Embed Size (px)

Citation preview

Page 1 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Sure Success Series

Principles

&

Practices of Banking ( As per NEW UPDATED SYLLABUS For

JAIIB/ Diploma in Banking & Finance

Examination for November 2015 exam onwards)

3rd Edition By: Vaibhav Awasthi

Page 2 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

The content of this book has been developed keeping in view courseware for the First

paper on Principles & Practices of Banking of JAIIB as per the revised syllabus for

November 2015 exam onwards..

An attempt has been made to cover fully the syllabus prescribed for each module/subject

and the presentation of topics may not always be in the same sequence as given in the

syllabus. Candidates are also expected to take note of all the latest developments

relating to the subjects covered in the syllabus by referring to RBI circulars, financial

papers, economic journals, latest books and publications in the subjects concerned.

Although due care has been taken in publishing this study material, yet the possibility of

errors, omissions and/or discrepancies cannot be ruled out.

We welcome suggestion for improving the book and its contents. You may write back to

us at [email protected]

All rights reserved. No part of this publication may be reproduced or transmitted, in any form

or by any means, without permission. Any person who does any unauthorized act in relation to

this publication may be liable to criminal proceedings and civil claim for damages.

This book is meant for educational and learning purpose. The author of this book has taken all reasonable care to ensure that the

contents of the book do not violate any existing copyright or other intellectual property rights of any person in any manner

whatsoever.

About the Author:

Vaibhav Awasthi, has experience of 11 years in Banking. He has done his graduation

from Kanpur University and MBA (Finance) from Delhi. He also holds the distinction

of being part of maiden batch of “Certified Banking Compliance Professional”

conducted by IIBF & ICSI.

He has been mentoring students for JAIIB/CAIIB since last 9 years and presently

works as Senior Manager in a leading Public Sector Bank.

He can be reached at [email protected]

Page 3 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

To the thought

“We all live under the same sky,

but we all don't have the same horizon”

Page 4 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Preface Dear Students,

Principles & Practices of Banking is the first paper of JAIIB exam. Typically this paper is

most useful as it provides deep knowledge to candidates about the day to day banking

operations. The syllabus is designed in a manner so that students can understand the

financial system, role of banks, various aspects of day to day banking and role of

technology and marketing in changing banking scenario

[[The subject is divided into four module and questions are evenly asked from all the

modules thus while preparing students must not ignore any module.

Easiest amongst the entire four modules is Module A. Students can not only finish it in

short time but also gain good marks in the final exam.

Module B is very important as it covers myriad topics ranging from banker customer

relationship, KYC, loans and advances. This module occupies prime importance in

questions being asked in exam. The question asked from this module is often with a twist

and based like a case study and thus students should have conceptual grasp over the

topics from this module.

Module C deals with computerization in banking and deals with the evolution of

technology in banking sector along with various technology used by banks currently for

performing various banking operations. A very important module and students should go

through it carefully.

The last module is of marketing. With growing competition and technology, role of

marketing has become very important for all the banks so as to stay in the market. So

what is marketing, what is branding & promotion? How banks have evolved various

marketing channels etc. is being discussed in this module.

[When students take up this subject, they are worried about the mock questions. We

assure you that students should focus on understanding the concept rather than being

over obsessed with solving objective mock questions and through this book we have tried

to impart concept based understanding to our students.

The book has been written based on our experience about prior year question papers. We

have tried to keep the book concise and most relevant by explaining all the important

points’ chapter wise along with objective questions for testing the knowledge.

The aim of our Sure Success Series- is to make sure that students are able to finish the

course in minimum possible time. We wish you all the best for your exams.

Page 5 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

MODULE-A

INDIAN FINANCIAL

SYSTEM

Page 6 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

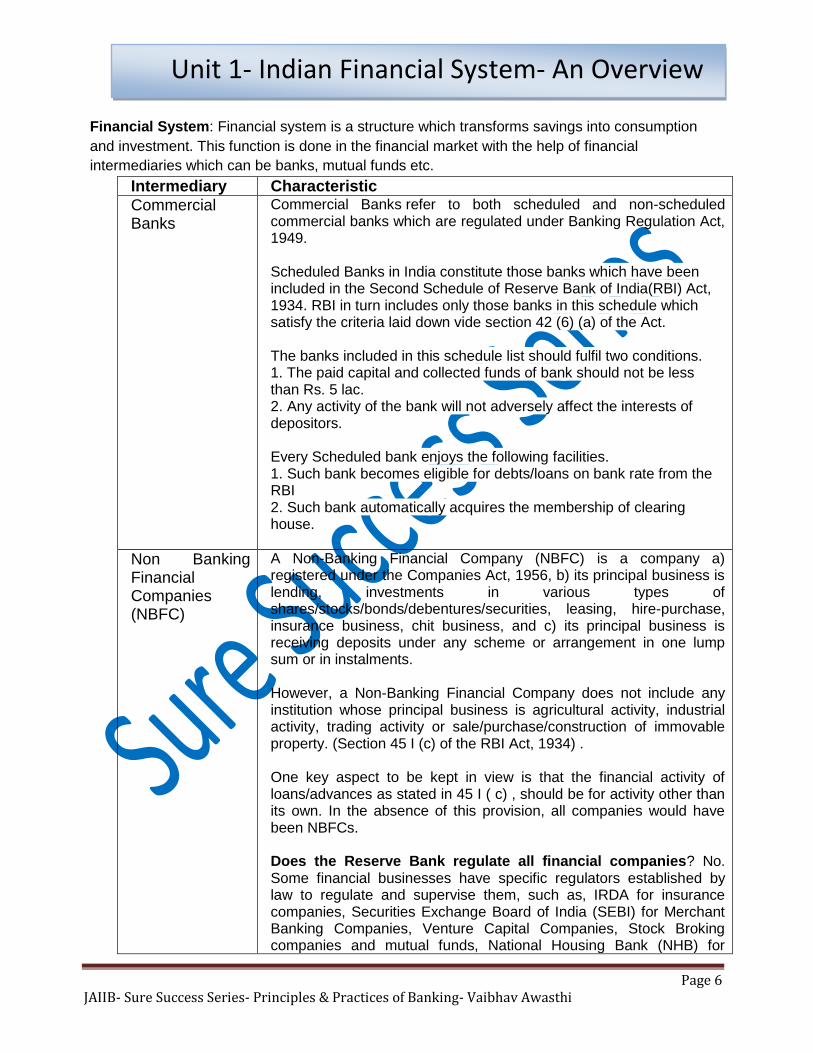

Financial System: Financial system is a structure which transforms savings into consumption

and investment. This function is done in the financial market with the help of financial

intermediaries which can be banks, mutual funds etc.

Intermediary Characteristic

Commercial Banks

Commercial Banks refer to both scheduled and non-scheduled commercial banks which are regulated under Banking Regulation Act, 1949. Scheduled Banks in India constitute those banks which have been included in the Second Schedule of Reserve Bank of India(RBI) Act, 1934. RBI in turn includes only those banks in this schedule which satisfy the criteria laid down vide section 42 (6) (a) of the Act. The banks included in this schedule list should fulfil two conditions. 1. The paid capital and collected funds of bank should not be less than Rs. 5 lac. 2. Any activity of the bank will not adversely affect the interests of depositors. Every Scheduled bank enjoys the following facilities. 1. Such bank becomes eligible for debts/loans on bank rate from the RBI 2. Such bank automatically acquires the membership of clearing house.

Non Banking Financial Companies (NBFC)

A Non-Banking Financial Company (NBFC) is a company a) registered under the Companies Act, 1956, b) its principal business is lending, investments in various types of shares/stocks/bonds/debentures/securities, leasing, hire-purchase, insurance business, chit business, and c) its principal business is receiving deposits under any scheme or arrangement in one lump sum or in instalments. However, a Non-Banking Financial Company does not include any institution whose principal business is agricultural activity, industrial activity, trading activity or sale/purchase/construction of immovable property. (Section 45 I (c) of the RBI Act, 1934) . One key aspect to be kept in view is that the financial activity of loans/advances as stated in 45 I ( c) , should be for activity other than its own. In the absence of this provision, all companies would have been NBFCs. Does the Reserve Bank regulate all financial companies? No. Some financial businesses have specific regulators established by law to regulate and supervise them, such as, IRDA for insurance companies, Securities Exchange Board of India (SEBI) for Merchant Banking Companies, Venture Capital Companies, Stock Broking companies and mutual funds, National Housing Bank (NHB) for

Unit 1- Indian Financial System- An Overview

Page 7 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

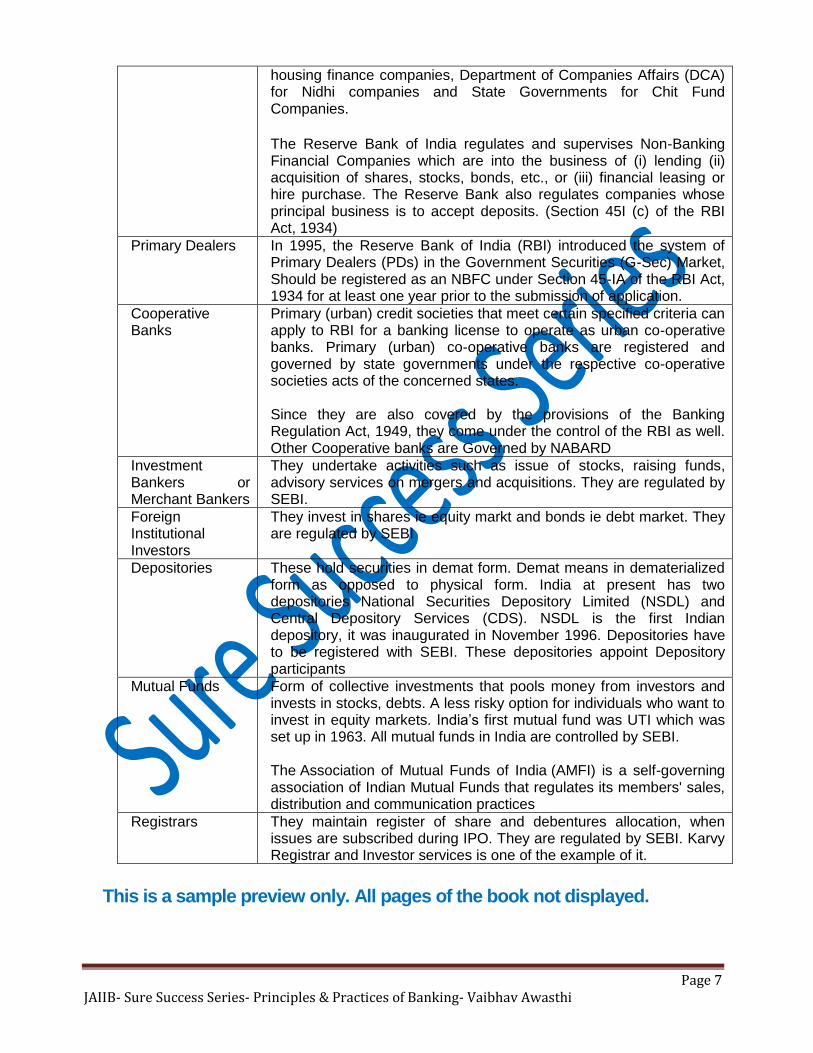

housing finance companies, Department of Companies Affairs (DCA) for Nidhi companies and State Governments for Chit Fund Companies.

