Embed Size (px)

Citation preview

Programme

Symposium: The Prospects of E-Mobility in Karachi

Arrival of guests : 0930

hrs

Guests to be seated : 0945

hrs

Recitation from the Holy Quran : 1000

hrs

Welcome Address by the President PAE : 1005

hrs

PRESENTATIONS

1. The Public & Private Transport System

in Karachi by Mr. Ijaz Hussain Khilji : 1015

hrs

Discussion by the Participants : 1045

hrs

2. The Cost of Traffic Congestion for Karachi

by Prof. Dr. Mir Shabbar Ali : 1100

hrs

Discussion by the Participants : 1115

hrs

3. International Scenario of Electric Road

Vehicles by Dr. Nasim A. Khan : 1120

hrs

Discussion by the Participants : 1150

hrs

4. The Ultimate Solution

by Dr.-Ing. Jameel Ahmad Khan : 1205

hrs

Discussion by the Participants : 1235

hrs

Concluding Observations : 1250

hrs

Lunch : 1300

hrs

PAKISTAN ACADEMY OF ENGINEERING

EDITOR. PROF DR NASIM A. KHAN

A REPORT

ON PAE

SYMPOSIUM

HELD ON

DECEMBER20, 2014

PROSPECTS OF

E-MOBILITY

IN KARACHI

ISLAMIC REPUBLIC OF

PAKISTAN

1

A REPORT

ON

PAKISTAN ACADEMY OF ENGINEERING

SYMPOSIUM

PROSPECTS OF E-MOBILITY IN KARACHI CITY,

ISLAMIC REPUBLIC OF PAKISTAN

held on December 20, 2014

The President; Pakistan Academy of Engineering is Ex Vice Chancellor of NED University of

Engineering & Technology, Karachi The Author-1 is an Ex- Managing Director, Karachi Urban Transport Corporation. Author-2 is Chairman of Department of Urban & transportation Engineering, NED University

of Engineering & Technology, Karachi Author-3 is Senior Executive Director at Osmani & Company (Pvt) Ltd, Ex Vice Chancellor of Hamdard University, Karachi and Ex Vice Chancellor of Nazeer Hussain University, Karachi Author-4 is The President Pakistan Academy of Engineering

Including

Address of President of Pakistan Academy of Engineering

Prof. Dr.-Ing. Jameel Ahmad Khan

Papers presented by

The Public & Private Transport System in Karachi by Ijaz Hussain Khilji The Cost of Traffic Congestion for Karachi by Prof Dr Mir Shabbar Ali

International Status of E- Mobility by Prof Brig. Dr. Nasim A. Khan

The Ultimate Solution by Prof. Dr.-Ing. Jameel Ahmad Khan

and

Recommendations of the Symposium

Pakistan Academy of Engineering

2

Address of the President, Dr. –Ing. Jameel Ahmad Khan

Honourable guests and my dear fellow engineers. Assalamo Alaikum 1. We are grateful that you very kindly agreed to grace this occasion. It is the first Symposium to address one of the Ten Grand Challenges that we have identified to be addressed by the engineering community. You may visit the subjects of our future symposia listed on our website (http://www.pacadengg.org). The Pakistan Academy of Engineering is a LEARNED SOCIETY and acts as a THINKING LABORATORY. 2. Ladies and gentlemen, I on behalf of the Pakistan Academy of Engineering heartily welcome you on this occasion and express my profound gratitude for your participation. Karachi with a population of almost 20 million is struggling to have a sustainable public and private transport system. This is the most pressing problem of the citizens, who are under extreme distress. Is there a solution, which the latest technologies can deliver? Let us examine the proposition. Mobility is one of human being’s fundamental desires, as well as necessity. It is likely to expand further in the future with the progress of the world economy. Transport consumes about one fourth of the total world energy. It has been recognized internationally that the future of humanity lies in de-carbonizing the transport system radically. According to the statistics released by the Government of Pakistan, the total Primary Energy Supplies amounted to 64.588 million tons of oil equivalent (TOE) in the year 2012-13 as shown in Figure-1 & Figure-2. The Transport Sector is supposed to have consumed 12.713 million TOE i.e. 19.68% of the total Primary Energy Supplies as shown in Figure-3. Petroleum products accounted for 10.368 million TOE and Gas 2.345 million TOE. Road transport alone shared 12.23 million TOE i.e. 18.94% of the total Primary Energy Supplies.

Pakistan Academy of Engineering

3

Figure-1: Energy Flow Chart 2012-13 [Source: Pakistan Energy Year Book 2013]

Figure-2: Primary Energy Supplies by Source [Source: Pakistan Energy Year Book 2013]

Pakistan Academy of Engineering

4

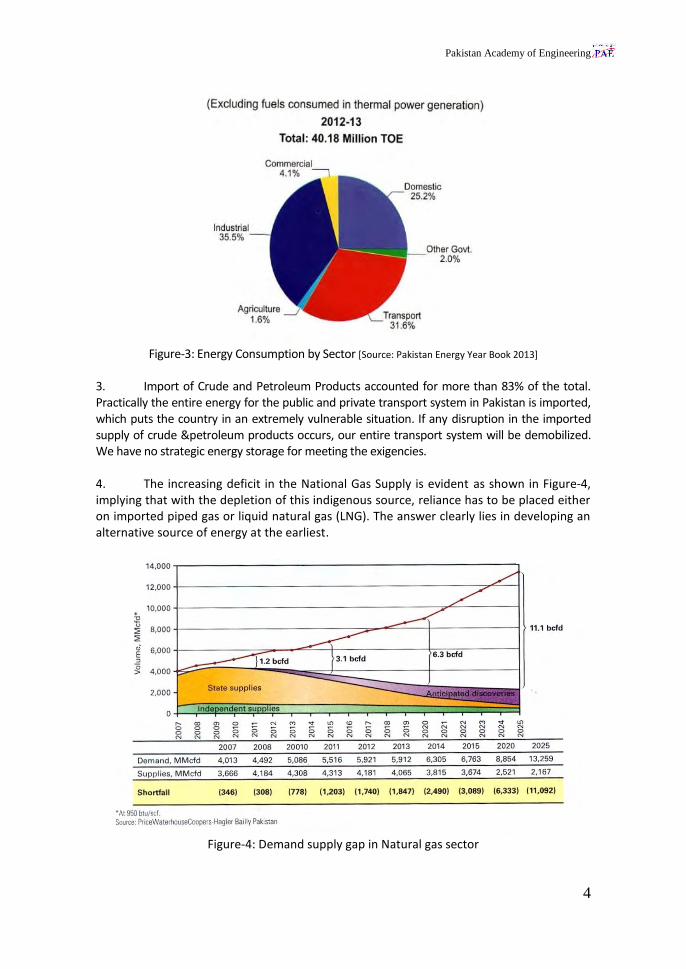

Figure-3: Energy Consumption by Sector [Source: Pakistan Energy Year Book 2013]

3. Import of Crude and Petroleum Products accounted for more than 83% of the total. Practically the entire energy for the public and private transport system in Pakistan is imported, which puts the country in an extremely vulnerable situation. If any disruption in the imported supply of crude &petroleum products occurs, our entire transport system will be demobilized. We have no strategic energy storage for meeting the exigencies. 4. The increasing deficit in the National Gas Supply is evident as shown in Figure-4, implying that with the depletion of this indigenous source, reliance has to be placed either on imported piped gas or liquid natural gas (LNG). The answer clearly lies in developing an alternative source of energy at the earliest.

Figure-4: Demand supply gap in Natural gas sector

Pakistan Academy of Engineering

5

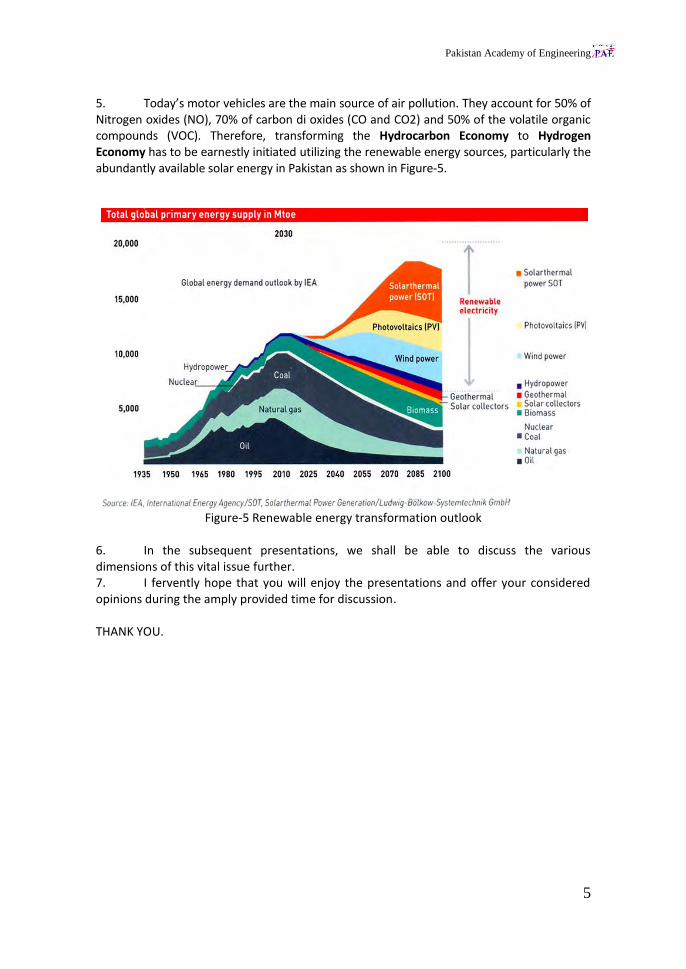

5. Today’s motor vehicles are the main source of air pollution. They account for 50% of Nitrogen oxides (NO), 70% of carbon di oxides (CO and CO2) and 50% of the volatile organic compounds (VOC). Therefore, transforming the Hydrocarbon Economy to Hydrogen Economy has to be earnestly initiated utilizing the renewable energy sources, particularly the abundantly available solar energy in Pakistan as shown in Figure-5.

Figure-5 Renewable energy transformation outlook

6. In the subsequent presentations, we shall be able to discuss the various dimensions of this vital issue further. 7. I fervently hope that you will enjoy the presentations and offer your considered opinions during the amply provided time for discussion. THANK YOU.

