Embed Size (px)

Citation preview

Property Development Finance Explained: London Edition

www.accumulatecapital.co.uk

IntroductionReal Estate investments have been gaining traction as reliable and profitable avenues to accumulating wealth for decades. Ever-more frequently, investors are drawn towards the attractive diversity of the property market and successfully navigating the abundance of opportunity can be challenging in itself. Thus, the first in a series of important decisions that must be made in relation to this is which option is best suited for you to become involved with. In the same way that purchasing a stock for its surface-value could mask intrinsic issues, the key to making a successful return from real estate is investing in a thoroughly researched, valuable asset.

Debatably, Britain´s fixation with owning property was kick-started by the implementation of the Housing Act 1988. This legislation was implemented to bolster the private rental sector and introduced a series of rights for tenants. One of which was the opportunity to purchase their home. This then evolved into the immensely popular buy-to-let (BTL) property investment scheme. However, in the past few years the property market has seen drastic changes to the regulation of private lease agreements and it has become increasingly difficult to manage the various obstacles introduced over the years. Accumulate Capital recently surveyed over 750 landlords, all of whom own three or more residential properties in the UK. Results revealed that over half (53%) expressed regret towards their initial purchase and professed they would not have invested in the scheme had they foreseen the regulatory challenges that lay ahead. A further 37% expressed an intention to sell at least one of their properties in the near future. Regardless, real estate remains an attractive asset and property investment is still extremely popular. However, landlords are increasingly looking for more lucrative opportunities, one of which is property development finance. The aforementioned research also found that over a fifth of UK landlords (21%) are now leaning towards this investment opportunity, and here we will discuss why.

In the wake of the financial crisis of 2007-2008, banks became far more sceptical and demonstrated a reluctancy when it came to lending money. The onset of familiar financial difficulties for the public economic sector have led property developers to consider alternative funding methods in order to fulfil project demand. From the various innovative funding methods utilised by developers came the evolution of property development finance.

With property finance, developers such as ourselves are able to gain significant funding prior to construction. In our case, the finance is provided by an investor who is given a legal document outlining the terms and conditions, amount of interest to be remunerated and the duration of the investment.

Property development has become an increasingly significant sector, without the finance we provide many projects would not be able to afford the project development process. Therefore, in return for the participation of our network of registered investors we are able to facilitate market-leading returns on their money.

How it Works

The first stage consists of thorough planning and preparation. A property developer decides what terms are achievable and necessary for the construction process, including the amount to be raised, the duration, conditions and interest rates involved with the loan. Their lawyer then drafts the documentation and structures the agreement. The investment opportunity is then offered to high net worth individuals or sophisticated investors by either the developer or a third-party promoter.

Investors loan the developer the required funding on the terms associated with the agreement. Interest payments are made according to the conditions which can either be for the entire duration of the investment or at the end of the term. On completion, the original capital is returned in addition to the remuneration outlined in the terms of the agreement at point of subscription.

What is Property Development Finance?

Despite turbulence to the economy this year activity has risen in the past few months as house prices, especially in London and surrounding arears indicate a buoyant market. According to research accumulated by Nationwide, house prices rose by 0.9% in September in a fairly even spread with the previously mentioned areas increasing by as much as 3% in the third quarter of this year. This strong price growth has been driven by high levels of competition and market activity. In fact, 76% of Surveyors in a recent RICS survey report a vast increase in new buyer enquiries with a further 69% reporting an increasing level of instructions.

The release of the OTS recommendation to double the rates of capital gains tax could bolster further activity in the property market, especially seen as these

changes are not likely to take effect until the second half of 2021.

More favourably, according to Hometrack the first quarter of 2021 is set to record a property uplift, with 100,000 additional sales expected to complete before the end of the stamp duty deadline. Market analysis continues to look positive as UK house price growth rises to +3.5%, the highest for almost 3 years. Though demand has dipped slightly to below pre-Covid levels, likely a reflection of the latest lockdown, it still remains 34% higher than last year.

Taking all of this into consideration, are we likely to see a correction to house prices in 2021?