The Reserve Bank of India regulates and supervises Non-Banking Financial Companies which are into the business of (i) lending (ii) acquisition of shares, stocks, bonds, etc., or (iii) financial leasing or hire purchase. The Reserve Bank also regulates companies whose principal business is to accept deposits. (Section 45I (c) of the RBI Act, 1934)

Primary Dealers In 1995, the Reserve Bank of India (RBI) introduced the system of Primary Dealers (PDs) in the Government Securities (G-Sec) Market, Should be registered as an NBFC under Section 45-IA of the RBI Act, 1934 for at least one year prior to the submission of application.

Cooperative Banks

Primary (urban) credit societies that meet certain specified criteria can apply to RBI for a banking license to operate as urban co-operative banks. Primary (urban) co-operative banks are registered and governed by state governments under the respective co-operative societies acts of the concerned states. Since they are also covered by the provisions of the Banking Regulation Act, 1949, they come under the control of the RBI as well. Other Cooperative banks are Governed by NABARD

Investment Bankers or Merchant Bankers

They undertake activities such as issue of stocks, raising funds, advisory services on mergers and acquisitions. They are regulated by SEBI.

Foreign Institutional Investors

They invest in shares ie equity markt and bonds ie debt market. They are regulated by SEBI

Depositories These hold securities in demat form. Demat means in dematerialized form as opposed to physical form. India at present has two depositories National Securities Depository Limited (NSDL) and Central Depository Services (CDS). NSDL is the first Indian depository, it was inaugurated in November 1996. Depositories have to be registered with SEBI. These depositories appoint Depository participants

Mutual Funds Form of collective investments that pools money from investors and invests in stocks, debts. A less risky option for individuals who want to invest in equity markets. India’s first mutual fund was UTI which was set up in 1963. All mutual funds in India are controlled by SEBI. The Association of Mutual Funds of India (AMFI) is a self-governing association of Indian Mutual Funds that regulates its members' sales, distribution and communication practices

Registrars They maintain register of share and debentures allocation, when issues are subscribed during IPO. They are regulated by SEBI. Karvy Registrar and Investor services is one of the example of it.

This is a sample preview only. All pages of the book not displayed.

Page 8 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

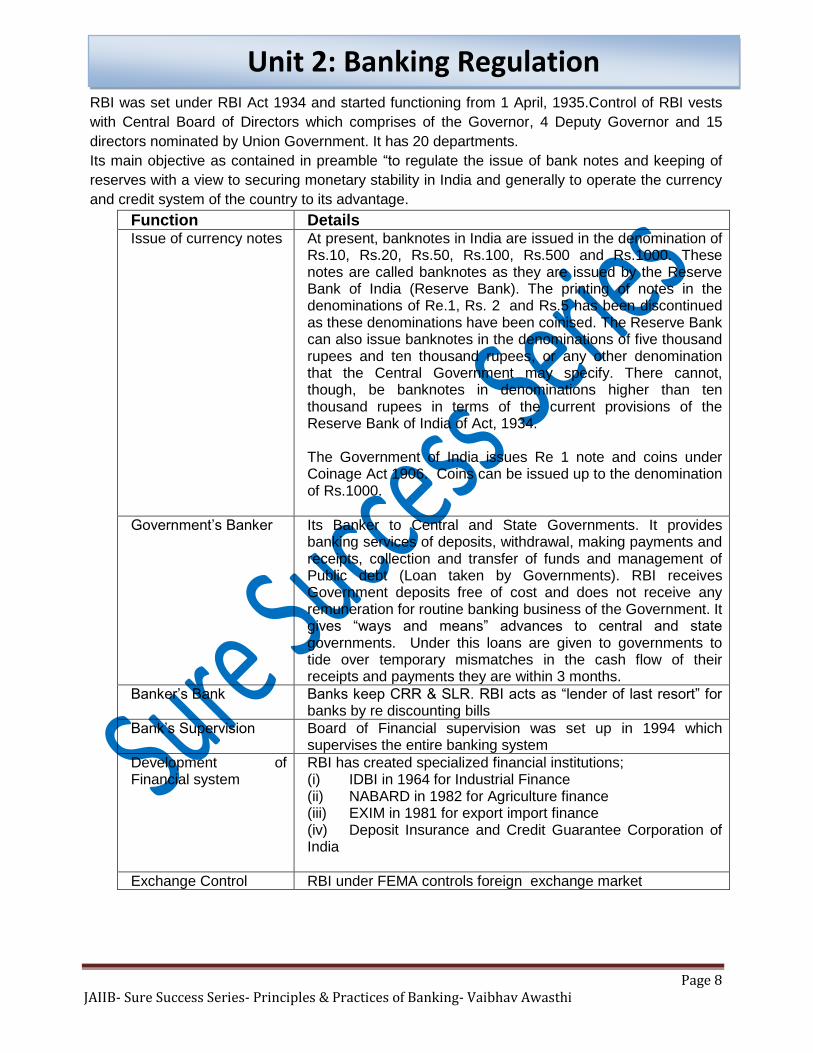

RBI was set under RBI Act 1934 and started functioning from 1 April, 1935.Control of RBI vests

with Central Board of Directors which comprises of the Governor, 4 Deputy Governor and 15

directors nominated by Union Government. It has 20 departments.

Its main objective as contained in preamble “to regulate the issue of bank notes and keeping of

reserves with a view to securing monetary stability in India and generally to operate the currency

and credit system of the country to its advantage.

Function Details Issue of currency notes At present, banknotes in India are issued in the denomination of

Rs.10, Rs.20, Rs.50, Rs.100, Rs.500 and Rs.1000. These notes are called banknotes as they are issued by the Reserve Bank of India (Reserve Bank). The printing of notes in the denominations of Re.1, Rs. 2 and Rs.5 has been discontinued as these denominations have been coinised. The Reserve Bank can also issue banknotes in the denominations of five thousand rupees and ten thousand rupees, or any other denomination that the Central Government may specify. There cannot, though, be banknotes in denominations higher than ten thousand rupees in terms of the current provisions of the Reserve Bank of India of Act, 1934. The Government of India issues Re 1 note and coins under Coinage Act 1906. Coins can be issued up to the denomination of Rs.1000.

Government’s Banker Its Banker to Central and State Governments. It provides banking services of deposits, withdrawal, making payments and receipts, collection and transfer of funds and management of Public debt (Loan taken by Governments). RBI receives Government deposits free of cost and does not receive any remuneration for routine banking business of the Government. It gives “ways and means” advances to central and state governments. Under this loans are given to governments to tide over temporary mismatches in the cash flow of their receipts and payments they are within 3 months.

Banker’s Bank Banks keep CRR & SLR. RBI acts as “lender of last resort” for banks by re discounting bills

Bank’s Supervision Board of Financial supervision was set up in 1994 which supervises the entire banking system

Development of Financial system

RBI has created specialized financial institutions; (i) IDBI in 1964 for Industrial Finance (ii) NABARD in 1982 for Agriculture finance (iii) EXIM in 1981 for export import finance (iv) Deposit Insurance and Credit Guarantee Corporation of India

Exchange Control RBI under FEMA controls foreign exchange market

Unit 2: Banking Regulation

Page 9 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Monetary control: RBI has to manage supply of money in the economy to control inflationary

or deflationary trends. Let’s take an example, let rate at which loan is available is just 2 % it

means people can take loan at just 2%. With money being available so easily people will start

taking loans and will buy cars, bikes, new houses, other goods. Supply of these goods cannot be

increased in short term, thus to meet the demand prices will increase, which will result in inflation.

Thus money supply needs to be controlled which can be done by reducing the ability of Banks to

lend at cheaper rates. This can be done by:

(i) CRR: Cash deposit which Banks need to keep with RBI as a percentage of their Demand

and Time liability. Banks do not get any interest on CRR.

(ii) SLR: Deposits which banks need to keep with RBI in the form of approved security, gold as

a percentage of their Demand and Term liability.

(iii) Bank Rate: It is the rate at which the Reserve Bank is ready to buy or rediscount bills of

exchange or other commercial papers.

(iv) Open market operations: RBI can buy or sell securities from open market (bond market).

If RBI sells securities, banks/other financial intermediaries will buy them thus liquidity (ie money)

will be sucked out of the system and Banks will not be able to lend and vice versa.

(v) Selective credit control: RBI issues directives under Sections 21 and 35A of BR act

stipulating certain restrictions on bank advances, against specified sensitive commodities.

Presently only buffer stocks of sugar, levy sugar and unreleased stocks of sugar with sugar mills

representing free sale sugar are covered under this.

Regulatory restrictions on lending: There are certain restrictions lending under BR Act:

1. No advance or loan can be granted against security of bank’s own share or partly paid

shares of other companies.

2. No loan against (i) CD (ii) FD issued by other banks (iii) Money market mutual funds

3. No Bank can hold shares in a company as a pledgee or mortgagee in excess of 30 % of

the paid up capital of that company or 30 % of Bank’s Paid up capital and reserves whichever is

less

4. Total investment in capital market should not exceed 40% of Bank’s networth as on end of

previous year

Extras for your knowledge: Zimbabwe is most classic case of Hyperinflation. At the height of inflation in 2008-2009, monthly inflation was 6.5 sextillion (sextillion = 1021) . Largest note of Zimbabwe was of 100 trillion dollar. At one point, a loaf of bread was Z$550 million in the regular market and Teachers were paid salaries of Z$ 1 trillion per month however it only equaled 1 US dollar. Zimbabwe abandoned its currency in 2009.

India’s public debt was around 450 billion dollar which roughly works out to Rs 27,00,786 crore as on quarter ended June 2014. Debt can be internal or external. Internal debt can be raised in the form short term borrowing up to 1 year in the form of Treasury bills. Treasury bills are of three maturities (91, 182 and 364 days). Debt of more than 1 year is raised by way of dated securities; at present maximum period of dated securities is 30 years in India.

This is a sample preview only. All pages of the book not displayed.

Page 10 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Retail Banking: Catering to banking requirements of Individuals. Retail banking can be both on

asset side as well as liability side. On liability side we have products like saving bank, current

account, term deposits account and on asset side there are products like home loans, personal

loans, vehicle loans, education loans, credit cards receivables, .

There are also a third side which includes credit cards, debit cards, ATMs, third party products.

Retail has become a major focus for all banks. Not only this widens the customer base of the

bank but also reduces the risk.

Wholesale Banking: Doing Banking business with industrial and business entities.The products

included fund based facilities like cash credit, term loans and also non fund based facilities like

bank guarantees and letter of credit.

Bank also plays a major role in enhancing the cross border trades. In a liberalized economy

export and import of goods and services is a major characteristic.

For a country like India, export is crucial. Not only it enhances the production capacity and

earnings of Indian manufactures but also earns valuable foreign exchange which is essential for

the health of any economy. Export credit has also been included under Priority sector lending.

