Embed Size (px)

Citation preview

CBI | Market Intelligence Product Factsheet Cloves in Germany | 1

CBI Product Factsheet:

Seasonless Fashion in Europe

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 2

Introduction

This product fact sheet provides you with information that is relevant if you plan to enter the market for Seasonless

Fashion in Europe. Recession and environmental concerns are creating demand among European consumers for high-

quality clothing items of a classic design that last several seasons. To enter this market, exporters from Developing

Countries need to have efficient and sustainable manufacturing practises and well-thought-out collections supported by

key marketing messages.

Product description

Seasonless design, sometimes also called ‘slow design’, refers to designing apparel products in a timeless manner. Focus is

shifted away from the seasons (spring/summer and autumn/winter) to emphasise the product itself. A piece of apparel is

valued not only by how current it is, but also by its quality and aesthetics. Global and environmental trends are creating a

need for apparel that is designed so that it can be worn any time of the year, anywhere in the world, with consideration for

the environment. The “less is more” consumption trend embodies this design philosophy. Collections focus on essentials

and classics, pieces that can be worn a lifetime, such as little black dresses, monty coats, pencil skirts.

Seasonless fashion refers to long and durable bestsellers, incorporating the assumption that clothing will be re-used over

several ‘fashion cycles’. The ability to extend the product life provides seasonless fashion with an aspect of sustainability.

In some cases, sustainable design principles are extended by using ethical manufacturing principles in material selection

and production process, with the objective of minimising the ‘carbon footprint’.

Product specifications

Seasonless fashion can be incorporated into all apparel category segments (e.g. clothing, shoes and accessories). Products

can be found in all subsectors under apparel:

Knitted and woven clothing (HS codes: 6101 – 6106; 6110; 6201-6206)

Product groups:

Trousers and shorts

T-shirts

Shirts and blouses

Jerseys and cardigans

Dresses and skirts

Jackets and coats

Suits and ensembles

Body wear (HS codes: 6107; 6108; 6115; 6207-6208; 6212)

Product groups:

Underwear

Night and indoor wear (pyjamas, nightshirts, bathrobes)

Hosiery (socks, tights)

Fashion accessories (HS codes: 6116; 6117; 6213-6217)

Product groups

Gloves, mittens & mitts

Neckwear (shawls, scarves)

Carrying products (handbags, shoulder bags, wallets, purses)

Other fashion accessories (handkerchiefs, belts, hats, and caps)

Material and design

Factors to consider when choosing materials are: quality-cost ratio, renewability, and source of the material.

Fibres are used as raw materials with which to create yarn, which is then woven, knitted, matted or bonded into fabric.

Fabrics can be made of natural or synthetic sources, or a blend of the two. The fibre compositions that are most commonly

used in textiles are:

Natural fibres

Natural fibres are found in nature and are not petroleum-based. Natural fibres can be categorised into two main groups: 1)

cellulose or plant fibres and 2) protein or animal fibres. The most common plant fibres are cotton and flax (linen). Other

plant fibres include jute, flax, hemp, ramie, abaca, bamboo (used for viscose), soy, corn, banana, pineapple and

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 3

beechwood (used for rayon). The most common animal fibres are wool and silk. Other animal fibres include angora, camel,

alpaca, llama, vicuna, cashmere and mohair.

Synthetic fibres

Most artificial fibres are produced synthetically from chemical elements or compounds developed by the petrochemical

industry. Viscose, acrylic, nylon, and polyester are common synthetic fibres.

Recycled fibres or materials

Recycled or reclaimed fibres are made from scraps of fabrics collected from clothing factories, which are reprocessed into

short fibres to be spun into new yarn. Only a few facilities in the world are able to process the clippings.

Recycling materials is one way of producing seasonless fashion. Material should be sourced from pre-consumer and post-

consumer waste. Seasonless materials can incorporate vintage, deadstock (stockpiles of clothes from warehouses that

have not been worn before), end-of-roll material or B-grade fabrics.

Any number of the materials and combinations with other materials can be used in the production of seasonless fashion.

Leather, fur, faux-fur, metal, glass, plastics and other materials can also be used. In many cases, shearling, cashmere,

wool, silk and similar materials are preferred. Seasonless pieces are also tending to revert to previously used fabrics,

including velvet, moleskin, cashmere and boiled wool.

