Embed Size (px)

Citation preview

1

Property Investment Decision-Making Behaviour in Urban

Post-Disaster Rebuild: A Theoretical Perspective

By

Ikenna Chukwudumogu & Prof. Deborah Levy

ABSTRACT

This paper which is part of an ongoing Doctoral research expands our theoretical knowledge

on the interactions, processes and factors that influence the decision-making behaviour of

private stakeholders (investors, developers and agents) in a post-disaster rebuild environment.

By exploring their attributes and relationship, we can achieve an in-depth understanding of

the unique and complex challenges faced by private property stakeholders after a major

disaster that requires massive rebuilding over a long term.

Post-disaster rebuild poses unique challenges and questions for property stakeholders and

institutions. This study takes a theoretical approach to look at these issues around

participation and decision-making behaviour, which is considered fundamental to long-term

post-disaster recovery (Manyena, 2006; Chang et al. 2010). The work presented in this paper

is a literature-based theoretical exploration and framework of an on-going doctoral research.

This paper takes a broadly theoretical approach to champion the need for a deeper

understanding of decision-making behaviour in urban disaster recovery through the lens of

property stakeholders and institutions such as investors, developers and agents. It is necessary

to engage this viewpoint because the implications of large scale disasters on the long-term

recovery in the commercial property market have not yet been substantially explored

2

INTRODUCTION AND OBJECTIVES

This study looks into the distinctive perceptions and decision-making behaviour of private

property stakeholders in an urban post-disaster rebuild environment. Decision-making

behaviour within the property market is shaped by the interactions of psychological, social,

cultural, institutional, political and economic processes at work within the local community

(Jackson et al. 2006 & McGregor et al. 2008). Thus, the links between post-disaster rebuilding

and the decision-making behaviour of property investors and developers merit further

attention.

The ongoing post-disaster rebuild of the Christchurch city centre rebuild presents a unique

platform for this paper. After the 2010 & 2011 earthquakes in Christchurch, property owners

and investors in the city centre were faced with unexpected and challenging decision on what

next to do. Whether to receive insurance compensation and invest elsewhere or stay back

and be a part of the rebuild. Although the rationale behind such decision-making behaviour

is typically complex, a theoretical concept is adopted based on preliminary discussions with

some property stakeholders.

Traditionally, when trying to understanding property investment markets researchers tend to

take a positivist approach and assume rational decision-making behaviour. Alternatively, non-

positivist approaches can also be used to explain the behaviour of stakeholders and this

allows us to discover the importance of social structures and processes lying beneath the

surface (Levy & Lee, 2009). In an attempt to understand the behaviour and actions of property

investors and developers Werlen, (1993), Guy & Heneberry, (2000) demonstrated the

usefulness of institutional approach and analysis by explaining it as a “methodological impulse

to unpack” the “competing ways” in which different players in the market (e.g developers,

investors, architects, financiers and agents) see and act. These individual experiences thus act

as the “frames of reference” of the individual players. In this regards, Studies such as Levy &

Schuck (1999, 2005); Levy, Murphy & Lee (2008); Ohman, Soderberg & Westerdahl (2013)

have adopted non-positivist approaches to increase understanding the property investment

markets. This paper utilizes a similar context to explore the social processes that exist among

3

private investors and developers participating in post-disaster rebuild through the lens of

property agents.

The paper will contribute to the academic literature by expanding our understanding of the

role played by private property stakeholders and institutions who represent an integral part

of urban post-disaster rebuilding. Shaw, (2003) and Wu & Lindell, (2004) suggest that the

rebuilding phase may be one of the most demanding forms of activity after a major disaster,

because it operates in unprecedented and complex conditions.

4

REVIEW OF LITERATURE

PROPERTY INVESTMENT MARKET BEHAVIOUR - A MAINSTREAM ECONOMICS INTERPRETATION A majority of the literature on decision-making behaviour in the property investment market

often reflects rational, normative models that treat behaviour as highly structured and

formalised (Galimore et al. 2000). But by contrast, behavioural psychology suggest that

individuals can act sub-optimally and this is often a neglected aspect of property investment

decision-making research. The post-disaster rebuild environment is perceived as dynamic and

quite chaotic. Therefore, a lot of property decision-making behaviour are not entirely rational

and will be subject to factors such as heuristics, sentiments, biases, passion, emotions and

fear.

The bulk of literature in this regard are positioned within the standard assumption of

mainstream or neo-classical economics (Ohman, Soderberg & Westerdahl, 2013). This idea is

based on the rationale that decision makers with stable preferences are acting in a perfect

market with many competitors, accessible information and homogenous products. The

practices of property professionals and stakeholders are most times based on these

conventional assumptions, which consists of paradigms inherited from both economics and

finance disciplines (Diaz III, 1999). A majority of this type of literature on the property

investment market according to Diaz III, (1999, p. 327) are “…theoretically underpinned by the

rational man construct and the efficient market hypothesis and uses regression-based

econometric techniques…” to analyse price and quantity.

5

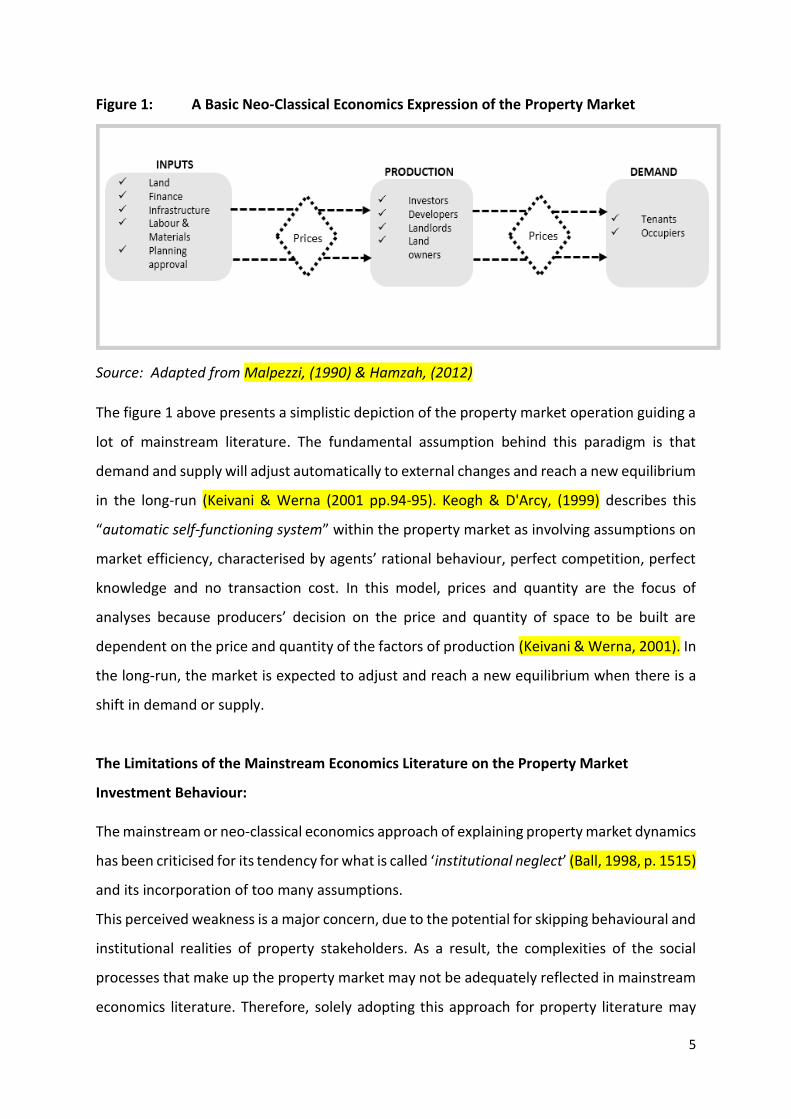

Figure 1: A Basic Neo-Classical Economics Expression of the Property Market

Source: Adapted from Malpezzi, (1990) & Hamzah, (2012)

