Embed Size (px)

Citation preview

Professional Liability and the Need for Quality Auditor Judgments and

Ethical Decisions

Learning Objectives

Articulate a framework for professional decisions

Define ethics and ethical theories Identify the two parts of the AICPA Code of

Professional Conduct Describe the AICPA (and IESBA) principles of

professional conduct Discuss each of the rules of conduct of the

AICPA, as well as the PCAOB & SEC’s independence rules

Describe the enforcement procedures for the Code of Professional Conduct

Describe monitoring of public accounting firms

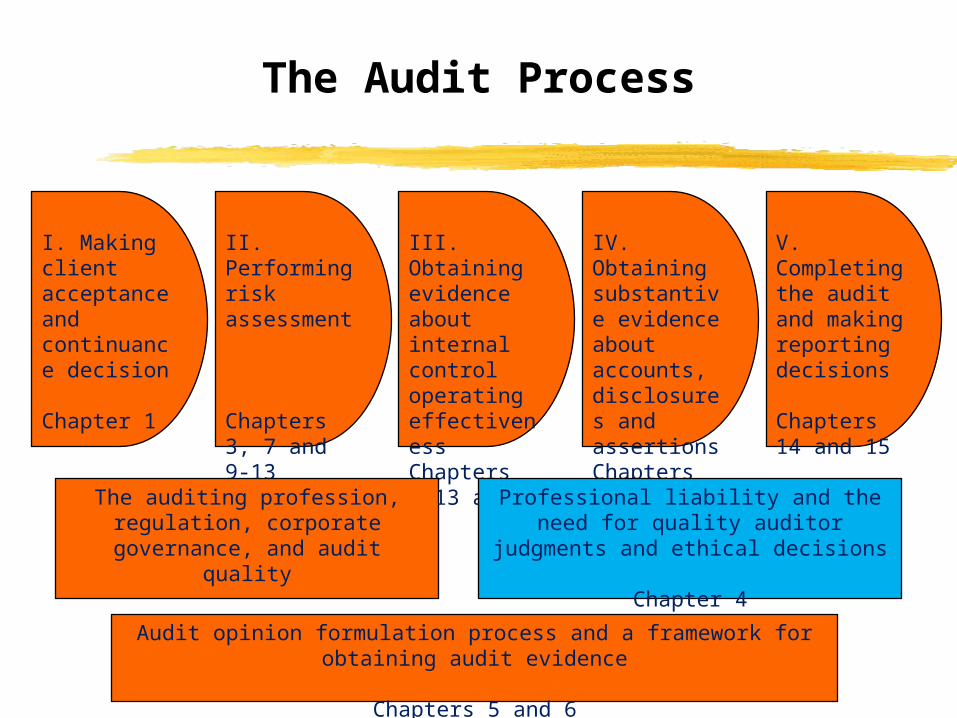

The Audit Process

I. Making client acceptance and continuance decision

Chapter 1

II. Performing risk assessment

Chapters 3, 7 and 9-13

III. Obtaining evidence about internal control operating effectivenessChapters 8-13 and 16

IV. Obtaining substantive evidence about accounts, disclosures and assertionsChapters 8-13 and 16

V. Completing the audit and making reporting decisions

Chapters 14 and 15

The auditing profession, regulation, corporate governance, and audit quality

Chapters 1 and 2

Professional liability and the need for quality auditor judgments and ethical decisions

Chapter 4

Audit opinion formulation process and a framework for obtaining audit evidence

Chapters 5 and 6

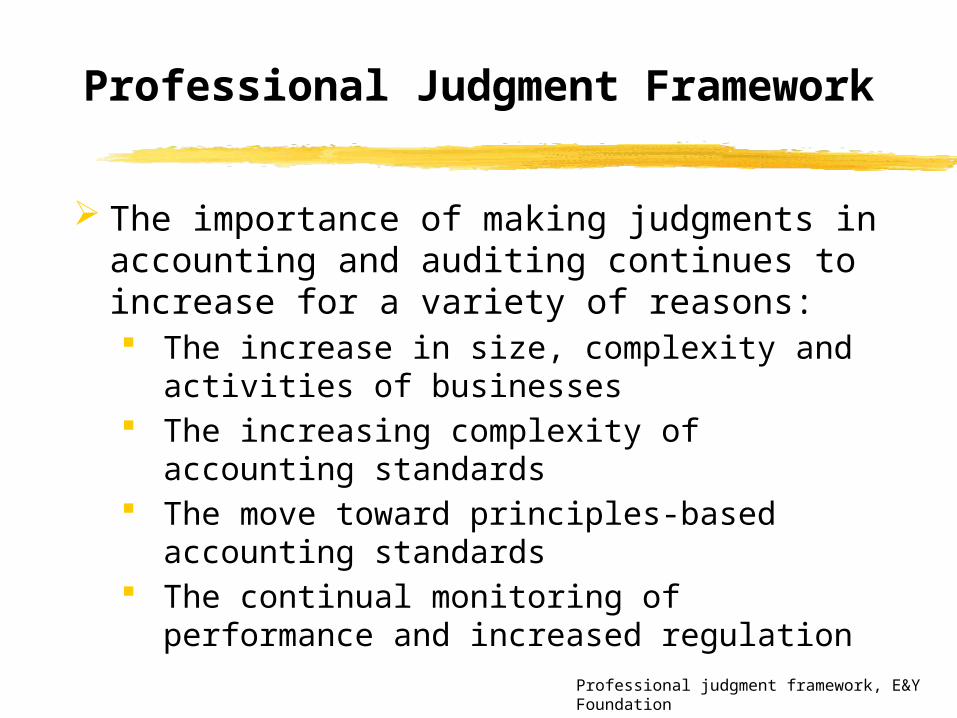

Professional Judgment Framework

The importance of making judgments in accounting and auditing continues to increase for a variety of reasons: The increase in size, complexity and activities