This has been a contentious topic with many leading analysts dissenting on whether recent data is indicative of an imminent housing

London’s thriving housing marketmarket crash. The fundamental factors which are considered in these predictions are: the rate of economic growth and subsequently interest rates; the availability and affordability of homes and any movement to wages or income rates. Needless to say, all of these factors have been directly impacted by the consequences of the pandemic and thus, the extent of the economic fallout largely depends on how long it will take for society to return to a form of normalcy. The increased interest rates stem from the Treasury and the Bank of England’s attempt to stimulate the economy with expenditure and it is likely that this method of quantitative easing will continue until the pace of economic growth strengthens. A continuation of low interest rates is favourable to the housing market as it ensures mortgage funding remains relatively cheap and this in turn keeps house prices high. The vastly greater

demand to supply situation in the UK will also be a preventative factor to a potential market crash. According to data collected from the Office for National Statistics (ONS), for the UK to meet the demand 300,000 new homes must be built each year and data from the past few years evidences a consistent and significant shortfall. Therefore, this is also a positive towards ensuring that house prices continue to accumulate value and will not drop to an amount that would cause a market crash.

The announcement of the extension of the furlough scheme until March 2021 is another round of welcome news as this may slow the rate of unemployment. The housing market has remained remarkably immune to the pitfalls caused by the pandemic, bolstered by the temporary stamp duty holiday and various income support schemes.

In the second week of December the World Economic Forum announced London’s recognised status as the world’s most ‘magnetic’ city for the ninth consecutive year. In spite of the difficulties endured, London increased its lead over its nearest rival (New York) as its popularity continues to grow. The Global Power City Index is a measure compiled by the Mori Memorial Foundation’s Institute for Urban Strategies based on official data and interviews conducted with approximately 1,000 people in each of the respective cities. The purpose of the index is to rank prominent world cities on their ability to attract people, capital and enterprises from elsewhere globally, using many indicative measures including their economy, research and development activity, cultural interaction, standard of living and accessibility.

The 2020 rankings place London in the lead for almost every category, a fact which left many critics confounded. Rather than the UK experiencing a ‘brain-drain’ migration of UK born nationals, The number of EU workers in the UK increased 133,000 to 2.44 million this past year, which according to official figures is the largest annual increase for some years. Furthermore, the city continues to rival New York for status as the world’s leading financial centre. With nearly half of the world’s euro currency trading activity taking place in this city, it is well on its way to achieving leading global financial status.

