Embed Size (px)

Citation preview

1

PROPERTY ASSESSMENT APPEAL BOARD

FINDINGS OF FACT, CONCLUSIONS OF LAW, AND ORDER

PAAB Docket No. 2015-100-00094I

Parcel No. 10-06-390-010

GPT Ames Owner, LLC,

Appellant,

vs.

City of Ames Board of Review,

Appellee.

Introduction

This appeal came on for hearing before the Property Assessment Appeal Board

(PAAB) on September 8, 2016. Daniel Manning, Sr. of Lillis O’Malley Law Firm, Des

Moines, represented GPT Ames Owner, LLC (GPT). Assistant City Attorney Mark

Lambert represented the City of Ames Board of Review.

GPT is the owner of an industrial warehouse located at 2825 E. Lincoln Way,

Ames. The warehouse was built between 1999 and 2002 and has 576,476 square-feet

of gross building area (GBA). There is approximately 1200 square feet of finished office

space. The site is 23.76 acres. (Exs. 2-3, 6, A, and B).

The property’s January 1, 2015 assessment was $26,200,000; allocated as

$1,690,700 in land value and $24,509,300 in improvement value. GPT protested to the

Board of Review claiming the property was assessed for more than the value authorized

by law under Iowa Code section 441.37(1)(a)(1)(b). The Board of Review reduced the

assessment to $24,200,000. GPT then appealed to PAAB, asserting the property’s

correct fair market value is $22,500,000.

Electronically Filed2017-02-13 10:51:30

PAAB

2

General Principles of Assessment Law

I. Jurisdiction and Scope of Review

PAAB has jurisdiction of this matter under Iowa Code sections 421.1A and

441.37A (2015). PAAB is an agency and the provisions of the Administrative Procedure

Act apply to it. Iowa Code § 17A.2(1). This appeal is a contested case. § 441.37A(1)(b).

PAAB considers only those grounds presented to or considered by the Board of

Review, but determines anew all questions arising before the Board of Review related

to the liability of the property to assessment or the assessed amount. §§ 441.37A(1)(a-

b). New or additional evidence may be introduced, and PAAB considers the record as a

whole and all of the evidence regardless of who introduced it. § 441.37A(3)(a); see also

Hy-Vee, Inc. v. Employment Appeal Bd., 710 N.W.2d 1, 3 (Iowa 2005). There is no

presumption that the assessed value is correct. § 441.37A(3)(a).

II. Property Assessment Valuation Under Iowa Law

In Iowa, property is to be valued at its actual value. Iowa Code § 441.21(1)(a).

Actual value is the property’s fair and reasonable market value. § 441.21(1)(b). Market

value essentially is defined as the value established in an arm’s-length sale of the

property. Id. Sale prices of the property or comparable properties in normal

transactions are to be considered in arriving at market value. Id. Conversely, sale

prices of abnormal transactions not reflecting market value shall not be taken into

account, or shall be adjusted to eliminate the factors that distort market value, including

but not limited to foreclosure or other forced sales. Id.

The sales comparison method is the preferred method for valuing property.

Compiano v. Polk Cnty. Bd. of Review, 771 N.W.2d 392, 398 (Iowa 2009); Soifer, 759

N.W.2d at 779; Heritage Cablevision v. Bd. of Review of Mason City, 457 N.W. 2d 594,

597 (Iowa 1990). “[A]lternative methods to the comparable sales approach to valuation

of property cannot be used when adequate evidence of comparable sales is available to

readily establish market value by that method.” Compiano, 771 N.W.2d at 398.

(emphasis added). However, where the market value of the property cannot be readily

established using comparable sales, one can turn to other factors to determine the

3

value. § 441.21(1)(b) (emphasis added); Soifer, 759 N.W.2d at 779. “Thus, a witness

must first establish that evidence of comparable sales was not available to establish

market value under the comparable sales approach before the other approaches to

valuation become competent evidence in a tax assessment proceeding” Id. (citing

Soifer 759 N.W.2d at 782); Carlon Co. v. Bd. of Review of Clinton, 572 N.W.2d 146, 150

(Iowa 1997).

The first step in this process is determining if comparable sales exist. Soifer, 759

N.W. 2d at 783. If PAAB is not persuaded as to the comparability of the properties, then

it “cannot consider the sales prices of those” properties. Id. at 782 (citing Bartlett & Co.

Grain Co. v. Bd. of Review of Sioux City, 253 N.W.2d 86,88 (Iowa 1977)). Whether

other property is sufficiently similar and its sale sufficiently normal to be considered on

the question of value is left to the sound discretion of the trial court or PAAB. Id. at 783

(citing Bartlett & Co. Grain, 253, N.W.2d at 94).

Here, GPT believes the subject’s fair market value cannot be readily established

by the sales comparison approach while the Board of Review believes it can. For

reasons that will be discussed, we conclude the subject’s fair market value cannot be

readily established by the sales comparison approach alone and, thus, also consider

the other approaches to value.

III. Burden of Proof

Initially, the burden of proof in an assessment protest rests with the taxpayer,

who “must establish a ground for protest by a preponderance of the evidence.”

Compiano v. Polk Cnty. Bd. of Review, 771 N.W.2d 392, 396 (Iowa 2009). However, if

the taxpayer “offers competent evidence by at least two disinterested witnesses that the

market value of the property is less than the market value determined by the assessor,

the burden shifts to the board of review to uphold the assessed value.” Id. at 396-397;

§ 441.21(3). Failure to shift the burden of proof is not equivalent to satisfying the burden

of proof. Id. at 397. “Ultimately, the burden of proof is one of persuasion,” which “comes

into play after all the evidence is introduced at hearing.” Id. at 397 n. 3.

4

In the case, GPT called two witnesses: GPT employee Anthony Nelson and

Appraiser Michael Olson. Nelson served as a fact witness. Only Olson valued the

subject property within the construct of section 441.21(1)(b).

We conclude GPT has failed to shift the burden of proof. However, GPT’s claim

does not fail for this reason. Rather, GPT retains the burden to prove the subject

property is over assessed based on a preponderance of the evidence when the record

is viewed as a whole.

IV. Claim of Over Assessment

In an appeal alleging the property is assessed for more than the value authorized

by law under Iowa Code section 441.37(1)(a)(1)(b), the taxpayer must show: 1) the

assessment is excessive and 2) the subject property’s correct value. Boekeloo v. Bd. of

Review of Clinton, 529 N.W.2d 275, 277 (Iowa 1995).

