Embed Size (px)

Citation preview

Projection of ACC Long Term Claim Numbers

weekly compensation

Todd NicholsonBee Wong Sim

22 November 2010

Outline• Purpose

• Background

• Modelling

Section 1: Purpose• Project the future size of the long-term claims pool

• Gain an insight into the characteristics of long-term claims

• Allow testing under different scenarios

• Assist in claims liability estimates

• Provide impact of targeted intervention analysis

• This model: weekly compensation claims

Section 2: Background

Weekly Compensation

• Definitions – weekly compensation (“WC”)– long term claims

• Outstanding claims liability provision for WC at June 2010 is $6.7 billion – 90% due to claims active one year post accident

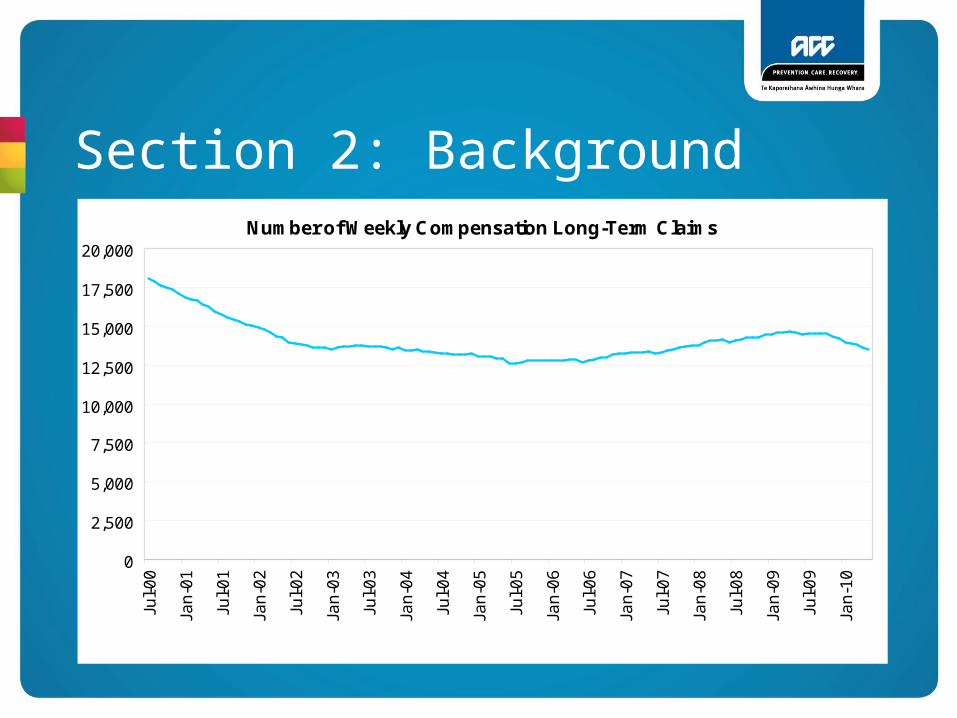

Section 2: BackgroundNumber of Weekly Compensation Long-Term Claims

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

Jul-

00

Jan

-01

Jul-

01

Jan

-02

Jul-

02

Jan

-03

Jul-

03

Jan

-04

Jul-

04

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

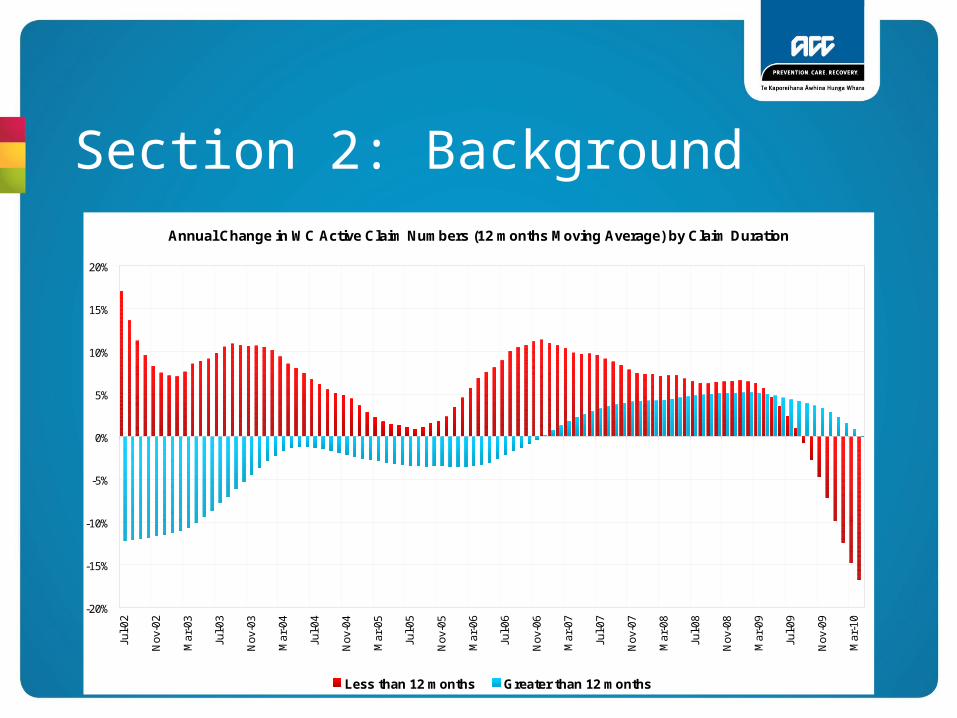

Section 2: BackgroundAnnual Change in WC Active Claim Numbers (12 months Moving Average) by Claim Duration

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

Jul-0

2

Nov

-02

Mar

-03

Jul-0

3

Nov

-03

Mar

-04

Jul-0

4

Nov

-04

Mar

-05

Jul-0

5

Nov

-05

Mar

-06

Jul-0

6

Nov

-06

Mar

-07

Jul-0

7

Nov

-07

Mar

-08

Jul-0

8

Nov

-08

Mar

-09

Jul-0

9

Nov

-09

Mar

-10

Less than 12 months Greater than 12 months

Section 2: Background

External Environment

• Recession

• Political landscape

• Decline in new claims

Section 2: Background

Internal Environment

• Renewed case management focus

• Changes to operations model

Section 2: Background

Old Operations Model

• Front-end and volume driven

• Process compliance focused

• Case management focus on new claims to detriment of long-term claims management

Section 2: Background

New Operations Model

• Get back to basics

• Auto-streaming

• Experts review to identify “at risk” claims

• Expert early psycho-social screening

Section 2: Background

Recover Independence Service (“RIS”)

• New specialist rehabilitation team

• Set up in July 2009

• Focuses on claims that have received weekly compensation in excess of 2.5 years

• Increased number of case managers

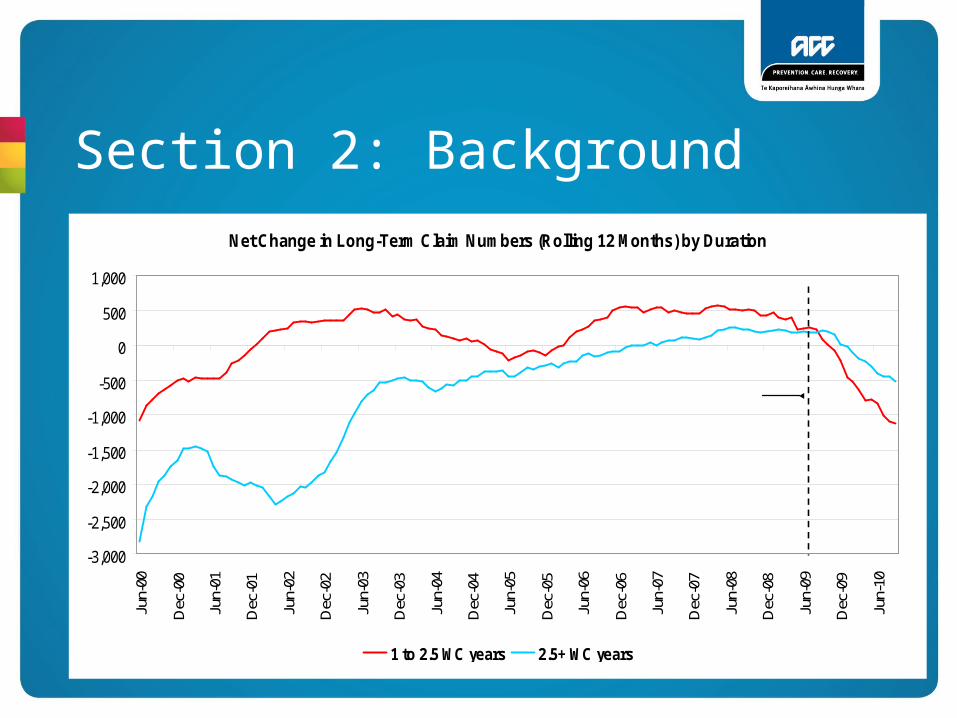

Section 2: BackgroundNet Change in Long-Term Claim Numbers (Rolling 12 Months) by Duration