of businesses The increasing complexity of accounting

standards The move toward principles-based accounting

standards The continual monitoring of performance and

increased regulationProfessional judgment framework, E&Y Foundation

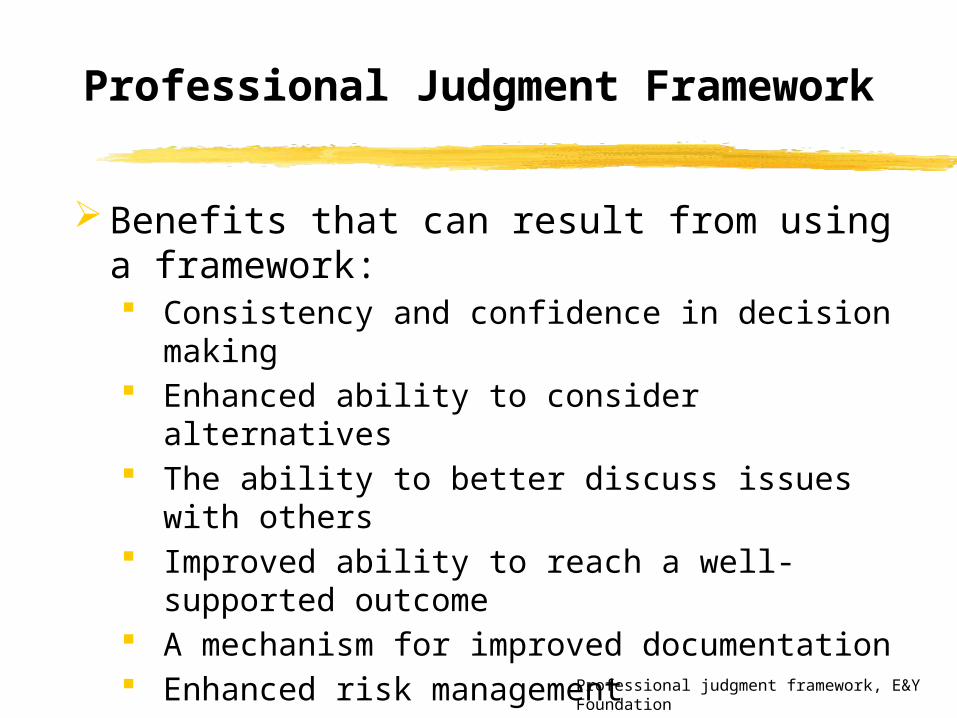

Professional Judgment Framework

Benefits that can result from using a framework: Consistency and confidence in decision

making Enhanced ability to consider alternatives The ability to better discuss issues with

others Improved ability to reach a well-supported

outcome A mechanism for improved documentation Enhanced risk management Better communication when consulting with

others

Professional judgment framework, E&Y Foundation

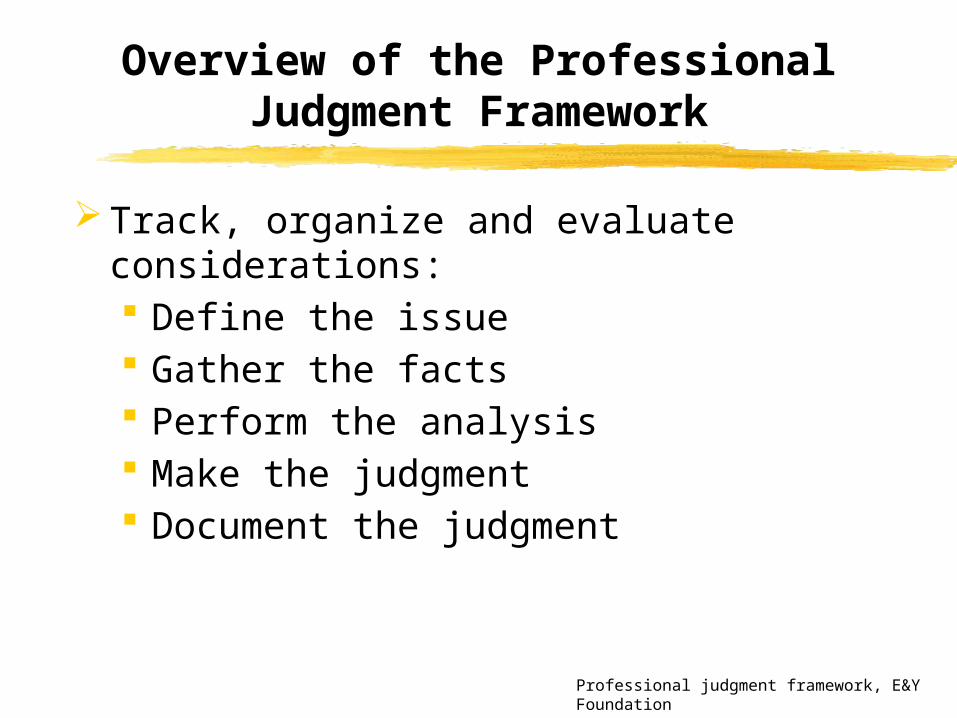

Overview of the Professional Judgment Framework

Track, organize and evaluate considerations: Define the issue Gather the facts Perform the analysis Make the judgment Document the judgment