Various facilities available to finance exporters are

(i) Packing credit in Indian rupees

(ii) Post shipment credit

(iii) Packing credit in foreign currency

(iv) Post shipment credit in foreign currency.

Export credits are eligible for concessional rate of interest.

Universal Banking: offering all financial products like banking, insurance, mutual funds, advisory

etc

Products: can be divided into 4 categories

1. Fund based: Term loans, working capital, export credit, bills discounting.

2. Non Fund based: Bank Guarantee, letter of Credit

3. Value Added services: Cash management services, channel financing,

syndication, tax collection

4. Internet Banking Services: Payment gateway services, Corporate Internet

Banking

Depository receipts: It is a negotiable (transferable) financial instrument traded on a local

stock exchange of a country, but represents a security in the form of equity, issued by foreign

public listed company.

For eg: If Infosys wants to raise money in US, it will issue ADRs, ADRs are just like shares which

needs to be listed on local stock exchange (NYSE, NASDAQ). These ADRs are denominated in

US Dollar and Investors in US can buy these ADRs just like they buy shares. Thus in this way

Indian Company can get dollars and Investors in US get a chance to buy equity holding in Indian

company.

Unit-3 Retail Banking, Wholesale Banking and International

Banking, ADR, GDR and Participatory notes

Page 11 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Two important depository receipts are ADRs and GDRs, while ADRs are listed on American

stock exchanges, GDRs are listed on European stock exchanges. There are IDRs ( Indian

Depository receipts) also under which foreign companies list their depository receipts on Indian

stock exchanges.

Participatory Notes : Commonly known as P- Notes or PN, are instruments issued by registered

foreign institutional investors (FII) to overseas investors, who wish to invest in the Indian stock

markets without registering themselves with SEBI.

How P-Notes work? To understand this first understand how foreign investors can invest in

Indian stock markets. Foreign Institutional Investors (FIIs), are entities established outside India

which buy and sell bulk shares. These FIIs need to be registered with SEBI. These registered FIIs

then buy Indian based securities, pool them together and issue Participatory notes to foreign

investors. For e.g.let’s say there is a FII called ABC, it will be registered with SEBI. It will buy

shares in Indian stock markets, pool them together and create a security instrument called P

Notes which is then issued to Investors in America, Europe, Malaysia or any country in the world.

This is a sample preview only. All pages of the book not displayed.

This is a sample preview. To purchase the complete Sure Success

Series log on to our website www.jaiibcaiib.co.in You can also call us

on 07600273309 for any assistance

SEBI") has introduced a new class of foreign investors in India known as the Foreign Portfolio

Investors ("FPIs"). This class has been formed by merging the existing classes of investors

through which portfolio investments were previously made in India namely, the Foreign

Institutional Investors1 ("FIIs"), Qualified Foreign Investors ("QFIs") and sub-accounts of the

FIIs. SEBI introduced the FPI Regulations by a notification4 dated January 7, 2014. The FPI

regulations had limited the use of P-Notes by entities which were not well-regulated.

“Those unregulated broad-based funds that are classified as Category-II FPIs by virtue

of their investment manager being appropriately regulated shall not issue, subscribe to

or otherwise deal in offshore derivative instruments, directly or indirectly,” went the

notification on the new FPI regulations .

The new FPI regime replaced the earlier FII regulations and classifies foreign investors

into three categories. Category-I deals with entities backed by foreign governments.

Category-II is for entities regulated by Sebi’s counterparts in foreign jurisdications, such

as their mutual funds. Those outside these two are in Category-III.

Foreign investors held Rs 2.07 lakh crore through the P-Note route, according to Sebi

data for March 14.

Page 12 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

The Kalyanasundaram Study Group was set up by the Reserve Bank of India in January 1988 to

examine the feasibility and mechanics of starting factoring organisations in the country paved the

way for provision of domestic factoring services in India. The Banking Regulation Act, 1949 was

amended to include factoring as a form of business in which the banks might engage.

What is Factoring?

Factoring is an arrangement whereby a Seller of goods sells his Accounts Receivables (AR) ie

Debtors to a third party specialized in providing such services – commonly referred to as a

Factor. Factor then assumes the responsibility of collection and accounting work.

For example, Company ABC is in business of selling washing machines. ABC sells its goods to

various dealers and offers them credit period of 120 days. Thus ABC will receive money on sales

after 120 days. Let’s say total outstanding debtor of ABC is RS 1 lakh. Now ABC reaches Factor

Company XYZ and sells its entire outstanding Debtors to XYZ. XYZ will buy these outstanding

debtors and will pay Rs 80,000 to ABC immediately after deducting its fees. Rest 20,000 to be

paid after 120 days when all the money from debtors is collected. Once XYZ purchases the

outstanding debtors entire responsibility of managing these debtors, their accounting, their

collection rests with XYZ.

Factoring can be with recourse which means in case after 120 days 1 dealers who owed

Rs 10,000 fails to pay debt XYZ will recover this amount from ABC. In case factoring is

without recourse then bad debt of Rs 10,000 is to be borne by XYZ

How it is different from Bill discounting?

1. Bill discounting is always with recourse, whereas factoring can be either with recourse or

without recourse.

2. In bill discounting, the drawer undertakes the responsibility of collecting the bills and remitting

the proceeds to the financing agency, while the Factor usually undertakes to collect the bills of

the client.

3. Bill discounting facility limits itself to a mode of finance and only that, but a Factor also provides

other services like sales ledger maintenance and advisory services.

4. Discounted bills may be rediscounted several times before they mature for payment. Debts

purchased for factoring cannot be rediscounted, they can only be refinanced.

5. Factoring implies the provision of bulk finance against several unpaid trade generated invoices

in batches; bill financing is individual transaction oriented i.e. each bill is separately assessed and

discounted.

6. Factoring is an off balance sheet mode of financing.

This is a sample preview only. All pages of the book not displayed.

Unit 7 Factoring, Forfaiting services and off balance sheet items

Page 13 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

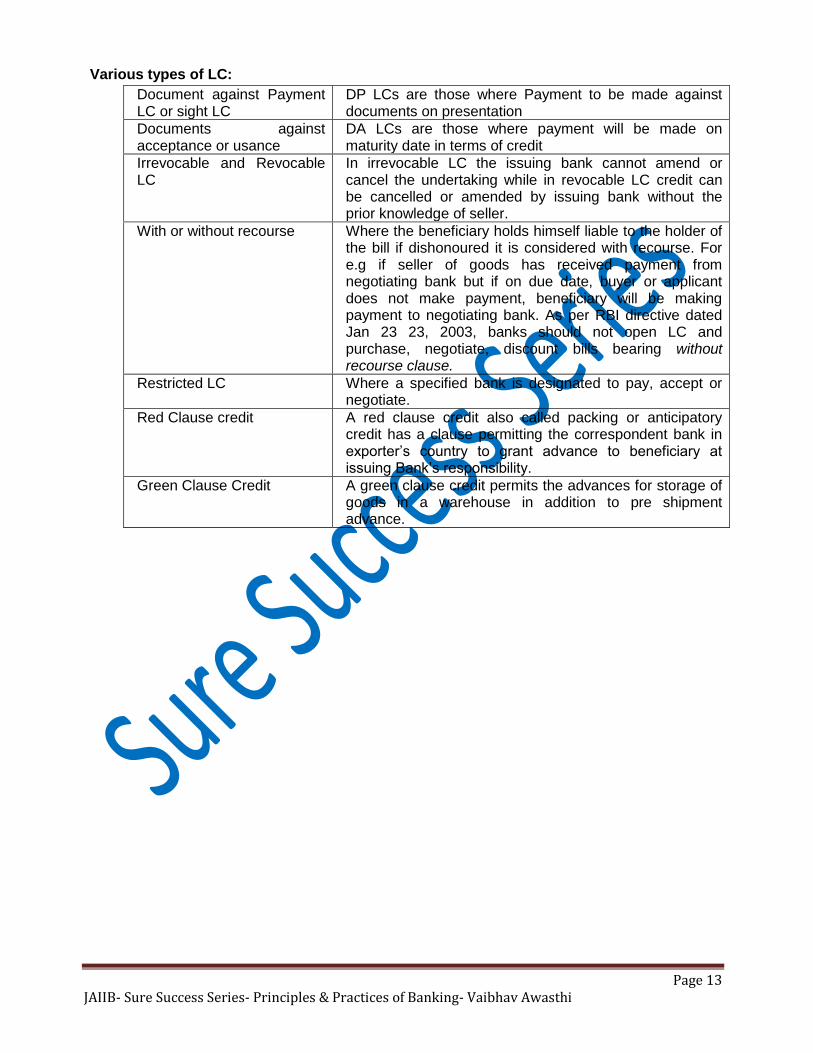

Various types of LC:

Document against Payment LC or sight LC

DP LCs are those where Payment to be made against documents on presentation

Documents against acceptance or usance

DA LCs are those where payment will be made on maturity date in terms of credit

Irrevocable and Revocable LC

In irrevocable LC the issuing bank cannot amend or cancel the undertaking while in revocable LC credit can be cancelled or amended by issuing bank without the prior knowledge of seller.

With or without recourse Where the beneficiary holds himself liable to the holder of the bill if dishonoured it is considered with recourse. For e.g if seller of goods has received payment from negotiating bank but if on due date, buyer or applicant does not make payment, beneficiary will be making payment to negotiating bank. As per RBI directive dated Jan 23 23, 2003, banks should not open LC and purchase, negotiate, discount bills bearing without recourse clause.

Restricted LC Where a specified bank is designated to pay, accept or negotiate.

Red Clause credit A red clause credit also called packing or anticipatory credit has a clause permitting the correspondent bank in exporter’s country to grant advance to beneficiary at issuing Bank’s responsibility.

Green Clause Credit A green clause credit permits the advances for storage of goods in a warehouse in addition to pre shipment advance.

Page 14 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Module B

Functions of Banks

Page 15 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

What are Banks?

Banking has been defined under section 5 (b) of BR act “banking" means the accepting, for the

purpose of lending or investment, of deposits of money from the public, repayable on demand or

otherwise, and withdrawable by cheque, draft, order or otherwise

Important points to be considered:

(i) Deposit should be accepted from public that is the reason nidhi and cooperative societies are

out of its purview.

(ii) Only a firm or company can be Bank, individuals cannot be banks

(iii) If it’s a firm it cannot have more than 10 partners.

(iv) Section 5 (c) banking company" means any company which transacts the business of banking

1[ in India]; Explanation.-- Any company which is engaged in the manufacture of goods or carries

on any trade and which accepts deposits of money from the public merely for the purpose of

financing its business as such manufacturer or trader shall not be deemed to transact the

business of banking within the meaning of this clause;

(v) Money lenders, mahajans, sahukar, shettys are not bankers as they run their business as

individuals or business groups.

(vi) It must accept deposit from public( Mahalaxmi Bank Limited vs Registrar of Companies. In this

company did not accept deposit from public and was thus not considered as bank)

Banker Customer Relationship

(i) Debtor- Creditor :When customer deposits money he is creditor and bank is debtor. When

Bank lends money, bank is creditor and customer is debtor.

Important features under this:

Demand should be made in a proper manner, not verbally or by telephone call but by cheque,

draft, withdrawal form or otherwise. Further demand should be made during working days and

working hours under section 25 & 65 of NI Act 1881.

