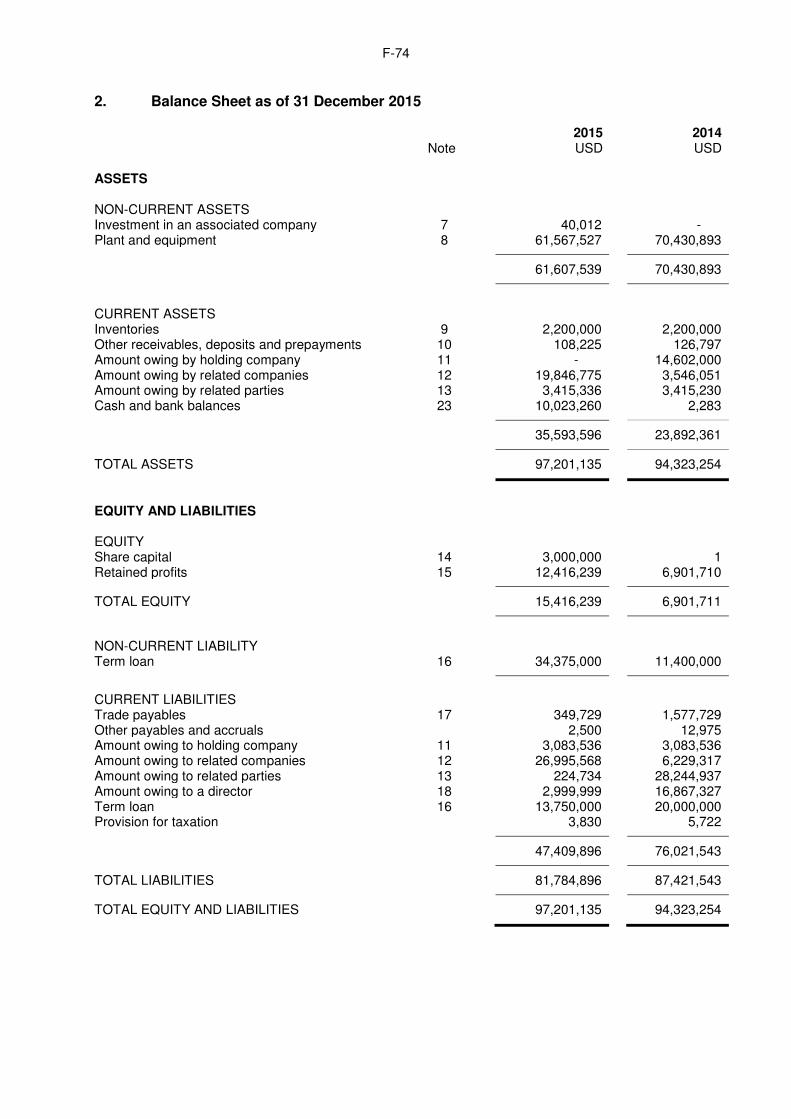

Selected Financial Information from the Balance Sheet of Hummingbird Energy (L) Inc

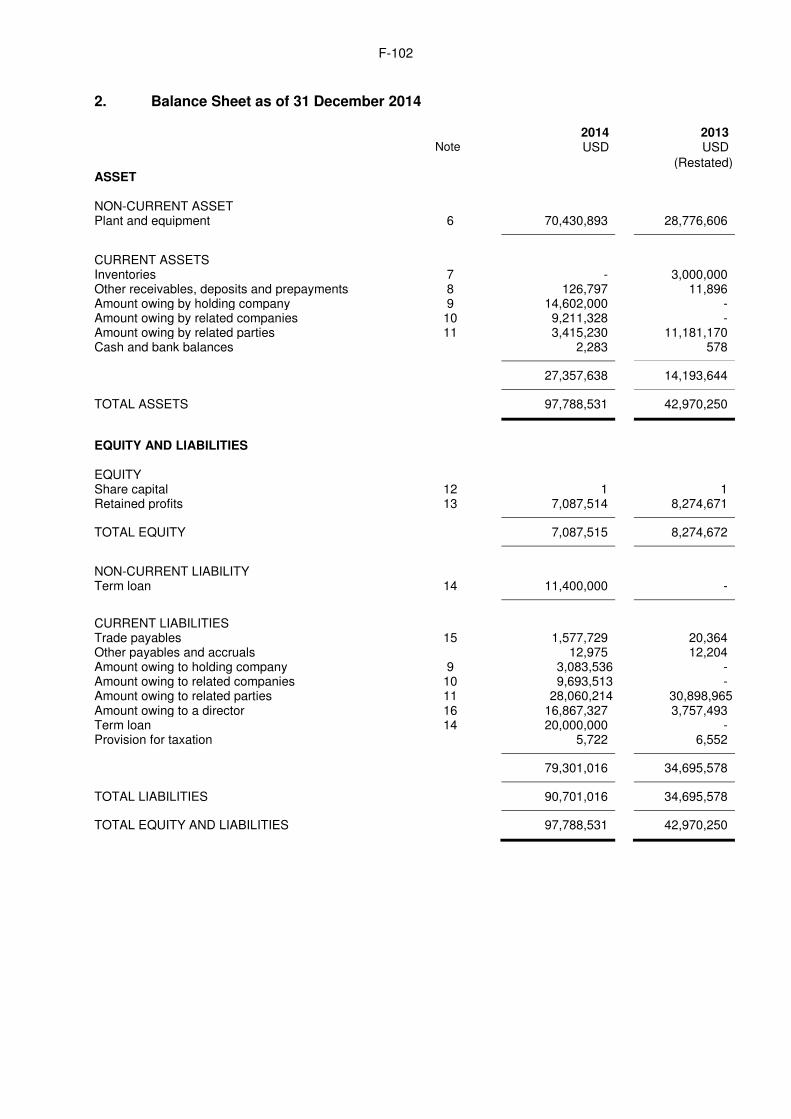

HUMMINGBIRD ENERGY (L) INC

(Incorporated in Federal Territory of Labuan, Malaysia )

STATEMENT OF FINANCIAL POSITION

<--------------IFRS, Audited Figures---------------->

31.12. 31.12. 31.12.

2016 2015 2014

USD USD USD

Assets

Non Current Assets - - -

Intangible assets - - -

Plant and Equipment 57.095.266 61.567.527 70.430.893

Inventories + Investment in an associated company

2.240.012 2.240.012 2.200.000

Total non-current assets 59.335.278 63.807.539 72.630.893

Current assets

Trade receivables

Income tax receivables

Other receivables and depos-its + Amount owed by Holding Company + Amount owing by related companies + Amount owing by related parties

13.064.574 23.370.336 21.690.078

Cash and bank balances 2.811.168 10.023.260 2.283

Total current assets 15.875.742 33.393.596 21.692.361

Total Assets 75.211.020 97.201.135 94.323.254

Equity and liabilities

Equity

- 14 -

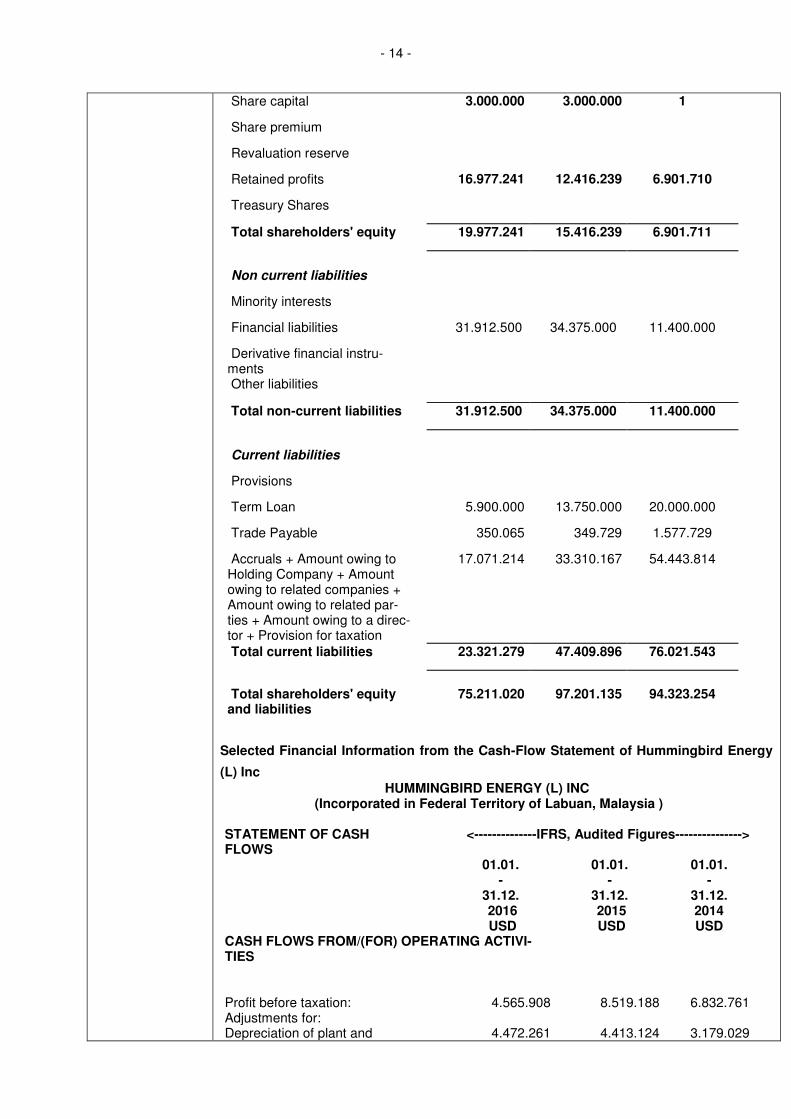

Share capital 3.000.000 3.000.000 1

Share premium

Revaluation reserve

Retained profits 16.977.241 12.416.239 6.901.710

Treasury Shares

Total shareholders' equity 19.977.241 15.416.239 6.901.711

Non current liabilities

Minority interests

Financial liabilities 31.912.500 34.375.000 11.400.000

Derivative financial instru-ments

Other liabilities

Total non-current liabilities 31.912.500 34.375.000 11.400.000

Current liabilities

Provisions

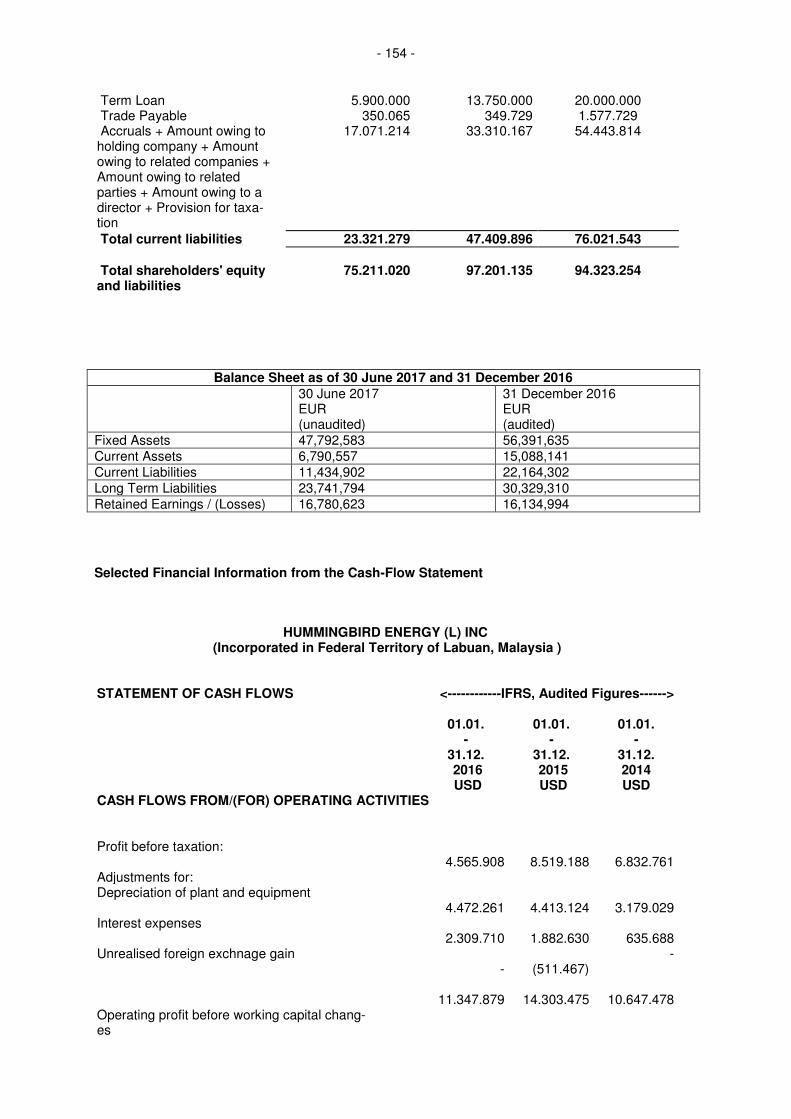

Term Loan 5.900.000 13.750.000 20.000.000

Trade Payable 350.065 349.729 1.577.729

Accruals + Amount owing to Holding Company + Amount owing to related companies + Amount owing to related par-ties + Amount owing to a direc-tor + Provision for taxation

17.071.214 33.310.167 54.443.814

Total current liabilities 23.321.279 47.409.896 76.021.543

Total shareholders' equity and liabilities

75.211.020 97.201.135 94.323.254

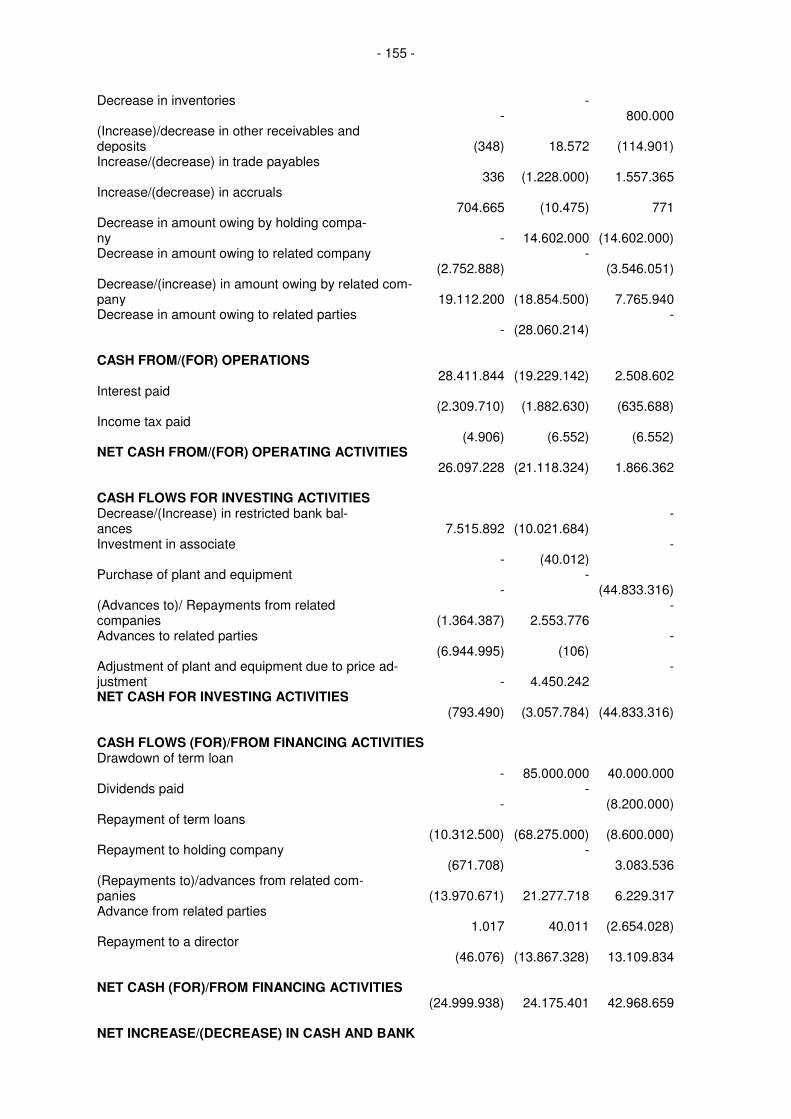

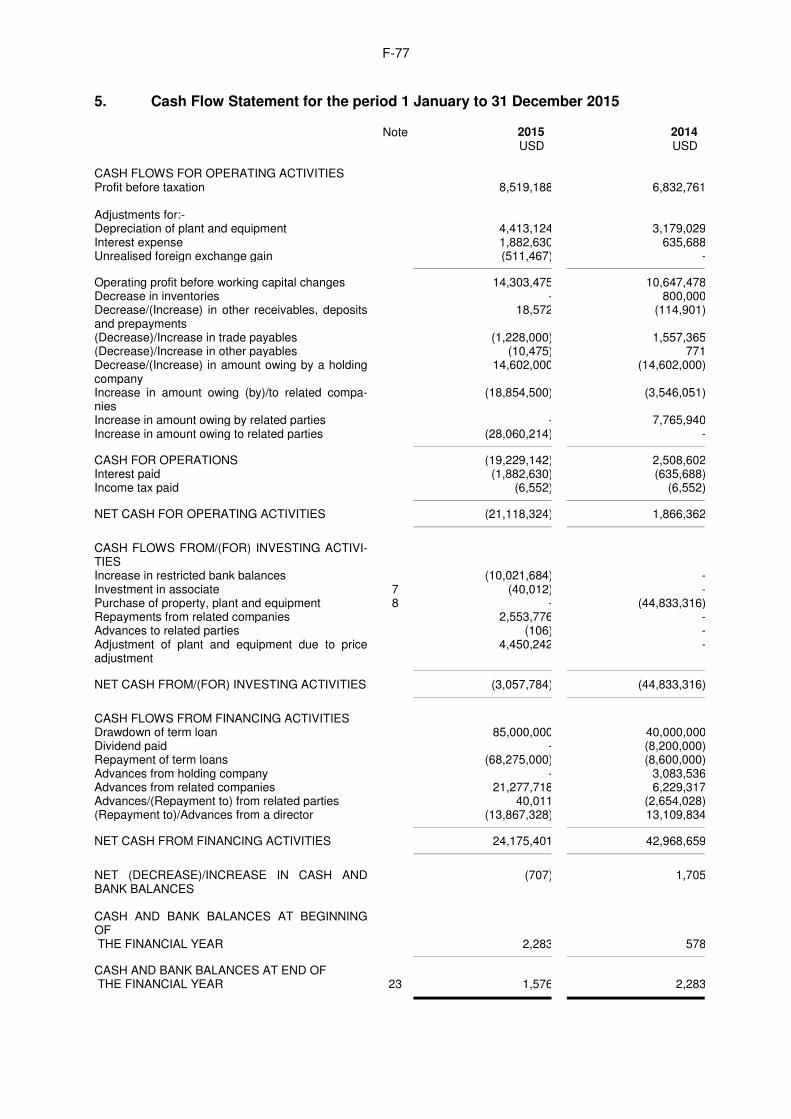

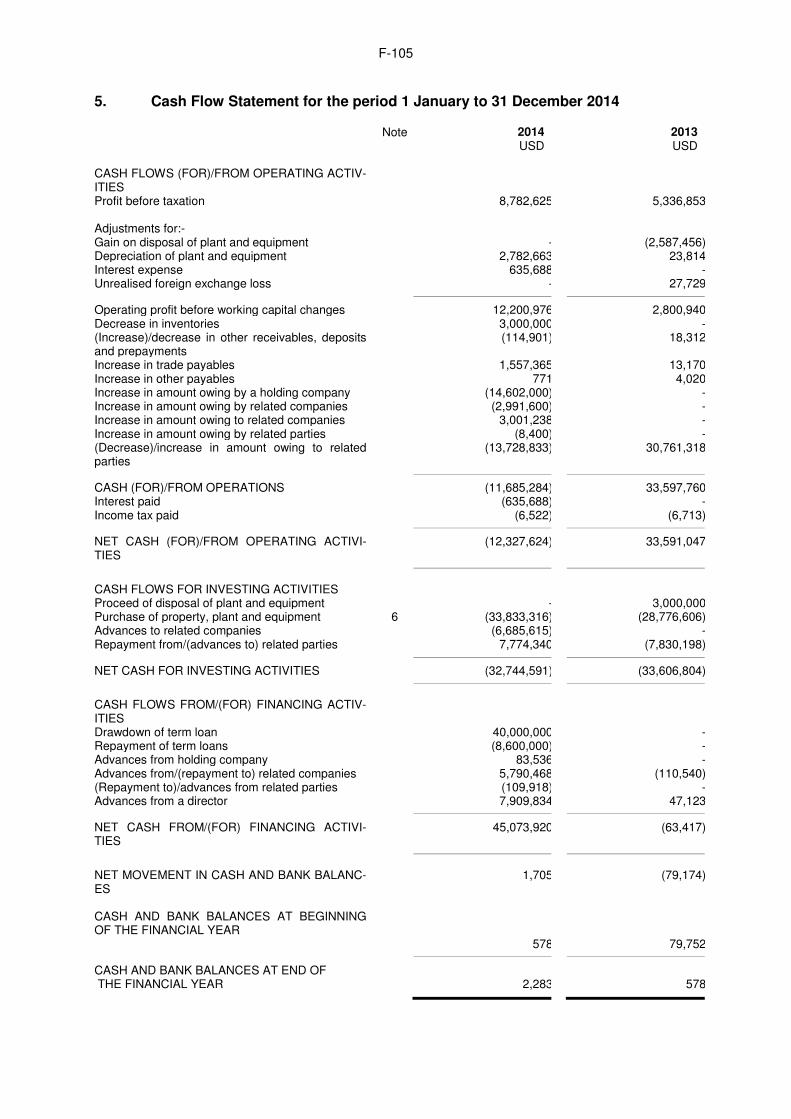

Selected Financial Information from the Cash-Flow Statement of Hummingbird Energy

