Embed Size (px)

Citation preview

Principles of Economics

Class 1Introduction to Economics

State and MarketSupply and Demand

PRINCIPLES OF ECONOMICS

• ECONOMICS is a science which investigates how societies use scarce resources in order to produce useful goods and how they are distributed among them.

• ECONOMY is the overall economic activity in a country (region)

• If resources were not scarce, there would have been no economics -> scarcity is the main trait of ECONOMIC GOODS.

• Resources are used efficiently if no additional unit of any good can be produced without reducing production of the other good.

MICROECONOMICS AND MACROECONOMICS

• MICROECONIMICS is a branch of economics which analyses the behaviour of individual entities (companies, consumers) and their intercation on the market.

• Found in 1776 (Adam Smith – Wealth of the Nations)• MACROECONOMICS is a branch of economics which

analyses the sum of economic activity.• Found in 1936 (John Maynard Keynes – General Theory

of Employment, Interest Rate and Employment).

ECONOMY TYPES

• MARKET ECONOMY is an economy where conumers and producers freely set prices and quantities. It boosts efficiency, but fails to solve situations like monopoly and lacks justice.

• PLANNED ECONOMY is an economy where consumption and production is commanded by the state (e.g. communistic economies)

• MIXED ECONOMY is the most common type where majority of the market is self-regulated, but state interferres when it is needed to provide justice.

Positive vs. Normative economy

POSITIVE ECONOMY – description of economic phenomena – the answer provided by economic analysis

Example: Why housekeepers earn less than doctors?NORMATIVE ECONOMY –value or normative

judgments about economic fairness or what the outcome of the economy or goals of public policy ought to be – the answer provided by political discussion and political decisions.

Example: Should production of some arms and drugs be made illegal?

INPUTS AND PRODUCTS

INPUTS are the goods used in production of the other goods and services. Basic inputs are labour, capital, land.

PRODUCTS are useful goods and services that are either consumed or used for production of other goods.

The three basic economic questions

1. What goods and services should be produced? Those that bring producers the most profit.

2. How should the goods and services be produced? To stay competitive, one has to minimize costs and produce efficiently.

3. For whom should the goods and services be produced? It depends on the input market – the product of all factors and its prices define the income of consumers,

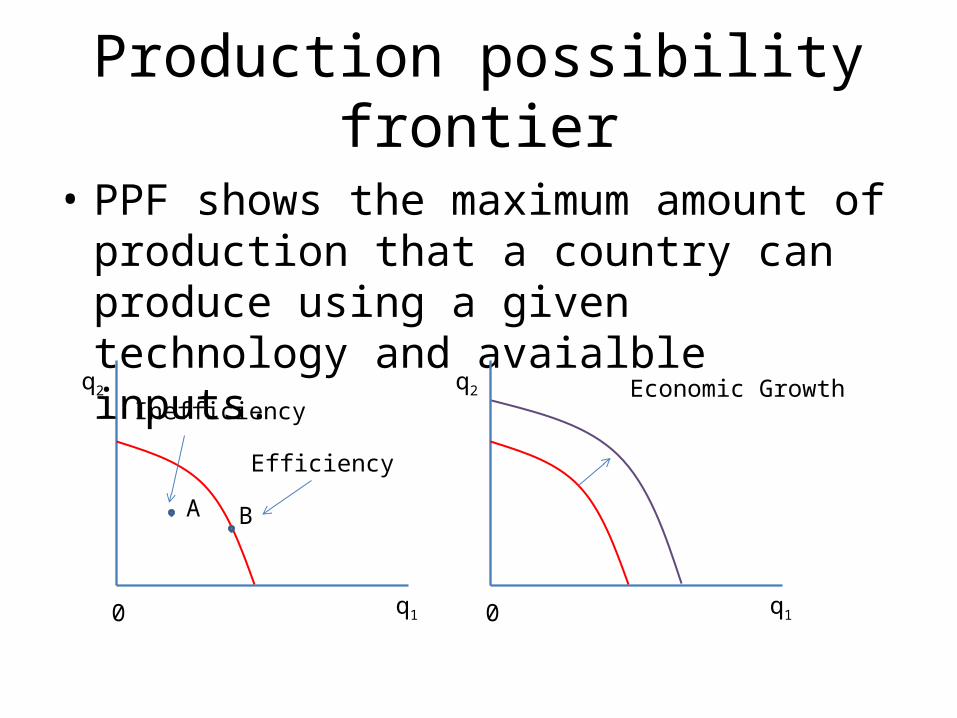

Production possibility frontier

• PPF shows the maximum amount of production that a country can produce using a given technology and avaialble inputs.

0 q1

q2

0 q1

q2

A

InefficiencyEconomic Growth

B

Efficiency

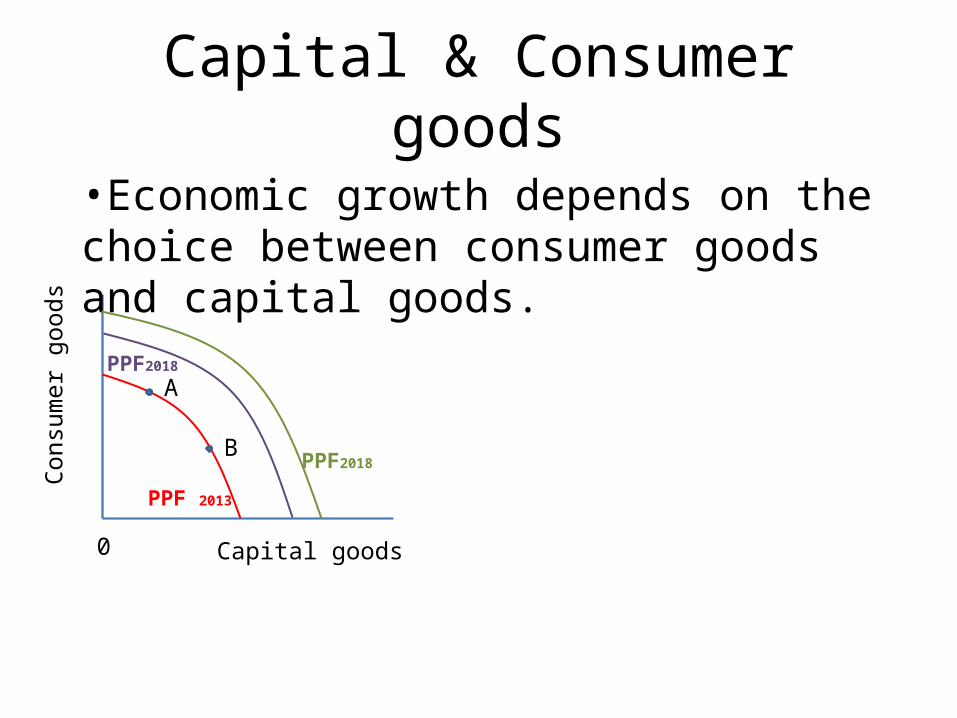

Capital & Consumer goods

0 Capital goods

•Economic growth depends on the choice between consumer goods and capital goods.

