Embed Size (px)

Citation preview

private equity

private equity

Table of contents

Introduction 5

I. Main Luxembourg private equity vehicles 6

Overview 6

Key features 7

Legal forms 8

Basics on legal forms 9

Eligible investments 13

Eligible investors 14

Prior authorisation 15

Fixed or variable share capital 16

Financing 17

Distributions to investors 18

Redemptions of shares/units 19

Asset valuation and publication requirements 20

Supervision 21

Basics on Luxembourg taxation 22

Taxation of the vehicle 22

Taxation of investors 24

II. Private equity at Arendt & Medernach 25

Arendt & Medernach private equity team 27

About Arendt & Medernach 28

A broad range of practice areas

5

Besides its long-standing position as European leader in the investment fund industry, Luxembourg has been increasingly appealing to the private equity community in recent years.

Luxembourg’s attractiveness in private equity results from a combination of factors which have been contributing to its success as premier international financial center: investor-friendly environment, flexible, contract-based company law provisions, responsiveness of the Luxembourg legislator to practitioners’ needs, highly skilled and multilingual community of professional service providers, and long-experienced and flexible authorities.

This brochure aims at giving its readers an overview of three of the most common Luxembourg investment vehicles used in private equity in a comparative perspective (SOPARFI, SICAR and SIF). It does not address all legal and tax aspects in relation thereto and does not purport to set out all the opportunities offered by Luxembourg to the private equity community1.

In particular, by introducing a regulatory and supervisory framework for alternative investment fund managers and indirectly investment funds, the Directive on Alternative Investment Fund Managers may have a significant impact on private equity schemes and current business models. Please refer to our brochure on the Directive on Alternative Investment Fund Managers for more details in this respect.

Introduction

1 This brochure is not intended for its content to be in any way a substitution for legal advice on specific matters.

6

l. Main Luxembourg private equity vehicles

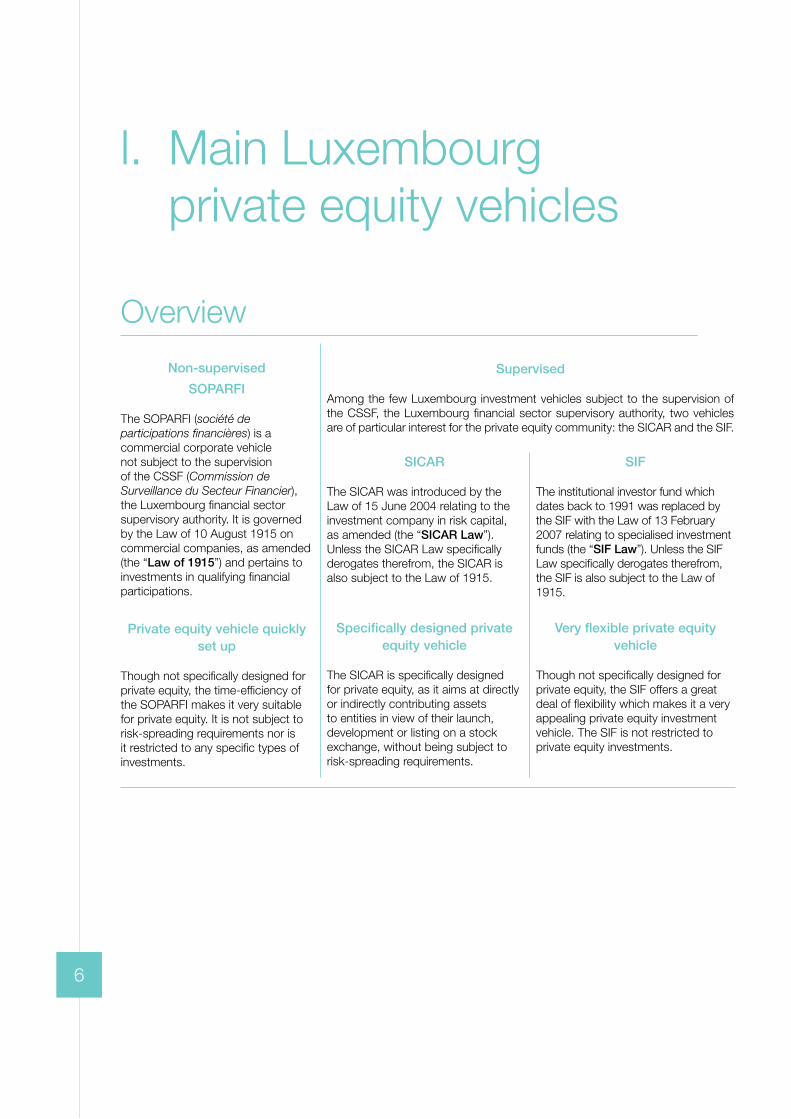

Overview

Non-supervised

SOPARFI

The SOPARFI (société de participations financières) is a commercial corporate vehicle not subject to the supervision of the CSSF (Commission de Surveillance du Secteur Financier), the Luxembourg financial sector supervisory authority. It is governed by the Law of 10 August 1915 on commercial companies, as amended (the “Law of 1915”) and pertains to investments in qualifying financial participations.

Private equity vehicle quickly set up

Though not specifically designed for private equity, the time-efficiency of the SOPARFI makes it very suitable for private equity. It is not subject to risk-spreading requirements nor is it restricted to any specific types of investments.

SICAR

The SICAR was introduced by the Law of 15 June 2004 relating to the investment company in risk capital, as amended (the “SICAR Law”). Unless the SICAR Law specifically derogates therefrom, the SICAR is also subject to the Law of 1915.

Specifically designed private equity vehicle

The SICAR is specifically designed for private equity, as it aims at directly or indirectly contributing assets to entities in view of their launch, development or listing on a stock exchange, without being subject to risk-spreading requirements.

Supervised

Among the few Luxembourg investment vehicles subject to the supervision of the CSSF, the Luxembourg financial sector supervisory authority, two vehicles are of particular interest for the private equity community: the SICAR and the SIF.

SIF

The institutional investor fund which dates back to 1991 was replaced by the SIF with the Law of 13 February 2007 relating to specialised investment funds (the “SIF Law”). Unless the SIF Law specifically derogates therefrom, the SIF is also subject to the Law of 1915.

Very flexible private equity vehicle

Though not specifically designed for private equity, the SIF offers a great deal of flexibility which makes it a very appealing private equity investment vehicle. The SIF is not restricted to private equity investments.

7

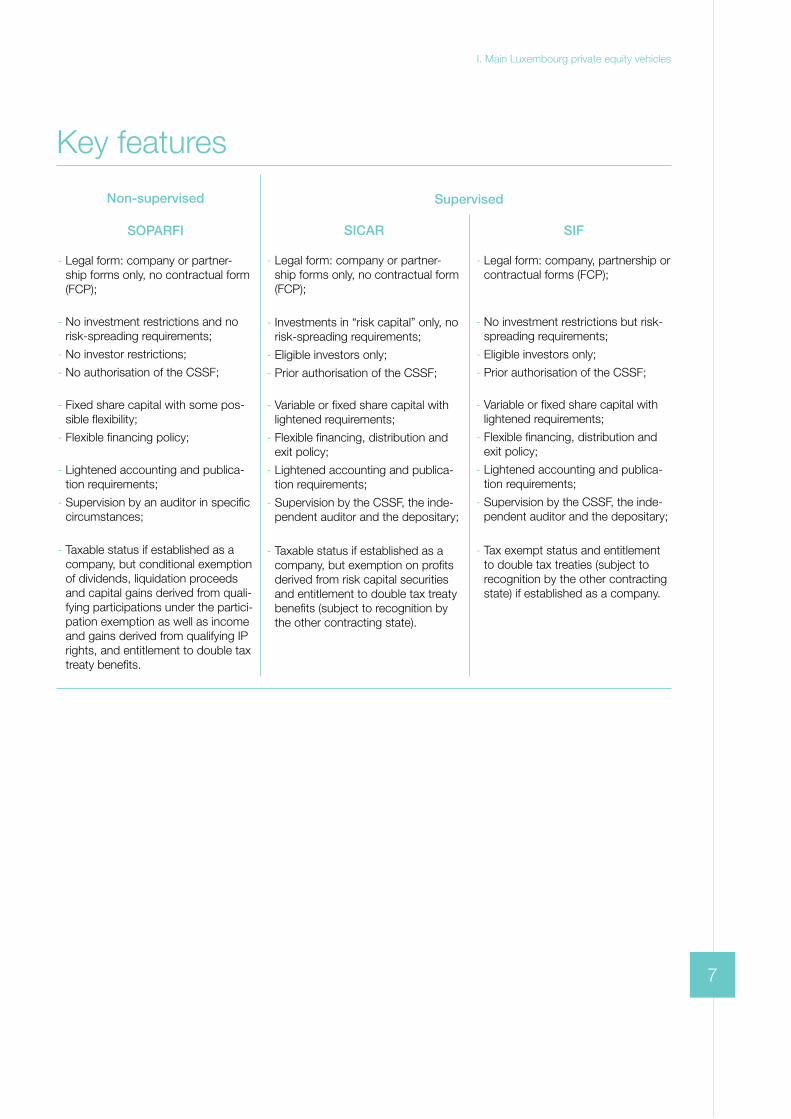

Key features

Non-supervised

SOPARFI

- Legal form: company or partner-ship forms only, no contractual form (FCP);

- No investment restrictions and no risk-spreading requirements;

- No investor restrictions;

- No authorisation of the CSSF;

- Fixed share capital with some pos-sible flexibility;

- Flexible financing policy;

- Lightened accounting and publica-tion requirements;

- Supervision by an auditor in specific circumstances;

- Taxable status if established as a company, but conditional exemption of dividends, liquidation proceeds and capital gains derived from quali-fying participations under the partici-pation exemption as well as income and gains derived from qualifying IP rights, and entitlement to double tax treaty benefits.

SICAR

- Legal form: company or partner-ship forms only, no contractual form (FCP);

- Investments in “risk capital” only, no risk-spreading requirements;

- Eligible investors only;

- Prior authorisation of the CSSF;

- Variable or fixed share capital with lightened requirements;

- Flexible financing, distribution and exit policy;

- Lightened accounting and publica-tion requirements;

- Supervision by the CSSF, the inde-pendent auditor and the depositary;

- Taxable status if established as a company, but exemption on profits derived from risk capital securities and entitlement to double tax treaty benefits (subject to recognition by the other contracting state).

Supervised

SIF

- Legal form: company, partnership or contractual forms (FCP);

- No investment restrictions but risk-spreading requirements;

- Eligible investors only;

- Prior authorisation of the CSSF;

- Variable or fixed share capital with lightened requirements;

- Flexible financing, distribution and exit policy;

- Lightened accounting and publica-tion requirements;

- Supervision by the CSSF, the inde-pendent auditor and the depositary;

- Tax exempt status and entitlement to double tax treaties (subject to recognition by the other contracting state) if established as a company.

