Embed Size (px)

Citation preview

Production, Process Investment, and the Survivalof Debt-Financed Startup Firms

Fehmi TanrıseverSchool of Industrial Engineering, Eindhoven University of Technology, Eindhoven, The Netherlands, [email protected]

S. Sinan ErzurumluTechnology, Operations and Information Management Division, Babson College, Babson Park, Massachusetts 02457, USA,

Nitin JoglekarSchool of Management, Boston University, Boston, Massachusetts 02215, USA, [email protected]

W hether to invest in process development that can reduce the unit cost and thereby raise future profits or to conservecash and reduce the likelihood of bankruptcy is a key trade-off faced by many startup firms that have taken on debt.

We explore this trade-off by examining the production quantity and cost reducing R&D investment decisions in a two periodmodel wherein a startup firm must make a minimum level of profit at the end of the first period to survive and operate in thesecond period. We specify a probabilistic survival measure as a function of production and investment decisions to track andmanage the risk exposure of the startup depending on three key market factors: technology, demand, and competitor’s cost.We develop managerial insights by characterizing how to create operational hedges against the bankruptcy risk: if a startupmakes a “conservative” investment decision, then it also selects an optimal quantity that is less than the monopoly level andhence sacrifices some of first period expected profits to increase its survival chances. If it decides to invest “aggressively,”then it produces more than the monopoly level to cover the higher bankruptcy risk. We also illustrate that debt constraintshrinks the decision space, wherein such process investments are viable.

Key words: production and process investment; operational hedging; startup operations; survival under debtHistory: Received: January 2010; Accepted: June 2011, after 2 revisions.

1. Introduction

According to a study by the US Bureau of the Census, itis estimated that over 700,000 startup firms are formedevery year in the United States. Startups are endowedwith unique characteristics regarding their asset struc-ture, organization type, andgrowthorientation (Gifford2003), and their operational decisions are oftenrestricted by debt and other financial considerations(Berger and Udell 2003). Only a small proportion of thestartups are able to grow their revenues and becomeprofitable, and even a smaller proportion of these firmscan show continued growth and make initial publicofferings (Acs and Armington 2003). These firms takeon debt and face immediate bankruptcy in the case of apayback default (Reid 1999). Hence, for startup manag-ers it is necessary to generate adequate short-term cashflows by exploiting immediate business opportunities tokeep upwith the cash outflows and avoid bankruptcy.

1.1. InvestmentChallenges at Process-FocusedStartupsStartups are not merely focused on survival. Theymust also create long-term growth. A growth-

oriented startup could initially differentiate itselfbased on its unique product features, or it could do soby developing a process that results into a low costsolution. Even in settings when it begins with uniqueproduct features, many startups have to invest intechnologies that reduce the unit cost to keep itscompetitive advantage. Empirical evidence on pro-cess re-engineering practices in small and mediumenterprises indicates that cost reduction is one of theirprimary concerns (Chang and Powell 1998). Startupsin certain types of industries (e.g., those based onchemical technologies, semiconductor fabrication,and component manufacturing technologies in cleantechnology) find that systematic cost reduction byinvesting in process technologies is a central piece oftheir business model (Erzurumlu et al. 2011, Hatchand Dyer 2004). Due to the long time horizon andlarge scale of these process-related investments, manyof these startups often turn to debt, rather thanventure capital, as a means of financing. Indeed, insti-tutions like Advanced Research Projects Agency-Energy in the United States are making special effortsto provide financial support, such as loan guarantees

Vol. 0, No. 0, xxxx–xxxx 2012, pp. 1–16 DOI 10.1111/j.1937-5956.2012.01319.xISSN 1059-1478|EISSN 1937-5956|12|0|0001 © 2012 Production and Operations Management Society

to raise debt, for process technology investments toclean technology startups (US Department of Energy2010).There have been bodies of aggregate empirical

studies on the nature of resources (Brush et al. 2001,Shane and Venkataraman 2000) and around theeffects of these resources on the development of capa-bilities, both for product- and process-based competi-tion in new ventures (Bamford et al. 2000, Choi andShepherd 2004, Mishina et al. 2004). Investments insuch resources are likely to improve the future pros-pects of the firm. However, these investments con-sume short-term cash reserves, may not generateimmediate cash flows, and may result in bankruptcy.The entrepreneurship literature (Bhide 2000, Reid1999) indicates that investment in long-term growthand creating short-term profits are intimately linked.In this article, we study a fundamental trade-off:whether to invest in process development that can reducethe unit cost and thereby raise future profits or to conservecash and reduce the likelihood of bankruptcy when a startupfirm has to take debt to fund such investments.

1.2. Operational ConcernsAlthough the relevance of process investments bystartups is articulated in the aggregate literature citedabove, we have created a questionnaire instrumentand conducted a series of interviews at several start-ups to understand operational challenges that affectprocess R&D investment decisions. These startupswere selected because they had stabilized their prod-uct development and were considering cost reductionas a central part of their business model.For example, Faradox was an Austin, TX-based

startup that supplied high energy density capacitorsusing its proprietary production process. The manag-ers at Faradox viewed process development to reduceunit cost as a key competitive aspect of their business.During our interviews, the vice president of opera-tions stated that there was a tremendous amount ofongoing research in the field of high energy densitycapacitors, and it was quite likely that new competi-tors might enter the market by developing new andpossibly more efficient production processes withlower unit costs. He acknowledged that althoughcost-reducing process R&D was expensive and itsreturn was highly uncertain, it was a key element oflong-term survival and growth for Faradox.Similarly, the president of BigFoot Networks, a

startup that provided microchips for lag and latencyreduction of online games, mentioned that he wasinterested in reducing unit manufacturing costs.However, while making such investment decisions hewas concerned about demand and generating cashflow in the short term, and possible future competi-tion from other startup and established firms such as

Intel and AMD in the long term. Allied issues regard-ing cash flow, demand, competition, and processtechnology also surfaced at other startups, such asAccuWater, a provider of automated irrigation sys-tems and AxsTracker, a high-tech security systemsmanufacturer.Hence, we provide a model accounting for three

key market factors—demand, technological perfor-mance, and competitor’s cost—as a decision supportframework to address the fundamental trade-offbetween investment and the likelihood of bankruptcy,while startup managers make their production andprocess investment decisions.

1.3. Modeling Opportunity, Approach, andManagerial GuidanceAlthough the startup decision-making literatureprovides anecdotal evidence on the relevance ofthe aforementioned trade-offs under uncertainty,we will illustrate in section 2 that there is a gap in theliterature in terms of a modeling framework toprovide precise assessment of production and processimprovement decisions. This has motivated ourefforts to model the trade-off according to the relevantmarket factors and formalize an operating policy,involving production and process investment, for astartup under survival conditions.For ease of exposition, the model specification and

analysis are developed in two stages. In the first stage,we analyze a base case (BC) under deterministicdemand with a two period model. This model charac-terizes an optimal invest-all-or-nothing policy whichderives the conditions for investment in processimprovement to enhance long-term profits. Theresults for the first stage are analytically tractable andserve as benchmarks for the second stage of ouranalysis.In the second stage, we extend the BC with stochas-

tic realization of demand. This is termed the stochas-tic demand and survival constraint (SDSC) case. Withstochastic demand, profits after the first period arenot guaranteed and a probabilistic survival constraintcomes into play. SDSC is amenable to closed-formsolutions under limited conditions; therefore, weexplore the underlying trade-off between long-termand short-term profits under bankruptcy risk througha combination of analytical and numerical analyses.Our results provide model-based guidelines for

production and process investment decisions at start-ups, that are dependent on debt while engaging involume-based competition, in three ways. First, wespecify a probabilistic survival measure to quantifythe risk exposure of the production and investmentdecisions. We identify parameters that must betracked to assess this exposure. Second, whenfaced with demand uncertainty and the consequent

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms2 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

probabilistic survival constraint, we obtain conditionswhen startup managers can respond to the bank-ruptcy risk by creating an operational hedge with pro-duction and process investment decisions. That is,while balancing the bankruptcy risk with futuregrowth opportunities, the startup may behave conser-vatively (aggressively) by investing and producing less(more) than the BC level. Our findings illustrate thatthe three market factors mentioned above—demand,technology, and competition—are intimately linkedin the creation of operational hedges. We study theirindividual impact, and point to the managerial impli-cations of their interactions. In particular, we illustratewhen to focus on either short-term profits by fullyexploiting the current business opportunities or long-term profits by investing in process R&D, under asurvival constraint. Finally, we show that debtconstraint shifts the decision away from an aggressiveoperating region toward a conservative region, and alsoshrinks the overall region where investment is viable.The rest of our article is organized as follows. Sec-

tion 2 provides a review of the related literature. Insection 3 we analyze the BC and characterize a closed-form solution under deterministic demand to offer abenchmark for the SDSC case. We extend our discus-sion to the SDSC case in section 4. In section 5 we dis-cuss the debt capacity constraint. Section 6 describesthe managerial implications of the results. Finally,section 7 concludes by providing a summary andidentifying limitations and potential future work.

