Embed Size (px)

Citation preview

Prof Greg Clark CBESenior Non Resident FellowBrookings Institution

Committee for Sydney

Sydney March 2017

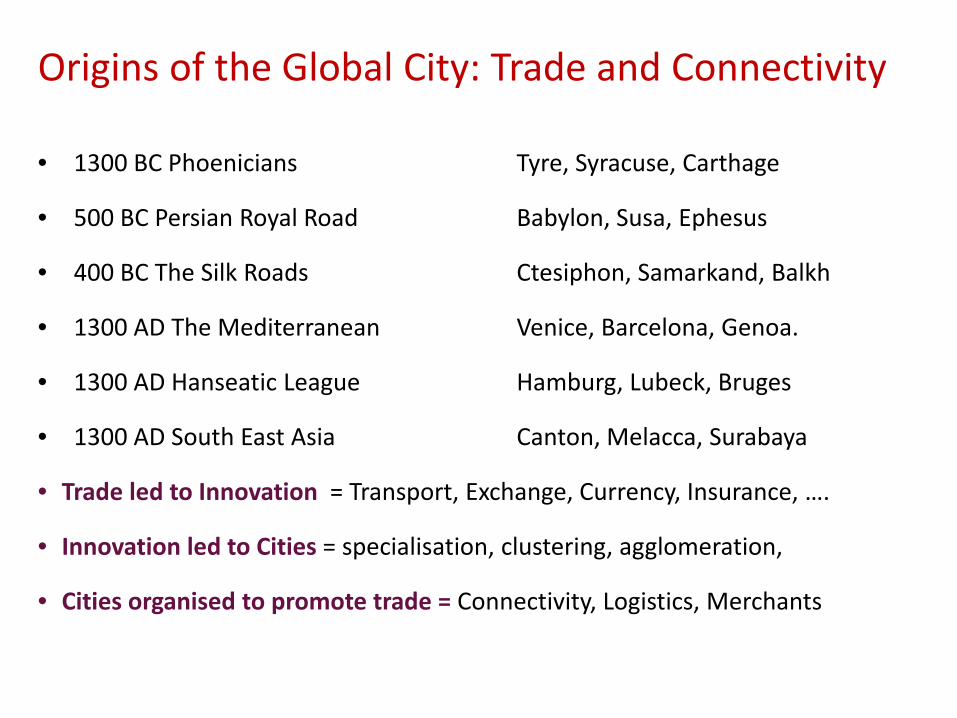

• 1300 BC Phoenicians Tyre, Syracuse, Carthage

• 500 BC Persian Royal Road Babylon, Susa, Ephesus

• 400 BC The Silk Roads Ctesiphon, Samarkand, Balkh

• 1300 AD The Mediterranean Venice, Barcelona, Genoa.

• 1300 AD Hanseatic League Hamburg, Lubeck, Bruges

• 1300 AD South East Asia Canton, Melacca, Surabaya

• Trade led to Innovation = Transport, Exchange, Currency, Insurance, ….

• Innovation led to Cities = specialisation, clustering, agglomeration,

• Cities organised to promote trade = Connectivity, Logistics, Merchants

Origins of the Global City: Trade and Connectivity

183 Pages, 7 Chapters

i. Navigating global cities.ii. Origins: Trade and cities.iii. Global Cities in the ancient world.iv. Global cities in the modern world.v. Understanding global cities. Theory and Benchmarking.vi. Global Cities today. New wave. Why and what?vii. Global City Futures: Challenges and leadership.

3

5 recurring ingredients of global cities over 5,000 years:• Trade and connectivity • Openness, diverse and entrepreneurial populations• Innovation and Influence• Discovery of new markets• Geo-political opportunity

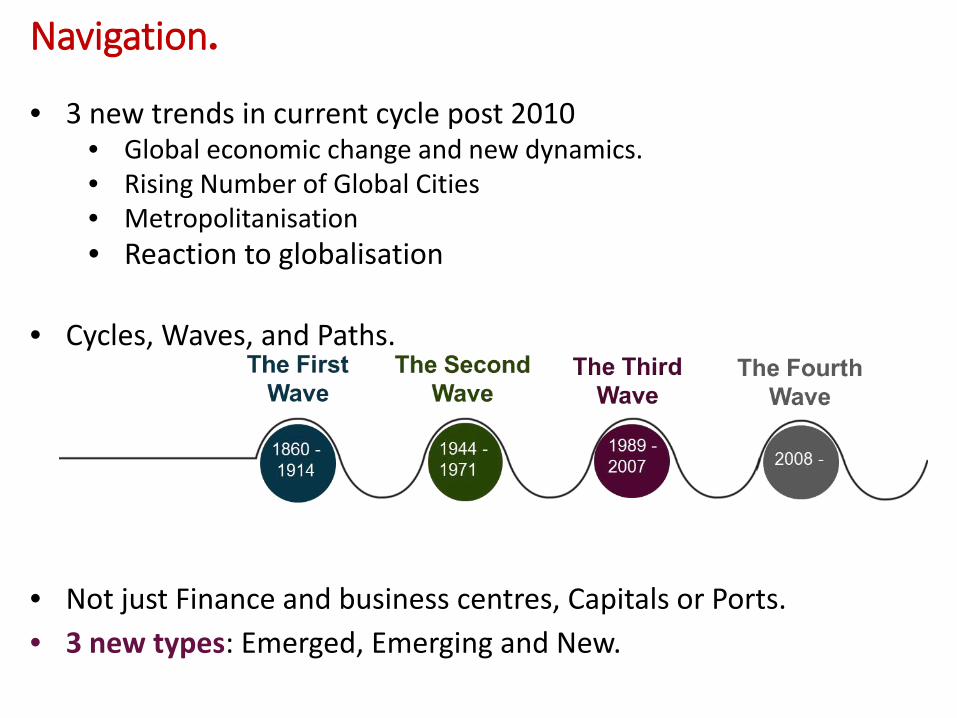

Navigation.

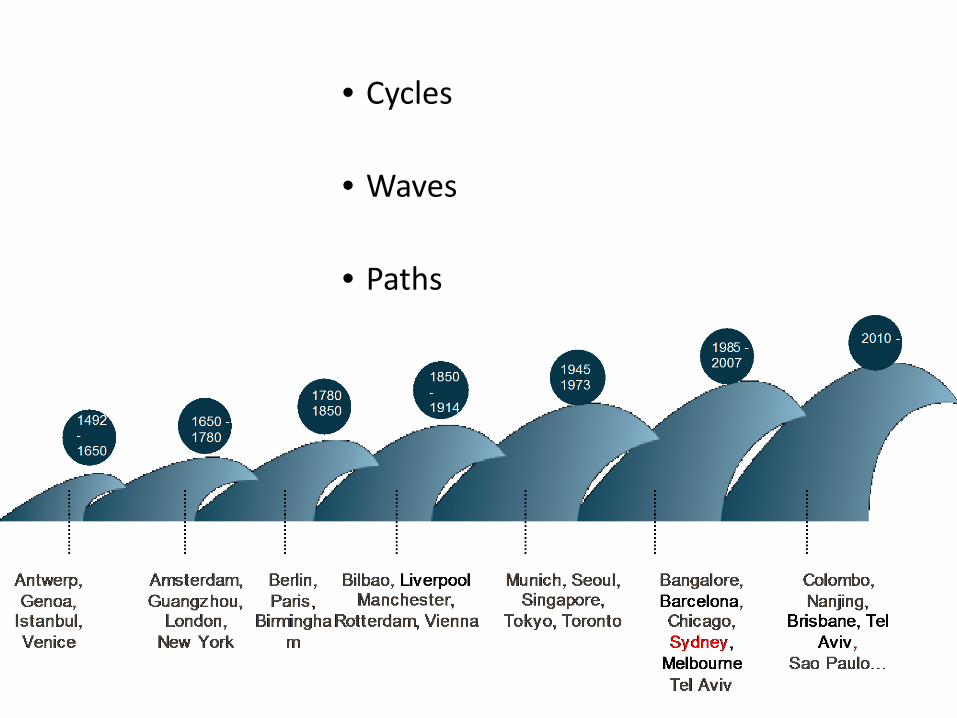

• 3 new trends in current cycle post 2010• Global economic change and new dynamics.• Rising Number of Global Cities• Metropolitanisation• Reaction to globalisation

• Cycles, Waves, and Paths.

