Embed Size (px)

Citation preview

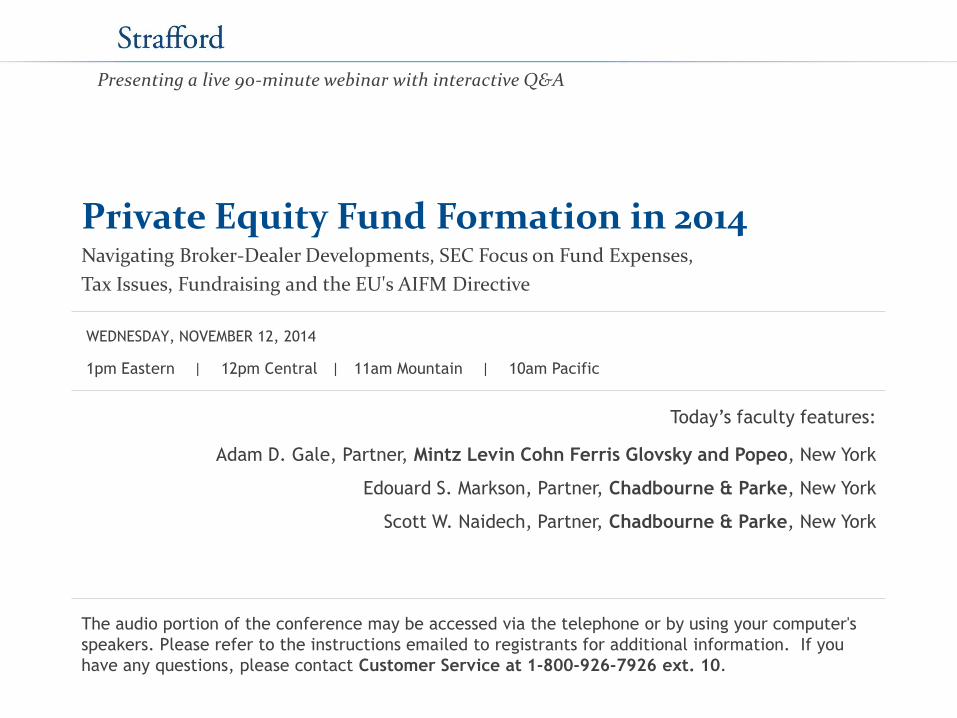

Private Equity Fund Formation in 2014 Navigating Broker-Dealer Developments, SEC Focus on Fund Expenses,

Tax Issues, Fundraising and the EU's AIFM Directive

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, NOVEMBER 12, 2014

Presenting a live 90-minute webinar with interactive Q&A

Adam D. Gale, Partner, Mintz Levin Cohn Ferris Glovsky and Popeo, New York

Edouard S. Markson, Partner, Chadbourne & Parke, New York

Scott W. Naidech, Partner, Chadbourne & Parke, New York

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-328-9525 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the word balloon button to send

FOR LIVE EVENT ONLY

MINTZ LEVIN Mintz Levin Cohn Ferris Glovsky and Popeo PC

Strafford Webinar:

Private Equity Fund Formation

in 2014

Scott Naidech, Chadbourne & Parke LLP

Adam Gale, Mintz Levin

Edouard S. Markson, Chadbourne & Parke LLP

November 12, 2014

MINTZ LEVIN Mintz Levin Cohn Ferris Glovsky and Popeo PC

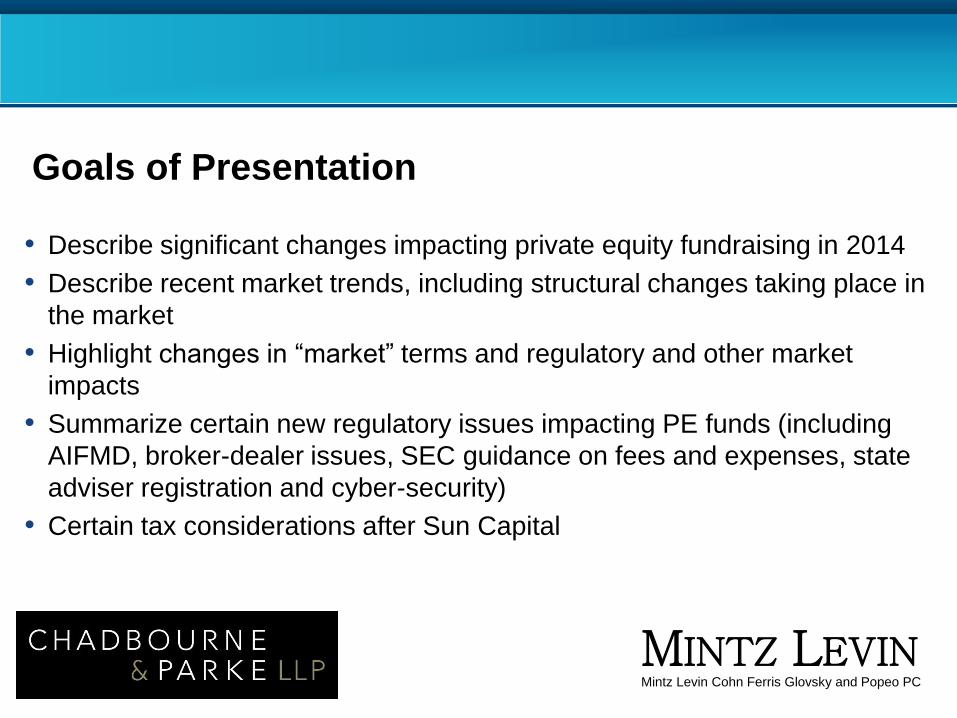

Goals of Presentation

• Describe significant changes impacting private equity fundraising in 2014

• Describe recent market trends, including structural changes taking place in

the market

• Highlight changes in “market” terms and regulatory and other market

impacts

• Summarize certain new regulatory issues impacting PE funds (including

AIFMD, broker-dealer issues, SEC guidance on fees and expenses, state

adviser registration and cyber-security)

• Certain tax considerations after Sun Capital

1. What do we mean by “Private Funds”?

• Any (i) “blind pool” vehicle (ii) invested by a sponsor (iii) who

often receives a management fee and profit participation (known

as a carried interest or performance fee) (iv) offered to qualified

high net worth investors only

• For purposes of this presentation, “Private Funds” means

“Private Equity Funds”. For example, Venture Capital Funds,

Growth Equity Funds, Buyout Funds, Real Estate Funds,

Distressed Debt Funds, Mezzanine Funds, etc., investing in

illiquid securities

6

2. Key incentives for raising a Private Fund?

• Key Economic Incentives for Sponsor Raising a Fund: Access to

private capital from alternative sources; Carried Interest and

Management Fee

• Key Economic Incentives for a Limited Partner Investing in a

Fund: Access to a diversified pool of investments in a targeted

geographic region and/or industry being managed by a specified

team of experts

7

3. Recent changes in key incentives…

• Ten years ago, most fund negotiations focused on economics;

five years ago…governance; in 2014…back to

economics…plus…

SEC new focus on private equity funds.

• Impacts on incentives altering the standard “2 and 20” model –

fundraising pressures/competition for capital/LP leverage

• Volume: currently over 2,000 Private Equity and Real Estate

Funds looking to raise capital, seeking almost $750 billion

• Total amount of probable commitments from this pool: only $250

to $300 billion/year (most of which will go to large multi-billion

funds)

• Conclusion: less than one-half of fundraises will successfully

raise their target amounts.

8

9

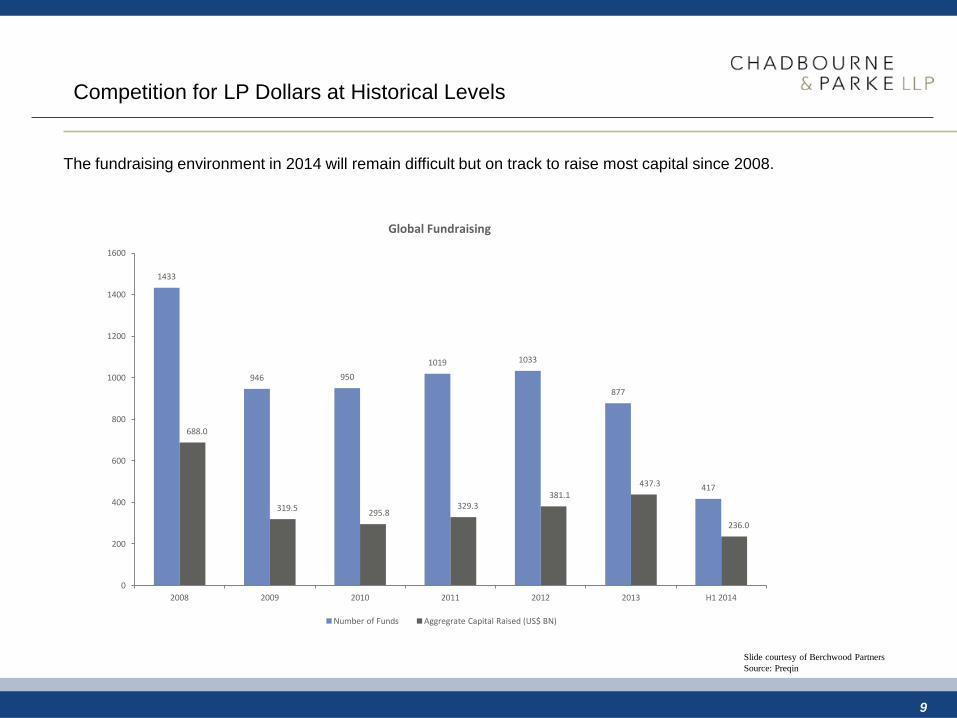

Competition for LP Dollars at Historical Levels

The fundraising environment in 2014 will remain difficult but on track to raise most capital since 2008.