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

500

1,000

Jun-

00

Dec

-00

Jun-

01

Dec

-01

Jun-

02

Dec

-02

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

1 to 2.5 WC years 2.5+ WC years

RIS established

Section 2: Background

Questions:

• Favourable experience in the past 6 months

• How significant is the “RIS” factor

• How long is it likely to last

• Project future WC claim numbers

Section 3: Model1. Segment the existing long-term WC claims pool to

understand claim-mix

2. Construct a survival analysis model to determine which factors influence claim duration

3. Construct a simulation model to project future long-term claim numbers

Section 3: Model

Data

Segmentation• Claims that had payments since 1 Jan 2000 and had

more than 365 WC days

Survival Analysis• Claims began on or after 1 Jan 2000 and had more than

365 WC days

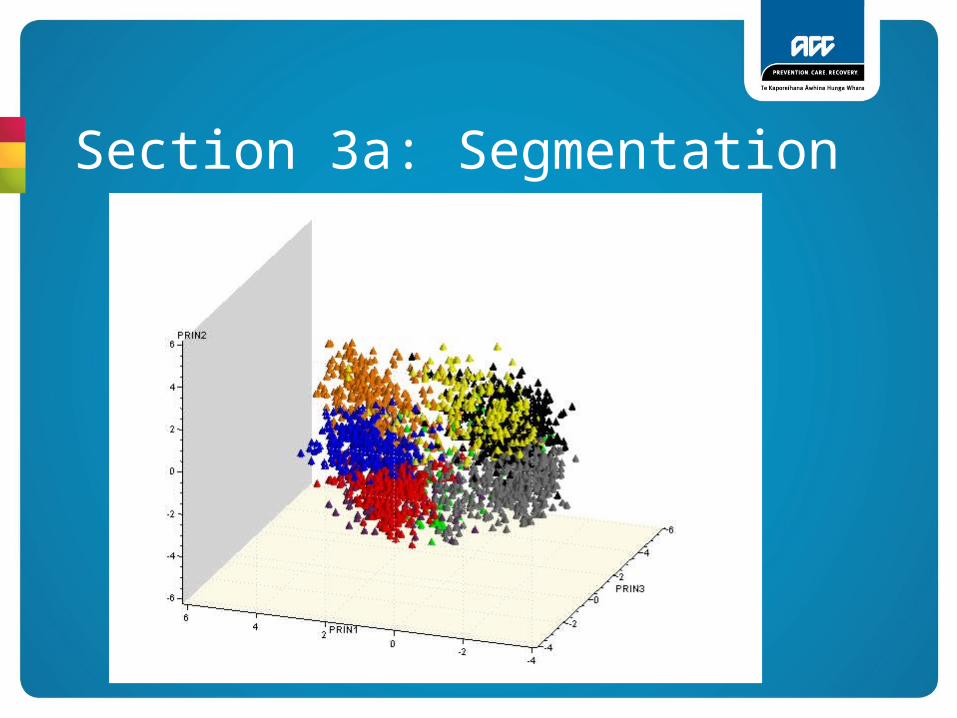

Section 3a: Segmentation• Use Principal Components Analysis to

– Identify the underlying factors that influenced claim characteristics

• 5 principal components

• Separate permanent pension and serious injury claims

• Use Cluster Analysis to

– Divide the remaining claims into segments– Further divide segment 1 into 2 segments (denoted 1A and 1B)

