Embed Size (px)

Citation preview

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 1/72

A

REPO

RT

O

N

IMPACT OF 6 % RATE OF INTEREST ON SAVING

ACCOUNTS

BY

KAPIL SHARMA

(11BSP0437)

1 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 2/72

KOTAK MAHINDRA BANK LTD

AREPORT

ON

IMPACT OF 6 % RATE OF INTEREST ON SAVING

ACCOUNTS

BY

KAPIL SHARMA

(11BSP0437)

A report submitted in partial fulfillment of the

requirements of PGPM program of IBS GURGAON :

Batch -2011-13

KOTAK MAHINDRA BANK LTD

Faculty Guide:

Company Guide:

2 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 3/72

Prof. Anupama Rao Mr.Bhupesh Bhardwaj

(Faculty Guide)(Company Guide)

.

Date of Submission: 11 June 2012

AUTHORIZATION

This is to certify that the project entitled “Impact Of 6 % Rate

of Interest on Saving Accounts” captured in entirety in the

following pages is submitted in partial fulfillment of the

requirement of PGPM Program of ‘IBS Gurgaon’ and is a record

of the bonafide work carried out by Kapil Sharma of IBS,

Gurgaon at Kotak Mahindra Bank LTD, Dwarka, New

Delhi under my supervision and has not been submitted

anywhere else for any other purpose.

The information given herein is after the due consent of the

officials working for “KOTAK MAHINDRA BANK LTD.” and is

not available for the usage of any third party whatsoever.

3 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 4/72

Prof. Anupama Rao Mr.

Bhupesh Bhardwaj

(Faculty, IBS Gurgaon)

(Branch Manager)

ACKNOWLEDGEMENT

This summer internship project has been a colossal opportunity for

learning and self-development coupled with in depth knowledge extractionprocess from the very ground amidst an environment of “real time “ Retail

banking. . It has been a very special project, brought to fruition through

the efforts of some very special people whom I thank from the bottom of

my heart.

At the outset i am deeply grateful to the entire management of “IBS-

Gurgaon” for giving me an opportunity to learn the practical aspects and

nuances of retail banking through real life experience. .

4 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 5/72

It would have been quite impossible without the immense help and

conducive environment offered at KOTAK MAHINDRA BANK LTD.

The project I had undertaken required a lot of information gathering and

guidance which had been provided by various people at various stages of the project. I would like to express my deep sense of gratitude to the

following :

• To Prof. Anupama Rao, Faculty Guide for not only being a guide

but also a mentor and her tireless support and guidance in the

course of my project and its completion.

• To Mr. Bhupesh Bhardwaj, Branch Manager. for giving me an

opportunity to work on this project in their organization. He took

additional efforts to bring my report to its fulfillment and

completion. His continuous encouragement through collaborative

freedom immensely helped me in understanding the concepts

practically , and to try out new things perennially during this

internship program.

•

To Mr. Shakti Singh and Mr. Mohit , Company Guide, forkeeping the continuous track of my work and performance and

guiding me on my project and teaching me many new things.

• To all my fellow colleagues and seniors too, for being an immense

help to me in this project.

Kapil Sharma

11BSP0437

IBS, Gurgaon

5 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 6/72

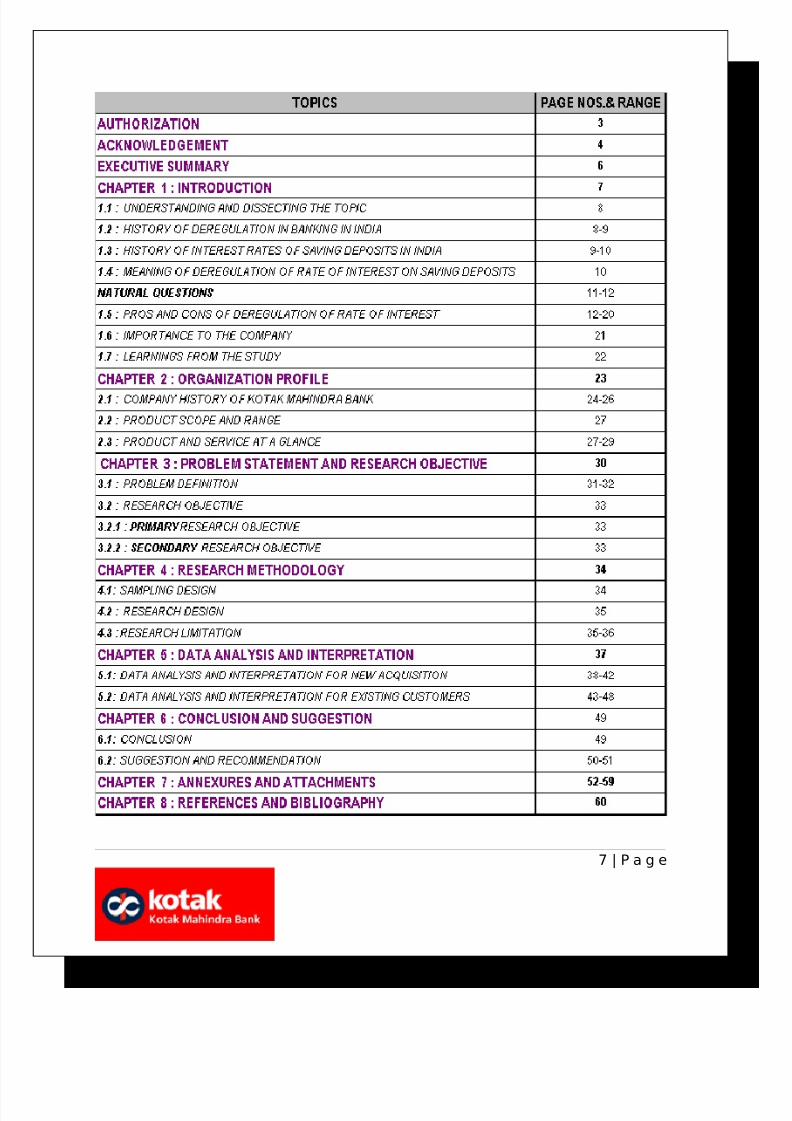

TABLE OF CONTENTS

6 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 7/72

7 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 8/72

EXECUTIVE SUMMARY

Raising Interest rates post deregulation unleashes the opportunity of Customer

acquisition as well as increasing portfolios in existing customers. With this ittriggers a price sensitive war within the already matured Urban Retail banking

space on the opportunity of increasing market share.

With it it also brings the question on profitability in CASA spreads and interest

income because merely acquiring customers through an interest war will have an

adverse and may impact on Cost of Funds as well as shrink the wallet size of

responding banks like Kotak Mahindra on controlling asset pricing and further

generating interest income through differential of asset liability spreads.

The following pages will traverse through a path of in depth analysis and learning

derived by customer interface in the target segment . The structure and the finalculmination will take route plans on customer awareness on the Savings account

interest rate upward changes post Deregulation at Kotak Mahindra bank, the

market responsiveness to this change both in terms of New Customer acquisition

and balance buildup in existing Savings account portfolio base. It will throw

adequate light on willingness to change purely basis “ an upward movement of

interest “ vis-à-vis host of other products, facilities, branding and so on..

It will allow the organization to take valid inputs from the derived market study to

Reframe strategies at a branch level/ market level in future to increment the

ultimate goal of Kotak Mahindra bank in increasing both market share on the

Savings account portfolio

8 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 9/72

Chapter : 1

INTRODUCTION

9 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 10/72

1.1 Understanding & Dissecting the

Topic “Impact of 6% Rate of Intereston Savings Accounts”

With the Reserve Bank Deregulation of interest rate on savings deposits, the

mid-size private lender Kotak Mahindra Bank was amongst the First to

announce that it will be offering 6 percent interest on savings deposits above Rs.

1 lakh and 5.5 percent those below Rs. 1 lakh effective from 1 Nov 2011. Kotak

Mahindra Bank had been operating as a primal force in Pvt Sector retail banks

with 31% CASA Ratios as the RBI announced de-regulation of Savings Bank

account interest rate.

As analysts had mixed responses to this announcement there was no questions

on a complete win –win situation as a choice of a consumer could be. One could

clearly visualize two distinct paths emerging. The increased interest rate being

used as a “ hook ‘ strategy by some banks like Kotak Mahindra and “ Yes “

through various marketing methods to increase and widen customer base and

CASA ratios as well as deepening wallet sizes by giving the right customer only

the right rates of interest.

There was also another school of thought which questioned the impact on

positive acquisition and wallet size deepening through increasing cost of Fundsby higher payouts ( Especially as a couple of months earlier the daily interest

calculation ) proposed by RBI had already seen income crunching in banks. With

the difference of interest spreads in assets and liabilities becoming slimmer the

banks were wondering whether to take a plunge of interest increment as a

proposition to woo customers at the time when Demand of assets especially

Corporate lending was declining.

1.2 History of Deregulation in Banking In india

The process of deregulation, which began in the early 1990s, was largelycompleted by 1997. A few categories of interest rates that continued to beregulated were small loans up to ` 2 lakh and rupee export credit on the lendingside, and savings deposit interest rate on the deposit side. The small loans up to` 2 lakh and rupee export credit were deregulated in July 2010 when the Reserve

10 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 11/72

Bank replaced the benchmark prime lending rate (BPLR) system with the BaseRate system. The only interest rate that continues to be regulated now is thesavings deposit interest rate. Deregulation of interest rates in India since theearly 1990s has improved the competitive environment in the financial system,imparted greater efficiency in resource allocation and strengthened thetransmission mechanism of monetary policy.

Savings deposit interest rate had not been deregulated for the reason that alarge portion of such deposits is held by low income households in rural andsemi-urban areas. It is more than 13 years when the deposit interest rates, otherthan savings deposits, were deregulated. The issue, therefore, is how relevantare these concerns in today’s context and what will be the implications if savingsdeposit interest rate is deregulated.

Regulation of savings deposit interest rate had imparted rigidity as savingsdeposit interest rate has not been changed since March 1, 2003 although otherinterest rates have moved in either direction. Interest rate paid on savingsdeposits was lower than those on term deposits of all maturities, other than forterm deposits at very short end for a brief period. Thus, it was the saver whohas been affected adversely because rate of return on savings deposithas generally been negative and unattractive vis-à-vis short termdeposits.

The empirical evidence suggests that unlike metropolitan areas, savings depositsin rural, semi-urban and urban areas are responsive to interest rate changes insavings deposits. Therefore, market-based interest rate may be beneficial tosavers. Since savings deposit is a hybrid product which combines the features of both current account and term deposit, a market based rate of interest on thisproduct has the potential to attract large savings from low income households.

Deregulation will also allow banks to introduce product innovations which couldalso benefit the depositors. Deregulation will have another major advantage inthat it will help improve the monetary transmission. Since savings depositsconstitute a significant portion of aggregate deposits, regulation of interest rateon such deposits has impeded the transmission of monetary policy impulses.

1.3 History of Interest Rates of Savings deposits in

India

One of the important functions of the Bank is to accept deposits from the public

for the purpose of lending. In fact, depositors are the major stakeholders of the

Banking System. The depositors and their interests form the key area of theregulatory framework for banking in India and this has been enshrined in the

Banking Regulation Act, 1949. The Reserve Bank of India is empowered to issue

11 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 12/72

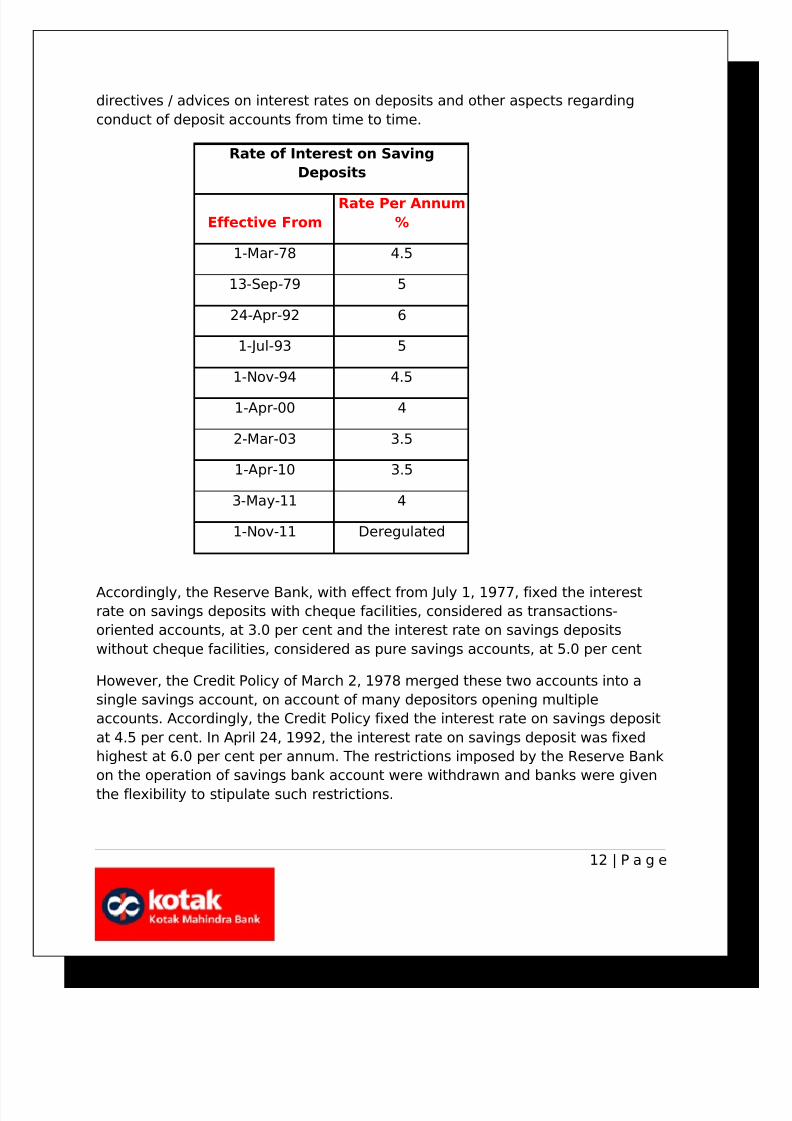

directives / advices on interest rates on deposits and other aspects regarding

conduct of deposit accounts from time to time.

Rate of Interest on Saving

Deposits

Effective From

Rate Per Annum

%

1-Mar-78 4.5

13-Sep-79 5

24-Apr-92 6

1-Jul-93 5

1-Nov-94 4.5

1-Apr-00 4

2-Mar-03 3.5

1-Apr-10 3.5

3-May-11 4

1-Nov-11 Deregulated

Accordingly, the Reserve Bank, with effect from July 1, 1977, fixed the interestrate on savings deposits with cheque facilities, considered as transactions-

oriented accounts, at 3.0 per cent and the interest rate on savings deposits

without cheque facilities, considered as pure savings accounts, at 5.0 per cent

However, the Credit Policy of March 2, 1978 merged these two accounts into a

single savings account, on account of many depositors opening multiple

accounts. Accordingly, the Credit Policy fixed the interest rate on savings deposit

at 4.5 per cent. In April 24, 1992, the interest rate on savings deposit was fixed

highest at 6.0 per cent per annum. The restrictions imposed by the Reserve Bank

on the operation of savings bank account were withdrawn and banks were given

the flexibility to stipulate such restrictions.

12 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 13/72

The SB interest rate was decreased in March 2003, from 4% to 3.5%, when

inflation was around 3%. In April 2010, after RBI changed the method of

calculating interest on SB accounts the depositors saw an increase in their

returns on savings and finally RBI decided to completely deregulate the rate of

interest effective from 25 oct 2011.

1.4 MEANING OF DEREGULATION OF RATE OF

INTEREST ON SAVING DEPOSITS

Deregulation of interest rates on deposits was announced by the Reserve Bank

Of India (RBI) on Oct 25th 2011, Before the announcement was made, all banks

in India used to payout the same interest rate on your savings account. That was

4% and was fixed by RBI.

This regulation now meant that RBI allowed banks, effective November1st - 2011, to fix their own interest rates on deposits or savings

account.

OR

That there is no restriction on fixing the rate of interest on the savings

account, the banks would be able to freely decide the interest rates

that suit them and their customers.

Details of the RBI Order followed some guidelines.

There would be 2 categories of deposits: Less than Rs. 1 Lakh and Rs. 1

Lakhs and above

The banks would have to offer a single rate of interest to all deposits below Rs. 1

Lakhs – the banks would decide this rate (say, 5% per year), but it would need to

be the same for ALL deposits lower than Rs. 1 Lakh.

For the deposits in the other category (Rs. 1 Lakh and above), it becomes

interesting. The banks would be able to come up with various slabs based on the

deposit amount, ad can offer a different interest rate for each slab.

13 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 14/72

Some natural questions which comes to mind

EFFECT OF SAVING A/C DEREGULATION

Was this going to be a gloomy, but hectic Diwali for most banks. The

sucker punch is not the 13th policy rate hike. For the past 20 months, therate hike has become rather like an occupational hazard for most Indianbankers. The deregulation of interest rate on savings accounts, however,is like a bolt, though perhaps not entirely out of the blue.

PROGRESSIVE STEP, BUT ARE BANKS AS COLLATERAL DAMAGE

Reform measures aimed at increasing the role of market forces ineconomic decision-making are generally beneficial. However, some of thestakeholders often lose out. Hence, while deregulation would beremembered as a landmark reform, listed banks may be adversely

affected.

FALLOUTS ON BANK EARNINGS, ASSET-LIABILITY ANDVALUATIONS

The step can have three major implications for banks — reduce averageearnings growth, enhance asset-liability mismatch (ALM) and increaseearnings volatility, thereby reducing the valuation multiples. Theanticipation of sovereign debt restructuring /default in the euro area isalready inflicting collateral damages on bank stocks globally. On thedomestic front, concerns are rising about accelerated growth in NPAs of

banks. The timing of the policy change, therefore, could not perhaps bemuch worse for most banks.

RISE IN COST

Savings deposits account for about 22% of the overall liabilities and 25%of overall deposits in the banking system. While the blended cost of fundsis currently around 6%, savings deposits till date command 4% interestrate. Therefore, if due to deregulation, the cost of funds on savingsaccount rises close to the system average, it would mean nearly a 55 bpsrise in the overall cost of funds. Such an increase is likely to happenbecause competition among banks may raise the interest rate until thecost of savings deposits reaches the system average.

14 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 15/72

FALL IN EARNINGS, RETURN RATIOS

This would reduce the interest spread by 55bps, or 25%, and return onassets (RoA) and return on equity (RoE) by 32bps and 450bps,respectively, ceteris paribus. This, however, is the worst-case impact on

bank earnings, as we are assuming no change in income. Moreover, theextent or even the direction of impact on individual banks would dependon the initial proportion of savings accounts in overall liabilities and theproactive nature with which the bank acts.