(ii) Bank as a trustee: If a customer keeps certain valuables or securities with the bank of for

safe keeping or deposits a certain amount of money for specific purpose the banker besides

becoming a bailee also becomes a trustee. In the case of Subramanyan Pillai and others vs Palai

Central Bank Ltd (AIR 1962 Ker 210) , customers deposited Rs 2000 in bank as guarantee

money for purchase of car. Bank failed before car was purchased, Court was of the view that

bank is trustee in this case and should return the money on the basis of preferential debt.

(iii) Bailee- bailor relationship: Bailee is person to whom Personal Property is entrusted for a

particular purpose by another person known as, the bailor, according to the terms of an express

or implied agreement. So if customer deposits certain valuables, bonds, securities or other

documents with bank, for their safe custody, bank becomes trustee as well as bailee. It is the duty

of the bailee to take care of these goods as an ordinary prudent man would.

(iv) Agent Principal Relationship: (Bank is agent, customer is principal) If bank provides

certain ancillary services such as collection of cheques, remittance, payment of bills etc. The

relationship of agency terminates on the death, insolvency, lunacy of the customer or on the

completion of the work assigned.

(v) Lessor- Lessee( Bank as a lessor and customer as a lessee) Bank provides safe deposit

lockers to customer on lease basis.

Unit 12- Banker Customer Relationship

Page 16 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Anti-Money laundering: Offence of money laundering has been defined in section 3 of

Prevention of Money laundering act, 2002 (PMLA) as “Whosoever directly or indirectly attempts

to indulge or knowingly assists or knowingly is a party or is actually involved in any process or

activity connected with the proceeds of crime and projecting it as untainted property shall be

guilty of offence of money laundering.

Stages of Money Laundering:

(i) Placement : First stage refers to physical disposal of proceeds

(ii) Layering: creation of complex layer of financial transactions to conceal audit trail and

anonymity

(iii) Integration: Placing laundered proceeds into legitimate economy as normal funds.

In order that Banks are not used for money laundering RBI has introduced KYC norms.

There are 4 elements of KYC Policy

(A) Customer Acceptance Policy (CAP): It means who can be accepted as customers:

No account is opened in anonymous or fictitious/ benami name(s);

Decide on acceptance criteria for each category of business

Accept customers after verifying their identity

Strive not to

It is important to bear in mind that the adoption of customer acceptance policy and

its implementation should not become too restrictive and must not result in denial of

banking services to general public, especially to those, who are financially or socially

disadvantaged.

RBI’s Recent simplified KYC Measures

Single document for proof of identity and proof of address

There is now no requirement of submitting two separate documents for proof of identity and proof of address. If the officially valid document submitted for opening a bank account has both, identity and address of the person, there is no need for submitting any other documentary proof.

Officially valid documents (OVDs) for KYC purpose include: Passport, driving licence, voters’ ID card, PAN card, Aadhaar letter issued by UIDAI and Job Card issued by NREGA signed by a State Government official.

To further ease the process, the information containing personal details like name, address, age, gender, etc., and photographs made available from UIDAI as a result of e-KYC process can also be treated as an ‘Officially Valid Document’.

Unit – 13 PMLA & KYC

Page 17 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

What is e-KYC?

e-KYC services offered by UIDAI, enables a resident having an Aadhaar number to share their demographic information (NAME, ADDRESS, DATE OF BIRTH etc.) and photograph with a UIDAI partner organization in an online, secure, auditable manner with the residents consent in form of Biometric authentication (Finger Print)or an One Time Password (OTP) authentication.

With use of e-KYC, account opening time can be reduced to a greater degree. Its utility is in following way for the Bank

1. Without integration to CBS, use print out or PDF as KYC document – this provide instant KYC document. In rural area, availability of KYC document, Xerox etc. is a problem. By using e-KYC we can do away with the need of Xerox etc.

2. In later phase, when e-KYC will be integrated with CBS the demographic details like name, father’s name, date of birth, address etc. will be directly inserted in CBS, thus drastically reducing the data entry time

This is a sample preview only. All pages of the book not displayed.

Mandate: A person competent to enter into a contract may authorise another person to open and operate an account on its behalf. This authority can be granted by a mandate or a power of attorney. Mandate is not acceptable from Institutions. Institutions can issue power of attorney. A mandate ceases to be valid on death, insanity, insolvency and bankruptcy of the account holder.

Power of Attorney (P/A)

It is a document executed by one person caller donor ( principal in favour of another person

called done agent) to act on behalf of the former.

Following are salient features of P/A:

(a) Two types of P/A are there

o General P/A – issued for acting in more than one transaction and confers wide powers to done

o Special or limited P/A- issued for specific purpose and is often for single transaction

(b) General P/A gives power to sign cheques, stop payment of cheques, to sign borrowal

documents on behalf of principal.

(c) It is a stamped document and is executed in the presence of a Notary.

Important Points :

If account is jointly operated, authority to third party can be given only when signed by all

account holders

In case of partnership firm, it should be signed by all the partners.

In case of limited companies, power of attorney to be affixed with common seal of company.

Unit 14 Banker’s Special Relationship

Page 18 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Fiduciaries (involving trust, especially with regard to the relationship between a trustee and a

beneficiary) like administrators and legal guardians cannot appoint agents

Garnishee order:

An order of the court obtained by a judgement creditor (one who has given money) for attaching

the funds belonging to a judgement debtor ( one who has taken money) which may be in bank

also. For example, Ram has given loan of Rs 10,000 to Shyam. Shyam has bank account with

Lena bank with deposit of Rs 5000. In case shayam refuses to pay money, Ram can go to court

and get garnishee order, garnishee order will prohibit Lena bank not to make any further

payment from the account till court proceedings are going on. A garnishee order is issued by the

court under order 21 rules 46 of the code of civil Procedure, 1908.

This is a sample preview only. All pages of the book not displayed.

This is a sample preview. To purchase the complete Sure Success Series log on

to our website www.jaiibcaiib.co.in You can also call us on 07600273309 for any

assistance

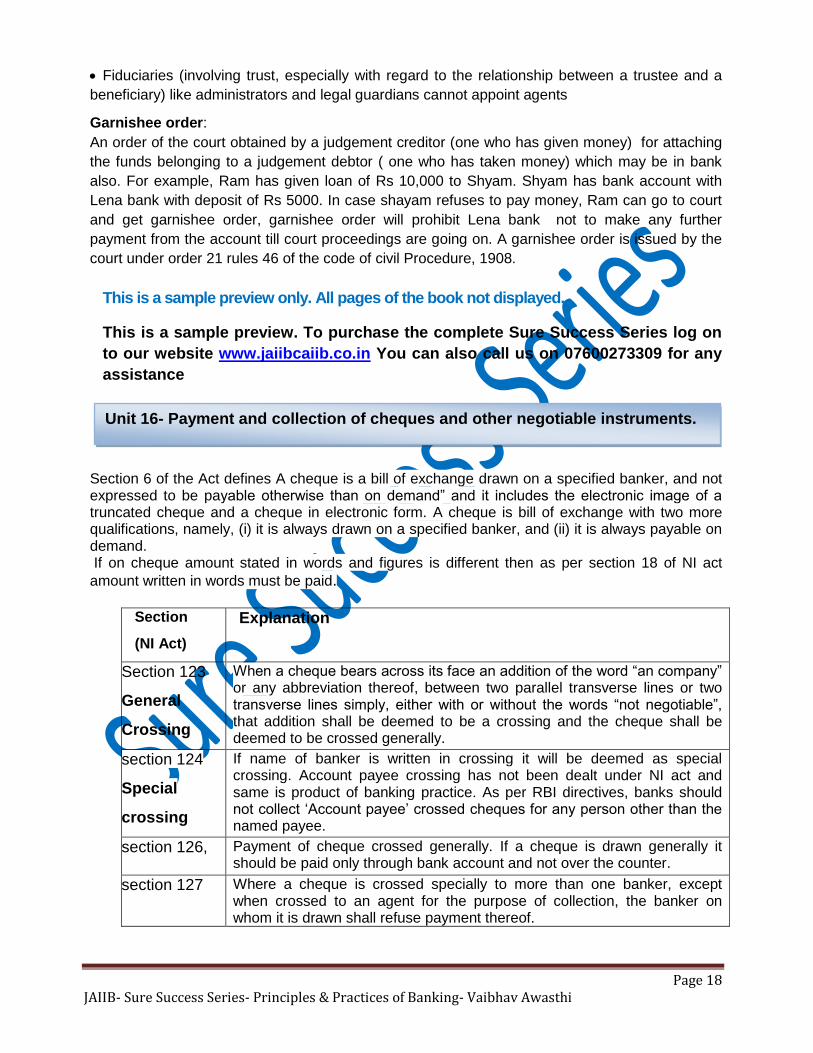

Section 6 of the Act defines A cheque is a bill of exchange drawn on a specified banker, and not expressed to be payable otherwise than on demand” and it includes the electronic image of a truncated cheque and a cheque in electronic form. A cheque is bill of exchange with two more qualifications, namely, (i) it is always drawn on a specified banker, and (ii) it is always payable on demand. If on cheque amount stated in words and figures is different then as per section 18 of NI act

amount written in words must be paid.

Section

(NI Act)

Explanation

Section 123

General

Crossing

When a cheque bears across its face an addition of the word “an company” or any abbreviation thereof, between two parallel transverse lines or two transverse lines simply, either with or without the words “not negotiable”, that addition shall be deemed to be a crossing and the cheque shall be deemed to be crossed generally.

section 124

Special

crossing

If name of banker is written in crossing it will be deemed as special crossing. Account payee crossing has not been dealt under NI act and same is product of banking practice. As per RBI directives, banks should not collect ‘Account payee’ crossed cheques for any person other than the named payee.

section 126, Payment of cheque crossed generally. If a cheque is drawn generally it should be paid only through bank account and not over the counter.

section 127 Where a cheque is crossed specially to more than one banker, except when crossed to an agent for the purpose of collection, the banker on whom it is drawn shall refuse payment thereof.

Unit 16- Payment and collection of cheques and other negotiable instruments.

