Embed Size (px)

Citation preview

12/16/2010

Contractor, Nayak & Kishnadwala 1

PROPERTY, PLANT & EQUIPMENT

Himanshu Kishnadwala21st December 2010

Topics covered in the presentation

• Background

• IAS 16• Exposure Draft on AS-10 (revised) issued by ICAI• Differences between AS-10, AS-6 and ED on AS-10 (revised)• Conflicting issues with Companies Act, 1956• Differences between IAS-16 and ED on AS-10

• IAS-23 Borrowing costs

• IAS 17 Leases• Accounting for PPE by local bodies (ASLB 5)• Extract from select Annual Reports• Case Studies

CNK

2

12/16/2010

Contractor, Nayak & Kishnadwala 2

IFRS Framework

As per Framework to IFRS:

• An asset is a resource controlled by the entity as a result of past events from which future economic benefits are expected to flow to the entity.

• An asset is recognised in the balance sheet when it is probable that the future economic benefits will flow to the entity and the asset has a cost or value that can be measured reliably.

• An asset is not recognised in the balance sheet when expenditure has been incurred for which it is considered improbable that economic benefits will flow to the entity beyond the current accounting period. These transactions are recognised as an expense in the income statement.

CNK

3

IAS 16

• Revised standard issued in December 2003

• Standard contains 80 paragraphs

• Other relevant standards:

� SIC 21: Income Taxes—Recovery of Revalued Non-Depreciable Assets

� SIC 29: Service Concession Arrangements: Disclosures

� SIC 32: Intangible Assets—Web Site Costs

� IFRIC 1: Changes in Existing Decommissioning, Restoration and Similar Liabilities

� IFRIC 4: Determining whether an Arrangement contains a Lease

� IFRIC 12: Service Concession Arrangements

CNK

4

12/16/2010

Contractor, Nayak & Kishnadwala 3

Objective & Scope of IAS 16

• To prescribe the accounting treatment for Property, Plant & Equipment (PPE)

• To enable users of FS get information about the entity’sinvestment in its PPE and the changes therein

• The principal issues in accounting for PPE are:

� The Recognition of assets

� Determination of carrying amount

� Depreciation

� Disclosures

CNK

5

Exclusions

IAS 16 does not apply to:

a)Property, plant and equipment classified as held for sale [IFRS 5 Non-current Assets Held for Sale and Discontinued Operations]

b)Biological assets related to agricultural activity

c)The recognition and measurement of exploration and evaluation assets or

d) Mineral rights and mineral reserves such as oil, natural gas and similar non-regenerative resources.

However, this Standard applies to property, plant and

equipment used to develop or maintain the assets described in (b) to (d).

CNK

6

12/16/2010

Contractor, Nayak & Kishnadwala 4

Definitions

• Property, Plant and Equipment are tangible items that:

(a) are held for use in the production or supply of goods or services, for rental to others, or for administrative purposes; and

(b) are expected to be used during more than one period.

Issue

• Does one period mean 1 year/quarter/accounting period?

• Entity specific Value is the present value of the cash flows an entity expects to arise from the continuing use of an asset and from its disposal at the end of its useful life or expects to incur when settling a liability.

• Recoverable amount is the higher of an asset’s fair value less costs to sell and its value in use.

CNK

7

Definitions …

• The residual value of an asset is the estimated amount that an entity would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.

• Useful life is:

(a) the period over which an asset is expected to be available for use by an entity; or

(b) the number of production or similar units expected to be obtained from the asset by an entity.

CNK

8

12/16/2010

Contractor, Nayak & Kishnadwala 5

Recognition of PPE

• The cost of an item of property, plant and equipment shall be recognised as an asset if, and only if:

(a) it is probable that future economic benefits associated with the item will flow to the entity;

and

(b) the cost of the item can be measured reliably.

• Spare parts and servicing equipments

� Normally classified as inventory

� If however, can be used only in connection with an item of PPE, they are accounted for as PPE

• Aggregation of individual insignificant items

CNK

9

Recognition of PPE …

• Initial Recognition includes PPE acquired for safety and environmental purposes

Issue

Safety related assets compulsorily acquired due to legislation vis-à-vis such assets acquired voluntarily?

• Subsequent costs do not include the costs of the day-to-day servicing of the item. Costs of day-to-day servicing are primarily the costs of labour and consumables, and may include the cost of small parts. These costs are recognised in profit or loss as incurred.

CNK

10

12/16/2010

Contractor, Nayak & Kishnadwala 6

Recognition of PPE …

• Parts of some items of PPE may require replacement at regular intervals. In that case, the carrying amount of an item of PPE will be adjusted as follows:

o Under the recognition principle in para 7, an entity recognises the cost of replacing part of such an item when that cost is incurred if the recognition criteria are met.

o The carrying amount of those parts that are replaced is derecognised.

o If it is impracticable for an entity to determine the carrying amount of the replaced part, it may use the cost of the replacement as an indication of what the cost of the replaced part was at the time it was acquired or constructed.

Issues

� Identification of Capital vs. Revenue?

� Tax implications??

CNK

11

Recognition of PPE …

Component Accounting

• A condition of continuing to operate an item of PPE (for example, an aircraft) may be performing regular major inspections for faults regardless of whether parts of the item are replaced. When each major inspection is performed, its cost is recognised in the carrying amount of the item of PPE as a replacement if the recognition criteria are satisfied.

• Any remaining carrying amount of the cost of the previous inspection (as distinct from physical parts) is derecognised.

• This occurs regardless of whether the cost of the previous inspection was identified in the transaction in which the item was acquired or constructed. If necessary, the estimated cost of a future similar inspection may be used as an indication of what the cost of the existing inspection component was when the item was acquired or constructed.

CNK

12

12/16/2010

Contractor, Nayak & Kishnadwala 7

Component Accounting …

Issues

� Identification of components

�How detailed should one go?