ALM TO WIDEN

Over time, the average maturity of bank deposits is reducing. With the

sharp rise in the share of infrastructure in bank credit, the average

maturity of bank liabilities is on the rise. While banking is the business of

maturity transformation, large asset-liability mismatches can destabilise

the system. With increase in savings account rates, the difference

between interest rate on fixed and savings deposits would reduce. Given

the greater liquidity of the latter, the share of savings may rise at the cost

of FDs. This is likely to further the asset-liability mismatch.

1.5 Pros & Cons of Deregulation of rate of interest

Pros

May Lead to Enhance Attractiveness of Savings Deposits

Regulation of interest rates imparts rigidity of instrument/product and as interest

rates are not changed in response to changing market conditions the product

loses it sheen.This has primarily affected the saving bank deposits.So

deregulating the interest rates would help in enhancing the attractiveness of this

product.

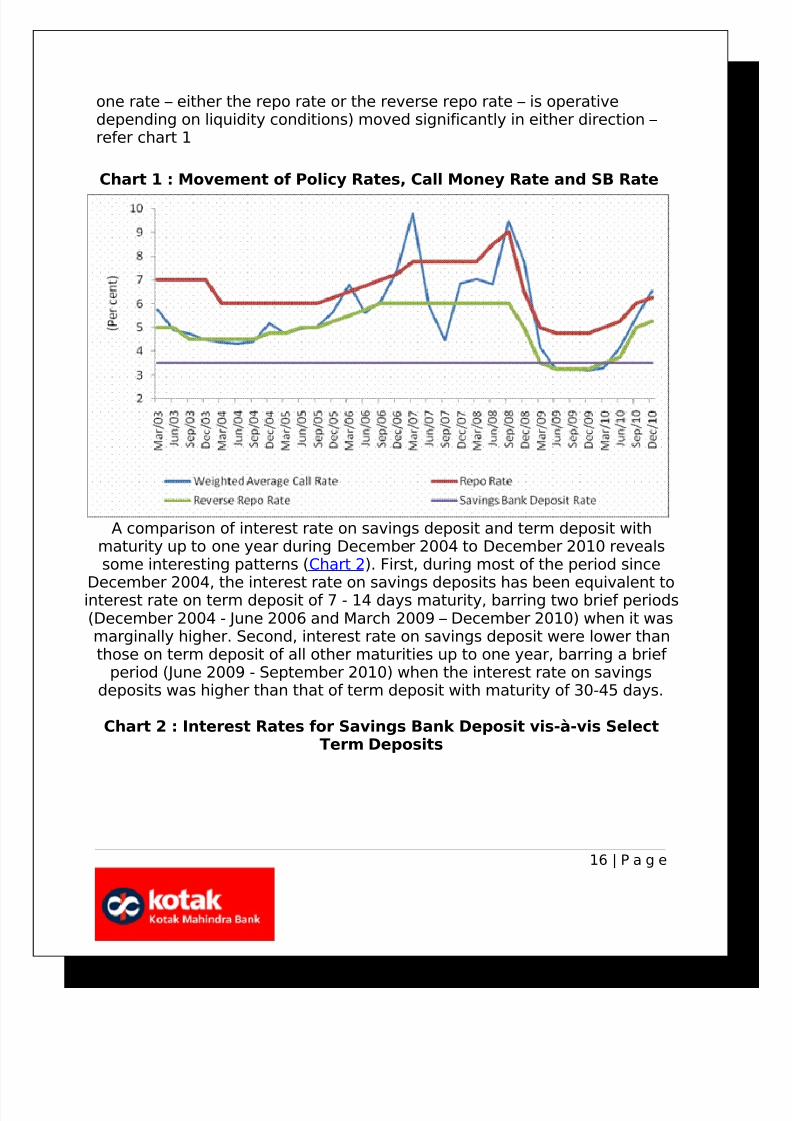

Savings bank deposits, its interest rate has remained unchanged at 3.5per cent since March 1, 2003 even as the Reserve Bank’s policy rates andcall rates (representing a proxy for operative policy rate as at a time, only

15 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 16/72

one rate – either the repo rate or the reverse repo rate – is operativedepending on liquidity conditions) moved significantly in either direction –refer chart 1

Chart 1 : Movement of Policy Rates, Call Money Rate and SB Rate

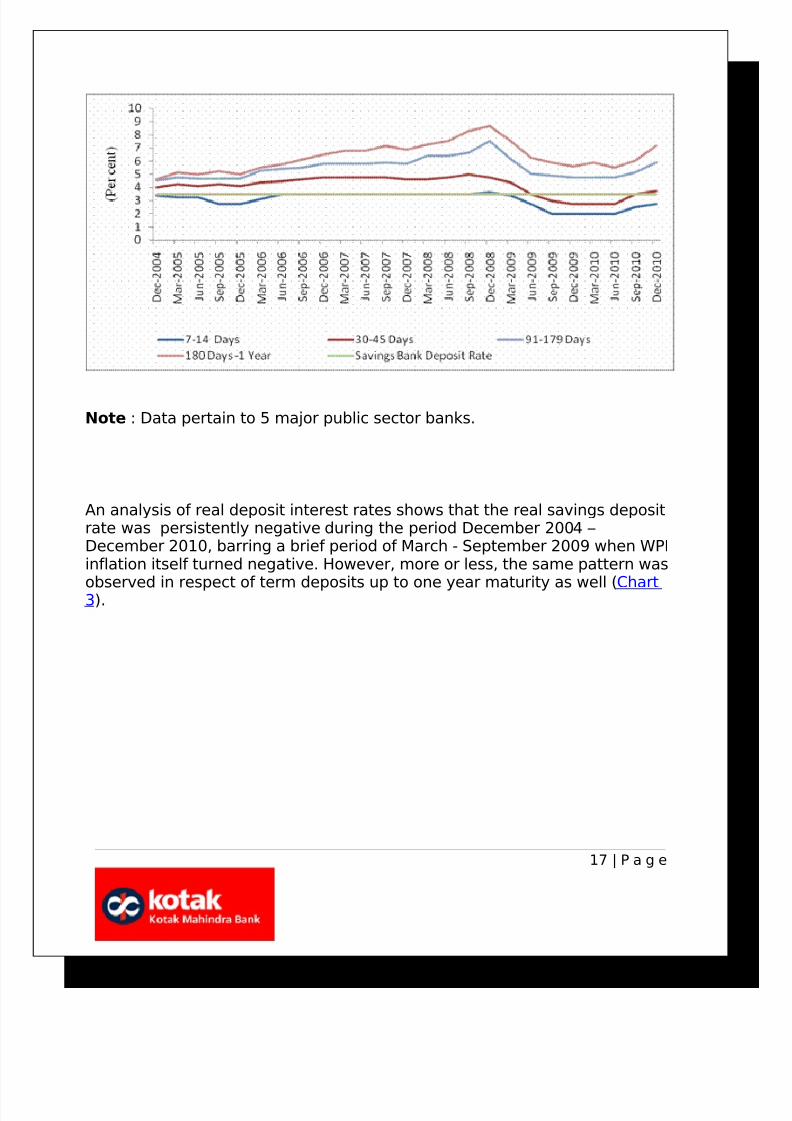

A comparison of interest rate on savings deposit and term deposit withmaturity up to one year during December 2004 to December 2010 revealssome interesting patterns (Chart 2). First, during most of the period since

December 2004, the interest rate on savings deposits has been equivalent tointerest rate on term deposit of 7 - 14 days maturity, barring two brief periods(December 2004 - June 2006 and March 2009 – December 2010) when it wasmarginally higher. Second, interest rate on savings deposit were lower thanthose on term deposit of all other maturities up to one year, barring a brief

period (June 2009 - September 2010) when the interest rate on savingsdeposits was higher than that of term deposit with maturity of 30-45 days.

Chart 2 : Interest Rates for Savings Bank Deposit vis-à-vis SelectTerm Deposits

16 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 17/72

Note : Data pertain to 5 major public sector banks.

An analysis of real deposit interest rates shows that the real savings depositrate was persistently negative during the period December 2004 –December 2010, barring a brief period of March - September 2009 when WPIinflation itself turned negative. However, more or less, the same pattern was

observed in respect of term deposits up to one year maturity as well (Chart3).

17 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 18/72

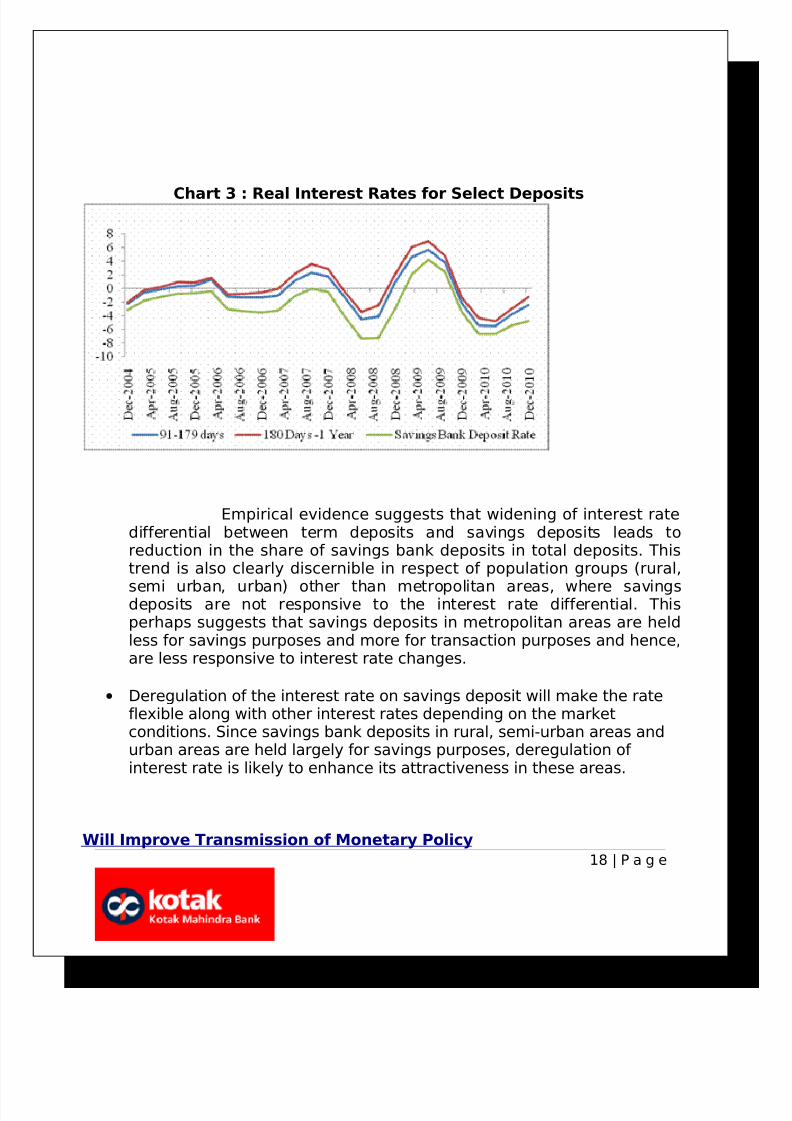

Chart 3 : Real Interest Rates for Select Deposits

Empirical evidence suggests that widening of interest ratedifferential between term deposits and savings deposits leads toreduction in the share of savings bank deposits in total deposits. Thistrend is also clearly discernible in respect of population groups (rural,

semi urban, urban) other than metropolitan areas, where savingsdeposits are not responsive to the interest rate differential. Thisperhaps suggests that savings deposits in metropolitan areas are heldless for savings purposes and more for transaction purposes and hence,are less responsive to interest rate changes.

• Deregulation of the interest rate on savings deposit will make the rateflexible along with other interest rates depending on the marketconditions. Since savings bank deposits in rural, semi-urban areas andurban areas are held largely for savings purposes, deregulation of interest rate is likely to enhance its attractiveness in these areas.

Will Improve Transmission of Monetary Policy18 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 19/72

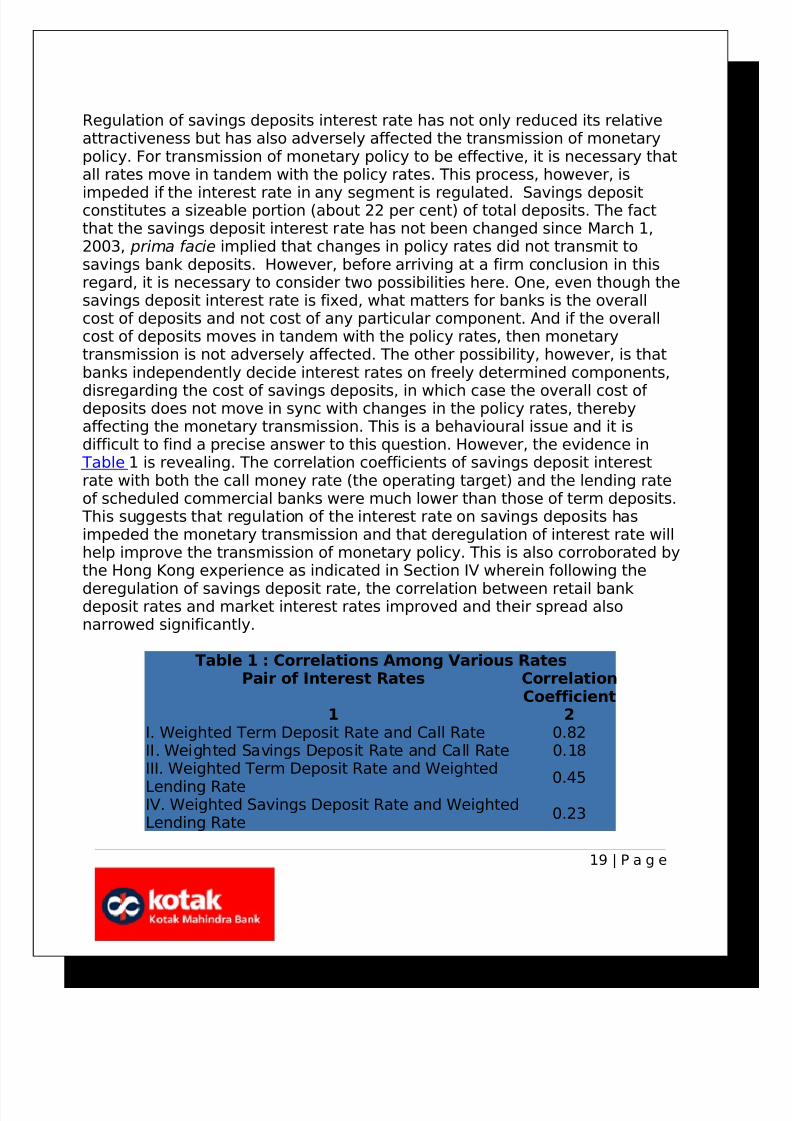

Regulation of savings deposits interest rate has not only reduced its relativeattractiveness but has also adversely affected the transmission of monetarypolicy. For transmission of monetary policy to be effective, it is necessary thatall rates move in tandem with the policy rates. This process, however, is

impeded if the interest rate in any segment is regulated. Savings depositconstitutes a sizeable portion (about 22 per cent) of total deposits. The factthat the savings deposit interest rate has not been changed since March 1,2003, prima facie implied that changes in policy rates did not transmit tosavings bank deposits. However, before arriving at a firm conclusion in thisregard, it is necessary to consider two possibilities here. One, even though thesavings deposit interest rate is fixed, what matters for banks is the overallcost of deposits and not cost of any particular component. And if the overallcost of deposits moves in tandem with the policy rates, then monetarytransmission is not adversely affected. The other possibility, however, is thatbanks independently decide interest rates on freely determined components,

disregarding the cost of savings deposits, in which case the overall cost of deposits does not move in sync with changes in the policy rates, therebyaffecting the monetary transmission. This is a behavioural issue and it isdifficult to find a precise answer to this question. However, the evidence in Table 1 is revealing. The correlation coefficients of savings deposit interestrate with both the call money rate (the operating target) and the lending rateof scheduled commercial banks were much lower than those of term deposits. This suggests that regulation of the interest rate on savings deposits hasimpeded the monetary transmission and that deregulation of interest rate willhelp improve the transmission of monetary policy. This is also corroborated bythe Hong Kong experience as indicated in Section IV wherein following the

deregulation of savings deposit rate, the correlation between retail bankdeposit rates and market interest rates improved and their spread alsonarrowed significantly.

Table 1 : Correlations Among Various RatesPair of Interest Rates Correlation

Coefficient1 2

I. Weighted Term Deposit Rate and Call Rate 0.82II. Weighted Savings Deposit Rate and Call Rate 0.18III. Weighted Term Deposit Rate and Weighted

Lending Rate 0.45IV. Weighted Savings Deposit Rate and WeightedLending Rate

0.23

19 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 20/72

May Lead to Product Innovations

Savings deposits constitute about 22 per cent of total deposits. However,owing to regulation of interest rate, there is hardly any competition in this

segment with both banks and depositors acting passively. This has inhibitedproduct innovations. The requirements of different banks and differentdepositors are not necessarily the same. Just as each bank may like to tailorthe savings product to suit its requirement, each depositor may like to choosea product which suits his requirements.

To create competition and encourage banks to introduce innovative products,it is, therefore, necessary to deregulate savings deposit interest rate. Productinnovations may include a variety of modes of operations such as branches,web-based channels, ATMs etc. Rates offered may also differ based on theflexibility of operation of savings bank account and the degree of liquidity

offered such as notice period for withdrawal, number of deposits and/orwithdrawals allowed per month and percentage of amount that can bewithdrawn in any given month, among others. It may be noted here that inresponse to the deregulation of savings deposit interest rate in Hong Kong in2001, a number of banks launched new products such as combined savingsand checking accounts and HIBOR linked savings products. Some also revisedfees and charges and minimum balance requirements, and introduced tieredstructures of interest rates.

