Embed Size (px)

Citation preview

Project Financial Statements & Project Financial Statements & Quarterly ReportsQuarterly Reports

Feb. 2012

IntroductionIntroductionIntroductionIntroduction

Project Accounting and Audit procedures should be based on best market

practice as per IFAD underlying guidelines. These provide accountability

and credibility as to use of funds

IFAD guidelines require all projects to maintain accounts & records

(separately or within a basket fund)

These accounts should be audited by an independent auditor on an

annual basis within a set timeframe (normally 6 months)

Where possible, national systems should be used

IFAD has a fiduciary role to ensure that its funds are used for the purpose for which intended

2

Project Financial Statements (PFS)Project Financial Statements (PFS)Project Financial Statements (PFS)Project Financial Statements (PFS)

ObjectiveObjective

• To provide information about the financial position, performance and resource flows of a project

Basis of PreparationBasis of Preparation

• Prepared in accordance with:– International Financial Reporting Standards (IFRS) (www.ifrs.org)

– International Public Sector Accounting Standards (IPSAS) (accruals or cash basis) (www.ipsas.org)

– National standards, if minimum disclosures are provided

• These standards define what & how to report

• Cash (when money is actually spent/ received) or accruals (when legal commitment incurred irrespective of cash) basis, as long as consistently applied

3

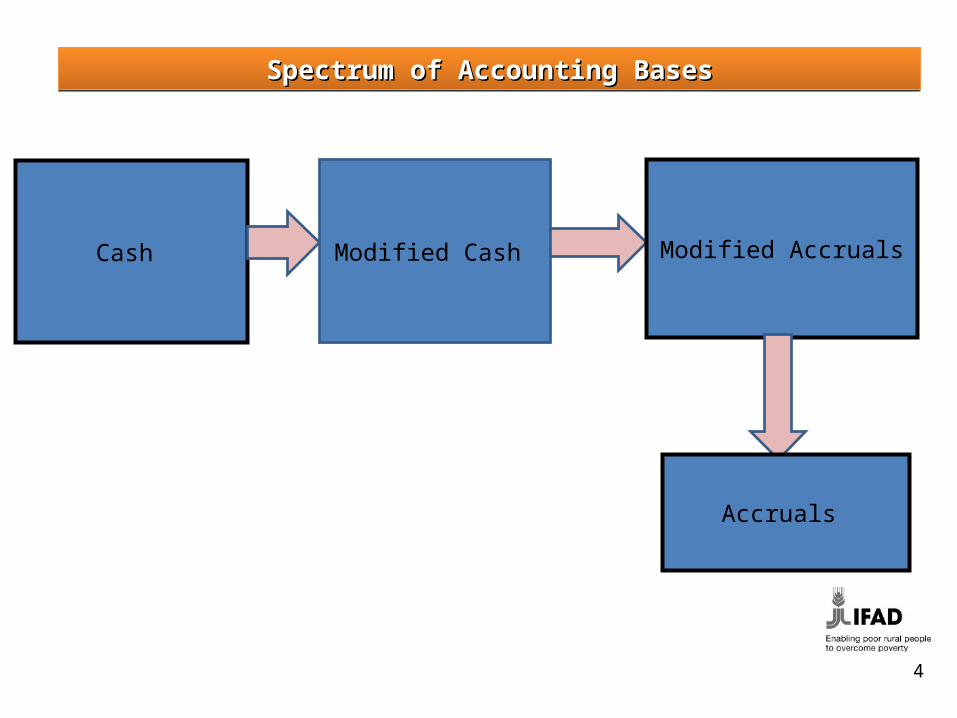

Spectrum of Accounting BasesSpectrum of Accounting BasesSpectrum of Accounting BasesSpectrum of Accounting Bases