Producers targeting the growing niche market for sustainable fashion should give preference to materials with low

environmental impact.

Colours should be attuned to specific target segments or demographic groups. Originally developed by high-end fashion

designers when presenting haute couture collections, the seasonless design concept has since spread to other market

segments. Design combined with marketing constitutes the key element in defining ‘seasonless’ clothing. It is important to

make classic shapes that stand the test of time. Products should be produced for the ready-to-wear market, and it can be

designed according to the demands of the targeted market segment. Designs should reflect the latest seasonless fashion

trends within the targeted segments.

Current (in 2015) seasonless trends:

Layers

Key pieces

Unique use of colours

Conscious materials

Attention to details

All season items

Monty coats

Little black dresses

A-line dresses

V-neck pullovers

Pencil skirts

Shearling

Cashmere

Woll

Silk

Seasonless fashion can be more expensive than seasonal clothing as it is of superior quality and meant to last longer (see for example the upper line of COS- collection of style), although some brands, are producing cheaper versions of seasonless fashion with still an emphasis on timeless silhouette, qualitative material and composition and “must have” concept pieces that form the basis of a good wardrobe.

Labelling and packaging

Labels for transport normally include information on the producer, consignee, composition of the product and the size

of the product, number of pieces, bale/box identification and the total number of bales/boxes, in addition to net and

gross weight.

The most important information on the product or packing labels for seasonless fashion includes composition, size,

origin and care labelling.

Additional information and illustrations of product labelling are provided under the heading ‘Labelling of home textiles

apparel’ in the section on ‘Legal requirements’.

Packaging usually consists of plastic wrapping to protect the fabric from humidity.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 4

Quality

Seasonless design incorporates the rationale of high quality and value for money for products intended for both the low-

end and high-end markets. Several factors contribute to the quality of apparel: performance, reliability, durability, and its

visual and perceived quality. Quality is calculated in terms of the quality and standard of fibres, yarns, fabric construction,

colour fastness, surface designs and final finish. It is important for shipment batches to be of an even quality that fulfils

the agreed-upon specifications.

European consumers expect seasonless design products to be of medium to high quality, in addition to being durable. The

ultimate level of quality depends upon the segment in which the clothing will be sold. For the high-end market, superior

quality is more important.

What is the demand for seasonless design products for Europe?

Notwithstanding the economic downturn, the European market for apparel still is the second largest after China, and is

forecasted to stay at this level until 2025, although the distance with China will widen. Although domestic demand is

slowing down in Europe, the region still represents an important trade, production and creative hub with access to other

growing regions, such as the United States and the BRIC (Brazil, Russia, India and China) countries.

The total European apparel market declined around 10% over the period 2009-2014 and its growth is still forecasted be

negative in 2019: -2%. The six biggest European apparel markets are Germany, United Kingdom, France, Spain, Italy and

the Netherlands, accounting for almost 70 percent of the total European market, still faced declining sales in 2014.

The role of Eastern European countries is becoming increasingly relatively important in Europe, both as a consumer market

and as a partner in production, given proximity and consequently low transport costs and high chances of co-creation.

The biggest apparel importing countries are Germany, France and the United Kingdom, followed by Spain and Italy.

Though it is a small country, the Netherlands is also a relatively big importer due to its role as a trade hub (re-exports).

After a period of three years of stable imports, the imports rose again in 2014 by about 10%. All product groups benefited.

Figure 3: Apparel import by main European buyers in 2014, € million

Source: Trademap

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 5

Figure 4: European imports of apparel by leading countries in € million

Figure 5: European exports of apparel by leading countries between 2010-2014, in € Billion

Source: Trademap

Germany is the biggest importer of apparel products, followed by France, the United Kingdom, Spain, Italy and the

Netherlands. The Netherlands is an interesting country for its role as trade hub within Europe. The same role is played by

Denmark within Scandinavian countries.

Italy is the biggest exporter of apparel in general, while the biggest exporter to other European countries is Germany,

followed by Italy and the Netherlands. Denmark often forms an entry point to the rest of Scandinavian countries.

What European trends offer opportunity for Seasonless Fashion products?

