Embed Size (px)

Citation preview

Roadmap Localization & AEC Game Plan

30 September 2015 | Xenia Hotel, Clark Freeport Philippines

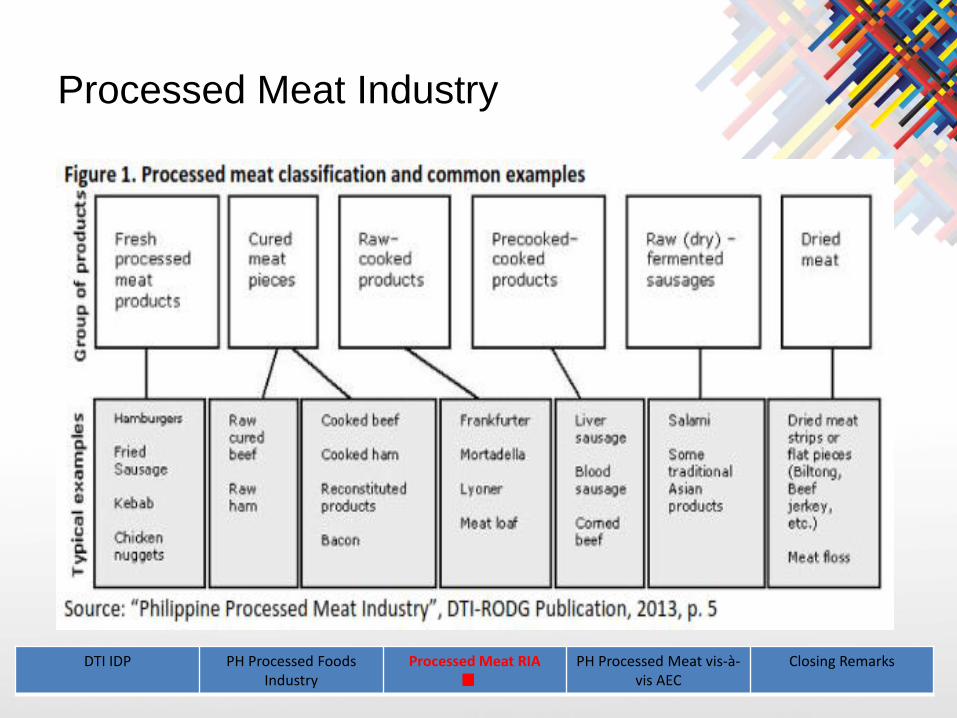

PROCESSED MEAT

INDUSTRY

JUDITH P. ANGELES

Regional Director, DTI-3

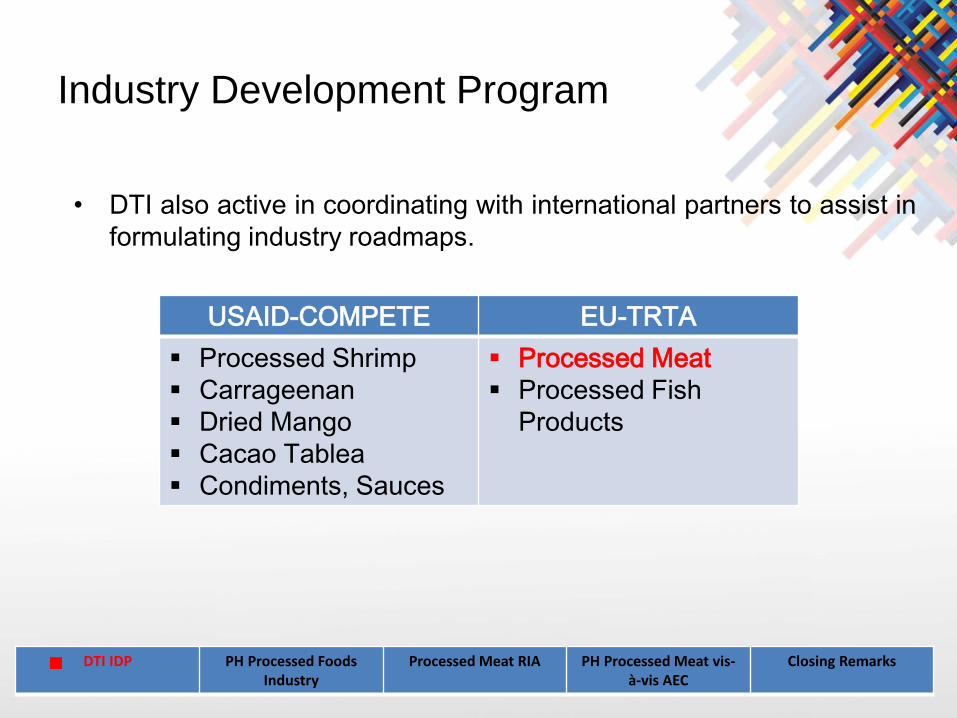

Industry Development Program

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

USAID-COMPETE EU-TRTA

Processed Shrimp

Carrageenan

Dried Mango

Cacao Tablea

Condiments, Sauces

Processed Meat

Processed Fish

Products

• DTI also active in coordinating with international partners to assist in

formulating industry roadmaps.

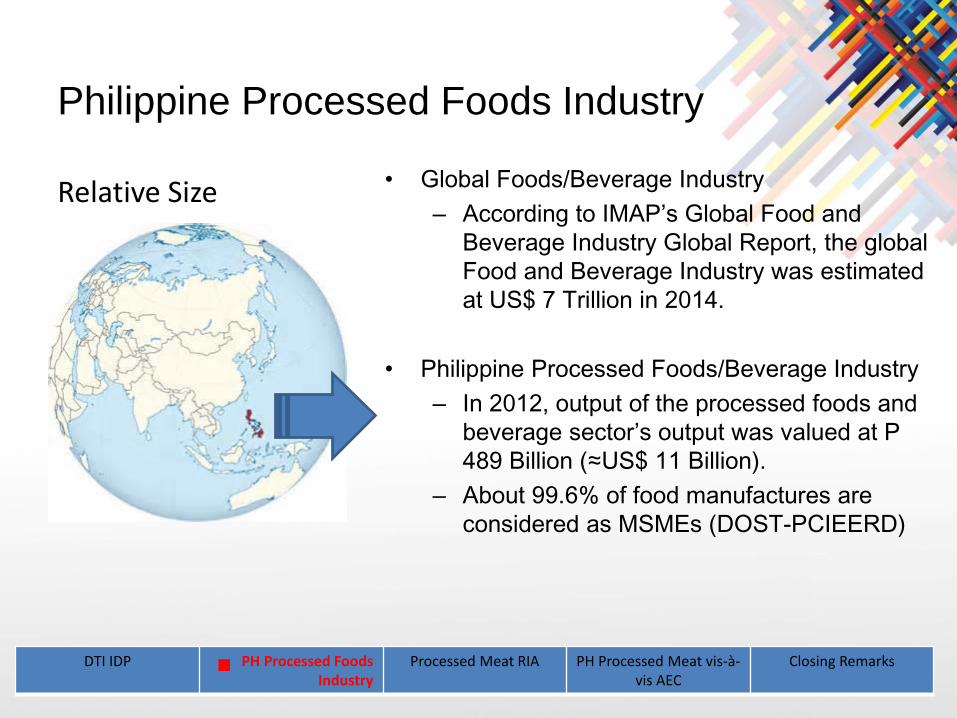

Philippine Processed Foods Industry

Relative Size • Global Foods/Beverage Industry

– According to IMAP’s Global Food and

Beverage Industry Global Report, the global

Food and Beverage Industry was estimated

at US$ 7 Trillion in 2014.