Findings of Fact

In support of its claim, GPT submitted an appraisal by Michael Olson, The Olson

Group, Urbandale. (Ex. 3). Kyran (Casey) Cook of Cook Appraisal, Iowa City,

completed an appraisal for the Board of Review. (Ex. B). The Board of Review also

submitted an appraisal completed by John Bouhan and Eric Enloe, Integra Realty

Resources (IRR), Chicago, commissioned by GPT when it was considering purchasing

the property in 2014. (Ex. C). Olson and Cook testified at the hearing. The following

table summarizes the appraisers’ approaches to value and their respective conclusions.

Appraiser Sales

Approach Income

Approach Cost

Approach Final Opinion of

Value

Olson $21,920,000 $23,150,000 $22,670,000 $22,500,000

Cook $25,940,000 $23,300,000 $25,950,000 $25,150,000

IRR $26,500,000 $26,500,000 N/A $26,500,000

The IRR appraisal concludes a leased-fee value as of April 2014 rather than a

fee-simple value as of the assessment date. For this reason, we do not find the final

opinion of value in the IRR appraisal relevant to the question before us. However, some

5

information contained in that appraisal is useful in analyzing the reliability of the two

remaining reports.

Both Olson and Cook completed all three approaches to value: cost, sales

comparison, and income, and gave weight to all three approaches in their final opinion

of value.

Sale History of the Subject Property

GPT, a Real Estate Invesment Trust (REIT), purchased the subject property in

July 2014 for $26,500,000, from another private REIT. (Ex. 6). “A REIT is a corporation

or trust that combines the capital of many investors to acquire or provide financing for all

forms of real estate. A REIT serves much like a mutual fund for real estate.” APPRAISAL

INSTITUTE, THE DICTIONARY OF REAL ESTATE APPRAISAL 160 (5TH ED. 2010). It is not

unusual for a REIT purchase to include multiple properties in a portfolio, which is the

case here. The subject property was one of three properties purchased in a single

transaction for a total of $69,000,000. (Ex. 6). The other two properties included in the

purchase, located in Georgia and North Carolina, were also warehouse properties like

the subject.

The parties disagree regarding whether the subject property’s sales price should

be considered in determining its fair market value. GPT asserts the original assessment

was based in large part on the purchase price. It further asserts the sale should not be

considered as it involved a REIT.

Anthony Nelson testified the property was purchased very early in the REIT’s

acquisition cycle. At that point, he asserted GPT was willing to pay a slight premium for

the subject property because of its desire to acquire the other two properties in the

portfolio, which were occupied by single, good-credit tenants with a net-lease and

located in “NFL Cities.” Nelson testified the structure of the sale also benefitted GPT’s

decision to purchase the property. Nelson explained the prices were established for the

properties in what GPT considered the portfolio-level price, which evaluates the risk of

each asset combined with the back-and-forth negotiation in an off-market deal.

Nelson explained if GPT were to sell this property “today” the challenges include

two tenants that occupy roughly half of the building with leases set to expire at the end

6

of 2016. Neither tenant has taken their renewal options. Moreover, Nelson testified the

third tenant, who is also the top credit tenant in the building, is potentially considering

subleasing about a third of their space. For these reasons, he asserts it would be

difficult to value the building. He opined they would sell the property for $20,000,000 to

$22,000,000.

City of Ames Assessor Greg Lynch testified for the Board of Review. Lynch

explained that as part of his analysis, he was aware of the subject sale in 2014 and

contacted the listing real estate broker, Dick Powell, in October 2014. Lynch explained

Powell indicated the subject had good tenants, with the main tenant having seven-years

left on its lease; and that the sale was arms-length and “at market”. Based on this

conversation, Lynch believed it to be a good sale to include in his analysis.

Olson reviewed the history of the subject sale, testifying it involved multiple

properties, was not a cash sale, and it involved stock and an assumption of roughly a

$17,000,000 dollar debt. (Ex. 3, p. 10). For these reasons, he does not believe that the

2014 sale of the subject reflected its fair market value. When questioned why a REIT

would pay more than fair market value for a property, Olson testified he believes when a

REIT purchases multiple properties in a portfolio they are able to spread their expenses

around with less duplication. He believes the IRR appraisal report bears this out by

reporting much lower expenses in their income approach. Olson conceded it is

reasonable that a REIT would have additional expenses because of its federal

regulatory requirements, but that he did not see those expenses considered in the IRR

appraisal report.

Cook believes the subject’s sales price fits in the market and is not out of line

with other sales.

A. Storage Warehouse vs. Distribution Warehouse

The subject property has thirty-one docks doors and five drive-in bays and both

parties agree the subject property is a Class C warehouse. (Ex. 3, p. 25 & 48; Ex. B, p.

22 & 30). The parties disagree as to whether the subject property should be valued as

a storage warehouse or distribution warehouse for purposes of the cost approach.

7

GPT and its witnesses assert the subject property should be considered a

storage warehouse. Anthony Nelson, GPT’s Vice President of Asset Management,

testified the building is set up in pods and this is not typical for a modern day distribution

facility. He stated that ideally the building design for a distribution warehouse would be

one that is completely cross-docked. He believes the building’s pod design is more akin

to a storage warehouse even if it used for distribution.

GPT’s appraiser Michael Olson asserts the subject property is a storage

warehouse and valued it as such in his cost approach. Olson bases this opinion on the

fact that the subject property only has 1200 square feet of office space, or 0.2% of the

GBA. Olson testified that Marshall Valuation Service (MVS) identifies storage

warehouse buildings as having between 3-12% office finish. On cross examination,

Olson acknowledged office space is not the only factor to consider in making a

determination between a storage warehouse and distribution warehouse, but he

maintained it is a primary factor in making a determination.

GPT also submitted a document apparently from MVS. (Ex. 10). The document

indicates warehouses in general “are designed primarily for storage and that an amount

of office space commensurate with the quality of the building is included in the costs.”

(Ex. 10). The document indicates storage warehouses typically have 3-12% of total

area for office space, distribution warehouses typically have 15-30%, and mega

warehouses (properties over 200,000 square feet) only 1-5%. (Ex. 10). Interestingly,

neither party contends this is a mega warehouse even though it falls within those

parameters.