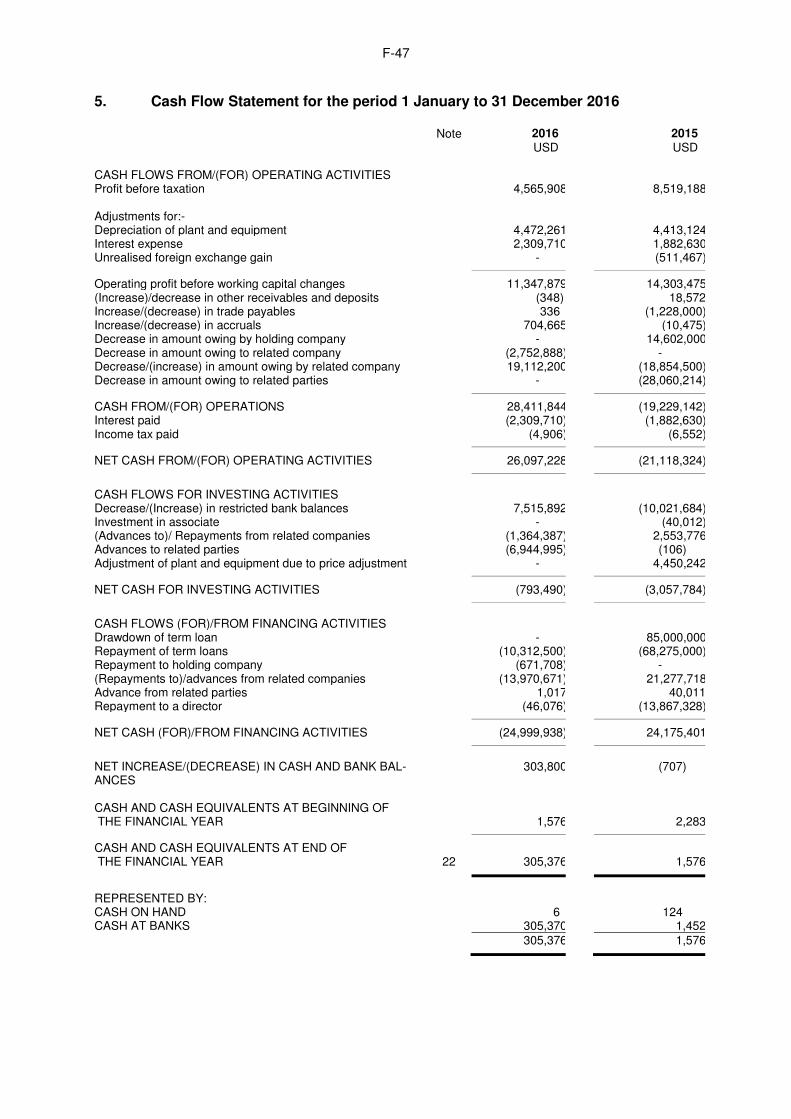

(L) Inc HUMMINGBIRD ENERGY (L) INC

(Incorporated in Federal Territory of Labuan, Malaysia )

STATEMENT OF CASH FLOWS

<--------------IFRS, Audited Figures--------------->

01.01. 01.01. 01.01. - - - 31.12. 31.12. 31.12. 2016 2015 2014 USD USD USD

CASH FLOWS FROM/(FOR) OPERATING ACTIVI-TIES

Profit before taxation: 4.565.908 8.519.188 6.832.761 Adjustments for: Depreciation of plant and 4.472.261 4.413.124 3.179.029

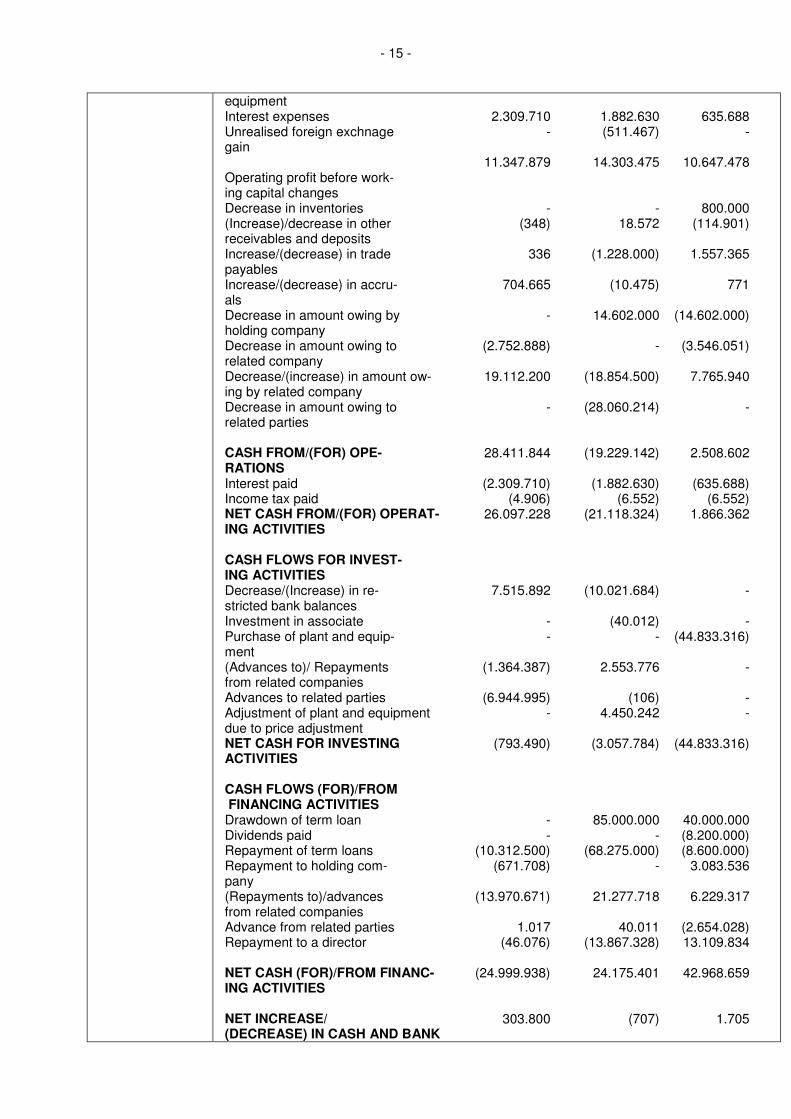

- 15 -

equipment Interest expenses 2.309.710 1.882.630 635.688 Unrealised foreign exchnage gain

- (511.467) -

11.347.879 14.303.475 10.647.478 Operating profit before work-ing capital changes

Decrease in inventories - - 800.000 (Increase)/decrease in other receivables and deposits

(348) 18.572 (114.901)

Increase/(decrease) in trade payables

336 (1.228.000) 1.557.365

Increase/(decrease) in accru-als

704.665 (10.475) 771

Decrease in amount owing by holding company

- 14.602.000 (14.602.000)

Decrease in amount owing to related company

(2.752.888) - (3.546.051)

Decrease/(increase) in amount ow-ing by related company

19.112.200 (18.854.500) 7.765.940

Decrease in amount owing to related parties

- (28.060.214) -

CASH FROM/(FOR) OPE-RATIONS

28.411.844 (19.229.142) 2.508.602

Interest paid (2.309.710) (1.882.630) (635.688) Income tax paid (4.906) (6.552) (6.552) NET CASH FROM/(FOR) OPERAT-ING ACTIVITIES

26.097.228 (21.118.324) 1.866.362

CASH FLOWS FOR INVEST-ING ACTIVITIES

Decrease/(Increase) in re-stricted bank balances

7.515.892 (10.021.684) -

Investment in associate - (40.012) - Purchase of plant and equip-ment

- - (44.833.316)

(Advances to)/ Repayments from related companies

(1.364.387) 2.553.776 -

Advances to related parties (6.944.995) (106) - Adjustment of plant and equipment due to price adjustment

- 4.450.242 -

NET CASH FOR INVESTING ACTIVITIES

(793.490) (3.057.784) (44.833.316)

CASH FLOWS (FOR)/FROM FINANCING ACTIVITIES

Drawdown of term loan - 85.000.000 40.000.000 Dividends paid - - (8.200.000) Repayment of term loans (10.312.500) (68.275.000) (8.600.000) Repayment to holding com-pany

(671.708) - 3.083.536

(Repayments to)/advances from related companies

(13.970.671) 21.277.718 6.229.317

Advance from related parties 1.017 40.011 (2.654.028) Repayment to a director (46.076) (13.867.328) 13.109.834

NET CASH (FOR)/FROM FINANC-ING ACTIVITIES

(24.999.938) 24.175.401 42.968.659

NET INCREASE/ (DECREASE) IN CASH AND BANK

303.800 (707) 1.705

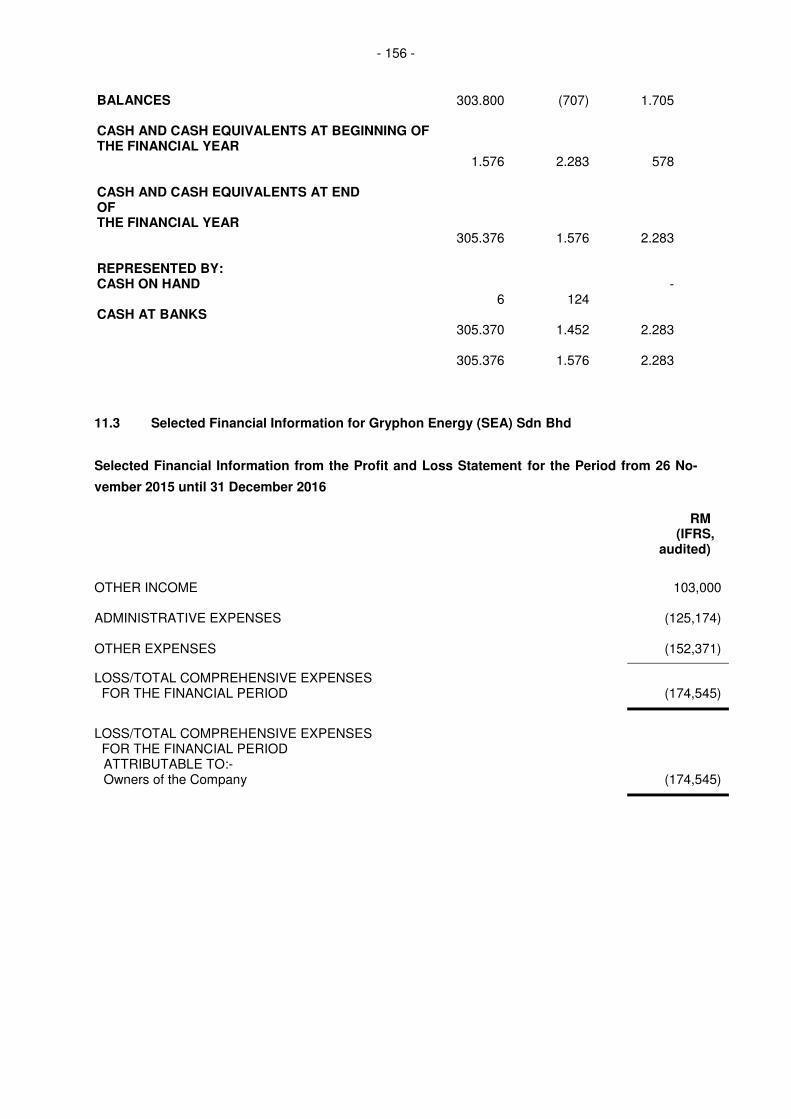

- 16 -

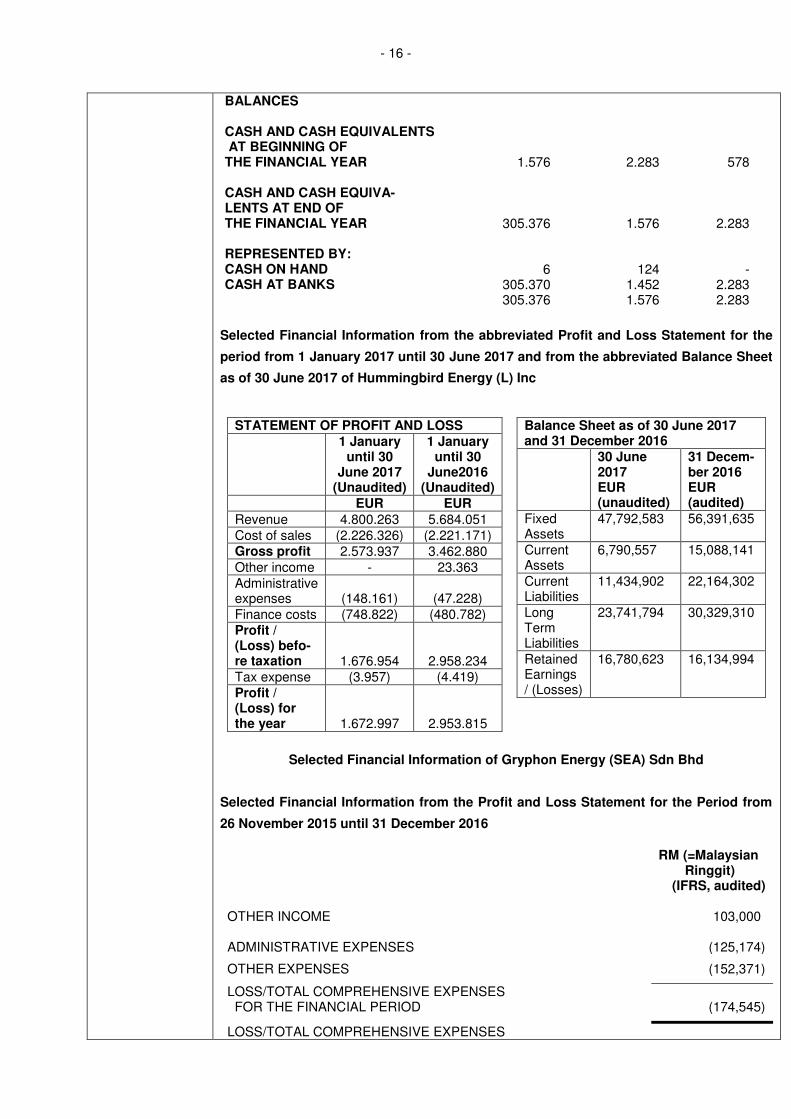

BALANCES

CASH AND CASH EQUIVALENTS AT BEGINNING OF

THE FINANCIAL YEAR 1.576 2.283 578

CASH AND CASH EQUIVA-LENTS AT END OF

THE FINANCIAL YEAR 305.376 1.576 2.283

REPRESENTED BY: CASH ON HAND 6 124 - CASH AT BANKS 305.370 1.452 2.283

305.376 1.576 2.283

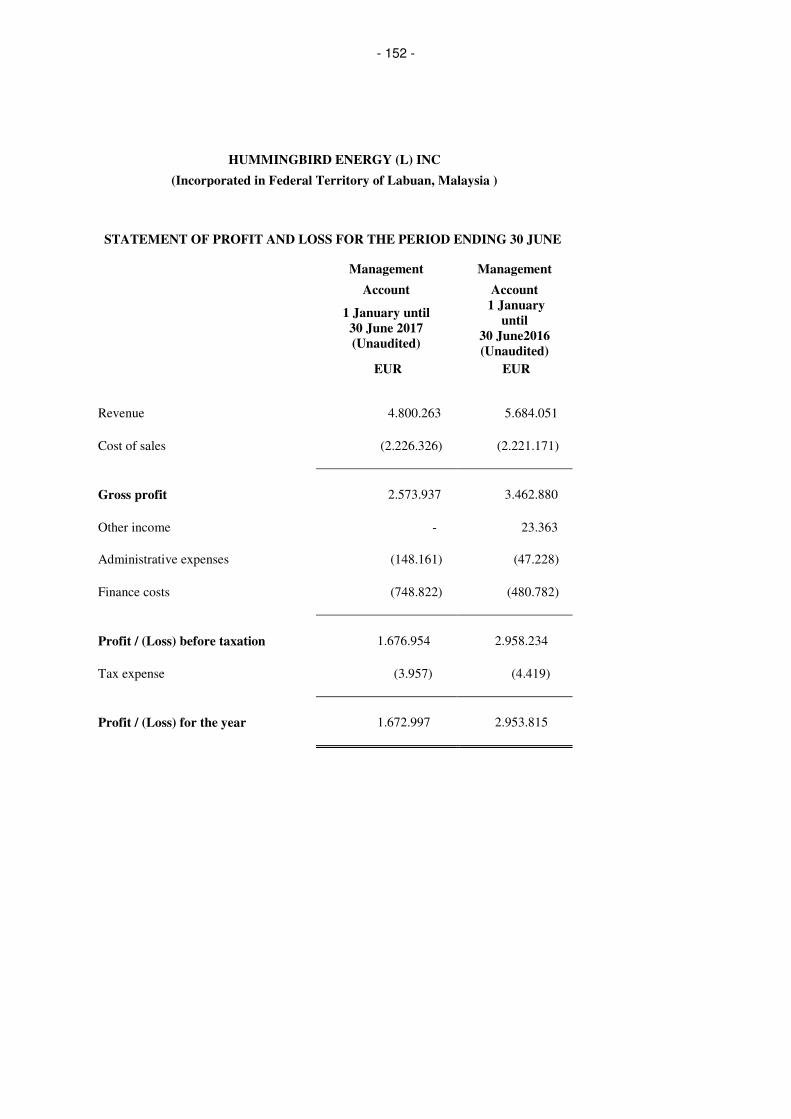

Selected Financial Information from the abbreviated Profit and Loss Statement for the

period from 1 January 2017 until 30 June 2017 and from the abbreviated Balance Sheet

as of 30 June 2017 of Hummingbird Energy (L) Inc

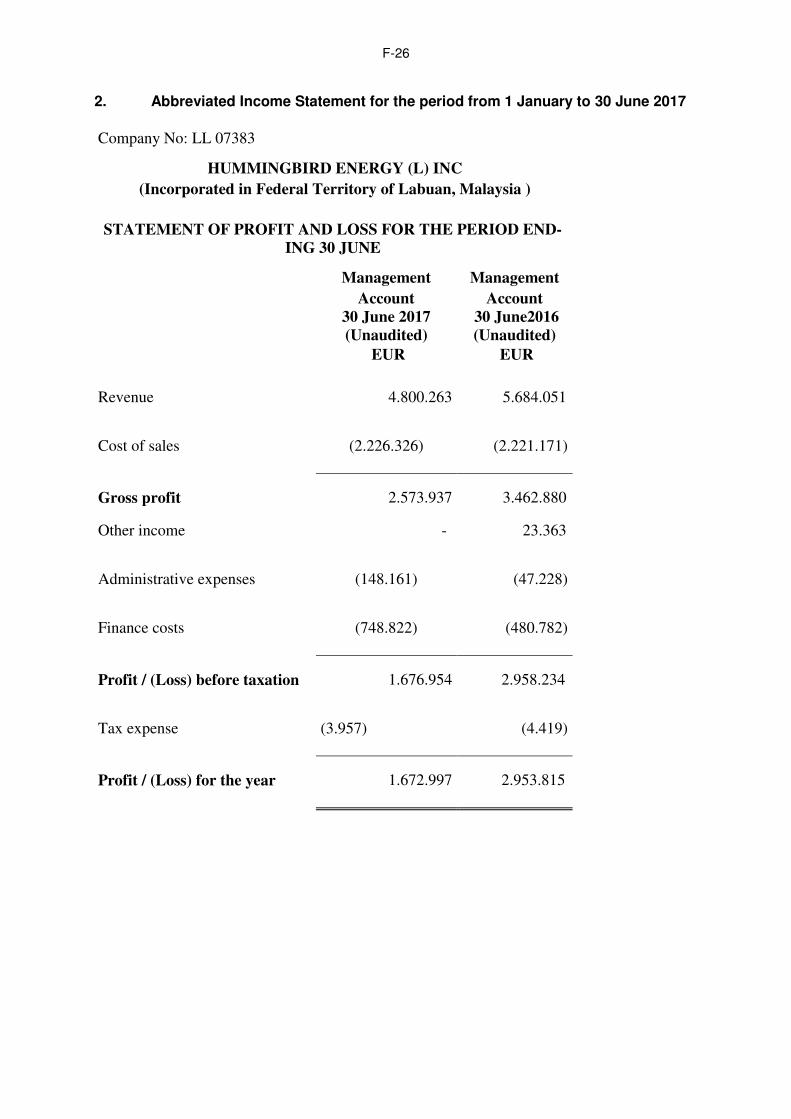

STATEMENT OF PROFIT AND LOSS 1 January

until 30 June 2017

(Unaudited)

1 January until 30

June2016 (Unaudited)

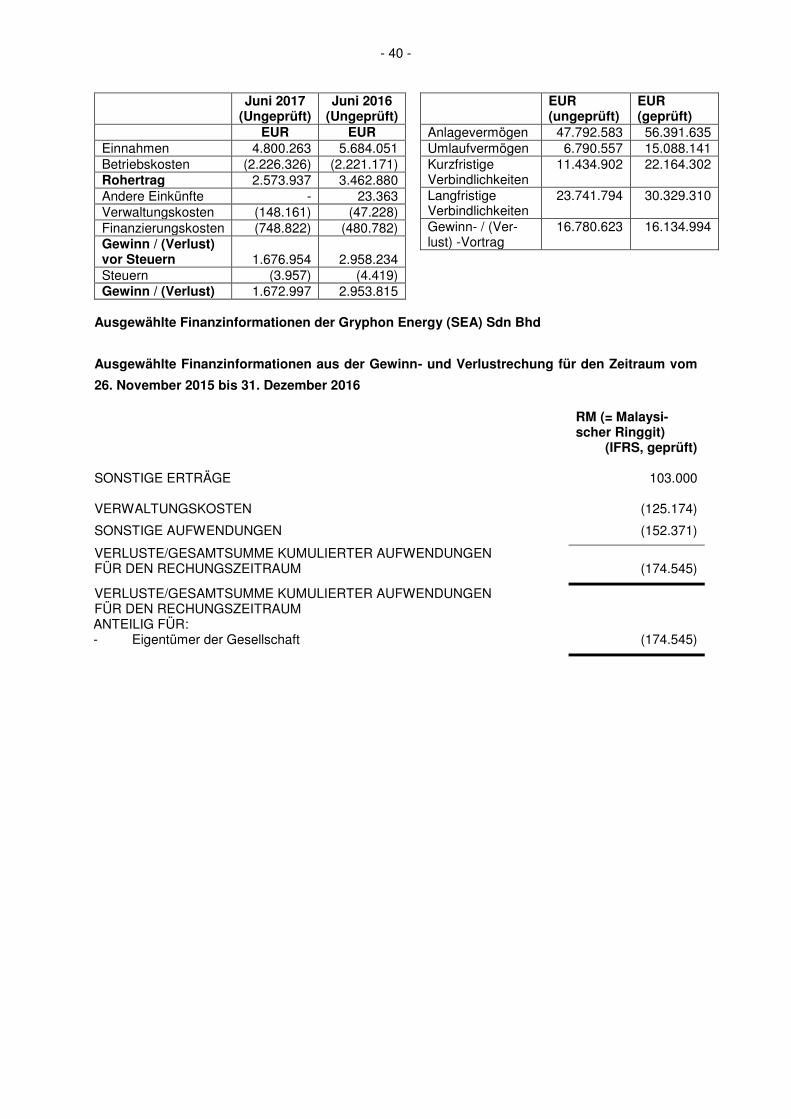

EUR EUR Revenue 4.800.263 5.684.051 Cost of sales (2.226.326) (2.221.171) Gross profit 2.573.937 3.462.880 Other income - 23.363 Administrative expenses (148.161) (47.228) Finance costs (748.822) (480.782) Profit / (Loss) befo-re taxation 1.676.954 2.958.234 Tax expense (3.957) (4.419) Profit / (Loss) for the year 1.672.997 2.953.815