Most important developments: Market drivers for seasonless fashion

The European fashion market is highly dynamic. It is market and brand-driven, with a wide diversity of individual

perceptions and attitudes towards brands and trends. Two consumer trends are predominant in the European market:

1) demand for low-cost fast fashion at 2) premium items that are viewed as investment pieces. Polarization squeezes

the middle or standard ranges. Seasonless design is well positioned in the higher range.

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

2011 2012 2013 2014

RoW DC countries EU 28 intra

0

5

10

15

20

25

In €

billion

2010 2011 2012 2013 2014

Tip:

For your seasonless products focus on traditional importers and exporters, especially those with a big

role within Europe which can facilitate access to other European countries, such as Germany, the

United Kingdom, Italy, Spain France and Scandinavian countries.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 6

Drivers of seasonless fashion:

o Economy

o Climate change

o Environmental awareness

o Co-creation

o Consumer trends

o Social media

Economy

The European recession is creating the need to slow down consumption and buy more durable products. In addition to a

shift in consumption patterns, weather conditions also drive seasonless fashion by providing artificially cold or warm

environments with air-conditioning and central heating.

Demand drivers; globalization and consumption change

Climate change

The distinctions between the seasons are not as clear as they once were. Irregular weather patterns, warmer winters, and

colder summers in Europe are bridging the gap between seasons.

Environmental awareness

In Europe, consumer awareness of environmental and sustainability issues is higher now than it ever has been.

People care about where the things they buy originate. Consumers regard the consumption of food and energy in a

different way than fashion. Transparency and traceability of processes and products could provide another route to large-

scale sustainability, allowing the consumer to easily see where their fashion really comes from and to compare the

sustainability of different brands. Increased consumer awareness of environmental issues is reflected in consumer

behaviour.

Regulatory initiatives at the European level have been launched to promote sustainable practises in the apparel industry.

Co-creation

European buyers are trying more and more to discern themselves from their competitors. Therefore they are focussing on

their own image and design. As a result they may not only look for products from your collection but for producers with

whom they can develop their own products. Therefore it is extra important to show your special skills and production

techniques, as well as the variety of raw materials you work with.

Consumer trends

Demand driving seasonless design comes from the desire to wear clothing items over seasons. Design clothes that

can be worn all year round and for several years, durable and re-use, with focus on appealing/trendy design with

regards to style, in all segments/demographics. These clothes are supposed to have a certain durability in terms of

quality, as well as in terms of style.

Growing interest for quality, natural and organic fibres: Consumers in Europe have a preference for natural, simple

materials, favouring in particular organic authentic products. The European consumer also likes natural fibres for

health reasons and for its feeling. Designers moving in that direction, are helping drive consumer awareness.

Growing use of social media by European brands in branding and communication

The use of social media by European brands makes it easier to exporters to get familiar with their requirements, directions,

preferences and style. Social media are used by European brands to connect with their customers and increase brand

awareness, but the same messages can give exporters good ideas about what is important to them.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 7

What requirements should seasonless apparel product comply with in order to be

allowed onto the European market?

Legal requirements

The General Product Safety Directive applies to all consumer products marketed in Europe. The purpose of the

legislation is to ensure consumer safety.

The European legislation on chemicals is known as REACH.

o Azo dyes are often used in the dyeing process for textile products. Certain azo dyes are carcinogenic and

illegal for use in consumer products in Europe.

o The use of flame retardants is restricted, including Tris (2,3 dibromopropyl) phosphate (TRIS),

Tris(aziridinyl)phosphineoxide (TEPA) and Polybromobiphenyles (PBB). See also CBI Buyer Requirements –

Apparel.

Europe has harmonised legislation regarding the name, composition and labelling of textile products. Any textile

product composed of two or more components with different compositions must bear a label stating the fibre content

of each component. If two or more textile products have the same composition and form a single unit, only one label

is required.

EU legislation: Liability for defective products: If you are an exporter of consumer products, food or similar products,

you are strongly advised to ensure that your products are safe, in order to avoid product liability claims against

defective products.

In theory, your EU buyer can be held responsible for damage caused by defects in your products. Because buyers can

pass claims along to exporters, however, EU legislation on product liability is also relevant to exporters from

developing countries (Directive 85/374/EC).

