Embed Size (px)

Citation preview

GuideAugust 1997

Product Costingand ManufacturingAccounting

Item # A81CEAMA

ReleaseA8.1

���� ��/�*�+ �(*%� �(-*�� �(&)�'0

� �� �- ,+ �.�'-�

��'.�*� �� ���

�()0*#!", ����� ��/�*�+ �(*%� �(-*�� �(&)�'0� ����� ����

�%% �#!",+ ��+�*.��

�"� #' (*&�,#(' #' ,"#+ !-#�� #+ �(' #��',#�% �'� � )*()*#�,�*0 ,*��� +��*�,

( ���� ��/�*�+ �(*%� �(-*�� �(&)�'0� �, &�0 '(, �� �()#��� �#+,*#�-,���

(* �#+�%(+�� /#,"(-, )*#(* /*#,,�' )�*&#++#('� �"#+ !-#�� #+ +-�$��, ,(

�"�'!� /#,"(-, '(,#�� �'� �(�+ '(, *�)*�+�', � �(&&#,&�', (' ,"� )�*,

( ���� ��/�*�+ � �(&)�'0 �'��(* #,+ +-�+#�#�*#�+� �"� +( ,/�*�

��+�*#��� #' ,"#+ !-#�� #+ -*'#+"�� -'��* � %#��'+� �!*��&�', �'� &�0

�� -+�� (* �()#�� ('%0 #' ���(*��'�� /#," ,"� ,�*&+ ( ,"� �!*��&�',�

���� ��/�*�+ �(*%� �(-*�� �(&)�'0 -+�+ �-,(&�,#� +( ,/�*� �#+��%#'!

*(-,#'�+ ,( &('#,(* ,"� %#��'+� �!*��&�',� �(* &(*� ��,�#%+ ��(-, ,"�+�

*(-,#'�+� )%��+� *� �* ,( ,"� ,��"'#��% )*(�-�, �(�-&�',�,#('�

PrerequisiteJ.D. Edwards

Software Fundamentals

Using MenusGetting HelpCustomizing DataReporting

Understanding YourEnvironmentCreating and MaintainingEnvironmentsSetting Up SecurityUpgrading Your System

Online HelpProgramFormField

System Administrationand Environment

Fundamentals

Guides

CD–ROMGuides

Where Do I Look?

TechnicalFoundation

CommonFoundation

Important Note for Students inTraining Classes

This guide is a source book foronline helps, training classes, and

user reference. Training classesmay not cover all the topics

contained here.

Welcome

About this Guide

���$ �&��� "#!'���$ !'�#'��($� ���&$%#�%�! $� "#!���&#�$� � � �)��"��$ �!# %���&##� % #����$� !� ��� ��(�#�$ $!�%(�#�� �!#�$ �$�#�� $ � � (� �!($� $�!( �#� ! �* �)��"��$� � *!&# �!�"� * !"�#�%�$ �% � �����#� % $!�%(�#� ��'��� *!&����% �� � ��$�#�"� ���$ ��%(�� (��% �$ $�!( � %��$ �&��� � � (��% *!& $��! *!&# $�#�� �

���$ �&��� � ��&��$ �)��"��$ %! ���" *!& & ��#$%� � �!( %! &$� %�� $*$%����!& �� ����$$ ��� !� %�� � �!#��%�! ��!&% � %�$� &$� � ��%��# %�� �&��� !# %��! �� � ���"�

���!#� &$� � %��$ �&���� *!& $�!&�� ��'� � �& ���� %�� & ��#$%� �� � !� %��$*$%��� &$�# ���� �� �!��$� � � ��%��!#* �!��$� �!& $�!&�� ��$! � !( �!( %!�

� �$� %�� �� &$

� � %�# � �!#��%�! � �����$

� ���� ��� ��� � � ����%� � �!#��%�!

� #��%� � � #& #�"!#% '�#$�! $

� ����$$ ! �� � �!�&�� %�%�!

Audience

���$ �&��� �$ � %� ��� "#���#��* �!# %�� �!��!(� � �&��� ��$�

� �$�#$

� ��$$#!!� � $%#&�%!#$

� ��� % ��#'���$ "�#$! ��

� ! $&�%� %$ � � ��"���� %�%�! %��� �����#$

Organization

���$ �&��� �$ ��'���� � %! $��%�! $ �!# ���� ���!# �& �%�! � ���%�! $ �! %�� ���"%�#$ �!# ���� %�$� !# �#!&" !� #���%�� %�$�$� ���� ���"%�# �! %�� $ %��� �!#��%�! *!& ��� %! ���!�"��$� %�� %�$�� #& %�� "#!�#��� !# "#� % %��

������� �� ����� ���� ��$ ���� �� � �!��!��"� ���� �� ������ � ������ �������� ����

Section Chapter

OverviewTasks

What You Should KnowAboutField DescriptionsProcessing OptionsTest Yourself

���� �� �� ������� ��� �� ����� ��� ����� �#�� �� ��� ��� ��� ���������� ������� ���������� �������� �� " ������ �� ����� ��� ������ ��� �� ��������� �� ����&����� ��� $� � �� � ����� ��� �� �������

���� � ��� � � ��� ���� � ��� �� �������� �� � ����# �� ���� $� ��� �������� ���� � ����$�

Conventions Used in this Guide

��� �����"��� ����� � !� �������� �� ����� "��� ��� �� ���� � ����

� ��� ������ �� ������ �� "����"�

� ����� ����� ��$ �� �� %������

�� �� �� � %������� ����������� � ��� ��� �� ������ �� ������ �� � ��� ���������� ��� ������ �� ��������� �� ��� ������ �� ������ ������ ����� ����� ������� �� �#���� "���� ������

A8.1 (8/97)

Table of Contents

Overview

�5/0#* �+0#%.�0',+ ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��#�01.#/ ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��.,"1!0 �,/0'+% �+" ��+1$�!01.'+% �!!,1+0'+% �+0#%.�0',+ ���� � � � � � ��!&'#2'+% �$$#!0'2# �,/0 ��+�%#*#+0 ��� � � � � � � � � � � � � � � � � � � � � � � � ��� )#/ ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��#+1 �2#.2'#3 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�.,"1!0 �,/0'+% ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���/0 ��0& �,**�+"/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

��+1$�!01.'+% �!!,1+0'+% ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���/0 ��0& �,**�+"/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

Product Costing

� ,10 �.,"1!0 �,/0'+% ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��#2'#3 �'))/ ,$ ��0#.'�) �+" �,10'+%/ ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�#2'#3'+% �'))/ ,$ ��0#.'�) �+" �,10'+%/ $,. �.,"1!0 �,/0'+% ��� � � � � ��#2'#3'+% �.,"1!0 �,/0'+% '+ �'))/ ,$ ��0#.'�) ��� � � � � � � � � � � � � � � � � ��#2'#3'+% �,10'+%/ $,. �.,"1!0 �,/0'+% �� � � � � � � � � � � � � � � � � � � � � � � �

�#0 �- �.,"1!0 �,/0'+% ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�#00'+% �- �.,"1!0 �,/0'+% ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��#00'+% �- �!!,1+0'+% �,/0 �1�+0'0'#/ ���� � � � � � � � � � � � � � � � � � � � � � � � ��#00'+% �- �0#* �,/0 �#2#)/ ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��,+2#.0'+% �0#* �,/0 �#2#)/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�.,!#//'+% �-0',+/ $,. �0#* �,/0 �#2#) �,+2#./',+ ��� � � � � � � � � � � ��#00'+% �- �0#* �,/0/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�.,!#//'+% �-0',+/ $,. �0#* �,/0 �#2'/',+/ ����� � � � � � � � � � � � � � � � ��#00'+% �- �,/0 �,*-,+#+0/ ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��#00'+% �- ��+1$�!01.'+% �,+/0�+0/ $,. �.,"1!0 �,/0'+% ����� � � � � � � � � ��#00'+% �- �'*1)�0#" ��0#/ $,. � �,.( �#+0#. ����� � � � � � � � � � � � � � � � � � �

�.#�0# �'*1)�0#" �,/0/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�.#�0'+% �'*1)�0#" �,/0/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��.#�0'+% 0&# �,/0'+% �4!#-0',+/ �#-,.0 ����� � � � � � � � � � � � � � � � � � � � � � � �

�.,!#//'+% �-0',+/ $,. �,/0'+% �4!#-0',+/ ���� � � � � � � � � � � � � � � � � ��.#�0'+% � �'*1)�0#" �,))1- ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�1*1)�0'2# �'#)" ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��-#.�0',+ �!.�- ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��.,!#//'+% �-0',+/ $,. �,/0 �'*1)�0',+ ����� � � � � � � � � � � � � � � � � � � � �

�,.( 3'0& �'*1)�0#" �,/0 �,*-,+#+0/ ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�,.('+% 3'0& �'*1)�0#" �,/0 �,*-,+#+0/ ����� � � � � � � � � � � � � � � � � � � � �

Product Costing and Manufacturing Accounting

A8.1 (8/97)

�%5)%6)-' !-$ �%5)2)-' �),4+!3%$ �.23 �.,/.-%-32 ���� � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �-3%1��(!-'% �.23 �.,/.-%-32 ��� � � � � � �

�%33)-' �/ �3!-$!1$ �!3% !-$ �!#3.1 �.$%2 ���� � � � � � � � � � � � � � � � � � � � ��22)'-)-' �!+4%2 3. �2%1 �%&)-%$ �.23 �.,/.-%-32 �� � � � � � � � � � � � � ��%5)%6)-' 3(% �3!-$!1$ �.23 �),4+!3).- �%/.13 ���� � � � � � � � � � � � � � � � ��%33)-' �/ �.23 �4#*%3 �.$%2 &.1 �.23%$ �)++2 .& �!3%1)!+ ���� � � � � � � ��%5)%6)-' �.23%$ �)++2 .& �!3%1)!+ ��� � � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �.23%$ �)++ .& �!3%1)!+ ����� � � � � � � � � � � � � � �

�%33)-' �/ �/%1!3).- �4#*%3 �.$%2 &.1 �.23%$ �.43)-'2 ����� � � � � � � � ��%5)%6)-' ! �.23%$ �.43)-' ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �.23%$ �.43)-' ����� � � � � � � � � � � � � � � � � � � � �

�/$!3% �1.9%- �.232 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�/$!3)-' �1.9%- �.232 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��.41-!+ �-31)%2 &.1 �-:�!-$ �!+!-#%2 ����� � � � � � � � � � � � � � � � � � � � � ��%3!)+ �.41-!+ �-31)%2 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��4,,!18 �.41-!+ �-31)%2 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�.41-!+ �-31)%2 &.1 �� ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��%3!)+ �.41-!+ �-31)%2 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��4,,!18 �.41-!+ �-31)%2 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�1.#%22)-' �/3).-2 &.1 �1.9%- �/$!3% ����� � � � � � � � � � � � � � � � � � � � � ��%5)%6 �.23)-' �-&.1,!3).- �� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�%5)%6)-' �.23)-' �-&.1,!3).- �� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��%5)%6)-' �1.9%- �.23 �.,/.-%-32 �� �� � � � � � � � � � � � � � � � � � � � � � � � � � ��%5)%6)-' 3(% �3%, �%$'%1 �� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �3%, �%$'%1 �-04)18 �� �� � � � � � � � � � � � � � � � �

�%5)%6)-' 3(% �)-'+% �%5%+ �.23%$ �)++ .& �!3%1)!+ �%/.13 �� �� � � � � � � � ��1.#%22)-' �/3).-2 &.1 �.23%$ �)++ .& �!3%1)!+ �%/.13 �� � � � � � � � � �

�%5)%6)-' 3(% �4+3):�%5%+ �.23%$ �)++ .& �!3%1)!+ �%/.13 �� �� � � � � � � � ��1.#%22)-' �/3).-2 &.1 �4+3)��%5%+ �.23%$ �)++ �%/.13 ����� � � � � � � �

�%5)%6)-' 3(% �.23 �.,/.-%-32 �%/.13 ����� � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �.23 �.,/.-%-3 �1)-3 ����� � � � � � � � � � � � � � �

�%5)%6)-' 3(% �.23 �-3%'1)38 �%/.13 ����� � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �.23 �.,/.-%-3��%$'%1 �-3%'1)38 ����� � � � �

.1* 6)3( �$$)3).-!+ �.23)-' �%!341%2 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � �

.1*)-' 6)3( �$$)3).-!+ �.23)-' �%!341%2 ���� � � � � � � � � � � � � � � � � � � � � ��./8)-' �.232 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �./8 �.23 �!+4%2 ����� � � � � � � � � � � � � � � � � � �

�./8)-' �1.9%- �.232 3. �),4+!3%$ �.232 ����� � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �.23 �),4+!3).- � �%&1%2( ����� � � � � � � � � � � �

�/$!3)-' �!+%2 �1$%1 �1)#%��.23 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �/$!3% �!+%2 �1$%1 �.23��1)#% ����� � � � � � � �

�/$!3)-' �1.$4#3 �.232 ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��1.#%22)-' �/3).-2 &.1 �3%, �.23 �%5)2).-2 ������ � � � � � � � � � � � � � � � �

Product Costing in ERPx Environments

�".43 �1.$4#3 �.23)-' )- ���7 �-5)1.-,%-32 ���� � � � � � � � � � � � � � � � � ��-$%123!-$ �!3#( �1.$4#3 �.23)-' ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�".43 �!3#( �1.$4#3 �.23)-' ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

Table of Contents

A8.1 (8/97)

&7-.;<=*7- ";8->,= �8<=270 /8; �2= �=.6< �� � � � � � � � � � � � � � � � � � � � � � � � � � �

�+8>= ";8->,= �8<=270 /8; �2= �=.6< �� � � � � � � � � � � � � � � � � � � � � � � � � � � �(8;4 @2=1 ";8,.<< �7-><=;B �8<=270 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