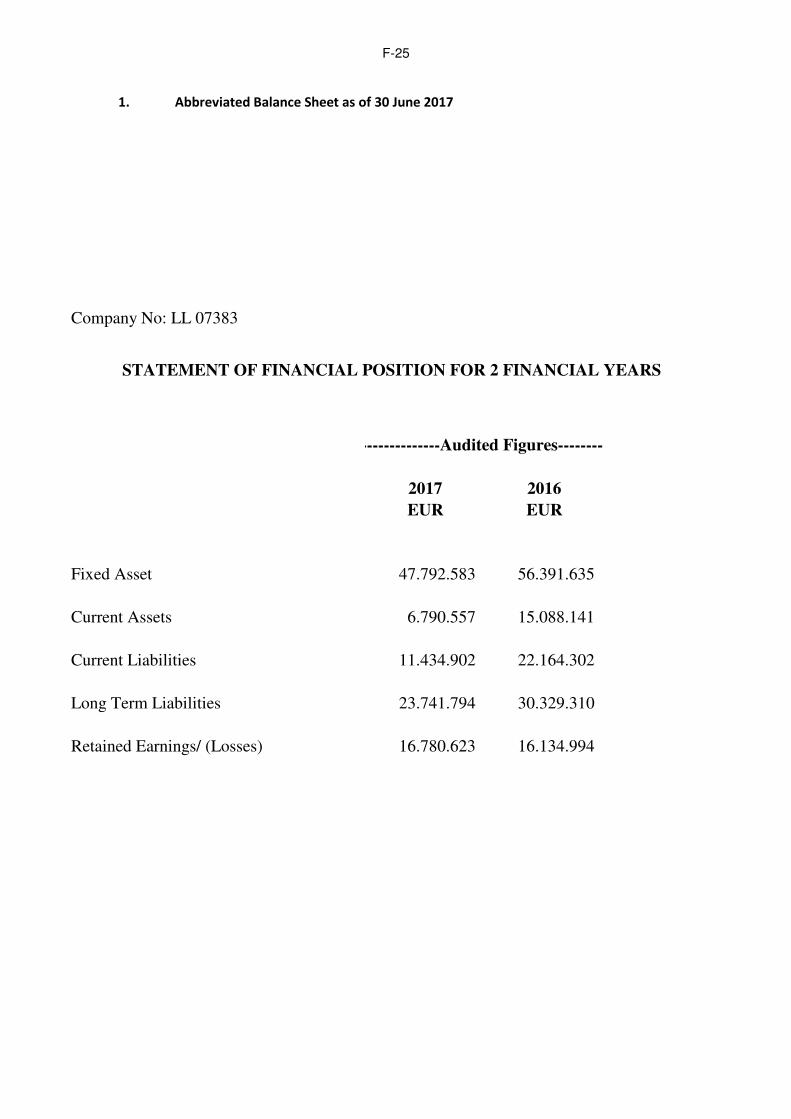

Balance Sheet as of 30 June 2017 and 31 December 2016 30 June

2017 EUR (unaudited)

31 Decem-ber 2016 EUR (audited)

Fixed Assets

47,792,583 56,391,635

Current Assets

6,790,557 15,088,141

Current Liabilities

11,434,902 22,164,302

Long Term Liabilities

23,741,794 30,329,310

Retained Earnings / (Losses)

16,780,623 16,134,994

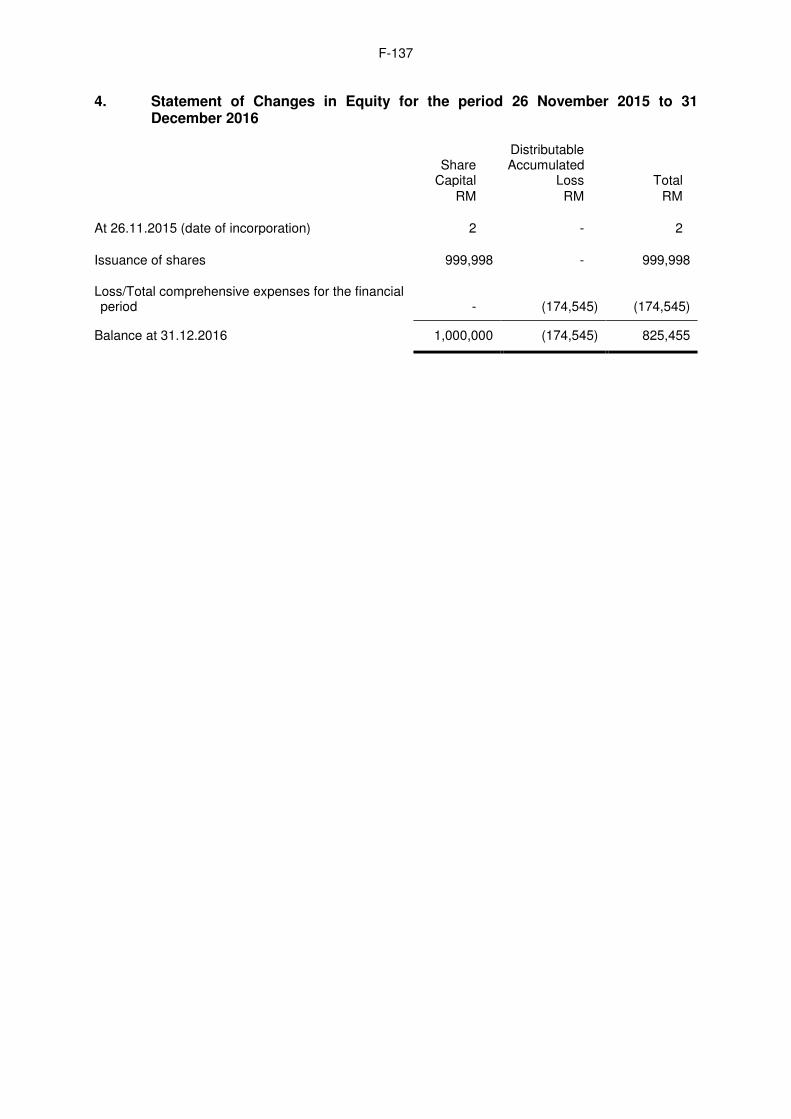

Selected Financial Information of Gryphon Energy (SEA) Sdn Bhd

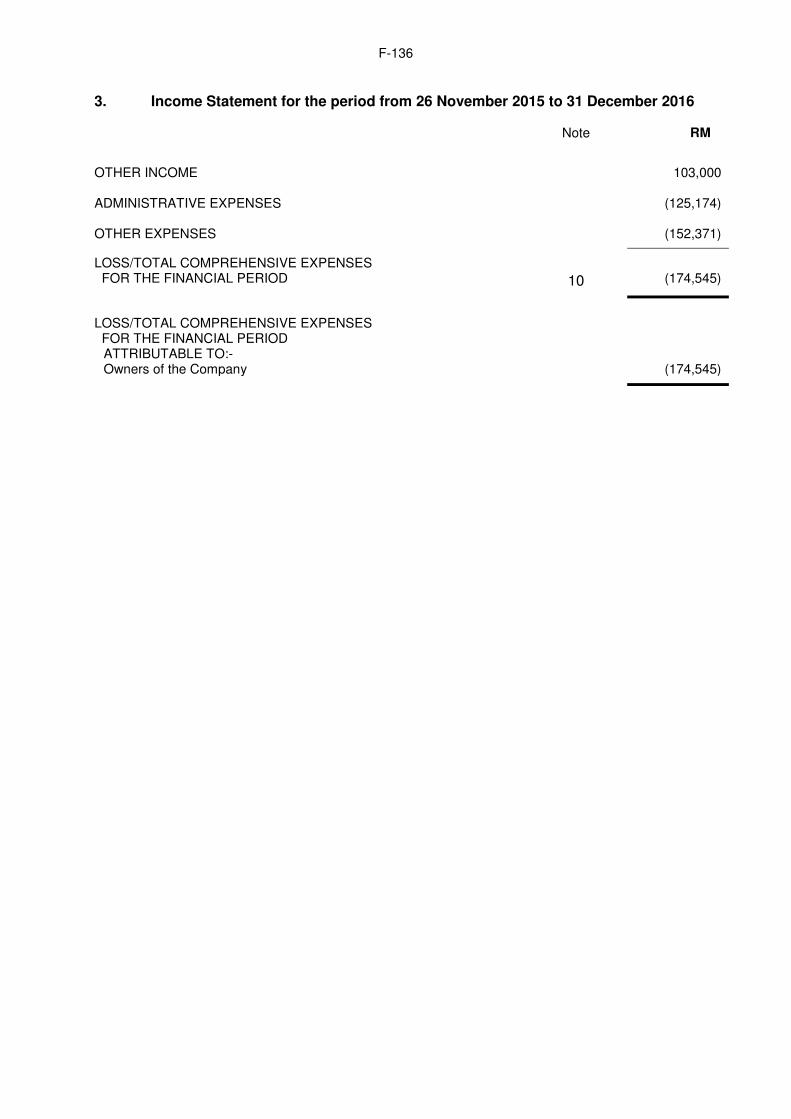

Selected Financial Information from the Profit and Loss Statement for the Period from

26 November 2015 until 31 December 2016 RM (=Malaysian

Ringgit) (IFRS, audited)

OTHER INCOME 103,000 ADMINISTRATIVE EXPENSES (125,174) OTHER EXPENSES (152,371) LOSS/TOTAL COMPREHENSIVE EXPENSES FOR THE FINANCIAL PERIOD

(174,545)

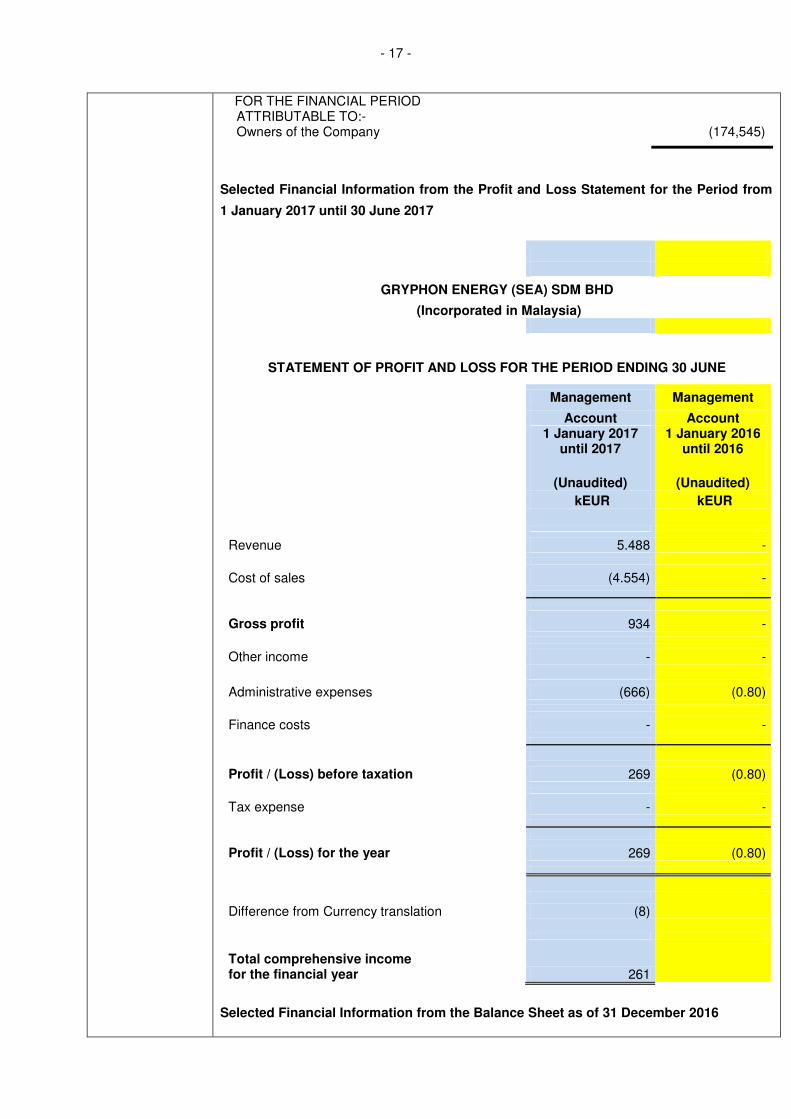

LOSS/TOTAL COMPREHENSIVE EXPENSES

- 17 -

FOR THE FINANCIAL PERIOD ATTRIBUTABLE TO:- Owners of the Company

(174,545)

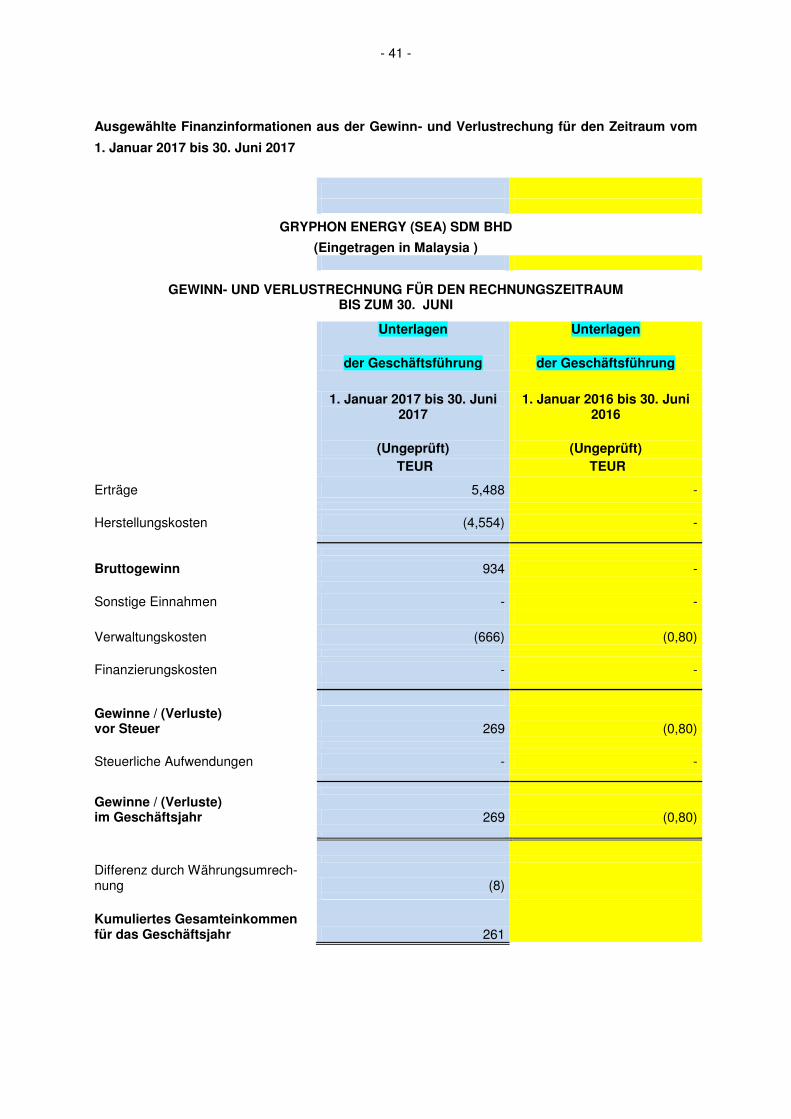

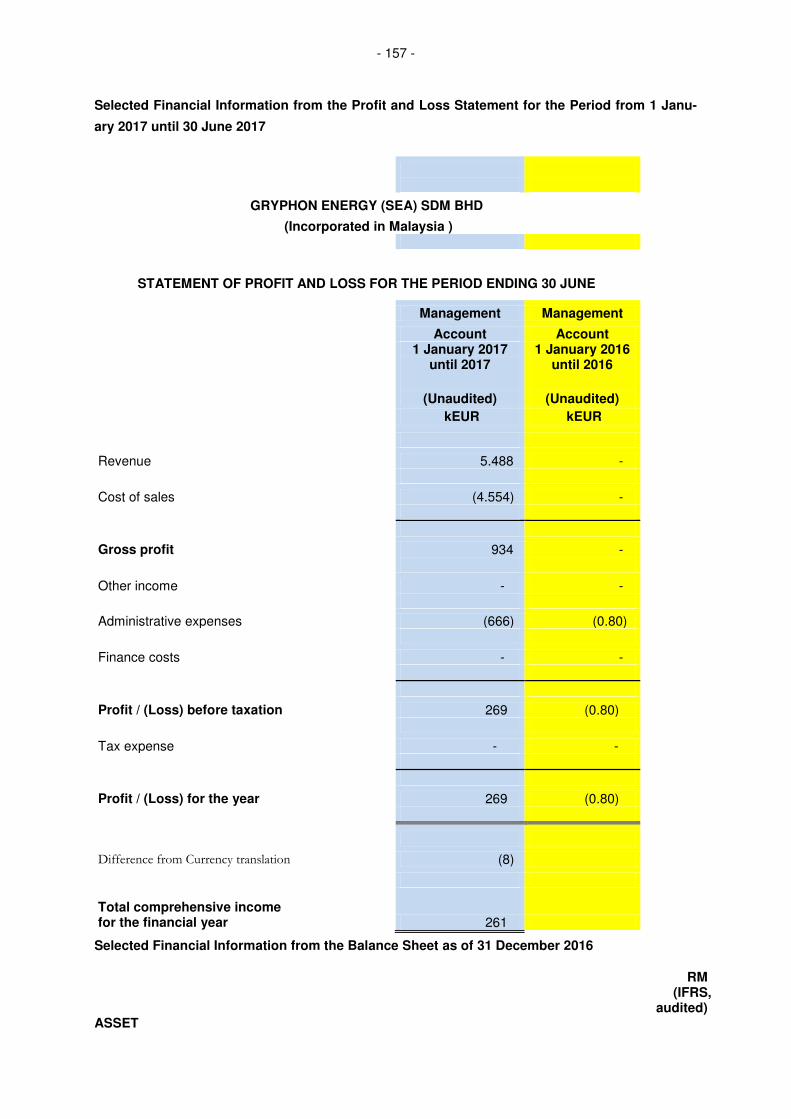

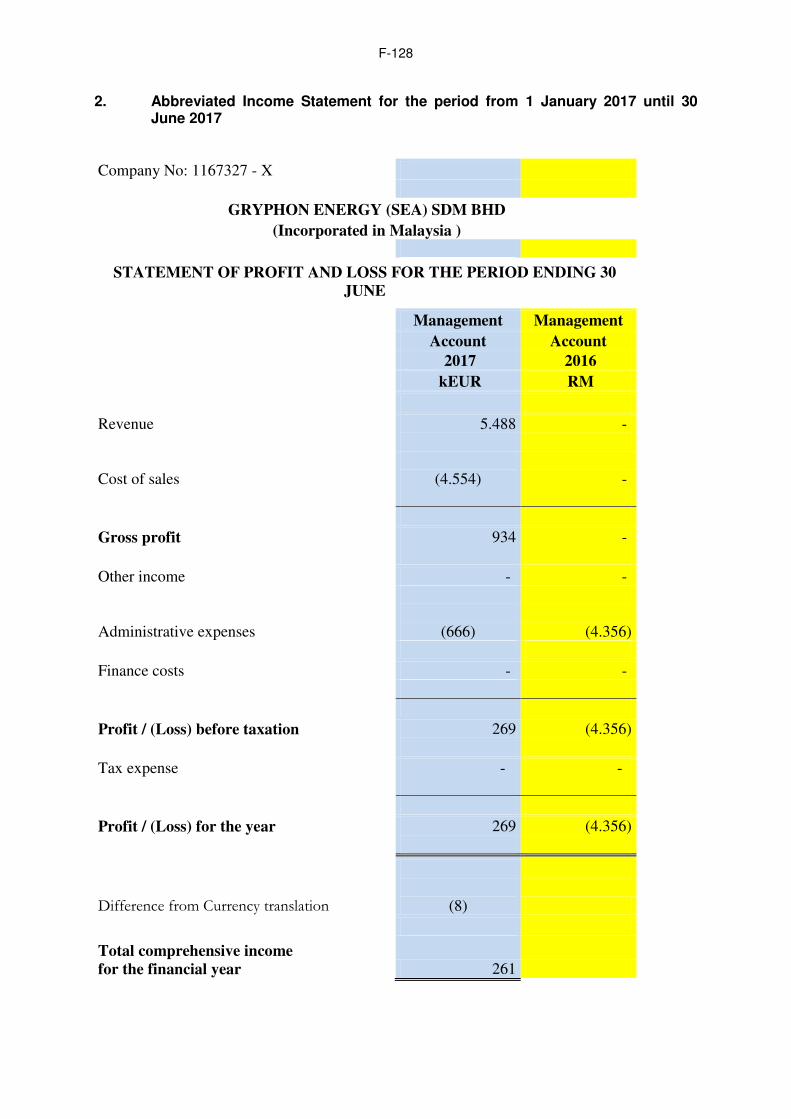

Selected Financial Information from the Profit and Loss Statement for the Period from

1 January 2017 until 30 June 2017

GRYPHON ENERGY (SEA) SDM BHD

(Incorporated in Malaysia)

STATEMENT OF PROFIT AND LOSS FOR THE PERIOD ENDING 30 JUNE

Management Management

Account Account 1 January 2017

until 2017

(Unaudited)

1 January 2016 until 2016

(Unaudited) kEUR kEUR

Revenue 5.488 -

Cost of sales (4.554) -

Gross profit 934 -

Other income - -

Administrative expenses (666) (0.80)

Finance costs - -

Profit / (Loss) before taxation 269 (0.80)

Tax expense - -

Profit / (Loss) for the year 269 (0.80)

Difference from Currency translation (8)