• Philippine Processed Foods/Beverage Industry

– In 2012, output of the processed foods and

beverage sector’s output was valued at P

489 Billion (≈US$ 11 Billion).

– About 99.6% of food manufactures are

considered as MSMEs (DOST-PCIEERD)

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

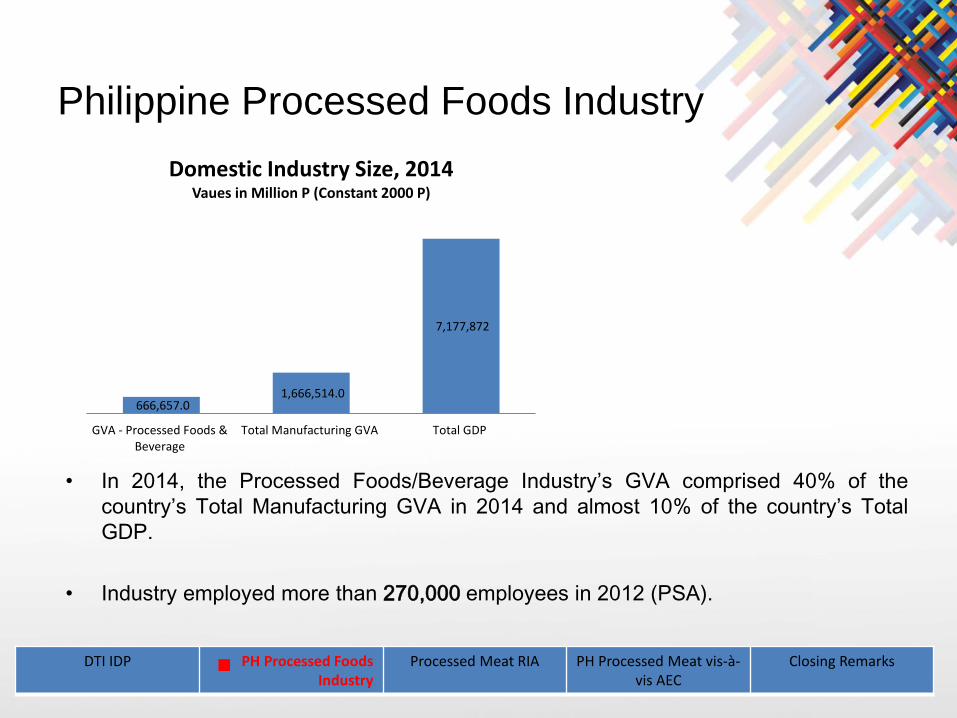

• In 2014, the Processed Foods/Beverage Industry’s GVA comprised 40% of the

country’s Total Manufacturing GVA in 2014 and almost 10% of the country’s Total

GDP.

• Industry employed more than 270,000 employees in 2012 (PSA).

666,657.0 1,666,514.0

7,177,872

GVA - Processed Foods &Beverage

Total Manufacturing GVA Total GDP

Domestic Industry Size, 2014Vaues in Million P (Constant 2000 P)

Philippine Processed Foods Industry

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

Philippine Processed Foods Industry

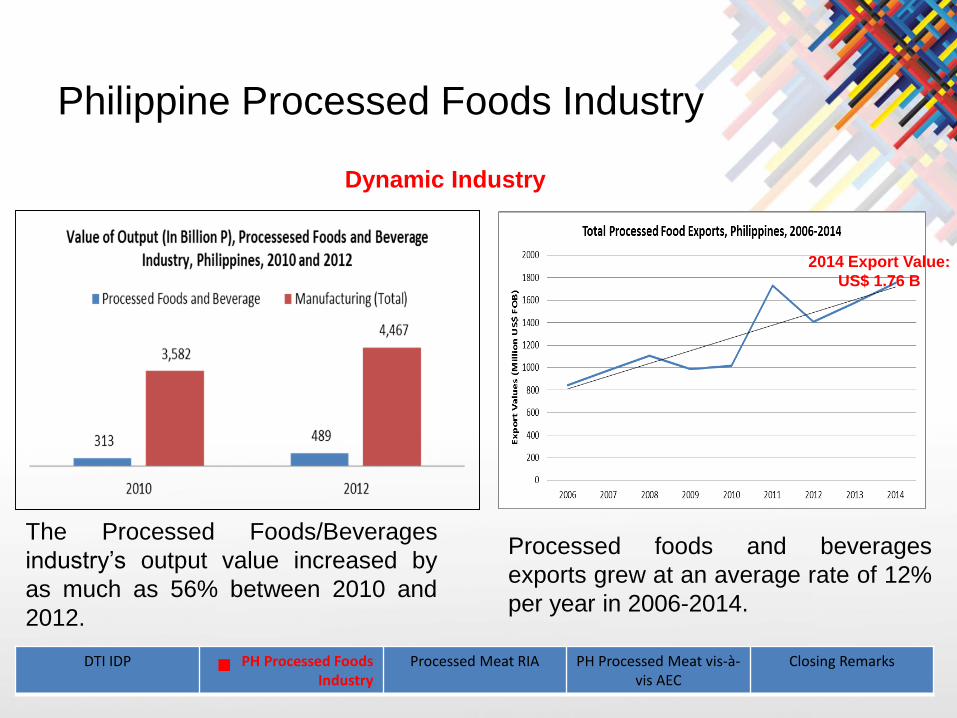

The Processed Foods/Beverages

industry’s output value increased by

as much as 56% between 2010 and

2012.

Processed foods and beverages

exports grew at an average rate of 12%

per year in 2006-2014.

Dynamic Industry

2014 Export Value:

US$ 1.76 B

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

Processed Meat Industry

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

Processed Meat Industry

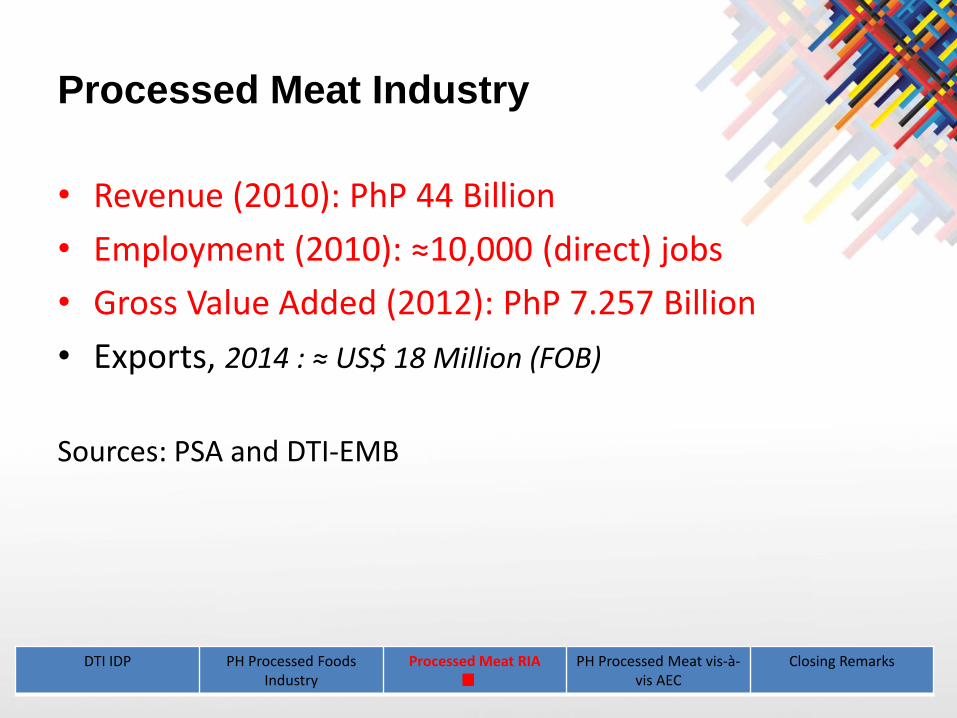

• Revenue (2010): PhP 44 Billion

• Employment (2010): ≈10,000 (direct) jobs

• Gross Value Added (2012): PhP 7.257 Billion

• Exports, 2014 : ≈ US$ 18 Million (FOB)