The Board of Review’s appraiser, Kyran “Casey” Cook, expressed an opinion

contrary to Olson. Cook agreed with Olson that office space is a factor in determining

the type of warehouse, but stated it is one characteristic of many to be considered;

others include availability of dock-high doors and the ability to get in/out of the building.

Cook noted that in a distribution warehouse the goods are moved in and out frequently,

resulting in a number of “turns” (in/out) of the inventory. He testified the number of

“turns” is significant at the subject property. Cook further testified that in order to

accomplish a flow of goods, a building requires docks on both sides, which the subject

8

has, to allow inventory to come into the warehouse and then out the other side.

Comparatively, a storage warehouse does not have this feature.

The appraisal completed by Integra Realty Resources (IRR) for the purchase of

the subject property in 2015 was submitted by the Board of Review. Although no

appraiser testified regarding the report, the appraisers conclude therein that the subject

property is a distribution warehouse.

Finally, it appears both appraisers used comparable sale properties identified as

distribution warehouses in their sales comparison approaches. Notably, at least one

sale used by both appraisers, referred to as the Toro sale located at 5500 SE Delaware,

Ankeny, was identified as a distribution warehouse by both Olson and Cook. This

property has only 1.4% of the building devoted to office space. (Ex. 3, p. 74; Ex. B, p.

33). Moreover, the appraisers did not make adjustments in their sales comparison

approach for storage versus distribution warehouses; and they did not distinguish

between these property types when selecting comparables to establish the market rent.

The Dictionary of Real Estate Appraisal defines both storage warehouses and

distribution warehouses. APPRAISAL INSTITUTE, THE DICTIONARY OF REAL ESTATE

APPRAISAL 224 (5th ed. 2010). A storage warehouse is defined as “a structure that is

designed and used for the storage of wares, goods, and merchandise; considered

obsolete by distribution building standards and is used for inventories with low turnover

or dead storage.” Conversely, a distribution warehouse is defined as “a storage building

designed to promote the logistical movement of goods. Special emphasis is placed on

providing adequate loading facilities and easy truck ingress and egress. Modern

distribution buildings feature 24-foot minimum clear height and typically one or more

dock-high doors for every 10,000 square feet.”

At the end of the day, we recognize this dispute primarily affects the conclusions

of the cost approach only.

9

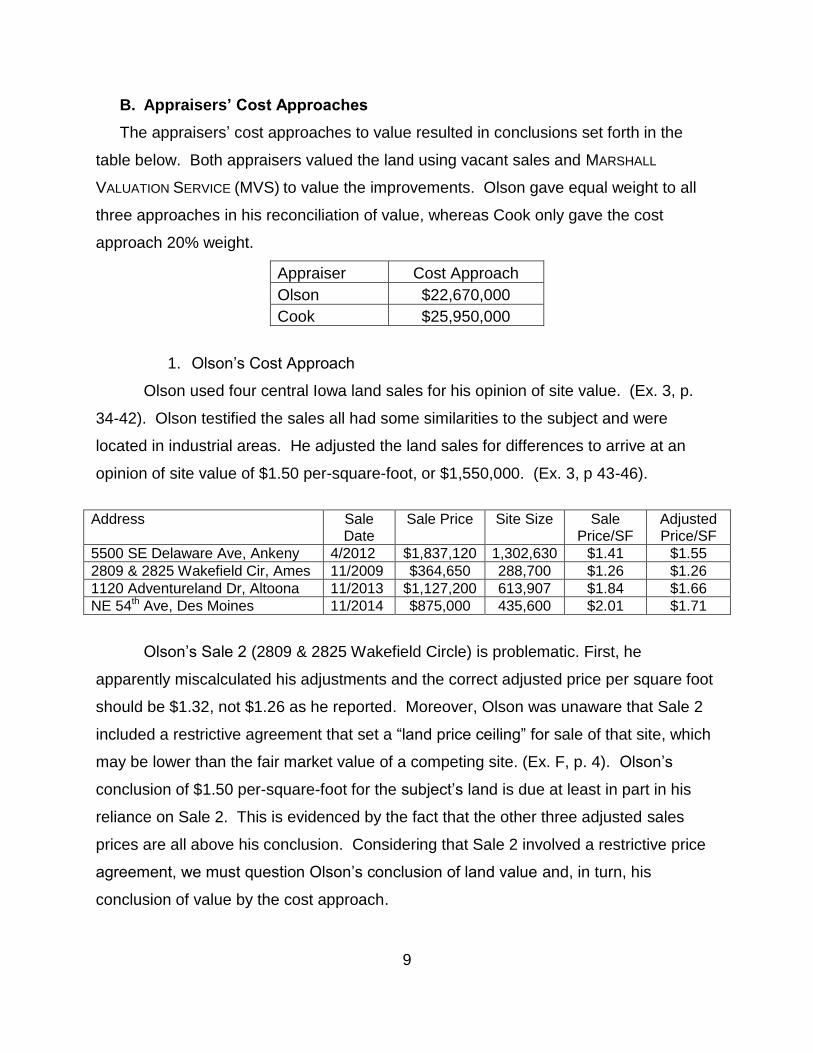

B. Appraisers’ Cost Approaches

The appraisers’ cost approaches to value resulted in conclusions set forth in the

table below. Both appraisers valued the land using vacant sales and MARSHALL

VALUATION SERVICE (MVS) to value the improvements. Olson gave equal weight to all

three approaches in his reconciliation of value, whereas Cook only gave the cost

approach 20% weight.

Appraiser Cost Approach

Olson $22,670,000

Cook $25,950,000

1. Olson’s Cost Approach

Olson used four central Iowa land sales for his opinion of site value. (Ex. 3, p.

34-42). Olson testified the sales all had some similarities to the subject and were

located in industrial areas. He adjusted the land sales for differences to arrive at an

opinion of site value of $1.50 per-square-foot, or $1,550,000. (Ex. 3, p 43-46).

