Embed Size (px)

Citation preview

Vaduz

«Private Label Funds» (PLFs) Tailor-made investment fund solutions for family assets Liechtenstein offers interesting solutions

Agenda

Part I – Private Label Funds and family foundations

1) Needs of family wealth / FO / trusts / foundations

2) Basics of Private Label Funds

3) Private Label Funds in detail

Part II – Concrete example of a Private Label Fund for UHNWI

1) Sub-funds and delegation to different asset managers

2) Fund-prospectus: The central document

3) Reporting of a Private Label Fund

Part III – Liechtenstein and LGT

Part IV – Summary, contacts and legal information

© LGT 2

Part I – Private Label Funds and family foundations

3

Needs of family wealth / FO / trusts / foundations

© LGT

Family wealth / FO / trusts / foundations have a need for …

a general consolidation of assets in a single structure (also with illiquid assets);

protection against splitting of the company and against fragmentation of investments;

a solution for family branches which face different regulatory and particular tax requirements (different domiciles of family members);

a consolidation of existing asset management mandates at several banks (if regulatory requirements

are met you can keep existing bank accounts)

allowing for different levels and forms (e.g. income or capital gains) of wealth consumption by different family members;

involving the appropriate third parties (persons or institutions of confidence to act as directors, asset

managers etc.) in managing family assets while maintaining the necessary safeguards and participation;

transparency / benchmarking / comparison of different asset managers;

integrating the specific requirements of the family in the investment or monitoring process;

enhancing privacy and data protection and benefitting from the higher degree of acceptance as well as assurance of disclosure duties which may apply to regulated investment vehicle;

4

© LGT

Family wealth / FO / trusts / foundations may benefit from…

Needs of family wealth / FO / trusts / foundations

control and supervision by independent third parties (auditors, FMA);

a possible limitation of their personal liability risks within the regulatory framework as members of the board of trustees;

the establishment of a well-structured long-term framework to carry out investments and entrepreneurial activities – also after the death of the original founder or controlling owner;

an efficient fiscal treatment offered under certain circumstances to regulated investment funds

(value added tax, stamp duties, income taxation, use of double taxation agreement);

the possibility to enable charity subject to specific conditions (e.g. performance fee in favor of charitable purposes);

… many more advantages.

5

Basics of Private Label Funds

6

Basics of Private Label Funds

What are Private Label Funds (PLFs)?

Investment funds: A collective investment vehicle which may belong to numerous investors and is managed by a professional fund management company (supervised by the FMA).

Private Label Funds are just tailor-made investment funds.

Name (label) of the fund and particulars are determined by the fund promoter

© LGT

Supervisory Authority

AIFM / Management Company Depositary (bank)

Auditor Private Label Fund Asset manager

Promoter of the fund

Investor

Asset management agreement

Cooperation agreement

Audit Under trusteeship

Investment

Investment decision

Depositary agreement

Only investments that comply with all regulatory, legal and tax conditions can

be invested in a PLF (or in funds in general)!

7

© LGT

Basics of Private Label Funds

Enhanced Protection of Private Label Funds

Private Label Funds enjoy the same benefits as commercial funds but they are tailored to the needs of the promoter:

PLFs benefit from the same degree of protection as public investment funds but are specifically designed to meet the customer’s needs (type of fund, legal structure, asset classes, allocation, investment strategies, currencies, use of income etc.).

PLFs provide enhanced safeguards due to extensive regulations.

Privacy and data security: PLFs act as legal owner and counterpart in all transactions in the interest of

its investors (who are not personally involved).

Asset protection: The assets and liabilities of a fund are segregated from those of its AIFM/ management company or depositary (off-balance sheet). Separation also applies among sub-funds.

PLFs can provide semiannual and audited annual reports, which are filed with the Financial Market Authority.

PLFs offer various legal forms under private law.

