Embed Size (px)

Citation preview

Product Note on: Masala Bonds

Vinod Kothari Consultants Private LimitedSpecial credits to Mr. Saurabh Jain

1006-1009 Krishna224 AJC Bose RoadKolkata – 700017Phone 033-22811276/ 22813742/ 22817715

601C, Neelkanth, 98, Marine Drive, Mumbai-400002Phone: 022-22817427

A/11, Huaz Khas (Opposite Vatika Medicare)

New Delhi-110016Phone: 011- 41315340

www.vinodkothari.comEmail: [email protected]

What are Masala Bonds?

• Masala Bonds are debt securities denominated in INR issued by Indian entities to

overseas investors but settled in foreign currency. In other words, they are rupee-

denominated bonds issued to overseas buyers.

• These are Indian rupee denominated bonds issued in offshore capital

markets. The issuance of rupee denominated bond is an attempt to shield issuers

from currency risk and instead transfer the risk to investors buying these bonds.

• Interestingly, currency risk is borne by the investor and hence, during repayment

of bond coupon and maturity amount, if rupee depreciates, RBI will realize marginal

saving.

• While masala bonds are issued to overseas investors, still the same is

denominated in Indian rupees. Accordingly, the term ‘masala’ is used to give Indian

flavour to the said bonds.

From where does Masala Bonds Originate?

• International Finance Corporation, an arm of the World Bank and a major

global financial institution that fosters private sector development in developing

countries, has seen its rupee-denominated borrowing in international markets

during fiscal 2015 (year ended June, 30, 2015);

• It came up with two bond issues: Maharaja Bonds which were issued to Indian

investors and the other one was Masala Bonds that were issued to overseas

investors.

• Further, in July 14, 2016, HDFC was the first Indian company to issue masala

bonds and in August 04, 2016, NTPC came up with green masala bonds to

support renewable power projects .

• HDFC was first to list its masala bond on the London Stock Exchange on

August 08, 2016

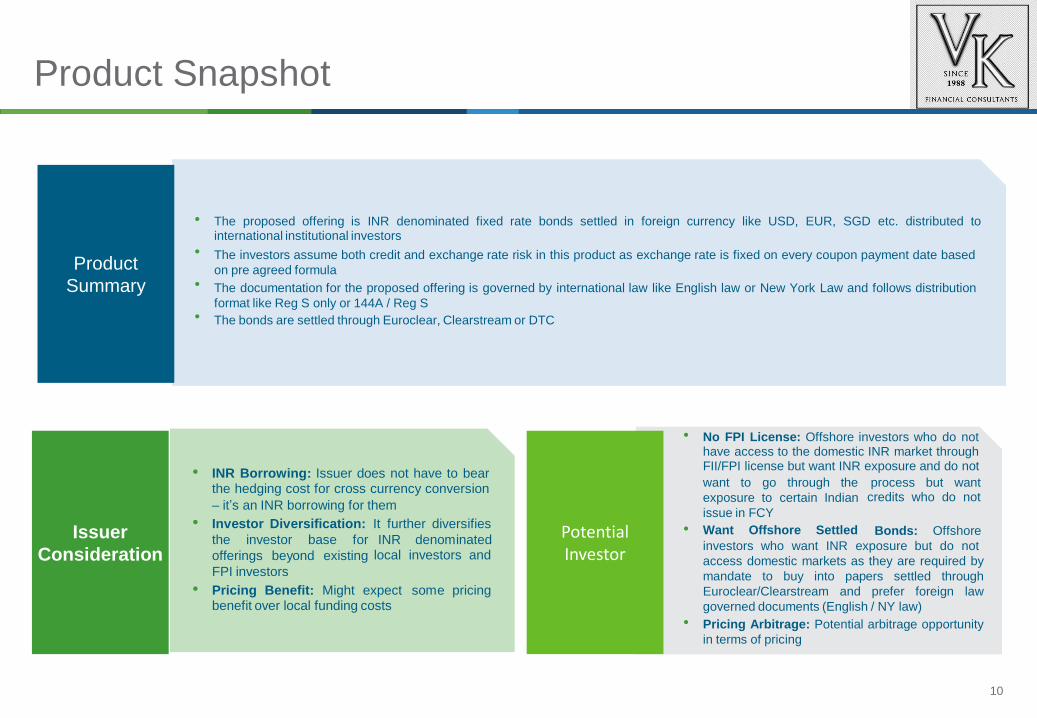

Product Snapshot

•

•

•

•

The proposed offering is INR denominated fixed rate bonds settled in foreign currency like USD, EUR, SGD etc. distributed tointernational institutional investors

The investors assume both credit and exchange rate risk in this product as exchange rate is fixed on every coupon payment date based

on pre agreed formula

The documentation for the proposed offering is governed by international law like English law or New York Law and follows distribution

format like Reg S only or 144A / Reg S

The bonds are settled through Euroclear, Clearstream or DTC

• No FPI License: Offshore investors who do nothave access to the domestic INR market throughFII/FPI license but want INR exposure and do not• INR Borrowing: Issuer does not have to bear

the hedging cost for cross currency conversion

– it’s an INR borrowing for them

want to go through the

exposure to certain Indian

issue in FCY

Want Offshore Settled

process but wantcredits who do not

• Investor Diversification:

the investor base for

offerings beyond existing

FPI investors

It further diversifies • Bonds: OffshoreINR

localdenominated

investors andinvestors who want INR exposure but do not

access domestic markets as they are required by

mandate to buy into papers settled through

Euroclear/Clearstream and prefer foreign law

governed documents (English / NY law)

