Embed Size (px)

Citation preview

Private CapitalFlows, EmergingEconomies, and

International Financial

ArchitectureA Paper from the Project on Development,

Trade, and International Finance

Glenn Yago

A Council on Foreign Relations Paper

The Council on Foreign Relations, Inc., a nonprofit, nonpartisan national organization found-

ed in 1921, is dedicated to promoting understanding of international affairs through the free

and civil exchange of ideas. The Council’s members are dedicated to the belief that Amer-

ica’s peace and prosperity are firmly linked to that of the world. From this flows the mis-

sion of the Council: to foster America’s understanding of other nations—their peoples, cultures,

histories, hopes, quarrels, and ambitions—and thus to serve our nation through study and

debate, private and public.

THE COUNCIL TAKES NO INSTITUTIONAL POSITION ON POLICY ISSUES

AND HAS NO AFFILIATION WITH THE U.S. GOVERNMENT. ALL STATE-

MENTS OF FACT AND EXPRESSIONS OF OPINION CONTAINED IN ALL ITS

PUBLICATIONS ARE THE SOLE RESPONSIBILITY OF THE AUTHOR OR

AUTHORS.

From time to time, books, monographs, reports, and papers written by members of the Coun-

cil’s research staff or others are published as a “Council on Foreign Relations Publication.” Any

work bearing that designation is, in the judgment of the Committee on Studies of the Coun-

cil’s Board of Directors, a responsible treatment of a significant international topic.

For further information about the Council or this paper, please write the Council on

Foreign Relations, 58 East 68th Street, New York, NY 10021, or call the Director of

Communications at (212) 434-9400. Visit our website at www.cfr.org.

Copyright 2000 by the Council on Foreign Relations, Inc.

All rights reserved.

Printed in the United States of America.

This paper may not be reproduced in whole or in part, in any form (beyond that copying

permitted by Sections 107 and 108 of the U.S. Copyright Law and excerpts by reviewers

for the public press), without written permission from the publisher. For information, write

Publications Office, Council on Foreign Relations, 58 East 68th Street, New York, NY 10021.

[iii]

CONTENTS

Foreword v

Acknowledgments vii

Introduction 1

Contagion as Metaphor 8

The Integration of Global Capital Markets 14

Deconstructing Global Financial Architecture Proposals 21

[v]

FOREWORD

In the wake of the 1997–98 financial crises in emerging economies,many prominent thinkers focused their energies on what went wrong,how it could have been prevented, and what reform measures arerequired for the future. While some concentrated specifically onfinancial markets within the economies in question, others exam-ined the larger system-wide implications. The Council on For-eign Relations Project on Development, Trade, and InternationalFinance convened a Working Group in an attempt to look at theproblem from both levels, to investigate the problems in theworld economy that led to the crises, and to propose policyoptions calculated to prevent future large-scale disturbances.

Specifically, the goal of the Working Group, which began in1999, was to promote discussion of different perspectives about thenecessity for change in the world economic system, and to lookat concrete forms that change might take.These included, but werenot limited to, discussions about reforming the internationalfinancial architecture to facilitate a transition from export-ledgrowth to internally or regionally demand-driven development strate-gies that offer the populations of the developing world an improvedstandard of living.

One of the Working Group’s several undertakings was to com-mission papers from the participants on a broad range of subjectsrelated to the international financial architecture.The authors comefrom a variety of backgrounds, and their papers reflect a diver-sity of perspectives. However, we believe that all of them provideuseful insights into international financial architecture, and thatthey represent collectively factors that should be considered by bothU.S. and international economic policy makers.

Lawrence J. KorbMaurice R. Greenberg Chair, Director of Studies

Council on Foreign Relations

[vii]

ACKNOWLEDGMENTS

The Project on Development, Trade, and International Financewas made possible by the generous support of the Ford Founda-tion. This project was directed by Walter Russell Mead, Senior Fellow for Foreign Policy at the Council on Foreign Relations,with the close assistance of Sherle Schwenninger, the SeniorProgram Coordinator for the project. The members of the Working Group—a collection of more than thirty experts froma wide range of backgrounds—participated in several sessions at which they provided key feedback on each of the papers. DavidKellogg, Patricia Dorff, Leah Scholer, Benjamin Skinner, LaurenceReszetar, and Maria Bustria provided editing and production assistance.

[1]

Private Capital Flows,Emerging Economies, and

International Financial Architecture1

INTRODUCTION

Firms and development strategies based on a rear-view mirror viewwill leave companies, projects, and entrepreneurs scrambling forcapital access.The control of capital in the developed world con-tinues to shift away from private and state-owned institutions andtoward public markets. Small and medium-sized firms with thebest prospects for innovation and income/wealth generation needto be liberated from their dependence upon bank-based financialsystems. They must also have the ability to turn to market-basedsystems with access to institutional capital providers at home andabroad.2

1This paper was presented to a meeting of the Council on Foreign Relations Work-ing Group on Trade, Development, and International Finance, New York, New York,June 10, 1999. It represents ongoing work underway at the Milken Institute with my col-leagues Lalita Ramesh, James Barth, and R. Dan Brumbaugh.

2The credit channel magnifies monetary/financial shocks disproportionately on thebasis of firm size. During the Korean crisis, spreads (which capture credit channeleffects) were disproportionately larger for small and medium-sized enterprises, which hadno access to close substitutes for bank credit.This echoes classic credit crunch problemsin the U. S. markets as well which gave rise to financial innovations and new capital mar-ket developments in the 1970s and 1980s. See Ilker Domac and Giovanni Ferri, “The RealImpact of Financial Shocks: Evidence from Korea,” World Bank Working Paper (Wash-ington, D.C., World Bank, October 1998).

Yago

[2]

Discussion of financial architecture cannot be separated fromthe problems of concentration of political power, industrial con-trol, and financial capital. Growth and equity in the economy islimited by entrepreneurs’ dependence upon commercial banksthat are state-owned or directed, and thus historically removed fromshareholder and creditor accountability. If politically connected hold-ing companies can shift most of their liabilities to a few subsidiariesand then give those units to the government for liquidationthrough restructuring authorities, new investment will not occur.As the Wall Street Journal recently reported, hints of recoverypromoted by financial assistance packages may well have stalledefforts at financial reform and corporate restructuring.3 In Thai-land, where thousands of companies stopped paying their debt in1997, restructuring is at a standstill. In Malaysia, corporate debtorshave been insulated with a government-directed credit commit-tee. In South Korea, chaebols have expanded their debt and state-linked companies and family conglomerates have resisted changethroughout the crisis countries.

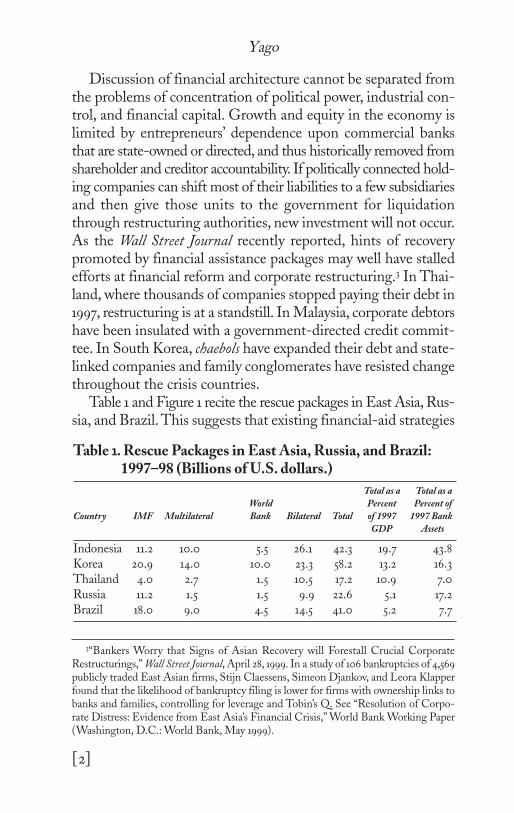

Table 1 and Figure 1 recite the rescue packages in East Asia, Rus-sia, and Brazil.This suggests that existing financial-aid strategies

3“Bankers Worry that Signs of Asian Recovery will Forestall Crucial CorporateRestructurings,” Wall Street Journal, April 28, 1999. In a study of 106 bankruptcies of 4,569publicly traded East Asian firms, Stijn Claessens, Simeon Djankov, and Leora Klapperfound that the likelihood of bankruptcy filing is lower for firms with ownership links tobanks and families, controlling for leverage and Tobin’s Q. See “Resolution of Corpo-rate Distress: Evidence from East Asia’s Financial Crisis,” World Bank Working Paper(Washington, D.C.: World Bank, May 1999).

Table 11. Rescue Packages in East Asia, Russia, and Brazil:1997–98 (Billions of U.S. dollars.)

Total as a Total as a

World Percent Percent of

Country IMF Multilateral Bank Bilateral Total of 1997 1997 Bank

GDP Assets

Indonesia 11.2 10.0 5.5 26.1 42.3 19.7 43.8Korea 20.9 14.0 10.0 23.3 58.2 13.2 16.3Thailand 4.0 2.7 1.5 10.5 17.2 10.9 7.0Russia 11.2 1.5 1.5 9.9 22.6 5.1 17.2Brazil 18.0 9.0 4.5 14.5 41.0 5.2 7.7

Private Capital Flows

[3]

have effectively recapitalized not only existing banking institutions,but also a considerable proportion of the respective countries’economies. The growth and expansion of bank credit supportedby this assistance appears to have exacerbated these crises.