Professional judgment framework, E&Y Foundation

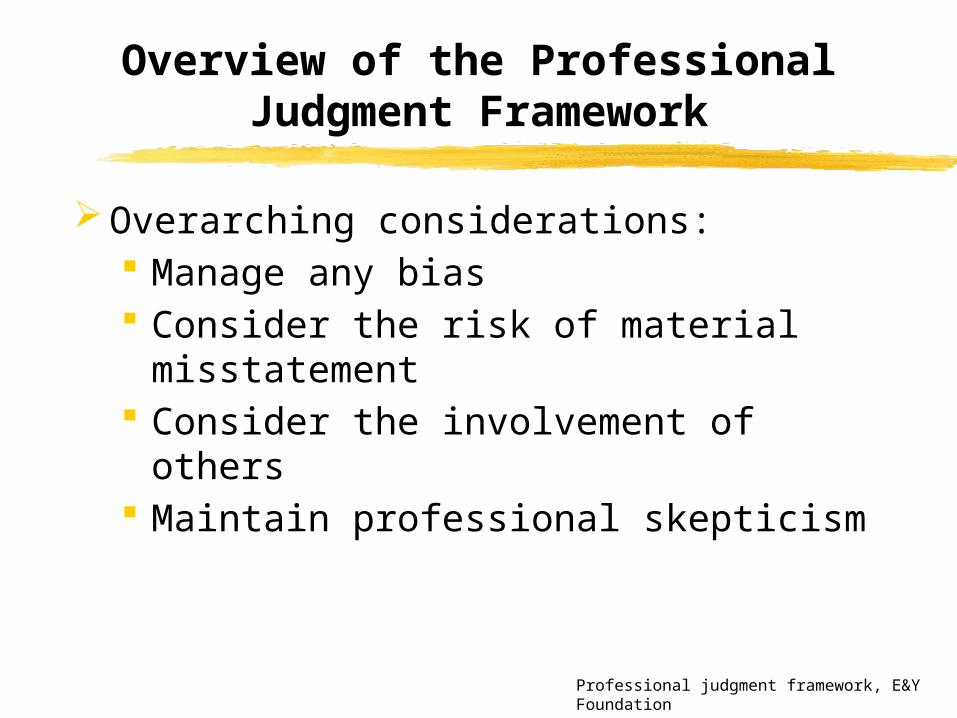

Overview of the Professional Judgment Framework

Overarching considerations: Manage any bias Consider the risk of material

misstatement Consider the involvement of others Maintain professional skepticism

Professional judgment framework, E&Y Foundation

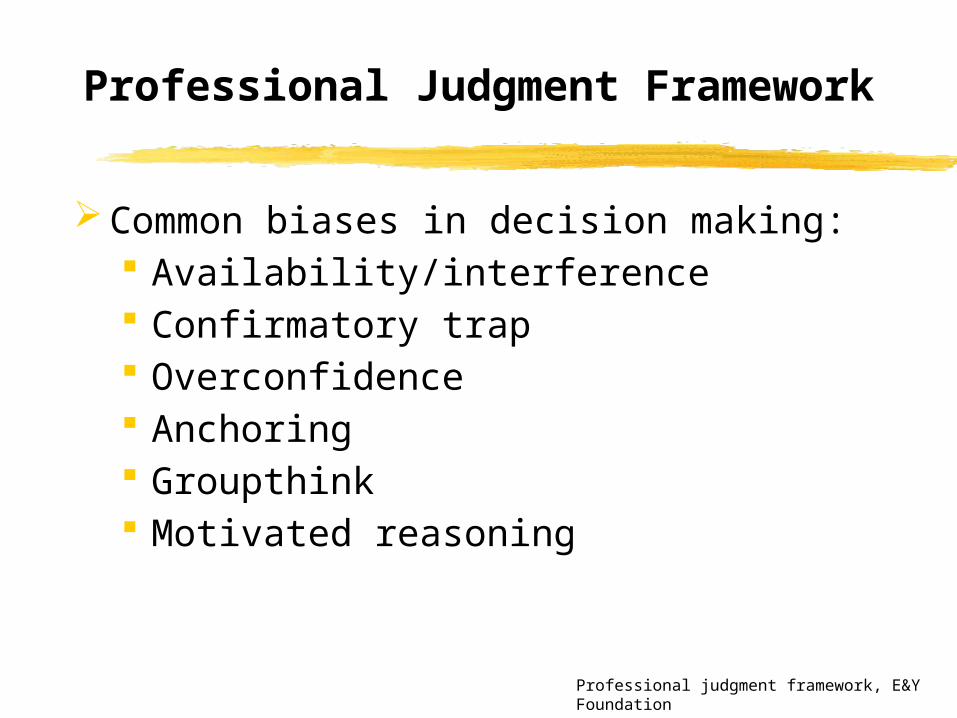

Professional Judgment Framework

Common biases in decision making: Availability/interference Confirmatory trap Overconfidence Anchoring Groupthink Motivated reasoning

Professional judgment framework, E&Y Foundation

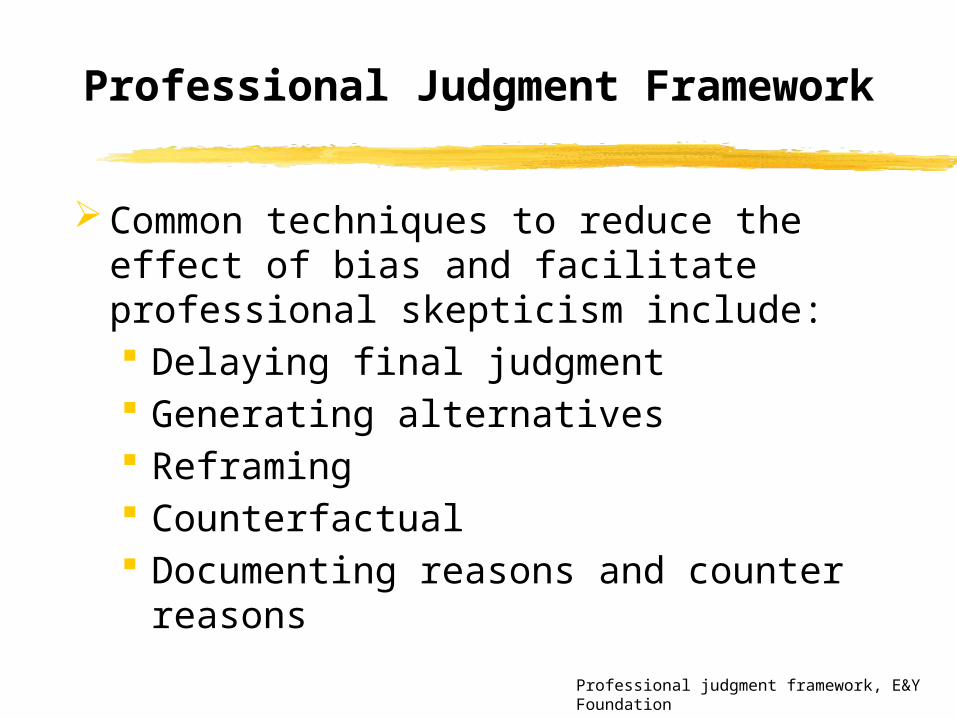

Professional Judgment Framework

Common techniques to reduce the effect of bias and facilitate professional skepticism include: Delaying final judgment Generating alternatives Reframing Counterfactual Documenting reasons and counter