(8;4270 @2=1 ";8,.<< �7-><=;B �8<=270 ���� � � � � � � � � � � � � � � � � � � � � � � �#.?2.@270 ";8->,= �8<=270 /8; ";8,.<<.< ���� � � � � � � � � � � � � � � � � � � � � � �#.?2.@270 ";8->,= �8<=270 /8; �7=.;6.-2*=.< ��� � � � � � � � � � � � � � � � � � �#.?2.@270 ";8->,= �8<=270 /8; �70;.-2.7=< ���� � � � � � � � � � � � � � � � � � � � �#.?2.@270 ";8->,= �8<=270 /8; �8D��BD";8->,=< ���� � � � � � � � � � � � � � � � �

�A*695.� �.*=>;. �8<= ".;,.7= *7- �8D��BD";8->,= �8<=270 ���� � �#.?2.@270 * �8<=.- ";8,.<< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

";8,.<<270 !9=287< /8; �8<=.- ";8,.<< �� � � � � � � � � � � � � � � � � � � � � �$.==270 &9 =1. �8D��BD";8->,=< "5*77270 %*+5. �� � � � � � � � � � � � � � � � � �#.?2.@270 ";8->,= �8<=270 /8; ".;,.7= �255< 8/ �*=.;2*5 ���� � � � � � � � � �

&7-.;<=*7- �87/20>;.- �=.6< ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�+8>= �8<=270 /8; �87/20>;.- �=.6< ����� � � � � � � � � � � � � � � � � � � � � � � � � � ��A*695.� �8<=270 * �87/20>;.- �=.6 ��� � � � � � � � � � � � � � � � � � � � � � � �";8,.<< (8;4 !;-.;< ";80;*6 ����� � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�A*695.� ";8,.<< (8;4 !;-.;< �*=* $.:>.7,. $.=>9 ����� � � � � �

Manufacturing Accounting

�+8>= �*7>/*,=>;270 �,,8>7=270 ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � �%1. �,,8>7=270 �:>*=287 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �%D�,,8>7=< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��.7.;*5 �.-0.; %;*7<*,=287< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��><27.<< &72=< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �!+3.,= *7- $>+<2-2*;B �,,8>7=< ���� � � � � � � � � � � � � � � � � � � � � � � � � � �

!+3.,= D C�*38; �,,8>7=� ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � �$>+<2-2*;B D C�278; �,,8>7=� ���� � � � � � � � � � � � � � � � � � � � � � � � � �

�,,8>7= >6+.;< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��.?.5 8/ �.=*25 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �$>+5.-0.; %B9.< ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�8;. $>+5.-0.; %B9.< ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �!=1.; $>+5.-0.; %B9.< ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

"8<=270 �-2= �8-.< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��A*695.� �1*;= 8/ �,,8>7=< �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

$.= &9 �*7>/*,=>;270 �,,8>7=270 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

$.==270 &9 �*7>/*,=>;270 �,,8>7=270 ���� � � � � � � � � � � � � � � � � � � � � � � � � �$.==270 &9 �.7.;*5 �.-0.; ����� �5*<< �8-.< ���� � � � � � � � � � � � � � � � � � �#.?2.@270 �*7>/*,=>;270 ���< ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

";8,.<<270 !9=287< /8; �*7>/*,=>;270 ���< �� � � � � � � � � � � � � � � � � �&7-.;<=*7- (8;4 !;-.;< 27 �,,8>7=270 ���� � � � � � � � � � � � � � � � � � � � � � � � � � �

�+8>= (8;4 !;-.;< 27 �,,8>7=270 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � �(1*= �< * (8;4 !;-.;� ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �(1*= �*99.7< (1.7 )8> �;.*=. * (8;4 !;-.;� ���� � � � � � � � � � � � � � � ��+8>= =1. "*;=< �2<= *7- #8>=270 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�A*695.� �7027..;270 '*;2*7,. �7:>2;B ���� � � � � � � � � � � � � � � � � � � � �(1*= �*99.7< (1.7 )8> #.?2<. * (8;4 !;-.;� ���� � � � � � � � � � � � � � � �(1*= �;. &7*,,8>7=.- &72=<� ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �(1*= �*99.7< (1.7 )8> �<<>. �*=.;2*5� ���� � � � � � � � � � � � � � � � � � � � � �

Product Costing and Manufacturing Accounting

A8.1 (8/97)

#,%6 �%33)15 #,)1 $27 �)'24( �2745 %1( �7%16-6-)5 !5)(� ��� � � �#,%6 �%33)15 #,)1 $27 �)'24( �20321)16 �'4%3� ��� � � � � � � � � � � �#,%6 �%33)15 #,)1 $27 �)'24( �203/)6-215� ��� � � � � � � � � � � � � � � � �

#24. 9-6, #24. �4()45 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

#24.-1+ 9-6, #24. �4()45 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��4)%6-1+ % #24. �4()4 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��66%',-1+ % �%465 �-56 %1( �276-1+ �15647'6-215 ��� � � � � � � � � � � � � � � � � �

�42')55-1+ �36-215 *24 �42')55 #24. �4()45 ��� � � � � � � � � � � � � � � ��557-1+ �%465 62 #24. �4()45 �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��)'24(-1+ �2745 %1( �7%16-6-)5 !5)( ��� � � � � � � � � � � � � � � � � � � � � � � � ��)'24(-1+ �20321)16 �'4%3 ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�42')55-1+ �36-215 *24 �20321)16 �'4%3 ��� � � � � � � � � � � � � � � � � � ��)'24(-1+ �203/)6-215 62 #24. �4()45 ��� � � � � � � � � � � � � � � � � � � � � � � �

�4)%6) �2741%/ �164-)5 �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�4)%6-1+ �2741%/ �164-)5 �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��2741%/ �164-)5 %1( 6,) ,4))= -)4 �42')55 �� � � � � � � � � � � � � � � � � ��)6%-/ %1( �700%4; �2741%/ �164-)5 ��� � � � � � � � � � � � � � � � � � � � � � � �

�4)%6-1+ �2741%/ �164-)5 *24 #24. -1 �42')55 24 �203/)6-215 � � � � � � ��21*-+74)( �6)05 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��42')55-1+ �36-215 *24 �2741%/ �164-)5 *24 #24. -1 �42')55 24�203/)6-215 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�)8-)9-1+ "%4-%1')5 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��4)%6-1+ �2741%/ �164-)5 *24 "%4-%1')5 ���� � � � � � � � � � � � � � � � � � � � � � � � � �

�42')55-1+ �36-215 *24 �2741%/ �164-)5 *24 "%4-%1')5 ���� � � � � � � � � ��4)%6-1+ �2741%/ �164-)5 *24 �7/. �%17*%'674-1+ �%-15 %1( �255)5 ����

�42')55-1+ �36-215 *24 �7/. �%17*%'674-1+ �%-15��255)5 ���� � � � ��)8-)9-1+ �700%4-<)( #24. �4()45 ���� � � � � � � � � � � � � � � � � � � � � � � � � �

�)8-)9 �)1)4%/ �)(+)4 �%6',)5 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�)8-)9-1+ �)1)4%/ �)(+)4 �%6',)5 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � ��256 62 6,) �)1)4%/ �)(+)4 � �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�256-1+ 62 6,) �)1)4%/ �)(+)4 � �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��256-1+ �%17*%'674-1+ �2741%/ �164-)5 � �� � � � � � � � � � � � � � � � � � � � � � � � �

�4)=�256 �42')55 � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��256 �42')55 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��42')55-1+ �36-215 *24 �256 �)1)4%/ �)(+)4 ���� � � � � � � � � � � � � � � � �

�)8-)9-1+ 6,) �256-1+ �(-6 �)3246 *24 �%17*%'674-1+ ���� � � � � � � � � � � ��20021 �256-1+ �44245 ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�)8-)9-1+ 6,) �256-1+ �2741%/ �)3246 ��� � � � � � � � � � � � � � � � � � � � � � � � � ��)8-)9-1+ 6,) �6)0 �)(+)4��''2716 �16)+4-6; �)3246 ��� � � � � � � � � � � � �

�42')55-1+ �36-215 *24 �6)0 �)(+)4��''2716 �16)+4-6; ���� � � � � � � ��)8-)9-1+ #24/( #4-6)4 �)32465 *24 �%17*%'674-1+ �''2716-1+ ���� � � �

Manufacturing Accounting in ERPx Environments

�&276 �%17*%'674-1+ �''2716-1+ -1 ���: �18-4210)165 ��� � � � � � � � �!1()456%1( �42')55 �1(7564; �''2716-1+ ��� � � � � � � � � � � � � � � � � � � � � � � � � �

�&276 �42')55 �1(7564; �''2716-1+ ��� � � � � � � � � � � � � � � � � � � � � � � � � � ��&276 !1%''2716)( !1-65 -1 �42')55 �1(7564; �''2716-1+ ��� � � � ��&276 �%/'7/%6)( �027165 -1 �42')55 �1(7564; �''2716-1+ �� � � �

Table of Contents

A8.1 (8/97)

Appendices

((�&�#. 0 ��$�,$�+#'&* #& �'*+ �'$$,( ��� � � � � � � � � � � � � � � � � � � � � � � �

��+�)#�$ �'*+ �'%('&�&+* ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��,)�"�*�� ��+�)#�$ �'*+� ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���+�)#�$ ��)�(� ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

�',+#&! �'*+ �'%('&�&+* �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��� ��#)��+ ���')� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �� ���+,( ���')� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �� ����"#&� �,&� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��� ����') � #�#�&�/� �� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ���� � ���)#��$���#.�� ���"#&� �-�)"���� �� � � � � � � � � � � � � � � � � ��� �� ���)#��$���#.�� ���') �-�)"���� �� � � � � � � � � � � � � � � � � � � �

�,+*#�� �(�)�+#'& �'*+ �'%('&�&+* ��*,�$$/ �.� ��� � � � � � � � � � � � � � ((�&�#. � 0 ��$�,$�+#'&* ') ��)#�&��* ���� � � � � � � � � � � � � � � � � � � � � � � � �

�+�&��)� �'*+* ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��,))�&+ �'*+* ���� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��$�&&�� �'*+* ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �+,�$ �'*+* ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ��'%($�+�����)�((�� �'*+* ��� � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �

((�&�#. � 0 �,)�"�*� �)#�� ��)#�&�� ���� � � � � � � � � � � � � � � � � � � � � � � � � � �

�.�%($�� �,)�"�*� �)#�� ��)#�&�� �&� ��+�)#�$ �,)��& ���� � � � � � � � � �

Glossary

Index

Exercises

Product Costing and Manufacturing Accounting

A8.1 (8/97)

Overview

Product Costing and Manufacturing Accounting

–10 A8.1 (8/97)

A8.1 (8/97) 1–1

Overview

�� &�� � � ���'$�&� � � �!�"��&� $��!$�% ! &�� (��'� !� � (� &!$+ �% ! � !�&�� ���!$ �! ��$ % !� �!%& �'%� �%%�% &!��+� ���"� � &!! �'�� !� � ' "$!��&���� %&!��� !$ '%� � � �""$!"$��&� ��&�!�% !� �!%&� � ��$&�� � (� &!$+�&��%� �� #'����+ ��"��&� +!'$ "$!��&%�

��� �$!�'�& !%&� � %+%&�� ���!)% +!' &! %&!$� � � $�&$��(� �!%& � �!$��&�! � �&��%! ���"% +!' &! �� ��� +!'$ �!%&% �+ "$!(��� � � �!$��&�! �� � "'&% &! +!'$�!�"� +�% �'%� �%% "�� � ��&� ���'$�&� "$!�'�& �!%&� �� +!' �� �(��'�&� &���!��!)� � �� '���&'$� � "$!��%%�% &! ��&�$�� � &�� ��"��& &! +!'$ �!�"� +�%�!&&!� �� ��

� � '���&'$� � �'���&% ���$��& ���!$� � ��$��& ���!$� � � !(�$�����

� �$!�'�& ��%�� ���%�� � � �� '���&'$� � � �� ��$� ��

� ���!' &� � ��$!%% ��$�� �+ "$!�'�& �� � !$ �&���

��&�$ +!' �%&����%� �!%&% � &�� �$!�'�& !%&� � %+%&��� &�� � '���&'$� ����!' &� � %+%&�� &$���% &�� �!%&%� $�"!$&% ! (�$�� ��%� � � "!%&%�� '���&'$� � &$� %��&�! % &! &�� �� �$�� �����$�

����%� !&� &��& &�� &�$� )!$� !$��$ �% '%�� &�$!'��!'& &��% �'���� � �� �$����!)�(�$� &$� %��&�! % &��& �����& )!$� !$��$% ��%! �����& $�&� %����'��%�

System Integration

�$!�'�& !%&� � � � � '���&'$� � ���!' &� � �$� &)! !� &�� %+%&��% &��& �$�� ��'��� � &�� &�$"$�%� ��#'�$��� &% ��� � � � � *��'&�! ���*� %+%&���

��* �% � ��!%��-�!!" �� '���&'$� � %+%&�� &��& �!$����,�% �!�"� + � �!"�$�&�! % "�� � �� � � &�� ��"���� &�&�! !� &�!%� "�� %� �%� &�� ��*%+%&�� &! �!!$�� �&� +!'$ � (� &!$+ � � ���!$ $�%!'$��% &! ����(�$ "$!�'�&%���!$�� � &! � �� ���� %����'���

Product Costing and Manufacturing Accounting

1–2 A8.1 (8/97)

� ��������� ������ � ��� � ������ � �� ��� �� ���� �� � ������� � �� � � �� ��������

Product Data Management(Systems 30 and 48)

Product Costing (System 30)

Configuration Management(System 32)

Inventory Management(System 41)

Sales Order Management(Systems 40 and 42)

Forecasting(System 36)

Distribution RequirementsPlanning (System 34)

Master ProductionSchedule

(System 34)

Material RequirementsPlanning

(System 34)

Purchase Management(Systems 40 and 43)