Figure 2 correlates the growth in lending with a crisis index (thesum for each country of the depreciation rate minus the percent-age change in international reserves). The countries with the

Figure 11.. IInnccrreeaassiinngg FFiinnaanncciiaall AAssssiissttaannccee FFrroomm tthhee IIMMFF::11998800––9988

Figure 22.. BBaannkk CCrreeddiitt BBoooomm:: 11999900––9966

Yago

[4]

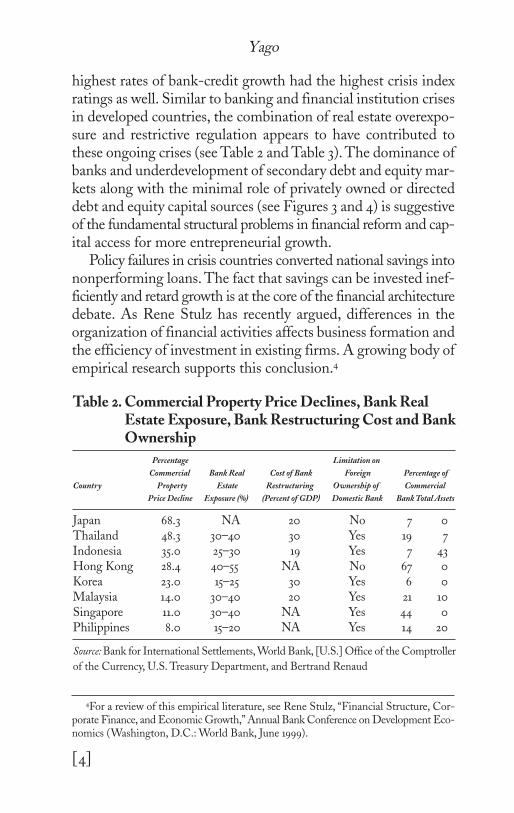

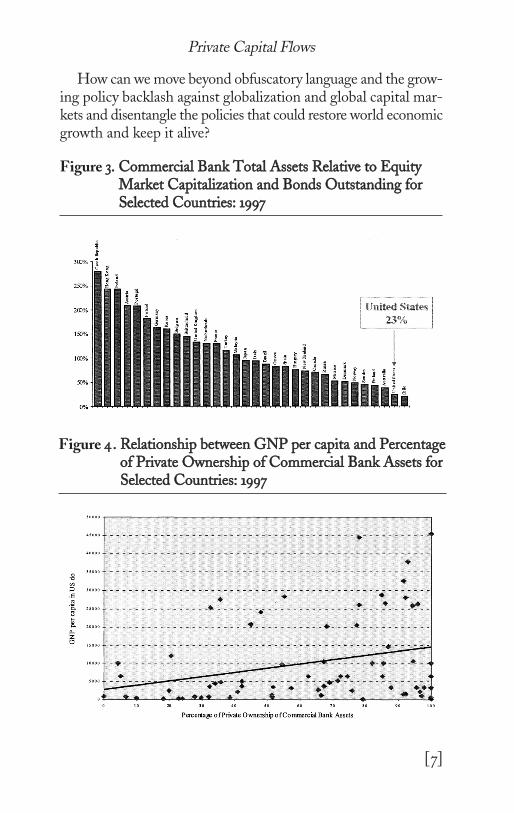

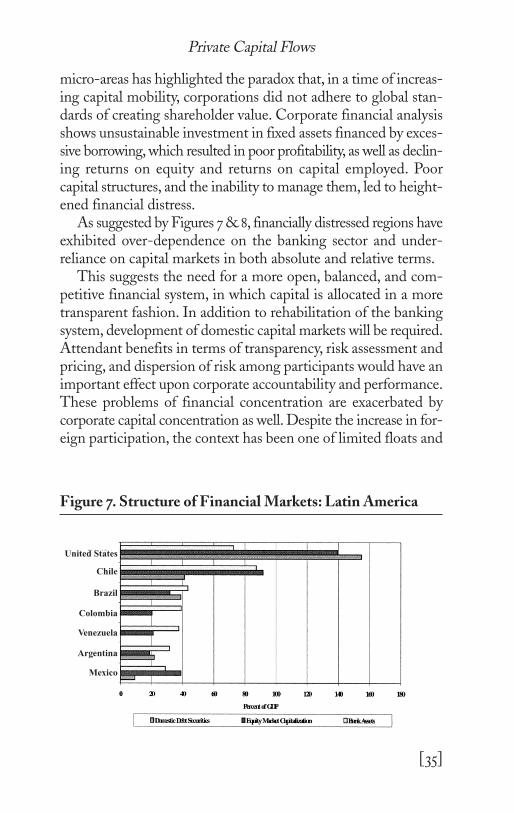

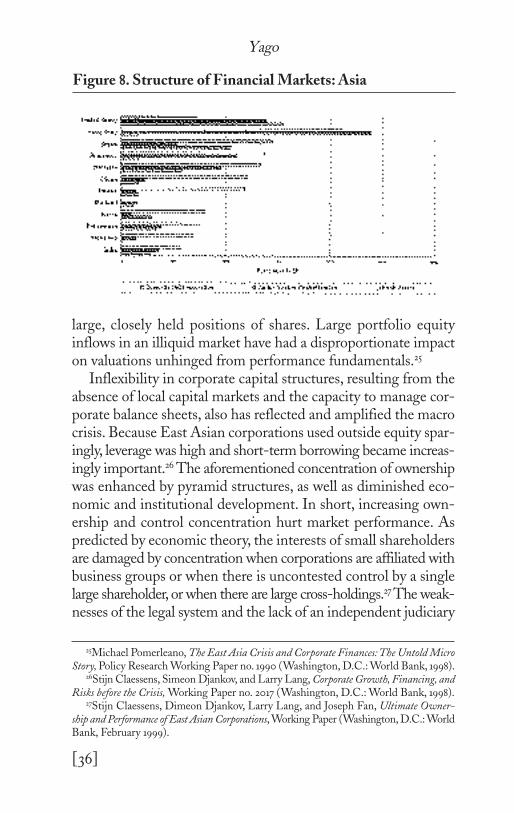

highest rates of bank-credit growth had the highest crisis indexratings as well. Similar to banking and financial institution crisesin developed countries, the combination of real estate overexpo-sure and restrictive regulation appears to have contributed tothese ongoing crises (see Table 2 and Table 3). The dominance ofbanks and underdevelopment of secondary debt and equity mar-kets along with the minimal role of privately owned or directeddebt and equity capital sources (see Figures 3 and 4) is suggestiveof the fundamental structural problems in financial reform and cap-ital access for more entrepreneurial growth.

Policy failures in crisis countries converted national savings intononperforming loans. The fact that savings can be invested inef-ficiently and retard growth is at the core of the financial architecturedebate. As Rene Stulz has recently argued, differences in theorganization of financial activities affects business formation andthe efficiency of investment in existing firms. A growing body ofempirical research supports this conclusion.4

4For a review of this empirical literature, see Rene Stulz, “Financial Structure, Cor-porate Finance, and Economic Growth,” Annual Bank Conference on Development Eco-nomics (Washington, D.C.: World Bank, June 1999).

Table 22. Commercial Property Price Declines, Bank RealEstate Exposure, Bank Restructuring Cost and Bank Ownership

Percentage Limitation on

Commercial Bank Real Cost of Bank Foreign Percentage of

Country Property Estate Restructuring Ownership of Commercial

Price Decline Exposure (%) (Percent of GDP) Domestic Bank Bank Total Assets

Japan 68.3 NA 20 No 7 0Thailand 48.3 30–40 30 Yes 19 7Indonesia 35.0 25–30 19 Yes 7 43Hong Kong 28.4 40–55 NA No 67 0Korea 23.0 15–25 30 Yes 6 0Malaysia 14.0 30–40 20 Yes 21 10Singapore 11.0 30–40 NA Yes 44 0Philippines 8.0 15–20 NA Yes 14 20

Source: Bank for International Settlements, World Bank, [U.S.] Office of the Comptroller

of the Currency, U.S. Treasury Department, and Bertrand Renaud

Private Capital Flows

[5]

Tab

le 33

.Rea

l Est

ate

Inve

stm

ent,

Dev

elo

pm

ent,

and

Man

agem

ent

as A

llo

wab

le A

ctiv

itie

s o

f C

om

mer

cial

Ban

ks

and

Ban

k P

rob

lem

s in

Sel

ecte

d C

ou

ntr

ies:

11999977

Inco

me

Gro

up

Su

bgro

up

Yes

No

Low

In

com

eA

rmen

ia*

Alb

ania

*P

akis

tan

*G

ambia

*G

han

a*R

wan

da*

Mol

dov

a*M

adag

asca

r*T

anza

nia

**M

ozam

biq

ue*

Zim

bab

we*

Russ

ia**

Kor

ea*

Bel

ize

Jord

an**

Per

u*

Pap

ua

New

Low

erG

uin

ea*

Bol

ivia

*L

atvi

a**

Suri

nam

eP

hilip

pin

es**

Fiji*

Mor

rocc

oB

elar

us*

Th

aila

nd

**G

uat

emal

aN

amib

iaG

uya

na*

Ton

gaM

idd

le I

nco

me

Cze

ch R

epublic*

Sau

di A

rabia

Bah

rain

Mal

aysi

a**

Est

onia

**S

eych

elle

sB

arbad

osM

alta

Upper

Hun

gary

*S

lova

kia*

Bot

swan

a*M

exic

o**

Isle

of

Man

Sou

th A

fric

a**

Bra

zil*

Om

anP

olan

d*

Ch

ile*

*T

urk

ey**

Leb

anon

**V

enez

uel

a**

( con

t.)