reasons

Professional judgment framework, E&Y Foundation

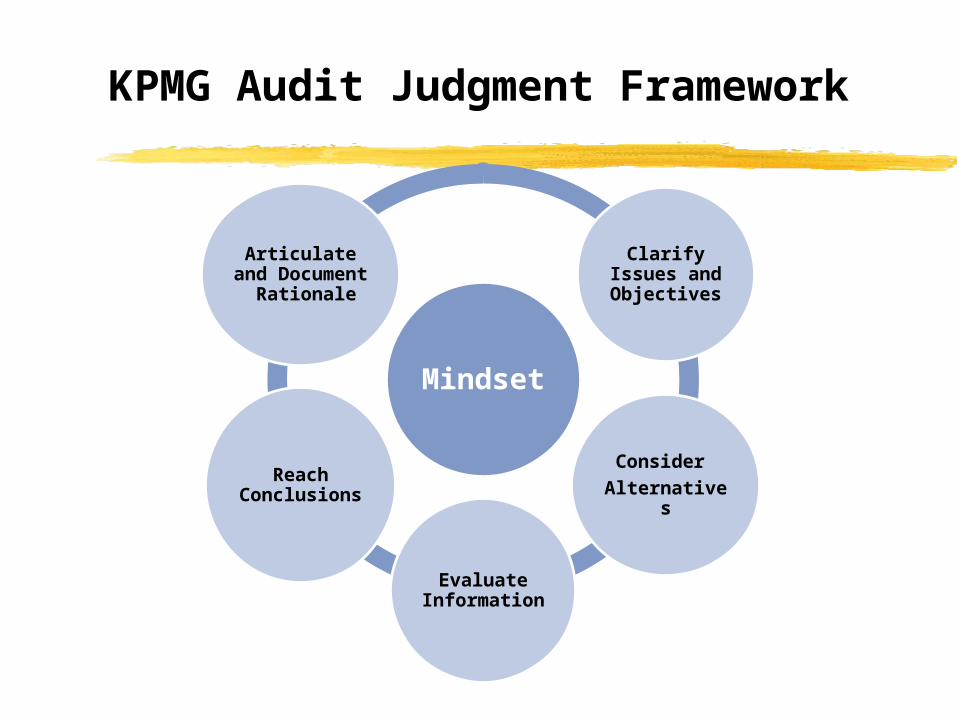

KPMG Audit Judgment Framework

Mindset

Clarify Issues and Objectives

Consider Alternatives

Evaluate Information

Reach Conclusions

Articulate and

Document Rationale

Ethics Defined

The term ethics in the philosophical sense refers to the set of moral standards for right or wrong that a person, a group, or a society develops.

Each person, group, or society uses moral reasoning to decide whether or not an action is ethical, i.e., to make an ethical decision.

Ethical Theories

Ethical decisions are guided by ethical theories, which can be explained by simple maxims: The utilitarian theory The rights theory The golden rule Kant’s categorical The professional ethics

A Framework for Ethical Decision Making

In applying ethical theories, the use of a checklist or a framework can be helpful.1. What are the relevant facts?2. What is the ethical issue/decision?3. What alternative courses of action are

available?4. What are the consequences of alternative

actions?5. What is the appropriate action?

Professional Ethics

Professional ethics differ from general/individual ethics in that they emphasize right and wrong behavior for members of a profession. They are much more specific.

Why do most professions have a code of ethics? Professions have a responsibility to provide

quality service. The body of knowledge in a profession is

complex. The public relies on the profession. Professions assume self-discipline beyond the

requirements of law.

The IESBA Code of Ethics

The IESBA Code of Ethics require accountants to adhere to five fundamental principles: IntegrityObjectivityProfessional Competence and Due CareConfidentialityProfessional Behavior

AICPA Code of Professional Conduct

The AICPA Code of Professional Conduct has two sections:

Principles. Principles are goals or ideal professional and ethical conduct by CPAs. They are not enforceable.

Rules. Rules reflect the principles. They are the min. standards of the profession & are enforceable.

The bylaws of the AICPA give authority to the Professional Ethics Executive Committee to interpret the rules and issue rulings (enforceable).

AICPA Code of Professional Conduct

In June 2014, the Professional Ethics Executive Committee (PEEC) adopted a revised Code, with an effective date of December 15, 2014, to converge the Code with the International Ethics Standards Board (IESBA) Code. The revised code is a codification of the existing principles, rules, interpretations, and rulings.

Additionally, the Code includes two conceptual frameworks (effective 2015) that members can use when facing circumstances not explicitly addressed by the Code.

Principles of the Code of Professional Conduct

1. CPA’s responsibilities (0.300.020) Members should exercise sensitive

professional and moral judgments in all activities

2. The public interest (0.300.030) Act in a way that will serve the public

interest, honor the public trust, and demonstrate commitment to professionalism

3. Integrity (0.300.040) Perform all professional responsibilities with

the highest sense of honesty and candidness

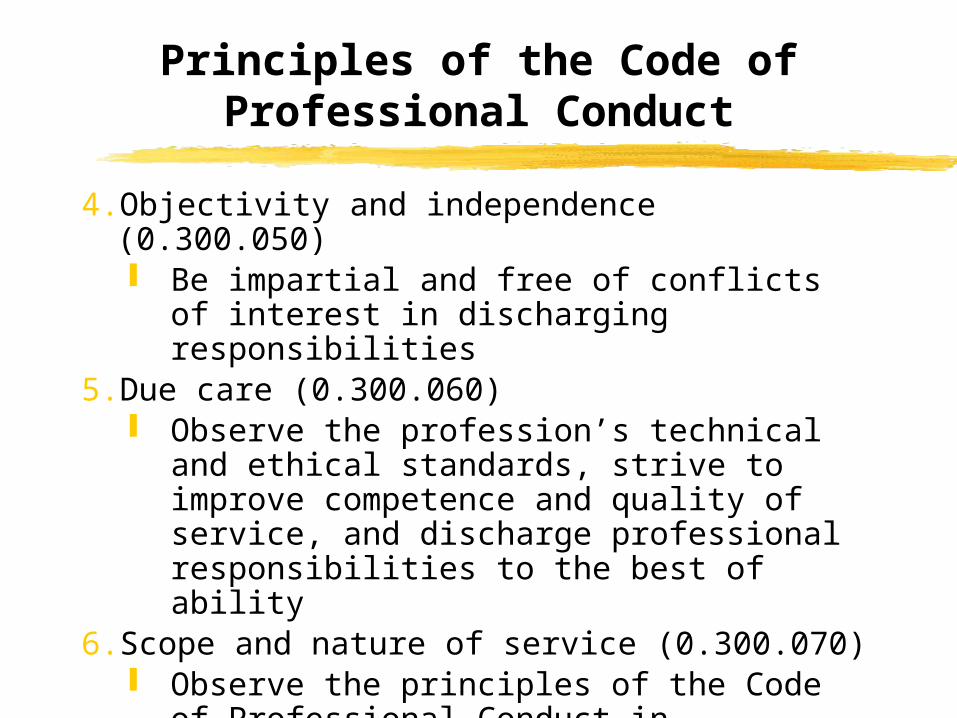

Principles of the Code of Professional Conduct

4. Objectivity and independence (0.300.050) Be impartial and free of conflicts of interest

in discharging responsibilities5. Due care (0.300.060)