2. Literature

We provide a brief review of the streams of literaturethat are closely related to our work: investment inprocess R&D, startup operations and financing, andentrepreneurial decision making.Investment in process R&D and allied cost reduc-

tion and capacity management decisions, by estab-lished firms, have long been key issues in themanagement of technology literature associated withoperations realm (Carrillo and Gaimon 2000, 2004,Chambers and Kouvelis 2003, Gaimon 1989, see espe-cially the review by Gaimon 2008). A relevant litera-ture stream explores the technology adoptiondecisions (Erat and Kavadias 2006, Fine and Freund1990, Gupta and Loulou 1998, Li et al. 2003), andanother aligned stream of literature investigates pro-cess improvement and learning (Lapre et al. 2000, Liand Rajagopalan 1998, 2008, Terwiesch and Xu 2004).For instance, Li and Rajagopalan (2008) consider thevalue of early investment in process improvementand learning, and how it creates an option to invest inprocess in future periods for established firms. Webuild on these ideas by illustrating conditions whereproduction volume might be used as a hedge against

process investment risk. R&D investment underuncertainty in a single-firm setting (Kornish 1999,Kwon 2010) and competitive settings (Mamer andMcCardle 1987) usually yield an “all-or-nothing” typeof policy: adopt the current best technology if the gapbetween current and state-of-the-art technologyexceeds a certain threshold. In this article, we showthat such “all-or-nothing” policies apply under lim-ited conditions in startup settings to avoid bank-ruptcy. Further, the above-mentioned literature doesnot address the startup’s concerns. Our modelendows the theories of investment in R&D and opera-tional practices with the startup’s concerns (Shaneand Ulrich 2004).As mentioned before, financing is a key concern for

startups. Research on operations with debt financinghas been growing (Boyabatli and Toktay 2007, Dadaand Hu 2008, Xu and Birge 2004). A growing body ofliterature deals with decision models involving thefinancing and operations of startups (Babich andSobel 2004, Buzacott and Zhang 2004, Erzurumluet al. 2011, Joglekar and Levesque 2009). Archibaldet al. (2002) argue that if the startups are more inter-ested in surviving than maximizing their profits, theyshould employ conservative strategies. Swinney et al.(2011) build the case on how competition betweenstartup and established firms differs from competitionbetween established firms and show that a startup’spreference to increase its survival affects the competi-tion. They consider a single-period model with a sur-vival maximizing startup. Our model, therefore,addresses a gap in this line of literature by: (i) provid-ing a profit maximization framework for a startupunder a survival constraint, and (ii) examining theeffects of strategic investment and market factorsassociated with the long-term growth and survival ofstartups. Further, we illustrate that financial limita-tions motivate a debt-financed startup to create anoperational hedge linking the production and invest-ment decisions.Finally, research in entrepreneurship identifies

operational risk as a key concern for entrepreneurs(Bamford et al. 2000, Morris et al. 2005). Wu andKnott (2006) empirically investigate the entrepre-neur’s decision of market entry combined with twodistinct sources of uncertainty: demand and the entre-preneur’s own ability to deliver on this demand. Theyargue that entrepreneurs are risk averse with respectto demand uncertainty and risk seeking with respectto their own ability. Corbett and Fransoo (2007)empirically investigate whether or not entrepreneursfollow the newsvendor logic and how their risk pref-erences affect their inventory decisions. However, weare unable to find a framework that links operationaldecisions to the survival risk. Accordingly, our modelestablishes a probabilistic survival measure to assess

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 3

the risk exposure of production and investment deci-sions. We explore circumstances under which thestartup firms focus on survival based on debt servicealong with long-term profitability considerations.

3. The Base Case

To study the impact of relevant market factors on theproduction and investment decisions, we begin byexamining a BC with deterministic demand. We con-sider a two-period model of a risk-neutral startupoffering a single new product (see, for exampleson risk-neutrality, Admati and Pfleiderer 1994,Casamatta 2003, Schmidt 2003). The firm makes pro-duction and process investment in the first period sothat the production costs can be reduced in the secondperiod. The first period begins when the firm borrowscash for production and process investment. The sec-ond period begins when the firm pays off the debtwith interest. Later we will also allow for competitiveentry at the beginning of the second period. Thestartup must generate a pre-specified level of profitfrom its operations during the first period to ensuresurvival into the second period. The objective of thefirm is to maximize the total of two-period profitsunder the survival requirement. We start with somekey assumptions to set up our model.

ASSUMPTION 1. Product R&D is frozen at the beginningof the first period, i.e., at market entry.

At least half of the startup firms in the United Statesenter the market with a novel product (GEM 2007),and many of them continue to invest in productdevelopment in terms of contrasting rates of productvs. process innovation over time (Klepper 1996). Forease of exposition, we do not allow for such invest-ments in product development, so that our analysis isnot confounded by the evolution of product quality.

ASSUMPTION 2. The startup is financed by bank loanswith a constant positive interest rate.

We consider a bank-financed startup, but ourresults trivially extend to bootstrapped firms. Loansare issued at a constant interest rate with a finite loanlimit, and upon fully paying its previous debt thestartup can borrow again to cover its production costand R&D investment. In general, once the loan isgranted to a small firm, the loan terms includinginterest rate and loan limit are determined by indus-try practices and market conditions, and do notdepend on the soft conditions of the borrower firm(Petersen and Rajan 1994). Further, as pointed out inthe economics literature, due to information asymme-tries, increasing interest rates create an adverse selec-

tion problem, i.e., only the high-risk firms borrow(Stiglitz and Weiss 1981). Our observations of prac-tice, at firms such as Faradox, also reveal that bankscontrol their risk exposures by setting debt limitsrather than increasing interest rates. For ease of expo-sition, we consider the effect of an explicit loan limitas an extension in section 5.

ASSUMPTION 3. The startup goes bankrupt and gets liq-uidated unless it pays its debt at the end of each period.

Most startups have limited access to capital marketsand cannot raise additional capital other than their ini-tial funds (Chrisman et al. 1998). In particular, infor-mation asymmetries between the owners of thestartups and the investors, and the uncertainties aboutthe future prospects of the startup severely limit thefirm’s access to capital markets (Shane 2007). Hence,most new businesses are built with limited capital andface bankruptcy in case of a default (Reid 1999).For ease of exposition, we build our model in sev-

eral steps. In section 3.1, we start with a simple modelwith deterministic demand, which serves as a bench-mark for our analysis. Then we sequentially introducetechnological uncertainty and future competition insections 3.2 and 3.3, respectively. Later, in section 4,we extend our analysis to stochastic demand and aprobabilistic survival constraint.

3.1. The Benchmark ModelLet pt, qt, ct, and pt denote the price, quantity, cost,and profits in period t (t = 1, 2), respectively. In thefirst period, the startup is a monopoly firm operatingwith a unit production cost of c1 = c, and receivesfunds, y1, with an interest rate of r. It allocates thesefunds at the beginning of the first period between pro-duction quantity, q1, and process R&D investment, A.We adopt a linear inverse demand function for thestartup’s product as pt(qt) = h � qt � 0, where hdenotes the constant market size. At the end of thefirst period the startup realizes revenues from sales.At the beginning of the second period, the firm makesthe debt payments and observes reduction in unit costif a process investment is made. A minimum profitlevel denoted by p is required for the survival. Theparameter p is an exogenous constant that can eitherbe zero, or greater (lesser) than zero based on the lia-bilities (assets) of the firm. In case the profits are lessthan p, the firm goes bankrupt and gets liquidated.Otherwise, the firm goes into the second period. Itcould then receive a second round of funding, y2, toinvest in production, as this is the final period.For ease of exposition, we assume that the process

R&D investment linearly reduces the unit productioncost in the second period to C2(A, b) = c � bA, whereb is the return on investment (Fine and Freund 1990,

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms4 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

Lenox et al. 2006, Porteus 1985). Our major resultscan be extended to convex and concave return oninvestment; however, we exclude their discussionbecause they provide little additional insights regard-ing the core trade-off. For the benchmark case weassume that b is deterministic, i.e., b = l. Later weconsider b as the stochastic return on investment withmean l and variance r2. We assume that the secondperiod cost cannot be driven to zero, i.e., c2(A, B) > 0.This assumption is similar to the one made in Guptaand Loulou (1998). For brevity, we use the terms“return on process investment” and “technologicalperformance” interchangeably. We offer the followingas the benchmark model:

p� ¼ maxq1;A;y1 � 0

p1ðq1Þ � cð Þq1 � ry1 �Aþ p2ðA;bÞ

s.t. cq1 þA� y1ð1aÞ

p1ðq1Þ � cð Þq1 � ry1 � A� p ð1bÞ

where p2ðA; bÞ ¼ maxq2;y2 � 0

p2ðq2Þ � c2ðA; bÞð Þq2 � ry2

s.t. c2q2 � y2 ð1cÞ

In this model, (1a) and (1c) represent the financialconstraints in the first and second periods, respec-tively, such that the total expenditures of the firm ineach period are limited by the amount of money bor-rowed. (1b) denotes the survival constraint requiringthat the money borrowed in the first period should bepaid back with interest at the end of the period. Basedon our model assumptions, (1a) and (1c) must bebinding. Therefore, we restate (1) as follows:

p� ¼ maxq1A�0

p1ðq1Þ�ð1þrÞcð Þq1�ð1þrÞAþp2ðA;bÞ

s.t. p1ðq1Þ�ð1þrÞcð Þq1�ð1þrÞA�p

where p2ðA;bÞ¼maxq2�0

p2ðq2Þ�ð1þrÞc2ðA;bÞð Þq2 ð2Þ

We characterize the optimal operating decisionsand profits of the benchmark case in Proposition 1.We use the superscript b to denote the benchmarkcase. Later we will use k for the case with competitionand tu for the case with uncertain return on invest-ment. (See the supporting information for the proofsof the lemmas, propositions, and corollaries unlessstated otherwise.)