Tips:

In order to successfully export your products to the European market for seasonless fashion, you

should incorporate sustainability and transparency at all levels of the production chain making it part

of your branding and point of differentiation. Developing country exporters of apparel products should

communicate their company’s performance on responsible water use, energy consumption and

chemicals, which may give them a competitive advantage.

Exporters who can innovate for the European market, by combining introduction of new fibres or

reintroduction of formerly used fabrics (such as velvet, moleskin, cashmere, boiled wool, etc.) with

innovative designs can find opportunities with European buyers seeking to revamp their competitive

advantage.

Get familiar with European brands’ social media and study their direction, requirements and

preferences in terms of quality and design in order to be able to offer added value.

Increasing environmental awareness is driving demand for seasonless sustainable design. Exporters

from Developing Countries should combine seasonless design with sustainable manufacturing

practises. Communicating your company’s efforts in sustainable design can give you a competitive

advantage.

Monitor the latest European fashion trends.

Design key “best sellers” of classic items. Stick with fewer items of good quality while at the same time

keeping costs low.

Focus on classic items and shapes, such as A-line dresses, twinsets, V neck light weight wool pullovers

Consider marketing your clothes as ‘seasonless’ to appeal to the European retail market by building a

story behind your clothes. Themes to use are seasonless, ‘must-have’, classic, eternal, and

sustainable.

Tips:

See the EU Export Helpdesk, for a full list of legal requirements applicable to your product.

Most buyers will require proof of compliance with legal requirements from Developing Country

exporters. You can read more about the General Product Safety Directive in the EU Export Helpdesk.

Make sure your products are free from any restricted substances, such as the mentioned azo dyes.

Find out more about the restricted chemicals in textile products in the EU Export Helpdesk.

Follow any new developments in the field of flame retardants, as new alternatives are being

developed. You can do so, for instance, through the European Flame Retardants Association (EFRA).

You can read more about textile labelling rules in the EU Export Helpdesk. Make sure your product

labels meet the European requirements. You are advised to follow ISO 3758: 2012 on using symbols

on care labelling for textiles.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 8

Non-legislative requirements

The Business Social Compliance Initiative (BSCI) is an auditing system for monitoring the social performance of

suppliers. It was developed by European retailers in order to improve social conditions in sourcing countries.

GOTS is a textile processing standard for organic fibres. This quality mark can be obtained when the producer

complies with standards of social responsibility and the product contains a minimum of 70% organic fibres.

The Oeko-Tex Standard is the world’s leading eco-label for testing textiles for harmful substances. It consists of three

certifications, which address the effects of textile production processes on humans and the environment, in addition

to the effects of the textiles themselves (including the chemicals) on the health and well-being of consumers.

The EU Ecolabel is a voluntary label for products and services with reduced environmental impact. It is awarded only

to products with the lowest environmental impact within a particular product range.