PLFs are generally subject to the same tax rules as public/commercial investment funds in Liechtenstein. PLFs, which qualify as collective investment schemes, do not pay taxes in Liechtenstein (no stamp duties, no withholding taxes in Liechtenstein or the value-added tax). 8

PLFs allow flexibility in asset allocation, investment strategies, investment regions, currencies, multi-manager-solutions, transactions, asset pooling, subscriptions, redemptions etc.

The promoter is free to choose the asset classes held in a PLF (assuming proper NAV calculation is possible and an appropriate legal structure is in place).

More credibility due to the recognition of the PLF’s regulation by various countries. In fact, Liechtenstein is part of the European Economic Area (EEA) and its funds (as European onshore funds) enjoy an enhanced standing.

Convenient transactions: Transactions with a PLF do normally not entail additional amount of effort since the investment funds are regulated

Basics of Private Label Funds

Flexibility characterizing Private Label Funds (PLFs)

© LGT 9

In case the depositary function and administration of the PLF is executed and the asset management is delegated to a third party: The AIFM/management company can represent your interests as a «Trusted Partner».

Private Label Funds:

For invest solutions in accordance with investment fund laws.

Provide flexibility, security and transparency for the fund promoter and investors of the fund.

Basics of Private Label Funds

«Trusted Partner»

© LGT 10

Clients often change the bank if they are dissatisfied with the investment performance and face the need to establish new client relations, provide documentation and negotiate new contracts which is often time-consuming. Within a fund structure the asset manager can be changed easily at the request of the client/fund promoter.

Additional advantages for the client:

The client has to find a sound and stable bank and open a PLF just once. Hence, he only goes through the effort of opening an account once.

Then, the client is free to choose/change the asset manager (while adhering to regulatory requirements) without having to change the bank relationship.

Furthermore, the client can always keep the same relationship.

Basics of Private Label Funds

© LGT

Advantages for clients with a PLF

11

© LGT

Basics of Private Label Funds

Legal basis: Acting in the best interest of the investor

Art. 20 para. 1 lit. a, b and e UCITS law:

The management company shall: – act honestly and fairly in conducting its business activities in the best interest of the UCITS it

manages and the integrity of the market; – act with due skill, care and diligence in the best interests of the UCITS it manages and the

integrity of the market; – act independently and only in the best interest of the investors in accordance with the laws and

constitutive documents.

‘UCITS’ is an Undertaking for Collective Investments in Transferable Securities (acc. to EU directives).

Art. 35 para. 1 lit. b and e AIFM law: The AIFM shall:

– act correctly and fairly in the best interests of the AIF, the investors and the integrity of the market;

– comply with all provisions applicable to the conduct of its activities in the best interest of the AIF, the investors and the integrity of the market.

‘AIF’ is an Alternative Investment Fund (acc. to EU directives).

12

13

Set-up: The foundation / trust for all «contracts», the fund for the asset management

Combination of two structures

The foundation holds the fund

(Private Label Fund) and regulates all agreements (succession plans, distribution of wealth among the beneficiaries).

The PLF holds all (liquid) assets and performs all asset management related tasks.

© LGT

Foundation

Board of directors

Foundation statutes By-laws Protector

Founder

Beneficiary

Fund

Assets / Portfolio

Basics of Private Label Funds

LGT does only provide the PLF (i.e. no trust or foundation business by LGT)

LGT Services

Basics of Private Label Funds

An ideal solution: Foundation / trust and PLF

© LGT

Foundation / trust PLF

Constituting documents/by- laws

Board of Foundation Asset Manager

Co-investors

14

A PLF provides additional options:

– The founder can hold the PLF by the foundation / or the founder can invest directly in the PLF via an outmost convenient subscription / redemption process.