Cons

Possibility of an Unhealthy Competition

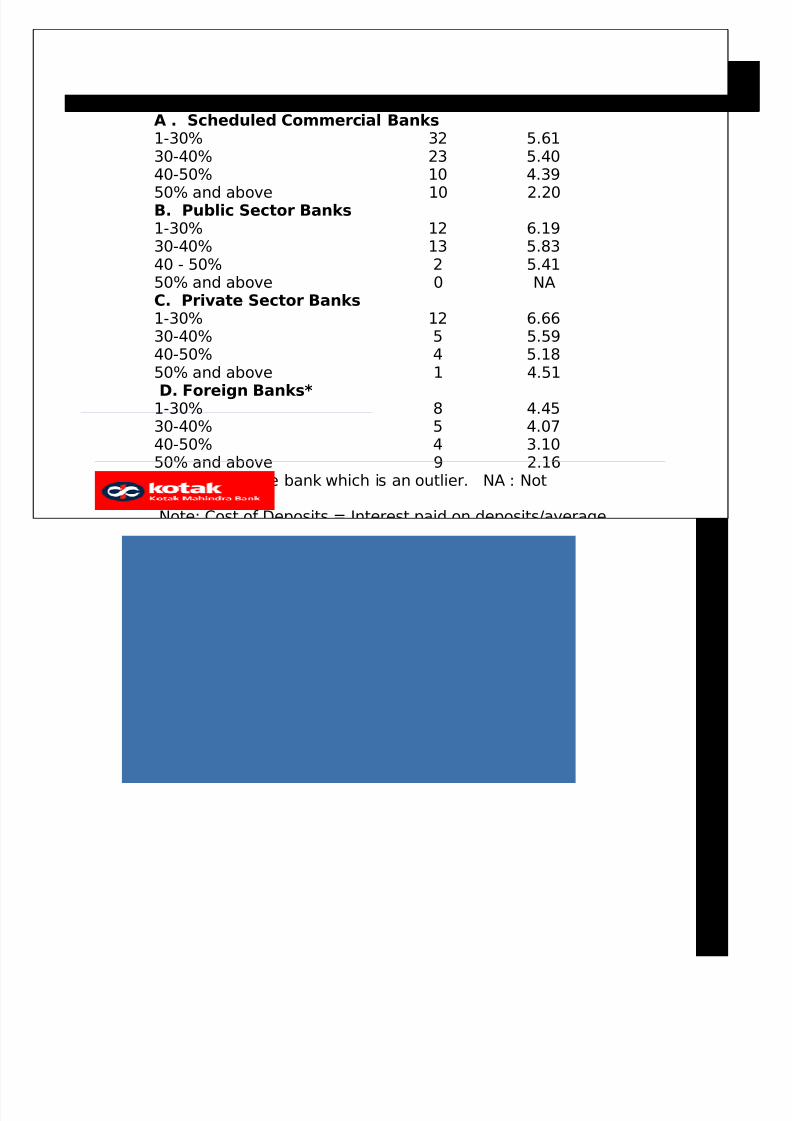

A major attraction of savings deposits for banks is that it offers a low costsource of funds. This is evident from the fact that bank groups with highershare of CASA (current account and savings account) deposits (of whichsavings deposit is a major component) enjoy relatively low cost of deposits. However, the distribution of CASA deposits among banks is notuniform ( Table 2).

Table 2 : Frequency Distribution of CASA Depositsamong Bank Groups - March 2010

(Per cent)Share of CASA No. of

BanksAverage Costof Deposits

20 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 21/72

1 2 3A . Scheduled Commercial Banks 1-30% 32 5.6130-40% 23 5.4040-50% 10 4.39

50% and above 10 2.20B. Public Sector Banks1-30% 12 6.1930-40% 13 5.8340 - 50% 2 5.4150% and above 0 NAC. Private Sector Banks1-30% 12 6.6630-40% 5 5.5940-50% 4 5.1850% and above 1 4.51

D. Foreign Banks*1-30% 8 4.4530-40% 5 4.0740-50% 4 3.1050% and above 9 2.16*: Excluding one bank which is an outlier. NA : Notapplicable.Note: Cost of Deposits = Interest paid on deposits/averageof current and previous year’s deposits.Source: Reserve Bank of India.

It has also been observed that 49 banks, which have below average CASAdeposits, constitute about 50 per cent of total asset of the banking sector. Therefore, given the attractiveness of savings deposits, it could be arguedthat deregulation may lead to unhealthy competition amongst banks. Shouldit really happen, it will have implications in that it will push up the cost of funds of the banking sector. This, if passed on to the borrower, will raise thecost of borrowings and if not, it will affect the interest margins andprofitability of the banking sector.

Risk of Asset Liability Mismatches

One of the issues often raised by banks in the context of deregulation of savings bank interest rate is that in the event of such deregulation, it wouldresult in an asset-liability mismatch. This is because, although savings bank

21 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 22/72

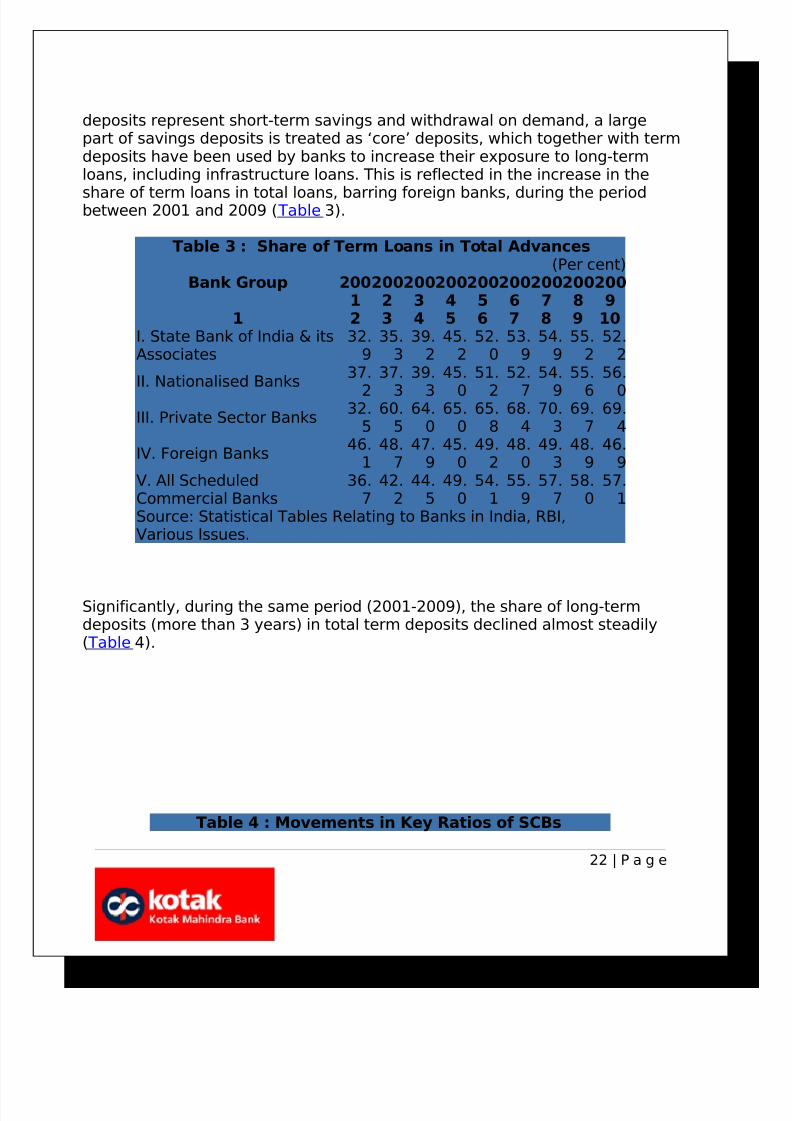

deposits represent short-term savings and withdrawal on demand, a largepart of savings deposits is treated as ‘core’ deposits, which together with termdeposits have been used by banks to increase their exposure to long-termloans, including infrastructure loans. This is reflected in the increase in the

share of term loans in total loans, barring foreign banks, during the periodbetween 2001 and 2009 ( Table 3).

Table 3 : Share of Term Loans in Total Advances(Per cent)

Bank Group 2001

2002

2003

2004

2005

2006

2007

2008

2009

1 2 3 4 5 6 7 8 9 10I. State Bank of India & itsAssociates

32.9

35.3

39.2

45.2

52.0

53.9

54.9

55.2

52.2

II. Nationalised Banks37.

2

37.

3

39.

3

45.

0

51.

2

52.

7

54.

9

55.

6

56.

0III. Private Sector Banks

32.5

60.5

64.0

65.0

65.8

68.4

70.3

69.7

69.4

IV. Foreign Banks46.

148.

747.

945.

049.

248.

049.

348.

946.

9V. All ScheduledCommercial Banks

36.7

42.2

44.5

49.0

54.1

55.9

57.7

58.0

57.1

Source: Statistical Tables Relating to Banks in India, RBI,Various Issues.

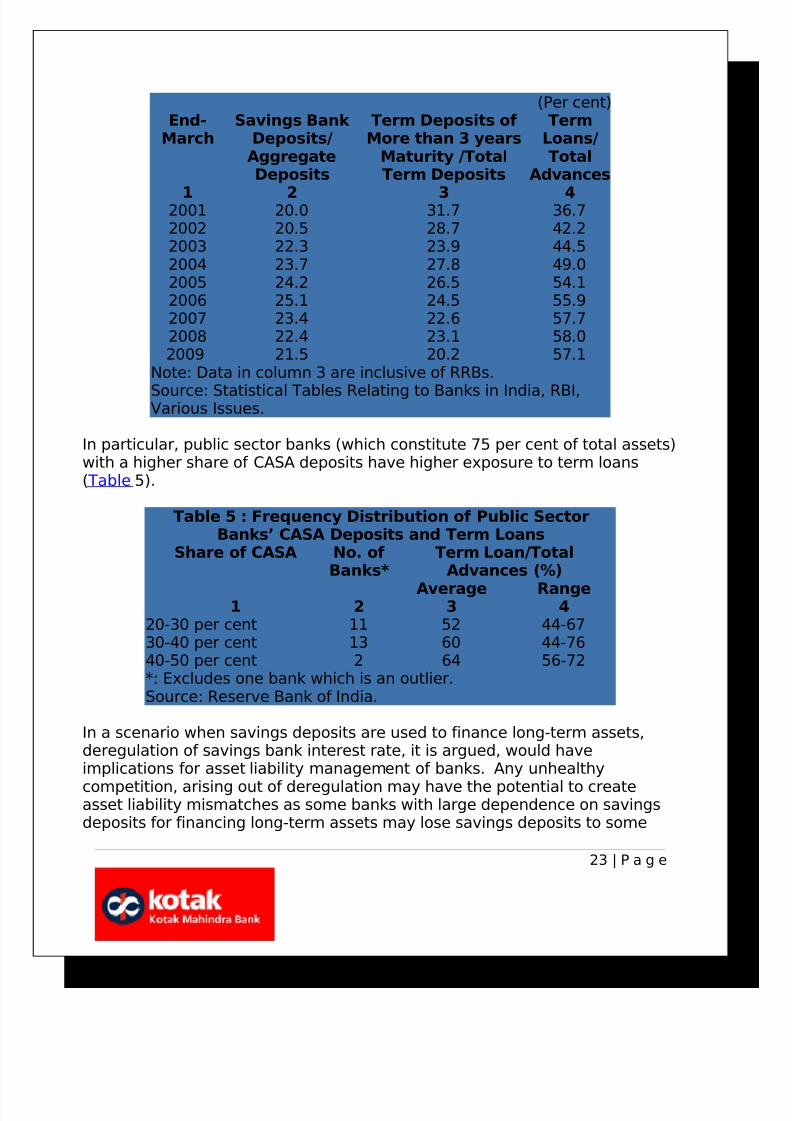

Significantly, during the same period (2001-2009), the share of long-termdeposits (more than 3 years) in total term deposits declined almost steadily( Table 4).

Table 4 : Movements in Key Ratios of SCBs

22 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 23/72

(Per cent)End-

MarchSavings Bank

Deposits/AggregateDeposits

Term Deposits of More than 3 years

Maturity /TotalTerm Deposits

TermLoans/Total

Advances

1 2 3 42001 20.0 31.7 36.72002 20.5 28.7 42.22003 22.3 23.9 44.52004 23.7 27.8 49.02005 24.2 26.5 54.12006 25.1 24.5 55.92007 23.4 22.6 57.72008 22.4 23.1 58.02009 21.5 20.2 57.1

Note: Data in column 3 are inclusive of RRBs.

Source: Statistical Tables Relating to Banks in India, RBI,Various Issues.

In particular, public sector banks (which constitute 75 per cent of total assets)with a higher share of CASA deposits have higher exposure to term loans( Table 5).

Table 5 : Frequency Distribution of Public SectorBanks’ CASA Deposits and Term Loans

Share of CASA No. of Banks*

Term Loan/TotalAdvances (%)

Average Range1 2 3 4

20-30 per cent 11 52 44-6730-40 per cent 13 60 44-7640-50 per cent 2 64 56-72*: Excludes one bank which is an outlier.Source: Reserve Bank of India.

In a scenario when savings deposits are used to finance long-term assets,deregulation of savings bank interest rate, it is argued, would haveimplications for asset liability management of banks. Any unhealthy

competition, arising out of deregulation may have the potential to createasset liability mismatches as some banks with large dependence on savingsdeposits for financing long-term assets may lose savings deposits to some

23 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 24/72

other banks.

May Lead to Financial Exclusion

Should unhealthy competition result in increase in interest rate and theoverall cost of funds, banks might be discouraged from maintaining savingsdeposits with small amounts due to the associated high transaction costs. Thiscould particularly be the case with public sector banks, which have a largenumber of savings accounts and which allows depositors to maintain very lowbalances. Thus, it is likely that banks either increase the minimum balance tobe maintained or reduce the number of transactions permitted free of costand increase the customer service charges too. This will discourage smallsavers, especially in rural and semi- urban areas from opening savingsdeposits accounts. The campaign for “No Frills Accounts” could also suffer asetback. In sum, deregulation of savings bank deposit rate might have

adverse implications for the process of financial inclusion.

Could Adversely Affect Small Savers/Pensioners

Many senior citizens, pensioners, small savers, particularly in rural and semi-urban areas, depend on interest as a source of regular income. In the recentperiod, interest rate on savings deposits has been lower than that on termdeposits and deregulation may push up savings deposits higher, in which casesmall savers/pensioners would benefit. However, there could be occasions,especially when the liquidity is in surplus, when savings deposit interest ratesmay decline even below the present level. This will affect the income flow to

small savers/pensioners. However, considering the fact that such occasionshave been few and far between and on most recent occasions, savingsinterest rate was lower than short-term deposits, concerns about the impactof deregulation of savings deposits on pensioners/small deposits need not beover-emphasised.

Possibility of Introduction of Complex and not so Easily UnderstoodSavings Products

Although deregulation of savings deposit interest rate may lead to productinnovation, which, in general, will benefit savers, it is also possible that banks

introduce some complex products, which may not be so easily understood bysavers. These strategies may result in increase in the mis-selling of savingsbank products, which will also result in increase in the number of customer

24 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 25/72

complaints.

Primarily the deregulation is being pushed for by the smaller/newer banks as

compared to older/bigger banks. These small banks have small percentage of CASA

deposits and in the current scenario attracting Saving bank deposits is not easy. Thereason being since the savers don't find any difference to shift to newer banks, theywould still continue to their existing bank than shifting to a newer one. With this

deregulation they could innovate in this space and attract a higher percentage of Saving bank deposits.

Internationally many countries especially developed ones and those havinghigh inflation rates have deregulated interest rates and the experiences have been

fairly satisfactory

25 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 26/72

1.6 IMPORTANCE TO THE

COMPANY

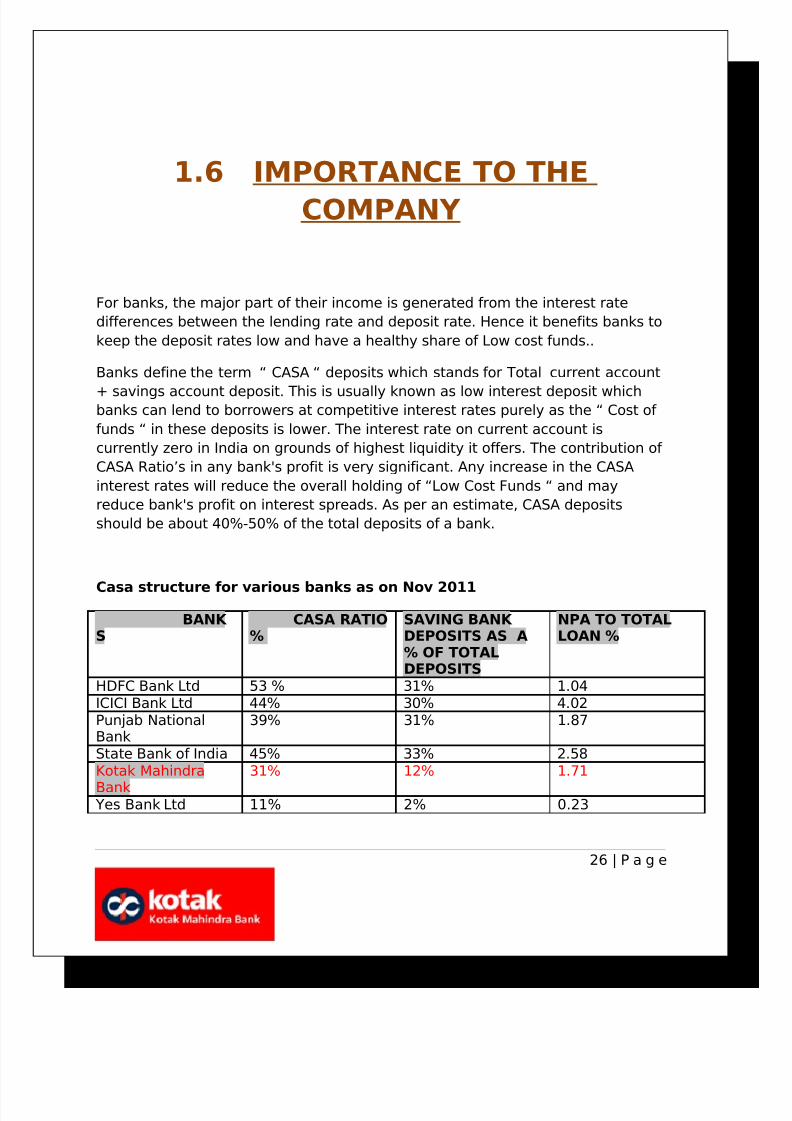

For banks, the major part of their income is generated from the interest rate

differences between the lending rate and deposit rate. Hence it benefits banks to

keep the deposit rates low and have a healthy share of Low cost funds..

Banks define the term “ CASA “ deposits which stands for Total current account

+ savings account deposit. This is usually known as low interest deposit whichbanks can lend to borrowers at competitive interest rates purely as the “ Cost of

funds “ in these deposits is lower. The interest rate on current account is

currently zero in India on grounds of highest liquidity it offers. The contribution of

CASA Ratio’s in any bank's profit is very significant. Any increase in the CASA

interest rates will reduce the overall holding of “Low Cost Funds “ and may

reduce bank's profit on interest spreads. As per an estimate, CASA deposits

should be about 40%-50% of the total deposits of a bank.

Casa structure for various banks as on Nov 2011

BANK S

CASA RATIO%

SAVING BANK DEPOSITS AS A% OF TOTALDEPOSITS

NPA TO TOTALLOAN %

HDFC Bank Ltd 53 % 31% 1.04ICICI Bank Ltd 44% 30% 4.02Punjab NationalBank

39% 31% 1.87

State Bank of India 45% 33% 2.58Kotak Mahindra

Bank

31% 12% 1.71

Yes Bank Ltd 11% 2% 0.23

26 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 27/72

Post Deregulation of interest rate on saving deposits ,it has been an opportunity

identification tool for Kotak Mahindra bank to increase its CASA share in total

deposits by offering higher Rate of interest on saving deposits than competition

there by also increasing market share by acquiring customers on Savings

portfolio of competition through this option.