�Aligning FA register with components

�Can result in subjectivity and different approaches by companies (even in same industry)

�Tax implications??

CNK

13

Measurement at Recognition of PPE

• Measurement at Initial Recognition is always at Cost

• An item of PPE that qualifies for recognition as an asset under para 7 shall be measured at its cost.

• The cost of an item of PPE comprises:

a) its purchase price, including import duties and non-refundable purchase taxes, after deducting trade discounts and rebates;

b) any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by management.

c) the initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located, the obligation for which an entity incurs.

Issues

� How to estimate dismantling and other costs?

CNK

14

12/16/2010

Contractor, Nayak & Kishnadwala 8

Measurement at Recognition

• Examples of directly attributable costs are:

o Costs of employee benefits (as defined in IAS 19 Employee Benefits) arising directly from the construction or acquisition of the item of PPE;

o Costs of site preparation;

o Initial delivery and handling costs;

o Installation and assembly costs;

o Costs of testing whether the asset is functioning properly, after deducting the net proceeds from selling any items produced while bringing the asset to that location and condition (such as samples produced when testing equipment); and

o Professional fees.

CNK

15

Measurement at Recognition …

• Examples of costs that are not costs of an item of property, plant and equipment are:

o costs of opening a new facility;

o costs of introducing a new product or service (including costs of advertising and promotional activities);

o costs of conducting business in a new location or with a new class of customer (including costs of staff training); and

o administration and other general overhead costs.

Issues

�Costs that can be recognised are more restrictive than under current AS 10.

�Tax implications??

CNK

16

12/16/2010

Contractor, Nayak & Kishnadwala 9

Measurement of Cost

• The cost of an item of PPE is the cash price equivalent at the recognition date. If payment is deferred beyond normal credit terms, the difference between the cash price equivalent and the total payment is recognised as interest over the period of credit unless such interest is recognised in the carrying amount of the item in accordance with the allowed alternative treatment in IAS 23.

• When an item of PPE is acquired in exchange for a non-monetary asset, its cost is measured as its fair value unless

(a) the exchange transaction lacks commercial substance or

(b) the fair value of neither the asset received nor the asset given up is reliably measurable.

• If the acquired item is not measured at fair value, its cost is measured at the carrying amount of the asset given up.

Issue: Recognition and Measurement of assets acquired for use –Consideration as a percentage of revenues of the entity?

CNK

17

Measurement after Recognition

Measurement after Recognition

Cost Model

After recognition as an asset, an item of property, plant and equipment shall be carried at its cost less any accumulated

depreciation and any accumulated

impairment losses.

Revaluation Model

An item of property, plant and equipment whose fair value can be measured reliably shall be carried at a

revalued amount.

Deemed cost model (para 30 of Ind-AS 41)

A first-time adopter of IFRS has an

option to voluntarily account as per Deemed Cost

Model

CNK

18

12/16/2010

Contractor, Nayak & Kishnadwala 10

Revaluation Model

• After recognition, an item of PPE shall be carried at revalued amount less any subsequent accumulated depreciation and Impairment losses

• Revaluation should be made at the Fair value of the asset i.e., after revaluation assets should be recognised at their fair values.

• Such revaluation should be made at regular intervals to ensure that the carrying amounts of any of the assets doesn't differ materially from the fair values

• Periodicity of revaluation depends upon the changes in fair values of the items of PPE that are being revalued.

• Entire class of PPE should be revalued at a time. • In case rolling revaluation is carried out for a class of assets each should be completed within a short span of time.

CNK

19

Determining Fair value

CNK

20

Fair value is the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length

transaction.

Determination of fair value in case of different items is as follows

Land and Buildings:

is usually determined from market-based evidence by appraisal that is normally

undertaken by professionally qualified

valuers.

Other Items of PPE :

Fair values depend upon the market values

If there is no market-based evidence of fair value

because of the specialized nature of the item of PPE and the item is rarely sold, an entity may need to

estimate fair value using an income or a depreciated

replacement cost approach.

12/16/2010

Contractor, Nayak & Kishnadwala 11

Accounting treatment of revaluation

• Treatment of Difference on revaluation

o Increase in value on revaluation shall be credited to a separate ‘Revaluation Surplus’ under Other Comprehensive Income(OCI) except to the extent it relates to previous decrease in value of same asset

o Reduction on revaluation to be taken to Income Statement except to the extent that can be adjusted against Revaluation Surplus.

CNK

21

Accounting treatment of revaluation …

• Treatment of Accumulated depreciation on revaluation of PPEo restated proportionately with the change in the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals its revalued amount. This method is often used when an asset is revalued by means of applying an index to determine its depreciated replacement cost or

o eliminated against the gross carrying amount of the asset and the net amount restated to the revalued amount of the asset. This method is often used for buildings.

• Incase of revaluation on Investment Property, the change in value (increase or decrease) to be taken to Comprehensive Income Statement.

CNK

22

12/16/2010

Contractor, Nayak & Kishnadwala 12

Depreciation

• Depreciation of each component should be based on its useful life

• All items of PPE with a cost that is significant in relation to the total cost of the item shall be depreciated separately.

• In case useful lives and depreciation charge are same for two or more significant items of the same PPE, then such parts may be grouped in determining the depreciation charge

• Insignificant items should be depreciated separately on the basis of approximation of useful lives and consumption pattern

• The depreciation charge for each period shall be recognised in profit or loss unless it is included in the carrying amount of another asset.

� For example, the depreciation of manufacturing plant and equipment is included in the costs of conversion of inventories as per IAS 2.

CNK

23

Depreciable amount and depreciation period

• Depreciable amount of an asset:� shall be allocated on a systematic basis over its useful life. � is determined after deducting its residual value.

• Depreciation method to be reviewed every year. Change in estimates of useful lives of assets resulting in change in depreciation shall be accounted for prospectively

• Begins when asset is available for use, i.e. when it is in the location and condition necessary for it to be capable of operating in the manner intended by management.