Total comprehensive income for the financial year 261

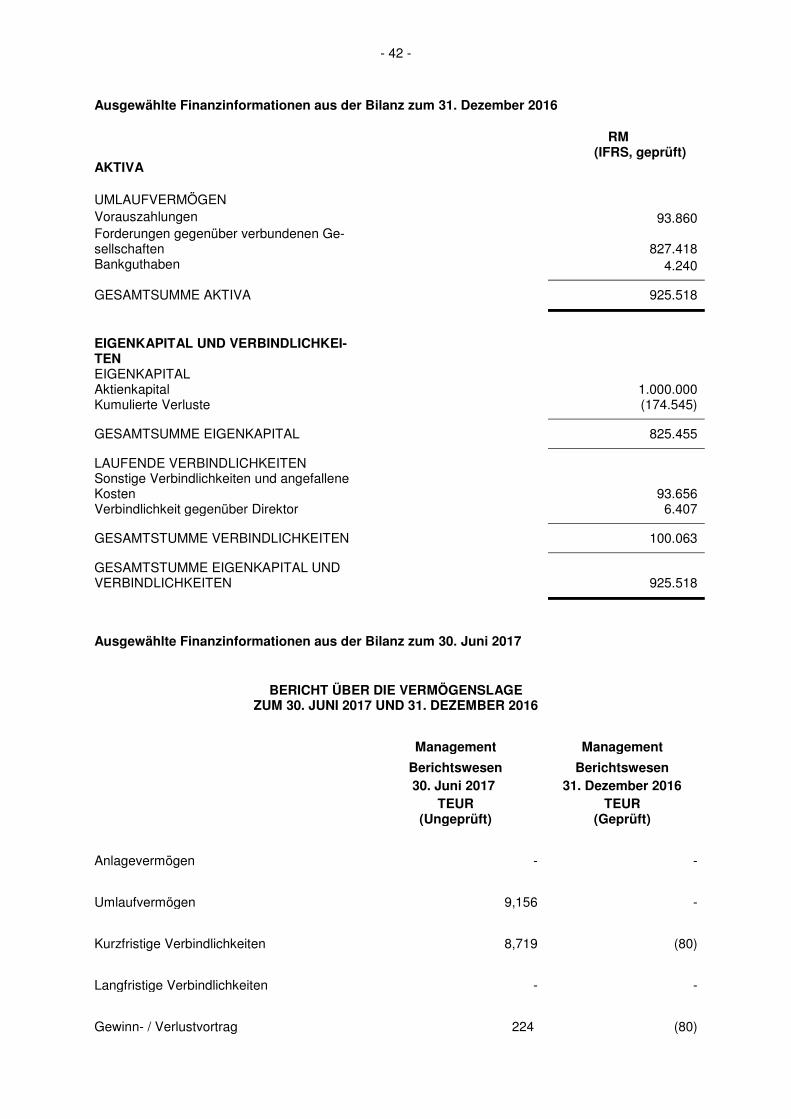

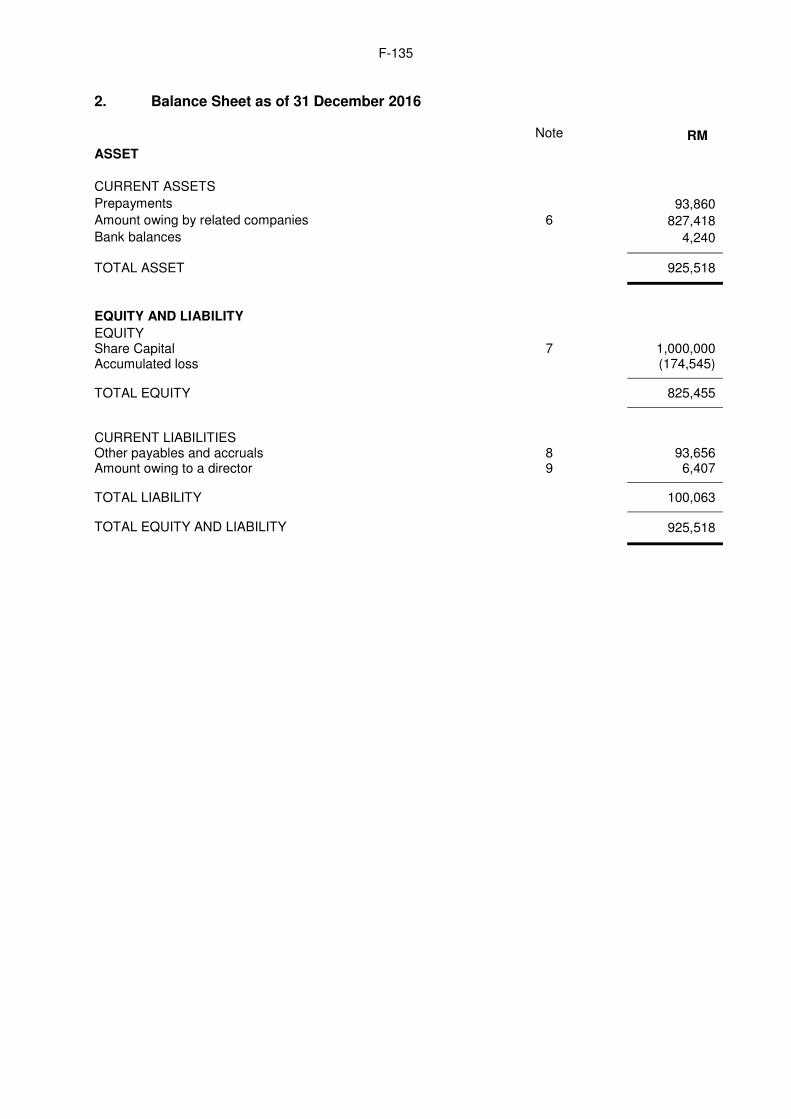

Selected Financial Information from the Balance Sheet as of 31 December 2016

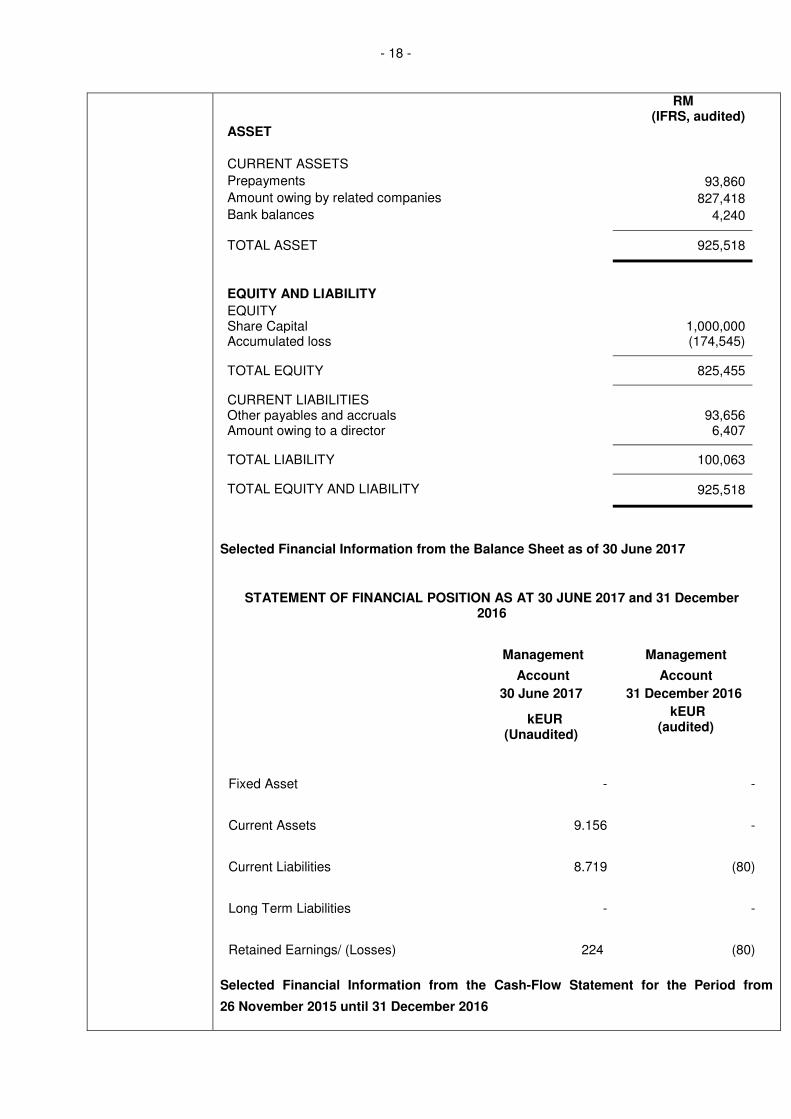

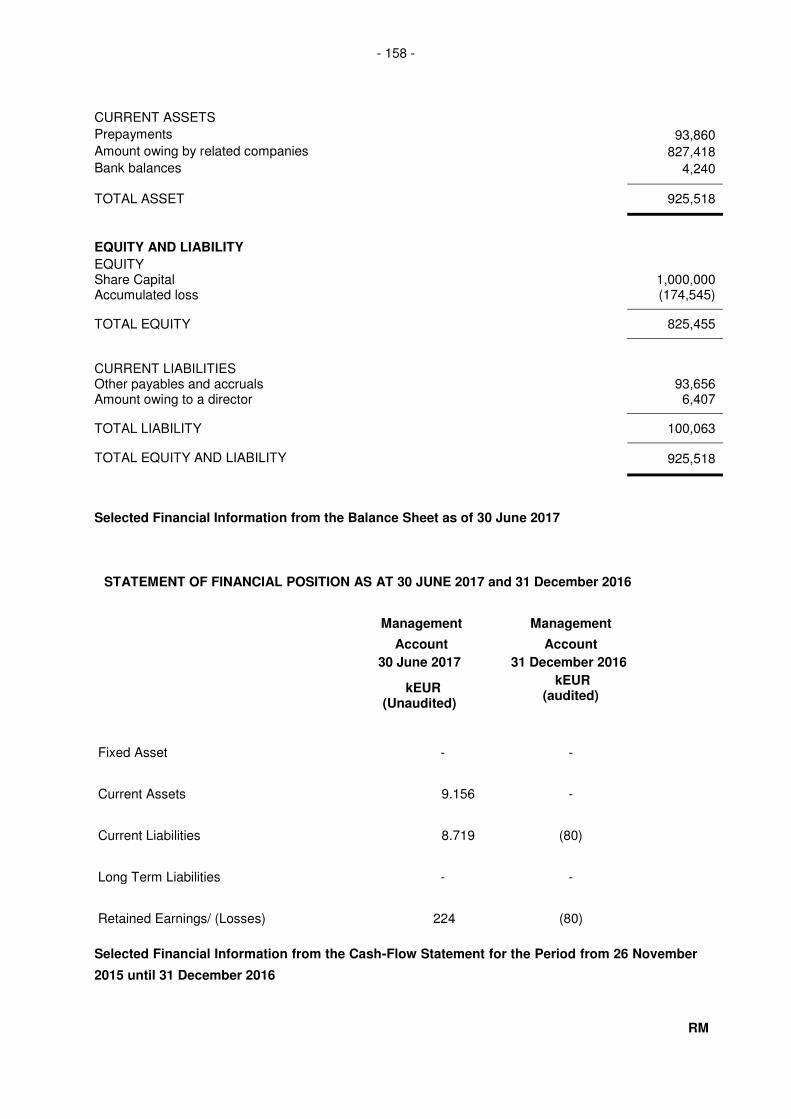

- 18 -

RM (IFRS, audited)

ASSET

CURRENT ASSETS

Prepayments 93,860 Amount owing by related companies 827,418 Bank balances 4,240 TOTAL ASSET 925,518

EQUITY AND LIABILITY

EQUITY Share Capital 1,000,000 Accumulated loss (174,545) TOTAL EQUITY 825,455 CURRENT LIABILITIES Other payables and accruals 93,656 Amount owing to a director 6,407 TOTAL LIABILITY 100,063 TOTAL EQUITY AND LIABILITY

925,518

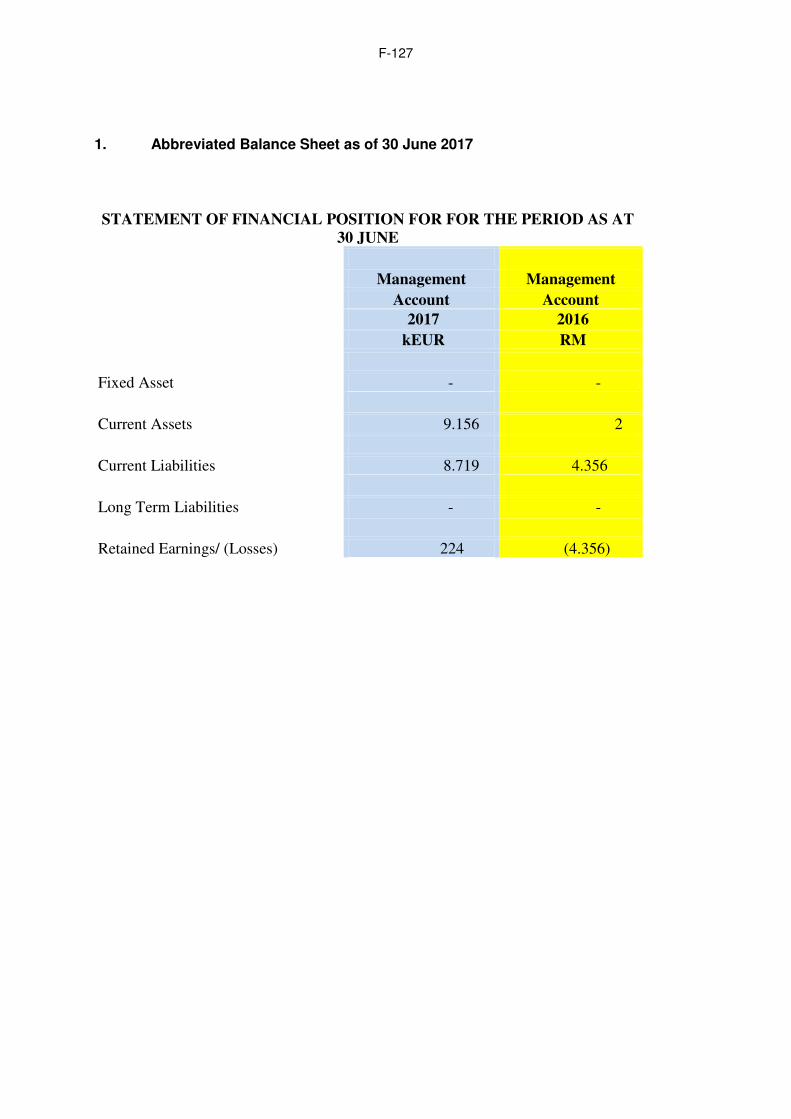

Selected Financial Information from the Balance Sheet as of 30 June 2017

STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2017 and 31 December 2016

Management Management

Account Account 30 June 2017 31 December 2016

kEUR (Unaudited)

kEUR (audited)

Fixed Asset - -

Current Assets 9.156 -

Current Liabilities 8.719 (80)

Long Term Liabilities - -

Retained Earnings/ (Losses) 224 (80)

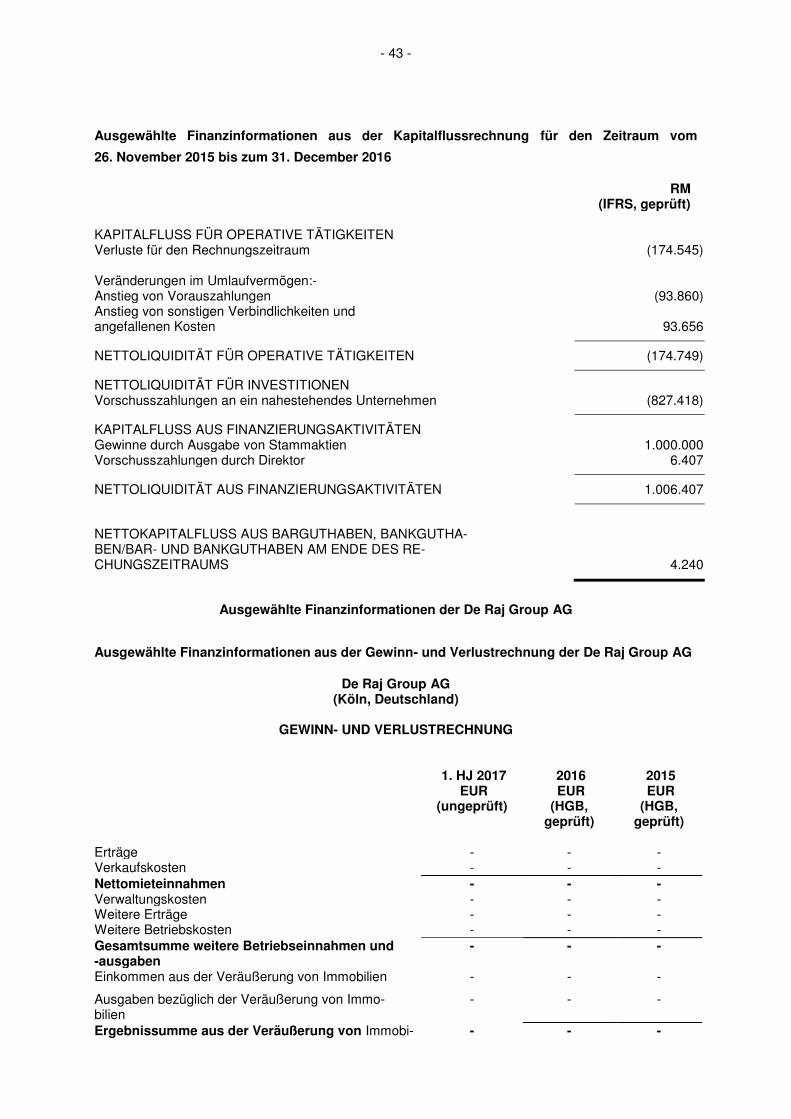

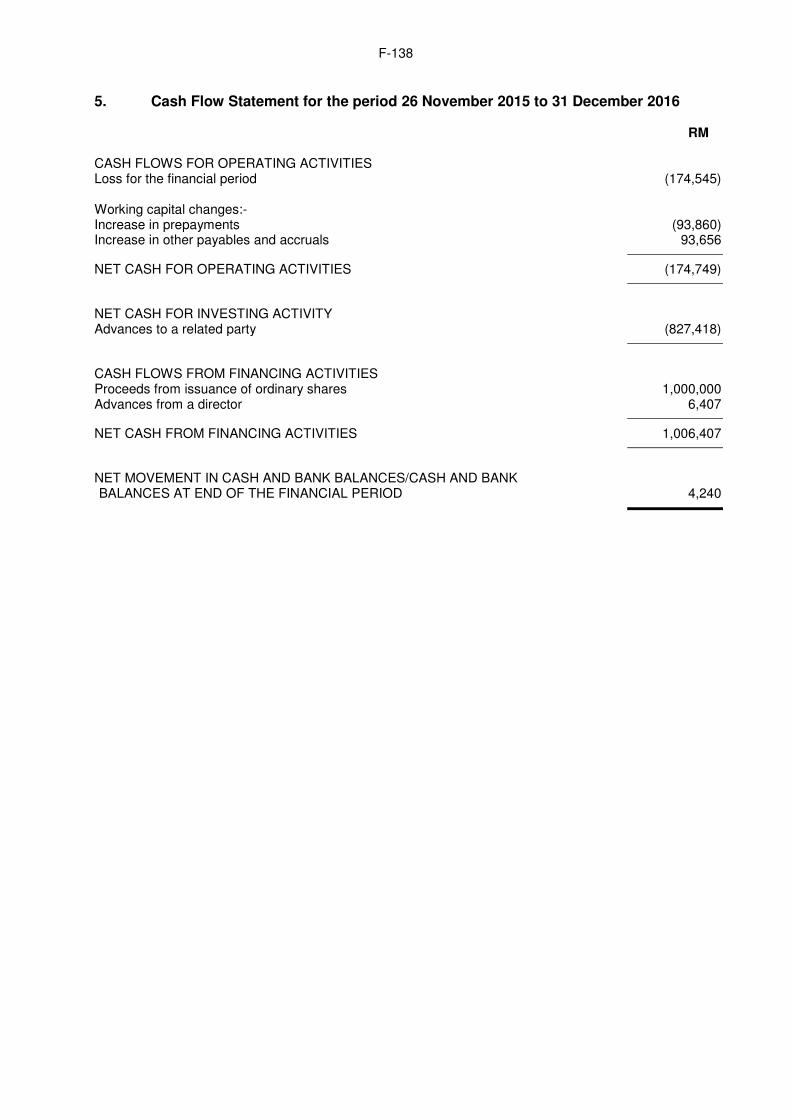

Selected Financial Information from the Cash-Flow Statement for the Period from

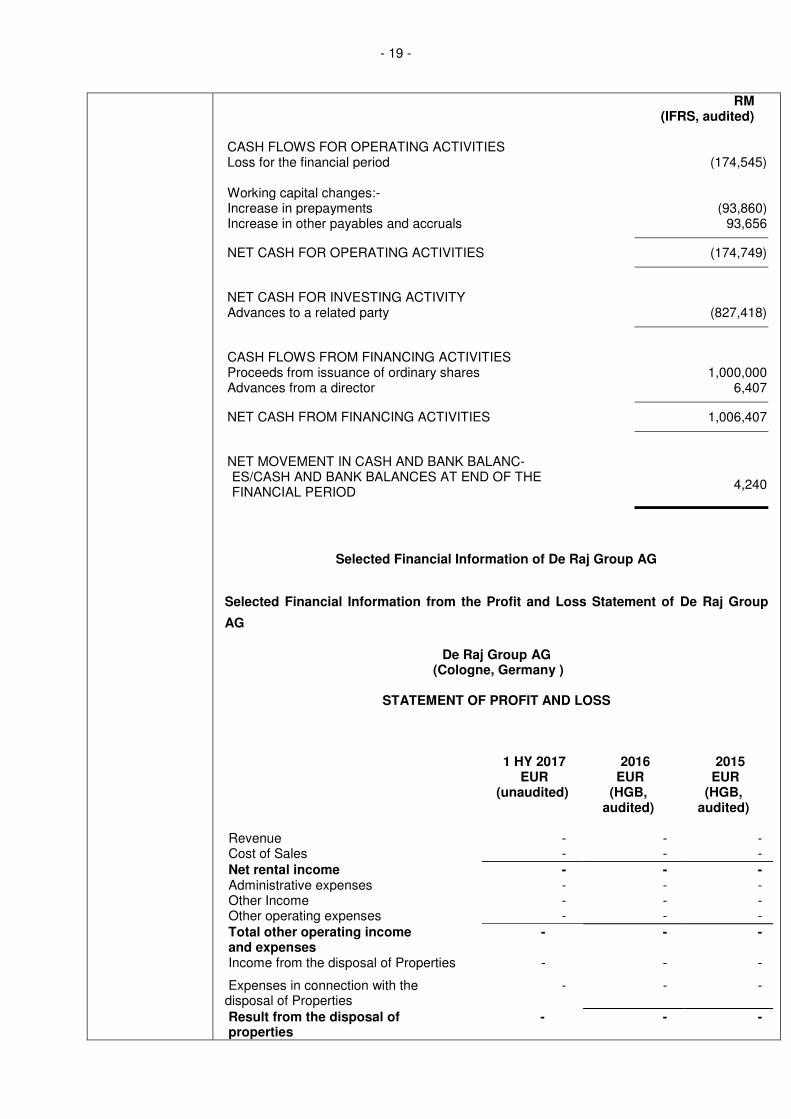

26 November 2015 until 31 December 2016

- 19 -

RM (IFRS, audited)

