Embed Size (px)

Citation preview

JAKARTA OFFICE MARKET research & forecast report

www.colliers.co.id

2Q 2012 i the knowledge

Property Sector Overviewoffice sectorIn the last six months, average asking base rental rates of CBD office buildings with US Dollar tariffs rose substantially by 25% to US$26.60 / sq m / month. In contrast the average asking rental rates for buildings quoted in Rupiah rose by only 13% to IDR143,807 / sq m / month during the same period. This continued upward trend occurred because the amount of available good-quality office space in the CBD is becoming scarce, leaving around 4.1% of office space vacant at the end of the quarter.

Supply

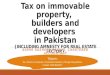

jakarta office cUMULatiVe sUppLY

Colliers International Indonesia - Research

JAKARTA SUPPLY: 1.7 million sq m of office space to enter Jakarta market

01,000,0002,000,0003,000,0004,000,0005,000,0006,000,0007,000,0008,000,0009,000,000

10,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2Q 2

012

2012

F

2013

F

2014

F

2015

F

sq m

Existing Supply Annual Supply

cbd After securing AXA insurance as the anchor tenant. AXA Tower was officially launched. This office tower is part of an integrated development called Kuningan City located in Jalan Satrio and is offered both as strata-title office space and office space for lease. Another office tower officially going into operation during the second quarter is a strata-title office building called Office 8, located in the Senopati area. Thus, the operation of these two buildings contributed another 122,073 sq m of office space during the quarter. Apart from those buildings, two smaller office buildings were also officially launched during the quarter. 18 Office Park located in the Sudirman CBD (SCBD) consisting of five small-scale towers has recently begun leasing space in one of the

The total office space in Jakarta area in 2Q 2012 was 6.48 million sq m of which around 70% is located in the CBD. In this quarter alone, 210,179 sq m of new office space flowed into Jakarta. This figure is the highest over the last two years, much higher than in the previous year. With the first half of 2012 gone, the amount of new office space projected to enter the market in the remainder of the year will be around 350,000 sq m, both in the CBD and outside the CBD. In the next two years, we expect to witness a significant amount of new office space, particularly during 2014. During 2013 - 2014 it is projected that not less than 1.4 million sq m of new office space will be supplied to the market. The annual supply in 2014 is expected to be the largest in history, despite construction being started on only a few of the projected buildings.

With four additional buildings in the CBD, the cumulative supply of office space is registered at 4.50 million sq m. This number will increase to 4.74 million sq m by the end of 2012. It is anticipated that in the three years ahead (2013 - 2015) there will be around 1.23 million sq m of office space of which 60% will be available in 2014.

Our supply projections are supported by the construction activities in the field. Office projects scheduled for the remainder of 2012 are expected to be completed as scheduled. This is also the case with office projects scheduled to begin operations in 2013 - 2015 of which some have shown commitment to deliver projects as planned. Menara Prima 2, located in the Mega Kuningan area, is an office tower scheduled to open in 2013 and is 50% complete. A high commitment to deliver projects on time was also shown by three projects scheduled for 2014 at which initial works such as land preparation up to the ground-breaking stage have been started. For example, The Noble House Office Tower project in Mega Kuningan and Wisma Mulia 2 in Gatot Subroto have entered the land preparation stage. The other project is Sahid Sudirman Center which will be one of the biggest office towers along Sudirman providing more than 100,000 sq m of office space. Another project is Life Tower in Jalan HR Rasuna Said. This building is in the process of completing the basement works. Meanwhile, Rasuna Tower which also located in Jalan HR Rasuna Said, due to have redesign, it seems that building will reschedule its completion.

Apart from the projects under construction, several projects have been officially announced,

including District 8 and the development of more office towers in the Sampoerna Strategic Square complex in Jalan Sudirman. Meanwhile, the future St. Regis Hotel planned to be built in Jalan Jenderal Jenderal Sudirman was cancelled but the plan for the St. Regis Hotel continues with a new landlord. Together with this hotel development is an office tower next to the future hotel and located in Jalan Jenderal Gatot Subroto.