Yago

[6]

Tab

le 33

.(co

nti

nu

ed))

Aust

ria

Luxe

mbou

rgA

ust

ralia*

Japan

*C

anad

a*N

eth

erla

nd

sB

elgi

um

Por

tuga

lO

EC

DD

enm

ark*

New

Zea

lan

d*

Gre

ece*

Spai

n**

Cou

ntr

ies

Fin

lan

d**

Nor

way

**Ir

elan

d*

Sw

eden

**H

igh

In

com

eF

ran

ce*

Sw

itze

rlan

dIt

aly*

Un

ited

Sta

tes*

Ger

man

y*U

nit

ed K

ingd

omIc

elan

d*

Aru

ba

Hon

g K

ong1

Cyp

rus

Lie

chte

nst

ein

Non

-OE

CD

Net

her

lan

ds

Cou

ntr

ies

Cay

man

Isl

and

sA

nti

lles

Gib

ralt

ar1

Qat

arG

uer

nse

y1K

uw

ait*

*S

love

nia

*N

ote:

Cou

ntr

ies

wit

h a

*d

enot

es a

sig

nif

ican

t ban

kin

g pro

ble

m a

nd

a *

*den

otes

a b

anki

ng

cris

is d

uri

ng

the

1980

to

1998

per

iod

.A “

cri-

sis”

refe

rs t

o ru

ns

or o

ther

subst

anti

al p

ortf

olio

sh

ifts

,col

lapse

s of

fin

anci

al f

irm

s,or

mas

sive

gov

ern

men

t in

terv

enti

on.A

“si

gnif

ican

tpro

ble

m”

refe

rs t

o ex

ten

sive

un

soun

dn

ess

shor

t of

a c

risi

s.

Private Capital Flows

[7]

How can we move beyond obfuscatory language and the grow-ing policy backlash against globalization and global capital mar-kets and disentangle the policies that could restore world economicgrowth and keep it alive?

Figure 33.. CCoommmmeerrcciiaall BBaannkk TToottaall AAsssseettss RReellaattiivvee ttoo EEqquuiittyyMMaarrkkeett CCaappiittaalliizzaattiioonn aanndd BBoonnddss OOuuttssttaannddiinngg ffoorrSSeelleecctteedd CCoouunnttrriieess:: 11999977

Figure 44.. RReellaattiioonnsshhiipp bbeettwweeeenn GGNNPP ppeerr ccaappiittaa aanndd PPeerrcceennttaaggeeooff PPrriivvaattee OOwwnneerrsshhiipp ooff CCoommmmeerrcciiaall BBaannkk AAsssseettss ffoorrSSeelleecctteedd CCoouunnttrriieess:: 11999977

[8]

CONTAGION AS METAPHOR

Contagion hysteria has infected most intelligent discussions aboutglobal financial policies since the Asian crisis struck in the sum-mer of 1997. But is fear of “contagion” a sociological, psycholog-ical, and political phenomenon, or is it an economic one? Carefuleconomic analysis emerging from the crisis confirms the inter-dependence of national economies, but does not confirm some kindof pathological and irrational “contagion.” Common structural prob-lems in those economies most exposed to crisis persist.5 The “con-tagion” characterization of the global financial crisis basicallypathologizes and institutionalizes bad economic policies andfinancial practices.6 For example, contagion language paintsArgentina and Chile with the brush of Brazil. Michael Bordo and

5Aaron Tornell, Common Fundamentals in the Tequila and Asian Crises, Working Paper(Cambridge, Mass.: Harvard University and National Bureau of Economic Research, July1998); James R. Barth, R. Dan Brumbaugh, Lalita Ramesh, and Glenn Yago, “TheRole of Governments and Markets in International Banking Crises: The Case of EastAsia,” in George Kaufman, ed., Research in Financial Services: Private and Public Policy,vol. 10 (New York: JAI Press, Inc., 1998), pp. 177–233.

6“Contagion” was indeed the most overused word to describe the global crisis bothin the press and including the recently released Economic Report of the President, Febru-ary 1999. Carmen Reinhart and Graciela Kaminsky define contagion as a situationwhere a crisis elsewhere increases the probability of a crisis at home even when the fun-damentals are accounted for. Possible transmission channels of “contagion”—internationalbank lending, cross-market hedging, and bilateral and third-party trade in propagatingcrisis—are found to be indistinguishable from trade-linked effects; see “On Crisis, Con-tagion and Confusion,” Working Paper (University of Maryland at College Park, 1999).Robert Rigobon examined the correlation between Mexican and Argentinean stock mar-kets and finds no evidence of such contagion in any recent crisis when account is takenof endogenicity, unobservable variables, and changes in the variance of stock market returns.In fact, there is little to distinguish this recent financial crisis from earlier ones; see “Onthe Measurement of Contagion,” presentation at Conference on Globalization, Capi-tal Markets Crises, and Economic Reform (Cartagena, Colombia, January 1999). Ser-gio Schmukler and Graciela Kaminsky examine financial cycles in twenty-eight countriesduring the last two decades, looking at duration of upturns and downturns, amplitude,and spillover effects across countries and regions.They find that financial cycles have notbecome more unstable in the 1990s and that they replicate experience with Latin Amer-ica in the 1980s; see “On Booms and Crashes: Are Financial Cycles Changing,” Work-ing Paper (Washington, D.C.: George Washington University, 1999).

Private Capital Flows

[9]

Anna Schwartz lead us to a more differentiated conclusion aboutthe propagation effects of structural crises:

Pure contagion would occur only in circumstances in which otheremerging countries were free of the problems facing the firstemerging country.We know of no evidence of pure contagion.Trans-mission is another story. Shocks to one country will spill over toother countries through trade and the capital accounts.When investorswithdraw their capital from countries with the same problems aswere present in the first such country, this is a demonstration effect,not contagion.7

When used in analyzing financial crises, contagion languageemploys a sometimes lethal metaphor of fear to supplant empir-ical analysis. As cultural critic Susan Sontag long ago observed,using illness as a metaphor can have damaging consequences forthose afflicted.8 This is as true in clinical situations in economicsand finance as in medicine.The contagion metaphor has stigmatizingeffects through the myths it creates; damaging the prospects of recov-ery both in diagnosing the problems and resolving them. Fear andloathing about globalization becomes common when such rhetoricdominates debates.9

International economic integration has always been a politicallycontentious topic. A spate of new books and conferences from Davosto Delhi have provided caricatures of the capital market operationsand financial-institution complexity that drive expanded partic-ipation in the global economy.10 But most empirical evidence

7Michael D. Bordo and Anna J. Schwartz, “Under What Circumstances, Past and Pre-sent, Have International Rescues of Countries in Financial Distress Been Successful?”Working Paper no. 6824 (Cambridge, Mass.: National Bureau of Economic Research,December 1998), pp. 44–45.

8Susan Sontag, Illness as Metaphor (New York: Farrar, Straus & Giroux, 1990).9See New York Times series on Global Contagion, February 15–18, 1999, and its edi-

torial “Global Markets Lethal Magic,” February 21, 1999.10Timothy Goringe, Fair Shares: Ethics and the Global Economy (London and New York:

Thames & Hudson, May 1999); Dani Rodrik, The New Global Economy and DevelopingCountries: Making Openness Work (Washington, D.C.: Overseas Development Council,November 1998); Harry Shutt, The Trouble with Capitalism: An Enquiry into the Causesof Global Economic Failure (New York: St. Martin’s Press, Inc., August 1998).

Yago

[10]

suggests that continued crises reflect the persistence of corporatistand socialist statist economies, not entrepreneurially driven mar-ket economics.

Nevertheless, the policy backlash against globalization permeatesmost discussions about the global financial crisis. Reaction tothe Anglo-American model of financial liberalization is widespread.The vice finance minister of Japan, Eisuke Sakakibara, put it thisway:

The Asian financial crisis occurred not because Asia had a prob-lem.The problem is the global capitalism that allows funds to moveall over the world based on a profit-oriented motive.11

Or take the position articulated by Karel van Wolferen:

The project of a globalized economic order ruled by unregulatedmarkets is utopian, as much as the notion of the withering awayof the state was in Communist imagery.12

Or former Mexican President Carlos Salinas de Gortari:

Insisting that North American neoliberalism is the only way turnspeople into enemies of the market because they see the marketsas enemies of the people.13

Lionel Jospin (prime minister of the Republic of France), GerhardSchroeder (chancellor of the Federal Republic of Germany),Oskar Lafontaine (finance minister of the Federal Republic of Ger-many), and other European Union political leaders continue to ham-mer away at the need for new international regulation andstate-mediated responses as opposed to market responses.14

Compare this blame-mongering by politicians to the recent-ly released essay by the currently embattled former deputyMalaysian prime minister, Anwar Ibrahim, who introduces his per-

11Eisuke Sakakibara, “Mahathir is Right,” New Perspectives Quarterly (Winter 1999),p. 10.

12Karel van Wolferen, “The Global Conceptual Crisis,” New Perspectives Quarterly, vol.16/1 (Winter 1999), p. 17.

13Carlos Salinas de Gortari and Roberto Mangabeira Unger, “From North AtlanticNeoliberalism to Market Pluralism,” Challenge, vol. 41/6 (February-March 1999).

14Oskar Lafontaine and Christa Mueller, Keine Angst vor der Globalisierung [Don’t FearGlobalization] (Frankfurt: Dietz Verlag, 1998).