Page 19 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

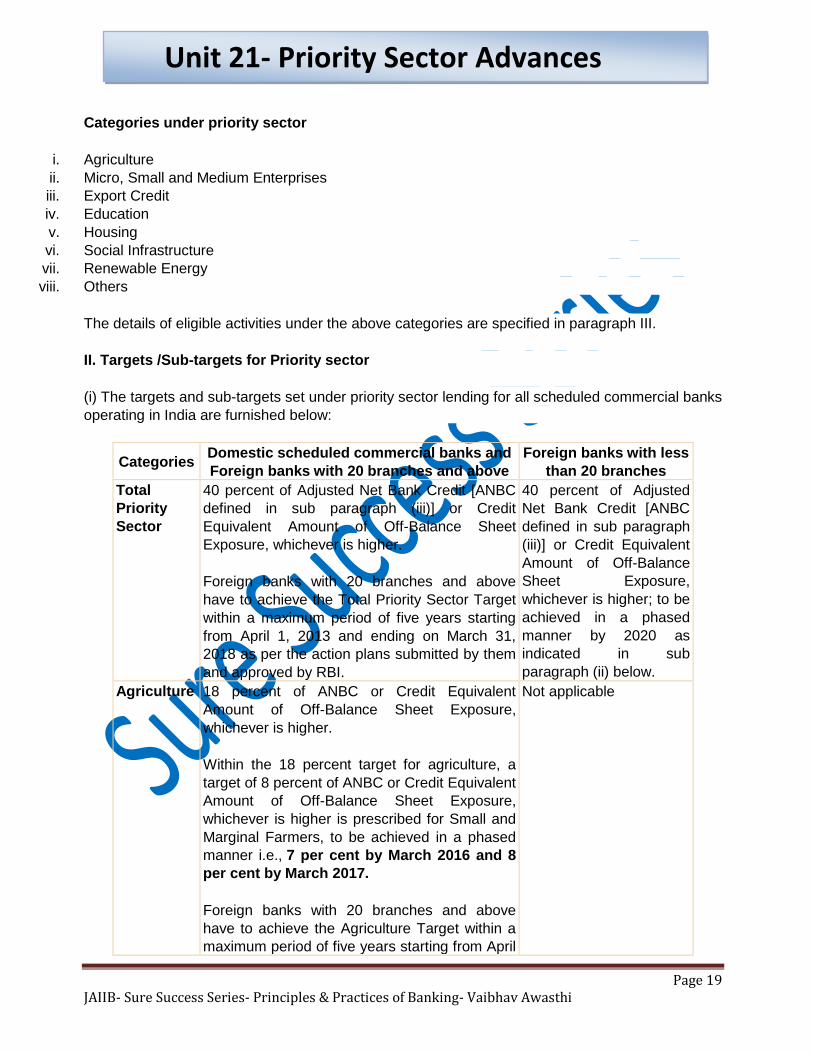

Categories under priority sector

i. Agriculture

ii. Micro, Small and Medium Enterprises

iii. Export Credit

iv. Education

v. Housing

vi. Social Infrastructure

vii. Renewable Energy

viii. Others

The details of eligible activities under the above categories are specified in paragraph III.

II. Targets /Sub-targets for Priority sector

(i) The targets and sub-targets set under priority sector lending for all scheduled commercial banks

operating in India are furnished below:

Categories Domestic scheduled commercial banks and

Foreign banks with 20 branches and above

Foreign banks with less

than 20 branches

Total

Priority

Sector

40 percent of Adjusted Net Bank Credit [ANBC

defined in sub paragraph (iii)] or Credit

Equivalent Amount of Off-Balance Sheet

Exposure, whichever is higher.

Foreign banks with 20 branches and above

have to achieve the Total Priority Sector Target

within a maximum period of five years starting

from April 1, 2013 and ending on March 31,

2018 as per the action plans submitted by them

and approved by RBI.

40 percent of Adjusted

Net Bank Credit [ANBC

defined in sub paragraph

(iii)] or Credit Equivalent

Amount of Off-Balance

Sheet Exposure,

whichever is higher; to be

achieved in a phased

manner by 2020 as

indicated in sub

paragraph (ii) below.

Agriculture 18 percent of ANBC or Credit Equivalent

Amount of Off-Balance Sheet Exposure,

whichever is higher.

Within the 18 percent target for agriculture, a

target of 8 percent of ANBC or Credit Equivalent

Amount of Off-Balance Sheet Exposure,

whichever is higher is prescribed for Small and

Marginal Farmers, to be achieved in a phased

manner i.e., 7 per cent by March 2016 and 8

per cent by March 2017.

Foreign banks with 20 branches and above

have to achieve the Agriculture Target within a

maximum period of five years starting from April

Not applicable

Unit 21- Priority Sector Advances

Page 20 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

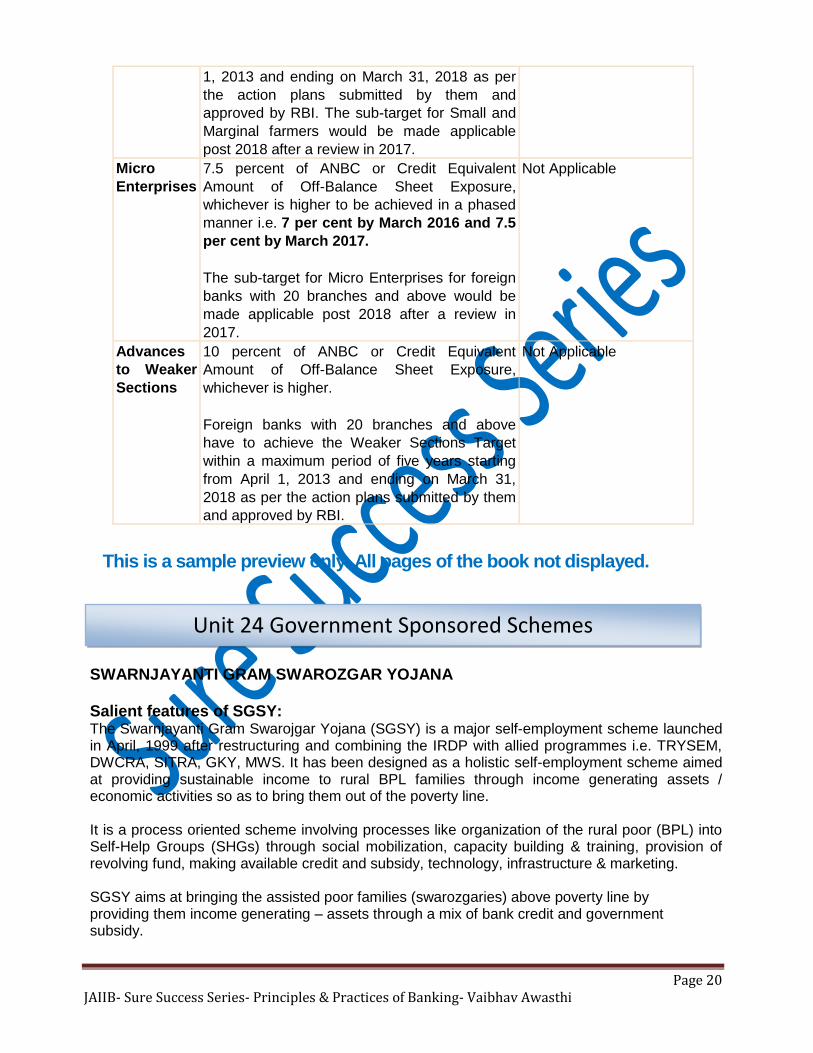

1, 2013 and ending on March 31, 2018 as per

the action plans submitted by them and

approved by RBI. The sub-target for Small and

Marginal farmers would be made applicable

post 2018 after a review in 2017.

Micro

Enterprises

7.5 percent of ANBC or Credit Equivalent

Amount of Off-Balance Sheet Exposure,

whichever is higher to be achieved in a phased

manner i.e. 7 per cent by March 2016 and 7.5

per cent by March 2017.

The sub-target for Micro Enterprises for foreign

banks with 20 branches and above would be

made applicable post 2018 after a review in

2017.

Not Applicable

Advances

to Weaker

Sections

10 percent of ANBC or Credit Equivalent

Amount of Off-Balance Sheet Exposure,

whichever is higher.

Foreign banks with 20 branches and above

have to achieve the Weaker Sections Target

within a maximum period of five years starting

from April 1, 2013 and ending on March 31,

2018 as per the action plans submitted by them

and approved by RBI.

Not Applicable

This is a sample preview only. All pages of the book not displayed.

SWARNJAYANTI GRAM SWAROZGAR YOJANA Salient features of SGSY: The Swarnjayanti Gram Swarojgar Yojana (SGSY) is a major self-employment scheme launched in April, 1999 after restructuring and combining the IRDP with allied programmes i.e. TRYSEM, DWCRA, SITRA, GKY, MWS. It has been designed as a holistic self-employment scheme aimed at providing sustainable income to rural BPL families through income generating assets / economic activities so as to bring them out of the poverty line. It is a process oriented scheme involving processes like organization of the rural poor (BPL) into Self-Help Groups (SHGs) through social mobilization, capacity building & training, provision of revolving fund, making available credit and subsidy, technology, infrastructure & marketing. SGSY aims at bringing the assisted poor families (swarozgaries) above poverty line by providing them income generating – assets through a mix of bank credit and government subsidy.

Unit 24 Government Sponsored Schemes

Page 21 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

The scheme is being implemented in the States through the District Rural Development Agencies (DRDAs) and funds are transferred by Ministry of Rural Development directly to the DRDAs with active involvement of Panchayati Raj Institutions(PRIs). Funds are allocated to the States on the basis of inter se poverty ratios fixed by the Planning Commission and further to the districts on the basis of their Below Poverty Line (BPL) population.

This is a sample preview only. All pages of the book not displayed.

Document means any matter expressed or described upon any substance by means of letters,

figures or by more than one of these means intended to be used or which may be used for the

purpose of recording that matter as per section 3 of Indian Evidence Act 1872.

Indian Stamp Act defines instrument as “ instrument includes every document by which any right

or liability is or purported to be created, transferred, limited, extended , extinguished or recorded (

Section 2(14) of Indian Stamp Act)

The purpose of taking documents are to fix the terms and conditions between the bankers and

the borrowers, to identify the borrowers, to identify the securities, to count the period of limitation,

to resort to legal remedies in case of need and so on. There are certain enactments such as

Indian Contract Act, Partnership Act, Companies Act, Indian Registration Act, Limitation Act,

Indian Stamps Act, etc., which affect directly the bankers' loan documentation.

DIFFERENT TYPES OF DOCUMENTS

(a) Personal security

(b) Primary security

(c) Collateral security

(d) tangible security

(a) Personal liability documents : Documents which make the executants personally liable

to the bank for any advance/loan . Examples are DP note, letter of guarantee, acknowledgment of

debt and security etc

(b) Charge creating documents : They are the documents which create some sort of charge on

executants property in favour of the bank. They are agreement of Hypothecation, Agreement of

pledge, Deed of mortgage, letter of lien and set off etc.

Documents obtained by the bank may be either be an agreement or a bond or a deed.

Agreement : Agreement attracts fixed stamp duty irrespective of the amount involved. This

document is not be attested or witnessed by a third party under any circumstances.

Unit 26 - Documentation

Page 22 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Bond: 5) As per Section 2 (5) of Indian Stamp act “bond” includes”

(a) any instrument whereby a person obliges himself to pay money to another, on condition that

the obligation shall be void if a specified act is performed, or is not performed, as the case many

be ;

(b) any instrument attested by a witness and not payable to order or bearer, whereby a person

obliges himself to pay money to another; and

The main test of the bond is attestation. It also attracts ad valorem stamp duty of the state

concerned

Deed: A deed is a signed and usually sealed instrument duly executed and delivered containing

some transfer, bargain or contract.