Address Sale

Date Sale Price Site Size Sale

Price/SF Adjusted Price/SF

5500 SE Delaware Ave, Ankeny 4/2012 $1,837,120 1,302,630 $1.41 $1.55

2809 & 2825 Wakefield Cir, Ames 11/2009 $364,650 288,700 $1.26 $1.26

1120 Adventureland Dr, Altoona 11/2013 $1,127,200 613,907 $1.84 $1.66

NE 54th Ave, Des Moines 11/2014 $875,000 435,600 $2.01 $1.71

Olson’s Sale 2 (2809 & 2825 Wakefield Circle) is problematic. First, he

apparently miscalculated his adjustments and the correct adjusted price per square foot

should be $1.32, not $1.26 as he reported. Moreover, Olson was unaware that Sale 2

included a restrictive agreement that set a “land price ceiling” for sale of that site, which

may be lower than the fair market value of a competing site. (Ex. F, p. 4). Olson’s

conclusion of $1.50 per-square-foot for the subject’s land is due at least in part in his

reliance on Sale 2. This is evidenced by the fact that the other three adjusted sales

prices are all above his conclusion. Considering that Sale 2 involved a restrictive price

agreement, we must question Olson’s conclusion of land value and, in turn, his

conclusion of value by the cost approach.

10

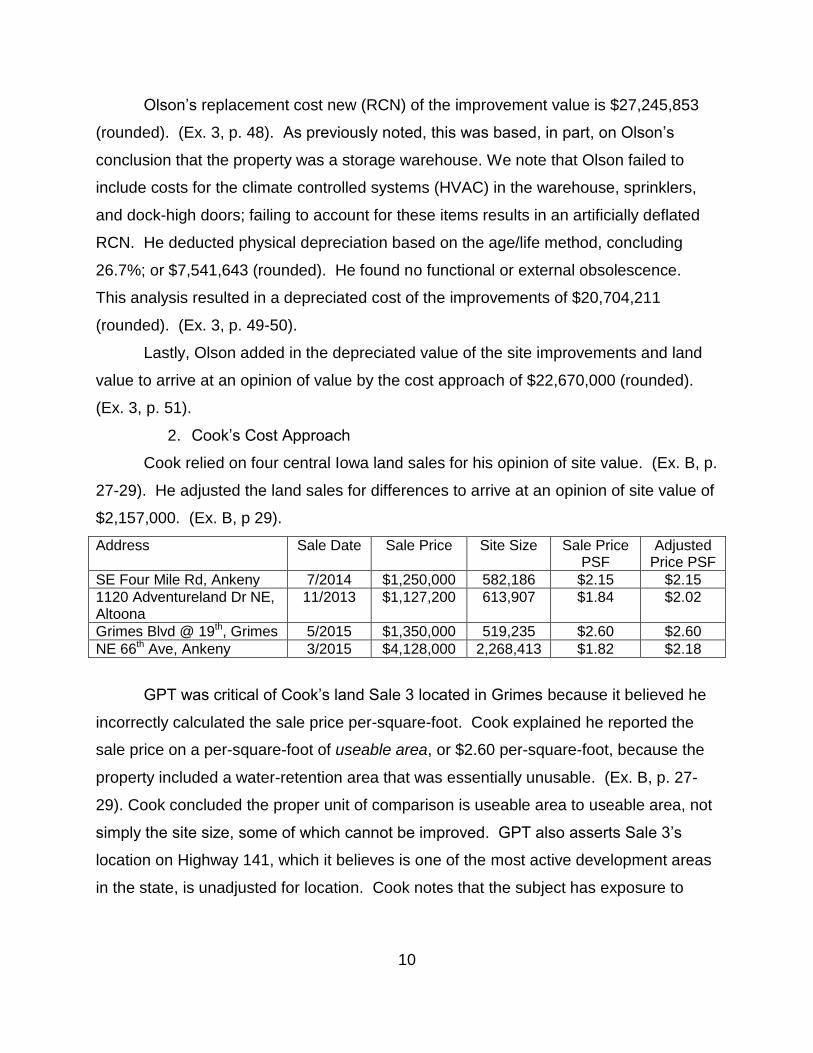

Olson’s replacement cost new (RCN) of the improvement value is $27,245,853

(rounded). (Ex. 3, p. 48). As previously noted, this was based, in part, on Olson’s

conclusion that the property was a storage warehouse. We note that Olson failed to

include costs for the climate controlled systems (HVAC) in the warehouse, sprinklers,

and dock-high doors; failing to account for these items results in an artificially deflated

RCN. He deducted physical depreciation based on the age/life method, concluding

26.7%; or $7,541,643 (rounded). He found no functional or external obsolescence.

This analysis resulted in a depreciated cost of the improvements of $20,704,211

(rounded). (Ex. 3, p. 49-50).

Lastly, Olson added in the depreciated value of the site improvements and land

value to arrive at an opinion of value by the cost approach of $22,670,000 (rounded).

(Ex. 3, p. 51).

2. Cook’s Cost Approach

Cook relied on four central Iowa land sales for his opinion of site value. (Ex. B, p.

27-29). He adjusted the land sales for differences to arrive at an opinion of site value of

$2,157,000. (Ex. B, p 29).

Address Sale Date Sale Price Site Size Sale Price PSF

Adjusted Price PSF

SE Four Mile Rd, Ankeny 7/2014 $1,250,000 582,186 $2.15 $2.15

1120 Adventureland Dr NE, Altoona

11/2013 $1,127,200 613,907 $1.84 $2.02

Grimes Blvd @ 19th, Grimes 5/2015 $1,350,000 519,235 $2.60 $2.60

NE 66th Ave, Ankeny 3/2015 $4,128,000 2,268,413 $1.82 $2.18

GPT was critical of Cook’s land Sale 3 located in Grimes because it believed he

incorrectly calculated the sale price per-square-foot. Cook explained he reported the

sale price on a per-square-foot of useable area, or $2.60 per-square-foot, because the

property included a water-retention area that was essentially unusable. (Ex. B, p. 27-

29). Cook concluded the proper unit of comparison is useable area to useable area, not

simply the site size, some of which cannot be improved. GPT also asserts Sale 3’s

location on Highway 141, which it believes is one of the most active development areas

in the state, is unadjusted for location. Cook notes that the subject has exposure to

11

I-35, and a short distance to access. Ultimately, Cook concluded a site value of $2.10

per-square-foot; or $2,157,000 (rounded). GPT was critical of this conclusion because

it was higher than the assessed value of the site, $1,690,700. However, we note that

IRR concluded a site value of $2.50 per-square-foot; or $2,600,000 rounded and GPT

was silent on those conclusions.

Cook estimated the RCN of the building improvements using MVS. He identified

the subject property as a “Class C Average Distribution Warehouse Building.”

(Emphasis Added). (Ex. B, p. 30). Cook determined the RCN of the improvement value

is $35,101,599. (Ex. B. p. 32). He deducted physical depreciation based on the age/life

method, concluding 33.33%; or $11,700,533; which he states considers functional

utility. He did not apply any additional functional or external obsolescence adjustments.