Private Capital Flows

[11]

spective by noting that “. . .it is not normal to conduct econom-ic discourse from behind prison walls.” He writes:

Do we not take the individual and collective responsibility for ourproblems, just as we have taken credit for our successes in the lastdecade?. .Asian nations would do well to put their houses inorder first. The international financial system does indeed need anew architecture, but structural reforms must begin at home. . .TheAsian renaissance should encompass not only political trans-parency and better corporate governance, but also reforms tosociety and culture, and respect for human rights, the environmentand the independence of the judiciary. Without this commit-ment to these values, debate on resolving the Asian crisis may wellturn out to be mere lip service.15

Taking Anwar’s lead, we should deconstruct the debate aboutglobal financial architecture. We must understand both its con-text and component parts. In this paper, we focus upon the emerg-ing globalization backlash in policy that could limit future capitaland job formation in both emerging and developed economies.Discussions of global financial architecture, when decomposed, rep-resent a new technocratic language that obscures discussion of thestructural problems. At the recent Davos conference of the WorldEconomic Forum, for example, there was a great deal of discus-sion about protectionism, prospective government controls overcapital flows, exchange rate differentials, and mergers and acqui-sitions.16

Remarkably absent was a discussion of how new job, income,and wealth creation are to occur in Europe and in the transitionand emerging economies, particularly during the process of busi-ness consolidation, restructuring, and transition to the new econ-omy.These topics lead to the fundamental question of alternativeregulatory proposals to achieve those goals.

15http://members.tripod.com/~Anwar_Ibrahim/main.htm16Lawrence Minard, “What They Didn’t Talk About in Davos,” Forbes Global

(February 22, 1999), p. 2.

Yago

[12]

The following questions need to be discussed as we evaluate dis-cussions of global financial architecture.

• How much globalization is there?

• Does globalization exacerbate inequality?

• How significant are the benefits of globalization?

• Are global governance structures adequate to deal with glob-alization?

• Are financial integration and globalization to blame for crisesand volatility, or do they simply reflect structural problems incorporate governance and unevolved financial institutions andcapital markets?

• Does global capital market integration require the loss ofnational macroeconomic policy autonomy?

• Can the International Monetary Fund and World Bank—designed for a world of fixed exchange rates and limited cap-ital mobility—promote stability in a radically changed world,or do their practices destabilize markets further?

Globalization and Deglobalization: Back to the Future?Today’s globalization is a resumption of trends that precededWorld War I. Indeed, many of the present debates about global-ization echo debates of that period. In examining globalization beforeWorld War I, a sobering picture emerges.The economy of the latenineteenth century was one of rapid globalization: capital and laborflowed and commodity trade boomed as transport costs dropped.The convergence of incomes, prices, and wages that occurredfrom 1850–1914, due to open trade and mass immigration, cameto a halt between 1914–50 as deglobalization and autarky emergedas dominant economic and political forms.

An important lesson from the implosion of past globalizationis that growing nation-state and intra-state inequality created a back-lash against globalization. Significant distributional events causeda drift toward more restrictive policies—in trade, migration, and

Private Capital Flows

[13]

capital flows.The deglobalization implosion after 1914 was not inde-pendent of economic events.The retreat from open immigrationpolicies was driven by a defense of the deteriorating relative posi-tion of the working poor. The retreat from free trade that culmi-nated in rabid protectionism after World War I was manifestedin protection of domestic agriculture from negative price shocksassociated with globalization and trade-induced deterioration inthe relative economic position of classes within Europe and theUnited States.17

17As Jeffrey Williamson writes, “(Prior to World War I) the evolution of well-func-tioning global markets in goods and labor eventually brought a convergence between nations.This factor price convergence planted, however, seeds for its own destruction since it cre-ated rising inequality in labor-scarce economies and falling inequality in labor-abundanteconomies. The voices of powerful interest groups who were hit hard by these global-ization events were heard, however, and these were in particular the ordinary worker inlabor scarce economics and the landlord in the labor abundant economies. These inter-est groups generated a political backlash against immigration and trade, and this back-lash, which had been building up for decades, was brought to a head by event aroundWorld War I.” See Journal of Economic Perspectives, vol. 12/4 (Fall 1998), p. 61.

[14]

THE INTEGRATION OF GLOBAL CAPITAL MARKETS

Today globalization, particularly of capital markets, is both exag-gerated and can be reversed as it has been in the past.

The two driving forces of globalization are technology and lib-eralization. The natural barriers of time and space that separatenational markets are collapsing at record speed as communications,information, and transportation technologies have transformed andintegrated national economies.

In examining product, labor, and capital markets, the degree ofintegration can be overstated. Though the ratio of trade to out-put in product markets has increased sharply in most countries sinceWorld War II, it is not substantially higher in Western Europeancountries than it was in 1914, and in Japan it is relatively less. Priceconvergence across countries is still elusive, and other indicatorsof product market integration still lag. Financial markets are alsonot fully integrated. Until recently, the index of capital controlswas declining and net private capital flows by banks, foreigndirect investment, and portfolio investment were increasing.18

The strict test of capital market integration—real (inflation-adjusted) interest rates—should converge; but real interest ratesdiffer substantially. Only 10 percent of domestic investment in emerg-ing economies has been financed from abroad. Foreign direct

18Survey evidence on the use of capital controls to attain objectives of monetary con-trol are largely pessimistic; see Michael P. Dooley, “A survey of Literature on Controlsover International Capital Transactions,” IMF Staff Papers 43 (Washington, D.C.:International Monetary Fund, December 1996), pp. 639–87). Reports on panel studiesof the incidence of capital controls for twenty industrial countries during the years1950–89, and for sixty-one industrial and developing countries from 1966–89 find thatthe probability of capital controls lowers the likelihood of more flexible exchange-rateregimes and greater central bank independence; see Vittorio Grilli and Gian Maria Mile-si-Ferretti, “Economic Effects and Structural Determinants of Capital Controls,” IMFStaff Papers 42 (Washington D.C.: International Monetary Fund, September 1995),pp. 517–51. Using liquid asset reserve requirements as opposed to capital controls mightbe a more effective strategy of reducing credit risk.

Private Capital Flows

[15]

investment relative to domestic GDP is much smaller now thanduring the period before World War I. The net outflow of capi-tal (i.e., the current account surplus) for most developed countriesis actually lower than before World War I.Today the average levelof current account balances has not quite attained the magnitudecommon before World War I. Labor markets are considerably lessintegrated than at the turn of the century, despite integration ofproduct and capital markets.

In short, gross capital flows may be very large. But net flowsare actually smaller than those observed during the period of thegold standard. Trade flows are not significantly higher than theywere prior to 1914, if measured against GDP, but are higher if mea-sured against industrial production. While international invest-ment flows commonly topped 3 percent of GDP before 1914,they slumped to less than half that level in the 1930s and only beganto move upward after 1970.

Current Trends in Financial IntegrationForeign direct investment is the largest source of net capital flowsto developing countries. The largest share of such investment isby multinational corporations in their overseas operations undertheir own control. It is the only area that has shown some stabil-ity. Net flows in portfolio equity, bond, and commercial bank loansgrew substantially during the 1990s but face severe declines, as shownin Figure 5.

The fundamental global financial crisis is this: The turmoil atthe end of the 1990s has created very wide spreads and curtailedmarket access. Net private capital flows to leading emerging mar-ket economies have fallen to $160 billion compared to $240 bil-lion in 1998, which was after a peak of $310 billion in 1996.Portfolio equity, bonds, and bank lending all reflect similar declines.(See Table 4). The context of this crisis, after ten years of explo-sive growth in international financial transactions, needs to be recalled:a tenfold increase in global foreign exchange markets, a fivefoldincrease in foreign direct investment, and a tenfold increase in cross-border bond and equities transactions.

Yago

[16]

Figure 55.. RReeggiioonnaall NNeett CCaappiittaall FFlloowwss

Source: Milken Institute; World Economic Outlook October 1997 & October 1998

Table 44.. Emerging Market Economies’ External Finance (billions of U.S. dollars)

11999955 11999966 11999977 11999988ff 11999999ff

Current account balance –95 –95.4 –76.2 –44.8 –27.1External financing net 267.8 311.1 282.4 200.4 184.6Private flows, net 228.1 307.6 241.7 158.2 158.3Equity investment 106.7 128.2 144.9 116.7 119.9Direct equity 82.2 94.9 119.7 105.9 101.8Portfolio equity 24.5 33.4 25.2 10.7 18.1Private creditors 121.4 179.3 96.8 41.5 38.3Commercial banks 103.1 113.3 22.2 –0.7 11.9Non-bank private creditors 18.3 66 74.6 42.2 26.4Official flows, net 39.7 3.5 40.7 42.2 26.3International financial institutions 20.4 7.2 28.3 32.2 14.1Bilateral creditors 19.3 –3.7 12.4 10 12.2Resident lending/other, net* –77.7 –128.6 –161.3 –115.9 –95.7Reserves excl. gold (– = increase ) –95 –87.1 –44.8 –39.7 –61.8

e = estimate f = forecast* Including resident net lending, monetary gold, and errors and omissionsSource: Institute of International Finance, Inc.

Private Capital Flows

[17]

Regulatory frameworks in developed countries have untilrecently created and exacerbated this problem. Present bank reg-ulation evaluates asset riskiness individually by using risk-basedcapital standards. As Credit Suisse First Boston Global Credit Strate-gist David Goldman has pointed out, “modern portfolio theoryoffers a different view, namely that portfolio risk is not additive:the riskiness of a portfolio is an entirely different thing from thesum of the risks of the individual assets. In effect the present risk-based capital standards sum the risk of individual assets. Diver-sified portfolios, however, may have a far lower level of risk thanthe average riskiness of their elements.” Portfolio-based risk mea-sures currently contemplated by the Bank for International Set-tlements would lower the cost of capital to borrowers and raise thereturn to equity for financial institutions.

Regulatory restrictions of various kinds19 discourage main-stream financial institutions such as banks, life insurance compa-nies, and pension funds from participating in the market forriskier credits in emerging countries. Most of the world’s popu-lation lives in emerging markets. Such countries must sell risky assetsto obtain capital. Newer market entrants in the developed worldare also riskier. Accordingly, given these restrictions, the unregu-lated segment has taken a disproportionately large role in such markets.