PROPOSITION 1. When demand and the return on invest-ment are deterministic, the startup’s total profits are maxi-mized by producing the monopoly quantity in the firstperiod, q�1 ¼ qm¼: ðh� ð1þ rÞcÞ=2; and the process R&Dinvestment of the startup is bounded by the discountedexcess monopoly operating profit, Am¼: ðpm � pÞ=1þ r

where pm ¼ ð h� ð1þ rÞcð Þ2Þ=4: Further, the optimal pro-cess investment for the startup, A*, and the optimalexpected profits, p*, are determined by the following:

A� ¼ Am if Db � 0

0 o=w

(; and

p� ¼ðh�ð1þrÞðc�lAmÞÞ2

4 þ p if Db � 0

ðh�ð1þrÞcÞ22 o=w

8<:

where Db ¼ l2ðh�ð1þrÞcÞ2þ8ðh�ð1þrÞcÞl�164 � l2p� 0:

Proposition 1 characterizes the trade-off betweenlong-term and short-term profits under the survivalrequirement. The short-term profits limit the invest-ment amount due to the survival constraint whilethe process investment reduces the unit cost andincreases the long-term profits. Therefore, the profit-maximizing startup is required to jointly considerproduction and investment decisions. In the first per-iod, the short-term profits increase initially and thendecrease with production quantity. Hence, the profitfunction is concave in the output level. This concavefunction yields the optimal monopoly quantity q�1.To explain the relation between the production and

process investment decisions and survival, we definethe firm’s propensity to invest in process improve-ment as Db. In particular, if Db < 0, the firm does notinvest in process improvement (A* = 0). Therefore, theprofits in each period are identical to the monopolyprofits. However, if the firm’s propensity to invest issufficiently high, Db � 0, then it would allocate all ofits excess profits in the first period in process improve-ment (A* = Am). It could later generate enough reve-nues from the second period sales to compensate forthe missed earnings of the first period. Therefore, theoptimal process investment decision for a startupmanager can be characterized by an invest-all-or-noth-ing threshold policy. A sensitivity analysis on Db

reveals that the startup’s propensity to investincreases with mean return on process investment l,market size h, and decreases with initial unit cost c. Ingeneral, the startup manager cannot make the finaldecision in isolation of any of these parameters.

3.2. Technology UncertaintySo far, we have assumed that process investmentreduces the future unit cost of the firm by a determin-istic amount. Nevertheless, for startups with a pro-prietary process like Faradox the return on processinvestment is inherently uncertain. Hence, we extendour discussion in the benchmark case and considerthe impact of the return on investment uncertaintyon the startup’s operating decisions and profits. In

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 5

particular, for every dollar invested, we assume thatthe second-period cost is reduced by a randomamount ~b, with a known distribution function, wð~bÞ,with a mean of l and variance of r2. The followingproposition characterizes the optimal production andinvestment decisions with technology uncertainty.

PROPOSITION 2. When demand is deterministic and thereturn on investment is uncertain, the startup’s optimalproduction quantity is equal to the monopoly quantity. Inaddition, the optimal process investment and profits forthe startup are given by

A� ¼ Am if Dtu � 0

0 o=w

(; and

p� ¼ðh�ð1þrÞðc�lAmÞÞ2

4 þ ð1þrÞ2r2A2m

4 þ p if Dtu � 0

ðh�ð1þrÞcÞ22 o=w

8<:

whereDtu ¼ ðr2þl2Þðh�ð1þrÞcÞ2þ8ðh�ð1þrÞcÞl�16

4 � ðr2 þ l2Þp� 0:

The firm’s propensity to invest increases with thereturn on investment uncertainty, i.e., Dtu ¼ Dbþr2 h� ð1þ rÞcð Þ2=4� r2p: Further, the firm profits arenon-decreasing in r. These imply thatwhen selecting itsproduction technology, the startup should choose thetechnology with more variable returns compared to theones with relatively certain returns. If the technologyinvestment proves to be successful, the firm couldobtain significant cost reduction and a major increase inprofits. Hence, the startup manager should place moreemphasis on process investment and focus on long-termprofits, as the return on investment getsmore variable.

3.3. CompetitionIn this section, we incorporate competition into ourbenchmark model. The sequence of decisions is pre-cisely the same as the case without competition except

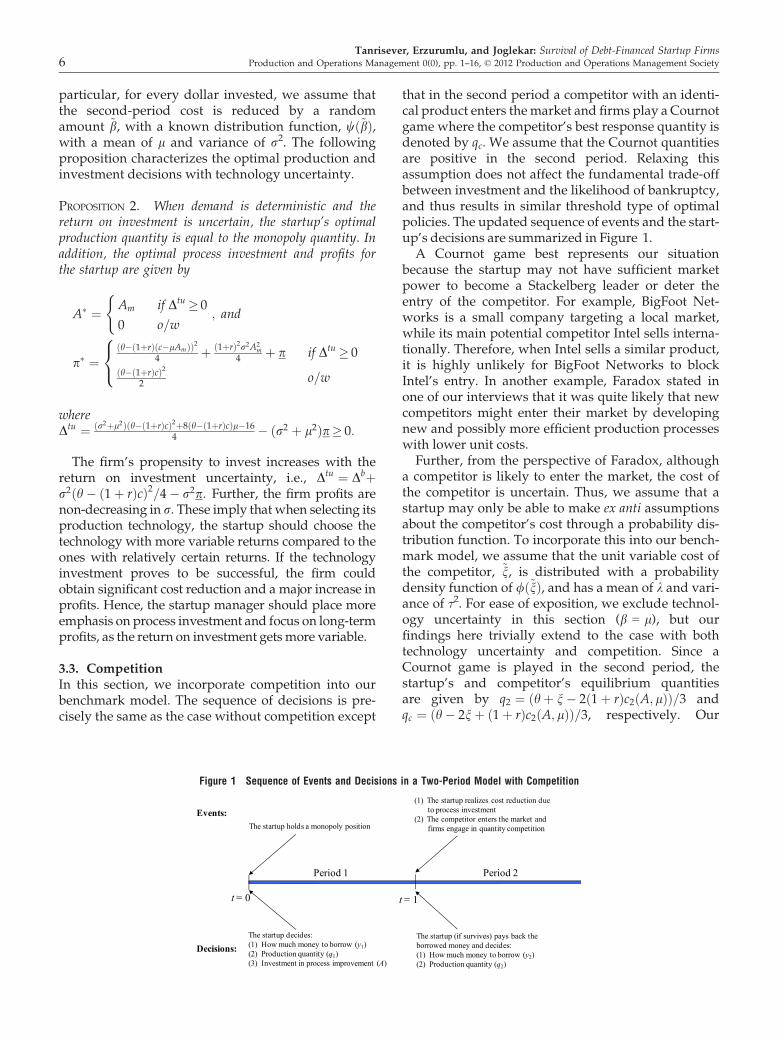

that in the second period a competitor with an identi-cal product enters themarket and firms play a Cournotgame where the competitor’s best response quantity isdenoted by qc. We assume that the Cournot quantitiesare positive in the second period. Relaxing thisassumption does not affect the fundamental trade-offbetween investment and the likelihood of bankruptcy,and thus results in similar threshold type of optimalpolicies. The updated sequence of events and the start-up’s decisions are summarized in Figure 1.A Cournot game best represents our situation

because the startup may not have sufficient marketpower to become a Stackelberg leader or deter theentry of the competitor. For example, BigFoot Net-works is a small company targeting a local market,while its main potential competitor Intel sells interna-tionally. Therefore, when Intel sells a similar product,it is highly unlikely for BigFoot Networks to blockIntel’s entry. In another example, Faradox stated inone of our interviews that it was quite likely that newcompetitors might enter their market by developingnew and possibly more efficient production processeswith lower unit costs.Further, from the perspective of Faradox, although

a competitor is likely to enter the market, the cost ofthe competitor is uncertain. Thus, we assume that astartup may only be able to make ex anti assumptionsabout the competitor’s cost through a probability dis-tribution function. To incorporate this into our bench-mark model, we assume that the unit variable cost ofthe competitor, ~n, is distributed with a probabilitydensity function of /ð~nÞ, and has a mean of k and vari-ance of τ2. For ease of exposition, we exclude technol-ogy uncertainty in this section (b = l), but ourfindings here trivially extend to the case with bothtechnology uncertainty and competition. Since aCournot game is played in the second period, thestartup’s and competitor’s equilibrium quantitiesare given by q2 ¼ ðhþ n� 2ð1þ rÞc2 A; lð ÞÞ=3 andqc ¼ ðh� 2nþ ð1þ rÞc2 A; lð ÞÞ=3, respectively. Our

Events:

Decisions:

t = 0

Period 1 Period 2

The startup holds a monopoly position

The startup decides:(1) How much money to borrow (y1)(2) Production quantity (q1)(3) Investment in process improvement (A)

(1) The startup realizes cost reduction due to process investment

(2) The competitor enters the market and firms engage in quantity competition

The startup (if survives) pays back the borrowed money and decides:(1) How much money to borrow (y2)(2) Production quantity (q2)

t = 1

Figure 1 Sequence of Events and Decisions in a Two-Period Model with Competition

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms6 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

assumption of a duopoly in the second period ensurespositive quantities and startup profits in the secondperiod is p2ðA; n; lÞ ¼ ððhþ n� 2ð1þ rÞc2ðA; lÞÞ2Þ=9:Substituting the expected second period profit, thefirst stage problem becomes:

p� ¼ maxq1;A� 0

fðq1Þ þ gðAÞ

s.t. A� fðq1Þ � p1þ r

; ð3Þ

where gðAÞ ¼ R ðððhþ n� 2ð1þ rÞc2ðA; lÞÞ2Þ = 9Þ/ðnÞdn� ð1þ rÞA and f(q1) = (h � q1 � (1 + r)c)q1. Next,we characterize the optimal operating policy for thebenchmark model with competition.