Manufacturing Accounting(System 31)

Resource Requirements Planning(System 33)

Rough Cut CapacityPlanning

(System 33)

Capacity Requirements Planning(System 33)

Finite SchedulerExecution

OperationalPlan

TacticalPlan

StrategicBusiness

Plan

Shop Floor Control(System 31)

ERPx�

Enterprise Requirements Planning and Execution

A8.1 (8/97) 1–3

Features

��� �#!�&�% !$%� � � � �� &���%&#� � ���!& %� � $*$%��$ "#!'��� ���)�����%* %!���!��!��%� *!&# �� &���%&#� � � '�#! �� %� �!�� !� %�� �� ���%$ � �

���%&#�$ !� %��$� $*$%��$ �#��

��� ������� ����

���"���

��� � � � ��� %�� � & ����%�� &���# !� �!$%

�!�"! � %$ �!# %#���� � $"������ �!$%$� $&�� �$ �#����%�

%�)�$� �&%*� � � ����%#���%*�

��� ������� ���� ������

�������

��� � � & ����%�� &���# !� �!$% ��%�!�$ %! &$� �

�!$% $��&��%�! � ��*$�$�

��� ������� ���� �������

��� �����

���!��%� �!$% ���%!#$ � � #�%�$ %! � $"������ �%��� �$�� (�%�

�!$% ���,! $ %! ����&��%� ����%�! �� �!$%$�

���� ��������� �#� % � �!�"��%� $�% !� #�"!#%$ %! �!�"�#� !�� �!$%$ (�%�

�( �!$%$ ���!#� ��"���� %� � � * ��� ��$�

���� �� �������� ������ ���&��%� %�� %!%�� ��%�#��� �!$% �* #�%#��'� � %�� ���� !�

��%�#��� �!# ��� �%��$ � � ���� � %�� %!%�� �!$% !� %��

�!�"! � %$�

���� ���������� �& � �!�"��%� $��&��%�! !� �!$%$ ���!#� � * ��'� ��%� �$

&"��%�� �$ %�� �#!+� $%� ��#��

����"�������! ������� ��� %�� �!$% � �!#��%�! �% %�� �#� ���"�� % ��'�� %!

���!( �!# �!$% '�#�� ��$ �% �����#� % �!��%�! $ �!# ��� %����

�� &���%&#�� �%��$�

��������� ��'��( �!&# �� �$ !� '�#�� ��$�

� � �� ��#� �� ��� ��

� ��%&�� ���%�#��� � � ���!#�� %��#

������� ������� ���

���������

#��%� ��%����� !# $&���#* �!&# �� � %#��$ �!# (!#� !#��#

'�#�� ��$�

������� ������� ��� ���

����� ������������

#��%� ��%����� !# $&���#* �!&# �� � %#��$ �!# (!#� �

"#!��$$ !# �!�"��%�! $�

��������� ����������

����������� ����� �� ���

��#�� �!���# ��!& %$ %! $"������� ���!& %$�

Product Costing and Manufacturing Accounting

1–4 A8.1 (8/97)

������� �/',1 /#.-/10 *'01',% "#1�'*#" !-010 �," 3�/'�,!#0 $-/ 4-/)

-/"#/0�

Product Costing and Manufacturing Accounting Integration

�/-"2!1 !-01',% .*�50 � 0'%,'$'!�,1 /-*# ', 1&# +�,2$�!12/',% #,3'/-,+#,1� �#$-/#5-2 !�, '+.*#+#,1 5-2/ ��,2$�!12/',% �!!-2,1',% 0501#+� 5-2 +201 0#1 2.$/-6#, 01�,"�/" !-01 !-+.-,#,1 3�*2#0 $-/ 1&# ./-"2!10 5-2 ./-"2!#� �-!�*!2*�1# 1�# !-01 !-+.-,#,1 3�*2#0� 5-2 +201 !-,0'"#/ 1&# $-**-4',% �0.#!10', 1&# +�,2$�!12/',% #,3'/-,+#,1�

� �-01 /#.-/1',% �4&�1 "-#0 1&# '1#+ /#�**5 !-01 1- ./-"2!#��

� ��/'�,!# /#.-/1',% �1&# �!12�* 3#/020 01�,"�/" !-010�

� �/-"2!1 �," (- !-01',% �"#1�'*#" ',$-/+�1'-,�

� ��1#/'�*0

� �� -/

� �3#/&#�"

�$1#/ 5-2 !�*!2*�1# 5-2/ !-01 !-+.-,#,1 3�*2#0 ', � 0'+2*�1#" +-"# �," �/#0�1'0$'#" 4'1& 1&# /#02*10� 5-2 +201 #01� *'0& $/-6#, 01�,"�/" !-01 !-+.-,#,10��** 0&-. $*--/ 1/�,0�!1'-,0 20# 1�# $/-6#, 01�,"�/"0 $-/ !�*!2*�1'-,0� 4&'!&� ',12/,� !/#�1# 1/�,0�!1'-,0 ', 5-2/ %#,#/�* *#"%#/ �," �/# 1&# �0'0 -$ 5-2/',3#,1-/5 3�*2�1'-,�

�#/1�', $2,!1'-,0 4'1&', 1&# �/-"2!1 �-01',% �," ��,2$�!12/',% �!!-2,1',%0501#+0 -3#/*�. 4'1& -1&#/ ��,2$�!12/',% �," �'01/' 21'-, 0501#+0� 02!& �0�/-"2!1 ��1� ��,�%#+#,1 �," �&-. �*--/ �-,1/-*� �&#/#$-/#� '1 '0 '+.-/1�,1 1&�15-2 &�3# � �0'! 2,"#/01�,"',% -$ 1&# $-**-4',% 1� *#0 �," &-4 1 ',1#/�!14'1& -1&#/ 0501#+0�

� �1#+ ��01#/ �������

� ��,2$�!12/',% ��1� ����� �

� �/�,!&��*�,1 ��01#/ ������

� �'** -$ ��1#/'�* ��01#/ �����

� �-21',% ��01#/ �����

� �-/) �#,1#/ ��01#/ �������

A8.1 (8/97) 1–5

��� �������� ������������ ������������ ��� ���������� � ����� ������ ��������� ������� ��� ���� ������� �������� ��������

Item Master(F4101)

Branch/PlantMaster(F4102)

Bill of MaterialMaster (F3002)

Routing Master(F3003)

Cost Rollupsand Freeze

Process WorkOrders

Parts List(F3111)

RoutingInstructions(F3112)

Work OrderMaster(F4801)

Cost Components(F30026)

ManufacturingAccounting

AAI Values(F4095)

AccountLedger(F0911)

General LedgerPosting

AccountBalances(F0902)

�Work Order Variances�Order Activity

Product Costing and Manufacturing Accounting

1–6 A8.1 (8/97)

Achieving Effective Cost Management

#$ � $�� ��� " �"��# " ��!�"$���$# '�$��� ) %" ���%���$%"��� � �!��)� �$"��%$� ��� "��$� � $ ) %" !" �%�$ � #$��� ��$�&�$��# ���� $��"�� "�� �����$ $�� &�"��� ���%"��) � ) %" ���%���$%"��� �%���$�

��� � �� '��� $���� ��#$# �(��!��# � ��!�"$���$# '�$��� ) %" � �!��) ��� $���#!��$# � $�� �" �%�$ � #$��� #)#$�� '���� �"� �����$�� �) $��$ ��!�"$���$�

����� ��������� ��� �#��� ������"��� �" %! �# "�#! �#���� � " ��#%"���

$��$�

� ��� ���� � ��$�"��� �# � �!��$�� ��� ����*�%) ��� "��$� � �# ���%"�$�

� ��� �������"��� ������ "��"# ���#� ��&� ����$���� ��$ ��� %�$

���� ��� #���# � "�� � �$"��%$�# ��! "$��$ ��� "��$� �

"���"���� $�"��$ ��"��$#� �# '��� �# $�� ��$�#$ $"���# ��

���%���$%"���� � " �����$�&� � #$ ���������$� �$ �#

��! "$��$ $��$ ) %" #���# � "�� !" &��� $����) ���

"��# ����� � "���#$#�

������������

���������

��� ��%���$%"��� ������"��� �" %! �# "�#! �#���� � "

����$��)����

� � ""��$ !" ��##�#� ������# $ �(�#$��� !" ��##�#

� ��%���$%"��� &�"����� ���%"�$� ��� "��$� � �� %$ ' "� ���$�"#

��� ����� � %" �%"���#��� ��!�"$���$ �%#$ !" &����

� ���%"�$� #%!!���" � #$#� ���%"�$� $"��#! "$�$� � � #$#

������������ ��%���$%"��� !�"�$� �# !" &��� &�$�� ��� "��$� � $ $��

!" �%�$ � #$��� ��� "$� � " �(��!��� $��) �%#$�

� ��!%$ $���" ��$� �� � $����) ��� ���%"�$� �����"� ����$��) ��) ��#�"�!�����# �� $�� ����# � ��$�"��� ���

" %$���#

�������� � %" ��� %�$��� #$��� �%#$�

� �#%"� $��$ ��� �$��# ��&� � #$#� ����$��) ����"�� ��� ������#$"�$�&� &�"����� �" �%�� $����) &�"����� "�! "$# �#$����"� � #$# &�"#%#

�%""��$ � #$#�

A8.1 (8/97) 1–7

��$� �� �"�� �!!#�! !��#�� �� ���!��� �� �! '�# ������ ��� ������ '�# ���#���"# ��� ��!"!� ����#�����

� ���� ���� ��% ��"��� �� '�# ������ !"���� � ��!"!�

� �% �� '�# ����" ����!!�

� ���� � � ��% �"��! �����"�� �� "�� !"���� ��

� �% �� '�# ����#�" �� ���� �"�! ��� %� � ���"� �$� �����

��# ����" ��!� ����#�"� "��!� "'����� �� �#�!"����! �! '�# ������ ��!"! ����� �� � ���#�!�

� ��" ��� !"���� �! � � �$������� ���� � '�# ���"��� ��!" ���#��

� ��# ��$� #!�� ���� ��" #��"! �� ���!# ��

� ��# ������' �����# �"��' ��� "! ���� ��# ! ��� ��!"!�

� ��% � ��#�"! � � ��" #���"�� �� � "����' ����� �

� �"���� �! � � #���"�� "�� � ��#��"�'�

� "��! ��$� ���� ����� "� � ����"�� � �� "�� ���� �� ��"� ��� !���� "�� ��!"��!" #���"��

� �"��! �� "�� �#"��� ��!"� ��$� ���� ������� !���� "�� ��!" ��!" #���"��

Tables

�� ������� �

�������

���"���! ��� ��!" ��"���! ��� ��!" ������"! �� ���� ��"���

�� ��� �"��!�

�� ������

������

���"���! "�� ��!"! �� ��� �"��! �! �� "�� ��!" � �(�� #���"��

���!��� !����

��� �� �

�������

�"� �! $� �����! "��" ������"� %��"�� "� ����#�� ���������' ��

"�� ��!" ���#� ��� %���� �$� ���� $��#�! "� #!��

���!��� !���� �� �

��������

�"� �! "�� ����#�"��� ��!" �#��"�"'� %���� "�� !'!"�� #!�! "�

��"� ���� "�� ������"��� �� ��&�� !�"#� ��!"! �� �� �"���

��! ��� ��� ��

�������

�"� �! �#"��� ���� ��"���� ����#���� ��� �"��� !��#�����

%� � ���"� � #� "���� !�"#� "���� ��� ������� "���� ��

!'!"�� #!�! "��! ���� ��"��� "� ����#��"� ���� � �������� ���

�$� ���� ��!"!�

Product Costing and Manufacturing Accounting

1–8 A8.1 (8/97)

�!## &� ��)�'!�#

��()�'

�������

�������� ����������� �� ��� ������ ��� ��!�� � � � ���� ��

��������� � �� �� � �������� �� ����������� �� �#���� ���

���� ����������� �� ���� ���� �������� ������

�&'" ��%)�' ��)�(

��������

�������� ��� ����� ��� ���� "��� ������� � �� �� �!������ ���

�� ���

�&'" ��%)�' ��()�'

�������

�������� �������� ���� � � � ��� ������� "��� ��������

���� ���� ���������#�

�)�$ �����'

�������

�������� ������������ ���� �������� ������� �� ��!�����# !�� ��

��&*%) ��()�'

�������

�������� ���� �� ������������ ���� ���� � � ��� ���

�������������

��&*%) �����'

�������

�������� �������� ������������ �� ��� ������� �������

��&*%) ��#�%��(

�������

�������� ��� �������� ��� ���� ������ ��� ����� #��� �������

���� ��� � � ����!��� ���� �� ��� ������ ��� ���� ��� ������

�#��� � ������� ������ #���� ��� ����������� � �����# �� ���

�(�' ���!%�� �&��(

������

�������� ��� ������� ����� ��� ����� ������������� ����

������� ����� �� ���� �� ������� ��� ��� ���� ����

���� ����� ���� ���

� ���� �������� ���� ����������

� ���� ������ ��������� ������ ������� ���� ������ ������� ������ �����

��)� �&%)'&#

�������

�������� �#����$��������� ���� ������ ������������

���� ���� ��� ���� � � ��� ���� ���� �� ��� ���� ����# �����

*)&$�)!�

��&*%)!%�

�%()'*�)!&% � ��

��#*�(

������

�������� ���� �� � � ��� ���� ��� ��� �� ������ �� ����

������� ��� ������ ������� �� ����� ���� ����

�&'" �'��' ��()�'

�������

�������� ��� "��� ����� ������ ������������ �� ���� ���� ����

�� �� ������� �� ���� ����� �����"���� �� �#���� ������

���� �� �� "��� ���������� ������������ ��� � ������� � "���

������

A8.1 (8/97) 1–9

��#%$ ��$%

� �����

��� ���� �� ��� � ��� �� �� � ����� � � #��� ������ �

��� ���� ��� ������ ��� ���� ��� � ��� �$� �� ���� �� ���

���� �� ���� �"��$ �� #��� $�! �!� �� ������ ��� �����

��������

�"&%�!� �!$%#&�%�"!$

� �����

��� ���� �� ��! ��� � ��� �� ��� � ����� � � #��� ������ �

��� ���� ��� ������ ��� ���� ����� ��� ���!���� �!���� ���

#��� ��� ��� ��� �$� �� ���� �� ��� ���� �� ���� �"��$ ��

#��� $�! �!� �� ������ ��� ����� ��������

�"#� �#��#

��#��!��$

� �����

��� ���� �� ���!� � !��� ��� #��� ����� "�������

����!�� ����� ��� �$� �� !��� �� ��� ���� �$ �� ������

��� ����� ������� ��� �$ �� ��!���� �� ���� ��� ��� ��

������ �� ������ ���� ��������

�%� ��$%�#

� ����

� ���� ����� ������� ��� ���! ���� ������� ��"�� ��$ � ���

�!�� �� � �� �!������ ������� ����� �� ����$ ������ ��� !�� �

�� ����!���

�#�!������!% ��$%�#

� ����

������� ��� ���� ���� #�����!�� �� ���� ��"�� ������� ����

�!�� �� ������ ��"�� �� ����$ ������

���#�$$ �""�

� �����

��� ���� � "���� $ �� ������� ���� ����!���� ������� ��� ���!