The Mega Kuningan area is a business district with quite a few vacant plots of land compared to other business districts. Besides the plan for The Noble House Office Tower project, one future office project will be developed by Farpoint in Mega Kuningan. There will be more commercial development built in this area given the availability of vacant land.

Another potential area where office development could be built is the Rasuna Epicentrum area. Two office towers called Gran Rubina are planned to be built.

With all of the under-construction office projects and the planned office towers in the pipeline, the CBD area is anticipating a huge office space supply particularly in 2014. It is very challenging to search for plots of land along Jalan Jenderal Sudirman or Jalan Thamrin, however the potential for new development in the CBD would appear along Jalan Jenderal Gatot Subroto and in the superblock locations like the SCBD, Rasuna Epicentrum and Mega Kuningan. Likewise, secondary roads with quick access to the main thoroughfare in the CBD would potentially become a location for commercial development.

cbd annUaL office sUppLY based on MarketinG scheMe

Colliers International Indonesia - Research

0

100,000

200,000

300,000

400,000

500,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2Q 2

012

2012

F

2013

F

2014

F

2015

F

sq m

For Lease For Strata-title

buildings (Tower D). Another building operating in 2Q 2012 is Indosurya Plaza (previously known as Exim Melati) in the Thamrin Nine complex. This is an old building being rejuvenated where operations were halted for

almost two years. With a new façade and modern look and given its strategic location, this building is trying to compete with other buildings.

coLLiers internationaL | p. 2

JAKARTA | 2q 2012 | oFFiCe

oUtside cbd annUaL office sUppLY based on MarketinG scheMe

Colliers International Indonesia - Research

The office market in the outside the CBD area is also anticipating more development in the years to come. During 2Q 2012, two new office towers, i.e. Grand Slipi Tower, known previously as Grand Soho in West Jakarta and Wisma Pondok Indah 3 in South Jakarta, were the newest to contribute a total of 88,106 sq m. The addition of these two office towers brought the cumulative supply in the outside the CBD area to 1.97 million sq m as of 2Q 2012.

By the end of 2012, the office market in this area will see further supply of another 120,520 sq m and should this officially open on time, the cumulative supply will reach two million square metres. The remaining office towers projected to be finished this year are all in the final construction stages.

In response to growing inquiries for office space in the outside the CBD area, supply is anticipated to significantly grow to almost 700,000 sq m in 2013 - 2015. Of these, around 45% will be offered as office space for strata-title sale. It is interesting to note that Jalan TB Simatupang will provide the most office development of 444,830 sq m while the remaining supply will be spread out in West Jakarta including GP Plaza, DIPO Business Center, Gallery West and Wisma 77 (Tower 2). In North Jakarta, there will be De Suites and Graha Kirana 2. Meanwhile, South Jakarta will also provide several office towers including Menara Sentraya, Eighty8 Tower B and a newly launched office tower, L’avenue, located in South Jakarta.

oUtside cbd The distribution of office development does not only focus on the CBD area. With the current road infrastructure, inadequate public transport and continued escalation of private car use, traffic is the major obstacle to companies opting for a CBD location. Nevertheless, traffic is Jakarta problem but being located in the outside of CBD would at least alleviate the travelling time to the office. Furthermore, several companies do not require the profile and prestige of CBD location, particularly for those in non-service industries like oil and gas, mining or consumer goods. The other factor is

accessibility. Companies in the industrial or manufacturing sector with workshops or factories in the surrounding cities like Tangerang, Serpong, Bekasi and Bogor will most probably find office locations in the outside of the CBD for easier accessibility. Likewise, the plan to entirely connect Jakarta Outer Ring Road (JORR 1) in the middle of 2013 will promote more office development particularly in the western part of Jakarta and most importantly, will shorten the travel time to the airport.