This analysis resulted in a depreciated cost of the improvements of $23,401,066. (Ex.

B, p. 32). Lastly, Cook added in the depreciated value of the site improvements and

land value to arrive at an opinion of value by the cost approach of $25,950,000

(rounded). (Ex. B, p. 32).

3. Analysis & Conclusion

The differences between Cook’s description of the subject property as a

distribution warehouse and Olson’s description as a storage warehouse result in

differences in the estimated base cost of the improvements.

As noted earlier, the appraisers also had other points of difference in their

valuation of the subject improvements that account for differences in their per-square-

foot valuations of the subject improvements.

One difference between the two appraisals is the property’s HVAC system.

Olson asserts only the office portion of the subject property is heated/cooled. Cook,

however, testified that the remainder of the building is temperature controlled and

referenced a picture of eight heating/cooling plants in the warehouse. (Ex. B, p. 6).

Cook stated the intent of the units is to keep the temperature of the building between 55

degrees in the winter and 85 degrees in the summer, so the employees working in the

area can be somewhat comfortable. He acknowledges it is not the same as an air-

conditioned office space, but it is a controlled environment. Cook explained that most

12

warehouse spaces have hanging gas-fired burners that heat the space, whereas this is

a considerable step-up and offers a competitive edge to the subject property. When

questioned whether temperature control in the warehouse would add value, Olson

testified it would.

Based on the aforementioned differences, Cook’s total replacement costs are

more than 20% higher than Olson’s.

While PAAB is persuaded the subject property is more akin to a distribution

warehouse than a storage warehouse, this issue only impacts the cost analysis. We

could put this concern aside by giving merit to both arguments and averaging the

Olson’s storage warehouse base costs with Cook’s distribution base warehouse costs.

But even doing this PAAB has noted inaccuracies in Olson’s appraisal as well as his

failure to account for some of the valuable features that make his conclusion of value by

the cost approach less reliable as compared to Cook’s analysis. Specifically, we are

concerned with his opinion of site value, as it seems to be based, in part, on a sale that

had a “land price ceiling.” Moreover, Olson failed to account for features such as the

heating/cooling, sprinklers, and dock-high doors, which would increase his costs by

$5.03 per-square-foot; or roughly $2,900,000. As a result, we find Olson’s cost

approach likely undervalues the subject.

Considering a blended base cost for both appraisers’ cost analysis, Cook’s

conclusions would be slightly lower than his reported value of $25,950,000. Without

reinventing the cost approaches of both appraisers, we find it sufficient to recognize the

value of the subject property by the cost approach would reasonably be no less than

$24,000,000, and not more than $25,950,000.

13

C. Income Approach

1. Olson’s Income Approach

To complete the income approach, Olson relied on the rents of four central Iowa

warehouse properties to establish the market rent of the subject property. (Ex. 3, p. 55-

63). He adjusted the properties for differences to arrive at a market rent of $3.75 per-

square-foot net (tenants paying all expenses), or an annual market rent of $2,163,285.

(Ex. 3, p. 66). He estimated vacancy, management, and a reserve for replacement to

be deducted as expenses to arrive at a net operating income (NOI) of $1,829,057

(rounded). (Ex. 3, p, 67). The final step in the income approach is to determine the

capitalization rate. In arriving at a capitalization rate, Olson relied on a mortgage equity

analysis. He reconciled an indicated capitalization rate of 7.9%. (Ex. 3, p. 68-71). He

testified that he did not load the capitalization rate, because the tenants are paying the

expense, so he considers this in the vacancy. We note this is not typical methodology

when valuing a property for ad valorem purposes. His conclusion of value, based on

the direct capitalization income approach is rounded to $23,150,000. (Ex. 3, p. 72).

2. Cook’s Income Approach

To complete the income approach, Cook relied on the rents of five Iowa

warehouse properties to establish the market rent of the subject property. (Ex. B, p.

37). He adjusted the properties for differences to arrive at a market rent of $3.60 per-

square-foot, or an annual market rent of $2,075,313. (Ex. B, p. 37). He estimated

vacancy, management, and a reserve for replacement to be deducted as expenses to

arrive at a NOI of $1,745,228. (Ex. B, p, 39). The final step in the income approach is

to determine the capitalization rate. In arriving at a capitalization rate, Cook relied on a

mortgage equity analysis. He reconciled an indicated capitalization rate of 7.25%;

which he then loaded for taxes to arrive at a tax capitalization rate of 7.49% (Ex. B, p.

41). His conclusion of value, based on the direct capitalization income approach is

rounded to $23,300,000. (Ex. B, p. 42).

3. Analysis & Conclusion

Both appraisers arrived at nearly identical conclusions, and have similar market

rents and overall expenses. Olson testified that because the tenants are paying the

14

taxes, in lieu of loading the capitalization rate, he accounts for this in his vacancy. We

note the total vacancy he applied in his income analysis is 7%; 5% for vacancy and 2%

for vacancy related expenses. (Ex. 3, p. 67). This is lower than Cook’s of 8.3%.

Additionally, despite not loading his capitalization rate for taxes, his rate is still higher

than Cook’s: 7.9% compared to 7.49%. A higher capitalization rate results in lower

values.

Although we recognize Olson’s methodology of developing the income approach

on a net basis has some merits, and all the appraisals in the record relied on

comparable properties that were leased on a net basis, we find a preference in ad-

valorem valuation is to load the capitalization rate. Despite this, in this case, we find

both appraisers’ conclusions are complimentary. We give both consideration and find

$23,225,000 to be a fair and reasonable estimate of the subject’s market value by the

income approach.

D. Sales Comparison Approach

1. REIT Sales

GPT asserts REIT sales should not be considered in valuing the subject

property.

Olson testified that REITs often purchase properties like the subject and tend to

pay a premium.

Cook asserts that it is the sale price that is the indicator of market value, not

whether it was purchased or sold by a REIT. In his opinion, it was reasonable to use

REIT sales in the sales comparison approach.

We note that both appraisers considered at least two comparable sales that

apparently were REIT purchases: 5500 SE Delaware Avenue, Ankeny, (Toro) and 3915

Delaware Avenue, Des Moines (Delaware). (Ex. 3, p, 74-75, 78-79, 83; Ex. B, p. 33,

and unnumbered pages following p. 35). Despite Olson’s testimony that he would not

consider REIT sales, he in fact did and did not make any quantitative adjustment for this

factor in his analysis.