�!� ������ �!�������� �����$���� ��� ������� ��

�&$�!�$$ �!�% ��$%�#

� ����

���� ����� ������� ��� ���! �!������ !�� �� �!�� �� ������$

����� ��� �� ����$ ����� �������� � �� �!������ !�� �

Product Costing and Manufacturing Accounting

1–10 A8.1 (8/97)

Menu Overview

�� ��&�!�" "'"#��" �!� ���$ �!�%��� ���$" �!� �!����(�� ����!���� #��$��#��� ��� �!� $���' �� $"��

Product Costing

����"" �!��$�# �"#��� �$��#���" �!�� #�� �!��$�# �#� ���������# ���$"�

� Daily Product Costing G3014

Daily Processes

� Periodic Product Costing G3023

Periodic Processes

� Product Costing Setup G3042

Setup Processes

Manufacturing Systems G3Product Data Management G30

Fast Path Commands

��� �����&��� #���� ���$"#!�#�" #�� ��"# ��#� �������" '�$ ��� $"� #� ��%������ #�� �!��$�# �"#��� ���$"�

���� �� �����

� ����� ���' �!��$�# �"#���

�� ����� ��!����� �!��$�# �"#���

�� ����� �!��$�# �"#��� ��#$�

A8.1 (8/97) 1–11

Manufacturing Accounting

���� ��"���!"���� ����"�!��� �"��!��� ���� !�� ���� ����� ��!��� ���" �

� Daily Manufacturing Accounting G3116

Daily Processes

� Periodic Manufacturing Accounting G3123

Periodic Processes

� Shop Floor Control Setup G3141

Setup Processes

Manufacturing Systems G3Shop Floor Control G31

Fast Path Commands

��� �����$��� !���� ���" !��!� !�� �� ! ��!� ������� %�" ��� " � !� ��#������ !�� ��"���!"���� ����"�!��� ���" �

���� �� �����

� ����� ���% ��"���!"���� ����"�!���

� � ����� �������� ��"���!"����

����"�!���

��� ����� ���� ����� ��!��� ��!"�

Product Costing and Manufacturing Accounting

1–12 A8.1 (8/97)

Product Costing

Product Costing and Manufacturing Accounting

1–14 A8.1 (8/97)

A8.1 (8/97) 2–1

Product Costing

Objectives

� �! ' ��$%&� � "$!�'�& �!%&� � � � �&% !(�$��� ��"!$&� �� � ��� '���&'$� � � (�$! �� &

� �! ���$ ��!'& %&� ��$� � � '%�$ ���� �� �!%& ��&�!�%

� �! ���$ ��!'& &�� �����$� ��% ��&)�� �$!,� � � %��'��&�� �!%&%

About Product Costing

�!$�� � )�&� &�� $!�'�& !%&� � %+%&�� �! %�%&% !� &�� �!��!)� � &�%�%�

� ��(��)� � ����% !� ��&�$��� � � $!'&� �%

� ��&&� � '" "$!�'�& �!%&� �

� $��&� � %��'��&�� �!%&%

� �!$�� � )�&� %��'��&�� �!%& �!�"! � &%

� �"��&� � �$!,� �!%&%

� ��(��)� � �!%&� � � �!$��&�!

� �!$�� � )�&� ����&�! �� �!%&� � ���&'$�%

What Are Standard Costs?

�!' �� )!$� )�&� � (�$��&+ !� �!%& ��&�!�% � &�� $!�'�& !%&� � %+%&����!)�(�$� &�� �� '���&'$� � ��!' &� � %+%&�� '%�% &�� %&� ��$� �!%& ��&�!������ ���% ��&�!� $�"$�%� &% &�� �*"��&�� �&�$��&� �!%& !� � �&�� �!$ � %"������"�$�!� !� &���� %'�� �% #'�$&�$�+� %���-� '���+� !$ � '���+�

��&� %&� ��$� �!%&� �� +!' �%&���&� �!%&% �!$ ���� � � �&�� �%%����+ � ��� '���&'$�� "�$& ! � ��(��-�+-��(�� ��%�% ���!$� "$!�'�&�! ���� %� ���%� �!%&�%&���&�% �$� ��%�� ! �!&� "�%& "�$�!$�� �� � � � ��+%�% !� �'&'$� �! ��&�! %�

Product Costing and Manufacturing Accounting

2–2 A8.1 (8/97)

������ � ����

�� ���� ���� ���� ����

�'�%-��+�

� ���(*� �.�*"���� �-,+#�� �)�*�,#('+� �0,*� �(+,+� ��,�*#�%+ � (* )-*�"�+�� )�*,+

('%1�

�'�%-��+�

� �"#+ #,�&�+ '�, ����� �(+,� �(,�% �(+, ( %(/�*4%�.�% �(&)('�',+

�"� '�, ����� �(+, *�)*�+�',+ ,"� �(+, ,( &�'- ��,-*� �' #,�& �, ,"#+ %�.�% #' ,"��#%% ( &�,�*#�%� �(* &�'- ��,-*�� )�*,+� ,"� �(+, #'�%-��+ %��(*� (-,+#��()�*�,#('+� �'� �(+, �0,*�+� �-, '(, &�,�*#�%+ �%(/�*4%�.�% #,�&+�� �(* )-*�"�+��)�*,+� ,"� '�, ����� �(+, #'�%-��+ ,"� �(+, ( &�,�*#�%+� �"� ,(,�% �(+, ( �' #,�&*�)*�+�',+ ,"� +-& ( ,"� '�, ����� �(+, �'� �%% %(/�*4%�.�% �(&)('�', #,�&�(+,+�

Why Maintain Standard Costs?

�1 �� #'#'! �'� &('#,(*#'! )*(�-�, �(+,+� 1(- ��' &��+-*� 1(-* �(&)�'1�+�-**�', &�'- ��,-*#'! )�* (*&�'�� �!�#'+, 1(-* +,�'��*� �,�*!�,� �(+,+� �*(�-�,�(+,#'! )*(.#��+ #' (*&�,#(' ��(-, ,"� �(%%�* #'.�+,&�',+ ,#�� ,( 1(-* &�,�*#�%+�/(*$ #' )*(��++� �'� )"1+#��% #'.�',(*1� �(- ��' -+� ,"#+ #' (*&�,#(' ,(��,�*&#'� )*#�#'! (' �'� #,�&+ �'� +�*.#�� �(&)('�',+�

Simulated versus Frozen Costs

�#&-%�,�� �(+,+ *�)*�+�', � 3/"�, # � �'�%1+#+ (* � !#.�' �(+, &�,"(�� �(- &#!",/�', ,( ��%�-%�,� +#&-%�,�� �(+,+ ����-+� ( �"�'!#'! ��,(*+ #' ,"� �-+#'�++�'.#*('&�',� +-�" �+ %��(* *�,�+ (* ,"� �(+, ( *�/ &�,�*#�%+� �(- ��' +#&-%�,��(+, �"�'!� +��'�*#(+ �*(%%-)+� �+ &�'1 ,#&�+ �+ '����� �� (*� 1(- #'�%#2� ,"��"�'!�+�

�(- #'�%#2� ,"� �"�'!�+ �1 )�* (*&#'! � *(2�' -)��,� (* ,"� !#.�' �(+,&�,"(�� *(2�' -)��,� �()#�+ 1(-* +#&-%�,�� .�%-�+ �'� &�$�+ ,"�& 1(-* *(2�' �(+,+� �'� -)��,�+ ,"� �(+, ���!�* ,��%� ����� /#," ,"� ,(,�% �(+,� �"�+��(+,+ *�&�#' #' � ��, -',#% 1(- -)��,� ,"�& /#," �'(,"�* *(2�' -)��,��

�(- ��' +#&-%�,� �(+,+ -+#'! ,"� +,�'��*� �(+, &�,"(� (* �'1 (,"�* �(+,&�,"(�� �(/�.�*� ,"� ��'- ��,-*#'! ��(-',#'! +1+,�& -+�+ ('%1 ,"� +,�'��*��(+, &�,"(� ,( �+,��%#+" �(+,+ (* +"() %((* ,*�'+��,#('+�

A8.1 (8/97) 2–3

What Are Cost Components?

��� �������� � �������� �� ����"��!�� ��� � �� ���� !� �� � ��� ����$������ �� ������ ������ �"������� ��� �$ ���� � ������ ������ ��� �"��������� � ��� �! ��� �����% ����!�� �� �% �� �%� ��� �$ �� ��� �� �!�� �� ���� ���� %���� ���!���% ��� �������

�� ��� �������� � � ���� ��� ������ � � �� ��� ��� ������� ���� ��! ���!�� ��� � �� !� ���!�� �� ��� ��������� � ���� ���� ��� �! !�� ��� ����������� � ������% �� ���!�� �� �� ���&�� �� ����� ��� � �� �������� ��� � �����% � ���

� ���� ���� %�! ����

� ����# ��� �$ �� ���'�� ��� � ���� �� � �� ���!��� !���� �� � ����!� ��!�� �� ���� ���� %� ���!������ #� ��� �� #�����!�� ������

� ��"��# �������� ����!�� ���� !��� � �� ������ ��� ���!� � ��� ��% � ���

� ��� ��� ��� � �% ������ ��� �!� �'������ % ����������� !� �'������ %���������� ����#� ��� �������� ��� ��� "��!�� ����� �� �������� ���!������ "���� �����

� �� !� ��� ��� �� �� �� �������� ��� ������ ��

� ������ ���� ����� ��� ��� ��� � ����!�� �� ����!� ��� ��� ����!�� �����

See Also

� ������� � ��� ��������� ��������

� ��������� ������ �� ��� ������ ��� ��������� ��������

Product Costing and Manufacturing Accounting

2–4 A8.1 (8/97)

A8.1 (8/97) 2–5

Review Bills of Material and Routings

Reviewing Bills of Material and Routings for Product Costing

�� ��� �� �� ��� �� ������� ��� � �� � ������ �������� ���������� ����� ��� �������� �� ���� ��� ���� ���������� �� � � �� ���� �����

� � �� � ������� ������� �� ���� �� �� ���

� � �� � �������� ��� ������� �������

Reviewing Product Costing in Bills of Material

From Product Data Management (G30), choose Daily PDM Discrete

From Daily PDM Discrete (G3011), choose Enter/Change Bill

� �� � ���� ���� �� �� ��� �� ��� ����� �� ����� ����� �� ���� �� ���������� ������ ���� �� �� ���� ��� ��� �� � � ���� ��

See Also

� ������� ���� ����� �� ���� � ������� �� �� ������� � � � ������

�������� ��� ������� ����

Product Costing and Manufacturing Accounting

2–6 A8.1 (8/97)

�� ������ ���� �� � ����� ����� ��

�� �$�"������ ����

�� ��&��' $�� � �� '��� �����#�

� �! ���$ �$��

� �%��$�$) ��"

� ���$ �� ��#%"�

� ��(�� " ��"�����

�� ����## $�� ��$��� �"���

Review Bills of Material and Routings

A8.1 (8/97) 2–7

�� ��(��) &�� �!��!)� � �����%�

� ��&'$� �!%& ��$�� &

� ��$�� & !� ��$�"