0

50,000

100,000

150,000

200,000

250,000

300,00020

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2Q 2

012

2012

F

2013

F

2014

F

2015

F

sq m

For Lease For Strata-title

p. 3 | coLLiers internationaL

JAKARTA | 2q 2012 | oFFiCe

tb siMatUpanG As part of the area in South Jakarta, TB Simatupang appears to be enjoying the fastest growth in the outside the CBD area. With continued inquiries for office space mainly derived from oil and gas industries, consumer goods, telecommunications, contractors etc., the TB Simatupang location has lured quite a few developers to build office towers. Currently,

from the launch of Ventura Tower in 1990 to the launch of Plaza Alstom in 2011, there has been 284,948 sq m of office space along TB Simatupang corridor representing around 14% of the total office space in the outside Jakarta area.

tb siMatUpanG office sUppLY

Colliers International Indonesia - Research

Despite no new office space being added during 2Q 2012, 44,020 sq m of office space will commence operations in the remainder of 2012. Nevertheless, the TB Simatupang office market is anticipating a surge in supply in 2013 - 2014 with a total new office space of 339,390 sq m. Several future office towers are concentrated around the Arcadia office complex including Green Kosmo Mansion, 18 Office Park and PHE Tower. PHE is the abbreviation for Pertamina Hulu Energi, the anchor tenant of this building which was previously known as Chitatex Tower. Not far from Arcadia is the planned Oleos Tower.

In the area surrounding the existing Talavera Office Park are Talavera Suite (the extension of Talavera Office Park) and Alamanda Tower. Further west, an integrated commercial complex next to FIF building called South Quarter is now being constructed.

Should the projected buildings finish in 2014, the TB Simatupang corridor will register 668,358 sq m of the cumulative office space which will more than double the current total office supply in 2013 - 2014. Traffic congestion will potentially become a drawback for this location.

0100,000200,000300,000400,000500,000600,000700,000800,000900,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2Q 2

012

2012

F

2013

F

2014

F

2015

F

sq m

Existing Supply Annual Supply

coLLiers internationaL | p. 4

JAKARTA | 2q 2012 | oFFiCe

fUtUre office bUiLdinGs

projected coMpLetion

tiMebUiLdinG naMe Location sGa

(sQ M) MarketinG scheMe statUs*

cbd area

4Q 2012 DBS Tower Satrio 64,000 For Lease and For Strata-title Under Construction

4Q 2012 18 PARK Tower A Sudirman 4,814 For Lease Under Construction

4Q 2012 World Trade Centre 2 Sudirman 57,000 For Lease Under Construction

4Q 2012 Tower 1 at The City Center KH Mas Mansyur 84,000 For Lease and For Strata-title Under Construction

4Q 2012 18 PARK Tower B Sudirman 4,570 For Lease Under Construction

4Q 2012 Perkantoran Setiabudi Setiabudi 11,000 For Lease and For Strata-title Under Construction

4Q 2012 18 PARK Tower C Sudirman 4,441 For Lease Under Construction

4Q 2012 18 PARK Tower E Sudirman 4,233 For Lease Under Construction

1Q 2013 Menara Prima 2 Mega Kuningan 40,000 For Lease Under Construction

1Q 2014 Life Tower HR Rasuna Said 30,500 For Lease Under Construction

2Q 2014 Gran Rubina Tower 1 HR Rasuna Said 40,000 For Strata-title In Planning

2Q 2014 The Noble House Office Tower Mega Kuningan 45,000 For Lease Under Construction

2Q 2014 The City Center (phase 2) KH Mas Mansyur 34,000 For Strata-title In Planning

4Q 2014 Menara Pertiwi Mega Kuningan 40,000 For Lease In Planning

4Q 2014 Graha Surya Internusa 2 HR Rasuna Said 40,000 For Lease In Planning

4Q 2014 Mangkuluhur Tower B Gatot Subroto 39,356 For Lease In Planning

4Q 2014 Menara Selaras Sudirman 36,596 For Lease In Planning

4Q 2014 Sahid Sudirman Center Sudirman 126,600 For Strata-title Under Construction

4Q 2014 The City Center (phase 3) KH Mas Mansyur 34,000 For Strata-title In Planning

