Embed Size (px)

Citation preview

Profiles of HSA Users

Roy Ramthun

April 2014

Meet RoyMr. HSA

1. Common myths about HDHPs & HSAs

2. Distinct profiles of HSA holders

3. How to use HSA profiles to your

advantage

Topics: What will we cover?

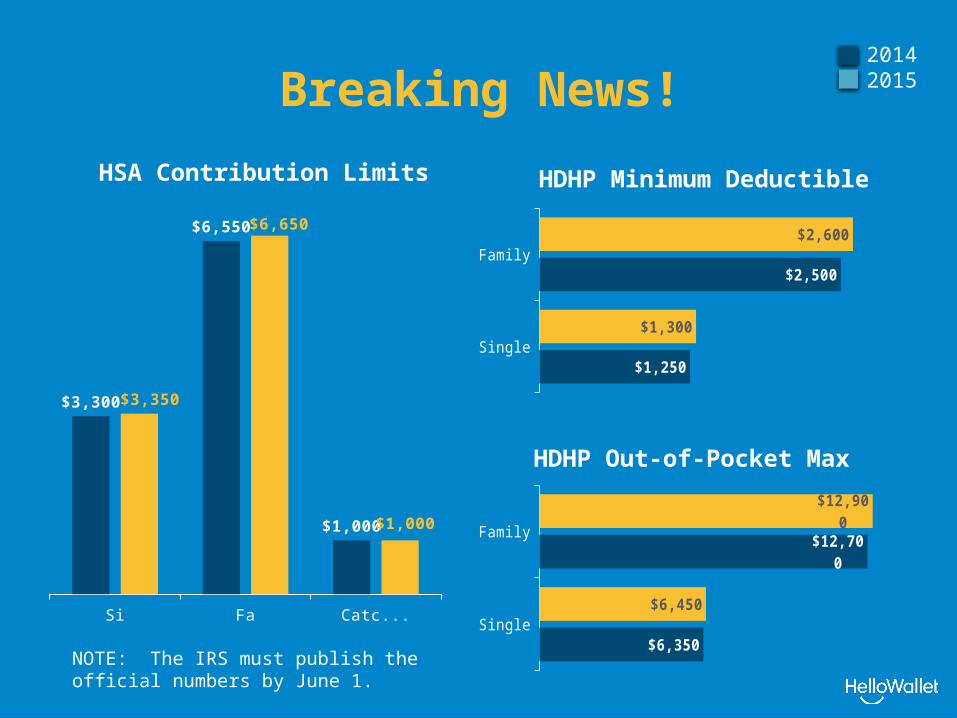

Breaking News!

Single Family Catch-Up

$3,300

$6,550

$1,000

$3,350

$6,650

$1,000

Single

Family

$1,250

$2,500

$1,300

$2,600

Single

Family

$6,350

$12,700

$6,450

$12,900

HSA Contribution Limits HDHP Minimum Deductible

HDHP Out-of-Pocket Max

NOTE: The IRS must publish the official numbers by June 1.

20142015

Common Myths

“HDHPs/HSAs are only good for healthy people”

MYTH #1

HSAs Are Good for Sick People, Too!

o Preventive care is exempt from the deductible• Disease management costs are not

o Catastrophic limits provide real protection• Limits apply to all covered benefits, including Rx• Limits cannot exceed (for 2014):

• $6,350 for singles• $12,700 for families• ACA adopted these limits for all plans for 2014

HSA vs. ACA Limits: 2015

Family

Single$6,450

$6,600

$12,900

$13,200

“HDHPs/HSAs are only good for young people”

MYTH #2

HDHP Enrollment Data

0-1927%

20-2912%

30-3913%

40-4918%

50-5921%

60+10%

Age distribution of people covered by HSA-qualified HDHPs, Individual Market, January 2013

“HDHPs/HSAs are only good for wealthy people”

MYTH #3

HSA Tax Deduction Data

o Average tax deduction/return = $3,051• < $50,000 -- $2,075• $50,000 - $100,000 -- $2,410• > $100,000 -- $3,936

o Percent of Returns, by income group• < $50,000 – 23%• $50,000 - $100,000 – 30%• > $100,000 – 47%

Source = IRS Statistics of Income Bulletin (Winter 2014), data from 2012 tax returns