A

B

Cons

umer

goo

ds

PPF 2013

PPF2018

PPF2018

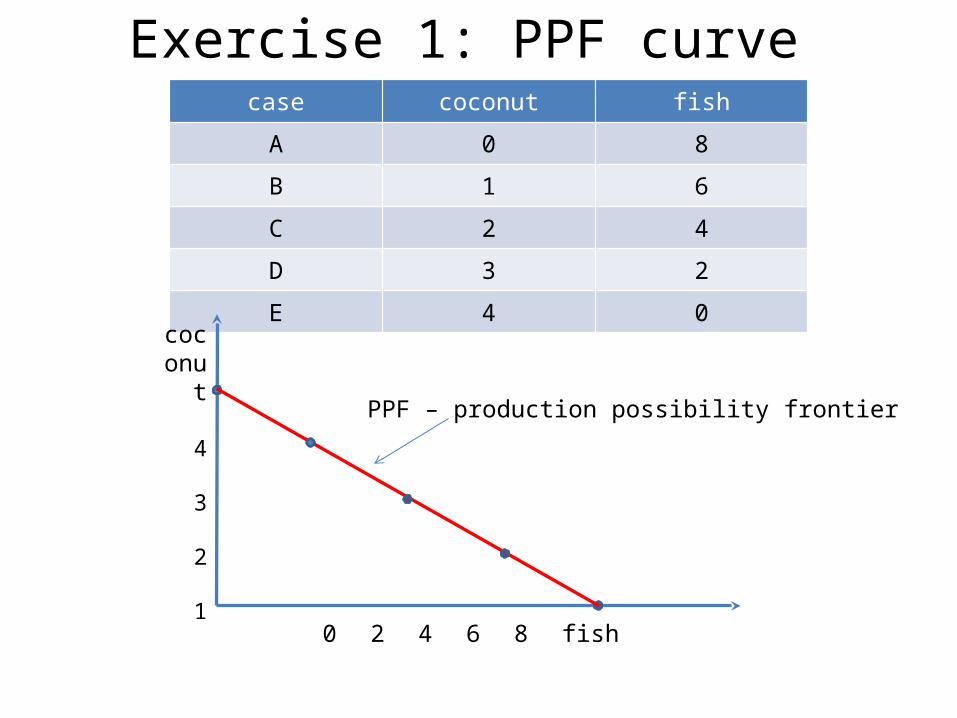

case coconut fish

A 0 8

B 1 6

C 2 4

D 3 2

E 4 0

0 2 4 6 8 fish

coconut

4

3

2

1

PPF – production possibility frontier

Exercise 1: PPF curve

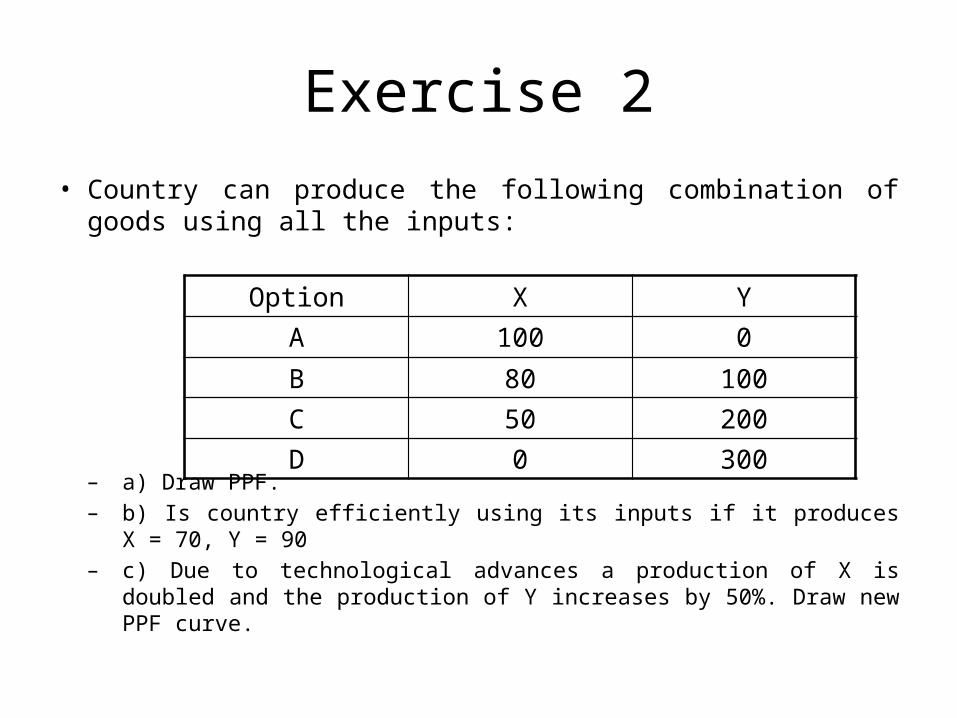

Exercise 2

• Country can produce the following combination of goods using all the inputs:

– a) Draw PPF.– b) Is country efficiently using its inputs if it produces X = 70, Y = 90– c) Due to technological advances a production of X is doubled and the

production of Y increases by 50%. Draw new PPF curve.

Option X Y

A 100 0

B 80 100C 50 200D 0 300

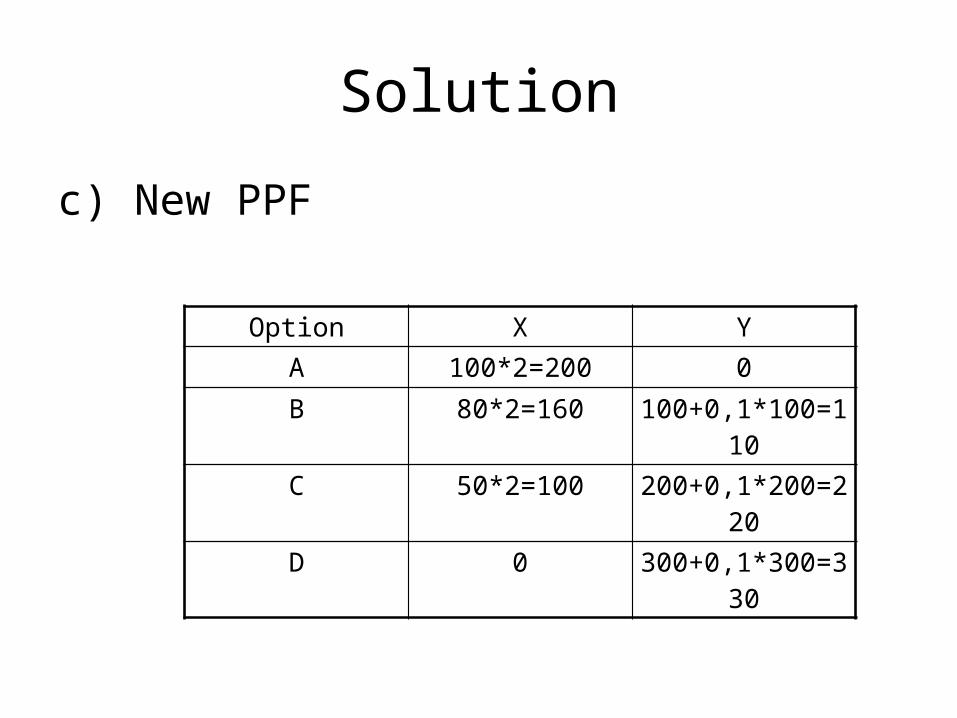

Solution

c) New PPF

Option X Y

A 100*2=200 0

B 80*2=160 100+0,1*100=110C 50*2=100 200+0,1*200=220D 0 300+0,1*300=330

Appendix 1 - Graphs

• A Graph is a picture that shows a relationship between 2 or more variables.

• 2D graphs – linear or nonlinear.• The slope of the curve shows by how much y

changes if x changes by 1 small unit. The sign of the slope tells whether an increase in x causes an increase in y (+), or a decrease (-).

x

y

z

1

0

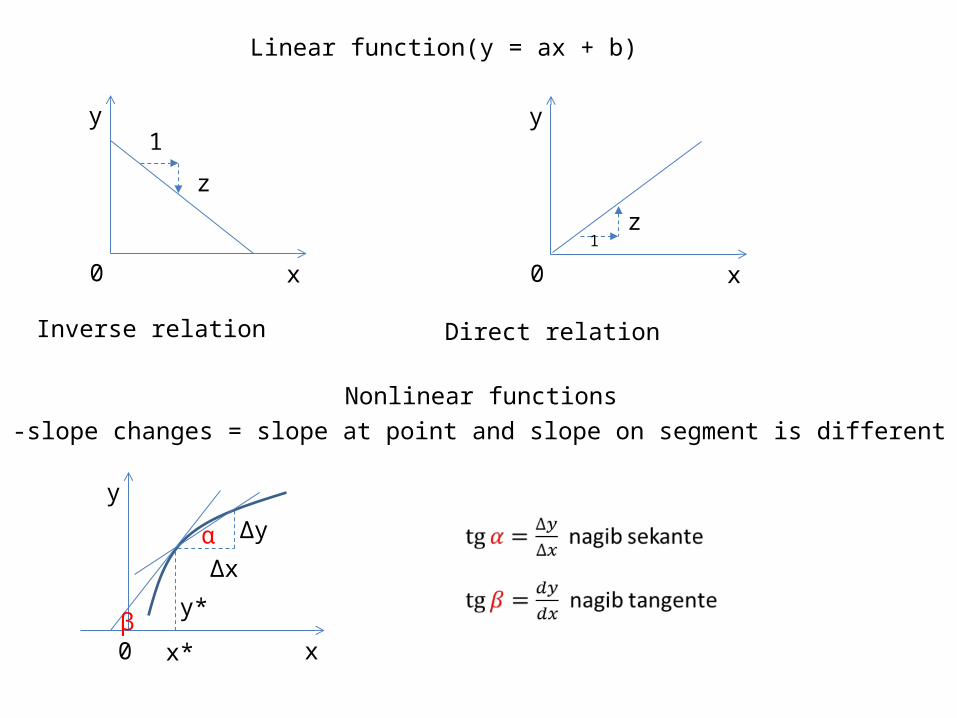

Inverse relation

x

y

z1

0

Direct relation

Linear function(y = ax + b)

Nonlinear functions-slope changes = slope at point and slope on segment is different

x

y

y*

Δx

0

Δy

x*

α

β

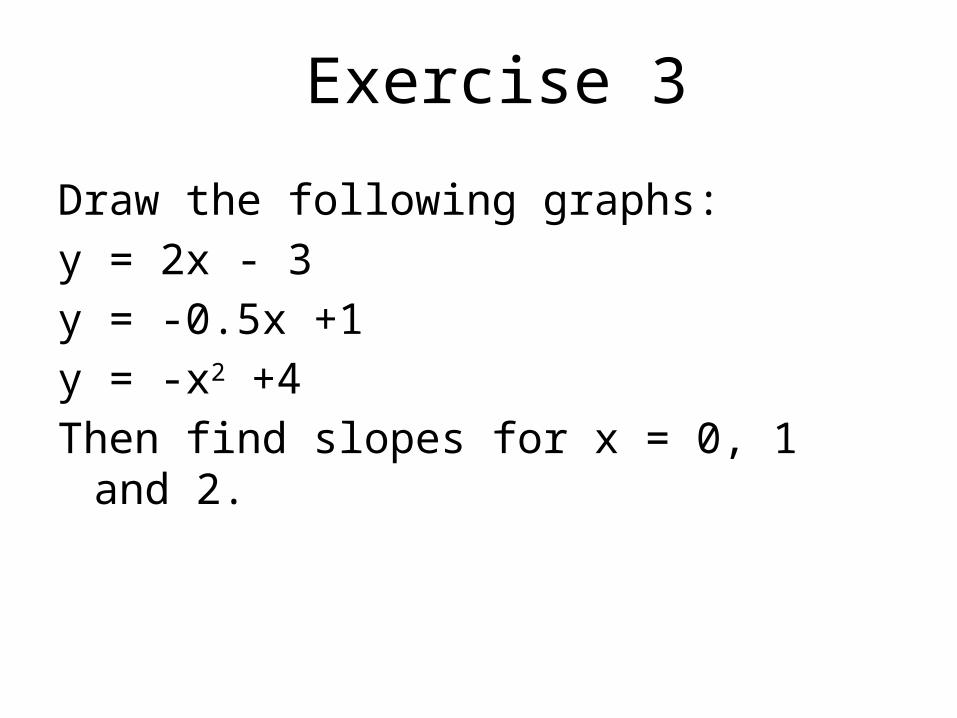

Draw the following graphs:y = 2x - 3y = -0.5x +1y = -x2 +4Then find slopes for x = 0, 1 and 2.