• Not just Finance and business centres, Capitals or Ports.• 3 new types: Emerged, Emerging and New.

• Cycles

• Waves

• Paths

The Royal Road ~500 B.C.

Money, road building, architecture, metallurgy, taxation, shared language

Innovations

Externalities Rise of separatist provinces, military disorganisation

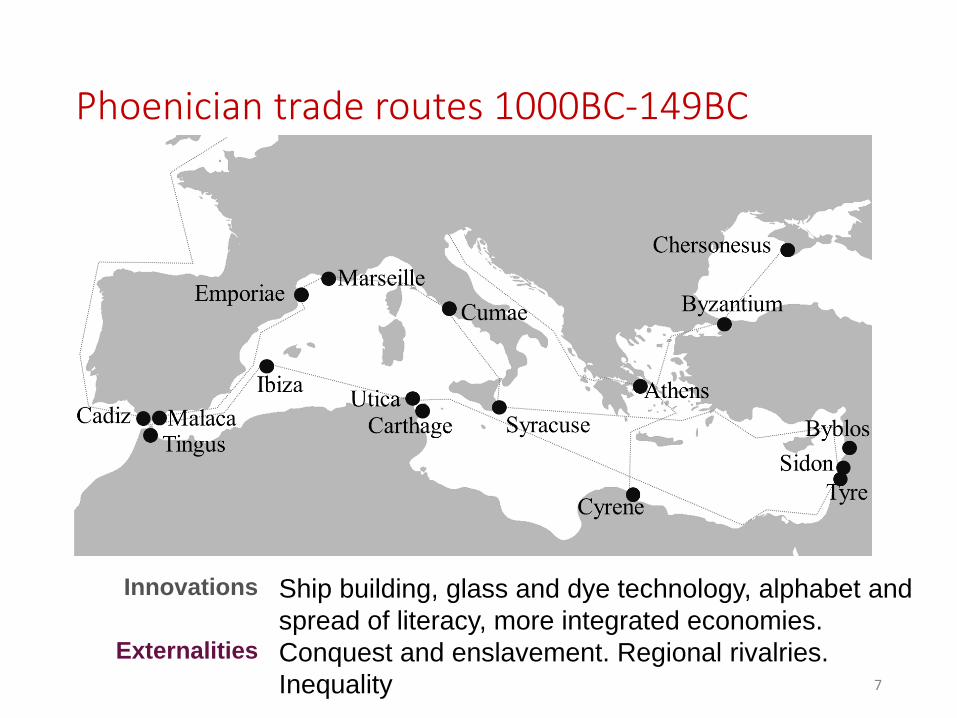

Phoenician trade routes 1000BC-149BC

7

Ship building, glass and dye technology, alphabet and spread of literacy, more integrated economies.Conquest and enslavement. Regional rivalries. Inequality

Externalities

Innovations

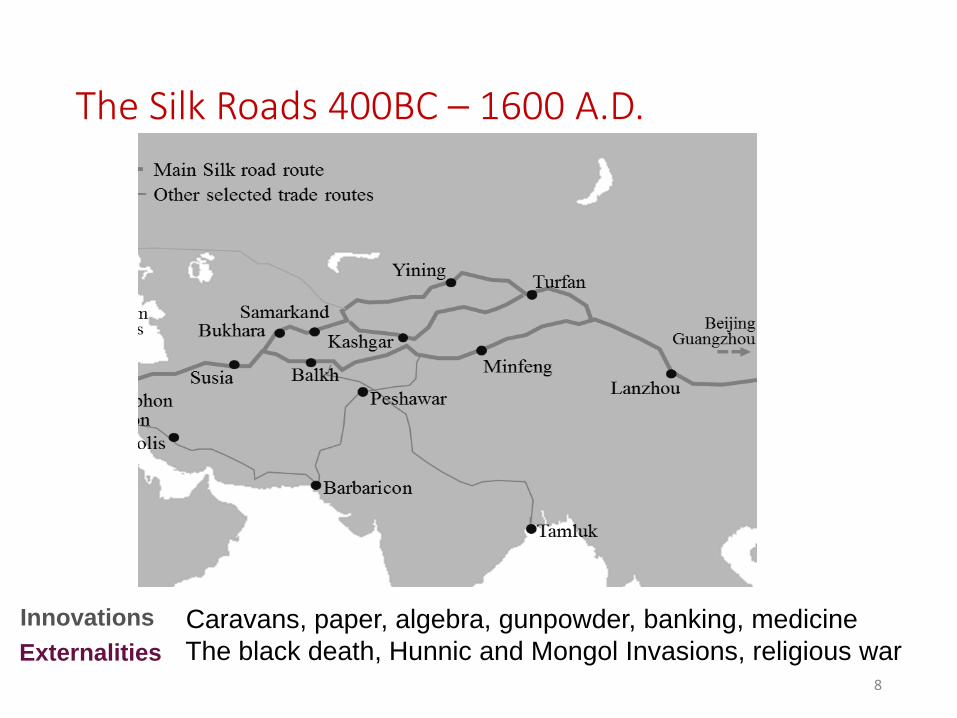

The Silk Roads 400BC – 1600 A.D.

8

Caravans, paper, algebra, gunpowder, banking, medicineThe black death, Hunnic and Mongol Invasions, religious warExternalities

Innovations

The Hanseatic League 1250-1550

9

Commercial organisationShipbuildingBanking

Restrictive trade monopoliesSelf interest of individual citiesFailure to adjust to new markets

Externalities

Innovations

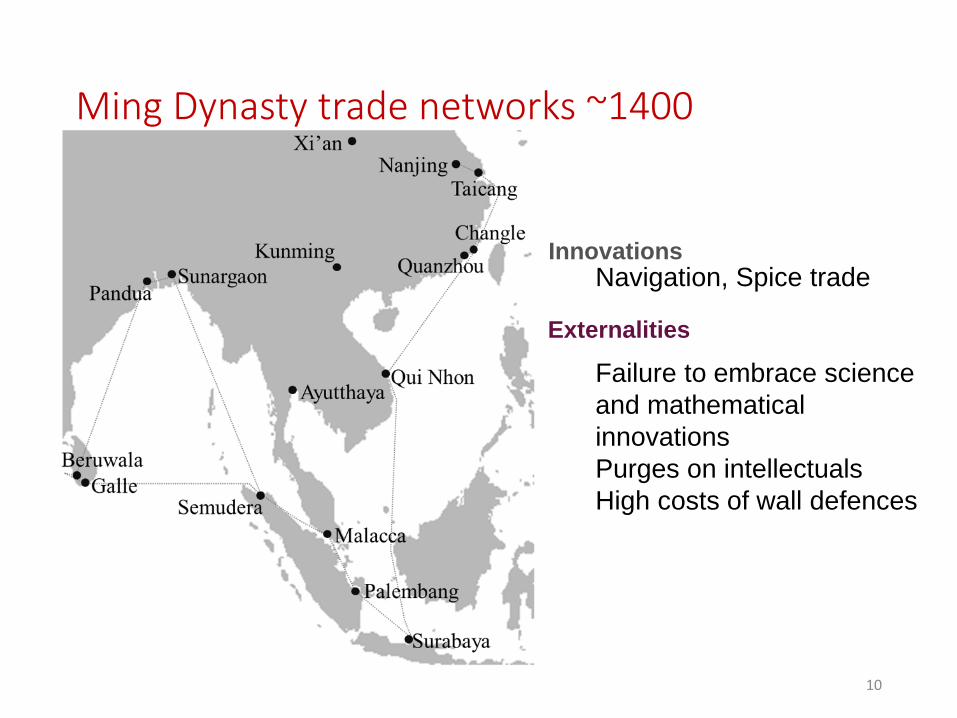

Ming Dynasty trade networks ~1400

10

Navigation, Spice trade

Failure to embrace science and mathematical innovationsPurges on intellectualsHigh costs of wall defences

Innovations

Externalities

Atlantic Slave Trade network 1500-1830

11

Externalities

InnovationsImprovements in navigation, ship-building, mercantilism, early capitalism, spread of Enlightenment ideals, property rights, capital markets, canals