Observe the profession’s technical and ethical standards, strive to improve competence and quality of service, and discharge professional responsibilities to the best of ability

6. Scope and nature of service (0.300.070) Observe the principles of the Code of

Professional Conduct in determining the nature and the scope of services to be provided

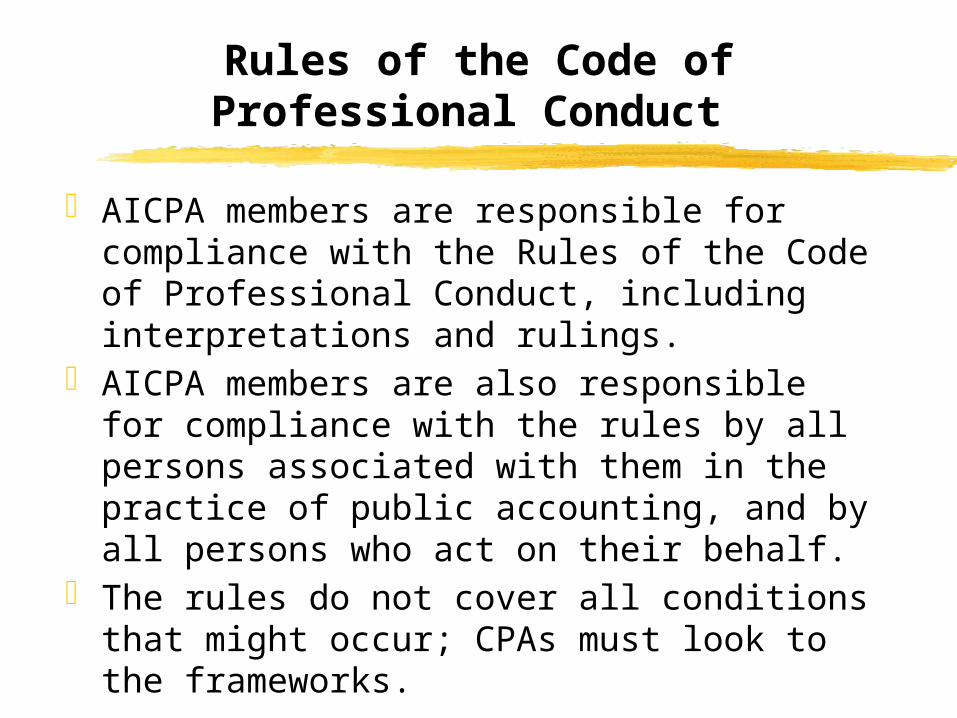

Rules of the Code of Professional Conduct

AICPA members are responsible for compliance with the Rules of the Code of Professional Conduct, including interpretations and rulings.

AICPA members are also responsible for compliance with the rules by all persons associated with them in the practice of public accounting, and by all persons who act on their behalf.

The rules do not cover all conditions that might occur; CPAs must look to the frameworks.

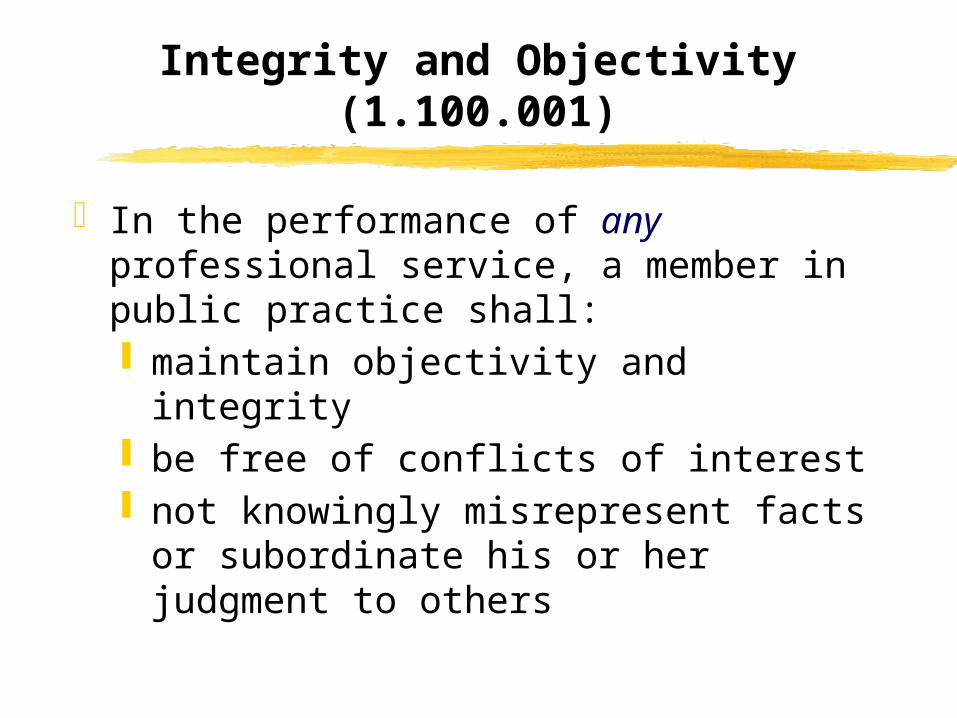

Integrity and Objectivity (1.100.001)