Cash Modified Cash Modified Accruals

Accruals

4

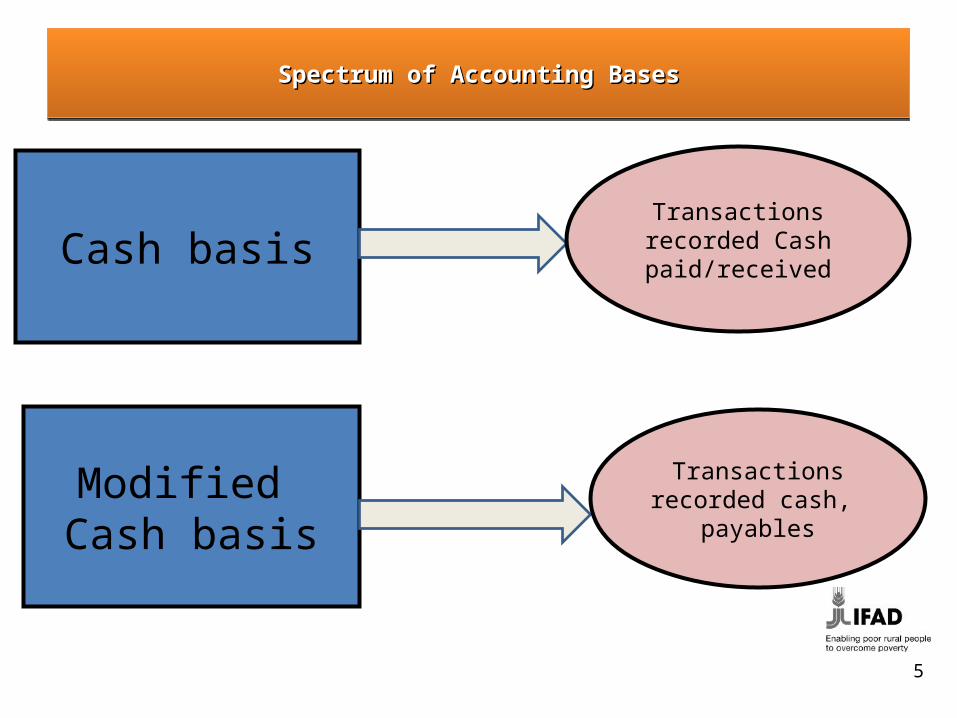

Spectrum of Accounting BasesSpectrum of Accounting BasesSpectrum of Accounting BasesSpectrum of Accounting Bases

Cash basisTransactions recorded

Cash paid/received

Modified Cash basis

Transactions recorded cash, payables

5

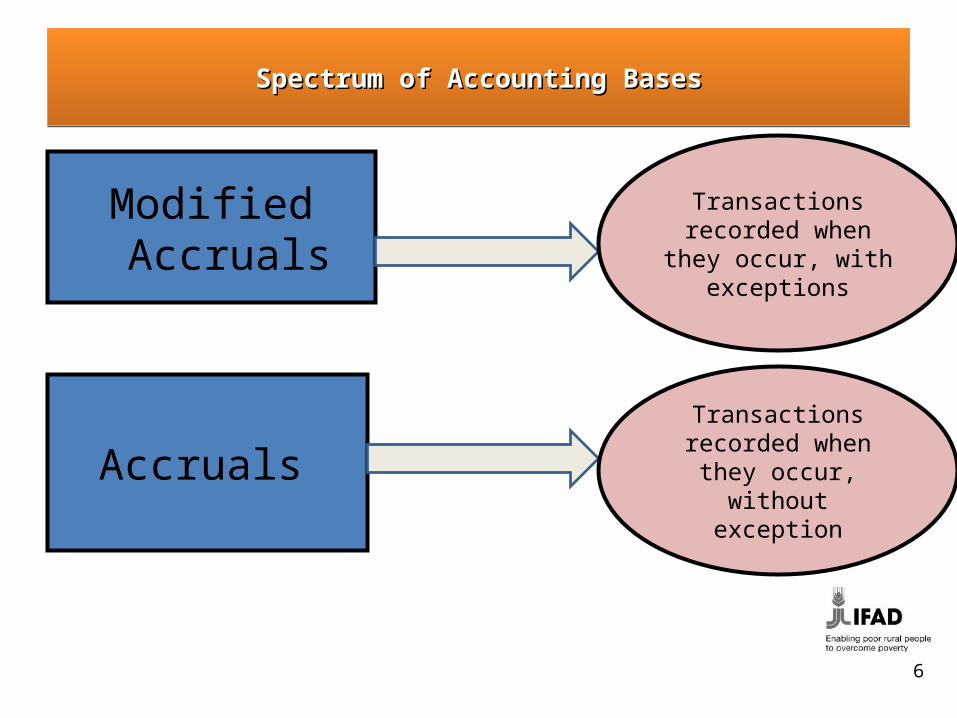

Spectrum of Accounting BasesSpectrum of Accounting BasesSpectrum of Accounting BasesSpectrum of Accounting Bases