15

GPT’s insistence that REIT sales not be used in the sales comparison approach

appears to be much ado about nothing. Neither appraiser took into consideration, in

analyzing comparable sales, which of those sales were purchased by a REIT, other

than Olson testifying he did not use a property directly north of the subject as a

comparable sale for this reason. As previously noted, however, both considered at

least two comparable sales that apparently were REIT purchases (Toro and Delaware

Avenue) and made no adjustment for this factor.

2. Appraisers’ Sales Comparison Approaches

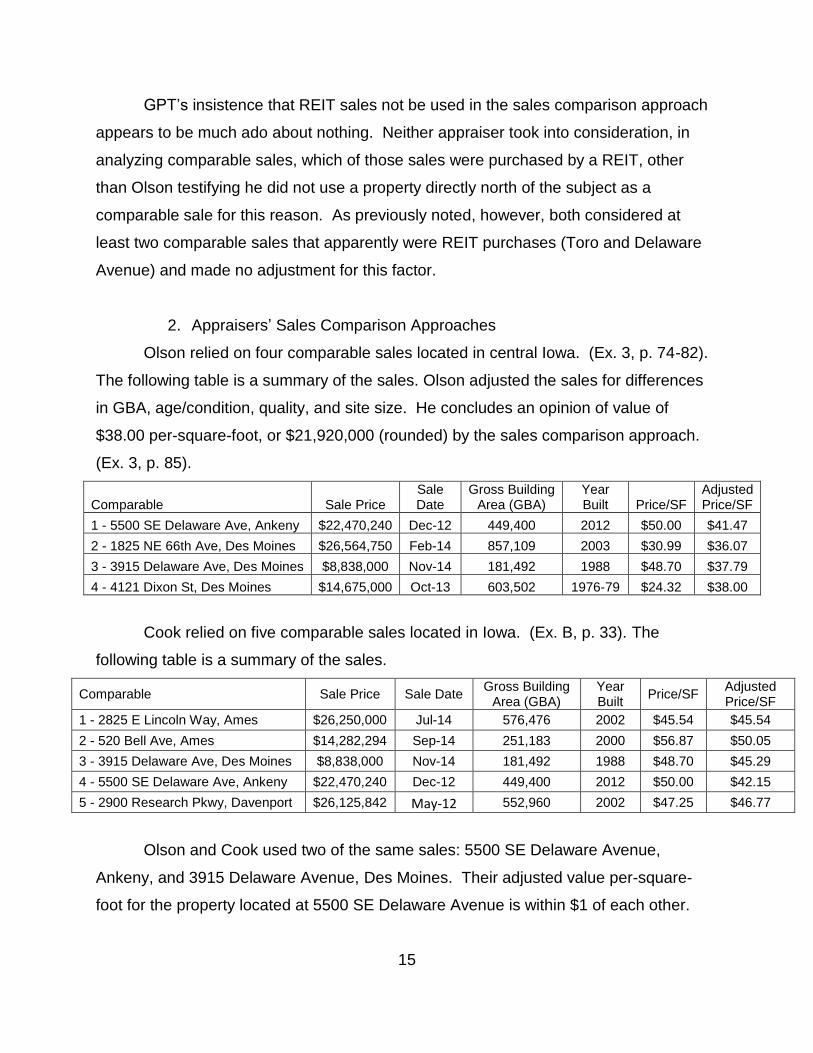

Olson relied on four comparable sales located in central Iowa. (Ex. 3, p. 74-82).

The following table is a summary of the sales. Olson adjusted the sales for differences

in GBA, age/condition, quality, and site size. He concludes an opinion of value of

$38.00 per-square-foot, or $21,920,000 (rounded) by the sales comparison approach.

(Ex. 3, p. 85).

Comparable Sale Price Sale Date

Gross Building Area (GBA)

Year Built Price/SF

Adjusted Price/SF

1 - 5500 SE Delaware Ave, Ankeny $22,470,240 Dec-12 449,400 2012 $50.00 $41.47

2 - 1825 NE 66th Ave, Des Moines $26,564,750 Feb-14 857,109 2003 $30.99 $36.07

3 - 3915 Delaware Ave, Des Moines $8,838,000 Nov-14 181,492 1988 $48.70 $37.79

4 - 4121 Dixon St, Des Moines $14,675,000 Oct-13 603,502 1976-79 $24.32 $38.00

Cook relied on five comparable sales located in Iowa. (Ex. B, p. 33). The

following table is a summary of the sales.

Comparable Sale Price Sale Date Gross Building

Area (GBA) Year Built

Price/SF Adjusted Price/SF

1 - 2825 E Lincoln Way, Ames $26,250,000 Jul-14 576,476 2002 $45.54 $45.54

2 - 520 Bell Ave, Ames $14,282,294 Sep-14 251,183 2000 $56.87 $50.05

3 - 3915 Delaware Ave, Des Moines $8,838,000 Nov-14 181,492 1988 $48.70 $45.29

4 - 5500 SE Delaware Ave, Ankeny $22,470,240 Dec-12 449,400 2012 $50.00 $42.15

5 - 2900 Research Pkwy, Davenport $26,125,842 May-12 552,960 2002 $47.25 $46.77

Olson and Cook used two of the same sales: 5500 SE Delaware Avenue,

Ankeny, and 3915 Delaware Avenue, Des Moines. Their adjusted value per-square-

foot for the property located at 5500 SE Delaware Avenue is within $1 of each other.

16

However, the two differ approximately $7.50 in adjusted value on the sale of 3915

Delaware Avenue. Olson notes the discrepancy in their opinions on this sale is primarily

the GBA adjustment he applied, which Cook did not.

Olson believes his Sale 2 (1825 NE 66th Avenue, Des Moines) is one of the best

sales available because a REIT was not involved and it was not a leased-fee sale. The

tenant purchased the property from the landlord for a negotiated price. We note a sale

from a tenant to a landlord is not typically recognized in appraisal methodology as a

sale representing market value, which generally assumes a buyer and seller with typical

motivations. § 441.21; APPRAISAL INSTITUTE, THE APPRAISAL OF REAL ESTATE 410-11

(14th ed. 2013). In the case of a tenant to landlord transaction, one or both parties may

have motivations to accept below market value or pay more than market value based on

their positions at the time of sale. This is supported by Cook’s analysis of the sale. Cook

criticized Olson’s use of this sale noting it had previously sold in March 2007 for

effectively the same price it sold for seven years later in 2014. Cook testified that when

it sold in 2014, it had a contract rent of $2.74 per-square-foot, which he believes was a

below-market rent. Further investigation by Cook revealed that Bridgestone bought out

their lease based on what they were paying. Because they purchased the property at

below-market rent, Cook asserts the resulting sale price was below market and this

explains why it sets the lower end of the range.