• Ceases at the earlier of the date that asset is classified as held for sale

• Depreciation does not cease when the asset becomes idle or is retired from active use unless it is fully depreciated.

• However, under usage methods of depreciation the depreciation charge can be zero if there is no production.

CNK

24

12/16/2010

Contractor, Nayak & Kishnadwala 13

Determination of useful life of PPE

• Useful lives to be determined considering following factors:� expected usage of the asset. � expected physical wear and tear, � technical or commercial obsolescence � legal or similar limits on the use of the asset, such as the expiry dates of related leases.

• Useful life of an asset may be shorter than its economic life. • The estimation of the useful life of the asset is a matter of judgement based on the experience of the entity with similar assets.

• The depreciation method used shall reflect the pattern in which the asset’s future economic benefits are expected to be consumed by the entity.

CNK

25

Determination of useful life of PPE

• An increase in the value of the land on which a building stands does not affect the determination of the depreciable amount of the building.

• If the cost of land includes the costs of site dismantlement, removal and restoration, that portion of the land asset is depreciated over the period of benefits obtained by incurring those costs

Issues• Review of Residual value and useful life every year?• Likely introduction of Schedule XIV equivalent?

• Tax implications ??

CNK

26

12/16/2010

Contractor, Nayak & Kishnadwala 14

De-recognition of PPE

• The carrying amount of an item of PPE shall be de-recognised:

� on disposal; or

� when no future economic benefits are expected from its use or disposal.

• The gain or loss arising from the de-recognition of an item of PPE shall be included in profit or loss when the item is de-recognised (unless IAS 17 requires otherwise on a sale and leaseback). Gains shall not be classified as revenue.

• The gain or loss arising from the de-recognition of an item of PPE shall be determined as the difference between the net disposal proceeds, if any, and the carrying amount of the item.

CNK

27

Disclosures

Para 73 to para 79 of IAS 16

CNK

28

12/16/2010

Contractor, Nayak & Kishnadwala 15

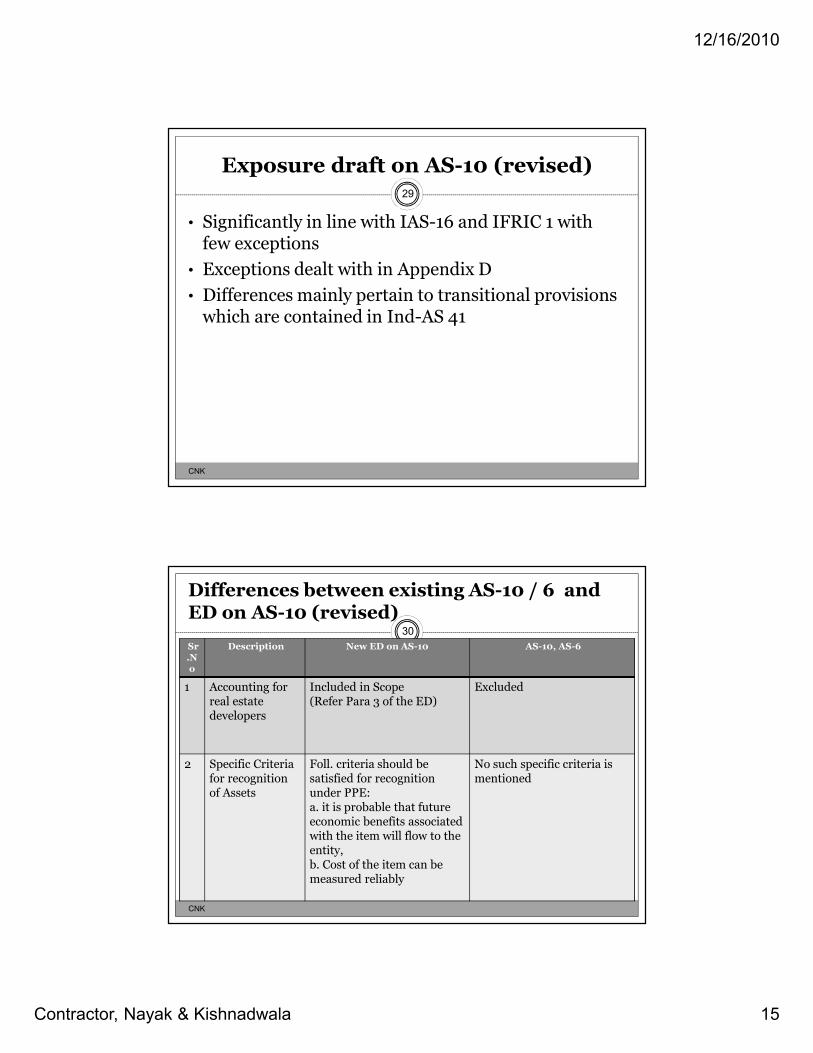

Exposure draft on AS-10 (revised)

• Significantly in line with IAS-16 and IFRIC 1 with few exceptions

• Exceptions dealt with in Appendix D

• Differences mainly pertain to transitional provisions which are contained in Ind-AS 41

CNK

29

Differences between existing AS-10 / 6 and ED on AS-10 (revised)

CNK

30

Sr.No

Description New ED on AS-10 AS-10, AS-6

1 Accounting for real estate developers

Included in Scope(Refer Para 3 of the ED)

Excluded

2 Specific Criteria for recognition of Assets

Foll. criteria should be satisfied for recognition under PPE:a. it is probable that future economic benefits associated with the item will flow to the entity,b. Cost of the item can be measured reliably

No such specific criteria is mentioned

12/16/2010

Contractor, Nayak & Kishnadwala 16

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

31

Sr.No

Description New ED on AS-10 AS-10, AS-6

3 Capitalisation of Subsequent expenditure

Treatment is same as that of initial costs

This can be capitalised only if it increases the benefits from the existing assets beyond the previously assessed standard of performance

4 Capitalisation of major spare parts with the cost of PPE

To be capitalized only when the entity intends to use them for more than 1 accounting period and can be used specifically in the connection of that PPE

Capitalisation of only those spares which can be used in connection with the fixed assets and whose use is irregular

5 Component Approach

Specifically deals with capitalising major components of an asset separately

Not mentioned in AS-10 and AS-6

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

32

Sr.No

Description New ED on AS-10 AS-10, AS-6

6 Cost of major Inspections

To be capitalised No mention of capitalising the inspection costs under AS-10

7 Costs of Dismantling and restoration

Initial estimate of the costs of dismantling and removing the item and restoring the site on which it is located should be included in the cost of the respective item of property plant and equipment. (Para 16c and 18 of revised AS-10)

As-10 does not contain any such requirement.