The figure 1 above presents a simplistic depiction of the property market operation guiding a

lot of mainstream literature. The fundamental assumption behind this paradigm is that

demand and supply will adjust automatically to external changes and reach a new equilibrium

in the long-run (Keivani & Werna (2001 pp.94-95). Keogh & D'Arcy, (1999) describes this

“automatic self-functioning system” within the property market as involving assumptions on

market efficiency, characterised by agents’ rational behaviour, perfect competition, perfect

knowledge and no transaction cost. In this model, prices and quantity are the focus of

analyses because producers’ decision on the price and quantity of space to be built are

dependent on the price and quantity of the factors of production (Keivani & Werna, 2001). In

the long-run, the market is expected to adjust and reach a new equilibrium when there is a

shift in demand or supply.

The Limitations of the Mainstream Economics Literature on the Property Market

Investment Behaviour: The mainstream or neo-classical economics approach of explaining property market dynamics

has been criticised for its tendency for what is called ‘institutional neglect’ (Ball, 1998, p. 1515)

and its incorporation of too many assumptions.

This perceived weakness is a major concern, due to the potential for skipping behavioural and

institutional realities of property stakeholders. As a result, the complexities of the social

processes that make up the property market may not be adequately reflected in mainstream

economics literature. Therefore, solely adopting this approach for property literature may

6

inadvertently provide an obscured view of the process and not accurately reflect actual

property market behaviour.

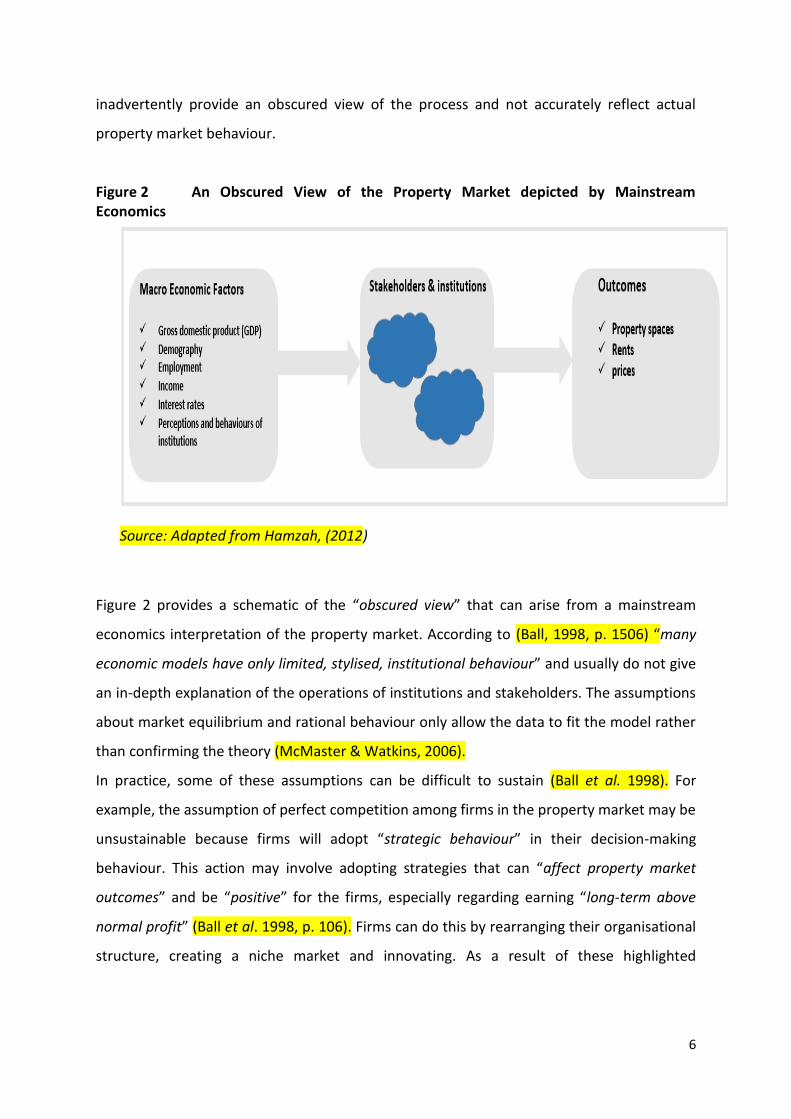

Figure 2 An Obscured View of the Property Market depicted by Mainstream Economics

Source: Adapted from Hamzah, (2012)

Figure 2 provides a schematic of the “obscured view” that can arise from a mainstream

economics interpretation of the property market. According to (Ball, 1998, p. 1506) “many

economic models have only limited, stylised, institutional behaviour” and usually do not give

an in-depth explanation of the operations of institutions and stakeholders. The assumptions

about market equilibrium and rational behaviour only allow the data to fit the model rather

than confirming the theory (McMaster & Watkins, 2006).

In practice, some of these assumptions can be difficult to sustain (Ball et al. 1998). For

example, the assumption of perfect competition among firms in the property market may be

unsustainable because firms will adopt “strategic behaviour” in their decision-making

behaviour. This action may involve adopting strategies that can “affect property market

outcomes” and be “positive” for the firms, especially regarding earning “long-term above

normal profit” (Ball et al. 1998, p. 106). Firms can do this by rearranging their organisational

structure, creating a niche market and innovating. As a result of these highlighted

7

shortcomings, there have been growing interests on how best to robustly explain the

decision-making behaviour of investors and developers.

A BEHAVIOURAL AND INSTITUTIONAL DIMENSION TO THE PROPERTY INVESTMENT MARKET As already pointed out, a significant proportion of mainstream literature on property

investment market adopt a positivist methodology that emphasises the application of rational

decision-making techniques and maximising utility within an economics paradigm (Guy &

Henneberry, 2000). While this approach has considerably increased our knowledge and

understanding of how property investment market works, it only offers a limited view of what

happens. Guy & Henneberry, (2000) have advocated for a more methodological and

theoretical approach that focuses on understanding the wider institutional and behavioural

components of the property market.

The property market comprises a network of actors with unique roles and distinct economic

behaviours in different circumstances depending on their organisational objectives (Ball,

1986, 2003, 2006, 2010). Some of these actors may include planners, investors, developers,

agents, government departments, financial institutions, landowners, (Ball, 1986). At a local

level, the disaggregation of the property markets and other pre-existing conditions tends to

moderate the activities of these actors (e.g. the political, social, economic and legal

institutions) as well as policies designed to influence them. In essence, the behavioural and

institutional examination can provide a harmonising effect on other theoretical approaches

adopted in property research.

Contemporary literature examining property decision-making suggests that the main-steam

economics explanation may accurately reflect the decisions of property market participants

(Soderberg and Westedahl, 2013). This study views decision-making behaviour is been shaped

by sentimental factors that are inherent to a post-disaster environment where there is a long

period of uncertainty and risk due to the “shock effect” of the disaster.