In the performance of any professional service, a member in public practice shall: maintain objectivity and integrity be free of conflicts of interest not knowingly misrepresent facts or

subordinate his or her judgment to others

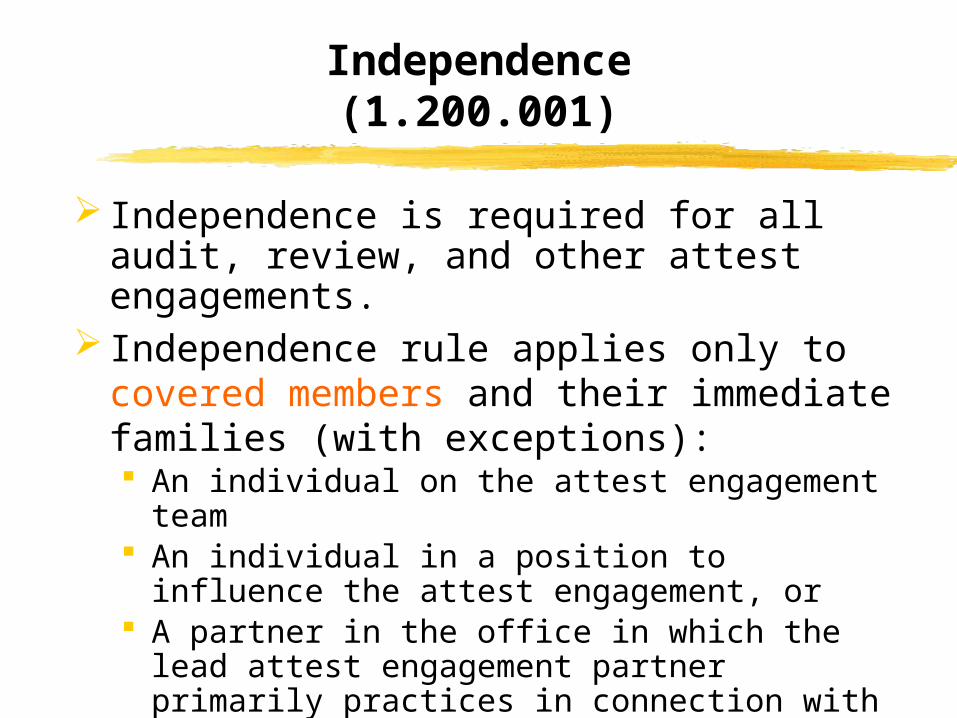

Independence(1.200.001)

Independence is required for all audit, review, and other attest engagements.

Independence rule applies only to covered members and their immediate families (with exceptions): An individual on the attest engagement team An individual in a position to influence the

attest engagement, or A partner in the office in which the lead attest

engagement partner primarily practices in connection with the attest engagement

Independence – Financial Interest (1.240.010)

Independence is considered impaired if during the period of the professional engagement:

a covered member had or was committed to acquire any direct or material indirect financial interest in the client;

a covered member was a trustee of any trust or executor or administrator of any estate if such trust or estate had or was committed to acquire ...;

a partner or professional employee of the firm, his or her immediate family, or together, had more than a 5 percent ownership interest in a client.

Direct and Indirect Financial Interest - Definition

A direct financial interest is: Owned directly by an individual or entity; or Under the control of an individual or entity; or Beneficially owned through an intermediary

(e.g., an investment vehicle, estate, trust) when beneficiary:

• Controls the intermediary; or• Has the authority to supervise or participate in the

intermediary’s investment decisions.

An Indirect financial interest is: beneficially owned but the beneficiary neither

controls the intermediary nor has the authority to supervise or participate in the intermediary’s investment decisions.

Independence – Loans, Leases, and Guarantees (1.260.010)

Independence is considered impaired if during the period of professional engagement a covered member had any loan to or from the client or any officer, director, or a stockholder with more than a 10% ownership interest, except as specifically permitted.

Permitted Loans:• Unsecured loans not material to covered member’s net

worth• Fully collateralized automobile loans and leases and

mortgages• Loans fully collateralized by cash surrender value of an

insurance policy or by cash deposits at the financial institution

• Credit cards and overdraft reserve accounts that are reduced to $10,000 or less on a current basis

Independence – Joint Closely Held Investments (1.265.020)

Independence is considered impaired if during the period of the professional engagement a covered member had any joint, closely held investment that was material to the covered member’s net worth.

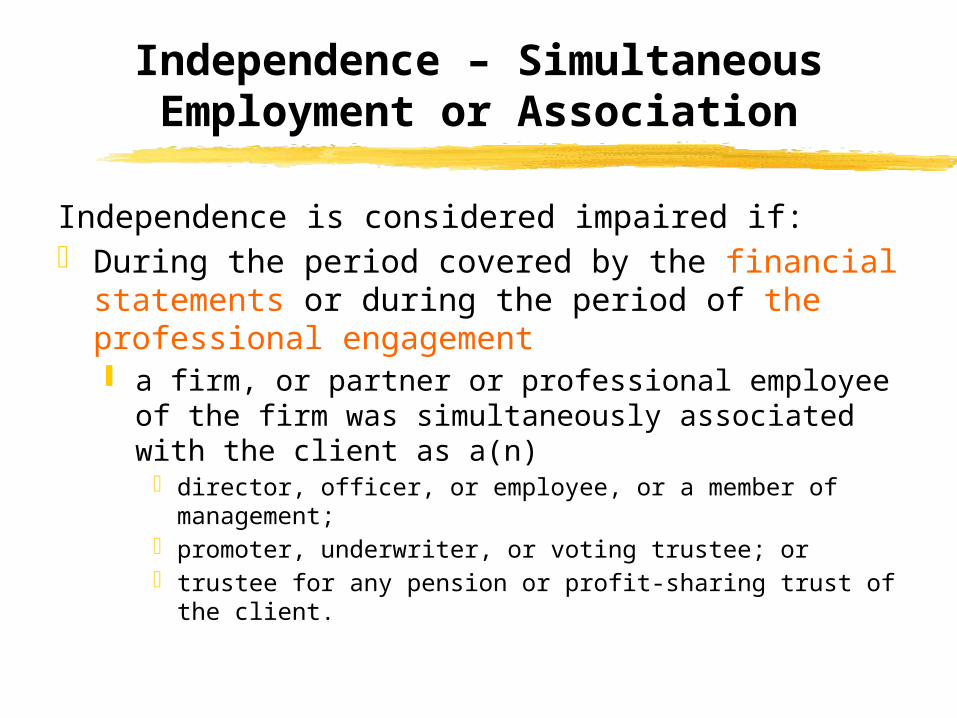

Independence – Simultaneous Employment or Association

Independence is considered impaired if: During the period covered by the financial

statements or during the period of the professional engagement a firm, or partner or professional employee of the

firm was simultaneously associated with the client as a(n)

director, officer, or employee, or a member of management; promoter, underwriter, or voting trustee; or trustee for any pension or profit-sharing trust of the client.