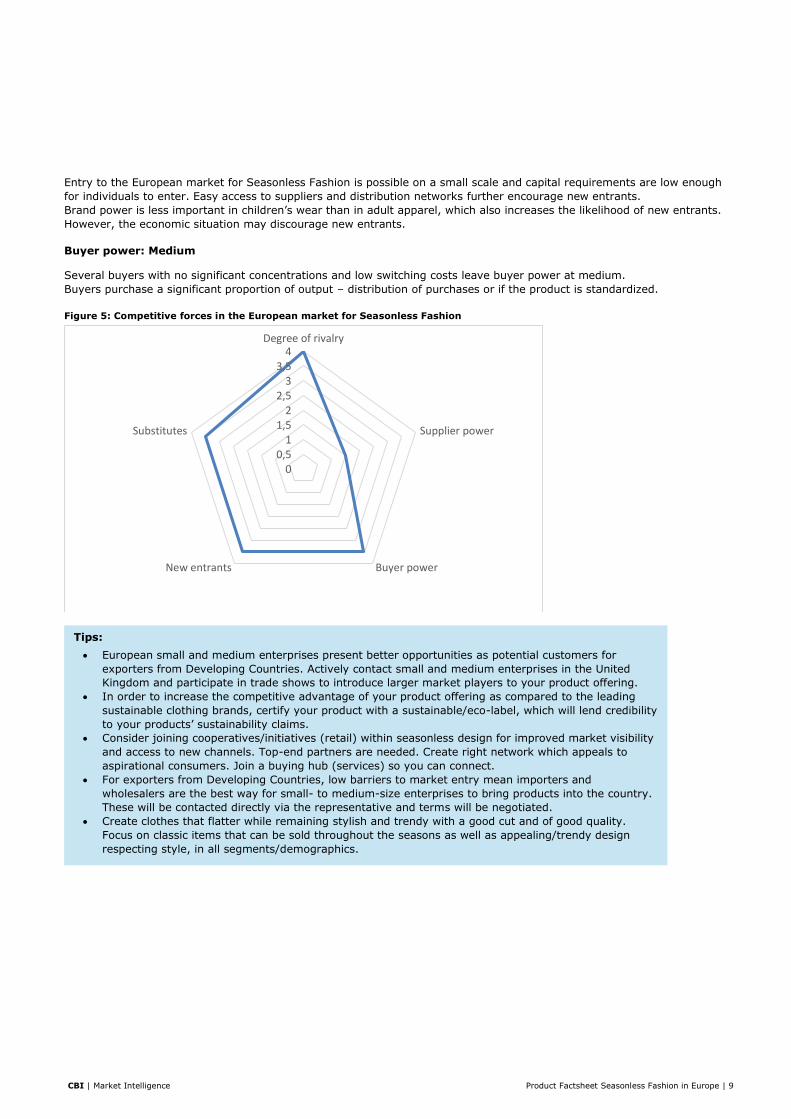

What competition do I face on the European Seasonless product market?

Market entry: Medium

Several retailers and clothing manufacturers have launched new seasonless fashion products. New players are also

entering the market.

Barriers to entry are present and strong brand names are important and new competitors need to establish brand

recognition in the market.

Product competition: High

The threat of substitutes is high as there is a low threshold for consumers to shop around. Brand loyalty could be high in some conscious design segments since the products can be assumed to have a ‘story’

behind them that increases brand loyalty.

Company competition

Degree of rivalry: Medium/High

Medium-high competitive rivalry is present between a large number of companies in the European clothing retail market.

The market is growing, which enables companies to improve revenues. This provides opportunities for suppliers from

Developing Countries looking to enter the market.

High product differentiation has a dampening effect on the degree of rivalry.

Supplier power: Low

Many independent retailers would argue that some of the brands supplying them are also their competitors.

High levels of competition among suppliers act to reduce prices to producers. This can be challenging from the perspective

of a supplier from Developing Countries.

Multiple distribution channels result in less bargaining power for individual distributors.

Substitutes: High

The European market for Seasonless Fashion sees a low threshold for consumers to shop around. Brand loyalty could be

elevated in some conscious design, as well as in high-end segments, since the products can be assumed to have a ‘story’

or a brand name behind them that increases brand loyalty.

New entrants: Moderate to high

Tips:

Consider adhering to the BSCI Code of Conduct. You can perform a self-assessment on your company,

using the tool on the BSCI website.

Try to meet the criteria for GOTS, Oeko-Tex and/or EU Ecolabel certification in order to appeal to the

fast growing organic product niche.

You can read more about voluntary standards, including fair production, in the ITC Standards map

database.

See the CBI Buyer Requirements database for more information on labels and standards: Labels and

Standards: Sustainability for Apparel.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 9

Entry to the European market for Seasonless Fashion is possible on a small scale and capital requirements are low enough

for individuals to enter. Easy access to suppliers and distribution networks further encourage new entrants.

Brand power is less important in children’s wear than in adult apparel, which also increases the likelihood of new entrants.

However, the economic situation may discourage new entrants.

Buyer power: Medium

Several buyers with no significant concentrations and low switching costs leave buyer power at medium.

Buyers purchase a significant proportion of output – distribution of purchases or if the product is standardized.

Figure 5: Competitive forces in the European market for Seasonless Fashion

00,5

11,5

22,5

33,5

4Degree of rivalry

Supplier power

Buyer powerNew entrants

Substitutes

Tips:

European small and medium enterprises present better opportunities as potential customers for

exporters from Developing Countries. Actively contact small and medium enterprises in the United

Kingdom and participate in trade shows to introduce larger market players to your product offering.