I. Main Luxembourg private equity vehicles

8

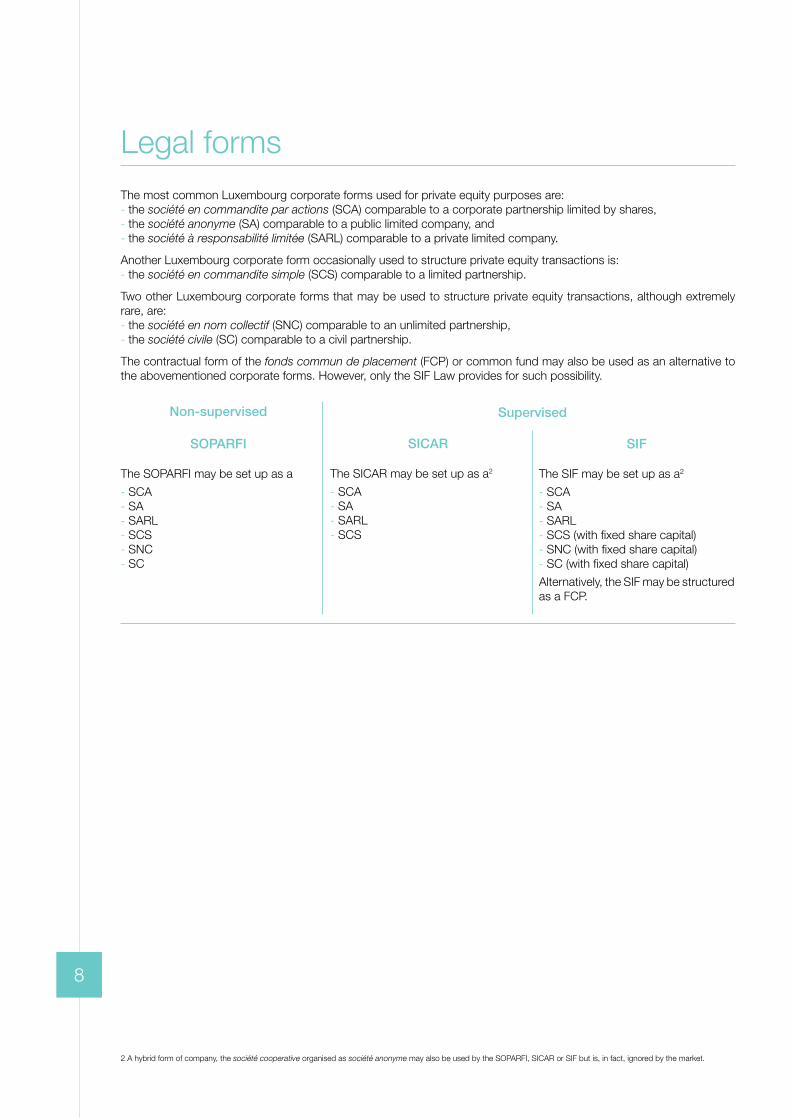

Legal formsThe most common Luxembourg corporate forms used for private equity purposes are:- the société en commandite par actions (SCA) comparable to a corporate partnership limited by shares,- the société anonyme (SA) comparable to a public limited company, and- the société à responsabilité limitée (SARL) comparable to a private limited company.

Another Luxembourg corporate form occasionally used to structure private equity transactions is:- the société en commandite simple (SCS) comparable to a limited partnership.

Two other Luxembourg corporate forms that may be used to structure private equity transactions, although extremely rare, are:- the société en nom collectif (SNC) comparable to an unlimited partnership,- the société civile (SC) comparable to a civil partnership.

The contractual form of the fonds commun de placement (FCP) or common fund may also be used as an alternative to the abovementioned corporate forms. However, only the SIF Law provides for such possibility.

Non-supervised

SOPARFI

The SOPARFI may be set up as a

- SCA- SA- SARL- SCS- SNC- SC

Supervised

SIF

The SIF may be set up as a2

- SCA- SA- SARL- SCS (with fixed share capital)- SNC (with fixed share capital)- SC (with fixed share capital)

Alternatively, the SIF may be structured as a FCP.

SICAR

The SICAR may be set up as a2

- SCA- SA- SARL- SCS

2 A hybrid form of company, the société cooperative organised as société anonyme may also be used by the SOPARFI, SICAR or SIF but is, in fact, ignored by the market.

9

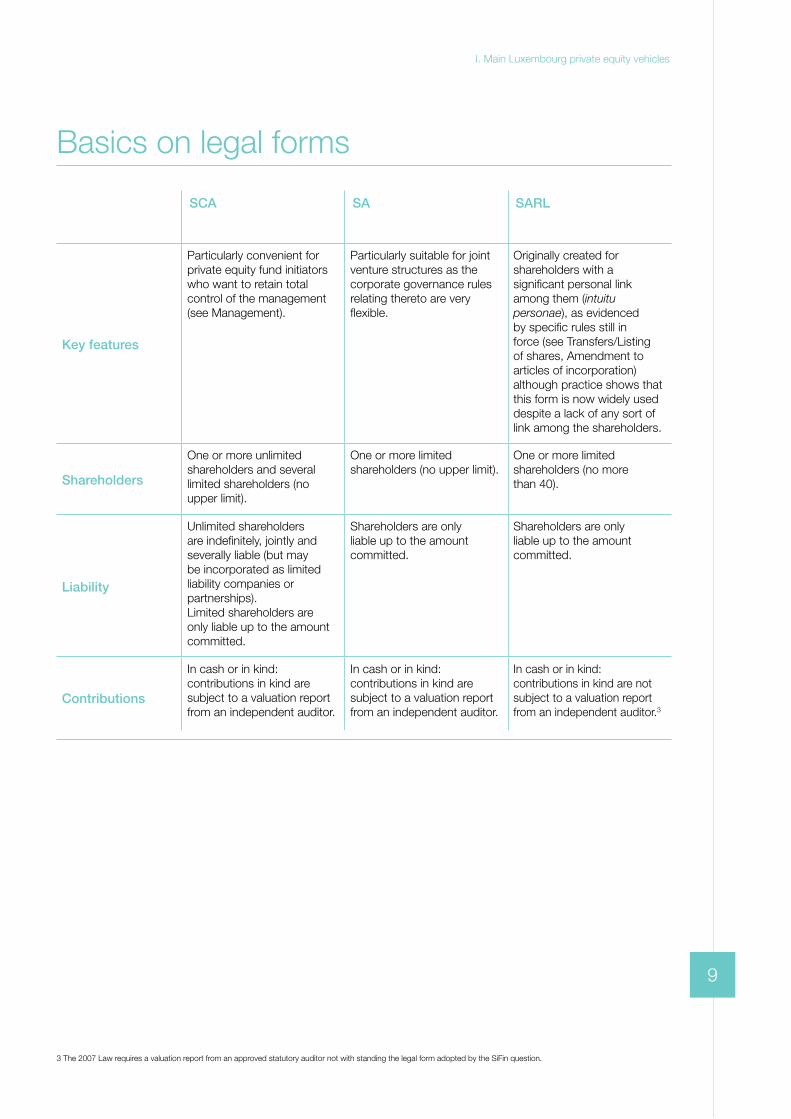

Basics on legal forms

SCA SA SARL

Key features

Particularly convenient for private equity fund initiators who want to retain total control of the management (see Management).

Particularly suitable for joint venture structures as the corporate governance rules relating thereto are very flexible.

Originally created for shareholders with a significant personal link among them (intuitu personae), as evidenced by specific rules still in force (see Transfers/Listing of shares, Amendment to articles of incorporation) although practice shows that this form is now widely used despite a lack of any sort of link among the shareholders.

Shareholders

One or more unlimited shareholders and several limited shareholders (no upper limit).

One or more limited shareholders (no upper limit).

One or more limited shareholders (no more than 40).

Liability

Unlimited shareholders are indefinitely, jointly and severally liable (but may be incorporated as limited liability companies or partnerships).Limited shareholders are only liable up to the amount committed.

Shareholders are only liable up to the amount committed.

Shareholders are only liable up to the amount committed.

Contributions

In cash or in kind: contributions in kind are subject to a valuation report from an independent auditor.

In cash or in kind: contributions in kind are subject to a valuation report from an independent auditor.

In cash or in kind: contributions in kind are not subject to a valuation report from an independent auditor.3

I. Main Luxembourg private equity vehicles

3 The 2007 Law requires a valuation report from an approved statutory auditor not with standing the legal form adopted by the SiFin question.

10

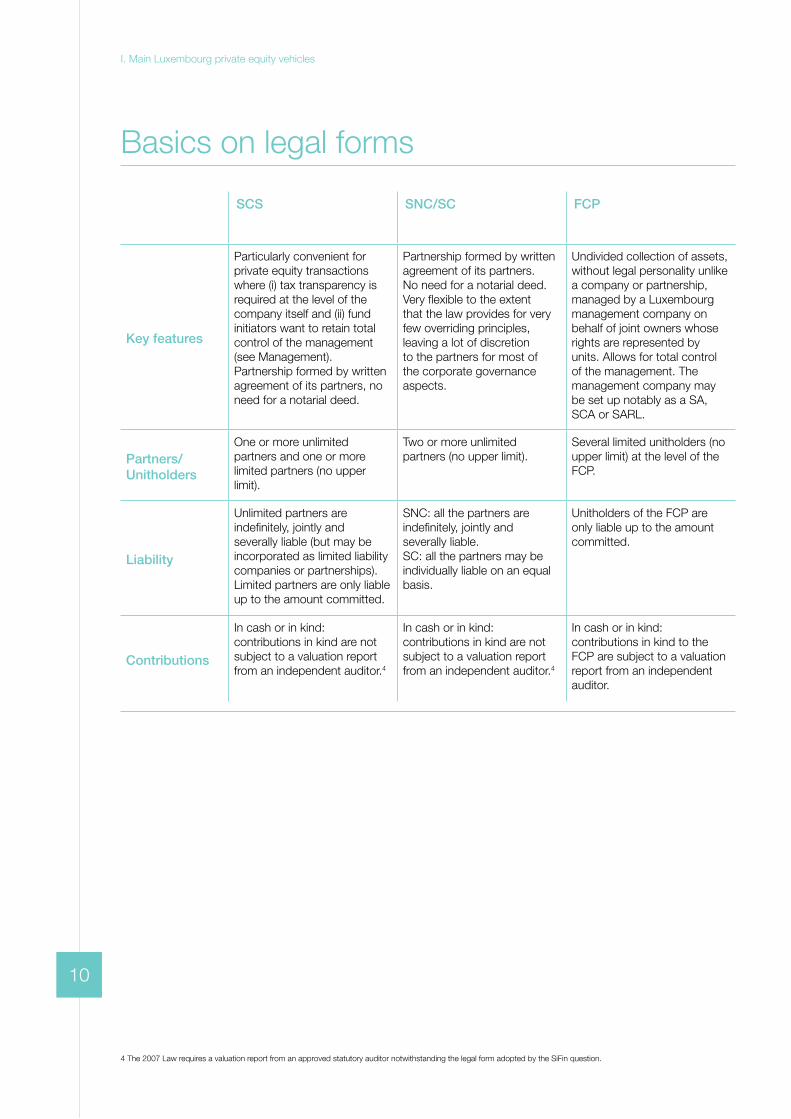

Basics on legal forms

SCS SNC/SC FCP

Key features

Particularly convenient for private equity transactions where (i) tax transparency is required at the level of the company itself and (ii) fund initiators want to retain total control of the management (see Management). Partnership formed by written agreement of its partners, no need for a notarial deed.

Partnership formed by written agreement of its partners. No need for a notarial deed. Very flexible to the extent that the law provides for very few overriding principles, leaving a lot of discretion to the partners for most of the corporate governance aspects.

Undivided collection of assets, without legal personality unlike a company or partnership, managed by a Luxembourg management company on behalf of joint owners whose rights are represented by units. Allows for total control of the management. The management company may be set up notably as a SA, SCA or SARL.

Partners/Unitholders

One or more unlimited partners and one or more limited partners (no upper limit).

Two or more unlimited partners (no upper limit).

Several limited unitholders (no upper limit) at the level of the FCP.

Liability

Unlimited partners are indefinitely, jointly and severally liable (but may be incorporated as limited liability companies or partnerships).Limited partners are only liable up to the amount committed.

SNC: all the partners are indefinitely, jointly and severally liable.SC: all the partners may be individually liable on an equal basis.

Unitholders of the FCP are only liable up to the amount committed.