Pricing Arbitrage: Potential arbitrage opportunity

in terms of pricing

• Pricing Benefit: Might expectbenefit over local funding costs

some pricing

•

10

Product

Summary

Issuer

Consideration

Potential Investor

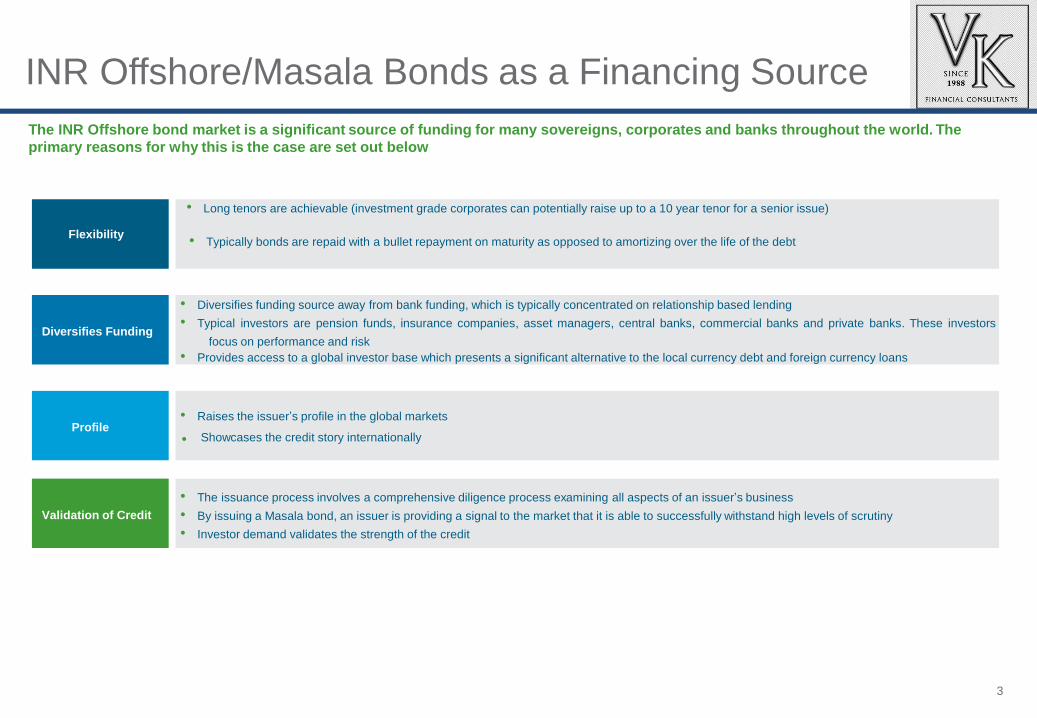

INR Offshore/Masala Bonds as a Financing Source

The INR Offshore bond market is a significant source of funding for many sovereigns, corporates and banks throughout the world. The

primary reasons for why this is the case are set out below

• Long tenors are achievable (investment grade corporates can potentially raise up to a 10 year tenor for a senior issue)

focus on performance and risk

• Showcases the credit story internationally

3

Flexibility

Diversifies Funding

Profile

Validation of Credit

• Typically bonds are repaid with a bullet repayment on maturity as opposed to amortizing over the life of the debt

• Diversifies funding source away from bank funding, which is typically concentrated on relationship based lending

• Typical investors are pension funds, insurance companies, asset managers, central banks, commercial banks and private banks. These investors

• Provides access to a global investor base which presents a significant alternative to the local currency debt and foreign currency loans

• Raises the issuer’s profile in the global markets

• The issuance process involves a comprehensive diligence process examining all aspects of an issuer’s business

• By issuing a Masala bond, an issuer is providing a signal to the market that it is able to successfully withstand high levels of scrutiny

• Investor demand validates the strength of the credit

INR Offshore/Masala Bonds as a Financing Source

• Ongoing equity reporting requirements means minimal effort required in preparation