� �"�$�&�! ��$�" ��$�� &

����� ���������

�!�"! � & �&�� � '���$ &��& &�� %*%&�� �%%�� % &! � �&��� �& �� �� �

%�!$&� �! �� !$ �$� �&�� '���$ �!$��&�

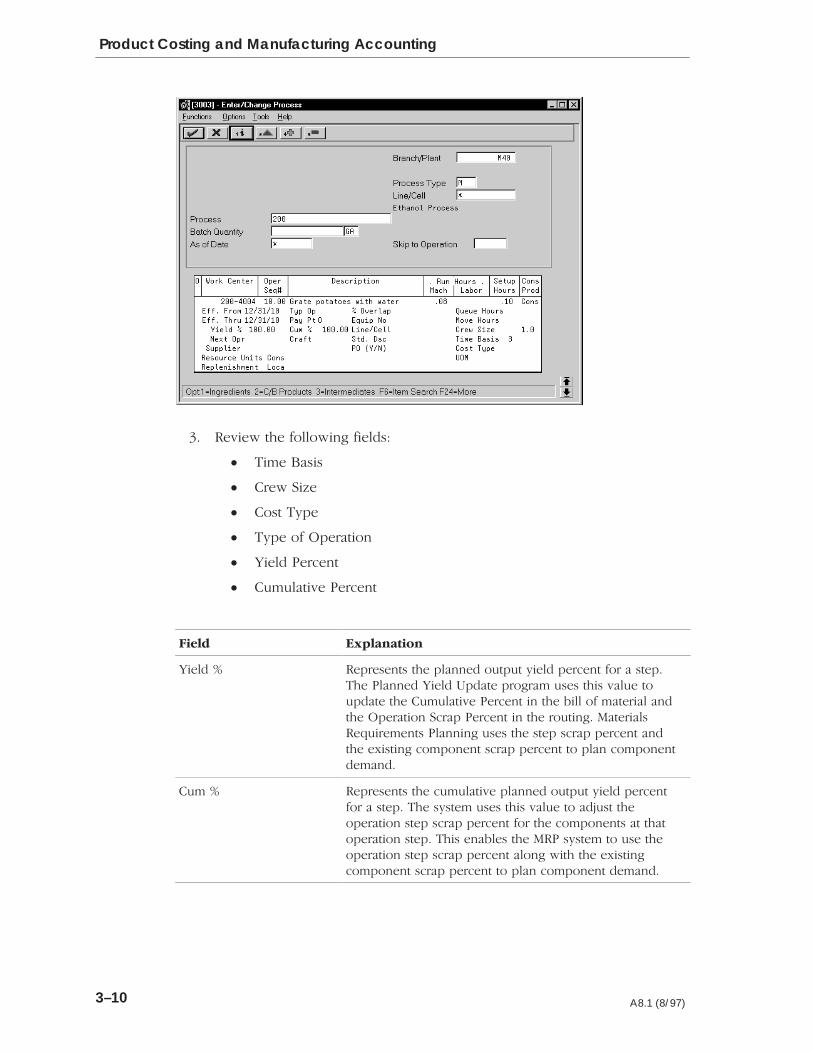

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�����$� ��� ��$� & ����� �! &�� % &�� �&�� '���$ !� &��

"�$� & �&���

�&���� ��� �!�"! � & �&�� ����� �! &�� % &�� �&��

'���$ !� &�� �!�"! � & �&���

�'� &�&* ��$ ��� '���$ !� ' �&% &! )���� &�� %*%&�� �""���% &��

&$� %��&�! �

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

� '���$ &��& � ����&�% �!) �� * �!�"! � &% *!' '%�

&! �� '���&'$� &�� "�$� & �&��� � #'� &�&* !� +�$! �% (�����

��� ����'�& (��'� �% ��

� ��� ����'�& (��'� �!��% �$!� &�� �!�"! � & � �

"$!�'�&�! ' �&% !� ���%'$� �$!� &�� �&�� �%&�$ &�����

Product Costing and Manufacturing Accounting

2–8 A8.1 (8/97)

����� ���������

� � �) %��/!. %" /$! ,0�)/%/4 +!- �..!(�'4 "*- �) %/!( *) /$!

�%'' *" (�/!-%�' 1�-%!. ���*- %)# /* /$! ,0�)/%/4 *" /$!

+�-!)/ %/!( +-* 0�! *- %. "%3! -!#�- '!.. *" /$! +�-!)/

,0�)/%/4� �$%. 1�'0! �'.* !/!-(%)!. %" /$! �*(+*)!)/

,0�)/%/4 %. � +!-�!)/ *" /$! +�-!)/ ,0�)/%/4� ��'% 1�'0!.

�-!�

� �%3! �0�)/%/4

� ��-%��'! �0�)/%/4 ��!"�0'/�

� �0�)/%/%!. �-! !3+-!..! �. � +!-�!)/�#! �)

(0./ /*/�' �

�*- "%3! ,0�)/%/4 �*(+*)!)/.� /$! �*-& �- !- �) ���

.4./!(. * )*/ !3/!) /$! �*(+*)!)/�. ,0�)/%/4 +!-

�..!(�'4 1�'0! �4 /$! *- !- ,0�)/%/4�

�*- �-*�!.. ��)0"��/0-%)#� /$! .4./!( ./*-!. +!-�!)/

�*(+*)!)/.� �$!-!"*-!� /$! .4./!( /-!�/. 5!-* ��/�$ .%5!.

'%&! 1�-%��'! ,0�)/%/4 �*(+*)!)/.� �) /-!�/. ��/�$ .%5!.

#-!�/!- /$�) 5!-* '%&! "%3! ,0�)/%/4 �*(+*)!)/.�

�!�/0-! �*./ � +!-�!)/�#! 0.! �4 /$! �%(0'�/! �*./ �*''0+ +-*#-�( /*

��'�0'�/! /$! �*./ *" � "!�/0-! *- *+/%*) %/!( �. �

+!-�!)/�#! *" /$! /*/�' �*./ *" /$! +�-!)/�

�)/!- /$! +!-�!)/�#! �. � 2$*'! )0(�!-� �� �. ��

�!-�!)/ *" ��-�+ ��-�+ %. /$! +!-�!)/�#! *" 0)0.��'! �*(+*)!)/ (�/!-%�'

�-!�/! 0-%)# /$! (�)0"��/0-! *" � +�-/%�0'�- +�-!)/ %/!(�

�0-%)# ����������� #!)!-�/%*)� /$! .4./!( %)�-!�.!.

#-*.. -!,0%-!(!)/. "*- /$! �*(+*)!)/ %/!( /* �*(+!).�/!

"*- /$! '*..�

�*/!� �$-%)& %. /$! !3+!�/! '*.. *" +�-!)/ %/!(. ��)

$!)�!� �*(+*)!)/.� 0! /* /$! (�)0"��/0-%)# +-*�!..�

�$-%)& �) .�-�+ �-! �*(+*0) ! /* "%#0-! /$! /*/�' '*..

%) /$! (�)0"��/0-! *" � +�-/%�0'�- %/!(� ��0-�/! .$-%)&

�) .�-�+ "��/*-. ��) $!'+ /* +-* 0�! (*-! ���0-�/!

+'�))%)# ��'�0'�/%*).�

�)/!- +!-�!)/. �. 2$*'! )0(�!-.� �� �. ��

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�$! �$*+ �'**- �*)/-*' �) ��/!-%�' �!,0%-!(!)/.

�'�))%)# .4./!(. %)"'�/! �*(+*)!)/ -!,0%-!(!)/. �4 /$%.

+!-�!)/�#!� �$%. .�-�+ +!-�!)/ %. 0)%,0! /* /$!

-!'�/%*).$%+ *" *)! +�-!)/ �) *)! �*(+*)!)/�

Review Bills of Material and Routings

A8.1 (8/97) 2–9

����� ���������

���� ��� ����� � �� �$� �� !��� ��� "��!� � �������� �� �������� ��

���!� �� �� ������ � ����!� ��� ���� #� ��� ��

����� ���� �� �$� �� !��� �� ��� "��!� �� �� ���������

���� �� �� ����� #��� $�! �!� �� ������ ����� ���� �

�������� �� �$� �� ����!�� �� ��� "��!� �$

�����!����� �� $���� ������ ���� ���� �� ���

����� ��� � �� ���� ����� ���� ��� � ���������� �� ��� ��

�� ��������� ��! ��� � ������ �� �$� �� � ����!�� �

�� �������� ����� ������ �

Reviewing Routings for Product Costing

From Product Data Management (G30), choose Daily PDM Discrete

From Daily PDM Discrete (G3011), choose Enter/Change Routing

��"��# $�!� ��! ���� � !����� ��� ���� ���! � $�!� ����� ��� �"������ ��� ��

See Also

� ������� ���� ������� ������ �� �� ���� � ���� ���������� ��� ����

������ ������ �����

Product Costing and Manufacturing Accounting

2–10 A8.1 (8/97)

� ������ � ��� �������

� �!��������� ��"!���

�� ��#��$ !�� �����$��� ����� �

� ���� ���!��

� ������� �"� �"�

� ����� �"� �"�

� ��!"� �"�

�� ���� !�� ��!��� �����

Review Bills of Material and Routings

A8.1 (8/97) 2–11

�� ��(��) &�� �!��!)� � �����%�

� ���� ��%�%

� $�) ��,�

� !%& �+"�

� �+"� "�$

� ����� ��$�� &

� '�'��&�(� ��$�� &

����� ���������

�!$� � &�$ � '���$ &��& ��� &����% � �$� ��� "�� &� )!$� �� &�$� !$

�'%� �%% ' �&�

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�!$ #'�"�� & '%�$%� &��% �% &�� �$��&�$�%!'$�� $�%"! %����

�!$ �!�"��&� � &�� ��� &� � �� ��&�(�&+�

���� ���% �% &�� %&� ��$� ����� � �!'$% �*"��&�� &! ��

� �'$$�� � &�� !$��� "$!�'�&�! !� &��% �&���

Product Costing and Manufacturing Accounting

2–12 A8.1 (8/97)

����� ���������

���+. �%&/ &/ 0%" /0�*!�.! %+1./ +# (��+. "4," 0"! &* 0%" *+.)�(

,.+!1 0&+* +# 0%&/ &0")�

�%" .1* (��+. %+1./ &* 0%" �+10&*$ ��/0". 0��(" �����

�." 0%" 0+0�( %+1./ &0 0�'"/ 0%" /," &#&"! ."3 /&6" 0+

+),("0" 0%" +,".�0&+*� �%" %+1./ �." )1(0&,(&"! �5 0%"

."3 /&6" !1.&*$ /%+, #(++. ."("�/" �*! ,.+!1 0 +/0&*$�

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�+. �-1&,)"*0��(�*0�

�%&/ &/ 0%" "/0&)�0"! *1)�". +# %+1./ *""!"! 0+ +),("0"

� )�&*0"*�* " � 0&2&05�

�+1./ �%" /0�*!�.! /"01, %+1./ 5+1 "4," 0 0+ &* 1. &* 0%"

*+.)�( +),("0&+* +# 0%&/ &0")�

�&)" ��/&/ 1/". !"#&*"! +!" �/5/0") �� 05," ��� 0%�0 &!"*0&#&"/

0%" 0&)" ��/&/ +. .�0" #+. )� %&*" +. (��+. %+1./ "*0"."!

#+. �*5 .+10&*$ /0",� �+1 �* /"0 .�0"/ ,". 1*&0� ,". ��� ,".

����� �*! /+ +*�

�%" /5/0") 1/"/ 0%" 2�(1"/ &* 0%" �"/ .&,0&+*7 #&"(! +*

0%" �/". �"#&*"! �+!"/ #+.) #+. +/0&*$ �*! / %"!1(&*$

�( 1(�0&+*/� �%" !"/ .&,0&+* &/ 3%�0 0%" +!" .",."/"*0/�

�10 &/ *+0 1/"! &* �( 1(�0&+*/�

�."3 �&6" �%" *1)�". +# ,"+,(" 3%+ 3+.' &* 0%" /," &#&"! 3+.'

"*0". +. .+10&*$ +,".�0&+*�

�%" /5/0") )1(0&,(&"/ 0%" �1* ���+. 2�(1" &* 0%" �+10&*$

��/0". 0��(" ����� �5 ."3 /&6" !1.&*$ +/0&*$ 0+

$"*".�0" 0+0�( (��+. !+((�./�

�# 0%" �.&)" �+�! �+!" &/ � +. �� 0%" /5/0") 1/"/ 0%" 0+0�(

(��+. %+1./ #+. �� '/ %"!1(&*$� �# 0%" �.&)" �+�! �+!" &/

� +. �� 0%" /5/0") 1/"/ 0%" 0+0�( )� %&*" %+1./ #+.

�� '/ %"!1(&*$ 3&0%+10 )+!&#& �0&+* �5 ."3 /&6"�

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�+. �%+, �(++. �+*0.+(�

�%" �."3 �&6" #&"(! +* 0%" �+10&*$ �"2&/&+*/ #+.)

!&/,(�5/ 0%" 2�(1" /"0 +* 0%" �*0".��%�*$" �+.' �"*0"./

#+.) ������� �+1 �* +2"..&!" 0%" 2�(1" �5 %�*$&*$ 0%&/

#&"(! +* 0%" �+10&*$ �"2&/&+*/ #+.)� �+3"2".� 0%"

�*0".��%�*$" �+.' �"*0"./ #+.) 3&(( *+0 ."#(" 0 0%&/

%�*$"�

Review Bills of Material and Routings

A8.1 (8/97) 2–13

����� ���������

�,01 �6-" �%&0 ,!" !"0&$+�1"0 "� % ")"*"+1 ,# ,01 #,/ �+ &1"*� +

"5�*-)" ,# 1%" ,!&+$ 01/2 12/" &0�

�2/ %�0"! /�4 *�1"/&�)

� �&/" 1 )��,/ /,21&+$ 0%""1 /,))2-

� �"12- )��,/ /,21&+$ 0%""1 /,))2-

� ��/&��)" �2/!"+ /,21&+$ 0%""1 /,))2-

� �&5"! �2/!"+ /,21&+$ 0%""1 /,))2-

�5 �02�))6 20"! #,/ ,210&!" -/, "00&+$ /,21&+$

0%""1 /,))2-

�5 �02�))6 20"! #,/ "51/� �!!8,+0� 02 % �0

")" 1/& &16� 4�1"/� �+! 0, #,/1%

�%" ,-1&,+�) �!!8,+ ,*-21�1&,+0 202�))6 ,-"/�1" 4&1%

1%" 16-" 7�� "51/� �!!8,+0� �%&0 ,01 01/2 12/" �)),40 6,2

1, 20" �+ 2+)&*&1"! +2*�"/ ,# ,01 ,*-,+"+10 1,

�) 2)�1" �)1"/+�1&3" ,01 /,))2-0� �%" 0601"* 1%"+

�00, &�1"0 1%"0" ,01 ,*-,+"+10 4&1% ,+" ,# 0&5 20"/

!"#&+"! 02**�/6 ,01 �2 ("10�

�6- �- 20"/ !"#&+"! ,!" �0601"* ��� 16-" ��� 1%�1 &+!& �1"0

1%" 16-" ,# ,-"/�1&,+� �,/ "5�*-)"�

)1"/+�1" /,21&+$

�� �/�3") 1&*"

�� �!)" 1&*"

� �"51 ��+1"/ 1"51 �1 �"0 /&-1&,+�

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�,/ �/,!2 1 �,01&+$�

�+)6 ,-"/�1&,+0 4&1% � 7�)�+(� 16-" ,-"/�1&,+ ,!" �/"

,01"!�

�&")! � �"-/"0"+10 1%" -)�++"! ,21-21 6&")! -"/ "+1 #,/ � 01"-�

�%" �)�++"! �&")! �-!�1" -/,$/�* 20"0 1%&0 3�)2" 1,

2-!�1" 1%" �2*2)�1&3" �"/ "+1 &+ 1%" �&)) ,# *�1"/&�) �+!