Enhanced flexibility

Prospectus

LGT does only provide the PLF (i.e. no trust or foundation business by LGT)

LGT Services

Private Label Funds in detail

15

Private Label Funds in detail

Fund structures

© LGT

UCITS

Fun

d t

ype

AIF IU

1 2 3

EU/EEA-Passport EU/EEA-Passport No EU/EEA-Passport

AIFM / Management Company

Contractual form / collective trusteeship

Externally managed

Self-managed Variable capital

SICAV

Fixed capital SICAF

Investment company corporate form

FUND Share classes

Umbrella-fund / Stand-alone fund

Master-Feeder-Structures Fun

d s

tru

ctu

res

Professional / qualified investors

16

Private Label Funds in detail

Private Label Fund set-up process

Initial discussion / questionnaire

– Internal audit (due diligence, viability of project)

– Offer and order confirmation are signed by client.

– Cooperation agreement / asset management agreement are signed.

– Documentation obtained from asset manager.

– Prospectus drawn up and signed by the depositary and AIFM / management company.

Auditor takes mandate

Application for authorization submitted to FMA.

Technical set-up: Determine subscription period / launch (among others).

© LGT

Promoter

PWC

FMA

1

2

3

4

1

2

3

4

Quelle: LGT

17

Indicative timeline for fund set-up

UCITS V Alternative Investment Fund (AIF)

Project work LGT (Onboarding asset manager, contracts, sign-off etc.)

approx. 1-5 weeks approx. 1-5 weeks

Review prospectus approx. 2 weeks approx. 2 weeks

FMA (max. time per law)

max. 4 weeks max. 4 weeks

Technical implementation approx. 1-2 weeks approx. 1-2 weeks

TOTAL TIME 6-13 weeks

(normally 7 weeks) 8-13 weeks

(normally 9 weeks)

Minimum requirements

The minimum volume for a Private Label Fund is CHF 20 million. In case of an umbrella-fund, the minimum volume is required for each sub-fund.

The asset manager must be licensed and prudentially supervised.

LGT does not give any seed money to catch up the minimum volume.

Private Label Funds in detail

© LGT 18

There cannot be a conclusive answer here as costs are affected by factors such as volume, asset classes, valuation cycle etc.

Private Label Funds in detail

What does a Private Label Fund cost?

© LGT

One-off costs

Set-up costs CHF 25’000

Authorization fees approx. CHF 750 -5’000

“Existing” costs

Depositary (custodian) approx. 4 - 15 bps

Transaction costs tbd

Incremental costs due to PLF

Fund administration approx. 4 - 10 bps

Auditing costs approx. CHF 10’000

FMA-fees CHF 2’000

A detailed offer can be made once the large questionnaire has been completed.

Likely costs: Approx. 8-25 bps per annum plus third-party costs (FMA fees, auditors etc.)

19

Part II – Concrete example of a Private Label Fund for UHNWI

20

Sub-funds and delegation to different asset managers

© LGT

Different sub-funds of a fund

Funds with several sub-funds offer high individualization, especially for foundations, trusts and family wealth.

Furthermore, they are suitable for family offices.

Advantages of a fund with several sub-funds:

No liability between sub-funds

Sub-funds are segregated and each sub-fund is basically protected in case of over-indebtedness of another sub-fund of the umbrella.

Sub-funds as a structural element (e.g. a family sub-fund)

Sub-funds can be customized regarding investment strategies, allocation, liquidity, risk, fees, etc.

Greater flexibility with investments due to the use of different asset managers in each sub-fund

Customizable transfer of assets

Sub-funds can include different classes and be subject to different risks profiles

PLF (Umbrella-Fund)

Sub-fund 1 Sub-fund 2 Sub-fund 3

«traditional investments»

risk averse investments

e.g. «hedge funds» or investments with

greater risks

family companies, private equity,

real estate

21

Sub-funds and delegation to different asset managers

Clear structure according to the liquidity of the asset classes

© LGT

Private Label Fund

Bond Issues Shares Alternative

Sovereign

Corporate

High Yield

Emerging Markets

North America

Europe

Pacific

Emerging Markets

Hedge Funds

Private Equity

Investors

Cash

22

Sub-Asset Manager

Sub-Asset Manager

Sub-Asset Manager

Sub-Asset Manager

LGT Fund Management Company Ltd.