The problem with emerging markets during 1998 stemmed fromthe fact that virtually all capital flows to emerging capital marketscame from hedge funds buying emerging-market securities:

The regulatory system in effect matched up borrowers with volatilereturns to lenders with volatile sources of capital and produced anear catastrophe. The problem with hedge funds and the unreg-ulated market was the interaction between well-informed specialistsand uninformed investors in the markets. As margin calls forcedhedge fund specialists to liquidate part of their holdings, the pricedownturn was amplified.To the extent that emerging markets and

19James Barth, R. Dan Brumbaugh, and Glenn Yago, eds., Restructuring Financial Reg-ulation (Santa Monica, Calif.: Milken Institute, Forthcoming).

Yago

[18]

their participants were liquidity-constrained, emerging-marketsecurity and bond prices were slow to recover. High interest ratescombined with the slow recovery to adversely affect demand,output, and employment.20

In response, securitization is only part of the answer. Chang-ing the regulatory structure in the industrial world is just asimportant.

The application of portfolio risk analysis in place of risk-basedcapital standards in financial institution regulation could wellincrease capital access and decrease imprudent uses of leverage. How-ever, the incentives for expanding net credit exposure by regulat-ed institutions may not be implemented as fast as the disincentivesfor hedge-fund lending, which could further exacerbate liquidi-ty shortages in the global financial markets.

Global Financial Architecture and the Evolution ofInternational Capital MobilityThere is an underlying tension between markets and govern-ments that explains the long stretch of high capital mobility priorto World War I, its subsequent breakdown, and then the slow rebuild-ing of the postwar world financial system. This tension involvesthe way in which openness to the world capital market constrainsgovernment power through the choice of the exchange rate mech-anism.

Before 1914, currency prices were pegged in terms of gold, whichmaintained a fixed rate of exchange. The Great Depression dis-credited gold-standard orthodoxy. Financial products and marketswere banned or otherwise more closely regulated.The Bretton Woodsconference set up a fixed, but adjustable, exchange-rate parity sys-tem in the belief that floating exchange rates would exhibit insta-bility that would damage international trade. Accordingly, after1973, industrial countries moved to a floating dollar-rate regime.21

20David P. Goldman, “Risk-Based Capital Standards and the Future of Banking,” (Cred-it Suisse First Boston, September 30, 1998), p. 4; see also Glenn Yago, Lalita Ramesh,and Noah Hochman, Hedge Funds and Systemic Risk Demystified (Santa Monica, Calif.:Milken Institute, December 1998).

21Maurice Obstfeld, “The Global Capital Market: Benefactor or Menace?” Journal ofEconomic Perspectives, vol. 12/4 (Fall 1998), pp. 9–30.

Private Capital Flows

[19]

Debates over financial architecture are part of that ongoing dis-course as markets discipline governments and meet resistance. Eachcountry’s financial system is an important intangible asset that canhelp to facilitate both its own and others’ economic growth.Given the enormous disparity in national wealth between rich andpoor countries, developed countries offer an important source ofdevelopment funds for countries unable to finance their future sole-ly with internal savings. In order for an efficient and innovativeglobal financial system to evolve, borrower countries’ financial sys-tems need some fundamental compatibility with those of lendercountries. Any discussion of global financial architecture must dealdirectly with the form developing financial systems take.

Financial systems are intangible assets that promote econom-ic growth by facilitating the transfer of funds from savers (saversor lenders) to borrowers (spenders or investors).This relationshipis depicted in Figure 6.The benefits provided to individuals by finan-cial systems involve risk sharing, liquidity, and information. Saverscan hold many different types of assets and thus diversify risk. Like-wise, investors can fund projects in large numbers of different ways.

Figure 66.. DDeessiiggnniinngg FFiinnaanncciiaall SSyysstteemmss

Yago

[20]

However, there are a host of economic obstacles to matchingsavers and investors.These obstacles include transaction costs, mar-ket failures, firm size, available information, sources of capital, prop-erty rights and information, regulation, negative externalities,bank runs, moral hazard, agency problems, barriers to entry, andexit by investors, to name a few.

[21]

22George Soros’ model suggests a new international agency that would insure investorsagainst debt defaults. Countries would pay a fee when floating loans in order to under-write the cost of insurance. Each country’s debts would be limited to a ceiling set by theIMF. Loans in excess of the ceiling would not be insured. And the IMF would not aid countries having difficulty servicing uninsured loans. See George Soros, The Crisisof Global Capitalism (New York: Public Affairs Press, 1998).