• 8 distinct segments

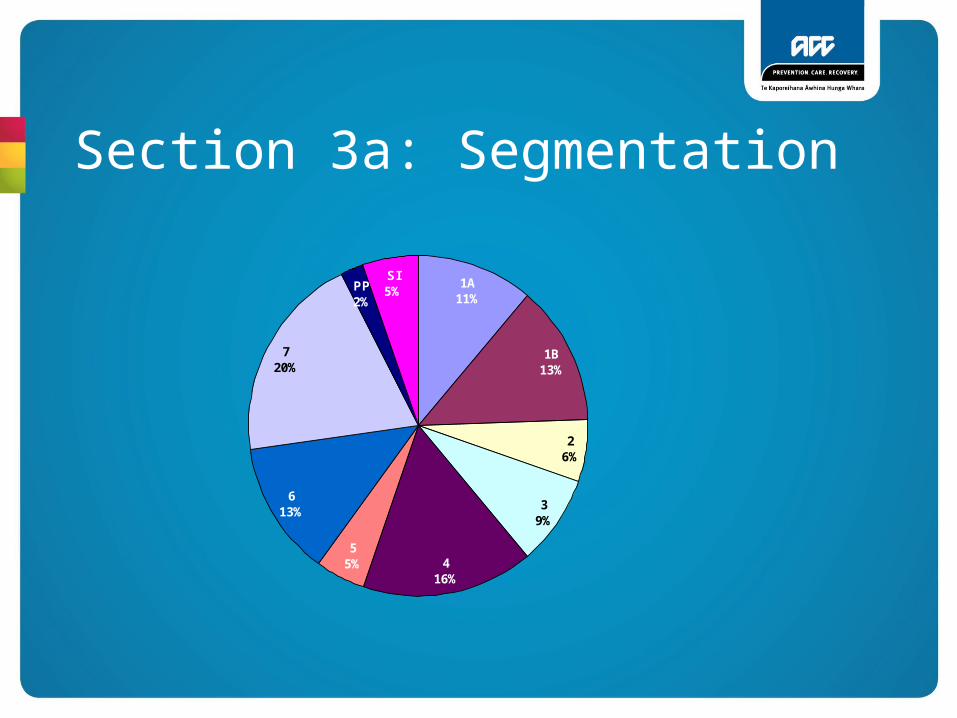

Section 3a: Segmentation

1A11%

1B13%

416%

55%

613%

SI5%

720%

39%

26%

PP2%

Section 3a: Segmentation

Section 3a: Segmentation

Section 3a: Segmentation

Section 3a: Segmentation

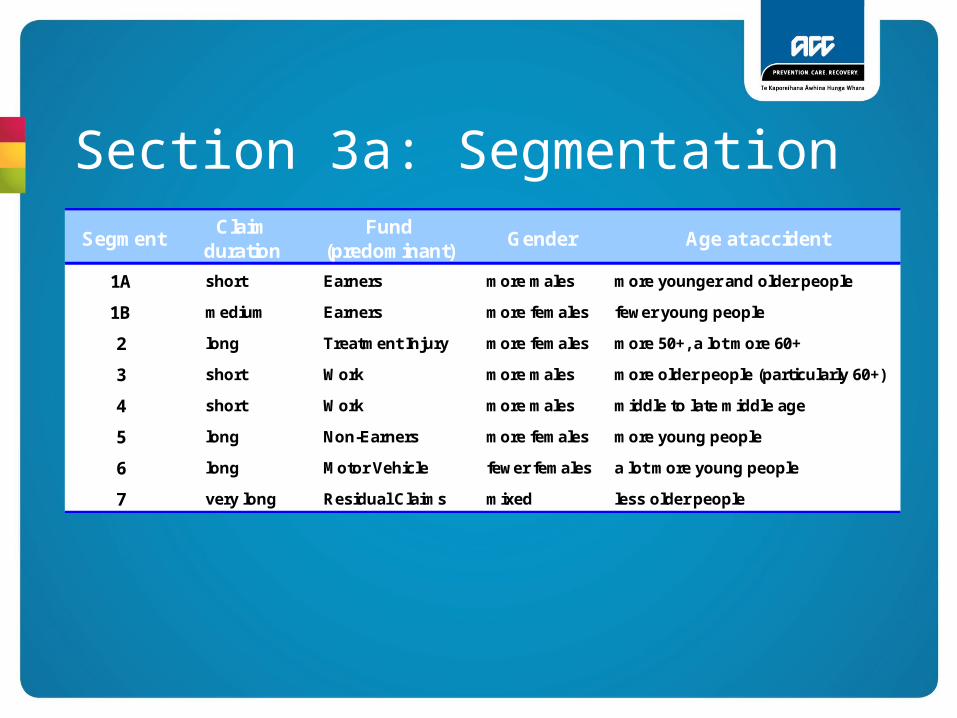

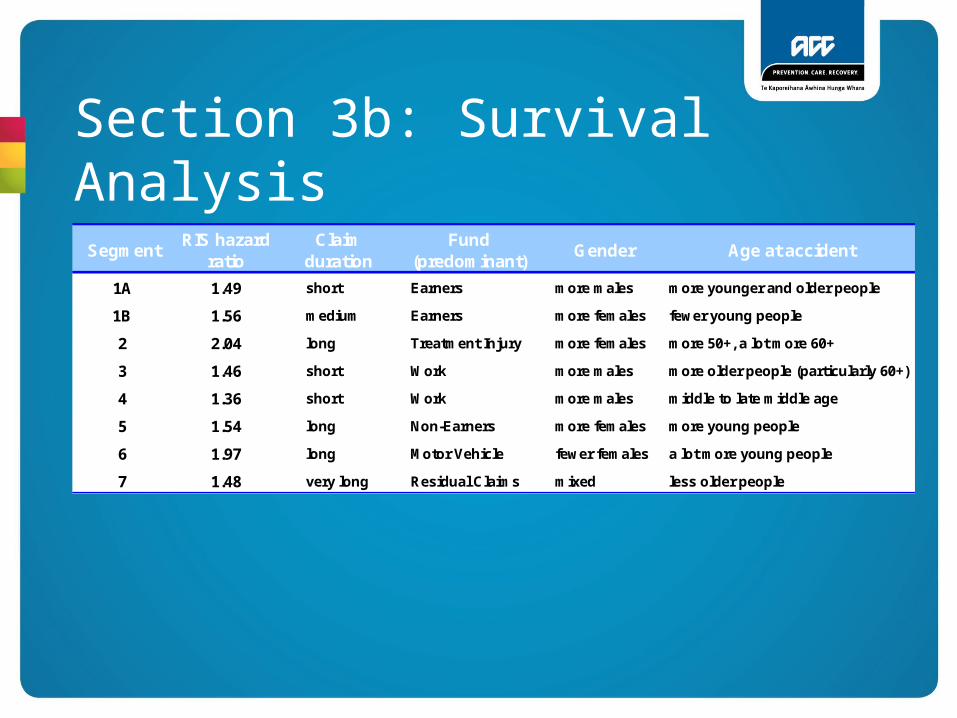

Section 3a: SegmentationSegment

Claim duration

Fund (predominant)

Gender Age at accident

1A short Earners more males more younger and older people

1B medium Earners more females fewer young people

2 long Treatment Injury more females more 50+, a lot more 60+

3 short Work more males more older people (particularly 60+)

4 short Work more males middle to late middle age

5 long Non-Earners more females more young people

6 long Motor Vehicle fewer females a lot more young people

7 very long Residual Claims mixed less older people

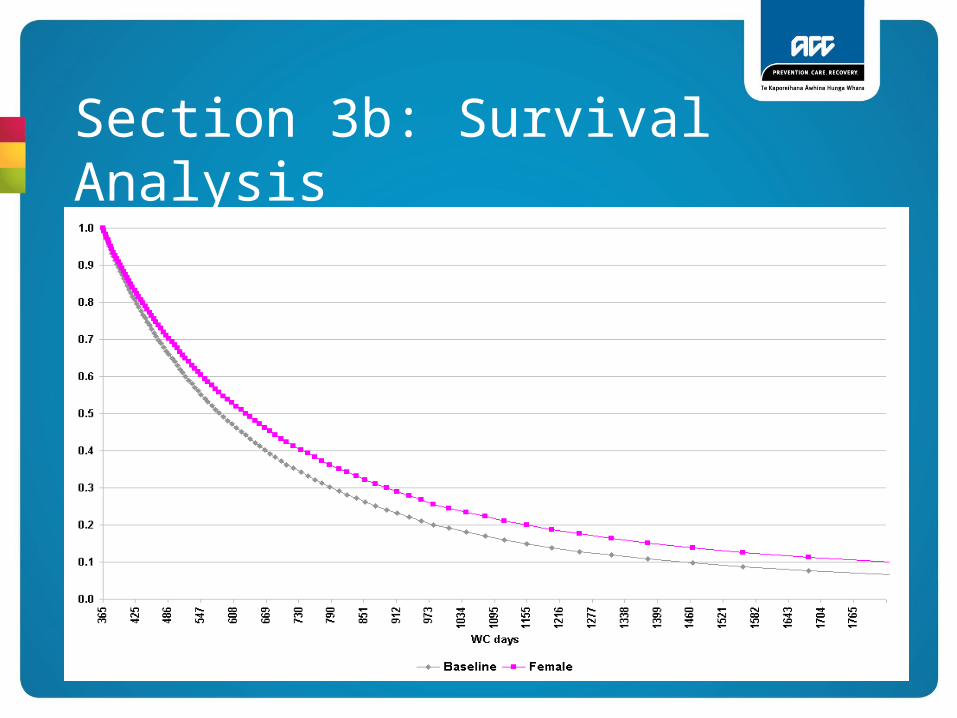

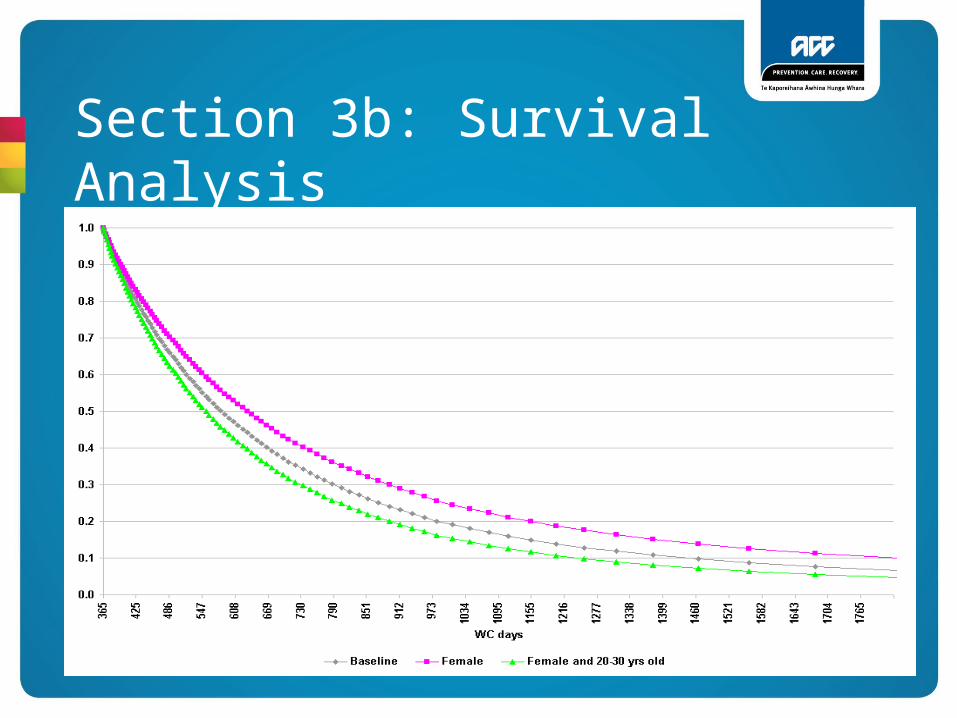

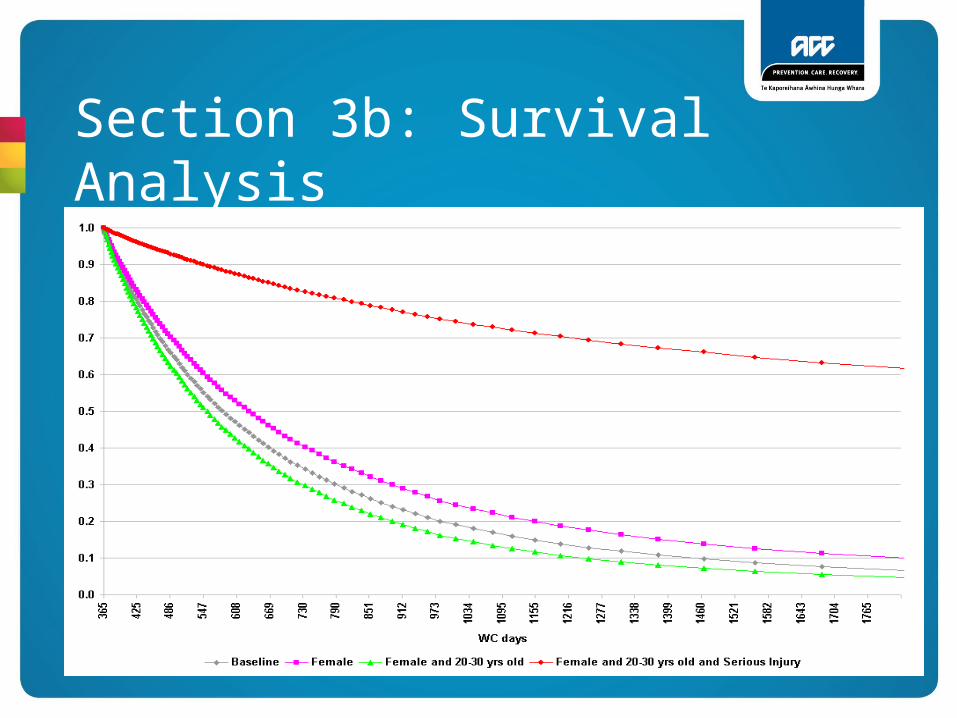

Section 3b: Survival Analysis• Use Survival Analysis to project duration for claims

with WC days longer than 365 days

• Use only claims data from January 2000 onwards

• Proportion hazards was used (after the assumptions were tested)

• Use claim related variables that are invariant to time, except for transfer to RIS.