Mass slavery, economic division, piracy, social dislocation

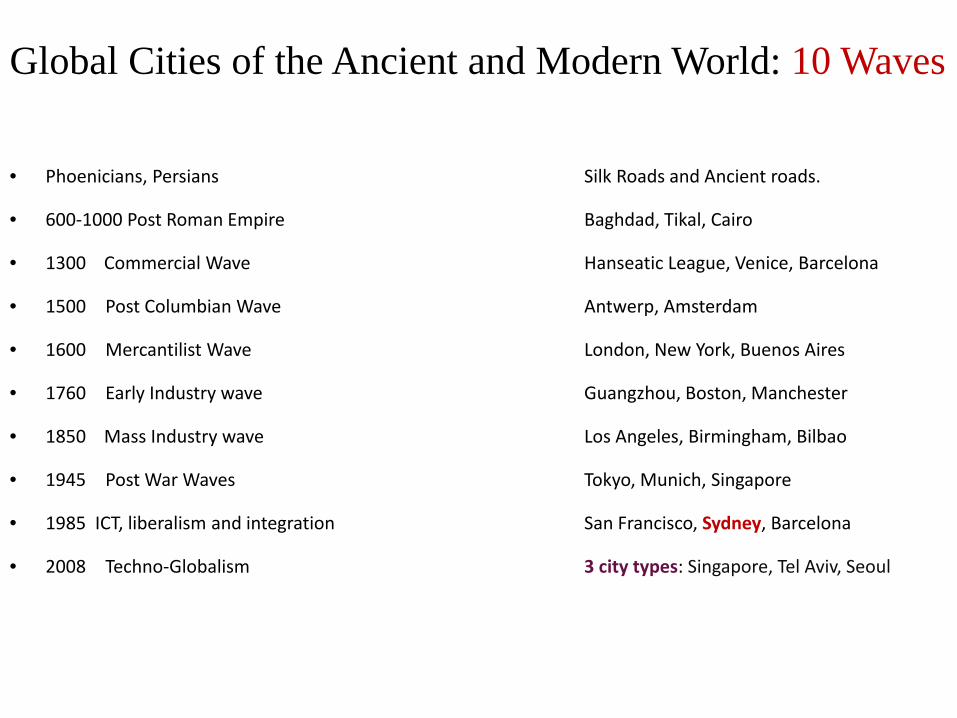

Global Cities of the Ancient and Modern World: 10 Waves

• Phoenicians, Persians Silk Roads and Ancient roads.

• 600-1000 Post Roman Empire Baghdad, Tikal, Cairo

• 1300 Commercial Wave Hanseatic League, Venice, Barcelona

• 1500 Post Columbian Wave Antwerp, Amsterdam

• 1600 Mercantilist Wave London, New York, Buenos Aires

• 1760 Early Industry wave Guangzhou, Boston, Manchester

• 1850 Mass Industry wave Los Angeles, Birmingham, Bilbao

• 1945 Post War Waves Tokyo, Munich, Singapore

• 1985 ICT, liberalism and integration San Francisco, Sydney, Barcelona

• 2008 Techno-Globalism 3 city types: Singapore, Tel Aviv, Seoul

Global Cities of the Ancient and Modern World

• Alexandria 334BC – 1450s

• Grain and Silk Roads port. Multicultural cross-roads and became city of knowledge.

13

Guangzhou 10th-15th C 1760-1850s

China’s maritime gatewayTea, opium, war.

Baghdad 8th-10th C Heart of Islamic single

market. A ‘showcase’ city open to new cultures:

progress in sciences.

Global Cities of the Ancient and Modern World

Vienna 1815-1914; 1995-Present• From cosmopolitan capital to

Fascism. Reborn as city of diplomacy, culture, tourism and regional finance.

14

San Francisco 1970s-Present• ICT driven by

R&D network, quality of life and local VC finance

Amsterdam 1550-1700

Financial and trade innovation. Colonies and canals = European distribution hub.

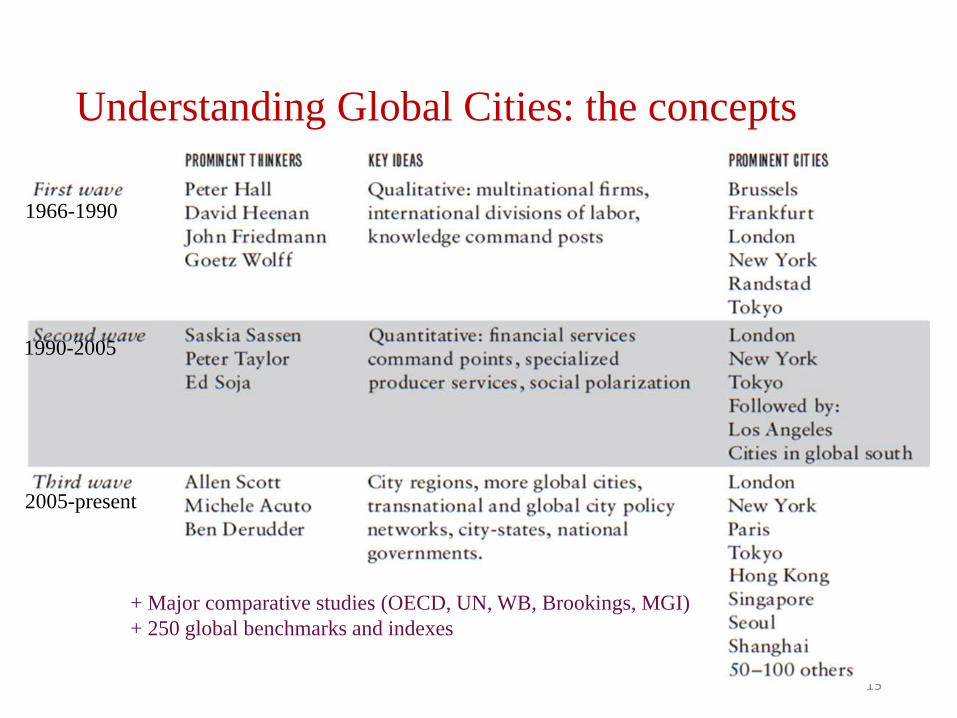

Understanding Global Cities: the concepts

15

+ Major comparative studies (OECD, UN, WB, Brookings, MGI) + 250 global benchmarks and indexes

1966-1990

1990-2005

2005-present

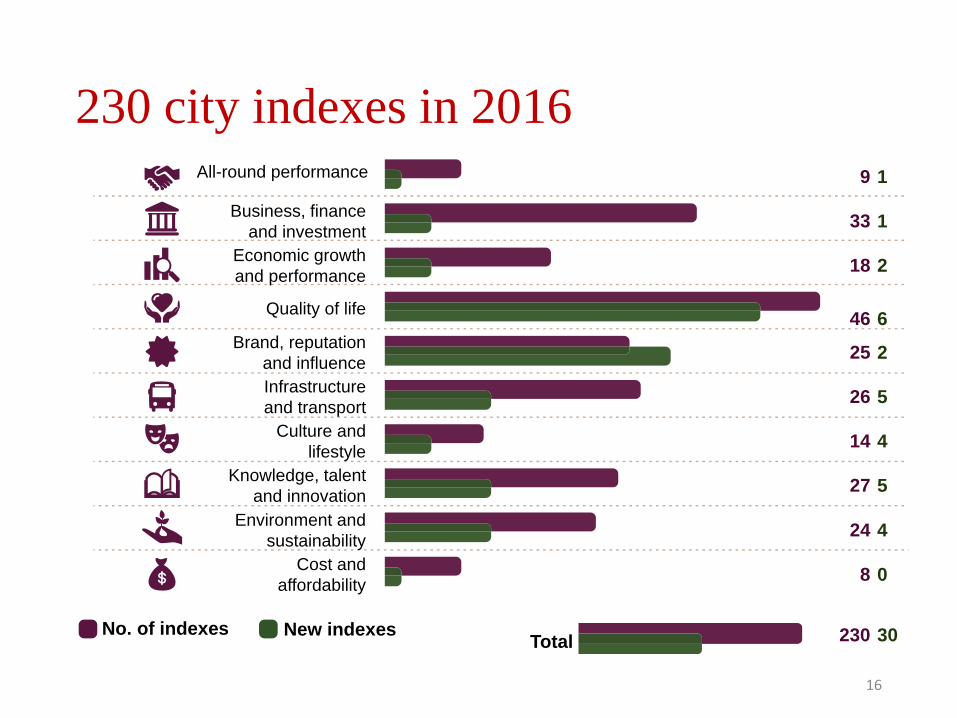

230 city indexes in 2016

16

All-round performance

Business, financeand investment

Economic growthand performance

Quality of life

Brand, reputationand influenceInfrastructureand transport

Culture andlifestyle

Knowledge, talentand innovation

Environment andsustainability

Cost andaffordability

No. of indexes Total

9

33

18

46

25

26

14

27

24

8

1

1

2

6

2

5

4

5

4

0

230 30New indexes

Current Wave: Global Cities today

• London

• New York• Hong Kong

• Paris

• Tokyo• Singapore

• + Toronto, Seoul, Sydney, Chicago, Amsterdam.