PWC Auditor

LGT Bank AG Depositary

Lead Asset Manager

Asset Management Agreement

Sub-Asset Management Agreement Sub-Asset Management

Agreement

Sub-Asset Management Agreement

Sub-Asset Management Agreement

Administration

Management Segregated

Account

Management Segregated

Account Management Segregated

Account Management Segregated

Account

Dynamic Global Endowment Fund

FqA

Sub-funds and delegation to different asset managers

Fund structure with delegations

© LGT 23

Fund-prospectus: The central document

24

25

Fund-prospectus: The central document

Prospectus: The entire information, e.g. investment policy

© LGT

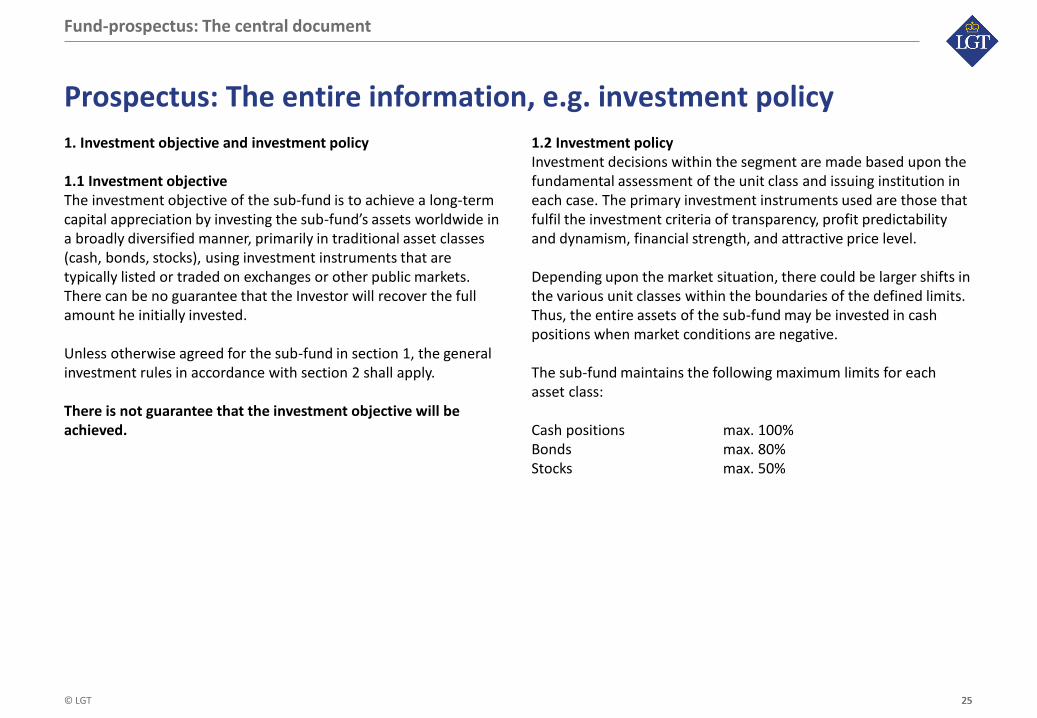

1. Investment objective and investment policy 1.1 Investment objective The investment objective of the sub-fund is to achieve a long-term capital appreciation by investing the sub-fund’s assets worldwide in a broadly diversified manner, primarily in traditional asset classes (cash, bonds, stocks), using investment instruments that are typically listed or traded on exchanges or other public markets. There can be no guarantee that the Investor will recover the full amount he initially invested. Unless otherwise agreed for the sub-fund in section 1, the general investment rules in accordance with section 2 shall apply. There is not guarantee that the investment objective will be achieved.