8

A Behavioural Context to the Property Investment Market:

While mainstream studies make several assumptions about the property markets, especially

on how to model them as a critical question, the alternative will be to observe how markets

are formed (Smith et al. 2006). In other words, the focus should be on the practices of

property stakeholders by acknowledging the specifics of the property market as simply

market fundamentals rather than property market imperfections (Soderberg and Westerdahl,

2013). A review of behavioural property research by Diaz III (1999), Diaz III & Hansz (2007)

and Wofford et al. (2010) all suggest that property investment research paradigms be aligned

with the management of risks associated with human cognitive abilities. Furthermore, French

& French (1997), De Bruin & Flint-Hartle (2003) also highlight that there are potential

limitations in the standard finance and economics-based models for analysing property

investment behaviour.

When it comes to research on property investment market behaviour, there have been

studies on various aspects of investment strategies for property investors. Adair et al. (1994)

examine attitudes to investment diversification and risk about property type, location, market

knowledge and transparency. They observe a mismatch between perceptions of investment

attraction and actual investment behaviour. As a result, investment analysis is highly

quantitative and empirical, so most investments are directed to sub-markets with adequate

information on market conditions. An analysis of market selection criteria and the decision-

making behaviour of international investors by Worzala & Newell (1997) and Falkenbach

(2009) showed that although diversification was an important rationale, certain investment

criteria are found to be threshold conditions, which indicates a bounded rational behaviour

(De Bruin & Flint-Hartle, 2003). Gallimore & Gray (2002) have also emphasised that decision

makers consider investor sentiments as an important form of information to be used

alongside other market fundamentals.

Soderberg & Westerdahl, (2013) identified that most property literature have shown very

little qualitative based studies that examine investment behaviour in the commercial

property market. For example, Gallimore et al. (2000) undertook a semi-structured interview

of investment property directors of fairly small property companies in the UK market. They

found that the decision-making behaviour of companies did not necessarily align with

standard quantitative descriptions. At the same time, investors mainly conduct satisficing,

9

rather than optimising behaviour in search for investment opportunities and market

information (Gallimore et al. 2000). Henneberry and Roberts, (2008) have also attributed

“calculative practices” and the “IPD benchmarking system” as reasons for irrational

behaviours. This system does not take a passive role in measuring and understanding the

market but instead helps shape the market. Consequently, they assert that the economy

cannot be considered “rational” in the sense assumed in mainstream economics.

An Institutional Context to the Property Investment Market:

Ohman, Soderberg & Westerdahl, (2013) suggest that mainstream studies re-apply the

institutional paradigm established by some of the pioneers of modern property research such

as Ratcliff (1972). Nevertheless, in a dominant environment of finance and economics-based

models, such application become isolated and provides little guidance for empirical research.

Hodgson (2006, p.2), defines institutions from an economics perspective as "… systems of

established and prevalent social rules that structure social interactions…”. He identifies a

distinction between ‘organisations’ and ‘institutions’ where organisations constitute entities

whilst institutions entail social rules, organisations may however also constitute institutions

in some cases (Hodgson, 2006, pp. 17-18). Ball et al (1998) concurred with this definition of

organisations as ‘players’ and institutions incorporating the ‘rules of the game’ and went

further by compressing the two concepts into just ‘institutions’ in their work.

This paper recognises a similar “casual approach to defining institutions” as “it is the easiest

approach and corresponds to common sense views on what is an institution” (Ball, 1998, p.

1502). Institutions in real estate encompasses tangible and intangible items such as “…a

characteristic group (e.g. developers, landowners, agents, financiers), a practice (e.g.

surveying, accountancy), a process (e.g. town planning, the process of law), a building that

has a special, well-established place in society (e.g. a hospital, school, prison), a characteristic

grouping of organisations (e.g. financial institutions, the Church), a sociological phenomenon

(e.g. the institution of marriage), an enduring body of settled doctrine employed to regulate

different legal relations, as in the ‘institution of property’.” Seabrooke & Hebe (2004, pp.9-

10). This institutional approach is particularly valid as reflected in Hodgson (1998, p.180),

which states that the study of institutions involves the examination of "human activity partly

through the continuing production and reproduction of habits of thought and action".

10

Hodgson (2000, p.327), also acknowledges the importance of focusing on the individual

whereby "the individual is moulded by social and institutional circumstances". The

examination of ‘human habits’ is underpinned by the belief that the market in itself does not

represent the overall economy (Samuels, 1995).

THE PROPERTY INVESTMENT AND DEVELOPMENT MARKET IN URBAN POST-DISASTER/REGENERATION. Conceptually, urban regeneration is a process of reversing economic, social and physical

decay in towns and cities where market forces alone will not suffice (Adair et al. 1999, p.

2031). It entails the perception of a declining inner-city that incorporates a process of physical

regeneration to establish a basis for economic growth and social well-being (Healey et al.

1992). On the other hand, urban post-disaster recovery as a concept still lacks any

authoritative definition with a definite aim, content and characteristics (Lizarralde, 2004; Yi &

Yang, 2014). The lack of definition is attributable to the fact that most of the literature on

post-disaster recovery has been relatively smaller when compared to traditional research

topics in the built environment and property regarding the intent, process and results (Yi and

Yang 2014). Nevertheless, some terms have been adopted to suit the framework of specific

research on related issues (Chang, 2013; Yi and Yang, 2014). A number studies have

somewhat discussed this concept in the context of post-disaster reconstruction (Chang et al.

2010); Post-disaster recovery (Alexander et al. 2006); post-disaster rebuilding (Olshansky, et

al. 2006); post-disaster redevelopment (Simunovich, 2008); and even urban regeneration

(Adair et al. 1999 & 2000). Yi and Yang (2014), suggests that there may be some subtle

differences between these concepts, but so far there are no reported comparisons or

contrasts.

This paper adopts a premise that there are unique similarities between the concept of urban

regeneration and urban post-disaster rebuilding, which has already being explained earlier.

As such, engaging with this literature has assisted in informing the study objectives. An

integral part of the urban regeneration literature involves understanding the role of the

private stakeholders concerning stimulating property investment and development (Adair et

al. 1999 and Nappi-Choulet, 2006).

11

The Behaviour of Private Investors and Developers in Urban Regeneration

Studies by McGreal et al. (2000), Adair et al. (1998 & 2003) and Nappi-Chouplet, (2006)

indicate that perceived total investment returns remain a primary influence on property

investment and development decisions. In a similar vein, Nappi-Chouplet (2006) also found

that the involvement of institutional property developers in the urban regeneration of the

Paris region of France was dependent on their ability to attain high returns on investment and

that the internal rate of return (IRR) was the main criteria for investment decision-making.

This influence is due to the requirement of above average returns on investments necessary

for addressing viability concerns. There are also other identifiable factors that are important

considerations for any investment decision and these include investment security, risk spread

and the potential for rental and capital growth McGreal et al. (2000).

Adair et al. (1998 & 2002), emphasised that private sector investment is opportunity driven

and needs to show returns commensurate with the risk and return profile of participants.

Therefore, efficient and a receptive property market is essential to lever investment into

urban regeneration locations. Adair et al. (1998), also highlights that typical institutional

investors set very high criteria for compensating risks when considering any investment in

urban regeneration location due to higher uncertainty. This perception translates into the

demand for a higher risk premium reflecting the seemingly poorer physical and locational

characteristics of many urban regeneration areas. Consequently, there is a psychological

preference for safer investment choices perpetuates certain misconceptions about urban

regeneration areas such as low returns, weak demand and high costs Adair et al. (1998 &

2002).