In order to increase the competitive advantage of your product offering as compared to the leading

sustainable clothing brands, certify your product with a sustainable/eco-label, which will lend credibility

to your products’ sustainability claims.

Consider joining cooperatives/initiatives (retail) within seasonless design for improved market visibility

and access to new channels. Top-end partners are needed. Create right network which appeals to

aspirational consumers. Join a buying hub (services) so you can connect.

For exporters from Developing Countries, low barriers to market entry mean importers and

wholesalers are the best way for small- to medium-size enterprises to bring products into the country.

These will be contacted directly via the representative and terms will be negotiated.

Create clothes that flatter while remaining stylish and trendy with a good cut and of good quality.

Focus on classic items that can be sold throughout the seasons as well as appealing/trendy design

respecting style, in all segments/demographics.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 10

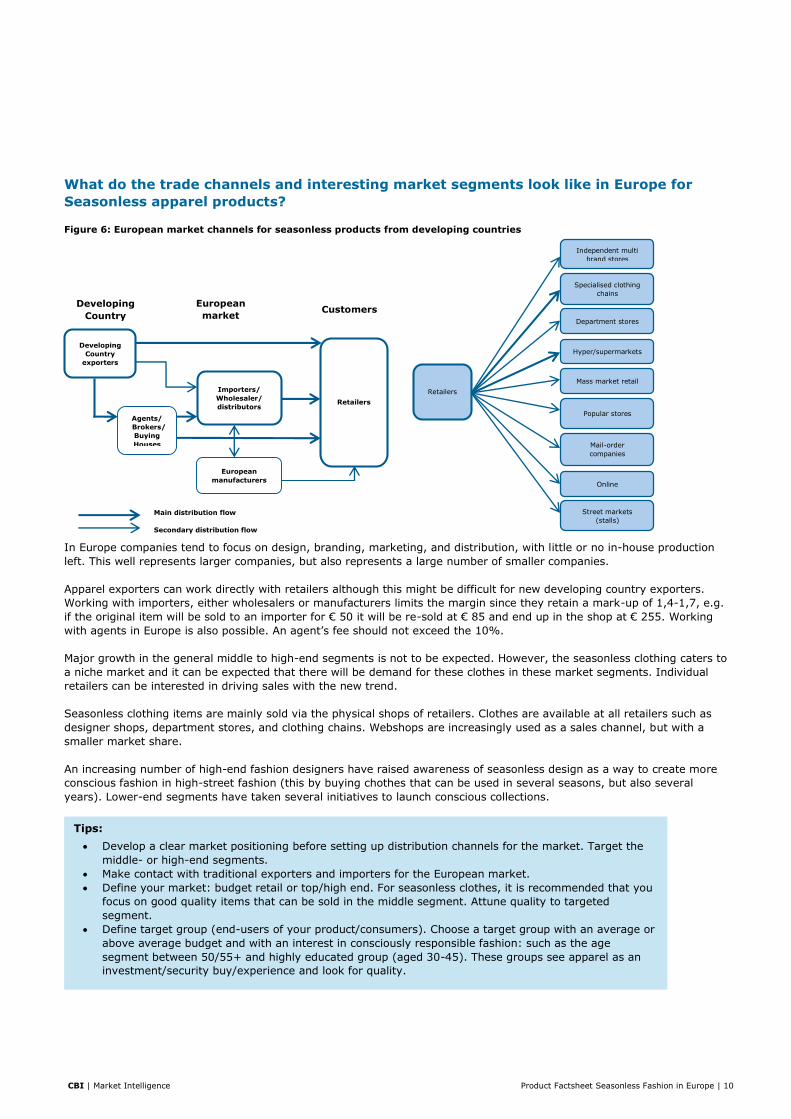

What do the trade channels and interesting market segments look like in Europe for

Seasonless apparel products?

Figure 6: European market channels for seasonless products from developing countries

In Europe companies tend to focus on design, branding, marketing, and distribution, with little or no in-house production

left. This well represents larger companies, but also represents a large number of smaller companies.

Apparel exporters can work directly with retailers although this might be difficult for new developing country exporters.

Working with importers, either wholesalers or manufacturers limits the margin since they retain a mark-up of 1,4-1,7, e.g.

if the original item will be sold to an importer for € 50 it will be re-sold at € 85 and end up in the shop at € 255. Working

with agents in Europe is also possible. An agent’s fee should not exceed the 10%.

