Embed Size (px)

Citation preview

Project Management – Return on Investment

ILM 2014 - Session 4Tara LovejoyJanuary 2015

Today

• Use a simple tool for determining the financial viability of the project• List areas where net savings can be achieved as a result of the

workplace project• Identify wider non-financial implications that can result from the project

1.Resources, cost and quality2.Investment appraisal and financial viability, including net savings 3.Social return on investment

Project management life cycle •Market research completed•Best practice identified and incorporated into project•Project objectives defined•Project scope defined•Outputs/outcomes•Stakeholder buy-In•Team assembled•Business case created•Appraisal of project concept (Project brief, PID or business case prepared)•Approvals gained

•Feasibility Study•Detailed planning – PID•Work Breakdown Structure•Resource Breakdown Structure•Gantt chart•Budgeting•Risk/quality measures•Risk Register•Quality Plan

•Project completion•Monitoring and evaluation•Impact assessment•Best practice shared•Project team future•Further phases of project decided

•Controlling delivery•Monitoring•Evaluation•Change management•Regular 4-way reporting•Review of estimate budget and timescales against actual•Variance analysis reporting to senior management

•Project manager leading project•Action plan published , issued to team•Implementation plan/Gantt chart used•Risk Register used•Quality Plan used•Regular project team meetings•Delegation and motivating team

Resources, cost and qualityGetting the balance right is important to maintain quality during the project period

Meeting operational, time and cost criteria• PID for setting out the criteria for project deliverables and scope• Gantt chart for time management• PBS and/or WBS for operational tasks and achieving project outcomes• Quality plan to manage quality criteria• Communication plan to ensure everyone knows expectations and how stakeholders will be kept up to

date• Risk register for overcoming obstacles and achieving targets for operations, time and cost• Variance analysis and financial ratios for managing profitability and return on investment

Costing budget and assessing viability

Costs Return

1. You may only have a vague idea of costs, so provide estimates

2. Include all capital and revenue costs (check the PBS/WBS/RBS)

3. Ideally, obtain 3 quotes/estimates for costs associated with the project

4. List your planned expenditure (costs) - consider the cash-flow and any expected deficits that may need approvals

5. Include any indirect costs and contingency sums

1. List your planned income (direct and indirect) as a result of the project

2. Focus on the tangible and intangible returns on investment (are there any social and/or strategic returns?)

3. Focus on break-even point (timescale and volume)

4. Focus on cost efficiency savings both direct and indirect

5. Consider sensitivity analysis based on a reduction of 10% and 20% income (or increased costs of 10% and 20%) to see if the project is still viable

Example:• All projects have costs

• If there is no equipment and/or materials associated with your project, there will be human resource costs that can be calculated

2014-15 2015-16

Equipment[item][item]

£ £

Materials[item][item]

£ £

Labour[item][item]

£ £

TOTALS: £ £

Resources £per hour[day/week/month]

Project manager £50 x 10 hrs = £500

Project admin £20 x 15 hrs = £300

[operations 1] £35 x 10 hrs = £350

[operations 2] £35 x 20 hrs = £700

TOTALS: £1,850

TASK: Let’s have a go …

TASK 1: Income TASK 2: Expenditure

• CALCULATE YOUR ESTIMATED INCOME

• What is your expected income?

• What are your expected cost savings?

• Will there be peaks and troughs e.g. seasonal trends?

• What are the indirect benefits that can realise additional income e.g. better quality of service may attract new customers

• CALCULATE YOUR ESTIMATED OUTGOINGS

• What are your start up costs?

• What are your running costs (operations)?

• All projects have expense, include your resource costs (staff time x no of hours)

Will you be using a cash-flow to manage finance?

Cash Flow

• Helps ensure that you have enough money each month to fund the project.

• The most important tool to use in managing your finances.

• The model is split into three categories:

1.Money in2.Money out3.The balance

• The majority of projects fail due to taking longer and costing more = contingency planning 10-20%, but good planning and managing deficits on cash flow will help avoid this.