PROPOSITION 3. Under deterministic demand and returnon investment, when there is competition in the futureperiod, the startup’s optimal production quantity is equalto the monopoly quantity. Further, the optimal processinvestment and profits are

A� ¼ Am if Dk � 00 o=w

�;

where

Dk ¼ ðlðh�ð1þ rÞcÞþ2Þ2�4lðð1þ rÞc�kÞ�13�4l2p9=4 ;

and

From Proposition 3, we find that the startup’s pro-pensity to invest increases with the expected unit costof the competitor, i.e., oDk/ok > 0. In other words, asthe competitor gets stronger (k ↓), the startup is lesswilling to invest since the benefit of investment isreduced with competition and the startup’s propen-sity to invest decreases (Dk ↓). According to ourinvestment policy, the variance of the competitor’scost would not affect the investment decision so longas the quantity response function is linear in the reali-zation of competitor’s cost (see the proof of Proposi-tion 3). Since the Cournot profits are convex inthe competitor’s cost, the startup disproportionately

benefits from high cost entrants. Hence, the optimalprofits increase with τ.Comparing the firm’s propensity to invest for the

cases with and without competition at various levelsof k, we obtain further insights on the impact of thecompetition:

COROLLARY 1. In the presence of competition, the start-up’s propensity to invest increases (decreases) relative tothe benchmark case if the expected competitor is relativelyweak (strong). In particular:

(i) Db �Dk if k� � 7l ððh�ð1þrÞcÞ2=4Þ�p16 þ 2ðhþ7ð1þrÞcÞ

16 ;(ii) Db�Dk o/w.

Corollary 1 shows that the presence of future com-petition may either motivate or deter processimprovement depending on the relative strength ofthe competitor. Against relatively weak rivals, processinvestment significantly mitigates the adverse effectof competition and helps to secure market share inthe future. For example, the firm may find it optimalto invest in the presence of competition although it isbetter off with no investment in the benchmark case,i.e., Db < 0 < Dk. In addition, as the mean return oninvestment increases, the firm becomes more willingto compete against stronger entrants.We have discussed the sensitivity of individual

parameters throughout section 3. Table 1 summarizesthese results. Formal proofs associated with the sensi-

tivity analysis results are available in the OnlineAppendices.

4. The Stochastic Demand and SurvivalCase

In this section, we examine the implications of stochas-tic demand for the startup’s operating decisions. Wereplace the deterministic survival requirement of theBCwith a probabilistic survival constraint. The presen-tation order of SDSC case parallels the development inthe previous section: in section 4.1, we begin with theSDSC model and derive key operational hedging

p� ¼1

9fðh� 2ð1þ rÞcþ kÞ2 þ 4Amð1þ rÞflðh� 2ð1þ rÞcþ kÞ þ ð1þ rÞl2Amg þ s2g þ p if Dk � 0

ðh� ð1þ rÞcÞ24

þ 1

9fðh� 2ð1þ rÞcþ kÞ2 þ sg2 o=w

8><>: :

Table 1 Sensitivity Analysis of the Base Case Propensity to Invest

Propensity toinvest

Market size(h)

Initial cost(c)

Mean return oninvestment (l)

SD of return oninvestment (r)

Mean cost of thecompetitor (k)

Db Increases Decreases Increases N/A N/ADtu Increases Decreases Increases Increases N/ADk Increases Decreases Increases N/A Increases

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 7

behavior together with the survival probabilitymeasure. This measure identifies the risk exposure ofoperational decisions under the market factors ofdemand, technological performance, and competition.Where the SDSC model is not analytically tractable,we resort to numerical analysis in section 4.2. Theresults of the SDSC case are compared with the BCresults in sequence analogous to the BC developmentby introducing technology uncertainty and competi-tor’s cost in sections 4.2.3 and 4.2.4, respectively.

4.1. A Model with Stochastic Demand andSurvivalIn this case, we consider a demand shock, ~et; in eachperiod t (t = 1, 2) with a known probability densityfunction, u(·), with mean zero and variance v2, andcumulative distribution function, ϑ(·). The demandshocks are realized at the end of each period. Weassume that the inverse demand function, ptðqtÞ ¼h� qt þ ~et, is non-negative. We define the first periodexpected excess monopoly operating profits, pm � p,as an index of the immediate economical viability ofthe firm (note that pm ¼ E½ðp1ðqm; ~e1Þ � ð1þ rÞcÞqm� ¼ððh� ð1þ rÞcÞ2Þ=4). Under the SDSC case with tech-nology uncertainty, competition, and stochasticdemand, the two-period expected profit maximiza-tion problem of the startup is given as:

where p1(e1) = (p1(q1, e1) � c)q1 � r(cq1 + A) � A. I isthe first period survival indicator (I = 1 if the firm sur-vives the first period) and M is a large number. In (4),the constraints in the second stage of the problemonly hold if the startup has survived the first period.Consistent with the stipulation in the BC, if the first-period profits are not larger than the minimum profitlevel p1ðe1Þ\pð Þ, the startup cannot play the second-period quantity game. If the startup survives the firstperiod p1ðe1Þ� pð Þ, firms engage in a Cournot compe-tition. Substituting the optimal second-period solu-tion, the startup’s problem in (4) reduces to

p� ¼maxq;A�0

E~e1 ðp1ðq;~e1Þ� cÞq� r cqþAð Þ�Af g

þE~e1;~n;~b

ðhþ ~n�2ð1þ rÞc2ðA; ~bÞÞ2

9jp1ð~e1Þ�p

( )ð5Þ

The first-period quantities in the reduced modelare denoted by q, hereafter. Unlike the BC, the maxi-

mization problem in (5) is not separable inproduction and investment decisions, and it isalso non-convex. Nevertheless, we can still provethe following key relationships for the optimaldecisions.

PROPOSITION 4. Let q* and A* denote the optimal produc-tion and investment levels for the startup in the first period,respectively, when the demand is stochastic. The startupinvests more (less) than the monopoly level, i.e., A* � Am

(A* � Am), if and only if it produces more (less) than themonopoly quantity, i.e., q* � qm (q* � qm).

Proposition 4 provides a justification for linkingoptimal production and investment decisions of astartup under stochastic demand and bankruptcyrisk. We show that, at the optimality, an aggressive(conservative) investment decision, i.e., A* � Am

(A*�Am), implies an aggressive (conservative)production decision, i.e., q* � qm (q* � qm), and viceversa. In particular, under an aggressive investmentplan, the expected cash flow generated by the mono-poly quantity is not sufficient to cover the undertakendebt. Hence, the firm increases its production quan-tity above the monopoly level so as to benefit fromupside demand realizations and increase its survivalchances. Under a conservative investment plan,

however, increasing production above themonopoly level will both decrease the immediateexpected profits and the survival chances of thestartup. Hence, it is never optimal to be aggressive(conservative) in investment and conservative(aggressive) in production. This means that the profitmaximizing startup manager should link the produc-tion and process investment decisions to create anoperational hedge. Accordingly, we define an aggres-sive (conservative) operating policy when the firm bothproduces and invests more (less) than the monopolylevels. We also characterize this linkage with asurvival probability, and provide an equivalentdefinition for aggressive and conservative operatingpolicies.

PROPOSITION 5. Suppose that the demand shock has asymmetrical probability density function (e.g., normal,uniform, etc.) Then, an optimal operating policy isaggressive (conservative) if and only if its survival probability,

p� ¼ maxq1;A� 0

E~e1 ðp1ðq1; ~e1Þ � cÞq1 � rðcq1 þ AÞ � A� �þ E~e1 ;~n;~bp2ðA; ~e1; ~n; ~bÞ

where p2ðA; e1; n; bÞ ¼ maxq2� 0;I2f0;1g

E~e2 ðp2ðq2 þ qc; ~e2Þ � ð1þ rÞc2ðA; bÞÞq2� �

s.t. p1ðe1Þ � p�MðI � 1Þq2 �MI

�Stochastic survival constraints

ð4Þ

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms8 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

P¼: 1� #~e1 ððpþ ð1þ rÞAÞ=qÞ þ q� hþ ð1þ rÞcð Þ; is less(more) than 0.5.

