Embed Size (px)

Citation preview

3

Control Plans:

Ensuring the Economic Return of the Application of Statistical Thinking in

Improvement Projects

Robert Mitchell3M Corporate Quality

3

Statistical Thinking is a philosophy of learning and action based on the following

fundamental principles:

All work occurs in a system of interconnected processes

Variation exists in all processes

Understanding and reducing variation are keys to success.

3

Improvement using Statistical Thinking

Process Variation Data Improvement

Statistical MethodsStatistical Thinking

Philosophy Analysis Action

3

Process

OutputsCustomers

ProcessInputs

Suppliers

S I P O C

A series of activities that converts inputs into outputs

3

The Bottom Line:

How do we capture the benefits from the application of Statistical Thinking ?

Y = f(x)

3

How Projects Impact The Business -Examples

Revenue Growth - Increase top line through capacity expansion and new product introduction/extension

Operating Margin - Bottom-line impact of capacity expansion (growth) or cost reduction (productivity)

Working Capital - Cash impact of inventory or receivable reductions or reduced thruput time (cycle time reduction - improved turns)

3

How Projects Impact The Business -Examples

Revenue Preservation - Maintain volume otherwise lost (due to stockouts or lost customers, etc.)

Cost Avoidance - Reduce the planned spend (that would have otherwise been incurred)

Reduce NVA - Redeployment of resources (personnel, equipment, etc.) without removing their cost from the overall system - consider customer satisfaction

3

Project Selection Elements

• Clarify the ‘big picture’ using the strategic plan and annual business plan for the business– Top-down project identification

• Establish productivity baseline– Bottom-up project identification

• Prioritize projects based on business metrics

• Select key projects with leadership support

• Check for accountability

3

Clarifying the Big Picture

• The functional goals should support the business plans.

• The key metrics (Critical Y’s) for the business are identified and goals set for each year.

• Projects should support the key business directives and should be measurable through the process key metrics.

3

Project Identification Methods

Two fundamental methods:• Top-Down

Projects are identified through association with the metrics of the company’s Strategic Plan

• Bottom-UpProjects are identified through association with current process issues.

3

Project Selection Approaches

Strategic / Operating Plan MetricsOpportunities to reach the

goals

Opportunities to reach the

goals

Problems, Defects, Dissatisfied Customers, Downtime, Pain

Issues needing attention

Issues needing attention

3

Example: Goal Tree Alignment

Productivity / Cost

Working Capital / Cash

Growth

Employee Satisfaction

Better

Increase Top Box

Yield, RTY

Faster

Rate

Cycle Time

Cheaper

Reduce Waste

COPQ

How

Reduce Rework

First Time Acceptance

Eliminate non-value add

Decrease RM Cost

GoalsGoals

MetricsMetrics

ProjectsProjects

Why

More Valued Features

Increase On-time delivery

Fewer Defects

Increase Capability

Reduce Cycle Time

Redesign Process Flow

Reduce Waste

Lower Inventory

Works Best for Operational Projects

3

Example: SIPOC Model

CustomersSuppliers x

x

x Outputs

DDefectefect

Inputs

Effectiveness of Effectiveness of InputsInputs• RM Consistency• Intellectual Property• RM Availability• Mgmt Strategic Goals• Market Presence• Availability of

Information

Efficiency of Efficiency of ProcessProcess• Rolled Throughput

Yield, First Pass Yield• Rework, Scrap, Waste• Throughput• % Things Gone Right• Days of Stock• Days Beyond Terms

Effectiveness of Effectiveness of OutputsOutputs• CTQ Performance• Product Features• On-Time Delivery• # Warranty Claims• Customer Loyalty• Response Time

Works Best for Transactional Projects

3

COPQ IcebergTip of COPQ Iceberg

Lost OpportunityHidden Factory

Full COPQ, 15-25% of Sales

Intangible, more difficult to measure

Tangible, easier to measure

Average COPQ Approximately 20% of Sales

Excessive Overtime, Premium Freight Costs, Expediting

Costs, Excess Inventory, Consumed Capacity, Customer Allowances, More Setups, Lost Sales,