Pakistan Academy of Engineering

6

THE PUBLIC & PRIVATE TRANSPORT SYSTEM IN KARACHI Ijaz Hussain Khilji

1 1. INTRODUCTION Travelling the distance has always been the necessity as well as ambition of mankind. Since the greatest invention – the wheel – human mobility has transformed from animal driven carts to steam and oil engines – moving onwards to jets and virtual movement in cyber space. The mobility however has been singularly dependent on development of pathways in the shape of dirt roads, fixed and flexible pavements, highways and eventually the air ways. The desire of mankind to create most efficient tools and means of travel has overtime given rise to most complex road and air networks facilitating commute and communication. The movement of knowledge, skills and physical transportation of teeming millions along with cascading incremental cargos has put enormous pressure on the ever crumbling communication infrastructure. The demands of a globalized world for seamless transportation of men and cargo have thrown challenges of unparallel dimensions to the planners, social scientists and engineers around the world. The big cities and metropolitans bursting at seams with population pressure are struggling hard to keep pace with the rapidly increasing requirements of road infrastructure. The ghost of ill planned and uncontrolled urbanization is visibly manifested in traffic jams, higher numbers of road accidents and virtual brocade of much desired efficient mobility. In particular, the developing economies and emerging markets like Pakistan are the worst hit. The gap between resources and requirements need imaginative efforts and planning. The city of Karachi from a population of 357,000 at the time of independence in the year 1947 has grown exponentially and at present, is estimated to be around 20 million and is expected to be 35 million by the year 2030. The urbanization of the city coupled with various industrial centers i.e. SITE, KITE, LITE, PQA and other small industrial zones spread over in the city of Karachi in a formal and informal manner, requires considerable work force, obviously causing manifold increase in the commuters and vehicles on the road. The socio economics status of Karachi is shown in slide # 2, the existing population and projected growth of population is shown in slide # 3, whereas the Urban Sprawl from 2005 to 2015 is shown in slide # 4, the growth of population in Karachi as estimated by JICA in their study Karachi Transport Improvement Plan (KTIP # 2012) is shown in slide # 5, to cater for growth in population, the planned Urban development projects are shown in slide # 6. However, this has not been matched with an appropriate master plan to provide an efficient transport system, leading to traffic congestion, more travel time, accidents, and environmental & social issues. Efforts have been made to cope with the increased traffic on road by providing detours, one-ways, flyover, expressways, road-widening, traffic education, new rules and heavy fines – racing against ever-growing operational demands the city thirsts for long-term solutions. Unable to fully handle the gush of heterogeneously jostling traffic, the arteries start getting blocked at vital points and the effect can be felt in every aspect of the city’s industrial, professional and personal life. It has snowballing negative effect on work, productivity, family bonds, health, happiness, environment and quality of living is hard to control. As cities grow physically and humanly, the load of vehicular trips on the road system also goes up and when the traffic level of any travel corridor in one direction exceeds 10,000 persons per hour it calls for a pragmatic policy shift towards encouraging the introduction of a Mass Transit System. The overview of transport sector i.e. Transportation of public vehicles are reflected in slide # 7, 8, 9& 10 whereas the Modal distribution of vehicle is shown in slide # 11. The vehicle ownership by town is shown in slide #

1 Mr Ijaz Hussain Khliji was Ex- Managing Director, Karachi Urban Transport Corporation

Pakistan Academy of Engineering

7

12, whereas the Nos. of vehicles registered and growth rate of same is shown in slide # 13.It can be seen that present percentage of ownership of public vehicles will increase to 16%,if Mass Transit Program is not implemented. Consequently the travel time will also increase and the pollution will also increase, as referred in slide # 14& 15. The aforesaid increase in population and vehicles are posing great threat and challenges which are reflected in slide # 16, 17 & 18.Therefore the immediate provision for a Mass Transit System i.e. vehicles with large carrying capacity, moving at higher speed, short intervals, and affordable fare level are shown pictorially in slide # 20. 2. HISTORY OF MASS TRANSIT The city of Karachi had a Mass transit System in the shape of Tramways, almost covering the old city of Karachi, in combination with an efficient bus operation. The Tramways were abandoned in the year 1975 due to increase in the vehicular traffic, leading to denial of accessibility of Right-of-Way to trams. The first master plan of the city of Karachi was prepared in the year 1952 by Swedish consultants MRVP who had recommended the provision of a mass transit in the shape of Karachi Circular Railway. In late 1950’s the planning and construction of KCR was undertaken by the railway management and KCR was commissioned in November 1964 and extended in 1970, having the route length of 43.1kmswith 14 stations and was highly patronized which is evident from the fact that in the year 1984, 104 trains were operating on the system. But due to lack of continued investment in KCR, the operating efficiency was marginalized resulting in long running time, frequent break downs, cancellation of trains leading to loss of ridership, thereby the number of Trains was gradually reduced and eventually KCR was closed for traffic in January 2000. The Karachi Mass Transit Study (KMTS) was commissioned under the World Bank funding in 1987. The study recommended an 87 km network of elevated and at grade transit ways to be initially used a bus ways and later to be converted to a light rail system around year 2000. The project could not be implemented due to financial constraints. 3. WHAT IS A METRO? Mass Transit System is normally synonymous with the word ‘Metro’. A ‘Metro’ can perhaps be best defined as a high-frequency, urban, Mass Rapid Transit System that operates totally independent from other modes of traffic. It can be underground, at-grade, elevated or a combination of any of the above. According to German Metro enthusiast Robert Schwandl, Steel Wheels, Rubber Tires, Double-rail, Monorail, Overhead Wire Electrification, Third Rail Power Supply, Narrow Gauge, Standard Gauge, Broad Gauge, Automatically-driven, Driver-driven… a ‘Metro’ can be based on a combination of any of the above systems. It doesn’t necessarily use heavy rail technology and that’s why some famous urban light rail systems that meet a metro’s generally accepted operating parameters are sometimes included in metro listings. SOME CHARACTERISTICS OF METRO: High acceleration Deceleration Close inter station distances Closed door High safety levels Pre boarding ticketing Intermodal connectivity Air conditioned Convenient access 4. STATUS OF PUBLIC AND PRIVATE TRANSPORT IN KARACHI In developed countries, the planning for a Mass Transit System generally starts when the city population crosses the one million mark. The system is in position by the time the city population

Pakistan Academy of Engineering

8

is two to three million and when the population exceeds four million or so, planned extensions to the Mass Rapid Transit Systems are vigorously initiated. Metro lines are not just for affluent countries. They are a necessity for any large city, to provide mobility to its people. Cities in Europe have an average 38-kms of metro rail per million populations. The corresponding figure in Asia and North America is 10 kms and 23 kms respectively, whereas world average is 19 kms. The demand analysis shows that road development in the master plan is not enough to reduce the projected traffic congestion in Karachi. In order to improve the traffic situation in the future, it is necessary to construct mass transit system. Karachi Circular Railway (KCR) will contribute to provide better transport in the center of the city, but it is proposed that the line should be extended to east because the future demand in Bin Qasim is expected to be very high. The demand analysis shows that the traffic demand will be high not only in radial directions including Tower – Super Highway, but also the corridor along Rashid Minhas Road. Railway systems are proposed for the two corridors. The growth of Karachi towards West and North East can be catered for by the provision of six BRT corridors as suggested in KTIP Plan prepared by JICA in 2012. 5. TRAVEL TIME COST 5.1 Revived KCR Project Provision of Mass Transit System reduces the travel time of the mobility of the commuters and results in saving of man-hours. In the case of revival of KCR Project the difference of travel time between road transport and revived KCR has been calculated on the basis of the speed of both the modes and the projected ridership of KCR. The annual saving will be PKR 5.110 Billion. As shown in slide # 14. 5.2 Provision of BRT The BRT project will bring about economic benefit such as travel time reduction for BRT passengers, vehicle operating cost reduction, and vehicle emission reduction. On the other hand, the project will cause negative impact on road traffic. Since existing bus passengers will use the BRT, and the system will reach its capacity by them, shift from car users to BRT system will not be large enough to compensate the reduction in the number of lanes. However, the project is economically feasible. The average travel time of minibuses is approximately 17km/h in Karachi. The travel speed of BRT is expected to be 33km/h on average. The benefits of time saving due to increase in speed are marginalized due to the following reasons: i. Lanes of carriage way for vehicular traffic will be reduced by BRT where the width of median is not wide enough for BRT lines, which will reduce the capacity of road and increase the travel time. ii. The average speed in peak hours along the BRT corridors is assumed as 33 km/h which will be reduced to 29.7 km/h [90%] iii. Delay at the Intersection of BRT. The BRT Project will change the signal free corridor to a signalized road for BRT operations, which will cause a delay at signalized intersection. Delay at intersection depends on the capacity and traffic volume. However, the average delay per vehicle at an intersection has been assumed as 40 seconds in the KTIP Study by JICA. 6. AIR & NOISE POLLUTION DUE TO INCREASE VEHICULAR EMISSIONS Karachi city’s air quality is one of the poorest in the world, with levels exceeding WHO guidelines. A major contributor to this pollution and generation of green-house gases (GHG) is the transportation sector, especially from an aging fleet of vehicles in poor mechanical condition and low levels of fuel efficiency. The high levels of sulphur in an automotive diesel (0.5% -1%) is seen as a major contributor to sulphur dioxide (SO2) and particulate matter (PM10) in ambient air. i. According to the Pakistan Environmental Protection Agency (PEPA), a major share of the emission load from motor vehicles in urban areas can be attributed to a relatively small

Pakistan Academy of Engineering

9

number of smoky diesel and 2-stroke (rickshaws) vehicles. Traffic congestion affects average speed of vehicles and consequently fuel consumption and greenhouse gases. ii. The environmental damage costs associated with urban air pollution are equivalent to 1% of GDP, as stated in one of the World Bank reports. iii. Particularly, at health risk are those living within a quarter of a mile of high-volume roads (those carrying 10,000 – 20,000 vehicles per day) and those living near roads with a large amount of truck traffic. iv. Noise pollution from vehicles, especially in residential areas, is above recommended levels. iv. Major contributors to the noise pollution are frequent and indiscriminate use of vehicle horns, removal of silencers on rickshaws and other 2-stroke vehicles, high volumes of traffic especially heavy vehicles. 6.1 Environmental Considerations in KCR The Revival of KCR Project is environment friendly as it is based on electric traction. It will result in estimated exhaust reduction of 44,584 ton / year for minibus and 1,342 ton per /year for bus and value of annual reduction is estimated at US$ 1.286 Billion per year as of 2023. 7. ISSUES AND CHALLENGES 7.1 Low Capacity of Bus Service Most mega-cities, like Karachi in developing countries suffer from a large number of small buses (minibus) which cause serious congestion in the center of these cities. Usually, introduction of a mass transit system can be justified from the huge demand in public transport in these cities. Karachi is an exception. The number of bus fleets is decreasing while the traffic demand is increasing with rapid population growth, city expansion,and economic growth. Rapid increase in private cars cannot explain the reason because car is still expensive in Pakistan and there still remains huge population who cannot afford to buy a private car. The number of minibuses and coaches are restricted while introduction of standard size buses has failed. Bus service in Karachi is having severe strain, due to increase in vehicle operating cost. The operators are therefore not bringing in new buses nor maintaining the existing fleet in a proper condition. 7.2 Improper Bus Routes The majority of the bus services concentrate on radial directions except the major circular route such as Rashid Minhas Road. Bus routes are designed to provide the service between major origin and destination through high demand routes, and the preferable routes for bus operators are busy while the bus service along non-popular routes is poor. There is no hierarchy of bus network, or trunk and feeder system. From this, passengers need to transfer their buses to reach their destination. Since there is no fare integration, passengers need to pay the fare for every transfer. 7.3 Poor Road Network Road network in Karachi has been significantly improved in recent years by construction of flyovers and underpasses. From this, traffic capacity problem is small at present. However, there are some network problems relating to urban structure. For example, the access, to and from Korangi Industrial Area is inconvenient because there are few access routes over Malir River. 7.4 Traffic Congestion Traffic congestion is one of the serious problems especially in the center of the city. A lot of traffic signals are installed at intersections in the down-town area compared to the suburban area. However, at very busy intersections, traffic is controlled by traffic police in peak hours due to the inefficacy of the signals provided therein.