Section 3b: Survival Analysis• lag between injury and lodgement of claim• multiple injury indicator• injury diagnosis• injury site• scene of injury• serious injury indicator• at work injury indicator• occupation• pre-injury work strenuousness• hours at weekend indicator• WC rate per week• gender• age at start of WC payment

Section 3b: Survival Analysis

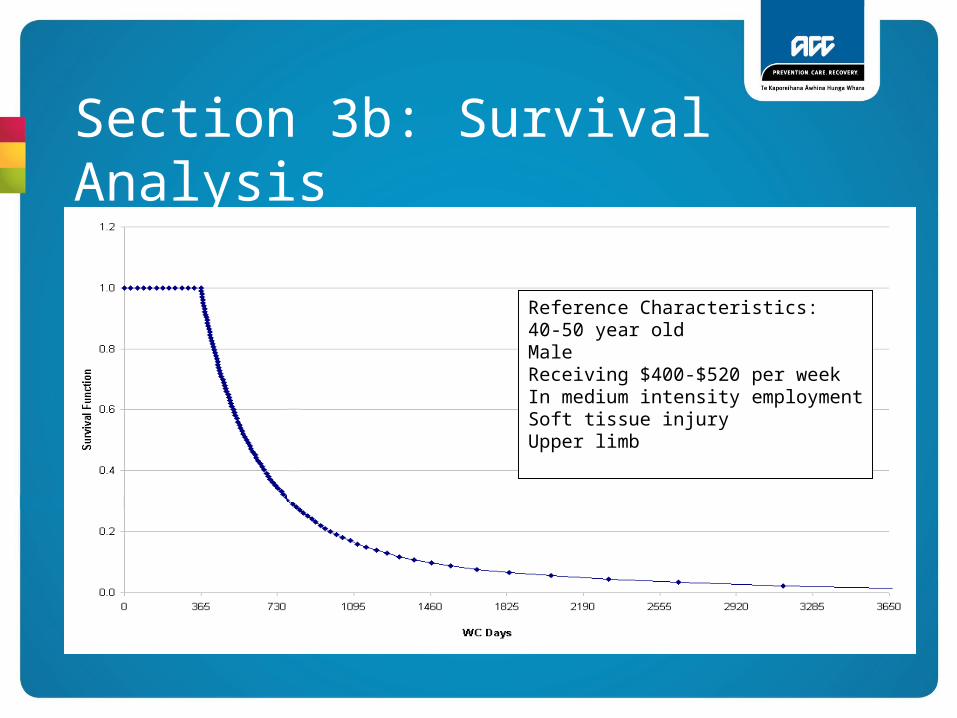

Reference Characteristics:40-50 year oldMaleReceiving $400-$520 per weekIn medium intensity employmentSoft tissue injuryUpper limb

Section 3b: Survival Analysis

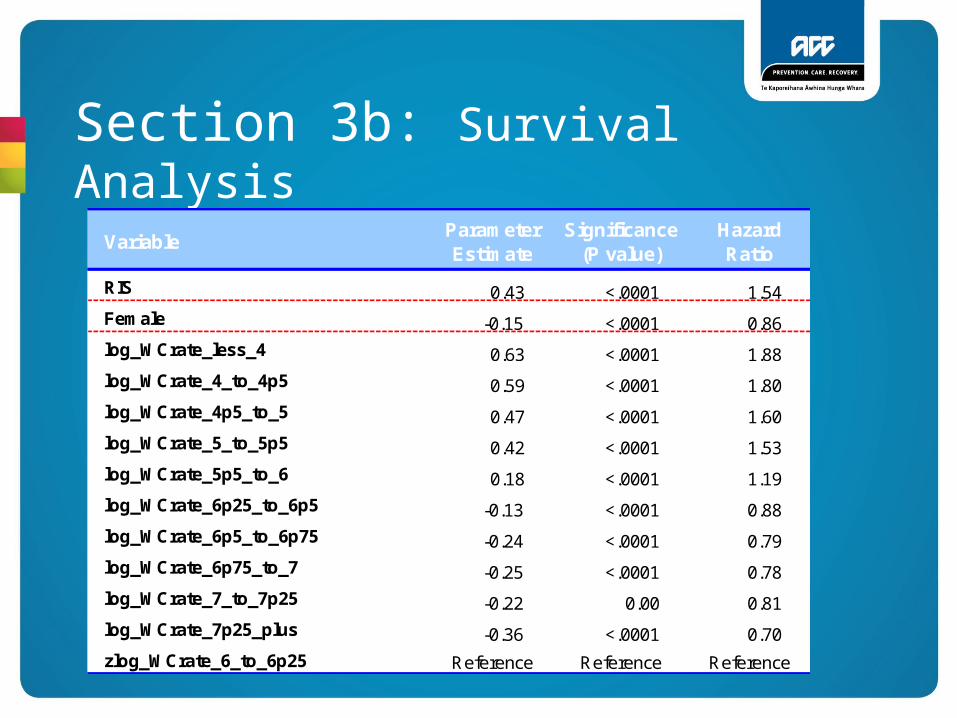

VariableParameter Estimate

Significance (P value)

Hazard Ratio

RIS 0.43 <.0001 1.54

Female -0.15 <.0001 0.86

log_WCrate_less_4 0.63 <.0001 1.88

log_WCrate_4_to_4p5 0.59 <.0001 1.80

log_WCrate_4p5_to_5 0.47 <.0001 1.60

log_WCrate_5_to_5p5 0.42 <.0001 1.53

log_WCrate_5p5_to_6 0.18 <.0001 1.19

log_WCrate_6p25_to_6p5 -0.13 <.0001 0.88

log_WCrate_6p5_to_6p75 -0.24 <.0001 0.79

log_WCrate_6p75_to_7 -0.25 <.0001 0.78

log_WCrate_7_to_7p25 -0.22 0.00 0.81

log_WCrate_7p25_plus -0.36 <.0001 0.70

zlog_WCrate_6_to_6p25 Reference Reference Reference

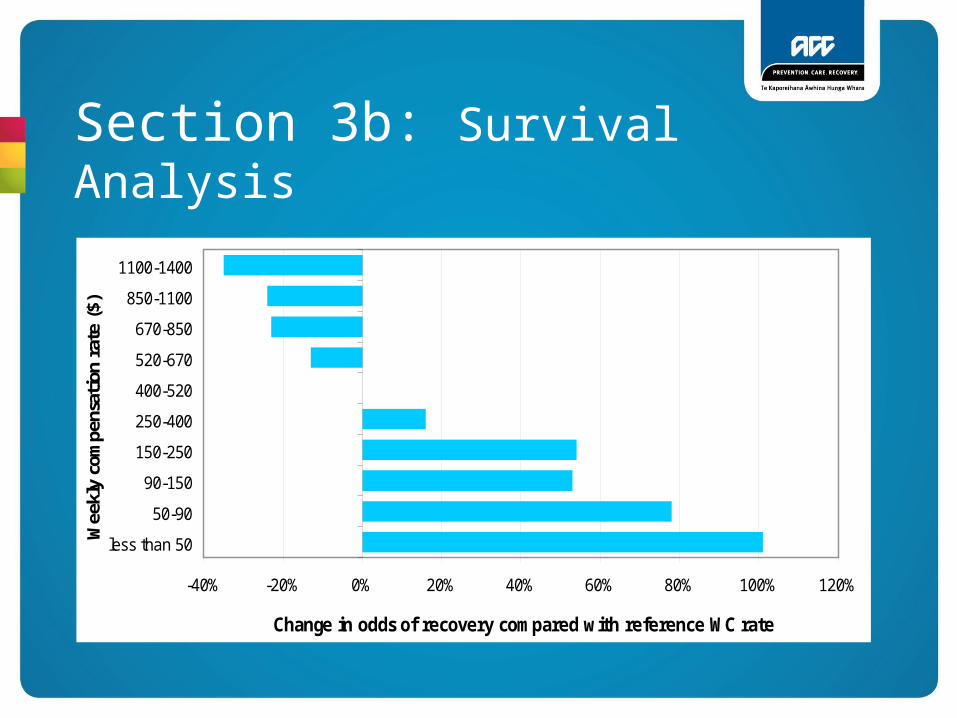

Section 3b: Survival Analysis

-40% -20% 0% 20% 40% 60% 80% 100% 120%

less than 50

50-90

90-150

150-250

250-400

400-520

520-670

670-850

850-1100

1100-1400

Wee

kly

com

pens

atio

n ra

te ($)