1%" �-"/�1&,+ � /�- �"/ "+1 &+ 1%" /,21&+$� ��1"/&�)0

�".2&/"*"+10 �)�++&+$ 20"0 1%" 01"- 0 /�- -"/ "+1 �+!

1%" "5&01&+$ ,*-,+"+1 0 /�- -"/ "+1 1, -)�+ ,*-,+"+1

!"*�+!�

�2* � �"-/"0"+10 1%" 2*2)�1&3" -)�++"! ,21-21 6&")! -"/ "+1

#,/ � 01"-� �%" 0601"* 20"0 1%&0 3�)2" 1, �!'201 1%"

,-"/�1&,+ 01"- 0 /�- -"/ "+1 #,/ 1%" ,*-,+"+10 �1 1%�1

,-"/�1&,+ 01"-� �%&0 "+��)"0 1%" ��� 0601"* 1, 20" 1%"

,-"/�1&,+ 01"- 0 /�- -"/ "+1 �),+$ 4&1% 1%" "5&01&+$

,*-,+"+1 0 /�- -"/ "+1 1, -)�+ ,*-,+"+1 !"*�+!�

Product Costing and Manufacturing Accounting

2–14 A8.1 (8/97)

A8.1 (8/97) 2–15

Set Up Product Costing

Setting Up Product Costing

�! ��� �!� ���&� �� ���!� ��� ��� �%� �� � ��� %�!� �����������!��� !���� ��"������� ������ ��� �%� �� !��� �� "��!�� %�! ������ ��� ������ %�!� ����!� ��� ��

�� ��� !� ����!� ��� ��� ������ � �� �� �����#����

� �� ��� !� ����!� ��� ��� �!�� � ���

� �� ��� !� � �� ��� ��"���

� ���"�� ��� � �� ��� ��"���

� �� ��� !� � �� ��� �

� �� ��� !� ��� �������� �

� �� ��� !� ���!��� !���� ���� �� � ��� ����!� ��� ���

� �� ��� !� ���!�� �� �� �� ��� � #��� ��� ��

Setting Up Accounting Cost Quantities

From Inventory Management (G41), choose Item Revisions

From Item Revisions (G4112), choose Manufacturing Data under the ItemBranch/Plant Information heading

��� �%� �� !��� ����!� ��� ��� �!�� � ��� � �� ������ �� ������ ��� �� ��$���� !� ��� � ��� �� � ��� ����!� ��� ��� �!�� � ��� �������� �� �"����� �!�� � %�� � #��� ����� ��� ��� � ��� �!���� ��� ����!�� �� �%� �� ��"���� �� ��$���� !� ��� � �% �� ����!� ��� ��� �!�� � % %�! ������% � �� ������ � !�� �� !���� ��$�� ��� �

� �� � �� ����� ��� �� ���� � �

� ���!��� !���� �� �

Product Costing and Manufacturing Accounting

2–16 A8.1 (8/97)

������#� �! !�%��& #�� �����&��� �����

� ����$�#��� ��"# �$��#�#(

����� ���������

����$�#��� ��"# �#( �� ���$�# #��# #�� "("#�� $"�" �� #�� ��"# !���$� �!��!��

#� ��#�!���� #�� ������#��� �� "�#$� ��"#"� ��� "("#��

#�#��" #�� "�#$� ��"#" ��� ��%���" #�� "$� �( #��" $��#�#(

#� ��#�!���� � $��# "�#$� ��"#� ��� ����$�# �" ��

Setting Up Item Cost Levels

From Inventory Management (G41), choose Inventory Master/Transactions

From Inventory Master/Transactions (G4111), choose Item Master Information

��� ��"# ��%�� (�$ �""��� #� �� �#�� ������#�" #�� ��%�� �# &���� #�� "("#������#���" ��"#"� ��$ ��#�!���� &��#��! #�� "("#�� ����#���" ��� �%�!��� ��"#��! �� �#�� ���"# ��%�� �� �! � �����!��# ��"# ��! #�� �#�� �� ���� �!���������#���"# ��%�� ��� ��� "("#�� ��� ��"� ����#��� � �����!��# ��"# ��! ���� ����#��� �����# &�#��� � �!���������# ���"# ��%�� �� �&�%�!� �� #�� �!��$�# ��"#��� "("#�����"#" �# ��"# ��%�� �!� ����!��#����� ���(� ��� �#��" $"�� �� � ���$���#$!�����%�!�����# "��$�� ��%� ��"# ��%��" �� � �! �� �'���# ������$!�� �#��"� &�����$"# �� ��"# ��%�� �

Set Up Product Costing

A8.1 (8/97) 2–17

� ��� �� �� ��� � �� ���

�# �(�" ��'(�& �#�$&"�( $#

�$"%!�(� $& &�* �+ (�� �$!!$+ #� � �!�

� �#*�#($&- �$'( ��*�!

��� ������� �

�#*�#($&- �$'( ��*�! � �$�� (��( #� ��(�' +��(��& (�� '-'(�" "� #(� #' $#�

$*�&�!! #*�#($&- �$'( �$& (�� (�"� � � ���&�#( �$'( �$&

���� �&�#���%!�#(� $& � � ���&�#( �$'( �$& ���� !$��( $#

�#� !$( + (� # � �&�#���%!�#(� ��� '-'(�" "� #(� #'

#*�#($&- �$'(' # (�� �$'( �����& (��!� ��������

��! � �$��' �&�

� �(�" !�*�!

�(�"��&�#�� !�*�!

�(�"��&�#����$��( $# !�*�! �#$( &��$�# .�� �-

(�� ��#)���()& #� '-'(�"� �,��%( �$& �$#� �)&��

(�"'�

Product Costing and Manufacturing Accounting

2–18 A8.1 (8/97)

Converting Item Cost Levels

From Inventory Management (G41), enter 27

From Inventory Advanced & Technical Ops (G4131), choose Item Cost LevelConversion

�*�( /&+ ��,� �%*�(�� �&)* %�&($�* &%� /&+ $ ��* %��� *& ���%�� �% *�$�)�&)* #�,�#� �&+ $+)* +)� *�� �*�$ �&)* ��,�# �&%,�() &% '(&�(�$ *& ���%�� �% *�$�) �&)* #�,�# ��*�( �&)* %�&($�* &% ��) ���% �%*�(���

�� /&+ (+% *� ) '(&�(�$� * ��#�*�) �## �. )* %� �&)* (��&(�) �&( *�� *�$ % *���&)* �����( *��#� ����� �%� �(��*�) %�- �&)* (��&(�) *��* �&((�)'&%� *& *��#�,�#� ��� )/)*�$ +)�) *�� )�#�)� %,�%*&(/ �&)* $�*�&� �&( *�� *�$ *& �(��*� *��%�- �&)* (��&(�)�

��� '(&�(�$ �&�) %&* ���%�� *�� �&)* ,�#+�* &% &� *�$) �%� �&�) %&* �(��*�!&+(%�# �%*( �)� �&( �.�$'#�� � /&+ ���%�� �% *�$�) �&)* #�,�# �(&$�(�%���'#�%* �%� #&��* &% *& �(�%���'#�%*� �## �. )* %� �&)* (��&(�) �&( *���(�%���'#�%* �%� #&��* &% $+)* �&%*� % *�� )�$� )�#�)� %,�%*&(/ �&)* $�*�&��%� �&)*�

�&+ ��% (+% �*�$ �&)* ��,�# �&%,�() &% % '(&&� $&�� &( � %�# $&��� ���%/&+ (+% *�� '(&�(�$ % '(&&� $&��� *�� )/)*�$ ��%�(�*�) *�� �*�$ �&)* ��,�#�&%,�() &% (�'&(*� )�&- %� �((&() *��* %��� �&((��* &%� �&+ )�&+#� �#-�/) (+%*�� '(&�(�$ % '(&&� $&�� � ()* �%� �&((��* �%/ � )�(�'�%� �)�

���% /&+ (+% *�� '(&�(�$ % � %�# $&��� *�� )/)*�$ +'��*�) *�� �&##&- %�*��#�)�

� �%,�%*&(/ �&)* ��,�# � �#� % *�� �*�$ ��)*�( ����

� �&)* �����( �����

���%� %� /&+( *�$ �&)* #�,�#) ���%��) ��*� *�(&+��&+* *�� )/)*�$� �&+ )�&+#�(�)*( �* ����)) *& *� ) '(&�(�$�

Before You Begin

� ���" +' /&+( ��*� *��#�) �&$'#�*�#/ ���&(� /&+ ��� % *�� ��*� �&%,�() &%'(&��))� �� *�� (�)+#*) &� *�� �&%,�() &% �(� +%)�* )���*&(/� /&+ ��% +)� *�����"+' *��#�) *& (�)*&(� ��*� *��#�) *& *�� ( &( � %�# �&($�*�

� ��( �/ *��* %& +)�() �(� ����)) %� *�� �*�$ ��)*�( &( �&)* �����( *��#�)-��% *� ) '(&�(�$ ) (+%% %� % � %�# $&���

Set Up Product Costing

A8.1 (8/97) 2–19

41815 J.D. Edwards & Company Page – 2 Item Cost Level Conversion Date – 4/10/ 98

*** Proof Mode ***

Item Number Branch Location Lot L CM Unit Cost Remark ––––––––––––––––––––––– –––––––––––– –––––––––––––––––––– –––––––––––– – –– ––––––––––––––– –––––––––––––––––––––––––––––––– E001 30 3 01 6.6378 Basing comparison on this record E001 30 DAMAGED 3 01 6.4100 Cost not the same P002 10 3 01 30.7500 Basing comparison on this record P002 10 1 B 1 3 02 30.3750 Costing Method/Cost not the same P002 20 3 01 31.4333 Basing comparison on this record P002 20 1 B 1 3 02 30.8417 Costing Method/Cost not the same P002 30 3 01 30.1049 Basing comparison on this record P002 30 1 B 1 3 02 30.2500 Costing Method/Cost not the same P002 40 3 02 30.5610 Basing comparison on this record P002 40 D 3 02 30.2500 Cost not the same P002 40 R 3 02 30.2500 Cost not the same P002 40 1 B 1 3 02 30.2500 Cost not the same P002 40 3 E 3 02 30.2500 Cost not the same TS002 10 3 01 43.1200 Basing comparison on this record TS002 10 1 C 1 3 02 43.5000 Costing Method/Cost not the same TS002 20 3 01 43.1200 Basing comparison on this record TS002 20 1 C 1 3 02 43.5000 Costing Method/Cost not the same TS002 30 3 01 66.0000 Basing comparison on this record TS002 30 1 C 1 3 01 43.9573 Cost not the same TS002 40 3 02 43.7336 Basing comparison on this record TS002 40 R 3 02 43.5000 Cost not the same TS002 40 1 C 1 3 02 43.5000 Cost not the same TS002 40 2 C 1 3 02 43.5000 Cost not the same V001 10 3 01 16.1500 Basing comparison on this record V001 10 1 A 1 9310140004 3 01 16.0000 Cost not the same V001 10 1 A 2 9310140002 3 01 16.0000 Cost not the same V001 20 3 01 16.1500 Basing comparison on this record V001 20 1 A 1 9310140005 3 01 16.0000 Cost not the same V001 20 1 A 2 9310140003 3 01 16.0000 Cost not the same V001 30 3 01 16.1500 Basing comparison on this record V001 30 1 A 1 00000006 3 01 16.0000 Cost not the same V001 30 1 A 2 00000005 3 01 16.0000 Cost not the same V001 40 3 02 16.1455 Basing comparison on this record V001 40 D 00000007 3 02 16.0000 Cost not the same V001 40 R 00000007 3 02 16.0000 Cost not the same V001 40 1 A 1 00000007 3 02 16.0000 Cost not the same V001 40 1 A 2 00000007 3 02 16.0000 Cost not the same V001 40 3 F 00000007 3 02 16.0000 Cost not the same

See Also

� � ����� �� �� � ���� � �� ������

Processing Options for Item Cost Level Conversion

PROCESS CONTROL:1. Enter the cost level to update to. ____________

2. If updating to cost level ’1’, enter ____________ the branch to default the costs from. If updating from a cost level ’3’, the costs will default from the primary location.

