Embed Size (px)

Citation preview

Morgan Stanley

Project Tower

Presentation to the Committee of Independent Directors of the Board of Directors of Tribune 1 April 2007

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64867

Project Tower

Morgan Stanley

Table of Contents

Section 1

Section 2

Section 3

Appendix A

Appendix B

Zell! ESOP Proposal Overv]e;y

Valuation Summary

Leveraged Recap I Broadcasting Spin Altcnlativc

Tmvcr Fimmcial Projcctions Ovcrvic\v

Discounted Cash Flow Anlllysis

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64868

Project Tower

Zell / ESOP Proposal Overview

Morgan Stanley

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64869

Project Tower

Morgan Stanley

Net Present Value Perspectives

• The current Zell ,I ESOP Proposal contemplates th .. '1t, upon consummation of the merger, Tmver shareholders 5hH11 receive .1 cHsh amount equal to:

- $34.00 per share (Lhe "Merger ConsideraLion"): plus

- A ticking fee of 8% per annum accming daily on the Merger Consideration beginning 1/1/08 through ,md including the date of consnmm<-ltion of the merger

• The economic value of the proposal to TO\ver shareholders is a flillction of the time to close and the <-Ippropriate risk-adjusted return

Net Present Value 01 Zell:' SSo'pproposal (Inclui:lirig:$17.:SO :Upfr'oot Oi~lribJition I

Assunied

6 Months

9 Months

12 Months

Assu nied Cost of Equity 5%

$33.38 $33.09

$33.07 $32.86 $32.66

$33.08 $32.53

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64870

Project Tower

Morgan Stanley

Comparative Zen I ESOP and Recapitalization Perspectives

Zell:fESOP Perspectives $ISn;lr~

40

35

30

25

20

15

10

5

o Merger

Consideration

P.·.:: ;::;' :1 Upfront Cash , .' ." Dstnbullon

Notes

Perspective #1 (NPV - 6 Month

Close) ",

PVofCash at ClOSing

Perspective #2 (NPV - 12 Month

Close) ,"

Publishing

Recapitalization Perspectives :$1S:h<!.rll

40

35

30

25

20

15

10

5

o Management Research

Plan Case DO\'.fiside

Case A DOlNrlside

Case B

Equity Value at 1.5:< _ Broadcasting _ EqUity Value at 9x

Broadcasting Equity Value at 11x

Source Management, Wall Street Research

1 Pe"'pectivo #1 end Pe"'pllCtive#2 ""ume e or 12 months to dose, respectively .nd 1 O'l(, cost of eqUity 2

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64871

Project Tower

Implied Premium Perspectives

Implied Pr.emium Perspectives

Recent Tower Prices

March 28. 2007

March 20 2007

52-Week Low

52-Week High

Rsference Price

$31.13

$28.81

$27.09

$34.28

Alferage Price Perspectlves (1)

1-Year $30.72

$32.45

$36.14

2-Years

3-Years

Merger

ConsideTatioil ($34.00)

9.2%

180%

255%

(0.8%)

10.7%

48%

(59%)

Recapitalization Perspectives _ Discounted EquityiValue III

Management Plan $31.r7 70%

Research Case

Dovmside Case A

Do'.vnslde Case B

Notes 1 As an~.rch 28, 2007

$31.37

$24.04

$21.18

84%

41 4%

605%

PErspeotive #1: NPV - 6 Month Close

100k :Cost of Equity 1133.23)

6.8%

15.3%

22.7%

(3.1%)

8.2%

2.4%

(8.0%)

4.6%

5.9%

38.2%

56.9%

PeJs:pet-ti:ve #2: NPV -:12:Month:Close

1{rlfo. Cost cif EqtiitY ($32.80)

5.4%

138%

211%

(43%)

6.8%

11%

(92%)

32%

46%

364%

549%

Morgan Stanley 2. Based on the pre,ent value orthe proiected equity value in 2009, a"uming a Pul:ii,hing EBITDA multiple 017.5><, a Broadcasting mukiple o19.0x and an 11% cost olequity 3

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS· EYES ONLY MS 64872

Project Tower

Morgan Stanley

Implied Transaction Multiples

Implied Transactlon Multiples til $MM; except per share values

Implied Equity Value ilTlpiit;lu Agglt;lQClit;l VCliut;l (t;lXL:i. UIIL:urr:::;.) '-~.

Implied Aggregate Value (incl. Uncons.)

M~rge:r

: Consideratlon 1$34,(0)

$8,242

11,127

13,327

Aggregate Value Multiples (exel. Uncons.) 12)(31 :

2007E EBITDA 8.9x

8.5x 2008E EBITDA

Aggregate Value Multiples (incl. Uncons.) (3)

2007E EBITDA 2008E EBITDA

Equity Value Multiples jJj

2007E Nellncome

2008E Nellncome

i;uu:~

10.7x 10.2x

17.0x

15.4x

1 Based on FDSO 01242.4MM net debt ofS5.095MM and unconsolidated asset vakJe ofS2.200MM 2 Unconsolidated assets valued al S2 200MM 3 Mu~iples based on management plan estimates

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

Perspet:l:ive =#1:

NPV • 6 Month Close :1Q% Cost of Equity

{$".2,)

$8,056

10,941

13,141

8.8x

8.3x

10.6x 10.0x

16.6x

15.0x

Perspective #2;

NPV· 12:Month Clcise 1 0%: Cost of Equity

($32 .• "1

$7,951

10,836

13,036

8.7x

8.3x

10.5x 9,9x

16.4x

14.8x

4

MS 64873

Project Tower

Pro Forma Capitalization

PrQ:Forma ToWer Capitaliiafion:- ZeU:1 ESOP:ProposaF

PmFonna Capit.lizalion

Cash and Cash Equivalenls

N_Terrn Loan B

lsi Priortty Guaranteed Debt

~Je'", Se,,;o, ~J0t""

Guaranteed !lebl

~ommeraal paper

Term Loan A

Bridge Loan

Medium Term Notes Roll-over Notes

Capitali2ed Real Estate Obligation

SVIaPS and OtherObllgatlons

Senior !lebl

PHO~!ES

Total Debt (incl. PHONESI

Less: PV of Tax Savings ~\

Total Adjusted Debl

Credtt Slalis~cs LTM PF Adj EBITDA

lsi Priority Guaranteed Debll L TM PF Adi. EBITDA

Guaranteed Debt I L TM PF Adj EBfTDA

Senior Debt I L Till PF Adj EBITDA Total Debt I L TM PF Adj, EBITDA

Net Debt I L TM PF Adj, EBITDA

Total AdJ Debt I LTM PF Adj. EBITDA

Morgan Stanley

"'''' PraForma

'" '" '" (10) '" 175

0 0 7,015 7,015 0'316'0 6,699 2,125 B 824

'" W $7,015 $6,699 $8,824

2,100 2WJ

'" W $7,015 $6,699 54,225 $10,924

" "' (S(I

1,500 , ~O (1,500)

1,310 1240 (1,240)

'"' '" '" '" '" 1,165 1 165 1,165 1.166 ,,~

;0 " " (15) " " " " " ,

" " $4,432 54,357 $8,535 $8,207 $12,432

9QO 9DQ 90D 9QO 900

$5,JJ2 $5,257 <$-~~~~) $9,107 ,~ ~$-~~-~.) (1,071) (1071)

$5,331 $5,157 59,435 $9,107 $3,154 $12,261 -"""'--""""-

$1437 $1412 $1,412 $1389 $1469

a.ox O~ ;~ 4.8x 00,

a.ox 00, ;lli 4.8x ", 3.1x ;h /i1h-·,. 5.9x /!".~.\ Ux ,~ r 6,7:{ \ 6.6x

3.6x ,~ ~ 6,~ i "" \ .. :,~;;j 3.1x 'h \.....6h/ 6.6x

i;uu:~

Shown pro forma for proceecls fi'om sale 01 seNI Assumes 01 cash ftow I""ces, cash IS used toward payoown ollhe e~lstlng bridge loan Esllmated value oIl"" savings as per Rallng Agency Presenlatlon daled March 2007 [calculaled as Ihe 1 lI-year presenlvalue olannual tax savings d,soountsd.t. 7.5% discount r.ts) Pro Form. for $BOMM of In ore mont. I e.oh eost oavlngo

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

BaJe. af Cubs { Pro Forma

175

(602) 8222

S8,222

2100 510,322

'" 1 166 ;0

" 511,829

9DQ

($~1,7;~') (1071)

$11,658 -""""--"""'-

$1434

;;, ,~

1~B2?\

\ ::: ) ',~y/

5

MS 64874

Project Tower

Valuation Summary

Morgan Stanley

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64875

Project Tower

L::'.::.:::'.:I Management Plan Projections

Morgan Stanley

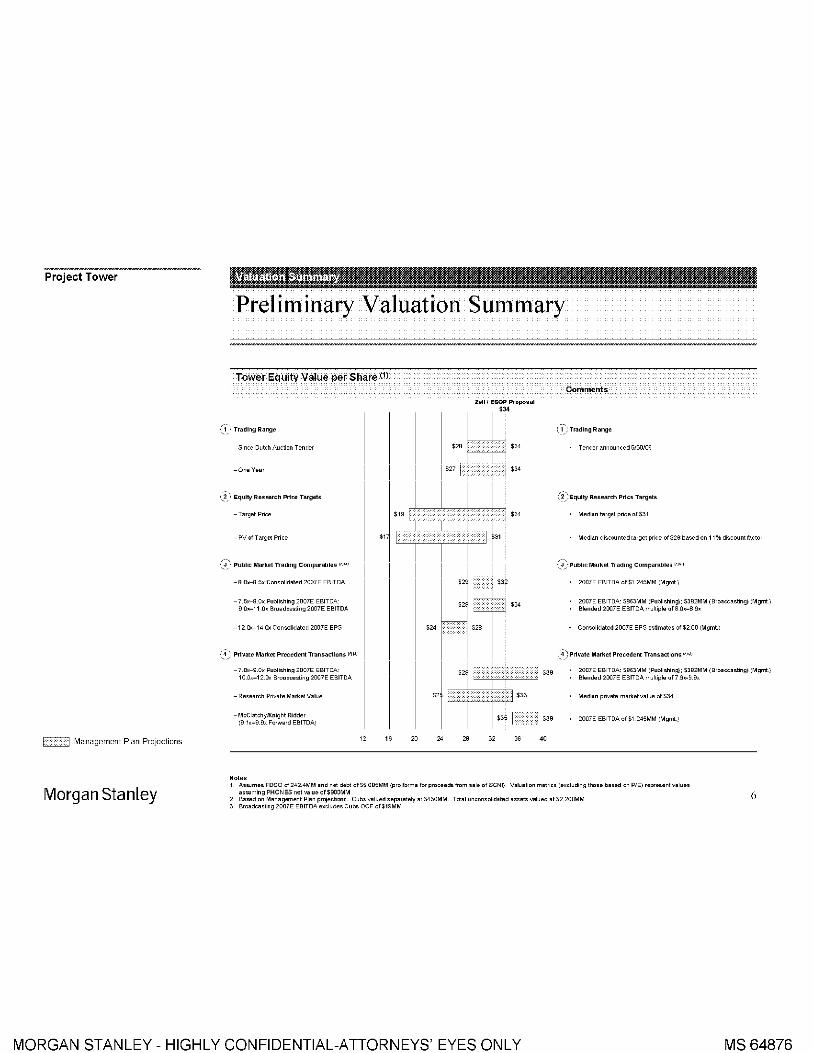

Preliminary Valuation Summary

Tower EquitY Vallie per Share (1)

-Since Dutch Auction Tender

_One Year

,:) " Equity Research Pr1ce Targets

- Targel Price

-PVoITargeiPrice

':,J ' Public Markot Trading Comparwles """

-8 Oll-ll,5x Consolidated 200/E EBITDA

-I 5x-l3.0x Publlshilg 2007E EBITDA 901<-11 0, Bro.dc.sting 2007E EBITDA

-12.0><-14.0.: Con.olidaled 2007E EPS

':,4) Private Market Preoedent Transactions [~P'

_/ OX---9,O~ Publ,shilg 2007E EBITDA 10 Dx_12 Ox SWH,JcH.i",y 20Q7E EStTDA

- Research Prlvale Market Value

- McClalchylKnlght Ridder (9 1<_9,9< Forw.rd EBITDA:O

Notes

Zelll ESOP PrDposal

Comments-

(I': Trading Range

• Tender announced 5/30/06

(2 :Equty Researoh Pr1ce Targets

Median target price 01$31

Median di.cwnted larget price oIS26 based on 11% discoum factor

200lE EBITDA 01 $1 245MM (Mgrnt)

200lE EBITDA: SB63MM IPubllshlng): $3B2MM (Broadcasijng) (Mgmt) Blended 2007E EBITDA mult'ple af8 0<_8 9,

Con.olidated 2007E EPS estimate. of $2.00 (Mgmt.)