Contributions

In cash or in kind: contributions in kind are not subject to a valuation report from an independent auditor.4

In cash or in kind: contributions in kind are not subject to a valuation report from an independent auditor.4

In cash or in kind: contributions in kind to the FCP are subject to a valuation report from an independent auditor.

I. Main Luxembourg private equity vehicles

4 The 2007 Law requires a valuation report from an approved statutory auditor notwithstanding the legal form adopted by the SiFin question.

11

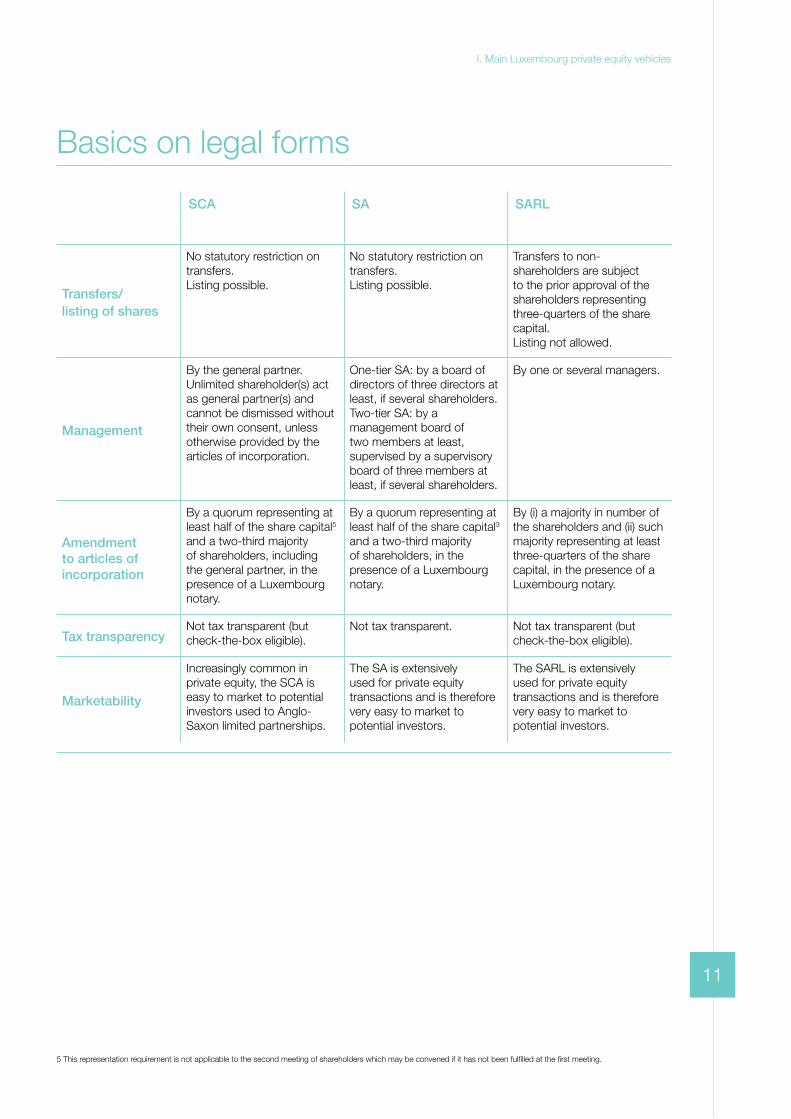

Basics on legal forms

SCA SA SARL

Transfers/listing of shares

No statutory restriction on transfers.Listing possible.

No statutory restriction on transfers.Listing possible.

Transfers to non-shareholders are subject to the prior approval of the shareholders representing three-quarters of the share capital.Listing not allowed.

Management

By the general partner. Unlimited shareholder(s) act as general partner(s) and cannot be dismissed without their own consent, unless otherwise provided by the articles of incorporation.

One-tier SA: by a board of directors of three directors at least, if several shareholders.Two-tier SA: by a management board of two members at least, supervised by a supervisory board of three members at least, if several shareholders.

By one or several managers.

Amendment to articles of incorporation

By a quorum representing at least half of the share capital5 and a two-third majority of shareholders, including the general partner, in the presence of a Luxembourg notary.

By a quorum representing at least half of the share capital3 and a two-third majority of shareholders, in the presence of a Luxembourg notary.

By (i) a majority in number of the shareholders and (ii) such majority representing at least three-quarters of the share capital, in the presence of a Luxembourg notary.

Tax transparencyNot tax transparent (but check-the-box eligible).

Not tax transparent. Not tax transparent (but check-the-box eligible).

Marketability

Increasingly common in private equity, the SCA is easy to market to potential investors used to Anglo-Saxon limited partnerships.

The SA is extensively used for private equity transactions and is therefore very easy to market to potential investors.

The SARL is extensively used for private equity transactions and is therefore very easy to market to potential investors.

I. Main Luxembourg private equity vehicles

5 This representation requirement is not applicable to the second meeting of shareholders which may be convened if it has not been fulfilled at the first meeting.

12

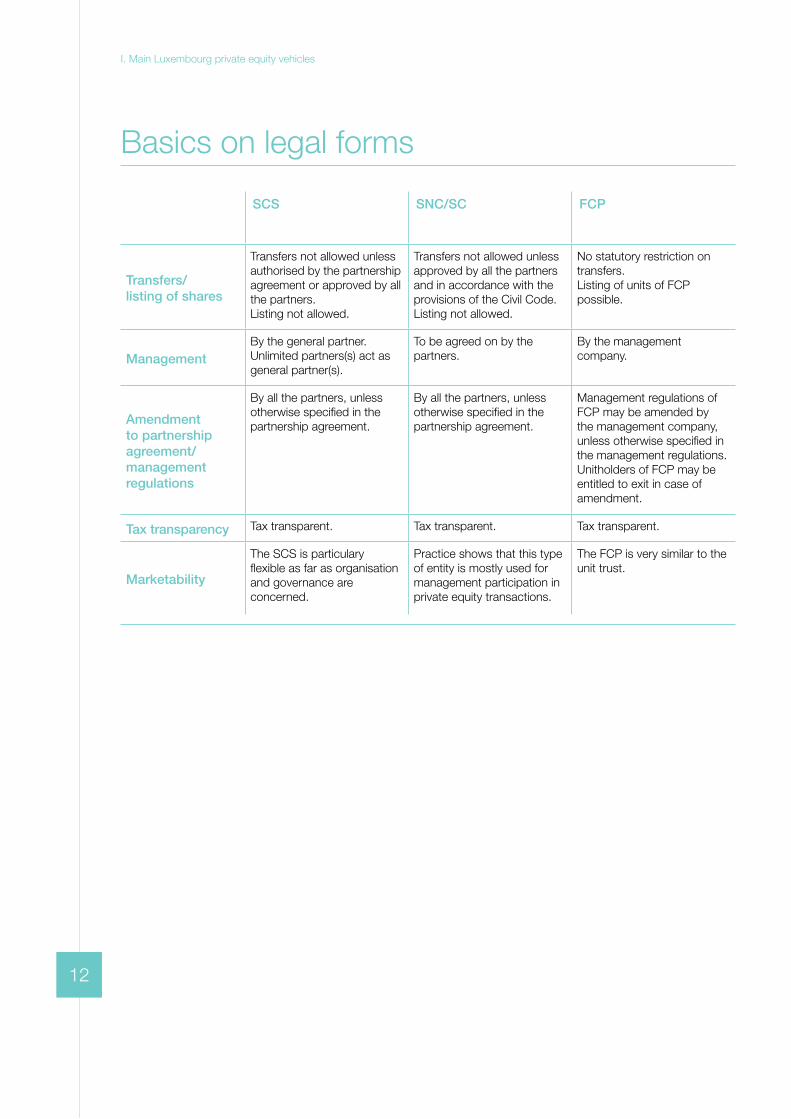

Basics on legal forms

SCS SNC/SC FCP

Transfers/listing of shares

Transfers not allowed unless authorised by the partnership agreement or approved by all the partners.Listing not allowed.

Transfers not allowed unless approved by all the partners and in accordance with the provisions of the Civil Code.Listing not allowed.

No statutory restriction on transfers.Listing of units of FCP possible.

ManagementBy the general partner. Unlimited partners(s) act as general partner(s).

To be agreed on by the partners.

By the management company.

Amendmentto partnershipagreement/managementregulations

By all the partners, unless otherwise specified in the partnership agreement.

By all the partners, unless otherwise specified in the partnership agreement.

Management regulations of FCP may be amended by the management company, unless otherwise specified in the management regulations. Unitholders of FCP may be entitled to exit in case of amendment.

Tax transparency Tax transparent. Tax transparent. Tax transparent.

Marketability

The SCS is particulary flexible as far as organisation and governance are concerned.

Practice shows that this type of entity is mostly used for management participation in private equity transactions.

The FCP is very similar to theunit trust.

I. Main Luxembourg private equity vehicles

13

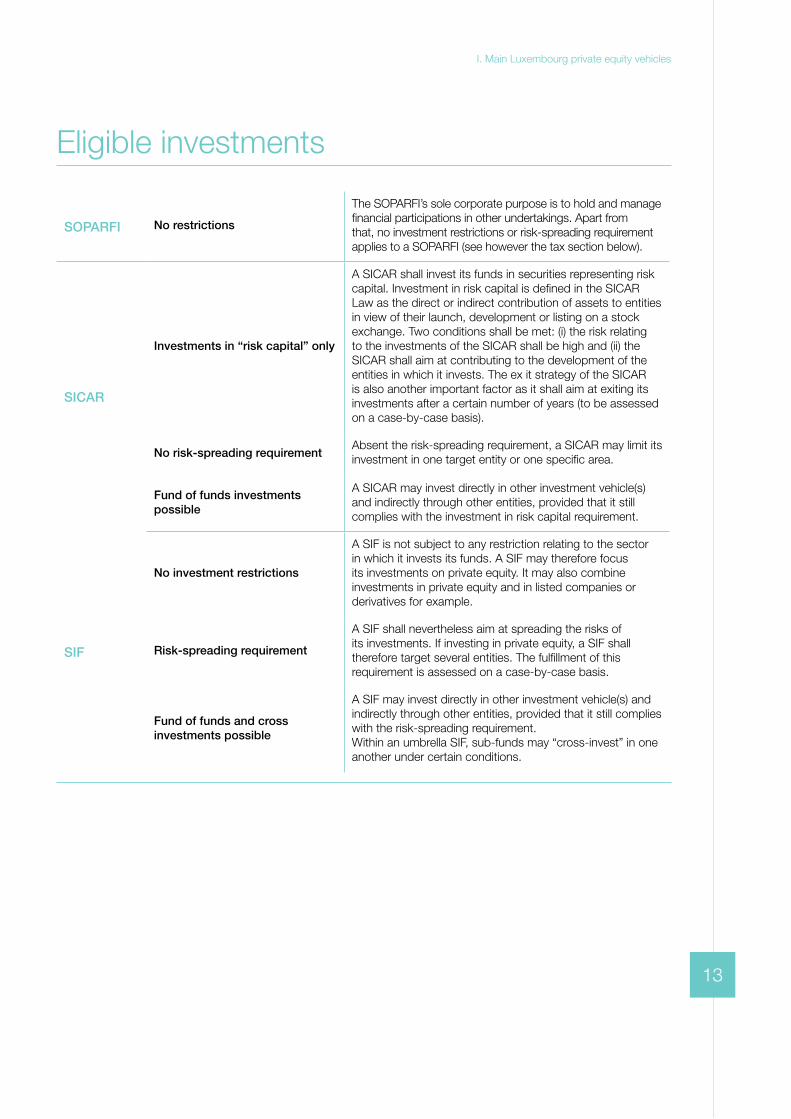

Eligible investments

SOPARFI No restrictions

The SOPARFI’s sole corporate purpose is to hold and manage financial participations in other undertakings. Apart from that, no investment restrictions or risk-spreading requirement applies to a SOPARFI (see however the tax section below).