Modified Accruals

Accruals

Transactions recorded when they occur, with

exceptions

Transactions recorded when they occur, without exception

6

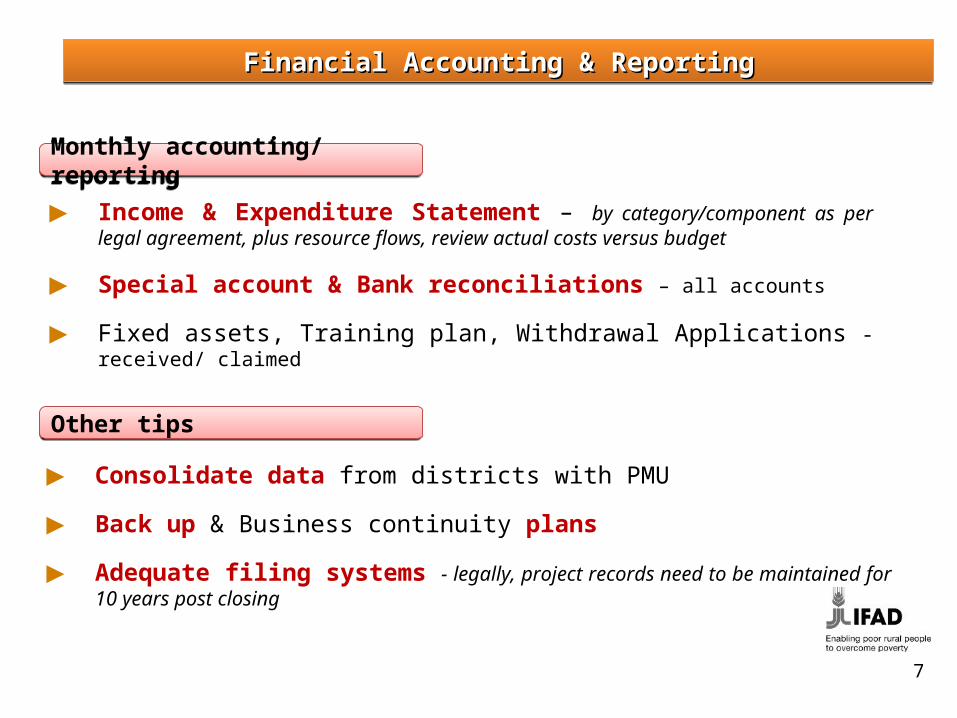

Financial Accounting & ReportingFinancial Accounting & ReportingFinancial Accounting & ReportingFinancial Accounting & Reporting

► Income & Expenditure Statement – by category/component as per legal agreement, plus resource flows, review actual costs versus budget

► Special account & Bank reconciliations – all accounts

► Fixed assets, Training plan, Withdrawal Applications - received/ claimed

Monthly accounting/ reportingMonthly accounting/ reporting

Other tipsOther tips

► Consolidate data from districts with PMU

► Back up & Business continuity plans

► Adequate filing systems - legally, project records need to be maintained for 10 years post closing