(4)Ptivate Market Precedent Transactions ~,,,,

200lE EBITDA: SB63MM (Publ,sh,ng:,; $3B2MM (Broodc.sting) ,:Mgml::, tlt~",J~J 2DiJ,E EBtTDA ",ui,,~i~ of, 9,_9,9,

2007E EBITDA of $1 245MM (Mgml::O

1 ASEJJmes FDSO of242.4MM .nd net debt 0lS5 OB5MM (pro form. lor prooM<is from s.l. 01 seN I:, Voluat,on metrloo (e~olud'ng those booed on PIE) repreoent yolues a.""ming PHONES net value of$900MM 6 2 B .... d on M.nagoment Plan projections, Cubs y.lued sep.rately.t 5450MM Tct.1 unoDnsol,d,tsd ."sls ""Iued.t S2 200MM

3 Broadcasting 200TE EBITDA rotcludes Cubs OCF or$19MM

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64876

Project Tower

~':::':':::':::':'::I Management Plan Projections

f:,:;',:,:;:,:;',) Rcsc~rch Prcjcctions

Management Downside Case A Projections

:'::,::':::::,::',:, Management Downside Case B Projections

Morgan Stanley

Preliminary Valuation Summary (cont'd)

Tower EquitY Vallie per Share (1)

_Management Plan

- Resean;n Case

-M~t. Downside Cas. A

-M~t Downside Case B

<~> 2009E Discounted Equity Value 11)(4)

"~;7.5x Publ.; 9_11x Broad. -Management Plan

- Resean;h Case

-M\Jllt. Downside Cas. A

-M""t Downside Case B

(j)8.0x Publ.; 9-11x Broad.

-Management Plan

-M~t Downside Case A

-M~t. Downside Cas. B

!'!otes

524 ::l $26

'"

$25 n $27

'"

Zelll ESOP Proposal

Comments

8-9x 2012E exit multiple, Discount rate, 7-8% (All cases) Cash tax rate ~33-35% (Alt oases)

2012E EBITDA ofS1.386MM IMgmt Plan)

20 i2E EBiTDA ofSi.319i,i~i \Researon)

2012E EBITDA of5932MM [Mgmt. DownSide Case A)

2012E EBITDA of5839MM [Mgmt. DownSide Case B)

,'~~, 2009E Discounted Equi1y Value (1][4)(5)

Ca)7.5X Publ.; 9-11x Broad. 2010E EBITDA (PubllBroad.): $B99MM I $460M~~

2010E EB[TDA (Publ,lBroad.): $872MM I $458MM

2010E EBITDA (Put> IBroad.): $692MM I $365MM

2010E EBITDA (Publ.lBroad,), $5S9MM I $::l54MM

Tax rate: ~33-35% IPubl,)139,5% IBroad,1 (A[I Ca,es)

(~)8.Ox Publ.; 9-11x Broad.

2010E EBITDA (PubIIBroad)' $899MM I $450MM

2uiuE EBITDA (Publ 'Broad.' $872;";;'; I $458,",,,

2010E EB[TDA (Pub[.IBroad,), $692MM I $::l65MM

2010E EBITDA (Put> IBroad.): $589t'AM I S354MM

Tax rate, ~33-35% (Publ.)139,5% (Broad,) I!\I[ Casesl

1 Assumes FDSO of 242 4~~M and net d.bt of$5,OO5MM (pro forma iJr proClleds from sal. ofSCNQ whloh assumes PHONES net value of$900MM Valuation IS as of March 31 2007

2 DCF assumes 0 WACC of 7_8%, and a 8 Ox·9.0x eXit multiple in 2012 Bo.ed on mono9oment e.tlmot"" ond re.eorcn e.tlmole •• o. Indlooled Cub. volued .ep<lrolety 8t $450MM T,"",I UnOOMot,doted 0 .. 01 ...... Iued ot $2,200MM Assumes unconsolidated assets currently valued at $1 ,600MM (Food Ne~'.'Ork, $8DOMM, CareerBui[der. S65DMM, Other Interactive Assets, $150MMI and that unconsolldoted asset value grows at 8,!(, pili" y.ar Cubs and Comeast SpcrtsNet are sold ot post.tax ""Iue of$602MM

5 For eaoh SCIll10rlO, eqUltyvolues ore based on PV of projected stock priee.t year end 20Q9 assuming. 11% cost of .qUlty

7

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS64877

Project Tower

Tower C ..... tal.z;il:.ori ~MM

Curr.nt Sh.r. Pric. ," FDSO,MM)

EqultyValue

Debt'"

Ca.h

Net Debt Agg, Value(lnol. Ultonsolldated assets)

Less' Unconsolidated A"eI,

Agg, Value(excl. Unconsolidated assets)

$31.13

2424

$7,546

5,260

--"-' ~

512,631

2,200

510,431

AVIEB1TDA PIE lOOlE :ZOO8E laD7E :20DllE

Gannett "", Beiu Q,h

Med,a General '"' M~" S.1><

Median a.ox

Unconsolidated: Assets

,MM

Publishing Ass~ls

Career Builder

Other tnteract,ve Assets

Tat,1 Publishing

Broadcasting Ass~ts

Chicago Cub.

Food Neh'rork

Comeast SportsNet

Tatal Broadcasting

, ", 7,G~

""' 7.Sx

7.6x

Morgan Stanley

119x ll1x

17,9~ 14,4~

16 8~ 126~

15.Sx 12.7)[

16.8>< 12.6x

Aml:umed Value

$800

S1.400

7,700

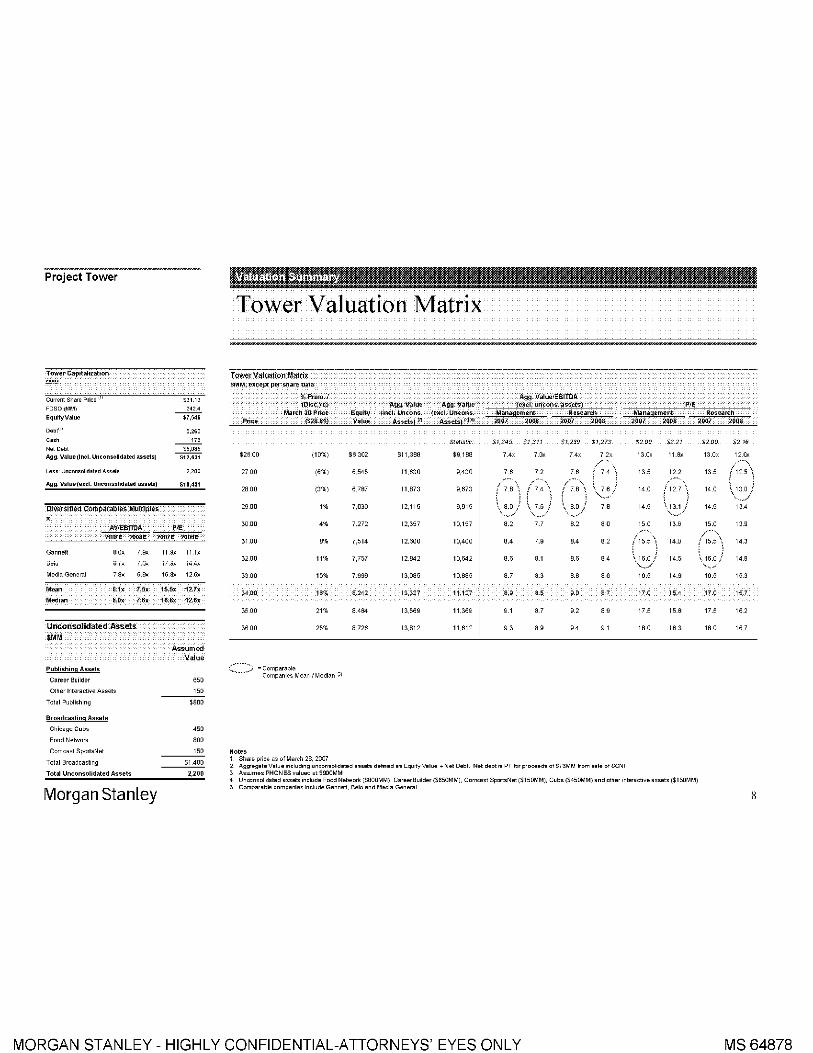

Tower Valuation Matrix

TU'm'r Valuatio'n Matrix ~M, except per:snare a.ta:

%Prem.J Agg.ValuelEBlmA ~Dis:c.):to Ayg. Valu~ Agg: VahJe: (ex ct. U<leOns.:"",,"t,,)

March 20 PMe EqUIt\l (Inct U1COM. (e~u: un~Ot'Is. Manaat!!!~nt ReSl!atch Price jS2:B-.~1) Vat .... A,.sd;sj I'l A""d';I(~l.r ~" '"00 :zoU] >OM

StatlStrc $1,245 $1,311 $1,239 tl.273

$2600 (10"") $6,302 $11,388 $9188 7Ax 7.0x 74x 72x / .. ,

2700 (6"") 6545 11,630 9,430 " " 7.6 i " (;~~ \ /'''', \ 7 6 2800 (3"") 6787 11,873 9,673 I " \ ! 7.8 :

\..\8~~) , ,,~~,

29,00 " 7,030 12,115 9,915 \ ,., 8.0/ 7,8 '-.,~.,

30,00 " 7,272 12,357 10,157 .. , U "' '.0

31,00 "' 7,514 12,600 10,400 .. , ,., "'

., 32,00 '" 7,757 12,842 10,542 .. , .. , ", ., 33,00 '" 7,999 13,085 10.885 .. , .. , ... eo

3'UO '" 8,~42. 13,3~7 11,127 .. , M M " 3500 '" "'"' 13,569 11,369 " OJ "' "" 3600 '" 8 726 13,812 11,612 '.0 ." ", Of

I'~.-.,

~ Comparable ", ... -"' C:ompe_~;e. M~en! M~d;"n ~,

Notes Sh,"~ pric~~" ofM~rch 2B, 2007 Agge9.le V.lue Including unconsolld.led ••• et. demed •• EqullyV.'ue + Nel Debl Nol debt,. PF lor procoed. of$73M'J ~om •• Ie of SeNI A<sumes PHON~S v.tued.t $OOOMM

PIE

Managtment: 2007 ,~

$200 $221

13.0,- II.ax

13.5 12.2 c .. ,

14.0 /12.7':. ! !

14.5 '- 13.1 ! , ..... '. 15,0 13.6

1155 ':, : ' , 14.0

. ; \. 16.0,' 14.5 'j

16,5 14.9

17.0 15.4

17.5 15.8

18.0 16.3

4 Unoonsolld.led ."lIIs indude Food Nolwork (S800MM) C.reerBullder ($B50MMI. Ceme.st SporlsNet ($150MM), Cubs ($45[t~M) .nd ether Inter.ctive ."ets ($150MM) 5 Comparable compantes Include Gannett, Beto and Media General

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

RHUrch ,.~ 2008

~2DO $216

13.0x 12 Ox -~

13.5 /125\

\ 13 0 ) 14.0 ,.j

14.5 13.4

15.0 13.9 /''''-. r 15.5 \ 14,3

~ i " 16.0/ 14,8 '-.,....-

16,5 15,3

17.0 15,7

17.5 '" 18.0 '"'

8

MS 64878

Project Tower

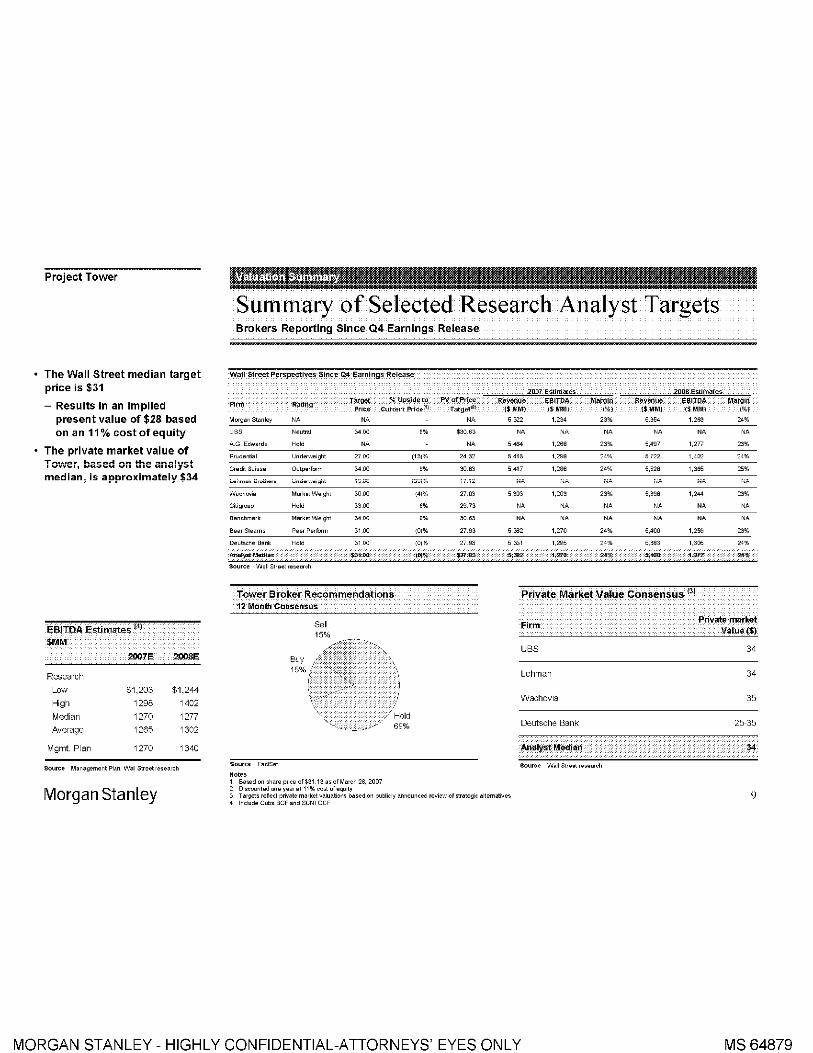

The Wall Street median target price is $31

Results in an implied present value of $28 based on an 11% cost of equity

The private market value of T ........... .... ........... or; ..- ........ 1 ....... 1 .... VV ... " ... A ......... ~.'''' ... ,AI.7""

median; is approximately $34

EBiTDA E~tirilaie~ 14)