HSA Enrollment Data

o 15.5M Americans enrolled in HDHPs

o 10.7M HSA accounts

o $19.3B in assets in HSA accounts (only $2.3B invested)

o $2,356 = average funded HSA account balance as of 12/13

Source = Devenir, data as of 12/31/13

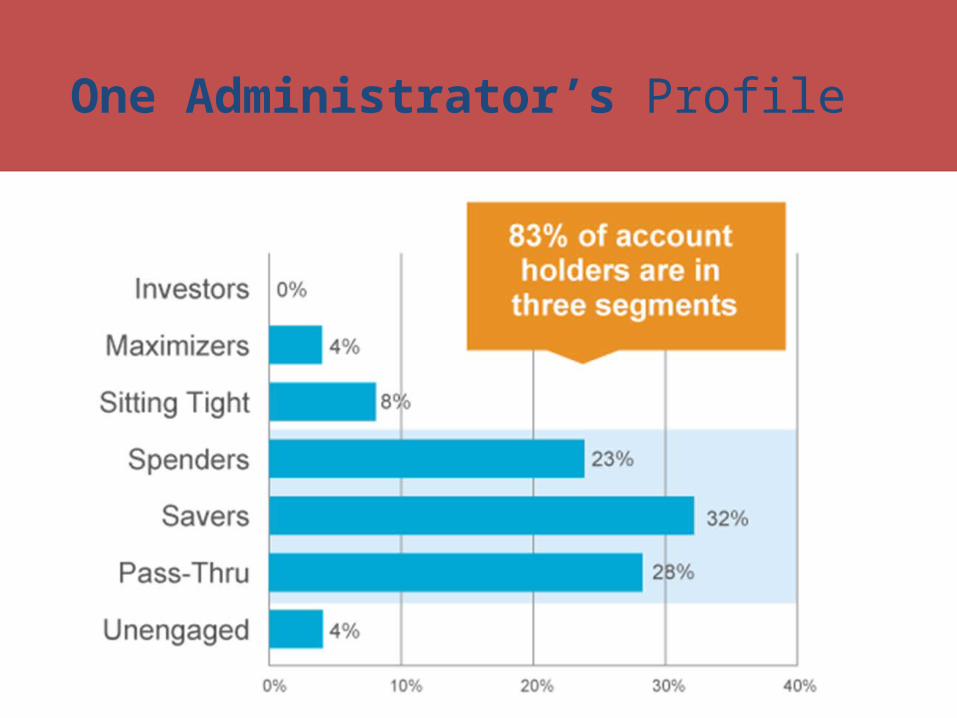

Participant Profiles

HSA Account Holders

UnengagedSitting Tight

Pass-Thru Spender

Saver Maximizer Investor

Unengaged

Sitting Tight

Pass-Thru

Spender

Saver

Maximizer

Investor

One Administrator’s Profile

HSA Experience Matters

HSA Investments, Low but Growing

Employer Strategies

EMPLOYER STRATEGIES To Help Sick & Low Paid Employees

o HSA funding – amount & timing

o HRA funding – post-deductible

o Cafeteria plan benefits• FSAs, wellness programs, disease management

programs, supplemental insurance

o Support – education & communication

EMPLOYER STRATEGIES

Don’t Undersell the HDHP

o Most employees assume HDHPs offer inferior coverage• Premium savings

o HSA funding can actually lead to a richer plan than before (i.e., higher actuarial value)• “Bronze” HDHP (AV = 62.0%)

AV with $500 contribution = 68.0% AV with $1,000 contribution = 73.6% AV with $2,000 contribution = 82.4%

EMPLOYER STRATEGIES

To Help Young Employees

Communicate the power of compound interest

EMPLOYER STRATEGIES

Measure Engagement

What data can help measure “engagement?”

• How many employees never opened their HSA?

• How many employees are not contributing any personal money to their HSA?

• How many employees are spending every dollar contributed (i.e., minimal or zero balance)?

• Are average balances or ?

• Does changing the employer contribution amount or timing affect employee behavior?

EMPLOYER STRATEGIES

Make Data Work for You

o The more employers know about their employees, the more they can:

• Improve employee well-being

• Reduce costs

• Generate positive experience

o Meaningful, usable data can help employers:

• Understand employee “engagement”

• Drive or align plan strategies

o If your HSA administrator cannot provide good data, it might be time to switch

EMPLOYER STRATEGIES

Leverage Personalization

Employee Strategies

EMPLOYEE STRATEGIES

How to Fund the HSA

o Many people can contribute more than their out-of-pocket risk

o Take advantage of employer matching contributions, if offered

o Pay attention to employer incentives that may increase contributions

o Don’t forget to factor in tax savings• Making contributions via payroll deduction is best

o If uncertain how much to contribute, use the “look back” method

o Ask questions – NEVER assume!

Questions?

Thank You!

![HSA Stud anchor - Hilti - Hilti Saudi Arabia€¦ · HSA Stud anchor 6 11 / 2016 Geometry washer Anchor Size M6 M8 M10 M12 M16 M20 Inner diameter d 1 HSA, HSA-R2/ R, HSA-F d 1 [mm]](https://img.pdfslide.us/doc/110x75/5b61cb307f8b9a09498cd093/hsa-stud-anchor-hilti-hilti-saudi-arabia-hsa-stud-anchor-6-11-2016-geometry.jpg)