1.2 Investment policy Investment decisions within the segment are made based upon the fundamental assessment of the unit class and issuing institution in each case. The primary investment instruments used are those that fulfil the investment criteria of transparency, profit predictability and dynamism, financial strength, and attractive price level. Depending upon the market situation, there could be larger shifts in the various unit classes within the boundaries of the defined limits. Thus, the entire assets of the sub-fund may be invested in cash positions when market conditions are negative. The sub-fund maintains the following maximum limits for each asset class: Cash positions max. 100% Bonds max. 80% Stocks max. 50%

25

Fund-prospectus: The central document

Prospectus: The entire information, e.g. basic information

© LGT

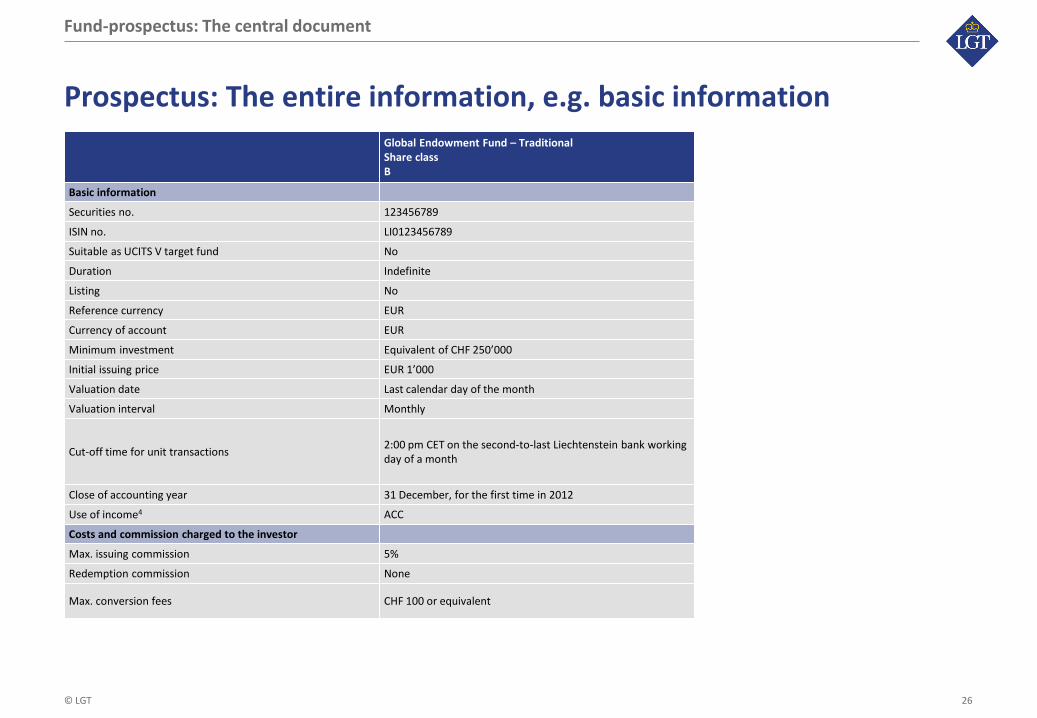

Global Endowment Fund – Traditional Share class

B

Basic information

Securities no. 123456789

ISIN no. LI0123456789

Suitable as UCITS V target fund No

Duration Indefinite

Listing No

Reference currency EUR

Currency of account EUR

Minimum investment Equivalent of CHF 250’000

Initial issuing price EUR 1’000

Valuation date Last calendar day of the month

Valuation interval Monthly

Cut-off time for unit transactions 2:00 pm CET on the second-to-last Liechtenstein bank working day of a month

Close of accounting year 31 December, for the first time in 2012

Use of income4 ACC

Costs and commission charged to the investor

Max. issuing commission 5%

Redemption commission None

Max. conversion fees CHF 100 or equivalent

26

Reporting Possibilities of a Private Label Fund

27

28

Reporting of a Private Label Fund

Reporting

© LGT

Model of institutional reporting

Mo

nth

ly

Performance, return- and Risk-indicator

Performance attribution

Qu

arte

rly

An

nu

ally

Qualitative reporting

Performance review

28

29

Reporting of a Private Label Fund

Reporting

© LGT

Price and Volume (As of: 31/12/2016)

