Embed Size (px)

Citation preview

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 1/18

Confidential - Private Circulation Only

Real Estate Review – Half Yearly ReportJuly 2014

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 2/18

1Source: PropTiger DataLabs July 2014

Executive Summary

• First half of 2014 has been a disappointment for real estate. Taking cues from slowingsales, developers have put a strong break on new launches resulting in 73% drop in new

launches in Q2’CY14 over Q2’CY13

• Significant (~83%) drop seen in new unit launches in Noida in Q2’CY14 over Q1’CY14

• Despite high demand of affordable housing, ~47% of the new units launched in first half

of the year are in >50 Lakh budget range

• Sales continue to slow down and have dropped ~50% since Q2’CY13

• Mumbai and Noida have most unsold inventory amongst all key metros whereas Mumbai

and Gurgaon leads in most expensive (>1 crore) unsold inventory

• Price charts across cities are flat reflecting sluggish sales in markets; Discounts of 5 –

10% are common across markets over the published prices

• Positive budget for real estate is a good news for the industry. We expect market torevive in second half of the year

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 3/18

2Source: PropTiger DataLabs July 2014

India – Market analysis and quarterly review

Outlook for H2 -CY’2014

Detailed market analysis

Agenda

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 4/18

3Source: PropTiger DataLabs July 2014

160,625

130,562

102,64299,546

81,360

35,867

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

Q1-CY'13 Q2-CY'13 Q3-CY'13 Q4-CY'13 Q1-CY'14 Q2-CY'14

New launches in top 9 cities*

130,562

35,867

- 73 %

# of units

Notes: * Top 9 Cities are Mumbai (includes Navi Mumbai and Thane), Pune, Noida (includes Greater Noida and Yamuna Expressway), Gurgaon(includes Bhiwadi, Dharuhera and Sohna), Bangalore, Chennai, Hyderabad, Kolkata, Ahmedabad

Quarterly new unit launches dropped ~73% since Q2-CY’13

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 5/184Source: PropTiger DataLabs July 2014

# of units

Notes: 1. Noida includes: Greater Noida and Yamuna Expressway2. Bhiwadi includes: Bhiwadi, Rewari, Dharuhera, Behror, Manesar and Neemrana