Shanghai, Beijing, Istanbul, Mumbai, Sao Paulo, Mexico City, Joburg+10-20 others

Sydney, Toronto, Stockholm, Barcelona, San Diego, Nanjing, Brisbane, Oslo, Tel Aviv, Cape Town,Auckland+20-40 others

5 Paths to globalisation….

• Trade led: Hamburg, Miami,….

• Geopolitical opportunities: Toronto, Singapore,…..

• Leverage Innovation: Nanjing, Tel Aviv,…..

• National Champions: Seoul, Santiago,…..

• Catalysts of Institutions or Events: Vienna, Nairobi,…..

18

19

20

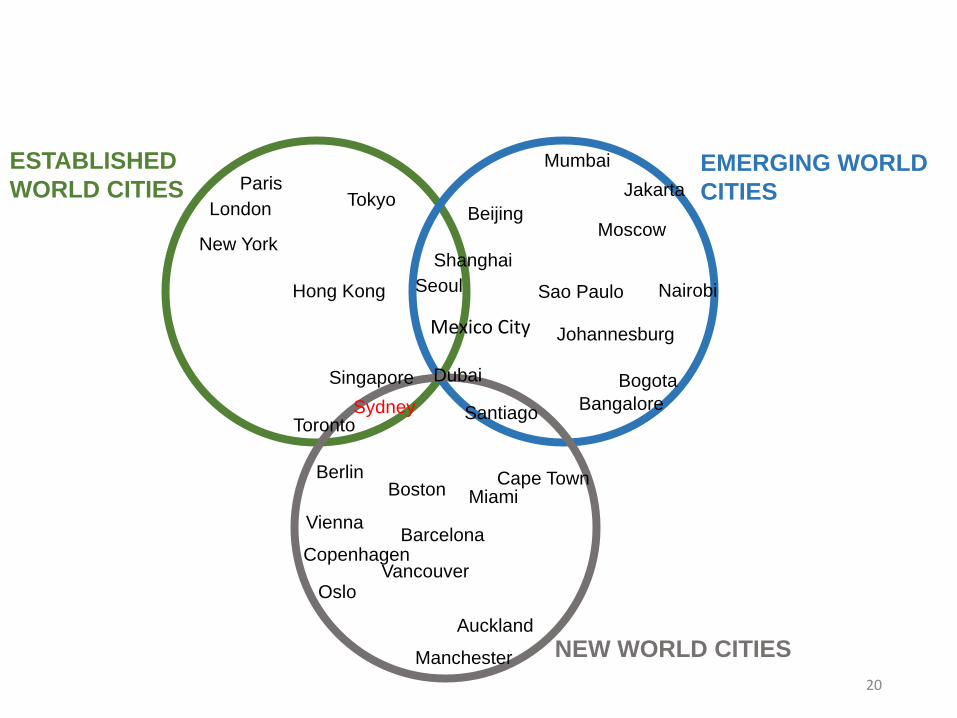

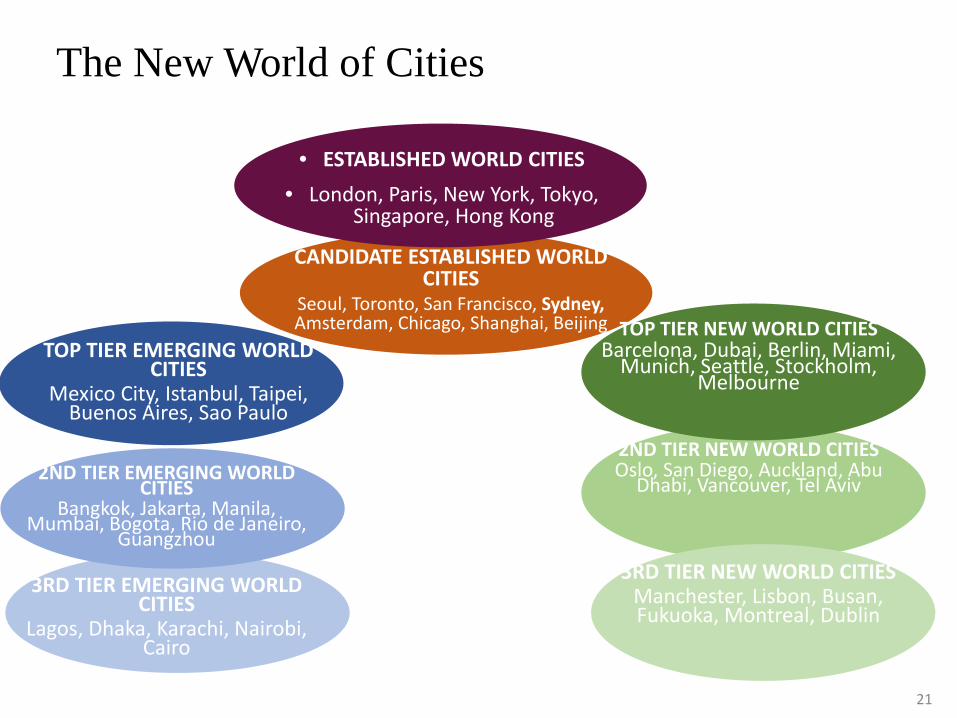

NEW WORLD CITIES

EMERGING WORLD CITIES

ESTABLISHED WORLD CITIES

London

New York

ParisTokyo

Hong Kong

Singapore

Shanghai

Beijing

Seoul

SydneyToronto

Berlin

Santiago

Sao Paulo

Johannesburg

Moscow

Jakarta

Dubai

Vancouver

Manchester

Auckland

Copenhagen

Vienna

Oslo

Boston

Barcelona

MiamiCape Town

Bogota

Nairobi

Bangalore

Mumbai

Mexico City

2ND TIER NEW WORLD CITIESOslo, San Diego, Auckland, Abu

Dhabi, Vancouver, Tel Aviv

3RD TIER NEW WORLD CITIESManchester, Lisbon, Busan, Fukuoka, Montreal, Dublin

• ESTABLISHED WORLD CITIES• London, Paris, New York, Tokyo,

Singapore, Hong Kong

21

CANDIDATE ESTABLISHED WORLD CITIES

Seoul, Toronto, San Francisco, Sydney, Amsterdam, Chicago, Shanghai, Beijing

TOP TIER EMERGING WORLD CITIES

Mexico City, Istanbul, Taipei, Buenos Aires, Sao Paulo

TOP TIER NEW WORLD CITIESBarcelona, Dubai, Berlin, Miami,

Munich, Seattle, Stockholm, Melbourne

2ND TIER EMERGING WORLD CITIES

Bangkok, Jakarta, Manila, Mumbai, Bogota, Rio de Janeiro,

Guangzhou

3RD TIER EMERGING WORLD CITIES

Lagos, Dhaka, Karachi, Nairobi, Cairo

The New World of Cities

Sydney among world cities

22

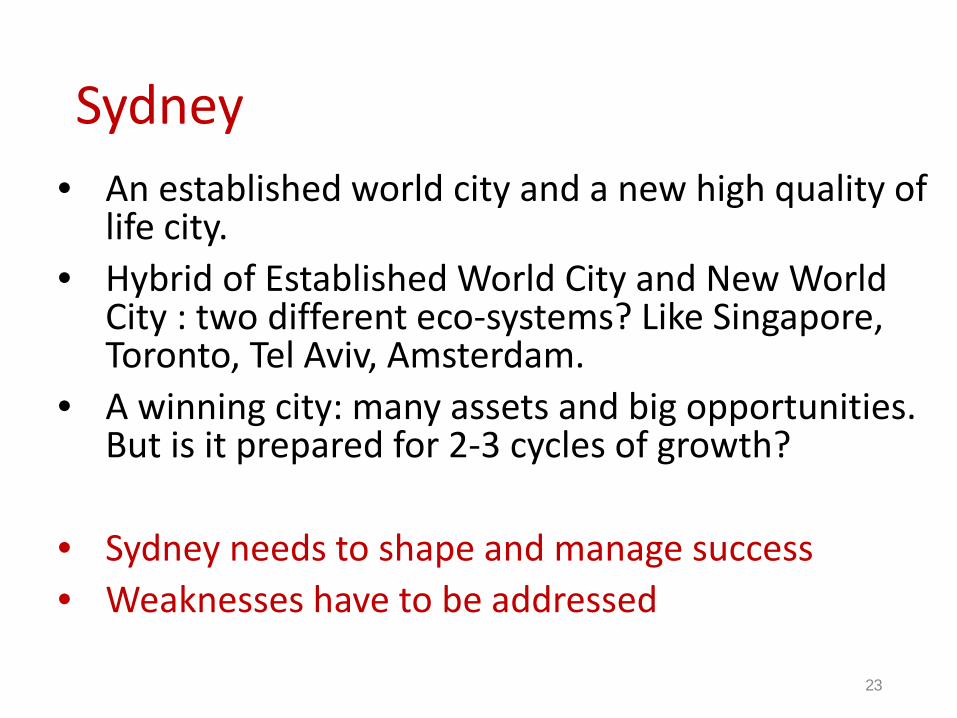

Sydney• An established world city and a new high quality of

life city.• Hybrid of Established World City and New World

City : two different eco-systems? Like Singapore, Toronto, Tel Aviv, Amsterdam.

• A winning city: many assets and big opportunities. But is it prepared for 2-3 cycles of growth?