Slide courtesy of Berchwood Partners

Source: Preqin

1433

946 950

1019 1033

877

417

688.0

319.5 295.8

329.3 381.1

437.3

236.0

0

200

400

600

800

1000

1200

1400

1600

2008 2009 2010 2011 2012 2013 H1 2014

Global Fundraising

Number of Funds Aggregrate Capital Raised (US$ BN)

10

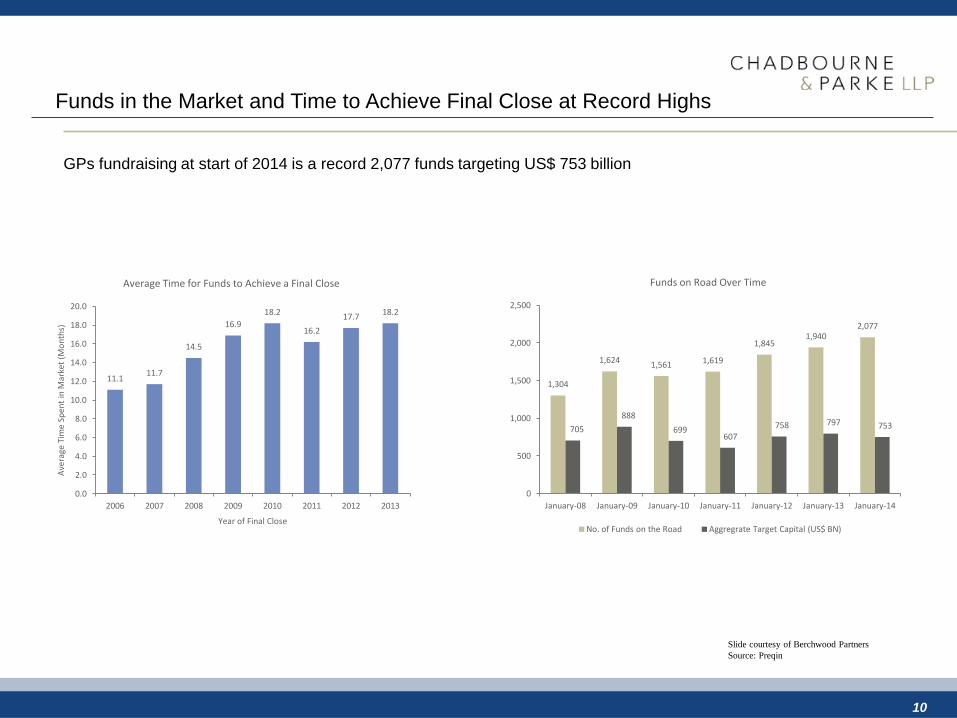

Funds in the Market and Time to Achieve Final Close at Record Highs

GPs fundraising at start of 2014 is a record 2,077 funds targeting US$ 753 billion

Slide courtesy of Berchwood Partners

Source: Preqin

11.1 11.7

14.5

16.9

18.2

16.2

17.7 18.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

2006 2007 2008 2009 2010 2011 2012 2013

Ave

rage

Tim

e Sp

ent

in M

arke

t (M

on

ths)

Year of Final Close

Average Time for Funds to Achieve a Final Close

1,304

1,624 1,561 1,619

1,845 1,940

2,077

705

888

699 607

758 797 753

0

500

1,000

1,500

2,000

2,500

January-08 January-09 January-10 January-11 January-12 January-13 January-14

Funds on Road Over Time

No. of Funds on the Road Aggregrate Target Capital (US$ BN)

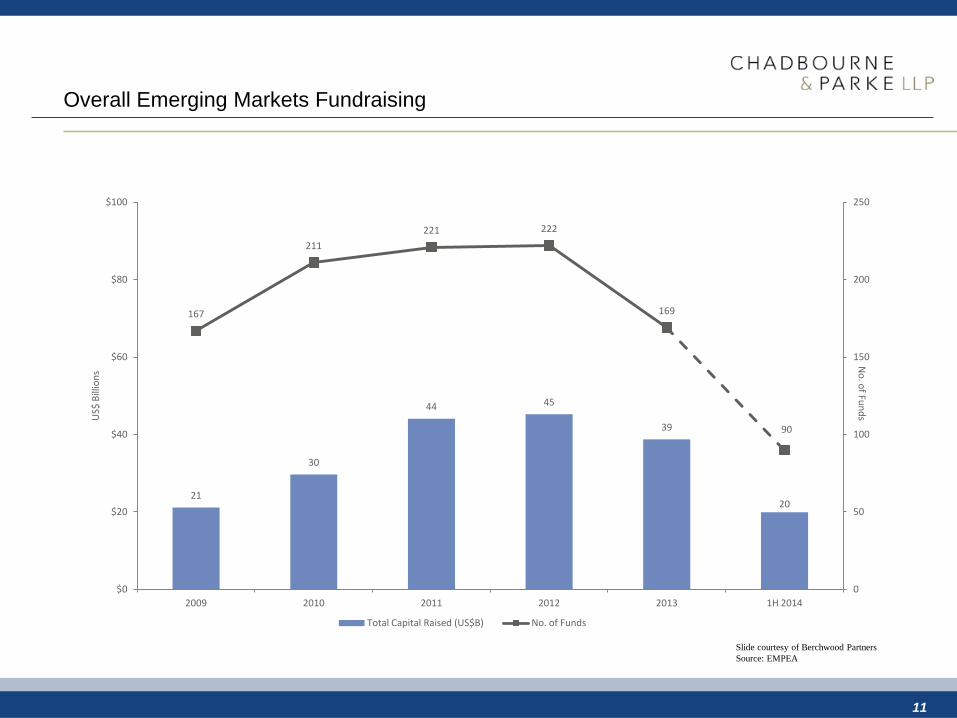

21

30

44 45

39

20

167

211

221 222

169

90

0

50

100

150

200

250

$0

$20

$40

$60

$80

$100

2009 2010 2011 2012 2013 1H 2014

No

. of Fu

nd

s US$

Bill

ion

s

Total Capital Raised (US$B) No. of Funds

Overall Emerging Markets Fundraising

Slide courtesy of Berchwood Partners

Source: EMPEA

11

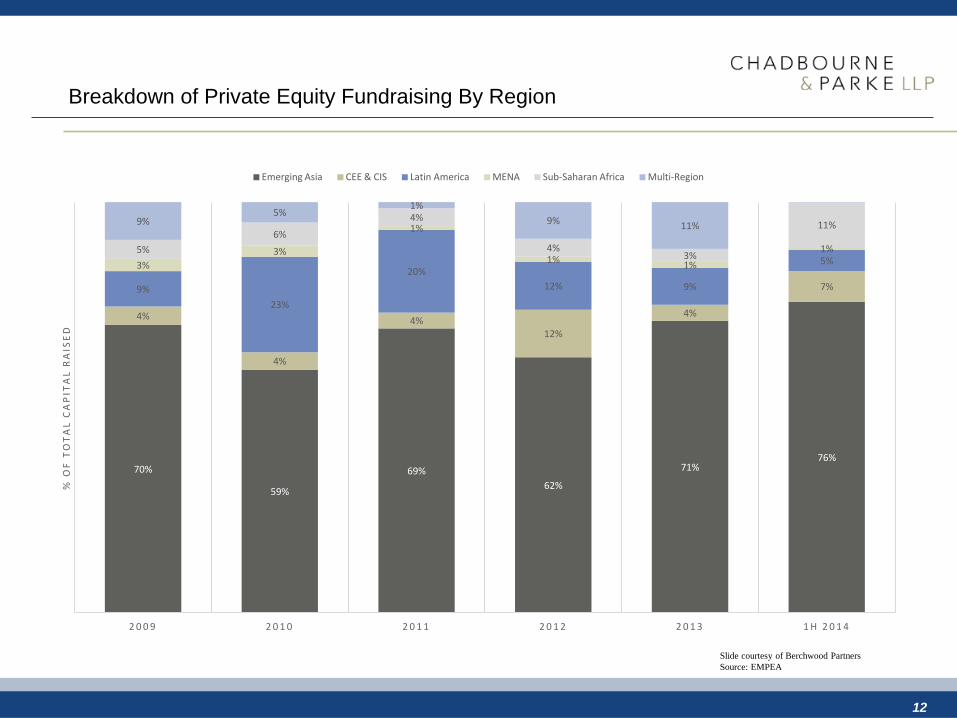

70%

59%

69%

62%

71% 76%

4%

4%

4% 12%

4%

7% 9%

23%

20%

12% 9%

5% 3%

3%

1%

1% 1%

1% 5%

6%

4%

4% 3%

11% 9% 5%

1%

9% 11%

2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 1 H 2 0 1 4

% O

F T

OT

AL

CA

PIT

AL

RA

ISE

D

Emerging Asia CEE & CIS Latin America MENA Sub-Saharan Africa Multi-Region

Breakdown of Private Equity Fundraising By Region

Slide courtesy of Berchwood Partners

Source: EMPEA

12

13

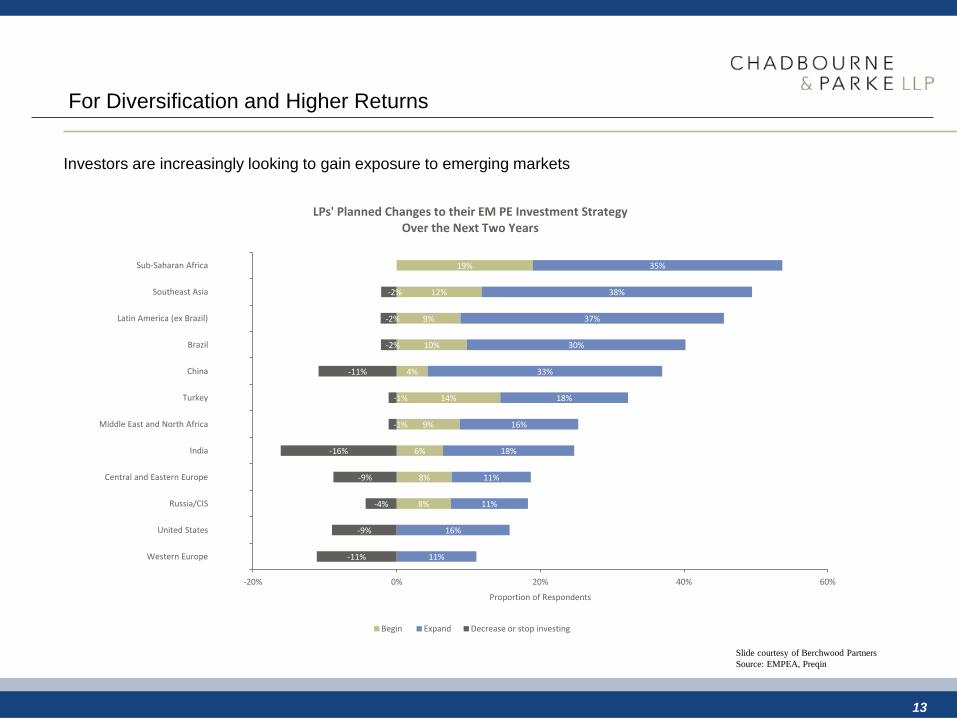

For Diversification and Higher Returns

Investors are increasingly looking to gain exposure to emerging markets

Slide courtesy of Berchwood Partners

Source: EMPEA, Preqin

8%

8%

6%

9%

14%

4%

10%

9%

12%

19%

11%

16%

11%

11%

18%

16%

18%

33%

30%

37%

38%

35%

-11%

-9%

-4%

-9%

-16%

-1%

-1%

-11%

-2%

-2%

-2%

-20% 0% 20% 40% 60%

Western Europe

United States

Russia/CIS

Central and Eastern Europe

India

Middle East and North Africa

Turkey

China

Brazil

Latin America (ex Brazil)