1.7 LEARNING FROM THE

STUDY

• For Customers : Deregulation is a complete win –win

situation for customers across geographies , because to acquirethem internal competition within bank’s offers a higher income on

Liquid and transaction able surplus kept in Savings accounts. On the

comparison chart of decision making on which bank to choose for

keeping a savings bank account, Deregulation of interest rates

offers one more point of positive choice to the customer.

• For Bank’s : Deregulation of Interest rates which is a working

and acceptable scenario in the banking world internationally hasboth positive and negative impact to Bank’s. Commercial bank’s

earn profits primarily through interest spread incomes of Assets

27 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 28/72

against interest payouts on Deposits. Deregulation brings in

Competition which may have a negative impact on % share of Low

cost funds taking, may increase cost of Funds if competition hottens

and also may change Market share in the long –run if not adequately

supervised by making better value propositions to existing & new

customers

28 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 29/72

CHAPTER 2

ORGANIZATION PROFILE

2.1 COMPANY HISTORY-OF KOTAK

MAHINDRA BANK

Kotak Mahindra group has been one of India's most reputed financial

conglomerates. In February 2003, Kotak Mahindra Finance Ltd, the group's

flagship company was given the license to carry on banking business by the

29 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 30/72

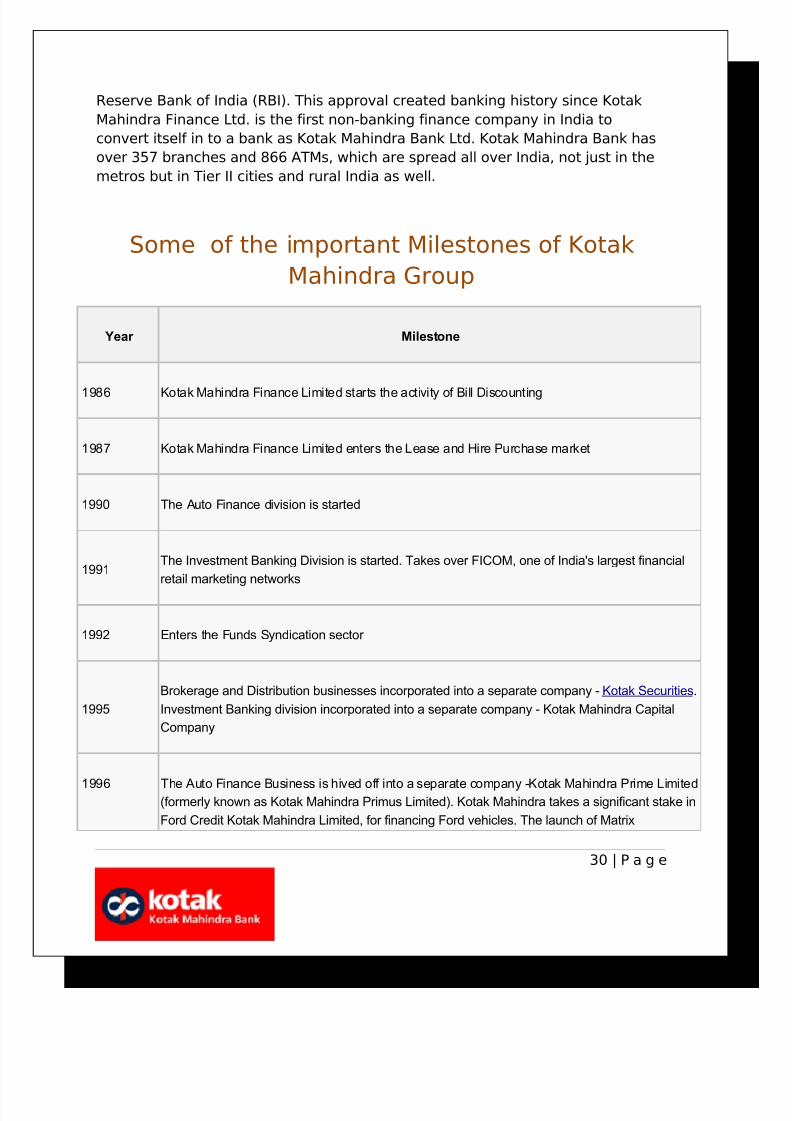

Reserve Bank of India (RBI). This approval created banking history since Kotak

Mahindra Finance Ltd. is the first non-banking finance company in India to

convert itself in to a bank as Kotak Mahindra Bank Ltd. Kotak Mahindra Bank has

over 357 branches and 866 ATMs, which are spread all over India, not just in the

metros but in Tier II cities and rural India as well.

Some of the important Milestones of Kotak

Mahindra Group

Year Milestone

1986 Kotak Mahindra Finance Limited starts the activity of Bill Discounting

1987 Kotak Mahindra Finance Limited enters the Lease and Hire Purchase market

1990 The Auto Finance division is started

1991The Investment Banking Division is started. Takes over FICOM, one of India's largest financial

retail marketing networks

1992 Enters the Funds Syndication sector

1995

Brokerage and Distribution businesses incorporated into a separate company - Kotak Securities.

Investment Banking division incorporated into a separate company - Kotak Mahindra Capital

Company

1996 The Auto Finance Business is hived off into a separate company -Kotak Mahindra Prime Limited(formerly known as Kotak Mahindra Primus Limited). Kotak Mahindra takes a significant stake in

Ford Credit Kotak Mahindra Limited, for financing Ford vehicles. The launch of Matrix

30 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 31/72

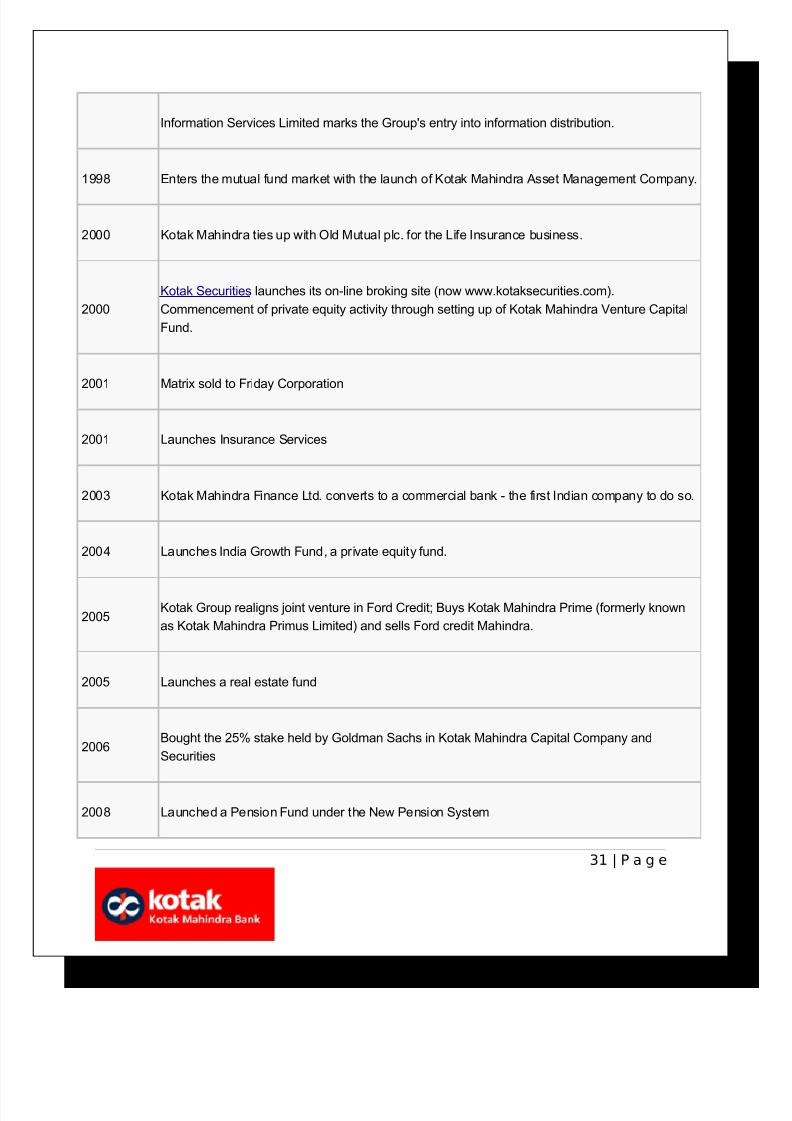

Information Services Limited marks the Group's entry into information distribution.

1998 Enters the mutual fund market with the launch of Kotak Mahindra Asset Management Company.

2000 Kotak Mahindra ties up with Old Mutual plc. for the Life Insurance business.

2000

Kotak Securities launches its on-line broking site (now www.kotaksecurities.com).

Commencement of private equity activity through setting up of Kotak Mahindra Venture Capital

Fund.

2001 Matrix sold to Friday Corporation

2001 Launches Insurance Services

2003 Kotak Mahindra Finance Ltd. converts to a commercial bank - the first Indian company to do so.

2004 Launches India Growth Fund, a private equity fund.

2005Kotak Group realigns joint venture in Ford Credit; Buys Kotak Mahindra Prime (formerly known

as Kotak Mahindra Primus Limited) and sells Ford credit Mahindra.

2005 Launches a real estate fund

2006Bought the 25% stake held by Goldman Sachs in Kotak Mahindra Capital Company and

Securities

2008 Launched a Pension Fund under the New Pension System

31 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 32/72

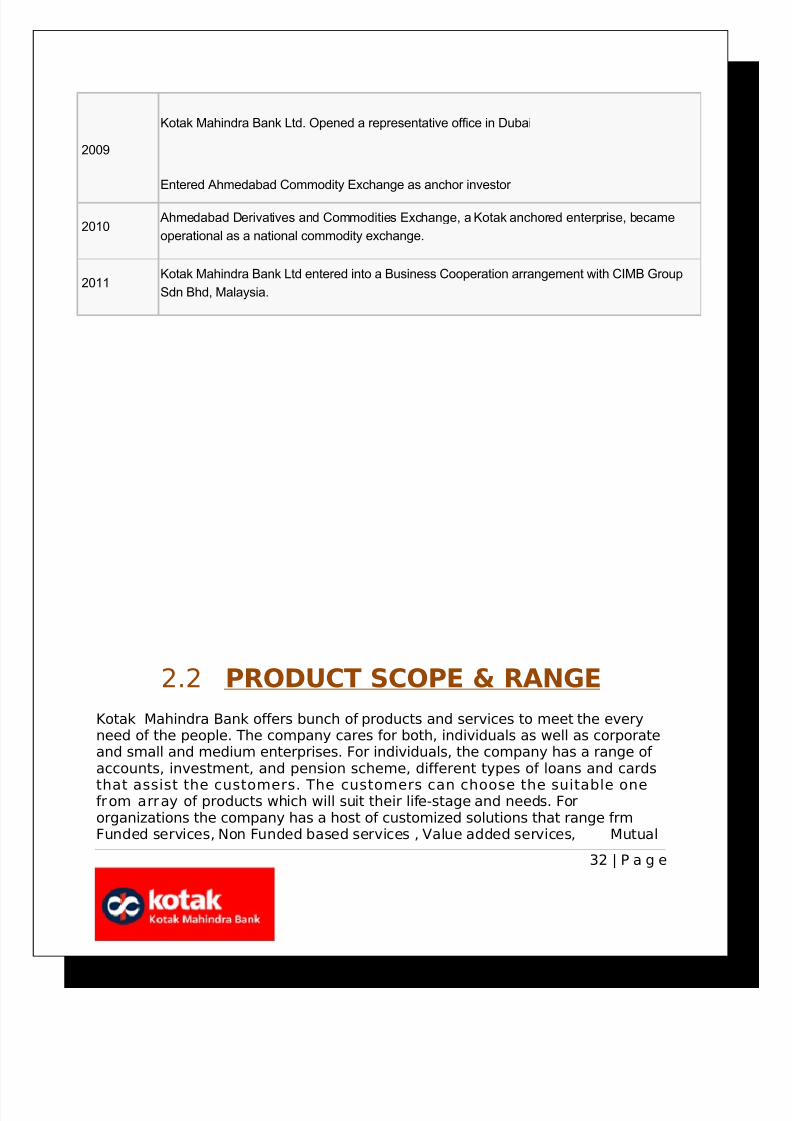

2009

Kotak Mahindra Bank Ltd. Opened a representative office in Dubai

Entered Ahmedabad Commodity Exchange as anchor investor

2010 Ahmedabad Derivatives and Commodities Exchange, a Kotak anchored enterprise, became

operational as a national commodity exchange.

2011Kotak Mahindra Bank Ltd entered into a Business Cooperation arrangement with CIMB Group

Sdn Bhd, Malaysia.

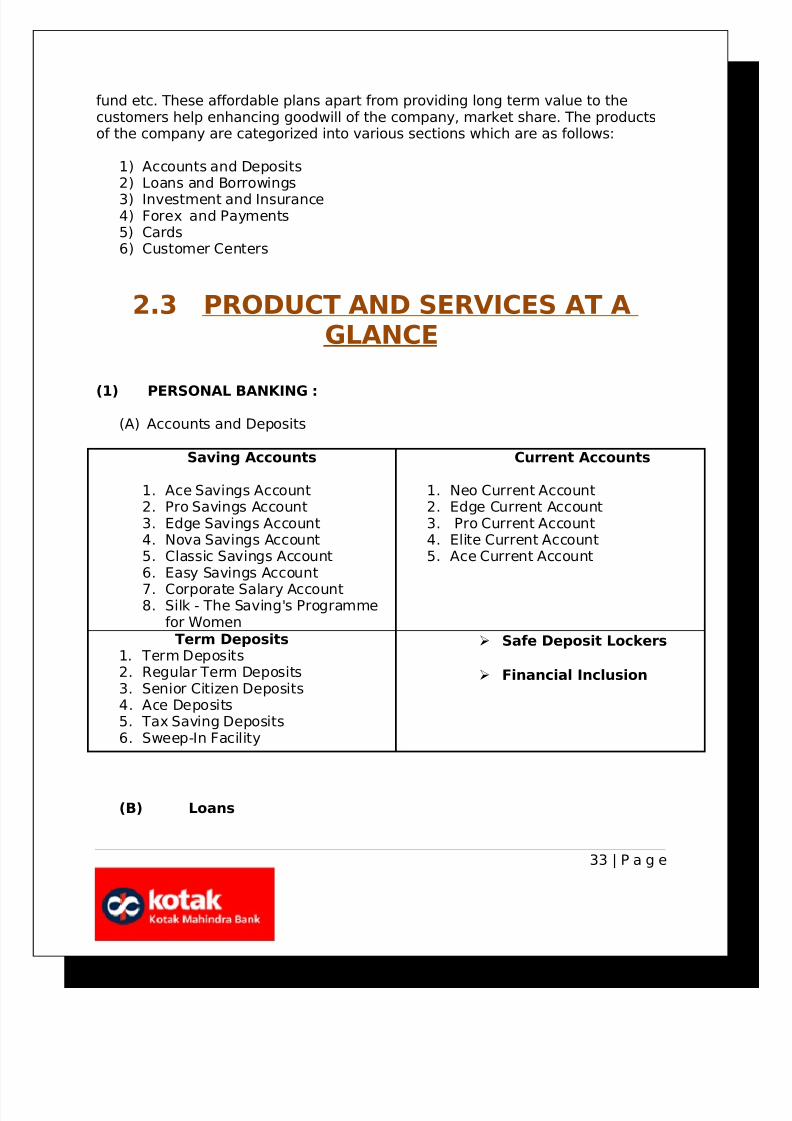

2.2 PRODUCT SCOPE & RANGE

Kotak Mahindra Bank offers bunch of products and services to meet the everyneed of the people. The company cares for both, individuals as well as corporateand small and medium enterprises. For individuals, the company has a range of accounts, investment, and pension scheme, different types of loans and cards

that assist the customers. The customers can choose the suitable onefrom array of products which will suit their life-stage and needs. Fororganizations the company has a host of customized solutions that range frmFunded services, Non Funded based services , Value added services, Mutual

32 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 33/72

fund etc. These affordable plans apart from providing long term value to thecustomers help enhancing goodwill of the company, market share. The productsof the company are categorized into various sections which are as follows:

1) Accounts and Deposits2) Loans and Borrowings

3) Investment and Insurance4) Forex and Payments5) Cards6) Customer Centers

2.3 PRODUCT AND SERVICES AT AGLANCE

(1) PERSONAL BANKING :

(A) Accounts and Deposits

Saving Accounts

1. Ace Savings Account2. Pro Savings Account3. Edge Savings Account4. Nova Savings Account5. Classic Savings Account6. Easy Savings Account

7. Corporate Salary Account8. Silk - The Saving's Programme

for Women

Current Accounts

1. Neo Current Account2. Edge Current Account3. Pro Current Account4. Elite Current Account5. Ace Current Account

Term Deposits1. Term Deposits2. Regular Term Deposits3. Senior Citizen Deposits4. Ace Deposits5. Tax Saving Deposits6. Sweep-In Facility