Change in odds of recovery compared with reference WC rate

Reference

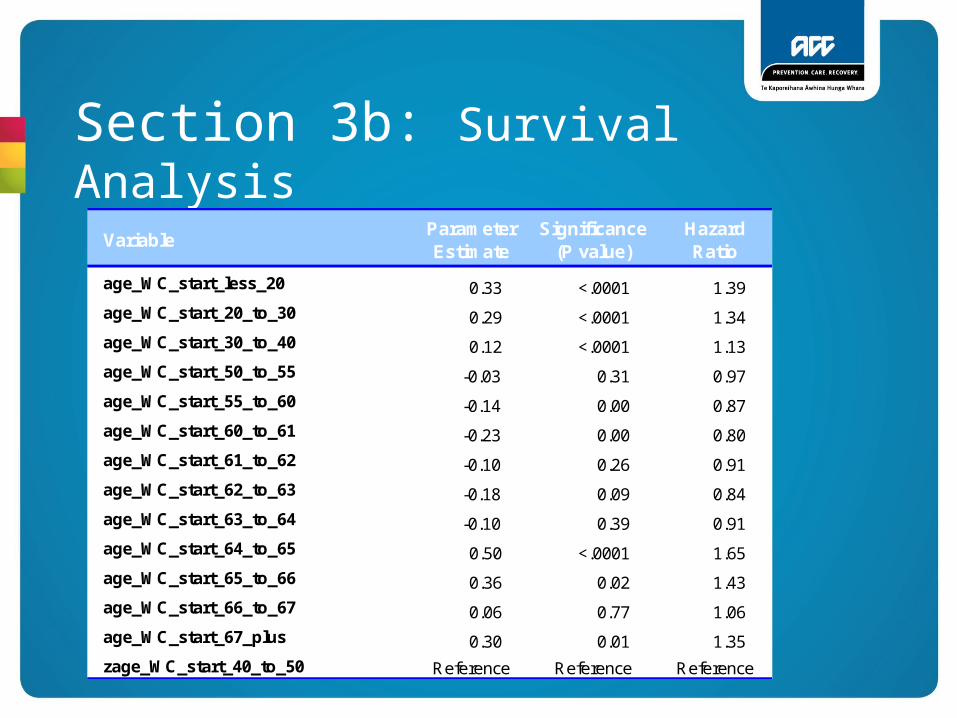

Section 3b: Survival Analysis

VariableParameter Estimate

Significance (P value)

Hazard Ratio

age_WC_start_less_20 0.33 <.0001 1.39

age_WC_start_20_to_30 0.29 <.0001 1.34

age_WC_start_30_to_40 0.12 <.0001 1.13

age_WC_start_50_to_55 -0.03 0.31 0.97

age_WC_start_55_to_60 -0.14 0.00 0.87

age_WC_start_60_to_61 -0.23 0.00 0.80

age_WC_start_61_to_62 -0.10 0.26 0.91

age_WC_start_62_to_63 -0.18 0.09 0.84

age_WC_start_63_to_64 -0.10 0.39 0.91

age_WC_start_64_to_65 0.50 <.0001 1.65

age_WC_start_65_to_66 0.36 0.02 1.43

age_WC_start_66_to_67 0.06 0.77 1.06

age_WC_start_67_plus 0.30 0.01 1.35

zage_WC_start_40_to_50 Reference Reference Reference

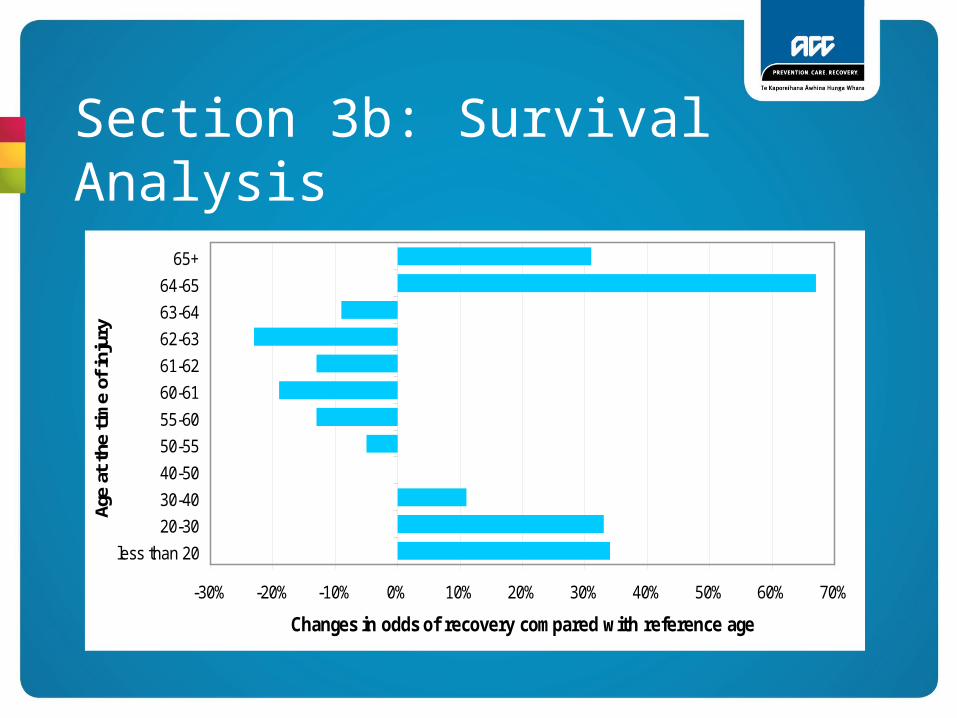

Section 3b: Survival Analysis

-30% -20% -10% 0% 10% 20% 30% 40% 50% 60% 70%

less than 20

20-30

30-40

40-50

50-55

55-60

60-61

61-62

62-63

63-64

64-65

65+

Age

at t

he t

ime

of in

jury

Changes in odds of recovery compared with reference age

Reference

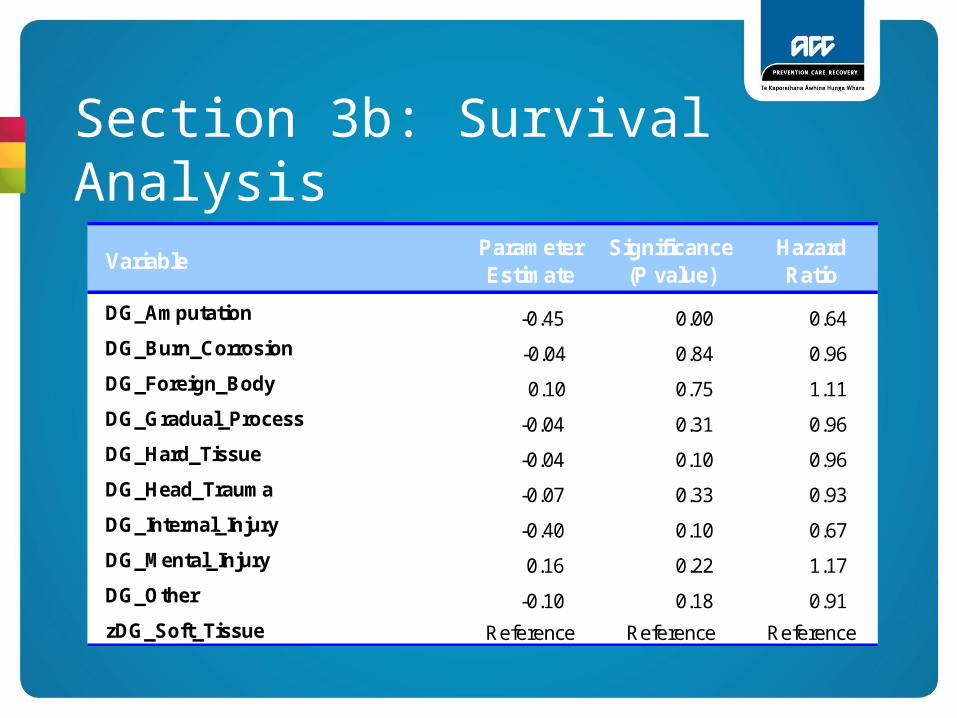

Section 3b: Survival Analysis

VariableParameter Estimate

Significance (P value)

Hazard Ratio

DG_Amputation -0.45 0.00 0.64

DG_Burn_Corrosion -0.04 0.84 0.96

DG_Foreign_Body 0.10 0.75 1.11

DG_Gradual_Process -0.04 0.31 0.96

DG_Hard_Tissue -0.04 0.10 0.96

DG_Head_Trauma -0.07 0.33 0.93

DG_Internal_Injury -0.40 0.10 0.67

DG_Mental_Injury 0.16 0.22 1.17

DG_Other -0.10 0.18 0.91

zDG_Soft_Tissue Reference Reference Reference

Section 3b: Survival Analysis

SegmentRIS hazard

ratioClaim

durationFund

(predominant)Gender Age at accident

1A 1.49 short Earners more males more younger and older people

1B 1.56 medium Earners more females fewer young people

2 2.04 long Treatment Injury more females more 50+, a lot more 60+

3 1.46 short Work more males more older people (particularly 60+)