Exercise 3

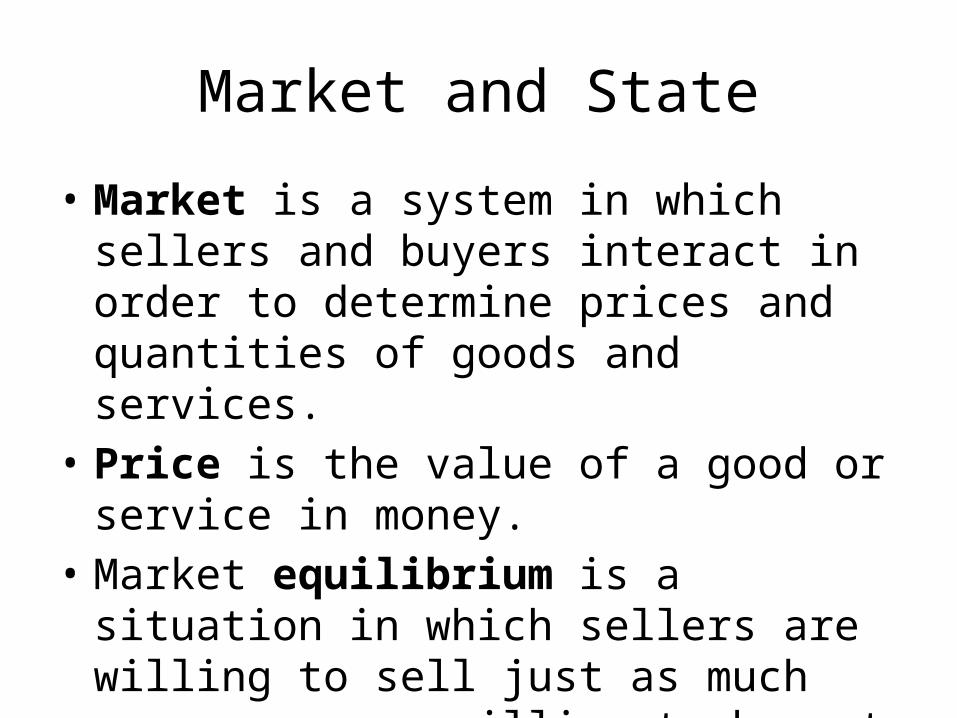

Market and State

• Market is a system in which sellers and buyers interact in order to determine prices and quantities of goods and services.

• Price is the value of a good or service in money.

• Market equilibrium is a situation in which sellers are willing to sell just as much consumers are willing to buy at certain price.

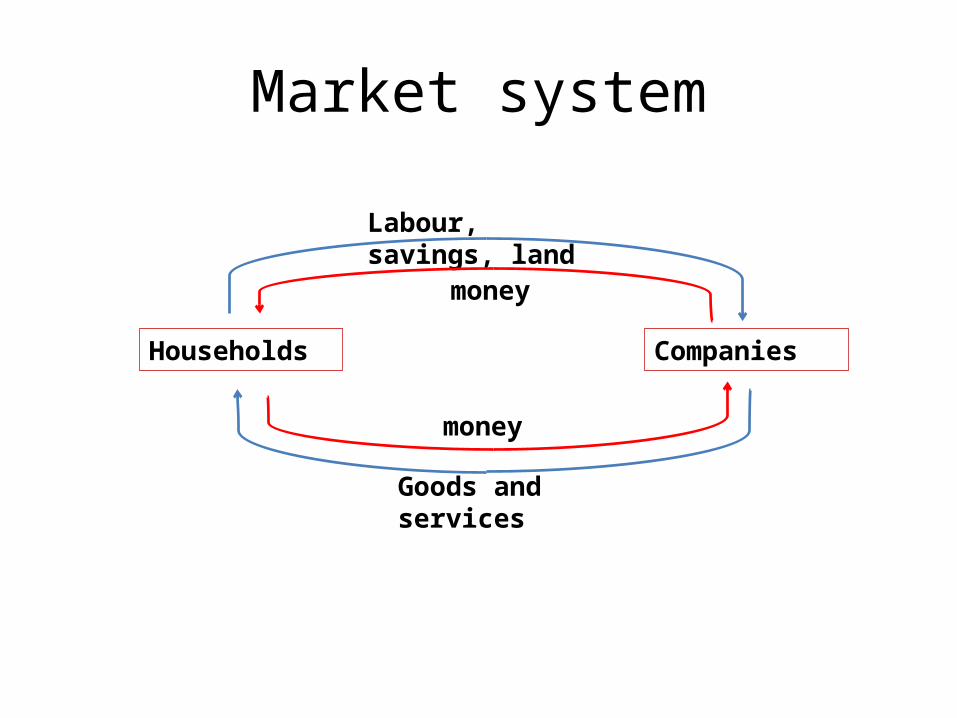

Market system

Labour, savings, land

Goods and services

Households Companies

money

money

Exchange, money and capital

• Exchange of goods is based on the specialisation and money is the mean for exchange.

• Specialization and division of labour increases productivity of labour which increases the amount of goods and thus the welfare of consumers.

• Capital is an input which is an accumulation of labour but more productive. Capital is made by sacrificing current consumption.

• Ownership of capital is protected – it is the foundation of capitalism.

Economic role of the state

• Laissez-faire (Fr.) – “let it be” – classical economics, today revised.

1. EFFICIENCY – best in perfect competition (invisible hand) but sometimes regulation of market competition needed:

• Imperfect competition appear – antitrust laws• Externalities - levying costs or benefits to others.• Public goods – financed by the state.• Taxes – price of the public goods.

2. JUSTICE• Unregulated markets can lead to the unjust

differencies bewteen the incomes.3. MACROECONOMIC GROWTH AND STABILITY• Fiscal policy (public spending, taxes) and

monetary policy (supply of money) affect the employment, GDP growth rate, inflation, etc.

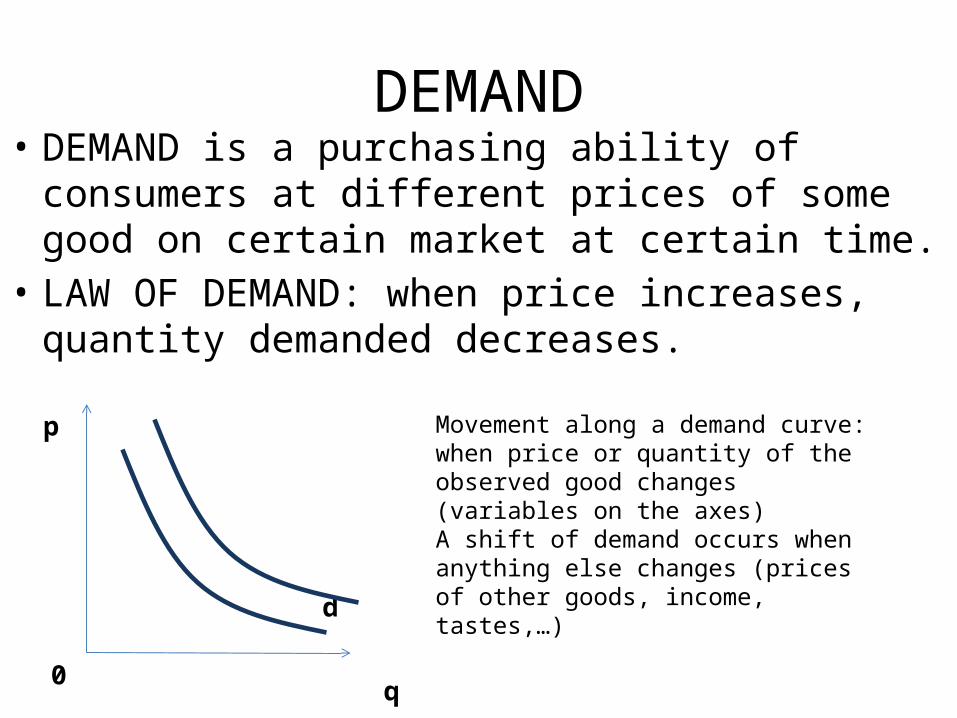

DEMAND• DEMAND is a purchasing ability of consumers at

different prices of some good on certain market at certain time.