Southeast Asia

Sub-Saharan Africa

Proportion of Respondents

LPs' Planned Changes to their EM PE Investment Strategy Over the Next Two Years

Begin Expand Decrease or stop investing

Changes of key incentives…

• Larger managers compete for the same capital (from government

plan, pension plans, foreign institutions, sovereign wealth funds)

• Greater competition for capital/competitive fundraising

environment

• lower fees and carry, greater LP controls, higher customization

• More conservative fundraising efforts

• PF Funds hesitant to make large jumps in fund sizes from predecessor

funds

• Desire to hit fundraising targets and reduce fundraising period result in

lower fund targets

• Still, sponsors increase their negotiating leverage through certain

key differentiators, including higher performance, strategy

diversification, oversubscription, better terms

• SEC focus on marketing and interim valuations during fundraising

14

4. Who are the Sponsors of Private Funds?

• Private Equity International released the “PEI 300” in May 2014:

1. The Carlyle Group (Wash DC): raised $30.7 billion in capital for their Private

Funds over the last five years

2. Kohlberg Kravis Roberts (New York): $27.2 billion

3. The Blackstone Group (New York): $24.7 billion

4. Apollo Global Management (New York): $22.3 billion

5. TPG (Fort Worth, TX): raised $18.8 billion

6. CVC Capital Partners (London): $18.1 billion

7. General Atlantic (Greenwich, CT): $16.6 billion

8. Ares Management (Los Angeles): $14.1 billion

9. Clayton Dubilier & Rice (New York): $13.5 billion

10. Advent International (Boston): $13.2

15

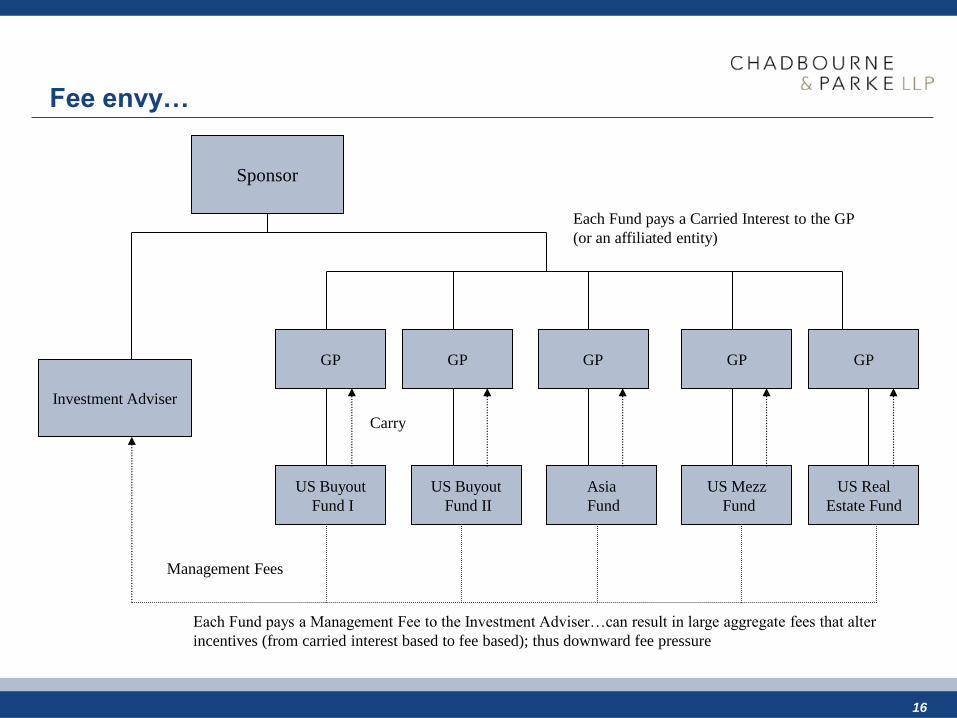

Fee envy…

16

US Buyout

Fund I

US Buyout

Fund II

Asia

Fund

US Mezz

Fund

US Real

Estate Fund

GP GP GP GP GP

Investment Adviser

Sponsor

Each Fund pays a Management Fee to the Investment Adviser…can result in large aggregate fees that alter

incentives (from carried interest based to fee based); thus downward fee pressure

Each Fund pays a Carried Interest to the GP

(or an affiliated entity)

Carry

Management Fees

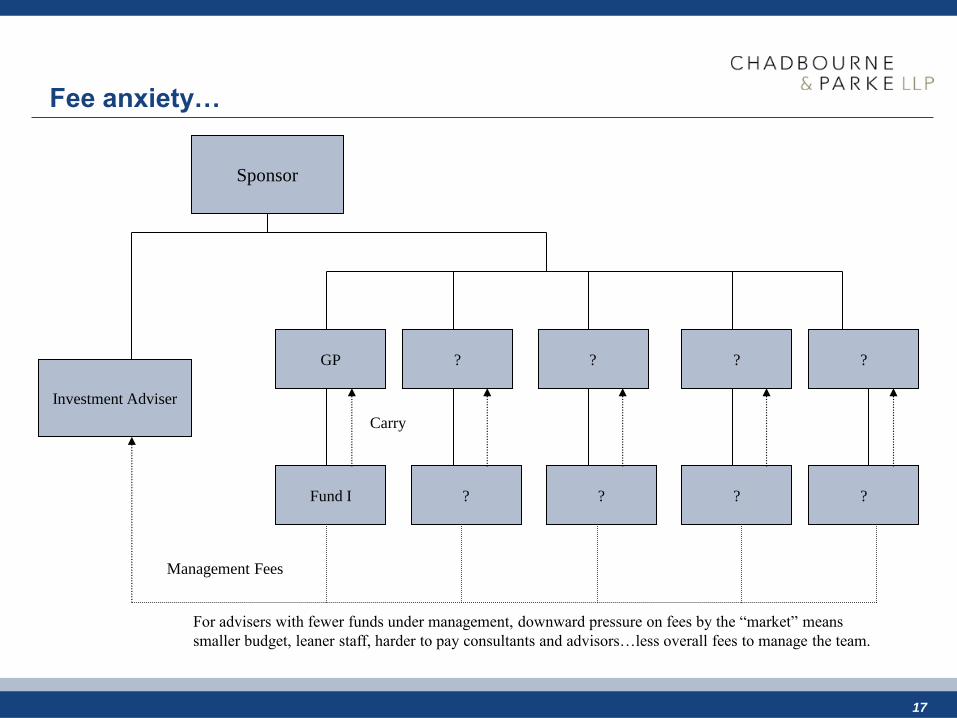

Fee anxiety…

17

Fund I ? ? ? ?

GP ? ? ? ?

Investment Adviser

Sponsor

For advisers with fewer funds under management, downward pressure on fees by the “market” means

smaller budget, leaner staff, harder to pay consultants and advisors…less overall fees to manage the team.

Carry

Management Fees

Zombies!

• Pressure on smaller and mid-sized managers to reduce fees and

fundraise

• Given the reduction in commitments and increased pressure, it is

possible that a significant portion of existing fund managers will

cease to continue meaningful operations, becoming so-called

“zombie funds”

• Governance provisions in some fund agreements may be

inadequate to handle orderly liquidations/terminations/Key

Person events/removal events (fund agreements often infer that

the team will remain in place to raise a subsequent fund)

• While the process may be clear, the cost of implementing may

discourage a single LP from pursuing.

• There may be little or no economic incentive for the GP to initiate the

process.