4 1.36 short Work more males middle to late middle age

5 1.54 long Non-Earners more females more young people

6 1.97 long Motor Vehicle fewer females a lot more young people

7 1.48 very long Residual Claims mixed less older people

Section 3b: Survival Analysis

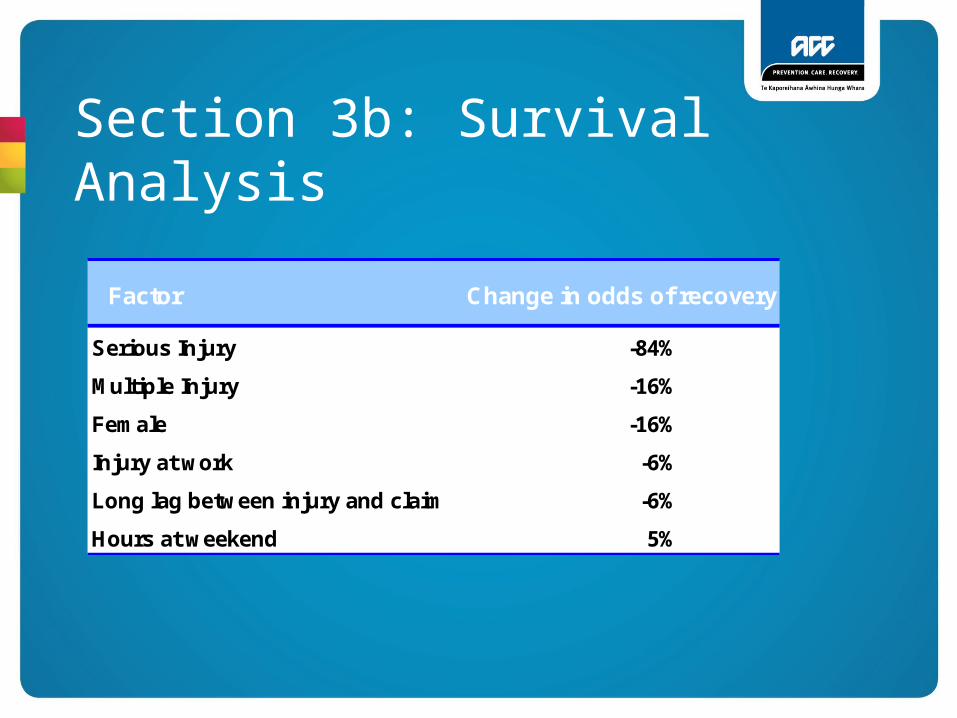

Factor Change in odds of recovery

Serious Injury -84%

Multiple Injury -16%

Female -16%

Injury at work -6%

Long lag between injury and claim -6%

Hours at weekend 5%

Section 3b: Survival Analysis

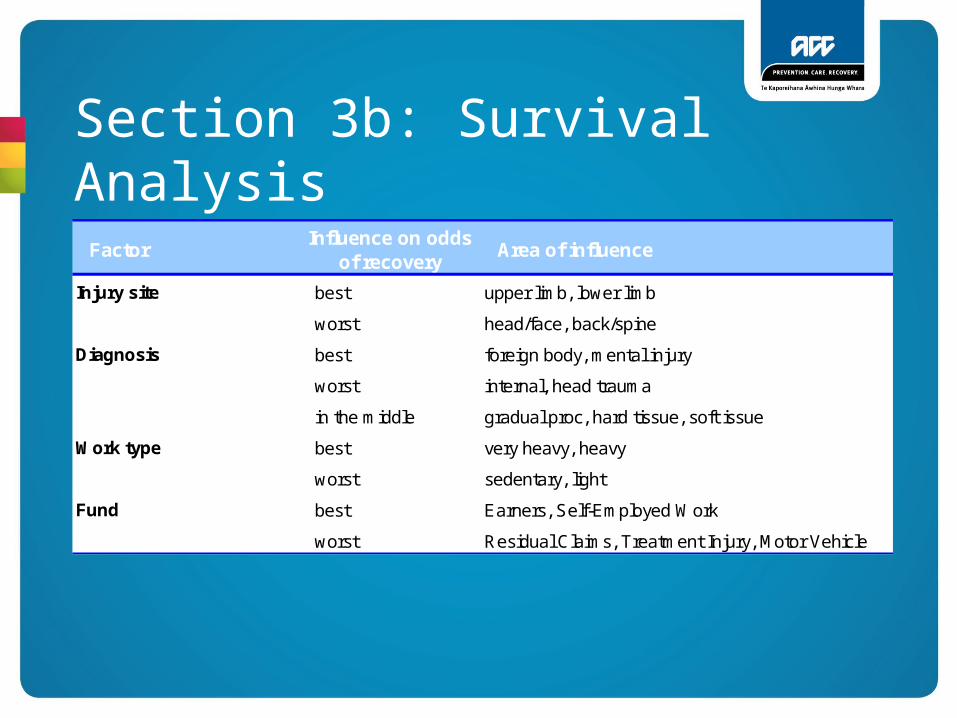

FactorInfluence on odds

of recoveryArea of influence

Injury site best upper limb, lower limb

worst head/face, back/spine

Diagnosis best foreign body, mental injury

worst internal, head trauma

in the middle gradual proc, hard tissue, soft issue

Work type best very heavy, heavy

worst sedentary, light

Fund best Earners, Self-Employed Work

worst Residual Claims, Treatment Injury, Motor Vehicle

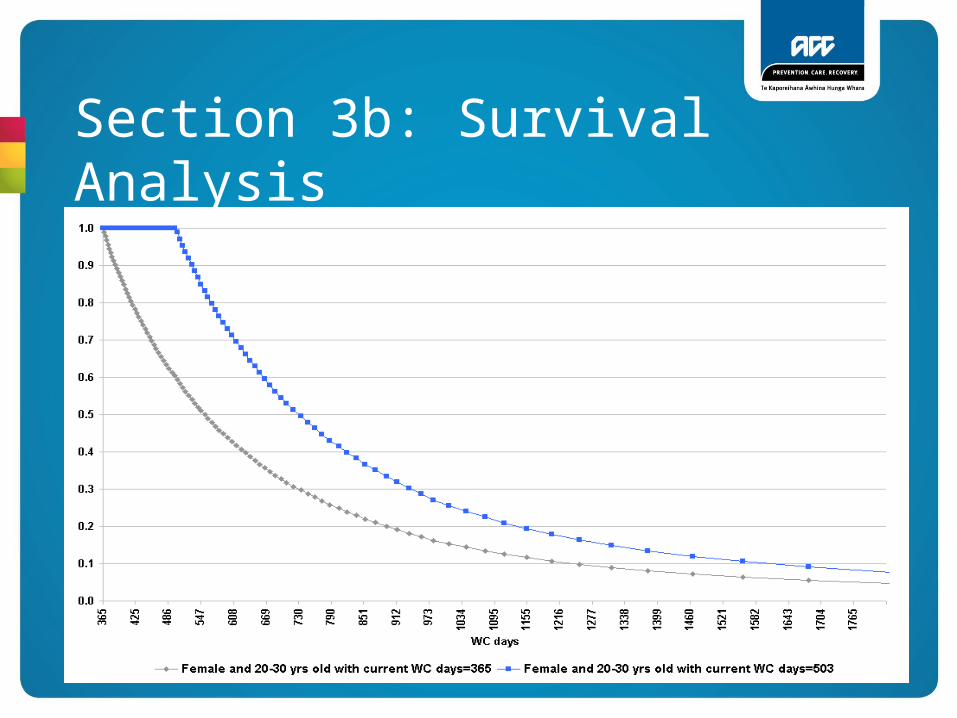

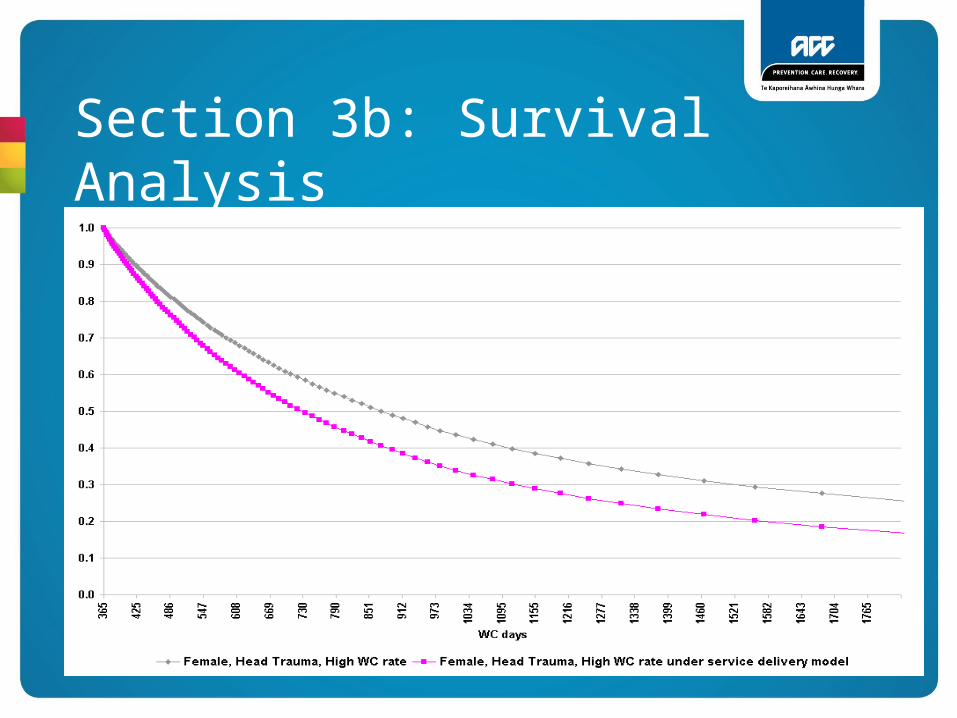

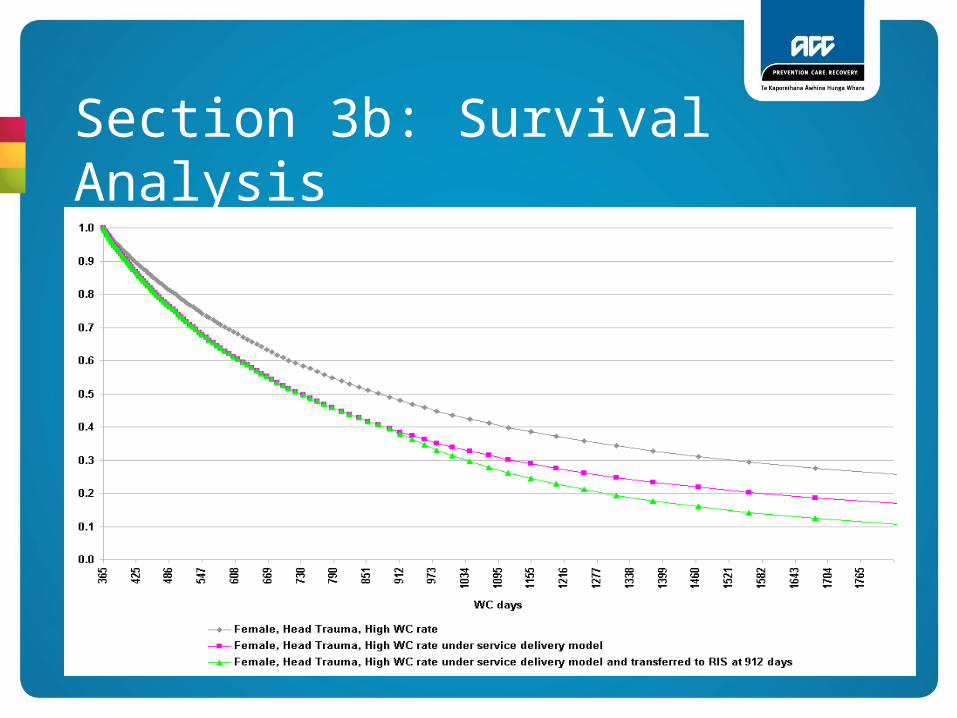

Section 3b: Survival AnalysisTo get the predicted survival curve for each claim we:

• Take the baseline survival curve

• Adjust for the claim characteristics