London: the world’s most ‘magnetic’ city

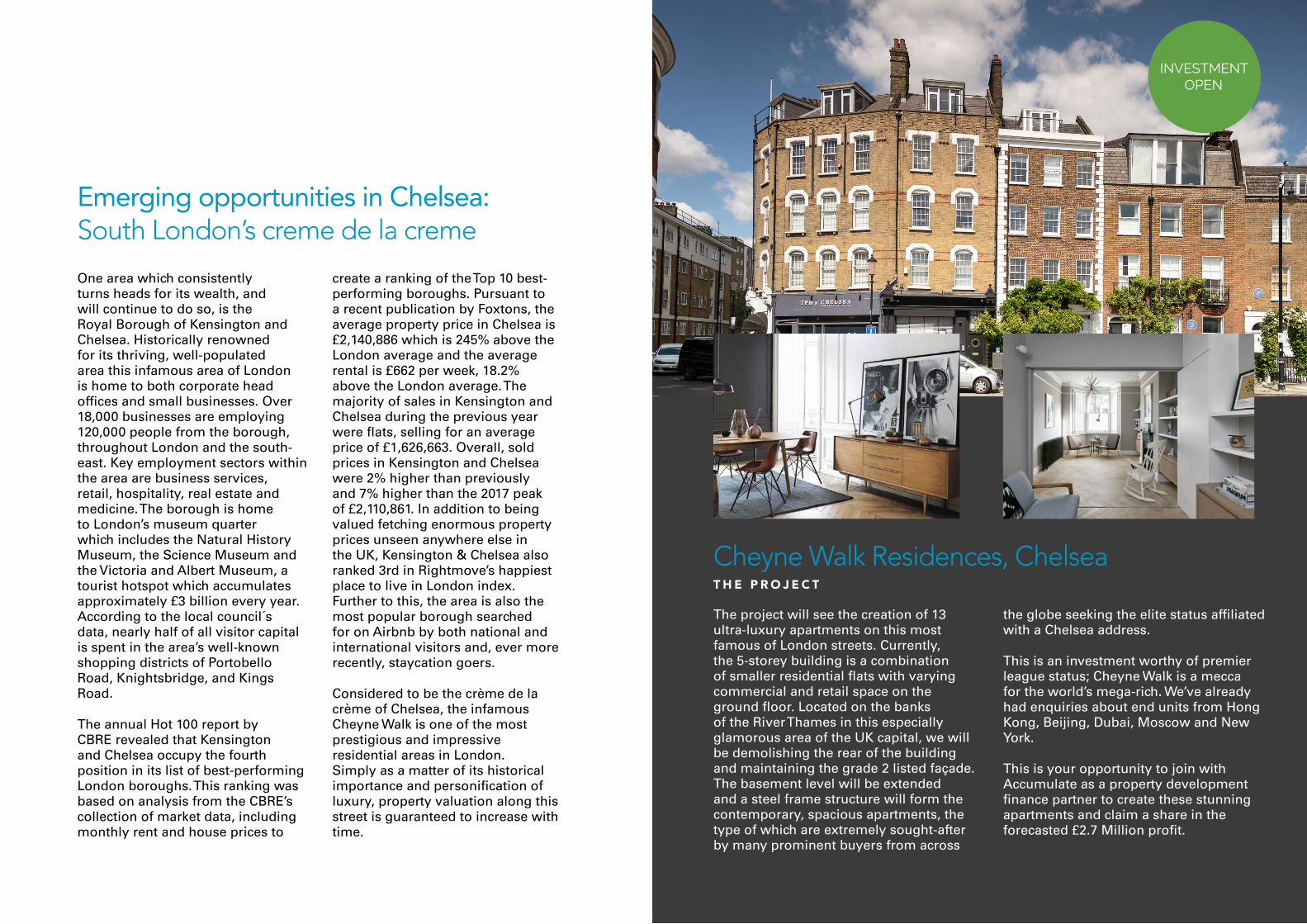

The project will see the creation of 13 ultra-luxury apartments on this most famous of London streets. Currently, the 5-storey building is a combination of smaller residential flats with varying commercial and retail space on the ground floor. Located on the banks of the River Thames in this especially glamorous area of the UK capital, we will be demolishing the rear of the building and maintaining the grade 2 listed façade. The basement level will be extended and a steel frame structure will form the contemporary, spacious apartments, the type of which are extremely sought-after by many prominent buyers from across

the globe seeking the elite status affiliated with a Chelsea address.

This is an investment worthy of premier league status; Cheyne Walk is a mecca for the world’s mega-rich. We’ve already had enquiries about end units from Hong Kong, Beijing, Dubai, Moscow and New York.

This is your opportunity to join with Accumulate as a property development finance partner to create these stunning apartments and claim a share in the forecasted £2.7 Million profit.

Cheyne Walk Residences, ChelseaT H E P R O J E C T

INVESTMENT OPEN

One area which consistently turns heads for its wealth, and will continue to do so, is the Royal Borough of Kensington and Chelsea. Historically renowned for its thriving, well-populated area this infamous area of London is home to both corporate head offices and small businesses. Over 18,000 businesses are employing 120,000 people from the borough, throughout London and the south-east. Key employment sectors within the area are business services, retail, hospitality, real estate and medicine. The borough is home to London’s museum quarter which includes the Natural History Museum, the Science Museum and the Victoria and Albert Museum, a tourist hotspot which accumulates approximately £3 billion every year. According to the local council´s data, nearly half of all visitor capital is spent in the area’s well-known shopping districts of Portobello Road, Knightsbridge, and Kings Road.