• Sydney needs to shape and manage success • Weaknesses have to be addressed

23

Sydney’s peers

Hybrid established/new world cities:

• Toronto, Singapore

Most similar global services firms concentrations:

• Chicago, Milan

Most similar basic economic profile:

• Vancouver, Amsterdam, Tel Aviv

Most similar post-crisis performance since 2008:

Berlin, Tel Aviv, Hamburg

Other similar cities by size, scale, assets and internationalisation:

Madrid, Miami, Barcelona, San Francisco, Vienna, San Diego, Taipei, Santiago, Cape Town Source: Brookings Global Metro Monitor 201524

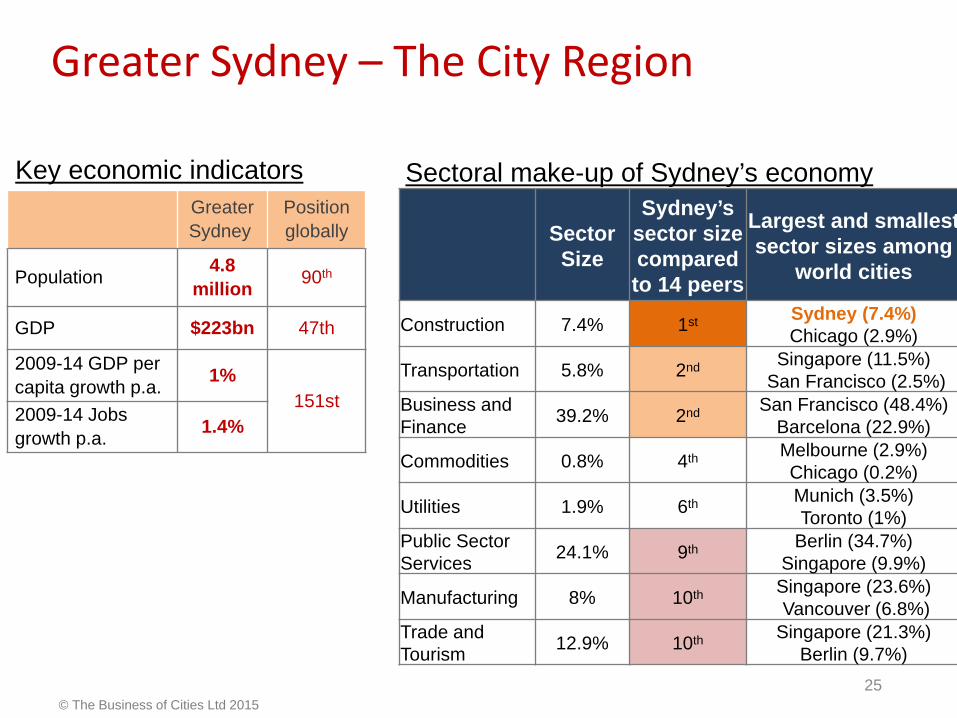

Greater Sydney

Position globally

Population 4.8 million 90th

GDP $223bn 47th

2009-14 GDP per capita growth p.a. 1%

151st2009-14 Jobs growth p.a. 1.4%

Greater Sydney – The City Region

© The Business of Cities Ltd 2015

Sector Size

Sydney’s sector size compared to 14 peers

Largest and smallest sector sizes among

world cities

Construction 7.4% 1st Sydney (7.4%) Chicago (2.9%)

Transportation 5.8% 2nd Singapore (11.5%)San Francisco (2.5%)

Business and Finance 39.2% 2nd San Francisco (48.4%)

Barcelona (22.9%)

Commodities 0.8% 4th Melbourne (2.9%)Chicago (0.2%)

Utilities 1.9% 6th Munich (3.5%)Toronto (1%)

Public Sector Services 24.1% 9th Berlin (34.7%)

Singapore (9.9%)

Manufacturing 8% 10th Singapore (23.6%)Vancouver (6.8%)

Trade and Tourism 12.9% 10th Singapore (21.3%)

Berlin (9.7%)

Sectoral make-up of Sydney’s economyKey economic indicators

25

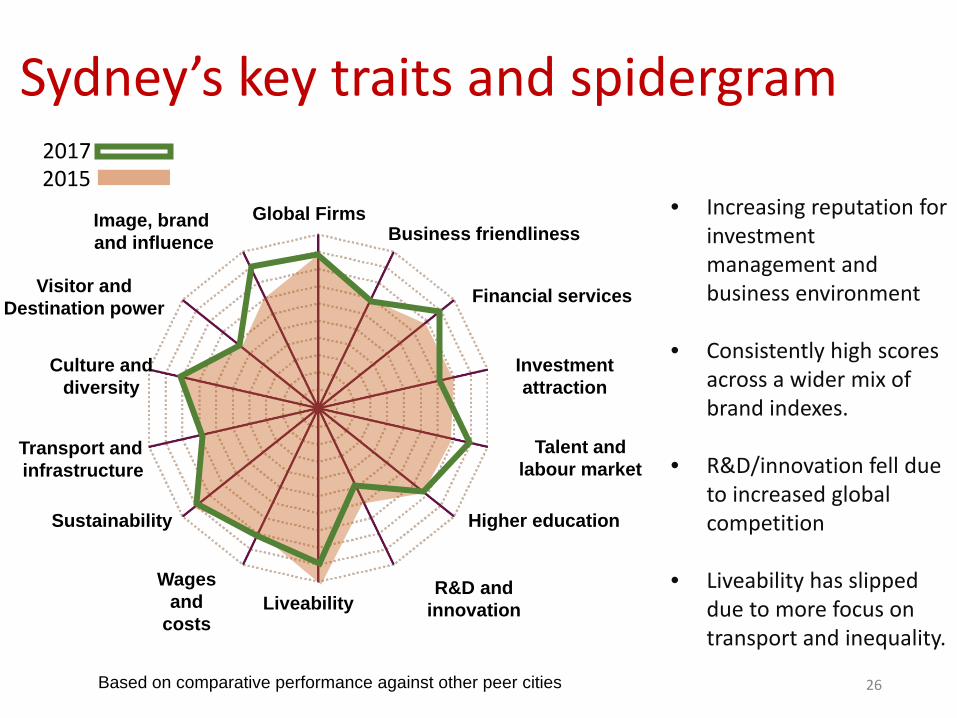

Sydney’s key traits and spidergram

26

Global FirmsBusiness friendliness

Financial services

Investment attraction

Talent and labour market

Higher education

R&D and innovationLiveability

Wages and

costs

Sustainability

Transport and infrastructure

Culture and diversity

Visitor and Destination power

Image, brand and influence

• Increasing reputation for investment management and business environment

• Consistently high scores across a wider mix of brand indexes.