Pakistan Academy of Engineering

10

7.5 Demand-Supply Gap of Parking Space The capacity of public parking is very small compared to the demand in roadside parking. This needs to be improved by the provision of parking plazas and restricted parking on the streets. 7.6 Lack of Proper Traffic Enforcement In Karachi, passenger riding on bus roof top is very popular and observed everywhere although it is prohibited. Double parking and other illegal parking are overlooked without proper enforcement. Due to lack of enough transport services; the violations occur and it is very difficult to fully regulate violations of traffic rules, problems in transport sector are complex and related to each other. 8. OPTIONS The aim for an efficient and effective Mass Transit System is to provide vehicles with large carrying capacity, operating at high frequency for the mobility of maximum number of passengers in shortest possible time. This can be achieved by providing a combination of Bus Rapid Transit (Metro-Bus), Trams, Metro-Rapid Transit (MRT), Subways, Suburban Rail System etc. 8.1 Underground Metro Rail This is an ideal system for providing mobility from the CBD’s Areas to the outskirts of the City and can be provided readily in combination with the circular connection depending upon the pattern of the commuters. In Karachi underground spine from Jehangir Park [Empress Market] to Tower via I.I. Chundrigar Road and M.A. Jinnah Road coupled with spine from Jahangir Park to NIPA would afford mobility from CBD areas to outskirts in shortest possible time. However, the cost of the Project imposes major constraints and is not doable in present condition. 8.2 Revival of Karachi Circular Railway (KCR) It has right of way available in almost all the districts of Karachi, and its revival does not involves any major traffic diversions and relocation of utility services. Karachi Circular Railway shall be revived as a modern commuter system with proper road connectivity and interface with the proposed BRT and MRT corridors. 8.3 MRT [Metro Rail Transit] at grade and elevated on high density corridors: i. Blue Line: Super Highway to Tower via Tin Hatti, M.A.Jinnah Road. ii. Brown Line: Korangi to North Karachi via Rashid Minhas Road 8.4 Bus Rapid Transit Bus Rapid Transit is a high quality bus system providing high speed, reliable, and comfortable services compared to traditional bus services. The concept of BRT is based on railway system, i.e. running along exclusive way, high speed, accurate travel time, and high capacity. KTIP study carried out by JICA, in 2009-12 as proposed the following BRT routes: i. Green Line: Surjani to Jamma Cloth Market via North Nazimabad, M.A. Jinnah Road ii. Red Line: Malir Cantt to Regal Chowk via University Road iii. Yellow Line: Dawood Chowrangi to Numaish/ Lucky Star via Korangi Road iv. Orange Line: Orangi Town to Matric Board Office v. Purple Line: Baldia to Sher Shah via Hub River Road vi. Aqua Line: Hawks Bay to Gulbai via Mauripur Road The option/solution in the shape of MRT/BRT and in short term/long term are presented in slide # 25, 26& 27,which will duly address the concerns of commuters as reflected in slide # 28. However the approved projects are listed at slide # 29 & 30 and the Policy and Strategy for the achievement of the same are given in 31, 32, 33 & 34. The proposed Mass Transit System are in line with the BRT system and LRT systems, operating in the world are reflected in the slide # 21, 22, & 23 and the underground Metro Rail Project are shown in slide # 24. There are a number of variations for BRT, and the boundary between BRT and conventional bus services is

Pakistan Academy of Engineering

11

not clear as far as the physical appearance is concerned. A typical BRT is the bus transit service on exclusive lanes in road spaces along the kerb line/centre of the road/dedicated lane. The maximum capacity of a standard BRT is approximately 13,000 passengers per hour per direction. BRT capacity depends on the service frequency and vehicle capacity. 8.5 BRT Type There are three levels of BRT system commonly used for the classification of BRT.

Level 1 Bus Lane Level 2 Bus way Level 3 BRT [dedicated lane]

Level-1 system usually provides a bus lane along kerb side. The bus lane is sometimes a priority lane which gives priority of using the lanes to buses but other vehicles can use the lanes when the bus traffic is not heavy, and other times an exclusive lane. In the urban street system where access demand along the road side exists and there are intersections with crossing streets, the bus lanes are easily interrupted by other vehicles. In Level-2 systems to avoid interweave of buses and other traffic, bus lanes are located in the center of roads. The Bus way system is usually a part of the network of general bus services. The improvement of bus services by introduction of this system would be insufficient in case that there are a number of operators (like Karachi) and it is allowed to use the bus way by many operators. The BRT systems in Seoul and Taipei are the examples of this system. Level-3 system is similar to railway system. In most cases, buses are only operated on the dedicated lanes controlled by a single operator along the lanes. Since the BRT buses need not run, in general traffic roads, advanced vehicle technologies can be used to increase the capacity and speed. In addition, pre-board fare collection reduces dwell time at bus stations. Metro bus (Istanbul) is the example of BRT of Level-3. Note that Level-3 does not necessarily mean high capacity system. For example, Trans-Jakarta (Jakarta) is categorized to Level-3 system but the capacity is very small. The service frequency depends on dwell time and clearance time. Additional stopping bays can increase the capacity.

9. APPROVED PROJECTS 9.1 Revival of Karachi Circular Railway

Pakistan Academy of Engineering

12

i. Approved by the Govt. of Pakistan at a cost of 1.558 Billion US$ (Sep 09) ii. Revised Cost 2.6 Billion US$ approved by the Govt. of Pakistan (Aug 12) iii. Feasibility Study completed (May 2009) iv. Feasibility Study, updated (November 2012) v. EIA Study conducted and approved by EPA GOS vi. Geotechnical investigations, hydrological & Geological studies done vii. Exemption of GST, Import Duty, Federal and Provincial taxes (March 2013) viii. JICA considering to fund the project 9.2 BRT Yellow Line Project [20.4 KM, estimated cost Rs.5.5 Billion] i. Project has been conceived under PPP Mode by PPP Unit GOS & Karachi Mass Transit Cell (KMTC) ii. Bidding is under process iii. The date of submission of financial bids by potential sponsors was December 18, 2014, which has been extended to Jan / Feb 2015. 9.3 BRT Green Line Project [21.1 KM, cost Rs.16 Billion for Infrastructure] i. The Prime Minister approved PKR 16.0 Billion for BRT Green Line ii. PC – I approved for Rs.16.0 Billion by Govt. of Pakistan (04-Dec-2014). iii. Ministry of Communications, GoP to provide funds. iv. Rolling Stock, ITS and other systems under PPP mode by GOS 9.4 BRT/MRT Blue Line Project i. PPP Policy Board approved the project & instructed PPP Unit, GOS for international bidding ii. The Public Hearing for EIA was conducted on Oct. 28, 2014 by EPA. iii. The PPP Unit GOS is preparing RFP for International Bidding 10. RECOMMENDATIONS In the present day scenario; the solution to the mobility problems in the city of Karachi can be as follows:-

Optimize traffic corridors Promote public transport Cleaner fuels Green vehicles

Short Term Implementation of:-

Revival of KCR Project BRT Projects

o Blue Line o Orange Line o Green Line o Yellow Line

Long Term Implementation of:-

KCR Extension to Airport KCR Extension to Steel Mill, Port Qasim BRT Corridors

o Red Line o Purple Line o Aqua Line

Provision of underground Metro to be explored.

Pakistan Academy of Engineering

13

OVERVIEW OF THE

SOCIOECONOMICS STATUS OF

KARACHI

1

Administrative Structure:• Total No. of Towns - 18• Total No. of Cantonments - 6• Total No. of UC’s - 178

Demographics:• Population (million) - 20• Households (millions) - 3.3• Annual Pop. Growth - 3.5%

BUILT-UP AREA [1,200 SQ. KM]

JURISDICTION [3,600 SQ. KM]

KARACHI AT A GLANCE

2

Pakistan Academy of Engineering

14

POPULATION GROWTH BY TOWN

Gadap

Town

Bin Qasim

Town

Kemari

Town

New Karachi

Town

Population in 20051,000,000500,000100,000

Population in 20201,000,000500,000100,000

Source: JICA KTIP 2030

3

New Built Up(2005⇒2010)

New Under Built Up(2005⇒2010)

Built Up Area (2005,2010)

URBAN SPRAWL AREA FROM 2005 TO 2015

DESCRIPTION 2005

(HA)

2015

(HA)

2015/2005

1. Built-up 33,088 35,931 1.1

2. Under Built-up 10,625 14,696 1.4

TOTAL 43,713 50,627 1.2

Built-up Area: About 50% or more of

the site is filled with buildings or houses.

Under Built-up Area: Less than 50% of

the site is filled.

Others (Non Built-up Area): Vacant

land or very few buildings or houses

4

Pakistan Academy of Engineering

15

GROWTH OF POPULATION IN KARACHI

31.9

29.7

15.1

18.9

23.1

27.6

32.7

38.9

36.1

31.6

10

15

20

25

30

35

40

2000 2005 2010 2015 2020 2025 2030 2035

(million)

Alternative A

Alternative B

Alternative C

KSDP2020

Year

Alternative

A

Alternative

B

Alternative

C

Rate in

2020

continues

Trend of

KSDP

2020

Half rate of

Alternative

B

2005 5.0%

2010 4.5%

2015 4.0%

2020 3.5%

2025 3.5% 3.0% 1.5%

2030 3.5% 2.5% 1.25%

NOTE:

AAGR from 2005 to 2020 are estimated in

KSDP 2020.

Annual Average Growth Rate (AAGR)

Source: JICA KTIP 2030

5

DHA City & Bahria Town Karachi

(25,000 ACRES)

Education City

(2,100 ACRES)

Textile City

(1,250 ACRES)Korangi Creek Industrial Park

(250 ACRES)

Bin Qasim Industrial Park

(930 ACRES)Waterfront

Development

Zulfiqarabad City Town

(Thatta Coastal Area)

New Nazimabad

LARGE-SCALE URBAN DEVELOPMENT PROJECTS

6

Pakistan Academy of Engineering

16

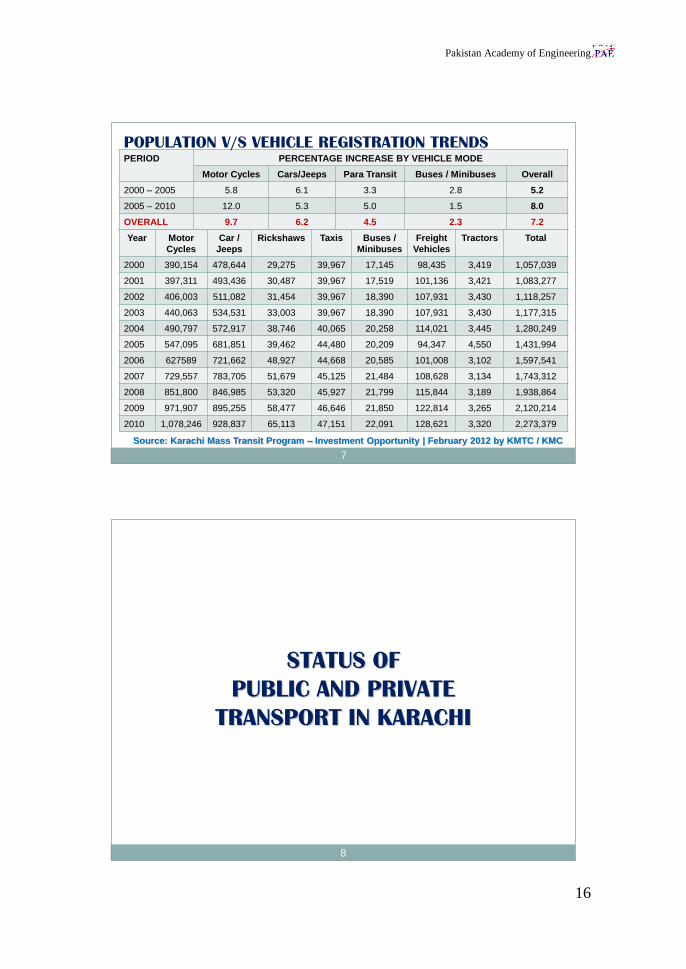

PERIOD PERCENTAGE INCREASE BY VEHICLE MODE

Motor Cycles Cars/Jeeps Para Transit Buses / Minibuses Overall

2000 – 2005 5.8 6.1 3.3 2.8 5.2

2005 – 2010 12.0 5.3 5.0 1.5 8.0

OVERALL 9.7 6.2 4.5 2.3 7.2

POPULATION V/S VEHICLE REGISTRATION TRENDS

Year Motor

Cycles

Car /

Jeeps

Rickshaws Taxis Buses /

Minibuses

Freight

Vehicles

Tractors Total

2000 390,154 478,644 29,275 39,967 17,145 98,435 3,419 1,057,039

2001 397,311 493,436 30,487 39,967 17,519 101,136 3,421 1,083,277

2002 406,003 511,082 31,454 39,967 18,390 107,931 3,430 1,118,257

2003 440,063 534,531 33,003 39,967 18,390 107,931 3,430 1,177,315

2004 490,797 572,917 38,746 40,065 20,258 114,021 3,445 1,280,249

2005 547,095 681,851 39,462 44,480 20,209 94,347 4,550 1,431,994

2006 627589 721,662 48,927 44,668 20,585 101,008 3,102 1,597,541

2007 729,557 783,705 51,679 45,125 21,484 108,628 3,134 1,743,312

2008 851,800 846,985 53,320 45,927 21,799 115,844 3,189 1,938,864

2009 971,907 895,255 58,477 46,646 21,850 122,814 3,265 2,120,214

2010 1,078,246 928,837 65,113 47,151 22,091 128,621 3,320 2,273,379

Source: Karachi Mass Transit Program – Investment Opportunity | February 2012 by KMTC / KMC