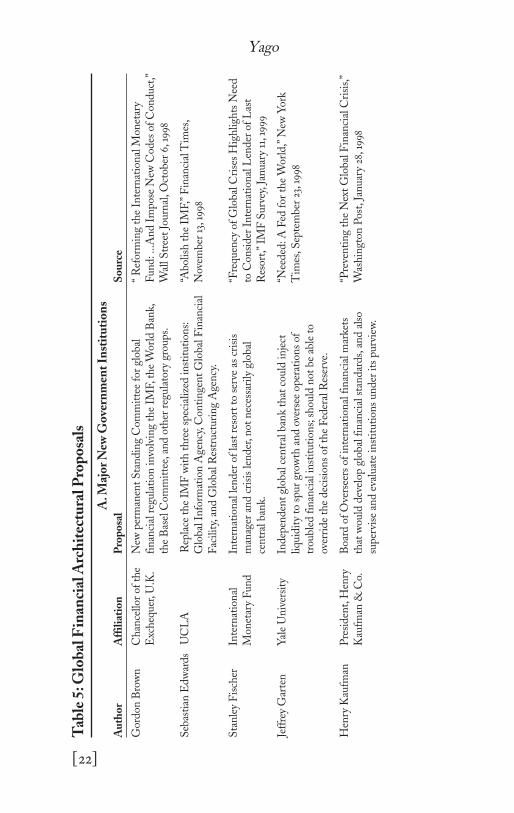

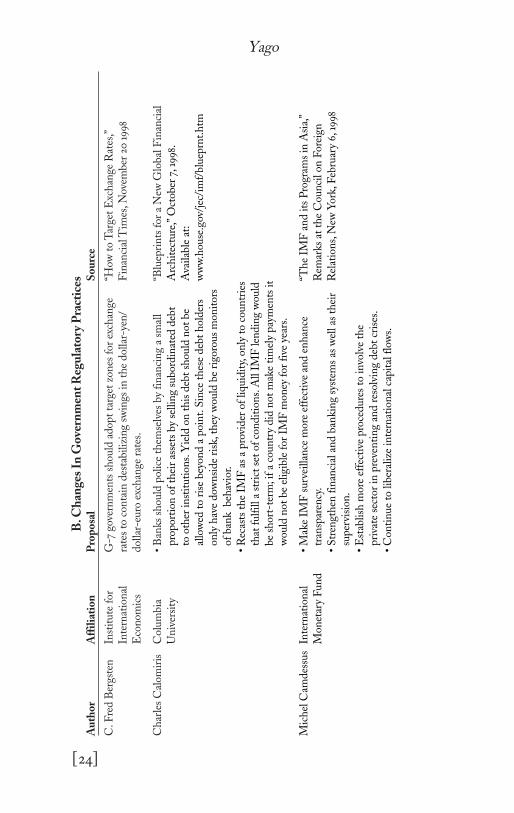

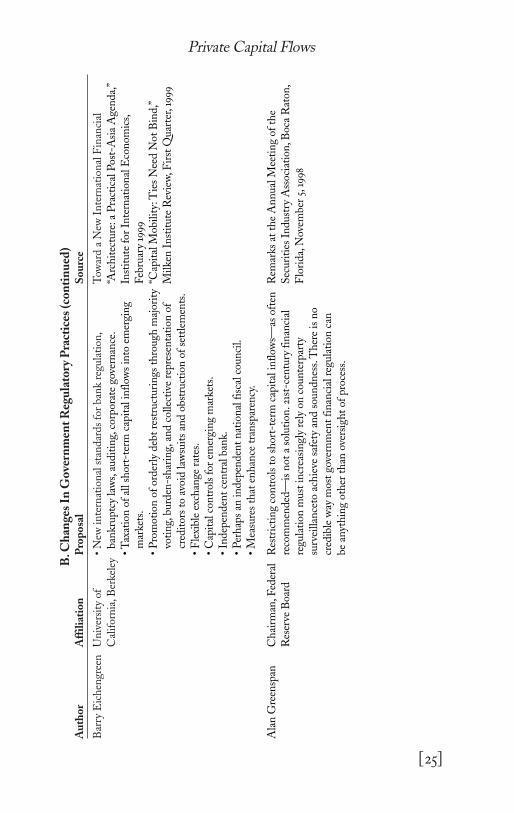

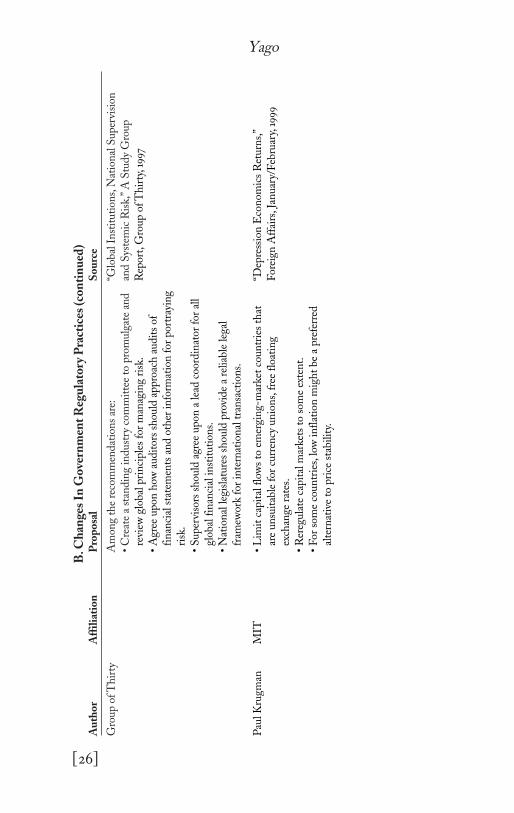

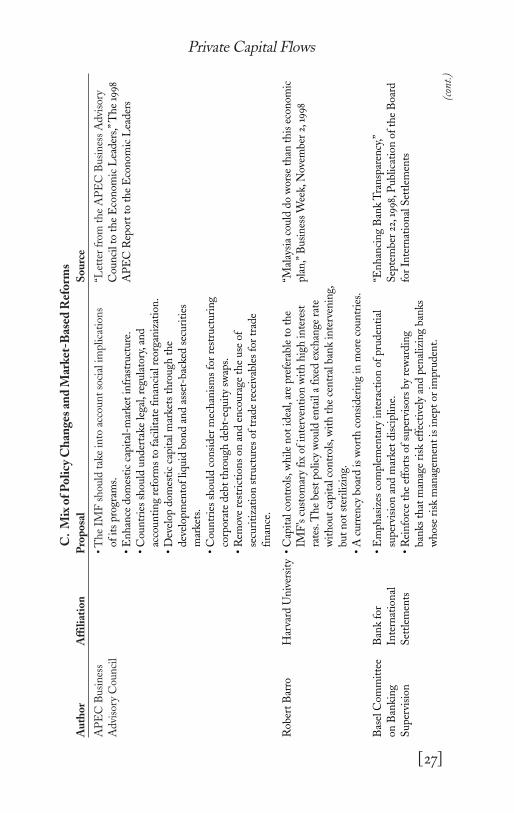

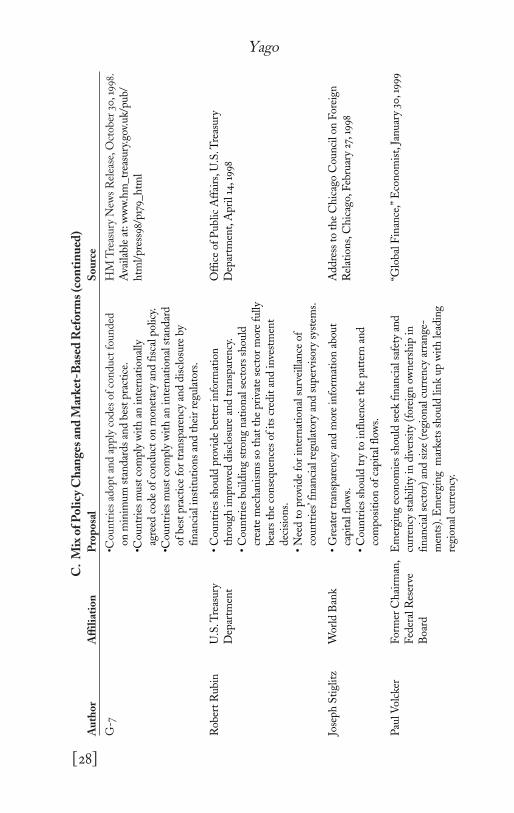

DECONSTRUCTING GLOBAL FINANCIALARCHITECTURE PROPOSALS

The Major Proposals (see Table 5) Since the spring of 1997, when the East-Asian financial crisis beganto develop, a proliferating number of proposals for a “new finan-cial architecture” have come forward to reduce the turbulence inworld financial markets.

Table 5 presents a representative listing of the major types ofreform proposals that have evolved. Although there are a seem-ingly ever expanding number of reform proposals, as the table shows,several trends have emerged among prominent economists and gov-ernment officials.22

These proposals can be roughly classified as those that advo-cate:

• major new government institutions;

• changes in government regulatory practices;

• a mix of policy changes and market-based reforms; and

• market-based reforms alone.

For those who want to rely on either increased or improved gov-ernment or trans-national agency intervention in financial mar-kets, there are three major strands of proposals. Many haveproposed some form of international lender of last resort or glob-al central bank. Others have argued for perfecting in some way howthe IMF presently works. Still others have proposed currency boards.

Yago

[22]

Tab

le 5

:Glo

bal

Fin

anci

al A

rch

itec

tura

l Pro

po

sals

A.M

ajo

r N

ew G

ove

rnm

ent

Inst

itu

tio

ns

Au

tho

rA

ffil

iati

on

Pro

po

sal

So

urc

e

Gor

don

Bro

wn

Ch

ance

llor

of

the

New

per

man

ent

Sta

nd

ing

Com

mit

tee

for

glob

al

“ R

efor

min

g th

e In

tern

atio

nal

Mon

etar

y E

xch

equer

,U.K

.fi

nan

cial

reg

ula

tion

in

volv

ing

the

IMF,

the

Wor

ld B

ank,

Fun

d:.

..An

d I

mpos

e N

ew C

odes

of

Con

duct

,”th

e B

asel

Com

mit

tee,

and

oth

er r

egula

tory

gro

ups.

Wal

l S

tree

t Jo

urn

al,O

ctob

er 6

,199

8

Seb

asti

an E

dw

ard

sU

CL

AR

epla

ce t

he

IMF

wit

h t

hre

e sp

ecia

lize

d in

stit

uti

ons:

“Abo

lish

th

e IM

F,”

Fin

anci

al T

imes

,G

lobal

In

form

atio

n A

gen

cy,C

onti

nge

nt

Glo

bal

Fin

anci

al

Nov

ember

13,

1998

Fac

ilit

y,an

d G

lobal

Res

truct

uri

ng

Age

ncy

.

Sta

nle

y F

isch

erIn

tern

atio

nal

In

tern

atio

nal

len

der

of

last

res

ort

to s

erve

as

cris

is

“Fre

quen

cy o

f G

lobal

Cri

ses

Hig

hligh

ts N

eed

M

onet

ary

Fun

dm

anag

er a

nd

cri

sis

len

der

,not

nec

essa

rily

glo

bal

to

Con

sid

er I

nte

rnat

ion

al L

end

er o

f L

ast

cen

tral

ban

k.R

esor

t,”

IMF

Surv

ey,J

anuar

y 11

,199

9

Jeff

rey

Gar

ten

Yal

e U

niv

ersi

tyIn

dep

end

ent

glob

al c

entr

al b

ank

that

cou

ld in

ject

“N

eed

ed:A

Fed

for

th

e W

orld

,”N

ew Y

ork

liquid

ity

to s

pur

grow

th a

nd

ove

rsee

oper

atio

ns

of

Tim

es,S

epte

mber

23,

1998

tr

ouble

d f

inan

cial

in

stit

uti

ons;

shou

ld n

ot b

e ab

le t

o ov

erri

de

the

dec

isio

ns

of t

he

Fed

eral

Res

erve

.

Hen

ry K

aufm

anP

resi

den

t,H

enry

B

oard

of

Ove

rsee

rs o

f in

tern

atio

nal

fin

anci

al m

arke

ts

“Pre

ven

tin

g th

e N

ext

Glo

bal

Fin

anci

al C

risi

s,”

Kau

fman

& C

o.th

at w

ould

dev

elop

glo

bal

fin

anci

al s

tan

dar

ds,

and

als

o W

ash

ingt

on P

ost,

Jan

uar

y 28

,199

8 su

per

vise

an

d e

valu

ate

inst

ituti

ons

un

der

its

purv

iew

.

Private Capital Flows

[23]

A.M

ajo

r N

ew G

ove

rnm

ent

Inst

itu

tio

ns

(co

nti

nu

ed)

Au

tho

rA

ffil

iati

on

Pro

po

sal

So

urc

e

Ste

ven

Rad

elet

&H

arva

rd U

niv

ersi

ty•

Inte

rnat

ion

al r

egula

tor

of b

ankr

uptc

y la

ws,

“Wh

at h

ave

we

lear

ned

,so

far,

from

th

e A

sian

Je

ffre

y D

.Sac

hs

• d

epos

it in

sura

nce

,len

der

of

last

res

ort.

Fin

anci

al C

risi

s?”

mim

eo,H

arva

rd I

nst

itute

for

• F

loat

ing

exch

ange

rat

e.In

tern

atio

nal

Dev

elop

men

t,Ja

nuar

y 4,

1997

.•

Ref

orm

IM

F c

ond

itio

nal

ity.

Ava

ilab

le a

t:w

ww

.hii

d.h

arva

rd.e

du

• R

estr

icti

ons

on s

hor

t-te

rm c

apit

al f

low

s.G

eorg

e S

oros

Ch

airm

an,S

oros

•

Inte

rnat

ion

al c

entr

al b

ank;

len

der

of

last

res

ort

to s

elec

t “T

he

Cri

sis

of G

lobal

Cap

ital

ism

,”F

un

d M

anag

emen

t•

grou

p o

f co

un

trie

s.W

all S

tree

t Jo

urn

al,S

epte

mber

15,

1998

• M

and

ator

y in

sura

nce

(si

milar

to

dep

osit

in

sura

nce

),•

issu

ed b

y an

in

tern

atio

nal

cre

dit

in

sura

nce

•

corp

orat

ion

to

mai

nta

in c

red

itor

con

fid

ence

.