• R&D/innovation fell due to increased global competition

• Liveability has slipped due to more focus on transport and inequality.

20172015

Based on comparative performance against other peer cities

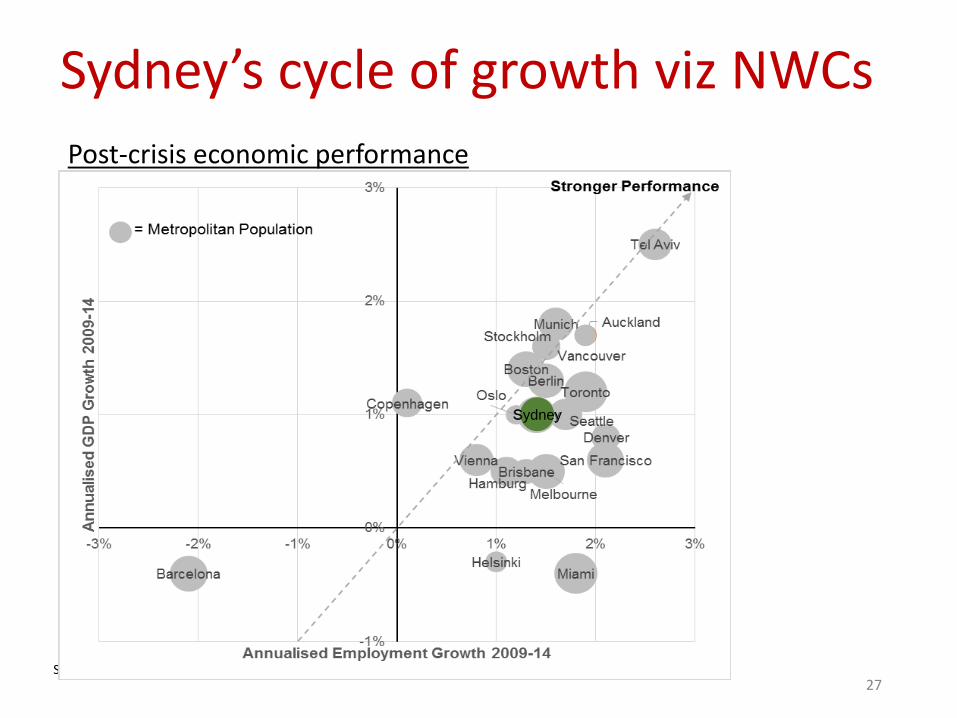

Sydney’s cycle of growth viz NWCs

27

Post-crisis economic performance

Source: Brookings and GaWC

Sydney

Sydney: one of the most important locations for global corporates among medium-sized world cities

28

Highly globalised corporate economy

GDP ($US bns)GDP per

Capita ($US ‘000)

Global Connectivity Rank (GaWC)

IBM Most Competitive Cities ‘International HQs’

No of Cities 300 300 300+ 100

Sydney 223 46 9 17

Toronto 276 45 17 8

Vienna 184 49 27 18

San Francisco 331 72 28 14

Melbourne 178 40 34 26

Miami 263 44 36 24

Barcelona 171 36 37 25

Boston 360 76 39

Munich 220 56 42

Stockholm 143 56 43 11

Copenhagen 127 42 48 15

Tel Aviv 153 43 60 49

Berlin 158 36 63 10

Auckland 50 32 72 35

Vancouver 110 44 76 23

Oslo 74 53 79

Brisbane 97 42 80

Helsinki 77 48 81 29

Seattle 267 73 99

Denver 170 62 106

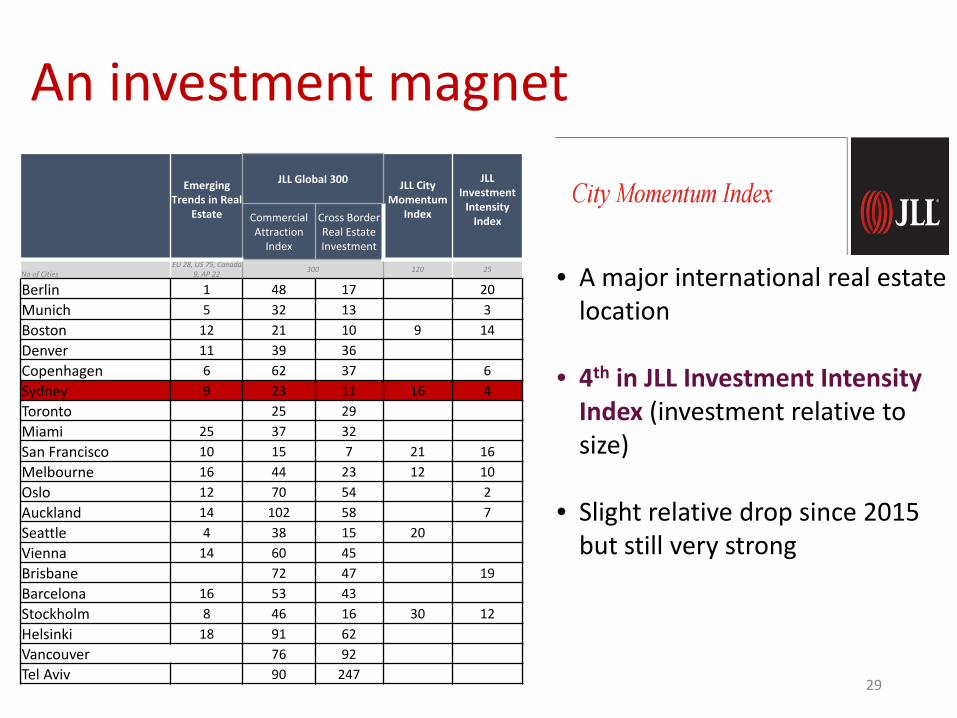

An investment magnet

29

Emerging Trends in Real

Estate

JLL Global 300 JLL City Momentum

Index

JLL Investment

Intensity IndexCommercial

Attraction Index

Cross Border Real Estate Investment

No of CitiesEU 28, US 75, Canada

9, AP 22 300 120 25

Berlin 1 48 17 20Munich 5 32 13 3Boston 12 21 10 9 14Denver 11 39 36Copenhagen 6 62 37 6Sydney 9 23 11 16 4Toronto 25 29Miami 25 37 32San Francisco 10 15 7 21 16Melbourne 16 44 23 12 10Oslo 12 70 54 2Auckland 14 102 58 7Seattle 4 38 15 20Vienna 14 60 45Brisbane 72 47 19Barcelona 16 53 43Stockholm 8 46 16 30 12Helsinki 18 91 62Vancouver 76 92Tel Aviv 90 247

• A major international real estate location

• 4th in JLL Investment Intensity Index (investment relative to size)

• Slight relative drop since 2015 but still very strong

A top 10 quality of life destination

30

Specialisation in newly traded

markets

RankMelbourne 2Sydney 4Berlin 9Munich 11Vancouver 13Toronto 13Boston 13Vienna 16Auckland 18Brisbane 18Stockholm 24Copenhagen 27San Francisco 27Barcelona 30Helsinki 34Oslo 60

QS Best Student Cities

Mercer Quality of

Living Survey

EIU Liveability Ranking

Global Liveable

Cities Ranking

ArcadisSustainable Cities Index

'People'

MonocleQuality of

Life Survey

No. of Cities 230 140 63 100 25

Vienna 1 2 4 3Berlin 13 20 11 5 2Munich 4 28 8 5Melbourne 15 1 13 22 6Helsinki 30 10 4 12Copenhagen 9 22 9 24 4Stockholm 19 24 5 14 10Vancouver 5 3 12 23 11Sydney 10 7 14 25 8Auckland 3 9 8 22Toronto 15 4 40Brisbane 36 18 21Barcelona 39 31 29 13 19Boston 34 33 23 41San Francisco 28 49 54Seattle 46 46 61Miami 66 37 89Tel Aviv 104 76

Exceptional brand with global audiences

31

City RepTrak Brand scores, 2016

• Strong reputation for visitor and resident amenities

• Less strong in measures of global influence, culture and nightlife.