12/16/2010

Contractor, Nayak & Kishnadwala 17

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

33Sr.No

Description New ED on AS-10 AS-10, AS-6

8 Revaluation of assets

•Fair value approach to be followed.•To be applied to entire class of assets•Revaluation to be done on a regular basis

• Approach is adhoc in nature.•Does not require adoption of fair value as accounting policy •Regularity in revaluation is not required.•Revaluation permissible for some assets within a particular class

9 Treatment of revaluation surplus

Transfers from revaluation surplus to retained earnings are not through profit and loss account.

AS 10 and AS 6 does not deal with this. GN on Treatment of Reserve created on Revaluation of Fixed Assets allows transfer of additional depreciation to PL a/c

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

34Sr.No

Description New ED on AS-10 AS-10, AS-6

10 Self Constructed Assets

Cost of abnormal amounts of wasted material,labour, or other resources incurred in the construction of an asset are not to be capitalised

As-10 does not deal with such aspects.

11 Provides that the cost of an item of PPE is the cash price equivalent at the recognition date. If payment is deferred beyond normal credit terms, the difference between the cash price equivalent and the total payment is recognised as interest over the period of credit unless such interest is capitalised in accordance with AS 16

No such mention under AS-10

12/16/2010

Contractor, Nayak & Kishnadwala 18

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

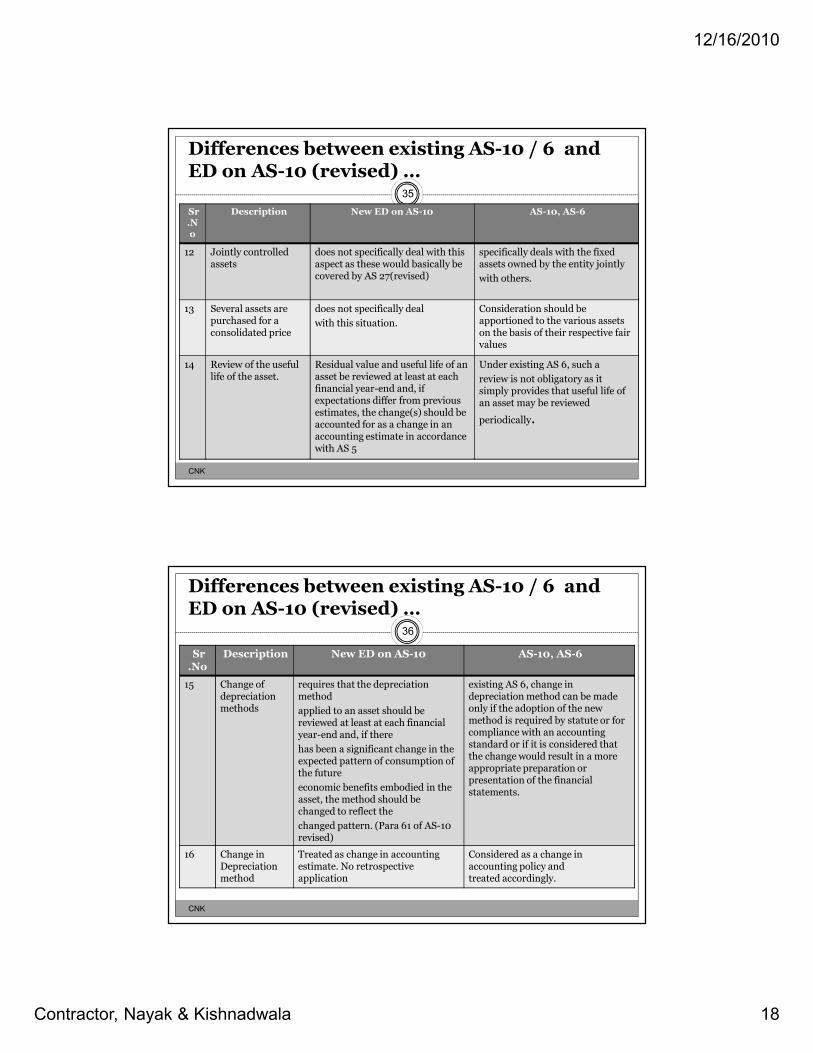

CNK

35

Sr.No

Description New ED on AS-10 AS-10, AS-6

12 Jointly controlled assets

does not specifically deal with this aspect as these would basically be covered by AS 27(revised)

specifically deals with the fixed assets owned by the entity jointly

with others.

13 Several assets are purchased for a consolidated price

does not specifically deal

with this situation.

Consideration should beapportioned to the various assets on the basis of their respective fair values

14 Review of the useful life of the asset.

Residual value and useful life of an asset be reviewed at least at each financial year-end and, if expectations differ from previous estimates, the change(s) should be accounted for as a change in an accounting estimate in accordance with AS 5

Under existing AS 6, such a

review is not obligatory as it simply provides that useful life of an asset may be reviewed

periodically.