The annual Hot 100 report by CBRE revealed that Kensington and Chelsea occupy the fourth position in its list of best-performing London boroughs. This ranking was based on analysis from the CBRE’s collection of market data, including monthly rent and house prices to

create a ranking of the Top 10 best-performing boroughs. Pursuant to a recent publication by Foxtons, the average property price in Chelsea is £2,140,886 which is 245% above the London average and the average rental is £662 per week, 18.2% above the London average. The majority of sales in Kensington and Chelsea during the previous year were flats, selling for an average price of £1,626,663. Overall, sold prices in Kensington and Chelsea were 2% higher than previously and 7% higher than the 2017 peak of £2,110,861. In addition to being valued fetching enormous property prices unseen anywhere else in the UK, Kensington & Chelsea also ranked 3rd in Rightmove’s happiest place to live in London index. Further to this, the area is also the most popular borough searched for on Airbnb by both national and international visitors and, ever more recently, staycation goers.

Considered to be the crème de la crème of Chelsea, the infamous Cheyne Walk is one of the most prestigious and impressive residential areas in London. Simply as a matter of its historical importance and personification of luxury, property valuation along this street is guaranteed to increase with time.

Emerging opportunities in Chelsea: South London’s creme de la creme

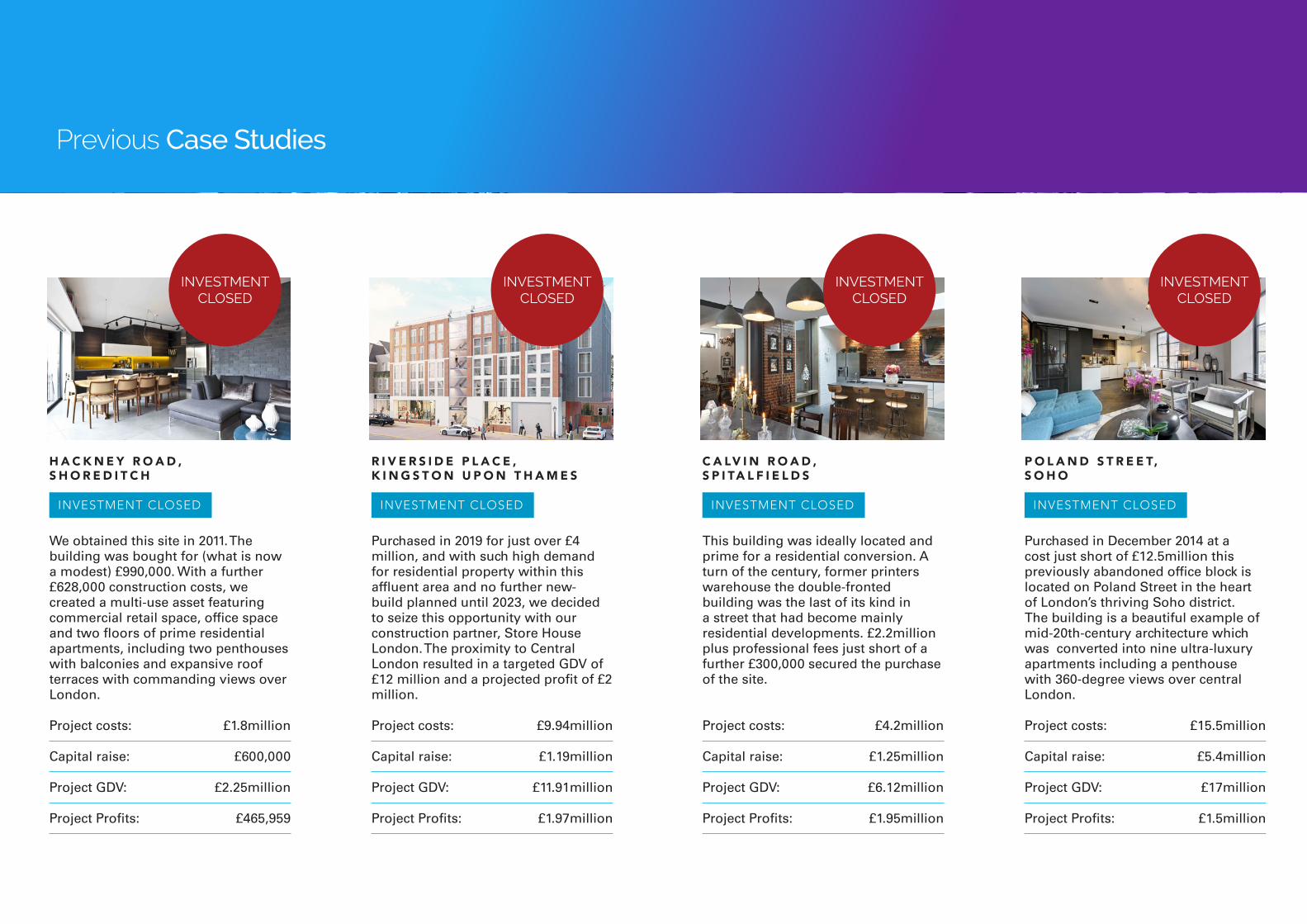

We obtained this site in 2011. The building was bought for (what is now a modest) £990,000. With a further £628,000 construction costs, we created a multi-use asset featuring commercial retail space, office space and two floors of prime residential apartments, including two penthouses with balconies and expansive roof terraces with commanding views over London.