Demand Promissory Notes: Where no specification for a fixed period for the repayment of loan

is given, the bankers take the DPN. In DPN, the borrower makes a promise to the banker to

repay the loan amount on demand with agreed rate of interest. The form of DPN should be in

conformity with Section 4 of the Negotiable Instruments Act, 1881. The form of a DPN varies

normally to suit the situation such as fixed rate of interest, floating rate of interest, single

borrower, joint borrowers, joint and several borrowers, etc. DPN attracts a stamp duty as per

Indian Stamp Act. The rate of stamp duty on DPN is uniform through out India. As per Section 35

of the Indian Stamp Act, if a DPN is unstamped or under-stamped, the defect cannot be rectified

even by paying a penalty. Such a DPN cannot be admissible as evidence in a court of law. It

must be ensured that the DPN is duly filled in and stamped before the borrower signs it.

Agreements: The form of an agreement should be in conformity with the Indian Contract Act.

The terms and conditions are set out in the agreement. The amount of loan, rate of interest, rate

of penal interest, percentage of margin, period of repayment, rights of the bankers, in case of

default of loan, details of security/securities charged, are included in the agreement. The

agreements attract a stamp duty as per Indian Stamp Act. The rate of stamp duty on agreements

varies from State to State. The bankers use different forms of agreement such as pledge

agreement, hypothecation agreement, term Loan agreement, clean loan agreement, Inter- se

agreement, guarantee agreement, etc. The agreement duly filled in and stamped, is checked

before the party signs it.

Forms: Forms are not in the nature of promise or agreement. These are obtained to specify

clearly the intention of the borrower. For example, when a loan is granted against the security of a

fixed deposit standing in joint names, one of the depositors gives an authorisation to the other to

raise a loan on the deposit. Such an authorisation is taken in a form. Similarly, when a payment is

to be made out of loan proceeds to a supplier of goods, a letter from the borrower authorising the

bank to pay the proceeds by means of draft or bankers cheque, is taken by means of a form.

Such forms are used as part of documentation to prove the intention of the borrowers

This is a sample preview only. All pages of the book not displayed.

Page 23 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

(a) Assignment: It is transfer of a right, property or a debt. The transferor is called assignor and

the transferee assignee. Borrowers generally assign the actionable claims to the banker as

security for an advance. In terms of Section 130 of the Transfer of Property Act, the transfer of an

actionable claim can be effected only by the execution of an instrument in writing, signed by

transferor or by his duly authorised agent. Section 3 of the Transfer of Property Act defines an

actionable claim as a claim to any debt other than a debt secured by mortgage of immovable

property or by hypothecation or pledge of movable property or to any beneficial interest in

movable property, not in the possession of the claimant, which the Civil Courts recognise as

affording grounds of relief. All the rights and remedies of the transferor vest in the transferee. The

transferee of an actionable claim takes it, subject to all the liabilities and equities to which the

transferor was subject on the date of the transfer. In banking practice, a borrower may assign the

book debt, money due from Government department, and life insurance policies as security for an

advance. As regards the mode of assignment, no particular form or words is necessary for

effecting an assignment, if the intention is clear from the language used. An assignment can be

absolute or by way of security.

(c)Set-off Set-off means total or partial merging of a claim of one person against another in a

counter claim by the latter against the former. It is in effect, the combining of accounts of the

debtor and creditor, to arrive at the net balance payable to one or the other. The right of set-off is

a statutory right and can also arise out of an agreement between parties.

Salient Features of Set-off

(a)Both debts must be for certain sums. A debt-accruing due cannot be set-off against the debt

already due.

(b)The banker cannot set-off the credit balance in the account of guarantor till the liability of the

guarantor is determined.

(c)The credit balance in the current account cannot be set-off against a contingent liability of a bill

discounted but not yet due.

(d)A banker cannot set-off a debt due to him upon a loan account repayable on demand or at a

specified date against a credit balance in the current account until the demand is made or due

date arrives.

(e)The parties must be mutually indebted in the same right.

(f)The credit balance in the partner's account can be set-off against the debit balance of a

partnership account since the liability of the partners is joint and several.

(g) The credit balance in the personal account of a sole proprietor can be set-off against the debit

balance of the sole proprietary concern and vice versa,

(h) When the right set-off is available to the bank, lien right cannot apply. These two different

rights cannot be exercised simultaneously at the same time.

Unit 27 Different Modes of Charging Security

Page 24 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Financial literacy aims at imparting knowledge to enable financial planning, inculcate saving

habits and improve the understanding of financial products leading to effective use of financial

services by the common man. Financial literacy should help them plan ahead of time for their

life cycle needs and deal with unexpected emergencies without resorting to debt. They

should be able to proactively manage money and avoid debt traps. The banks as providers of

financial services, have an inherent gain in the spread of financial inclusion and financial literacy,

as it would help them capture the untapped business opportunities. Small customer is the key

and banks should harness the business opportunities available at the bottom of the pyramid.

Hence, banks must view the financial literacy efforts as their future investments. Banks must

provide a bouquet of banking services comprising of a small overdraft facility, variable recurring

deposit account, KCC, remittance facilities to the account holders in order to make the accounts

transactional. People should be encouraged to make transactions in these accounts so that the

cost of maintaining the accounts is recovered to make it a viable and profitable

business of the banks.

This is a sample preview only. All pages of the book not displayed.

Unit 31- Financial Literacy

Page 25 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Module – C

Banking Technology

Page 26 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Bank computerization began after first Rangrajan committee report on bank mechanization submitted in year 1984. Committee was head by then deputy governor of RBI C Rangrajan. Computer is needed for (i) customer service (ii) housekeeping (iii) decision-making (iv) productivity and profitability. Stand alone computer system is the initial stage of computerisation of bank where a single computer is used by one user. They are used by executives for decision making. Its major advantage is it had low cost. Multi user system involves a computer system with several computers. Mini computers, mainframe computers, super computers fall under this. Multi user computer networking: they are based on centralised processing concept. System like unix are used as operating system. Most of banking system are developed using centralised computing concept. Most of Relational Data base management systems (RDBMS) and Data base management systems (DBMS) use unix platform. Advantages of a centralised data processing system are (i) availability of all information at one place (ii) overall cost of acquiring hardware software reduces as bulk purchases can be made(iii) due to high level of data processing, computing resources are fully utilized (iv) technical power also better utilized. Computerization in Banking is done at branch level for customer transactions, at RO/ZO level for for credit monitoring, personnel data management and inter branch reconciliation. Computerisation at HO level is done for operations (ii) planning (iii) personnel management(iv) branch profiles(v) credit monitoring etc LAN: a computer network is an interconnected system of autonomous computers, each system being capable of independent operations as well as being able to communicate with other systems. In LANs, each independent system is known as a node and when such nodes are interconnected, it is known as a LAN. Usually, there will be one central node (Server).Sharing common cabling and pooling resources within a work group are the key elements of LAN operation

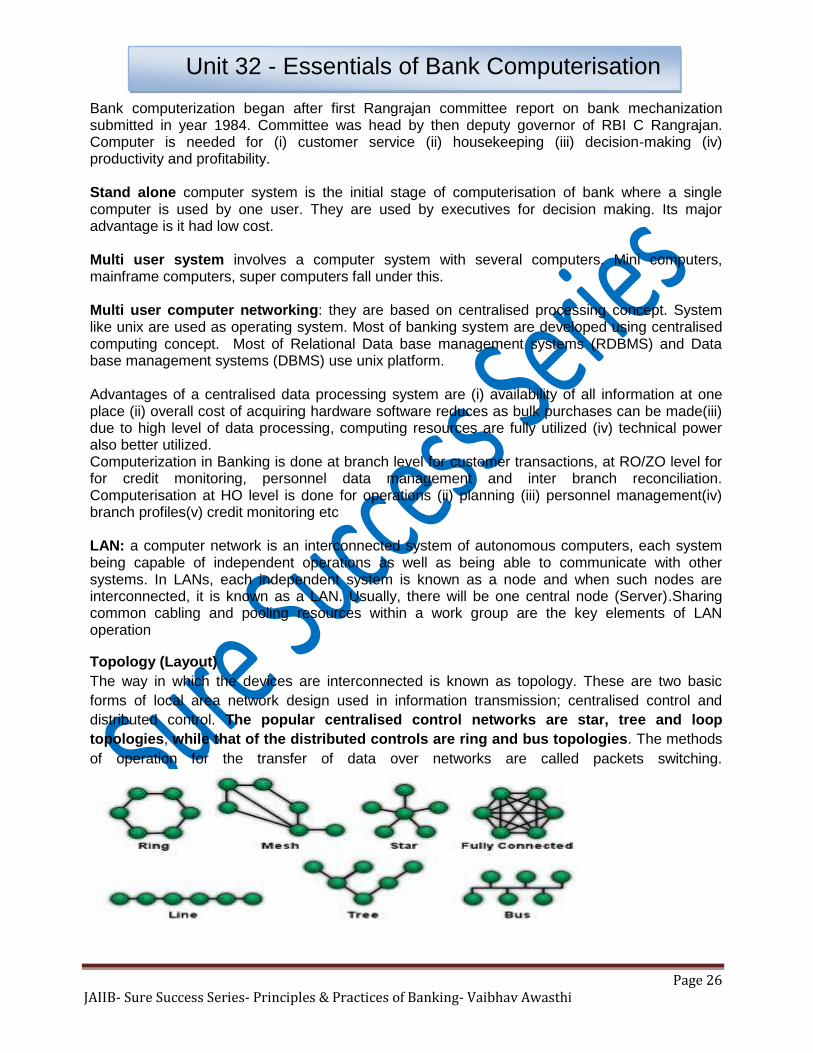

Topology (Layout)

The way in which the devices are interconnected is known as topology. These are two basic

forms of local area network design used in information transmission; centralised control and

distributed control. The popular centralised control networks are star, tree and loop

topologies, while that of the distributed controls are ring and bus topologies. The methods

of operation for the transfer of data over networks are called packets switching.

Unit 32 - Essentials of Bank Computerisation

Page 27 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Automated Teller Machines (ATMs): The committee headed by Dr. C. Rangarajan recommended

the setting up of ATMs in India.

ATM Models in India

Online: When the ATM is connected to the bank's database and provides online real time access

to the customers’ accounts, it is said to be 'online.

Offline: When an ATM is not connected to bank's database, it is stated to be 'offline.' In this

mode, withdrawals are permitted up to a pre-fixed limit only, irrespective of the balance available

in customers' accounts.

Stand-alone: When an ATM is not connected to any ATM network, it is said to be 'stand-alone'.

In this case, transactions at an ATM are restricted to customers of the ATM branch and its link

branches.

Networked: When ATMs are connected to an ATM network, they are said to be 'networked'. The

advantage of networked ATMs is that cardholders can use their ATM cards at any of the

networked-ATMs.

Cash Dispenser (CD)

Cash dispenser is a pruned down version of the ATM. CD is an ATM without a depository and is

intended to serve the customers for making cash withdrawals only.

Networking of ATMs :To optimise the cost on investments in ATMs, Banks join together as

clusters at the national level, the IDRBT initiated the process of setting up a 'National Financial

Switch' to facilitate apex level connectivity of other switches established by banks.

Indian Banks' Association (IBA) was the first to set up a shared payment network system (SPNS)

or SWADHAN network of ATMs of its member banks in Mumbai.