• LAW OF DEMAND: when price increases, quantity demanded decreases.

d

p

0 q

Movement along a demand curve: when price or quantity of the observed good changes (variables on the axes)A shift of demand occurs when anything else changes (prices of other goods, income, tastes,…)

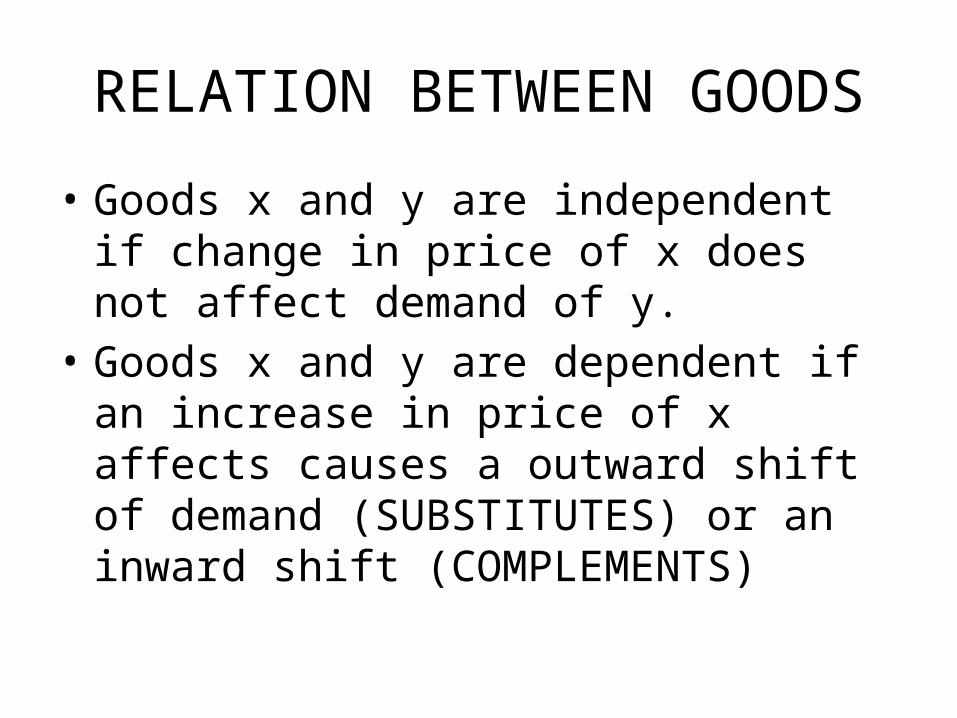

RELATION BETWEEN GOODS

• Goods x and y are independent if change in price of x does not affect demand of y.

• Goods x and y are dependent if an increase in price of x affects causes a outward shift of demand (SUBSTITUTES) or an inward shift (COMPLEMENTS)

FACTORS THAT AFFECT DEMAND

INCOMEPOPULATIONPRICES OF RELATED GOODSTASTESOTHER

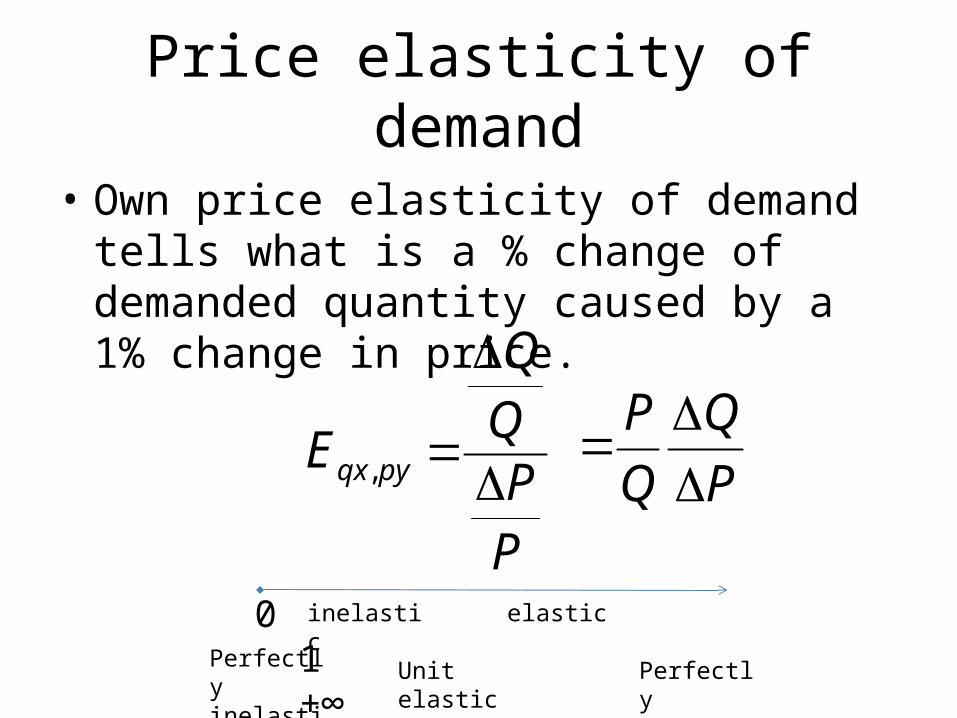

Price elasticity of demand

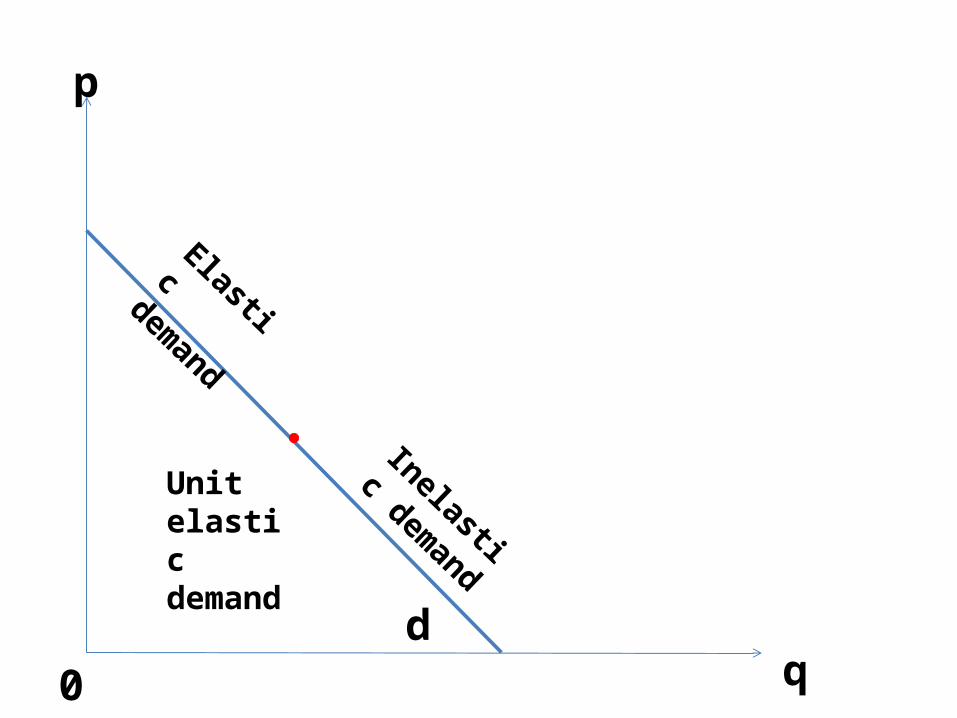

• Own price elasticity of demand tells what is a % change of demanded quantity caused by a 1% change in price.