3. Enter a ’1’ to run in final mode and ____________ update files. If blank, no file updates will occur.

PROCESS CONTROL (cont.):

Product Costing and Manufacturing Accounting

2–20 A8.1 (8/97)

4. Enter a ’1’ to print only exceptions ____________ on the edit report. A blank will print all items.

Setting Up Item Costs

�(- &-+, )*(.#�� �(+, #' (*&�,#(' (* ���" ( 1(-* #,�&+ (* ,"� +1+,�& ,( ,*��$#'.�',(*1 �(+,+� �(- +)��# 1 ,"� �(+, &�,"(� ,"�, ,"� +1+,�& -+�+ ,( ��,�*&#'��' #,�&�+ �(+, (*

� ��%�+�#'.�',(*1 ,*�'+��,#('+

� �-*�"�+� (*��*+

�(* �0�&)%�� #' � �#+,*#�-,#(' �'.#*('&�',� 1(- ��' "�.� ,"� +1+,�& -+� ,"�/�#!",�� �.�*�!� �(+, &�,"(� ,( ��,�*&#'� ,"� #'.�',(*1 �(+, (* �' #,�& �'�-+� ,"� %�+,2#' �(+, &�,"(� ,( ��,�*&#'� ,"� #,�&�+ -'#, �(+, (* )-*�"�+� (*��*+��(/�.�*� #' � &�'- ��,-*#'! �'.#*('&�',� 1(- &-+, -+� ,"� +,�'��*� �(+,&�,"(� ,( ��,�*&#'� ,"� #'.�',(*1 �(+,�

�(* ���" �(+, &�,"(� 1(- �++#!' ,( �' #,�&� 1(- &-+, �%+( +)��# 1 � �(+,� �(*�0�&)%�� ,( -+� ,"� %�+,2#' �(+, &�,"(� (* �' #,�&� 1(- &-+, �',�* �' #'#,#�%�(+, (* ,"�, �(+, &�,"(�� �"� +1+,�& -)��,�+ ,"� %�+,2#' �(+, ��+�� (' ,"� �(+,( ,"� #,�& �+ ( ,"� %�+, *���#), ��,��

�(* )-*�"�+�� #,�&+ �'� (-,+#�� ()�*�,#('+� ,"� &�#' #')-,+ ,( )*(�-�, �(+,#'!�*� �',�*�� (' �(+, ��.#+#('+ (* �(+, �(&)('�',+�

�( +�, -) #,�& �(+,+� �(&)%�,� ,"� (%%(/#'! ,�+$+

� ��, -) '�/ �(+, &�,"(�+

� �++#!' �(+, &�,"(�+

See Also

� ������ � ����� �����

� �� �� � �� �� �� ��

�(- ��' +�, -) -+�* �� #'�� �(��+ ������ ,( �� #'� 1(-* (/' �(+, &�,"(�+��(* �0�&)%�� 1(- &#!", /�', ,( �+,��%#+" � �(+, &�,"(� ,( &�#',�#' � "#+,(*1 ( %�+, 1��*�+ �(+,+� �(��+ � ,"*(-!" �� �*� "�*�2�(��� �'� ��''(, �� �%,�*����(��+ �� ,"*(-!" � �*� *�+�*.�� (* ���� ��/�*�+ -+��

Set Up Product Costing

A8.1 (8/97) 2–21

� �!� ������ ���� ��$�!���!

������"� "�� �����%��� �����!�

� ����

� �!� ��"���

� �!� ��"���(�

��� ����� ����

���� ���! ���#�� ���"���! � ��!" �� $���� ����! �� � !�������

#!� ������� ���� ��!"� ��� �#��� �� ��� ��"� ! "��" �

���� ��� ���"��� ����� ! �� "�� ���#�� "�"���

�!� ��"��� � #!� ������� ���� � ��� ��

�!� ��"����� ����"����� "�&" "��" �# "�� ��!� ���! � ��� ����! � ����� ��

��� �%� �! !'!"��!�

What You Should Know About

�� ���! ���� ������! ��!" ��"���! "��" � � #!�� �� "�� ��!"

���#� ��� �!!����� "� �"��!� ���! �! � "%�(��� ��"� �

������#�� �� ������

��������� � ����"����! "�� ��!" ��"����

Product Costing and Manufacturing Accounting

2–22 A8.1 (8/97)

���������� � ��!&����% ����&�"!�� �!�"$ �&�"! ��"'& &�� �"%& �&�"��

�� ���� ���� ������

From Product Data Management (G30), choose Daily Product Costing

From Daily Product Costing (G3014), choose Enter/Change Item Costs

���� &� � *"' ��� �! �&� "! &��% �"$ � &�� #$"�$� ��%#��*% ��� �"%& �&�"�%%�& '# �! &�� '%�$ ����!�� �"�� &���� ������ ���% �!��'��% ����& #$�����!�� �&�"�% &��& &�� #$"�$� #$"(���% �!� �!* ����&�"!�� �&�"�% *"' �$��&�� �"'%#����* )���� �&�"�% &" �##�* &" �! �&� �* �%%��!�!� � '!�& �"%& �"$ ���� �&�"��

�! �"%& ��(�%�"!% ��!&�$����!�� &� �"%&%�

�� �" #��&� &�� �"��")�!� ����� �"$ ���� �##������� �"%& �&�"�

� �!�& �"%&

� �!&�$ &�� �##$"#$��&� �"%& �&�"�% �! &�� �"��")�!� �����%

� ����%� !(�!&"$*

� �'$���%�!�

Set Up Product Costing

A8.1 (8/97) 2–23

� �� �������� ��

�#�) $() ��%�#��#� $# )�� �$() "�)�$�� )��( ��)� ��# �$"� �'$"

+�'�$*( ($*'��(� �$' �-�"%!�� %*'���(�#� $' )�� �$()

'$!!*%�

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

��� �$() �$' $#� *#�) $� )��( �)�"� ��(�� $# )��

�$''�(%$#��#� �$() "�)�$��

��!�(��#+�#)$'. � �$�� �)��!� �� �� )��) �#����)�( )�� �$() "�)�$� )��)

)�� (.()�" *(�( )$ ��!�*!�)� )�� �$() $� �$$�( ($!� �$' )��

�)�"� $() "�)�$�( ��0� �'� ��'�0�$����

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�� .$* "��#)��# �$()( �) )�� �)�" !�+�!� )�� (.()�" '�)'��+�(

)�� ����*!) +�!*� �$' )��( ���!� �'$" )�� ��)� ���)�$#�'.� ��

.$* "��#)��# �$()( �) )�� �)�" �#� �'�#���%!�#) !�+�!� )��

(.()�" '�)'��+�( )�� ����*!) +�!*� �'$" �'�#����!�#)

$#()�#)(�

�*'���(�#� � �$�� �)��!� �� �� )��) �#����)�( )�� �$() "�)�$� )��)

)�� (.()�" *(�( )$ ��)�'"�#� )�� �$() $� )�� �)�" �$'

%*'���(� $'��'(� $() "�)�$�( ��0� �'� ��'�0�$����

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�� .$* "��#)��# �$()( �) )�� �)�" !�+�!� )�� (.()�" '�)'��+�(

)�� ����*!) +�!*� �$' )��( ���!� �'$" )�� ��)� ���)�$#�'.� ��

.$* "��#)��# �$()( �) )�� �)�" �#� �'�#���%!�#) !�+�!� )��

(.()�" '�)'��+�( )�� ����*!) +�!*� �'$" �'�#����!�#)

$#()�#)(�

What You Should Know About

��� �� �� � ���� �����

� ����� ��� � �� �

����

�� .$* �((��# � �$() "�)�$� �$' (�!�(��#+�#)$'. $'

%*'���(�#� )��) �( #$) (�) *% ,�)� � �$() �"$*#)� �

,�'#�#� "�((��� �%%��'(� �� .$* �$ #$) �#)�' � �$()

�"$*#) �$' )�� �$() "�)�$�� )�� (.()�" �((��#( � /�'$

�$()�

����� �� �� � ����� �$* ��# ���#�� )�� �$!!�' �"$*#) �$' �#. �$() "�)�$� �)

�#. )�"�� �� .$* ���#�� )�� �"$*#) �$' )�� �$() "�)�$�

.$* *(�� )$ )'�� �$()( $� �$$�( ($!�� )�� (.()�" �%%!��(

)�� #�, �"$*#) )$ .$*' $#0��#� &*�#)�). $� )�� �)�"� �)

�!($ �'��)�( �$*'#�! �#)'��( )$ ���$*#) �$' )�� �����'�#��

��),��# )�� $!� �#� )�� #�, �"$*#)(�

Product Costing and Manufacturing Accounting

2–24 A8.1 (8/97)

������� ��� � ��� �$&�� "$!�$��% '"��&� &�� �!���$ ��!' & �!$ �!%&

��&�!�% ������ �!$ �*��"��

� �%&-� ��&�!� . ��� %+%&�� � &�$��&�(��+ '"��&�%&��% ' �& �!%& ��%�� ! &�� ��%& �!%& !� &�� �&�� �& &��&��� !� � "'$���%� !$��$ $����"& !$ ��&�$ � � (� &!$+���'%&�� &�

� �����&�� �(�$��� ��&�!� . ��� %+%&�� ����'��&�%� � '"��&�% &��% ��!' & �+ ���� � &$� %��&�! #'� &�&��%� ���� � &$� %��&�! �!%&%� � � ��(��� � &��&!&�� �!%& �+ &�� &!&�� #'� &�&+�

� �'$���%� ��&�!� . %��� �% ��%&-� ��&�!�� �'&)�&�!'& �� ��� �!%&%�

� �&� ��$�� �'$$� &� � � �'&'$� ��&�!�% . '"��&�� �+&�� �$!,� �"��&� "$!�$���

�� +!' � ��'�� ����&�! �� �!%&� � ��&�!�%� +!' �'%&

'"��&� &��� �� '���+�

��� ��� � � �� ��� � �!' �� $��!(� � �!%& ��&�!� �!$ � �&�� �� �& �% !

�! ��$ �""�������� �� +!' &$+ &! $��!(� +!'$

%���%�� (� &!$+ !$ "'$���%� � �!%& ��&�!�� &�� %+%&��

��%"��+% � )�$ � � ��%%���� ��� %+%&�� �!�% !& ����&�

&�� �!%& ��&�!�� �'& '"��&�% �& &! � ,�$! �!%&�

Processing Options for Item Cost Revisions

DISPLAY CONTROL: 1. Enter a ’1’ for Speed Cost Update. ____________ If left blank, the screen will default to Item Cost Revisions.

DEFAULT VALUES: 2. Enter the default cost method to ____________ display when the Speed Cost Update format is selected.

PROCESS CONTROL: 3. Enter a ’1’ to prevent the ____________ standard cost from being changed.

Set Up Product Costing

A8.1 (8/97) 2–25

Setting Up Cost Components

From Product Data Management (G30), enter 29

From Product Data Management Setup (G3041), choose Product CostingSetup

From Product Costing Setup (G3042), choose Cost Components

�#� ��#$ ��� ����$# $� ����$��) ��� $"��� ���� ������$ �" $) � �� ��#$ ��" ���$��� ��#$ ��� ����$# $��$ ����� '�$� �� �� ��� � �"� ��"�+����� �) ����'�"�# ��� �����$ �� �������� ��% ��� ������ �� %�����$�� �%���" ������$����� ��#$ ��� ����$# $� ����%�$ ��" �($"� ��#$# ��" �� �$��� #%�� �#����$"���$) �" "�#��"�� ��� ��&��� ���$� ���#� %#�" ������� ��#$ ��� ����$#��� ����� '�$� ��) ��$$�" �(�� $ �� �� �" �� ��� �'�"�# "��������#� �%$ ���#��$ "�!%�"�� $��$ )�% %#� ��#$ ��� ����$ � ��" �%$#��� � �"�$���#� ��% ����##��� #� �"�$� ��#$ ��� ����$# �) ��$���"��# $��$ �"� � ������� $� )�%"�%#���##�

��$��%�� �$ ����$ � ��" $��$ )�% ��� #�$ % �($"� ��#$ ��� ����$# $��$ �����'�$� �� �� �" �� $�� ��%��$� ��#$ ����% "��"�� ��$%���) ����$�# $��#� ��#$��� ����$#� ��� �'�"�# "��������# $��$ )�% ������ �($"� ��#$# '�$� �� *����" ��#) ����$�����$����

See Also

� ��������� ������ �� ��� ������ ��� ��������� ��������

� �������� � ����������� �� ��� ������

�� �� � � ��� ��������

�� �#�" ������� ���� ��&�#���#

Product Costing and Manufacturing Accounting

2–26 A8.1 (8/97)

�������� ��� �����"��� �������

� ����

� �����������

� �������������

��� ����� ����

���� ���� ��� �� �������� � ���� �� !���� ����� ��� � ��������

��� ������� ���� ����� ��� � ���� �� ���������� ���� �

���� ��� ������� ������� �� ��� ��� �� ������

����������� � ��� ������� ���� �� �������

������������� ���������� ��#� ���� � ����� ��������� �� ��������� � ����� ��

���� �"���� �$������

What You Should Know About

�� �� ���� ���� �� �������$ ��� �� ��� �������� ����

���������� ���� ��� �� ��� �� ��� ���� ���� � ��� ��

�����

��������� ��������� "��� ���� ���� ��������� �����������

��������� � ���������� ��#� ���� � ����� ��������� �� ��������� ��� ����

�����������

Set Up Product Costing

A8.1 (8/97) 2–27

Setting Up Manufacturing Constants for Product Costing

From Product Data Management (G30), enter 29

From Product Data Managment Setup (G3041), choose Product Costing Setup

From Product Costing Setup (G3042), choose Manufacturing Constants

��� ���� ���� ���� ����������� ���� �� ������ �� "��� ������������ ��������������� ��������� �� ��� ������� ���� ����������

� ��! �� ��������� � ������ �����

� ������ �� �������� !��� ������ ���������" !��� ����������� ������ �� ����� � ������

� ������ � ������� ��� ���������� �� �������� �� �����

See Also

� ������� � ������������ ��������� ������� �� ��� ������� ����

��������� �������� ������������ ����

�� ��� �� �� ������� �� ��� �� �� ������� �����

�� ������������� ���������

Product Costing and Manufacturing Accounting

2–28 A8.1 (8/97)

�+),("/" /%" #+((+2&*$ #&"(!.

� �1"-%"�!. �. �"- "*/. +- ��/".

� �+! +./ �4 �+-' �"*/"- �##& &"* 4

� �* (0!" �+-' �"*/"- �##& &"* 4 &* �1"-%"�!