Net asset value per share USD 1,195.12

12-month high (end of month data) USD 1,209.17

12-month low (end of month data) USD 1,172.08

Returns Fund Benchmark

Last month 1.97% -0.63%

Last 3 months 1.97% 0.72%

Last 12 months 1.86% -0.35%

Last 24 months p.a. 4.09% 1.49%

Last 36 months p.a. 6.12% 3.94%

Last 60 months p.a. – –

Since inception p.a. (31/03/2012) 4.87% 3.50%

Year-to-date 1.86% -0.35%

Maximum monthly return 3.74% 2.18%

Minimum monthly return -3.07% -1.91%

Risk and performance Fund Benchmark

Volatility p.a. 4.10% 3.50%

Sharpe ratio 1.48 1.11

Tracking error 4.88%

Information ratio 0.45

Correlation 0.18

Active return p.a. 2.18%

Beta 0.21

Maximum draw down -3.07% -4.68%

Maximum draw down period (months) 1 4

Calculation: Rolling window of 36 months. Average risk free rate p.a.: 0.05%

29

30

Reporting of a Private Label Fund

Reporting

© LGT

0.0

0%

0.0

0%

-3.0

7%

0.0

0%

0.0

0%

1.9

7%

0.2

1%

-1.8

7%

-1.9

1%

0.9

4%

0.4

2%

-0.6

3%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

07/15 08/15 09/15 10/15 11/15 12/15

Monthly Returns Annual Returns

0.0

0%

10

.30

%

6.3

6%

1.8

6%

1.3

3%

9.0

0%

3.3

7%

-0.3

5%

-5.0%

0.0%

5.0%

10.0%

15.0%

(03/12 - 12/12) 2013 2014 2015

Performance (rebased) 31/03/2012 – 31/12/2015

92.096.0

100.0104.0108.0112.0116.0120.0124.0

03

.12

05

.12

07

.12

09

.12

11

.12

01

.13

03

.13

05

.13

07

.13

09

.13

11

.13

01

.14

03

.14

05

.14

07

.14

09

.14

11

.14

01

.15

03

.15

05

.15

07

.15

09

.15

11

.15

30

31

Reporting of a Private Label Fund

Reporting

© LGT

Client Fund Traditional (EUR)

37.85%

26.32%

17.09%

8.26%

4.00%

6.48%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00%

USD

EUR

CHF

JPY

GBP

Others

33.49%

20.52%

14.22%

6.51%

4.37%

4.09%

2.54%

2.27%

11.99%

0.00% 10.00% 20.00% 30.00% 40.00% 50.00%

Luxembourg*

Switzerland*

Switzerland

United States

Japan

Japan*

n.a.