1

6 ,

9 0 0

7 ,

7 2 5

2 0 ,

9 4 4

8 ,

6 0 1

8 ,

1 7 7

4 ,

0 5 0

1 , 0

8 7

1

, 8 4 3

2 ,

4 7 8

6 5 0

3 ,

5 4 5

2

, 2 0 8

3 ,

1 5 2

9 ,

7 4 6

6 ,

0 6 8

3 ,

6 2 6

3 ,

5 6 5

3 ,

1 8 0

3 ,

0 8 3

8 2 4

2 ,

5 2 0

0

0

1 ,

6 4 6

1 , 2

4 4

3 6 5

0

5,000

10,000

15,000

20,000

25,000

Bangalore Pune Noida Chennai Mumbai Thane NaviMumbai

Gurgaon Bhiwadi Sohna Kolkata Ahmedabad Hyderabad

Total new unit launches –Q1-CY’14 & Q2-CY’14 Q1-CY'14

Q2-CY'14

1 2

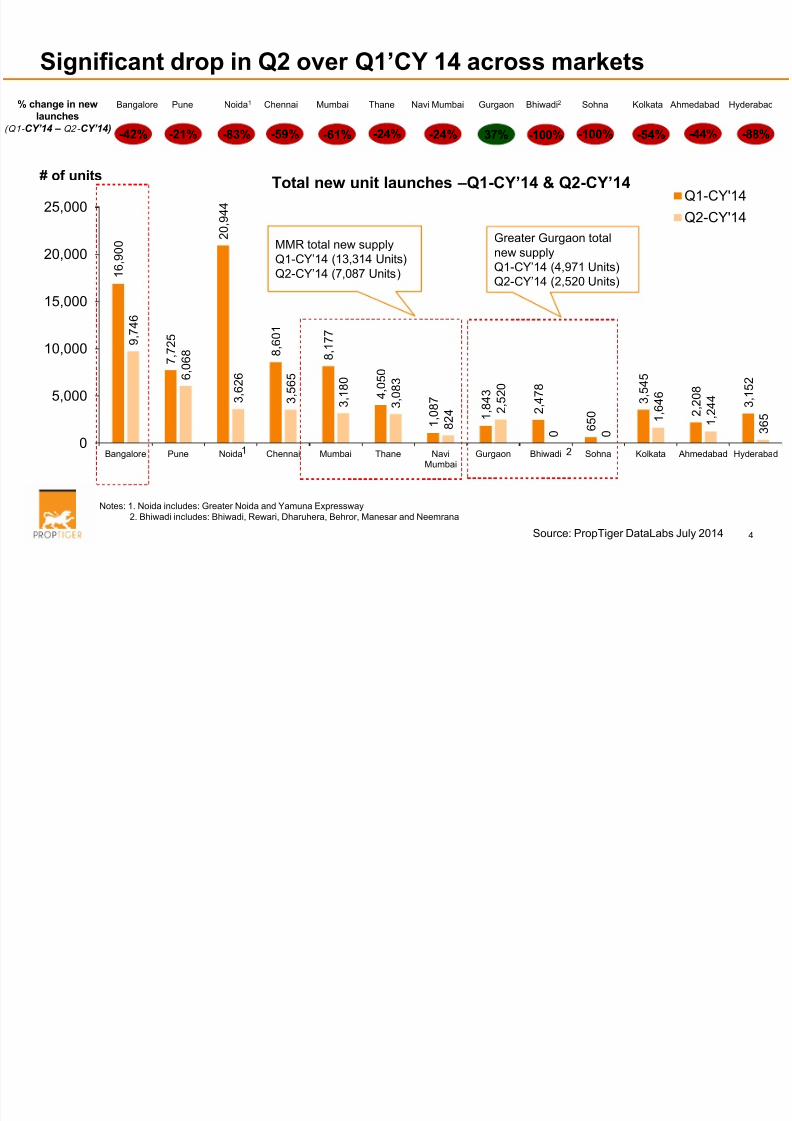

MMR total new supplyQ1-CY’14 (13,314 Units)

Q2-CY’14 (7,087 Units)

Greater Gurgaon totalnew supplyQ1-CY’14 (4,971 Units)

Q2-CY’14 (2,520 Units)

-83% -59% -61% -24% -24% 37% -100% -100% -54% -44% -88%-42% -21%

% change in new

launches

(Q1- CY’14 – Q2- CY’14)

Bangalore Pune Noida1 Chennai Mumbai Thane Navi Mumbai Gurgaon Bhiwadi2 Sohna Kolkata Ahmedabad Hyderabad

Significant drop in Q2 over Q1’CY 14 across markets

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 6/185Source: PropTiger DataLabs July 2014

28%

25%18%

7%

22%

<35 Lakhs

35-50 Lakhs

50-75 Lakhs

75-100 Lakhs

+1 crore

Budget wise breakup of new

launch units in H2-CY’13

Budget wise breakup of new

launch units in H1-CY’14

36%

24%

17%

7%

16%

~47% of new units launched in H1’CY14 costs >50 Lakh

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 7/186Source: PropTiger DataLabs July 2014

Notes: ** Top 9 Cities are Mumbai (includes Navi Mumbai and Thane), Pune, Noida (includes Greater Noida and Yamuna Expressway), Gurgaon(includes Bhiwadi, Dharuhera and Sohna), Bangalore, Chennai, Hyderabad, Kolkata, Ahmedabad

113,213

106,306

99,18093,761

77,856

56,699

0

20,000

40,000

60,000

80,000

100,000

120,000

Q1-CY'13 Q2-CY'13 Q3-CY'13 Q4-CY'13 Q1-CY'14 Q2-CY'14

Absorption trend in top 9 cities**

- 27 %

77,856

56,699

106,306

- 47%

Quarterly new units sales dropped ~50% since Q2’CY14

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 8/187Source: PropTiger DataLabs July 2014

Sales drop seen across cities; Thane seen the least drop

across cities

Notes: 1. Noida includes: Greater Noida and Yamuna Expressway2. Bhiwadi includes: Bhiwadi, Rewari, Dharuhera, Behror, Manesar and Neemrana

Quarterly new home sales (# of units)

City Q2-CY'13 Q2-CY'14

Absorption Change

(Q2-CY'13 – Q2-CY'14)

Mumbai 11,512 5,401 -53%

Navi Mumbai 4,379 2,362 -46%

Thane 5,447 4,465 -18%

Noida 17,834 7,758 -56%

Gurgaon 5,772 2,715 -53%

Bhiwadi 3,358 1,682 -50%

Bangalore 19,256 10,049 -48%

Chennai 9,567 5,257 -45%

Pune 12,111 7,563 -38%

Hyderabad 6,317 2,823 -55%

Kolkata 5,348 3,141 -41%

Ahmedabad 5,358 3,290 -39%

1

2

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 9/188Source: PropTiger DataLabs July 2014