Sources: PSA and DTI-EMB

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

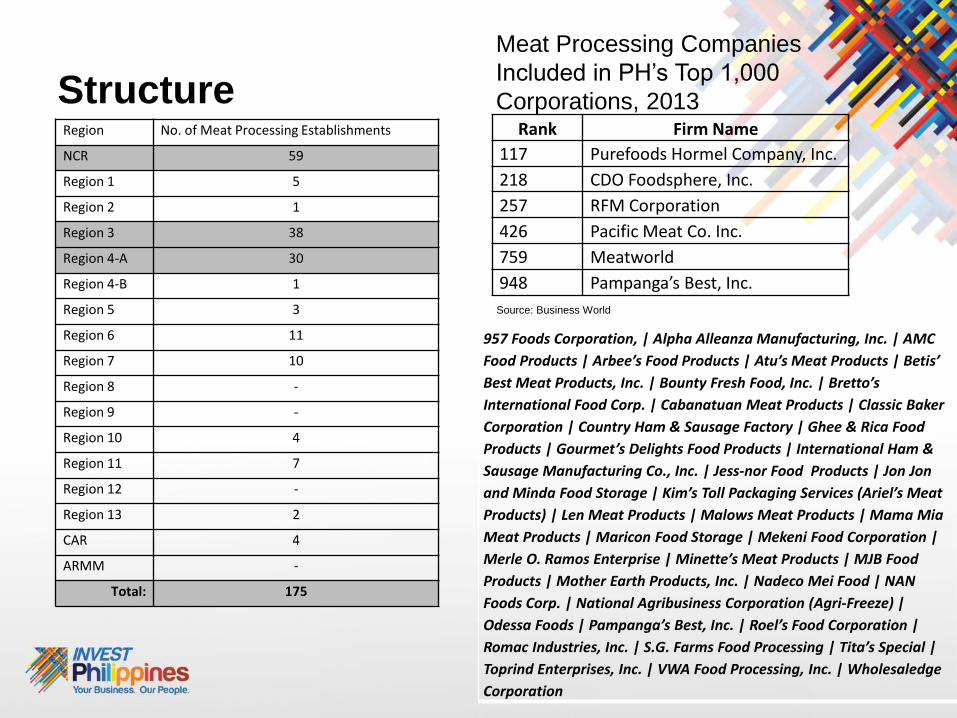

StructureRegion No. of Meat Processing Establishments

NCR 59

Region 1 5

Region 2 1

Region 3 38

Region 4-A 30

Region 4-B 1

Region 5 3

Region 6 11

Region 7 10

Region 8 -

Region 9 -

Region 10 4

Region 11 7

Region 12 -

Region 13 2

CAR 4

ARMM -

Total: 175

957 Foods Corporation, | Alpha Alleanza Manufacturing, Inc. | AMC

Food Products | Arbee’s Food Products | Atu’s Meat Products | Betis’

Best Meat Products, Inc. | Bounty Fresh Food, Inc. | Bretto’s

International Food Corp. | Cabanatuan Meat Products | Classic Baker

Corporation | Country Ham & Sausage Factory | Ghee & Rica Food

Products | Gourmet’s Delights Food Products | International Ham &

Sausage Manufacturing Co., Inc. | Jess-nor Food Products | Jon Jon

and Minda Food Storage | Kim’s Toll Packaging Services (Ariel’s Meat

Products) | Len Meat Products | Malows Meat Products | Mama Mia

Meat Products | Maricon Food Storage | Mekeni Food Corporation |

Merle O. Ramos Enterprise | Minette’s Meat Products | MJB Food

Products | Mother Earth Products, Inc. | Nadeco Mei Food | NAN

Foods Corp. | National Agribusiness Corporation (Agri-Freeze) |

Odessa Foods | Pampanga’s Best, Inc. | Roel’s Food Corporation |

Romac Industries, Inc. | S.G. Farms Food Processing | Tita’s Special |

Toprind Enterprises, Inc. | VWA Food Processing, Inc. | Wholesaledge

Corporation

Meat Processing Companies

Included in PH’s Top 1,000

Corporations, 2013Rank Firm Name

117 Purefoods Hormel Company, Inc.

218 CDO Foodsphere, Inc.

257 RFM Corporation

426 Pacific Meat Co. Inc.

759 Meatworld

948 Pampanga’s Best, Inc.

Source: Business World

Organization

51 company members as of 2014

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

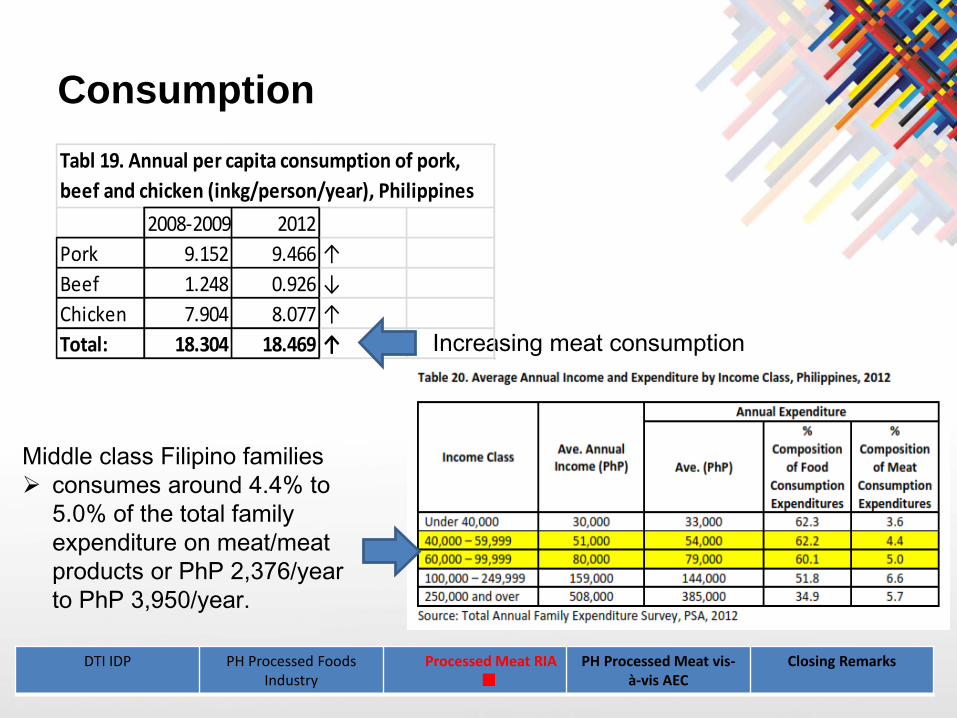

Consumption

Increasing meat consumption

2008-2009 2012

Pork 9.152 9.466 ↑

Beef 1.248 0.926 ↓

Chicken 7.904 8.077 ↑

Total: 18.304 18.469 ↑

Tabl 19. Annual per capita consumption of pork,

beef and chicken (inkg/person/year), Philippines

Middle class Filipino families

consumes around 4.4% to

5.0% of the total family

expenditure on meat/meat

products or PhP 2,376/year

to PhP 3,950/year.

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

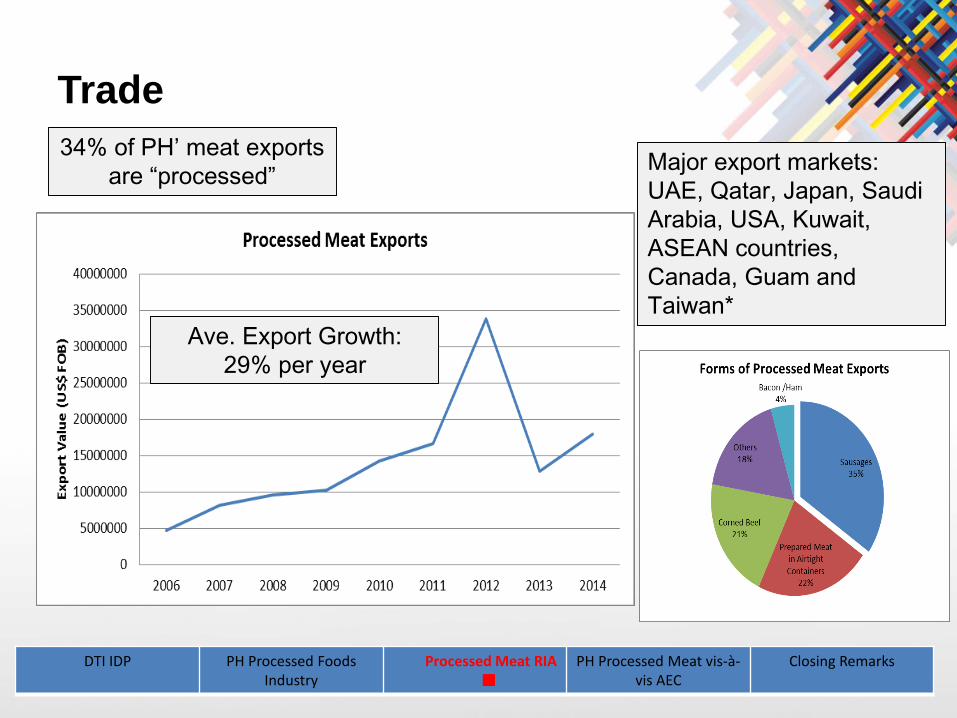

Trade

Major export markets:

UAE, Qatar, Japan, Saudi

Arabia, USA, Kuwait,

ASEAN countries,

Canada, Guam and

Taiwan*

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

Ave. Export Growth:

29% per year

34% of PH’ meat exports

are “processed”

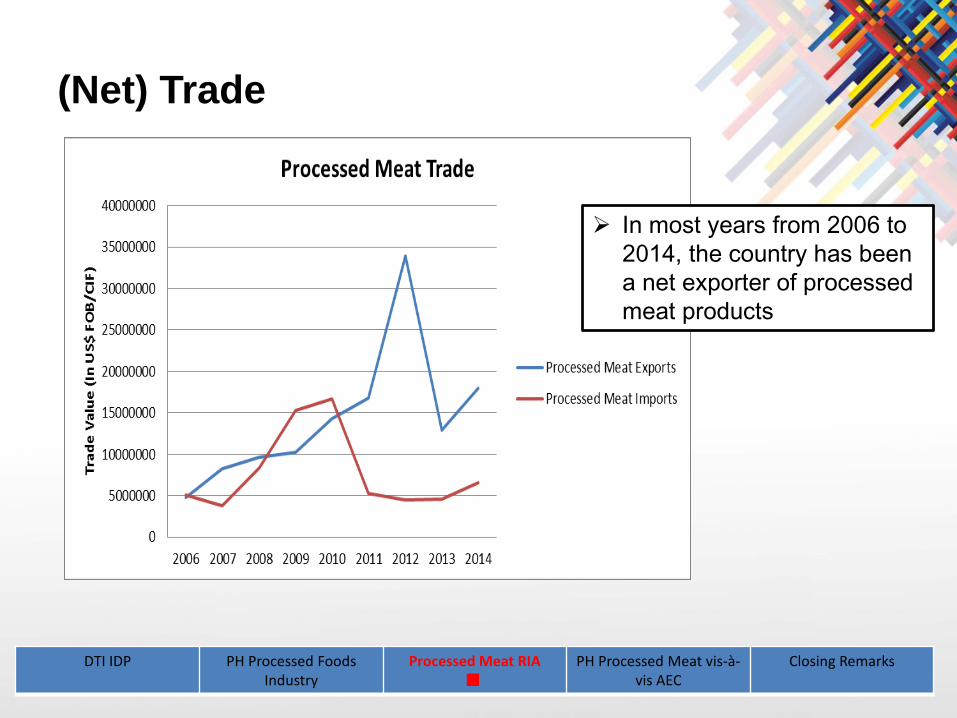

(Net) Trade

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

In most years from 2006 to

2014, the country has been

a net exporter of processed

meat products

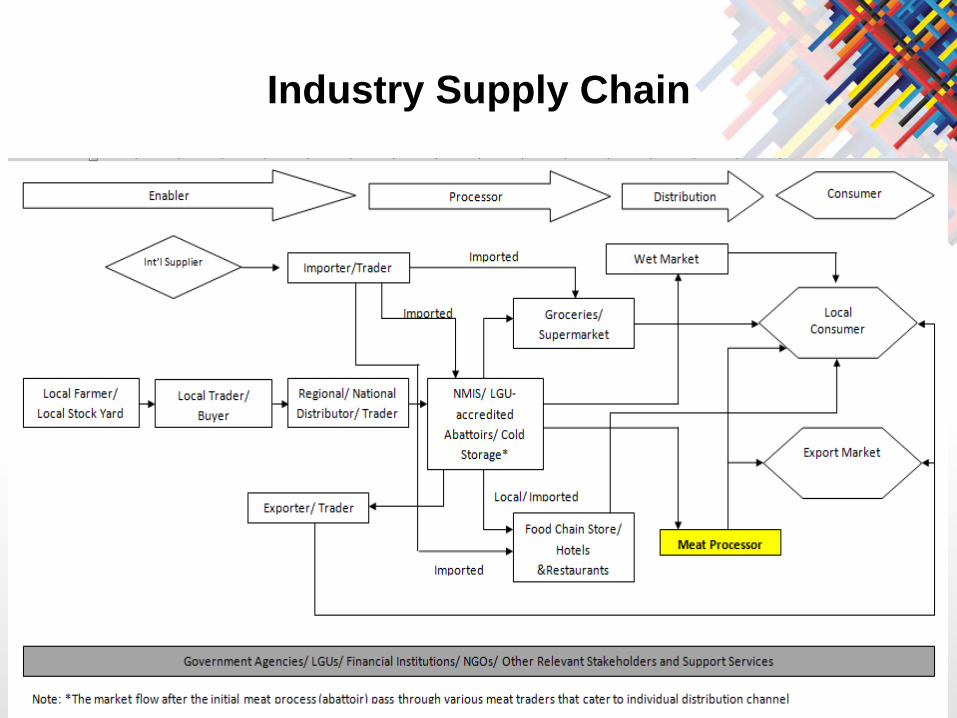

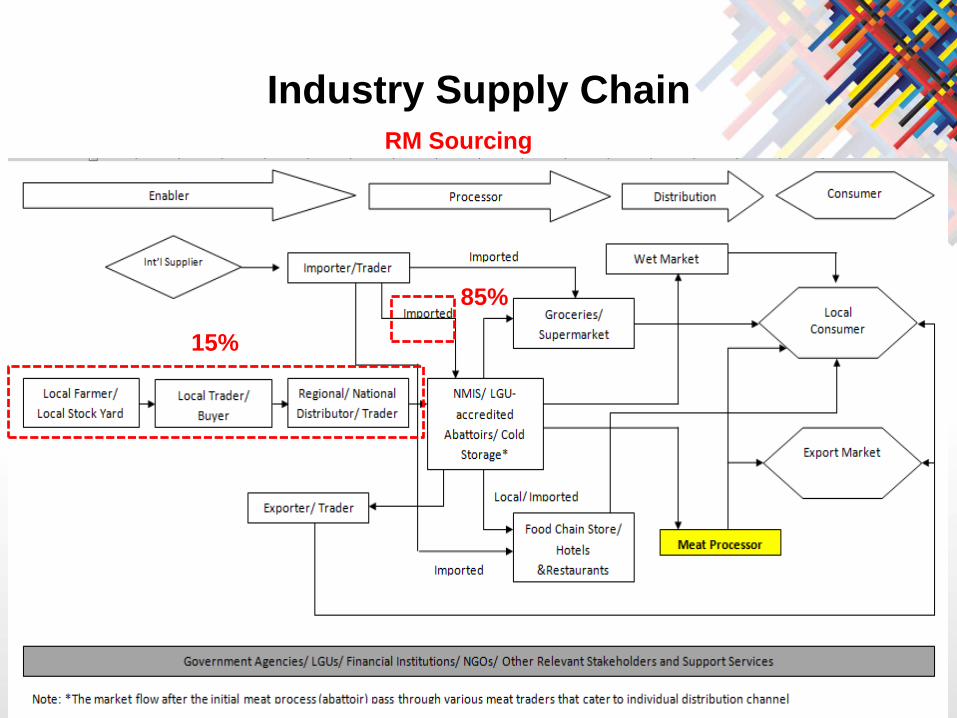

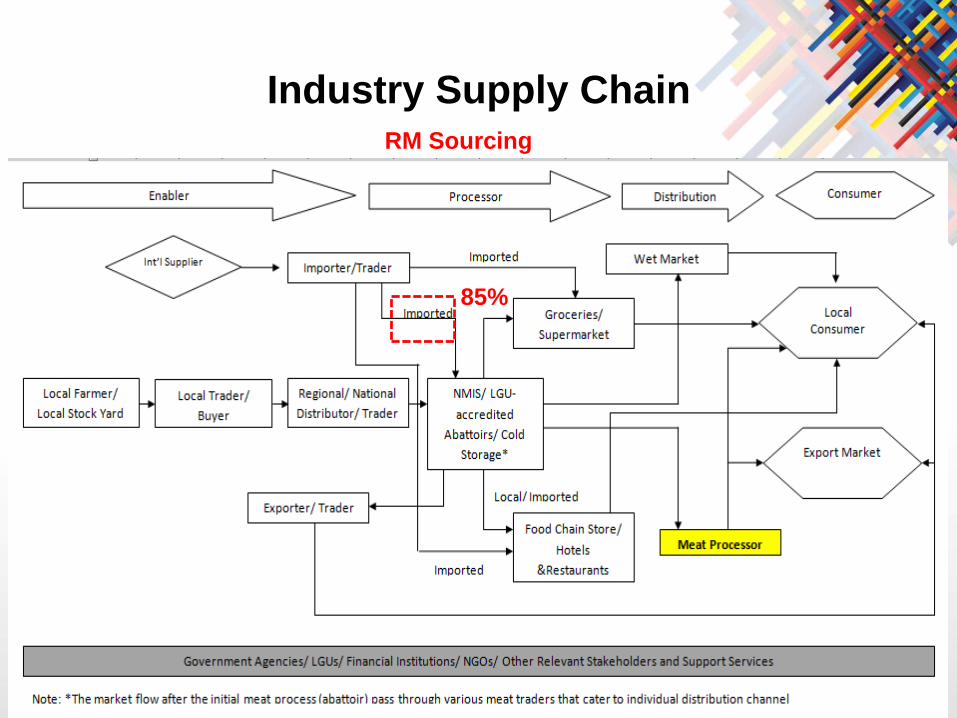

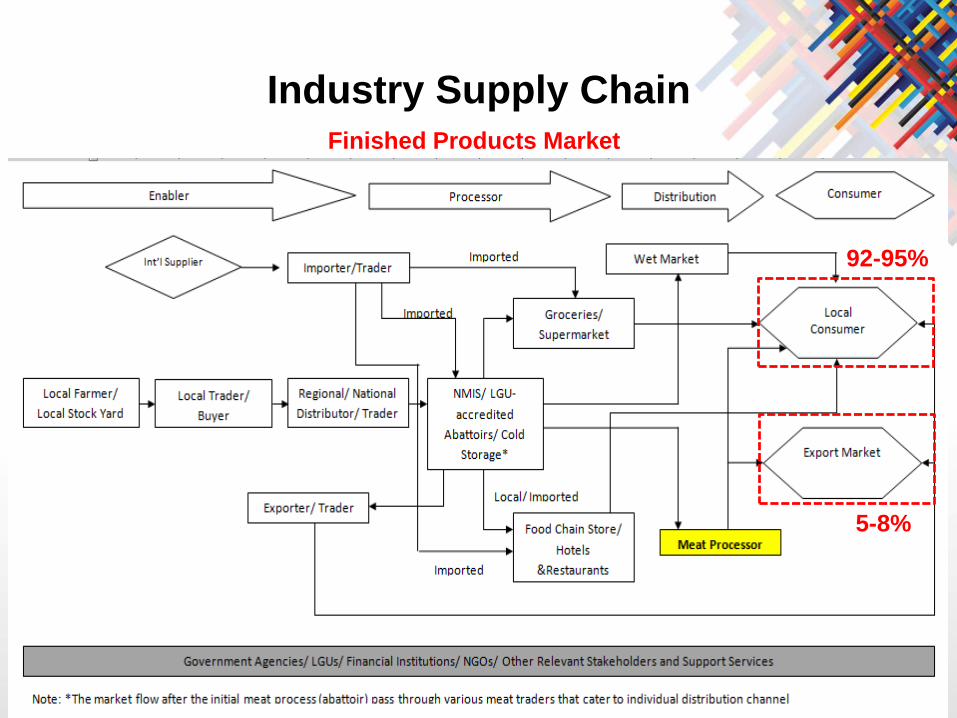