� �* (0!" ��-&��(" ���+- �1"-%"�! &* �+./

� ��( 0(�/" ��-&��(" +* �&-" / ���+-

� ��( 0(�/" ��-&��(" +* �"/0, ���+-

� �* (0!" �&3"! ���+- �1"-%"�! &* �+./

� ��( 0(�/" �&3"! +* �&-" / ���+-

� ��( 0(�/" �&3"! +* �"/0, ���+-

� �* (0!" ��-&��(" �� %&*" �1"-%"�! &* �+./

� �* (0!" �&3"! �� %&*" �1"-%"�! &* �+./

����� ���������

�1"-%"�!. �. �"- "*/. +-

��/".

�"/"-)&*". %+2 1�(0". #+- +1"-%"�! #&"(!. � +./

+),+*"*/. �� /%-+0$% �� &* /%" �+-' �"*/"- ��/"

�"1&.&+*. /��(" ������� �-" "3,-".."!� ��(&! +!". �-"

� �3,-".. +1"-%"�! 1�(0". �. -�/". � 0--"* 4

1�(0".�� �+- "3�),("� "*/"- #&1" !+((�-. �. �����

� �3,-".. +1"-%"�! 1�(0". �. ,"- "*/.� �*/"-

,"- "*/. �. 2%+(" *0)�"-.� �+- "3�),("� "*/"-

#&1" ,"- "*/ �. �����

�+! +./ �4 �+-'

�"*/"- �##

�+*/-+(. 2%"/%"- /%" +./ -+((0, -"�/". +./ +),+*"*/

� �#+- (��+- "##& &"* 4� ��."! +* /%" !&-" / (��+- 1�(0"

� +./ +),+*"*/ ��� �*! /%" �+-' �"*/"- �##& &"* 4

,"- "*/ #-+) /%" �+-' �"*/"- �"1&.&+*. /��(" �������

��(&! 1�(0". �-"

� �".� �-"�/" +./ +),+*"*/ ��

� �+� �+ *+/ -"�/" +./ +),+*"*/ ��

�* (0!" �##& &"* 4 &*

�1"-%"�!

�# 4+0 .," &#&"! /%�/ 4+0 2�*/ /+ )+! +./. �4 2+-'

"*/"- "##& &"* 4� /%&. #&"(! !"/"-)&*". 2%"/%"- /%" +./

-+((0, &* (0!". 2+-' "*/"- "##& &"* 4 2%"* �( 0(�/&*$

+1"-%"�! 1�(0".� ��(&! 1�(0". �-"

� �* (0!" 2+-' "*/"- "##& &"* 4�

� �3 (0!" 2+-' "*/"- "##& &"* 4�

�* (0!" ��-� ���+-

�1"-%"�! &* +./

�+*/-+(. 2%"/%"- /%" +./ -+((0, -"�/". +./ +),+*"*/

� �#+- 1�-&��(" (��+- +1"-%"�!� &* /%" �+./ �+),+*"*/.

/��(" �������� ��(&! 1�(0". �-"

� �".� �-"�/" +./ +),+*"*/ ��

� �+� �+ *+/ -"�/" +./ +),+*"*/ ��

Set Up Product Costing

A8.1 (8/97) 2–29

����� ���������

�!�)!�(� ��&� $# � &��(

���$&

��(�&" #�' +��(��& (�� �$'( &$!!)% #�!)��' � &��( !��$&

�,%�#'�' ��$'( �$"%$#�#( ��� # (�� ($(�! )'�� ($

��!�)!�(� *�& ��!� !��$& $*�&���� ��$'( �$"%$#�#( ���

��! � *�!)�' �&��

� �#�!)�� � &��( !��$& �,%�#'�'�

� �,�!)�� � &��( !��$& �,%�#'�'�

�!�)!�(� ��&� $# ��()%

���$&

��(�&" #�' +��(��& (�� �$'( &$!!)% #�!)��' '�()% !��$&

�,%�#'�' ��$'( �$"%$#�#( ��� # (�� ($(�! )'�� ($

��!�)!�(� *�& ��!� '�()% $*�&���� ��$'( �$"%$#�#( ���

��! � *�!)�' �&��

� �#�!)�� '�()% !��$& �,%�#'�'�

� �,�!)�� '�()% !��$& �,%�#'�'�

�#�!)�� � ,�� ���$&

�*�&���� # �$'(

$#(&$!' +��(��& (�� �$'( &$!!)% �&��(�' �$'( �$"%$#�#(

��$& � ,�� !��$& $*�&����� # (�� $'( $"%$#�#('

(��!� �������� ��! � *�!)�' �&��

� ��'� &��(� �$'( �$"%$#�#( �

� �$� �$ #$( �&��(� �$'( �$"%$#�#( �

�!�)!�(� � ,�� $# � &��(

���$&

��(�&" #�' +��(��& (�� �$'( &$!!)% #�!)��' � &��( !��$&

�,%�#'�' ��$'( �$"%$#�#( ��� # (�� ($(�! )'�� ($

��!�)!�(� � ,�� !��$& $*�&���� ��$'( �$"%$#�#( �� ��! �

*�!)�' �&��

� �#�!)�� � &��( !��$& �,%�#'�'�

� �,�!)�� � &��( !��$& �,%�#'�'�

�!�)!�(� � ,�� $# ��()%

���$&

��(�&" #�' +��(��& (�� �$'( &$!!)% #�!)��' '�()% !��$&

�,%�#'�' ��$'( �$"%$#�#( ��� # (�� ($(�! )'�� ($

��!�)!�(� � ,�� '�()% $*�&���� ��$'( �$"%$#�#( �� ��! �

*�!)�' �&��

� �#�!)�� '�()% !��$& �,%�#'�'�

� �,�!)�� '�()% !��$& �,%�#'�'�

�#�!)�� ��&� ���� #�

�*�&���� # �$'(

$#(&$!' +��(��& (�� �$'( &$!!)% �&��(�' �$'( �$"%$#�#(

� ��$& *�& ��!� "��� #� $*�&����� # (�� $'(

$"%$#�#(' (��!� �������� ��! � *�!)�' �&��

� ��'� &��(� �$'( �$"%$#�#( ��

� �$� �$ #$( �&��(� �$'( �$"%$#�#( ��

�#�!)�� � ,�� ���� #�

�*�&���� # �$'(

$#(&$!' +��(��& (�� �$'( &$!!)% �&��(�' �$'( �$"%$#�#(

� ��$& � ,�� "��� #� $*�&����� # (�� $'( $"%$#�#('

(��!� �������� ��! � *�!)�' �&��

� ��'� &��(� �$'( �$"%$#�#( ��

� �$� �$ #$( �&��(� �$'( �$"%$#�#( ��

Product Costing and Manufacturing Accounting

2–30 A8.1 (8/97)

Setting Up Simulated Rates for a Work Center

From Manufacturing Systems (G3), choose Product Costing

From Daily Product Costing (G3014), choose Enter/Change Work Center Rate

��� � � ������� ��" � � �� �� ���� �� !��� ������ �" �� ����� � ��� ��� � ��� �� � ����� ������ ��� � � ��� �� ����� ��� � ��� ��� � ����� �� � ��� ������" !��� ������ �� ���� ������� �� �"���� ���� ����� ���� �� ������ ��� ������� � ���� ������ ���� � ������ ��������� � ��� � �� �� ��� �������� �� ������ � ��� ���������" ��������

Before You Begin

� ��� ���� ��� �� "��� !��� ������� �� �������� ��� ���� ������� ������"�� � � ����� � ���� �� �������� ���� ������ �� ��� ������� ���

���������� ������� ������������� ����� ��� �������� ������ ���� ��������� �� !��� ��������

See Also

� �������� ������ ��� ���������� ���������� �������� �� ��� �������

��� ���������� ������� ������������� �����

� ��� �� �������� ����� � � � � � ������

�� �������� ��� ���� ������ � ��

Set Up Product Costing

A8.1 (8/97) 2–31

�(&)%�,� ,"� (%%(/#'! #�%�+�

� �(*$ ��',�*

� �(+, ��,"(�

� �#&-%�,�� �#*��, ���(*

� �#&-%�,�� ��,-) ���(*

� �#&-%�,�� ���(* ��*#��%� �.�*"���

� �#&-%�,�� ���(* �#0�� �.�*"���

� �#&-%�,�� ���"#'� �-'

� �#&-%�,�� ���"#'� ��*#��%� �.�*"���

� �#&-%�,�� ���"#'� �#0�� �.�*"���

����� ���������

�(*$ ��',�* � '-&��* ,"�, #��',# #�+ � �*�'�"� )%�',� /(*$ ��',�*� (*

�-+#'�++ -'#,�

�(+, ��,"(� � -+�* �� #'�� �(�� �+1+,�& �� ,1)� ��� ,"�, #��',# #�+ �

�(+, &�,"(�� �(+, &�,"(�+ �� ,"*(-!" � �*� "�*�2�(����

�� ��������� ��� ����� � � � � � � � � � � � � � � � � � � � � � � � � � �

�"#+ �(�� /�+ �',�*�� (' *�'�"��%�', �('+,�',+�

�#*��, ���(* �"#+ *�,�� #' �(+, )�* "(-*� #+ ,"� *�,� -+�� ,( ��%�-%�,� ,"�

�-**�', %��(* �(+, �+ ( ,"� %�+, +#&-%�,#(' �'� -)��,��

��,-) ���(* �"#+ *�,�� #' �(+, )�* "(-*� #+ ,"� *�,� -+�� ,( ��%�-%�,� ,"�

�-**�', +�,-) %��(* �(+, �+ ( ,"� %�+, +#&-%�,#(' �'�

-)��,��

���(* ��*� �.�*"��� �"#+ *�,�� #' �(+, )�* "(-* (* )�*��', ( %��(*� #+ ,"� *�,�

-+�� ,( ��%�-%�,� ,"� �-**�', .�*#��%� %��(* (.�*"��� �(+,

�+ ( ,"� %�+, +#&-%�,#(' �'� -)��,��

���(* �#0�� �.�*"��� �"#+ *�,�� #' �(+, )�* "(-* (* )�*��', ( %��(*� #+ ,"� *�,�

-+�� ,( ��%�-%�,� ,"� �-**�', #0�� %��(* (.�*"��� �(+, �+

( ,"� %�+, +#&-%�,#(' �'� -)��,��

���"#'� �-' �"#+ *�,�� #' �(+, )�* "(-*� #+ ,"� *�,� -+�� ,( ��%�-%�,� ,"�

�-**�', &��"#'� �(+, �+ ( ,"� %�+, +#&-%�,#(' �'� -)��,��

���"#'� ��*� ��� �"#+ *�,�� #' �(+, )�* "(-* (* )�*��', ( %��(*� #+ ,"� *�,�

-+�� ,( ��%�-%�,� ,"� �-**�', .�*#��%� &��"#'� (.�*"���

�(+, �+ ( ,"� %�+, +#&-%�,#(' �'� -)��,��

���"#'� �#0�� ��� �"#+ *�,�� #' �(+, )�* "(-* (* )�*��', ( %��(*� #+ ,"� *�,�

-+�� ,( ��%�-%�,� ,"� �-**�', #0�� &��"#'� (.�*"��� �(+,

�+ ( ,"� %�+, +#&-%�,#(' �'� -)��,��

Product Costing and Manufacturing Accounting

2–32 A8.1 (8/97)

ÑÑ Exercises��� ��� ����� � �� �� ��������

A8.1 (8/97) 2–33

Create Simulated Costs

Creating Simulated Costs

�"( ��! (&� '�� �%"�(�' "&'�!� &,&'� '" ����(��'� �"&'& "! � .*��' ��� ��&�&��"( ��! )��* '�� �����' "� �!, ���!��& ,"( *�!' '" �!�"%#"%�'� *�'�"(' ��'�%�!�'�� �%"-�! &'�!��%� �"&'&� �! ����'�"!� ,"( ��! &� (��'� �"&' ���!�� &��!�%�"&�%"��(#&� �& �!, '� �& �& !����� ���"%� ,"( ��!���-� '�� ���!��& �(%�!� '���%"-�! (#��'� #%"��&&�

�"% �+� #��� ,"( ��! (&� &� (��'�� %"��(#& '"�

� �� (��'� �! �!�%��&� �! �'�%��� �"&'&

� �"%���&' '�� � #��' "� ���!��& '" ���"% %�'�&

� �)��"# &'%�'����& �"% #%���!�� �"!'%��'(��� "% ���"% !��"'��'�"!

%��'�!� &� (��'�� �"&'& �"!&�&'& "� '�� �"��"*�!��

� %��'�!� '�� "&'�!� �+��#'�"!& %�#"%'

� %��'�!� � &� (��'�� %"��(#

��� &� (��'�� %"��(# (&�& �!�"% �'�"! �%" '�� �"��"*�!� '����& '" ��!�%�'��"&'&�

�������������

�������� �������

���(�& �%" ��!(���'(%�!� "!&'�!'& �!����'� *��'��%

")�%���� &�"(�� �� �!��(��� �! �"&' �" #"!�!'

����(��'�"!&�

���� ����� ����

��������

��� %"��(# #%"�%� (&�& �"���% � "(!'& �!� #�%��!'���&

�"% '�� ����(��'�"! "� ���"%� ����!�� �!� ")�%���� �"&'&�

������ ������ ������� "(%& %�$(�%�� �"% ���� "#�%�'�"! �!� �%�* &�-� )��(�&

�%� �%" '�� �"('�!� ��&'�% '�����

��� �� �������� ������

�������

��� ���� "� ��'�%��� '���� #%")���& �!�"% �'�"! "! '��

�'�%��� %�$(�%�� �' ���� ��)�� "� '�� �����

Product Costing and Manufacturing Accounting

2–34 A8.1 (8/97)

���� �� �� ������ ��� ���� ����� ����� ��� ���� ����� ��� ��������� �����

��� ������� �����������

��� �������� ���� ����� ������� ���� ��� ����� �� ��� ��� ���������� �� ������ �� �� ��� ������ ������ ���� �� �������� �� ���� � �� � ����� ���� ��� ��� �����������

Creating the Costing Exceptions Report