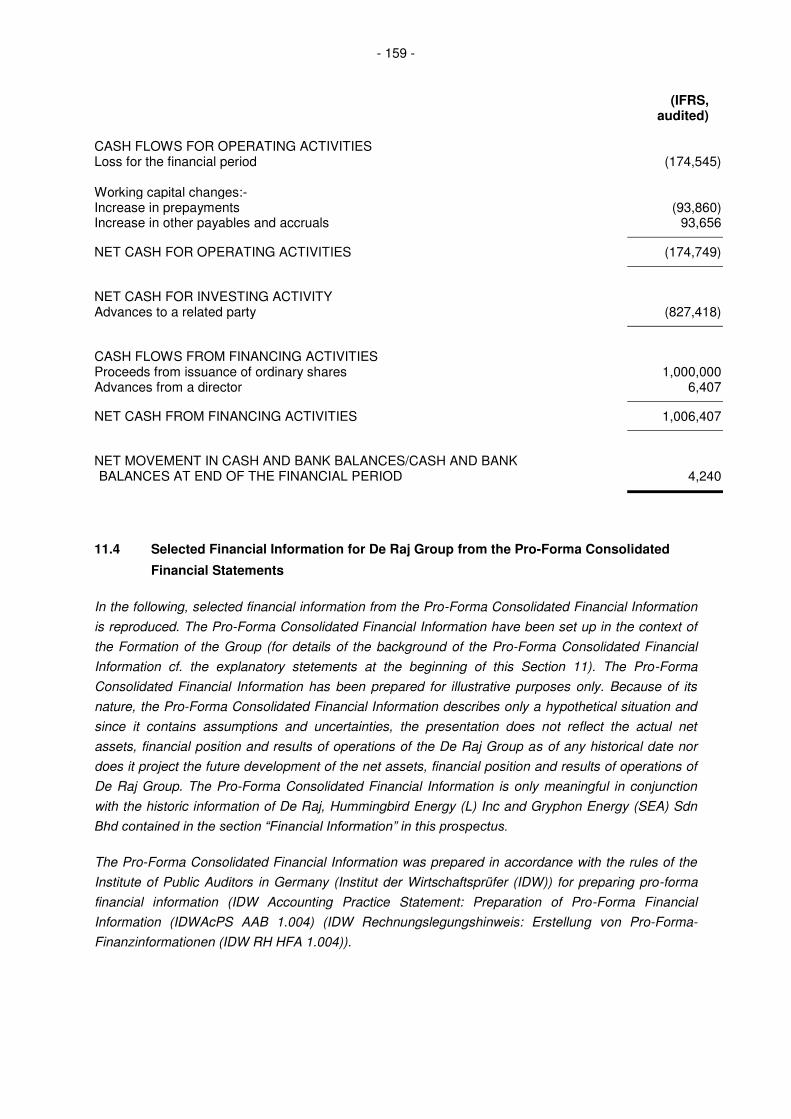

CASH FLOWS FOR OPERATING ACTIVITIES Loss for the financial period (174,545) Working capital changes:- Increase in prepayments (93,860) Increase in other payables and accruals 93,656 NET CASH FOR OPERATING ACTIVITIES (174,749) NET CASH FOR INVESTING ACTIVITY Advances to a related party (827,418) CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from issuance of ordinary shares 1,000,000 Advances from a director 6,407 NET CASH FROM FINANCING ACTIVITIES 1,006,407 NET MOVEMENT IN CASH AND BANK BALANC-ES/CASH AND BANK BALANCES AT END OF THE FINANCIAL PERIOD

4,240

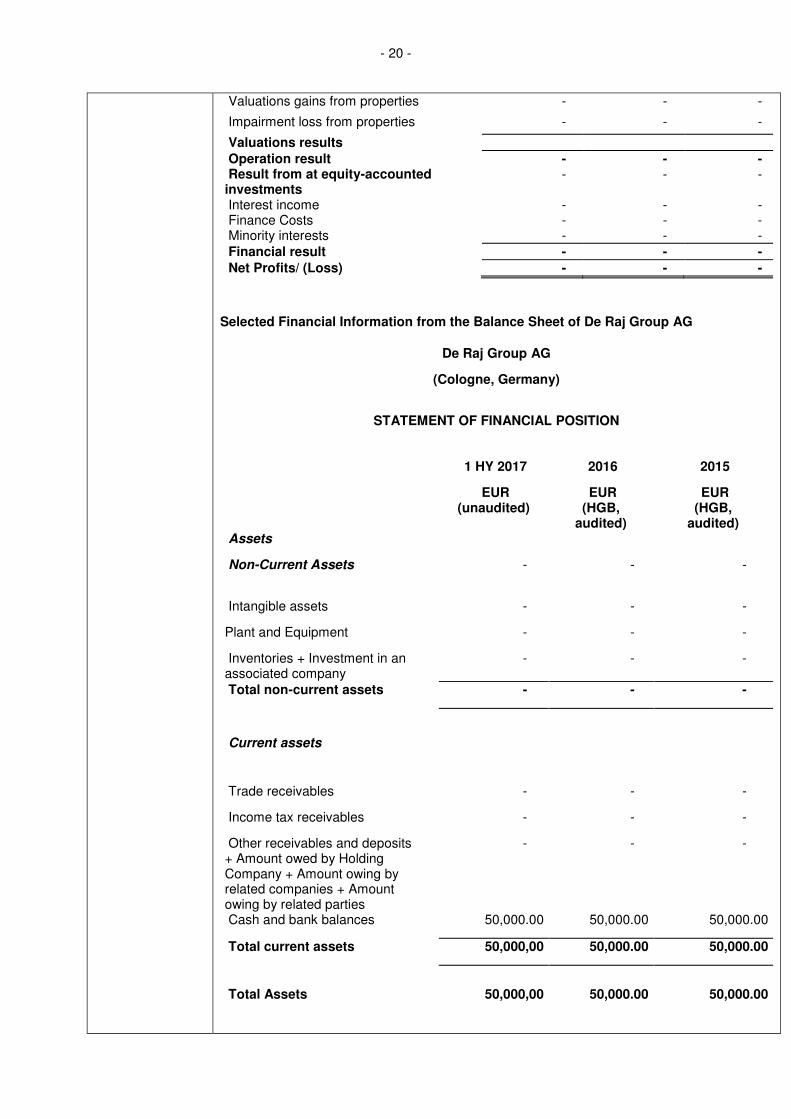

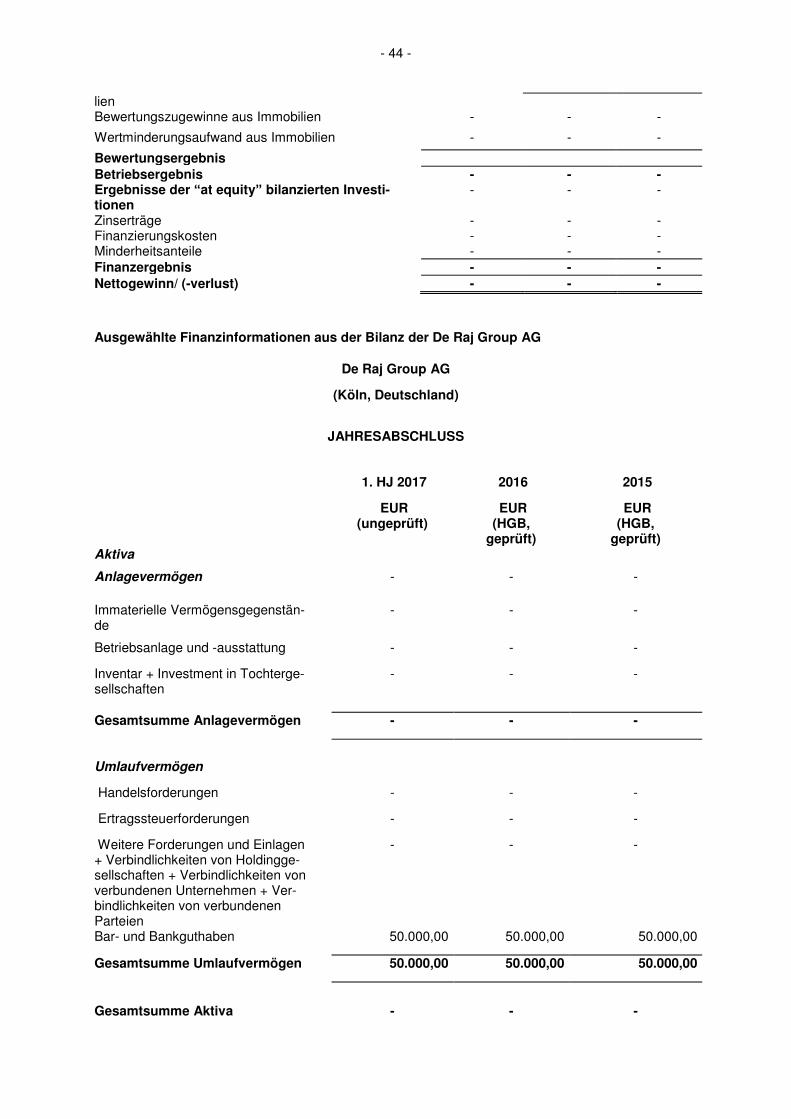

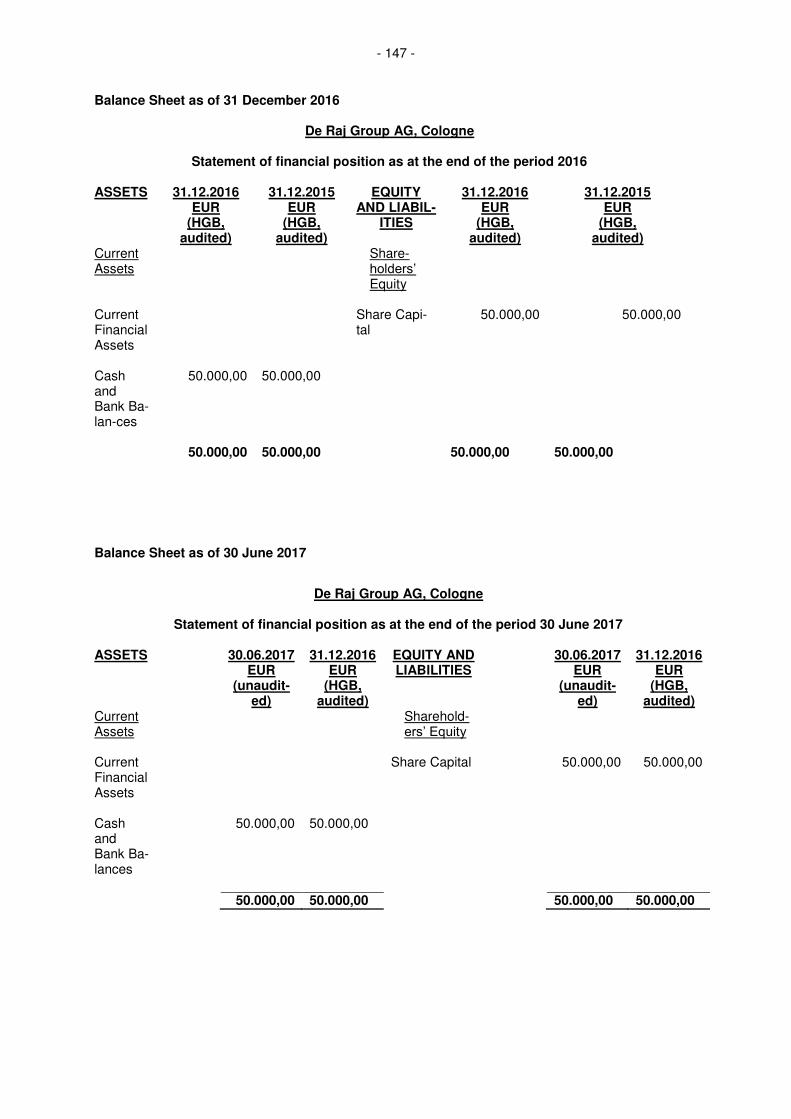

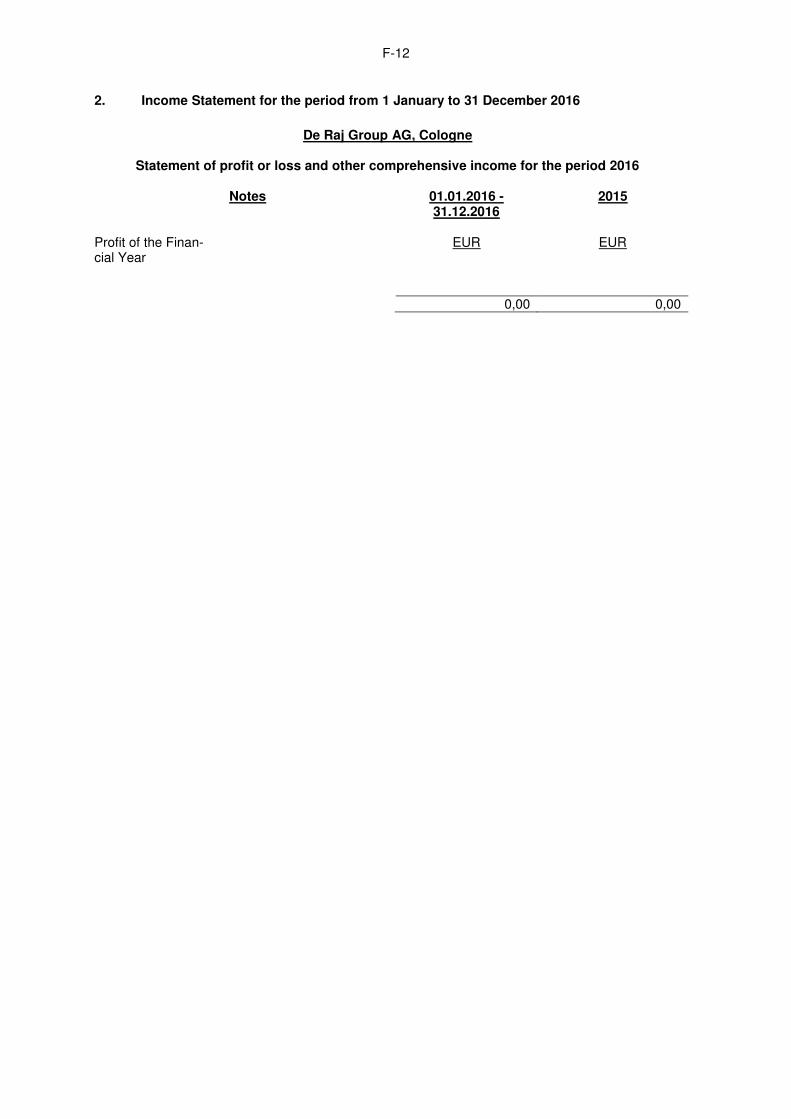

Selected Financial Information of De Raj Group AG

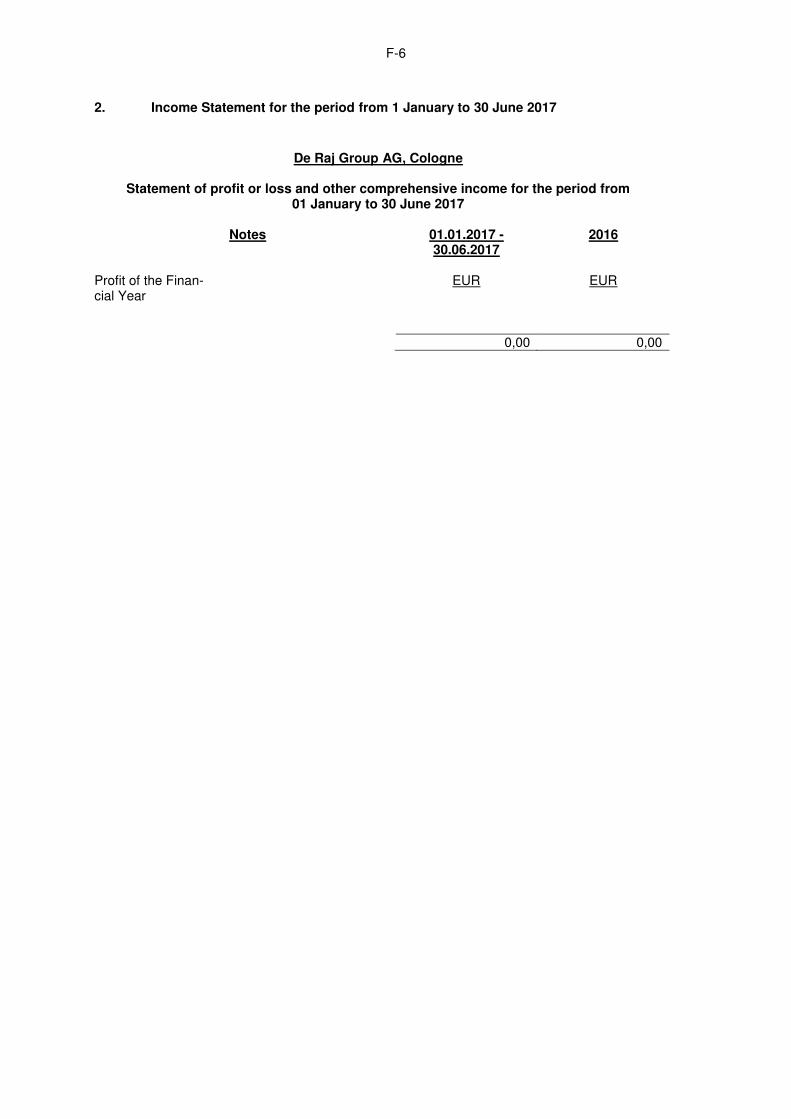

Selected Financial Information from the Profit and Loss Statement of De Raj Group

AG

De Raj Group AG (Cologne, Germany )

STATEMENT OF PROFIT AND LOSS

1 HY 2017 2016 2015 EUR

(unaudited) EUR (HGB,

audited)

EUR (HGB,

audited)

Revenue - - - Cost of Sales - - - Net rental income - - - Administrative expenses - - - Other Income - - - Other operating expenses - - - Total other operating income - and expenses

- -

Income from the disposal of Properties - - -

Expenses in connection with the disposal of Properties

- - -

Result from the disposal of - properties

- -

- 20 -

Valuations gains from properties - - -

Impairment loss from properties - - -

Valuations results Operation result - - - Result from at equity-accounted investments

- - -

Interest income - - - Finance Costs - - - Minority interests - - - Financial result - - - Net Profits/ (Loss) - - -

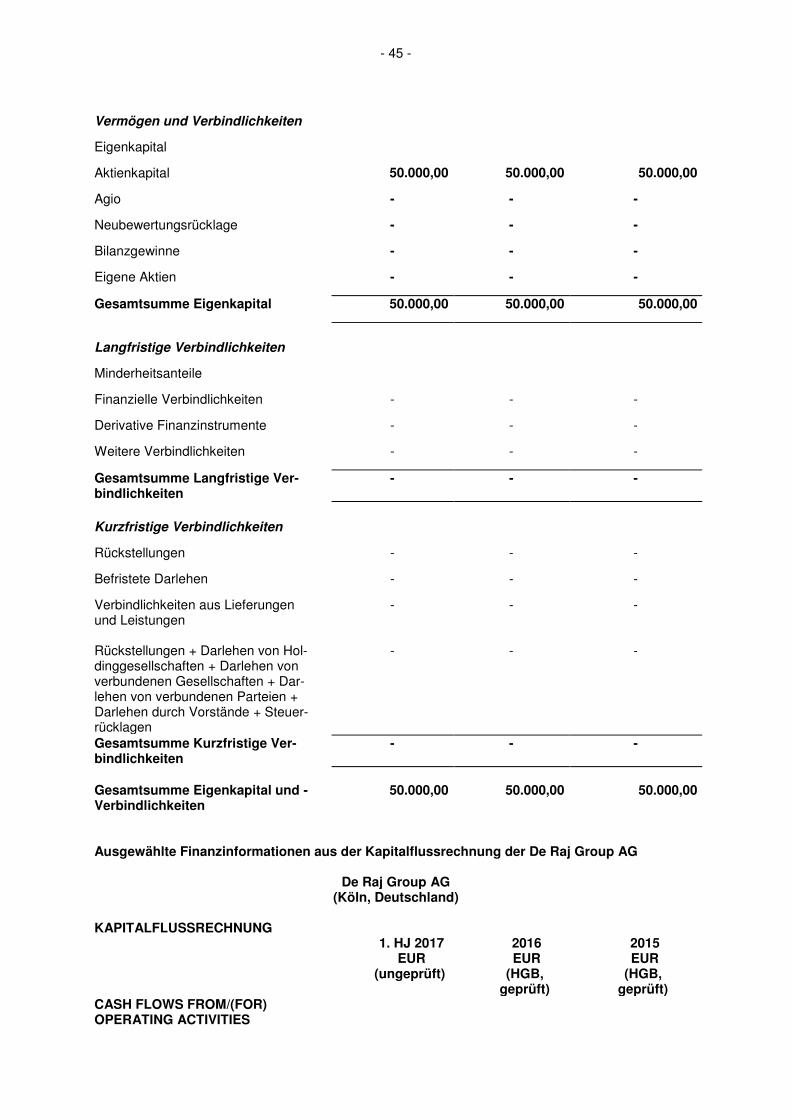

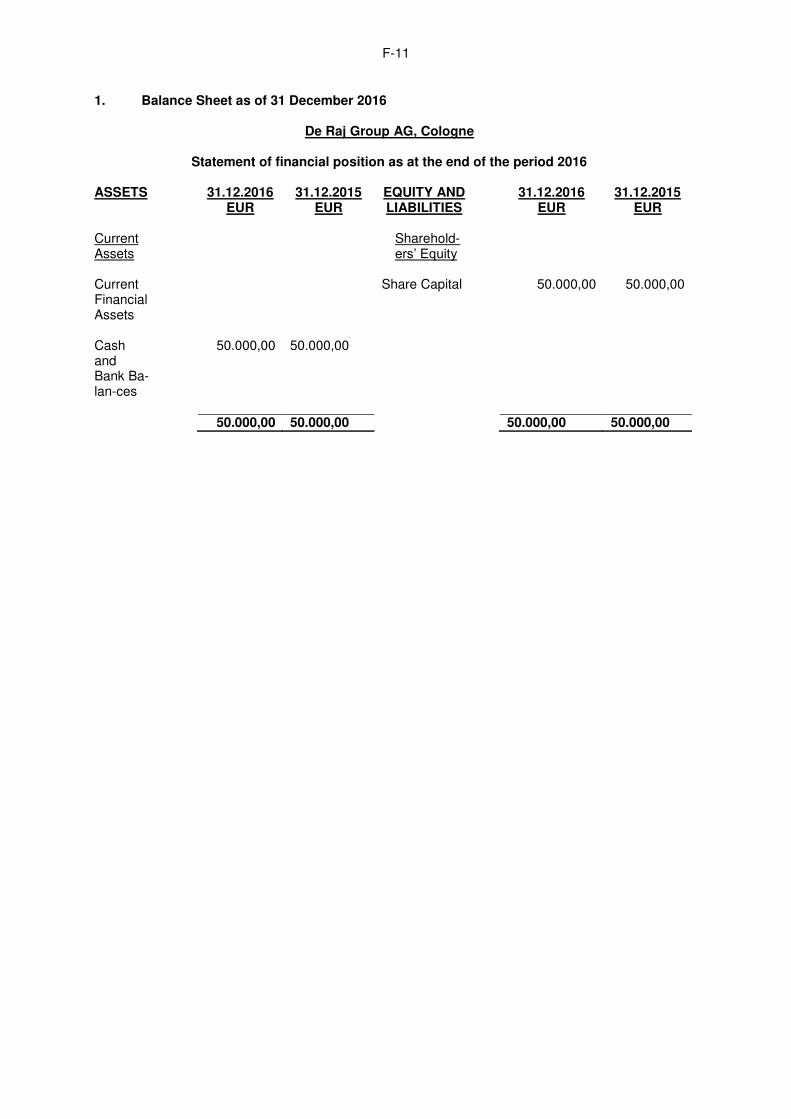

Selected Financial Information from the Balance Sheet of De Raj Group AG

De Raj Group AG

(Cologne, Germany)