The probability measure in Proposition 5 providesa survival-based characterization of optimal aggres-sive and conservative operating decisions. An optimalaggressive (conservative) operating policy surviveswith less (more) than probability 0.5. An operatingpolicy is considered to be riskier as the survival prob-ability decreases. Proposition 5 establishes the inti-mate connection between the operating policy of thefirm and the survival probability.So far, we have implicitly assumed that the startup

would find a process investment opportunity, but thatmay not be the case. For example, one of the startupswe interviewed, Accuwater, was considering processimprovement for its irrigation system, but could notidentify an opportunity with high return on invest-ment. In the remainder of this section we furtherexplore the availability of investment opportunitiesand the immediate economical viability of the startupthat drive the optimal operating decisions. Corol-lary 2 considers the impact of the availability ofinvestment opportunities on the operating decisionsof immediately economically viable startups.

COROLLARY 2. Suppose the startup is immediately eco-nomically viable in the first period, i.e., pm � p � 0. Ifthere are no process investment opportunities, the firmalways adopts a conservative operating policy. That is,the firm produces less than the monopoly quantity.

In the absence of strategic investment opportuni-ties, adopting aggressive operating plans is not justi-fied for immediately economically viable startups. Toillustrate our finding, we examine a situation with nominimum level of profits, p = 0; and let the demandshocks in each period (et) be uniformly distributedwith U[�b, +b]. We find that when there are no invest-ment opportunities, the objective function is concavein q. In this case, the optimal quantity is given by

q� ¼ h�ð1þrÞc2 � 1

4bðhþk�2ð1þrÞcÞ2þs2

9

� �� qm: Here the first

term is the monopoly quantity, and the second termrepresents the under-production amount due tobankruptcy risk. Note that, if the bankruptcy risk isremoved from the decision framework, the firmsimply produces the first-best production level, i.e.,

the monopoly quantity. That is, the bankruptcy riskdrives an immediately economically viable startup toadopt a conservative policy in the absence of invest-ment opportunities.We now turn our attention to a firm that is not eco-

nomically viable in the first period. We implicitlyassume that the firm is economically viable over theplanning horizon. Otherwise, it is optimal to liquidatethe firm at time zero. Corollary 3 shows thatwhen the startup is not immediately economicallyviable, the firm would always choose an aggressiveoperating policy to benefit from upside deviationsupon which its survival is contingent.

COROLLARY 3. Suppose the startup is not immediatelyeconomically viable in the first period, i.e., pm � p � 0,then the firm always adopts an aggressive operating policy,regardless of the availability of investment opportunities.

We summarize the effects of the immediate eco-nomical viability and the availability of investmentopportunities on the operating policy of the startupin Table 2. As shown in the top left of Table 2, animmediately economically viable startup with invest-ment opportunities may either adopt a conservativeor an aggressive operating policy depending on themarket parameters. We note that this case is not ana-lytically tractable because the problem in (5) is not aconvex optimization problem for all feasible set ofparameter settings. In this case, to further investigatethe effect of market parameters on the choice of con-servative/aggressive operating decisions, we presenta comprehensive computational analysis in the nextsection.

4.2. Computational AnalysisIn this section, we provide a set of numerical analysesto characterize the optimal operating policies for animmediately viable startup with investment opportu-nities.

4.2.1. Design of Numerical Experiments. Ourexperimental design focuses on the survival probabil-ity as the relevant measure of the risk taken by thefirm. Recall that the survival probability is an endoge-nous variable determined by the firm’s productionand investment decisions. We use it as an outcomemeasure to compare results. We begin with examin-

Table 2 Optimal Operating Policy and the Immediate Economical Viability of the Startup

Immediately economicallyviable startup pm � p� 0ð Þ

Immediately economically non-viablestartup pm � p� 0ð Þ

With investment opportunities Conservative or aggressive operatingpolicy depending on market factors

Aggressive operating policy

With no investment opportunities Conservative operating policy Aggressive operating policy

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 9

ing the impact of mean return on investment in sec-tion 4.2.2 in a setup that has no competition, deter-ministic return on investment and zero interest rate(r = 0), similar to the benchmark model in section 3.In this case the optimization problem in (5) reduces to(see the developments in the proof of Proposition 4):

maxq;A� 0

hðq;AÞ ¼ maxq;A� 0

ðh� qÞq� cq� A½ �

þ ðh� ðc� lAÞÞ24

1� #~e1pþ cqþ A

qþ q� h

� �

We explore the impact of technological uncertainty(r) and competition (k) on the operating decisions insections 4.2.3 and 4.2.4, respectively. Allied parame-ters l, r, and k are continuously varied within reason-able ranges in the relevant subsections. Throughoutour numerical analysis we fix the market size and ini-tial unit cost (h = 10, c = 7), so qm = 1.5 and pm = 2.25.Unless otherwise stated, we set v = 1.2 and p = 0. Theimpact of different levels of minimum requiredinvestment (p) and demand uncertainty (v) are inves-tigated in sections 4.2.2 and 4.2.5, respectively. Wepresent a selective set of our results, but we havetested and confirmed similar results with a widerrange of parameter values, selected from the follow-ing sets of data: c ∊ {4, 5, 6, 7, 8}, v ∊ {0, 0.6, 0.9, 1.2,1.5}, and p ∊ {0, 0.5, 1, 1.5}.

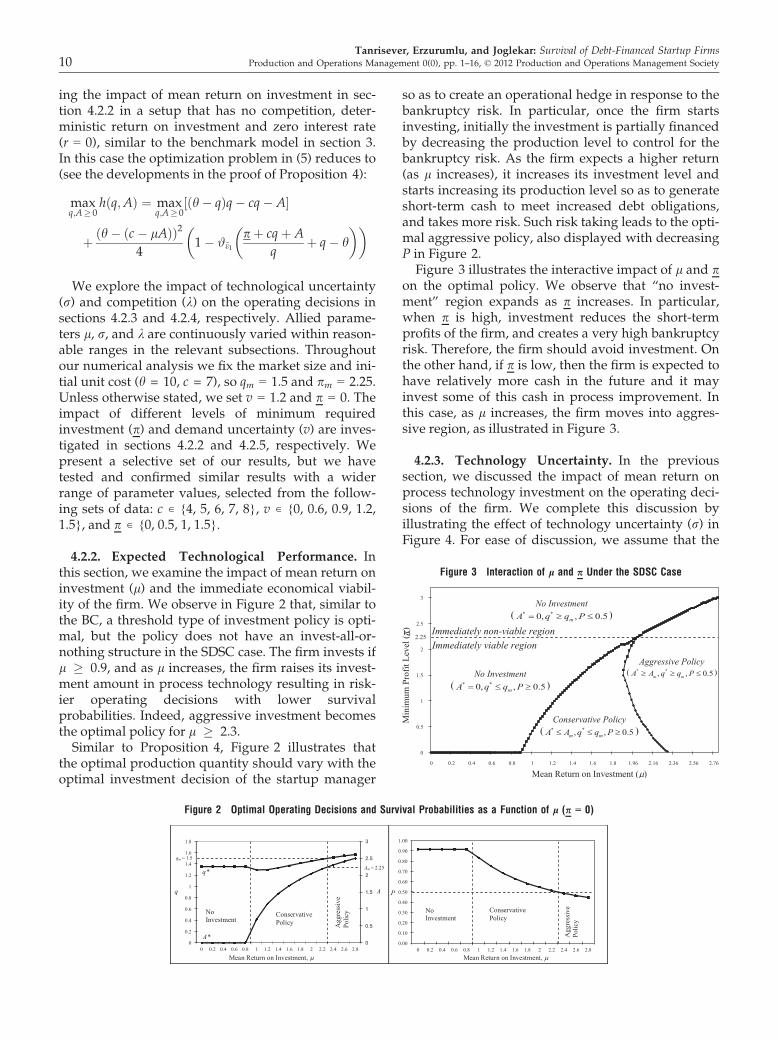

4.2.2. Expected Technological Performance. Inthis section, we examine the impact of mean return oninvestment (l) and the immediate economical viabil-ity of the firm. We observe in Figure 2 that, similar tothe BC, a threshold type of investment policy is opti-mal, but the policy does not have an invest-all-or-nothing structure in the SDSC case. The firm invests ifl � 0.9, and as l increases, the firm raises its invest-ment amount in process technology resulting in risk-ier operating decisions with lower survivalprobabilities. Indeed, aggressive investment becomesthe optimal policy for l � 2.3.Similar to Proposition 4, Figure 2 illustrates that

the optimal production quantity should vary with theoptimal investment decision of the startup manager

so as to create an operational hedge in response to thebankruptcy risk. In particular, once the firm startsinvesting, initially the investment is partially financedby decreasing the production level to control for thebankruptcy risk. As the firm expects a higher return(as l increases), it increases its investment level andstarts increasing its production level so as to generateshort-term cash to meet increased debt obligations,and takes more risk. Such risk taking leads to the opti-mal aggressive policy, also displayed with decreasingP in Figure 2.Figure 3 illustrates the interactive impact of l and p

on the optimal policy. We observe that “no invest-ment” region expands as p increases. In particular,when p is high, investment reduces the short-termprofits of the firm, and creates a very high bankruptcyrisk. Therefore, the firm should avoid investment. Onthe other hand, if p is low, then the firm is expected tohave relatively more cash in the future and it mayinvest some of this cash in process improvement. Inthis case, as l increases, the firm moves into aggres-sive region, as illustrated in Figure 3.