• SEC increased focus on zombie funds and zombie managers

18

Results…

• Overall result:

• increased LP leverage and lower capital commitments alter dynamics

of negotiation

• longer fundraising periods, or smaller funds/shorter investment

periods

• lower fees and carry

• greater LP participation in investment process

• co-investment rights

• deal-by-deal opt-outs and investment vetoes

• “Classes” of LPs: concern that larger LPs have leverage and can

therefore negotiate better terms in side letters, or in separate

parallel or co-investment funds

• SEC focus on marketing during fundraising periods, favortism,

and allocation of fees and expenses across managed funds

19

5. New SEC Areas of Focus: Private Equity

• Broken Windows Policy

• Drew Bowden Sunshine Speech (May 6, 2014)

• Inherent risks and temptations in private equity business model

• Observed violations and weaknesses

• Poor controls regarding collection of fees and allocation of expenses

• Hidden Fees

• Marketing and Valuation

• Need for thorough, detailed, and continuously adapting compliance

program

• Norm Champ Conflicts of Interest Speech (Sept 11, 2014)

• 50+% increase in SEC-registered private fund advisers since Dodd

Frank

• Tailor and adapt compliance policies and procedures

20

New SEC Areas of Focus: Private Equity (cont’d)

• Continuously review own business models to identify emerging conflict

and risks

• SEC Examination Priorities

• Valuations

• Zombie Funds

• Bowden Speech

• Expense Shifting

• Ancillary Revenue and Hidden Fees

• Co-Investments and Investment Opportunities

• Advertising and Fund Performance

• In re Williamson

• Broker-Dealer Issues

• David Blass/M&A Broker Letter

21

6. Other key terms being negotiated…

• Key Man

• New funds

• Established funds

• Removal Events

• For Cause/other than for Cause

• Mechanics and Voting

• Clawbacks

• Reporting

• ILPA forcing standardization

• Co-Investments

• Pipeline

• Disclosure

• Securities concerns

22

7. ILPA and Changes in Legal Terms

• Institutional Limited Partners Association (ILPA)

• Download ILPA Principals from www.ilpa.org

• Private Equity Principles 1.0 published in Sept 09

• Private Equity Principles 2.0 published in Jan 2011

• Goals: to establish “best practices” regarding fund partnerships

between GPs and LPs

• Three guiding principles:

• Alignment of Interests

• Governance

• Transparency

23

ILPA: a pretty good outline of issues and considerations…

• ILPA: Outlines Key Principles and Concepts, along with reporting

templates

• Economics:

• carried interest calculation and waterfall structures (deal-by-deal vs.

aggregate-return waterfall structures and considerations)

• Management fee considerations, along with GP Expenses and Fee

Income offsets

• Clawbacks: Principles 2.0 contains detailed Appendix on Carry Clawback

Best Practices (e.g., considerations such as a guarantee or escrow;

clarification that the GP clawback is net of taxes paid; other

considerations based on the waterfall structure)

• Governance:

• Key Man events considerations

• Investment Strategy considerations

• Conflicts of interest, fiduciary duties and LP Advisory Committee

(Appendix A)

24

…but not a checklist!

• Transparency

• Fee disclosures

• ILPA standardized templates

• Capital call and distribution notices

• Annual and quarterly reports

• Appendix C covers additional considerations on reporting

• Not a laundry list of must-haves

• ILPA: our terms are not to be applied as a “checklist”; each partnership

should be considered separately and holistically

• Goal is to provide terms and principles to be considered and that will result in

better investment returns and a more sustainable private equity industry

• Generally, considered more “pro-LP” and not the “market standard”; the ILPA

terms continue to be discussed, debated and augmented

25

1. AIFMD

2. Broker-Dealer Issues for PE Funds

3. SEC Guidance on Fees & Expenses, and Marketing

4. State Investment Adviser Exemptions

5. Cyber-Security

Regulatory Issues

26

• Applies if meet any of the following:

o Market to European Union investors (including UK)

o Fund vehicle is organized in EU

o Fund manager based in EU (including a branch office)

• Applies even if Non-EU Fund Manager and Non-EU Fund

• Applies to all types of private funds, including PE, VC and RE funds

• Need to consider AIFMD before any contact with any EU investor

• Transitional period ended on July 22, 2014, so fully in effect

1. AIFMD (Alternative Investment Fund Managers Directive)

27

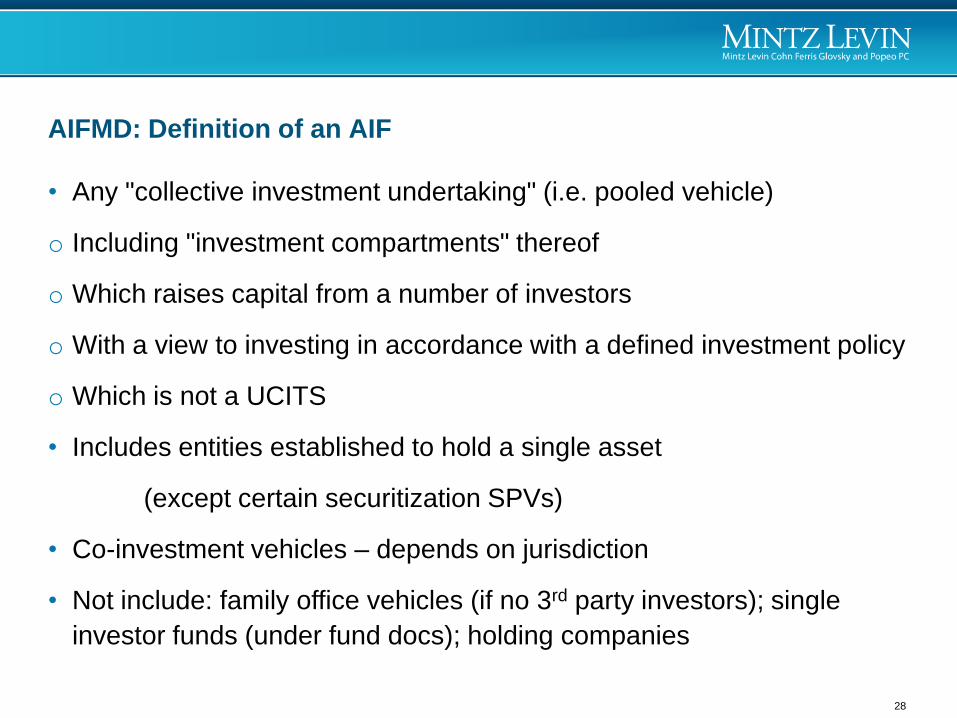

• Any "collective investment undertaking" (i.e. pooled vehicle)

o Including "investment compartments" thereof

o Which raises capital from a number of investors

o With a view to investing in accordance with a defined investment policy

o Which is not a UCITS

• Includes entities established to hold a single asset

(except certain securitization SPVs)

• Co-investment vehicles – depends on jurisdiction

• Not include: family office vehicles (if no 3rd party investors); single

investor funds (under fund docs); holding companies

AIFMD: Definition of an AIF

28

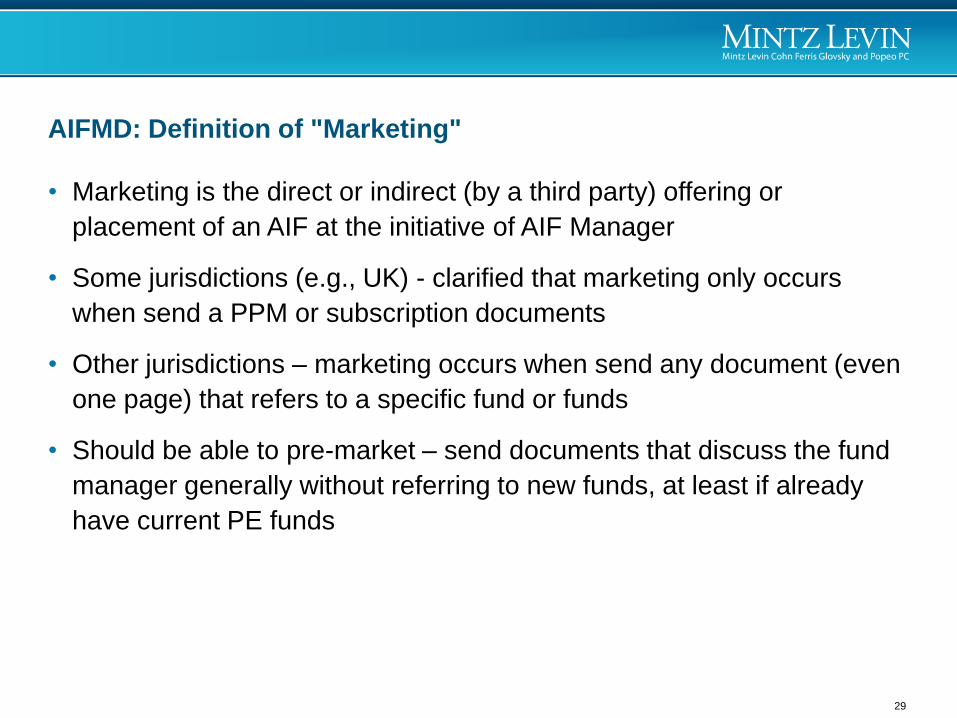

• Marketing is the direct or indirect (by a third party) offering or

placement of an AIF at the initiative of AIF Manager

• Some jurisdictions (e.g., UK) - clarified that marketing only occurs

when send a PPM or subscription documents

• Other jurisdictions – marketing occurs when send any document (even

one page) that refers to a specific fund or funds

• Should be able to pre-market – send documents that discuss the fund

manager generally without referring to new funds, at least if already

have current PE funds

AIFMD: Definition of "Marketing"