Yago

[24]

B.C

han

ges

In G

ove

rnm

ent

Reg

ula

tory

Pra

ctic

esA

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

C.F

red

Ber

gste

nIn

stit

ute

for

G

-7 g

over

nm

ents

sh

ould

ad

opt

targ

et z

ones

for

exc

han

ge

“How

to

Tar

get

Exc

han

ge R

ates

,”In

tern

atio

nal

rate

s to

con

tain

des

tabiliz

ing

swin

gs in

th

e d

olla

r-ye

n/

Fin

anci

al T

imes

,Nov

ember

20

199

8E

con

omic

sd

olla

r-eu

ro e

xch

ange

rat

es.

Ch

arle

s C

alom

iris

Col

um

bia

•

Ban

ks s

hou

ld p

olic

e th

emse

lves

by

fin

anci

ng

a sm

all

“Blu

epri

nts

for

a N

ew G

lobal

Fin

anci

al

Un

iver

sity

• pro

por

tion

of

thei

r as

sets

by

sellin

g su

bor

din

ated

deb

t

Arc

hit

ectu

re,”

Oct

ober

7,1

998.

• to

oth

er in

stit

uti

ons.

Yie

ld o

n t

his

deb

t sh

ould

not

be

A

vailab

le a

t:•

allo

wed

to

rise

bey

ond

a p

oin

t.S

ince

th

ese

deb

t h

old

ers

w

ww

.hou

se.g

ov/j

ec/i

mf/

blu

eprn

t.h

tm•

only

hav

e d

own

sid

e ri

sk,t

hey

wou

ld b

e ri

goro

us

mon

itor

s •

of b

ank

beh

avio

r.•

Rec

asts

th

e IM

F a

s a

pro

vid

er o

f liquid

ity,

only

to

coun

trie

s •

that

fulf

ill a

stri

ct s

et o

f co

nd

itio

ns.

All I

MF

len

din

g w

ould

•

be

shor

t-te

rm;i

f a

coun

try

did

not

mak

e ti

mel

y pay

men

ts it

• w

ould

not

be

elig

ible

for

IM

F m

oney

for

fiv

e ye

ars.

Mic

hel

Cam

des

sus

Inte

rnat

ion

al

• M

ake

IMF

surv

eillan

ce m

ore

effe

ctiv

e an

d e

nh

ance

“T

he

IMF

an

d its

Pro

gram

s in

Asi

a,”

Mon

etar

y F

un

d•

tran

spar

ency

.R

emar

ks a

t th

e C

oun

cil on

For

eign

•

Str

engt

hen

fin

anci

al a

nd

ban

kin

g sy

stem

s as

wel

l as

th

eir

Rel

atio

ns,

New

Yor

k,F

ebru

ary

6,19

98•

super

visi

on.

• E

stab

lish

mor

e ef

fect

ive

pro

ced

ure

s to

in

volv

e th

e •

pri

vate

sec

tor

in p

reve

nti

ng

and

res

olvi

ng

deb

t cr

ises

.•

Con

tin

ue

to lib

eral

ize

inte

rnat

ion

al c

apit

al f

low

s.

Private Capital Flows

[25]

B.C

han

ges

In G

ove

rnm

ent

Reg

ula

tory

Pra

ctic

es (

con

tin

ued

)A

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

Bar

ry E

ich

engr

een

Un

iver

sity

of

• N

ew in

tern

atio

nal

sta

nd

ard

s fo

r ban

k re

gula

tion

,T

owar

d a

New

In

tern

atio

nal

Fin

anci

al

Cal

ifor

nia

,Ber

kele

y •

ban

kruptc

y la

ws,

aud

itin

g,co

rpor

ate

gove

rnan

ce.

“Arc

hit

ectu

re:a

Pra

ctic

al P

ost-

Asi

a A

gen

da,

”•

Tax

atio

n o

f al

l sh

ort-

term

cap

ital

in

flow

s in

to e

mer

gin

g In

stit

ute

for

In

tern

atio

nal

Eco

nom

ics,

• m

arke

ts.

Feb

ruar

y 19

99•

Pro

mot

ion

of

ord

erly

deb

t re

stru

cturi

ngs

th

rough

maj

orit

y “C

apit

al M

obilit

y:T

ies

Nee

d N

ot B

ind

,”•

voti

ng,

burd

en-s

har

ing,

and

col

lect

ive

repre

sen

tati

on o

f M

ilke

n I

nst

itute

Rev

iew

,Fir

st Q

uar

ter,

1999

• cr

edit

ors

to a

void

law

suit

s an

d o

bst

ruct

ion

of

sett

lem

ents

.•

Fle

xible

exc

han

ge r

ates

.•

Cap

ital

con

trol

s fo

r em

ergi

ng

mar

kets

.•

Ind

epen

den

t ce

ntr

al b

ank.

• P

erh

aps

an in

dep

end

ent

nat

ion

al f

isca

l co

un

cil.

• M

easu

res

that

en

han

ce t

ran

spar

ency

.

Ala

n G

reen

span

Ch

airm

an,F

eder

al

Res

tric

tin

g co

ntr

ols

to s

hor

t-te

rm c

apit

al in

flow

s—as

oft

enR

emar

ks a

t th

e A

nn

ual

Mee

tin

g of

th

eR

eser

ve B

oard

reco

mm

end

ed—

is n

ot a

sol

uti

on.2

1st-

cen

tury

fin

anci

alS

ecuri

ties

In

dust

ry A

ssoc

iati

on,B

oca

Rat

on,

regu

lati

on m

ust

in

crea

sin

gly

rely

on

cou

nte

rpar

ty

Flo

rid

a,N

ovem

ber

5,1

998

surv

eillan

ceto

ach

ieve

saf

ety

and

sou

nd

nes

s.T

her

e is

no

cred

ible

way

mos

t go

vern

men

t fi

nan

cial

reg

ula

tion

can

be

anyt

hin

g ot

her

th

an o

vers

igh

t of

pro

cess

.

Yago

[26]

B.C

han

ges

In G

ove

rnm

ent

Reg

ula

tory

Pra

ctic

es (

con

tin

ued

)A

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

Gro

up o

f T

hir

tyA

mon

g th

e re

com

men

dat

ion

s ar

e:“G

lobal

In

stit

uti

ons,

Nat

ion

al S

uper

visi

on

• C

reat

e a

stan

din

g in

dust

ry c

omm

itte

e to

pro

mulg

ate

and

an

d S

yste

mic

Ris

k,”

A S

tud

y G

roup

• re

view

glo

bal

pri

nci

ple

s fo

r m

anag

ing

risk

.R

epor

t,G

roup o

f T

hir

ty,1

997

• A

gree

upon

how

aud

itor

s sh

ould

appro

ach

aud

its

of

• fi

nan

cial

sta

tem

ents

an

d o

ther

in

form

atio

n f

or p

ortr

ayin

g •

risk

.•

Super

viso

rs s

hou

ld a

gree

upon

a lea

d c

oord

inat

or f

or a

ll

• gl

obal

fin

anci

al in

stit

uti

ons.

• N

atio

nal

leg

isla

ture

s sh

ould

pro

vid

e a

reliab

le leg

al

• fr

amew

ork

for

inte

rnat

ion

al t

ran

sact

ion

s.

Pau

l K

rugm

anM

IT•

Lim

it c

apit

al f

low

s to

em

ergi

ng-

mar

ket

coun

trie

s th

at

“Dep

ress

ion

Eco

nom

ics

Ret

urn

s,”

• ar

e un

suit

able

for

curr

ency

un

ion

s,fr

ee f

loat

ing

For

eign

Aff

airs

,Jan

uar

y/F

ebru

ary,

1999

• ex

chan

ge r

ates

.•

Rer

egula

te c

apit

al m

arke

ts t

o so

me

exte

nt.

• F

or s

ome

coun

trie

s,lo

w in

flat

ion

mig

ht

be

a pre

ferr

ed

• al

tern

ativ

e to

pri

ce s

tabilit

y.

Private Capital Flows

[27]

C.

Mix

of

Po

licy

Ch

ange

s an

d M

ark

et-B

ased

Ref

orm

sA

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

AP

EC

Busi

nes

s •

Th

e IM

F s

hou

ld t

ake

into

acc

oun

t so

cial

im

plica

tion

s “L

ette

r fr

om t

he

AP

EC

Busi

nes

s A

dvi

sory

A

dvi

sory

Cou

nci

l•

of its

pro

gram

s.C

oun

cil to

th

e E

con

omic

Lea

der

s,”

Th

e 19

98

• E

nh

ance

dom

esti

c ca

pit

al-m

arke

t in

fras

truct

ure

.A

PE

C R

epor

t to

th

e E

con

omic

Lea

der

s•

Cou

ntr

ies

shou

ld u

nd

erta

ke leg

al,r

egula

tory

,an

d

• ac

coun

tin

g re

form

s to

fac

ilit

ate

fin

anci

al r

eorg

aniz

atio

n.

• D

evel

op d

omes

tic

capit

al m

arke

ts t

hro

ugh

th

e •

dev

elop

men

tof

liquid

bon

d a

nd

ass

et-b

acke

d s

ecuri

ties

•

mar

kets

.•

Cou

ntr

ies

shou

ld c

onsi

der

mec

han

ism

s fo

r re

stru

cturi

ng

• co

rpor

ate

deb

t th

rough

deb

t-eq

uit

y sw

aps.

• R

emov

e re

stri

ctio

ns

on a

nd

en

coura

ge t

he

use

of

• se

curi

tiza

tion

str

uct

ure

s of

tra

de

rece

ivab

les

for

trad

e •

fin

ance

.

Rob

ert

Bar

roH

arva

rd U

niv

ersi

ty•

Cap

ital

con

trol

s,w

hile

not

id

eal,

are

pre

fera

ble

to

the

“Mal

aysi

a co

uld

do

wor

se t

han

th

is e

con

omic

• IM

F’s

cust

omar

y fi

x of

in

terv

enti

on w

ith

hig

h in

tere

st

pla

n,”

Busi

nes

s W

eek,

Nov

ember

2,1

998

• ra

tes.