7

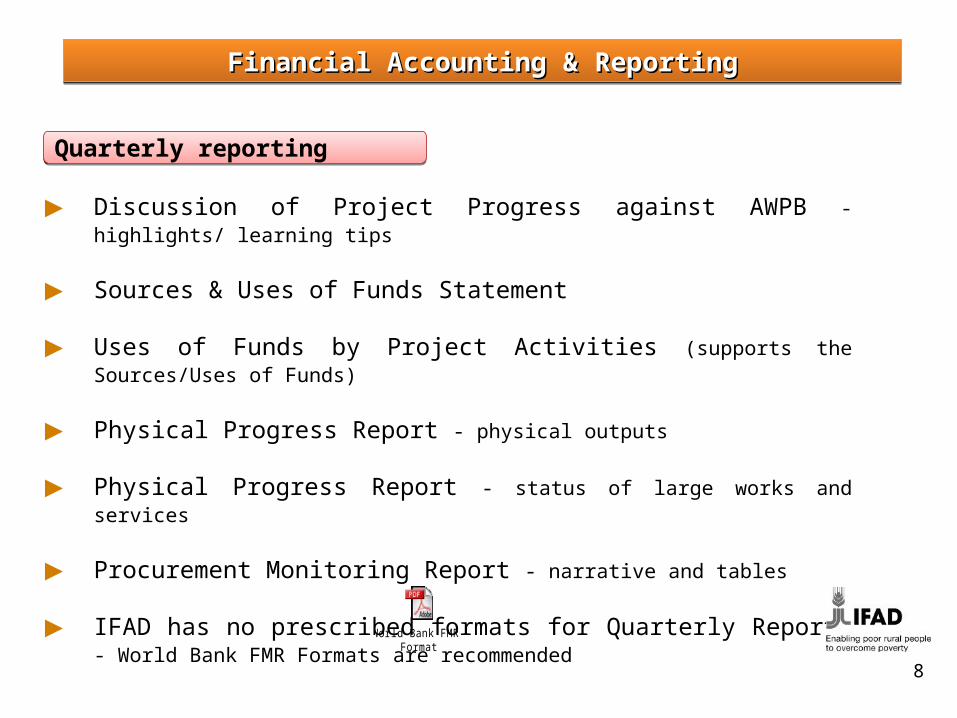

Financial Accounting & ReportingFinancial Accounting & ReportingFinancial Accounting & ReportingFinancial Accounting & Reporting

► Discussion of Project Progress against AWPB - highlights/ learning tips

► Sources & Uses of Funds Statement

► Uses of Funds by Project Activities (supports the Sources/Uses of Funds)

► Physical Progress Report - physical outputs

► Physical Progress Report - status of large works and services

► Procurement Monitoring Report - narrative and tables

► IFAD has no prescribed formats for Quarterly Reports - World Bank FMR Formats are recommended

Quarterly reportingQuarterly reporting

World Bank FMR Format

8

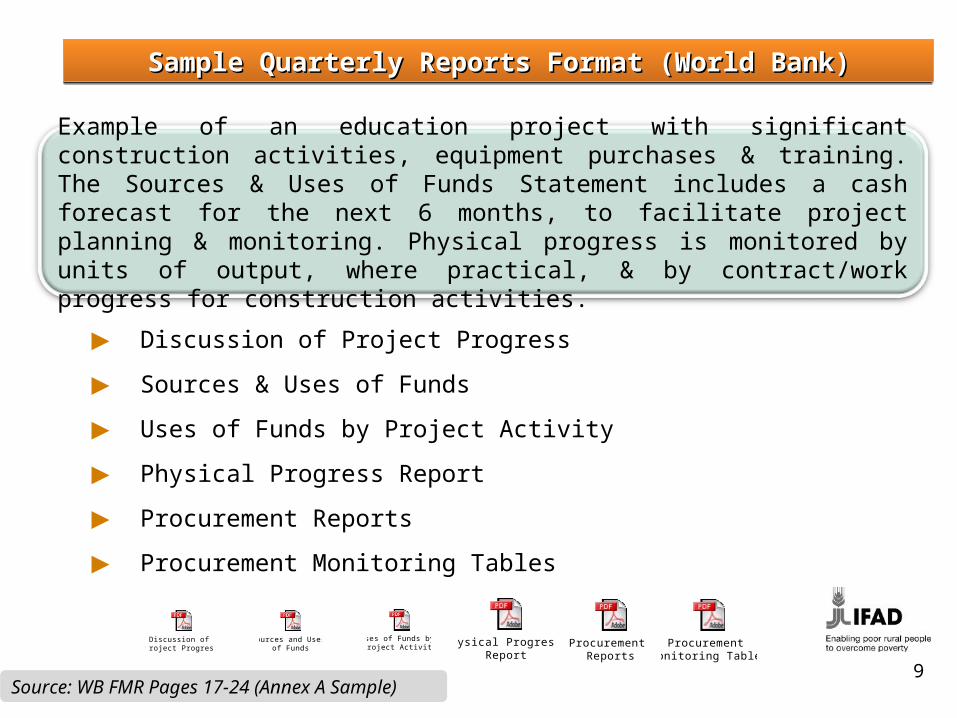

Example of an education project with significant construction activities, equipment purchases & training. The Sources & Uses of Funds Statement includes a cash forecast for the next 6 months, to facilitate project planning & monitoring. Physical progress is monitored by units of output, where practical, & by contract/work progress for construction activities.