Major growth in the general middle to high-end segments is not to be expected. However, the seasonless clothing caters to

a niche market and it can be expected that there will be demand for these clothes in these market segments. Individual

retailers can be interested in driving sales with the new trend.

Seasonless clothing items are mainly sold via the physical shops of retailers. Clothes are available at all retailers such as

designer shops, department stores, and clothing chains. Webshops are increasingly used as a sales channel, but with a

smaller market share.

An increasing number of high-end fashion designers have raised awareness of seasonless design as a way to create more

conscious fashion in high-street fashion (this by buying chothes that can be used in several seasons, but also several

years). Lower-end segments have taken several initiatives to launch conscious collections.

Tips:

Develop a clear market positioning before setting up distribution channels for the market. Target the

middle- or high-end segments.

Make contact with traditional exporters and importers for the European market.

Define your market: budget retail or top/high end. For seasonless clothes, it is recommended that you

focus on good quality items that can be sold in the middle segment. Attune quality to targeted

segment.

Define target group (end-users of your product/consumers). Choose a target group with an average or

above average budget and with an interest in consciously responsible fashion: such as the age

segment between 50/55+ and highly educated group (aged 30-45). These groups see apparel as an

investment/security buy/experience and look for quality.

Developing

Country

European

market Customers

Main distribution flow

Secondary distribution flow

Developing

Country

exporters

Importers/

Wholesaler/

distributors

European

manufacturers

Retailers

Agents/

Brokers/

Buying

Houses

Retailers

Independent multi

brand stores

Specialised clothing

chains

Department stores

Hyper/supermarkets

Mass market retail

Popular stores

Mail-order

companies

Online

Street markets

(stalls)

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 11

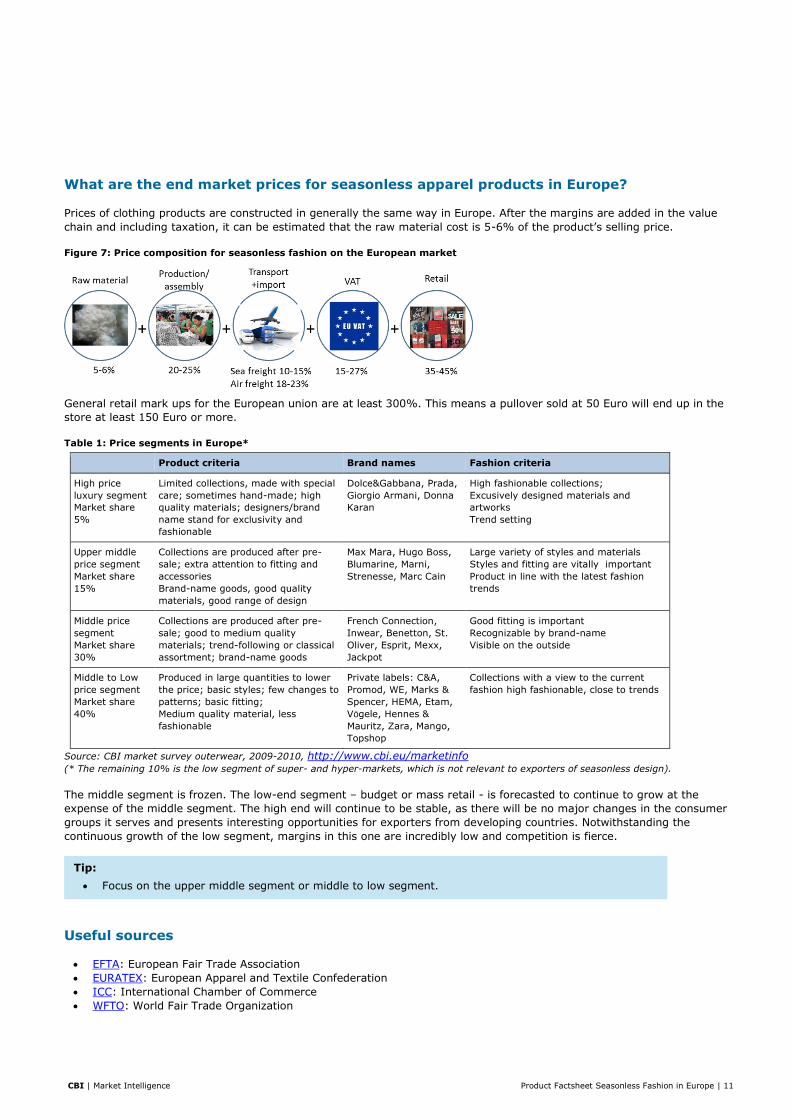

What are the end market prices for seasonless apparel products in Europe?