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

36

Sr.No

Description New ED on AS-10 AS-10, AS-6

15 Change of depreciation methods

requires that the depreciation method

applied to an asset should be reviewed at least at each financial year-end and, if there

has been a significant change in the expected pattern of consumption of the future

economic benefits embodied in the asset, the method should be changed to reflect the

changed pattern. (Para 61 of AS-10 revised)

existing AS 6, change in depreciation method can be made only if the adoption of the new method is required by statute or for compliance with an accounting standard or if it is considered that the change would result in a more appropriate preparation or presentation of the financial statements.

16 Change in Depreciation method

Treated as change in accounting estimate. No retrospective application

Considered as a change in accounting policy andtreated accordingly.

12/16/2010

Contractor, Nayak & Kishnadwala 19

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

37

Sr.No

Description New ED on AS-10 AS-10, AS-6

17 Compensation from third parties for assets lost, impaired, given up

As per the ED, all such items should be included in Statement of Profit and loss when compensation becomes receivable

No such mention in the standard

18 Gains arising on derecognition

Such gains should not be treated as revenue

AS-10 is silent on this aspect

19 Items of PPE held as for rental to others and subsequently to be sold

ED on AS-10 specifically deals with such situations

No such mention in the standard

Differences between existing AS-10 / 6 and ED on AS-10 (revised) …

CNK

38

Sr.No

Description New ED on AS-10 AS-10, AS-6

20 Assets held for sale ED on AS-10 does not deal with these aspects as they are specifically covered by AS-24 revised

Assets held for sale shall be separately shown on the face of the balance sheet. Depreciation on the asset should be stopped from the date that it is held for disposal

21 Disclosure requirements

The disclosure requirements are very elaborate

Not as elaborate

12/16/2010

Contractor, Nayak & Kishnadwala 20

ED on AS-10 (revised)Conflicting Issues with Companies Act,1956

• Appendix C to ED on AS-10

• Component Approach not recognised under the Companies Act,1956

• Sch XIV requires , assets to be depreciated as per the rates mentioned therein and depending upon the number of shifts for which the asset is used Whereas under AS-10 Depreciation is to be calculated based on the useful lives of the assets

• Units of Production Method recognised under AS-10 but not under Companies Act, 1956

• Section 205(1) of the Companies Act, 1956, and Schedule VI-PART II to the Companies Act, 1956 recognise the situation of non-provision of depreciation. No such situation has been recognised in AS 10

CNK

39

Deemed Cost- Exception under IFRS 1 (Ind – AS 41)

• Deemed Cost: An amount used as a surrogate for cost or depreciated cost at a given date. Subsequent depreciation/ amortisation assumes that the entity had initially recognised the asset or liability at the given date and that its cost was equal to the deemed cost.

• This exemption (option) of using fair value or revaluation asdeemed cost at the date of transition applies to:

� property, plant and equipment;

� investment property, if an entity elects to use the costmodel in IAS 40 Investment Property; and

� intangible assets that meet the criteria for recognition andrevaluation of IAS 38 Intangible Assets.

CNK

40

12/16/2010

Contractor, Nayak & Kishnadwala 21

Deemed Cost- Exception …

• The exemption may be used selectively within the classes ofassets.

• This exemption is not available for other assets andliabilities.

• Fair value; or a revaluation under previous GAAP, or an‘event-driven’ value may be used as the ‘deemed cost.

• Previous GAAP revaluation of PPE can be used as Deemed Cost if the revaluation was at the date of revaluation broadly comparable to:• Fair Value or• Cost or depreciated cost adjusted to reflect changes in price index

• Subsequent depreciation is based on the deemed cost• Increase/decrease is adjusted against Retained earnings

CNK

41

Borrowing Costs (IAS-23) (AS 16)

CORE PRINCIPLE

Borrowing costs that are directly attributable to the acquisition, construction or production of a qualifying asset form part of the cost of that asset.

Other borrowing costs are recognised as an expense.

CNK

42

12/16/2010

Contractor, Nayak & Kishnadwala 22

Borrowing Costs (IAS-23) …

• Borrowing Costs include:

o Interest expense calculated using the effective interest rate method;

Interest and commitment charges on bank borrowings and other short-term

and long-term borrowings;

� amortisation of discounts or premiums relating to borrowings;

� amortisation of ancillary costs incurred in connection with the arrangement of borrowings;

� finance charges in respect of finance leases recognised in accordance with AS 19 (Revised) Leases; and

� exchange differences arising from foreign currency borrowings to the extent that they are regarded as an adjustment to interest costs.

CNK

43

Borrowing Costs (IAS-23) …

• Qualifying asset (QA) is generally the one that takes substantial period of time for generation( substantial period is not defined under IFRS)

• Capitalisation of Borrowing Costs

o only in case of qualifying assets

o BC directly attributable to acquisition/construction or production of a qualifying asset shall be capitalised as a part of the cost of the asset

• Capitalisation of Interest on Borrowings :

o Specific Borrowings: attributable for QA shall be capitalised

o General borrowings capitalised using weighted average of the BC

• Capitalisation of BC should commence when:

� Expenditure for that asset is being incurred

� BC are incurred

� Activities that are necessary to prepare the asset for its intended use or sale are in progress

CNK

44

12/16/2010

Contractor, Nayak & Kishnadwala 23

Borrowing Costs (IAS-23) …

• Suspension of Capitalisation:

• During extended periods in which active development is interrupted

• Cessation of capitalisation :

• when substantially all the activities necessary to prepare the qualifying asset for its intended use or sale are complete

• Disclosure :

� Accounting policy adopted for BC.

� Amounts of BC capitalised during the period

� Rate of capitalisation used for capitalisation of assets

CNK

45

IAS 17 – LEASES

12/16/2010

Contractor, Nayak & Kishnadwala 24

Background, Objective and Scope

• What is a Lease� A lease is an agreement whereby the lessor conveys to the lessee in return for payment or a series of payments the right to use an asset for an agreed period of time

• Objective� To prescribe, for lessee and lessor, the appropriate accounting policies and disclosures to apply in relation to finance and operating leases.