United Kingdom

Others

Risk Currencies Risk Countries

* Emitee country because no risk country is available

31

Part III – Liechtenstein and LGT

32

Liechtenstein and LGT

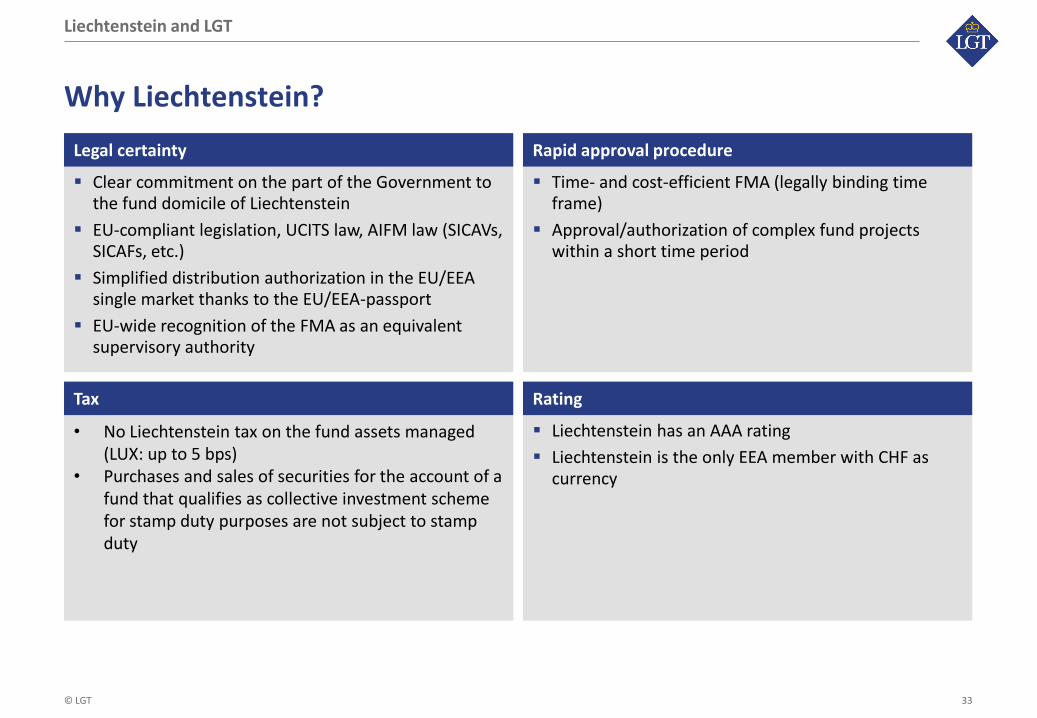

Why Liechtenstein?

© LGT

Time- and cost-efficient FMA (legally binding time frame)

Approval/authorization of complex fund projects within a short time period

• No Liechtenstein tax on the fund assets managed (LUX: up to 5 bps)

• Purchases and sales of securities for the account of a fund that qualifies as collective investment scheme for stamp duty purposes are not subject to stamp duty

Liechtenstein has an AAA rating

Liechtenstein is the only EEA member with CHF as currency

Clear commitment on the part of the Government to the fund domicile of Liechtenstein

EU-compliant legislation, UCITS law, AIFM law (SICAVs, SICAFs, etc.)

Simplified distribution authorization in the EU/EEA single market thanks to the EU/EEA-passport

EU-wide recognition of the FMA as an equivalent supervisory authority

Tax Rating

Legal certainty Rapid approval procedure

33

Part IV – Summary, contacts and legal information

34

Segregation and supervision: PLFs are off-balance sheet, have FMA supervision and PWC audit.

Privacy and data security: The PLF acts as legal owner and counterparty in all transactions in the interest of its investors (who are not personally involved).

LGT as «Trusted Partner» Control: Bound by the provisions of the prospectus, LGT is obligated to monitor and check all the

specifications.

Only investments that comply with all regulatory, legal and tax requirements can be invested in a PLF!

→ Private Label Funds (PLF): tailor-made in accordance with investment fund laws

Summary, contacts and legal information

© LGT

Private Label Funds: tailor-made investment fund solutions

Privacy and data security

Segregation and supervision

Trusted Partner Control

Customer needs

35

Summary, contacts & legal information

Contacts for your private label solution

Dr. Stefan Lindemann, LL.M. CEO LGT Fund Management Company Ltd. Tel. +423 235 2253 [email protected]

© LGT

Thomas Marte, LL.M. Investment Fund Solutions Tel. +423 235 2837 [email protected]

Dr. Susanne Fabjan Investment Fund Solutions Tel. +423 235 1760 [email protected]