7

STATUS OF

PUBLIC AND PRIVATE

TRANSPORT IN KARACHI

8

Pakistan Academy of Engineering

17

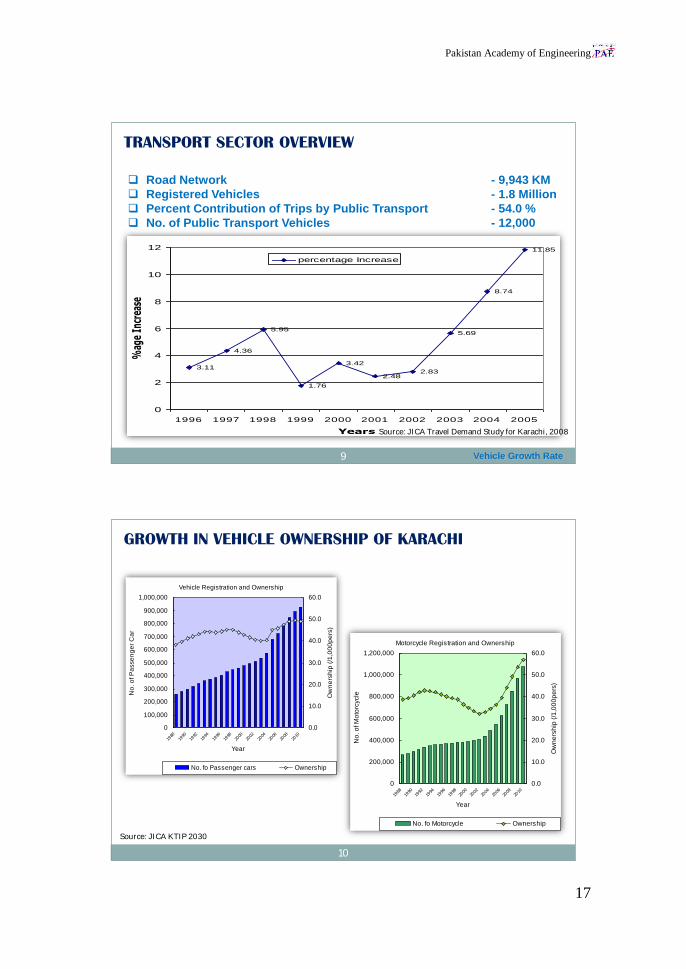

TRANSPORT SECTOR OVERVIEW

Road Network - 9,943 KM

Registered Vehicles - 1.8 Million

Percent Contribution of Trips by Public Transport - 54.0 %

No. of Public Transport Vehicles - 12,000

3.11

4.36

5.95

1.76

3.42

2.482.83

5.69

8.74

11.85

0

2

4

6

8

10

12

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Years

%ag

e In

crea

se

percentage Increase

Vehicle Growth Rate

Source: JICA Travel Demand Study for Karachi, 2008

9

GROWTH IN VEHICLE OWNERSHIP OF KARACHI

Vehicle Registration and Ownership

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Year

No

. o

f P

asse

ng

er

Ca

r

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Ow

ne

rsh

ip (

/1,0

00

pe

rs)

No. fo Passenger cars Ownership

Motorcycle Registration and Ownership

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Year

No

. o

f M

oto

rcycle

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Ow

ne

rsh

ip (

/1,0

00

pe

rs)

No. fo Motorcycle Ownership

Source: JICA KTIP 2030

10

Pakistan Academy of Engineering

18

STATUS OF EXISTING PUBLIC TRANSPORT(VEHICLE COUNT V/S OCCUPANCY COMPARISON)

4.5% composition of Public Transport Vehicles carry

42% of Total Persons Traveling in the City.

Private Cars which is 36.5% of Total Vehicular Traffic

carries only 21% of Persons. Showing Lesser

Average Vehicle Occupancy.

The above leads to the conclusion that there is still

deficiency of Public Transport availability on all

Major Routes in the city.

Source: KTIP Study by JICA (2010-12)

11

VEHICLE OWNERSHIP BY TOWN

Source: JICA KTIP 2030

12

Pakistan Academy of Engineering

19

POPULATION V/S VEHICLE REGISTRATION TRENDS(COMPARISON)

NOTE:

No. of Vehicles projected based on an Annual

Growth Rate of 4.5% after 2014, without any

Mass Transit Project.

NOTE:

Present percentage of ownership of private

vehicles is about10%. This will increase to 16% if

Mass Transit Program is not implemented.

13

TIME SAVING BENEFITS

A Average pay per month 7,000/-

B Working days 30

C Working hours/Day 8

D Total working hours in a month [B*C] 240

E Average cost per hour [A/D] 29.166

F Average pay per minute 0.49

G Bus running time for 19.5 km @ 35 km/h speed 78 mins

H Train running time for 19.5 km @ 35 km/h speed 35 mins

I Time saving by KCR travel [F-G] 43 mins

J Time saving cost per day / per passenger [F*I] Rs. 21.07

K KCR passengers per day 698,955

L KCR passengers per year 242,537,385

M Time Cost saving per year [J*L] Rs 5,069,589,182

N Time cost saving per year [Rs. Million] 5,110.26

Say US$ Millions [US$ 1 = Rs.82.5] 61.94

14

14

Pakistan Academy of Engineering

20

99%

1%0%0%0%

CO2

Hydrocarbon

Sulphur dioxide

Nitrogen oxide

Particulate Matter

52%

2%

37%

9%

PETROL CONSUMPTION

CO2

Hydrocarbon

Sulphur dioxide

Nitrogen oxide

Particulate Matter

99%

7%

54%

32%

7%

DIESEL CONSUMPTION

VEHICULAR AIR POLLUTION EMISSIONS FROM

FUEL CONSUMPTION (KM PER DAY)

15

ISSUES AND CHALLENGES

1

Pakistan Academy of Engineering

21

20 m

22 m

MILLION

2.2 m

5.21 m5.43 m

0.58 m

VEHICLE POPULATION TRIPS

TRAVEL DEMAND

1987 2015

30

28

26

24

22

20

18

16

14

12

10

8

6

4

2

0

17

TRANSPORT CHALLENGES

Fast urbanization

Rapid Motorization

Increasing Traffic Congestion

Absence of an efficient Mass Transit System

Declining Road Safety, Air Quality and Growing Noise Pollution

In-Effective Traffic Police and Motor Vehicle Inspection System

Fragmentation of Authorities

18

Pakistan Academy of Engineering

22

OPTIONS AND SOLUTIONS

19

20

MASS

TRANSIT

SYSTEM

OPERATING

AT HIGH

FREQUENCY

MOBILITY OF

MAXIMUM

NUMBER OF

PASSENGERS

SHORTEST

POSSIBLE

TIME

VEHICLES

WITH LARGE

CARRYING

CAPACITY

Pakistan Academy of Engineering

23

BUS Rapid Transit (BRT) System

Bagota, Columbia (Center of Road) Guangzhou, China (Center of Road)

Santiago, Chile (On Kerb) Guangzhou, China (Center of Road)

21

Light Rapid Transit (LRT) In Bangkok

VARIOUS MASS TRANSIT MODES (LRT)

22

Pakistan Academy of Engineering

24

VARIOUS MASS TRANSIT MODES (Metro Rail)

Tokyo Metro Rail London Underground

Dubai Metro London Underground

Dehli Metro23

OPTIONS AND SOLUTIONS

Underground Metro Rail:

Ideal system for providing mobility from the CBD’s Areas to theoutskirts of the City.

Underground spine from Jahangir Park [Empress Market] to Towervia I. I. Chundrigar Road and M. A. Jinnah Road.

Spine from Jahangir Park to NIPA

Cost of the Project imposes major constraints and is not doable inpresent condition

24

Pakistan Academy of Engineering

25

Revival of Karachi Circular Railway

Land for Right of Way and Terminals available

No major Traffic Diversions: Relocation of Utility Services

Feasibility study completed

MRT [Metro Rail Transit] at grade and elevated on high density corridors

Bus Rapid Transit:

Level – 1: Bus Lane along kerb side

Level – 2: Bus Way in center of road

Level – 3: BRT on dedicated lane at grade / elevated

OPTIONS AND SOLUTIONS

25

SHORT TERM:

Implementation of Revival of KCR Project

BRT Projects

Blue Line

Red Line

Green Line

Yellow Line

LONG TERM:

KCR Extension to Airport

KCR Extension to Steel Mill, Port Qasim

Implementation of BRT Corridors

Orange Line

Purple Line

Aqua Line

Provision of underground Metro to be explored

OPTIONS AND SOLUTIONS

26

Pakistan Academy of Engineering

26

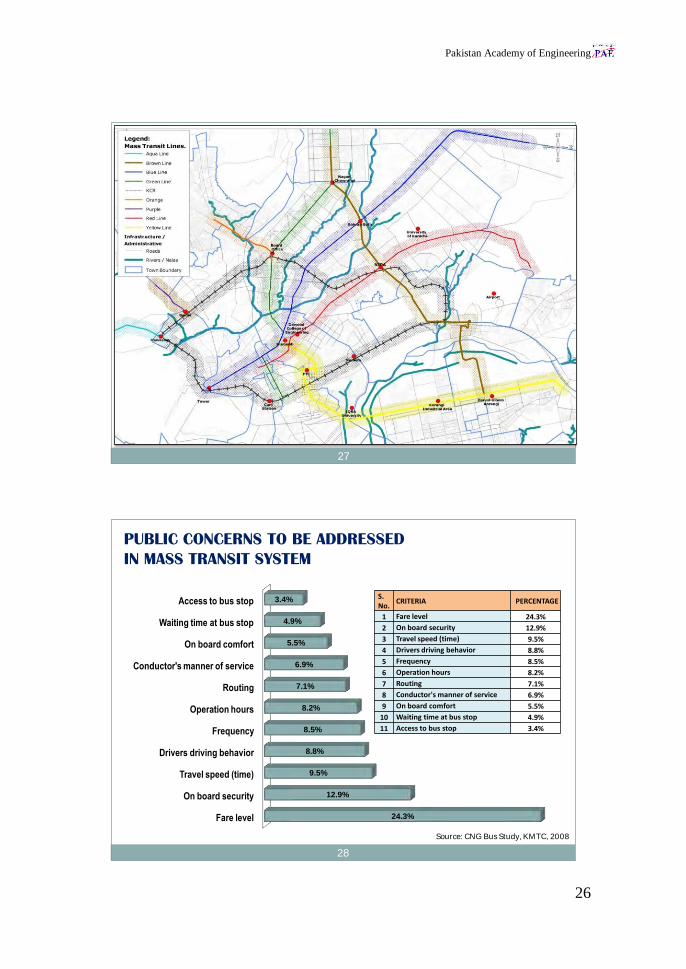

27

Fare level

On board security

Travel speed (time)

Drivers driving behavior

Frequency

Operation hours

Routing

Conductor's manner of service

On board comfort

Waiting time at bus stop

Access to bus stop

24.3%

12.9%

9.5%

8.8%

8.5%

8.2%

7.1%

6.9%

5.5%

4.9%

3.4% S. No.