PPQQ

E pyqx

, P

Q

Q

P

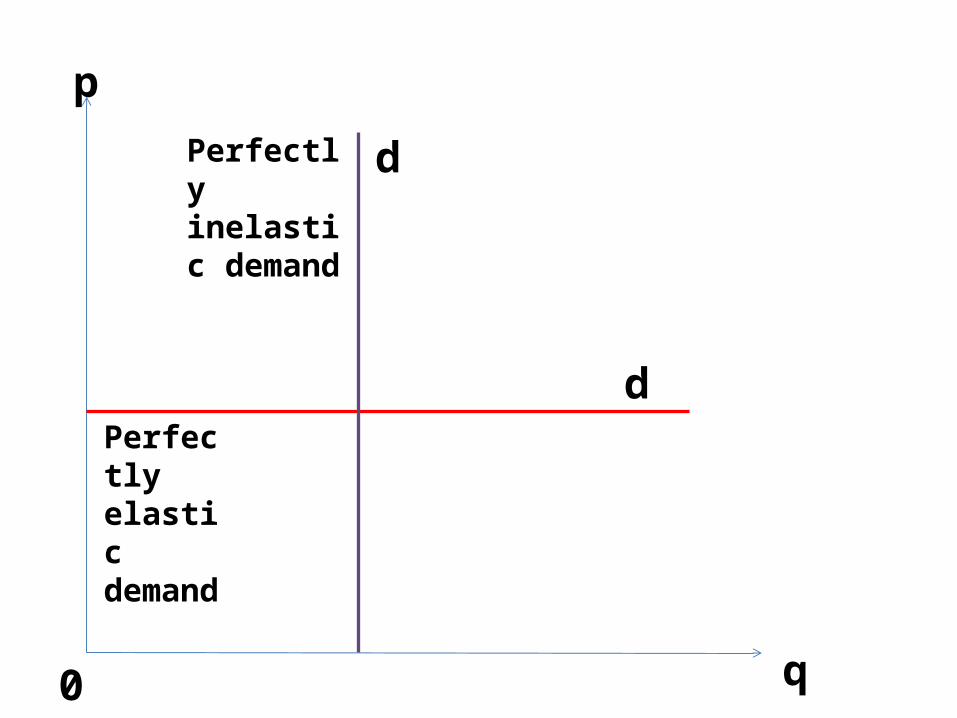

0 1 +∞ Perfectly inelastic

Unit elastic Perfectly elastic

inelastic elastic

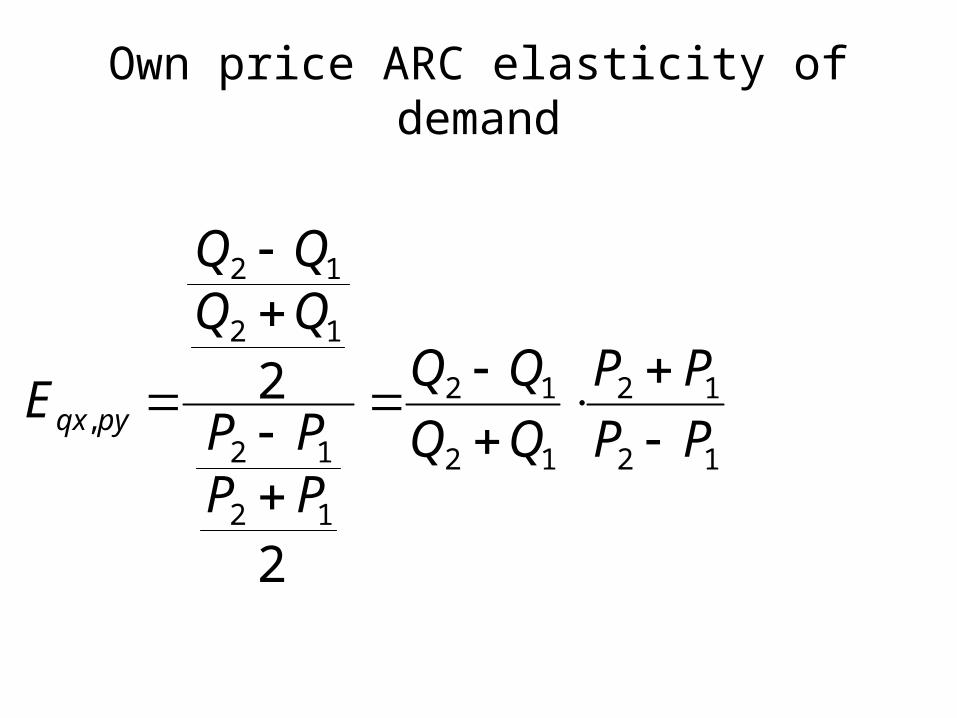

Own price ARC elasticity of demand

12

12

12

12

12

12

12

12

,

2

2PP

PP

PPPP

QQQQ

E pyqx

d

p

0 q

Elastic demand

Inelastic demand

Unit elastic demand

d

p

0 q

Perfectly elastic demand

Perfectly inelastic demand

d

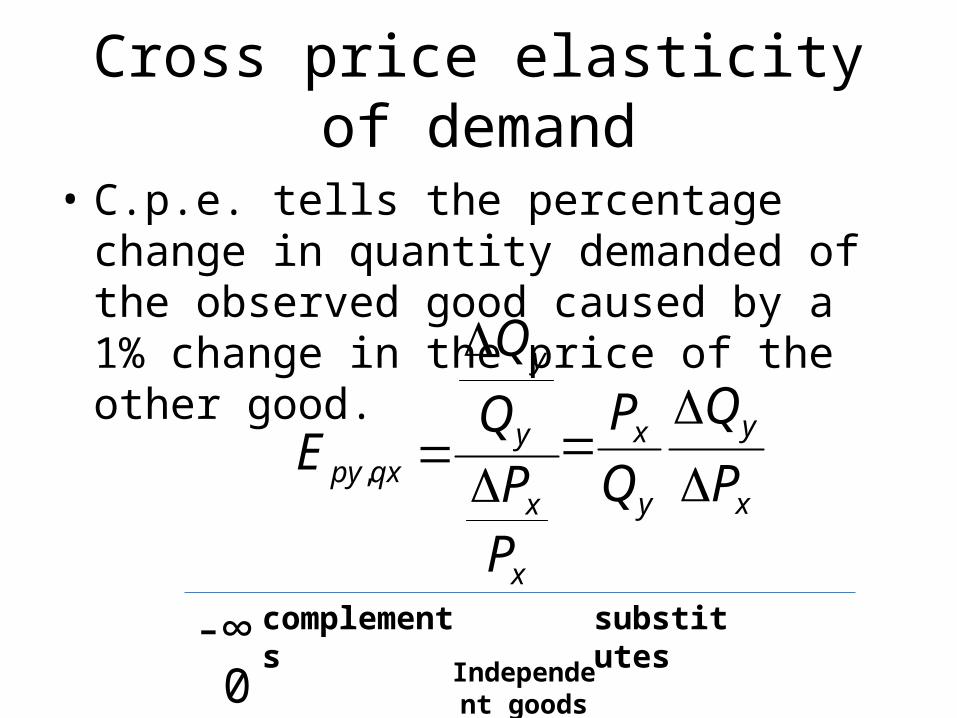

Cross price elasticity of demand

• C.p.e. tells the percentage change in quantity demanded of the observed good caused by a 1% change in the price of the other good.

x

x

y

y

qxpy

PP

Q

Q

E

,x

y

y

x

P

Q

Q

P

-∞ 0 +∞ Independent

goods

complements substitutes

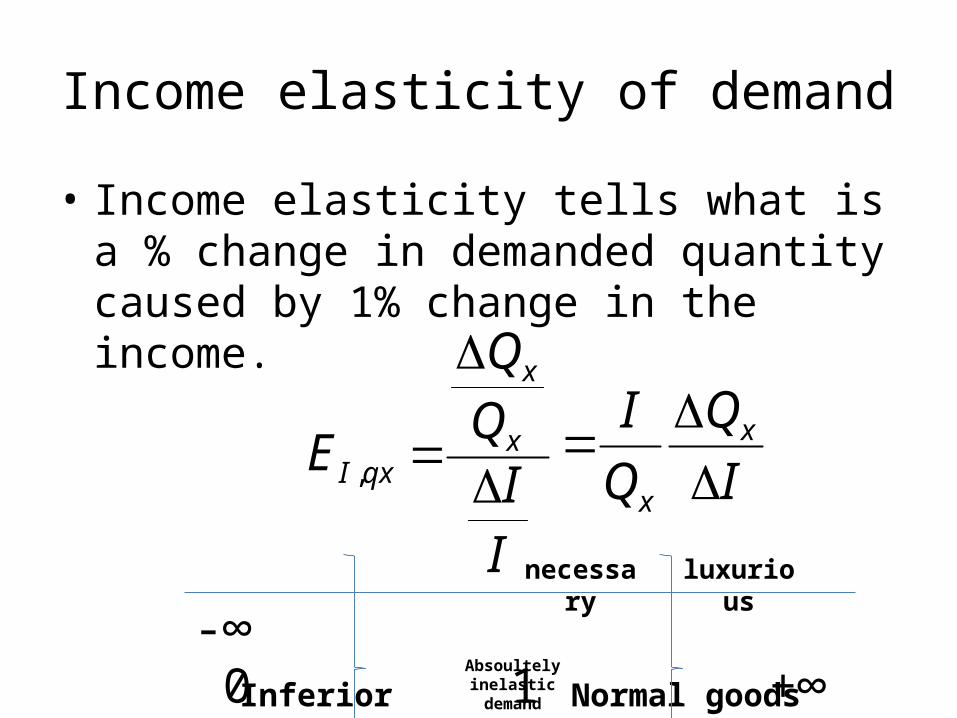

Income elasticity of demand

• Income elasticity tells what is a % change in demanded quantity caused by 1% change in the income.