Th

e bes

t pol

icy

wou

ld e

nta

il a

fix

ed e

xch

ange

rat

e •

wit

hou

t ca

pit

al c

ontr

ols,

wit

h t

he

cen

tral

ban

k in

terv

enin

g,•

but

not

ste

rilizi

ng.

• A

curr

ency

boa

rd is

wor

th c

onsi

der

ing

in m

ore

coun

trie

s.

Bas

el C

omm

itte

e B

ank

for

• E

mph

asiz

es c

omple

men

tary

in

tera

ctio

n o

f pru

den

tial

“E

nh

anci

ng

Ban

k T

ran

spar

ency

,”on

Ban

kin

g In

tern

atio

nal

•

super

visi

on a

nd

mar

ket

dis

ciplin

e.S

epte

mber

22,

1998

,Publica

tion

of

the

Boa

rdS

uper

visi

onS

ettl

emen

ts•

Rei

nfo

rce

the

effo

rts

of s

uper

viso

rs b

y re

war

din

g fo

r In

tern

atio

nal

Set

tlem

ents

•

ban

ks t

hat

man

age

risk

eff

ecti

vely

an

d p

enal

izin

g ban

ks

• w

hos

e ri

sk m

anag

emen

t is

in

ept

or im

pru

den

t.(c

ont.

)

Yago

[28]

C.

Mix

of

Po

licy

Ch

ange

s an

d M

ark

et-B

ased

Ref

orm

s (c

on

tin

ued

)A

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

G-7

•C

oun

trie

s ad

opt

and

apply

cod

es o

f co

nd

uct

fou

nd

ed

HM

Tre

asury

New

s R

elea

se,O

ctob

er 3

0,1

998.

• on

min

imum

sta

nd

ard

s an

d b

est

pra

ctic

e.A

vailab

le a

t:w

ww

.hm

_tre

asury

.gov

.uk/

pub/

•Cou

ntr

ies

must

com

ply

wit

h a

n in

tern

atio

nal

ly

htm

l/pre

ss98

/p17

9_h

tml

• ag

reed

cod

e of

con

duct

on

mon

etar

y an

d f

isca

l pol

icy.

•Cou

ntr

ies

must

com

ply

wit

h a

n in

tern

atio

nal

sta

nd

ard

•

of b

est

pra

ctic

e fo

r tr

ansp

aren

cy a

nd

dis

clos

ure

by

• fi

nan

cial

in

stit

uti

ons

and

th

eir

regu

lato

rs.

Rob

ert

Rubin

U.S

.Tre

asury

•

Cou

ntr

ies

shou

ld p

rovi

de

bet

ter

info

rmat

ion

O

ffic

e of

Public

Aff

airs

,U.S

.Tre

asury

D

epar

tmen

t•

thro

ugh

im

pro

ved

dis

clos

ure

an

d t

ran

spar

ency

.D

epar

tmen

t,A

pri

l 14

,199

8•

Cou

ntr

ies

build

ing

stro

ng

nat

ion

al s

ecto

rs s

hou

ld

• cr

eate

mec

han

ism

s so

th

at t

he

pri

vate

sec

tor

mor

e fu

lly

• bea

rs t

he

con

sequen

ces

of its

cre

dit

an

d in

vest

men

t •

dec

isio

ns.

• N

eed

to

pro

vid

e fo

r in

tern

atio

nal

surv

eillan

ce o

f •

coun

trie

s’fi

nan

cial

reg

ula

tory

an

d s

uper

viso

ry s

yste

ms.

Jose

ph

Sti

glit

zW

orld

Ban

k•

Gre

ater

tra

nsp

aren

cy a

nd

mor

e in

form

atio

n a

bou

t A

dd

ress

to

the

Ch

icag

o C

oun

cil on

For

eign

•

capit

al f

low

s.R

elat

ion

s,C

hic

ago,

Feb

ruar

y 27

,199

8•

Cou

ntr

ies

shou

ld t

ry t

o in

fluen

ce t

he

pat

tern

an

d

• co

mpos

itio

n o

f ca

pit

al f

low

s.

Pau

l Vol

cker

For

mer

Ch

airm

an,

Em

ergi

ng

econ

omie

s sh

ould

see

k fi

nan

cial

saf

ety

and

“G

lobal

Fin

ance

,”E

con

omis

t,Ja

nuar

y 30

,199

9F

eder

al R

eser

ve

curr

ency

sta

bilit

y in

div

ersi

ty (

fore

ign

ow

ner

ship

in

B

oard

fin

anci

al s

ecto

r) a

nd

siz

e (r

egio

nal

curr

ency

arr

ange

-m

ents

).E

mer

gin

g m

arke

ts s

hou

ld lin

k up w

ith

lea

din

g re

gion

al c

urr

ency

.

Private Capital Flows

[29]

D.M

ark

et-B

ased

Ref

orm

sA

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

Jam

es B

arth

,R.

Milke

n I

nst

itute

• E

lim

inat

e st

ate-

own

ed b

anks

.“T

he

Rol

e of

Gov

ern

men

ts a

nd

Mar

kets

in

D

an B

rum

bau

gh,

• A

llow

for

eign

ban

k en

try.

Inte

rnat

ion

al B

anki

ng

Cri

ses:

Th

e C

ase

of

Lal

ita

Ram

esh

,•

Per

mit

th

e fr

eer

flow

of

inte

rnat

ion

al c

apit

al.

Eas

t A

sia,

”R

esea

rch

in

Fin

anci

al S

ervi

ces:

& G

len

n Y

ago

• P

rom

ote

allo

cati

on o

f cr

edit

by

mar

ket

forc

es.

Pri

vate

an

d P

ublic

Pol

icy,

JAI

Pre

ss I

nc.

,199

8•

Dis

coura

ge in

appro

pri

ate

bai

louts

for

cre

dit

ors.

Mic

hae

l B

ord

o N

atio

nal

Bure

au o

f •

Flo

atin

g ex

chan

ge r

ates

.“U

nd

er W

hat

Cir

cum

stan

ces,

Pas

t an

d

& A

nn

a E

con

omic

Res

earc

h•

In a

wor

ld o

f d

eep c

apit

al m

arke

ts,f

ew g

ood

rea

son

s P

rese

nt,

Hav

e In

tern

atio

nal

Res

cues

of

S

chw

artz

• w

hy

pri

vate

mar

kets

can

not

per

form

as

the

role

of

len

der

C

oun

trie

s in

Fin

anci

al D

istr

ess

Bee

n

• of

las

t re

sort

in

stea

d o

f th

e IM

F.S

ucc

essf

ul?

”N

BE

R,W

orki

ng

Pap

er n

o.68

24

Rud

iger

M

ITE

stab

lish

men

t of

a c

urr

ency

boa

rd.

“Aft

er A

sia:

New

Dir

ecti

ons

for

the

Dor

nbusc

hIn

tern

atio

nal

Iin

anci

al S

yste

m,”

July

199

8 A

vailab

le a

t:h

ttp:/

/ww

w.m

it.e

du/~

rud

i/pap

ers.

htm

l

Ste

ve H

anke

Joh

ns

Hop

kin

s D

evel

opin

g co

un

trie

s sh

ould

un

ify

thei

r cu

rren

cies

wit

hC

ato

Inst

itute

ís 1

6th

An

nual

Mon

etar

y U

niv

ersi

tyst

ron

ger

ones

via

fix

ed e

xch

ange

rat

es s

uppor

ted

by

Con

fere

nce

,mim

eo,O

ctob

er 2

2,19

98cu

rren

cy b

oard

mon

etar

y in

stit

uti

ons.

Ran

dal

l K

rosz

ner

Un

iver

sity

of

• P

ublic

regu

lati

on s

hou

ld n

ot c

row

d o

ut

pri

vate

reg

ula

tion

.“T

he

Rol

e of

Pri

vate

Reg

ula

tion

in

C

hic

ago

• A

un

ifie

d in

tern

atio

nal

reg

ula

tor

is lik

ely

to s

low

M

ain

tain

ing

Glo

bal

Fin

anci

al S

tabilit

y,”

16

• in

nov

atio

ns

and

gro

wth

of

inte

rnat

ion

al f

inan

cial

mar

kets

.A

nn

ual

Mon

etar

y C

onfe

ren

ce,C

ato

Inst

itute

,•

Public

regu

lati

ons

shou

ld b

e su

bje

ct t

o a

rough

cos

t-O

ctob

er 2

2,19

98•

ben

efit

an

alys

is t

o as

sess

fea

sibilit

y.(c

ont.

)

Yago

[30]

D.M

ark

et-B

ased

Ref

orm

s (c

on

tin

ued

)A

uth

or

Aff

ilia

tio

nP

rop

osa

lS

ou

rce

Rob

ert

Lit

anB

rook

ings

•

Cou

ntr

ies

shou

ld p

ass

sim

ple

ban

kruptc

y le

gisl

atio

n.

“Ban

kruptc

y B

ailo

ut

Cou

ld F

ix A

sia’

s In

stit

uti

on•

No

nee

d f

or n

ew in

tern

atio

nal

ban

kruptc

y ag

ency

.Deb

tW

oes,

”N

ewsd

ay,M

arch

4,1

998

• pro

ble

ms

are

inte

rnal

an

d p

lagu

e fi

rms,

not

gov

ern

men

ts.

“Asi

an P

roble

ms

and

th

e IM

F,”

test

imon

y

Allan

Mel

tzer

Car

neg

ie M

ello

n

Th

e B

IS (

as a

cen

tral

ban

k fo

r al

l ce

ntr

al b

anks

) ca

npre

par

ed f

or t

he

Join

t E