3

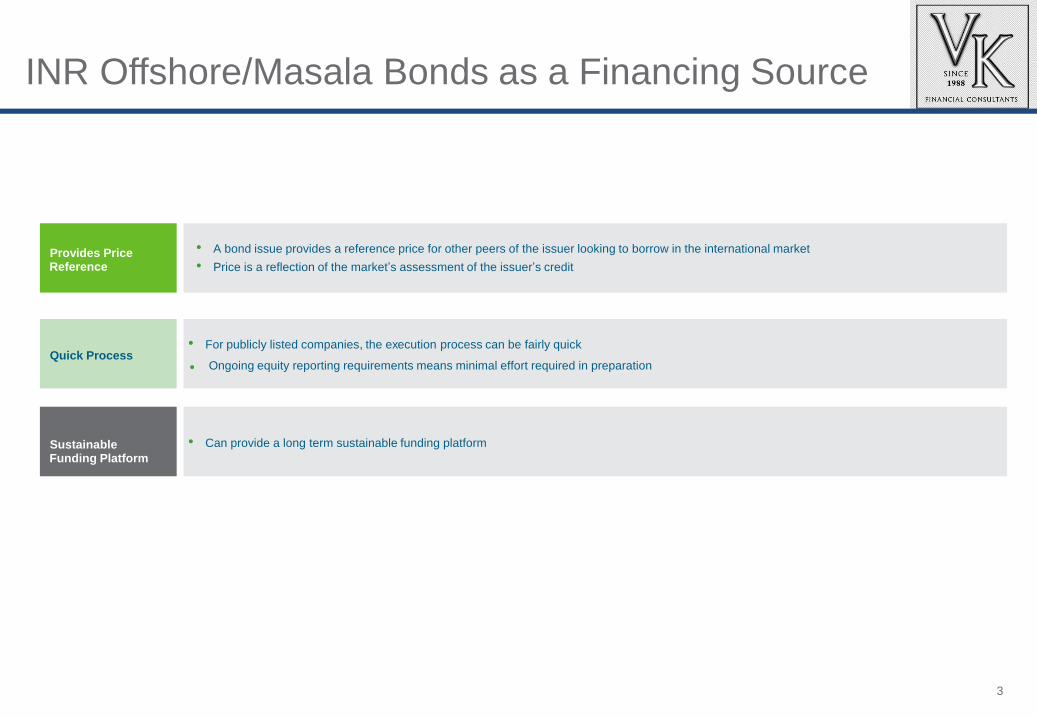

Provides PriceReference

Quick Process

SustainableFunding Platform

• A bond issue provides a reference price for other peers of the issuer looking to borrow in the international market

• Price is a reflection of the market’s assessment of the issuer’s credit

• For publicly listed companies, the execution process can be fairly quick

• Can provide a long term sustainable funding platform

Key Documentation & Process

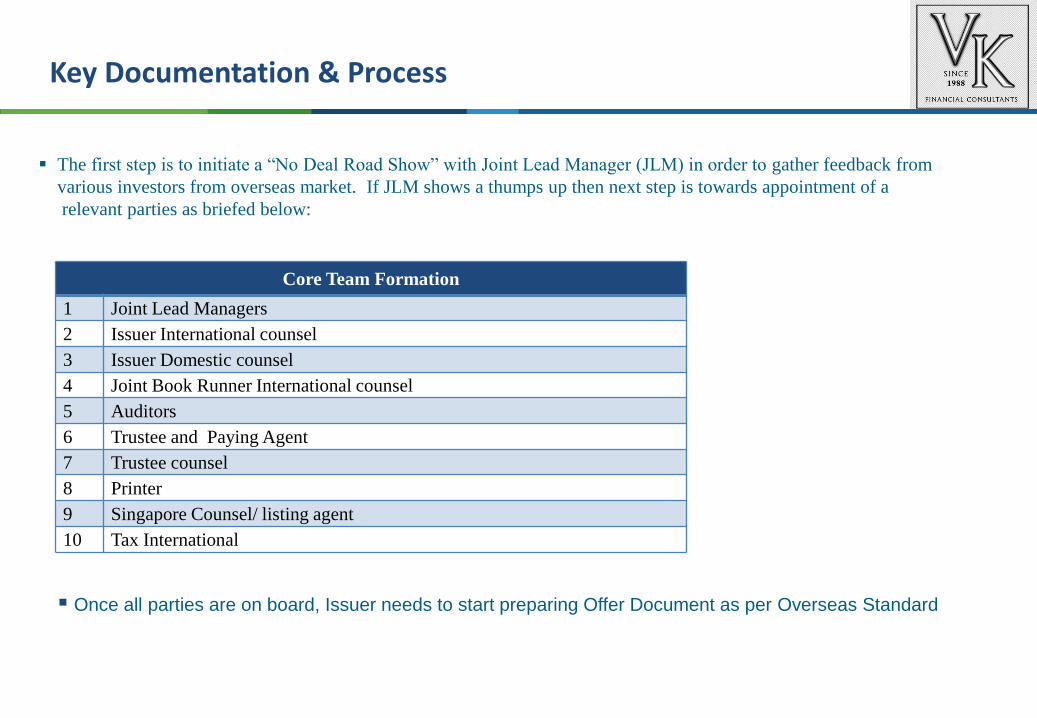

The first step is to initiate a “No Deal Road Show” with Joint Lead Manager (JLM) in order to gather feedback from

various investors from overseas market. If JLM shows a thumps up then next step is towards appointment of a

relevant parties as briefed below:

Once all parties are on board, Issuer needs to start preparing Offer Document as per Overseas Standard