SICAR

Investments in “risk capital” only

A SICAR shall invest its funds in securities representing risk capital. Investment in risk capital is defined in the SICAR Law as the direct or indirect contribution of assets to entities in view of their launch, development or listing on a stock exchange. Two conditions shall be met: (i) the risk relating to the investments of the SICAR shall be high and (ii) the SICAR shall aim at contributing to the development of the entities in which it invests. The ex it strategy of the SICAR is also another important factor as it shall aim at exiting its investments after a certain number of years (to be assessed on a case-by-case basis).

No risk-spreading requirementAbsent the risk-spreading requirement, a SICAR may limit its investment in one target entity or one specific area.

Fund of funds investments possible

A SICAR may invest directly in other investment vehicle(s) and indirectly through other entities, provided that it still complies with the investment in risk capital requirement.

SIF

No investment restrictions

A SIF is not subject to any restriction relating to the sector in which it invests its funds. A SIF may therefore focus its investments on private equity. It may also combine investments in private equity and in listed companies or derivatives for example.

Risk-spreading requirement

A SIF shall nevertheless aim at spreading the risks of its investments. If investing in private equity, a SIF shall therefore target several entities. The fulfillment of this requirement is assessed on a case-by-case basis.

Fund of funds and crossinvestments possible

A SIF may invest directly in other investment vehicle(s) and indirectly through other entities, provided that it still complies with the risk-spreading requirement. Within an umbrella SIF, sub-funds may “cross-invest” in one another under certain conditions.

I. Main Luxembourg private equity vehicles

14

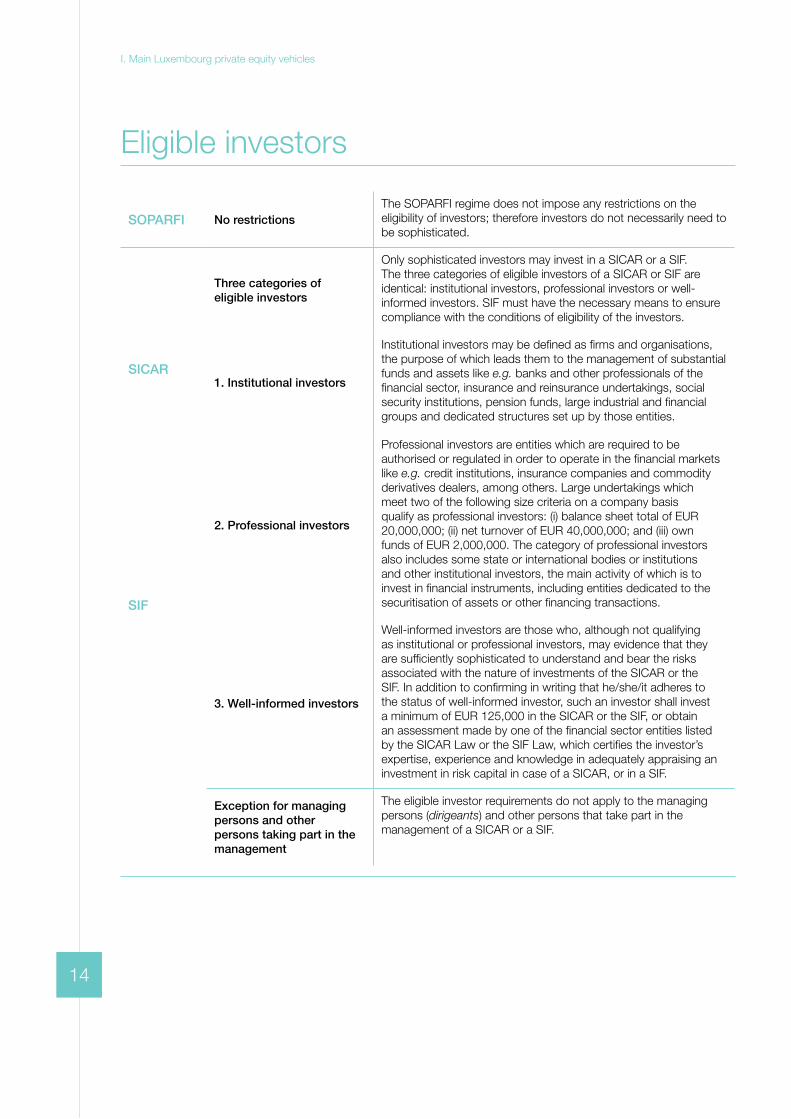

Eligible investors

SOPARFI No restrictionsThe SOPARFI regime does not impose any restrictions on the eligibility of investors; therefore investors do not necessarily need to be sophisticated.

SICAR

SIF

Three categories ofeligible investors

Only sophisticated investors may invest in a SICAR or a SIF. The three categories of eligible investors of a SICAR or SIF are identical: institutional investors, professional investors or well-informed investors. SIF must have the necessary means to ensure compliance with the conditions of eligibility of the investors.

1. Institutional investors

Institutional investors may be defined as firms and organisations, the purpose of which leads them to the management of substantial funds and assets like e.g. banks and other professionals of the financial sector, insurance and reinsurance undertakings, social security institutions, pension funds, large industrial and financial groups and dedicated structures set up by those entities.

2. Professional investors

Professional investors are entities which are required to be authorised or regulated in order to operate in the financial markets like e.g. credit institutions, insurance companies and commodity derivatives dealers, among others. Large undertakings which meet two of the following size criteria on a company basis qualify as professional investors: (i) balance sheet total of EUR 20,000,000; (ii) net turnover of EUR 40,000,000; and (iii) own funds of EUR 2,000,000. The category of professional investors also includes some state or international bodies or institutions and other institutional investors, the main activity of which is to invest in financial instruments, including entities dedicated to the securitisation of assets or other financing transactions.

3. Well-informed investors

Well-informed investors are those who, although not qualifying as institutional or professional investors, may evidence that they are sufficiently sophisticated to understand and bear the risks associated with the nature of investments of the SICAR or the SIF. In addition to confirming in writing that he/she/it adheres to the status of well-informed investor, such an investor shall invest a minimum of EUR 125,000 in the SICAR or the SIF, or obtain an assessment made by one of the financial sector entities listed by the SICAR Law or the SIF Law, which certifies the investor’s expertise, experience and knowledge in adequately appraising an investment in risk capital in case of a SICAR, or in a SIF.

Exception for managing persons and other persons taking part in the management

The eligible investor requirements do not apply to the managing persons (dirigeants) and other persons that take part in the management of a SICAR or a SIF.

I. Main Luxembourg private equity vehicles

15

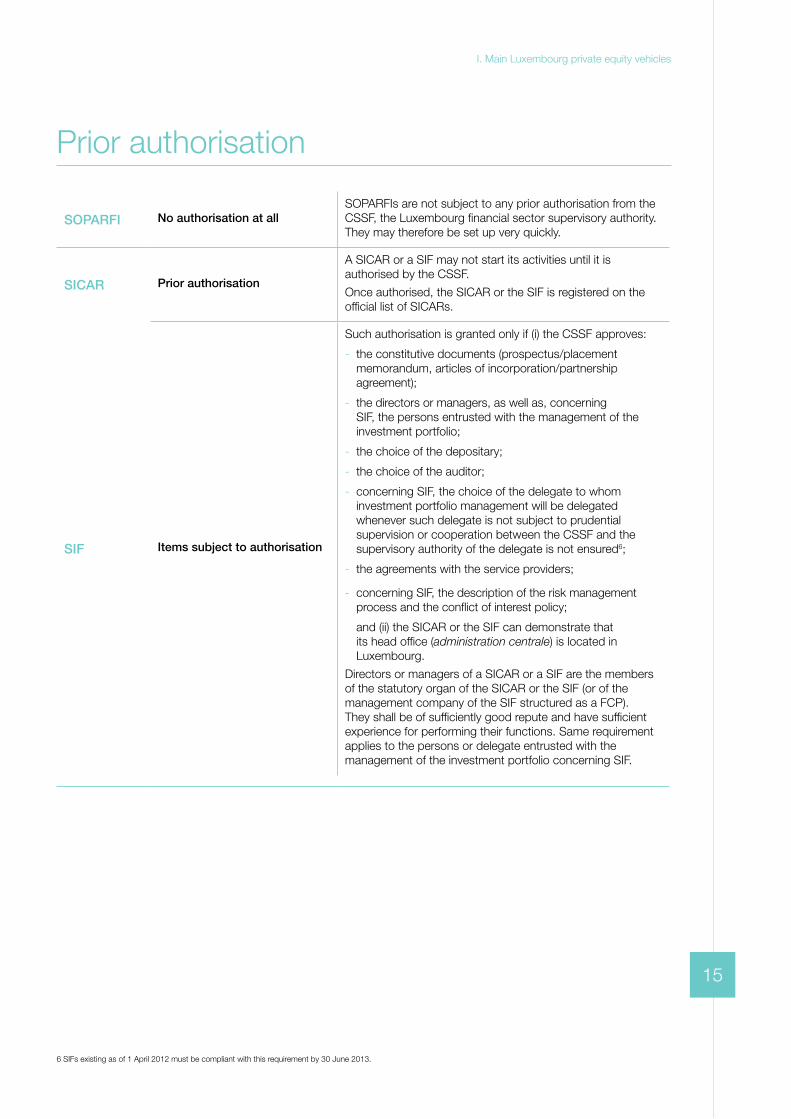

Prior authorisation

SOPARFI No authorisation at allSOPARFIs are not subject to any prior authorisation from the CSSF, the Luxembourg financial sector supervisory authority. They may therefore be set up very quickly.

SICAR Prior authorisation

A SICAR or a SIF may not start its activities until it is authorised by the CSSF.

Once authorised, the SICAR or the SIF is registered on the official list of SICARs.

SIF Items subject to authorisation

Such authorisation is granted only if (i) the CSSF approves:

- the constitutive documents (prospectus/placement memorandum, articles of incorporation/partnership agreement);

- the directors or managers, as well as, concerning SIF, the persons entrusted with the management of the investment portfolio;

- the choice of the depositary;

- the choice of the auditor;

- concerning SIF, the choice of the delegate to whom investment portfolio management will be delegated whenever such delegate is not subject to prudential supervision or cooperation between the CSSF and the supervisory authority of the delegate is not ensured6;

- the agreements with the service providers;

- concerning SIF, the description of the risk management process and the conflict of interest policy;

and (ii) the SICAR or the SIF can demonstrate that its head office (administration centrale) is located in Luxembourg.

Directors or managers of a SICAR or a SIF are the members of the statutory organ of the SICAR or the SIF (or of the management company of the SIF structured as a FCP). They shall be of sufficiently good repute and have sufficient experience for performing their functions. Same requirement applies to the persons or delegate entrusted with the management of the investment portfolio concerning SIF.

I. Main Luxembourg private equity vehicles

6 SIFs existing as of 1 April 2012 must be compliant with this requirement by 30 June 2013.

16

Fixed or variable share capital

SOPARFI

Only fixed share capital, but authorised capital possible

The share capital of a SOPARFI must be fixed to an amount set forth in the articles of incorporation/partnership agreement. As a result, any issue of new shares is subject to the formalities, quorum and majority requirements applicable to amendments of the articles of incorporation/partnership agreement (see p. 10 and 11). However, a SOPARFI set up as a SA or SCA may provide for an authorised share capital whereby the shareholders delegate to the management their power to increase the share capital within certain limits.