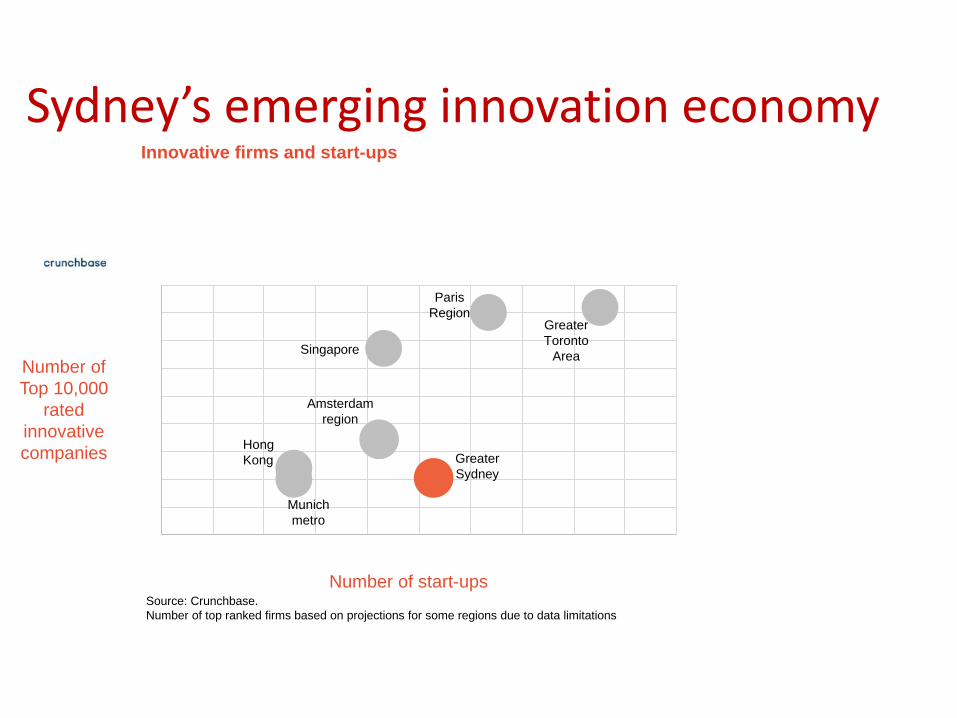

Sydney’s emerging innovation economy

Hong Kong

Paris Region

Singapore

Greater Sydney

Greater Toronto

Area

Munich metro

Amsterdam region

Number of Top 10,000

rated innovative companies

Number of start-ups

Innovative firms and start-ups

Source: Crunchbase. Number of top ranked firms based on projections for some regions due to data limitations

33

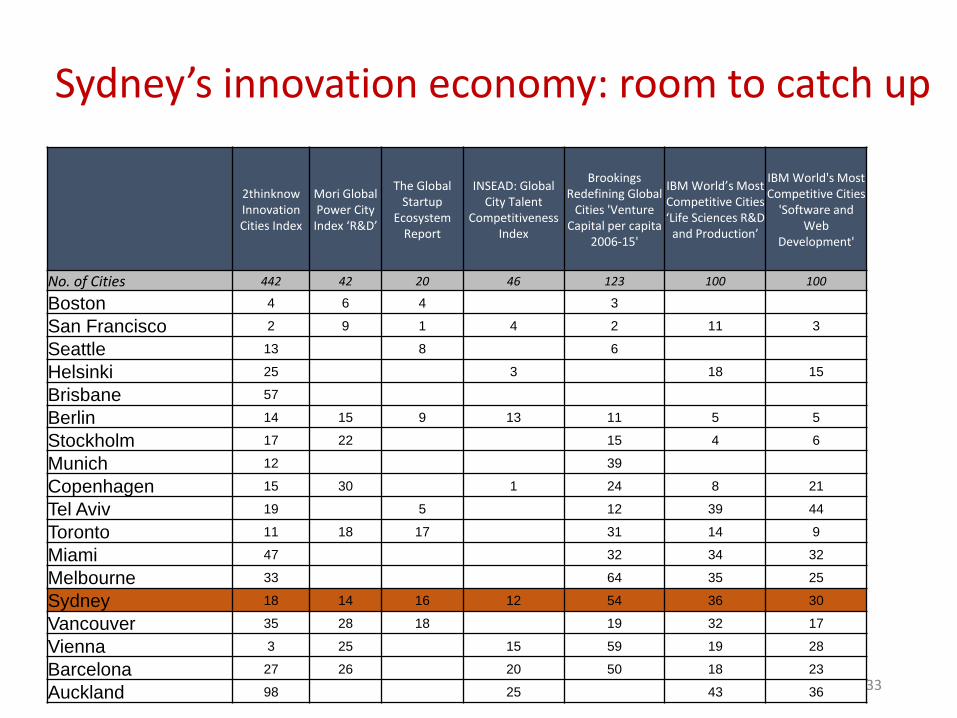

Sydney’s innovation economy: room to catch up

2thinknow Innovation Cities Index

Mori Global Power City Index ‘R&D’

The Global Startup

Ecosystem Report

INSEAD: Global City Talent

Competitiveness Index

Brookings Redefining Global

Cities 'Venture Capital per capita

2006-15'

IBM World’s Most Competitive Cities ‘Life Sciences R&D

and Production’

IBM World's Most Competitive Cities

'Software and Web

Development'

No. of Cities 442 42 20 46 123 100 100

Boston 4 6 4 3

San Francisco 2 9 1 4 2 11 3

Seattle 13 8 6

Helsinki 25 3 18 15

Brisbane 57

Berlin 14 15 9 13 11 5 5

Stockholm 17 22 15 4 6

Munich 12 39

Copenhagen 15 30 1 24 8 21

Tel Aviv 19 5 12 39 44

Toronto 11 18 17 31 14 9

Miami 47 32 34 32

Melbourne 33 64 35 25

Sydney 18 14 16 12 54 36 30

Vancouver 35 28 18 19 32 17

Vienna 3 25 15 59 19 28

Barcelona 27 26 20 50 18 23

Auckland 98 25 43 36

Infrastructure challenges remain stark

Modal share of non-car based public transport1 Hong Kong2 Singapore3 Greater London4 Amsterdam region/G45 Paris Region6 San Francisco Bay Area7 Munich metropolitan region8 Greater Boston9 Greater Toronto10 Greater Sydney

Source: Numbeo Rent Index (0= cheapest)

Price rises and unaffordability happening faster than in most other medium-sized regions

Numbeo Housing Rent Index, 2016

Increasing affordability issues

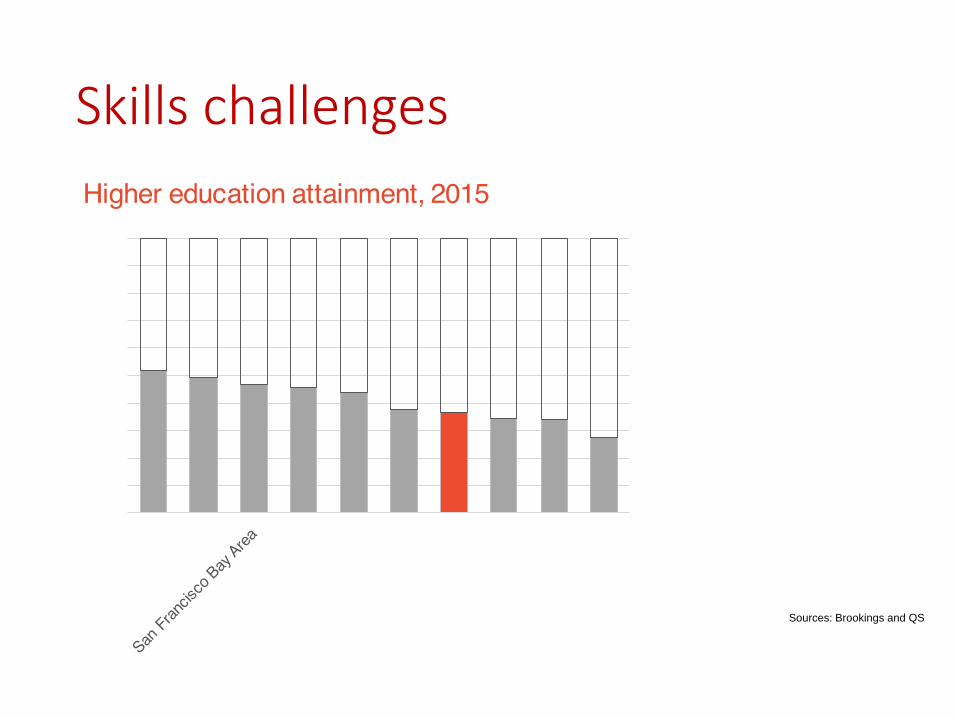

Skills challenges

Sources: Brookings and QS

37

Source: PwC Cities of Opportunity

Sydney summary

• Has rapidly gained attributes of a mature, globally respected city

• Entertainment and Tourism brand much stronger than business brand.