Mumbai and Noida have the most unsold inventory

0

20,000

40,000

60,000

80,000

100,000

120,000

Noida Bangalore Pune Mumbai Thane NaviMumbai

Chennai Hyderabad Ahmedabad Kolkata Gurgaon Bhiwadi Sohna

Unsold Inventory levels at the end of H1-CY’14 +4BHK

3BHK

2BHK

1BHK

# of units

1 2

101,635

Notes: 1. Noida includes: Greater Noida and Yamuna Expressway2. Bhiwadi includes: Bhiwadi, Rewari, Dharuhera, Behror, Manesar and Neemrana

92,862

54,608 51,081

34,588

17,757

46,442

25,892 24,624 19,583 19,724

2,026

16,525

Unsold Inventory = 103,426

Unsold Inventory = 38,134

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 10/189Source: PropTiger DataLabs July 2014

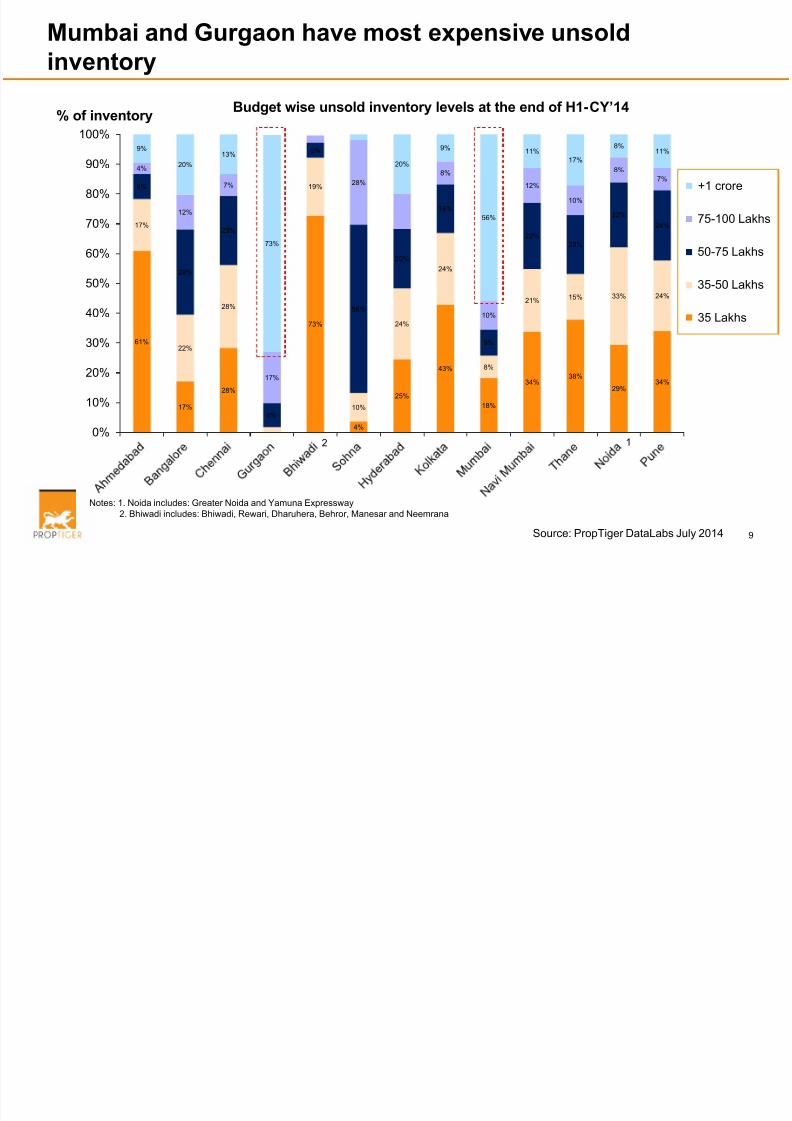

Mumbai and Gurgaon have most expensive unsold

inventory

61%

17%

28%

73%

4%

25%

43%

18%

34%38%

29%34%

17%

22%

28%

19%

10%

24%

24%

8%

21% 15% 33% 24%

8%

29%

23%

8%

5%

56%

20%

16%

9%

22%

20%

22%

24%

4%

12%

7%

17%

28%

8%

10%

12%

10%

8%

7%

9%

20%

13%

73%

20%

9%

56%

11%

17%

8%11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

+1 crore

75-100 Lakhs

50-75 Lakhs

35-50 Lakhs

35 Lakhs

% of inventory

Notes: 1. Noida includes: Greater Noida and Yamuna Expressway2. Bhiwadi includes: Bhiwadi, Rewari, Dharuhera, Behror, Manesar and Neemrana

12

Budget wise unsold inventory levels at the end of H1-CY’14

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 11/1810Source: PropTiger DataLabs July 2014