► Discussion of Project Progress

► Sources & Uses of Funds

► Uses of Funds by Project Activity

► Physical Progress Report

► Procurement Reports

► Procurement Monitoring Tables

Source: WB FMR Pages 17-24 (Annex A Sample)

Discussion of Project Progress

Sources and Uses of Funds

Uses of Funds by Project Activity

Physical Progress Report

Procurement Reports

Procurement Monitoring Tables

Sample Quarterly Reports Format (World Bank)Sample Quarterly Reports Format (World Bank)Sample Quarterly Reports Format (World Bank)Sample Quarterly Reports Format (World Bank)

9

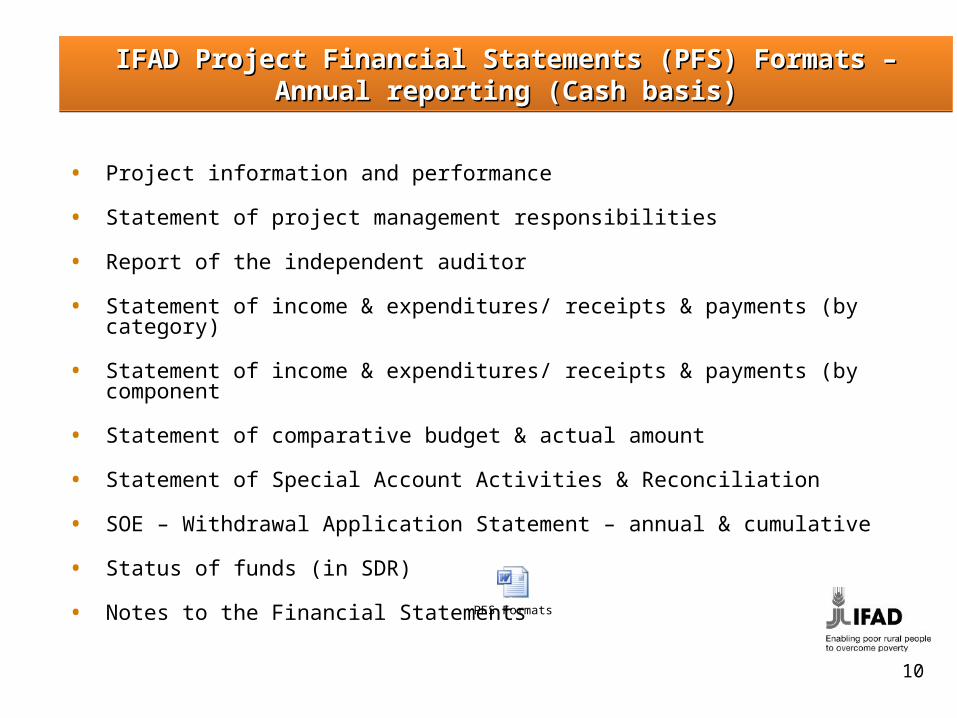

• Project information and performance

• Statement of project management responsibilities

• Report of the independent auditor

• Statement of income & expenditures/ receipts & payments (by category)

• Statement of income & expenditures/ receipts & payments (by component

• Statement of comparative budget & actual amount

• Statement of Special Account Activities & Reconciliation

• SOE – Withdrawal Application Statement – annual & cumulative

• Status of funds (in SDR)

• Notes to the Financial Statements

IFAD Project Financial Statements (PFS) Formats – Annual reporting IFAD Project Financial Statements (PFS) Formats – Annual reporting (Cash basis)(Cash basis)

IFAD Project Financial Statements (PFS) Formats – Annual reporting IFAD Project Financial Statements (PFS) Formats – Annual reporting (Cash basis)(Cash basis)