29

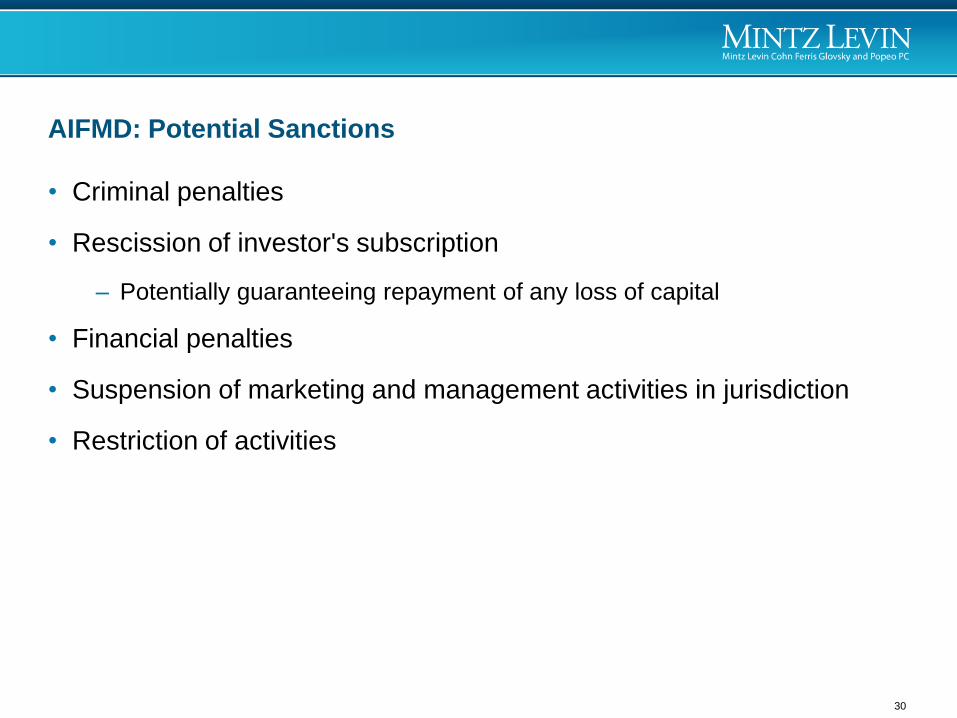

• Criminal penalties

• Rescission of investor's subscription

– Potentially guaranteeing repayment of any loss of capital

• Financial penalties

• Suspension of marketing and management activities in jurisdiction

• Restriction of activities

AIFMD: Potential Sanctions

30

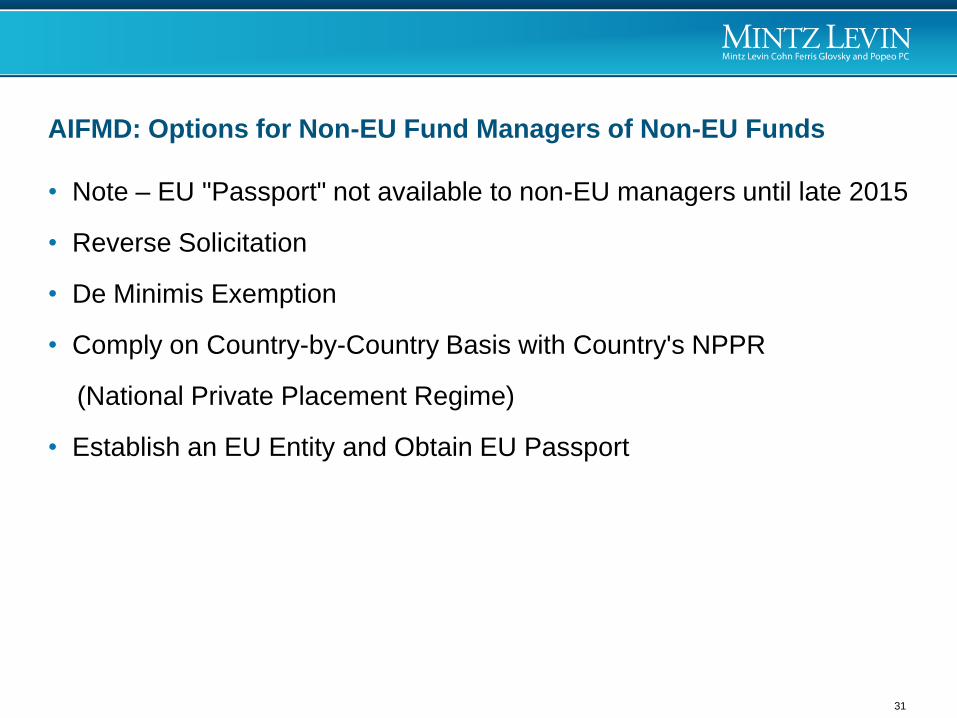

• Note – EU "Passport" not available to non-EU managers until late 2015

• Reverse Solicitation

• De Minimis Exemption

• Comply on Country-by-Country Basis with Country's NPPR

(National Private Placement Regime)

• Establish an EU Entity and Obtain EU Passport

AIFMD: Options for Non-EU Fund Managers of Non-EU Funds

31

• Potential investor requests (solicits) the fund manager to provide

information about investing in the manager's funds

• Request must occur before "marketing" by the fund manager

• Documentation – Recommended to obtain a written request from the

investor prior to discussing or sending documents as to specific funds

• A representation in subscription documents by itself is insufficient

• Use of template letter from investors may raise questions

• If can rely on reverse solicitation, do not need to comply with the

jurisdiction's NPPR

AIFMD: Reverse Solicitation

32

• AUM below €100 million (~US$135M), or

• AUM below €500 million (~US$690M),

- if no leverage and no redemptions allowed for 5 years

• Must count Fund Manager's total AUM for all funds, including funds

with no EU investors

• Still need to comply with each country's NPPR, but not with disclosure

obligations

AIFMD: De Minimis Exemption

33

• Each country has its own requirements

• Notification jurisdictions (e.g., UK) - only require notification to

regulator, and then can begin marketing immediately upon filing

• Approval jurisdictions (e.g., Germany) – must register with regulator

and wait to market until obtain approval

• Approval process can take several months

AIFMD: National Private Placement Regimes (NPPRs)

34

If neither nor de minimis nor reverse solicitation available, need to

comply with NPPR and meet other requirements:

• Include specific disclosures in PPM, such as relating to fund expenses

• Report to the country's regulator, including disclosure of remuneration

to fund manager's staff, and update report annually

• If acquiring control of an EU company:

- disclosure to the company, its shareholders and regulators

- comply with asset-stripping restrictions

• For some jurisdictions, need an EU depositary, minimum capital, so

that requirements are basically the same as for an EU manager

AIFMD: Disclosure and Other Requirements

35

• If will be soliciting a large number of EU investors in many EU

countries, consider establishing an EU entity

• Can then obtain an EU passport, and only need to register once

• But need to comply with further requirements, including restrictions on

how the fund manager pays its principals and employees

AIFMD: Establish an EU Entity

36

• Still a hot topic for SEC

- See April 2013 SEC Div. of Trading & Markets speech

• Investment Banking/Acquisition/Disposition Fees

o Fund manager (or affiliate) charges success fee to portfolio

company or to fund for identifying sellers or purchasers, or

structuring transactions

o Unless 100% of that success fee is offset against fund

management fees, then SEC suggesting that fund manager must

register as a B-D

o But SEC subsequently issued an M&A Brokers no-action letter,

setting forth an exception to the BD registration requirements

o Note that still need to comply with state (blue sky) BD laws

2. Broker-Dealer ("B-D") Issues

37

No BD registration if sale of company meets following requirements:

• Privately-held company (cannot be a shell company)

• Buyer must control the company (control presumed at 25% of voting

rights or, for LLCs, obtain 25% of capital upon dissolution)

• Buyer must "actively operate" the company (can be through power to

elect executive officers and annual budget approval, or serve as exec.)

• Broker may not: have ability to bind a party; directly or indirectly

provide financing; have custody of , or handle, funds or securities; form

a group of brokers; have been barred or suspended

• May not involve a public offering and securities must be restricted

• Broker must obtain consent if represents buyers and sellers

BD Issues: M&A Brokers No-Action Letter

38

• Personnel in Marketing Department

o Dedicated sales force, regardless of how compensated, "may

strongly indicate" B-D registration required

o For example, consider status of head of Investor Relations

• Paying Commissions to "Finders"

o Beware of potential consequences – Ranieri matter; rescission

Other BD Issues

39

• Use of "Operating Partners"

- Payment of Operating Partners directly by portfolio company or

fund without sufficient disclosure

- Operating Partner functions like other members of fund

manager team (but not paid by the fund manager)

- Payments not offset against management fees

• Shifting of Employees to "Consultants"

- Employees at fundraising stage, but then terminated and

rehired as consultants

3. SEC Guidance on Fees & Expenses, and Marketing

40

• Back office functions paid by fund without sufficient disclosure,

especially compliance, legal and accounting

• Charges to fund for automated creation of investor reports

• Accelerated Monitoring Fees to Portfolio Companies

- Portfolio company required to sign agreement for payment of

monitoring fee for a long period (e.g., 10 years)

- Upon merger or IPO, fee charged to terminate the monitoring

agreement, which is acceleration of all fees due for entire term

Other Fees & Expenses Issues

41

• IRRs in marketing materials that are gross numbers (without deduction

of fees and expenses) without disclosure

• Use of a valuation methodology different than as disclosed

• Changing valuation methodology period to period, to increase fund

valuation

• Use of projections instead of actual valuations, without disclosure

• Key members of management team resigning soon after fundraising

completed

SEC Guidance on Marketing Issues

42

• Fund managers who are exempt from SEC registration still need to

check the investment adviser registration requirements of the state of

their principal office and place of business

• Some states have added additional requirements to meet the state

exemption, following NASAA model rules:

o For 3(c)(1) funds:

- can only charge carried interest to investors that are Qualified Clients

under Adviser Act definition

- must include additional disclosures to investors

o Some states have different exemption for 3(c)(1) VC funds

o Must file Form ADV as Exempt Reporting Adviser

4. State Investment Adviser Registration Exemptions

43

• OCIE Cyber-Security Alert – April 2014:

o Consider cyber-security risks and how to detect unauthorized activity

o Responsible for third party vendors' cyber-security

o Principals should understand issues, not just IT personnel

o Recordkeeping of security processes

• Unclear whether should include disclosure of cybersecurity issues in

PPM, but risk factor probably useful

• Red Flags Rule applies to certain RIAs (need policies and procedures

to identify, detect and respond to Red Flags indicating possible identity

theft)

5. Cyber-Security

44

45

Sun Capital & Private Equity Funds

46

• A PE Fund's portfolio company (SBI) was in bankruptcy and stopped its contributions to a multiemployer pension plan (TPF)

• TPF demanded payment of SBI's withdrawal liability under ERISA

• TPF also asserted that the PE Fund was jointly and severally liable for the withdrawal liability under ERISA, on the basis that it was a "trade or business" that is "under common control" with the primary ERISA obligor (29 U.S.C. § 1301)

Sun Capital – Basic Facts

47

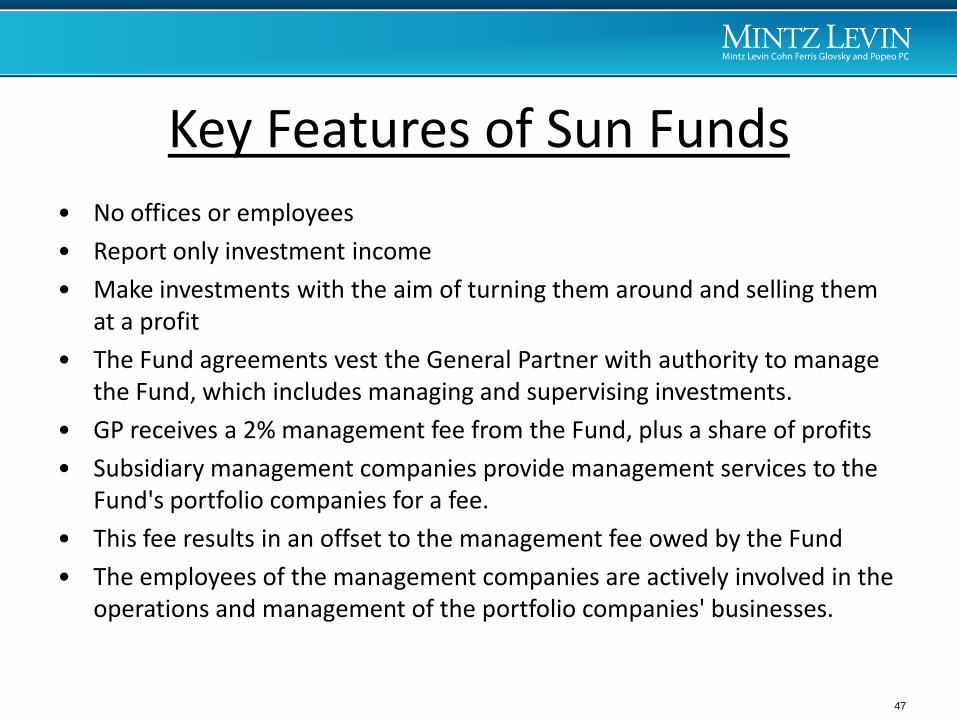

• No offices or employees

• Report only investment income

• Make investments with the aim of turning them around and selling them at a profit

• The Fund agreements vest the General Partner with authority to manage the Fund, which includes managing and supervising investments.