Lack of genuine demand continues in northern market as

large share of buyers are investors

51%60%

67% 70% 72%81%

86%91%

49%40%

33% 30% 28%19%

14%9%

Noida Gurgaon Pune Chennai Mumbai Ahmedabad Bangalore Kolkata

Investors End User

3500 35881800 3400 3800 6001400900

XXXX# of respondents in Survey

conducted in Q2’CY14

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 12/1811Source: PropTiger DataLabs July 2014

Price continued to be flat, if not fallen across marketsWeighted average1 BSP (Rs /sq. ft.) of Apartment units as on quarter end

Notes: 1. Price weighed on number of units in respective projects in a city

City Q2-CY'13 Q3-CY'13 Q4-CY'13 Q1-CY'14 Q2-CY'14Price Change

(Q2-CY'13- Q2-CY'14)

Ahmedabad 2,692 2,718 2,742 2,782 2,790 4%

Bangalore 4,078 4,173 4,239 4,314 4,368 7%

Chennai 4,531 4,599 4,616 4,652 4,684 3%

Hyderabad 3,326 3,366 3,402 3,457 3,508 5%

Kolkata 3,973 3,956 3,967 3,866 3,913 -2%

Pune 4,615 4,678 4,739 4,763 4,816 4%

Noida 4,476 4,524 4,513 4,506 4,538 1%

Greater Noida 3,537 3,547 3,626 3,580 3,593 2%

Yamuna Expressway 3,009 2,962 2,944 2,893 2,824 -6%

Gurgaon 7,563 7,699 7,723 7,828 7,844 4%

Bhiwadi 2,766 2,730 2,814 2,795 2,801 1%

Mumbai 11,298 11,520 11,648 11,701 12,132 7%

Navi Mumbai 5,506 5,530 5,592 5,678 5,744 4%

Thane 5,861 5,992 5,977 6,095 5,961 2%

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 13/18

12Source: PropTiger DataLabs July 2014

India – Market analysis and quarterly review

Outlook for H2 -CY’2014

Detailed market analysis

Agenda

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 14/18

13Source: PropTiger DataLabs July 2014

Budget 204-15 have fulfilled 5 major demands of Industry

1. Relaxation of FDI Norms

• Minimum built up area reduced from 50,000 sq mts to 20,000 sq mts

• Minimum capital reduced from $10mn to $5mn

• No capital and area limitation if 30% of total project is affordable housing

2. Pass through tax status to REIT

• No double taxation of interest income received by REIT

3. Increased tax incentives to buyers

• Tax exemptions on interest paid on self occupied home loans increased to 2 Lakh from 1.5 Lakh

4. Budgetary allocation to affordable housing

• 4,000 crores have been allocated to NHB for provision of cheaper loans to affordable housing buyers

• 8,000 crores have been additionally allocated for Rural Housing

• Recently RBI also removed SLR and CRR requirements for loans upto 50 Lakh in metros and 40 Lakh inother cities

5. Focus on infrastructure development

• 7,060 crores have been allocated for building 100 smart cities across India

• ~50,000 crores have been allocated for highways and road development

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 15/18

14Source: PropTiger DataLabs July 2014

Markets will see turnaround in second half of the year

FDI will improve liquidity of builders helping new launches in the market

• Many fund houses are raising money to invest in real estate projects• HDFC $250 mn, Amplus Capital $50 – 100 mn, Capri Global $400 mn

• Piramal Fund ~58 mn, IIFL~125 mn, IDFC ~125 mn

• Few builders have already raised FDI and many others will follow

• Shriram raised $80mn from Tata Opportunities Fund, $10 mn from Arvind Mills Realty PE

• Nirmal Group raised $50 mn from Kotak Realty fund and Omkar $25 mn from Piramal Fund

• Parsvanath, Omaxe etc. are looking to raise fund shortly

Buyer Sentiment

• Will improve with improvement in economy, arrival of festive season, improved taxincentives and ease of home loan availability

Political Situation

• Will stabilize post election in key states of Maharashtra, Haryana and Delhi

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 16/18

15Source: PropTiger DataLabs July 2014

India – Market analysis and quarterly review

Outlook for H2 -CY’2014

Detailed market analysis

Agenda

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 17/18

16Source: PropTiger DataLabs July 2014

Detailed market analysis for 9 cities available on request

1. Bangalore

2. Mumbai

3. Noida

4. Gurgaon

5. Pune

6. Chennai

7. Hyderabad

8. Ahmedabad

9. Kolkatta

On request

8/11/2019 Proptiger - Half Year (2014) Market Assessment

http://slidepdf.com/reader/full/proptiger-half-year-2014-market-assessment 18/18

17Source: PropTiger DataLabs July 2014

Contact PropTiger for:• Detailed analysis of Individual markets

• Micro market surveys

• Real estate data

Ankur Dhawan

+91-9873 9076 67