$MM

2007E 2OO8E

R~C3rch

Lov,. S1,203 $1,244

High 1298 1402

Median 1270 1277

Average 1265 1302

Mgmt. Plan 1270 1340

source Management Plan. Wall Street research

Morgan Stanley

Summary of Selected Research Analyst Targets Brokers Reporting Since Q4 Earnings Release

Wall Street Perspectives Since Q4 Earnings Rele<lse:

"= T;\I'~ % Upside to PV of:Ptice RevenlH; Marg!n: RiwMUe M:arOirt Rating

Pric.e Cureent pricJ>I'1 Ta'gel'Oj (lM.M) (%) ($:!liM) (%)

Mor~an Stanley " "' "' 5,:>22 1.234 '" 5.354 1.2133 ~%

UBS Neunl ~O" 9% $3063 " " " " "' " '.G Edwards Held "' "' ,- 1,268 23% 5,497 1,277 ~" Prudential Underweight 2/00 (13)% 2432 5,415 1,298 24% 5,/22 1,402 24'!<',

Credit Suisse Outporform ~O" 0%, 3063 5,41/ 1,286 24% 5,528 1,365 ~" L~I-",-, .. , 8,~tt,~'~ U"~""i~'91,t 18,00 lJ8i% 17,12 NA r,A r,A r,A NA r,A

Wachcvla MarkotWelght 3000 (4)% 2/03 5,303 1,203 23% 5,398 1,244 ~" C~igroup Hold 33,00 0% 29,73 " " " " "' " Benchmark Market Weight ~O" " ~o e3 "' " " " "' " Bear Stearns Peer Perform 31,00 (01% 27,93 5,382 1,270 '" 5,400 1,259 n%

Deutsche Bank Hold 3100 (01% 2/93 5,351 1,295 24% 5,383 1,305 ~"

:~~~~ :' :'¥':D~::: :iD)!~ :'~::g~":" ;5i~-:: ' _102'76' ;24~ .- ~i;U-! :-~~::

Source Watl Strsot research

Tower Broker Recommendations: 12 Month Consensus

Private Market Value Consensus (3:)

Sourc. FadSel

Buy 15%

Sell 15%

1'·.· .•. ·•· .•• · .•. Er:;~··· •• · •• ·· •• ·· •• · •• ·· •• ·i

Based on share price 01$31,13 as 01 March 28, 2007 Discounted OIlS yoar at 11%, oest ef e<pJlty

3 Targets reftect plivate market valuaijon, based on pubtlcly announced review ofstrnteglc alternatives 4 Include Cubs BCF and SeNI OCF

Firm

UBS

Lehman

Wachovla

Deutsche Bank

Souroe W.II Str~ot ",.nrch

Private marke't Value ($)

34

34

35

25-35

:34:

9

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64879

Project Tower

fmpJied Tower Shan; Price'Base-d:on Mg'mt. Plan'

2001E Towor Munlplo '" '" Tower EBITDA (excl CubsBeF) $1,245 $1,245

Impled Tower Aggregate Value S9,957 S10,579

Less' Net Debt (5,0851 (5,085)

Plus' Uncon,oMaiM Assels 2,200 2,200

Impled Tower EqultyValue 51,071 51,6g4-

FDSa ~" ~" !!!!P!"" T~ ... e,V"'!.., !"e, ~~._'" S?~ "' S~, 7",

Morgan Stanley

Selected Public Market Trading Comparables 2007 and 2008 EBITDA Multiples Without Unconsolidated Assets

AV) 2007E EBITDA 0)(2)

(J!:I

Tower 4Di~eraified Publishing Pure Play Publishing Broadcasting

14_1 13,2 1 16 14 12 10 8.4 8.4 87 8.0

+-7]-"::'; 116

7 ~, . 1~'7, 18',6

1 ~',~ I ~, ,n:'::1 :::j IT] ::::?I

.- --;--4. . ............ --;--4 .......... f--................ J--........... ·.f--;--- •.•...•...... f-- .......•. f--......•.......•.. f--.•...•...•. ·.t ' ------L-l ;",;' ~ ',;", !----';",;' l--;' ;",l_----L-,:,:"l----', ',:l----:':'"I----:,: :'

. I 1111 ·1111

Tower eo,

Tower Mgmt

Bela Gsnnetl Media Journal Lee NY Times McClatchy i Hearst- LIN TV Gray Sinclair

AV i2008E E6i luA r:)f21 (!C)

•

General Reg

Di~eraified Publishing 4 J

Arg\lle

Pure Play Publishing • Broadcasting • 14

12 10 8

8 , 8,0 1

, J

118

-~~--rcrr~-'lc9'-----7'-.6"--6-9-~~8~9"--_~,~.,,-_<'~.''-__ 7_,_,-.· •• ·.~~':'~'0L --c---rr~·· .• ·.·r-I ---'-Cl-'---•• ·• +- 11>11 6 I

4

··1 TI 2

0 Tower Tower Gannett Ro> Mgmt

Notes 1 Based on ,hare prices a, of March 28, 2007 2 EBITDA includes ,lock, based oompensallon

II >1111(11 8elo Media Journal Lee NY Times McClatchy, Hearst- Sinclair Gray LIN TV

General Reg Arg\lle

10

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64880

Project Tower

Privale:MiorkeE ValilaEior> ~M~'

Hig!1

2007E Tower Publ Muniple ,~ '"' Tower Pub!. EBITDA 5803 $803

Implied PltIl. Aggr.gate ..... ue $6,0 .... 1 $1,161

2007E TaWl!r Bro.d. Muilipl. 100, 120,

Taw" Broad EBITDA S:l82 $382

Implied Broad. Ag!regate value $3,816 $4,579

Implied Tower Aggregate "'alue $9,857 $12,346

L"" ..... iD ... \5.065, \5.ua5)

PI"" Unoan,olid.I.;A,,,,,t, 2.2DO 2.20D

Implied Tower Equlty"'alue $6,971 $1,461

FDSO "" ", ImplIed Tower ... alue Per Share i28.16 $39.03

Morgan Stanley

Selected Private Market Precedent Transactions Newspapers and TV Broadcasting

Selected Newspaper PtecooelitTransaclions Aggfegat~ Vah,re} Traillng J;eITPA 1:x1

16

12

8

4

o

Purchase Price (S~:

Date:

AVI31B1 Star Tribune

", ", "~

Phll.dolph,. Medial

Phll.dolph,.

Inquirer

562:2,

'" ,,~

Selected 1V B roadcastirig;pr.etederlt Transactions Aggregate. ValileJSCFlxJ

30

10

o

Purohase Price ($MM):

Date:

14.9

Oak HIli!

M"

575 ,., 2007

Sources Company dam, Wall Strosl estimates

Notes

14.6'

Sunbeam I Freedom I Tribune Tribune Boston Albany

'" " ''" '"" 2006 2006

Medi. New, & He.r:;;!1

McClatchy Nowspapers

1,000

Ae' 2005

12.4")

Gannett! Tribune I'Jlanta

", '"' 2006

1 Asrumes 2005 EBITDA lor Star Tribune ol$79MM ~urchase price excluding tw benent 0IS150MM would result In a 6 7x mU~lole 2 Purthase price indudes pension liability ofS47MM 3 9.5, forw~rd multlpl~ ~,cludlng non,cOr9 u .. ~N, B,7x with 'i'n~r91~' and 11 ,Ox pom u .. ot ,ulu 4 Based on forward BCF 5 Based on trailing BCF 6 BaSBd on 2005·2006 blended BCF multiple

BaSBd on 2004·2005 blended BCF multiple

Hearst Argyle! EnmlS Orlando

'" M., ,"00

Mccr.lchyl Knight Ridder

5500 ,,, 2006

Median: 13.2)(

14,0'

MEG! NBC

stations

"00 Aeo 2006

11

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64881

Project Tower

On March 13, 2006, McClatchy and Knight Ridder entered into a definitive agreement under which McClatchy acquired Knight Ridder in a transaction valued at$S7,25 per share(1)

The combined Company has 32 daily newspapers and approximately 50 non-dailies and total daily circulation of 3.2MM (pro forma fer divestiture of 12 Knight Ridder papers)

Second largest newspaper company in the U.S, based on circulation

Morgan Stanley

McClatchy Acquisition of Knight Ridder Transaction Overview

KeY: Transactian:Terms Offer: Price: SerlsitNity

• Consideratioll:(l) - S40 per share in cash

- 0.5118 rvlcClatchy Class A shares (fixed exchange ratio)

McClatchy Shares % of 3/10/06

Knight Ridder Consideration Total Offer '05 EBITDA

Price Price Value Multiple

- S4.5Bll equity value 10/31/2005 $62.68 18% S72.08 10.7x

- S(i.5Bn aggrcgat0 value iil1412005 66.17 24% 73.87 iO 9x

12 1lcwspap.:;rs " .... ith daily circuiati011 of 1.5\·fl\..T (S6%.

of\vhich is Philadelphia. Bay Area, Akron. and st. Paul) and "05 ERITDA o[$"219\·fl\·f an; schcdukd for divcstitur.:;

r-------------------------·-------------·--------------------- -----------------------.----------. : 311 012006 53.24 0% 67.25 10.2>: t _________________________ • _____________ • ____________________________________________ • _________ ~

Govt:rn:mct:: "2 Knight Riddt:r dirt:ulors wt:n; askt:d to

join tht: rvfL:C'1alch~· noard of Dire\:lors

Source Company press release

Valuatiofl:and:Multiples:

Implied value per share: $67.25(1)

Premium to last close (3110/06): 3.5':"0

Premium to U11aff.:;ctcd (10131 105): 20.0%

Pro forma kvt:ragt:: 4.gx lkbl / '05 PI- EUlIDA (prt:msct divc~titurcs)

No Synergies Qnd. Unconsolldated

Assetsl

'05 EBITDA'" 10.2><

'06 EBITDA , .. Source Company prBs. rBllIBSB

Notes

WHh$60MIII No Synergies of Annrunced (Excl. Unconsolldated ~.!]ies Assetsl

"~ 9.5>:

9.1x 9.2x

311312006'" 51.73 (3%)

411312006''3) 47.18 (11%)

612612006'" 40.63 (24%)

Source Company filings, company pre .. releases

Ass~t Sales (ffiM~)

Pffi.Tax Pre.Trix

TTarn,,\~tjQn P(-Q.,~d:; Mutliel'il

Northern Callfomla I St Paul $1.000 11 5;:

Philadelphia 562 10.1

other") 538 3 1

,oia; 2, HiD 10.2x

PF Multiple Paid w/oul Synergies 11.0x

PF Leverage 38,

1 ~iXt~e~~h:;~:nM~~~~ ~g~~~~tlon and 0 5119 shares orMcClalclTy Class A common stock S67.25 merger cons,d.".at,on based on McClalchy closing price