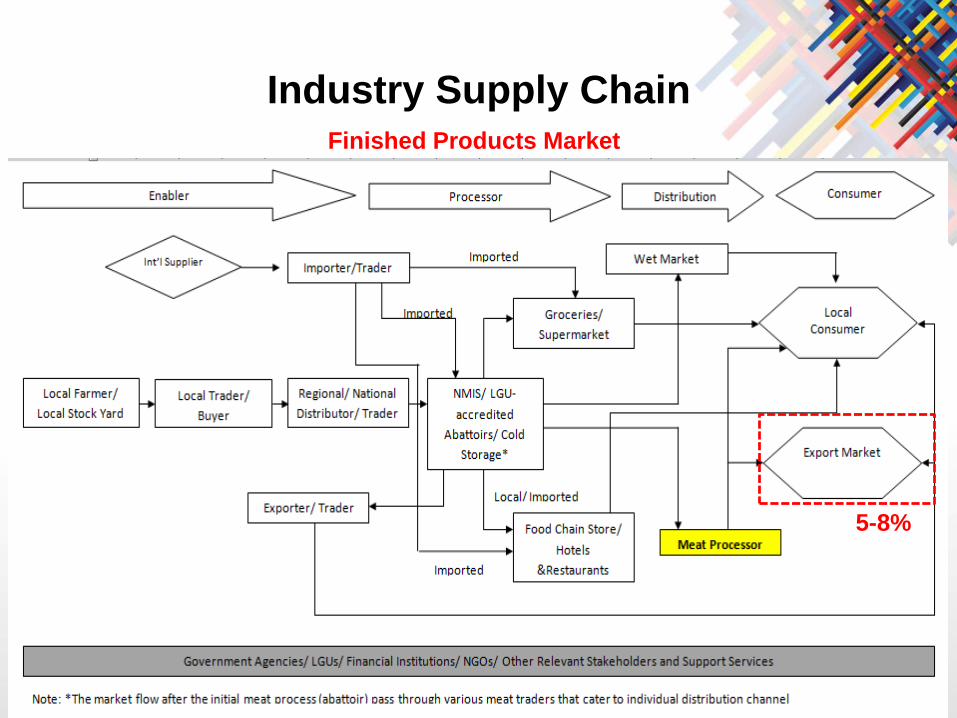

Industry Supply Chain

Industry Supply Chain

15%

85%

RM Sourcing

Industry Supply Chain

85%

RM Sourcing

Industry Supply Chain

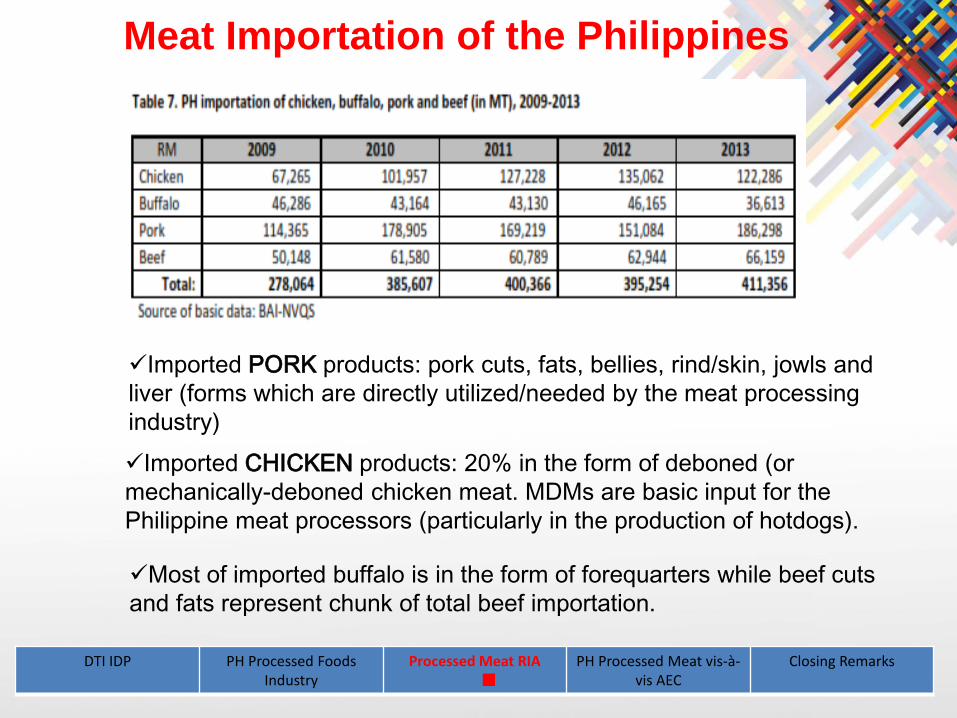

Meat Importation of the Philippines

Imported PORK products: pork cuts, fats, bellies, rind/skin, jowls and

liver (forms which are directly utilized/needed by the meat processing

industry)

Imported CHICKEN products: 20% in the form of deboned (or

mechanically-deboned chicken meat. MDMs are basic input for the

Philippine meat processors (particularly in the production of hotdogs).