CRITERIA PERCENTAGE

1 Fare level 24.3%

2 On board security 12.9%

3 Travel speed (time) 9.5%

4 Drivers driving behavior 8.8%

5 Frequency 8.5%

6 Operation hours 8.2%

7 Routing 7.1%

8 Conductor's manner of service 6.9%

9 On board comfort 5.5%

10 Waiting time at bus stop 4.9%

11 Access to bus stop 3.4%

PUBLIC CONCERNS TO BE ADDRESSED

IN MASS TRANSIT SYSTEM

Source: CNG Bus Study, KMTC, 2008

28

Pakistan Academy of Engineering

27

APPROVED PROJECTS

29

Sr.

No.

Mass Transit

Line

Length

in km

Estimated

Cost

(PKR Billion)

StatusSource of

Funding

1. BRT Blue Line 42 30.0 (tentative)RFP on PPP mode

under preparation

KMC under PPP

Arrangement

2. BRT Yellow Line 20.4 15.0

Financial BIDS

opening on

02-Jan-15

KMC Under PPP

Arrangement

3. BRT Green Line 21.1

16.0 (infrastructure)

Rolling Stock

under PPP Mode

PC-I approved by

GOP (04-Dec-14)

Financed by GoP

(Ministry of

Communications)

4. BRT Red Line 24.4To be

ascertainedUnder negotiations

Finance by Asian

Development Bank

5. KCR 43.1

US$ 1.558 Ml

(Sep 09)

US$ 2.609 Ml

(Aug 12)

Appraisal Mission

of JICA awaited

Japan International

Cooperation

Agency (JICA)

APPROVED PROJECTS

30

Pakistan Academy of Engineering

28

Policy and Strategy

31

POLICY STRUCTURE

Travel in Karachi is no longer stressful.

Transport capacity satisfies the demand.

Mass transit is operated.

Road traffic is safe.

Bus service is available in entire Karachi

Road supports economy with minimum environmental impact.

OBJECTIVES / VISION

RESOURCE COMMITMENT

PROJECTS / PROGRAMS

INSTITUTIONAL SETUP

Monitoring

Performance Evaluation

32

Pakistan Academy of Engineering

29

TRANSPORTATION STRATEGY (SUSTAINABLE & INTEGRATED APPROACH)

LAND USE

Long-Term Urban Planning, Integration of Developments

Vehicle Ownership

Restraint

Vehicle Usage

Restraint

Traffic Management /

ITS

Enhance Safety &

Accessibility

Judiciously Expand

Road Network

Develop / Expand

Rapid Transit

Improve Bus

Services

Integrate Bus / Rail

Network & Ticketing

Enhance Commuter

Accessibility

Conducive Financing Options

Transport

Integrated Land-Use /

Transport Planning

ENVIRONMENT

Emission Standards, Cleaner Fuels, Enforcement

Green Vehicles, Education

33

CONDUCIVE ENVIRONMENT FOR MASS TRANSIT PROGRAM

Local and International Investors would be comfortable with the availability ofthe following:

Karachi strategic Development plan 2020

Karachi Transport Master Plan (2030)

Population Forecast, Travel Demand Trend, Road Network, Transit

Network, Implementation Cost Profile etc.

Feasibility Report of two + four BRT lines

Pre-feasibility of Blue Line and Brown Line for MRT

Legal cover in the form of PPP act (2010)

Government support at all levels.

Political will and commitment

34

Pakistan Academy of Engineering

30

THE COST OF TRAFFIC CONGESTION FOR KARACHI Prof. Dr. Mir Shabbar Ali

2

1. INTRODUCTION In the last two decades, rapid growth and urbanization brings precarious issues to the under developing countries. Mainly all these issues are classified as public issues which leads towards drastic impact to the settlements. One of the eminent problems faced by all classes of population is road transportation. The inefficient transportation infrastructure has been the main restraint for the development [1]. The large cities of Pakistan face similar types of congestion problems, and there is no such effort present at the moment that quantifies the amount of monetary losses due to congestion. Although, there are a number of efforts made to accommodate and facilitate the increasing traffic in urban areas but congestion seems to be an unresolved issue. Karachi Metropolitan Corporation (KMC) formerly known as CDGK established a command and control system to monitor traffic flow but the data that has been generated, Lahore Mass Transportation System (BRT) initiated to tackle traffic congestion. Keeping this in view, this research was conducted to investigate the amount of congestion and then quantify it in terms of cost. For this purpose one of the busiest and significantly important road stretch of Karachi were selected which mainly serves the activities associated with an industries and port. The research was designed to ascertain the traffic congestion with a conventional approach. Numbers of traffic parameters were collected through field surveys. This paper contains the description about study area, type of data collected for this study and findings 2. LITERATURE REVIEW 2.1 The problem of traffic congestion in major cities of the world like Karachi is a frequent phenomenon. The traffic congestion tends to prolong and hinder a number of economic activities in the city. The studies on traffic associated issues and threats are examine under different domains such as environment and health. In contrast, economical loss due to traffic is also investigated in a number of ways. Arnott and Small [2] studied and described the undesirable effects of traffic to their environments, like air degradation due to vehicle emission and traffic noise pollution along with the congestion. McKinnon [3] studied the effect of traffic congestion on logistical operations. Goodwin [4] discussed about the transportation management issues for resolution of traffic congestion faced in Europe. Thomson and Bull [5] discussed about the concerns associated with traffic congestion.

2 Department of Urban and Infrastructure Engineering, NED University of Engineering and Technology,

Karachi, 75270, Pakistan

Pakistan Academy of Engineering

31

2.2 A recently released documents show that future commuters using the proposed US29 Western Bypass will save up to 22:30 minutes each day by utilizing the bypass. A comparison of travel times for the year 2040 with and without the Bypass was developed. Table below provides this data. The figure below provides 20 minutes time-speed data. Australian Government, Department of Transport and Regional Service,[6] estimated congestion cost for a year approximately USD 10 billion which comprises operating cost, private time cost and business time cost for all Australian cities. Another research was also conducted for Dhaka city; Bangladesh [7], estimated congestion cost for a year was USD 3.868 billion. This cost comprises environmental, vehicle operating cost, social cost, travel time cost etc. The methodology was based on collecting data regarding travel time, and number of vehicles. Goodwin [8] came up with the findings for UK that economic cost of traffic congestion was approximately USD 30 billion for a year in 2004 and predicted that this may increase up to USD50 billion in 2010. The method used was composed of collecting data for free flow speed, traffic volume, congestion delay and value of time. Congestion cost is also estimated through a simulation the study, Garrido [9] used micro simulation technique to estimate the traffic congestion cost of the Antofagasta, Chile having population of around 0.4 million inhabitants. The study described the simulation procedure and concluded that the average congestion cost of working day is approximately USD 1.02 Million.

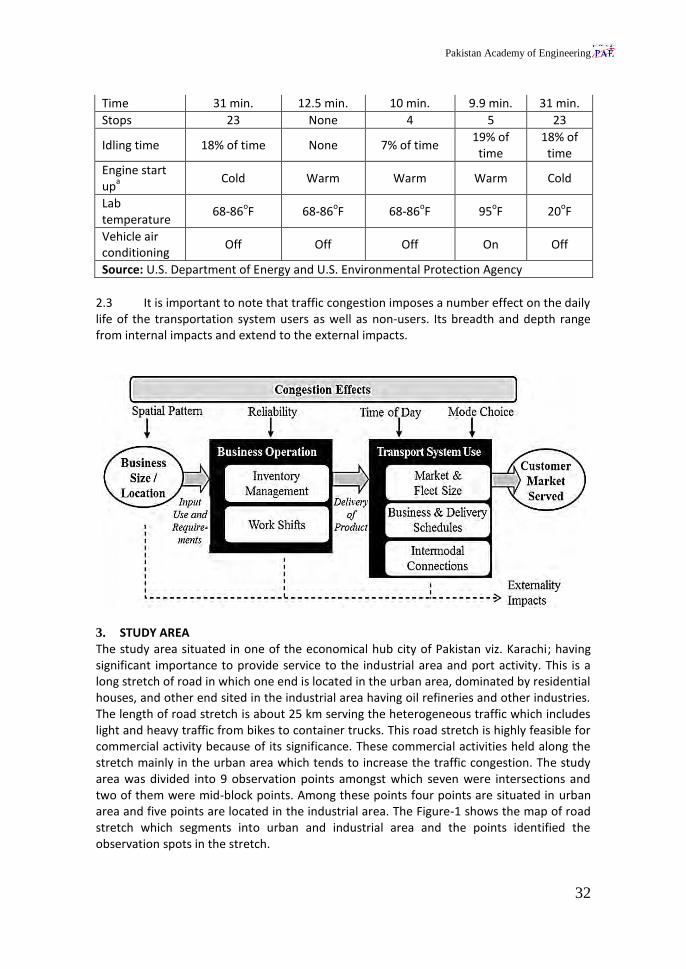

DRIVING CYCLE ATTRIBUTES

Test schedule

City Highway High speed AC Cold temp

Trip type Low speeds in stop-and-go urban traffic

Free-flow traffic at highway speeds

Higher speeds; harder

acceleration & braking

AC use under hot ambient

conditions

City test w/colder outside

temperature

Top speed 56 mph 60 mph 80 mph 54.8 mph 56 mph

Average speed

20 mph 48 mph 48 mph 22 mph 20 mph

Max. acceleration

3.3 mph/sec 3.2 mph/sec 8.46 mph/sec 5.1

mph/sec 3.3

mph/sec

Simulated distance

11 mi. 10 mi. 8 mi. 3.6 mi. 11 mi.

Pakistan Academy of Engineering

32

Time 31 min. 12.5 min. 10 min. 9.9 min. 31 min.

Stops 23 None 4 5 23

Idling time 18% of time None 7% of time 19% of

time 18% of

time

Engine start up

a

Cold Warm Warm Warm Cold

Lab temperature

68-86oF 68-86

oF 68-86

oF 95

oF 20

oF

Vehicle air conditioning

Off Off Off On Off

Source: U.S. Department of Energy and U.S. Environmental Protection Agency

2.3 It is important to note that traffic congestion imposes a number effect on the daily life of the transportation system users as well as non-users. Its breadth and depth range from internal impacts and extend to the external impacts.

3. STUDY AREA The study area situated in one of the economical hub city of Pakistan viz. Karachi; having significant importance to provide service to the industrial area and port activity. This is a long stretch of road in which one end is located in the urban area, dominated by residential houses, and other end sited in the industrial area having oil refineries and other industries. The length of road stretch is about 25 km serving the heterogeneous traffic which includes light and heavy traffic from bikes to container trucks. This road stretch is highly feasible for commercial activity because of its significance. These commercial activities held along the stretch mainly in the urban area which tends to increase the traffic congestion. The study area was divided into 9 observation points amongst which seven were intersections and two of them were mid-block points. Among these points four points are situated in urban area and five points are located in the industrial area. The Figure-1 shows the map of road stretch which segments into urban and industrial area and the points identified the observation spots in the stretch.