Safe Deposit Lockers

Financial Inclusion

(B) Loans

33 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 34/72

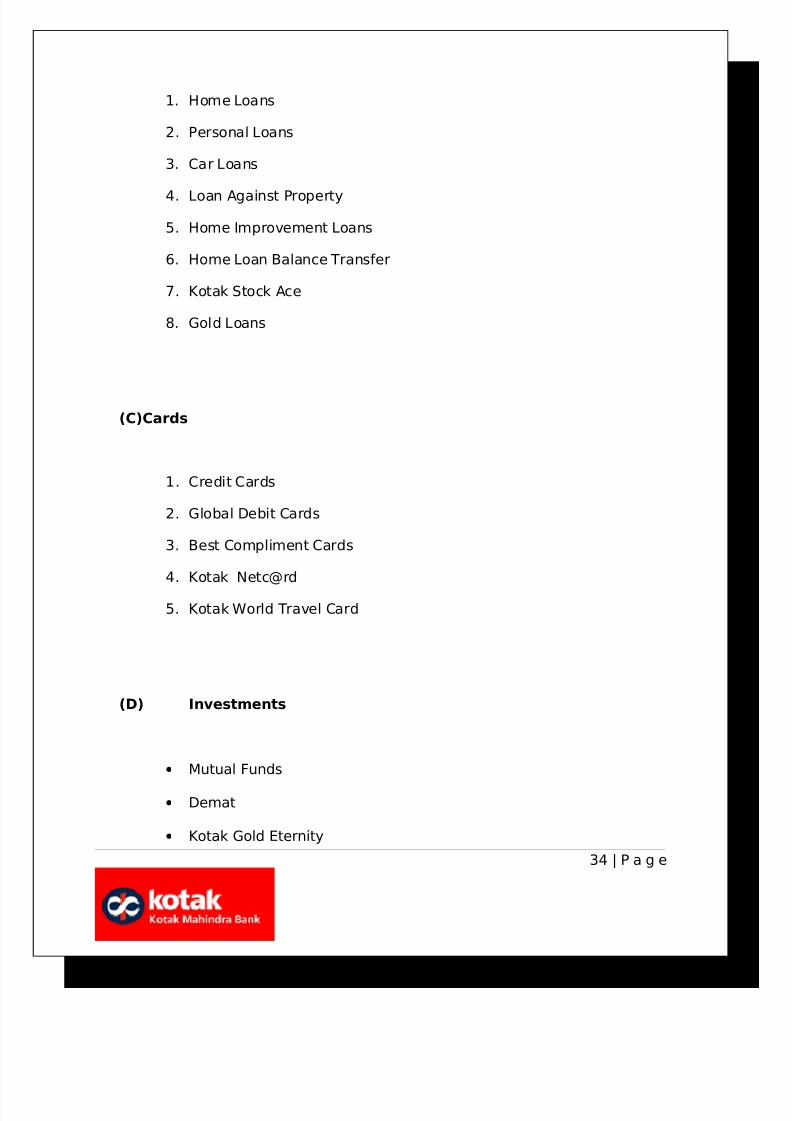

1. Home Loans

2. Personal Loans

3. Car Loans

4. Loan Against Property

5. Home Improvement Loans

6. Home Loan Balance Transfer

7. Kotak Stock Ace

8. Gold Loans

(C)Cards

1. Credit Cards

2. Global Debit Cards

3. Best Compliment Cards

4. Kotak Netc@rd

5. Kotak World Travel Card

(D) Investments

• Mutual Funds

• Demat

• Kotak Gold Eternity

34 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 35/72

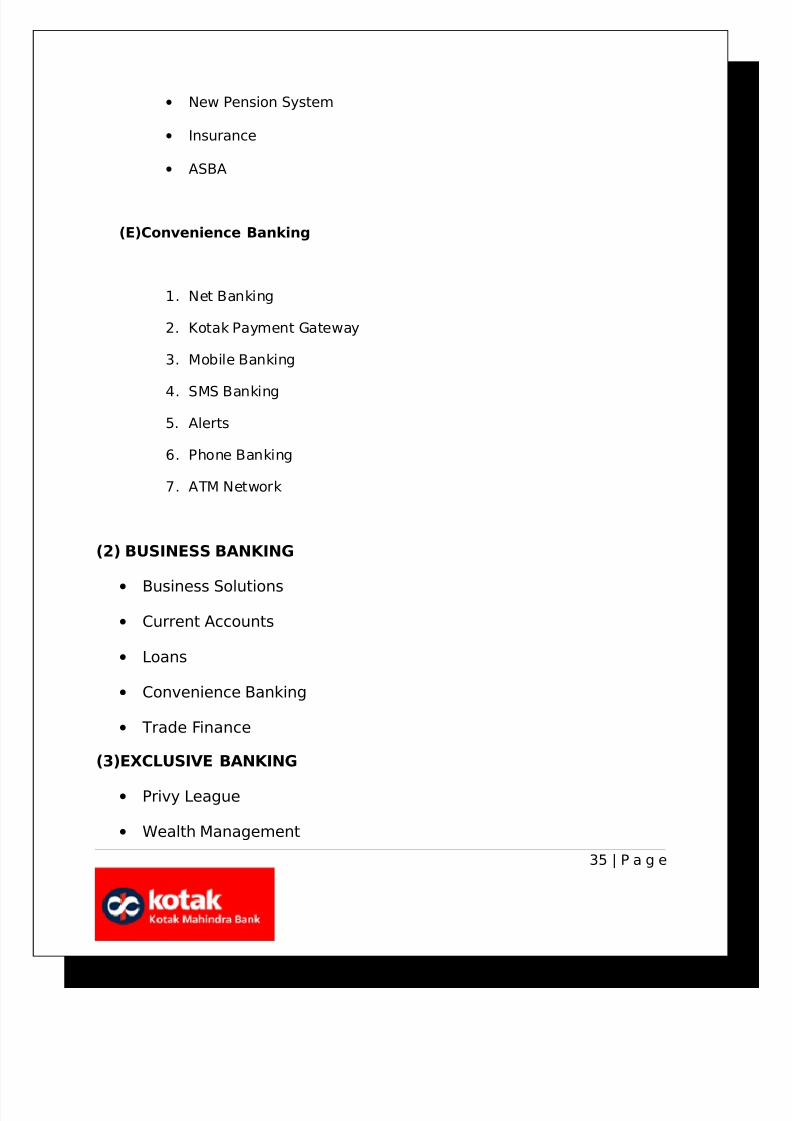

• New Pension System

• Insurance

• ASBA

(E)Convenience Banking

1. Net Banking

2. Kotak Payment Gateway

3. Mobile Banking

4. SMS Banking

5. Alerts

6. Phone Banking

7. ATM Network

(2) BUSINESS BANKING

•Business Solutions

• Current Accounts

• Loans

• Convenience Banking

• Trade Finance

(3)EXCLUSIVE BANKING

• Privy League

• Wealth Management

35 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 36/72

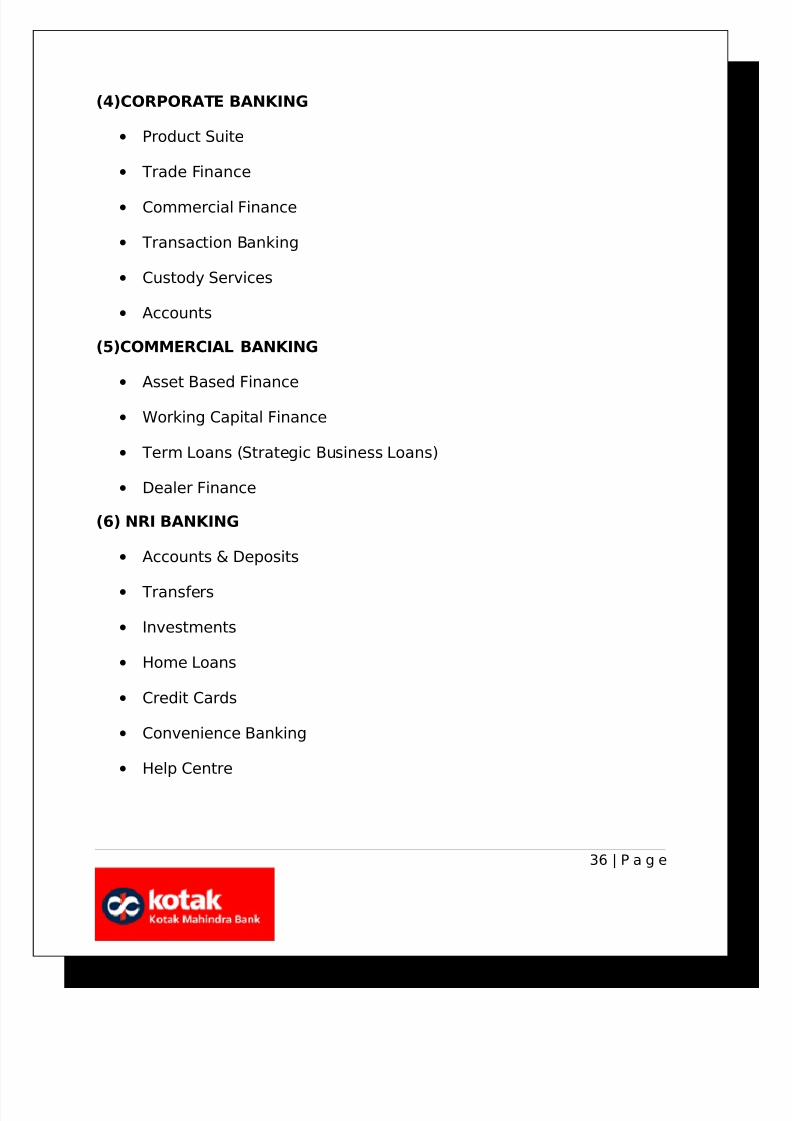

(4)CORPORATE BANKING

• Product Suite

• Trade Finance

• Commercial Finance

• Transaction Banking

• Custody Services

• Accounts

(5)COMMERCIAL BANKING

• Asset Based Finance

• Working Capital Finance

• Term Loans (Strategic Business Loans)

• Dealer Finance

(6) NRI BANKING

• Accounts & Deposits

• Transfers

• Investments

• Home Loans

• Credit Cards

• Convenience Banking

• Help Centre

36 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 37/72

CHAPTER 3

“PROBLEM STATEMENT AND

RESEARCH OBJECTIVE”

37 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 38/72

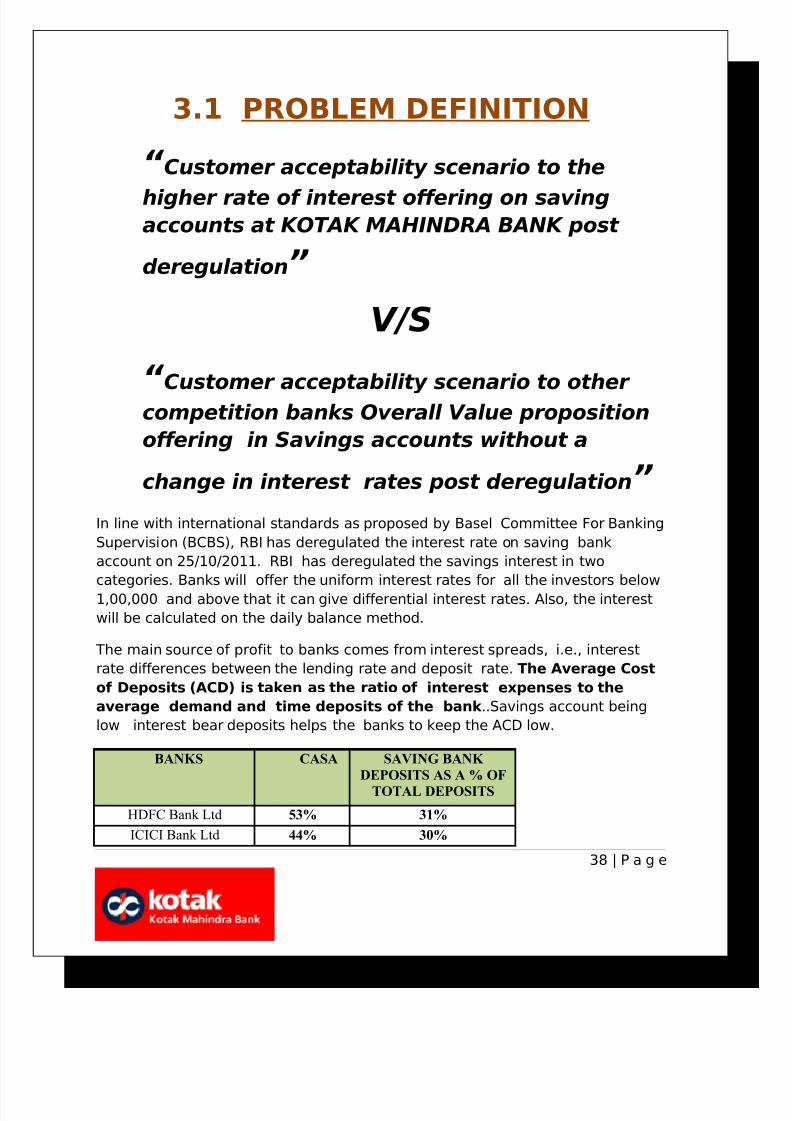

3.1 PROBLEM DEFINITION

“ Customer acceptability scenario to the

higher rate of interest offering on savingaccounts at KOTAK MAHINDRA BANK post

deregulation”

V/S

“ Customer acceptability scenario to other competition banks Overall Value proposition

offering in Savings accounts without a

change in interest rates post deregulation”In line with international standards as proposed by Basel Committee For Banking

Supervision (BCBS), RBI has deregulated the interest rate on saving bank

account on 25/10/2011. RBI has deregulated the savings interest in two

categories. Banks will offer the uniform interest rates for all the investors below

1,00,000 and above that it can give differential interest rates. Also, the interest

will be calculated on the daily balance method.

The main source of profit to banks comes from interest spreads, i.e., interest

rate differences between the lending rate and deposit rate. The Average Cost

of Deposits (ACD) is taken as the ratio of interest expenses to the

average demand and time deposits of the bank ..Savings account being

low interest bear deposits helps the banks to keep the ACD low.

BANKS CASA SAVING BANK

DEPOSITS AS A % OF

TOTAL DEPOSITS

HDFC Bank Ltd 53% 31%

ICICI Bank Ltd 44% 30%

38 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 39/72

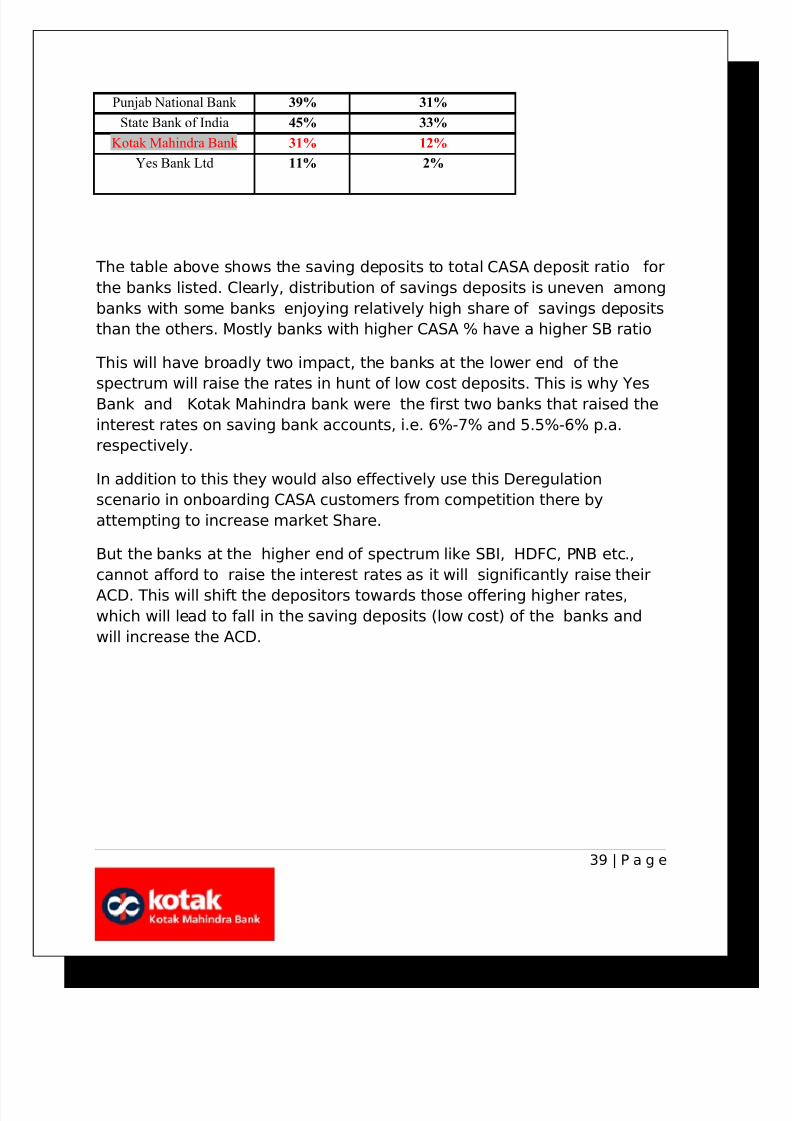

Punjab National Bank 39% 31%

State Bank of India 45% 33%

Kotak Mahindra Bank 31% 12%

Yes Bank Ltd 11% 2%

The table above shows the saving deposits to total CASA deposit ratio for

the banks listed. Clearly, distribution of savings deposits is uneven among

banks with some banks enjoying relatively high share of savings deposits

than the others. Mostly banks with higher CASA % have a higher SB ratio

This will have broadly two impact, the banks at the lower end of the

spectrum will raise the rates in hunt of low cost deposits. This is why Yes

Bank and Kotak Mahindra bank were the first two banks that raised the

interest rates on saving bank accounts, i.e. 6%-7% and 5.5%-6% p.a.

respectively.

In addition to this they would also effectively use this Deregulation

scenario in onboarding CASA customers from competition there by

attempting to increase market Share.

But the banks at the higher end of spectrum like SBI, HDFC, PNB etc.,

cannot afford to raise the interest rates as it will significantly raise their

ACD. This will shift the depositors towards those offering higher rates,which will lead to fall in the saving deposits (low cost) of the banks and

will increase the ACD.

39 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 40/72

3.2 RESEARCH OBJECTIVE

3.2 .1 PRIMARYRESEARCH

OBJECTIVE

Impact of 6% interest rate on New – to- bank customer

acquisition in Kotak Mahindra bank and related acceptability,

awareness & responsiveness scenario in the market

40 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 41/72

3.2 .2 SECONDARY RESEARCH

OBJECTIVEImpact of 6% interest rate on Existing customers Balance build

up and Savings Bank account portfolio movement in Kotak

Mahindra bank and related acceptability , awareness &

responsiveness by the Existing customers

CHAPTER - 4

RESEARCH METHODOLOGY Finite data sampling spread across the entire hinterland on

the Medium to Higher income group customer class which the

brand Kotak Mahindra Bank positions itself in through ground

level & marketing activity related promos was the basic

methodology used which involved me in the following

activities :

• Developing Sample questionnaire for both New-to-bank &

Existing customers41 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 42/72

• Interviewing and data collection from the hinterland of

designated branch for checking awareness &

acceptability

•

Selling and lead generation activity performed by self inacquiring customers primarily for Savings Bank

accounts.

4.1 SAMPLING DESIGN

While it is practically not possible to study whole universe, it becomes

necessary to take sample from the universe to know about its characteristics

and base our analysis and forecasts on the derivations of the above sampling

unit

4.1.1 Sampling Unit : Self Employed professionals, Salaried Class, Service

providers, Doctors and housewives of Dwarka (Delhi ) city.

4.1.2 Sampling Technique : Non probability - Convenience Sampling

4.1.3 Research Instrument : Structured Questionnaire

4.1.4 Contact Method : Personal Interview

4.1.5 Sample Size : Have acted and studied a total sample size of 200respondents ,In which 100 respondents are the Existing customer of KOTAK

MAHINDRA BANK and remaining 100 are the account holders of other banks.

4.2 RESEARCH DESIGN

Research design can be defined as the plan and structure of enquiry, formulatedin order to obtain relevant answers to research Question on business aspects or

42 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 43/72

we can say that it outlines the actual research problem on hand and details the

process for solving it.

This project report is based on the descriptive as well as causal research

because it tries to find out the impact of higher rate of interest on existing as well

as on non existing customer of Kotak Mahindra Bank.

Universe of the study : All sectors of Dwarka both residential and commercial

(New Delhi)

Unit of investigation: Residents of Dwarka who are A/C holder of Kotak

Mahindra bank or other banks.

Duration of Study : 10 Weeks

Research Type : Descriptive & Causal

4.3 RESEARCH LIMITATION

1. Although there has been a finite yet sizeable sample taken , the

sample class does not cover entire range of population mix

especially pertaining to rural and semi –urban population as well as

Senior citizens category.

2. While the research methodology has been performed under a “

Direct interview “ at the customer touch point it has limitations on

internal database study of the Savings portfolio movements / shifts

post deregulation. This would have been possible provided complete

section of RM Base or managed RO base would have been shared to

see the Month – on – month movement of Savings balances. This if

provided the research would have better and deeper analysis of

customer acceptability of “ 6% interest rate “ and would have

thrown adequate light on pattern of savings and stickiness to the

brand purely post deregulation.