Most of imported buffalo is in the form of forequarters while beef cuts

and fats represent chunk of total beef importation.

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

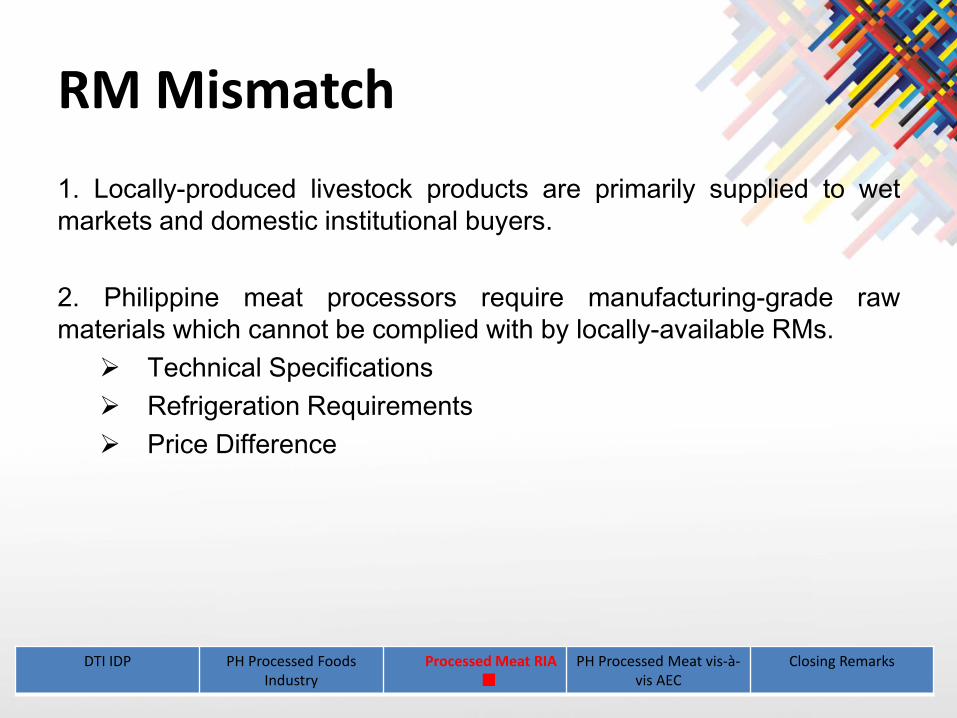

RM Mismatch

1. Locally-produced livestock products are primarily supplied to wet

markets and domestic institutional buyers.

2. Philippine meat processors require manufacturing-grade raw

materials which cannot be complied with by locally-available RMs.

Technical Specifications

Refrigeration Requirements

Price Difference

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

Industry Supply Chain

5-8%

92-95%

Finished Products Market

Industry Supply ChainFinished Products Market

5-8%

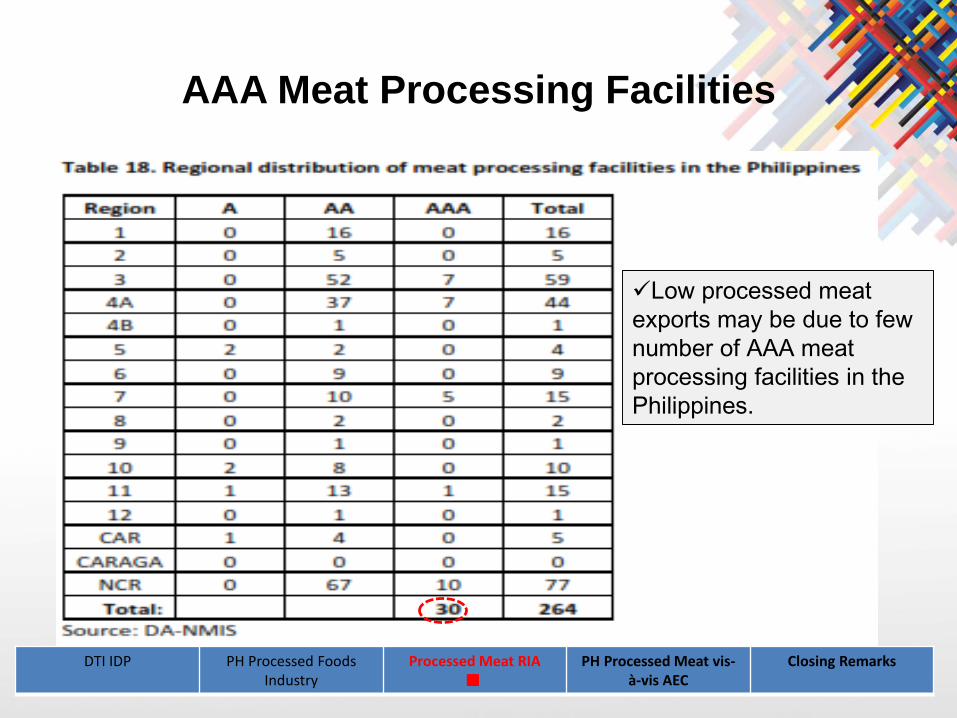

AAA Meat Processing Facilities

Low processed meat

exports may be due to few

number of AAA meat

processing facilities in the

Philippines.

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

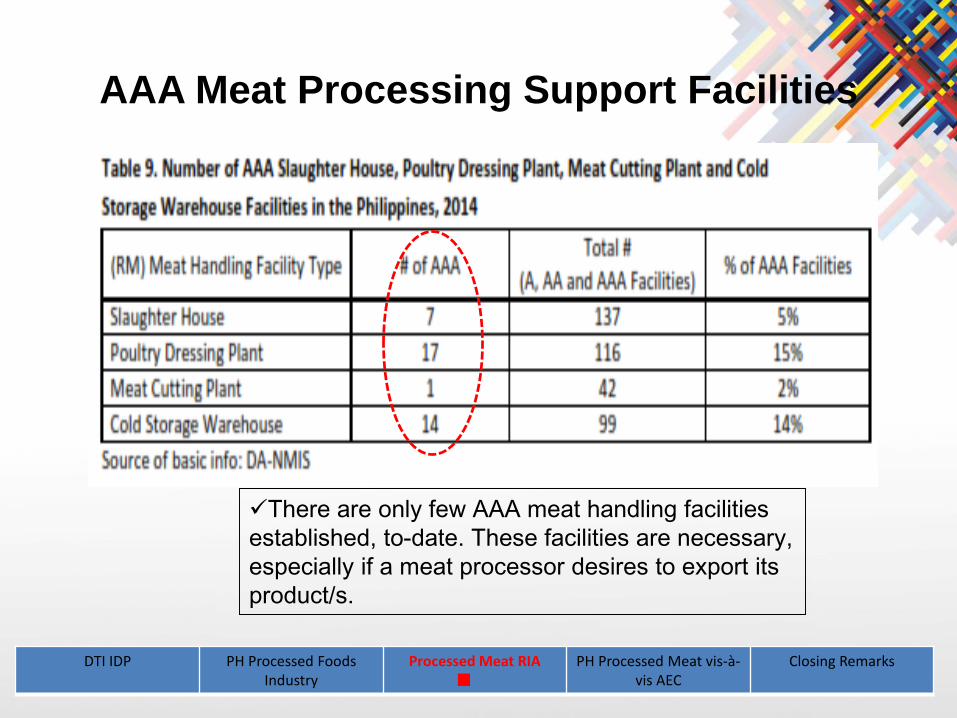

AAA Meat Processing Support Facilities

There are only few AAA meat handling facilities

established, to-date. These facilities are necessary,

especially if a meat processor desires to export its

product/s.