STATEMENT OF FINANCIAL POSITION

1 HY 2017 2016 2015

EUR (unaudited)

EUR (HGB,

audited)

EUR (HGB,

audited) Assets

Non-Current Assets - - -

Intangible assets - - -

Plant and Equipment - - -

Inventories + Investment in an associated company

- - -

Total non-current assets - - -

Current assets

Trade receivables - - -

Income tax receivables - - -

Other receivables and deposits + Amount owed by Holding Company + Amount owing by related companies + Amount owing by related parties

- - -

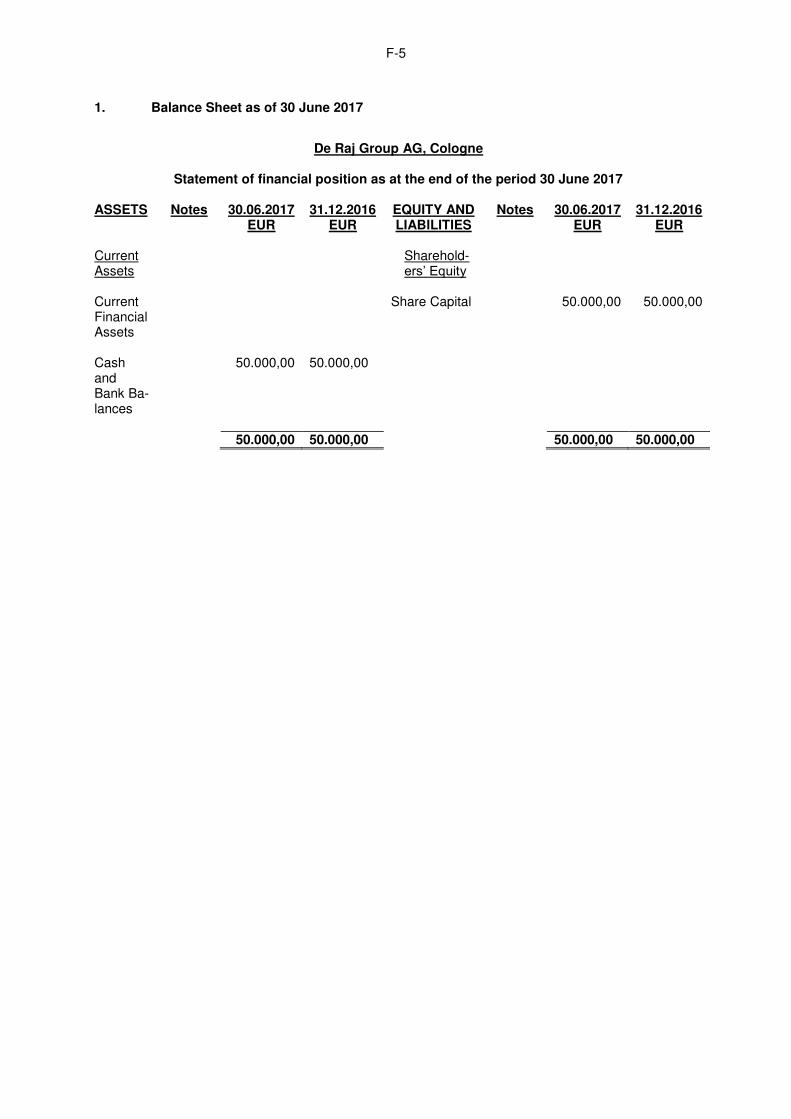

Cash and bank balances 50,000.00 50,000.00 50,000.00

Total current assets 50,000,00 50,000.00 50,000.00

Total Assets 50,000,00 50,000.00 50,000.00

- 21 -

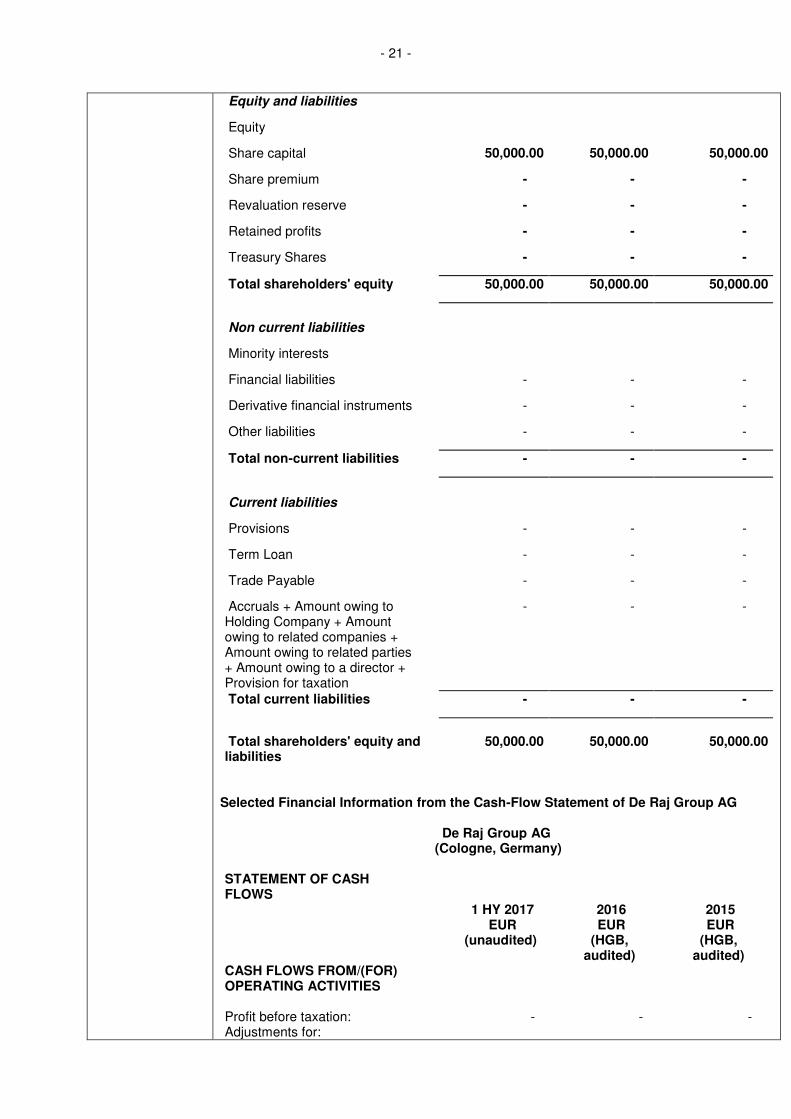

Equity and liabilities

Equity

Share capital 50,000.00 50,000.00 50,000.00

Share premium - - -

Revaluation reserve - - -

Retained profits - - -

Treasury Shares - - -

Total shareholders' equity 50,000.00 50,000.00 50,000.00

Non current liabilities

Minority interests

Financial liabilities - - -

Derivative financial instruments - - -

Other liabilities - - -

Total non-current liabilities - - -

Current liabilities

Provisions - - -

Term Loan - - -

Trade Payable - - -

Accruals + Amount owing to Holding Company + Amount owing to related companies + Amount owing to related parties + Amount owing to a director + Provision for taxation

- - -

Total current liabilities - - -

Total shareholders' equity and liabilities

50,000.00 50,000.00 50,000.00

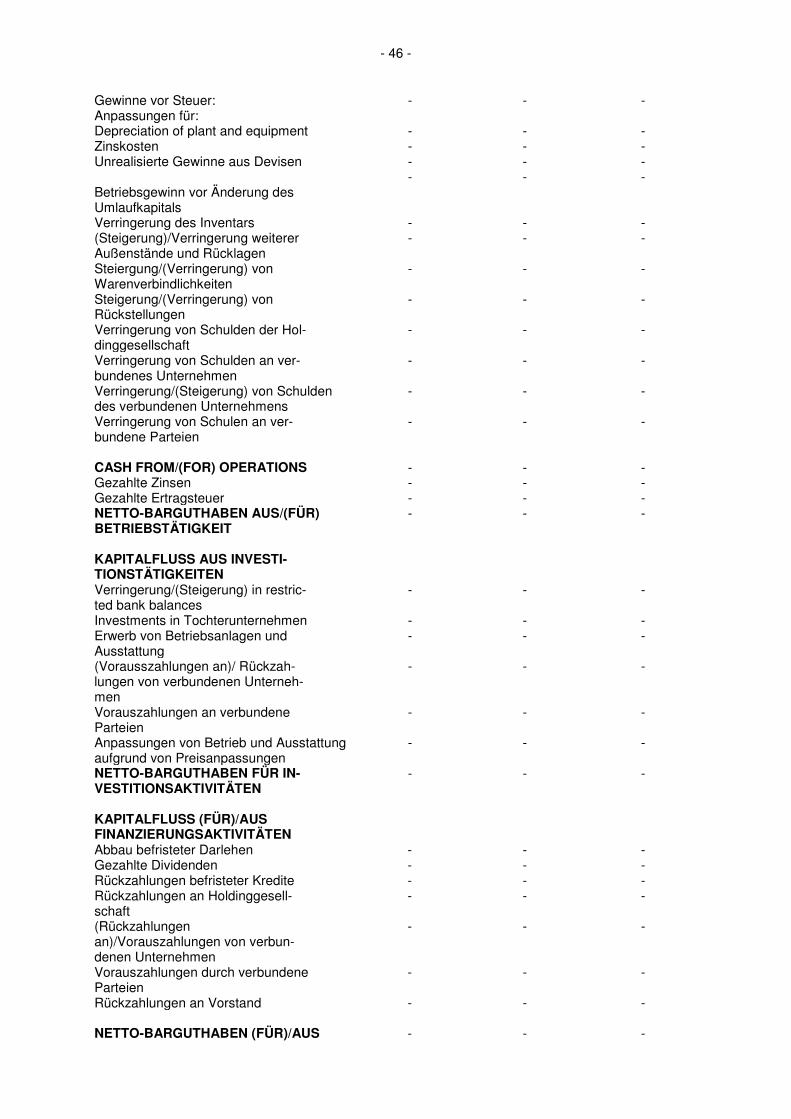

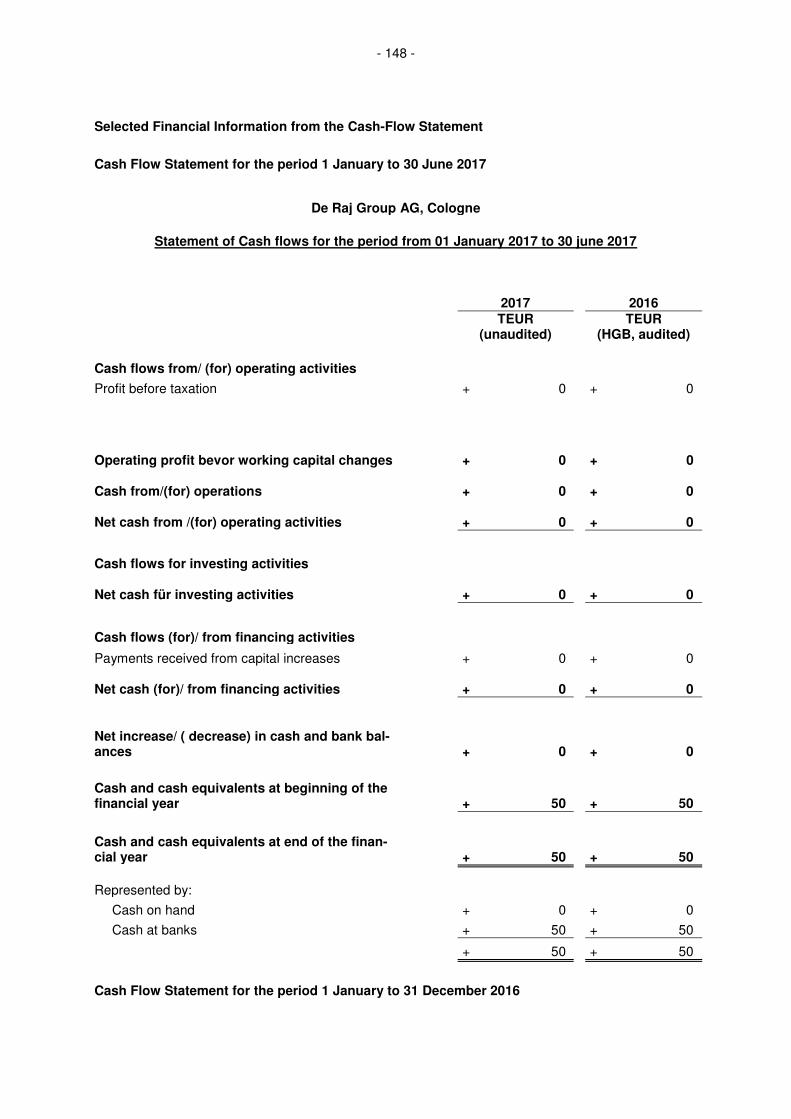

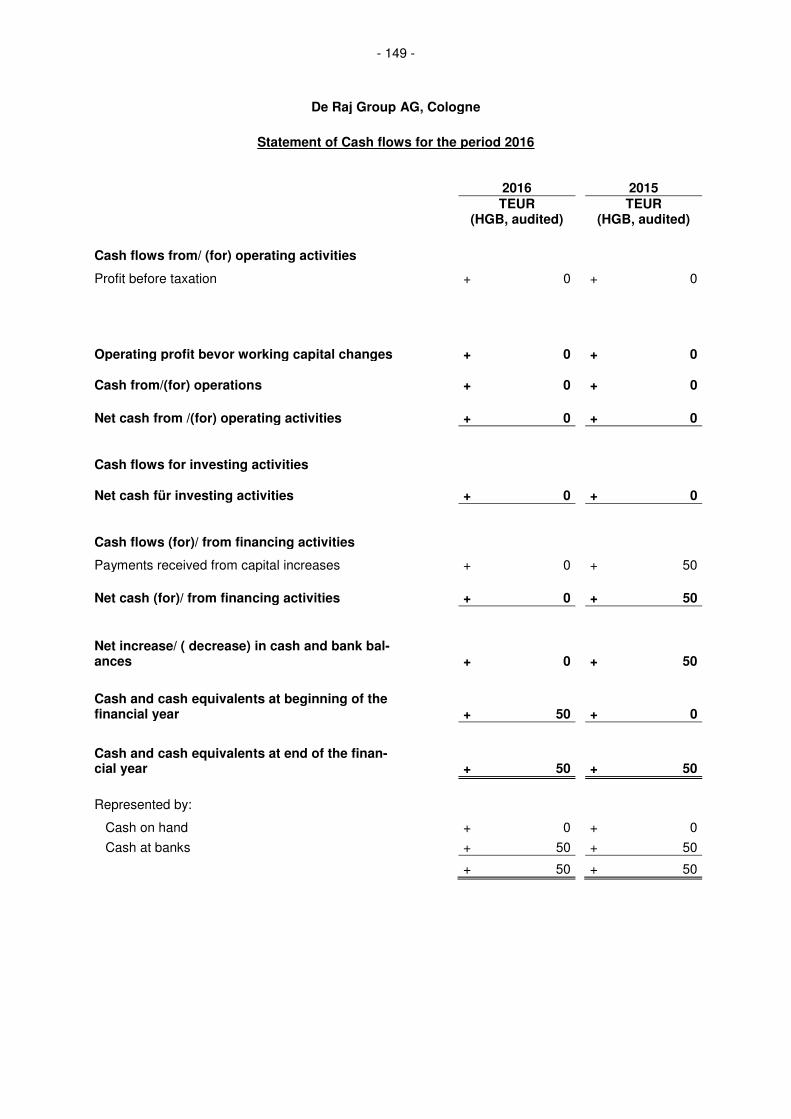

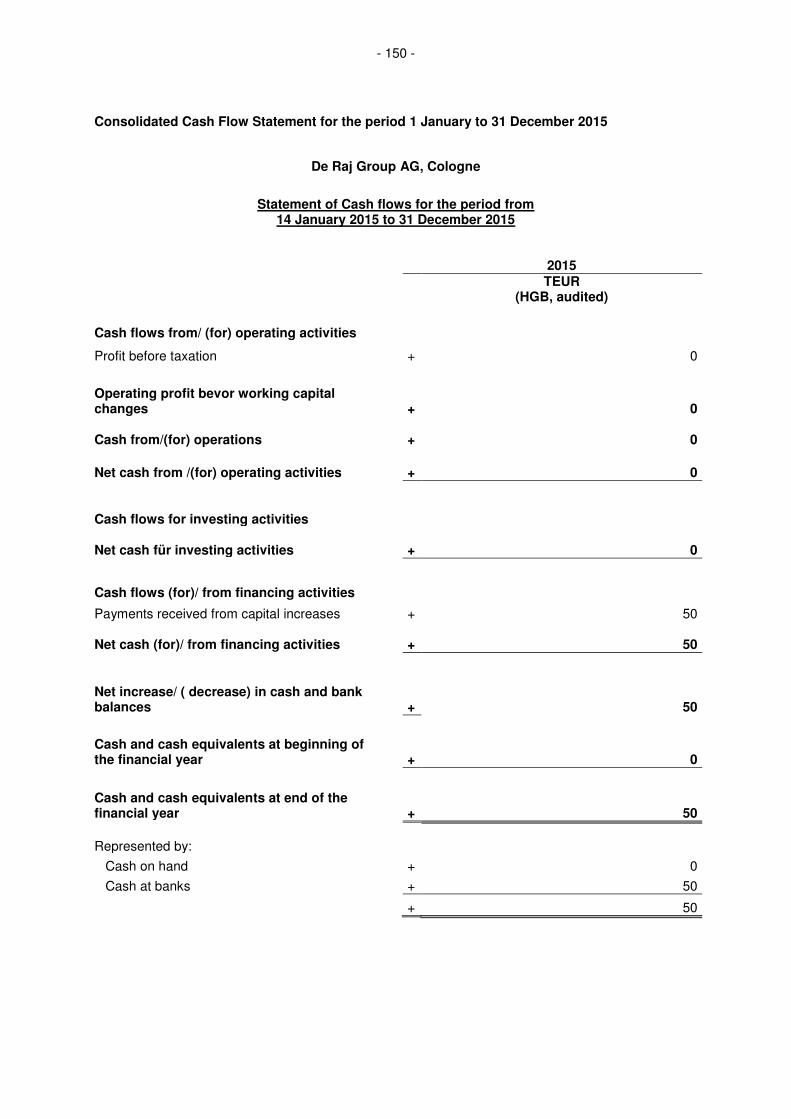

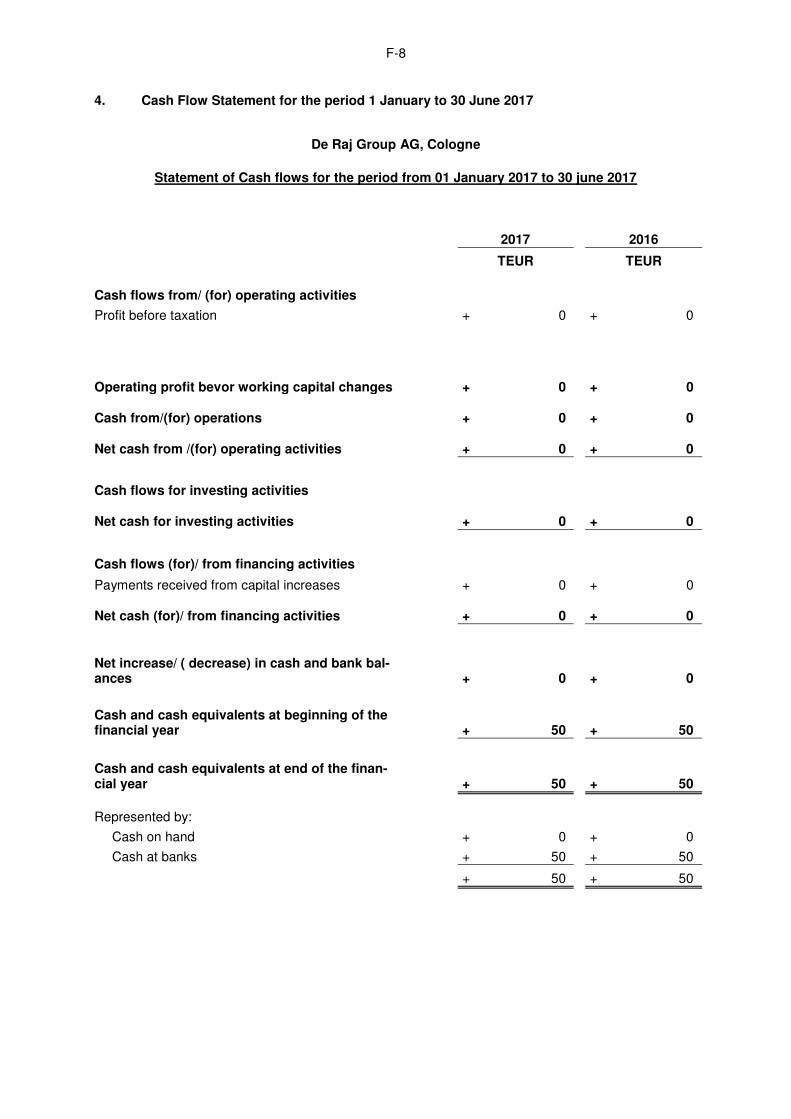

Selected Financial Information from the Cash-Flow Statement of De Raj Group AG

De Raj Group AG (Cologne, Germany)