Core Team Formation

1 Joint Lead Managers

2 Issuer International counsel

3 Issuer Domestic counsel

4 Joint Book Runner International counsel

5 Auditors

6 Trustee and Paying Agent

7 Trustee counsel

8 Printer

9 Singapore Counsel/ listing agent

10 Tax International

Key Documentation Features

Key Documentation & Process

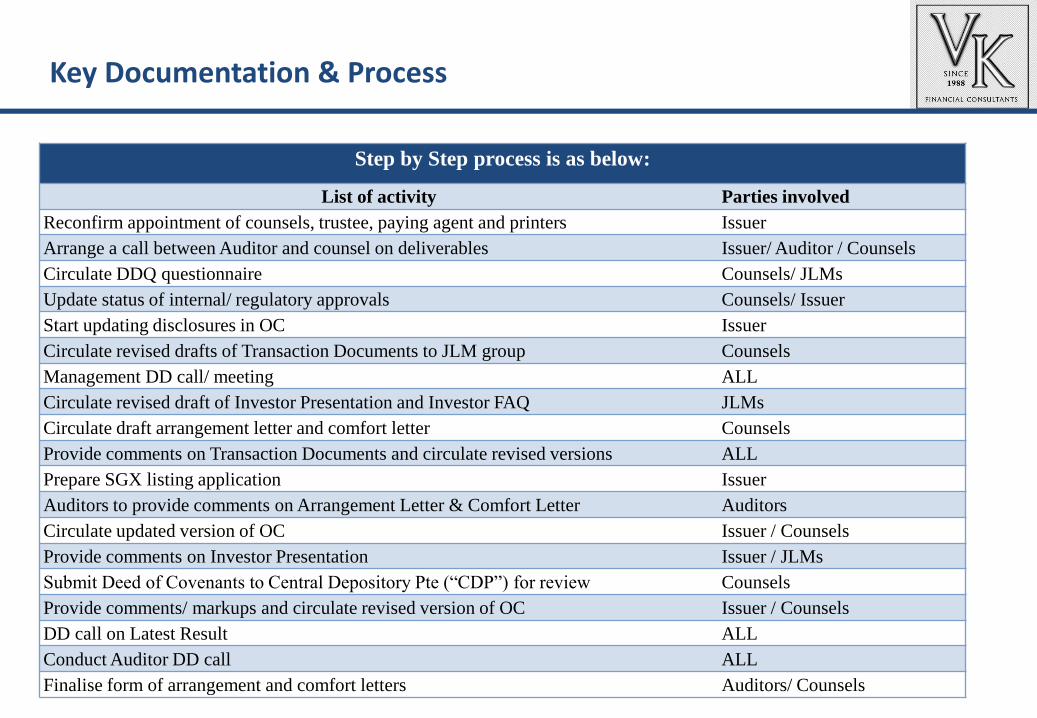

Step by Step process is as below:

List of activity Parties involved

Reconfirm appointment of counsels, trustee, paying agent and printers Issuer

Arrange a call between Auditor and counsel on deliverables Issuer/ Auditor / Counsels

Circulate DDQ questionnaire Counsels/ JLMs

Update status of internal/ regulatory approvals Counsels/ Issuer

Start updating disclosures in OC Issuer

Circulate revised drafts of Transaction Documents to JLM group Counsels

Management DD call/ meeting ALL

Circulate revised draft of Investor Presentation and Investor FAQ JLMs

Circulate draft arrangement letter and comfort letter Counsels

Provide comments on Transaction Documents and circulate revised versions ALL

Prepare SGX listing application Issuer

Auditors to provide comments on Arrangement Letter & Comfort Letter Auditors

Circulate updated version of OC Issuer / Counsels

Provide comments on Investor Presentation Issuer / JLMs

Submit Deed of Covenants to Central Depository Pte (“CDP”) for review Counsels

Provide comments/ markups and circulate revised version of OC Issuer / Counsels

DD call on Latest Result ALL

Conduct Auditor DD call ALL

Finalise form of arrangement and comfort letters Auditors/ Counsels

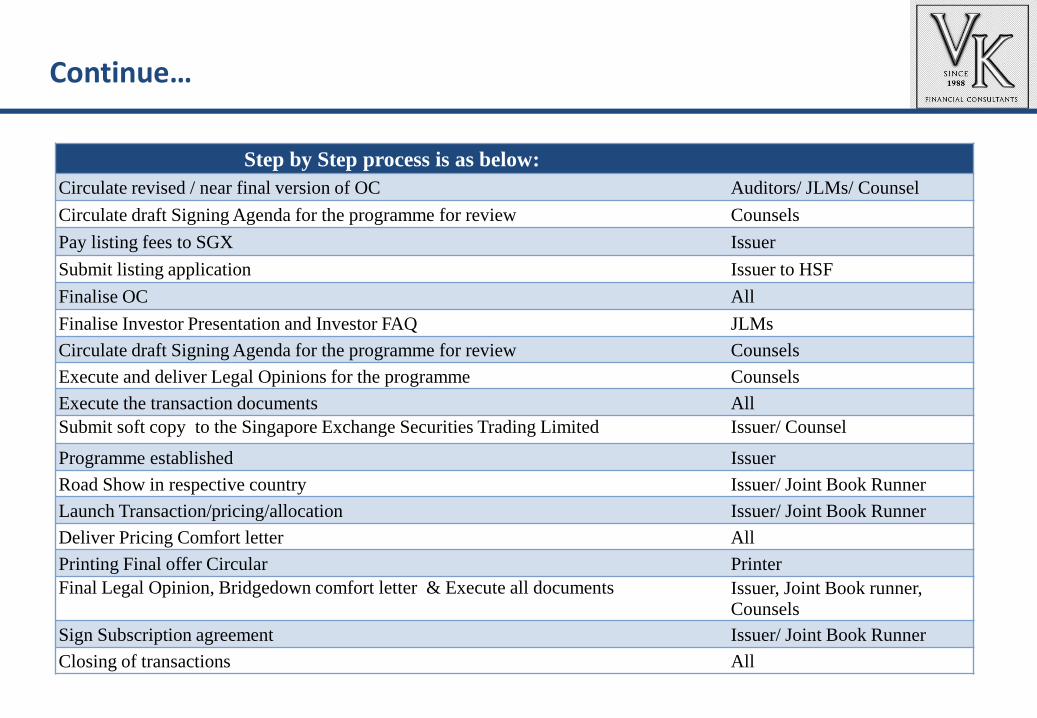

Continue…

Step by Step process is as below:

Circulate revised / near final version of OC Auditors/ JLMs/ Counsel

Circulate draft Signing Agenda for the programme for review Counsels

Pay listing fees to SGX Issuer

Submit listing application Issuer to HSF

Finalise OC All

Finalise Investor Presentation and Investor FAQ JLMs

Circulate draft Signing Agenda for the programme for review Counsels

Execute and deliver Legal Opinions for the programme Counsels

Execute the transaction documents All

Submit soft copy to the Singapore Exchange Securities Trading Limited Issuer/ Counsel

Programme established Issuer

Road Show in respective country Issuer/ Joint Book Runner

Launch Transaction/pricing/allocation Issuer/ Joint Book Runner

Deliver Pricing Comfort letter All

Printing Final offer Circular Printer

Final Legal Opinion, Bridgedown comfort letter & Execute all documents Issuer, Joint Book runner, Counsels

Sign Subscription agreement Issuer/ Joint Book Runner

Closing of transactions All

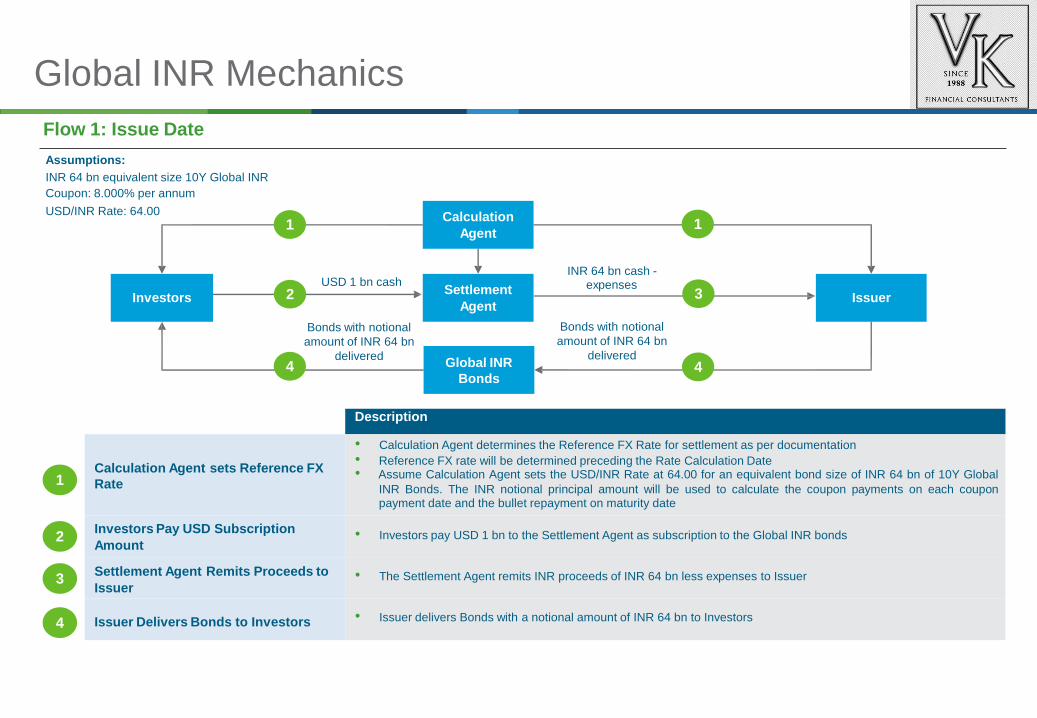

Global INR Mechanics

Flow 1: Issue Date

Assumptions:

INR 64 bn equivalent size 10Y Global INR

Coupon: 8.000% per annum

USD/INR Rate: 64.0011

INR 64 bn cash -expensesUSD 1 bn cash

32

Bonds with notional

amount of INR 64 bn

delivered

Bonds with notional

amount of INR 64 bn

delivered4 4

• Reference FX rate will be determined preceding the Rate Calculation Date

1

2

3

4

Description

Calculation Agent sets Reference FX

Rate

Investors Pay USD Subscription

Amount

Settlement Agent Remits Proceeds to

Issuer

Issuer Delivers Bonds to Investors

• Calculation Agent determines the Reference FX Rate for settlement as per documentation

• Assume Calculation Agent sets the USD/INR Rate at 64.00 for an equivalent bond size of INR 64 bn of 10Y Global

INR Bonds. The INR notional principal amount will be used to calculate the coupon payments on each couponpayment date and the bullet repayment on maturity date

• Investors pay USD 1 bn to the Settlement Agent as subscription to the Global INR bonds