Pakistan Academy of Engineering

33

Figure-1: Showing road stretch as Urban Area and Industrial Area

4. DATA COLLECTION AND PROCESSING 4.1 The project methodological framework encompassed the data collection, data processing, data analysis and the final step of congestion estimation and valuation, based on the collected data. For data collection, an instrumented vehicle which was indigenously developed by NED University having mounted video cameras and tracker system was used for traffic volume observations at 9 different locations mentioned above. The data was collected in two time phases, morning and evening, with time interval between 8:00am to 1:00pm and 3:00pm to 8:00pm respectively. The morning and evening data hours were considered so as to record the peak traffic hours. The data at each point was collected for two days in order to counter the effect of the variations. Among these survey points two control points were established. The purpose of these control points was to control the data variation of non-counted hours and to develop an urban and industrial average data throughout the link. The data at control points, Malir Kalaboard and Bin Qasim Intersection, was collected for longer durations with the strategy to extrapolate the data for supplementary intervals. Volume data was characterized into different travel modes such as: Cars, Motorcycles, Rickshaw, Pickup, Buses, Trucks and Trailers, Bicycles and Animal Carts for non-motorized modes of transport. The delay study conducted on the field with the help of same indigenous vehicle running on the road stretch (from Star Gate to Pakistan Steel) to quantify the delay and their reasons. The delay time was calculated based on the definition that total accumulated time of the vehicle for a trip at which the vehicle is travelling below the reference speed. Various reference speeds such as20, 40 and 60km/hr were used for calculation of delay time as literature does not provide any firm guideline regarding the choice of reference speed [8].Special emphasis was given on the accuracy of the delay data which was calculated manually (through average vehicle technique) as well as through Tracker data set. 4.2 Value of time (VOT) is estimated using a socio-economic survey data from the commuters of this road stretch. The socio-economic survey was based on the questionnaire which provides information about commuter’s mode choice and different

Pakistan Academy of Engineering

34

attributes of the travel modes such as travel cost, travel time and waiting time in case of Public and Para transit types of mode. The idea was to estimate VOT of the individuals travelling in different modes using an indirect technique which is based on estimating mode specific utility equations that includes travel time and travel cost parameters, as a part of multinomial logic model form [10].The estimated VOT values are utilized to measure opportunity cost component of traffic congestion. Fuel efficiency and fuel consumption data for different types of modes, prevailing along that road stretch, was gathered to estimate vehicle operating cost component of traffic congestion cost. Equation (1) and (2) represents the expressions utilized to compute opportunity and vehicle operating costs.

𝑂𝐶 = ∑ (𝑉𝑂𝑇𝑚 × 𝐷𝑒𝑙𝑎𝑦𝑚 × 𝑉𝑚 × 𝑉𝑜𝑐𝑐𝑚)𝑚

𝑚=1 Eq. (1)

Where, OC= Opportunity Cost of traffic congestion, 𝑉𝑂𝑇𝑚= Value of time for specific mode m, 𝐷𝑒𝑙𝑎𝑦𝑚=travel delay in time units observed for mode m (estimated at some reference speed),𝑉𝑚=number of vehicles of type m per day, 𝑉𝑜𝑐𝑐𝑚= Average vehicle occupancy for specific mode m.

𝑉𝑂𝐶 = 𝐿 ∗ ∑ (𝐹𝐶𝑚 × 𝐷𝑒𝑙𝑎𝑦𝑚 × 𝑉𝑚)𝑚

𝑚=1 Eq. (2)

Where, VOC= Vehicle operating Cost, 𝐹𝐶𝑚= Fuel cost in Rs/hr for specific mode m, 𝑉𝑚 and 𝐷𝑒𝑙𝑎𝑦𝑚 have the same meaning mentioned earlier and L= length of stretch in km. Where, 𝐹𝐶𝑚is calculated using equation (3).

𝐹𝐶𝑚 = ∑ (𝐹𝑐𝑞𝑚𝐹𝑡 × 𝐹𝑝𝐹𝑡 × 𝜇𝐹𝑡)3

𝐹𝑡=1

Eq.(3)

Where, 𝐹𝑐𝑞𝑚= Fuel consumption quantity in litres/km or kg/km of specific mode m, 𝐹𝑝𝐹𝑡= fuel price of specific fuel typesFt = 1, 2 and 3 such as CNG, Gasoline and Diesel, respectively in Rs. / liter or Rs/kg.𝜇𝐹𝑡=proportion of specific mode type m using a particular fuel type for travelling on that road stretch.

5. RESULTS AND DISCUSSION 5.1 The collected data was compiled according to the parameters described in equations (1), (2) and (3). The average values of the volume collected at 9 different locations are given in Table-1. As the survey data was gathered only for 16 hours of the day, these values are adjusted to represents values for a single average day. Some past studies results were utilized to derive those adjustment factors. In addition to this, Table-1 also provides observed values of vehicle occupancy for each different type of mode travelling on the stretch of the segment. The travel mode, bike (motorcycles) contributed largely to the traffic stream compared to all other vehicle types. The presence of significant amount of bikes is mainly due to the inconvenient public transport system prevailing in Karachi. There is also significant numbers of Trucks present in the traffic stream because of the type of land use in the neighborhood of this road stretch. Large numbers of industries are located nearby and also this road provides access to a major seaport in Karachi. Due to this fact significant number of office Vans (privately hired vehicle such as coasters and Hiace) are

Pakistan Academy of Engineering

35

also seen frequently during peak hours; which carries passengers from the residence to the industries and vice versa. It is interesting to note that the average vehicle occupancy of car obtained was low compared to its seating capacity. This is because most of the commuters which are using car for their own travel. Figure-2 further describes the percentage of different modes present in the stream.

Table-1: Classified volume and vehicle occupancy

Modes Volume(veh/ day) Vehicle Occupancy

Car 2970 2.2

Taxi 481 3.2

Office Van 978 13

Three Wheeler 432 2

Bike 3419 1.2

Public Transport 1334 38

Truck 1188 4

Figure- 2: Mode percentage share in the traffic stream

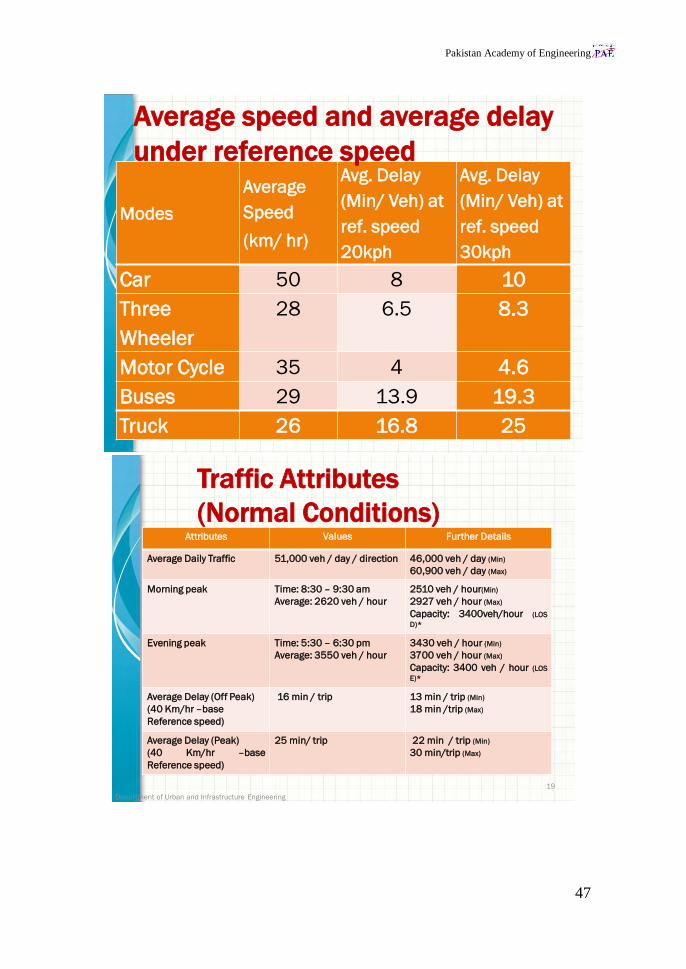

5.2 Table-2 describes the average speed of classified modes on that road stretch. The road is classified as major urban arterial road, which basically fulfills the purpose of mobility and the design speed is around 110 km/hr. The average speed of the road clearly depicting the prevailing condition of the arterial that is partly due to the deteriorated pavement structure and partly due to the increased demand, both of these factors in combination creating frequent traffic jams along the road stretch. Table-2 also shows estimated travel delays for each representative travel mode at two reference speeds (i.e. 20km/hr and 30km/hr). The table demonstrates that the delay of a particular mode is directly proportional but the increment of delay is not similar among the modes which describe the mobility characteristic of that mode. It may be clearly observed from that the table the bike has less delay and truck has the largest delay in both the reference speed, which in mainly due to their size.

Car 27%

Taxi 4%

Office Van 10% Three

Wheeler 4%

Bike 30%

Public Transport

13%

Truck 12%

PERCENTAGE SHARE OF MODE

Pakistan Academy of Engineering

36

Table-2: Average speed and average delay under reference speed

Modes Average Speed

(km/ hr) Avg. Delay (Min/ Veh)

at ref. speed 20kph Avg. Delay (Min/ Veh)

at ref. speed 30kph

Car 50 8 10

Taxi 45 8 11

Office Van 42 9.5 12.4

Three Wheeler 28 6.5 8.3

Bike 35 4 4.6

Public Transport

29 13.9 19.3

Truck 26 16.8 25

5.3 The value of time was also estimated in this study using an indirect approach, more details of this can be seen in Adnan et al [11], however, VOT values are shown with respect to mode users in Table-3. Average fuel consumption quantity of classified modes and their proportions (i.e.µ1,µ2, µ3)are also shown in same table. Fuel consumption quantities are estimated by running various test vehicles of same mode type on the road stretch. The proportions of vehicles using different fuel type is determined based on physical examination of various travel modes based on sample size of 300 vehicle of each mode type. 5.4 The results shown in the Table 1, 2 and 3 are utilized in quantifying the level of congestion and traffic congestion cost using equations (1), (2) and (3). As shown in the Table-2 above, time loss for average vehicle type is approximately 10minutes/trip using conservative definition of delay (i.e. 20km/hr reference speed) along with the volume of traffic which is 60,000 vehicles/day. On these bases, total delay was found out to be 600,000 minutes/day which is nearly 410 days/day. The Level of Service (LOS) for this stretch was fond out to be D. The free flow travel time for the stretch, was 17 minutes, but in actual circumstances average travel time per average vehicle is found to be 30minutesfor the complete stretch of road which is around 21km. The per trip additional time as associated to the free flow speed is approximately 175%of the free flow travel time, which provides travel time index value as 1.75. Furthermore, a very interesting fact is that the free flow speed is hardly achievable on this track at any time of the day.

Table-3. Vehicle classified VOT with µ-factor and fuel consumption quantity

Modes VOT (Rs/hr)

µ1 µ2 µ3 FcqCNG

(kg/km)

FcqGasoline

(lt/km)

FcqDiesel

(lt/km)

Car 87 0.56 0.44 - 17-19 10-12 -

Taxi 80 0.63 0.37 - 18-20 10-12 -

Office Van 75 0.57 0.43 - 10-11 7-8 -

Three Wheeler 60 0.79 0.21 - 28-30 25 -

Bike 44 - 1 - - 55-60 -

Public Transport

34 0.59 - 0.41 6-8 -

2-4

Truck 35 - - 1 - - 1-2

Pakistan Academy of Engineering

37

Table-4: Total Cost of direct traffic congestion per day in Pak Rupees

Items Loss in PKR

Opportunity Cost (OC) 1,897,800

Vehicle Operating Cost (VOC) 1,042,000

Wear and Tear Cost (10% of VOC) 104,200

Total Cost 3,044,000

5.5 Based on the collected data and observed results, the Table-4 shows total direct traffic congestion cost as around 3million PKR per day (30,440 USD per day) for the road stretch under study using conservative definition of travel delay (i.e. 20 km/hr reference speed). On per year basis, this figure will be approximately 11 Million USD per annum. This is significant amount of monetary value that could be avoided by taking counteractive measures. It is a very high cost especially when compared to the GDP. Therefore, as happened in the Western World, serious mitigation steps needs to be implied here as well. Furthermore, this is the loss incurred due to traffic congestion at a particular commuter stretch. This value when extrapolated to the whole of Karachi city it makes the issue more cumbersome. Thus, the policy making institutions needs to take serious actions to deal with it.