• Work ahead to improve innovation system• (R&D, start-ups, software/multimedia, sciences, commercialised knowledge) –

• Infrastructure and built environment becoming a big disadvantage in global indexes• low mass transit coverage, high car-dependency and travel times, low density,

environmental inefficiencies

• Scores highlight need for metropolitan approach. Software good, hardware weak.

38

What is a City Deal?

• A negotiated contract, not a programme.• Growth, productivity, and performance oriented• Focused on infrastructure investment packages and

growth priorities• Based on pre-agreed metrics and performance• Designed to foster multi-municipal leadership and

governance that lead to reforms• Innovative financing model including value capture

and forward financing

Growth and improvement

appetite

Institutional Reforms to guarantee outcomes

Whole of Gov+ negotiated/

customisedapproach

Transformative Investment

Value capture mechanisms to

finance investment

City Deals: the interlocking requirements

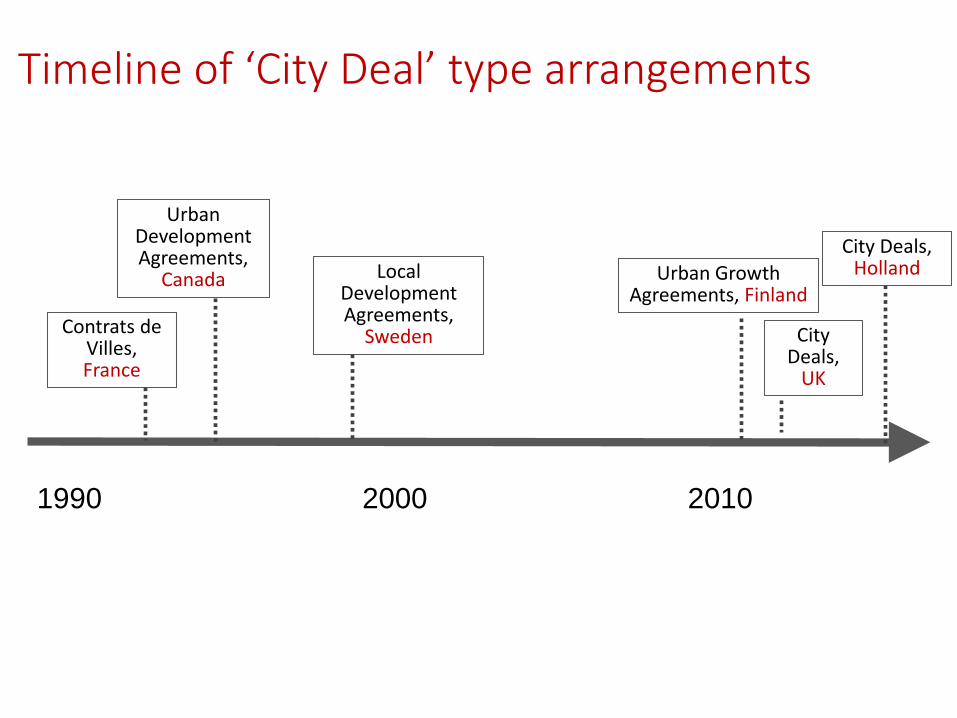

Timeline of ‘City Deal’ type arrangements

1990 2000 2010

Contrats de Villes, France

Urban Development Agreements,

Canada Local Development Agreements,

Sweden City Deals,

UK

Urban Growth Agreements, Finland

City Deals, Holland

• Lyon first to apply it at metro scale: regenerating struggling neighbourhoods (housing, skills, jobs) with state funding and coordinated strategy

• Latest in Lyon: 2015-2020: 37 neighbourhoods, €80m: housing, public spaces, skills, jobs.

• Nationwide: 5-7 year terms. 435 signed for 2015-20• Brings together all local stakeholders: state, regions, city, service

agencies• Has improved horizontal collaboration, especially including civil

society.

Contrat de Ville: Example - Lyon

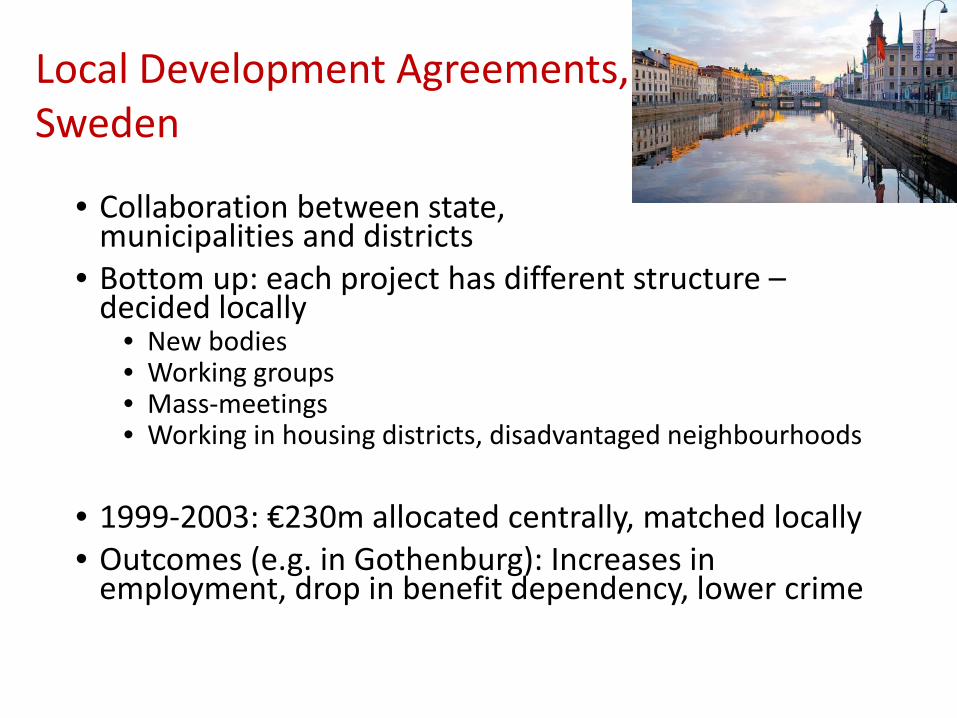

• Collaboration between state, municipalities and districts

• Bottom up: each project has different structure –decided locally

• New bodies• Working groups• Mass-meetings• Working in housing districts, disadvantaged neighbourhoods

• 1999-2003: €230m allocated centrally, matched locally• Outcomes (e.g. in Gothenburg): Increases in

employment, drop in benefit dependency, lower crime

Local Development Agreements, Sweden

Vancouver Tri-Partite Agreement

• 2000: Federal, state and city governments agree to cooperate on economic and social issues in downtown Vancouver up to 2010

• Response to acute public health crisis in Downtown Eastside (drugs, social deprivation)

• Vancouver did not have jurisdiction or funding to deal with complex problems: participation from other govt. tiers required.

• Coordinated, ‘whole of government’ intervention: jobs, health, skills, businesses

• Initiatives: Economic Revitalization; Safety; Housing; Quality of Life

Manchester City Deal

• A revolving infrastructure fund: ‘earn back’ model following infrastructure tax uplift. Gov help up to £150m

• Establishes Greater Manchester Investment Framework

• Creates City Apprenticeship and Skills hub: local labour force matching

• A Housing Investment Fund: to pool local + national resources for house building

• Facilitates integration of regional transpor

• Manchester Combined Authority gains new mayor, powers and resources

The Future and global challenges

• Global cities will continue to emerge despite external threats.

• Why? • Global economy and nation states need them (talent and capital and trade and innovation)

• Diversification from Established WCs by talent, capital, technology and firms. Appetite for more.

• Infrastructure investment will create them. New global infrastructure scenario will reinforce open cities.

• What does change in city functionality and connectivity mean for global cities?

• 3 strategic imperatives…

1. How to compete and achieve inclusion, resilience, flexibility?

2. How to manage success and unintended consequences of growth?

3. How to resolve external challenges to global city model?46

Thank You47