43 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 44/72

3. The methodology does not throw light on the most accepted way of

information flow( Print/ Audio Visual/ Personal call/ Marketing drives

) to customers telling about the rate change and does not fully

confirm a standardized and compulsory medium in terms of

information flow which would have the highest impact in creating

customer inquisitiveness and would be a catalyst for incrementing a

beeline of customers to open bank accounts in Savings portfolio

post the increase of interest rate.

4. The sample size of analysis done for Dwarka branch may not be fully

in line with the entire behavior of the existing customers of the bank

as it had only an analysis of a specific branch. Hence the customer

awareness made by RM’s / RO’s may differ and the overall picture

may / or may not have exactly similar trends in the bank as a whole.

44 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 45/72

CHAPTER - 5

DATA ANALYSIS OF

SAMPLING RESEARCH

METHODOLOGY

45 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 46/72

5.1 : DATA ANALYSIS ANDINTERPRETATION

FOR NEW ACQUISITION

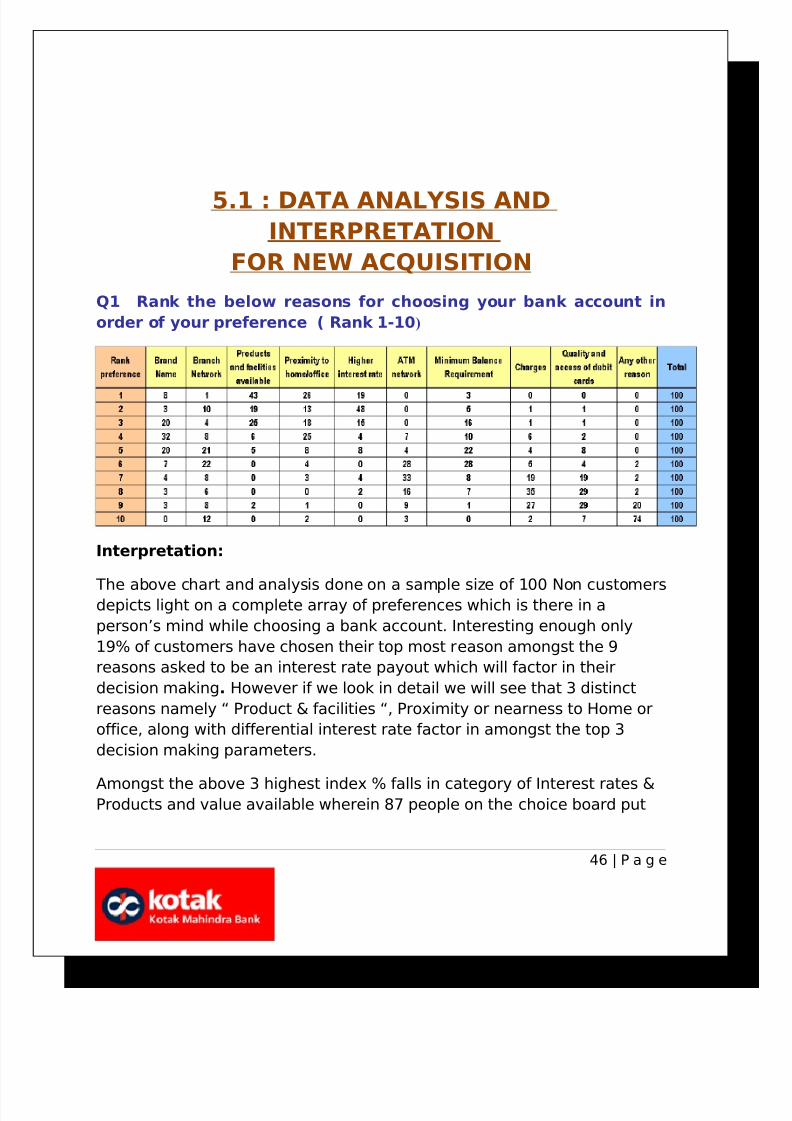

Q1 Rank the below reasons for choosing your bank account in

order of your preference ( Rank 1-10)

Interpretation:

The above chart and analysis done on a sample size of 100 Non customersdepicts light on a complete array of preferences which is there in a

person’s mind while choosing a bank account. Interesting enough only

19% of customers have chosen their top most reason amongst the 9

reasons asked to be an interest rate payout which will factor in their

decision making. However if we look in detail we will see that 3 distinct

reasons namely “ Product & facilities “, Proximity or nearness to Home or

office, along with differential interest rate factor in amongst the top 3

decision making parameters.

Amongst the above 3 highest index % falls in category of Interest rates &Products and value available wherein 87 people on the choice board put

46 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 47/72

Products & facilities as Priority over 82 ranking in Interest being the only

option for decision making.

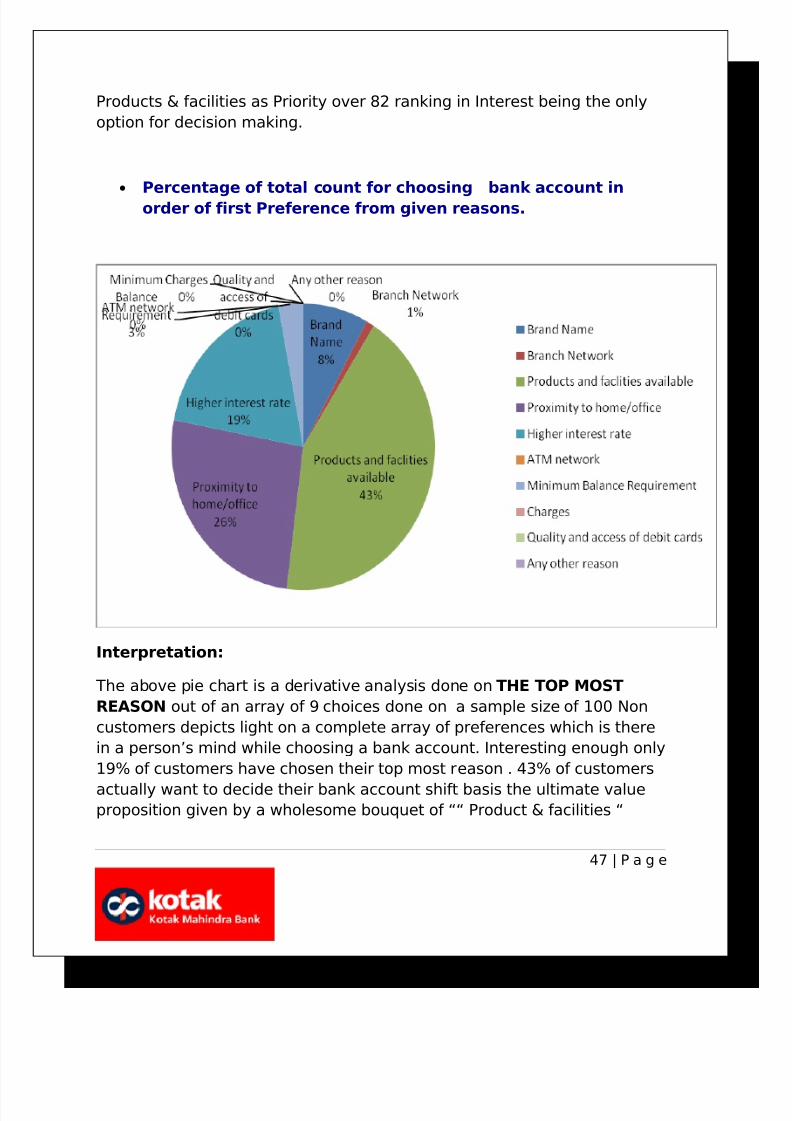

•

Percentage of total count for choosing bank account inorder of first Preference from given reasons.

Interpretation:

The above pie chart is a derivative analysis done on THE TOP MOST

REASON out of an array of 9 choices done on a sample size of 100 Non

customers depicts light on a complete array of preferences which is there

in a person’s mind while choosing a bank account. Interesting enough only

19% of customers have chosen their top most reason . 43% of customers

actually want to decide their bank account shift basis the ultimate valueproposition given by a wholesome bouquet of ““ Product & facilities “

47 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 48/72

Proximity / nearness of branch to home or office becomes a first priority of

26% customers ( mainly housewives/ working people who can also operate

lockers ). Going by the analysis 8% think that the solidity and goodwill of

the Brand name comes as a priority over anything else.

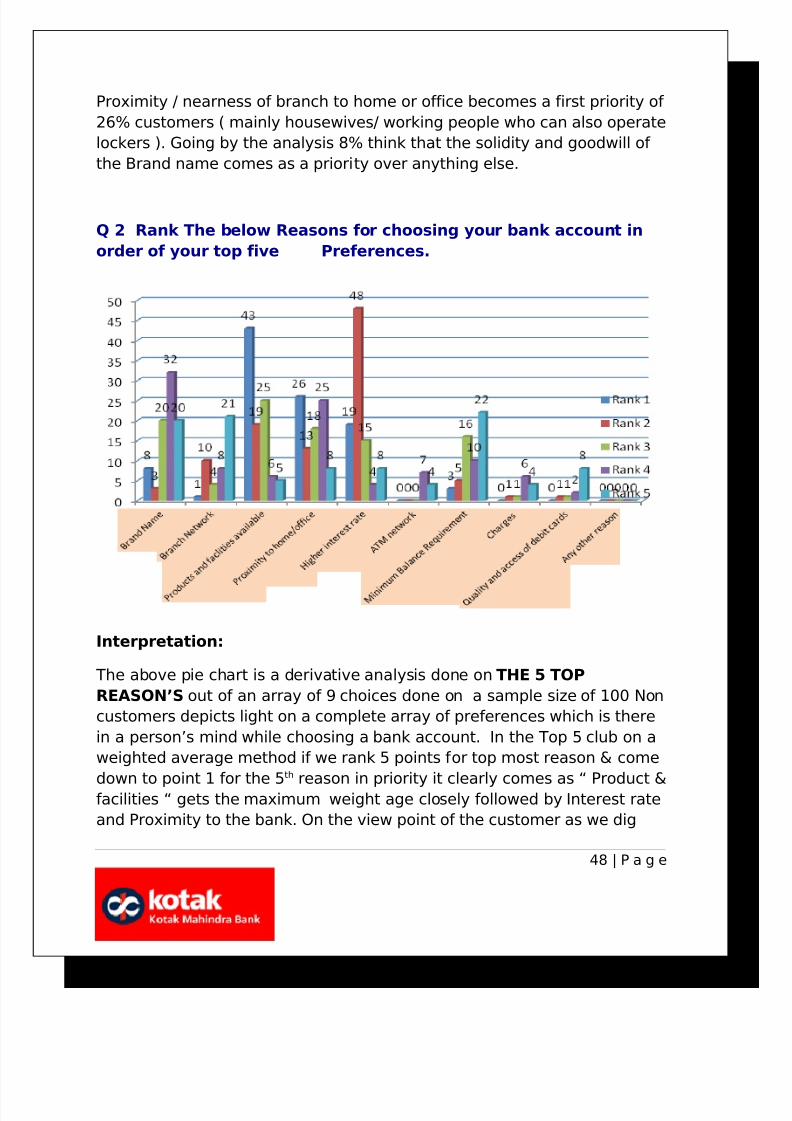

Q 2 Rank The below Reasons for choosing your bank account in

order of your top five Preferences.

Interpretation:

The above pie chart is a derivative analysis done on THE 5 TOP

REASON’S out of an array of 9 choices done on a sample size of 100 Non

customers depicts light on a complete array of preferences which is there

in a person’s mind while choosing a bank account. In the Top 5 club on a

weighted average method if we rank 5 points for top most reason & come

down to point 1 for the 5

th

reason in priority it clearly comes as “ Product &facilities “ gets the maximum weight age closely followed by Interest rate

and Proximity to the bank. On the view point of the customer as we dig

48 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 49/72

deep Minimum balance requirements and Brand name start to grow bigger

and responsive decision deciders.

Hence while acquiring New – to –bank customers the above 5 reasons

must be appropriately blended as benefits to be used as a combined “

Hook “ for decision making. All marketing promos and catchmentexercises should keep these in mind while designing a promo./

advertisement

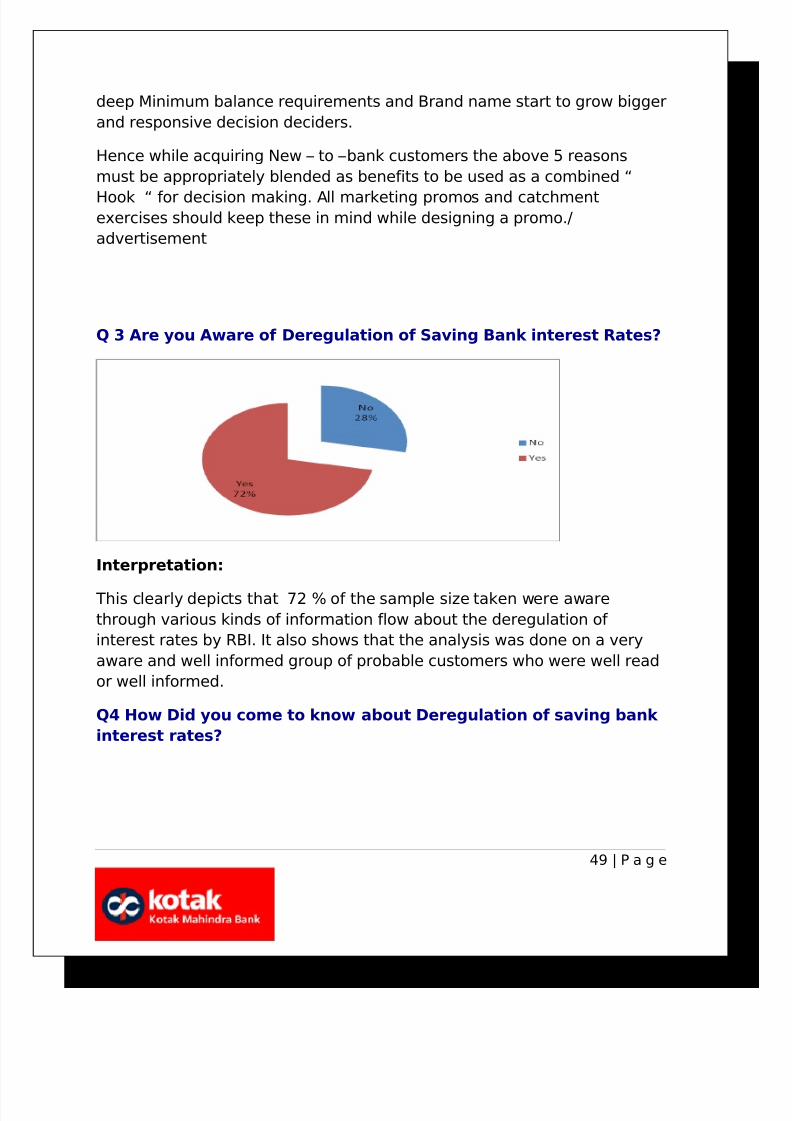

Q 3 Are you Aware of Deregulation of Saving Bank interest Rates?

Interpretation:

This clearly depicts that 72 % of the sample size taken were aware

through various kinds of information flow about the deregulation of

interest rates by RBI. It also shows that the analysis was done on a very

aware and well informed group of probable customers who were well read

or well informed.

Q4 How Did you come to know about Deregulation of saving bank

interest rates?

49 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 50/72

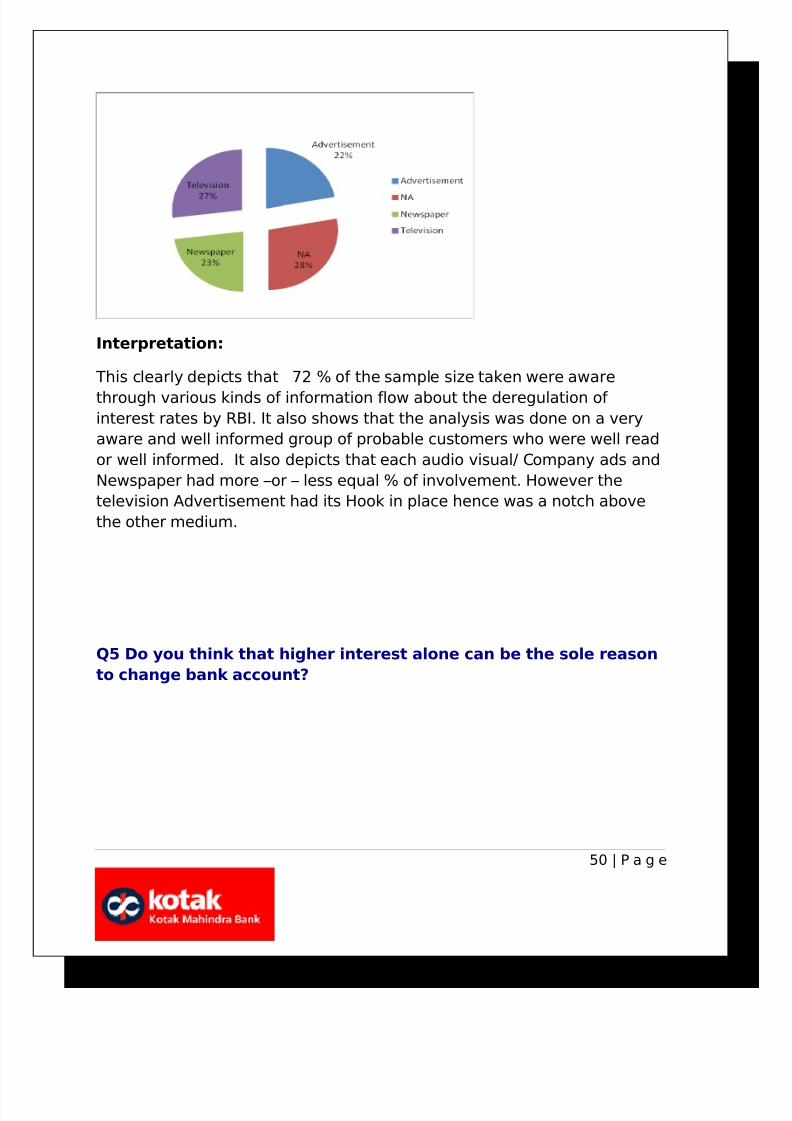

Interpretation:

This clearly depicts that 72 % of the sample size taken were aware

through various kinds of information flow about the deregulation of interest rates by RBI. It also shows that the analysis was done on a very

aware and well informed group of probable customers who were well read

or well informed. It also depicts that each audio visual/ Company ads and

Newspaper had more –or – less equal % of involvement. However the

television Advertisement had its Hook in place hence was a notch above

the other medium.

Q5 Do you think that higher interest alone can be the sole reason

to change bank account?