IIQQ

E x

x

qxI

, I

Q

Q

I x

x

-∞ 0 1 +∞ Absoultely

inelastic demandInferior goods Normal goods

necessary luxurious

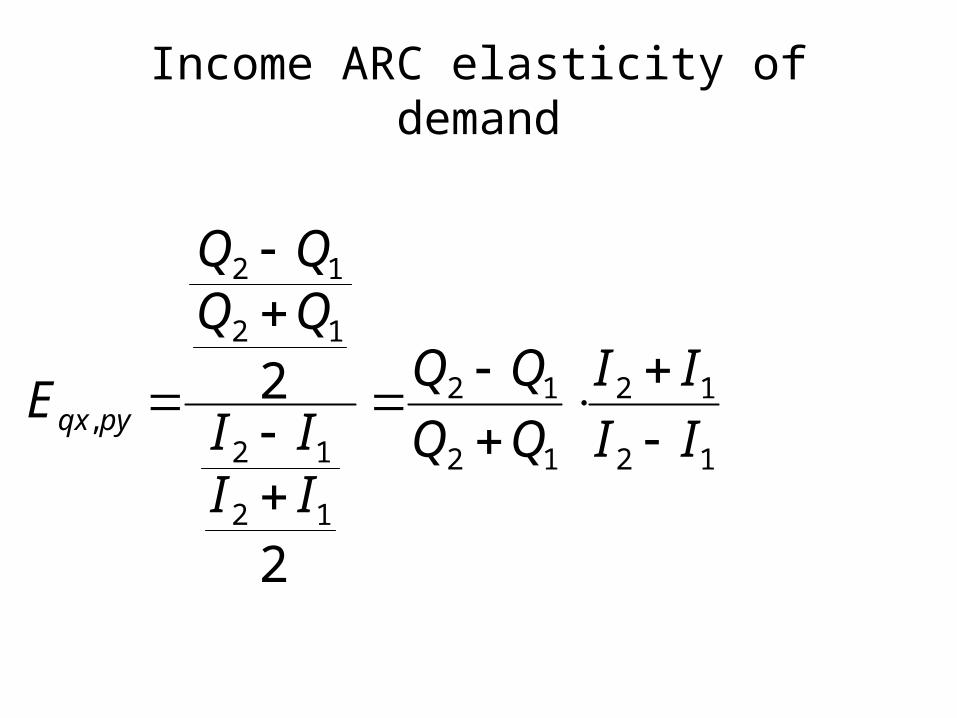

Income ARC elasticity of demand

12

12

12

12

12

12

12

12

,

2

2II

II

IIII

QQQQ

E pyqx

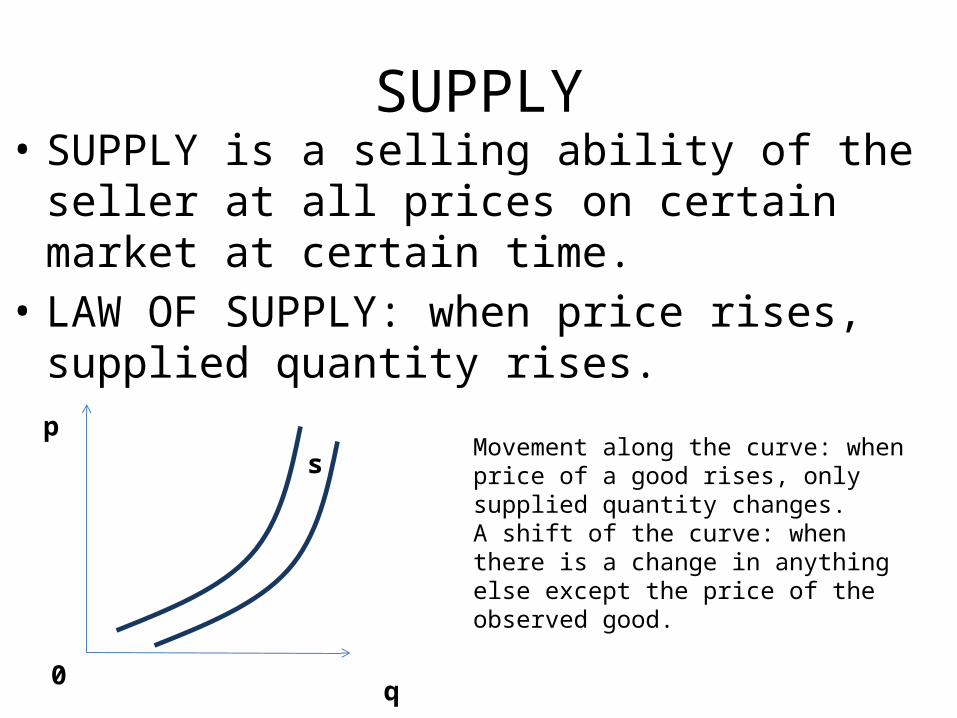

SUPPLY• SUPPLY is a selling ability of the seller at all prices on

certain market at certain time.• LAW OF SUPPLY: when price rises, supplied quantity

rises.

sp

0 q

Movement along the curve: when price of a good rises, only supplied quantity changes.A shift of the curve: when there is a change in anything else except the price of the observed good.

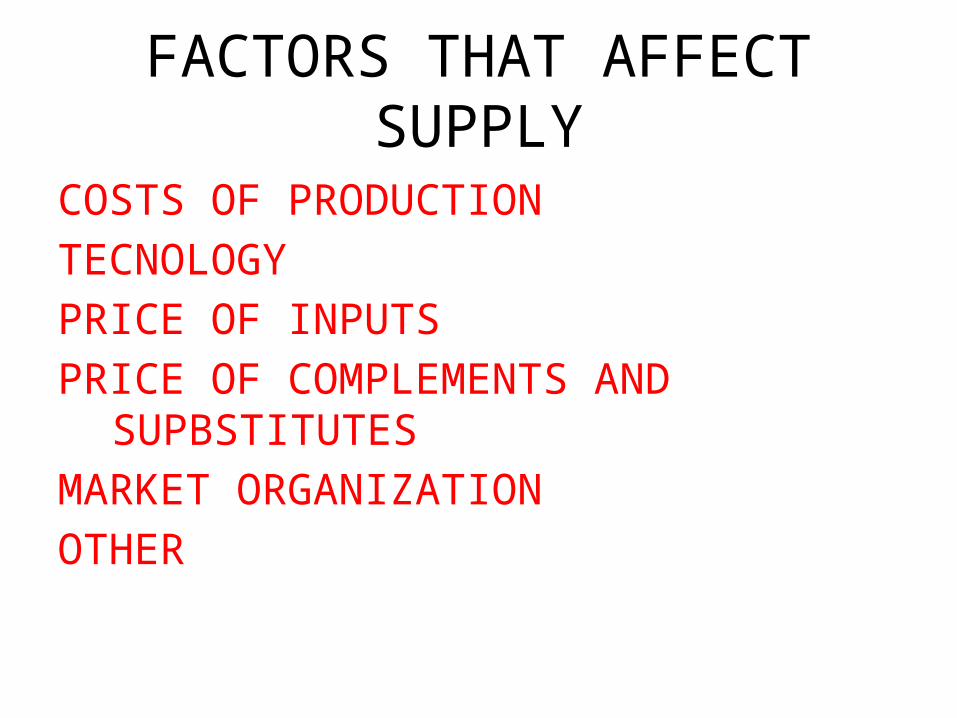

FACTORS THAT AFFECT SUPPLY

COSTS OF PRODUCTIONTECNOLOGYPRICE OF INPUTSPRICE OF COMPLEMENTS AND SUPBSTITUTESMARKET ORGANIZATIONOTHER

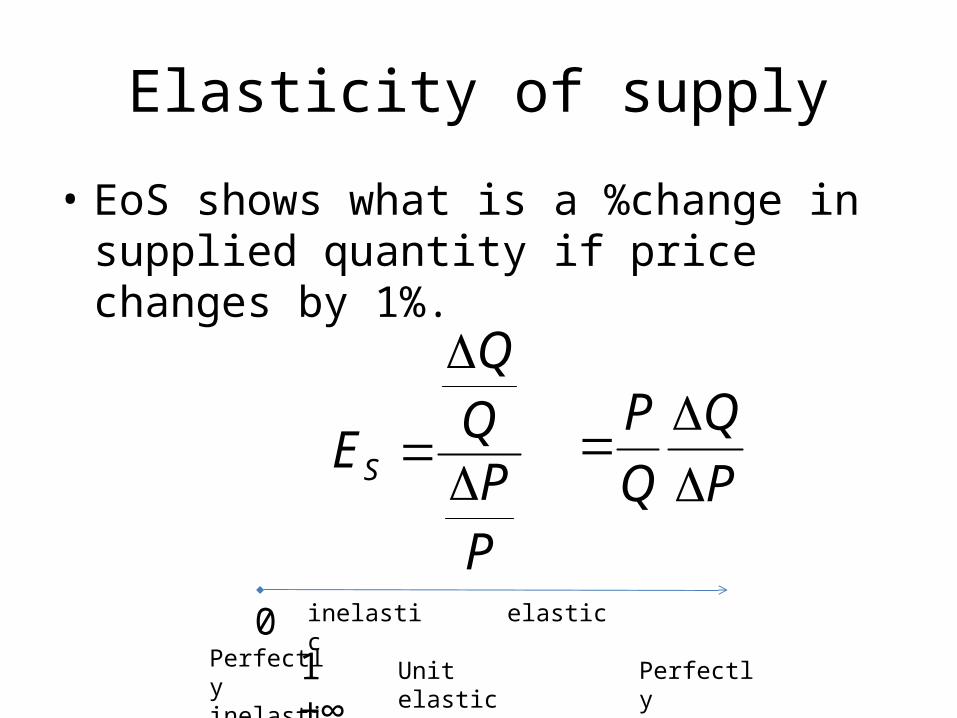

Elasticity of supply

• EoS shows what is a %change in supplied quantity if price changes by 1%.