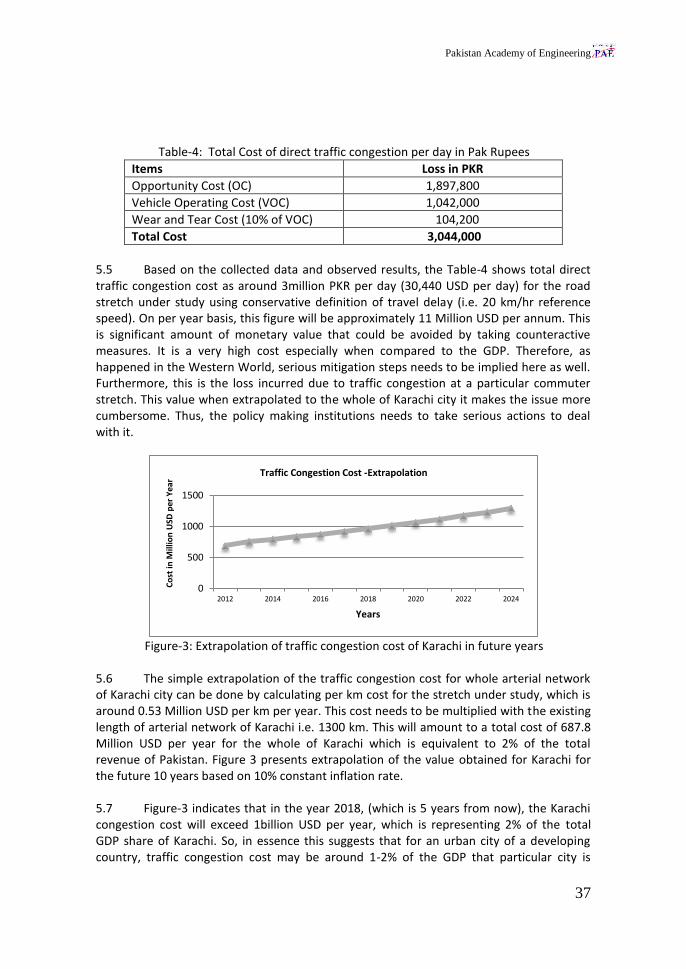

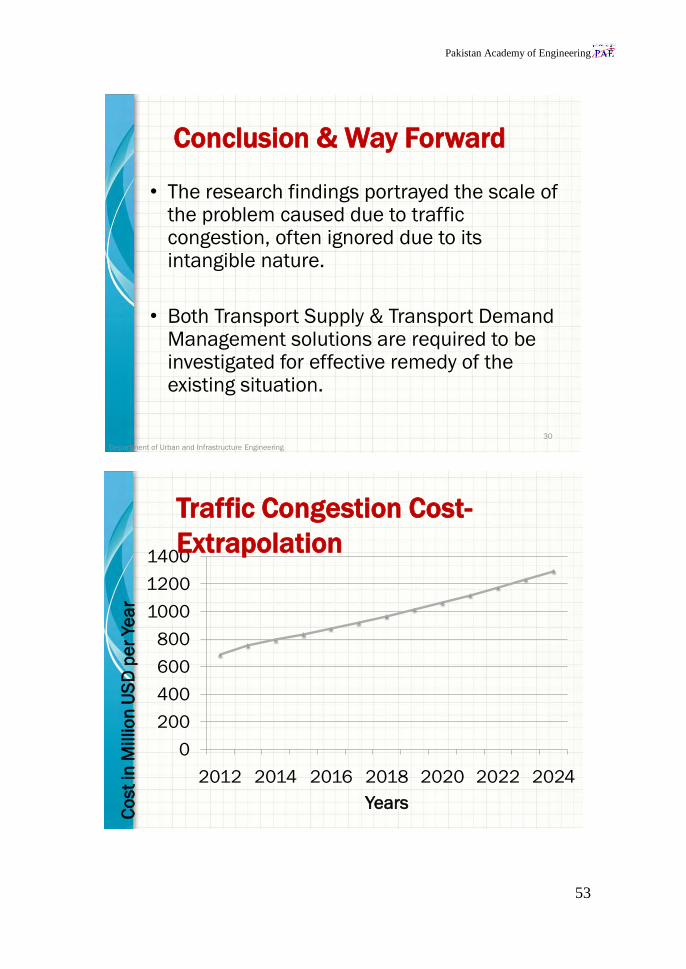

Figure-3: Extrapolation of traffic congestion cost of Karachi in future years

5.6 The simple extrapolation of the traffic congestion cost for whole arterial network of Karachi city can be done by calculating per km cost for the stretch under study, which is around 0.53 Million USD per km per year. This cost needs to be multiplied with the existing length of arterial network of Karachi i.e. 1300 km. This will amount to a total cost of 687.8 Million USD per year for the whole of Karachi which is equivalent to 2% of the total revenue of Pakistan. Figure 3 presents extrapolation of the value obtained for Karachi for the future 10 years based on 10% constant inflation rate. 5.7 Figure-3 indicates that in the year 2018, (which is 5 years from now), the Karachi congestion cost will exceed 1billion USD per year, which is representing 2% of the total GDP share of Karachi. So, in essence this suggests that for an urban city of a developing country, traffic congestion cost may be around 1-2% of the GDP that particular city is

0

500

1000

1500

2012 2014 2016 2018 2020 2022 2024

Co

st in

Mill

ion

USD

per

Yea

r

Years

Traffic Congestion Cost -Extrapolation

Pakistan Academy of Engineering

38

contributing. In this manner, four major urban cities GDP share is noted, and against that traffic congestion cost is estimated in the Table-5.

Table-5: Total Cost of direct traffic congestion for other cities in Pakistan

City GDP Share in Pakistan Economy (231 Billion USD)

Traffic Congestion Cost ( Billion USD per year)

Lahore 15% 0.519

Faisalabad Rawalpindi Multan

8% 1% 1%

0.277 0.030 0.030

6. CONCLUSIONS This research study estimated the traffic congestion cost of Karachi, a metropolis city of Pakistan. In addition to it also estimates the possible cost of traffic congestion in other large cities of Pakistan based on an assumed extrapolation strategy. This research is the first of its kind in the country, and paves way for further assessment in other parts of the country in order to find out the scale of the problem that is being caused by traffic congestion. The current and projected cost of this traffic congestion as compared with GDP demonstrates the importance of this problem. The policy making institutions needs to take serious actions to deal with it. Furthermore, this is the loss incurred directly due to traffic congestion and does not included the cost associated with environmental degradation cost. If this cost is also included it will gives a more horrifying picture. References [1] Goulias, K. G., 2003. Transportation system and Planning, Methods and Application. [2] Arnott, R., Small, K.A., 1994. The economics of traffic congestion. American Scientist 82,

p. 446. [3] McKinnon, A., 1999. The effect of traffic congestion on the efficiency of logistical

operations. International Journal of Logistics: Research and Applications 2 (2), p. 111. [4] Goodwin, P.B. and Dargay, J., 1999. Traffic congestion in Europe, OECD, ECMT Round

Table 110. [5] Thomson, I. and Bull, A., 2001. La congestion deltra´nsitourbano: causas y

consecuenciasecono´micas y 38ocials [Urban traffic congestion: economic and social causes and consequences]. Serie de RecursosNaturales e Infraestructura. Cepal. No. 25.

[6] Australian Government, Department of Transport and Regional service, Estimating urban traffic and congestion cost trends for Australian cities, work paper 71.

[7] Khan, T., and Islam, R. M., 2013. Estimating Costs of Traffic Congestion in Dhaka City, International Journal of Engineering Science and Innovative Technology (IJESIT), 2(3).

[8] Goodwin, P.B., 2004. The economic costs of road traffic congestion. London: University College London, ESRC Transport Studies Unit, Discussion Paper.

[9] Garrido, N. 2012. Computing the cost of traffic congestion: a micro simulation exercise of the City of Antofagasta, Chile, Transportation Planning and Technology.

[10] Hess, S., Bierlaire, M. and PolakJ.W., 2004. Estimation of value-of-time using mixed Logit Models, Technical Paper RO-040528.

[11]Adnan M., Ali,M.S. BaqueriS. F.A, Noman S.M, 2013, Estimation of Value of Time for commuters in Karachi, Fourth International Symposium on Infrastructure Engineering in Developing Countries, IEDC 2013.Submitted for publication.

Pakistan Academy of Engineering

39

PRESENTATION

Presentation Outlook

• Understanding the real issue

• Devising Methodology to gather information

• Data processing and results

• Macro scale results

• Conclusion and way forward

Department of Urban and Infrastructure

Engineering2

3

Department of Urban and Infrastructure Engineering

Significance of the issue

– How much these

frequent traffic jams

cost to society?

– Numbers required for

appropriate decision

making

– Realize cost impacts,

and consequences if

remedial measures are

not taken.

Pakistan Academy of Engineering

40

Economics of Traffic Congestion

• Urban traffic congestion imposes economic

costs which may expand outside metropolis

• business costs affects productivity and

output levels

• Industry sector is sensitive to traffic

congestion

• Transportation-based market area has

dependence on access to skilled labor,

access to specialized inputs.Department of Urban and Infrastructure Engineering 5

Pakistan Academy of Engineering

41

Traffic Congestion Cost

Beneficial for industries to ascertain

the role of traffic congestion in their

overall costing/budgeting

Effectiveness of congestion reduction

strategies can be identified.

Tax and Tariff rationalization

Urban development policy framework

Department of Urban and Infrastructure

Engineering6

DRIVING CYCLE ATTRIBUTESCity Highway High speed AC Cold temp

Trip typeLow speeds in stop-

and-go urban traffic

Free-flow

traffic at

highway

speeds

Higher

speeds;

harder

acceleration

& braking

AC use under

hot ambient

conditions

City test

w/colder

outside

temperature

Top speed 56 mph 60 mph 80 mph 54.8 mph 56 mph

Average speed 20 mph 48 mph 48 mph 22 mph 20 mph

Max.

acceleration3.3 mph/sec 3.2 mph/sec

8.46

mph/sec5.1 mph/sec

3.3

mph/sec

Simulated

distance11 mi. 10 mi. 8 mi. 3.6 mi. 11 mi.

Time 31 min. 12.5 min. 10 min. 9.9 min. 31 min.

Stops 23 None 4 5 23

Idling time 18% of time None 7% of time 19% of time18% of

time

Engine startupa Cold Warm Warm Warm Cold

Lab temperature 68-86oF 68-86 oF 68-86 oF 95 oF 20 oF

Vehicle air

conditioningOff Off Off On Off

Source: U.S. Department of Energy and U.S. Environmental Protection Agency

Pakistan Academy of Engineering

42

• Roadway Demand/Flow Level

• Roadway Geometric and Driver Characteristics

Traffic Congestion

•More than anticipated time for Journey

Travel Delays

• Opportunity Cost/ Lost Business

• Social CostEconomic

Cost

8

Department of Urban and Infrastructure Engineering

Research Methodology

JINNAH TERMINAL

MALIR HALT

MALIR

KALABOARDMALIR 15

QUAIDABAD

Y B CHORANGIFAST UNI STOP

BIN QASIM ROAD

PAKISTAN STEEL

9

Department of Urban and Infrastructure Engineering

Study Area

Sharea Faisal from Star gate intersection-Pakistan Steel intersection

Pakistan Academy of Engineering

43

7 INTERSECTIONS HOURS

STAR GATE 12

MALIR HALT 12

MALIR KALABOARD 16

MALIR 15 12

QUAIDABAD 12

MANZIL PUMP 12

FAST UNIVERSITY 12

PORT QASIM 16

PAKISTAN STEEL 12

9 SURVEY POINTS

2 MIDLINKS HOURS

QUAIDABAD 12

FAST UNIVERSITY 12

2 CONTROL POINTS

DATA WAS COILLECTED FOR 2

DAYS AT EACH POINT

Volume Data Collection

– Ascertaining the level of congestion

through key traffic parameters of a

selected road of Karachi

– Quantification of the cost of congestion

as a general estimate incorporating all

road users.