HWAK (The Intelligent Auto-teller and Netware Management System)Intelligent auto-teller

systems are a special breed of auto-teller machines capable of thinking for themselves.

CHEQUE TRUNCATION: Originally, Section 6 of the Negotiable Instruments Act, defined cheque as 'a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand'. This section has been amended in September 2002 to include cheque truncations and electronic cheques within the definition of cheque. The amended Section 6 reads as under:'A cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand and it includes the electronic image of a cheque truncation and a cheque in the electronic form.' Cheque truncation - Definition A cheque truncation is defined by the new Section 6(b) of Negotiable Instruments Act as 'a cheque which is truncated during the course of a clearing cycle, either by the Clearing House or by the bank, whether paying or receiving payment, immediately on generation of an electronic image for transmission, substituting the further physical movement of the cheque in writing.' Characteristics of a Cheque Truncation (a)It is an electronic image of a paper cheque.

Unit 33- Payment System and Electronic Banking

Page 28 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

(b)Only the banks involved and the Clearing House can truncate a cheque. The drawer/holder of a cheque cannot truncate a cheque. (c)The electronic image of the 'cheque truncation' will substitute the physical cheque from the point and time of truncation onwards. (d)Truncation is to be done only during the course of a clearing cycle to reduce the time taken for realisation. (e)The paper cheque, after truncation, is to be kept in the custody of the bank/clearing house that truncated the cheque. (f)Addition of digital signature of the truncating Bank/Clearing House to the electronic image of the cheque truncation is optional. Ways in which truncation can be done 1. Using MICR data: MICR cheques have the cheque number, city, bank and branch numbers, and transaction code pre-coded. Abroad, even the account number of the customer is precoded. During encoding at the collecting bank, the amount, as well as the payee's name, is inserted in the MICR line. The entire MICR line is then captured electronically. The electronic information is then exchanged with other for clearing (Inter Bank Data Exchange or IBDE). The cheques do not move any further. 2. Using image processing: Image processing, as we have seen earlier, is the latest document handling system. Cheque image processing involves scanning of both sides of the cheque and storing the image in digital form. The cheque itself is moved to some offsite storage and the image is used for further processing.

MICROFICHE

For storage and backup of huge data microfilm or microfiche are uses as they can retain

voluminous information and the relative inability to readily ascertain their contents. The following

controls should be put in place for the protection of this media. Efforts must be made to protect

the security of this data against any damages or unauthorized access.

National Payments Corporation of India: Reserve Bank of India, after setting up of the Board for Payment and Settlement Systems in 2005, released a vision document incorporating a proposal to set up an umbrella institution for all the RETAIL PAYMENT SYSTEMS in the country. National Payments Corporation of India (NPCI) was incorporated in December 2008 and the Certificate of Commencement of Business was issued in April 2009. It has been incorporated as a Section 25 company under Companies Act and is aimed to operate for the benefit of all the member banks and their customers. The authorized capital has been pegged at Rs 300 crore and paid up capital is Rs 100 crore so that the company can create infrastructure of large dimension and operate on high volume resulting payment services at fraction of the present cost structure.

RUPAY RuPay is an Indian domestic card scheme conceived and launched by the National Payments Corporation of India (NPCI).. RuPay facilitates electronic payment at all Indian banks and financial institutions, and competes with MasterCard and Visa in India.RuPay card was launched on 26 March 2012. NPCI entered into a strategic partnership with Discover Financial Services (DFS) for RuPay Card, enabling the acceptance of RuPay Global Cards on Discover’s global payment network outside of India.

This is a sample preview only. All pages of the book not displayed.

Page 29 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Keeping in view the changing threat milieu and the latest international standards, it was felt that

there was a need to enhance RBI guidelines relating to the governance of IT, information security

measures to tackle cyber fraud apart from enhancing independent assurance about the

effectiveness of IT controls. To consider these and related issues, RBI announced the creation of

a Working Group on Information Security, Electronic Banking, Technology Risk Management and

Tackling Cyber Fraud in April, 2010. The Group was set up under the Chairmanship of the

Executive Director Shri.G.Gopalakrishna.

Major Recommendations of the working group are as under:

On IT Governance:

Banks need to formulate a Board approved IT strategy/plan document. An IT policy needs to be framed for regular management of IT functions and ensure that detailed documentation in terms of procedures and guidelines exists and are implemented. The strategic plan and policy need to be reviewed annually.

A need was felt for the position of CIO in banks, to be the key business player and play a part in the executive decision-making function.

IT Steering Committee needs to be created with representations from various IT functions, HR, Legal and business functions as appropriate. The role of the IT Steering Committee would be to assist the Executive Management in the implementation of the IT strategy approved by the Board.

Key focus areas of IT Governance that need to be considered include strategic alignment, value delivery, risk management, resource management and performance management.

There is also a need to maintain an “enterprise data dictionary” that incorporates the organization’s data syntax rules.

An IT balanced scorecard may be considered for implementation, with approval from key stakeholders, to measure IT performance along different dimensions such as financial aspects, customer satisfaction, process effectiveness, future capability, and for assessing IT management performance.

This is a sample preview. To purchase the complete Sure Success Series log on to our website www.jaiibcaiib.co.in. You can also call us on 07600273309 for any assistance.

Unit 37 Overview of IT Act

Page 30 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Module D

Support Services- Marketing of

Banking Services/ Products

Page 31 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

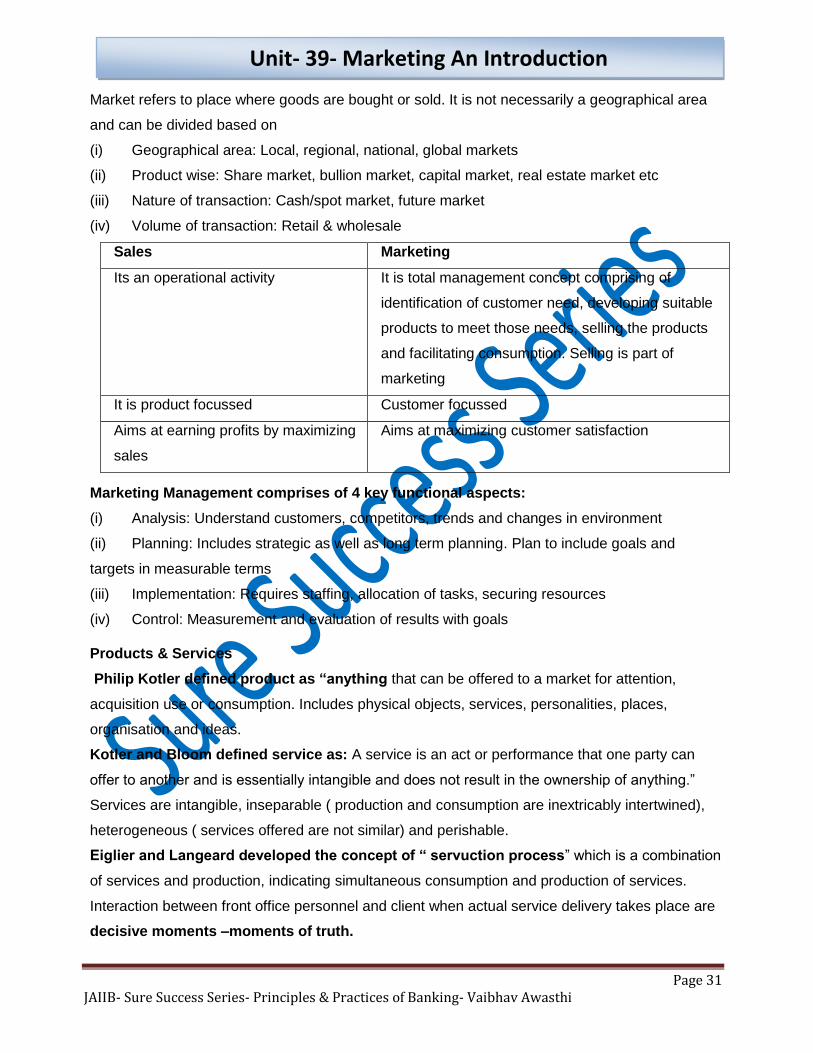

Market refers to place where goods are bought or sold. It is not necessarily a geographical area

and can be divided based on

(i) Geographical area: Local, regional, national, global markets

(ii) Product wise: Share market, bullion market, capital market, real estate market etc

(iii) Nature of transaction: Cash/spot market, future market

(iv) Volume of transaction: Retail & wholesale

Sales Marketing

Its an operational activity It is total management concept comprising of

identification of customer need, developing suitable

products to meet those needs, selling the products

and facilitating consumption. Selling is part of

marketing

It is product focussed Customer focussed

Aims at earning profits by maximizing

sales

Aims at maximizing customer satisfaction

Marketing Management comprises of 4 key functional aspects:

(i) Analysis: Understand customers, competitors, trends and changes in environment

(ii) Planning: Includes strategic as well as long term planning. Plan to include goals and

targets in measurable terms

(iii) Implementation: Requires staffing, allocation of tasks, securing resources

(iv) Control: Measurement and evaluation of results with goals

Products & Services

Philip Kotler defined product as “anything that can be offered to a market for attention,

acquisition use or consumption. Includes physical objects, services, personalities, places,

organisation and ideas.

Kotler and Bloom defined service as: A service is an act or performance that one party can

offer to another and is essentially intangible and does not result in the ownership of anything.”

Services are intangible, inseparable ( production and consumption are inextricably intertwined),

heterogeneous ( services offered are not similar) and perishable.

Eiglier and Langeard developed the concept of “ servuction process” which is a combination

of services and production, indicating simultaneous consumption and production of services.

Interaction between front office personnel and client when actual service delivery takes place are

decisive moments –moments of truth.