The Board of Review noted that Olson’s Sale 4 (4121 Dixon Street, Des Moines)

was adjusted upward 25% for age/condition and 25% for quality, for a total of a 50%

upward adjustment and questioned him regarding the comparability and reliability of this

sale to the subject. Cook notes this is an older property with much lower rents than the

subject property. He is not convinced it competes with the subject’s more modern

building. Olson admitted it was a weaker and less reliable comparable as a result of the

adjustments.

The Board of Review questioned Olson on his rationale for not including a sale

located immediately north of the subject property at 520 Bell Avenue, which was

considered by Cook. Olson testified that he did not use the sale because it was a REIT

transaction involving multiple properties.

17

Cook’s Sale 1 (2825 E Lincoln Way, Ames) is the subject property. Cook

believes it is important to look at the subject sale to test its sale price per-square-foot

against other sales to determine if it is a fair market sale price and not influenced by

being a REIT purchase. Cook was aware that the $17,000,000 mortgage at 5% was

assumed by GPT as part of the purchase, which was slightly above market rates of

4.5% at that time. However, comparing this sale to other market sales, he did not see

any undue influence, upward or downward, to the sale price per-square-foot. Moreover,

based on conversations with the listing broker, Dick Powell, Cook believed it was a

cash-equivalency sale.

Cook’s Sale 2 (520 Bell Avenue, Ames) is located immediately north of the

subject. Cook notes that while the building is smaller than the subject, it is still

considered a large building in the market. It is 23% air-conditioned, some unfinished

mezzanine space, and the finished area is about 4% of the total. Because of its location

and many similar features to the subject, Cook believed it was not a sale he could

ignore. We agree. GPT was critical of Cook for not making an adjustment for the

differences in GBA. Cook asserts he considered the size of this property within his

overall analysis, and did not feel compelled to make an adjustment because many of

the features of this property compared to the subject were offsetting. GPT noted that

the buyer of this property was also a REIT. Cook admitted that he did not have specific

terms of the sale.

Both Cook and Olson relied on the sale located at 3915 Delaware Avenue, Des

Moines. Cook testified it has 9.2% office space, 24 foot wall height, and he considers it

a distribution warehouse because of the number of dock doors. Cook adjusted this sale

downward for the significantly higher amount of finished space. Similar to its critique of

Cook’s Sale 2 (520 Bell Avenue, Ames), GPT questioned why Cook did not make an

adjustment for the smaller GBA of this sale. Cook’s response was the same as his

rationale for not adjusting Bell Avenue for its smaller GBA.

Cook’s Sale 4 (5500 SE Delaware Avenue, Ankeny) was also used by Olson

(Sale 1). Cook testified this is a distribution warehouse, 80% dock-high floors, 29-foot

wall height, and 1.4% of the building is devoted to offices. This was a REIT sale. Cook

18

did not know the terms of the sale. He confirmed the sale price from the Declaration of

Value (DOV). PAAB notes that Olson also did not adjust this sale, despite it being a

REIT transaction. It is unknown if he chose not to adjust it despite being a REIT

transaction; or knew it was a REIT and chose not to adjust it. If the former is correct,

then it further demonstrates the difficulties of analysts being able to confirm the intricate

details and specific properties that may be part of a REIT transaction. If the latter is

correct, it indicates that a REIT transaction is a reasonable representation of the fair

market value; and would also suggest that the subject sale represents market value.

Lastly, Cook included Sale 5 (2900 Research Parkway, Davenport), which is

located in a newer industrial development in Davenport. It has less than 2% office

finish, 32 foot clearance height, 75 truck docks, and John Deere has a 15-year lease

$2.53 per-square-foot with an escalation clause. GPT also asserts this was a REIT

purchase. Cook was unclear as to whether the Grantee, listed as ARCP JDDPTIA01,

LLC, was a REIT. Again, PAAB finds this demonstrates the difficulties in determining

when a transaction has REIT involvement.

After adjusting the sales for differences, Cook concludes an opinion of value of

$45.00 per-square-foot, or $25,940,000 (rounded) by the sales comparison approach.

(Ex. B, p. 35).

3. Analysis & Conclusion

The sales comparison approach is the preferred method of valuation under Iowa

law. Having fully considered the foregoing evidence, we conclude that while there are

sales available to develop a sales comparison approach, there are concerns about the

reliability of the data. Specifically, REITs are the primary seller and purchasers of

properties comparable to the subject, and there is a disagreement amongst

professionals as to whether this may or may not reflect the fee-simple fair market value

of the properties. In the end, both parties relied on REIT sales either knowingly or

unknowingly.

While there were differences between the appraisers in the sales they selected

for analysis as well as the adjustments they applied, we find both analyses are generally

reasonable. However, Olson relied on a sale (1825 NE 66th Avenue, Des Moines)

19

between a tenant and landlord, and based on Cook’s analysis of it, we question whether

it represents a fair market value. In this case the tenant was able to buy-out the lease

and purchase the property based on below-market rents; resulting in what appears to

be a below-market sale price and, arguably, a leased-fee value. Olson did not adjust for

this factor, and considered it “one of the best sales available.” This sale set the lower

end of his range, and it appears he simply averaged the adjusted values of his four

sales to arrive at his value conclusion of $38.00 per square foot.

We also note that despite differences between the two appraisers’ analyses, they

both relied on the Toro sale (5500 SE Delaware Avenue, Ankeny) and both arrived at

an adjusted value of this sale of roughly $42 per square foot. This adjusted value, of

what appears to be the most comparable property in the record, is at the high end of

Olson’s range and the low end of Cook’s range. Giving it the most consideration, we

find a fair and reasonable value of the subject property by the sales comparison

approach is $24,212,000 (rounded), which is only slightly higher than simply averaging

the conclusion of both appraisers.