4.2.3. Technology Uncertainty. In the previoussection, we discussed the impact of mean return onprocess technology investment on the operating deci-sions of the firm. We complete this discussion byillustrating the effect of technology uncertainty (r) inFigure 4. For ease of discussion, we assume that the

Figure 2 Optimal Operating Decisions and Survival Probabilities as a Function of l (p = 0)

Figure 3 Interaction of l and p Under the SDSC Case

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms10 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

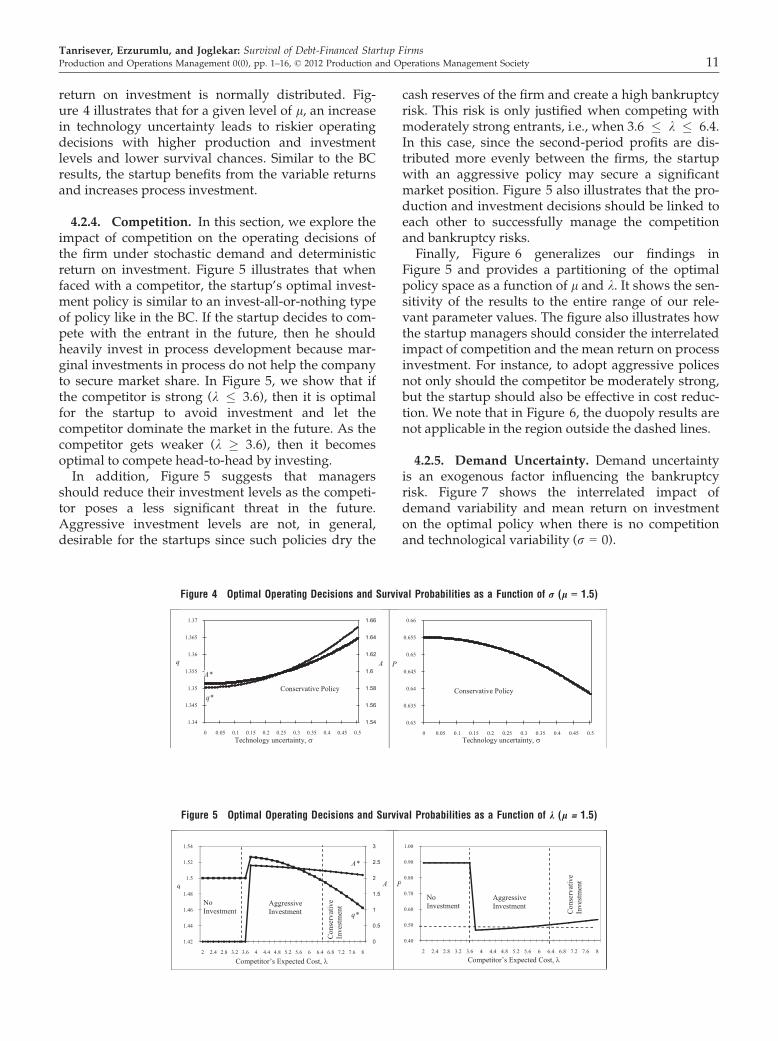

return on investment is normally distributed. Fig-ure 4 illustrates that for a given level of l, an increasein technology uncertainty leads to riskier operatingdecisions with higher production and investmentlevels and lower survival chances. Similar to the BCresults, the startup benefits from the variable returnsand increases process investment.

4.2.4. Competition. In this section, we explore theimpact of competition on the operating decisions ofthe firm under stochastic demand and deterministicreturn on investment. Figure 5 illustrates that whenfaced with a competitor, the startup’s optimal invest-ment policy is similar to an invest-all-or-nothing typeof policy like in the BC. If the startup decides to com-pete with the entrant in the future, then he shouldheavily invest in process development because mar-ginal investments in process do not help the companyto secure market share. In Figure 5, we show that ifthe competitor is strong (k � 3.6), then it is optimalfor the startup to avoid investment and let thecompetitor dominate the market in the future. As thecompetitor gets weaker (k � 3.6), then it becomesoptimal to compete head-to-head by investing.In addition, Figure 5 suggests that managers

should reduce their investment levels as the competi-tor poses a less significant threat in the future.Aggressive investment levels are not, in general,desirable for the startups since such policies dry the

cash reserves of the firm and create a high bankruptcyrisk. This risk is only justified when competing withmoderately strong entrants, i.e., when 3.6 � k � 6.4.In this case, since the second-period profits are dis-tributed more evenly between the firms, the startupwith an aggressive policy may secure a significantmarket position. Figure 5 also illustrates that the pro-duction and investment decisions should be linked toeach other to successfully manage the competitionand bankruptcy risks.Finally, Figure 6 generalizes our findings in

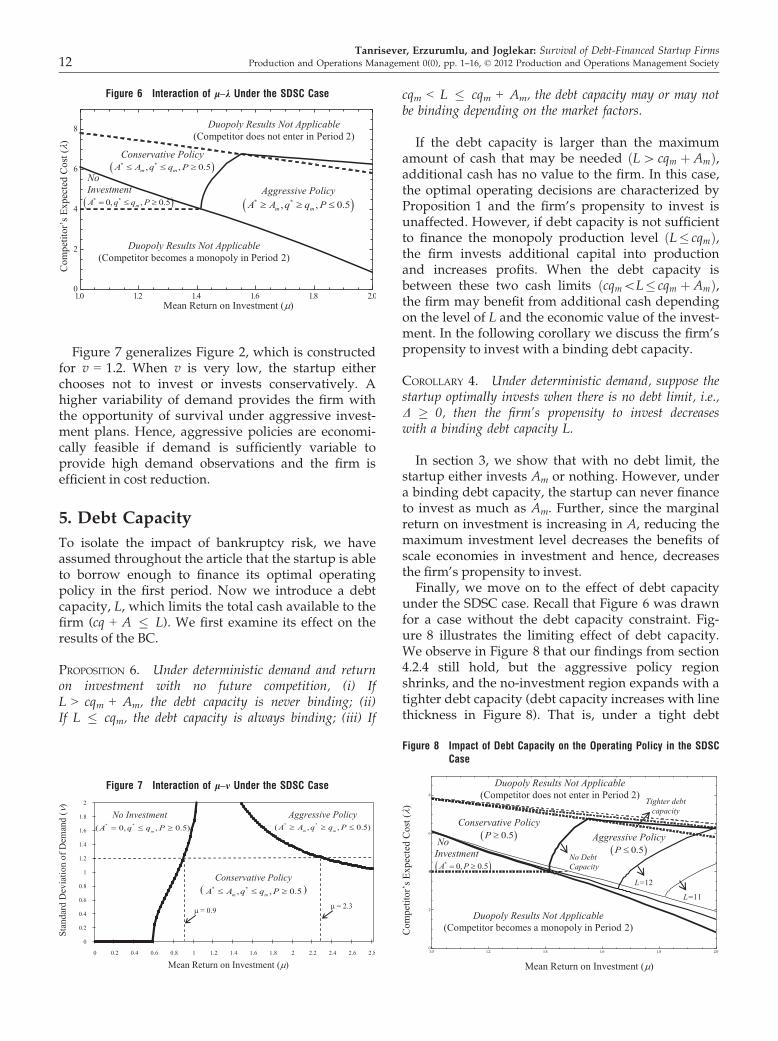

Figure 5 and provides a partitioning of the optimalpolicy space as a function of l and k. It shows the sen-sitivity of the results to the entire range of our rele-vant parameter values. The figure also illustrates howthe startup managers should consider the interrelatedimpact of competition and the mean return on processinvestment. For instance, to adopt aggressive policesnot only should the competitor be moderately strong,but the startup should also be effective in cost reduc-tion. We note that in Figure 6, the duopoly results arenot applicable in the region outside the dashed lines.

4.2.5. Demand Uncertainty. Demand uncertaintyis an exogenous factor influencing the bankruptcyrisk. Figure 7 shows the interrelated impact ofdemand variability and mean return on investmenton the optimal policy when there is no competitionand technological variability (r = 0).

Figure 5 Optimal Operating Decisions and Survival Probabilities as a Function of k (l = 1.5)

Figure 4 Optimal Operating Decisions and Survival Probabilities as a Function of r (l = 1.5)

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 11

Figure 7 generalizes Figure 2, which is constructedfor v = 1.2. When v is very low, the startup eitherchooses not to invest or invests conservatively. Ahigher variability of demand provides the firm withthe opportunity of survival under aggressive invest-ment plans. Hence, aggressive policies are economi-cally feasible if demand is sufficiently variable toprovide high demand observations and the firm isefficient in cost reduction.

5. Debt Capacity

To isolate the impact of bankruptcy risk, we haveassumed throughout the article that the startup is ableto borrow enough to finance its optimal operatingpolicy in the first period. Now we introduce a debtcapacity, L, which limits the total cash available to thefirm (cq + A � L). We first examine its effect on theresults of the BC.

PROPOSITION 6. Under deterministic demand and returnon investment with no future competition, (i) IfL > cqm + Am, the debt capacity is never binding; (ii)If L � cqm, the debt capacity is always binding; (iii) If

cqm < L � cqm + Am, the debt capacity may or may notbe binding depending on the market factors.

If the debt capacity is larger than the maximumamount of cash that may be needed L[ cqm þ Amð Þ,additional cash has no value to the firm. In this case,the optimal operating decisions are characterized byProposition 1 and the firm’s propensity to invest isunaffected. However, if debt capacity is not sufficientto finance the monopoly production level L� cqmð Þ,the firm invests additional capital into productionand increases profits. When the debt capacity isbetween these two cash limits cqm\L� cqm þ Amð Þ,the firm may benefit from additional cash dependingon the level of L and the economic value of the invest-ment. In the following corollary we discuss the firm’spropensity to invest with a binding debt capacity.