Nominal or par valueshare issue price

New shares of a SOPARFI are usually issued at (and cannot be issued below) the nominal value, if any, or par value of existing shares, possibly with a share premium.

Payment of sharesrequirements dependingon legal form

Each of the shares of a SA or SCA must be paid up up to at least 25%. Each of the shares of a SARL must be entirely paid up. No requirement applies to the payment of shares in a SCS, SNC or SC.

SICAR/SIF

Variable share capital possible

A SICAR set up as a SA, SCA, SARL or SCS, or a SIF set up as a SA, SCA or SARL may have a variable share capital, i.e. a share capital the amount of which is equal to the net asset value of the company at all times. A SICAR or SIF with variable share capital, as well as a SIF structured as a FCP can issue new shares/units in accordance with the conditions and procedures set forth in its articles of incorporation/management regulations.

Net asset value share issue price

New shares of SICAR or SIF may be issued on the basis of the net asset value per share or any other value, according to the method set forth in its articles of incorporation/management regulations.

5% paid-up shares

Each of the shares of a SICAR or SIF must be paid up up to at least 5%, except for a SICAR or SIF set up as a SCS and for a SIF set up as a SNC or a SC, in which case no such minimum applies.

I. Main Luxembourg private equity vehicles

17

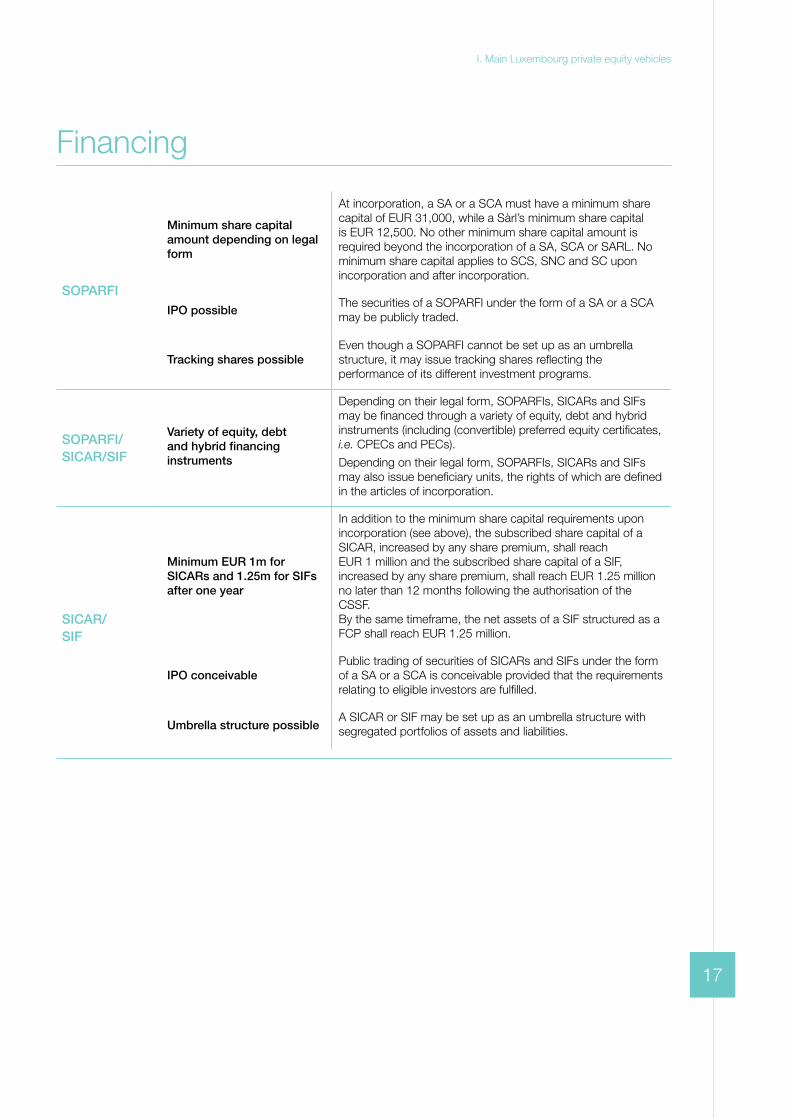

Financing

SOPARFI

Minimum share capital amount depending on legal form

At incorporation, a SA or a SCA must have a minimum share capital of EUR 31,000, while a Sàrl’s minimum share capital is EUR 12,500. No other minimum share capital amount is required beyond the incorporation of a SA, SCA or SARL. No minimum share capital applies to SCS, SNC and SC upon incorporation and after incorporation.

IPO possibleThe securities of a SOPARFI under the form of a SA or a SCA may be publicly traded.

Tracking shares possibleEven though a SOPARFI cannot be set up as an umbrella structure, it may issue tracking shares reflecting the performance of its different investment programs.

SOPARFI/SICAR/SIF

Variety of equity, debt and hybrid financing instruments

Depending on their legal form, SOPARFIs, SICARs and SIFs may be financed through a variety of equity, debt and hybrid instruments (including (convertible) preferred equity certificates, i.e. CPECs and PECs).

Depending on their legal form, SOPARFIs, SICARs and SIFs may also issue beneficiary units, the rights of which are defined in the articles of incorporation.

SICAR/SIF

Minimum EUR 1m for SICARs and 1.25m for SIFs after one year

In addition to the minimum share capital requirements upon incorporation (see above), the subscribed share capital of a SICAR, increased by any share premium, shall reach EUR 1 million and the subscribed share capital of a SIF, increased by any share premium, shall reach EUR 1.25 million no later than 12 months following the authorisation of the CSSF.By the same timeframe, the net assets of a SIF structured as a FCP shall reach EUR 1.25 million.

IPO conceivablePublic trading of securities of SICARs and SIFs under the form of a SA or a SCA is conceivable provided that the requirements relating to eligible investors are fulfilled.

Umbrella structure possibleA SICAR or SIF may be set up as an umbrella structure with segregated portfolios of assets and liabilities.

I. Main Luxembourg private equity vehicles

18

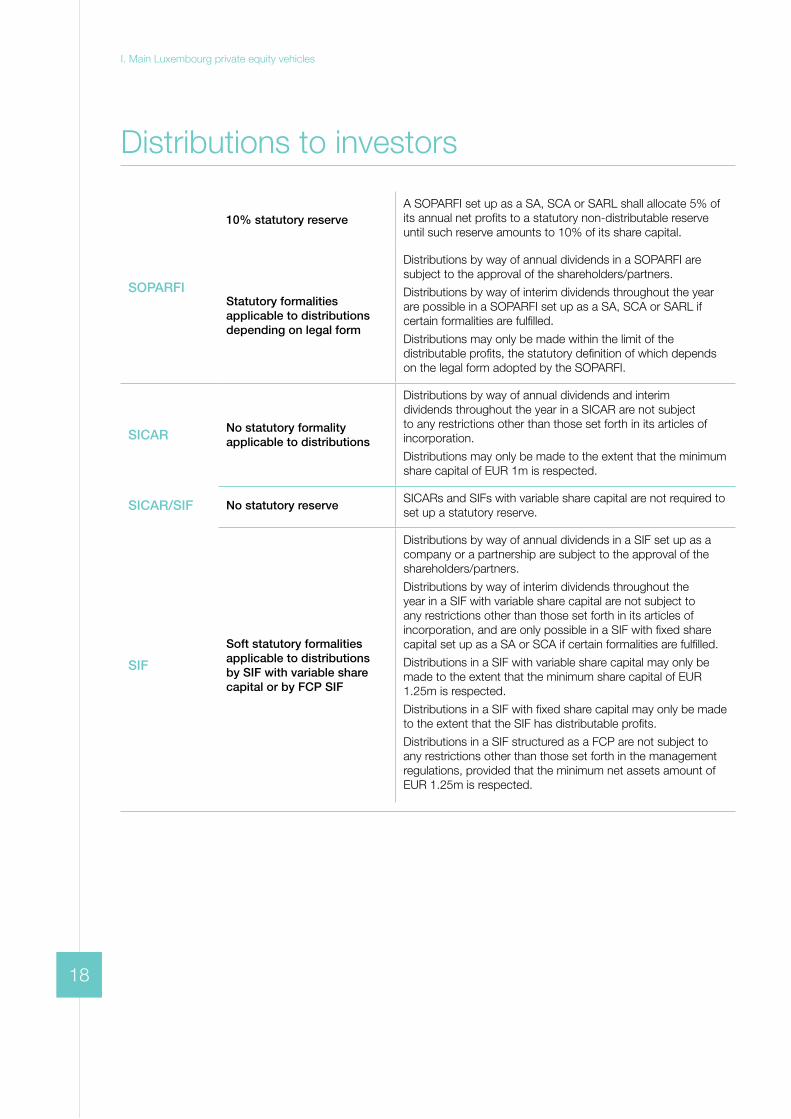

Distributions to investors

SOPARFI

10% statutory reserveA SOPARFI set up as a SA, SCA or SARL shall allocate 5% of its annual net profits to a statutory non-distributable reserve until such reserve amounts to 10% of its share capital.

Statutory formalities applicable to distributions depending on legal form

Distributions by way of annual dividends in a SOPARFI are subject to the approval of the shareholders/partners.

Distributions by way of interim dividends throughout the year are possible in a SOPARFI set up as a SA, SCA or SARL if certain formalities are fulfilled.

Distributions may only be made within the limit of the distributable profits, the statutory definition of which depends on the legal form adopted by the SOPARFI.

SICAR No statutory formality applicable to distributions

Distributions by way of annual dividends and interim dividends throughout the year in a SICAR are not subject to any restrictions other than those set forth in its articles of incorporation.

Distributions may only be made to the extent that the minimum share capital of EUR 1m is respected.

SICAR/SIF No statutory reserveSICARs and SIFs with variable share capital are not required to set up a statutory reserve.

SIF

Soft statutory formalitiesapplicable to distributionsby SIF with variable sharecapital or by FCP SIF

Distributions by way of annual dividends in a SIF set up as a company or a partnership are subject to the approval of the shareholders/partners.

Distributions by way of interim dividends throughout the year in a SIF with variable share capital are not subject to any restrictions other than those set forth in its articles of incorporation, and are only possible in a SIF with fixed share capital set up as a SA or SCA if certain formalities are fulfilled.

Distributions in a SIF with variable share capital may only be made to the extent that the minimum share capital of EUR 1.25m is respected.

Distributions in a SIF with fixed share capital may only be made to the extent that the SIF has distributable profits.

Distributions in a SIF structured as a FCP are not subject to any restrictions other than those set forth in the management regulations, provided that the minimum net assets amount of EUR 1.25m is respected.