PPQQ

ES

P

Q

Q

P

0 1 +∞ Perfectly inelastic

Unit elastic Perfectly elastic

inelastic elastic

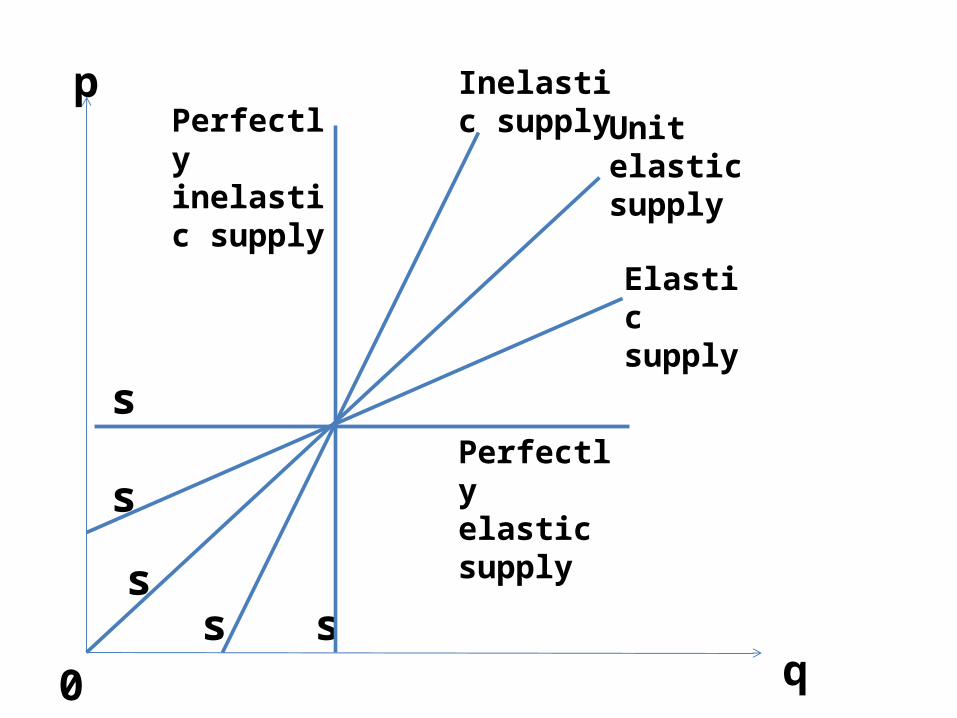

s

p

0 q

Elastic supply

Inelastic supplyPerfectly

inelastic supply

Perfectly elastic supply

ss

s

s

Unit elastic supply

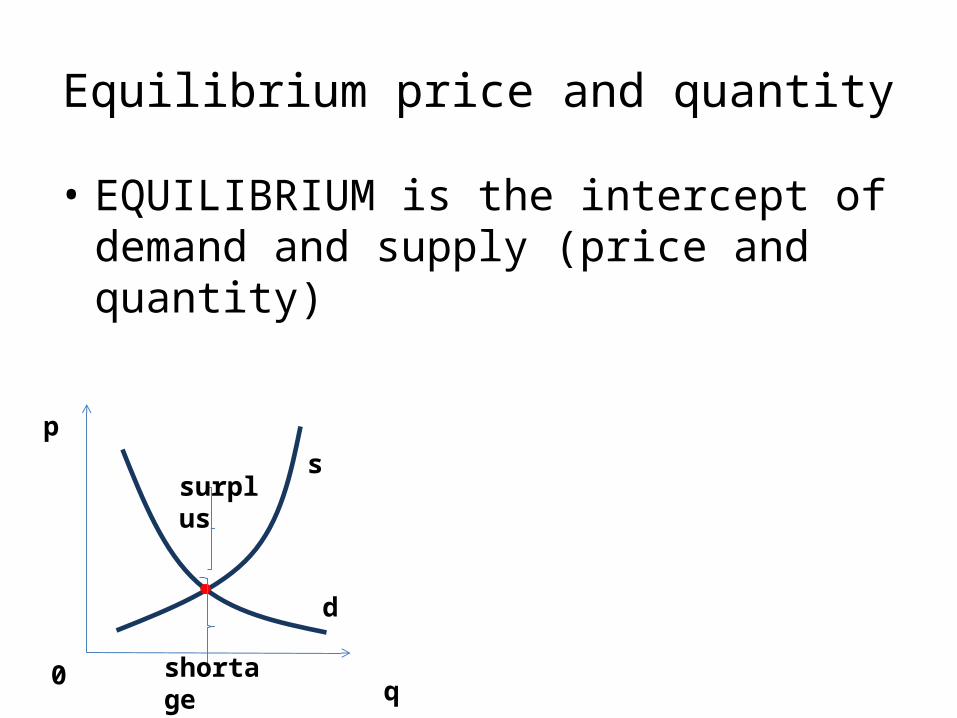

Equilibrium price and quantity

• EQUILIBRIUM is the intercept of demand and supply (price and quantity)

d

p

0 q

ssurplus

shortage

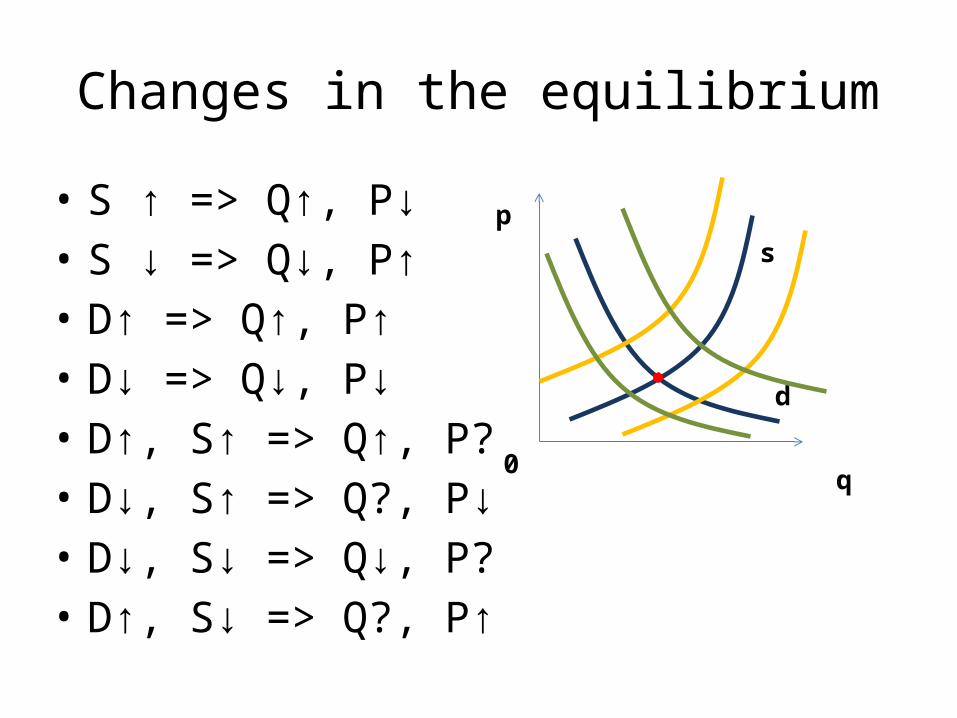

Changes in the equilibrium

• S ↑ => Q↑, P↓• S ↓ => Q↓, P↑• D↑ => Q↑, P↑• D↓ => Q↓, P↓• D↑, S↑ => Q↑, P?• D↓, S↑ => Q?, P↓• D↓, S↓ => Q↓, P?• D↑, S↓ => Q?, P↑

d

p

0 q

s

Taxation and equilibrium

• Taxes are prices of public goods• Taxes can be imposed on wages, profit, capital

gain, consumption or some special goods like alcohol, tobaco and gas.

• Taxes cause total surplus of the economy to fall.

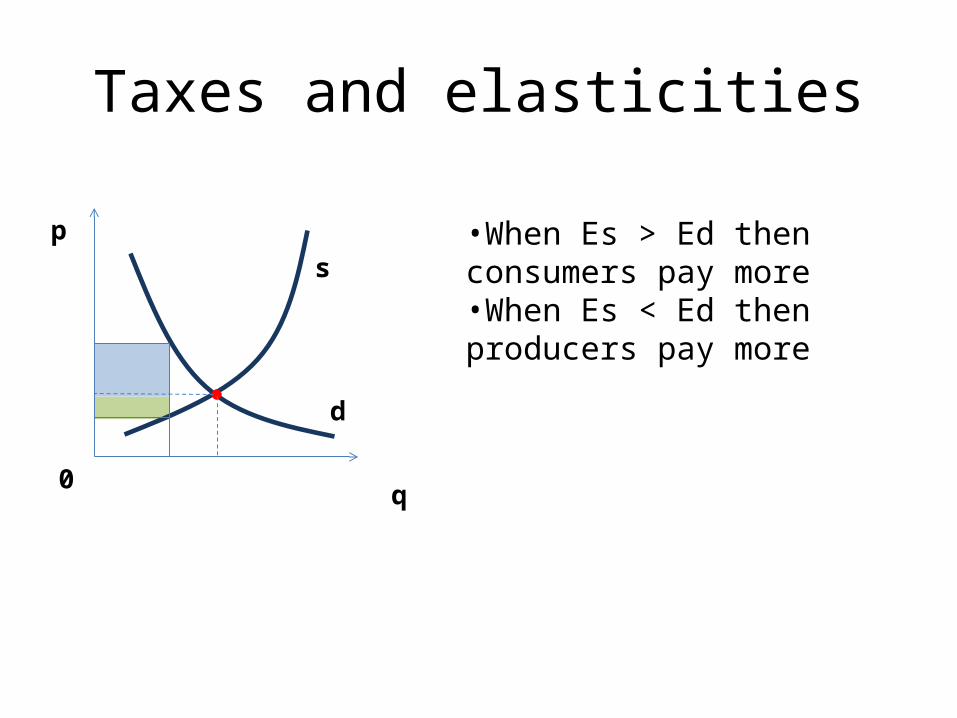

Taxes and elasticities

d

p

0 q

s•When Es > Ed then consumers pay more•When Es < Ed then producers pay more

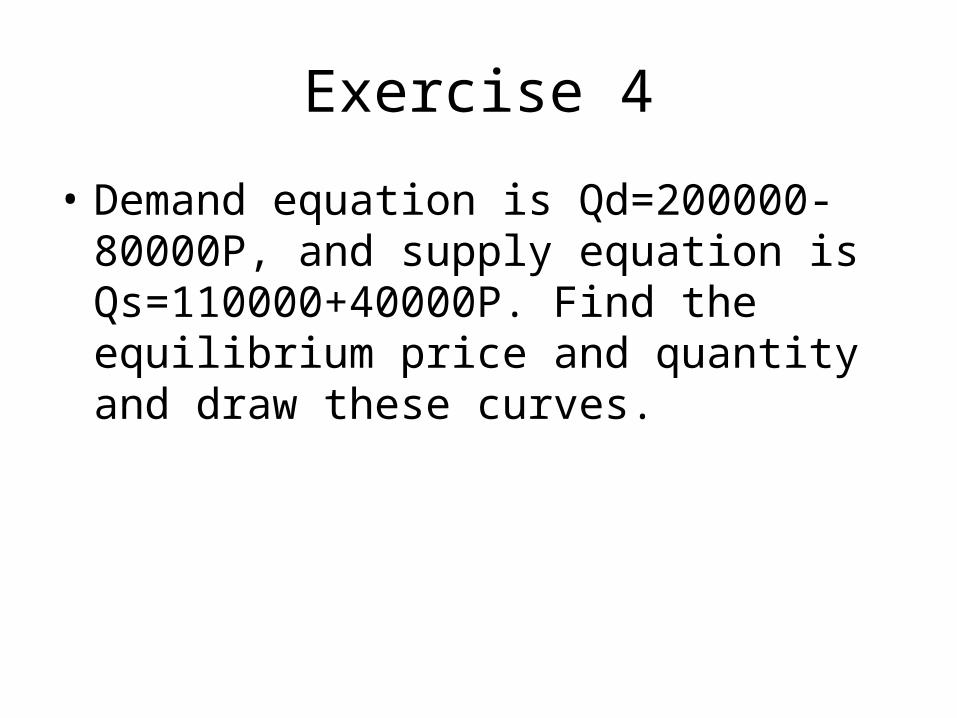

Exercise 4

• Demand equation is Qd=200000-80000P, and supply equation is Qs=110000+40000P. Find the equilibrium price and quantity and draw these curves.