Adair et al. (1998 & 2003 p.2032) highlight some of the anecdotal perceptions of investors in

urban regeneration locations to include;

Investors perceive urban regeneration sites as offering weak investment opportunities

due to the potential for a high risk and low return profile. Therefore, new and

innovative measures such as financial and non-financial incentives are necessary to

attract private investment

The primary driver for investment in urban regeneration projects is the risk-adjusted

return and limited availability of alternative property investment

12

Investors only adopt specific decision-making parameters to urban regeneration

investments such as seeking higher returns over of what is achievable in prime

locations

There may be some downsides to these perceptions because by placing too much emphasis

on the prospects of financial viability, investors may miss any potential investment

opportunity that may come from urban regeneration locations. In a final analysis, Nappi-

Chouplet (2006) and Tranch & Green (2001) are of the opinion that smaller local investors

and developers have the advantage of intimate knowledge of the local market and close

relationship with local authorities and clients. On the other hand, this contrasts with the

decisions of institutional investors who respond to complex extrinsic factors before making

an investment decision in a particular location.

13

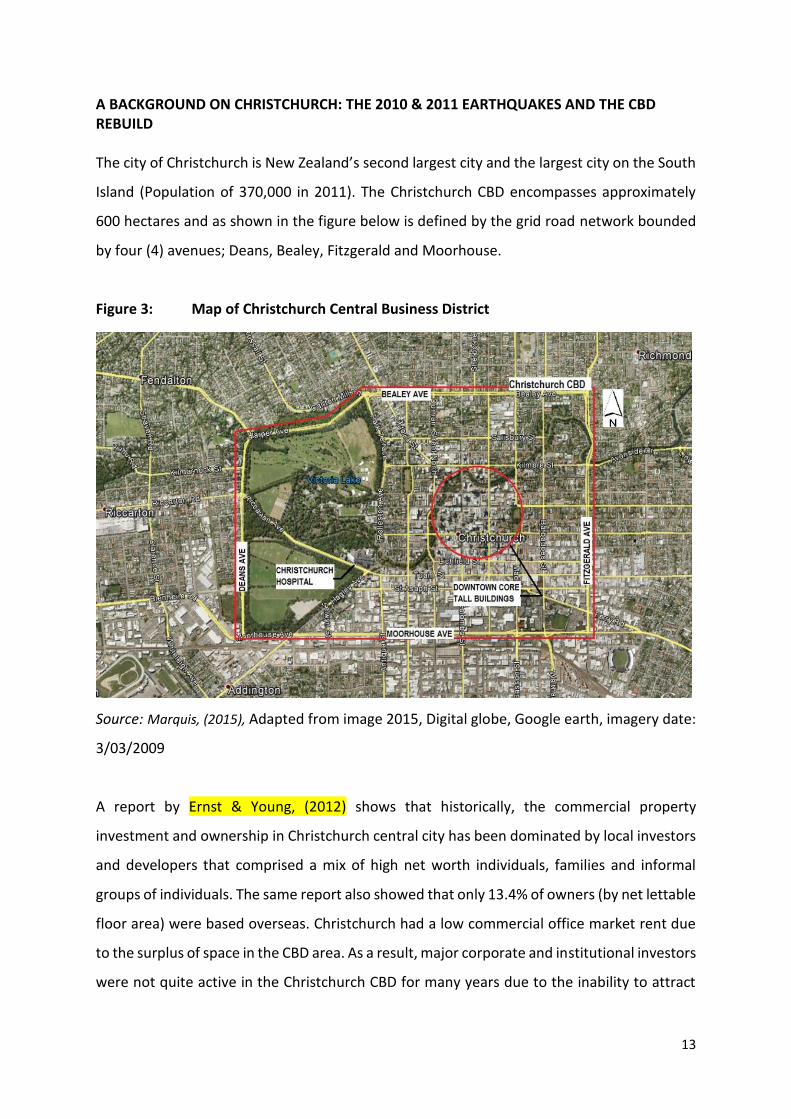

A BACKGROUND ON CHRISTCHURCH: THE 2010 & 2011 EARTHQUAKES AND THE CBD REBUILD The city of Christchurch is New Zealand’s second largest city and the largest city on the South

Island (Population of 370,000 in 2011). The Christchurch CBD encompasses approximately

600 hectares and as shown in the figure below is defined by the grid road network bounded

by four (4) avenues; Deans, Bealey, Fitzgerald and Moorhouse.

Figure 3: Map of Christchurch Central Business District

Source: Marquis, (2015), Adapted from image 2015, Digital globe, Google earth, imagery date:

3/03/2009

A report by Ernst & Young, (2012) shows that historically, the commercial property

investment and ownership in Christchurch central city has been dominated by local investors

and developers that comprised a mix of high net worth individuals, families and informal

groups of individuals. The same report also showed that only 13.4% of owners (by net lettable

floor area) were based overseas. Christchurch had a low commercial office market rent due

to the surplus of space in the CBD area. As a result, major corporate and institutional investors

were not quite active in the Christchurch CBD for many years due to the inability to attract

14

high rent tenants. In this regards, the economics context prior to the earthquakes may have

influenced decision-making behaviour in a post-disaster environment.

Figure 4: Commercial (Office) ownership profiles in Christchurch before February,

2011

Source: Ernst & Young (2012)

The earthquake events of 2010 and 2011 in Christchurch was a catastrophe of enormous

proportions and the New Zealand Treasury put the cost of damage at about 10% of national

G.D.P (Bollard & Ranchhod, 2011). The New Zealand budget policy statement of 2012 stated

that the Christchurch rebuilding will, without a doubt, be the biggest economic undertaking

in New Zealand’s history (Brook 2012). In fact, the New Zealand government did indeed fear

for the worst and worried that the second biggest city in the country might simply implode

from the shock (McCrone, 2014). The city was well insured, the local economy did not entirely

collapse as initially feared (Brown, et al 2013). This advantage was attributed to the fact that

New Zealand has one of the highest insurance penetration rates in the world (Brown, Seville

& Vargo 2013; CBRE, 2012).