2 Ba""d on transaction value 01 $a 5Bn and a<suming:lO value lor Knighl Ridder's off_balance <>hoet assot< and S638MM 012005 Knight Ridd~r EBITOA (pro

~~~~~J ;:;;'lt~s~11°~~~:~S~·a~ly;:p::,~·t~~ Bellingha~ newspapers) Includes Akron Beacon JournaIIOH). Oululh News Tribune (MN), Grand Forks Herald (ND). FortWayne Ne\'" .. Sentinel (INI, Aberdeen American News (SOl, Wilkes-Barre Times Leader [PAl

66.48 10 lx

64.15 99><

60.79 95,

Estimated After·Tax Affec_Tai<

PrQce!'ld!S Muftiel'il

$705 e" 426 7.7

368 5.5

$1,498 7.3x

12

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64882

Project Tower

Public Mail<et:Valliati<m

gM~'

High

2007E Tower Publ Muniple 'fu eo. Tower Pub!. EBITDA 5803 $863

Implied Pltll. Aggr.gate ..... ue $6,473 $1,90 ....

2007E TaWl!r Broad. Muilipl. '"' 110,

Tower Broad. EBITDA 5382 $J82

Implied Broad. AQ!regate "'alue $JAJ4 $4,1Q7

Implied To_rAggregai:e V .. ue $UD1 $11,101

L ..... N.tD.t.; ':;.08G) ,:;.08:;, Plus. Un,on,olidaled As ... t, 2.200 2.200

Impliad To_rEqultyValu. $7,021 $1,:1:16

FDS:D "" ". Impli"" To_r Val ... P ... S:h.", $28.91 $3].89

Privale'Mirket Vililaiiolt

"" ,~ l'iigt1

2007E Tower Publ Mu~\,le 'fu '" Tow", P"hl FRlm~ S863 $863

Impliad PLtJI. Aggr.gat ..... lu. $6,041 $1,167 2007E To,,".r Brood. Muilipl. 10.0x 12.0x Tower Broad EBITDA 5382 $382

Implied Broad. Ag!regate "'alue $3.816 $4.579 Impliad To_r Agg"'g.m V_lua $9,857 $1!~6

L""s:N.tD.bI (5.085) (5.0851 Plus' Un,on,olld"led Asset, 2.200 2.200

Implied Tower EqullyValue $6,971 $1,461

FDSD "" ". rmplied To_r Var"" Per Share U8.76 $3<J.03

Morgan Stanley

Sum-of-the-Parts Valuation Perspectives

trripii~ Sha:re PticEiPI(2} l'ita:n~erjlen'l p-lan

Sr¢ad<;;aisllng W07E .EBITDA

1it~ltipiel~) 7.0)( 7.5x 8~Ox 3.5x

8.5x S26.40

':) Ux 2f.19

9.5x 27.97

10.0x 28.76

10.5x 29.55

11.Ox 30.33

11.5x 31.12

12.Ox 31.91

12.5x 32.69

Public Market Valuation

Note

$28.18

3290

3369

3448

Private Market Valuation

S29.96

3U fj

3i .53

3468

3547

3626

$31.74

::J:.:' j3

33.31

3410

3489

3567

3646

3725

3804

~ .... d on ~l)<;O ot L4:.'.4MM not dabl 01 ~~.OH~MM (pro term. ter proc.ods trnm s.l. ol<;(;NI) Hnd unconsolld.tod .ssats al~L :.'OOMM (road Notwork ($BOOMM). Car~~rBulld~r ($6S0I.llM). ComO"s! Sport<N~ ($1S0MM). Cub~ ($450MM) .no <rl:h~r inl~r"dlv~ as<oI~ ($lS0MM)) Corporate overhead has been alocated to Publishing and Broadca.ting ba.ed on 2007E revenue contribution B .... d on Bro.do_stlng EBITDAinciuding st""k·b.sod camponsHtlOn of $382MM (axludlng $19MM for Cubs)

4 Bared on Publishing EBITDA including stock-based rompen5<ltion of$8e""~M

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

9.0x 9:5):

S33.52 $35.30

3431 31:) u,:)

35.09 36.87

3588 3766

3667 3845

3745 3923

3824 4002

3903 4081

3932 4160

13

MS 64883

Project Tower

Premiums Paid in Public-to-Private Transactions Selected Transactions> $58n

Premium Paid in: Pubtic~to-Ptivabl:rran$actiori$:(Deats ofSS.O:BnOJ m:ow since:20041 1'm,;",:V9llie Pri<:e:P<!r

AilnOtinc-ed Tatge! A£<f,limr lfBiI) Shat'el$)'

26-Feb 07 TXU Corp KKR, TPG 45.0 69.25

19-Nov-06 Equity Ofke Properties Blackstone 39.0 55.50

24-Ju106 HCA Inc Investor Group 32.1 51.00

18-Dec-06 Harrah's Entertainment Inc Apollo. TPG 219 9000

29-May-06 Kinder Morgan Inc Investor Group 276 10750

16-Nov-06 Clear Channel Comms Inc Investor Group 267 3760

13-Nov-05 Georgia-Pacific Corp Koch Forest Products Inc 20.5 48.00

15-Sep-06 Freescale Semiconductor Inc Firestone Holdings LLC 175 40.00

22-Jan-06 Albertsons Inc SupeNalu. Investor Group 174 2629

8-Gct-06 Cablevislon Systems Corp Investor Group 165 2700

27 Jun-06 Unlvlsion Communications Inc Investor Group 13.4 36.25

13-Dec-06 Quantas Airways Investor Group 131 441

18-Dec 06 Biomet Inc Investor Group 10.9 44.00

28-Mru--0~· SunGard Data Systems Investor Group 108 3600

26-Feb_07 Siabon Casinos Inc Colony Capital 85 9000

2-Aug-04 Cox Communications Cox EnterpriSes 84 34 15

1-May-06 ARAMARK Corp Investor Group 8.2 33.80

24-Nov-06 ASE Group Carlyle Group 64 594

29-Aug-05 PanAmSaI Holding Corp Intelsat Ltd 63 2500

17-Mar-05 Toys "R" Us Inc Investor Group 6 1 26 15

3O-Jun-06 Mlchael~ store~ Inc Investor Group 5.6 44.00

2-May-05 Neiman Marcus Group Inc Investor Group 52 10000

12 Dec 06 Sabre Holdings Corp TPG, Silver Lake 5.0 32.75

Maan:

Madfan:

Tower Zell! ESOP snoo

Source PubliC ftllngs and FactSet

Premiuil1ro DayPri'or 1 Wee~ AV~ 4 W"er. AV~ 31\1<itiflAvg llM:intllA.vg

23.5%

23.1%

6.5%

9.5%

27.4%

10.2%

38.5%

6.6%

9.0%

12.8%

13.2%

10.5%

4.8%

141%

7.6%

26.0%

20.2%

12.9%

26.3%

8.0%

15.8%

1.1%

7.6%

14.6%

12.8%

61%

22.0%

21.2%

12.3%

127%

287%

91%

43.4%

115%

122%

156%

8.5%

91%

5.4%

145%

79%

236%

21.8%

152%

261%

114%

16.3%

17%

14.5%

16'.1%

14.5%

90%

24.8%

30.7%

16.6%

145%

244%

118%

49.2%

272%

184%

157%

3.4%

195%

12.6%

330%

82%

241%

19.2%

228%

259%

161%

15.6%

63%

19.9%

20.0%

19.2%

99%

25.2%

38.1%

16.6%

20.1%

20.1%

22.4%

47.9%

35.9%

11.3%

19.3%

3.3%

36.0%

20.7%

34.0%

11.4%

17.6%

19.3%

22.6%

24.6%

23.1%

15.8%

21.9%

29.4%

23.3%

21.9%

8.4%

17.8%

45.0%

12.3%

294%

171%

242%

46.2%

357%

136%

215%

7.4%

561%

27.4%

270%

124%

23.4%

253%

313%

330%

22.(%

331%

40.[1"",

27.7%

27.0%

50%

Morgan Stanley 14

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64884

Project Tower

Leveraged Recap I Broadcasting Spin Alternative

Morgan Stanley

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64885

Project Tower

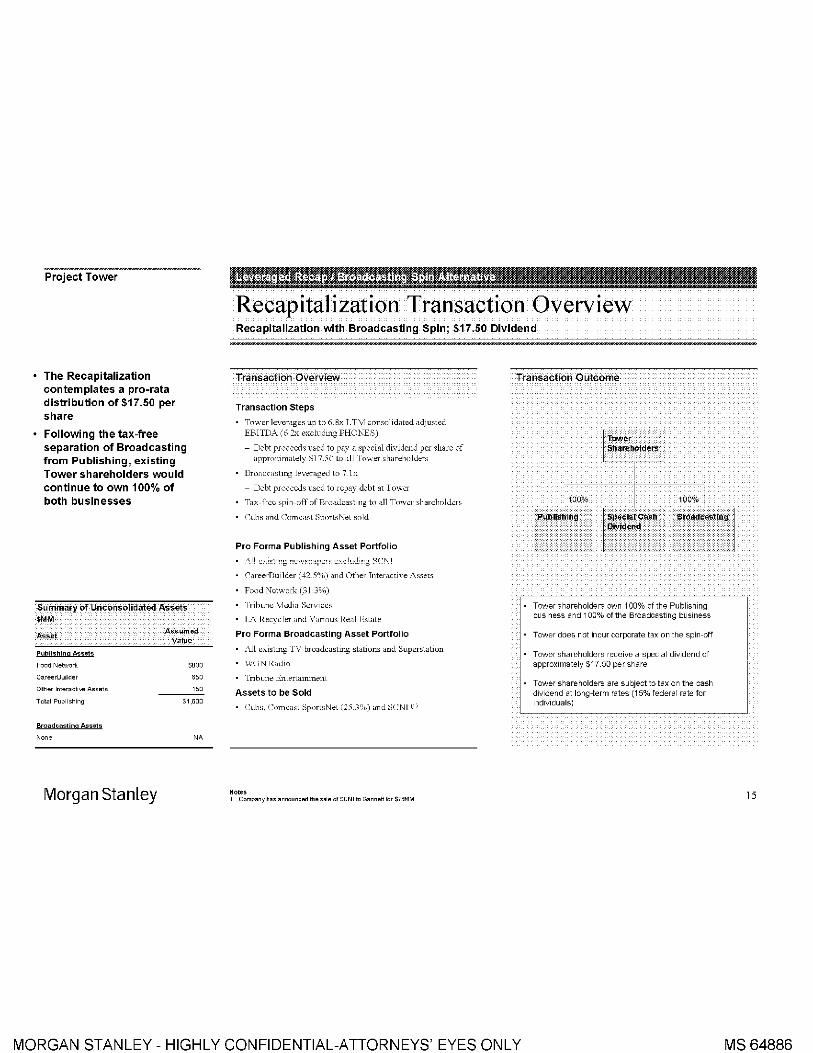

The Recapitalization contemplates a pro-rata distribution of $17.50 per share

Following the tax-free separation of Broadcasting from Publishing; existing Tower shareholders would continue to own 100% of both businesses

Summary of Unconsolidated Assets $MM

Asset ASJil.umed

Value

Publishing Assets

Food Network

Olh .. r Inl .. r~cli"" As ... ls

Tolal Publishing

Broadcasting Ass81s

None

Morgan Stanley

S800

650

51,600

i

Recapitalization Transaction Overview Recapitalization with Broadcasting Spin; $17.50 Dividend

TransaCtion:Overv[ew

Transaction Steps

Tower 1everage~ up to" Rx T .Tv! consolidated adJu~ted EBlmA (6 2.--:: exchldlllg PH01<ES)

- D::bt pr0c-;eds ll~cd to pay a sp-;cial dividcnd pcr share 0f apprw;lmatdy $17,50 to all Tow<;;r ,hard-told"'r~

Broi\d(,i\~til1g kveraged to 7 Ix

- D-;bt pr0c-;eds ll~cd to repay d-;bt at Iowcr

Tax-fr-;e ~pin-0ff of Br0adca~tillg to all To\',--;r ~harcholdcr,

(,uh~ and Corn cast SporbNet ~old

Pro Forma Publishing Asset Portfolio

('areerDU11der (4~ S~"[)'I and Other Tnteractlve A~set~

F00d Network (3IY,o)

I'nhune ~vlt:(.ba Services

LA Recycler and Varillus l<!eall':sLaLe

Pro Forma Broadcasting Asset Portfolio

.'\11 e70.1~Lmg TV bruaJ~<J!;Lmg ~lallons and Superslallon

\VCiN l{aUID

Tnbune Elllt'namlllt'lli

Assets to be Sold

• C,~b~. Com~a~\ Sport~Nd (25,3"'oj and SeNl (1)

Notes 1 Company has announcBd ths sal .. of SCNI Ie Gannstt fer $73MM

Transaction Outcome

Tower shareholders own 100% of the Publishing bUSiness and 100% of the Broadcasting bUSiness

Tower does not incur corporate tax on the spin-off

Tower shareholders receive a special diVidend of approximately $17.50 per share

Tower shareholders are su bjeot to tax on the oash diVidend at long-term rates (15% federal rate for Individuals)

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

15

MS 64886

Project Tower

A $17.50 special dividend would represent the second largest special dividend in aggregate dollar value and the largest as a percent of current stock price in the last two years