Prices of clothing products are constructed in generally the same way in Europe. After the margins are added in the value

chain and including taxation, it can be estimated that the raw material cost is 5-6% of the product’s selling price.

Figure 7: Price composition for seasonless fashion on the European market

General retail mark ups for the European union are at least 300%. This means a pullover sold at 50 Euro will end up in the

store at least 150 Euro or more.

Table 1: Price segments in Europe*

Product criteria Brand names Fashion criteria

High price

luxury segment

Market share

5%

Limited collections, made with special

care; sometimes hand-made; high

quality materials; designers/brand

name stand for exclusivity and

fashionable

Dolce&Gabbana, Prada,

Giorgio Armani, Donna

Karan

High fashionable collections;

Excusively designed materials and

artworks

Trend setting

Upper middle

price segment

Market share

15%

Collections are produced after pre-

sale; extra attention to fitting and

accessories

Brand-name goods, good quality

materials, good range of design

Max Mara, Hugo Boss,

Blumarine, Marni,

Strenesse, Marc Cain

Large variety of styles and materials

Styles and fitting are vitally important

Product in line with the latest fashion

trends

Middle price

segment

Market share

30%

Collections are produced after pre-

sale; good to medium quality

materials; trend-following or classical

assortment; brand-name goods

French Connection,

Inwear, Benetton, St.

Oliver, Esprit, Mexx,

Jackpot

Good fitting is important

Recognizable by brand-name

Visible on the outside

Middle to Low

price segment

Market share

40%

Produced in large quantities to lower

the price; basic styles; few changes to

patterns; basic fitting;

Medium quality material, less

fashionable

Private labels: C&A,

Promod, WE, Marks &

Spencer, HEMA, Etam,

Vögele, Hennes &

Mauritz, Zara, Mango,

Topshop

Collections with a view to the current

fashion high fashionable, close to trends

Source: CBI market survey outerwear, 2009-2010, http://www.cbi.eu/marketinfo (* The remaining 10% is the low segment of super- and hyper-markets, which is not relevant to exporters of seasonless design).

The middle segment is frozen. The low-end segment – budget or mass retail - is forecasted to continue to grow at the

expense of the middle segment. The high end will continue to be stable, as there will be no major changes in the consumer

groups it serves and presents interesting opportunities for exporters from developing countries. Notwithstanding the

continuous growth of the low segment, margins in this one are incredibly low and competition is fierce.

Useful sources

EFTA: European Fair Trade Association

EURATEX: European Apparel and Textile Confederation

ICC: International Chamber of Commerce

WFTO: World Fair Trade Organization

Tip:

Focus on the upper middle segment or middle to low segment.

CBI | Market Intelligence Product Factsheet Seasonless Fashion in Europe | 12

Trade fairs

Visiting and, especially, participating in trade fairs is highly recommended as one of the most efficient methods for testing

market receptivity, obtaining market information and finding prospective business partners. Trade fairs continue to be the

most important way to meet new clients on the European apparel market. The most relevant trade fairs in Europe for

seasonless fashion exporters are:

Who's Next Prêt-à-Porter: International trade show Paris

Apparel Sourcing Paris: International Apparel Sourcing Show

London Fashion Week: London

The Sourcing Connection: Worldwide Fashion Sourcing, Paris

PremiereVision: The global event for fashion manufacturing experts, Paris

CBI Market Intelligence

P.O. Box 93144

2509 AC The Hague

The Netherlands

www.cbi.eu/market-information

This survey was compiled for CBI by The Network Academy

in collaboration with CBI sector expert Dhyana van der Pols

Disclaimer CBI market information tools: http://www.cbi.eu/disclaimer

January 2016