I. Main Luxembourg private equity vehicles

19

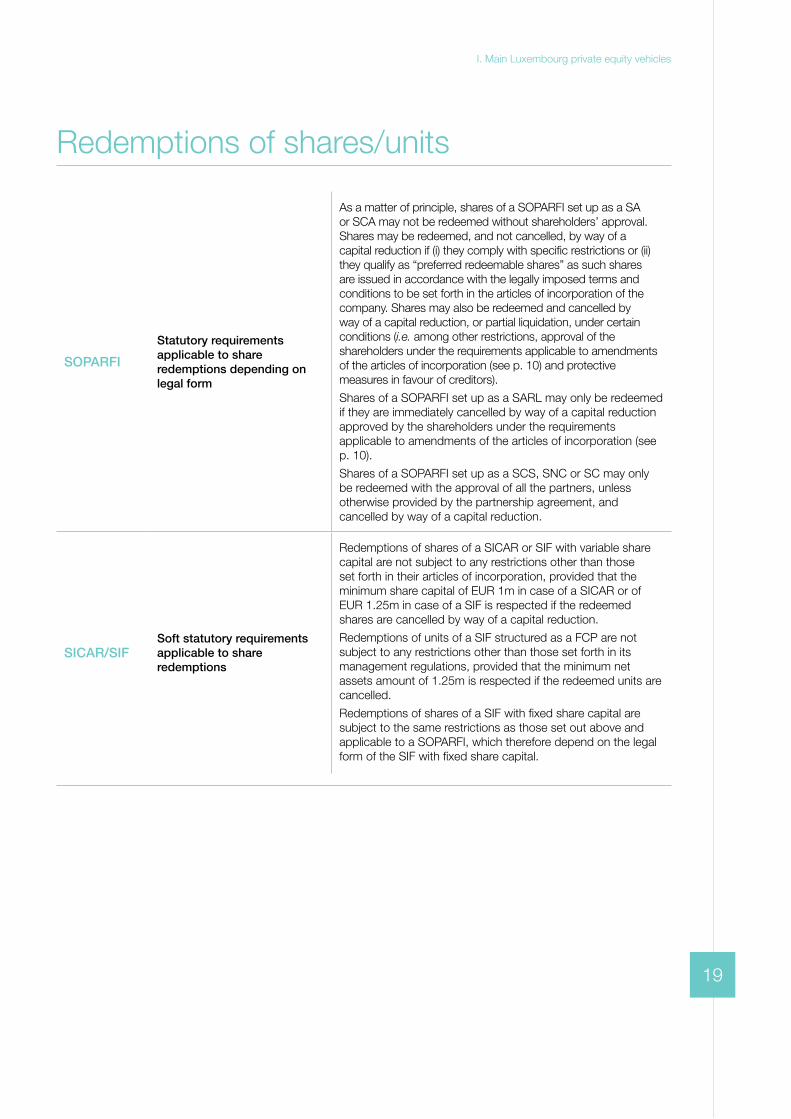

Redemptions of shares/units

SOPARFI

Statutory requirements applicable to share redemptions depending on legal form

As a matter of principle, shares of a SOPARFI set up as a SA or SCA may not be redeemed without shareholders’ approval. Shares may be redeemed, and not cancelled, by way of a capital reduction if (i) they comply with specific restrictions or (ii) they qualify as “preferred redeemable shares” as such shares are issued in accordance with the legally imposed terms and conditions to be set forth in the articles of incorporation of the company. Shares may also be redeemed and cancelled by way of a capital reduction, or partial liquidation, under certain conditions (i.e. among other restrictions, approval of the shareholders under the requirements applicable to amendments of the articles of incorporation (see p. 10) and protective measures in favour of creditors).

Shares of a SOPARFI set up as a SARL may only be redeemed if they are immediately cancelled by way of a capital reduction approved by the shareholders under the requirements applicable to amendments of the articles of incorporation (see p. 10).

Shares of a SOPARFI set up as a SCS, SNC or SC may only be redeemed with the approval of all the partners, unless otherwise provided by the partnership agreement, and cancelled by way of a capital reduction.

SICAR/SIFSoft statutory requirementsapplicable to share redemptions

Redemptions of shares of a SICAR or SIF with variable share capital are not subject to any restrictions other than those set forth in their articles of incorporation, provided that the minimum share capital of EUR 1m in case of a SICAR or of EUR 1.25m in case of a SIF is respected if the redeemed shares are cancelled by way of a capital reduction.

Redemptions of units of a SIF structured as a FCP are not subject to any restrictions other than those set forth in its management regulations, provided that the minimum net assets amount of 1.25m is respected if the redeemed units are cancelled.

Redemptions of shares of a SIF with fixed share capital are subject to the same restrictions as those set out above and applicable to a SOPARFI, which therefore depend on the legal form of the SIF with fixed share capital.

I. Main Luxembourg private equity vehicles

20

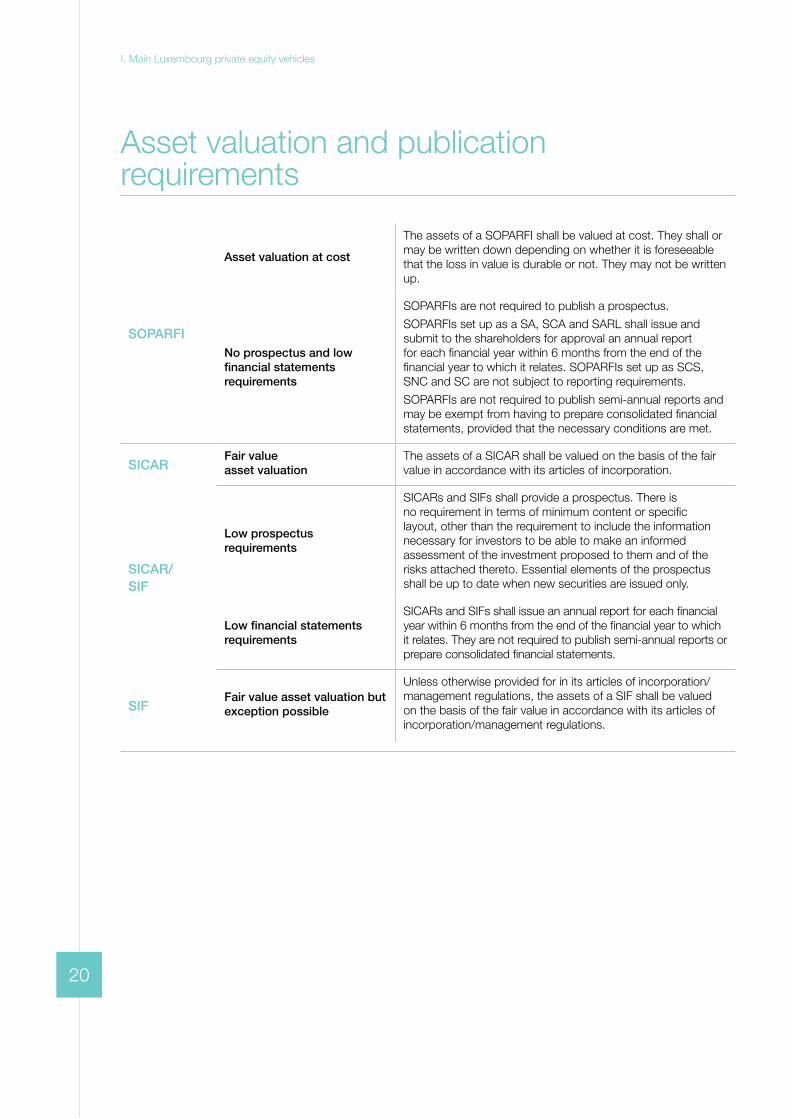

Asset valuation and publicationrequirements

SOPARFI

Asset valuation at cost

The assets of a SOPARFI shall be valued at cost. They shall or may be written down depending on whether it is foreseeable that the loss in value is durable or not. They may not be written up.

No prospectus and low financial statements requirements

SOPARFIs are not required to publish a prospectus.

SOPARFIs set up as a SA, SCA and SARL shall issue and submit to the shareholders for approval an annual report for each financial year within 6 months from the end of the financial year to which it relates. SOPARFIs set up as SCS, SNC and SC are not subject to reporting requirements.

SOPARFIs are not required to publish semi-annual reports and may be exempt from having to prepare consolidated financial statements, provided that the necessary conditions are met.

SICARFair valueasset valuation

The assets of a SICAR shall be valued on the basis of the fair value in accordance with its articles of incorporation.

SICAR/SIF

Low prospectus requirements

SICARs and SIFs shall provide a prospectus. There is no requirement in terms of minimum content or specific layout, other than the requirement to include the information necessary for investors to be able to make an informed assessment of the investment proposed to them and of the risks attached thereto. Essential elements of the prospectus shall be up to date when new securities are issued only.

Low financial statementsrequirements

SICARs and SIFs shall issue an annual report for each financial year within 6 months from the end of the financial year to which it relates. They are not required to publish semi-annual reports or prepare consolidated financial statements.

SIFFair value asset valuation but exception possible

Unless otherwise provided for in its articles of incorporation/management regulations, the assets of a SIF shall be valued on the basis of the fair value in accordance with its articles of incorporation/management regulations.

I. Main Luxembourg private equity vehicles

21

Supervision

SOPARFI

No CSSF supervision,no depositary

SOPARFIs are not submitted to the supervision of the CSSF and are not required to entrust the custody of their assets with a depositary.

SA, SCA and SARLare subject to supervisionby auditors

However, the operations and the annual financial statements shall be supervised by one or more statutory auditor(s) in a SA, a supervisory board in a SCA and one or more statutory auditor(s) in a SARL, unless the SARL has less than 25 shareholders. No statutory auditor is required in SOPARFIs set up as SCS, SNC or SC.

In addition, an independent auditor shall be appointed and replace the statutory auditor(s) in a SOPARFI set up as a SA, SCA or SARL if certain thresholds (on total balance sheet, turnover and/or number of employees) are exceeded.

SICARPermanent supervisionby the CSSF

SICARs and SIFs remain subject to the permanent supervision of the CSSF until their liquidation.

Any amendment to their constitutive documents (prospectus/placement memorandum, articles of incorporation/partnership agreement), any appointment of new directors or managers and any change of the management company (of a SIF structured as a FCP) or their depositary is subject to prior approval of the CSSF.

SICAR/SIF DepositaryA depositary located in Luxembourg and qualifying as a credit institution shall be entrusted with the oversight of the assets of SICARs and SIFs.

SIF Audit

A Luxembourg independent auditor shall audit the accounting information contained in the annual reports of SICARs and SIFs. The auditor’s report and qualifications, if any, shall be included in full in the annual report of SICARs and SIFs. In addition, the auditor has some duties of notification to, and of extensive supervision at the request of, the CSSF in certain circumstances.

SIF

Risk Management

Appropriate risk management systems must be implemented in order to detect measure, manage and monitor the risk of the position and their contribution to the overall risk profile of the portfolio.

Conflict of Interest

SIF must be structured and organised in such a way to minimize the risk of investors’ interests being prejudiced by conflicts of interest arising between the SIF and any person contributing to the business activity of the SIF or linked to the SIF.