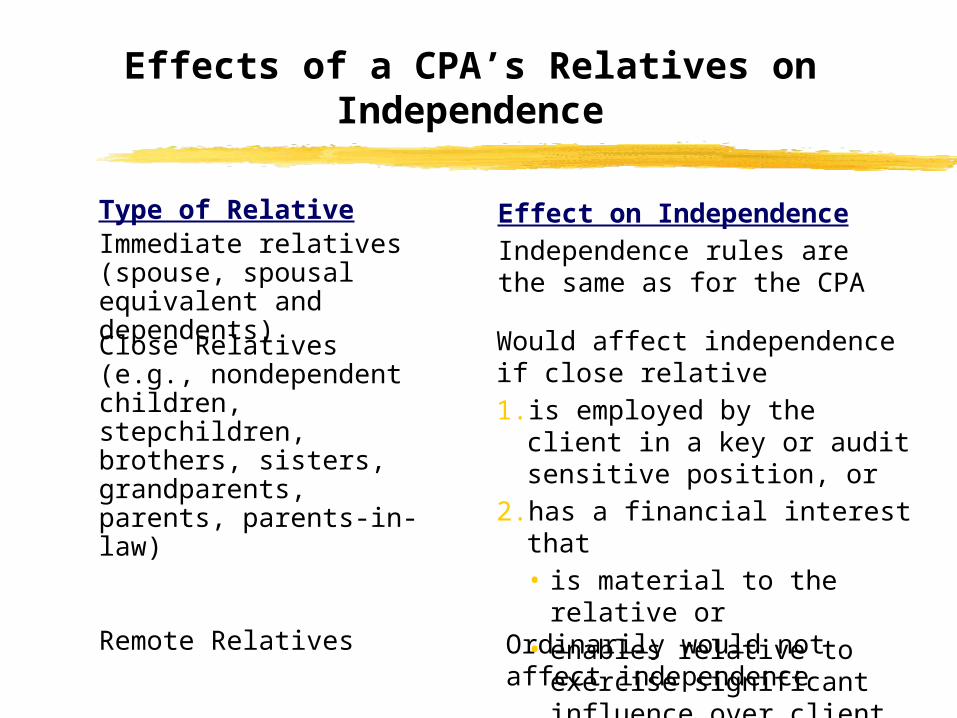

Effects of a CPA’s Relatives on Independence

Type of RelativeImmediate relatives (spouse, spousal equivalent and dependents)

Effect on IndependenceIndependence rules are the same as for the CPA

Close Relatives(e.g., nondependent children, stepchildren, brothers, sisters, grandparents, parents, parents-in-law)

Would affect independence if close relative1. is employed by the client in

a key or audit sensitive position, or

2. has a financial interest that• is material to the relative

or• enables relative to

exercise significant influence over client

Remote Relatives Ordinarily would not affect independence

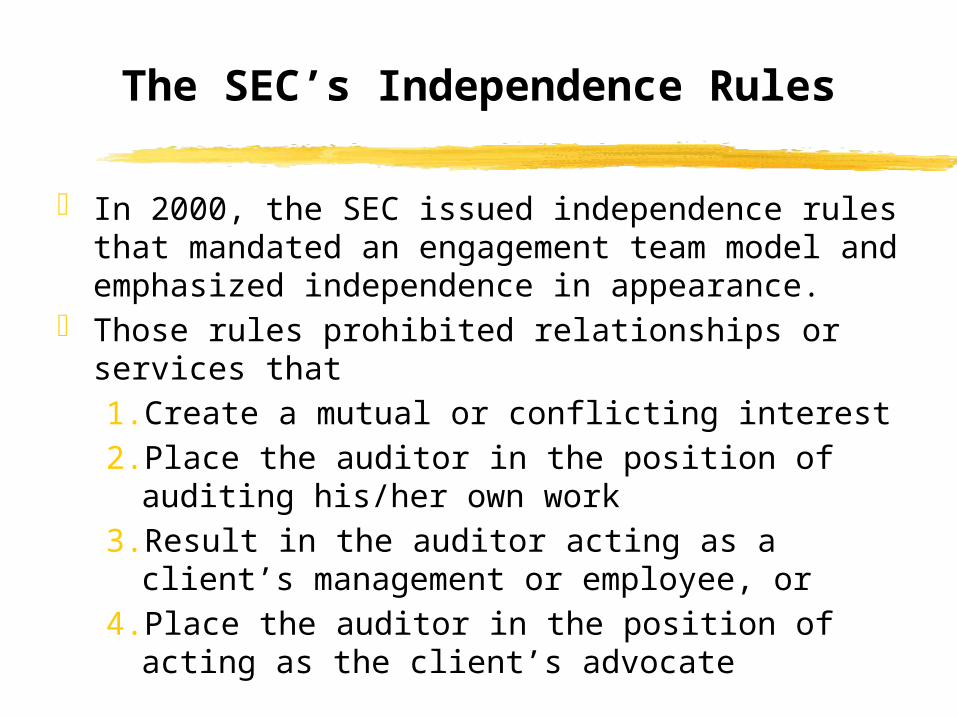

The SEC’s Independence Rules

In 2000, the SEC issued independence rules that mandated an engagement team model and emphasized independence in appearance.

Those rules prohibited relationships or services that1. Create a mutual or conflicting interest2. Place the auditor in the position of auditing