• The Settlement Agent remits INR proceeds of INR 64 bn less expenses to Issuer

• Issuer delivers Bonds with a notional amount of INR 64 bn to Investors

Global INR

Bonds

IssuerSettlement

AgentInvestors

Calculation

Agent

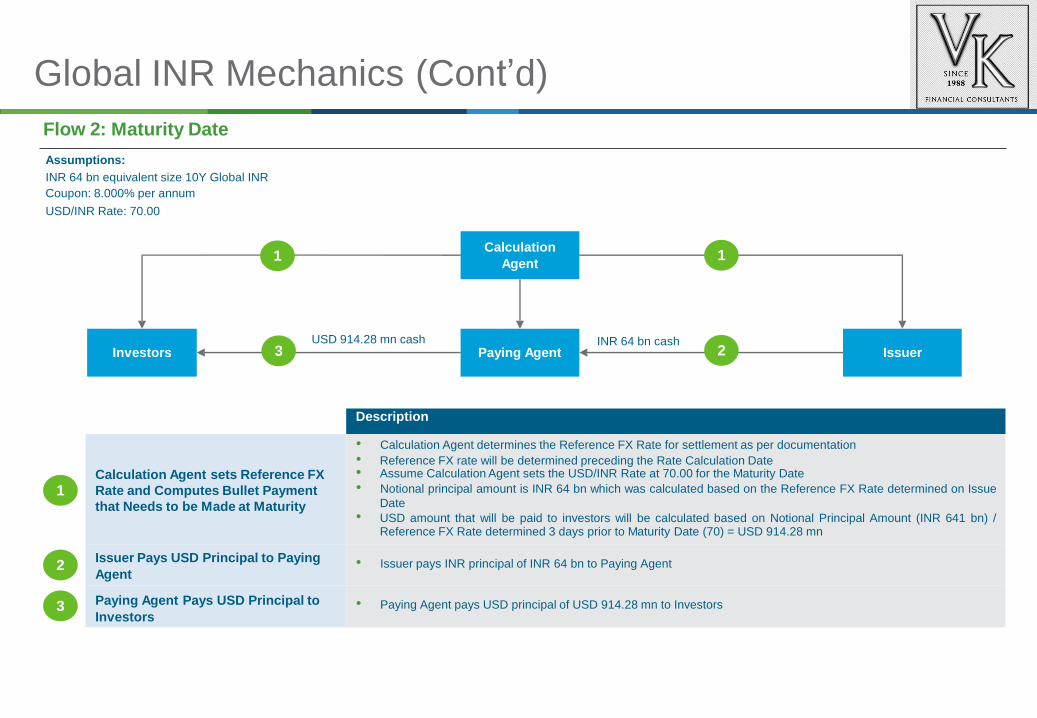

Global INR Mechanics

Flow 2: Maturity Date

Assumptions:

INR 64 bn equivalent size 10Y Global INR

Coupon: 8.000% per annum

USD/INR Rate: 70.00

(Cont’d)

11

USD 914.28 mn cash INR 64 bn cash23

• Reference FX rate will be determined preceding the Rate Calculation Date

1

• USD amount that will be paid to investors will be calculated based on Notional Principal Amount (INR 641 bn) /

2

3

Description

Calculation Agent sets Reference FX

Rate and Computes Bullet Payment

that Needs to be Made at Maturity

Issuer Pays USD Principal to Paying

Agent

Paying Agent Pays USD Principal to

Investors

• Calculation Agent determines the Reference FX Rate for settlement as per documentation

• Assume Calculation Agent sets the USD/INR Rate at 70.00 for the Maturity Date

• Notional principal amount is INR 64 bn which was calculated based on the Reference FX Rate determined on Issue

Date

Reference FX Rate determined 3 days prior to Maturity Date (70) = USD 914.28 mn

• Issuer pays INR principal of INR 64 bn to Paying Agent

• Paying Agent pays USD principal of USD 914.28 mn to Investors

IssuerPaying AgentInvestors

Calculation

Agent

Key Considerations for Investors

• Global INR Bonds is a important investment route for Offshore investors who do not have access to domestic marketthrough FII / FPI license and are not able to currently take exposure in INR denominated credit risks

• Transactions are settled through Euroclear / Clearstream

• Investors who have a view on the currency (USD – INR) and India Credit would be best placed to invest in GlobalINR Bonds

This product become very attractive as the current view is positive on the Indian growth story going forward.•

• Due to market dynamics, different markets could be pricing same credit differently and this provides a window ofopportunity to investors to take exposure in Global INR Bonds

• Investors would prefer liquidity in secondary market to manage their exposure based on their views on credit and FXrate, thus size of the offering will an important parameter for investors

Fungibility of Offshore INR bonds with onshore bonds will help induce liquidity•Liquidity

Arbitrage

Risk

Settlement

Limitation of

Access

Provisions of Companies Act, 2013 applicable to Masala

Bonds

• Masala Bonds are debt securities under section 2(30) of the Companies Act, 2013 ('Act'). Therefore, provisions as applicable to issuance of debt securities shall apply to Masala Bonds as well.

• However, MCA vide its General Circular No: 09/2016 dated 3rd August, 2016 has issued a clarification regarding the applicability of provisions of Chapter III (Prospectus and Issue of Securities) of the Act with respect to the issuance of Rupee denominated bonds to overseas investors by an Indian company;

• Accordingly, Indian companies issuing Rupee denominated bonds overseas (Masala Bonds) under RBI’S policy on ECB Guidelines will not be required to comply with the following:

o Provisions of Chapter III of the Act; ando Provisions governing the issue of secured debentures under Rule 18 of the Companies (Share Capital

and Debentures) Rules, 2014.

• In addition to the above, listed entities in India shall also comply with the provisions of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 with respect to issuance of debt securities.

Peep into the relaxations given through

MCA’s clarification

• In broad terms issuance of Masala Bonds will not require compliance relating to :

o Issue of private placement offer letter (PAS-4);o Preparation of list of allotees (PAS-5);o Filing of return of allotment (PAS-3);o Mentioning the prescribed particulars in the prospectus;o Various other requirements mentioned under Chapter III of the Act; ando Provisions of rule 18 of the Companies (Share Capital and Debentures) Rules, 2014.