Project costs: £1.8million

Capital raise: £600,000

Project GDV: £2.25million

Project Profits: £465,959

H A C K N E Y R O A D , S H O R E D I T C H

Previous Case Studies

INVESTMENT CLOSED

Purchased in 2019 for just over £4 million, and with such high demand for residential property within this affluent area and no further new-build planned until 2023, we decided to seize this opportunity with our construction partner, Store House London. The proximity to Central London resulted in a targeted GDV of £12 million and a projected profit of £2 million.

Project costs: £9.94million

Capital raise: £1.19million

Project GDV: £11.91million

Project Profits: £1.97million

R I V E R S I D E P L A C E , K I N G S T O N U P O N T H A M E S

INVESTMENT CLOSED

This building was ideally located and prime for a residential conversion. A turn of the century, former printers warehouse the double-fronted building was the last of its kind in a street that had become mainly residential developments. £2.2million plus professional fees just short of a further £300,000 secured the purchase of the site.

Project costs: £4.2million

Capital raise: £1.25million

Project GDV: £6.12million

Project Profits: £1.95million

C A LV I N R O A D , S P I TA L F I E L D S

INVESTMENT CLOSED

Purchased in December 2014 at a cost just short of £12.5million this previously abandoned office block is located on Poland Street in the heart of London’s thriving Soho district. The building is a beautiful example of mid-20th-century architecture which was converted into nine ultra-luxury apartments including a penthouse with 360-degree views over central London.