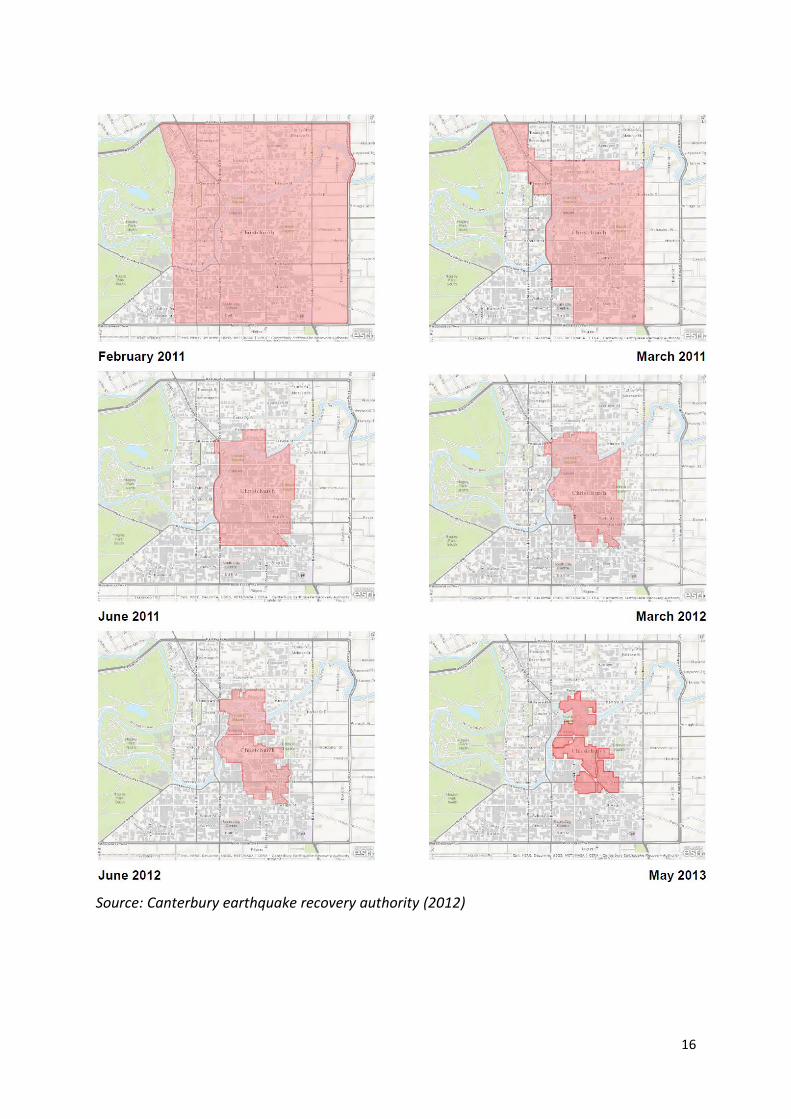

The government declared a state of national emergency and Civil Defence became lead

agency, with a cordon established around the CBD area. Chang et al. (2014) provides a

detailed description of the impacts of the CBD cordon which had been reduced to about half

its original size by July 2011 and removed entirely in June 2013. The Figure below shows the

15

extent of the CBD cordon at various timeframes, which was also prolonged by the continued

aftershocks.

Figure 5: Extent of central business district cordon, February 2011 to May, 2013:

16

Source: Canterbury earthquake recovery authority (2012)

17

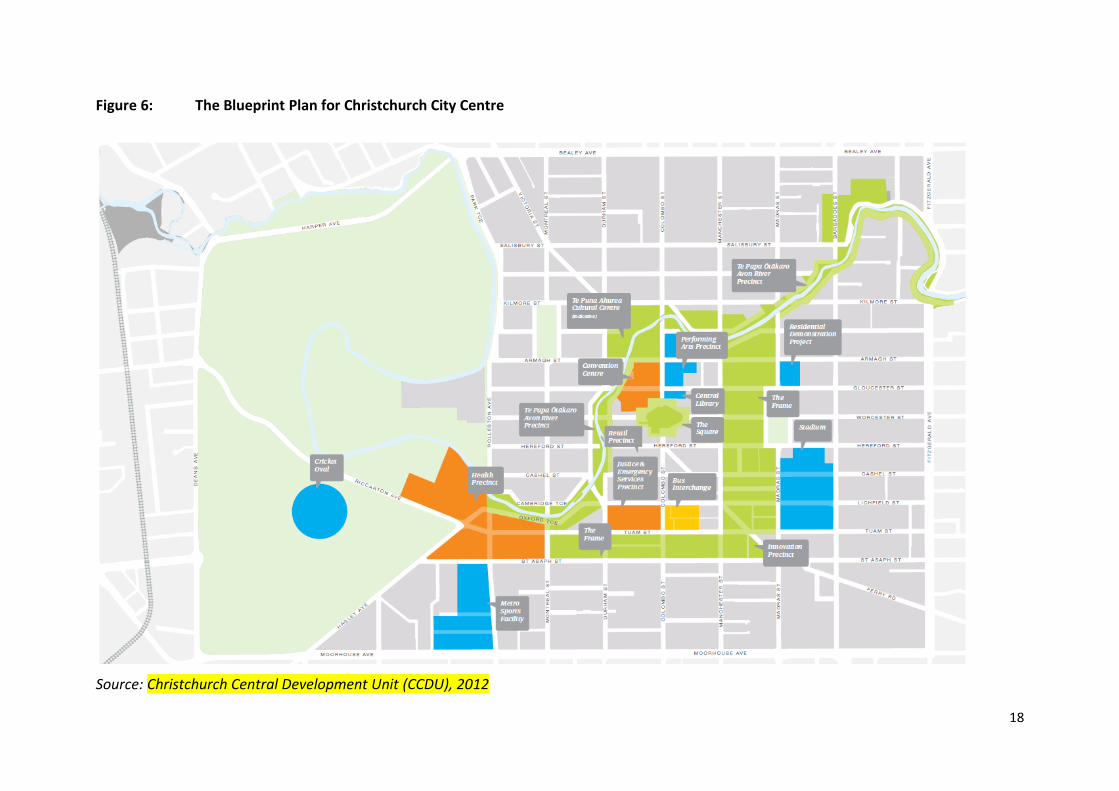

Generally, compelling and sometimes controversial decisions were taken such as cordoning

the central business district; residential zoning; creation of the Canterbury Earthquake

Recovery Authority (CERA) & Christchurch Central Development Unit (CCDU); developing of

the Christchurch central recovery plan also known as “The Blueprint” shown in figure 6 have

been made by the government after the earthquakes (Chang et al 2012; Rodrigues, 2012).

These decisions were made to bring some level of confidence and certainty among potential

private property stakeholders who would engage in the post-disaster rebuild (Taylor, 2013).

The Christchurch Central City Blueprint took off in 2012 as shown in figure 6 below was

considered a bold choice that would spearhead the post-disaster rebuild in Christchurch City

Centre by providing a clear direction for collaboration between the private and public sector

(JLL, 2012). However, it has most times fallen short of inspiring confidence among property

stakeholders and this has been attributed to a lack of coordination, governance and inefficient

procurement in the overall implementation of the Christchurch city centre blueprint (NZCID,

2013). Studies by (McCrone, 2014; NZCID, 2013) show that the implementation of the central

city Blueprint may not live up to the high expectations and in fact, the post-disaster recovery

in Christchurch city centre has sometimes stalled on different occasions since the rebuild

started. Their studies also acknowledged the failure of the Christchurch central city Blueprint

to inspire initial confidence among property stakeholders. Some of the identified reasons for

this included but not limited to;

Historical political tensions between local city council and the business community;

The amalgamation of national government agencies and departments with elected

city council to form the Christchurch central development Unit (CCDU);

Failure to impose moratorium on the approval for commercial developments outside

the city centre and suburban locations;

The decision by the Christchurch central development Unit (CCDU) to force the

agglomeration of commercial redevelopment in a particular precinct and

The aggressive internal disputes over cost-sharing on anchor projects in the

Christchurch city centre blueprint.

18

Figure 6: The Blueprint Plan for Christchurch City Centre

Source: Christchurch Central Development Unit (CCDU), 2012

19

It is important to note that after a major disaster, there are profound changes that occur with

long-term repercussions on affected locations and this was clearly manifested in the over 90%

of the office space stock lost in the central city of Christchurch due to the earthquakes (Moricz

et al. 2012; Anthony, 2014 and Sellars, 2013). This massive shortfall had a reverberating effect

on the commercial property market because it contributed over two-thirds of the available

stock of office space in the entire Canterbury region (Anthony, 2014).