Unit- 39- Marketing An Introduction

Page 32 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

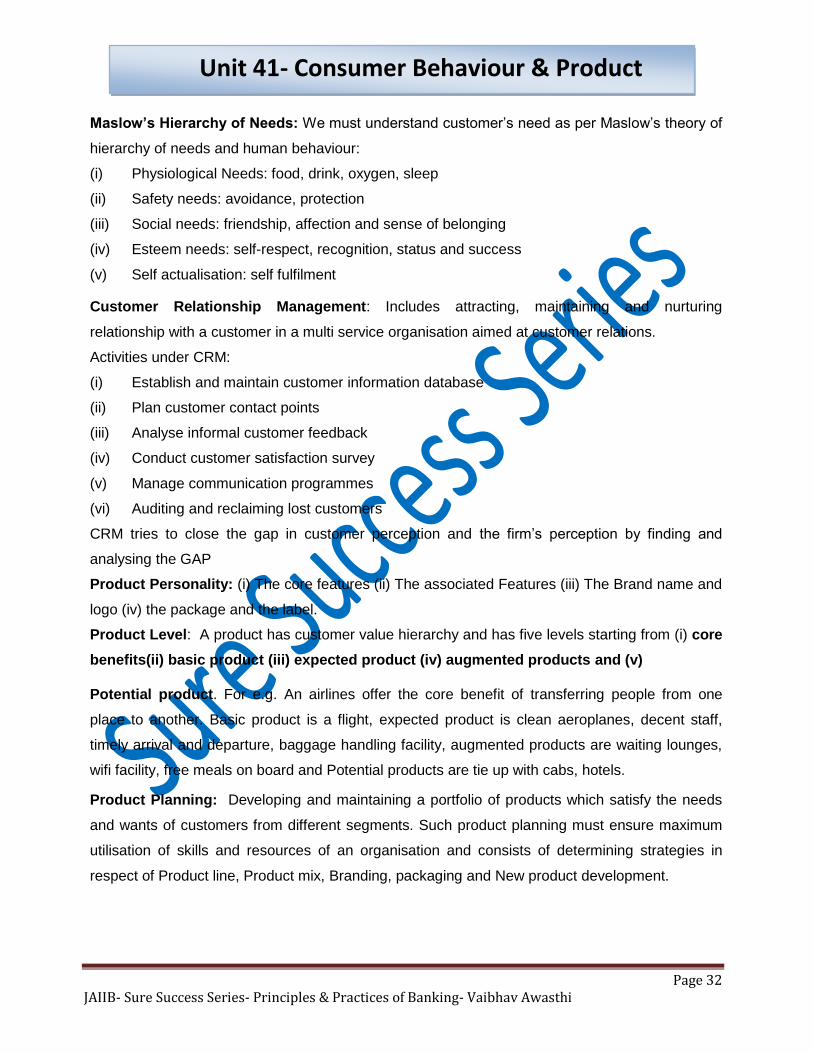

Maslow’s Hierarchy of Needs: We must understand customer’s need as per Maslow’s theory of

hierarchy of needs and human behaviour:

(i) Physiological Needs: food, drink, oxygen, sleep

(ii) Safety needs: avoidance, protection

(iii) Social needs: friendship, affection and sense of belonging

(iv) Esteem needs: self-respect, recognition, status and success

(v) Self actualisation: self fulfilment

Customer Relationship Management: Includes attracting, maintaining and nurturing

relationship with a customer in a multi service organisation aimed at customer relations.

Activities under CRM:

(i) Establish and maintain customer information database

(ii) Plan customer contact points

(iii) Analyse informal customer feedback

(iv) Conduct customer satisfaction survey

(v) Manage communication programmes

(vi) Auditing and reclaiming lost customers

CRM tries to close the gap in customer perception and the firm’s perception by finding and

analysing the GAP

Product Personality: (i) The core features (ii) The associated Features (iii) The Brand name and

logo (iv) the package and the label.

Product Level: A product has customer value hierarchy and has five levels starting from (i) core

benefits(ii) basic product (iii) expected product (iv) augmented products and (v)

Potential product. For e.g. An airlines offer the core benefit of transferring people from one

place to another. Basic product is a flight, expected product is clean aeroplanes, decent staff,

timely arrival and departure, baggage handling facility, augmented products are waiting lounges,

wifi facility, free meals on board and Potential products are tie up with cabs, hotels.

Product Planning: Developing and maintaining a portfolio of products which satisfy the needs

and wants of customers from different segments. Such product planning must ensure maximum

utilisation of skills and resources of an organisation and consists of determining strategies in

respect of Product line, Product mix, Branding, packaging and New product development.

Unit 41- Consumer Behaviour & Product

Page 33 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

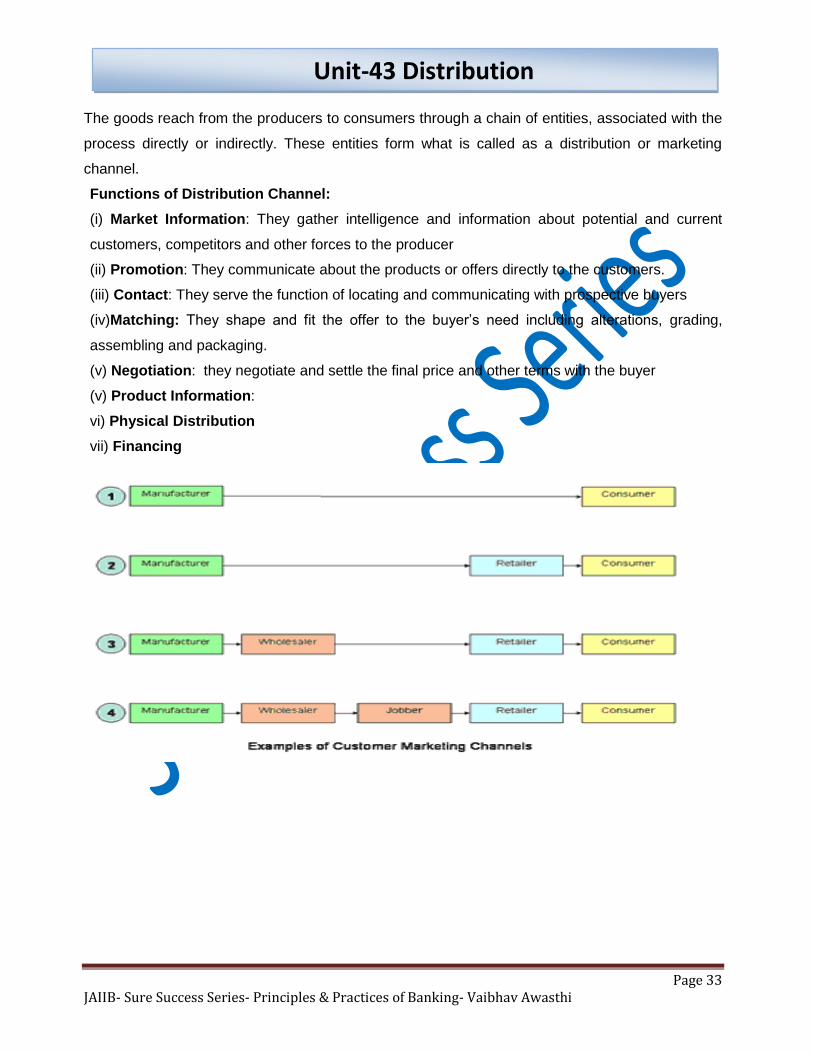

The goods reach from the producers to consumers through a chain of entities, associated with the

process directly or indirectly. These entities form what is called as a distribution or marketing

channel.

Functions of Distribution Channel:

(i) Market Information: They gather intelligence and information about potential and current

customers, competitors and other forces to the producer

(ii) Promotion: They communicate about the products or offers directly to the customers.

(iii) Contact: They serve the function of locating and communicating with prospective buyers

(iv)Matching: They shape and fit the offer to the buyer’s need including alterations, grading,

assembling and packaging.

(v) Negotiation: they negotiate and settle the final price and other terms with the buyer

(v) Product Information:

vi) Physical Distribution

vii) Financing

Unit-43 Distribution

Page 34 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Q1. Global Bank is having a current account of M/s Ruchi Enterprises and a cheque of Rs.13500 is presented through clearing, drawn in favour of Mr. Ramesh. Through an oversight the cheque is dishonoured wrongfully. When information about this dishonour is received by Mr. Ramesh, he sends a notice to the Global Bank for wrongful dishonour and claims damages. What would you do with this notice? a. Bank should contact Mr. Ramesh for withdrawls of the notice for damages. b. Banks should contact the drawer and ask them to prevail upon the payee for withdrawal of the notice. c. Bank can ignore this notice as the bank is not liable for such damages to the payee. d. Bank is liable to the drawer of the cheque and no one else. e. c and d above Q2. Corporate Bank had opened a saving bank account in the name of Mr. Subramanian and Murlidhar operated as `former or survivor’. The wife of Mr. Subramanian, who is nominee in the account comes to your branch and informs you that Mr. Subramanian has expired a month back. She also hands over the death certificate and requests for payment of the balance. a. the payment to the nominee will be made on proper identification as she is also having the death certificate. b. the payment will be made to the wife of deceased being legal heir of the former. c. the payment will not be made as with the death of the former, nomination has been cancelled. d. the payment will not be made as with the death of the former, survivor gets the authority to operate the account and nominee comes in to picture only when none of the account holders is available e. any of the above Q3 Bank Universal Limited receives a letter of credit of $ 20000 in favour of M/s Diamond Exports Pvt Ltd for exports to Germany. After verification of the genuineness of the credit, it is forwarded to the beneficiary through registered letter. Unfortunately, due to postal strike, by the time the letter of credit is delivered, its validity period expires. The exporter threatens legal action against the bank: a. bank is liable as bank has not handed over the credit in time to the beneficiary b. postal department is liable for the loss and exporter has to take up the matter with the postal department c. bank is not liable as it does not assume any liability for the consequences arising out of delay in transit due to actions beyond its control d. bank could persuade the opening bank to extend the validity date so that it is not put to loss any of the above Q4 Your branch has received a garnishee order in the name of your customer having saving bank account, with following transactions. Which among these is not subject matter of the garnishee order: a. an advice ready for despatch to another branch after debit to the account in payment of cheque b. an advice received for a cheque which was sent in collection, from another branch but not credited to the account so far c. a cheque sent in clearing, the amount of which has been credited to the account d. an amount of Rs.4000 relating to his wife’s account credited by mistake to the account of the customer e. all the above

Mock test 1

Page 35 JAIIB- Sure Success Series- Principles & Practices of Banking- Vaibhav Awasthi

Q5 Your branch opens a fixed deposit of Rs.50000 in the joint name of Mr. Anil Kumar and Mr. Suhail Kumar payable to either or survivor. They also nominate Miss Konica a minor daughter of Mr. Suhail Kumar with the provision that the payment can be claimed by Mrs. Suhail Kumar on behalf of the minor. Unfortunately, Mr. Suhail Kumar expired and subsequently Mr. Anil Kumar decides to change the nomination from Miss Konica to his own son. To this, Mrs. Suhail Kumar objects and asks your branch not to accept the instruction of Mr. Anil Kumar: a. bank has no option to ignore the request from Mr. Anil Kumar as, being survivor all rights relating to deposit are vested with him. b. bank can request Mr. Anil Kumar to decide the case in consultation with the existing nominee c. bank has to accept the request from Mrs. Suhail Kumar, as she was the nominee coupled with interest d. bank will ask them to go to a court of law for decision and would implement the decision of the court e. b and c above Q6 Sh. Amrit Lal opens a term deposit account with Bank of Bengal and nominates his niece Ms Aruna Pande. Unfortunately, he expires in an accident but Ms Aruna Pande does not turn up despite a notice from the bank. Meantime, the legal heirs of Mr. Amrit Lal i.e. his two sons, visit the bank and request for making payment of the deposit. They also present a probate from court of law in which they are executors of the will of the deceased: a. the payment of the balance in the account will be made by the bank to Ms Aruna Pande only b. the payment of the balance would be made to the legal heirs in terms of probate c. the payment will be made in equal proportion to the legal heirs and the nominee d. the bank will advise the legal heirs to bring specific order from the court in the light of nomination e. none of the above

Q7 The liability of a minor co‑parcener in an HUF, for the acts of a Karta is:

a. unlimited b. nil c. to the extent of his share in the family property d. 50% of the loss as per his share e. none of the above

*******************************END OF FREE PREVIEW**************************

To purchase the complete Sure Success Series log on to our website

www.jaiibcaiib.co.in You can also call us on 07600273309 for any assistance