Project costs: £15.5million

Capital raise: £5.4million

Project GDV: £17million

Project Profits: £1.5million

P O L A N D S T R E E T, S O H O

INVESTMENT CLOSED

INVESTMENT CLOSED

INVESTMENT CLOSED

INVESTMENT CLOSED

INVESTMENT CLOSED

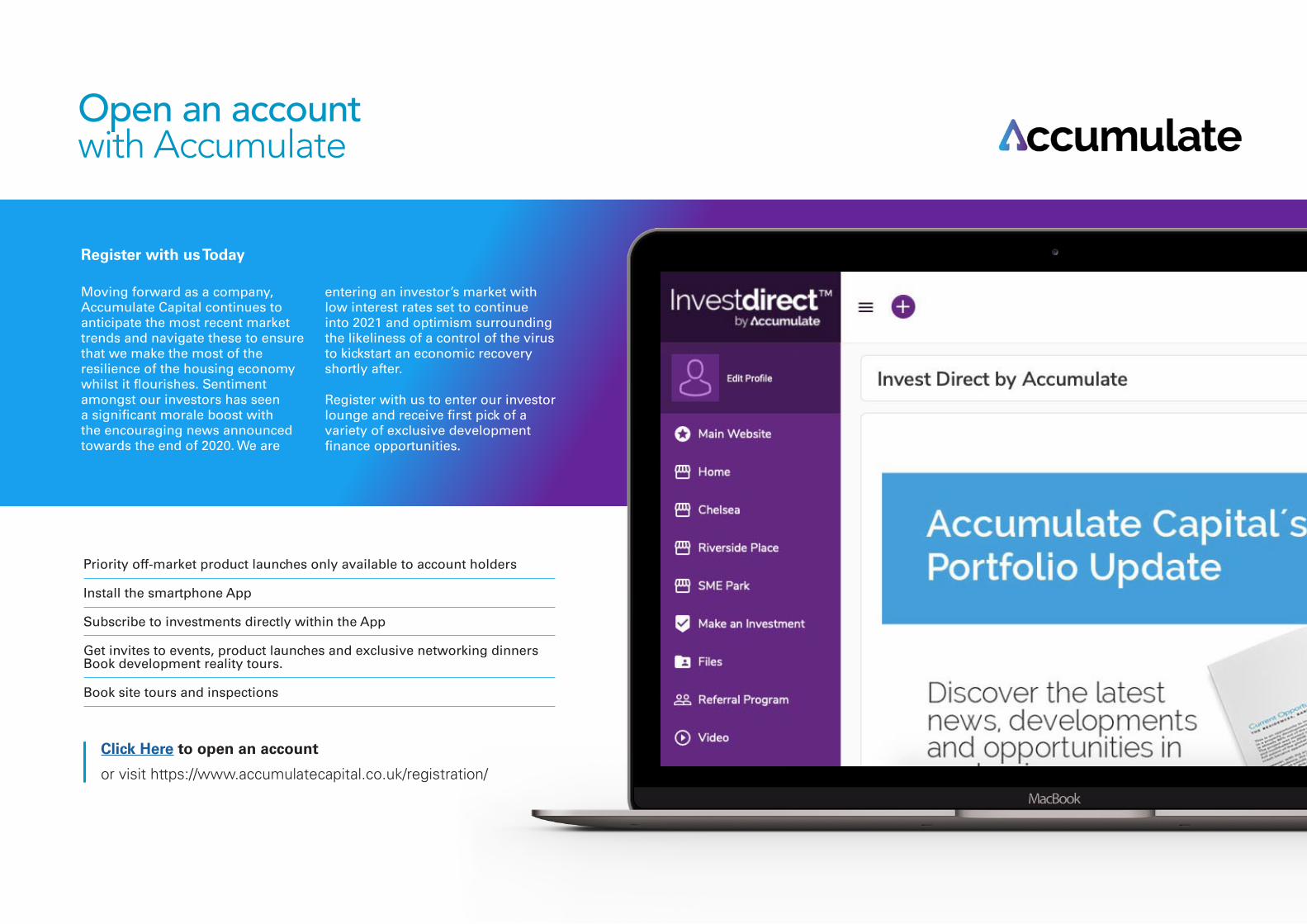

Register with us Today

Open an account with Accumulate

Moving forward as a company, Accumulate Capital continues to anticipate the most recent market trends and navigate these to ensure that we make the most of the resilience of the housing economy whilst it flourishes. Sentiment amongst our investors has seen a significant morale boost with the encouraging news announced towards the end of 2020. We are

entering an investor’s market with low interest rates set to continue into 2021 and optimism surrounding the likeliness of a control of the virus to kickstart an economic recovery shortly after.

Register with us to enter our investor lounge and receive first pick of a variety of exclusive development finance opportunities.

Priority off-market product launches only available to account holders

Install the smartphone App

Subscribe to investments directly within the App

Get invites to events, product launches and exclusive networking dinners Book development reality tours.

Book site tours and inspections

Click Here to open an account

or visit https://www.accumulatecapital.co.uk/registration/

Canterbury Innovation Centre

University Road, Canterbury, Kent. CT2 7FG

Email: [email protected]

Tel: 01227 936 996

www.accumulatecapital.co.uk

https://www.weforum.org/agenda/2020/12/london-top-world-city-poll-brexit-covid-19/

References