COROLLARY 4. Under deterministic demand, suppose thestartup optimally invests when there is no debt limit, i.e.,D � 0, then the firm’s propensity to invest decreaseswith a binding debt capacity L.

In section 3, we show that with no debt limit, thestartup either invests Am or nothing. However, undera binding debt capacity, the startup can never financeto invest as much as Am. Further, since the marginalreturn on investment is increasing in A, reducing themaximum investment level decreases the benefits ofscale economies in investment and hence, decreasesthe firm’s propensity to invest.Finally, we move on to the effect of debt capacity

under the SDSC case. Recall that Figure 6 was drawnfor a case without the debt capacity constraint. Fig-ure 8 illustrates the limiting effect of debt capacity.We observe in Figure 8 that our findings from section4.2.4 still hold, but the aggressive policy regionshrinks, and the no-investment region expands with atighter debt capacity (debt capacity increases with linethickness in Figure 8). That is, under a tight debt

Figure 6 Interaction of l–k Under the SDSC Case

Figure 7 Interaction of l–m Under the SDSC Case

Figure 8 Impact of Debt Capacity on the Operating Policy in the SDSCCase

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms12 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

capacity the startup manager should avoid riskierpolicies.

6. Managerial Implications

Managerially, our results reveal three key themes. Wenote that these themes and allied decision makingcould not be implemented without the help of amodel based on the analysis of production and pro-cess investments.

6.1. Managers Should Be Able to Quantify TheirRisk ExposureWe specify a probabilistic survival measure (P) toquantify the risk exposure of the production andinvestment decisions in Proposition 5. We illustratethe impact of technological performance and competi-tor’s cost in this measure in Figures 2, 4, and 5. Man-agers ought to be able use their ex ante assessments ofreturn on investment for the process technology (l),allied uncertainty (r), and the cost of the competitor’sproduct (k) to quantify their risk exposure using thesefigures.

6.2. Managers May Create Operational HedgesAgainst Bankruptcy RisksWhen faced with demand uncertainty and the conse-quent probabilistic survival constraint, a startup mayrespond to the bankruptcy risk by creating an opera-tional hedge with its production and process invest-ment decisions. That is, while balancing thebankruptcy risk with future growth opportunities, thestartup may behave conservatively (aggressively) byinvesting and producing less (more) than the BClevel. In the conservative case, the firm underproduces (less than the monopoly quantity) so as toallocate more cash to process R&D while controllingthe survival chances. In the aggressive case, however,the startup overproduces (more than the monopolyquantity) to cover the higher bankruptcy risk due toaggressive process investment. In this sense, the deci-sions in the first stage create a process option for thesecond stage (Li and Rajagopalan 2008). Our results,summarized in Figures 3 and 6, indicate that suchhedges are not panacea. If the expected return is low,the competitor is strong, and/or the minimum sur-vival requirement is high, no investment in processimprovement may turn out to be a sound policy.Our results confirm that the three factors mentio-

ned above—demand, technology, and competition—along with the level of profit needed for survival, areintimately linked in the creation of operational hedges—our results quantify their individual impact. Forinstance, Figure 3 documents the impact of the interac-tion of return on investment and the level of minimumacceptable profit. Figures 6 and 7 show the interactions

between return on investment with competitor’s costand level of demand uncertainty, respectively. Manage-rially, these results imply that the firm must track allthese three factors, and update its process investmentdecisions appropriately.

6.3. Debt Constraint Motivates ConservativeDecisionsAlthough this is an intuitive result, our analysis offersa method to account for these constraints and docu-ments their impact on the operating policies (asshown in Figure 8): debt constraint shifts the decisionaway from aggressive operating region toward a con-servative region, and also shrinks the overall regionwhere investment is viable.We illustrate the applicability of our findings by

going back to the examples that we have offered insection 1.2. Consider the technology startups whichcompete on cost and require distinctive productioncapabilities. We discussed Faradox’s efforts todevelop a cost-effective production process. Our anal-ysis indicates that the startup should adopt riskieroperating plans with lower survival chances when itsefficiency of cost reduction increases or when facedwith moderately strong competitors. Also, since thesurvival of aggressive policies is dependent on theupside realizations in demand, highly variable mar-kets create an incentive to follow aggressive policies.Hence, our framework would recommend an aggres-sive operating policy to Faradox since the firm wasfacing high demand variability, high return on invest-ment, and moderately strong competitors. Faradoxreported using a technology fund to develop a newfabrication process as a key part of their long-termbusiness model while seeking manufacturing part-ners to quickly ramp up its production (Hawkins2008).In contrast, BigFoot Networks was in a situation

characterized with high demand variability, moderatelevels of return on investment, and a very strongpotential competitor like Intel. The president of Big-Foot indicated that he currently outsourced manufac-turing and was “cautiously” looking for in-sourcingoptions, which might enhance cost-reduction oppor-tunities.

7. Conclusions

The trade-off between long- and short-term expectedprofits under bankruptcy risk is a relevant problemfor startup managers who wish to make processinvestment decisions aimed at reducing their unitcost. Our contribution toward studying this problemis as follows. First, we develop a model to provide arisk-based justification of the optimal operating policyfor the startups, under debt constraints, by linking

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 13

production with process R&D investment decisions.In particular, we introduce a probabilistic survivalconstraint. This constraint is a unique risk driver thathas not been addressed in the literature. Second, weoffer the following set of model-based recommenda-tions to inform decision making: (i) managers shouldbe able to quantify their risk exposure using a proba-bilistic survival measure developed in this paper; (ii)managers may create operational hedges againstbankruptcy risks; (iii) debt constraint motivates con-servative decisions. Allied results for key factors fromour analysis are summarized in Table 3.Although our stylized model lets us study the fun-

damental trade-off in detail, several assumptions, andrelated potential of extensions, need to be acknowl-edged. First, we focus on a profit-maximizing startup.Yet, a startup may optimize its decisions to maximizethe survival probability explicitly. Second, we con-sider a risk-neutral startup. A further analysis ofstartup firms with different risk attitudes and survivalprobability maximization may provide new insights.Similarly, one could consider learning curve effects orother forms of strategic investment, such as qualityenhancing R&D and marketing. Third, a significantportion of the new firms are financed by bootstrap-ping (Bhide 2000). Our model and results triviallyapply to bootstrapped startups. Venture capital-funded startups and stage financing may introducealternative financial structures and incentive compati-bility issues, and are deemed to be useful researchdirections. Finally, although we provide anecdotalevidence to some of our findings, an empirical studymay further test our findings and strengthen our mes-sage. Future research on these issues will enhance ourunderstanding of startup decision making underfinancial limitations.

Acknowledgments

The authors are grateful to the anonymous referees, thesenior editor, and the department editor for their helpfulcomments. We thank Moren Levesque and Karthik Rama-chandran for their insightful feedback on earlier versions of

this paper. The third author wishes to thank the IC2 Insti-tute and the IROM Department at the University of Texas atAustin for support while the initial draft of this paper wasdeveloped. This research is supported partially by BabsonFaculty Research Fund.

Appendix: Notation

Notation Description

yt Amount of funding borrowed by the startup at the beginningof period t (decision variable)

qt Production quantity of the startup in period t (decisionvariable)

qc Production quantity of the competitor in period 2 (competitor’sdecision variable)

q Production quantity of the startup in period 1 in the reducedmodels (decision variable)

A Process R&D investment of the startup (decision variable)pt Price of the startup’s product in period tct Unit production cost in period tθ Market sizer Interest rateπt Profits of the startup in period tp Minimum profit level required for survivalπm Monopoly operating profitsAm Discounted excess monopoly operating profits~b Stochastic rate of return on investmentwð~bÞ The probability density function of the return on investment, ~bl Mean of the return on investment, ~bσ Standard deviation of the return on investment, ~b~n Stochastic unit variable cost of the competitor/ð~nÞ The probability density function of the competitor’s cost, ~nλ Mean of the competitor’s cost, ~nτ Standard deviation of the competitor’s cost, ~nΔb The startup firm’s propensity to invest in process under

benchmark caseΔtu The startup firm’s propensity to invest in process under

technology uncertaintyΔk The startup firm’s propensity to invest in process under

competition~et Demand shock at period t with cumulative distribution

function, ϑ( · ) with mean zero and standard deviation of vI First period survival indicator (=1 if the firm survives the first

period)M A large numberP The survival probabilityL Debt capacity

Table 3 Impact of Key Factors on the Startup’s Optimal Operating Policy

Factor Impact on optimal operating policy

Return on process investment No investment for low returnsConservative operating policy with moderate returnsAggressive operating policy with sufficiently high l and r

Immediate economical viability No investment at low level of immediate economical viability, pm � pAggressive operating policy for moderate levels of pm � pConservative operating policy for high levels of pm � p

Competition No investment with strong competitorsConservative operating policy with weak competitorsAggressive operating policy with moderately strong competitors

Demand Aggressive operating policy with higher demand variabilityDebt capacity Conservative operating policy with tighter debt capacity

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms14 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society

ReferencesAcs, Z., C. Armington. 2003. Endogenous growth and entrepre-

neurial activity in cities. Working paper. U.S. Bureau of theCensus, Center for Economic Studies, Washington, DC.