• Scope� Applies to all leases other than

� lease agreements for minerals, oil, natural gas, and similar regenerative resources and

� licensing agreements for films, videos, plays, manuscripts, patents, copyrights, and similar items.

CNK

47

Scope …

• IAS 17 also does not apply as the basis of measurement for the following leased assets:

� Property held by lessees that is accounted for as investment property for which the lessee uses the fair value model (IAS 40).

� Investment property provided by lessors under operating leases (IAS 40).

� Biological assets held by lessees under finance leases (IAS 41).

� Biological assets provided by lessors under operating leases (IAS 41).

CNK

48

12/16/2010

Contractor, Nayak & Kishnadwala 25

Classification of Leases

• Classification to be made at the time of the inception • Classification is based on the Extent to which Risks and Rewards incidental to ownership are transferred

• If there is a change in the terms of the agreement subsequently, to the extent of affecting the classification, then such changed agreement has to be treated as a new agreement

• Changes in estimates or changes in circumstances would not affect the classification

CNK

49

Risks vs. Rewards

� Risks Include –

� Possibilities of losses from idle capacity or

� Technological obsolescence

� Variation in return because of changing economic conditions

� Rewards Include –

� Expectation of profitable operation over the assets economic life

� of gain from appreciation in value

� or realization of a residual value

CNK

50

12/16/2010

Contractor, Nayak & Kishnadwala 26

Definitions

• Finance Lease� A lease that transfers substantially all the risks and rewards incident to ownership of an asset. Title may or may not eventually be transferred.

• Operating Lease� A lease other than a finance lease

CNK

51

Lease vs. Sale

• Lease

� right to use an asset for an agreed period of time

� may transfer significant risks and rewards associated with ownership of asset

• Sale

� sellers transfer significant risks and rewards associated with ownership of asset

� seller has no continuing managerial involvement/ control in the asset

CNK

52

12/16/2010

Contractor, Nayak & Kishnadwala 27

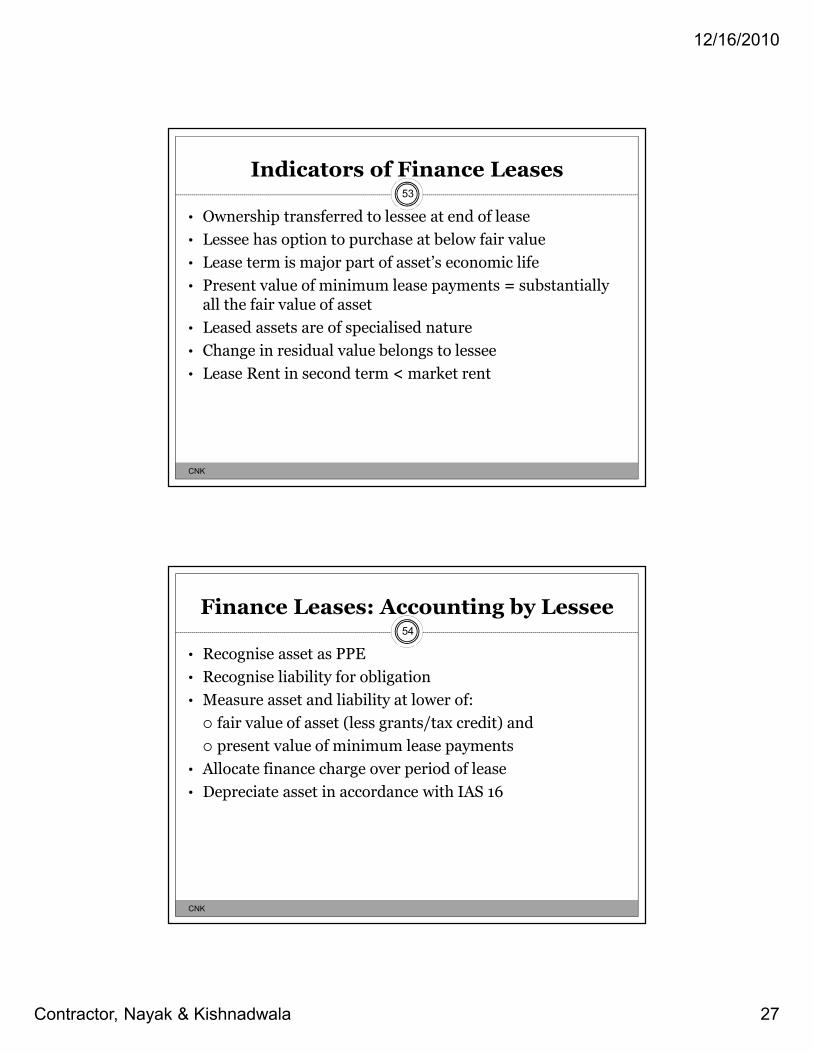

Indicators of Finance Leases

• Ownership transferred to lessee at end of lease

• Lessee has option to purchase at below fair value

• Lease term is major part of asset’s economic life

• Present value of minimum lease payments = substantially all the fair value of asset

• Leased assets are of specialised nature

• Change in residual value belongs to lessee

• Lease Rent in second term <market rent

CNK

53

Finance Leases: Accounting by Lessee

• Recognise asset as PPE

• Recognise liability for obligation

• Measure asset and liability at lower of:

� fair value of asset (less grants/tax credit) and

� present value of minimum lease payments

• Allocate finance charge over period of lease

• Depreciate asset in accordance with IAS 16

CNK

54

12/16/2010

Contractor, Nayak & Kishnadwala 28

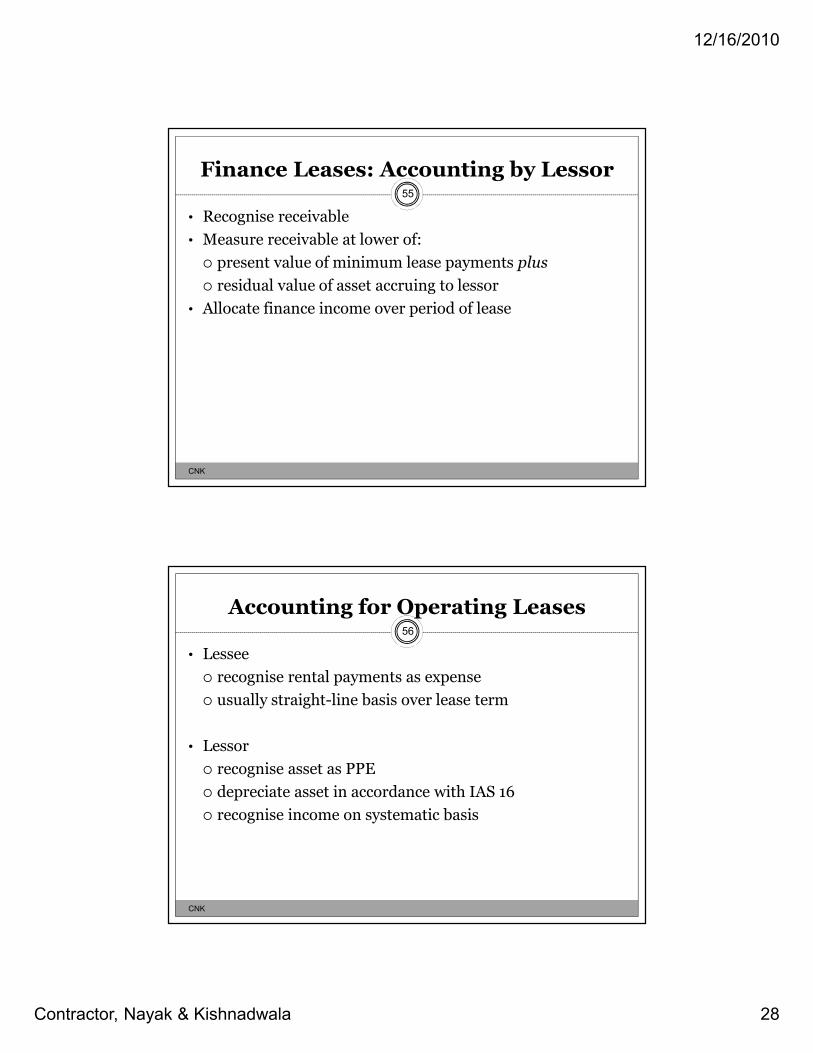

Finance Leases: Accounting by Lessor

• Recognise receivable

• Measure receivable at lower of:

� present value of minimum lease payments plus

� residual value of asset accruing to lessor

• Allocate finance income over period of lease

CNK

55

Accounting for Operating Leases

• Lessee

� recognise rental payments as expense

� usually straight-line basis over lease term

• Lessor

� recognise asset as PPE

� depreciate asset in accordance with IAS 16

� recognise income on systematic basis

CNK

56

12/16/2010

Contractor, Nayak & Kishnadwala 29

IFRIC 4DETERMINING WHETHER

AN ARRANGEMENT CONTAINS A LEASE

Determining Whether An Arrangement Is A Lease?

Determining whether an arrangement is, or contains, a lease shall be based on the substance of the arrangement and requires an assessment of whether:

� fulfilment of the arrangement is dependent on the use of a specific asset/s; and

� the arrangement conveys a right to use the asset

CNK

58

12/16/2010

Contractor, Nayak & Kishnadwala 30

Use Of A Specific Asset

• If the supplier is obliged to deliver a specified quantity of goods or services and has the right and ability to provide those goods and services using other assets not specified in the arrangement, then the arrangement does not contain a lease, even if a specific asset is explicitly identified

• An asset has been implicitly specified if, for example, the supplier owns or leases only one asset with which to fulfil the obligation, and it is not economically feasible or practicable for the supplier to perform its obligation through the use of alternative assets

CNK

59

Arrangement That Conveys A Right To Use The Asset

• An arrangement conveys the right to use the asset if the arrangement conveys to the purchaser the right to control the use of the underlying asset

• The purchaser has the ability or right to operate the asset while obtaining or controlling more than a significant amount of the output

• The purchaser has the ability or right to control physical access to the asset while obtaining or controlling more than a significant amount of the output

CNK

60

12/16/2010

Contractor, Nayak & Kishnadwala 31

Arrangement That Conveys A Right To Use The Asset ...

• Facts and circumstances indicate that it is remote that one or more parties other than the purchaser will take more than an insignificant amount of the output; and

• The price for the output is neither contractually fixed per unit of output nor equal to the current market price per unit of output as at the time of delivery of the output

CNK

61

IFRIC 4 Implications

• Outsourcing arrangement for � Pharma Industry

� Automobile Industry

� Data processing functions

� Telecommunications industry

CNK

62

12/16/2010

Contractor, Nayak & Kishnadwala 32

Modifications to Lease Accounting

Framework for preparation and Presentation of FS

• Asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity

• Liability is a present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow from the entity of resources embodying economic resources

• Most Leases would classify for recognition as Asset and Liability

• Distinction between Finance and Operating Lease is not supported at conceptual level itself.

CNK

63

Property Plant and Equipment-ASLB -5

• Standard specifically prescribes accounting treatment for

local bodies

• It is based on the corresponding International Public Sector Accounting Standard-17 (IPSAS-17)- property plant and equipment.

• It deals with Accounting for Heritage assets and infrastructure assets.- recognition. Measurement, subsequent measurement Disposal etc.

Issue� Determining fair value of infrastructure and heritage assets.

CNK

64

12/16/2010

Contractor, Nayak & Kishnadwala 33

Interview of Mr. Salman Khurshid on IFRS

• From Day 1, we have said we will converge, not adopt. There will be different standards on specific issues on which we need to have different standards. Convergence gives you the flexibility to stop where you want to stop, adjust where you want to adjust and make an exception where you want to make an exception.