STATEMENT OF CASH FLOWS

1 HY 2017 2016 2015 EUR

(unaudited) EUR (HGB,

audited)

EUR (HGB,

audited) CASH FLOWS FROM/(FOR) OPERATING ACTIVITIES

Profit before taxation: - - - Adjustments for:

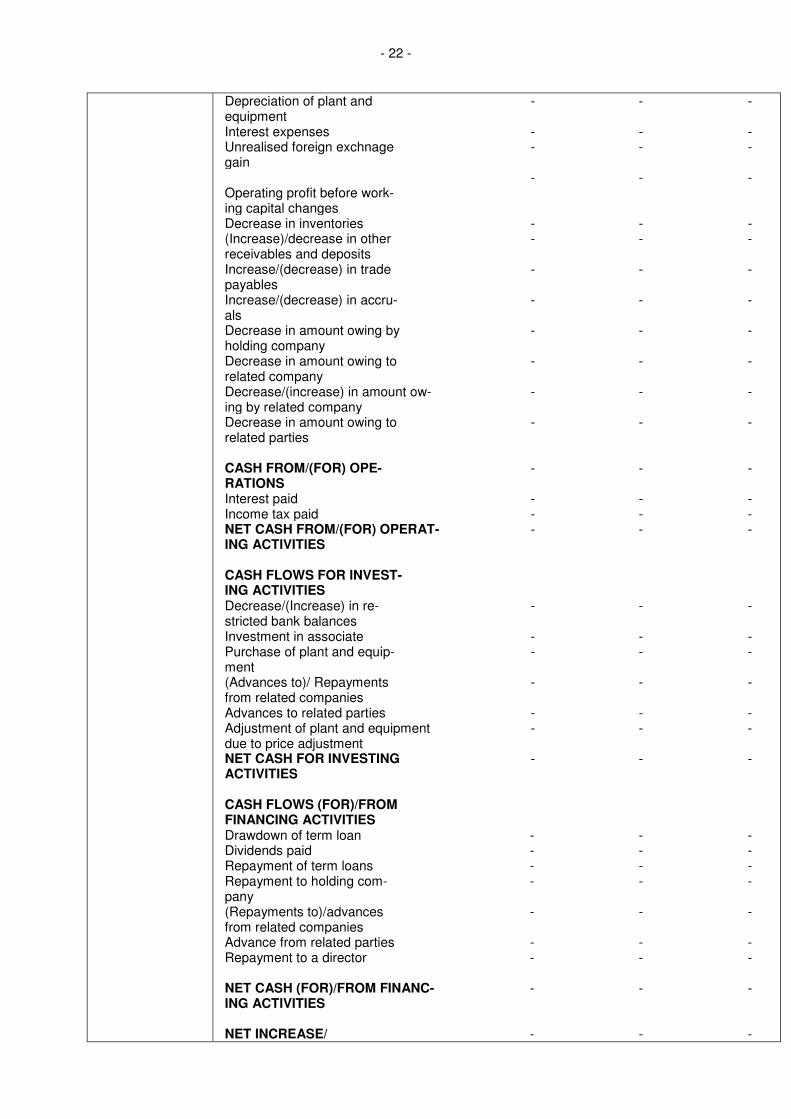

- 22 -

Depreciation of plant and equipment

- - -

Interest expenses - - - Unrealised foreign exchnage gain

- - -

- - - Operating profit before work-ing capital changes

Decrease in inventories - - - (Increase)/decrease in other receivables and deposits

- - -

Increase/(decrease) in trade payables

- - -

Increase/(decrease) in accru-als

- - -

Decrease in amount owing by holding company

- - -

Decrease in amount owing to related company

- - -

Decrease/(increase) in amount ow-ing by related company

- - -

Decrease in amount owing to related parties

- - -

CASH FROM/(FOR) OPE-RATIONS

- - -

Interest paid - - - Income tax paid - - - NET CASH FROM/(FOR) OPERAT-ING ACTIVITIES

- - -

CASH FLOWS FOR INVEST-ING ACTIVITIES

Decrease/(Increase) in re-stricted bank balances

- - -

Investment in associate - - - Purchase of plant and equip-ment

- - -

(Advances to)/ Repayments from related companies

- - -

Advances to related parties - - - Adjustment of plant and equipment due to price adjustment

- - -

NET CASH FOR INVESTING ACTIVITIES

- - -

CASH FLOWS (FOR)/FROM FINANCING ACTIVITIES

Drawdown of term loan - - - Dividends paid - - - Repayment of term loans - - - Repayment to holding com-pany

- - -

(Repayments to)/advances from related companies

- - -

Advance from related parties - - - Repayment to a director - - -

NET CASH (FOR)/FROM FINANC-ING ACTIVITIES

- - -

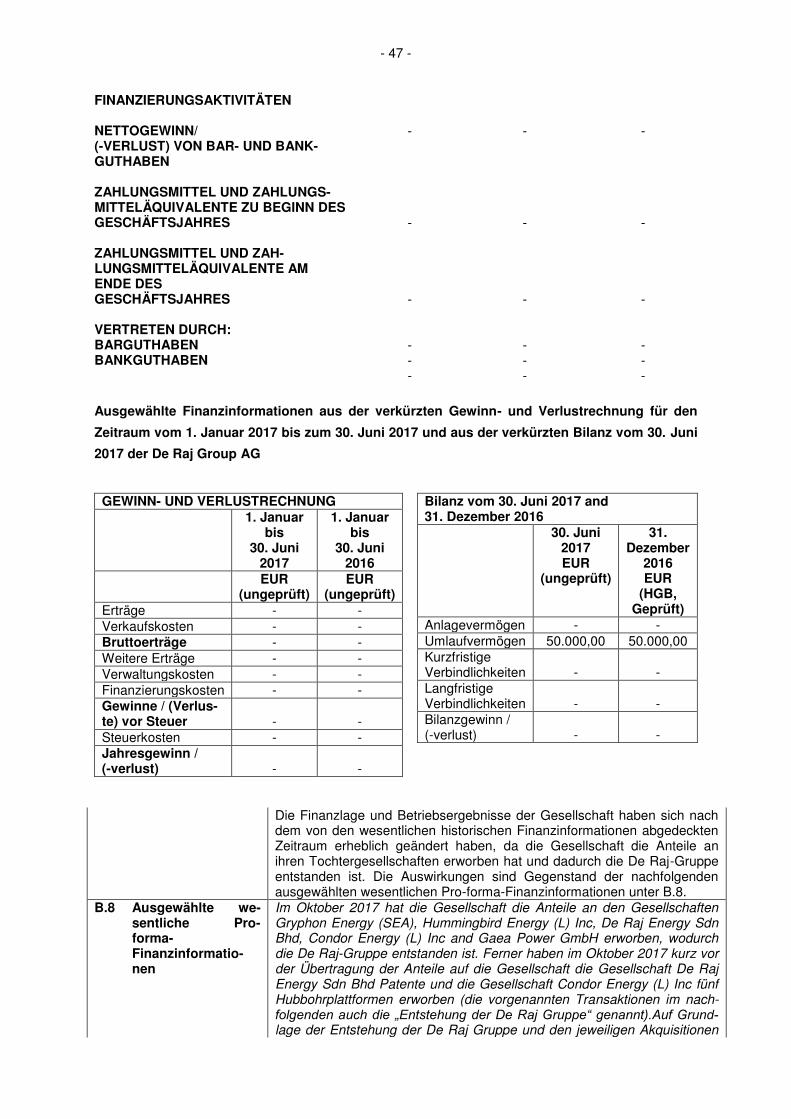

NET INCREASE/ - - -

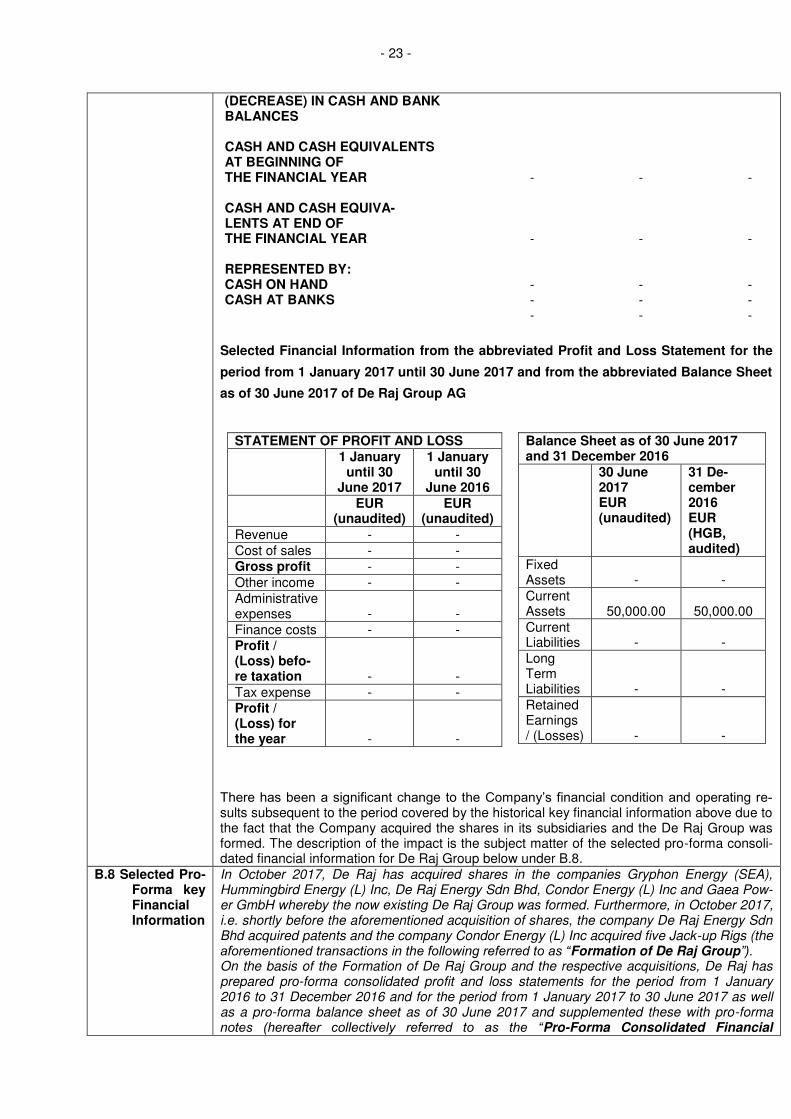

- 23 -

(DECREASE) IN CASH AND BANK BALANCES

CASH AND CASH EQUIVALENTS AT BEGINNING OF

THE FINANCIAL YEAR - - -

CASH AND CASH EQUIVA-LENTS AT END OF

THE FINANCIAL YEAR - - -

REPRESENTED BY: CASH ON HAND - - - CASH AT BANKS - - -

- - -

Selected Financial Information from the abbreviated Profit and Loss Statement for the

period from 1 January 2017 until 30 June 2017 and from the abbreviated Balance Sheet

as of 30 June 2017 of De Raj Group AG

STATEMENT OF PROFIT AND LOSS 1 January

until 30 June 2017

1 January until 30

June 2016 EUR

(unaudited) EUR

(unaudited) Revenue - - Cost of sales - - Gross profit - - Other income - - Administrative expenses - - Finance costs - - Profit / (Loss) befo-re taxation - - Tax expense - - Profit / (Loss) for the year - -

Balance Sheet as of 30 June 2017 and 31 December 2016 30 June

2017 EUR (unaudited)

31 De-cember 2016 EUR (HGB, audited)

Fixed Assets - - Current Assets 50,000.00 50,000.00 Current Liabilities - - Long Term Liabilities - - Retained Earnings / (Losses) - -

There has been a significant change to the Company’s financial condition and operating re-sults subsequent to the period covered by the historical key financial information above due to the fact that the Company acquired the shares in its subsidiaries and the De Raj Group was formed. The description of the impact is the subject matter of the selected pro-forma consoli-dated financial information for De Raj Group below under B.8.

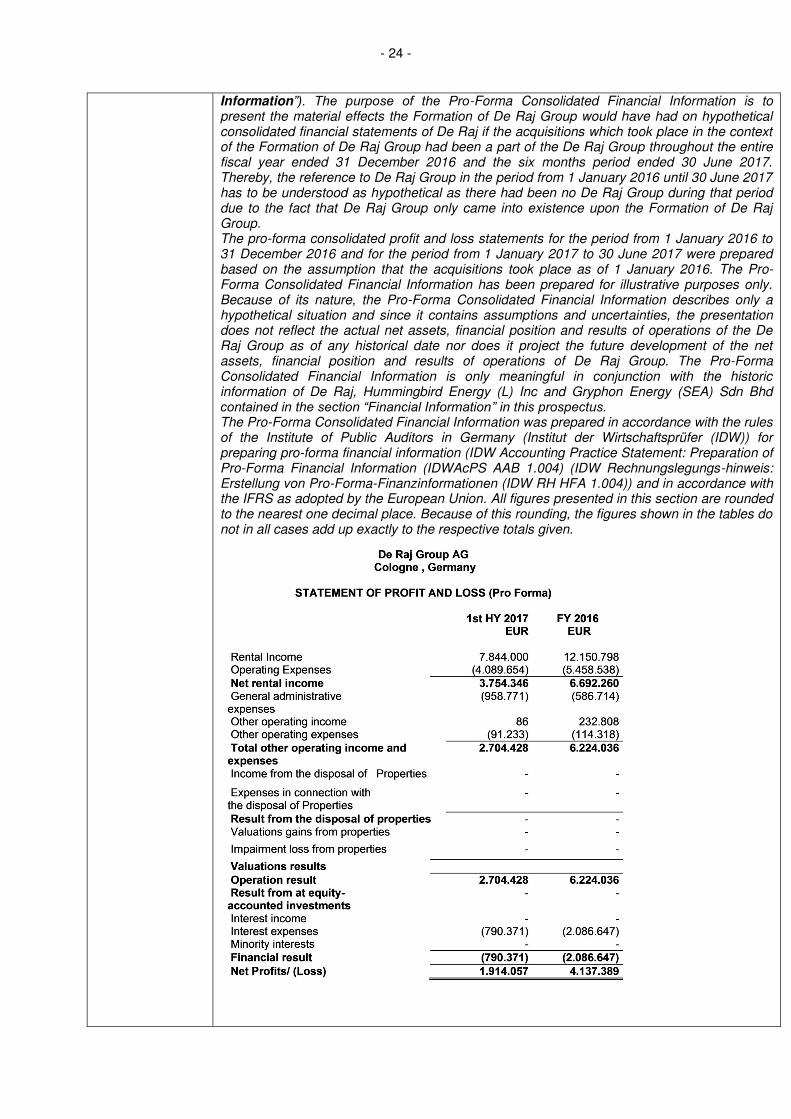

B.8 Selected Pro-Forma key Financial Information

In October 2017, De Raj has acquired shares in the companies Gryphon Energy (SEA), Hummingbird Energy (L) Inc, De Raj Energy Sdn Bhd, Condor Energy (L) Inc and Gaea Pow-er GmbH whereby the now existing De Raj Group was formed. Furthermore, in October 2017, i.e. shortly before the aforementioned acquisition of shares, the company De Raj Energy Sdn Bhd acquired patents and the company Condor Energy (L) Inc acquired five Jack-up Rigs (the aforementioned transactions in the following referred to as “Formation of De Raj Group”). On the basis of the Formation of De Raj Group and the respective acquisitions, De Raj has prepared pro-forma consolidated profit and loss statements for the period from 1 January 2016 to 31 December 2016 and for the period from 1 January 2017 to 30 June 2017 as well as a pro-forma balance sheet as of 30 June 2017 and supplemented these with pro-forma notes (hereafter collectively referred to as the “Pro-Forma Consolidated Financial

- 24 -

Information”). The purpose of the Pro-Forma Consolidated Financial Information is to present the material effects the Formation of De Raj Group would have had on hypothetical consolidated financial statements of De Raj if the acquisitions which took place in the context of the Formation of De Raj Group had been a part of the De Raj Group throughout the entire fiscal year ended 31 December 2016 and the six months period ended 30 June 2017. Thereby, the reference to De Raj Group in the period from 1 January 2016 until 30 June 2017 has to be understood as hypothetical as there had been no De Raj Group during that period due to the fact that De Raj Group only came into existence upon the Formation of De Raj Group. The pro-forma consolidated profit and loss statements for the period from 1 January 2016 to 31 December 2016 and for the period from 1 January 2017 to 30 June 2017 were prepared based on the assumption that the acquisitions took place as of 1 January 2016. The Pro-Forma Consolidated Financial Information has been prepared for illustrative purposes only. Because of its nature, the Pro-Forma Consolidated Financial Information describes only a hypothetical situation and since it contains assumptions and uncertainties, the presentation does not reflect the actual net assets, financial position and results of operations of the De Raj Group as of any historical date nor does it project the future development of the net assets, financial position and results of operations of De Raj Group. The Pro-Forma Consolidated Financial Information is only meaningful in conjunction with the historic information of De Raj, Hummingbird Energy (L) Inc and Gryphon Energy (SEA) Sdn Bhd contained in the section “Financial Information” in this prospectus. The Pro-Forma Consolidated Financial Information was prepared in accordance with the rules of the Institute of Public Auditors in Germany (Institut der Wirtschaftsprüfer (IDW)) for preparing pro-forma financial information (IDW Accounting Practice Statement: Preparation of Pro-Forma Financial Information (IDWAcPS AAB 1.004) (IDW Rechnungslegungs-hinweis: Erstellung von Pro-Forma-Finanzinformationen (IDW RH HFA 1.004)) and in accordance with the IFRS as adopted by the European Union. All figures presented in this section are rounded to the nearest one decimal place. Because of this rounding, the figures shown in the tables do not in all cases add up exactly to the respective totals given.

- 25 -

B.9 Profit fore-cast and estimate.

Not applicable. The Company has not issued a profit forecast or estimate.

B.10 Qualifica-tions in the audit re-port on the historical financial infor-mation.

Not applicable. The auditor’s reports on the historical financial information included in this prospectus have been issued without qualification.

B.11 Insuffi-ciency of the issu-er’s work-

Not applicable. The Company believes that the De Raj Group has sufficient working capital to be able to settle its liabilities as they fall due at least for the next twelve months.

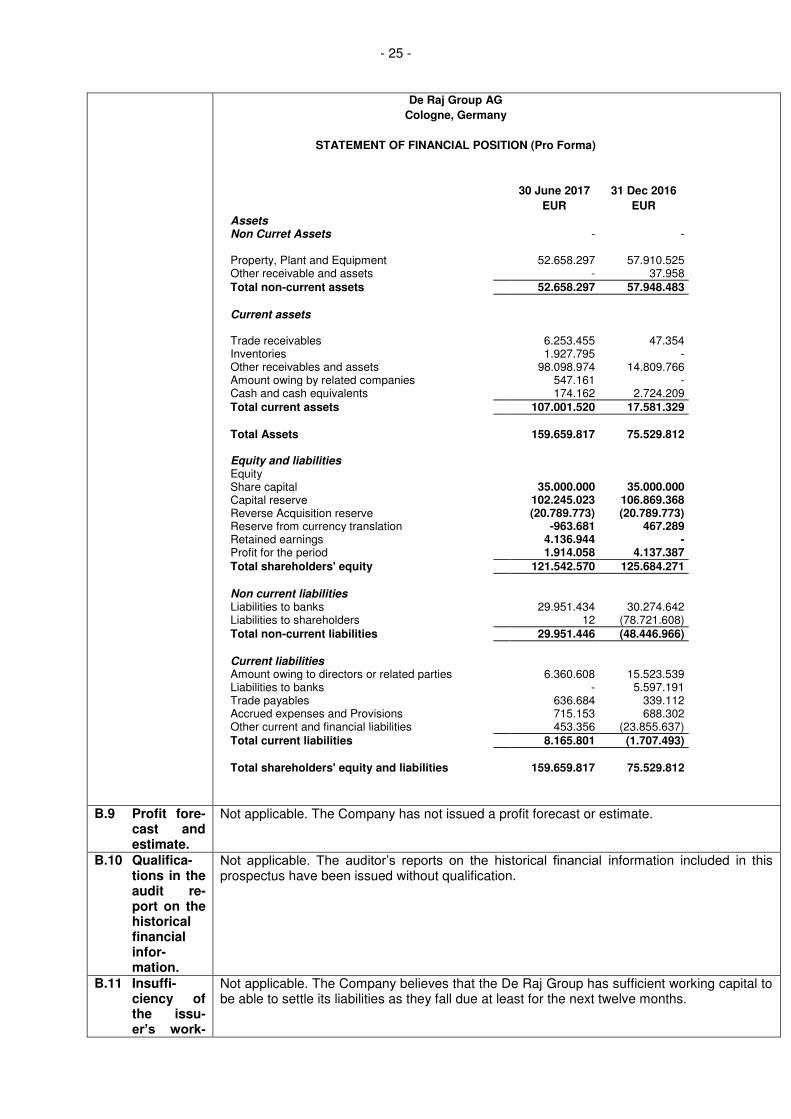

De Raj Group AG Cologne, Germany

STATEMENT OF FINANCIAL POSITION (Pro Forma)