Late Delivery, Long Cycle Times,

Engineering Change Orders, Lost

Customer Loyalty

Customer Returns, Waste, Scrap,

Rejects, Inspection Costs, Recalls,

Rework, Warranty Claims

Traditional Quality Costs, 4-5% of Sales

3

Entitlement

Defines what’s possible - a vision

Provides a performance level for which to aim

Tells you how your process performance relates to perfection

Provides an internal benchmark

3

EntitlementBest Possible Performance– Rolled Throughput Yield = 100%– Cost of Poor Quality = $0– Speed:

• Best observed performance over a “short” period of time• Predicted by business process design• Predicted by “should” map

– Capacity: • Performance specified by equipment manufacturer• Predicted by engineering & scientific fundamentals• Best observed performance over a “short” period of time• Best performance predicted by empirical relationships developed

from process data

3

Improvement Methodology

PLAN

DOCHECK

ACT

Define

Measure

AnalyzeImprove

Control

PDCA DMAIC

3

Control Plans / MethodsImportance to the improvement process

Documented control methods for all critical Process Output Variables and Process Input Variables in the process drives sustained gainsEffective control methods maintain the level of performance over the long termProvides a complete ‘critical to operation’ list of variables and their associated measurement systems / control methodsIdentifies the Reaction Plan for the Process Owners to resolve any out-of-control occurrences

3

Control Plans / MethodsOutputs

Updated Control Plans and methods for all critical Process Output Variables and Process Input Variables

Completed Reaction Plan for each Process Input Variable / Process Output Variable

Sampling methods and measurement system controls in place for each Critical Process Input Variable and Process Output Variable

Procedures and appropriate documentation

Identified and completed training for all pertinent personnel / functions affected by changes in the process

3

ISO 9001:2000

ManagementResponsibility

Measurement,analysis,

improvement

ResourceManagement

ProductRealization

Input Output

3

Three Diamonds of ISO

Management Review(5.6.1)

Corrective/Preventive Action(8.5)

Internal Auditing(8.2.2)

3

Benefits That Can Be Maintained/ Gained With ISO 9001:2000

• Improved consistency of products and services through documentation of standards and specifications

• Organizational retention and transfer of process knowledge through improved documentation.

• Current and accurate raw material specifications• Improved calibration and accuracy of measuring

devices

3

Benefits That Can Be Maintained/ Gained With ISO 9001:2000

• Discipline to follow documented processes• Established requirements for training and record

keeping• Improved system performance• Provides a process to reliably deliver what you

promise to customers

3

Benefits That Can Be Maintained/ Gained With ISO 9001:2000

• Identifies improvement project opportunities with supporting information about:

• Current performance levels

• Measures and

• Processes used

• Provides a framework to sustain the gains of continuous improvement projects

3

Case Study – Adhesive Performance

CorporateCritical Y:

• Growth• Cost• Cash

Business UnitCritical Y

Project Y

FinancialImpact

3

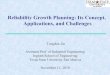

Adhesion Performance ImprovementFinal Capability• Process in control• Mean on target @29.9

oz/inch • 50% reduction in variation

Initial Capability• 3 KPOV out of Control• Mean 35 oz/inch over

target of 30

0S u b g ro u p 5 0 1 0 0

2 03 04 05 06 07 08 09 0

Indi

vidua

l Val

ue

1 2P ro c e ss

M e a n = 2 9 .9 0U C L = 3 7 .2 8

L C L = 2 2 .5 1

1 2

0

1 0

2 0

3 0

Mov

ing

Ran

ge

R = 2 .7 7 6

U C L = 9 .0 7 0

L C L = 0

1 2

P S A - A d h e s io n

3

Adhesion Performance Control Plan

• Transitioned 8 of 12 identified critical X’s from uncontrolled to controlled variables

• Documented new SOPs, implemented mistake proofing, and instituted training– Critical Y’s

• Adhesion to Glass• 5-Bond

– Critical X’s• Ct Wt Profile• Coating Appearance• Adhesive Formulation

• ISO 9001:2000 Management Review– Quarterly internal audits of control plan

3

Key Learnings - Control Plans

• Start developing the control plan as soon as possible– After completion of Measure or Analyze phase

• Select the appropriate process owner and keep him / her informed of and involved in the Control Plan – Team membership of Process Owner is crucial.– If project outcome is not important to the PO, you have

chosen the wrong Process Owner.

3

Key Learnings - Control Plans

• Keep the Control Plan as simple as needed to sustain the desired results– Don’t replace a complex project with an equally complex

control plan.– Use existing culture and SOP

• Simplify or mistake proof process to prevent the need for Active Control