• There was no confusion about alignment of IFRS with tax laws. There will be two parallel systems — the accounting system and the tax system.

Business Line, July 17, 2010

CNK

65

QUESTIONS ??

CNK

66

Case Studies Page 1

CASE STUDIES

IAS-16 PROPERTY PLANT AND EQUIPMENT

1. A company acquires a type of equipment that its employees have never operated

before. During the installation period, the employees receive extensive training on the

equipment. The cost to the company includes the incremental cost of hiring experts to

conduct the training, and the directly attributable cost of wages to the employees

during the training period.

Do these training costs qualify as a component of the cost of the equipment?

2. A ski resort operator in Gulmarg has developed a piece of land into a skiing report.

To do that the operator has cut the trees, cleared and graded the land and hills, and

constructed Ski Park.

Should the tree cutting, land clearing and grading costs be capitalised as part of the

cost of land (and therefore, not depreciated) or as part of the cost of the ski park (and

therefore subject to depreciation)?

3. Company A enters into a contract with Company B to produce and sell a specific

asset. Entity A needs to transform a major part of its plant to be able to produce this

specific asset. These costs are significant and exclusively for the purpose of this sales

contract. Therefore, A & B enter into an agreement in which A will re-invoice to B a

part of the transformation costs.

Can the reimbursement be deducted from the cost of the transformation?

4. Company A was allotted a plot of land on perpetual lease for construction of a

building subject to fulfillment of certain conditions. The agreement specifies that the

plot would be on license under an agreement and upon successful fulfillment of the

terms of the contract, lease would be given. The lease will, however, commence from

the date of allotment.

Case Studies Page 2

Should the amount paid to the government be accounted as a security deposit up to

the successful fulfillment of the terms of the contract or should it be accounted as a

leasehold land?

5. A company follows the accounting policy to charge to revenue all items of small

plant and equipment valuing less than ` 1 lakh. It contends that the accounting policy

is similar to the policy followed by Indian Railways and it is engaged in the same

business activities as the Indian Railways.

Whether the company’s accounting policy of charging small value items to revenue

is in conformity with IAS 16?

6. Company X is engaged in the manufacture of diversified value added jute products to

cater to the international market. For manufacture of such items, the company has

been carrying out continuous modernisation and renovation of its plant and

machinery by replacing major components on a regular basis. The components

generally have a useful life different from the machinery to which they relate. This

routine replacement increases the standard performance of the machine, maintained

efficiency in production and has increased the economic lives.

Should the expenses incurred on renovation charged to revenue as normal repairs or

should be treated as an addition to Plant & Machinery?

7. Company A has installed 2 turbines; 1 of which will produce energy for the plant, the

other will be used as a backup in case the 1st turbine fails or is otherwise rendered out

of service. The probability that the spare turbine actually will be used is very low,

however, the spare turbine is necessary to ensure the continuity of the production

process if the 1st turbine fails. The useful life of the stand-by turbine will equal the

life of the plant, which is the same as the useful life of the primary turbine. What

should be the accounting treatment and depreciation for the 2 turbines?

Case Studies Page 3

8. Company Z acquires land for its projects from a land owner in accordance with a

Land Acquisition Act. The affected land owner if aggrieved by the compensation

awarded may make a reference to court. If court awards enhanced compensation,

interest is payable from the date the company gets possession of land till the enhanced

amount is deposited in the court.

Whether interest paid is eligible for capitalisation by company Z?

9. Green-Dart Logistics Ltd. has acquired a heavy road truck at cost of ` 35 lakhs (with

no breakdown of the component parts). The estimated useful life is 10 years. At the

end of the sixth year, the power unit requires replacement, as further maintenance is

uneconomical due to the off- road time required. The remainder of the vehicle is

perfectly roadworthy and is expected to last for the next four years. The cost of a new

power unit is ` 5 lakhs. The original invoice for the transporter did not specify the

cost of the power unit.

How would the replacement cost of the power unit be treated?

10. Queen fisher Airways, an aviation company, acquired an aircraft for ` 15 crores. The

aircraft is expected to have life of 10 years. Queen fisher Airways is required to have

aircraft inspected every three years to ascertain whether they are travel-worthy.

Without the inspection, which requires a high degree of expertise, Queen Fisher

Airways cannot operate the aircraft. The cost attributable to inspection is ` 50 lakhs.

Queen fisher acquired the aircraft on the previous inspection, which was carried out

on 1 April 2007, As at 1 April 2010, Queen fisher Airways incurred `55 lakhs as the

cost of the new inspection.

How would the inspection cost be treated?

11. At 1st Jan. 2000, Mr. A bought office premises at `5 crores. Mr. A aimed to use it for

40 years until the end of its estimated useful life. The original estimated residual

value is `25 lakhs. Depreciation is calculated on a straight-line basis. At 31 Dec.

2009, the depreciated historical cost (and carrying amount) of the property was

`11.87 lakhs.

Case Studies Page 4

The price of similar premises today is about `7 crores. Can A revise the residual

value?

If A changes its intention and aims to dispose of the flat in 10 years, can it revise the

residual value?

12. At the beginning of the year the entity, domiciled in the India, has a $1m foreign

currency loan. The interest rate on the loan is 4% and is paid at the end of the period.

An equivalent borrowing in local ` currency would carry an interest rate of 6%. The

spot rate at the beginning of the year is `1 = US$ 1.55 and at the end of the year it is

`1 = US$ 1.50.

13. X Ltd acquired machinery from USA by raising ECB loan of USD 10 Mn. In

pursuance of the amendment to AS 11 (vide MCA notification dated 31st March

2009), the company capitalised exchange fluctuation of ` 20 lakhs towards the

fluctuations arising in 2007-08 and 2008-09. Discuss the implications of the above for

a company implementing IFRS.

14. X Ltd follows calendar year as its accounting year. In Nov 2009, it acquired machine

tools for ` 15 lakhs having a life of 9 months. Discuss the accounting treatment of the

above.