Admati, A., P. Pfleiderer. 1994. Robust financial contracting andthe role of venture capitalists. J. Finance 49(2): 371–402.

Archibald, T. W., L. C. Thomas, J. M. Betts, R. B. Johnston. 2002.Should startup companies be cautious? Inventory policieswhichmaximize survival probabilities.Manage. Sci. 48(9): 1161–1174.

Babich, V., M. J. Sobel. 2004. Pre-IPO operational and financialdecisions. Manage. Sci. 50(7): 935–948.

Bamford, C. E., T. J. Dean, P. P. McDougall. 2000. An examinationof the impact of initial founding conditions and decisionsupon the performance of new bank start-ups. J. Bus. Ventur.15(3): 253–277.

Berger, A. N., G. F. Udell. 2003. Small Business Debt and Finance.Acs, Z. J., D. B. Audretsch, eds. Handbook of EntrepreneurshipResearch. Kluwer Academic Publishers, Boston, 299–328.

Bhide, A. V. 2000. The Origin and Evolution of New Businesses.Oxford University Press, New York.

Boyabatli, O., B. Toktay. 2007. Stochastic capacity investment andtechnology choice in imperfect capital markets. Workingpaper, Singapore Management University, Singapore.

Brush, C. G., P. G. Greene, M. M. Hart, H. S. Haller. 2001. Frominitial idea to unique advantage: The entrepreneurial chal-lenge of constructing a resource base. Acad. Manage. Exec. 15(1): 64–78.

Buzacott, J., R. Zhang. 2004. Inventory management with asset-based financing. Manage. Sci. 50(9): 1274–1292.

Carrillo, J. E., C. Gaimon. 2000. Improving manufacturing perfor-mance through process change and knowledge creation. Man-age. Sci. 46(2): 265–288.

Carrillo, J. E., C. Gaimon. 2004. Managing knowledge-basedresource capabilities under uncertainty. Manage. Sci. 50(11):1504–1518.

Casamatta, C. 2003. Financing and advising: Optimal financialcontracts with venture capitalists. J. Finance 58(5): 2059–2086.

Chambers, C., P. Kouvelis. 2003. Competition, learning andinvestment in new technology. IIE Trans. 35(9): 863–878.

Chang, L., P. Powell. 1998. Business process re-engineering inSMEs: Current evidence. Knowl. Process Manage. 5(4): 264–278.

Choi, Y. R., D. A. Shepherd. 2004. Entrepreneurs’ decisions toexploit opportunities. J. Manage. 30(3): 377–395.

Chrisman, J. J., A. Bauerschmidt, C. W. Hofer. 1998. The determi-nants of new venture performance: An extended model.Entrepreneurship Theory Pract. 23(1): 5–29.

Corbett, C. J., J. C. Fransoo. 2007. Entrepreneurs and newsven-dors: Do small businesses follow the newsvendor logic whenmaking inventory decisions? Working paper, UCLA, LosAngeles.

Dada, M., Q. Hu. 2008. Financing newsvendor inventory. Oper.Res. Lett. 36(5): 569–573.

Erat, S., S. Kavadias. 2006. Introduction of new technologies tocompeting industrial customers. Manage. Sci. 52(11): 1675–1688.

Erzurumlu, S. S., F. Tanrisever, N. Joglekar. 2011. Operationalhedging strategies to overcome financial constraints for cleantechnology startups. Z. Luo, ed. Advanced Analytics for Greenand Sustainable Economic Development. IGI Publishing, Hershey,PA, 112–131.

Fine, C. H., R. M. Freund. 1990. Optimal investment inproduct flexible manufacturing capacity. Manage. Sci. 36(4):449–466.

Gaimon, C. 1989. Dynamic game results on the acquisition of newtechnology. Oper. Res. 37(3): 410–425.

Gaimon, C. 2008. The management of technology: A productionand operations management perspective. Prod. Oper. Manag.17(1): 1–11.

Gifford, S. 2003. Risk and uncertainty. Acs, Z. J., D. B. Audretsch,eds. Handbook of Entrepreneurship Research. Kluwer AcademicPublishers, Boston, 37–54.

Global Entrepreneurship Monitor (GEM). 2007. Executive Report.Babson College, Wellesley, MA.

Gupta, S., R. Loulou. 1998. Process innovation, product differenti-ation and channel structure: Strategic incentives in a duopoly.Mark. Sci. 17(4): 301–316.

Hatch, N., J. Dyer. 2004. Human capital and learning as a sourceof sustainable competitive advantage. Strateg. Manag. J. 25(12):1155–1178.

Hawkins, Lori. 2008, November 17. Emerging Technology Fundgrants for Austin firms, Texas state. Austin American-States-man.

Joglekar, N. R., M. Levesque. 2009. Marketing, R&D and startupvaluation. IEEE Trans. Eng. Manage. 56(2): 239–242.

Klepper, S. 1996. Entry, exit, growth, and innovation over theproduct life cycle. Am. Econ. Rev. 86(3): 562–583.

Kornish, L. J. 1999. On optimal replacement thresholds with tech-nological expectations. J. Econ. Theory 89(2): 261–266.

Kwon, D. H. 2010. Invest or exit? Optimal decisions in the face ofa declining profit stream. Oper. Res. 58(3): 638–649.

Lapre, M. A., A. S. Mukherjee, L. N. van Wassenhove. 2000.Behind the learning curve: Linking learning activities to wastereduction. Manage. Sci. 46(5): 597–611.

Lenox, M. J., S. F. Rockart, A. Y. Lewin. 2006. Interdependency,competition, and the distribution of firm and industry profits.Manage. Sci. 52(5): 757–772.

Li, G., S. Rajagopalan. 1998. Process improvement, quality, andlearning effects. Manage. Sci. 44(11): 1517–1532.

Li, G., S. Rajagopalan. 2008. Process improvement, learning, andreal options. Prod. Oper. Manag. 17(1): 61–74.

Li, S., R. Loulou, A. Rahman. 2003. Technological progress andtechnology acquisition: Strategic decision making underuncertainty. Prod. Oper. Manag. 12(1): 102–119.

Mamer, J. W., K. F. McCardle. 1987. Uncertainty, competition, andthe adoption of new technology. Manage. Sci. 33(2): 161–177.

Mishina, Y., T. G. Pollock, J. F. Porack. 2004. Are more resourcesalways better for growth? Resource stickiness in market andproduct expansion. Strateg. Manag. J. 25(12): 1179–1197.

Morris, M., M. Schindehutte, J. Allen. 2005. The entrepreneur’sbusiness model: Toward a unified perspective. J. Bus. Res. 58(6): 726–735.

Petersen, M., R. Rajan. 1994. The benefits of lending relationships:Evidence from small business data. J. Finance 49: 3–37.

Porteus, E. 1985. Investing in reduced setups in the EOQ model.Manage. Sci. 31(8): 998–1010.

Reid, G. C. 1999. Complex actions and simple outcomes: How newentrepreneurs stay in business. Small Bus. Econ. 13(4): 303–315.

Schmidt, K. M. 2003. Convertible securities and venture capitalfinance. J. Finance 58(3): 1139–1166.

Shane, S. 2007. A General Theory of Entrepreneurship. Edward ElgarPublishing Limited, Northampton, MA.

Shane, S. A., K. T. Ulrich. 2004. Technological innovation, productdevelopment, and entrepreneurship in management science.Manage. Sci. 50(2): 133–144.

Shane, S., S. Venkataraman. 2000. The promise of entrepreneur-ship as a field of research. Acad. Manag. Rev. 25(1): 217–226.

Stiglitz, J. E., A. Weiss. 1981. Credit rationing in markets withincomplete information. Am. Econ. Rev. 71(3): 393–410.

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup FirmsProduction and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society 15

Swinney, R., G. P. Cachon, S. Netessine. 2011. Capacity invest-ment timing by start-ups and established firms in new mar-kets. Manage. Sci. 57(4): 763–777.

Terwiesch, C., Y. Xu. 2004. The copy-exactly ramp-up strategy:Trading-off learning with process change. IEEE Trans. Eng.Manage. 51(1): 70–84.

US Department of Energy. 2010. Department of energy awards$92 million for groundbreaking energy research projects.Available at http://arpa-e.energy.gov/Media/News/tabid/83/ItemId/22/vw/1/Default.aspx (accessed date September23, 2010).

Wu, B., A. Knott. 2006. Entrepreneurial risk and market entry.Manage. Sci. 52(9): 1315–1330.

Xu, X., J. R. Birge. 2004. Joint production and financing decisions:modeling and analysis. Working paper, Northwestern Univer-sity, Evanston, IL.

Supporting InformationAdditional Supporting Information may be found in theonline version of this article:

Appendix S1: Proofs.

Appendix S2: Sensitivity Analysis of Db, Dtu, and Dk.

Appendix S3: Computational Procedure.

Please note: Wiley-Blackwell is not responsible for thecontent or functionality of any supporting materials sup-plied by the authors. Any queries (other than missing mate-rial) should be directed to the corresponding author for thearticle.

Tanrisever, Erzurumlu, and Joglekar: Survival of Debt-Financed Startup Firms16 Production and Operations Management 0(0), pp. 1–16, © 2012 Production and Operations Management Society