I. Main Luxembourg private equity vehicles

22

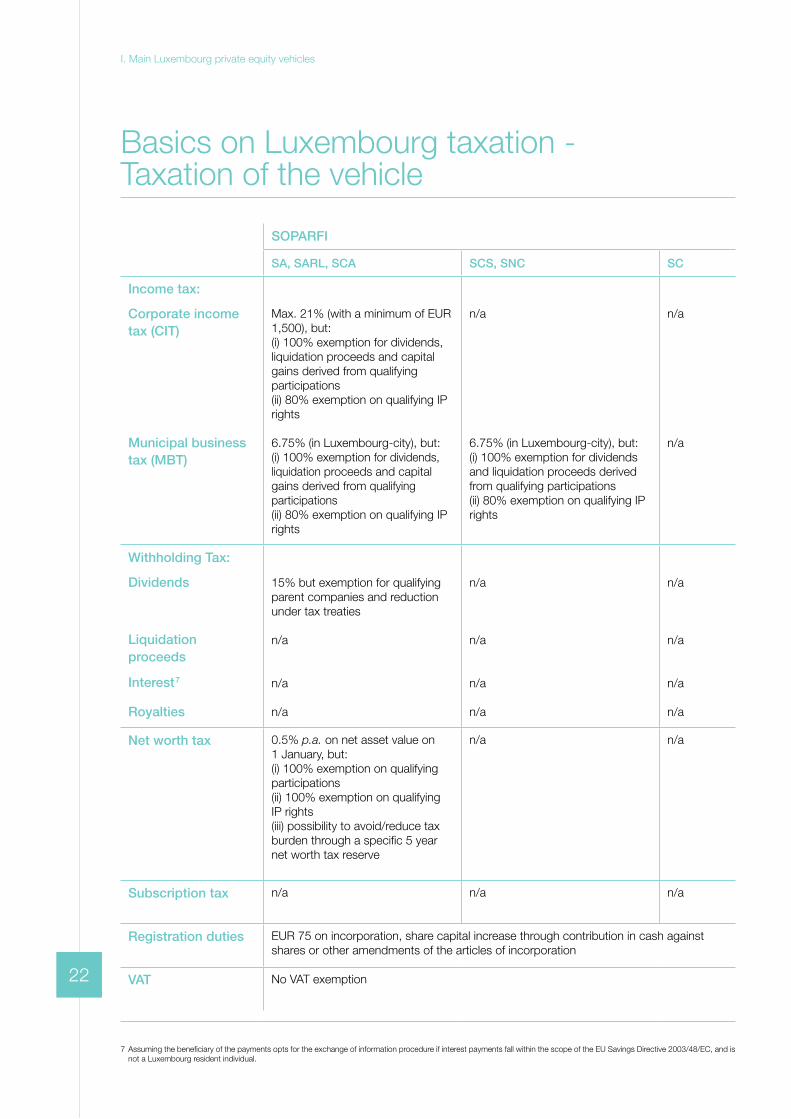

SOPARFI

SA, SARL, SCA SCS, SNC SC

Income tax:

Corporate income tax (CIT)

Municipal business tax (MBT)

Max. 21% (with a minimum of EUR 1,500), but:(i) 100% exemption for dividends, liquidation proceeds and capital gains derived from qualifying participations(ii) 80% exemption on qualifying IP rights

6.75% (in Luxembourg-city), but:(i) 100% exemption for dividends, liquidation proceeds and capital gains derived from qualifying participations(ii) 80% exemption on qualifying IP rights

n/a

6.75% (in Luxembourg-city), but:(i) 100% exemption for dividends and liquidation proceeds derived from qualifying participations(ii) 80% exemption on qualifying IP rights

n/a

n/a

Withholding Tax:

Dividends

Liquidation proceeds

Interest7

Royalties

15% but exemption for qualifying parent companies and reduction under tax treaties

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

Net worth tax 0.5% p.a. on net asset value on 1 January, but:(i) 100% exemption on qualifying participations(ii) 100% exemption on qualifying IP rights(iii) possibility to avoid/reduce tax burden through a specific 5 year net worth tax reserve

n/a n/a

Subscription tax n/a n/a n/a

Registration duties EUR 75 on incorporation, share capital increase through contribution in cash against shares or other amendments of the articles of incorporation

VAT No VAT exemption

Basics on Luxembourg taxation - Taxation of the vehicle

I. Main Luxembourg private equity vehicles

7 Assuming the beneficiary of the payments opts for the exchange of information procedure if interest payments fall within the scope of the EU Savings Directive 2003/48/EC, and is not a Luxembourg resident individual.

23

Basics on Luxembourg taxation - Taxation of the vehicle

I. Main Luxembourg private equity vehicles

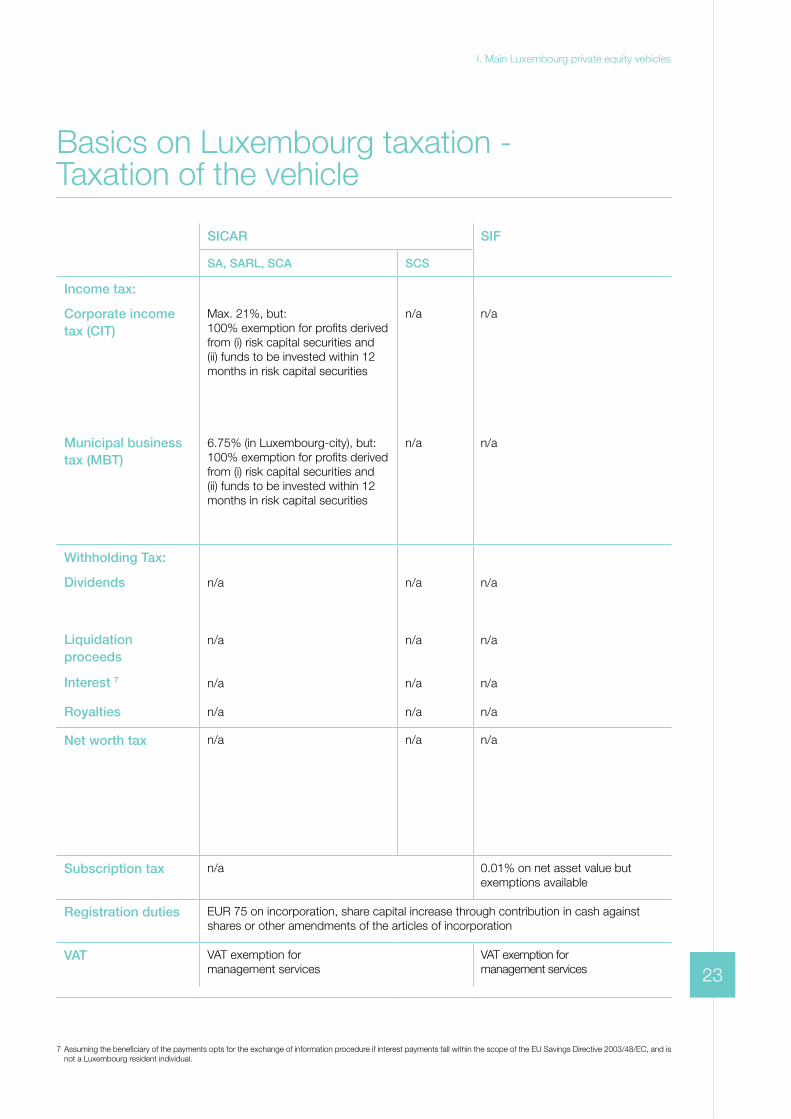

SICAR SIF

SA, SARL, SCA SCS

Income tax:

Corporate income tax (CIT)

Municipal business tax (MBT)

Max. 21%, but:100% exemption for profits derived from (i) risk capital securities and (ii) funds to be invested within 12 months in risk capital securities

6.75% (in Luxembourg-city), but:100% exemption for profits derived from (i) risk capital securities and (ii) funds to be invested within 12 months in risk capital securities

n/a

n/a

n/a

n/a

Withholding Tax:

Dividends

Liquidation proceeds

Interest 7

Royalties

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

n/a

Net worth tax n/a n/a n/a

Subscription tax n/a 0.01% on net asset value but exemptions available

Registration duties EUR 75 on incorporation, share capital increase through contribution in cash against shares or other amendments of the articles of incorporation

VAT VAT exemption for management services

VAT exemption for management services

7 Assuming the beneficiary of the payments opts for the exchange of information procedure if interest payments fall within the scope of the EU Savings Directive 2003/48/EC, and is not a Luxembourg resident individual.

24

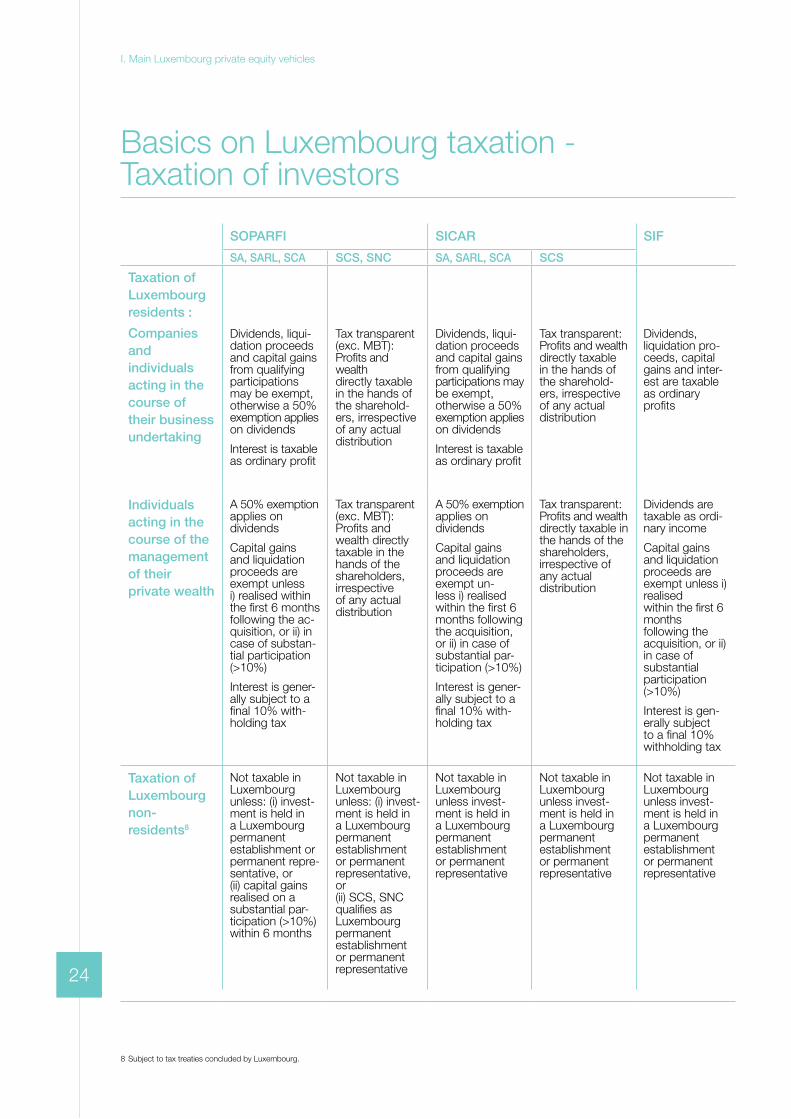

SOPARFI SICAR SIF

SA, SARL, SCA SCS, SNC SA, SARL, SCA SCS

Taxation of Luxembourg residents :

Companiesand individuals acting in the course of their business undertaking

Dividends, liqui-dation proceeds and capital gains from qualifying participations may be exempt, otherwise a 50% exemption applies on dividends

Interest is taxable as ordinary profit

Tax transparent (exc. MBT): Profits and wealth directly taxable in the hands of the sharehold-ers, irrespective of any actual distribution

Dividends, liqui-dation proceeds and capital gains from qualifying participations may be exempt, otherwise a 50% exemption applies on dividends

Interest is taxable as ordinary profit

Tax transparent: Profits and wealth directly taxable in the hands of the sharehold-ers, irrespective of any actual distribution

Dividends, liquidation pro-ceeds, capital gains and inter-est are taxable as ordinary profits

Individualsacting in the course of the managementof their private wealth

A 50% exemption applies on dividends

Capital gains and liquidation proceeds are exempt unless i) realised within the first 6 months following the ac-quisition, or ii) in case of substan-tial participation (>10%)

Interest is gener-ally subject to a final 10% with-holding tax

Tax transparent (exc. MBT): Profits and wealth directly taxable in the hands of the shareholders, irrespective of any actual distribution

A 50% exemption applies on dividends

Capital gains and liquidation proceeds are exempt un-less i) realised within the first 6 months following the acquisition, or ii) in case of substantial par-ticipation (>10%)

Interest is gener-ally subject to a final 10% with-holding tax

Tax transparent: Profits and wealth directly taxable in the hands of the shareholders, irrespective of any actual distribution

Dividends are taxable as ordi-nary income

Capital gains and liquidation proceeds are exempt unless i) realised within the first 6 months following the acquisition, or ii) in case of substantial participation (>10%)

Interest is gen-erally subject to a final 10% withholding tax

Taxation of Luxembourg non-residents8

Not taxable in Luxembourg unless: (i) invest-ment is held in a Luxembourg permanent establishment or permanent repre-sentative, or (ii) capital gains realised on a substantial par-ticipation (>10%) within 6 months

Not taxable in Luxembourg unless: (i) invest-ment is held in a Luxembourg permanent establishment or permanent representative, or (ii) SCS, SNC qualifies as Luxembourg permanent establishment or permanent representative

Not taxable in Luxembourg unless invest-ment is held in a Luxembourg permanent establishment or permanent representative

Not taxable in Luxembourg unless invest-ment is held in a Luxembourg permanent establishment or permanent representative

Not taxable in Luxembourg unless invest-ment is held in a Luxembourg permanent establishment or permanent representative

Basics on Luxembourg taxation - Taxation of investors

I. Main Luxembourg private equity vehicles

8 Subject to tax treaties concluded by Luxembourg.

25

Luxembourg has positioned itself as a favourite jurisdiction for structuring private equity transactions. In this complex legal, tax and regulatory environment, our dedicated private equity team, with its longstanding experience, fully understands the changing context of the private equity market and the underlying high expectations of our clients. In particular, our team recognises the importance of providing top-quality legal and tax advice in a timely and practical manner which allows our clients to respond quickly to opportunities in this competitive environment.