• GP receives a 2% management fee from the Fund, plus a share of profits

• Subsidiary management companies provide management services to the Fund's portfolio companies for a fee.

• This fee results in an offset to the management fee owed by the Fund

• The employees of the management companies are actively involved in the operations and management of the portfolio companies' businesses.

Key Features of Sun Funds

48

• The Funds were in a "trade or business" under ERISA (and remanded for other issues) – but the business of SBI itself.

• Holding was based on the fact that the Funds were not merely passive investors (as mere investment is not a "trade or business"), but were, through agents, "actively," "extensively" and "intimately" involved in the management, operation and supervision of SBI.

• The court focused heavily on the management fee offset, characterizing it as the "economic benefit" that most clearly distinguished the Fund from an ordinary, passive investor.

– "It is one thing to manage one's investments in businesses. It is another to manage the businesses in which one invests"

– "Under Delaware law, it is clear that the GP of [the Fund], in providing management services to SBI, was acting as an agent of the Fund."

• The standard used by the court was not taken from tax precedent, but was held to be not inconsistent with such precedent, including the Supreme Court's decisions in Groetzinger (1987), Higgins (1941) and Whipple (1963).

The Sun Capital Holding

49

• The Sun Capital decision emphasized the fee offset arrangement as a key factor in its holding

• Practitioners have historically expressed concern that the offset arrangement gives rise to the characterization of the offending fees as having been received by the fund itself in respect of services performed "on behalf of" the fund

• For this reason, management fee offsets are commonly carved out of many LP covenants.

• But isn't this just an economic arrangement? How does it change the nature of the Fund's activities?

Management Fee Offset

50

• A Private Equity Fund that invests in securities of portfolio companies treated as corporations for U.S. tax purposes is not engaged in a trade or business, notwithstanding the substantial managerial activities that the GP/Manager may conduct.

• This is based on the fact that a PE Fund acquires portfolio companies as investments with a view to long-term appreciation, doesn’t execute enough trades to be a "trader," and doesn’t have the customers that are necessary for "dealer" status.

Traditional View

51

• Sponsor – Ordinary income on gains?

– §1221(a)(1)

– Investor vs. Trader vs. Dealer. "Promoter"?

• Tax-Exempt Investors – UBTI

– Statutory exemption (§512(b)(5))

• Significance of "customers" in both of these categories. Further guidance would likely be necessary

• Non-U.S. Investors – ECI

– Eligibility for trading safe harbor of §864?

• Management fee deductions?

– Possible pro-taxpayer overall result

What are the potential ramifications if a PE Fund is treated as engaged in a business for tax purposes?

52

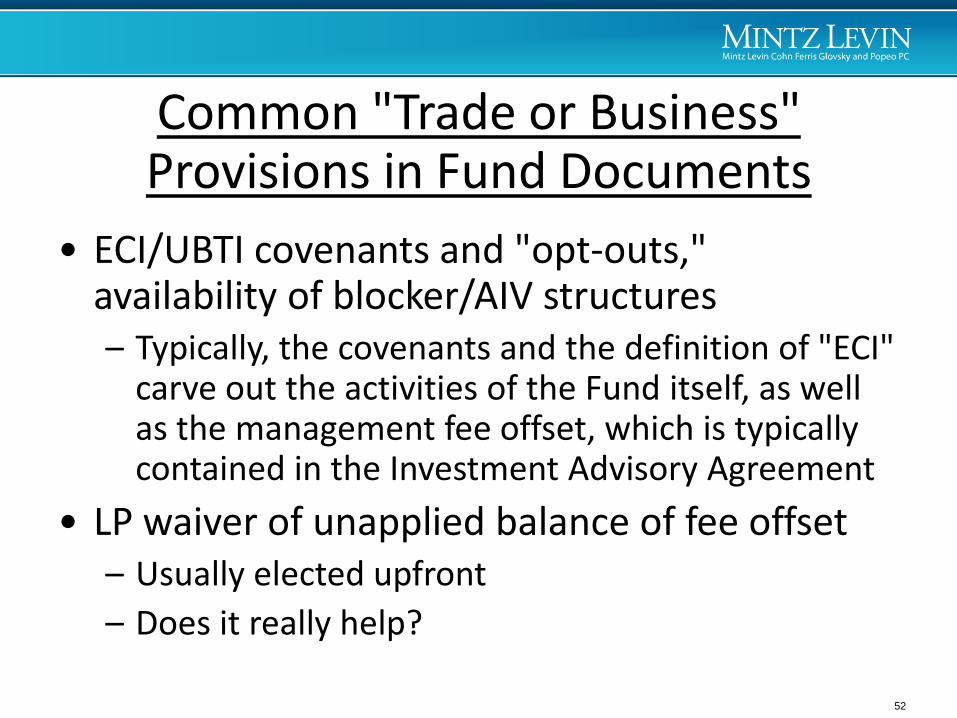

• ECI/UBTI covenants and "opt-outs," availability of blocker/AIV structures – Typically, the covenants and the definition of "ECI"

carve out the activities of the Fund itself, as well as the management fee offset, which is typically contained in the Investment Advisory Agreement

• LP waiver of unapplied balance of fee offset – Usually elected upfront

– Does it really help?

Common "Trade or Business" Provisions in Fund Documents

53

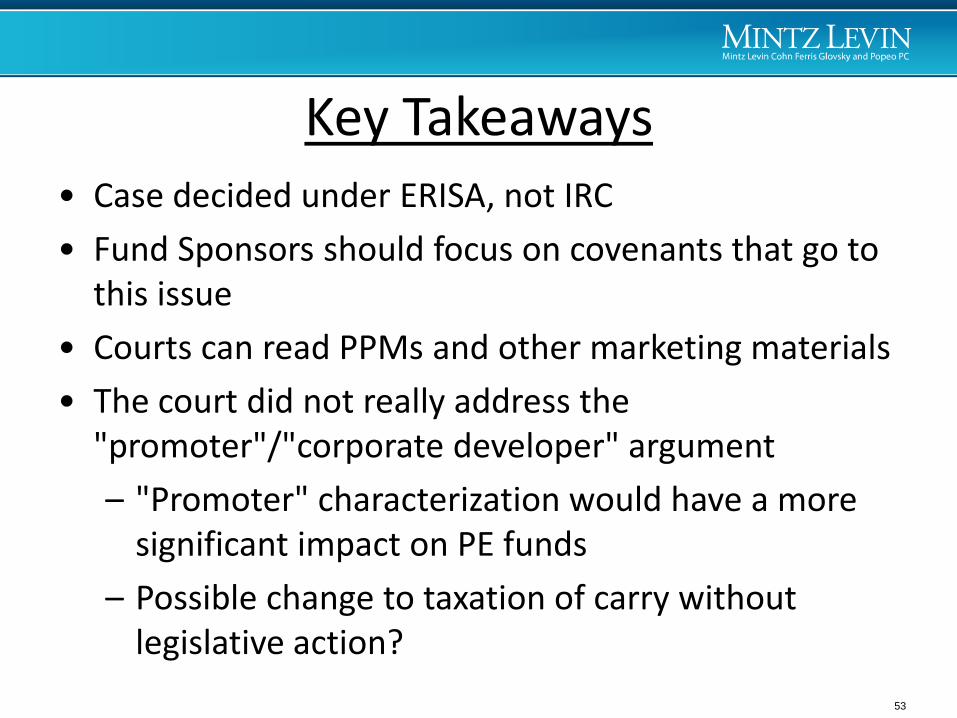

• Case decided under ERISA, not IRC

• Fund Sponsors should focus on covenants that go to this issue

• Courts can read PPMs and other marketing materials

• The court did not really address the "promoter"/"corporate developer" argument

– "Promoter" characterization would have a more significant impact on PE funds

– Possible change to taxation of carry without legislative action?