PFS Formats

10

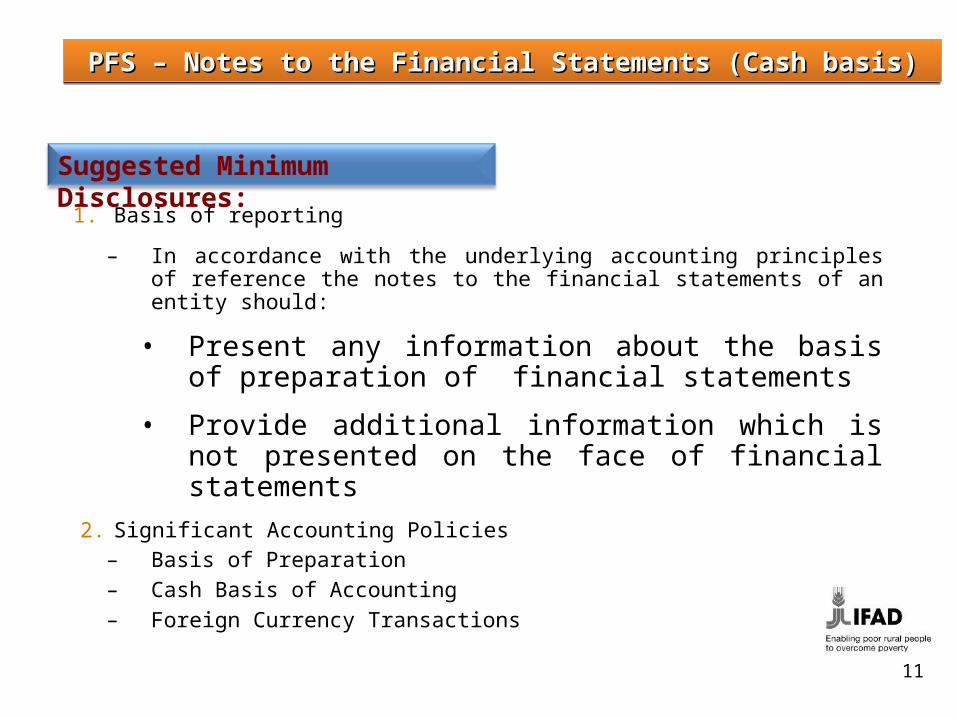

1. Basis of reporting

– In accordance with the underlying accounting principles of reference the notes to the financial statements of an entity should:

• Present any information about the basis of preparation of financial statements

• Provide additional information which is not presented on the face of financial statements

2. Significant Accounting Policies– Basis of Preparation – Cash Basis of Accounting – Foreign Currency Transactions

PFS – Notes to the Financial Statements (Cash basis)PFS – Notes to the Financial Statements (Cash basis)PFS – Notes to the Financial Statements (Cash basis)PFS – Notes to the Financial Statements (Cash basis)

Suggested Minimum Disclosures:

11

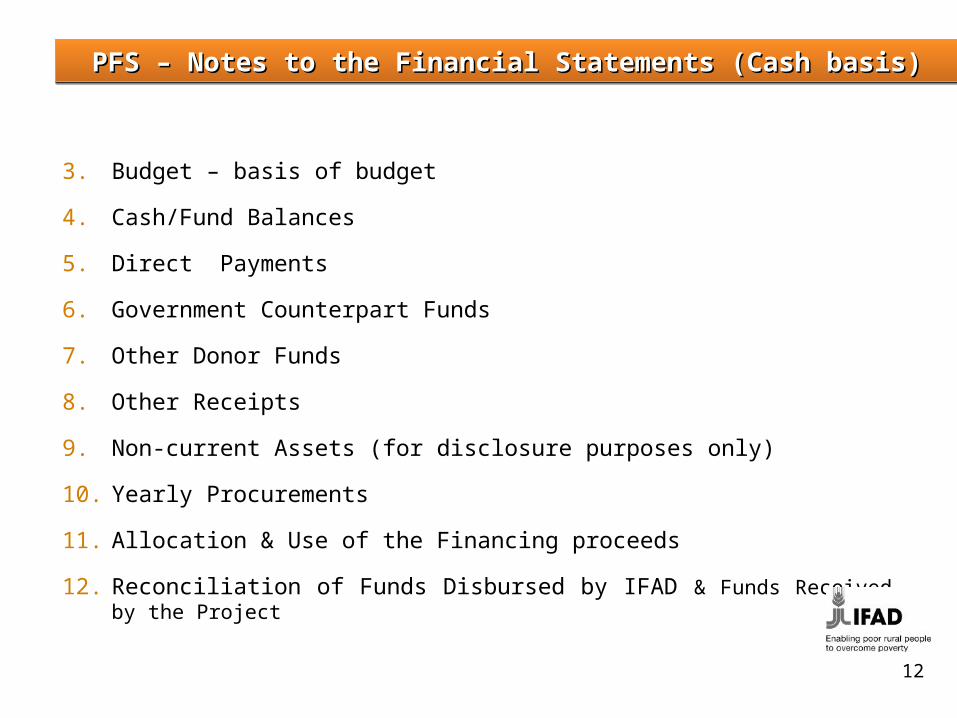

3. Budget – basis of budget

4. Cash/Fund Balances

5. Direct Payments

6. Government Counterpart Funds

7. Other Donor Funds

8. Other Receipts

9. Non-current Assets (for disclosure purposes only)

10. Yearly Procurements

11. Allocation & Use of the Financing proceeds

12. Reconciliation of Funds Disbursed by IFAD & Funds Received by the Project

PFS – Notes to the Financial Statements (Cash basis)PFS – Notes to the Financial Statements (Cash basis)PFS – Notes to the Financial Statements (Cash basis)PFS – Notes to the Financial Statements (Cash basis)

12

Accrual basis of accountingAccrual basis of accountingAccrual basis of accountingAccrual basis of accounting

“The IPSASB encourages governments to progress to the accrual basis of accounting and to harmonize national requirements with the IPSASs prepared for application by entities adopting the accrual basis of accounting.” IPSASB

13

Accrual basis of accountingAccrual basis of accountingAccrual basis of accountingAccrual basis of accounting

“Accrual accounting was created to fill textbooks since it is more complicated than cash accounting” -CPA Student

14

Highlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual Accounting

FINANCIAL STATEMENTS

1.Statement of Operating performance replaces statement of receipts and Payments

2.Balance Sheet reflecting project assets, liabilities and sources of financing

3.Statement of Cashflows

4.Additional disclosures in Notes to the Accounts

15

Highlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual Accounting

STATEMENT OF OPERATING PERFORMANCE

Recognise income when earned, i.e WA approved by IFAD, NOT when funds are received by project.

Recognise expenses when incurred, i.e when billed to the project, NOT when paid.

Disclose income and expenses by category and component, same as cash basis

16

Highlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual Accounting

• BALANCE SHEET Recognise advances and prepayments as current assets in

the balance sheet e.g in cases of replenishment of pre-financed expenditure

Recognise Fixed assets at historical cost or re-valued amount, less depreciation and impairment losses

Recognise payables as current and non current liabilities (due after one year)

Recognise IFAD funds received in advance as deferred income (e.g in cases of disbursement by revolving fund)

17

Highlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual AccountingHighlights of Project Accrual Accounting

STATEMENT OF CASH FLOWSAdjustments to recoincile net cash to surplus/deficit

Changes in working capital

Cashflows from investing activities

Cashflows from financing activities

Template Accrual financial statements

18

Benefits to IFAD Project OperationsBenefits to IFAD Project OperationsBenefits to IFAD Project OperationsBenefits to IFAD Project Operations

Identifies project risks such as credit risk in projects with significant credit components, e.g in microfinance where project funds are advanced to beneficiaries

Identifies cross debts/commingling of donor/counterpart funds since balance sheet has sources of financing

Counterpart finances i.e tax exemptions can be accounted for even when no cash is paid out.

Analytical review of balance sheet items provides useful information for risk analysis.

19

Accounting Software for IFAD Projects Accounting Software for IFAD Projects Accounting Software for IFAD Projects Accounting Software for IFAD Projects

Expenditure by components & categories per legal agreement

Expenditure by Financier

Ability to print Financial Statements according to Govt/IFAD/IPSAS accounting policy

Advances utilisation by Service Providers & staff duly aged to facilitate follow-up

Bank balances held by service providers

Commitments beyond actual billings/ invoices

Budgetary control information to ensure expenditures do not exceed set limits

Bank reconciliation using the system

Receivables in form of replenishment applications in transit & any refunds that may be due from Government

Withdrawal application form automatically produced by the system

Contract & Procurement plan monitoring

Capacity Analysis

20