Morgan Stanley

i

Precedent Special Dividends

~!~ei!id LargllSt SPIl<iia/ DfVidlll¥Js '

.Di~idend

Declared Amolln! S~cial Dhidllnd C",rlij Rating ftI Pricelme!!c:f Company D~' lMM! Amount Yie1d P~Div. PO$tDiv. ,., Microsoft 07120104 $32,640 $3.00 10.6% AA AA 1.3%

To .... er" $17 50 Di"";dend Illustrative CF·357.') $17.50 (~~i2%~) 6<l.lIB6+' Bll B~ :",

"A Cablevision 04107106 $2.896 $10.00 37.0% "' Bl :-, 09%

Cammark Rx Inc 01116107 $2.526 $6.00 10.6% '" '" (1.0%)

Health Management Assoc 01117107 $2,407 $10.00 48.5% '" ,. 2.6%

Aiberta-Cuiver Co 06ii9JCi6 $2.3·i9 $25.00 53.6% Baa i i BBB+ Baa2i BBB- 20%

Dean Foods Co 03102107 $1,926 $15.00 33.0% Ball BB+ Bal: 'I BB 3.6%

Clear Channel Ccrnmunications 04129105 $1.644 $300 9.4% Baa3 1 BBB- Baa3 '-II BBB- :-1 (02%)

Ashland Inc 09114106 $725 $10.20 16.1% BBB- ". 1.3%

Potlatch 09119105 $440 $15.15 27.2% ". " (2.3%)

Saks 10103106 $548 $4.00 23.4% B+ ,- B+ ,+, 2.7%

Scotts Miracle-8m 12112106 $500 $7.6B 15.1% Ba11 BB Ba1 ( 'I B8 50%

Longview Fibre 06114106 $385 $7.54 30.1% ,,' " 04%

Montpelier Re Holdings 02125105 $342 $5.50 14.0% BBB' BBB" 07%

Banta 09114106 $386 $16.00 33.9% " Ba2IBB: 1 (1.5%)

Gr""l AII~nlic & P~clfi~ T~~ 04104106 $298 $7.25 20.9% B31 B_ eo' 'I B- I 1"1.

Commonwealth Telephone En!. 05103105 $275 $13.00 27.8% " " 8.4%

Sun-Times r,ledia Group Inc 01127105 $272 $3.00 20.8% " " (1.0%)

Mar""~ 01117106 $213 $7.00 30.7% " " 16.2%)

Emmis Communi~ations 09118106 $149 $400 34.0% Ba31 B+ Ball B 20%

r.l<;<;ij'" 10.20/. 0.2~

M"dian"~ 2.8% O.9%:

Notes 1 Includes cash dividends by Index members at the ijme of announcement

Cr~Jil r~ii"y> ~r~ ,,~>~ci 1.0, Curl-'Jr~i~ F~r"iiy R~li"y iur iviuuui~ ~"ci Curl-'Jr~'" Cr~uii Rcij"y iur S&P i-) l ,.,., i"ciic~i~~ lI~y~ii,~ l ~u>ilj"" uuliu"," Sh;Ye price appreciation less return In the S&P 500 over the same period Denotes Illustrative rating for To','er Illustrative rating for Broadcasting SpilCo is B118+to Ba3IBB-

5 Excludes Tower

,+30

11.8%)

"A (231%)

114%

11.5%)

(0.3%)

" (7.1%)

4.5%

(159%)

12.2%

34%

124.6%)

(129%)

(0.7%)

(21 B%)

13.3%

(20.7%)

2.6%

(03%)

(1.~0/.)

O."%:

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

:Excess Return,:'1 ,., ,+30

0.6% 11.2%)

" " ,me (244%)

(1.1%) '~A

2.7% 13.2%)

20'"' Ci ;,ok,

4.8% " (1.4%) (12.0%)

1.4% 0.9'%

(2.3%) (11.8%)

2.5% 9.4%

;" '~A

(0.2%) (26.1%)

(0.2%) (10 5%)

(1.4%1 (4.3%)

05% (223%)

8.5% 9.9'%

(1.1%) (23.9%)

(5.8%) 3.2%

CO% (38%)

o..1'k (2.Q0/.)

0.8% •. "1

16

MS 64887

Project Tower

Pri:l:Form'a ToWer Capitalii:<Itiort ~ $17,50Dfvii:lend

Pro Forma Capitalization -Publishing (Parent]

Cash and Cash Equivalents

Roll_ov@rNot@s

Term Loan A Bridge Loan Oth~, E~;'t;~g D~bt'"

Total Existing Debl

New I erm Loan A New Term Loan B

Total Debl (excl. PHONES)

PHONES

Total Debl (incl. PHONES)

Prooeed. tom Exerci.ed Option.

Total Sources

LTM PF Adj. EBITDA

Actual 121J1120(J6

m

1,526 1,500 1,310 ,. '''''

4,433

''" 5,333

$1,437

15t Priority Guaranteed Debt I LUI PF Adj. EBITDA SeniorDebtILTMPFAdj.EBrrDA 31x Total Debt I L TM PF Ad) EBITDA 3.7x

prQ- Forma CapiWizaiioo ~erQadeasting

New Term Loan A New Term Loan B

Bari-; Debt

New Senior Sub Noles

Tota! Debt

Credit Statistics LTM PF Adj. EBITDA

Senior Debt I L TM PF Adj. EBrrDA Total Debt I L TM PF Adj EBITDA

Morgan Stanley

i

Pro Forma Capitalization - $17.50 Dividend

------------,

Q1 Cash Flaw

~1.(S(rh~nl$

Pmjecte:d:,,: R"",apitalizatlO'n:j Pro:Forma:

JIJ1r.!O(1r !\;ljU?Il"flE!~t$ i 313112tJ07

'" '" I" 1 521

1 500 (1,500) (70) 1 240 (1,240)

97 {97)

4,358

~."UU 4.695

4.358 7,195

000

5.258 7,195

'"

$1.423 $1.412

Notes Sh"""" ~r" '''rrrl~ lur >~i~ '" SCi,i ~mi H"y ""'N>~~~"'~ Includes lees olS144MM

", 1 521

1,521

~."uu 4,695

8.716

000

9.616

'" ____ .~,~~_9 _______

$1.412

5.1x 62x eo,

Q2:&Q3t

!'IilIU'ln1el1t~

(10)

1"

I"~) (126)

Assumes Ql cash How I excess cash IS used toward paydown olthe rotlsling bridge loan 4 Includes c'p,talizod ReBI EstBts Option Bnd S"'BPS Bnd Oth~r obligotlons

Include. $33MM f •• ",b.te .Ithe time of the Spin_off

Projected 9I31lJ2007

m

1,512

1,512

~.44" 4.569

3,526

''" 9,426

'"

$1.390

5.0x 6.h 6.ax

Spin-off

Adj!lSI)'nenj$

(~.44:O)

(376»'

(2,321)

Spin"",if Adjusbnents

"0 1.600

1000

Pro F:orma

9JJDllOIrI

m

1,512

1,512

4.193

5,705

''" 6,605

'" 6,748

$986

4.3x ,~

6.7x

Pro Forma 09!3D1D7

''" 1,600 1,850

1,000

"01 ,.~

7.1x

:Sale otCub",/

com:cast

{602',

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

Pro:Forma

1113012007

1 512

1,512

3,591

5.103

'"' 6.003

,<0 6,146

Pro Forma 091JD1D7 ,,,

1.600 1,850

1 000

$401

,.~

",

17

MS 64888

Project Tower

Management Plan $T5hwe

40

35

30

25

20

15

10 17 50

5

a Publishing "I 75x

Broadcas1lng' , 9x

~ Cash Distribution

Projected Equity V3lue in 2009 (${Sh3re): - Broadcasting $6_00-- Publishlnf] $12.77

17.50

7.5x

'"

$9.70 $12.77

Morgan Stanley

i

Recapitalization Package Value 7.5x Publishing Multiple Includes Upfront Cash Dls'b'lbutlon and Publishing and Broadcasting Equity Values (1)

Research Case Management Downside Case: A (4) Management OownstdeCase:B(~) $Oi Sn~re

40

35

30

25

20

15 -

10

5

a

1750

7.5x

'"

1750

40

35

30

25

20

15

10

5

a

l1li Publishing Equity Value ::.: illJJ Broadcasting Equity Value 1'1

$580 $12AJ

$9,48 $12.42,

unconsolldaled assel value grows al S% per year 2 Assumed forNard EBITDA mUlllple al year end 2009

$2404

1750

7.5x

'"

5222 $6.;:0

$2624

17.50

7.5x 11,

$515 $6.20

3 For Bach SCBnariC eqUltyvaluBs arB based cn PV cfprojllC!ed stock prieB at year Bnd 2Q09 assuming a 11% cost of .""ty

$:; 5hwe

40

35

30

25

20

15

10

5

o 75x 9,

4 Management Downside Case A project< nat Broadcasting OCF and a 2')0 decline In publIShing revenue per year Management Downside Case B project<; a 1% decline in Broadcasting OCF and a 3% decline in publishing revenu. per year

$2331

75x

'"

$5.90-$J.71

18

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64889

Project Tower

40

35

30

25

20

15

10 17.50

5

o PUDlisning . 8x

Broad~asilng ," 9x

~ Cash Distribution

Projet1aJl Equity Value in 2009 ($IShartl); - BrOOdcaSnhg $6.00 - PubllstJing $14.58

$3590

17.50

8,

,"

$9.70 $14.58

Morgan Stanley

-

i

Recapitalization Package Value - 8x Publishing Multiple Includes Upfront Cash Dls"b'lbutlon and Publishing and Broadcasting Equity Values (1)

Research Case:

40

35

30

25

20

15 -

10

5

o

17.50

8,

"

$35 44

17.50

8, 11<

40

35

30

25

20

15

10

5

o

Publishing Equity Value ::.: U2W Broadcasting Equity Value 1'1

Notes

$5.80 $14.18

$9:.48 $14.112.

17.50

S2.22 57.04

$2728

17.50

8, 11,

$5.15 $7.64

40

35

30

25

20

15

10 17.50

5

0

" 9,

52.26 55.2::'

1 Assumes unconsolidated assets currently valued at $1 600MM (Food Network' SSOOMM: CareerBUIlder: S650~~M' Other Interactive Assets' $150MMI and that uncon,oliaated a,.et value gro",. at B-::. per year A«um~d r!m .... d EIlITDA Multipl~.1 Y".r ~nd 2009 For each scenario, eqUlt~ value, are based on PV of proJecled stock price .I~ear end 2009. assuMing. 11% ,oslofeqully

4 Mo"ogsmont D"""Slds Coss AproJsots fio! B",odoosting OCF ond 0 2%, dsolins in publishing rovsnus psr ylIBr Monagsmon! Downslds Case B prOjscts a 1%, d@cin@ln Bro8dc • .tlng OCF 8nd. 3% d@cllnolnpubl,.hlngr ..... en ... p"r Y08r

$2420

17.50

$5.90 $5.23

19

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64890

Project Tower

Management Plan $TShare

15

12

9

6

3

a

$12,29

Multiple: n 7 Ox 7 5x 8 Ox 8.5x

l1li Publishing EquityValue 12)