Key Takeaways

54

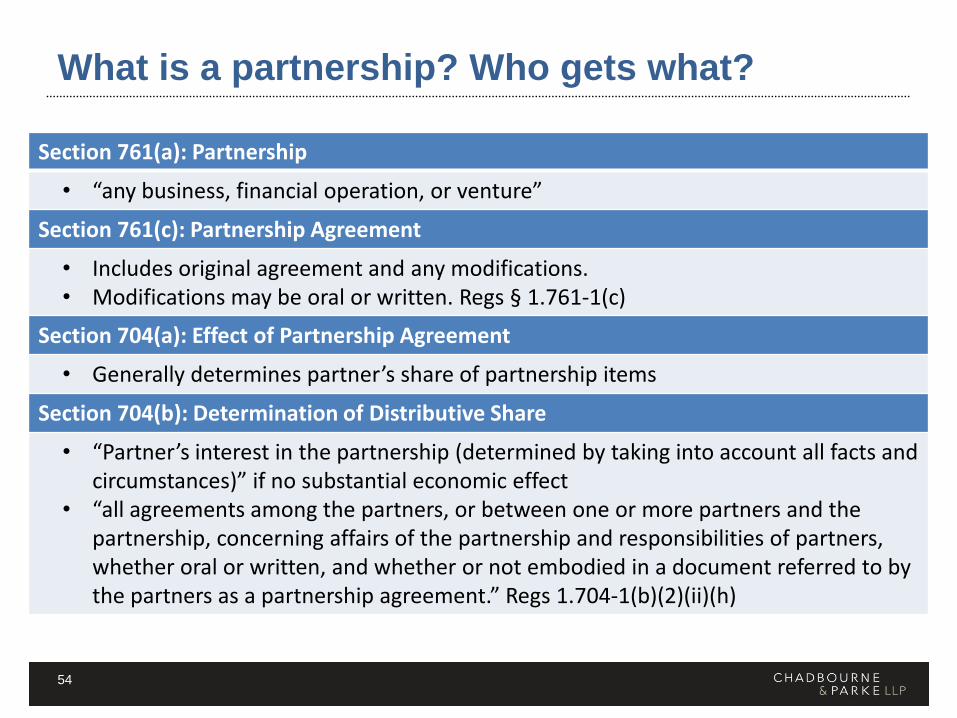

What is a partnership? Who gets what?

Section 761(a): Partnership

• “any business, financial operation, or venture”

Section 761(c): Partnership Agreement

• Includes original agreement and any modifications. • Modifications may be oral or written. Regs § 1.761-1(c)

Section 704(a): Effect of Partnership Agreement

• Generally determines partner’s share of partnership items

Section 704(b): Determination of Distributive Share

• “Partner’s interest in the partnership (determined by taking into account all facts and circumstances)” if no substantial economic effect

• “all agreements among the partners, or between one or more partners and the partnership, concerning affairs of the partnership and responsibilities of partners, whether oral or written, and whether or not embodied in a document referred to by the partners as a partnership agreement.” Regs 1.704-1(b)(2)(ii)(h)

55

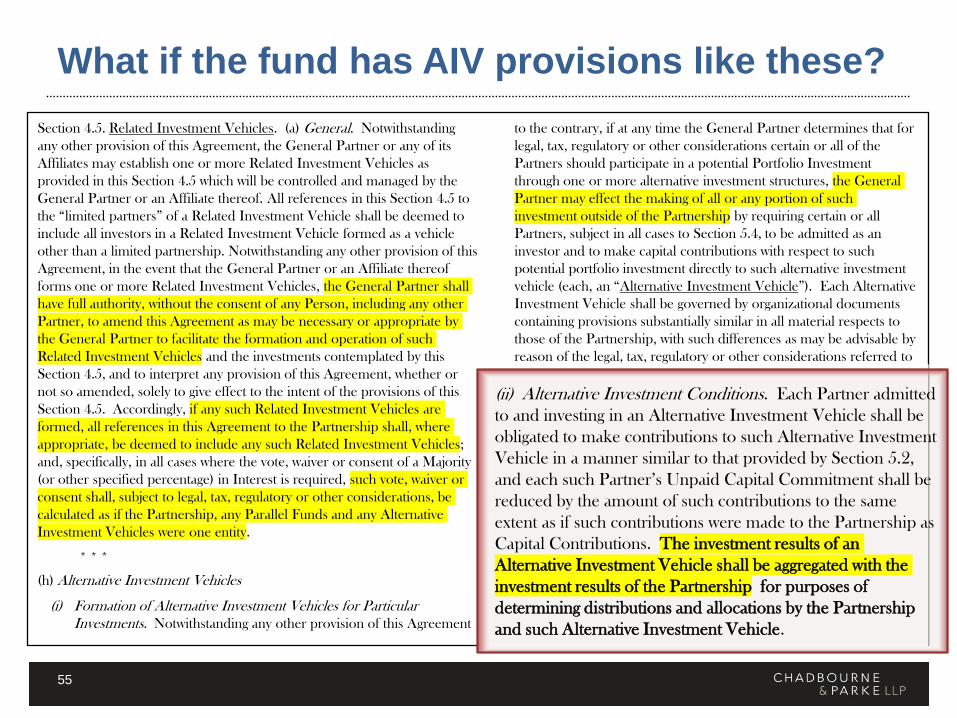

Section 4.5. Related Investment Vehicles. (a) General. Notwithstanding

any other provision of this Agreement, the General Partner or any of its

Affiliates may establish one or more Related Investment Vehicles as

provided in this Section 4.5 which will be controlled and managed by the

General Partner or an Affiliate thereof. All references in this Section 4.5 to

the “limited partners” of a Related Investment Vehicle shall be deemed to

include all investors in a Related Investment Vehicle formed as a vehicle

other than a limited partnership. Notwithstanding any other provision of this

Agreement, in the event that the General Partner or an Affiliate thereof

forms one or more Related Investment Vehicles, the General Partner shall

have full authority, without the consent of any Person, including any other

Partner, to amend this Agreement as may be necessary or appropriate by

the General Partner to facilitate the formation and operation of such

Related Investment Vehicles and the investments contemplated by this

Section 4.5, and to interpret any provision of this Agreement, whether or

not so amended, solely to give effect to the intent of the provisions of this

Section 4.5. Accordingly, if any such Related Investment Vehicles are

formed, all references in this Agreement to the Partnership shall, where

appropriate, be deemed to include any such Related Investment Vehicles;

and, specifically, in all cases where the vote, waiver or consent of a Majority

(or other specified percentage) in Interest is required, such vote, waiver or

consent shall, subject to legal, tax, regulatory or other considerations, be

calculated as if the Partnership, any Parallel Funds and any Alternative

Investment Vehicles were one entity.

* * *

(h) Alternative Investment Vehicles

(i) Formation of Alternative Investment Vehicles for Particular

Investments. Notwithstanding any other provision of this Agreement

to the contrary, if at any time the General Partner determines that for

legal, tax, regulatory or other considerations certain or all of the

Partners should participate in a potential Portfolio Investment

through one or more alternative investment structures, the General

Partner may effect the making of all or any portion of such

investment outside of the Partnership by requiring certain or all

Partners, subject in all cases to Section 5.4, to be admitted as an

investor and to make capital contributions with respect to such

potential portfolio investment directly to such alternative investment

vehicle (each, an “Alternative Investment Vehicle”). Each Alternative

Investment Vehicle shall be governed by organizational documents

containing provisions substantially similar in all material respects to

those of the Partnership, with such differences as may be advisable by

reason of the legal, tax, regulatory or other considerations referred to

above and, if the General Partner requires an ERISA Partner to

invest in an Alternative Investment Vehicle, the Alternative

Investment Vehicle shall provide such an investor with the same

rights as provided under the Partnership.

What if the fund has AIV provisions like these?

(ii) Alternative Investment Conditions. Each Partner admitted

to and investing in an Alternative Investment Vehicle shall be

obligated to make contributions to such Alternative Investment

Vehicle in a manner similar to that provided by Section 5.2,

and each such Partner’s Unpaid Capital Commitment shall be

reduced by the amount of such contributions to the same

extent as if such contributions were made to the Partnership as

Capital Contributions. The investment results of an

Alternative Investment Vehicle shall be aggregated with the

investment results of the Partnership for purposes of

determining distributions and allocations by the Partnership

and such Alternative Investment Vehicle.

56

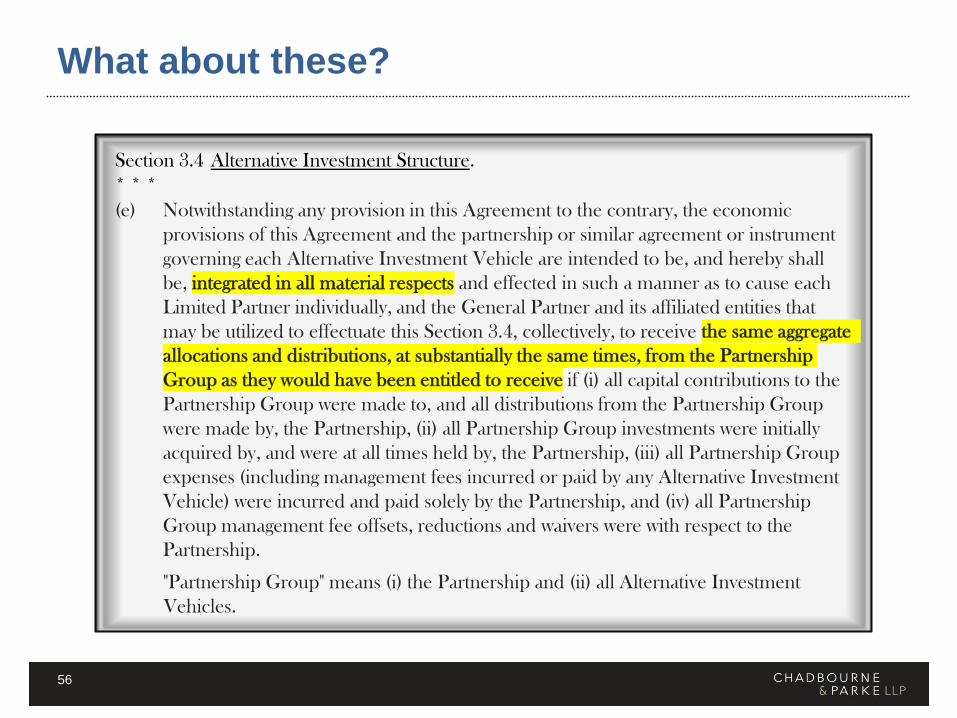

What about these?

Section 3.4 Alternative Investment Structure.

* * *

(e) Notwithstanding any provision in this Agreement to the contrary, the economic

provisions of this Agreement and the partnership or similar agreement or instrument

governing each Alternative Investment Vehicle are intended to be, and hereby shall

be, integrated in all material respects and effected in such a manner as to cause each

Limited Partner individually, and the General Partner and its affiliated entities that

may be utilized to effectuate this Section 3.4, collectively, to receive

if (i) all capital contributions to the

Partnership Group were made to, and all distributions from the Partnership Group

were made by, the Partnership, (ii) all Partnership Group investments were initially

acquired by, and were at all times held by, the Partnership, (iii) all Partnership Group

expenses (including management fees incurred or paid by any Alternative Investment

Vehicle) were incurred and paid solely by the Partnership, and (iv) all Partnership

Group management fee offsets, reductions and waivers were with respect to the

Partnership.