4Q 2014 Rifa 2 Satrio 30,000 For Strata-title In Planning

4Q 2014 Wisma Mulia 2 Gatot Subroto 70,000 For Lease Under Construction

4Q 2014 Chase Tower Sudirman 83,000 For Lease In Planning

4Q 2014 Gran Rubina Tower 2 HR Rasuna Said 70,000 For Lease In Planning

1Q 2015 Office Tower @St Regis Gatot Subroto 90,000 For Lease In Planning

1Q 2015 Menara Palma 2 HR Rasuna Said 50,000 For Lease In Planning

2Q 2015 Ciputra World Jakarta 2 Satrio 60,000 For Lease and For Strata-title In Planning

2Q 2015 International Financial Center 2 Sudirman 40,000 For Lease In Planning

4Q 2015 District 8 Sudirman 71,545 For Strata-title In Planning

2Q 2015 Tower 1 at Sampoerna Strategic Square Sudirman 43,000 For Strata-title In Planning

4Q 2015 Tower 2 at Sampoerna Strategic Square Sudirman 118,000 For Lease In Planning

oUtside cbd area (exclude tb siMatUpanG)4Q 2012 Blue Green Office Boutique Meruya 20,000 For Lease Under Construction

4Q 2012 Eighty8 Tower A Kasablanka 56,500 For Lease and For Strata-title Under Construction

2Q 2013 Eighty8 Tower B Kasablanka 31,000 For Lease Under Construction

4Q 2013 DIPO Business Park Slipi 19,600 For Strata-title Under Construction

1Q 2014 De Suites Pantai Indah Kapuk 8,000 For Lease In Planning

2Q 2014 Wisma 77 Tower 2 Letjen S. Parman 24,200 For Strata-title In Planning

2Q 2014 L’Venue Pasar Minggu 41,597 For Strata-title In Planning

2Q 2014 Graha Kirana 2 Yos Sudarso 25,000 For Lease In Planning

2Q 2014 GP Plaza Slipi 12,204 For Strata-title Under Construction

2Q 2014 Menara Sentraya Iskandarsyah 52,072 For Lease and For Strata-title In Planning

2Q 2014 Gallery West Kebon Jeruk 22,800 For Strata-title In Planning

p. 5 | coLLiers internationaL

JAKARTA | 2q 2012 | oFFiCe

Colliers International Indonesia - Research*) Under Construction: where construction activity is in progress, including either foundation or superstructure. Under Planning: no contruction activities on site but all permits have been approved by the Government.

projected coMpLetion

tiMebUiLdinG naMe sGa

(sQ M) MarketinG scheMe statUs*

tb siMatUpanG

3Q 2012 Sovereign Plaza 16,020 For Lease and For Strata-title Under Construction

4Q 2012 PHE Tower (Chitatex Tower) 28,000 For Lease Under Construction

2Q 2013 Alamanda Tower 33,000 For Lease and For Strata-title Under Construction

4Q 2013 Talavera Suite 17,172 For Lease Under Construction

4Q 2013 Green Kosmo Mansion (GKM) 23,000 For Strata-title Under Construction

4Q 2013 Oleos 2 4,181 For Lease Under Construction

1Q 2014 The Manhattan Square 37,699 For Lease and For Strata-title Under Construction

1Q 2014 Beltway Office Park Tower B 9,600 For Lease Under Construction

1Q 2014 Gedung Aneka Tambang Tower 2 16,000 For Lease Under Construction

1Q 2014 South Quarter Tower 1 40,778 For Strata-title In Planning

2Q 2014 18 Office Park (Cityland Tower) 36,627 For Strata-title In Planning

2Q 2014 South Quarter Tower 2 40,778 For Lease In Planning

4Q 2014 South Quarter Tower 3 40,778 For Lease In Planning

4Q 2014 Plaza Oleos 39,778 For Lease and For Strata-title In Planning

1Q 2015 The Manhattan Square Tower 2 33,440 For Lease and For Strata-title In Planning

2Q 2015 Signum North Tower 18,000 For Lease In Planning

4Q 2015 Signum South Tower 54,000 For Lease In Planning

DemandEXISTING DEMAND

cbd The activity of tenant expansions has again lifted the overall occupancy performance during the quarter which was recorded at 95.9%, a Y-o-Y increase of 3.4%. During the quarter alone, several operating buildings have recorded an increase in the occupancy level. The amount

of office space being absorbed by these buildings ranged from 1,000 to 6,000 sq m. Leasing activities were mostly dominated by mining, oil and gas, IT, shipping and cargo, insurance and finance-related industries.