Conclusion

Olson considered all of the approaches to value. He testified that most weight

was given to the income approach because it is an income-driven property. He also

believes the cost approach is a strong indicator of value. He reasserts the sales

comparison approach is difficult to develop because many sales represented a leased-

fee transaction reducing the reliability of this approach. He reconciles the three

approaches to an opinion of $22,500,000, as of January 1, 2015. Despite testifying that

he gave the income approach the most consideration, we note his final opinion is very

near the average of three approaches.

Cook gave some weight to all of the approaches to value. He gave 20%

emphasis on the cost approach, because there is a lot of warehouse space being built –

which impacts the marketability of the subject property that would compete with the new

construction. Cook gave most consideration to the sales comparison approach

because in his opinion he had five comparable sales, including the subject, with overall

20

minimal adjustments required, resulting in a reliable range of value. For this reason, he

has a lot of confidence in the sales comparison approach and gave it 50% weight.

Cook believes the income approach is also a viable indicator of value because of the

available data to examine the market rents. He gave the income approach 30%. He

reconciles the three approaches to an opinion of $25,150,000, as of January 1, 2015.

GPT believes the subject’s fair market value cannot be readily established by the

sales comparison approach alone, and thus the other approaches to value must be

considered. On the other hand, the Board of Review contends that the sales

comparison approach can establish the subject’s value without turning to the other

approaches. Here, both appraisers relied, in part, on REIT sales, either knowingly or

unknowingly, and it has been suggested REIT sales may not be reflective of market

value. At the same time, the appraisers did not rely solely on the sales comparison

approach to value in reconciling to their final value conclusions. For these reasons, we

find the subject’s fair market value cannot readily be established by the sales

comparison approach alone and must examine the other value approaches.

Typically, PAAB finds the cost approach a relevant approach, specifically in

property like the subject that is of modern construction with no functional or external

obsolescence noted. However, in this case there is disagreement regarding the type of

warehouse, which would directly impact the base costs used in this analysis. Moreover,

we find there is ample market data available to develop the income and sales

comparison approaches, which were both developed and heavily relied on by both

Olson and Cook. For these reasons, we do not give consideration to the cost approach

and rely solely on the income and sales comparison approaches.

Olson gave his sales comparison analysis 33% weight and Cook gave his sales

comparison analysis 50% weight. Likewise, both appraisers developed the income

approach and arrived at near identical conclusions. Moreover, we note that market

participants would place considerable weight on the income analysis as this is primarily

purchased as an income producing asset. Therefore, we give equal weight to the sales

comparison and income approaches to value and find a reasonable, fair estimate of the

subject’s market value is $23,718,500.

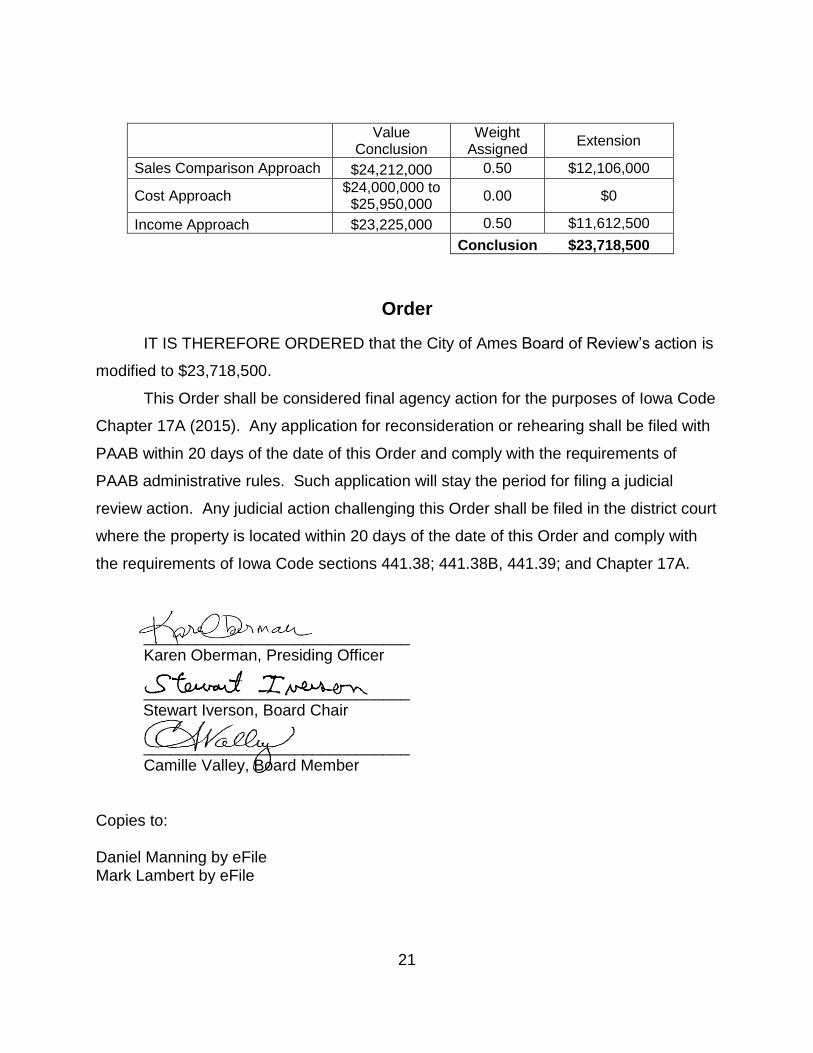

21

Value

Conclusion Weight

Assigned Extension

Sales Comparison Approach $24,212,000 0.50 $12,106,000

Cost Approach $24,000,000 to $25,950,000

0.00 $0

Income Approach $23,225,000 0.50 $11,612,500

Conclusion $23,718,500

Order

IT IS THEREFORE ORDERED that the City of Ames Board of Review’s action is

modified to $23,718,500.

This Order shall be considered final agency action for the purposes of Iowa Code

Chapter 17A (2015). Any application for reconsideration or rehearing shall be filed with

PAAB within 20 days of the date of this Order and comply with the requirements of

PAAB administrative rules. Such application will stay the period for filing a judicial

review action. Any judicial action challenging this Order shall be filed in the district court

where the property is located within 20 days of the date of this Order and comply with

the requirements of Iowa Code sections 441.38; 441.38B, 441.39; and Chapter 17A.

______________________________ Karen Oberman, Presiding Officer

______________________________

Stewart Iverson, Board Chair

______________________________ Camille Valley, Board Member

Copies to: Daniel Manning by eFile Mark Lambert by eFile