11

Department of Urban and Infrastructure Engineering

Key Deliverablesof the Research Project

Pakistan Academy of Engineering

44

Volume Data Collection

12

Method Used

-Instrumented Vehicle based video recording at

selected points

-2 control points are established where data

was collected for 16 hours (0800-2300hrs)

-10 hours data with the split of morning (0800-

1300hrs) and evening (1500-2000hrs)rush hours

at all locations except control points.

-Volume data were also collected during Ramadan at

control points.

-To capture effects of increased oil tanker movements,

this data was collected again at various spots of the

stretch.

Department of Urban and Infrastructure Engineering

INSTRUMENTED VEHILCE WAS USED FOR THIS PURPOSE

1. VOLUMETRIC COUNT

Volume Data Collection

Pakistan Academy of Engineering

45

14

Department of Urban and Infrastructure Engineering

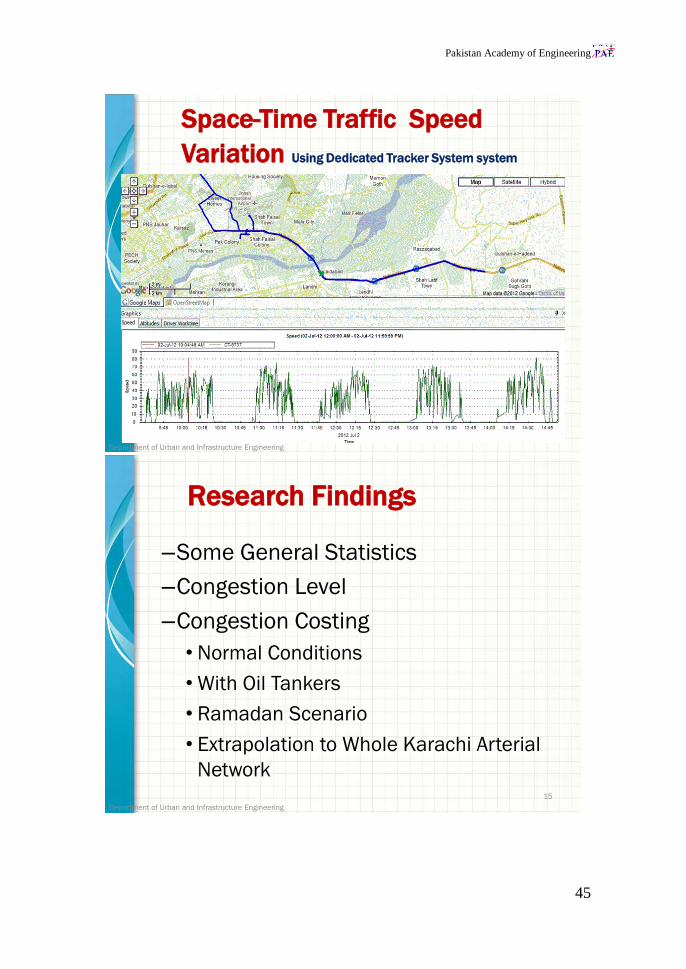

Space-Time Traffic Speed

Variation Using Dedicated Tracker System system

15

Department of Urban and Infrastructure Engineering

Research Findings

–Some General Statistics

–Congestion Level

–Congestion Costing

• Normal Conditions

• With Oil Tankers

• Ramadan Scenario

• Extrapolation to Whole Karachi Arterial

Network

Pakistan Academy of Engineering

46

Transport Modes Distribution

(Over the stretch length)

Department of Urban and Infrastructure Engineering 16

Car , 30%

Taxi, 8%

Office

Vans, 7%

Three –

Wheeler,

4%

Bike, 28%

Public

Transport

, 14%

Heavy

Vehicles

(Trucks),

8%

Car , 28%

Taxi,

5%

Office

Vans,

8%Three –

Wheeler,

1%

Bike,

7%

Public

Transport

, 12%

Heavy

Vehicles

(Trucks),

38%

ModesVolume

(veh/ day)

Vehicle

Occupancy

Car 2970 2.2

Taxi 481 3.2

Office Van 978 13

Three Wheeler 432 2

Motorcycle 3419 1.2

Public

Transport

1334 38

Truck 1188 4

Traffic Volume

and vehicle occupancy

Pakistan Academy of Engineering

47

Modes

Average

Speed

(km/ hr)

Avg. Delay

(Min/ Veh) at

ref. speed

20kph

Avg. Delay

(Min/ Veh) at

ref. speed

30kph

Car 50 8 10

Three

Wheeler

28 6.5 8.3

Motor Cycle 35 4 4.6

Buses 29 13.9 19.3

Truck 26 16.8 25

Average speed and average delay

under reference speed

19

Traffic Attributes

(Normal Conditions)Attributes Values Further Details

Average Daily Traffic 51,000 veh / day / direction 46,000 veh / day (Min)

60,900 veh / day (Max)

Morning peak Time: 8:30 – 9:30 am

Average: 2620 veh / hour

2510 veh / hour(Min)

2927 veh / hour (Max)

Capacity: 3400veh/hour (LOS

D)*

Evening peak Time: 5:30 – 6:30 pm

Average: 3550 veh / hour

3430 veh / hour (Min)

3700 veh / hour (Max)

Capacity: 3400 veh / hour (LOS

E)*

Average Delay (Off Peak)

(40 Km/hr –base

Reference speed)

16 min / trip 13 min / trip (Min)

18 min /trip (Max)

Average Delay (Peak)

(40 Km/hr –base

Reference speed)

25 min/ trip 22 min / trip (Min)

30 min/trip (Max)

Department of Urban and Infrastructure Engineering

Pakistan Academy of Engineering

48

Congestion Level

• Free-Flow Travel Time of the stretch has been

found as 17 minutes, corresponding to 70 km/hr

travel speed. (Design speed of the stretch is more

than 100 km/hr).

• Travel Time Index (TTI) has been estimated as

around 1.75 ~ 1.95, corresponding to avg. travel

time of more than 30 minutes.

• Roadway Congestion Index (RCI) was found as

2.36 for overall stretch.

Department of Urban and Infrastructure Engineering 20

Congestion Cost

Estimation

Department of Urban and Infrastructure Engineering 21

Pakistan Academy of Engineering

49

ECONOMIC COST

ECONOMIC COST

DIRECT COST INDIRECT COST

Cost beared directly by

the user

• Opportunity Cost

• Vehicle Operating Cost

• Cost incurred to

industries (loss in

business)

• Social cost

• Noise pollution

Project Focus

Economic COST

Department of Urban and Infrastructure Engineering

Vehicle operating cost

Congestion cost estimation

framework

Fuel Consumption (liters/km)

Opportunity cost

Pakistan Academy of Engineering

50

Value of Time (VOT)

Department of Urban and Infrastructure Engineering 24

Transport Mode Average Income

Group

Rs.

Avg. Value of

time (VOT)

Rs./hr

% in Sample Size

Car 50,000 – 80,000 87 10%

Taxi 50,000 – 80,000 80 5%

Office Van 30,000 – 50,000 75 48%

Motor Cycle 10,000 – 30,000 44 10%

Public

Transport

< 10,00034

25%

Truck 10,000-15,000 35 1%

Average 70.1

(0.7 US$)Value of time for India = 0.75 US$

Value of time for Bangladesh = 0.72 US$

Vehicle Operating Cost

• VOC is considered only in terms of fuel consumption.

• Fuel consumption parameters were gathered for different modes in terms of the following: – Vehicle fuel consumption in terms of Kg/Km and

Liters/km

– Estimated proportion of vehicles using different types of fuels such as CNG, Gasoline (Patrol) and Deisel

– Fuel Prices (Rs. /kg) or (Rs. /liter)

Department of Urban and Infrastructure

Engineering25

Pakistan Academy of Engineering

51

Modes VOT

(Rs/hr)

Car 87

Taxi 80

Office Van 75

Three Wheeler 60

Bike 44

Public Transport 34

Truck 35

Vehicle classified Value of time

Items Loss in PKR

Opportunity Cost (OC) 1,897,800

Vehicle Operating Cost

(VOC)

1,042,000

Wear and Tear Cost

(10% of VOC)

104,200

Total Cost 3,044,000

Total Cost of traffic congestion per

day in Pak Rupees

Pakistan Academy of Engineering

52

Spot Contributions

S.

NoSpot Reason

Current

Contribution

(Million

PKR/Day)

Impact After

5 Years

(Million

PKR/Day)

1Malir 15

Intersection

Encroachment,

Improper Traffic

Management

2.51 3.35

2 Railway Crossing

Access point,

Manual Traffic

Management

0.68 1.02

3

Illegal Parking of

Oil Tanker near

Port Qasim

Encroachment,

Lane blocking3.09 20.6

4Encroachment at

Ganchi Market

Encroachment

Decrease in ROW0.26 0.65

Department of Urban and Infrastructure Engineering28

Karachi Congestion Cost-

Extrapolated• According to results obtained from this study, per km

cost of traffic congestion is around 0.51 million PKR /day, which is significantly high.

• If extrapolation is made for the whole Karachi metropolitan (for arterial stretch of around 1300 km) this will surpass the figure of 663 Million PKR per day (annually around 2.5 Billion US dollars).

• This suggests that authorities need to find feasible solutions to reduce this cost, which is in principle non-tangible cost and easily avoidable.

Department of Urban and Infrastructure Engineering

29

Pakistan Academy of Engineering

53

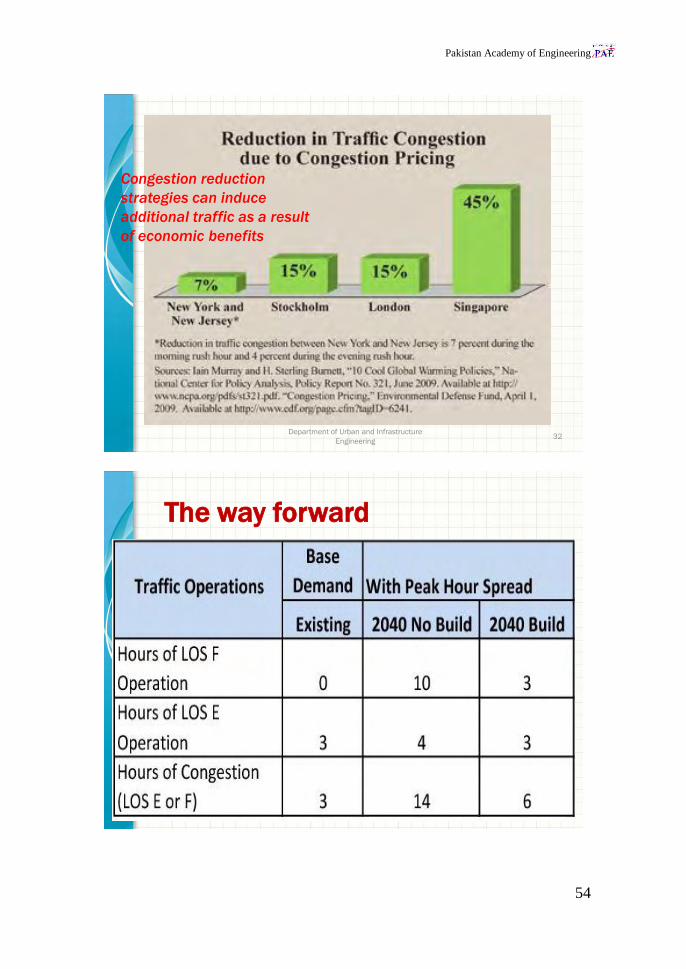

Conclusion & Way Forward

• The research findings portrayed the scale of the problem caused due to traffic congestion, often ignored due to its intangible nature.

• Both Transport Supply & Transport Demand Management solutions are required to be investigated for effective remedy of the existing situation.

Department of Urban and Infrastructure Engineering

30

0

200

400

600

800

1000

1200

1400

2012 2014 2016 2018 2020 2022 2024

Co

st