• Adjust for how long they have survived so far

• Adjust for the introduction of the service delivery model

• Adjust for the claim being transferred to the RIS team

Section 3b: Survival Analysis

Section 3b: Survival Analysis

Section 3b: Survival Analysis

Section 3b: Survival Analysis

Section 3b: Survival Analysis

Section 3b: Survival Analysis

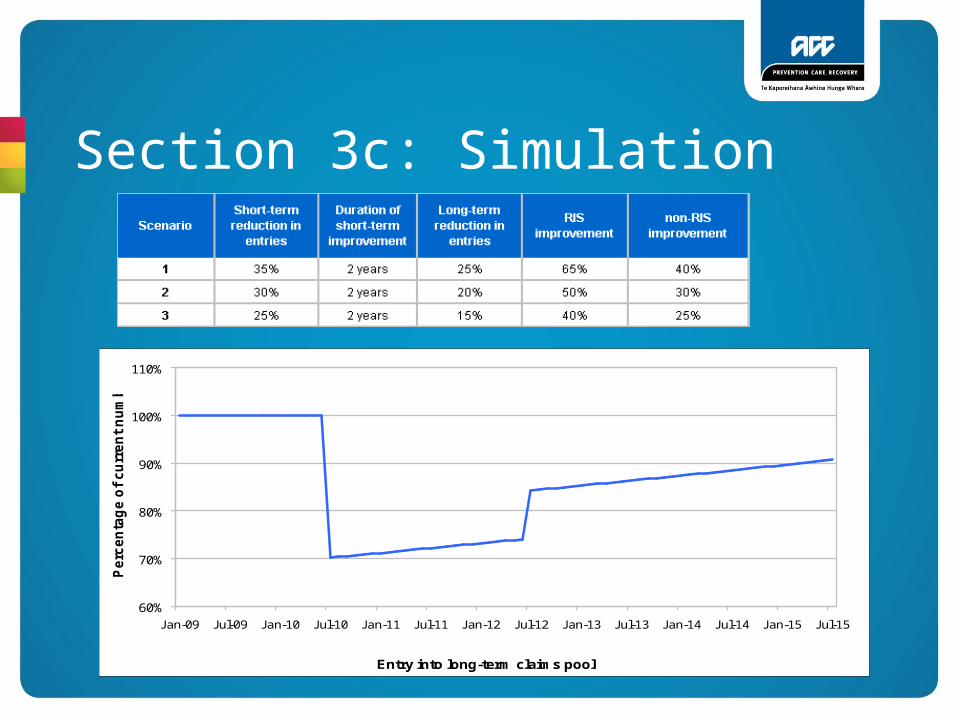

Section 3c: SimulationIn the simulation each claim has a simulated opening

and closing date. The advantages of using a simulation include:

• Easier for non-statistical audience to understand the output

• Output has the same format as real data so we can run any existing report on the simulated data

• Easier to track changes in the case mix

• Easier to trial different scenarios such as number and case mix of new claims

Section 3c: SimulationModelling Steps

• Determine the baseline survival function for each claim

• Adjust for individual claim characteristics, the influence of RIS and the service delivery model

• Generate a random number ( U[0,1] ) and use it to determine the closing duration of the claim

• Simulate new claims by taking the last year of claims and putting them in again each year