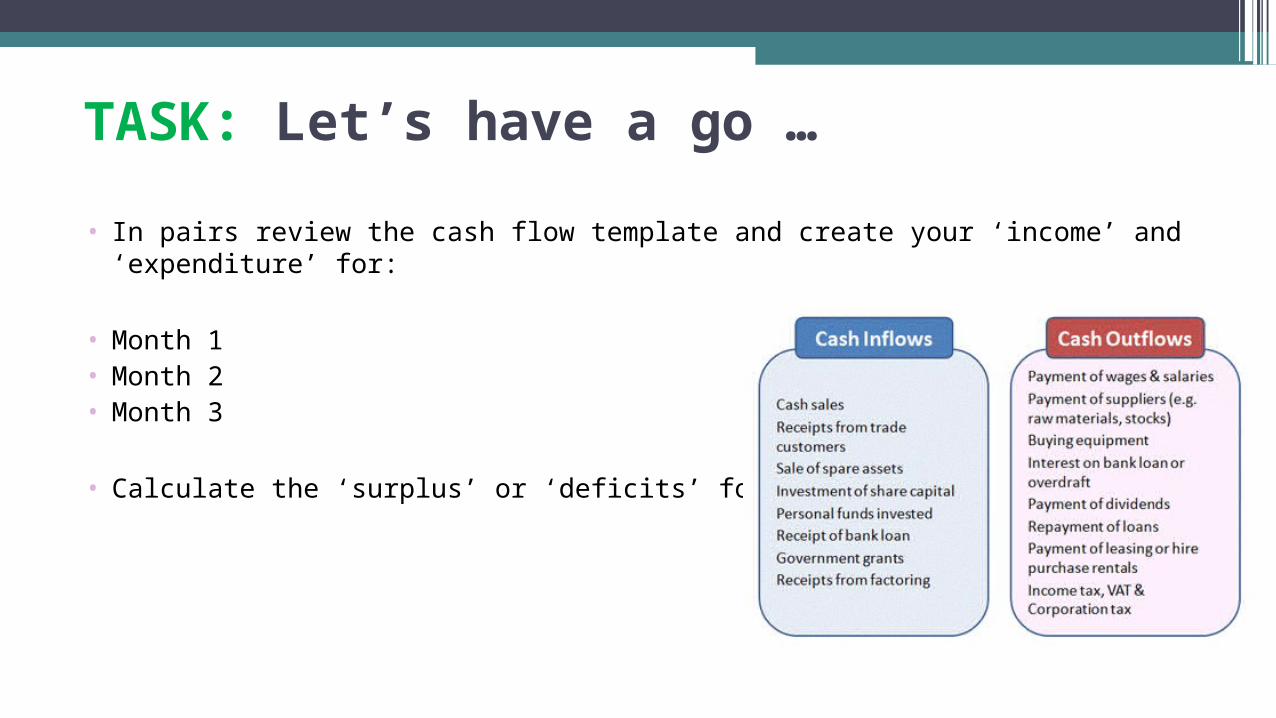

TASK: Let’s have a go …

• In pairs review the cash flow template and create your ‘income’ and ‘expenditure’ for:

• Month 1• Month 2• Month 3

• Calculate the ‘surplus’ or ‘deficits’ for these months

Variance reports

Quality management

• Quality planning - clear definition of the project aims, outcome and what the deliverable are and how these are going to be measured. Include assessing the risks, setting high standards, keeping an audit trail and measurement of success

• Quality assurance - uses a system of quantitative and qualitative metrics to determine whether or not the quality plan is proceeding in an acceptable manner, mostly through intermittent quality audits

• Quality control - involves operational techniques meant to ensure quality standards. Control is reactionary and occurs after a problem has been identified, unlike quality assurance which occurs before a problem is identified. The monitoring of specific project outputs, compliance, risk factors/mitigation and overcoming unsatisfactory performance

• How will you manage quality?

Why is a quality plan important?

• Increasing pressure to effectively manage time and budget

• In the long term, quality aspects are an important indicator of project success

• Two aspects of project quality are:▫ satisfaction with project execution▫ satisfaction with the outcome

Investment appraisalFinancial viabilityNet savingsSocial return

Measuring success

1. What difference will the project make - what are the planned outcomes and outputs?

2. What criteria (key performance indicators, KPIs) will you use to measure successful achievement of your aims and objectives?

3. What have you benchmarked the project against?

4. How does your project align with corporate strategy/business plan?

5. What are the planned financial and/or social returns?

6. What are the forecast timings and cost?

• Think about the project outputs and outcomes (deliverables):

• Outputs are the products and services you deliver as part of your project i.e. Number of training courses, support sessions, jobs created and publications etc. They can be easily captured during the project, even if it’s a short project.

• Outcomes are the changes, benefits, learning or other impact that happens as a result of your project – what difference it has made

Non-financial factors for investment appraisal• Offering strategic benefits i.e. you might invest in extending your product range so that

you can supply more of the products that your key customers want which could help strengthen your brand and relationship with customers.

• Meeting the requirements of current and future legislation or industry standards and good practice

• Improving staff morale, making it easier to recruit and retain employees

• Improving relationships with suppliers and customers

• Improving your business reputation and relationships with the local community

• Developing the capabilities of your business, such as building skills and experience in new areas or strengthening management systems

• Anticipating and dealing with future threats, such as protecting intellectual property against potential competition

Gross profit margin and payback period (all levels)

Financial viability and benefit – simple techniques• Accounting Rate of return - the average annual profit expected over the life of an

investment project, compared with the average amount of capital invested i.e. a project requires an average investment of £100k and is expected to produce an average annual profit of £15k. The ARR would be 15% - companies have their set IRRs and each project IRR depends on the timing of cash in/outflows.