50 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 51/72

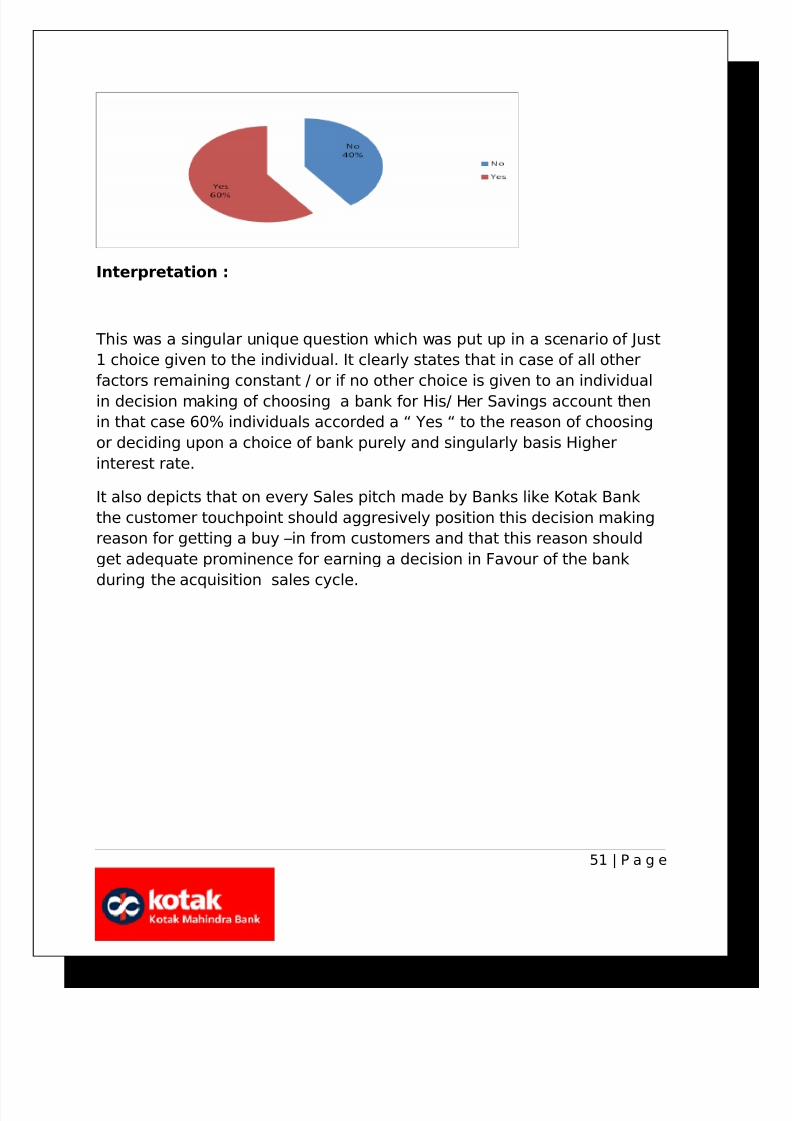

Interpretation :

This was a singular unique question which was put up in a scenario of Just

1 choice given to the individual. It clearly states that in case of all other

factors remaining constant / or if no other choice is given to an individual

in decision making of choosing a bank for His/ Her Savings account then

in that case 60% individuals accorded a “ Yes “ to the reason of choosing

or deciding upon a choice of bank purely and singularly basis Higher

interest rate.

It also depicts that on every Sales pitch made by Banks like Kotak Bank

the customer touchpoint should aggresively position this decision making

reason for getting a buy –in from customers and that this reason should

get adequate prominence for earning a decision in Favour of the bank

during the acquisition sales cycle.

51 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 52/72

5.2 :DATA ANALYSIS AND

INTERPRETATION FOR EXISTING

CUSTOMERS

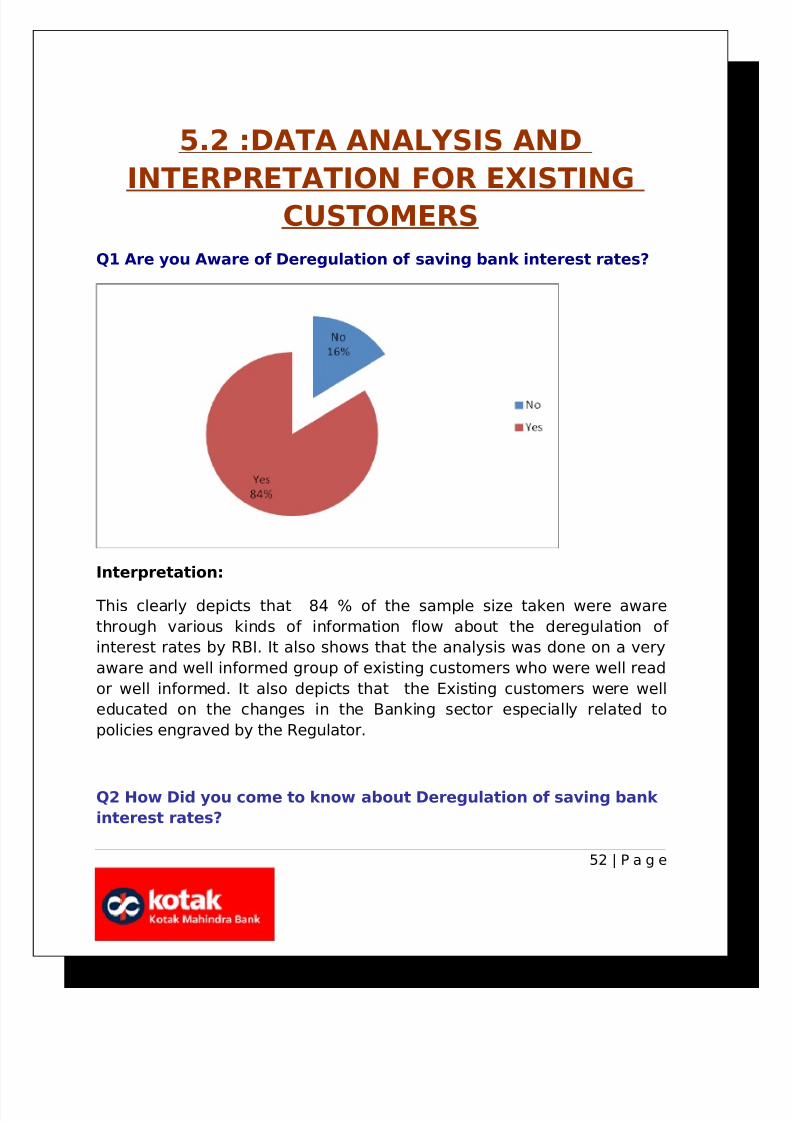

Q1 Are you Aware of Deregulation of saving bank interest rates?

Interpretation:

This clearly depicts that 84 % of the sample size taken were aware

through various kinds of information flow about the deregulation of

interest rates by RBI. It also shows that the analysis was done on a very

aware and well informed group of existing customers who were well read

or well informed. It also depicts that the Existing customers were well

educated on the changes in the Banking sector especially related to

policies engraved by the Regulator.

Q2 How Did you come to know about Deregulation of saving bank

interest rates?

52 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 53/72

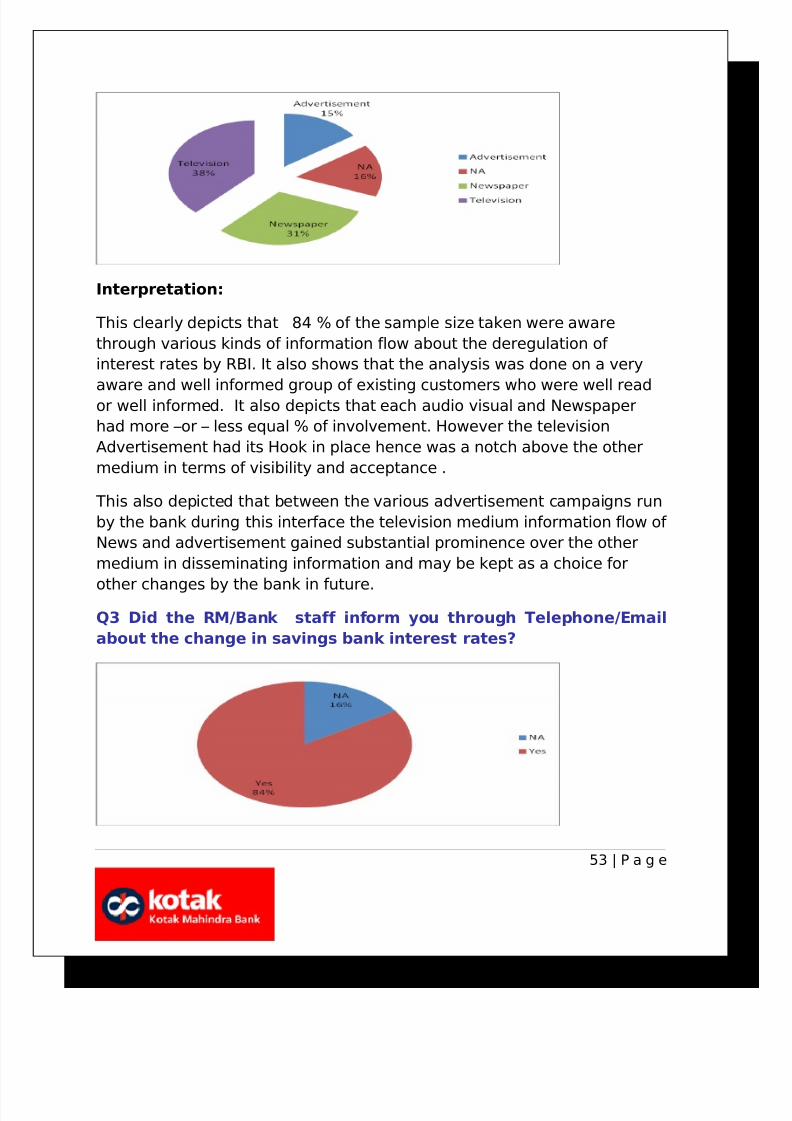

Interpretation:

This clearly depicts that 84 % of the sample size taken were aware

through various kinds of information flow about the deregulation of

interest rates by RBI. It also shows that the analysis was done on a very

aware and well informed group of existing customers who were well reador well informed. It also depicts that each audio visual and Newspaper

had more –or – less equal % of involvement. However the television

Advertisement had its Hook in place hence was a notch above the other

medium in terms of visibility and acceptance .

This also depicted that between the various advertisement campaigns run

by the bank during this interface the television medium information flow of

News and advertisement gained substantial prominence over the other

medium in disseminating information and may be kept as a choice for

other changes by the bank in future.

Q3 Did the RM/Bank staff inform you through Telephone/Email

about the change in savings bank interest rates?

53 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 54/72

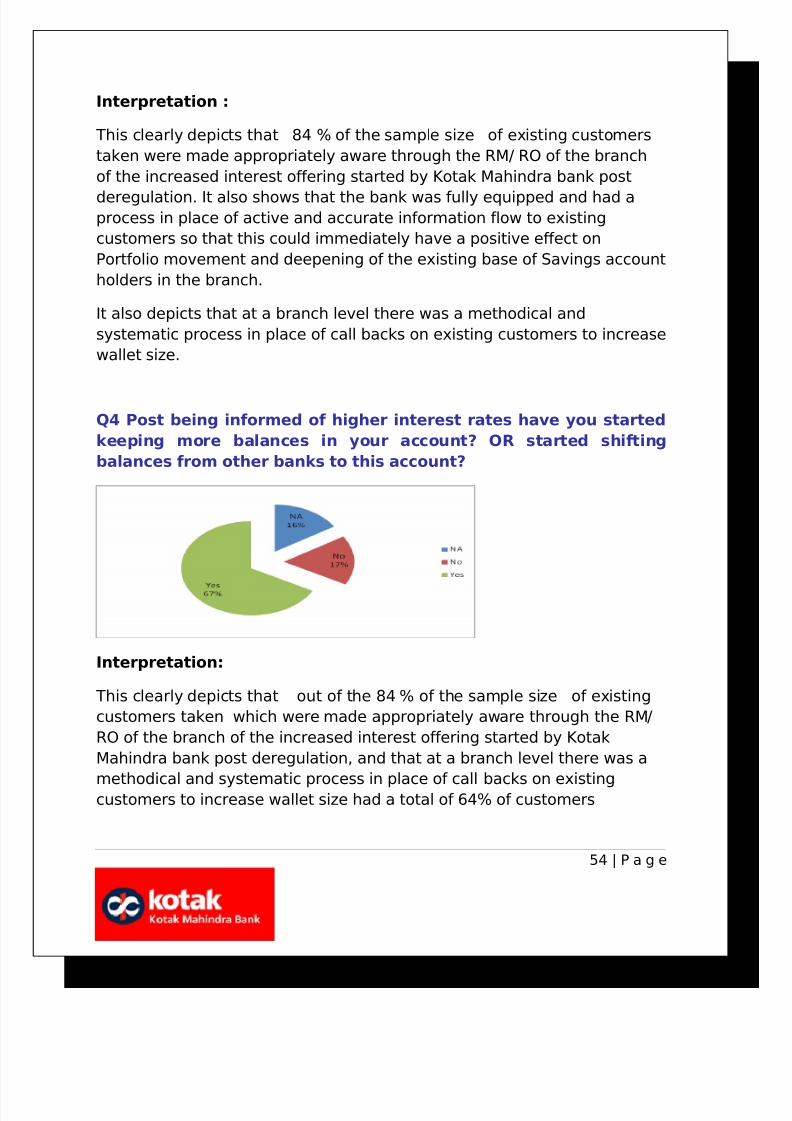

Interpretation :

This clearly depicts that 84 % of the sample size of existing customers

taken were made appropriately aware through the RM/ RO of the branch

of the increased interest offering started by Kotak Mahindra bank post

deregulation. It also shows that the bank was fully equipped and had aprocess in place of active and accurate information flow to existing

customers so that this could immediately have a positive effect on

Portfolio movement and deepening of the existing base of Savings account

holders in the branch.

It also depicts that at a branch level there was a methodical and

systematic process in place of call backs on existing customers to increase

wallet size.

Q4 Post being informed of higher interest rates have you started

keeping more balances in your account? OR started shifting

balances from other banks to this account?

Interpretation:

This clearly depicts that out of the 84 % of the sample size of existing

customers taken which were made appropriately aware through the RM/

RO of the branch of the increased interest offering started by Kotak

Mahindra bank post deregulation, and that at a branch level there was a

methodical and systematic process in place of call backs on existingcustomers to increase wallet size had a total of 64% of customers

54 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 55/72

responding positively on incrementing wallet size or Savings account

balances.

It showed that the Bank and the branch were involved in extracting better

balances from existing customers post the interest rate hike.

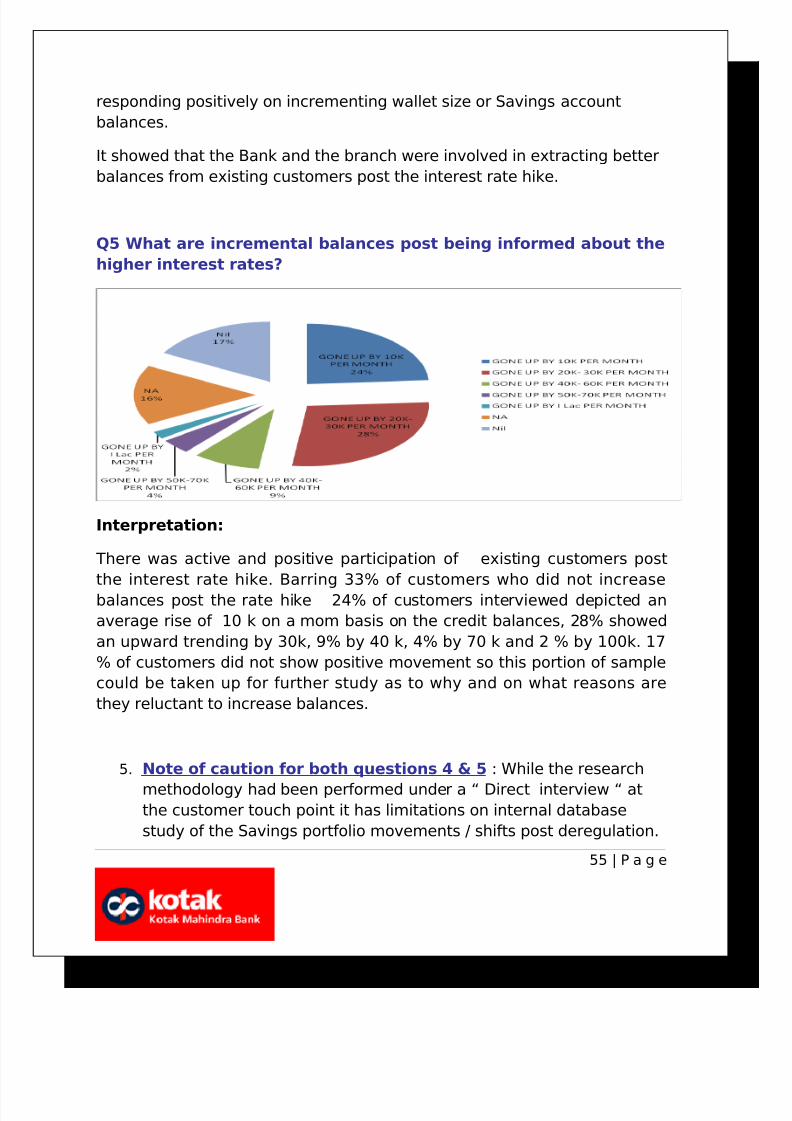

Q5 What are incremental balances post being informed about the

higher interest rates?

Interpretation:

There was active and positive participation of existing customers post

the interest rate hike. Barring 33% of customers who did not increase

balances post the rate hike 24% of customers interviewed depicted an

average rise of 10 k on a mom basis on the credit balances, 28% showed

an upward trending by 30k, 9% by 40 k, 4% by 70 k and 2 % by 100k. 17

% of customers did not show positive movement so this portion of sample

could be taken up for further study as to why and on what reasons are

they reluctant to increase balances.

5. Note of caution for both questions 4 & 5 : While the research

methodology had been performed under a “ Direct interview “ atthe customer touch point it has limitations on internal database

study of the Savings portfolio movements / shifts post deregulation.

55 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 56/72

This may not be a completely accurate data as it does not include

validated balance growth on portfolio from the system on a month –

to- month base from November -2011. The same would have been

possible provided complete section of RM Base or managed RO base

would have been shared to see the Month – on – month movement

of Savings balances. This if provided the research would have better

and deeper analysis of customer acceptability of “ 6% interest rate “

and would have thrown adequate light on pattern of savings and

stickiness to the brand purely post deregulation.