cUMULatiVe sUppLY, deMand and occUpancY of office space in the cbd

Colliers International Indonesia - Research

0%

20%

40%

60%

80%

100%

0

900,000

1,800,000

2,700,000

3,600,000

4,500,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2Q 2

012

sq m

Cumulative Supply Cumulative Demand Occupancy (%)

coLLiers internationaL | p. 6

JAKARTA | 2q 2012 | oFFiCe

The better performance of occupancy rates during the quarter was also fuelled by the performance of newly operating office buildings with high pre-commitment levels before they

are in operation. AXA Tower, 18 Park (Tower D) and Indosurya Plaza operate with high occupancy and this helped to maintain the overall occupancy level during the quarter.

oUtside the cbd The overall occupancy for outside the CBD area registered a slight increase compared to the previous quarter, moving upward to 92.4%. Some buildings scattered in East, North and South Jakarta registered higher occupancy

which helped to lift the overall modest occupancy level. The limited supply of office space in East and North Jakarta was the reason for the occupancy rate increase.

cUMULatiVe sUppLY, deMand and occUpancY of office space in oUtside the cbd

Colliers International Indonesia - Research

tb siMatUpanGSome old buildings (built during the 90s) experienced a slowdown in occupancy.

Compared to the previous quarter, occupancy slowed by around 3.7% to reach 92%.

pre-coMMitted deMand During 2012 there will be 378,131 sq m of new office space of which around 80% has been absorbed. The remaining six months ahead will be a lot easier for buildings scheduled in 2012 to continue their peak performance. The next year will be a tough year to find new office space as only limited space will be available, however, the period of 2014 - 2015 will be quite challenging for the office market given the huge projected supply. None of these office projects expected during that period has confirmed pre-committed demand.

What is available during 2012 in the outside the CBD area of 227,396 sq m has been 55% secured. In the remaining six months, the

search for tenants will continue. Most absorption in 2012 occurred in buildings located along Jalan TB Simatupang. In 2013, the total projected office supply of 127,953 sq m has been 26% absorbed and most absorption was experienced by strata-title office buildings. The big challenge will occur in 2014 when a significant 447,911 sq m of office space is projected to be finished. Of the total supply, less than 2,000 sq m has been committed so far. Office buildings projected to be finished in 2014 will be facing a very challenging situation, particularly those located in Simatupang because more than half of the office space will be in this location.

0%

20%

40%

60%

80%

100%

0

400,000

800,000

1,200,000

1,600,000

2,000,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

1Q 2

012

2Q 2

012

sq m

Cumulative Supply Cumulative Demand Occupancy (%)

p. 7 | coLLiers internationaL

JAKARTA | 2q 2012 | oFFiCe

Rental Rates, Service Charge and Prices

space aVaiLabLe and coMMitted in 2011 - 2014

Colliers International Indonesia - Research

cbd oUtside cbd

aVeraGe askinG rentaL rates in jakarta

Colliers International Indonesia - Research

RENTAL RATES: US$27.43/sq m/monthAround 22 buildings quoting rents in Rupiah adjusted their base rents upward in the range of IDR10,000 to 50,000 per sq m per month. During the quarter. This brought the average rental rates for buildings quoting Rupiah rent to climb by 7.2% to IDR143,807 for all class of buildings in the CBD. Similarly, with 18 buildings announcing new rental rates ranging from US$1.00 to 12.00 , the average US dollar rent also moved upward Q-o-Q by 13.8% to an average of US$26.60 per sq m per month. In recent times, landlords are generally aware that the office market is peaking due to limited supply and this psychologically led quite a few landlords to test the market by adjusting base rental rates close to the market rate.

Albeit moderately, a similar trend was also shown by offices in the outside the CBD area. An increase of 5.1% brought the average rental rates for Rupiah denominated buildings to IDR99,610 per sq m per month. The increase was triggered by some office buildings asking for higher rates of between IDR15,000 and 20,000. On a regional scale, South Jakarta fetched the highest average rental rates of IDR121,872 per sq m per month given the higher quality of most buildings in this area, particularly buildings in the TB Simatupang area.