Our clients range from sponsors of private equity firms to private/institutional investors, financial institutions and funds of funds, and we are committed to creatively tailoring our services to such diversity of client expectations. With this in mind, we have dedicated a team to private equity matters composed of specialists combining the private equity experience and know-how of our corporate, tax and regulatory lawyers.

Arendt & Medernach’s private equity practice distinguishes itself from its competitors by providing to its clients a “one-stop shop” of high quality services across the board. As such, we represent private equity funds in all aspects of their activities. We design strategic and tax-efficient structures, offering innovative features as necessary. We assist in the setting-up of virtually all types of funds (buyout, real estate, distressed and hedge funds) and in the satisfaction of regulatory requirements. Our lawyers are familiar with the dynamics of the different stages of the investment cycle, including the making of investments and exiting therefrom. We are also in a position to deliver legal and tax opinions confirming the solid grounds of the structure. Also key to our clients, our advice includes the ongoing general representation of our private equity clients that is necessary during the life of the fund, including in terms of corporate and tax compliance (both with respect to direct taxes and VAT aspects) follow-ups.

It is this full range of services and our skilled professional advisers that make us one of the market leaders in Luxembourg, allowing us to address any legal and tax problem that might arise when establishing and running a successful private equity fund.

II. Private equity at Arendt & Medernach

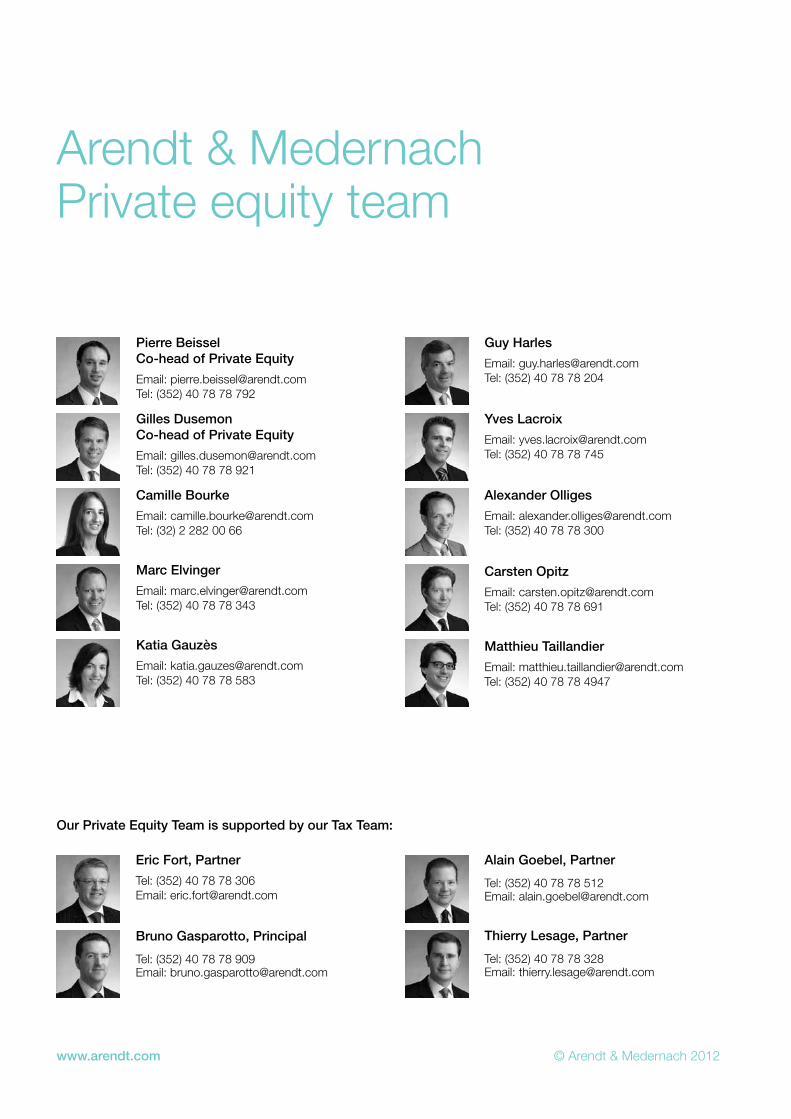

Pierre Beissel Co-head of Private Equity

Email: [email protected] Tel: (352) 40 78 78 792

Gilles Dusemon Co-head of Private Equity

Email: [email protected] Tel: (352) 40 78 78 921

Camille Bourke

Email: [email protected] Tel: (32) 2 282 00 66

Marc Elvinger

Email: [email protected] Tel: (352) 40 78 78 343

Katia Gauzès

Email: [email protected] Tel: (352) 40 78 78 583

Guy Harles

Email: [email protected] Tel: (352) 40 78 78 204

Yves Lacroix

Email: [email protected] Tel: (352) 40 78 78 745

Alexander Olliges

Email: [email protected] Tel: (352) 40 78 78 300

Carsten Opitz

Email: [email protected] Tel: (352) 40 78 78 691

Matthieu Taillandier

Email: [email protected] Tel: (352) 40 78 78 4947

Eric Fort, Partner

Tel: (352) 40 78 78 306 Email: [email protected]

Bruno Gasparotto, Principal

Tel: (352) 40 78 78 909 Email: [email protected]

Alain Goebel, Partner

Tel: (352) 40 78 78 512 Email: [email protected]

Thierry Lesage, Partner

Tel: (352) 40 78 78 328 Email: [email protected]

www.arendt.com © Arendt & Medernach 2012

Arendt & MedernachPrivate equity team

Our Private Equity Team is supported by our Tax Team:

Arendt & Medernach is a leading, independent, full-service law firm with its head office in Luxembourg. The firm’s international team of more than 290 legal professionals provides Luxembourg law related services to clients from offices in Luxembourg, Brussels, Dubai, Hong Kong, London and New York.

Our philosophy is expressed through our five values: vision – commitment – people – independence – energy. We strive for excellence in order to achieve the best results for our clients and we always look for creative solutions.

Our specialised practice areas which allow us to offer our clients a complete range of Luxembourg legal services tailored to their individual needs across all areas of business law.

In order to provide our clients with unparalleled legal advice, we have developed specific expertise in five key industry groups: Banking & Insurance, Investment Management, Multinational Companies and Public Sector, Private Equity, Real Estate. These industry groups possess a deep understanding of our clients’ businesses from a commercial, economic and legal standpoint.

About Arendt & Medernach

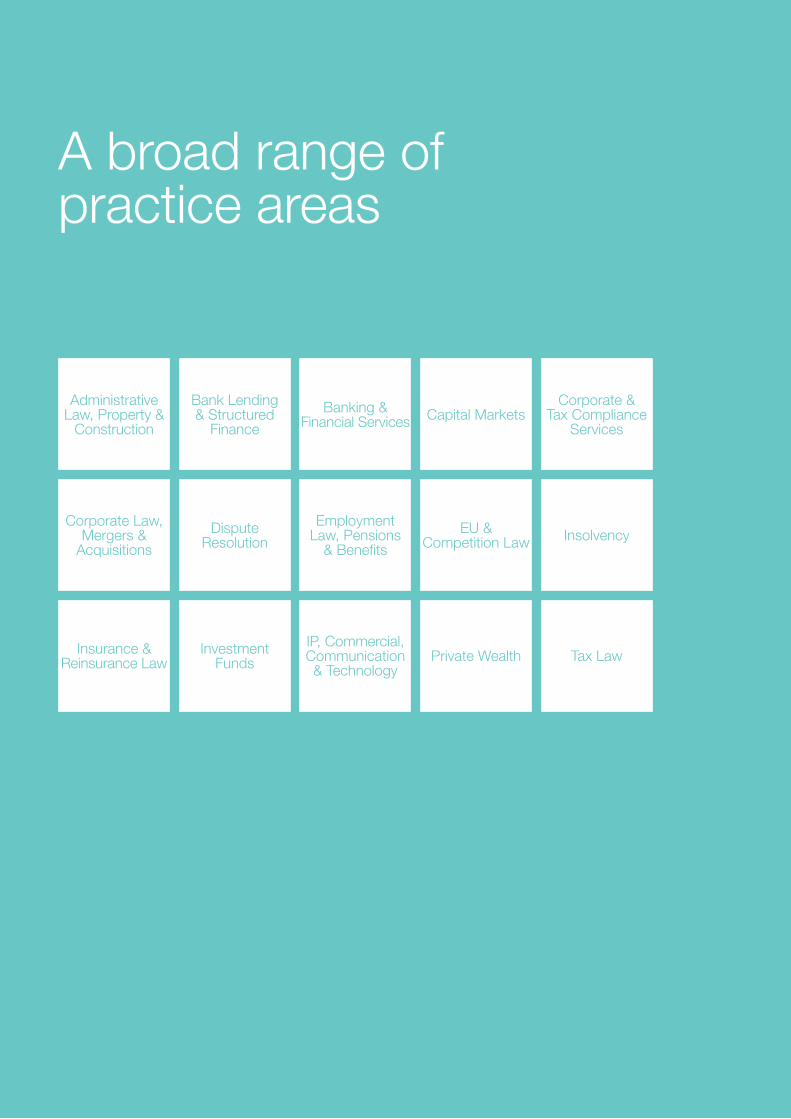

A broad range of practice areas

Administrative Law, Property &

Construction

Bank Lending & Structured

Finance

Banking & Financial Services Capital Markets

Corporate & Tax Compliance

Services

Corporate Law, Mergers &

Acquisitions

Dispute Resolution

Employment Law, Pensions

& Benefits

EU &Competition Law Insolvency

Insurance & Reinsurance Law Tax Law

IP, Commercial, Communication & Technology

Private WealthInvestmentFunds

www.arendt.com

06/2012

BRUSSELSRue d’Arlon 92B-1040 BRUSSELSBELGIUMTel: (32) 2 282 00 60

LONDON14 Devonshire SquareLONDON, EC2M 4YTUNITED KINGDOMTel: (44) 207 776 2962

LUXEMBOURG14, rue ErasmeL-2082 LUXEMBOURGLUXEMBOURGTel: (352) 40 78 78 1

HONG KONGSuites 3711-12, 37th Floor, Jardine House,1 Connaught Place, Central,HONG KONGTel: (852) 2801 5808

NEW YORKRockefeller Center1270 Avenue of the Americas - Suite 1705 NEW YORK, NY 10020, USATel: (1) 212 554 3541

DUBAIDubai International Financial CentreCurrency House, Level 6, Suite 4P.O. Box 482012, DUBAI, UAETel: (971) 44 34 88 96

© Copyright Arendt & Medernach