Section 3c: Simulation

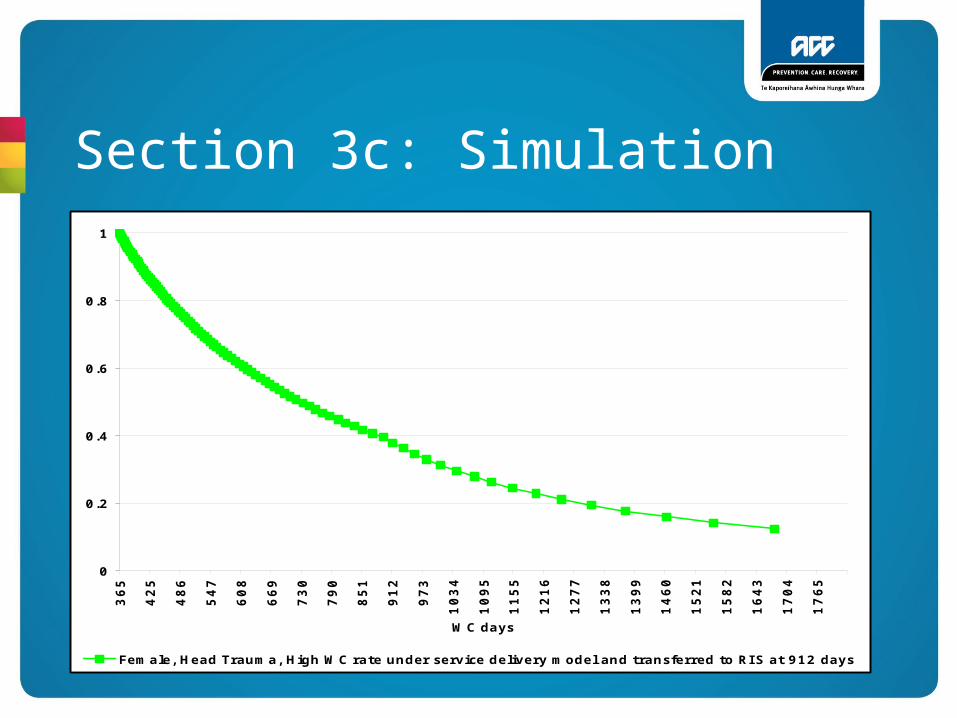

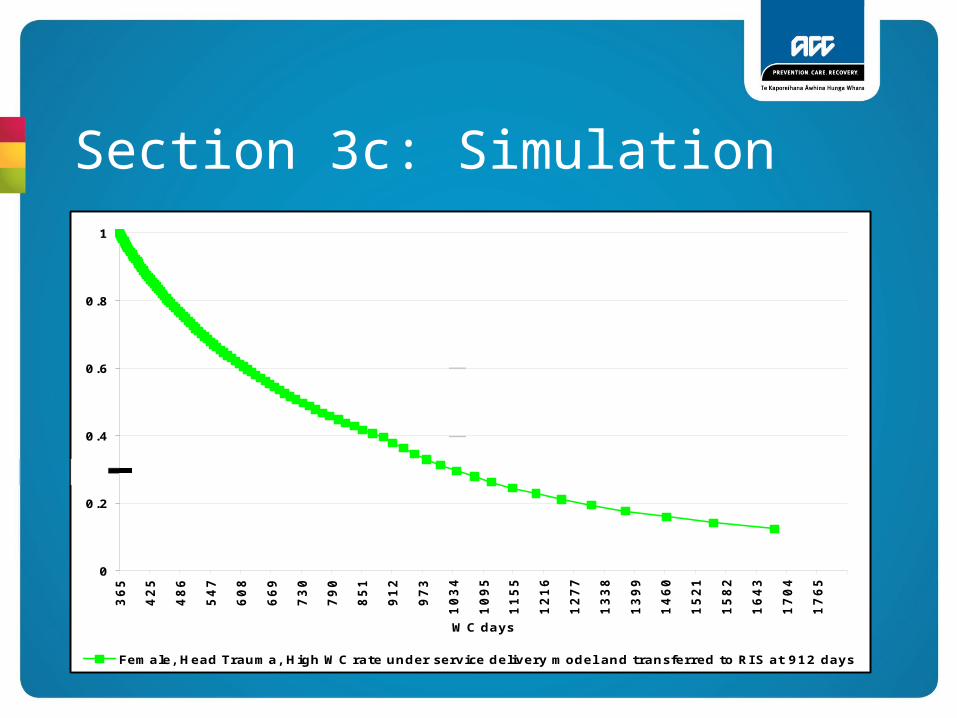

0

0.2

0.4

0.6

0.8

1

36

5

42

5

48

6

54

7

60

8

66

9

73

0

79

0

85

1

91

2

97

3

10

34

10

95

11

55

12

16

12

77

13

38

13

99

14

60

15

21

15

82

16

43

17

04

17

65

WC days

Female, Head Trauma, High WC rate under service delivery model and transferred to RI S at 912 days

Section 3c: Simulation

0

0.2

0.4

0.6

0.8

1

36

5

42

5

48

6

54

7

60

8

66

9

73

0

79

0

85

1

91

2

97

3

10

34

10

95

11

55

12

16

12

77

13

38

13

99

14

60

15

21

15

82

16

43

17

04

17

65

WC days

Female, Head Trauma, High WC rate under service delivery model and transferred to RI S at 912 days

Section 3c: Simulation

60%

70%

80%

90%

100%

110%

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

Entry into long-term claims pool

Perc

en

tag

e o

f cu

rre

nt

nu

mb

er

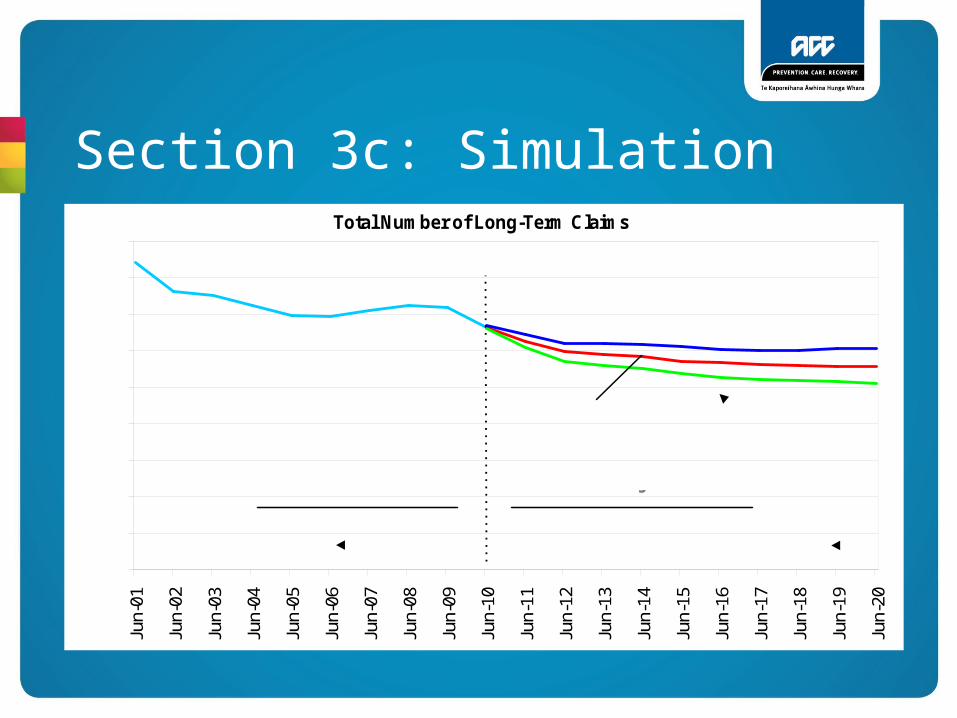

Section 3c: SimulationTotal Number of Long-Term Claims

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

Jun-

13

Jun-

14

Jun-

15

Jun-

16

Jun-

17

Jun-

18

Jun-

19

Jun-

20

Scenario 1

Actual Projected

Scenario 3

Scenario 2

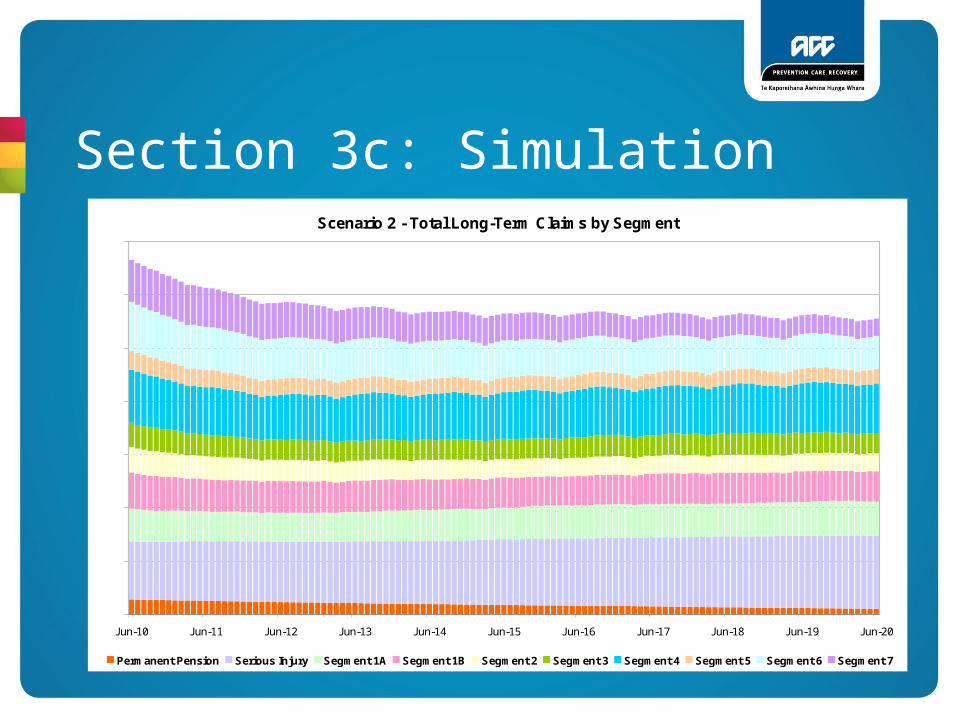

Section 3c: SimulationScenario 2 - Total Long-Term Claims by Segment

0

2000

4000

6000

8000

10000

12000

14000

Jun-10 Jun-11 Jun-12 Jun-13 Jun-14 Jun-15 Jun-16 Jun-17 Jun-18 Jun-19 Jun-20

Permanent Pension Serious Injury Segment 1A Segment 1B Segment 2 Segment 3 Segment 4 Segment 5 Segment 6 Segment 7

Questions…