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

Rp-

Rp46,000

Rp92,000

Rp138,000

Rp184,000

Rp230,000

Rp276,000

Premium Grade A Grade B Grade C

Rp US$

0 250,000 500,000 750,000

2011

2012F

2013F

2014F

sq m

Space Absorbed Annual Supply

0 250,000 500,000 750,000

2011

2012F

2013F

2014F

sq m

Space Absorbed Annual Supply

coLLiers internationaL | p. 8

JAKARTA | 2q 2012 | oFFiCe

serVice charGe Though several buildings did renovation work, service charges remained stable during the quarter. The average service charge was only raised by IDR545 to 55,631 per sq m per month

in the CBD. Meanwhile the service charges in the outside the CBD was IDR42,593 per sq m per month and only climbed by IDR1,145 over last quarter.

strata-titLe office space for saLe

cbd The absorption level of strata-title office space in the CBD reached 96.9% as of 2Q 2012. Consequently, with limited strata-title office space being available, the price continues to move upward. Compared to last year, the price of strata-title office space has gone up 21.5%

while the price under Q-o-Q review went up by 7.8%. The average price of strata-title office space sold at the US Dollar rate was US$2,867 per sq m while that in Rupiah were offered at an average of IDR25.8 million per sq m.

oUtside cbd The overall take-up rates of offices outside the CBD area dropped substantially from 94.6% to only 83.8% in 2Q 2012. The operation of new and sizeable office buildings during 2Q 2012 with relatively low take-up rates changed the overall absorption performance. In term of strata-title office space price per square metre,

a significant jump was recorded Q-o-Q to IDR2.76 million which put the average price at IDR20.9 million per sq m. Most of operating strata-title buildings adjusted the price in the range of IDR1 to 4 million while some others have confidently raised the price between IDR7 and 11.5 million.

p. 9 | coLLiers internationaL

JAKARTA | 2q 2012 | oFFiCe

coLLiers internationaL indonesia:

World Trade Centre 10th & 14th floorJalan Jenderal Sudirman Kav. 29 - 31Jakarta 12920IndonesiateL 62 21 521 1400faX 62 21 521 1411

512 offices in 61 countries on 6 continentsUnited States: 125Canada: 38Latin America: 18Asia Pacific: 214EMEA: 117

• $1.5 billion in annual revenue

• 979 billion square feet under management

• Over 12,500 professionals

Copyright 2012 Colliers International

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has bee made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inac-curacies. Readers are encouraged to consult their pro-fessional advisors prior to acting on any of the material contained in this report.

www.colliers.co.id

Accelerating success.

Michael Broomell Managing Director

World Trade Centre 10th & 14th floorJalan Jenderal Sudirman Kav. 29 - 31Jakarta 12920IndonesiateL 62 21 521 1400 ext 131faX 62 21 521 1411

Ferry SalantoAssociate Director, Research

World Trade Centre 10th & 14th floorJalan Jenderal Sudirman Kav. 29 - 31Jakarta 12920IndonesiateL 62 21 521 1400 ext 134faX 62 21 521 1411

The absorption rates of office space is projected to mildly increase at least until 2013 because new supply in the CBD is very limited during that year. The types of industry which drive this sector will remain, i.e. banking, insurance, oil and gas and the mining and natural resources business. However, a challenging situation will occur both in the CBD and in the non-CBD areas because a significant number of new office space is projected to come on stream.

Again, the rents showed an upward trend Q-o-Q with buildings quoting US Dollar rates experiencing a significant climb. To date, the

market is very confident because quite a few developers are trying to adjust rental tariffs to rival the average market. Buildings with very high occupancy rates are even arbitrarily setting their new prices with the confidence that the market will absorb the office space.

The continuing adjustment in the office rents would open more opportunity for the sales of strata-title office space. In the long term, owning office space will be very attractive and this is shown by the good performance of strata-title office space sales.

Outlook

JAKARTA | 2q 2012 | industrial estate