"Partnership Group" means (i) the Partnership and (ii) all Alternative Investment

Vehicles.

57

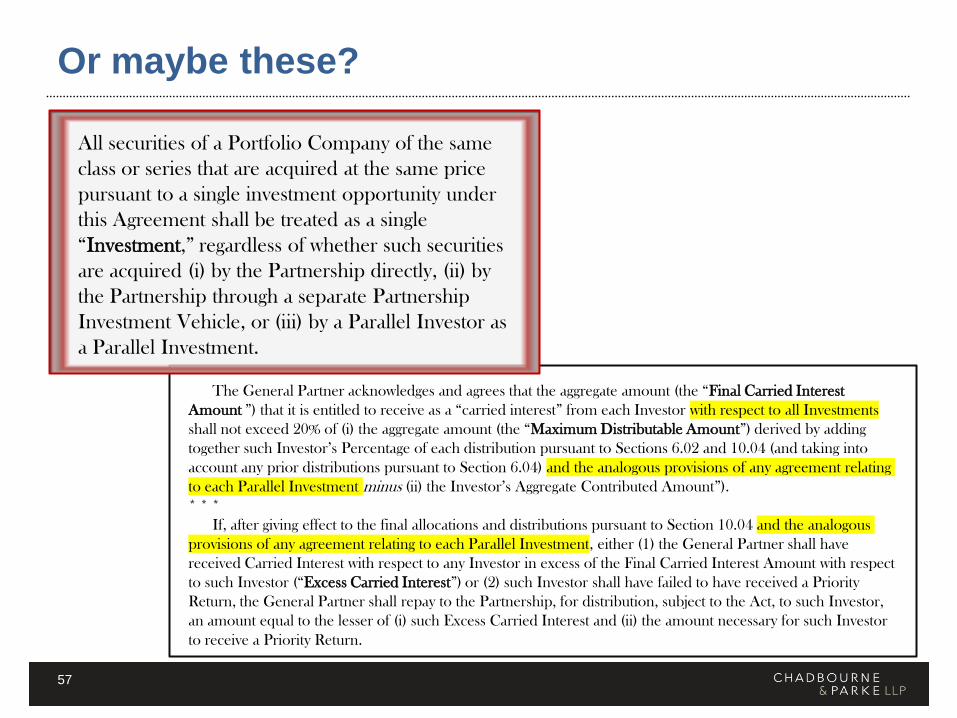

Or maybe these?

The General Partner acknowledges and agrees that the aggregate amount (the “Final Carried Interest

Amount ”) that it is entitled to receive as a “carried interest” from each Investor with respect to all Investments

shall not exceed 20% of (i) the aggregate amount (the “Maximum Distributable Amount”) derived by adding

together such Investor’s Percentage of each distribution pursuant to Sections 6.02 and 10.04 (and taking into

account any prior distributions pursuant to Section 6.04) and the analogous provisions of any agreement relating

to each Parallel Investment minus (ii) the Investor’s Aggregate Contributed Amount”).

* * *

If, after giving effect to the final allocations and distributions pursuant to Section 10.04 and the analogous

provisions of any agreement relating to each Parallel Investment, either (1) the General Partner shall have

received Carried Interest with respect to any Investor in excess of the Final Carried Interest Amount with respect

to such Investor (“Excess Carried Interest”) or (2) such Investor shall have failed to have received a Priority

Return, the General Partner shall repay to the Partnership, for distribution, subject to the Act, to such Investor,

an amount equal to the lesser of (i) such Excess Carried Interest and (ii) the amount necessary for such Investor

to receive a Priority Return.

All securities of a Portfolio Company of the same

class or series that are acquired at the same price

pursuant to a single investment opportunity under

this Agreement shall be treated as a single

“Investment,” regardless of whether such securities

are acquired (i) by the Partnership directly, (ii) by

the Partnership through a separate Partnership

Investment Vehicle, or (iii) by a Parallel Investor as

a Parallel Investment.

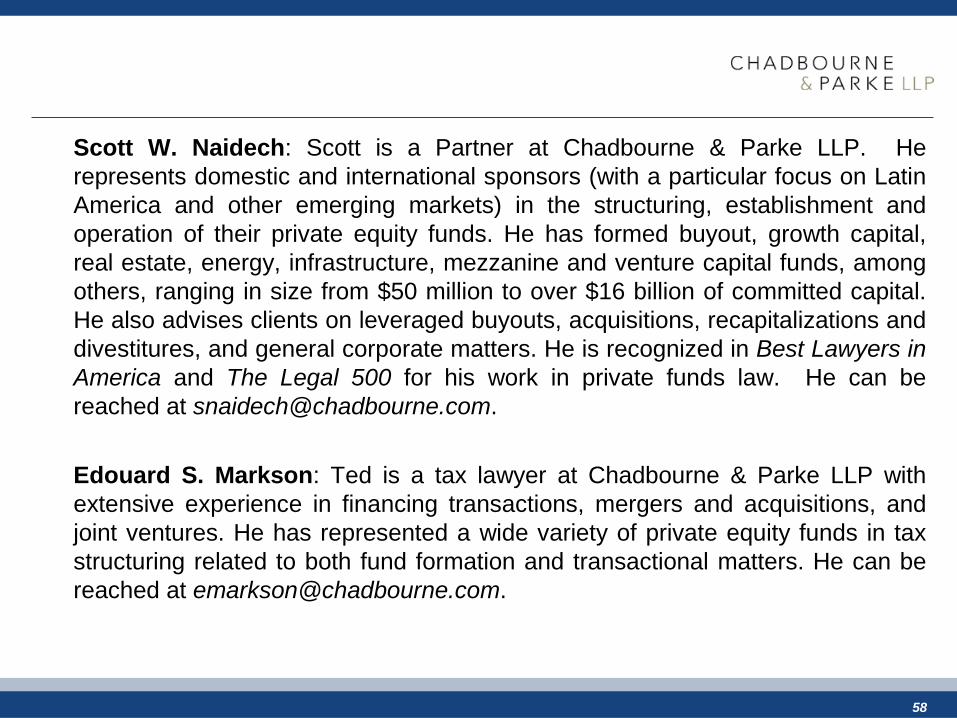

Scott W. Naidech: Scott is a Partner at Chadbourne & Parke LLP. He

represents domestic and international sponsors (with a particular focus on Latin

America and other emerging markets) in the structuring, establishment and

operation of their private equity funds. He has formed buyout, growth capital,

real estate, energy, infrastructure, mezzanine and venture capital funds, among

others, ranging in size from $50 million to over $16 billion of committed capital.

He also advises clients on leveraged buyouts, acquisitions, recapitalizations and

divestitures, and general corporate matters. He is recognized in Best Lawyers in

America and The Legal 500 for his work in private funds law. He can be

reached at [email protected].

Edouard S. Markson: Ted is a tax lawyer at Chadbourne & Parke LLP with

extensive experience in financing transactions, mergers and acquisitions, and

joint ventures. He has represented a wide variety of private equity funds in tax

structuring related to both fund formation and transactional matters. He can be

reached at [email protected].

58

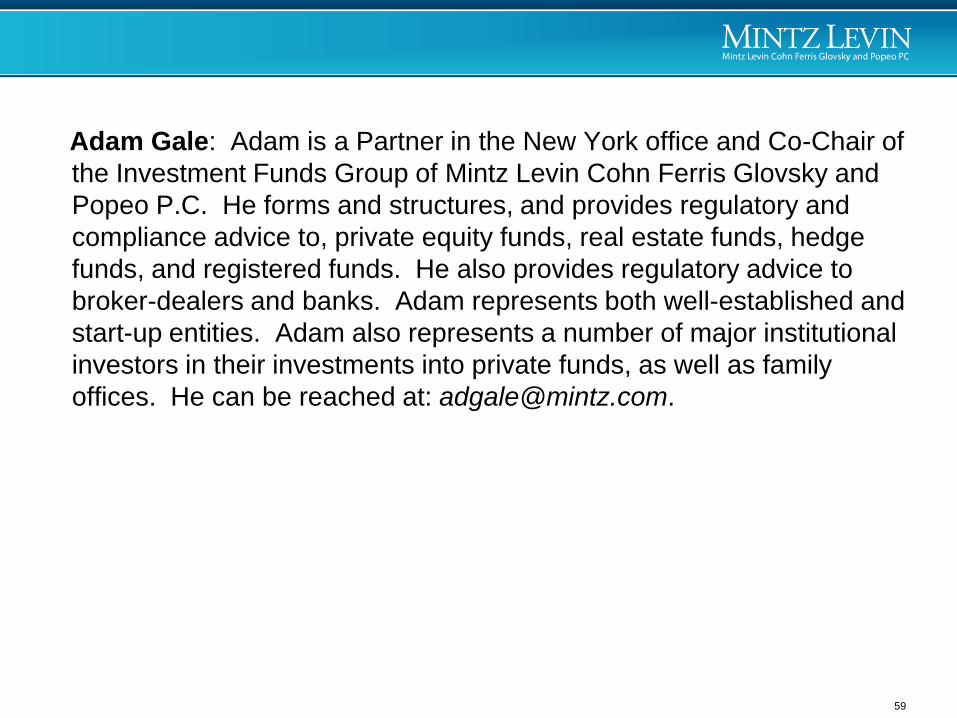

Adam Gale: Adam is a Partner in the New York office and Co-Chair of

the Investment Funds Group of Mintz Levin Cohn Ferris Glovsky and

Popeo P.C. He forms and structures, and provides regulatory and

compliance advice to, private equity funds, real estate funds, hedge

funds, and registered funds. He also provides regulatory advice to

broker-dealers and banks. Adam represents both well-established and

start-up entities. Adam also represents a number of major institutional

investors in their investments into private funds, as well as family

offices. He can be reached at: [email protected].

59