his/her own work3. Result in the auditor acting as a client’s

management or employee, or4. Place the auditor in the position of acting as the

client’s advocate

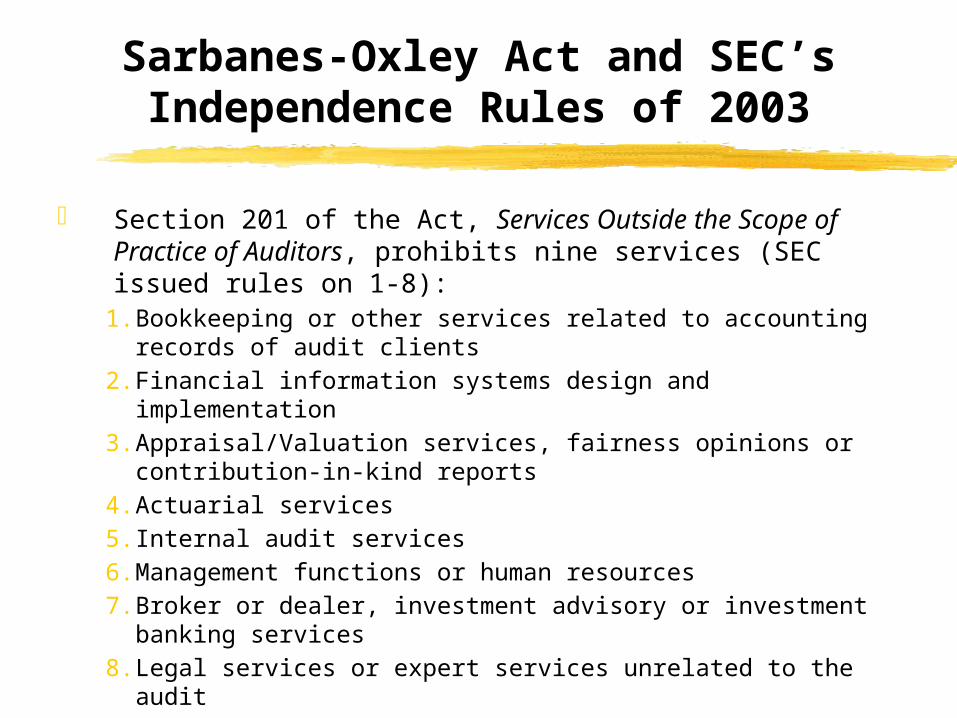

Sarbanes-Oxley Act and SEC’s Independence Rules of 2003

Section 201 of the Act, Services Outside the Scope of Practice of Auditors, prohibits nine services (SEC issued rules on 1-8):

1. Bookkeeping or other services related to accounting records of audit clients

2. Financial information systems design and implementation3. Appraisal/Valuation services, fairness opinions or contribution-

in-kind reports4. Actuarial services5. Internal audit services6. Management functions or human resources7. Broker or dealer, investment advisory or investment banking

services8. Legal services or expert services unrelated to the audit9. Any other service that the Board (PCAOB) determines is

impermissible Other services have to be approved by client’s BOD in

advance.

Sarbanes-Oxley Act and the SEC’s Independence Rules

In addition to revising rules for provision of non-audit services, and requiring that the audit committee pre-approve all audit and non-audit services the auditor provides, in January 2003 the SEC issued new rules that1. Require rotation of lead and concurring Partners

after no more than five years2. Prohibit accounting firms from auditing a client

which employs one of the client’s former auditors within the one-year period preceding the audit

3. Prohibit partners from earning compensation from selling non-attest services to an audit client

General Standard(1.300.001)

A member shall comply with the following standards: Professional competence Due professional care Planning and supervision Sufficient relevant data

Compliance With Standards(1.300.001)

A member who performs professional services shall comply with the standards promulgated by bodies designated by the council.

Accounting Principles(1.320.001)

A member shall not: affirm that financial data or statements are in

conformity with GAAP, or state that he or she is not aware of any

material modifications that should be made for the financial statements to be in conformity with GAAP,

if such data or statements contain any departuresfrom GAAP

Acts Discreditable(1.400.001)

A member shall not commit an act discreditable to the profession.

Discreditable acts include: Retention of client records (not CPA’s work

paper) by a CPA after a demand is made for them

Violation of any anti-discriminatory laws of the US, a state, or municipality

Soliciting or knowingly disclosing CPA exam questions or answers

Contingent Fees(1.510.001)

A member in public practice shall not:a. Performs for a contingent fee

i. an audit or review of financial statements

ii. a compilation of financial statements that are expected to be used by a third party and the compilation report does not disclose a lack of independence

iii. an examination of prospective financial information

b. Prepare an original or amended tax return or claim for a tax refund for a contingent fee for any client

Commissions and Referral Fees(1.520.001)

A member in public practice who is engaged to perform attestation services in Contingent Fees rule is prohibited: from recommending or referring for a

commission any product or service to a client, from recommending or referring for a

commission any product or service to be supplied by a client, or

from receiving a commission Permitted commissions and fees must be

disclosed.

Advertising and Other Forms of Solicitation (1.600.001)

A member in public practice shall not seek to obtain clients by advertising, or other forms of solicitation, in a manner that is false, misleading, or deceptive.

Advertising is false, misleading, or deceptive if it: creates false expectations of favorable results implies the ability to influence any court,

tribunal, regulatory agency, or similar body or official

contains a representation about fee or fee range that is substantially lower than the fee likely to be charged

contains a representation that is likely to cause a reasonable person to misunderstand or be deceived

Confidential Client Information(1.700.001)

A member in public practice shall not disclose any confidential information without the specific consent of the client.

Confidentiality rule does not apply: when court ordered subpoenas or summons

exist in examination of work papers as part of ethics

division inquiry or quality review In addition, confidentiality rule does not

relieve members of their duties under Compliance with Standards rule and Accounting Principles rule.

Form of Organization and Name(1.800.001)

A member may practice public accounting only in the form of organization permitted by state law or regulation, or a professional corporation whose characteristics conform to resolutions of the council.

A member shall not practice under a firm name that is misleading.

A firm may not designate itself as members of AICPA unless all of its CPA owners are members.

Enforcement of the Code of Ethics

Enforcement of ethics potentially involves four groups:

1. State Board of Accountancy grants the license to practice public

accounting can impose penalties for violation of the

code typically has adopted the AICPA rules of

conduct or a set of similar ones2. Securities and Exchange Commission

rules may differ significantly from those of AICPA

can impose penalties for violating SEC rules

Enforcement of the Code of Ethics

3.AICPA Professional Ethics Division interprets and enforces Code of Professional

Conduct investigates complaints and other information

that comes to its attention if violation is found, member may be required

to take CE courses and submit future work for Division review

if violation is severe, the member is referred to the Joint Trial Board

4.AICPA Joint Trial Board conducts hearing of charges brought by the

Ethics Division and/or state societies can suspend or dismiss violators from AICPA

member

Monitoring Public Accounting Firms

For all firms Quality control – policies and procedures a firm

establishes to ensure consistent performance in conformity with professional standards

Firms with public audit clients PCAOB Rules for Inspection & AICPA Center for

Public Company Audit Firms Firms without public audit clients

Practice monitoring (peer review)