36

Legal information This document is intended solely for the recipient and may not be duplicated, distributed or published either in electronic or any other form without the prior written consent of LGT Group Foundation. This publication is for your information only and is not intended as an offer, solicitation of an offer, public advertisement or recommendation to buy or sell any investment or other specific product. Its content has been prepared by our staff and is based on sources of information we consider to be reliable. However, we cannot provide any undertaking or guarantee as to it being correct, complete and up to date. The circumstances and principles to which the information contained in this publication relates may change at any time. Once published, therefore, information shall not be understood as implying that no change has taken place since its publication or that it is still up to date. The information in this publication does not constitute an aid for decision-making in relation to financial, legal, tax or other consulting matters, nor should any investment or other decisions be made on the basis of this information alone. It is recommended that advice be obtained from a qualified expert. Investors should be aware that the value of investments can fall as well as rise. Positive performance in the past is therefore no guarantee of positive performance in the future. Forecasts are not a reliable indicator of future value developments. The risk of price and foreign currency losses and of fluctuations in return as a result of unfavorable exchange rate movements cannot be ruled out. There is a possibility that investors will not recover the full amount they initially invested. We disclaim without qualification all liability for any loss or damage of any kind, whether direct, indirect or consequential, which may be incurred through the use of this publication. This publication is not intended for persons subject to legislation that prohibits its distribution or makes its distribution contingent upon an approval. Any person coming into possession of this publication shall therefore be obliged to find out about any restrictions that may apply and to comply with them. It is up to potential investors to obtain comprehensive information and appropriate advice in their home country, country of residence or country of domicile about the applicable legal requirements and any tax consequences, foreign currency restrictions or foreign exchange controls and any other aspects that are of relevance prior to any decision to subscribe to, purchase, own, exchange or redeem such investments, or enter into any other transaction in relation to same. The securities and rights mentioned in this document may not be purchased or held by investors or for investors domiciled in the USA and/or with US citizenship, nor may such securities and rights be transferred to them.

37

Legal information This document is for distribution solely to persons permitted to receive it and to persons in jurisdictions who may receive it without breaching applicable legal or regulatory requirements. In particular:

in Hong Kong, this document may be issued by either (a) LGT Bank AG, Hong Kong Branch which is an authorized financial institution regulated by the Hong Kong Monetary Authority and the Securities and Futures Commission (“SFC”) or (b) LGT Investment Management (Asia) Ltd. which is a licensed corporation regulated by the SFC, and is intended for distribution, (i) only to professional investors within the meaning of the Securities and Futures Ordinance (Cap 571) and any rules made under that ordinance; or (ii) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies (Winding up and Miscellaneous Provisions) Ordinance (Cap 32) (the “CO CAP 32”) or which do not constitute an offer to the public within the meaning of the CO CAP 32.

in Singapore, this document is issued by LGT Bank (Singapore) Ltd, (Company Registration No.200200473E) to accredited investors within the meaning of the Securities and Futures Act (Cap.289).

In Dubai International Financial Centre (DIFC), LGT (Middle East) Ltd is regulated by the Dubai Financial Services Authority (“DFSA”). This material is directed to Clients who qualify as Professional Clients under the Rules enacted by the DFSA, and no other Person shall act upon it.

The contents of this document have not been reviewed by any regulatory authority in the countries in which it is distributed. You are advised to exercise caution in relation to any information in this document. If you are in doubt about any of the contents of this document, you should seek independent professional advice.

The LGT Group, LGT’s analysts and/or their associates who were involved in preparing and/or publishing this document may from time to time, have financial interest in the financial instruments, underlying referenced assets or related investments referred to in this document and this may give rise to conflicts of interest that affect the objectivity of this document.

This document must not be forwarded, reproduced, redistributed, amended, modified, adapted, transmitted in any form or otherwise made available to any other person without the express consent of LGT.

© LGT 38

Picture description "Portrait of Albert (1614–1657) and Nikolaus (1618–1655) Rubens", c.1626/1627

PETER PAUL RUBENS 1577–1640

This double portrait depicts Rubens' sons Albert and Nikolaus, from his first marriage with Isabella Brant, at the age of about 13 and 9 respectively. Nikolaus, the younger of the two, still looks entirely uninhibited - he pays no attention to the viewer and is fully occupied, playing with his goldfinch which he keeps on a string. Albert, by contrast, seems serious, almost grown-up, not least in the casual elegance of his pose. His father had encouraged him to study the classics and the boy published his first Latin poem at the age of 13. Albert Rubens was to become one of the most esteemed classical scholars of his day.

© LIECHTENSTEIN. The Princely Collections, Vaduz-Vienna

39