Property investors and developers may have become extremely cautious to participate in new

projects due to the unique risks and uncertainty they have to take on. In fact, the usual

property investment cycle may become very lopsided and difficult to predict for a very long

time.

A Theoretical Framework on the Decision-Making Behaviour of Property Stakeholders in a

Post-Disaster Rebuild Environment

This paper leans on the argument that the behavioural and institutional approaches can offer

a credible balance to mainstream economic models especially in understanding the decision-

making behaviour of private property stakeholders in a post-disaster environment. The

premise here is that an institutional and behavioural perspective offers a robust contribution

to the literature on decision-making in urban post-disaster rebuild. With this in mind, a

theoretical understanding of the processes in the market through the habits and social

interactions of property stakeholders (investors, developers and agent) in post-disaster

rebuild environment can be developed. Samuels, (1995 p.571) argues that this approach also

yields a “deeper answer” to the phenomenon under study. The knowledge revealed is reliable

“although changes in institutions and working rules occur frequently, they normally change

slowly, through both non-deliberative (for example, habitual and customary) and deliberative

(typically legal) modes” (Samuels, 1995, p. 573).

20

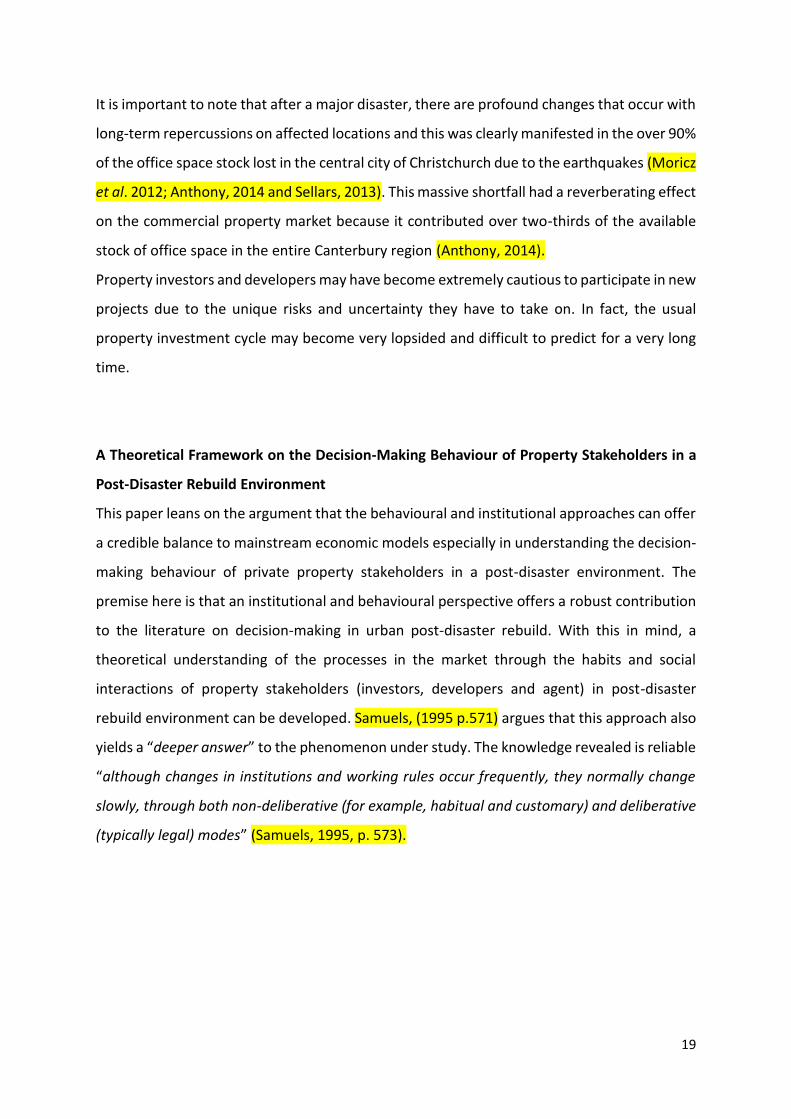

Figure 7 A Transparent View of The Property Market Showing Institutional Dynamics.

Source: Author’s Analysis and Adapted from Hamzah, (2012)

The figure 7 above illustrates how the hidden intricacies of the property market can open up

by engaging the behavioural and institutional dynamics through pre-existing social, economic,

political and legal institutions revealed in the diagram. According to Rosenberg, (1994, p.1),

“by examining the particular sequence of events and institutions within specific industries, one

can extract insights into the process… knowledge of a kind that cannot be deduced from some

mere theoretical framework”.

In other words, property stakeholders will assimilate and interpret these endogenous and

exogenous factors in their operations. These interactions ultimately shape property prices

and space supply and demand, which are critical in a post-disaster environment. The goal of

analysing institutions is usually to offer an in-depth explanation and meaningful insights that

enriches the understanding of property market processes (Ball et al. 1998). By embracing this

approach, insights into the perceptions and decision-making behaviour of private property

stakeholders particularly in a post-disaster environment can be robustly “fleshed out” by

21

posing questions that examine their perceptions and motivations for investment and

development.

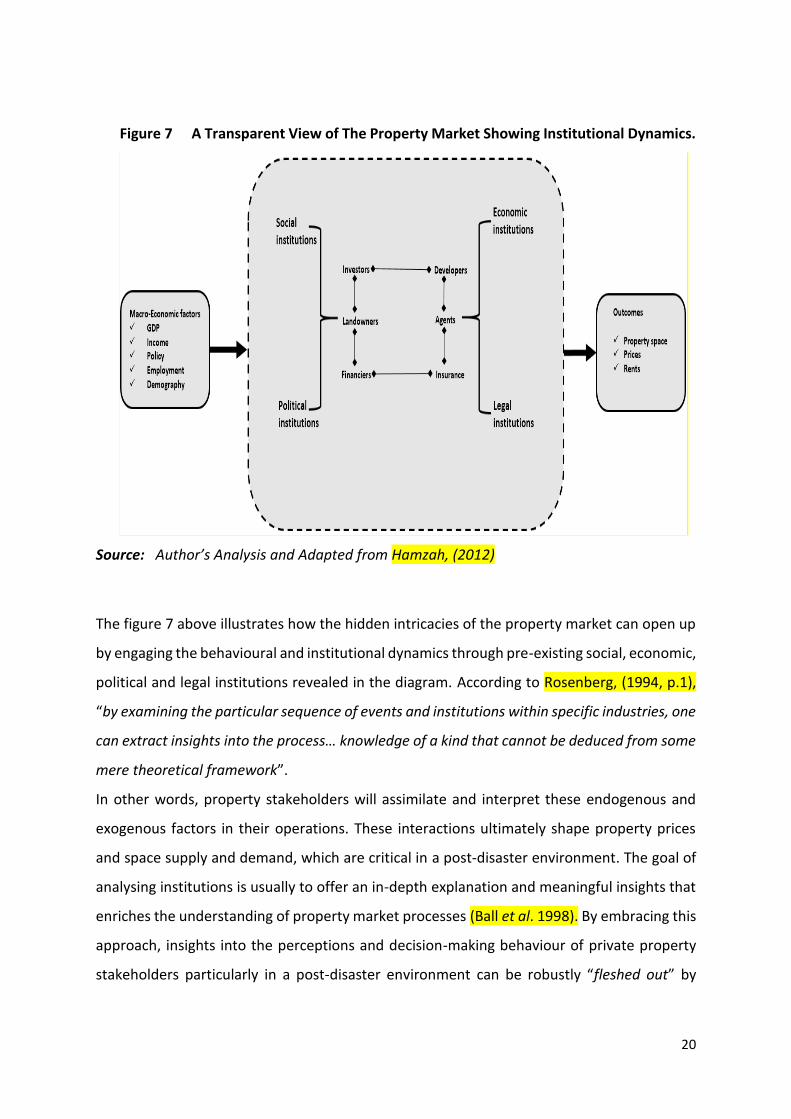

Figure 8: A Decision-Making Framework for Stakeholders in a Post-Disaster

Environment:

Source: Adapted from Egbelakin, (2013)

The framework in the figure 8 above provides a structure on how the literature has

progressed in line with the study objective. By providing an underpinning for this paper, the

literature review has identified a gap area in the decision-making behaviour of private

property stakeholders in a post-disaster rebuild environment. The review of the literature,

suggests that a common theme points to the importance of the social process and

environment that exist among property stakeholders and institutions.