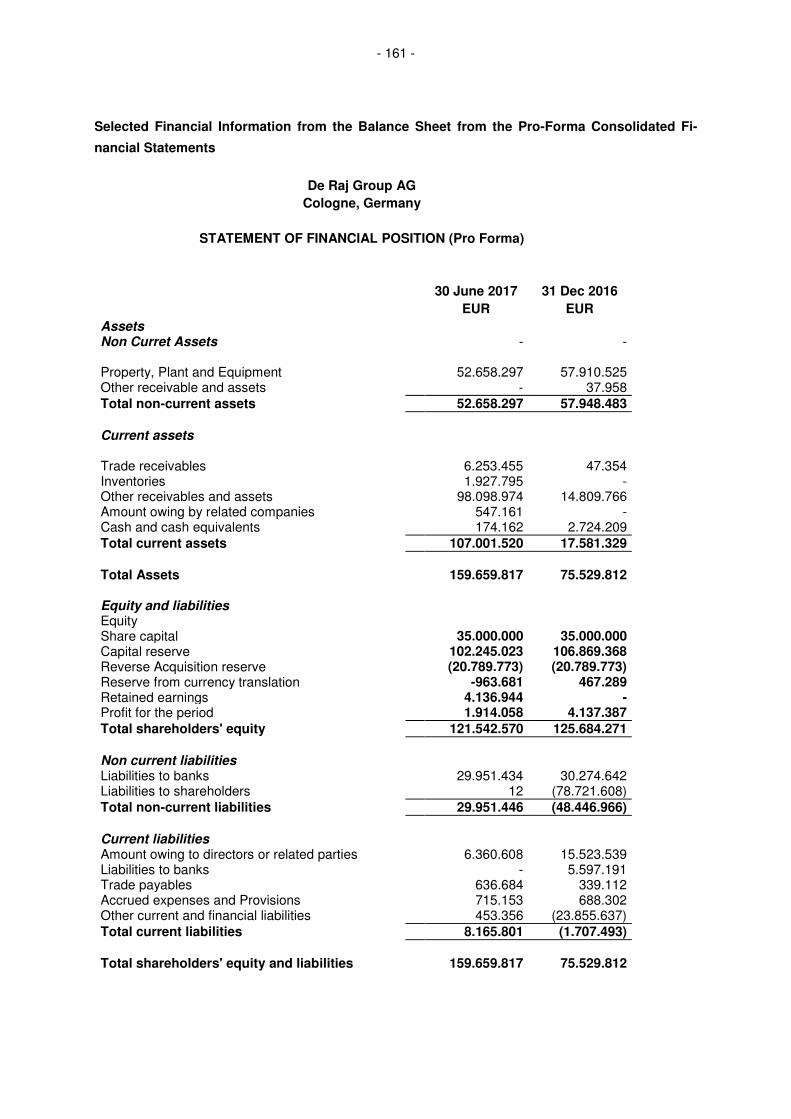

30 June 2017 31 Dec 2016 EUR EUR

Assets Non Curret Assets - -

Property, Plant and Equipment 52.658.297 57.910.525 Other receivable and assets - 37.958 Total non-current assets 52.658.297 57.948.483 Current assets Trade receivables 6.253.455 47.354 Inventories 1.927.795 - Other receivables and assets 98.098.974 14.809.766 Amount owing by related companies 547.161 - Cash and cash equivalents 174.162 2.724.209 Total current assets 107.001.520 17.581.329

Total Assets 159.659.817 75.529.812

Equity and liabilities Equity Share capital 35.000.000 35.000.000 Capital reserve 102.245.023 106.869.368 Reverse Acquisition reserve (20.789.773) (20.789.773) Reserve from currency translation -963.681 467.289 Retained earnings 4.136.944 - Profit for the period 1.914.058 4.137.387 Total shareholders' equity 121.542.570 125.684.271

Non current liabilities Liabilities to banks 29.951.434 30.274.642 Liabilities to shareholders 12 (78.721.608) Total non-current liabilities 29.951.446 (48.446.966) Current liabilities Amount owing to directors or related parties 6.360.608 15.523.539 Liabilities to banks - 5.597.191 Trade payables 636.684 339.112 Accrued expenses and Provisions 715.153 688.302 Other current and financial liabilities 453.356 (23.855.637) Total current liabilities 8.165.801 (1.707.493) Total shareholders' equity and liabilities 159.659.817 75.529.812

- 26 -

ing capital for its pre-sent re-quire-ments.

C - Securities C.1 Type and

class of the securities admitted to trading.

Ordinary bearer shares with no par value (Stückaktien), each representing a notional value of EUR 1.00 and full dividend entitlement from January 1, 2017.

Security identification number.

International Securities Identification Number (ISIN): DE000A2GSWR1 German Securities Code (Wertpapier-Kenn-Nummer): A2GSWR

Trading Symbol.

Trading Symbol: DRJ

C.2 Currency. Euro. C.3 The number

of shares is-sued and ful-ly paid.

35,000,000.00 bearer shares with no par value (Stückaktien) (“Shares”). The share capital has been fully paid up.

Notional value.

Each of the Shares of the Company represents a notional share of EUR 1.00 in the Compa-ny’s share capital.

C.4 A descrip-tion of the rights at-tached to the securities.

Each share in the Company carries one vote at the Company’s shareholders’ meeting. There are no restrictions on voting rights. The Shares carry full dividend entitlement from January 1, 2017.

C.5 A descrip-tion of any restrictions on the free transferabil-ity of the se-curities.

Not applicable. The Company’s Shares are freely transferable in accordance with the legal requirements for bearer shares. There are no prohibitions or restrictions on disposals with respect to the transferability of the Company’s shares.

C.6 Application for admis-sion to trad-ing on a regulated market and identity of regulated markets where the securities are to be traded.

The Company expects to apply for admission of the Shares to trading on the regulated mar-ket segment (regulierter Markt) of the Frankfurt Stock Exchange (Frankfurter Wertpa-pierbörse), sub-segment General Standard. The listing approval is expected to be an-nounced on 21 November 2017. Trading of the Shares on the Frankfurt Stock Exchange is expected to commence on 22 November 2017.

C.7 Dividend policy.

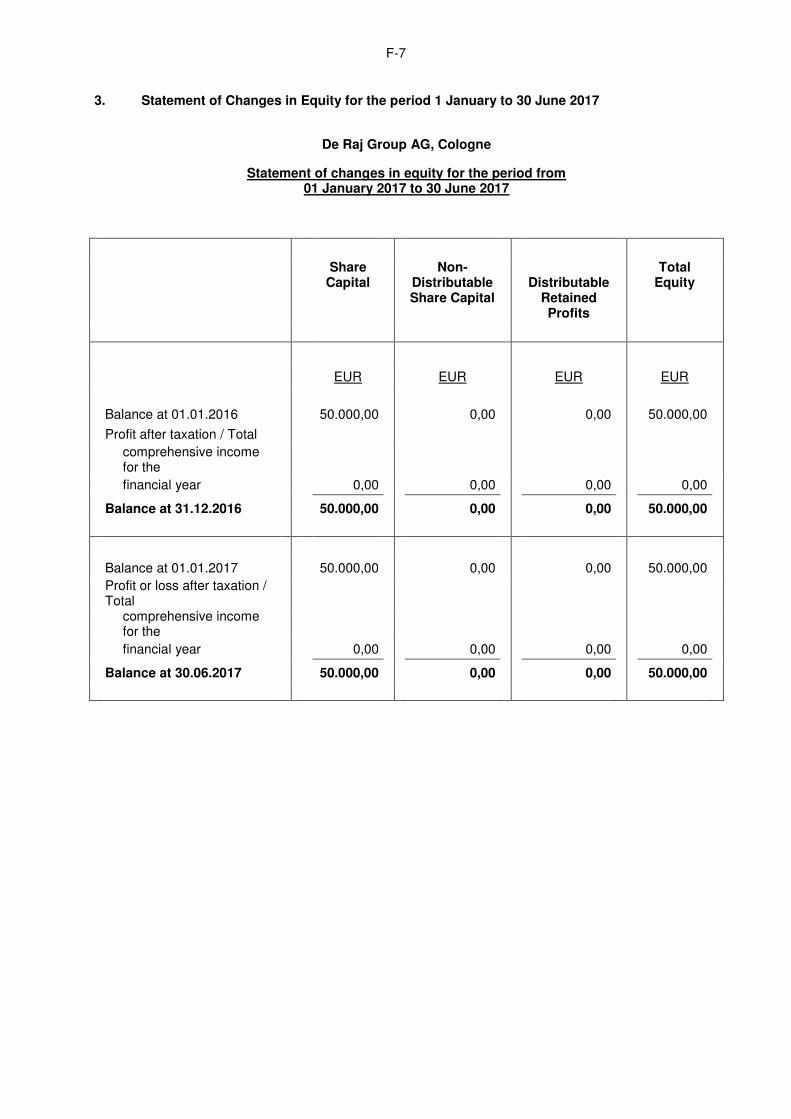

Due to the fact that the Company was a shelf company and its business purpose was re-stricted to the administration of its own assets until August 2017, there have been no net retained earnings available for distribution for the abbreviated financial year 2015 and the full financial year 2016. Correspondingly, there was no distribution of dividends for the ab-breviated financial year 2015 and the financial year 2016. The Company can make no pre-dictions as to the size of future profits available for distribution, or whether distributable prof-its will be achieved at all. Hence the Company cannot guarantee that dividends will be paid in the future. Moreover, the results of operations as set out in the financial statements may not be necessarily indicative of the results that should be expected in the future or amounts of future dividend payments

D - Risks D.1 Key risks

specific to When considering whether to purchase shares of De Raj investors should take into account, along with carefully considering the other information contained within this Prospectus, the

- 27 -

the issuer and its in-dustry

following risk factors. The occurrence of one or more of these risks may have material ad-verse effects on the business, assets and financial and earning positions of De Raj and its subsidiaries. The market price of the Company’s shares could drop significantly as a result of each of these risks and investors could lose all or part of their invested capital. Risks as-sociated with the Company and its industry are described below. The risks described below do not represent an exhaustive list of risks to which De Raj is exposed. Additional risks and uncertainties that are not currently known to the Com-pany could also adversely affect the business operations of De Raj and have a negative effect on the business, assets and fi-nancial and earning positions of the Company. The order in which the risks are listed does not correspond to or indicate the likelihood of their occurrence or the extent of their potential economic impact. Selection and content of the included risk factors were based on assump-tions that may subsequently prove incorrect. The risks described may occur individually or cumulatively.

Market and Business Risks • De Raj Group is dependent on a limited number of major customers. • Risks arise in view of contracts, which were entered into for the implementation of the

economically most important contract for De Raj Group regarding the deployment of an oil rig.

• De Raj Group may not be able to procure inputs, including equipment assembly parts and chemicals, from suppliers in a timely manner, on satisfactory terms or at all.

• Some of De Raj Group’s services contracts may be terminated prematurely under vari-ous circumstances.

• De Raj Group’s insurance coverage may not be adequate to cover all losses or liabili-ties that may arise in connection with the operations of De Raj Group.

• As De Raj Group continues to expand internationally, it is increasingly susceptible to legal, regulatory, political, economic and competitive conditions outside of Malaysia, as well as operational risks different from those that De Raj Group faces in Malaysia.

• De Raj Group may not be able to grow successfully through future acquisitions or to effectively integrate the acquired businesses.

• De Raj Group’s internal organizational structures, particularly its risk management, might prove insufficient and might fail to identify or avoid undesirable developments and risks and impending or already perpetrated violations of the law in a timely manner.

• Repair and maintenance of De Raj Group’s key assets, equipment and facilities may require substantial expenditure, and breakdown, non-performance or loss of the key assets, equipment and facilities on which De Raj Group is dependent may cause it to incur losses.

• De Raj Group may not be able to effectively manage its present or future assets and joint ventures.

• De Raj Group is exposed to the credit risk of its customers and counterparties with whom it does business.

• Global capital and credit market issues could negatively affect De Raj Group’s liquidity, increase its costs of borrowing and disrupt the operations of its suppliers and custom-ers.

• De Raj Group is exposed to foreign exchange risk arising from changes in the ex-change rates between the functional currencies of companies in its Group and other currencies.

• De Raj Group’s IT-systems could malfunction or become impaired. • The potential future use of derivative instruments, such as currency forward contracts,

may not fully hedge the risks of price fluctuations. • Forward-looking statements in this Prospectus may not be accurate. • Risks arise for the De Raj Group's business from the transformation of the energy mar-

ket, particularly in Europe. • Risks arise for the De Raj Group's business from an increase in renewable power gen-

eration and the resulting displacement of conventional power plants among the compe-tition.

• Risks arise for the De Raj Group's business from the availability of fossil fuels such as gas and oil as well as biomass.

• Risks arise for the De Raj Group's business from unusual seasonal fluctuations in de-mand for oil and gas as well as power generation.

• Risks arise for the De Raj Group's business from human errors, technical failures in operating procedures or interruptions of business operations.

- 28 -

• Risks arise for the De Raj Group's business from qualified personnel not being availa-ble and any inability to recruit qualified personnel or a high degree of staff fluctuation.

• Risks arise for the De Raj Group's business from increased competition. • There are reputational risks related to the De Raj Group's business. • De Raj is a holding company and, as a result, is dependent on dividends from its sub-

sidiaries. • Risks arise for the De Raj Group's business from the acquisition of patents • Risks arise for the De Raj Group's business from possible conflicts in view of intellectu-

al property rights • De Raj Group’s major shareholders may have interests that may not be aligned or may

conflict with those of its other shareholders. Legal and Regulatory Risks

• De Raj Group’s may be adversely affected by changes to the general legal, and regula-tory environment in the countries in which it operates.

• Risks arise for the De Raj Group's business from potential amendments of the German promotion scheme for renewables energies.

• Risks arise for the De Raj Group's business from possible political actions and/or legal measures with respect to the usage of palm oil as fuel for CHP plants.

• Risks arise for the De Raj Group's business from of legal uncertainties with regard to provisions on the determination of the promotion amount.

Tax Risks • De Raj Group may have to pay additional taxes following tax audits. • De Raj Group may subject to additional taxes in Germany. • De Raj Group’s business is subject to the general legal and tax environment in Germa-

ny and the other countries in which De Raj Group is active. D.3 Key risks

specific to the securi-ties

The key risks specific to the securities are summarized as follows: The trading volumes and market price for De Raj’s shares could fluctuate considerably,

and the market price could decline in the future Any future sales of a considerable number of De Raj’s shares by a major shareholder or

a number of shareholders could lead to a decrease in the market price of the shares Future capital measures could lead to a decrease in the market price for De Raj’s

shares and a substantial dilution of existing shareholders’ interests in De Raj A sale and/or transfer of shares of the Company may in the future be subject to financial

transaction tax. E - Offer E.1 The total net

proceeds and Estimate of the total expenses of the offering and listing, including es-timated ex-penses charged to the investor by the issu-er.

The subject matter of the prospectus is only a listing, there is no offer of shares. The Com-pany estimates that the total costs of the listing will amount to approximately EUR 515,000.00. The costs of the listing include, inter alia, costs for external advice (in particular by banks (including the listing agreement with ACON), legal and tax advisors), audit fees (auditors), transaction costs, costs for notarial recordings, costs for filings with the commercial register and costs of the planned stock exchange admissions, including their preparation. Neither the Company nor ACON will charge expenses to investors.

E.2a Reasons for the offering.

Not applicable. An offer of securities is not subject of the prospectus.

Use of Pro-ceeds, esti-mated net amount of the pro-ceeds.

E.3 Offer condi-tions.

Not applicable. An offer of securities is not subject of the prospectus.

E.4 Description of all inter-

Not applicable. There are no third parties who have an interest in the admission to trading of the Shares.

- 29 -

ests material to the offer.

E.5 Name of the person or entity offer-ing to sell the security.

Not applicable. An offer of securities is not subject of the prospectus.

Lock-up agreement: the parties involved; and indica-tion of the period of the lock up.

The shareholders of the Company Mr Nagendran C Nadarajah, Ms Renata Anita de Raj, Mr Nicholas Arnand de Raj, Mr Alexander Arjun de Raj, Maya Terang Sdn. Bhd. and Lexanda International Limited have agreed with ACON that, to the extent permitted by law, for a peri-od of six months after the listing of the shares to the Regulated Market of the Frankfurt Stock Exchnage not to directly or indirectly sell, offer, commit to sell or offer, or announce a sale or an offer to dispose of, any of their shares in the Company or rights that can be con-verted into, or exchanged for, such shares or that carry rights to acquire such shares and not to enter into other transactions (including transactions concerning derivative instru-ments) the economic effect of which would be similar to that of the measures described above, without the prior written consent of ACON.

E.6 Amount and percentage of immediate dilution re-sulting from the offer.

Not applicable. An offer of securities is not subject of the prospectus.

E.7 Estimated expenses charged to the investor by the issu-er.

Not applicable. Neither the Company nor ACON will charge expenses to investors.

- 30 -

2. GERMAN TRANSLATION OF THE SUMMARY OF THE PROSPECTUS -

ZUSAMMENFASSUNG DES PROSPEKTES Zusammenfassungen zu Wertpapierprospekten bestehen aus offenzulegenden Angaben, die als „Ele-mente“ bezeichnet werden. Diese Elemente sind in den Abschnitten A bis E (A.1 bis E.7) aufgeführt. Die-se Zusammenfassung enthält alle Elemente, die für diese Art von Wertpapieren und den Emittenten in die Zusammenfassung aufzunehmen sind. Weil einige Elemente nicht aufgeführt werden müssen, können sich Lücken in der fortlaufenden Nummerierung der Elemente ergeben. Selbst wenn ein Element auf-grund der Art des Wertpapiers und aufgrund des Emittenten in die Zusammenfassung mit aufgenommen werden muss, ist es möglich, dass hinsichtlich dieses Elements keine betreffende Information angegeben werden kann. In diesem Fall ist eine kurze Beschreibung des Elements in die Zusammenfassung aufge-nommen worden zusammen mit dem Hinweis „entfällt“. A - Einleitung und Warnhinweise A.1 Warnhinweise Diese Zusammenfassung sollte als Einleitung zu diesem Prospekt (der „Pros-

pekt“) verstanden werden. Bei jeder Anlage in die betreffenden Wertpapiere sollte sich der Anleger auf die Prüfung des gesamten Prospekts stützen.

Für den Fall, dass vor einem Gericht Ansprüche aufgrund der in diesem Pros-pekt enthaltenen Informationen geltend gemacht werden, könnte der als Klä-ger auftretende Anleger in Anwendung der einzelstaatlichen Rechtsvorschrif-ten der Staaten des Europäischen Wirtschaftsraums die Kosten für eine Über-setzung dieses Prospekts vor Prozessbeginn zu tragen haben, bevor das Ver-fahren eingeleitet werden kann.

Die De Raj Group AG (die „Gesellschaft“, „De Raj“ oder der „Emittent“) und die ACON Actienbank, München („ACON“ oder „Listing Agent“) haben nach § 5 Abs. 2b Nr. 4 Wertpapierprospektgesetz („WpPG“) die Verantwortung für den Inhalt dieser Zusammenfassung einschließlich etwaiger Übersetzungen übernommen. Diejenigen Personen, welche die Verantwortung für die Zu-sammenfassung einschließlich ihrer Übersetzung übernommen haben oder von denen der Erlass ausgeht (Veranlassung), können haftbar gemacht wer-den, jedoch nur für den Fall, dass die Zusammenfassung irreführend, unrichtig oder widersprüchlich ist, wenn sie zusammen mit den anderen Teilen des Prospekts gelesen wird, oder sie, wenn sie zusammen mit den anderen Teilen des Prospekts gelesen wird, nicht alle erforderlichen Schlüsselinformationen vermittelt.

A.2 Angabe über spätere Verwen-dung des Pros-pekts.

Entfällt. Eine Zustimmung zur Verwendung des Prospekts für eine spätere Weiterveräußerung oder Platzierung der Aktien wurde nicht erteilt.

B - Emittent B.1 Juristische und

kommerzielle Bezeichnung.

Die Firma und der Handelsname des Emittenten lauten De Raj Group AG.

B.2 Sitz und Rechts-form des Emit-tenten, gelten-des Recht, Land der Gründung.

Der Emittent hat seinen Sitz in Köln, Deutschland, (Geschäftsanschrift: c/o Heuking Kühn Lüer Wojtek, Magnusstr. 13, 50672 Köln), und ist im Handelsre-gister des Amtsgerichts Köln, Deutschland, unter HRB 92007 eingetragen. Der Emittent ist eine in Deutschland gegründete und bestehende Aktiengesell-schaft, für die das Recht der Bundesrepublik Deutschland anwendbar ist.

B.3 Art der derzeiti-gen Geschäfts-tätigkeit und Haupttätigkeiten des Emittenten sowie Haupt-märkte, auf de-nen der Emittent vertreten ist.

Die De Raj ist die Muttergesellschaft der Gesellschaften Gryphon Energy (SE-A) Sdn Bhd, Hummingbird Energy (L) Inc, Condor Energy (L) Inc, De Raj Energy Sdn Bhd und Gaea Power GmbH (“De Raj Gruppe”). Das Geschäft der De Raj Gruppe konzentriert sich auf die Sparte Öl und Gas in der Region Südostasien sowie die Sparte deutsche Energieerzeugung. Sparte Öl und Gas Die Sparte Öl und Gas der De Raj-Gruppe ist ein Dienstleistungsbereich, der das volle Spektrum der Erkundung und Förderung (Upstream) Öl-und-Gas-Lieferkette auf offenem Meer umfasst. Dieser Bereich kann in folgende Tätig-keiten involviert sein: 1. Erkundung (Exploration) auf offenem Meer; dies umfasst die Suche nach

Felsformationen mit Öl- und natürlichen Gasvorkommen sowie die geo-physikalische Suche nach Bodenschätzen bzw. Explorationsbohrungen,

2. Entwicklung von Bohrlöchern, die stattfindet, wenn ein ökonomisch för-

- 31 -

derbares Gebiet gefunden wurde; dies umfasst die Konstruktion von ei-nem oder mehreren Bohrlöchern vom Beginn an (das sog. „spudding“) oder auch die Stilllegung, wenn keine Kohlenwasserstoffe gefunden werden konnten, oder die Fertigstellung von Bohrlöchern, wenn Kohlen-wasserstoffe in ausreichender Menge gefunden werden konnten.

3. Produktion; dies umfasst den Prozess des Herauslösens der Kohlen-wasserstoffe und der Trennung des Gemischs von flüssigen Kohlenwas-serstoffen, Gas, Wasser und Feststoffen durch Herauslösen der Be-standteile, die nicht verkäuflich sind, und Verkauf des flüssigen Kohlen-wasserstoffes und Gases, und schließlich

4. Stilllegung des Gebiets; dies umfasst das Verschließen der Bohrlöcher und die Wiederherstellung des Gebiets, wenn ein vor kurzem gebohrtes Bohrloch nicht genügend Potential aufweist, um ökonomisch sinnvolle Mengen an Öl und Gas vorzubringen, oder wenn die Produktion nicht länger ökonomisch sinnvoll ist.