Pr<l-j~ct~d EquilyValu~ SI0.OO $12n S14.58 $1538 in 2009 ($ISham):

Morgan Stanley

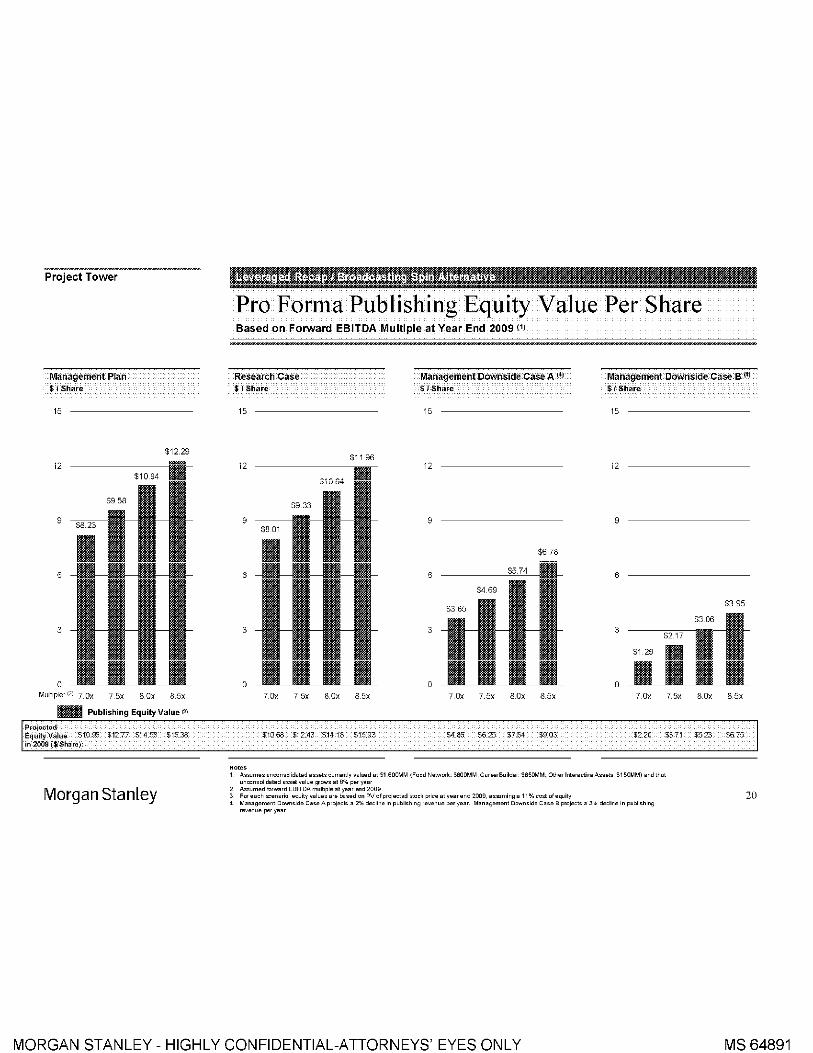

Pro Forma Publishing Equity Value Per Share Based on Forward EBITDA Multiple at Year End 2009 (1)

Researcli Case $ JSliare

Management DoWilside Case A (4)

$1 Share

Management Dowriside Case;H(4j $JSliare

15 15 15

$1196 12 ----- 12 12

9 9 9

$6,78

6 6 6

5395

3 3 3

a a a 70x 75x 80x 85x 7 Ox 7.5x 8 Ox 8.5x 70x 75x BOx 85x

$1068 $12.43 514 18 515,93 $2.20 $371 $523 $675

Notes A •• um~. "nwn.oiid~:~d ~ .. ~:. cu" .. ':I, ~~I ... d~: Sj,eOOMM (Fcod n":-"ori;: S800MM, C~r~;B"ild~;, $$SOMM; 0tl1~, In:~r~ctlv~A .. ~tl, S150MM) ~nd th~t unoonsolld.lsd .,,'" v.lue ,,"ows.1 8% psr y •• r Assumed forward EBITDA mUlllple al year end 2009 For each scenario, equity value. are b .. ed on PV oiproiect.d .wck price at yearend 2009, a.""ming a 11 % cosl oiequity M"nag~monl D",,'n~ld~ Ca<~ Aprol~ol<" 2% d~olino In publi<hlng r~v~nu~ p~ry~ .. M"n.g~m~nt Down<ldo C"~~ B P"'J~ot<" 3% d~ol,"~ In publl<hlng revenue por year

20

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64891

Project Tower

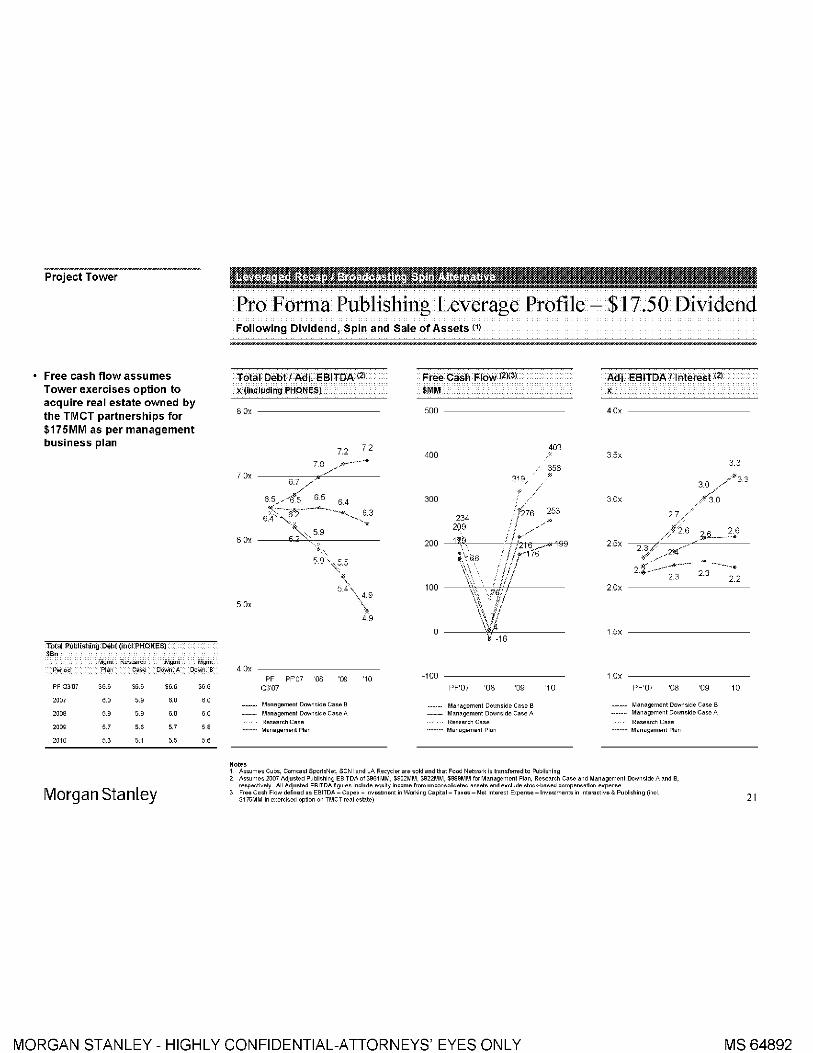

Free cash flow assumes Tower exercises option to acquire real estate owned by the TMCT partnerships for $175MM as per management business plan

Total Publishing:OIlllI (incl PHONES] $BiI

~g(rri Re'ea"'h ivJl'lmi ilijgrtn: I'arioil PI~n c~~~ O:QVM:A ClQ\Vn.:S:

PF 03'07 S6,6 S6,6 $6,6 $6,6

2007 " 5.9 ,., " 2008 5,9 5.9 " " 2009 ,; ,., ,; " 2010 5,3 5.1 5,5 5,6

Morgan Stanley

i

Pro F onna Publishing Leverage Profile - $17.50 Dividend Following Dividend, Spin and Sale of Assets (1)

Total Debt IAdj.EBITDA(2) x:{in~luding PHONES}

8,Ox

7.2 {,2

Free Cash Flow 12)(3)

$MM

500 ---------

400

319

300

234

403

356 •

Adj.E8ITDAIlnt.fe.t(~

•

3.0

27,/ .

3.3

60,

299

200 1 '1m., 2,5x /1"'2 6 ~.1§-- ~~6

~~,~.rl·~ 5,9 ",\5.5

, '-5.4, 2,Ox

\4.9

\, 49

1,5x

40, PF PF'07 08 '09 ,0 -100 ------------ 10x

03'07 PP07 '08 '09 '10 PF'07 '08 '09

- M.nBgsment DawnSids Case B

- Management Downside Case A Management Downside Case B

__ Management Downside Case A Management Downside Case B

••••••. Management Downside Case A

Research Case Research Case Research Case

- Management Ptan -- Management Plan ~ Manag.ment Plan

Notes 1 Assume. Cub., Com"".t Sport.Net. SCNI and LA Recycler are sold and that Food Network i. tran.rerred to Publi.hing 2 Assumes 2007 Adjusted PubtlShlng EBITDA of S961 111M. $952MM $S22MM $OO9MM for Management Plan. Research Case and lIIanagement Downsicle A and B.

respectively. All Adjusted ~BITDA figures include equity income rrOOl unconsolidated assets and e.clude stock·based compensatim expense 3 Free CBsh Flow definsd.s EBITDA _ Capex _ InvBStment in Working Capltat _ T.xes _ Net Interest Expense _ tnvestments In IntsrHctlvs & PublIShing (lncl

S175MM in exercISed option on TMCT reat estate)

'10

21

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64892

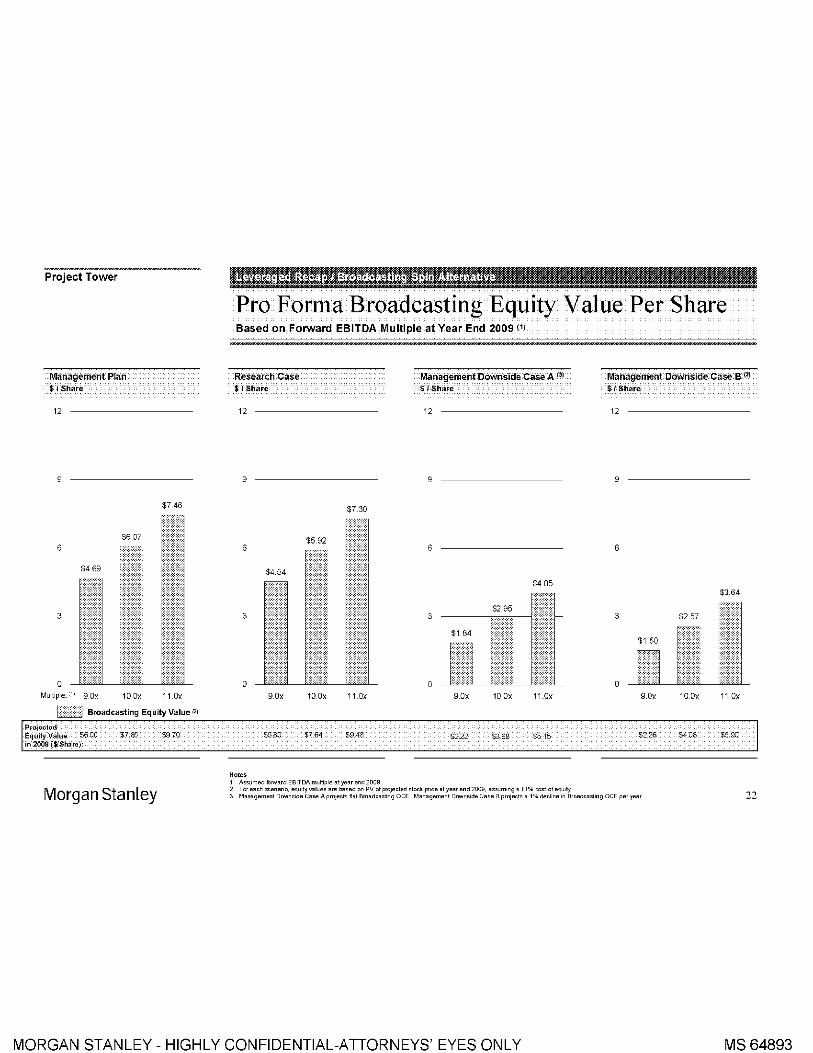

Project Tower

Management Plan $TShare

12

9

6

3

0 Multiple' :', 90, 10 Ox

$7.46

110x

Broadcasting EquityValue (21

$785 '" 70

Morgan Stanley

i

Pro Forma Broadcasting Equity Value Per Share Based on Forward EBITDA Multiple at Year End 2009 (1)

Researcli Case $ JSliare

12

9

6

3

0 90,

S580

r-lotcs

$7.30

10 Ox 11 Ox

$7,64 $9.48

Assumed fo~,,'ard EBITDA multiple at year end 2009

Management DOwnside Case A (~l $1 Share

12

9

6

$405

3

0 90, 10 Ox 11.0x

5222 $3.68 $515

For each scenario. eqUlt~ vatue, are based on PV of projected stock price at year end 2009, assuming a 11% cost ofequl!y

Management Dowriside Case;a: lJ) $JSliare

12

9

6

$3.64

3

0 9.0x 10 Ox 110x

$2.26 $4,08 $590

3 MB"BgSmont D"""Slds CB"" AproJeots fiB! BroBdoB:mng O(;F. Management Downside Case B projects a 1'" dedlne In Broadcasting OCF per 1ear 22

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64893

Project Tower

Tot; Broadcasting: Debt $Br.

",,", Research Mgmt 'oM I"eflod """ Case Dowo.A Dowo. B.

PF Q3'OT "" "" ,," S2.9

2007 '" '" '" '" 2008 " " '" n

2009 " " " " 2010 " " " , .•

Morgan Stanley

i

Pro F onna Broadcasting Leverage Profile - $17.50 Dividend Following Dividend and Spin (1)

Total Debt I Adj.EBITDA(~ x :iilOlt;ll,Idif!g:PHQ!\IE$)

74 74

7,Ox

6,Ox

40, PF PF'07 " '09 ,0

03'07

---- Management Down.ide Case B

- Mene9smsnt DownSids Cess A

Rsssarch Cess

- Management Plan

Notes

Free Cash Flow (2X3) $MlVI

200

150 139

" //125

100

50

o PF'07

.;{~~. 100-/102./"

;/ / 88' .

,I oj

'08 '09

___ m Mene9smsn! Downs,ds Case B _ Management Downside Cass A

Research Case ~ Management Plan

'10

1 Assumes Cubs and Comeast SportsNet are sold and thai Food Nel,mrk is Irnnsferred to Publishing

Adj. EBITDA II nt.,.st1~ , 30, ----------

25, _________ --'2C'L-

19 . .-;; ,.' 2 0 1.8

1,V" 1.7 .~. Jl>--' _.~ :;;. ~~~ -'--~"'" ~_r' 1.8 18

1 7 1.7

15, ----------

10x -----------

PF'07 '08 '09

~~anagemenl Downside Case B ~ Management Downside Case A

Reseerch Caso -~ Management Plan

'10

2 AS"-lmes 2007 Mjusted Broadcasting EBITDA of$390M~4. $393M~4. $382M, $382MM for Management Plan Research Ca,e and Management Downside Case A and B, respedivsly All Adjusted EBITDA ~gu",s 'ndude squity Income from unconsol,datsd e"ets end e,dude stock-based componsatIOn expsnss

3 Free Cash Flow de~ned", EBITDA- Cape~ -Inves/menlln Working Capital - T""M - Net Interest Bqlense

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64894

Project Tower

Tower Financial Projections Overview

Morgan Stanley

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64895

Project Tower

For Tower Consolidated we have analyzed four sets of projections for the period 2007E - 2011E

Management Plan based on Management's Revised Operating Budget received on March 17, 2007

Research Case based on current '.'Vall Street consensus

Management Downside A projects a 2% annual decline in Publishing revenue and flat Broadcasting OCF as per management projections as of March 17, 2007

Management Downside B projects a 3% annual decline in Publishing revenue and a 1% annual decline Broadcasting OCF as per management projections as of March 17, 2007

Consolidated HistmiQaI:Fimmcial:s \<Ci

$M:r.1 2G03A N.l4A 20a~ 200""';

R .. ""nu .. $5,456 55,591 $5,473 S5395

% Growth 3.9% '" 12.1)% (14!%

EBITDA ,', $1543 $1,410 $1,361 $1301

% Growth 7.9% (861% 13.5)% (44!%

% Margll7 28.3% 25.2% 24,9% 24,1%

Morgan Stanley

Tower Consolidated Projections Management, Research and Management Downside Cases (1)

toWer Consaiidated:Revenue (2)

$MM ••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••••

CAGR '07E '11E 7,000 ManagemenlPlan 11%

Research Case 1 4% 6,500 Mgmt DownSide Case A (1 2%)

Mgmt Downside Case B 120%)

6,000 ~""O~'"'~'~'""~'"5~30"'15".~?6~,~="''"'S.~''"9=O~'-,-c------s-.. -,-"c.-"cs------CoCooC'"5'.5""'-----'5'.5,""",,5'.6~4rn6-----~j~~ ----"Cr""-'"'II "-'.>li~I~II~l~"'~=-~5-------J-----,I=-iiil---=In=5~S04C--91---cITIIm-II-=i-4948-----jllJ~::"-oc

2009E 2010E 2011E 2007E

Ma nagement Plan

2008E

Research Gase _ Management DownSide Case A U Management Downside Case B

Source Management BUSiness ~Ian and Wall Street research

'MOl

CAGR '07E-'11!: Mgmt Case 22%

1 800 Research Case 24% Mgmt DownSide Case A (4.3%)

1 600 Mgmt Downside Case B (6.9%)

1 400

1 200

1,000

800

1, 386 1,357 1,3811381

2009E 2010E 2011E 200lE ED Management Plan

2008E Research Case Management DownSide Case A C Management DOINnside Case B

Margin (%] 236236229225 245239223215 248241219205

Source Management BuS;'BSS ~Ian and Wall Street r.sBarch