22

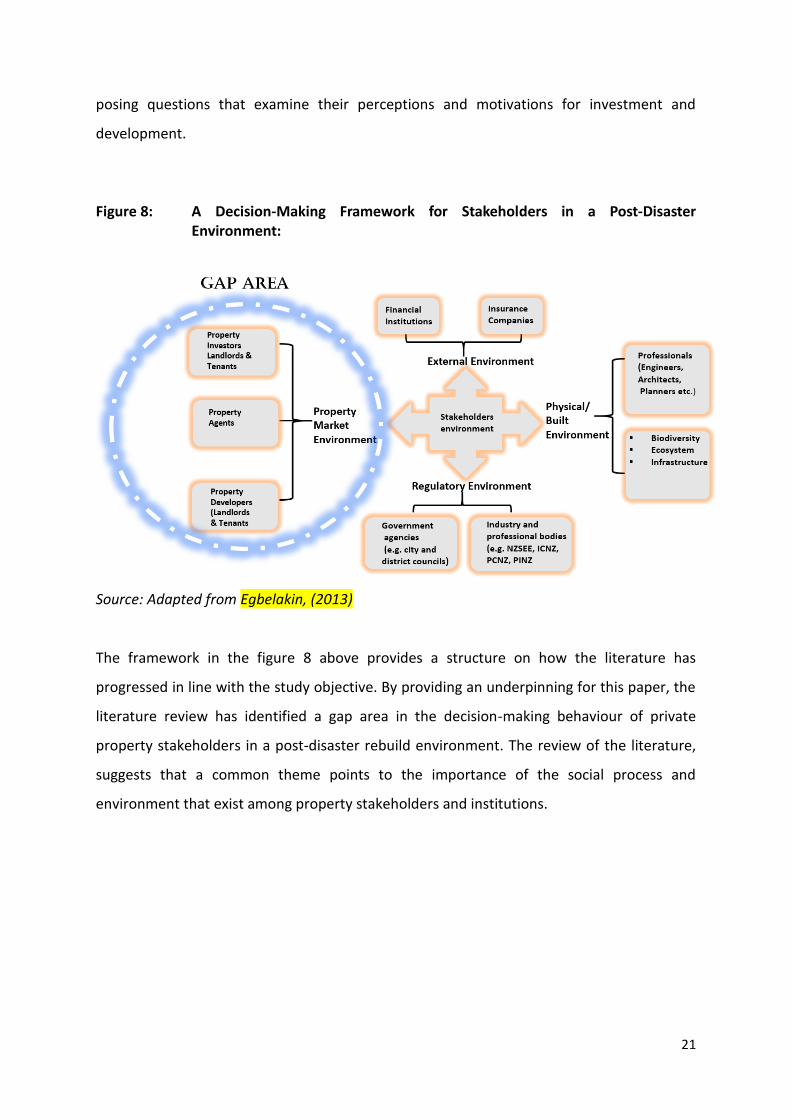

Figure 9: Conceptual Framework

The goal of this literature was to inform the study from a theoretical perspective by putting

into context the general understanding of decision-making behaviour of private property

stakeholders. Therefore, the objective here is to make a unique contribution to the property

literature by providing a robust understanding of this complex social process that influence

decision-making behaviour in an urban post-disaster rebuild environment.

23

CONCLUSION

The objective of this study was to allow for a holistic and deeper understanding of the

decision-making behaviour in a post-disaster rebuild environment through the lens of private

property stakeholders. Although normative models provide an “ideal world” view of

investment, the chaotic nature of the property investment market as visible in a post-disaster

recovery environment appears to preclude any rigid and rational decision-making behaviour.

In this case, individual investors may make decisions based on sentimental factors such as

passion, love, emotion, prestige, limited domain and cognitive powers. In this regards, this

paper provides a valuable insight into the behavioural dynamics of private property

stakeholders (investors, developers and agents) involved in the post-disaster rebuild. Till date

not much has been done in this area of property literature. The purpose of this study

therefore, was to address this shortcoming by developing an a priori view the factors

influencing the decision-making behaviour of property investors and developers involved in

the post-disaster rebuild of Christchurch city centre through the lens of agents who represent

a vital link among property stakeholders.

24

REFERENCES & BIBLIOGRAPHY

Adair, A., Berry, J., & McGreal, W. (1994). Investment decision making: A behavioural perspective. Journal of Property Finance, 5(4), 32-32. Adair, A., Berry, J., McGreal, S., Deddis, B., & Hirst, S. (1999). Evaluation of investor behaviour in Urban regeneration. Urban Studies, 36(12), 2031-2045. Adair, A., Berry, J., McGreal, S., Deddis, B., & Hirst, S. (2000). The financing of urban regeneration. Land use Policy, 17(2), 147-156. Adams, D. (1994) Urban Development and Planning. UCL Press, London. Anthony, K. (2014). Christchurch office market: There and back again. CBRE Ball, M. (1998). Institutions in British property research: A review. Urban Studies, 35(9), 1501-1517. Ball, M., Lizieri, C. & MacGregor, B. (1998). The Economics of Commercial Property Markets. Routledge, London. Bollard, A., and S. Ranchhod. (2011) Economic impacts of seismic risk: lessons for Wellington. Speech delivered to the Rotary Club of Wellington and Victoria University of Wellington one day conference 'Organisational Effectiveness in Times of Seismic Risk'. Brook, A. M. (2013). Making fiscal policy more stabilising in the next upturn: Challenges and policy options. New Zealand Economic Papers, 47(1), 71-94. Brown, C., Seville, E., & Vargo, J. (2013). The role of insurance in organisational recovery following the 2010 and 2011 Canterbury earthquakes. (Research No. 2013/04). University of Canterbury: resilient Organisations. Canterbury Earthquake Recovery Authority (CERA) (2012). Amendments to Christchurch City Council’s District Plan. Updated in July 2013. Christchurch: Canterbury Earthquake Recovery Authority. Available at: http://cera.govt.nz/maps (accessed on the 27th March, 2015) Chang, Y. (2013). Resourcing for post-disaster housing reconstruction. Unpublished PhD, University of Auckland, Auckland, New Zealand. Chang, Y., Wilkinson, S., Brunsdon, D., Seville, E., & Potangaroa, R. (2011). An integrated approach: Managing resources for post‐disaster reconstruction. Disasters, 35(4), 739-765. Chang, Y., Wilkinson, S., Potangaroa, R., & Seville, E. (2010). Resourcing challenges for post-disaster housing reconstruction: A comparative analysis. Building Research & Information, 38(3), 247-2 Christchurch earthquakes. Christchurch Central Development Unit (CCDU) (2012) The Recovery Plan, available at: http://ccdu.govt.nz/the-plan (accessed on the 27th February, 2016). De Bruin, A. and Flint-Hartle, S. (2003), “A bounded rationality framework for property investment behaviour”, Journal of Property Valuation & Investment, Vol. 21 No. 3,