Q6 Rank the below Reasons for increasing balances in your saving

account in order of your preference ( Rank them 1-10)

Interpretation:

The above chart and analysis done on a sample size of 100 existing

customers depicts light on a complete array of preferences which is therein a customer’s mind while he tends to increase balances in a given bank

account against others and in a way graduates to treating Kotak as a

56 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 57/72

primary banker in the SB portfolio. Interestingly 29% of customers have

chosen their top most reason amongst the 9 reasons asked to be an

interest rate payout which will factor in their decision making. However if

we look in detail we will see that 4 distinct reasons namely “ Product &

facilities available in the basket “,Personalized attention by bank staff and

Service delivery on operational efficiency and seamless transaction

processing to be amongst the top 4 decision making parameters.

The above chart can be used as a derivative analysis done on THE 5 TOP

REASON’S out of an array of 9 choices done on a sample size of 100

Existing customers depicts light on a complete array of preferences which

is there in a person’s mind while he switches gears in balance buildup. In

the Top 5 club on a weighted average method if we rank 5 points for top

most reason & come down to point 1 for the 5th reason in priority it clearly

comes as “ Interest paid “ gets the maximum weight age closely followed

by Personalised service and Service delivery .

This analysis can clearly also spell out the retention and deepening

strategy for the branch and bank and can throw light on how to tackle

customer attention.

6. Note of caution : The cross sell of asset products and linking of

EMI’s surprisingly does not account for as a major customer

acceptability reason for incrementing balances. The interview modeof analysis may not be a complete fool –proof way of looking at this

objective as this solely has been accepted worldwide across banking

companies to be the single most driver of increasing stickiness,

incrementing credit balances and negating attrition .

Q7. Percentage of TOPMOST ranking reason for increasing

balances in saving accounts.

57 | P a g e

7/31/2019 Project for Sip (1)

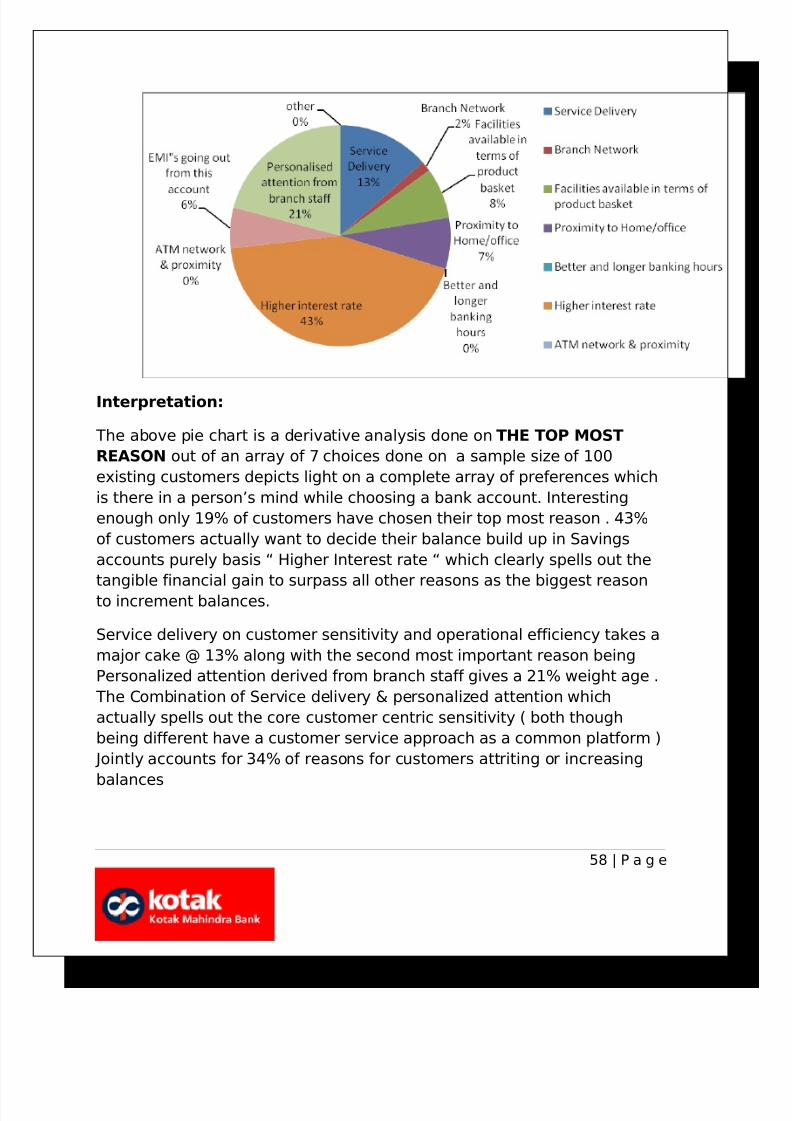

http://slidepdf.com/reader/full/project-for-sip-1 58/72

Interpretation:

The above pie chart is a derivative analysis done on THE TOP MOST

REASON out of an array of 7 choices done on a sample size of 100

existing customers depicts light on a complete array of preferences which

is there in a person’s mind while choosing a bank account. Interesting

enough only 19% of customers have chosen their top most reason . 43%

of customers actually want to decide their balance build up in Savings

accounts purely basis “ Higher Interest rate “ which clearly spells out the

tangible financial gain to surpass all other reasons as the biggest reason

to increment balances.

Service delivery on customer sensitivity and operational efficiency takes a

major cake @ 13% along with the second most important reason being

Personalized attention derived from branch staff gives a 21% weight age .

The Combination of Service delivery & personalized attention which

actually spells out the core customer centric sensitivity ( both though

being different have a customer service approach as a common platform )

Jointly accounts for 34% of reasons for customers attriting or increasing

balances

58 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 59/72

CHAPTER - 6 - CONCLUSION & SUGGESTIONS

6.1 CONCLUSION

"New customers belong to various segments - corporate salary accounts,small-scale enterprises, self-employed professionals and salariedindividuals," adds KVS Manian, president, consumer banking at Kotak Mahindra Bank . "The response to the hike in our savings bank rate has

been reasonably good, both in terms of new customers and our existingcustomers. Ever since we increased our rates to 6% on domestic savingsdeposits, our rate of acquisition has been hovering at around 80%."

In the December 2011 quarter, the CASA (current account and savingsaccount) deposits of Kotak Mahindra Bank's CASA rose from 9,355 croreas of September 2011 to 10,615 crore in the December quarter.

Now, higher returns act as a huge incentive for customers to

switch banks. However, should it be the sole criterion? The

natural questions were Is it the right time, is Kotak Mahindra

Bank adequately positioned ?

The core essence of the entire project had hovered around the factual

analysis and interpretation of change in Consumer ( Referred to as Non

Customers and Existing customers ) in the above pages in the changed

scenario of Interest deregulation in Savings bank account with a study of

customer behavior pattern change, acceptability quotient index in retail

Savings bank accounts in Kotak Mahindra bank.

Raising Interest rates post deregulation has unleashed the opportunity

of Customer acquisition as well as increasing portfolios in existingcustomers. With this it had sprung off a price sensitive war within the

59 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 60/72

already matured Urban Retail banking space on the opportunity of

increasing market share at least with bottom CASA spread banks.

The analysis done also brings certain answers to the question on

profitability in CASA spreads and interest income because merely

acquiring customers through an interest war will have an adverse andmay impact on Cost of Funds as well as shrink the wallet size of

responding banks like Kotak Mahindra on controlling asset pricing and

further generating interest income through differential of asset liability

spreads.

The above pages have traversed through a path of in depth analysis andlearning derived by customer interface in the target segment. Thestructure and the final culmination based on data research and samplinghave thrown logical light on customer awareness on the Savings account

interest rate upward changes post Deregulation at Kotak Mahindra bank,the market responsiveness to this change both in terms of New Customer acquisition and balance buildup in existing Savings account portfolio base.It will throw adequate light on willingness to change purely basis “ anupward movement of interest “ vis-à-vis host of other products, facilities,branding and so on.

6.2 SUGGESTIONS &

RECOMMENDATIONS

7. On the strategy of acquisition of New to Bank customers ,

the bank has to recurringly follow a principle of highlighting the

Increased interest offering on Savings account recurringly. This

could be achieved in the following ways

1. On each Marketing activity the entry point or main activity area to

be completely covered with Banners clearly projecting the 1st

invitation to customers through highlighting the same.

2. DMRC stations near Kotak Mahindra Branches and off site ATM

outers to be manned with Staff wearing a complete dress depicting

the following message “ If you do not earn 6% on your Savings yet

then you haven’t earned enough “ with a very big Kotak Logo.

60 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 61/72

3. DMRC Train route announcements to be dotted with running ads on

this interest rates

4. All off AUS ie all Non Kotak Bank txns done on Kotak Bank ATM’s

needs to be analysed and in specific slots wherein there are more

Non Kotak Transactions, RE’s may be mapped and should bedelivering a sales pitch during those hours/ slots to maximise

conversions.

5. Restaurants in all nearby areas where footfalls are high should have

the bank furnishing the “ Feedback card “ to be filled in by visitors.

The Feedback form should have the last point “ We are sure that

you have enjoyed your meal and as you proceed homewards do you

think we can have you coming here more often? Only if you believe

in the power of 6% from Kotak Bank” The data of feedback form

needs to be captured by the bank.

6. On all weeks a continuous Morning walker activity can be done in

specific residential catchments. This activity should have a complete

sales force wearing a complete dress depicting the following

message “ If you do not earn 6% on your Savings yet then you

haven’t earned enough “ with a very big Kotak Logo.

7. Women clubs, SPA’s, healthclub & Dancing clubs which have niche

female audience attending.Female staff should be deployed on

weekends “ If you do not earn 6% on your Savings yet then youhaven’t earned enough “ with a very big Kotak Logo. Or “ Have you

experienced the power of SILK Account if not.. just speak to us “

• On the strategy of acquisition of Existing customers , thebank has to recurringly follow a principle of highlighting the

61 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 62/72

Increased interest offering on Savings account recurringly. This

could be achieved in the following ways

1. Each bank account statement, loan statement, credit card

statement to depict the following message “ If you do not earn 6%

on your Savings yet then you haven’t earned enough – So it paysmore to keep more money with us “ with a very big Kotak Logo.

2. Both the Relationship Manager scorecard and the Relationship offer

scorecard should have a mandatory calling exercise on 2 calls per

customer per month mandated for service queries and updating

him/ her about the change of interest. 20% weightage should be

given in SB portfolio increment over the base of last month and 20%

weightage to be given on cross sell of family accounts within the

portfolio across unique groups.

3. The WEB page, Web links, mobile banking platform, SMS alerts

should all be centered on repeat information flow to existing

customers.

4. The internet banking platform should have Pop up alerts coming to

the customer when he does a transactions in his account or

accesses it.

62 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 63/72

CHAPTER -7 ANNEXURES &

ATTACHMENTS

CUSTOMER SURVEY DETAILS- NTB

Name ( Mr./Mrs. ) _____________________________________________

Occupation _____________________________________________

Address _____________________________________________

Mobile # _____________________________________________

E Mail Address _____________________________________________

Residence: OWNED RENTED

Vehicle: SUV CAR BIKE

Spouse Name ( Mr./Mrs. ) _____________________________________________

No of Children ____________________________________________

Age of Children 1)________ 2)________ 3)_______

Primary Banker _____________________________________________

No of Account _____________________________________________

Type of Account _____________________________________________

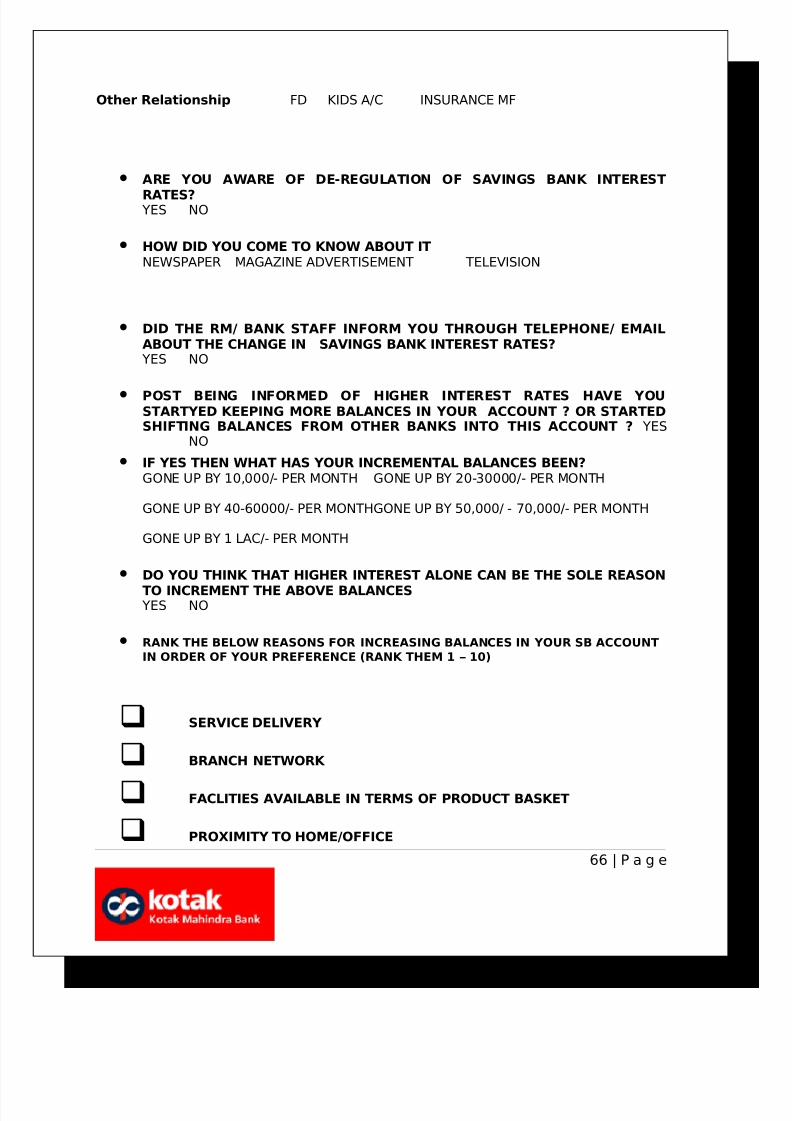

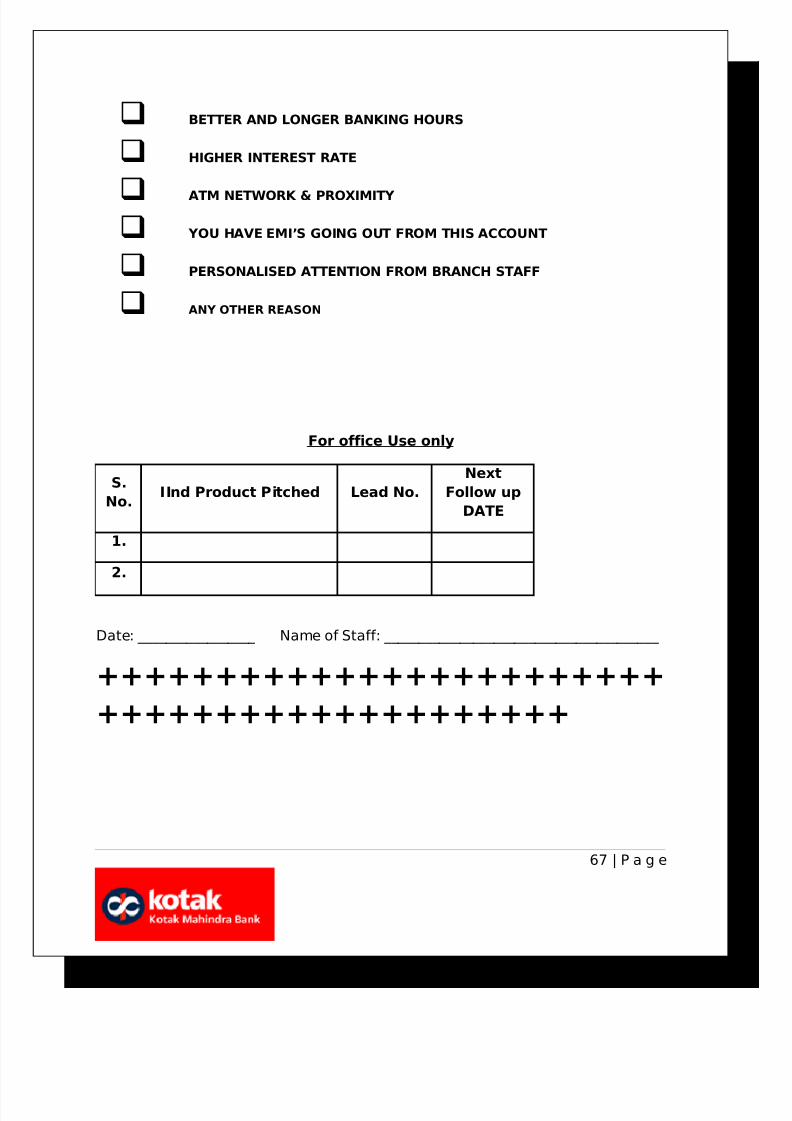

Other Relationship FD KIDS A/C INSURANCE MF

63 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 64/72

• RANK THE BELOW REASONS FOR CHOOSING YOUR BANK ACCOUNT INORDER OF YOUR PREFERENCE (RANK THEM 1 – 10)

BRAND NAME

BRANCH NETWORK

PRODUCTS AND FACLITIES AVAILABLE

PROXIMITY TO HOME/OFFICE

HIGHER INTEREST RATE

ATM NETWORK

MINIMUM BALANCE REQUIREMENT

CHARGES

QUALITY AND ACCESS OF DEBIT CARDS

ANY OTHER REASON

•ARE YOU AWARE OF DE-REGULATION OF SAVINGS BANK INTERESTRATES?

YES NO

• HOW DID YOU COME TO KNOW ABOUT ITNEWSPAPER ADVERTISEMENT TELEVISION

• DO YOU THINK THAT HIGHER INTEREST ALONE CAN BE THE SOLE REASONTO CHANGE BANK ACCOUNT

YES NO

For official Use only

64 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 65/72

S.

No.Product Pitched Lead No.

Next Follow up

DATE

1.

2.

Date: _________________ Name of Staff: _________________

++++++++++++++++++++++++

++++++++++++++++++++

EXISTING CUSTOMER SURVEY DETAILS

Name ( Mr./Mrs. ) _______________________________________________

Occupation _______________________________________________

Account No. _______________________________________________

Mobile # _______________________________________________

E Mail Address _______________________________________________

Residence: OWNED RENTED

Vehicle Owned: SUV CAR BIKE

Spouse Name ( Mr./Mrs. ) _______________________________________________

No of Children _____________________________________________

Age of Children 1)________ 2)________ 3)_______

Does your spouse have an account with the Bank already ? YES NO

Does your children have an account with the Bank already ? YES NO

65 | P a g e

7/31/2019 Project for Sip (1)

http://slidepdf.com/reader/full/project-for-sip-1 66/72

Other Relationship FD KIDS A/C INSURANCE MF

• ARE YOU AWARE OF DE-REGULATION OF SAVINGS BANK INTEREST

RATES? YES NO

• HOW DID YOU COME TO KNOW ABOUT ITNEWSPAPER MAGAZINE ADVERTISEMENT TELEVISION