,",ore 1 Management Plan and Management Downside Case. based on March 2007 revised Tower financial packa~e 2 All caSBS arB ~ro forma for sale of seNI and Albany Atlanta and Boston TV "'atims 3 Includes stock-based compensation ""pense and allocated corporate overhead based on revenue con1ributlon

248241219205 24.7245202183

24

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64896

Project Tower

For the Publishing business we have analyzed four sets of projections for the period 2007E - 2011 E

Publi5hing Historical Financials 1!)

$M,~ 2~~lA ~~MA 2.!lQ!;A WCM

R .. venu" $3,998 $4,090 $4,058 53987

% GIUt,'th '" 2.3% (08)% (17)%

EBITDA )1 $1,016 $991 S942 $880

% GIUt\·th 3,5% 12.51% [4,91% r6,7)%

% Margin "" 24.2% 23.2% 221%

Morgan Stanley

Publishing Projections Management, Research and Management Downside Cases (1)

Punlishlrig ReventieY) $MM

CAGR '07E-'11E 5,000 Management Plan 07%

Research Case 04% Mgmt Downside Case A (2.0%)

4,500 ~Mcg,mc'cDcocwco'c;dcecCc'c'cecB~_c(c3cOc%"i~

3 9463,93t 3,9083 867 3,9683,960 3 B29_ __ 3, 997 3,948 4, 0233,969 4,0523,991

-C;C.':"'C::':C:':lB~~C"'oo."'CI --cr::C:'::C'::'~::1 'CC"."'-',c, "OO,-----,lcfc::::c:::Ic:c~~CJ'52"3-6-3-8---"·~:~"·: "ti"1 =c3c,OC,"O-3-3-,,----iNTI'---,13-,s-o-,---

I,ll I I III I IIIII II ILl INTI I, 15 4,000

3,500

3,000 2009E 2010E 2011E 2007E

IJ] Management Plan 2008E

Research Case _ Management DoVllllslde Case A D Management Downside Case B

Source Management BUSiness ~Ian and Wall Sireel research

Publishing ESITDA (<'l(~

'MOl

CAGR '07E-'11E Mgmt Case 1 4%

1,200 Research Case 07% Mgmt Downside Case A (6.4%)

1 000 L'M,g"m~'~D,O"W"O,,",'"C~'",,',B---'(100",2~%.i._~------------'"~'".------------.ec-c"'----------~H4-,,~""----------863 854,824 791 ITT 856 782 ._._ ~ 864 ITa 815

bOO IlI1IIl I II Iil!iF"=II .:. '" III I Hili '-HI 600

400 2009E 2010E 2011E 2007E

rrrn Management Plan 200SE

Research Case

222216204193

Management Downside Case A I Management DownSide Case B

Margin (%] 21 921 7 21 1 205 223219197180

Source Managem.nt Busiless Plan and Wall Street r.search

,",ore 1 Management PI"" and Managemenl Downside Case. based on March 2007 revised Tower financial package 2 All cases are pro forma for sale ofSCNI 3 Includes slock-ba,ed compensallon ""pense and allocaled corporale overhead based on revenue con1ribullon

224220189166 225220176151

25

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64897

Project Tower

For the Broadcasting business we have analyzed four sets of projections for the period 2007E - 2011 E

Revenue

% Gro .... th

EBITDA 1<

% Gro .... tll

% Margin

$1,457 $1,501 51,415

7.9% 30% (57j%

$525 $549 S447 11.9% '" (1851%

36,0% 36,6% 31.6%

Morgan Stanley

$1,408

(05)%

$422 (571%

29,9%

Broadcasting Projections Management, Research and Management Downside Cases (1)

B roadcastirig: Revenue: (2) $:MM

CAGR '07E-'11E 2,200 Management Plan 2,2% Research Case 4,1% 2,000 Mgmt Downside A 11%

l,800L!M=g~m~'~D;g~W~g'~'d~e~C;;~;=====Oi6~%~~~~~~====~~~~~~~====='~~~~~~~==~~~~~~~:===

:;:: ~.';lt4IOm'393~'4:0~1402hlF.'4II~C .. , •... ,.:' .. : •... , •.• I~ ~liiilrli'4T= 'm ==11·111 I =i l I PIIII I =il I . I

2009E 201 DE 2011 E 2007E lJj Management Plan

2008E L Research Case IIfM Management Downside Case A U Management DOlNrlside Case B

Source Management BlJSlnBSS Plan and Wall Street r.sBarch

'MOl

600

500

CAGR MgmtCase Research Case Mgmt Downside A Mgmt Downside C

'07E-'11E 41% 5,6%

(0.2%) (1.3%) 484 482 470 502 ___ _

_,,4c01""4_04 .. 3,,92.,39_' __ -jmTIt-----l391 387 ?rn390 382 mIT in 377

1

If:i:::i::::i!: 373

1 jJJI i ~Jil I b:1 I =1It I HI I t 400

300

200

20D7E 2008E 2009E 2010E 2011E

W:t Management Plan Research Case m Management Downside Case A U Management Downside Case B

Margin (%] 28,628,628,228,2 30,6 29,9 27,5 27,6 31 ,4 29,7 27,6 27, 1 31,6 30,0 27,1 26,6 30,7 30,3 26,7 26,1

Source Management Busiless Plan and Wall street research

"o(e 1 Management PI"" and Management Downside Case. ba.ed on March 2007 revised T"wer financial package 2 All caSBS arB pro forma for sale of Albany, Atlanta and Bosten TV st,tlons 3 Includes stock-based compensation ""pense and allocated corporate overhead based on revenue con1ributlon 26

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64898

Project Tower

Discounted Cash Flow Analysis

Morgan Stanley

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64899

Project Tower

Key assumptions

4.75 year DCF

3/31107 valuation date

Mid-year discounting

Cash tax rate of -33-35%

Treais ::;iock-based compensation as cash

Cubs separately valued

Unconsolidated assets include Food Network ($800MM) and CareerBuilder ($650MM), Comeasl SportsNet ($150MM), Cubs ($450MM) and other interactive assets ($150M M)

Morgan Stanley

DCF Analysis: Management Plan

sumhHtl)' Of KeyFlhM:elaFS for DCFAnatySIS:

Revenue Growth (%)

EBITDA

Margm (%)

D&A

Operating Income

Less Tax Tax Rate (%)

Add Back' D&A

Less' Capex & Investments

Change In Working Capital

Unlevered Free Cash Flow

Source Management Busilsss plan

Manageillent,Plan !5MM,exQept Pili" $hil;re iIIT\O!.Injsf

Di$Co\.lit Rate 2012 E"it Multiple

Presenl Value of

C~sh flew _ Ys~rs 1 _ 5

Terminal Value

Aggregate Value

Less Net Debt

Add: Unconsolidated Investments' I,

EquityValue

Valu .. psr ShHr .. ll • P......,.,oumIjDlscaunl) ill "",,..,,t /%/,'<)

Terminal Value as % of Agg Value

Implied Perpetual Gro'Nlh:"

Implied 2007 EBITDA Multiple-

Notes

S5,407

$1,357

($208)

S1,149

($344) 29,9%

$208

($276)

(S39) $698

8.0"

$2,177

7,512

$10,181

(5,085)

2,200

$7,295

$30.10

(33%j

74%

(04%)

"',

S5,195 $5,153 $5,246 (08%) 18%

$1,278 $1,245 $1,311 246% 242% 250%

($221) ($236) ($236)

Sl,057 $1,008 $1,074

($358) ($334) ($373) 33,8% 33,1% 34,7%

$221 $236 $236

($425) ($221) ($446)

(S56) (S20) (S27) $440 $670 $484

7.00% 8.5". ,."

$2177 $2,177

7981 8,451

$10,649 $11,118

',5085) (5,085)

2,200 2,200

$7764 $8,233

",.ro $33.96

2);1% ,,.

'" 7&'10

(00%) 03%

" ", " ",

$5,278 $5,345 06% 13%

$1,336 $1,362 253% 25.5%

($240) ($240)

$1,095 $1,122

($379) ($381) 34.5% 33.9%

$240 $240

($226) ($224)

(S28) ($28) $703 $729

8.00";1, ,", ".

$2121 $2,121

7120 7,565

$9,733 810,177

(5085) (5,085,'

2,200 2,200

$5847 $7,291

$28.25 $W.OS

(9.3%! 134%)

'" 74%

04% 0.8%

, ", "~

1 Unconsolidated assets include Food Network (SBOOMM) and CareerBUIlde, ($650MM) Comca" SportsNetl$150MMI Cubs ($450MM) and other interactive ~»~,~(SI50ivi;,;!

Based on 242 4MM FDSO Based on Tower share price ofS31.13 as of March 213, 2007

4 Excludes value ofunoon.olidated inve"'menls

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

$5,370 05%

$1,358 25.3%

($181)

$1,177

($356) 30.2%

$181

($224)

($28) $749

", $2,121

8,010

$10,i121

(5,085)

2,200

$7,736

$'3:1;91

''''' '" 12%

e "

27

MS 64900

Project Tower

Key assumptions

4.75 year DCF

3/31107 valuation date

Mid-year discounting

Cash tax rate of -33-35%

Treais ::;iock-based compensation as cash

Cubs separately valued

Unconsolidated assets include Food Network ($800MM) and CareerBuilder ($650MM), Comeasl SportsNet ($150MM), Cubs ($450MM) and other interactive assets ($150M M)

Morgan Stanley

DCF Analysis: Research Case

sumhHtl)' Of KeyFlhM:elaFS for DCFAnatySIS:

Revenue Growth (%)

EBITDA Margm (%)

D&A

Operating Income

Less Tax Tax Rate (%)

Add Back' D&A

Less' Capex & Investments

Change In Working Capital

Unlevered Free Cash Flow

Source Wall Street researoh

Research Gase t-$!.'IM; ~Jl<;ept:p"rsh:ilT!>"IlJDI<I"sl

DiSccil..i1tRate 2Q12 ElIitMultipie

Presenl Value of