25

Diaz III, J. (1999). The first decade of behavioural research in the discipline of property Journal of property investment & finance, 17(4), 326-332. Diaz, J. III and Hansz, J. (1997), “How valuers use the value opinion of others”, Journal of Property Valuation and Investment, Vol. 15 No. 3, pp. 256-60. Diaz III, J., & Hansz, A. (2007). Understanding the behavioural paradigm in property research. Pacific Rim Property Research Journal, 13(1), 16-34. Egbelakin, T., K. (2013). Incentives and motivators for enhancing earthquake risk mitigation decision. (PhD, University of Auckland). Ernst and Young (2012) CERA Christchurch Central City - Commercial Property Market Study. Released by the Minister for Canterbury Earthquake Recovery. May 2012. French, N. and French, S. (1997), “Decision theory and real estate investment”, Journal of Property Valuation & Investment, Vol. 15 No. 3, pp. 226-232. Gallimore, P. and Gray, A. (2002), “The role of investor sentiment in property investment decisions”, Journal of Property Research, Vol. 19 No. 2, pp. 111-120. Gallimore, P., Hansz, J.A. and Gray, A. (2000), “Decision making in small property companies”, Journal of Property Valuation & Investment, Vol. 18 No. 6, pp. 602-612. Goulding, C. (1998), “Grounded theory: the missing methodology on the interpretivist agenda”, Qualitative Market Research: An International Journal, Vol. 1 November, pp. 50-7. Guy, S. & Henneberry, J. (2000) Understanding urban development processes: integrating the economic and the social in property research. Urban Studies, 37(13), 2399-2416. Guy, S., Henneberry, J. and Rowley, S. (2002) Development cultures and urban regeneration, Urban Studies, 39(7), pp. 1181–1196. Henneberry, J. & Rowley, S. (2002) Property market processes and development outcomes in cities and regions. RICS Research Foundation Research Papers, 3(9), 1-59. Henneberry, J. (1999) Convergence and difference in regional office development cycles. Urban Studies, 36(9), 1439-1465. Henneberry, J. and Roberts, C. (2008), “Calculated inequality? Benchmarking and regional office property investment in the UK”, Urban Studies, Vol. 45 Nos 5/6, pp. 1217-1241. Hodgson, G. M. (1998). The approach of institutional economics. Journal of Economic Literature, 36(1), 166-192. Hodgson, G. M. (2006). What are institutions? Journal of Economic Issues, XL (1), 1-25. Jackson, J., N. Allum and G. Gaskell (2006). Bridging levels of analysis in risk perception research: the case of the fear of crime.

26

Jones, L., Lasalle. (2013) Rome wasn’t built in a day: Christchurch retail, red zones and the rebuild. Retrieved from http://www.propertynz.co.nz/media/wysiwyg/pdf/justin_kean_jll.pdf Jones, L.L. (2012) Christchurch rethink, revitalise and renew. Retrieved from http://www.jll.co.nz/new-zealand/en-gb/research/166/christchurch-rethink-revitalise-and-renew Journal of Property Finance, 5(4), 32-32. Levy, D., & Schuck, E. (1999). The influence of clients on valuations. Journal of Property Investment & Finance, 17(4), 380-400. Levy, D.S. and Schuck, E. (2005). The influence of clients on valuations: The clients’ perspective Lizarralde, G. (2004). Organisational System and Performance of Post-Disaster Reconstruction Marquis, F. (2015). A framework for understanding post-earthquake decisions on multi-storey concrete buildings in Christchurch, New Zealand (Doctoral dissertation, UNIVERSITY OF BRITISH COLUMBIA (Vancouver). Maykut, P. and Morehouse, R. (1994), Beginning Qualitative Research: A Philosophical and Practical Guide, Falmer, London. McCRONE, J. (2014). Christchurch rebuild: A city stalled. The Press, New Zealand. McMaster, R., & Watkins, C. (2006). Economics and under determination: a case study of urban land and housing economics. Cambridge Journal of Economics, 30, 901-922. Moricz, Z., Wong, C., & Bond, S. (2012). The impacts of the Canterbury earthquake on the commercial office market. CBRE and Lincoln University. Murphy, L. (2011). The global financial crisis and the Australian and New Zealand housing markets. J House and the Built Environ, 26:335–351. NZ Council for Infrastructure Development" (NZCID). (2013). Insights into Canterbury: Findings of research on the Canterbury earthquakes recovery. New Zealand: NZ Council for Infrastructure Development. doi:http://www.nzcid.org.nz/Category?Action=View&Category_id=217 Ohman, P., Söderberg, B., & Westerdahl, S. (2013). Property investor behaviour: Qualitative analysis of a very large transaction. Journal of Property Investment & Finance, 31(6), 522-544. Ratcliff, R.U. (1972), Valuation for Real Estate Decisions, Democrat Press, Santa Cruz, CA. Roberts, C., & Henneberry, J. (2007). Exploring office investment decision-making in different European contexts. Journal of Property Investment & Finance, 25(3), 289-305. Rodrigues, A. J. (2012) Factors influencing the reconstruction of commercial buildings following the Rosenberg, N. (1994). Exploring the black box: Technology, economics and history. Samuels, W. J. (1995). The present state of institutional economics. Cambridge Journal of Economics, 19, 569-590.

27

Satsangi, M. (2011). Feminist epistemologies and the social relations of housing provision. Housing, Theory and Society, 28(4), 398-409. Seabrooke, W., & Hebe, H. H. H. (2004). Real estate transactions: An institutional approach. In W. Seabrooke, P. Kent & H. H. H. Hebe (Eds.), International real estate: An institutional approach. Oxford: Blackwell Publishing. Sellars, G. (2013). Property Council New Zealand market summit: The Rebuild. Colliers International. Shaw, R. and Sinha, R. (2003), “Towards sustainable recovery: future challenges after Gujarat earthquake”, Risk Management: An International Journal, Vol. 5 No. 2, pp. 35-51. Smith, S.J., Munro, M. and Christie, H. (2006), “Performing (housing) markets”, Urban Studies, Vol. 43 No. 1, pp. 81-98. Taylor, J.,Elis. (2013). The Christchurch earthquake sequence: Government decision-making and confidence in the face of uncertainty (Master of Arts). Whitehead, C., & Yates, J. (2009). Editorial: Economic methods and their contribution to housing. Housing Studies, 24(1), 1-6. Wofford, L.E., Troilo, M.L. and Dorchester, A.D. (2010), “Managing cognitive risk in real estate”, Journal of Property Research, Vol. 27 No. 3, pp. 269-287. Worzala, E. and Newell, G. (1997), “International real estate: a review of strategic investment issues”, Journal of Real Estate Portfolio Management, Vol. 3 No. 2, pp. 87-96. Wu, J.Y. and Lindell, M.K. (2004), “Housing reconstruction after two major earthquakes: the 1994 Northridge earthquake in the United States and 1999 Chi-Chi earthquake in Taiwan”, Disasters, Vol. 28 No. 1, pp. 63-81.