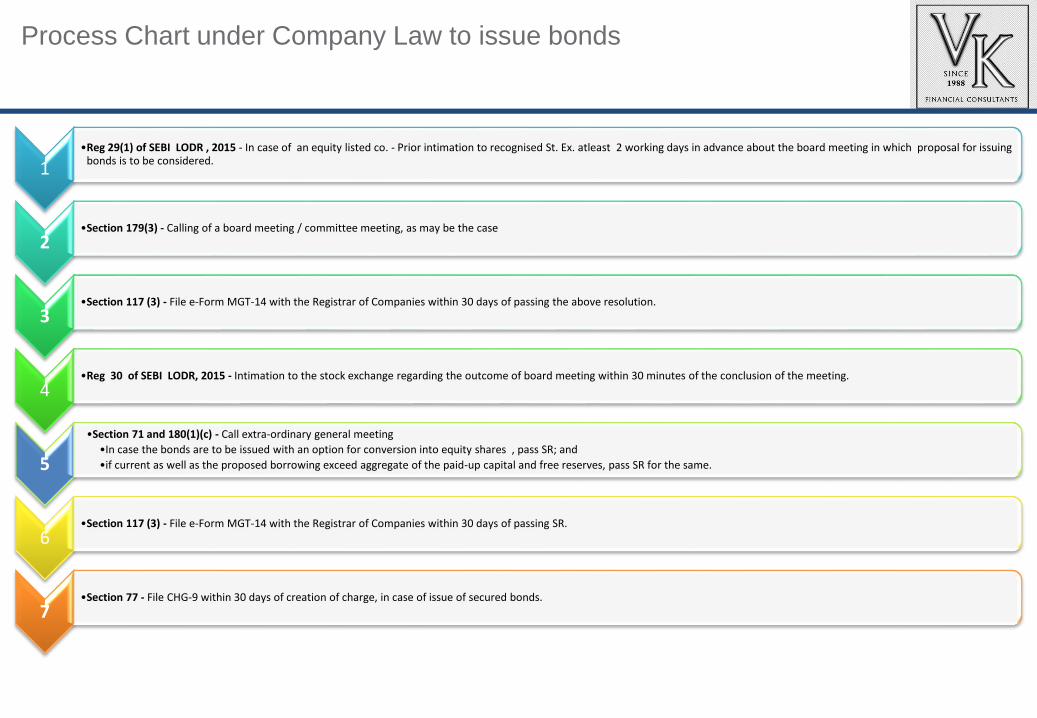

Process Chart under Company Law to issue bonds

1•Reg 29(1) of SEBI LODR , 2015 - In case of an equity listed co. - Prior intimation to recognised St. Ex. atleast 2 working days in advance about the board meeting in which proposal for issuing

bonds is to be considered.

2•Section 179(3) - Calling of a board meeting / committee meeting, as may be the case

3•Section 117 (3) - File e-Form MGT-14 with the Registrar of Companies within 30 days of passing the above resolution.

4•Reg 30 of SEBI LODR, 2015 - Intimation to the stock exchange regarding the outcome of board meeting within 30 minutes of the conclusion of the meeting.

5

•Section 71 and 180(1)(c) - Call extra-ordinary general meeting

•In case the bonds are to be issued with an option for conversion into equity shares , pass SR; and

•if current as well as the proposed borrowing exceed aggregate of the paid-up capital and free reserves, pass SR for the same.

6•Section 117 (3) - File e-Form MGT-14 with the Registrar of Companies within 30 days of passing SR.

7•Section 77 - File CHG-9 within 30 days of creation of charge, in case of issue of secured bonds.