Cash flow - Years 1 - 5

Terminal Value

Aggregate Value

leSS: Net UeOt

Add: Unconsolldaled InvestmMts'-'

EqUity Value

Value p~r Share'''!

Pr",,,hlm/(Disoo,mllio ow-renl (~I (:

Terminal Value as % of Agg Value

Implied Perpetual Gro',Ah';

Implied 2007 EBITDA Multiple'"

Notes

S5,407

$1,357

($208)

S1,149

($344) 29,9%

$208

($196)

S70 $887

a.ox

$2,321

7476 $10,304

(),u~~)

2.200 $7,419

$30.61

111%/

73%

(1.1%) 8.3)(

S5,302 $5,147 (29%)

$1,299 $1,239 245% 241%

($232) ($224)

Sl,067 $1,01e,

($361) ($336) 33,8% 33,1%

$232 $224

($203) ($192)

(S56) (S20)

$679 $692

7.00~

8.5x

$2,321

7,943

810,770

1~,Utl»)

2,200

$7,665

$:325-3 ". ,,%

0'07%1

",

$5,227 $5,293 $5,364 16% 13% 13%

$1,273 $1,301 $1,333 243% 246% 24.9%

($228) ($230) ($233)

$1,04e. $1,071 $1,100

($363) ($370) ($373) 34,7% 34.6% 33.9%

$228 $230 $233

($364) ($178) ($174)

(S27) ($28) ($28)

$519 $725 $757

8.1J0";l, 9.0x , .... a<,

82,321 $2,260 82,260

8410 7,086 7529 811,237 $9,654 $10,296

(),Utl:>l 1~,UtIO) (),U~~I

2,200 2,200 2,200

86,351 $6,969 87,411

$34.45- $28.75- $30.57

tol%. f7.fi%; (1B%/

>0% n% n% (0.3%) (03%) ,,%

9.1x ", 8.3)(

1 Unconsolidated assets include Food Network (SBOOMM) and CareerBUIlder ($650MM) Cornca" SportsNetl$150MMI Cubs ($450MM) and other interactive ~»~,~(SI50ivi;';.'

Based on 242 4MM FDSO Based on Tower share price ofS31.t3 as ofM"rch 213, 2007

4 Excludes value of uno en. elida ted inve"'menls

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

$5,434 13%

$1,358 25.0%

($236)

$1,122

($339) 30.2%

$236

($173)

($28)

$818

9.0x

$2,260

7,972

$10,736

(~,OOO)

2,200

$7,653

$324U

'" 74%

06% 8.7)(

28

MS 64901

Project Tower

Key assumptions

4.75 year DCF

3/31107 valuation date

Mid-year discounting

Cash tax rate of -33-35%

Treais ::;iock-based compensation as cash

Cubs separately valued

Unconsolidated assets include Food Network ($800MM) and CareerBuilder ($650MM), Comeasl SportsNet ($150MM), Cubs ($450MM) and other interactive assets ($150M M)

Morgan Stanley

DCF Analysis: Downside Case A

sumhHtl)' Of KeyFlhM:elaFS for DCFAnatySIS:

Revenue Growth (%)

EBITDA Margm (%)

D&A

Operating Income

Less Tax Tax Rate (%)

Add Back' D&A

Less' Capex & Investments

Change In Working Capital

Unlevered Free Cash Flow

Source Wall street research

Man agem ehtDoWti side:Case: A t-$!.'IM; ~Jl<;ept:p"rsh:ilT!>"IlJDI<I"sl

DiSccil..i1tRate 2Q12 ElIitMultipie

Presenl Value of

Cash flow - Years 1 - 5

Terminal Value

Aggregate Value

leSS: Net UeOt

Add: Unconsolldaled InvestmMts'-'

EqUity Value

Value p~r Share'''!

Pr",,,hlm/(Disoo,mllio ow-renl (~I (:

Terminal Value as % of Agg Value

Implied Perpetual Gro',Ah';

Implied 2007 EBITDA Multiple'"

Notes

S5,407

$1,357

($208)

S1,149

($344) 29,9%

$208

($276)

(S39) $698

a.ox

$1,761

5323

$7,550

(),u~~)

2,200

$4,664

$19.24

1382%1

71%

(0.6%)

6.3)(

S5,195 $5,107 $5,047 (17%) (12%)

$1,278 $1,197 $1,150 246% 234% 228%

($221) ($223) ($216)

Sl,057 $97e, $934

($358) ($322) ($324) 33,8% 33,1% 34,7%

$221 $223 $216

($425) ($221) ($376)

(S56) (S20) (S27) $440 $634 $422

7.00~

8.5x 9.0x

$1,761 81,761

5,656 "" $7,662 86,213

1~,lJtI») (),Utl:>l

2,200 2,200

$4,996 85,326

"',., $21.111

1338%) 12Q 4%/

n% n% 0'02%'1 0>%

", O~

$4,957 $4,905 (18%) (10%)

$1,106 $1,061 223% 21.6%

($214) ($209)

$392 $352

($308) ($289) 34.6% 33.9%

$214 $209

($176) ($174)

(S28) ($28)

.'" $569

8.1J0";l, , .... a<,

$1,717 81,717

5,046 5361

$7,226 87,542

1~,lJtI») (),U~~I

2,200 2,200

$4,343 84,657

$17.91 $19.21

1425%; 1383%/

'~h '" O~h ,'" 0', 6.3)(

1 Unconsolidated assets include Food Network (8BOOMM) and CareerBUIlder ($650MM) Corncast SportsNetl$150MMI Cubs ($450MM) and other interactive ~»~,~(SI50ivi;';.' Based on 242 4MM FDSO Based on Tower share price ofS31.13 as of March 213, 2007

4 Excludes v.lue ofunoon.olidated inve"'menls

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

$4,845 (12%)

$997 20.6%

($163)

S334

($252) 30.2%

$163

($174)

($28)

.'"

9.0x

$1,717

5,677

$7,857

(~,OO»)

2,200

$4,972

OW" (341%;

n% 10%

6.6)(

29

MS 64902

Project Tower

Key assumptions

4.75 year DCF

3/31107 valuation date

Mid-year discounting

Cash tax rate of -33-35%

Treais ::;iock-based compensation as cash

Cubs separately valued

Unconsolidated assets include Food Network ($800MM) and CareerBuilder ($650MM), Comeasl SportsNet ($150MM), Cubs ($450MM) and other interactive assets ($150M M)

Morgan Stanley

DCF Analysis: Downside Case B

Summary of Key :Finarn::ials for DCF:Analys[s

Revenue Growth (%)

EBITDA Margm (%)

D&A

opcmt:ng inccmc

Less: Tax Tax Rate (%)

Add Back OM

Less: Capex & Investments

Cha nge in Working Ca pita I

Unlevered Free Cash Flow

Source Wall street research

Man agem ehtDoWti side:Case: B t-$!.'IM; ~Jl<;ept:p"rsh:ilT!>"IlJDI<I"sl

DiScciLi1tRate 2Q12 ElIitMultipie

Presenl Value of

Cash flow - Years 1 - 5

Terminal Value

Aggregate Value

LeSS: Net UeOt

Add: Unconsolldaled Investm€!nts'-'

EqUity Value

Value p~r Share'''!

Pr",,,hlm/(Disoo,mllio owrenl (~I (:

Terminal Value as % of Agg Value

Implied Perpetual Gro',Ah';

Implied 2007 EBITDA Multiple'"

Notes

$5,323

$1,357

(S221)

$1,136

(S340) 299%

S221

(S108)

($39)

$870

a.ox

$1.602

4550

$6.608 ().u~~)

2.200

$3.722

$15.36

1507%1

69%

10.7%) 5.7)(

$5,195 35066 S4950 (2_5%) (23%)

$1,278 $1,164 $1,087 246% 230% 220%

(S221) ($221) ($212)

$1,057 $943 $875

(S358) ($312) ($304) 338% 331% 347%

S221 $221 $212

(S247) ($211) ($356)

($56) ($20) ($27)

$617 $621 $400

7.00~

S.5x 9.0x

$1,602 81.602

4,834 5118

$6,891 57.175

1~,lJtI») ().Utl:>l

2,200 2.200

$4,006 54.289

$:16;5-3 $17.70

1469%) 1432%/

,,% ,,%

m2%1 0;%

;" 6~

$4,843 $4,739 (22%) (21%)

$1,014 '946 209% 20_0%

($209) ($202)

$805 $744

($278) ($252) 34_6% 33_9%

$209 $202

($156) ($154)

($28) (S28)

$552 $511

8.1J0";l, S .... a<,

$1,56.2 81.562

4,313 4582

$6,331 56.599

1~,lJtI») ().U~~I

2,200 2.200

$3,445 53.714

$14.21 $15.32

15-4-3%; (5Q8%/

68% 00%

O~h 00%

", 5_7)(

1 Unconsolldaled assets include Food Nelwork (SBOOMM) and CareerBUIlder ($650MM) Corncast SportsNell$150MMI Cubs ($450MM) and other inleractlve ~»~,~(SI50ivi;,;!

Based on 242 4MM FDSO Based on Tower share price ofS31_13 as of March 213, 2007

4 Excludes v.lue ofunoon.olidated inve"'menls

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY

$4,638 (21%)

'864 18_6%

($157)

$707

($214) 30_2%

$157

($154)

(S28)

$468

9.0x

$1,562

4,852

$6,008 (~,OO»)

2,200

$3,983

$"16;43

1472%;

71%

10% 5_9)(

JO

MS 64903

Project Tower

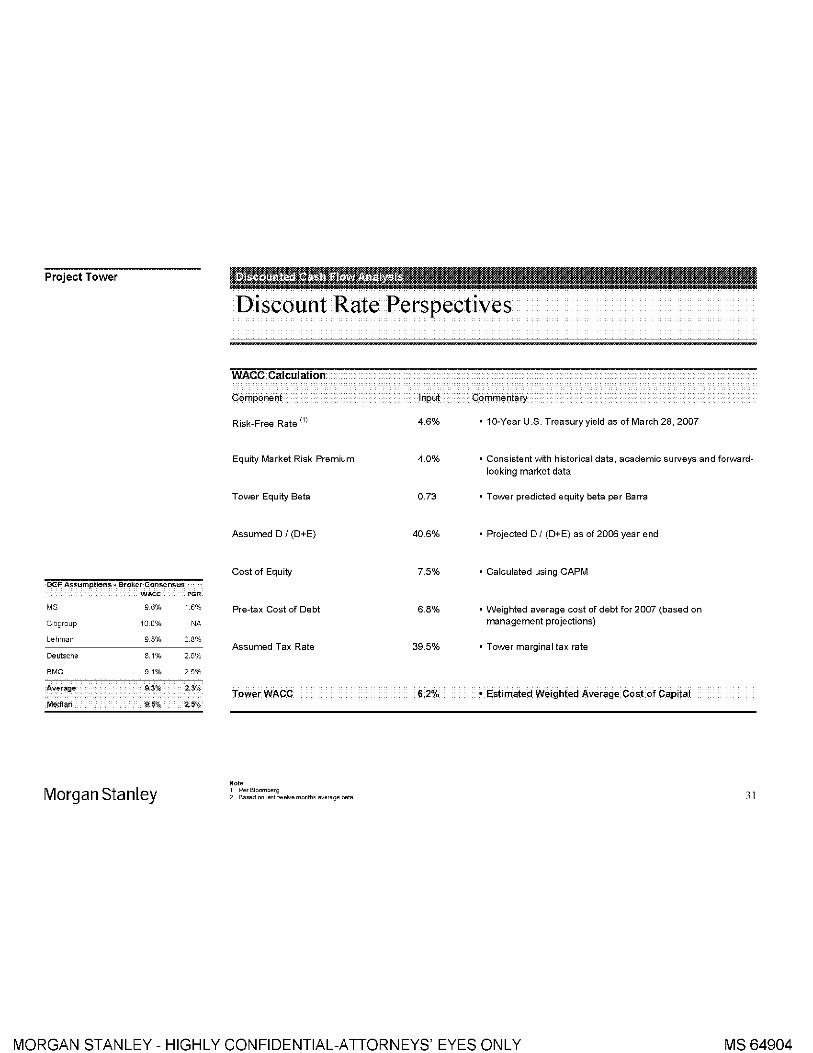

DCI" Assumptlens - Broker Consensus w~c ,G,

MS 96% 1.6%

Cltlgroup 100% NA

Lehman 9.5% 2.8%

Deutsche 8.1% 2.5%

BMO 91% 2.5%

Average g.~% 2.~%

Median 9.5% 2.5%

Morgan Stanley

Discount Rate Perspectives

WACC Ca]culation

Component

Risk-Free Rate (1)

Equity Market Risk Premium

Tower Equity Beta

Assumed D I (D+E)

Cost of Equity

Pre-tax Cost of Debt

Assumed Tax Rate

TowerWACC

Note 1 Per Bloomberg 2 B .... d on I.st lws"s months .v.r.ge bsm

Input

4.6%

4.0%

0.73

40.6%

7.5%

6.8%

39.5%

Commentary:

• 10-Year U.S. Treasury yield as of March 28, 2007

• Consistent with historical data, academic surveys and forwardlooking market data

• Tower predicted equity beta per Barra

• Projected D I (D+E) as of 2006 year end

• Calculated using CAPM

• Weighted average cost of debt for 2007 (based on management projections)

• Tower marginal tax rate

• Estimated Weighted Average Cost of Capital

31

MORGAN STANLEY - HIGHLY CONFIDENTIAL-ATTORNEYS' EYES ONLY MS 64904