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

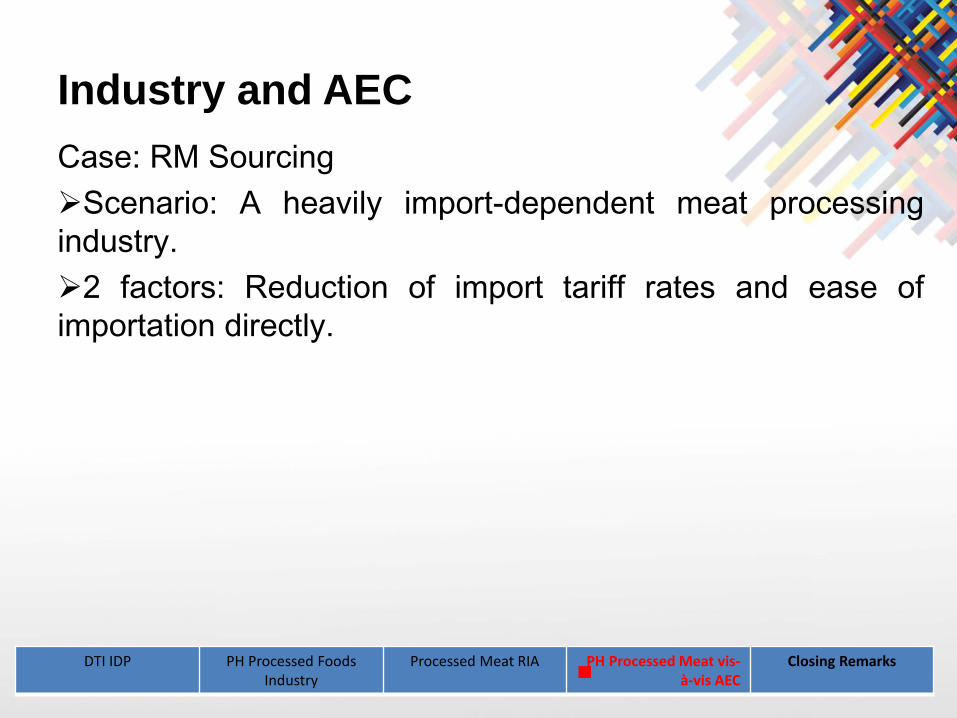

Industry and AEC

Case: RM Sourcing

Scenario: A heavily import-dependent meat processing

industry.

2 factors: Reduction of import tariff rates and ease of

importation directly.

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

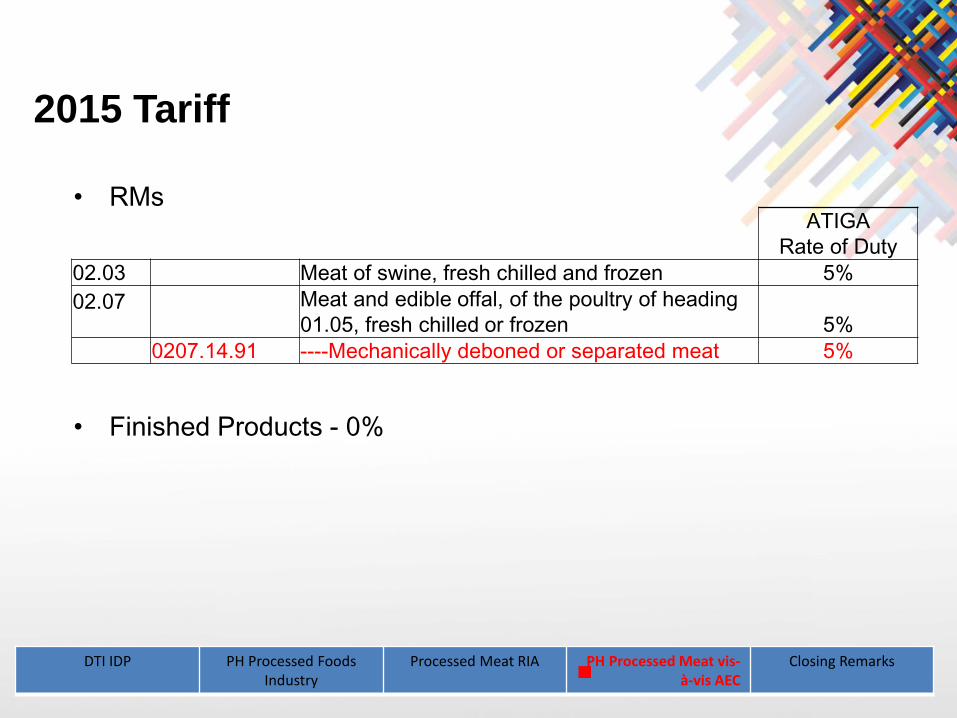

2015 Tariff

• RMs

• Finished Products - 0%

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

ATIGA

Rate of Duty

02.03 Meat of swine, fresh chilled and frozen 5%

02.07 Meat and edible offal, of the poultry of heading

01.05, fresh chilled or frozen 5%

0207.14.91 ----Mechanically deboned or separated meat 5%

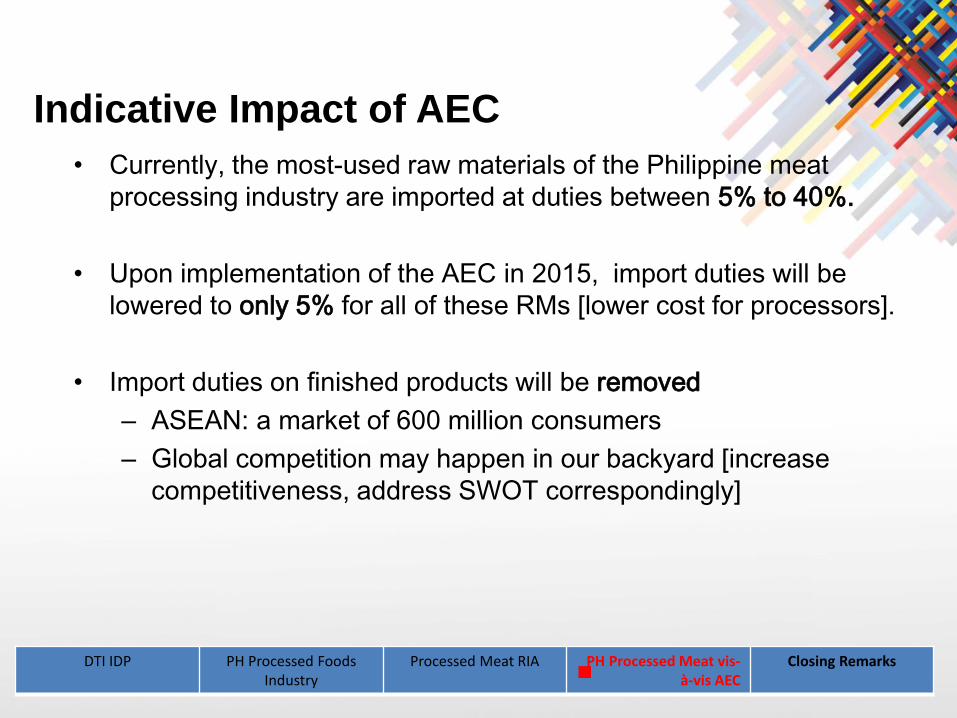

Indicative Impact of AEC

• Currently, the most-used raw materials of the Philippine meat

processing industry are imported at duties between 5% to 40%.

• Upon implementation of the AEC in 2015, import duties will be

lowered to only 5% for all of these RMs [lower cost for processors].

• Import duties on finished products will be removed

– ASEAN: a market of 600 million consumers

– Global competition may happen in our backyard [increase

competitiveness, address SWOT correspondingly]