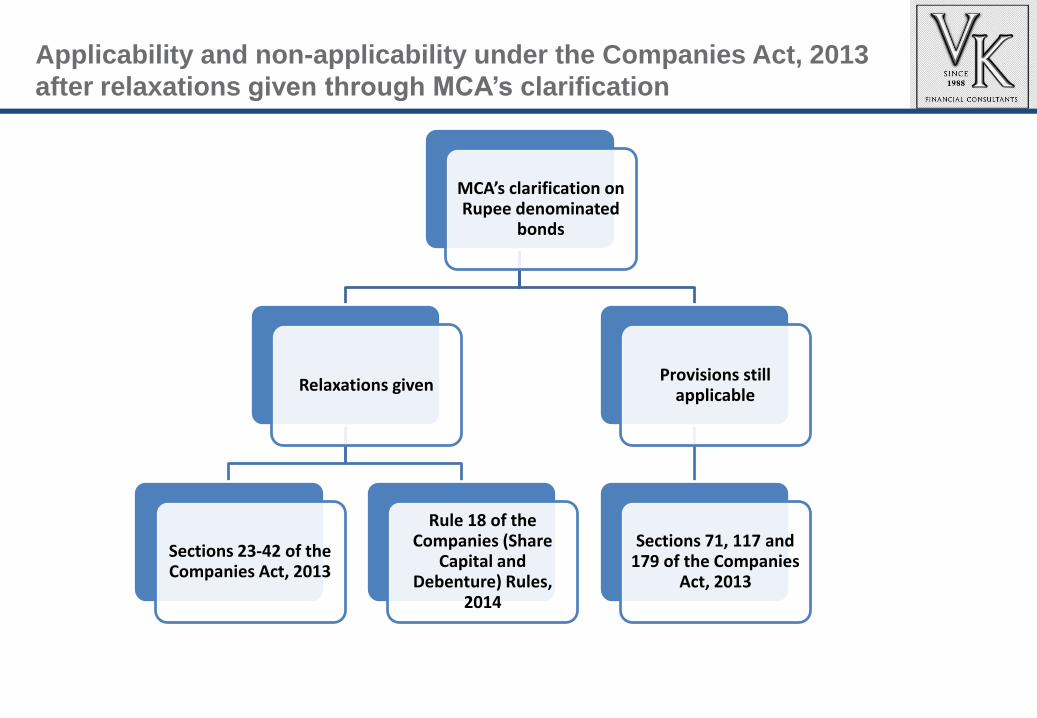

Applicability and non-applicability under the Companies Act, 2013

after relaxations given through MCA’s clarification

MCA’s clarification on Rupee denominated

bonds

Relaxations given

Sections 23-42 of the Companies Act, 2013

Rule 18 of the Companies (Share

Capital and Debenture) Rules,

2014

Provisions still applicable

Sections 71, 117 and 179 of the Companies

Act, 2013

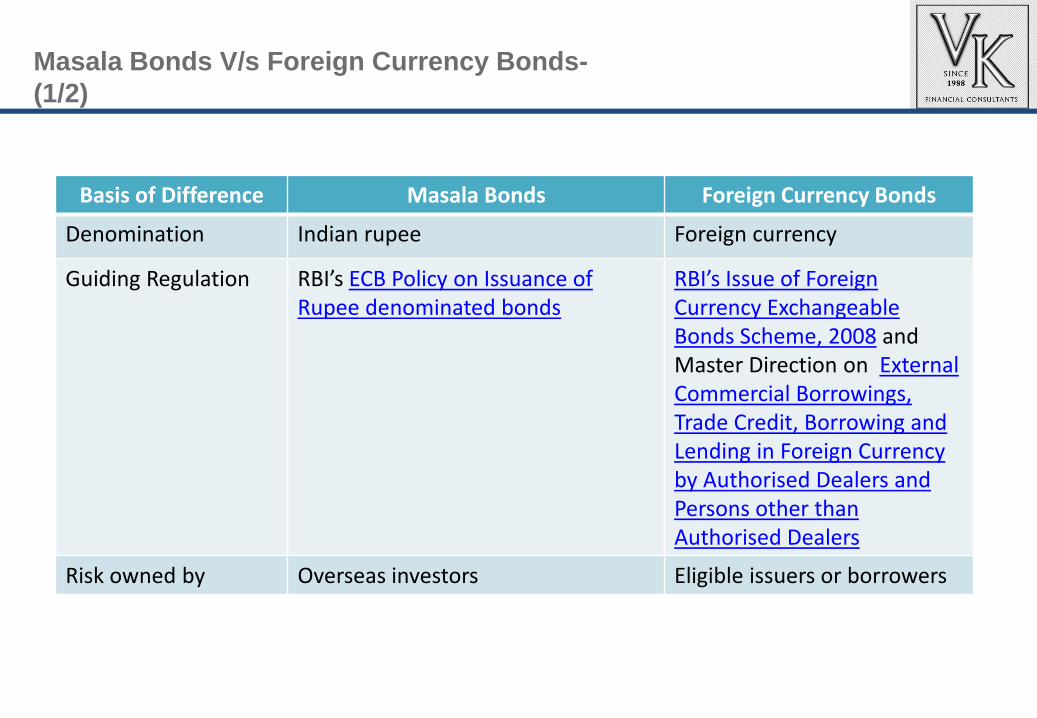

Masala Bonds V/s Foreign Currency Bonds-

(1/2)

Basis of Difference Masala Bonds Foreign Currency Bonds

Denomination Indian rupee Foreign currency

Guiding Regulation RBI’s ECB Policy on Issuance of Rupee denominated bonds

RBI’s Issue of Foreign Currency Exchangeable Bonds Scheme, 2008 and Master Direction on External Commercial Borrowings, Trade Credit, Borrowing and Lending in Foreign Currency by Authorised Dealers and Persons other than Authorised Dealers

Risk owned by Overseas investors Eligible issuers or borrowers

Masala Bonds V/s Foreign Currency Bonds-

(2/2)

Apart from the differences mentioned in the previous slide, both masala bonds and foreign currency bonds are similar with respect to the following:

• Both are issued by Indian companies under ECB route;

• Both are issued to person resident outside India and compliant with the disclosure requirements pursuant to laws of the foreign investor’s jurisdiction; and

• Both are listed on offshore stock exchanges, if listing is contemplated.

SEBI’s circular on Rupee denominated bonds-

• Considering the fact that Masala Bonds are governed by RBI and in order to further streamline the regime, SEBI vide its circular SEBI/HO/IMD/FPIC/CIR/P/2016/67 dated 4th August, 2016 has clarified the following:

• Foreign investment in Masala Bonds will not be treated as investment by Foreign Portfolio Investors (FPIs) ; and

• Will not be covered under the purview of SEBI (Foreign Portfolio Investors) Regulations, 2014, as amended.

• Foreign investments in Masala Bonds will be calculated against the existing corporate debt limit set for investment by FPIs, presently INR 244,323 crore and will be available on tap to the foreign investors.