• Pay back period – for assessing an investment by the length of time it takes to repay i.e. an investment of £100k expects an annual cash-flow of £25k = payback period 4 years

• Break-even analysis – how many sales to break even from the costs that you have spent. Once you've reached that point, you've recovered all costs associated with producing your product (both variable and fixed) i.e. Break even point = fixed costs/(unit selling price - variable costs) i.e. after spending £10k on all salaries and materials and you are selling items at £1k each, you will need to sell x10 and make sales of £10k

• Gross profit margin – measures company efficiency i.e. Gross Profit/turnover x100 i.e. sales are £10k and costs are £5k, gross profit is £5k and gross profit margin is 50%

Formulas …

• Payback PeriodCost of Project/Annual Cash Inflows (income)

• Break even analysis (point)

• It costs £50 to produce a widget• There are fixed costs of £1,000

▫ The break-even point for selling the widgets would be:

▫ Selling @ £100:▫ x20 widgets (1000/(100-50)=20)

▫ Selling @ £200:▫ x7 widgets (1000/(200-50)=6.7)

Selling for a higher price results in quicker break-even point. But, it may be easier to sell 20 widgets at £100 than 7 widgets at £200

Financial viability – investment appraisal (L5+)

Is it viable?How much is needed?What is the return on investment (tangible and intangible)?What are the options?What are the key measurables?

Considerations

• Size and risk of project

• Ease of use/degree of simplicity required

• Degree of accuracy required

• Extent to which future cash flows need to be measured accurately

Financial appraisal methods in practice1. Accounting rate of return2. Payback period3. Net present value4. Internal rate of return

• All four methods are widely used• The discounting methods (NPV and IRR) show a steady increase in usage over

time• Many businesses use more than one method• Larger businesses seem to be more sophisticated in their choice and use of

appraisal methods than smaller ones

Payback period (PP)

• The length of time that it takes for cash outflow for the initial investment to be repaid out of resulting cash inflows

• The shorter the payback period, the more attractive the project• Easy to understand and provides an insight into liquidity, has widespread use• Does not take into consideration future cash inflows after the payback period• Basic in terms of analysis

Linder, S (2005). Fifty years of research on accuracy of capital expenditure project estimates: a review of findings and their validity. Otto Beisham Graduate School of Management

Net present value (NPV)• The sum of the discounted values of the net cash flows from the investment

• Uses the concept that money has a time value - assumes £1 now is more valuable than £1 in the future

• Positive NPV investments enhance shareholders’ wealth – the greater the NPV, the more attractive the project

• Takes account of the timing of cash flows• Takes all relevant information into account• Provides clear signals and is practical to use• Discount rate (DCF) might be applied by the company to reflect the cost of borrowing• Example: A bank rate might be 4%, but few capital investment projects are risk free, so a risk

premium might be applied by the company to provide a discount rate of say 10%• If the DCF were positive, it could be assessed against other projects to decide which one to

invest in

Linder, S (2005). Fifty years of research on accuracy of capital expenditure project estimates: a review of findings and their validity. Otto Beisham Graduate School of Management

Net present value (NPV)

• If I asked you to give me £100 now and I told you that I would give you back £100 in one year, would you do it? There is no clear advantage to you and you might be better keeping the £100 and investing it in a bank account where you might get some interest.

• What if I said that if you gave me the £100 now I will give you £110 in a year? It would depend on how much money you could earn yourself by investing the £100 compared to the £110 I will give you as you might be able to earn more than £10.

• Think about getting approvals for your project ...... If the project investment of £100k which would provide cost savings in year one of £50k and savings of £70k in year 2 is this worthwhile for the business? Considerations here would be on how well the business could use this £100k elsewhere on other projects.

http://www.clearlytraining.co.uk/whats-npv-net-present-value-dcf-discounted-cash-flow-all-about/

Internal rate of return (IRR)

• The discount rate that, when applied to the cash flows of a project, causes it to have a zero NPV

• Represents the average %return on the investment, taking account of the fact that cash may be flowing in and out of the project at various points in its life

• Projects that have a greater IRR than the cost of capital are acceptable, the greater the IRR, the more attractive the project

• Can be seen as inferior to NPV, especially when there are competing projects of different size

Linder, S (2005). Fifty years of research on accuracy of capital expenditure project estimates: a review of findings and their validity. Otto Beisham Graduate School of Management

Sensitivity analysis (SA) – dealing with risk

•Takes each input factor into consideration•It assess how much each one can vary from estimate

before the project is not viable

Next session

• Staff development day – no class

• Week after:

• Project evaluation techniques and introduction to risk management

• Level 3’s last class

![Lovejoy Gear[1]](https://img.pdfslide.us/doc/110x75/55122cc74a7959f1028b486b/lovejoy-gear1.jpg)