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

UA&P Study: RM Industry

• Derived Wholesale Price vs. Domestic Wholesale Price

• At current level of tariff: mostly competitive for pork and pork

products and chicken leg quarters

• At 0% MFN: mostly not-competitive

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

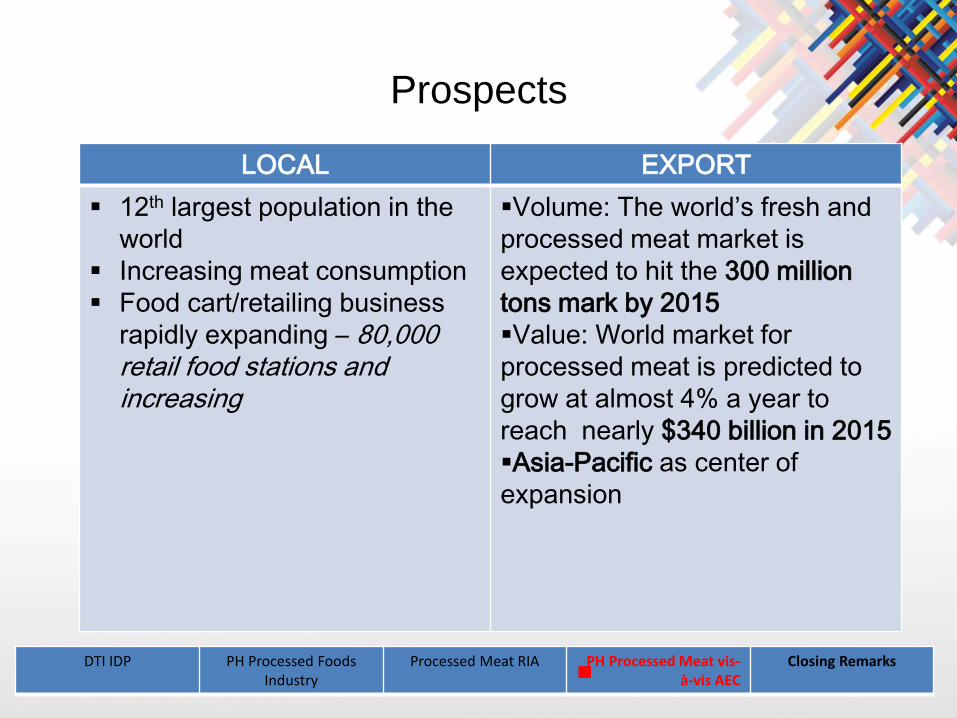

Prospects

LOCAL EXPORT

12th largest population in the

world

Increasing meat consumption

Food cart/retailing business

rapidly expanding – 80,000 retail food stations and increasing

Volume: The world’s fresh and

processed meat market is

expected to hit the 300 million

tons mark by 2015

Value: World market for

processed meat is predicted to

grow at almost 4% a year to

reach nearly $340 billion in 2015

Asia-Pacific as center of

expansion

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

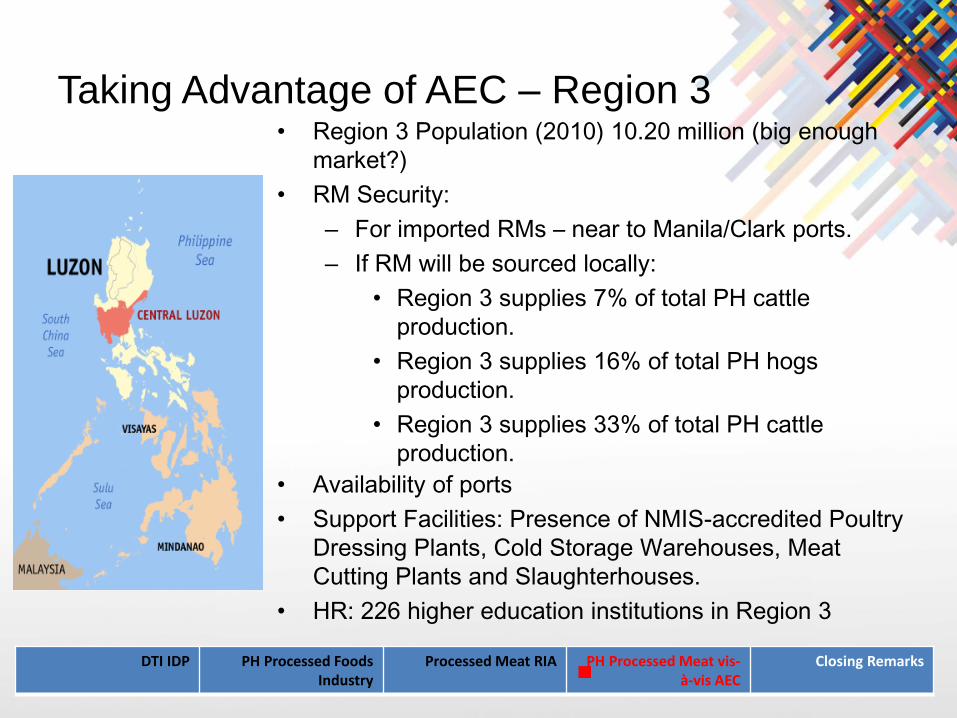

Taking Advantage of AEC – Region 3• Region 3 Population (2010) 10.20 million (big enough

market?)

• RM Security:

– For imported RMs – near to Manila/Clark ports.

– If RM will be sourced locally:

• Region 3 supplies 7% of total PH cattle

production.

• Region 3 supplies 16% of total PH hogs

production.

• Region 3 supplies 33% of total PH cattle

production.

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

• Availability of ports

• Support Facilities: Presence of NMIS-accredited Poultry

Dressing Plants, Cold Storage Warehouses, Meat

Cutting Plants and Slaughterhouses.

• HR: 226 higher education institutions in Region 3

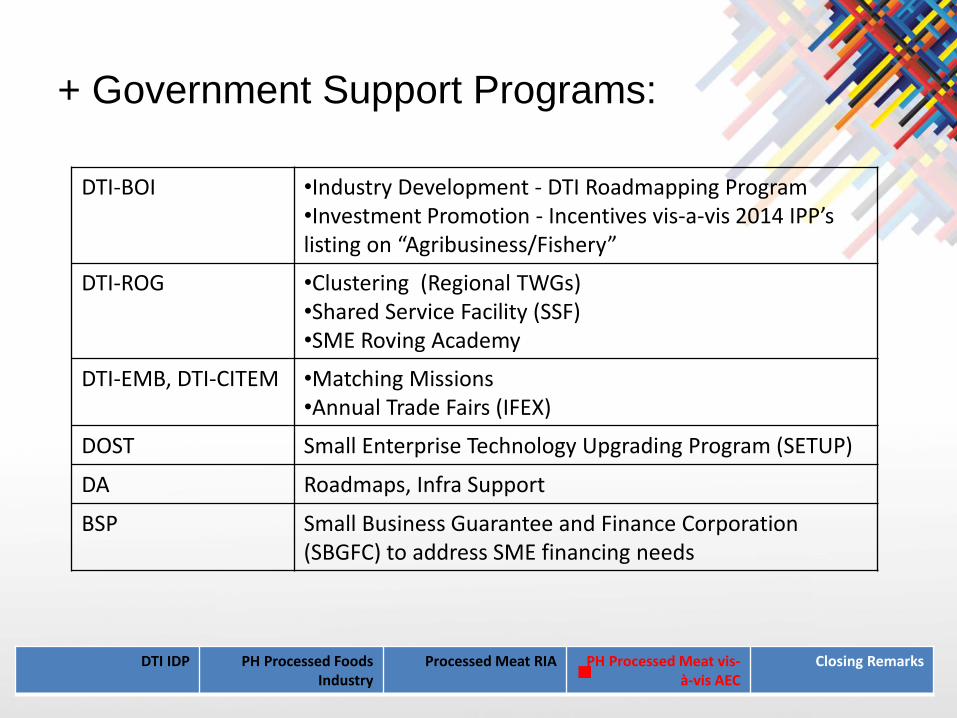

+ Government Support Programs:

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

DTI-BOI •Industry Development - DTI Roadmapping Program•Investment Promotion - Incentives vis-a-vis 2014 IPP’s listing on “Agribusiness/Fishery”

DTI-ROG •Clustering (Regional TWGs)•Shared Service Facility (SSF)•SME Roving Academy

DTI-EMB, DTI-CITEM •Matching Missions•Annual Trade Fairs (IFEX)

DOST Small Enterprise Technology Upgrading Program (SETUP)

DA Roadmaps, Infra Support

BSP Small Business Guarantee and Finance Corporation (SBGFC) to address SME financing needs

Some additional interventions needed:

• Food Safety (RA 10611, Food Safety Act of 2013)

• Competitive livestock and poultry industries (DA)

• Establishment of additional/new support facilities

– Sufficient Poultry Dressing Plants (many AAA-accredited)

– AAA Meat Cutting Plants

– AAA Slaughterhouses

– Additional Cold Storage Warehouses

• Predictable and transparent import regulations (RMs)

• Country-specific export market promotion approach

– Identification of competent national authority (EU)

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks

Concluding Remarks

• Roadmap Acceptance (Target: Not later than December 2015)

• Implementation

• Areas for enhancement:

Comprehensive value/supply chain analysis

Benchmark (Comparative) Study [goal: optimize the country’s

position in the regional/global value chain and facilitate the

country’s integration into the international and regional trading

and investment system]

Investment opportunity studies within or related to the industry

Role of Regions (Region 3)

DTI IDP PH Processed Foods Industry

Processed Meat RIA PH Processed Meat vis-à-vis AEC

Closing Remarks