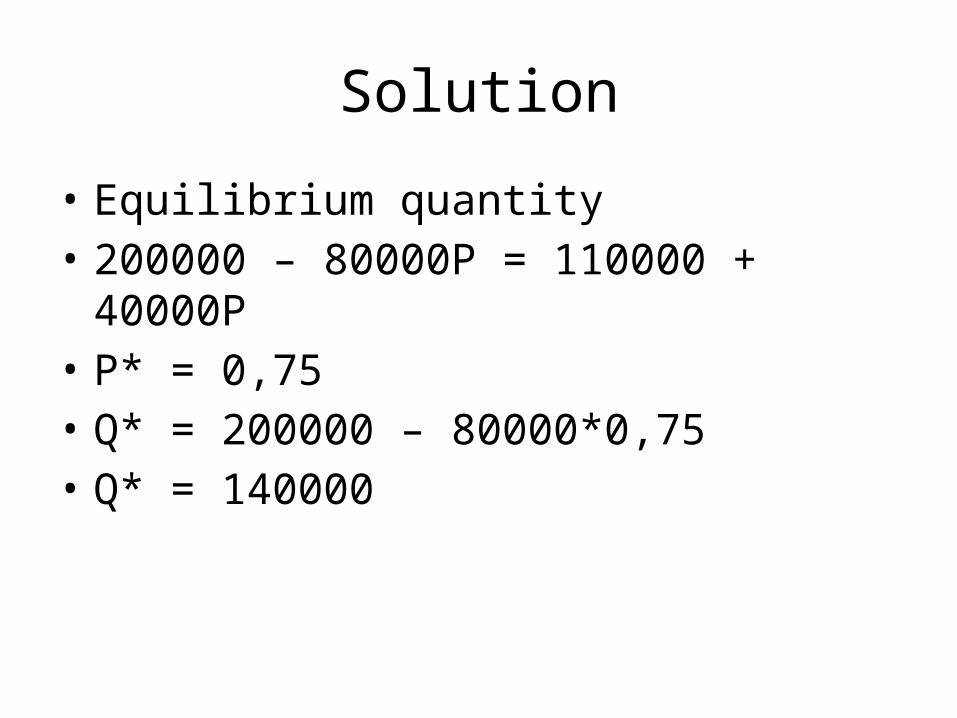

Solution

• Equilibrium quantity• 200000 – 80000P = 110000 + 40000P • P* = 0,75 • Q* = 200000 – 80000*0,75• Q* = 140000

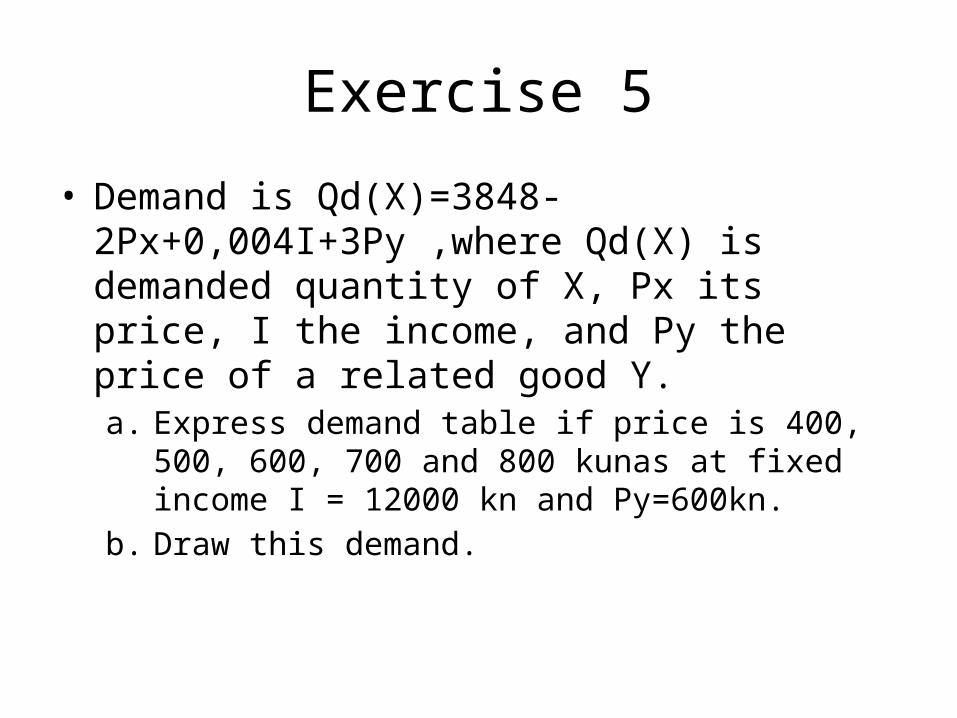

Exercise 5

• Demand is Qd(X)=3848-2Px+0,004I+3Py ,where Qd(X) is demanded quantity of X, Px its price, I the income, and Py the price of a related good Y.a. Express demand table if price is 400, 500, 600, 700 and

800 kunas at fixed income I = 12000 kn and Py=600kn.b. Draw this demand.

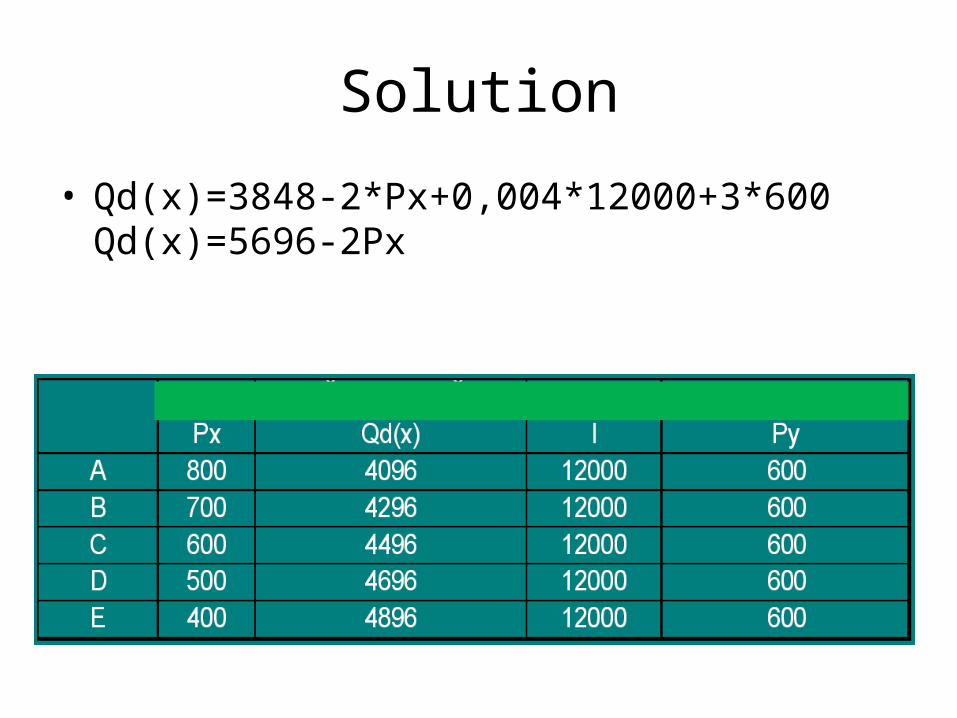

Solution

• Qd(x)=3848-2*Px+0,004*12000+3*600 Qd(x)=5696-2Px

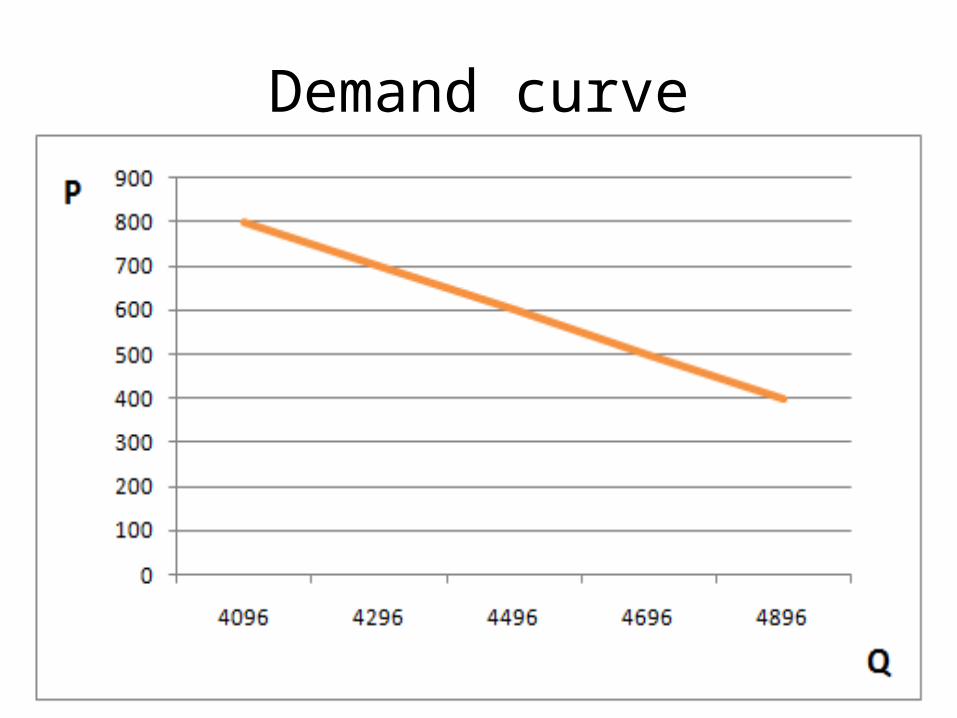

Demand curve

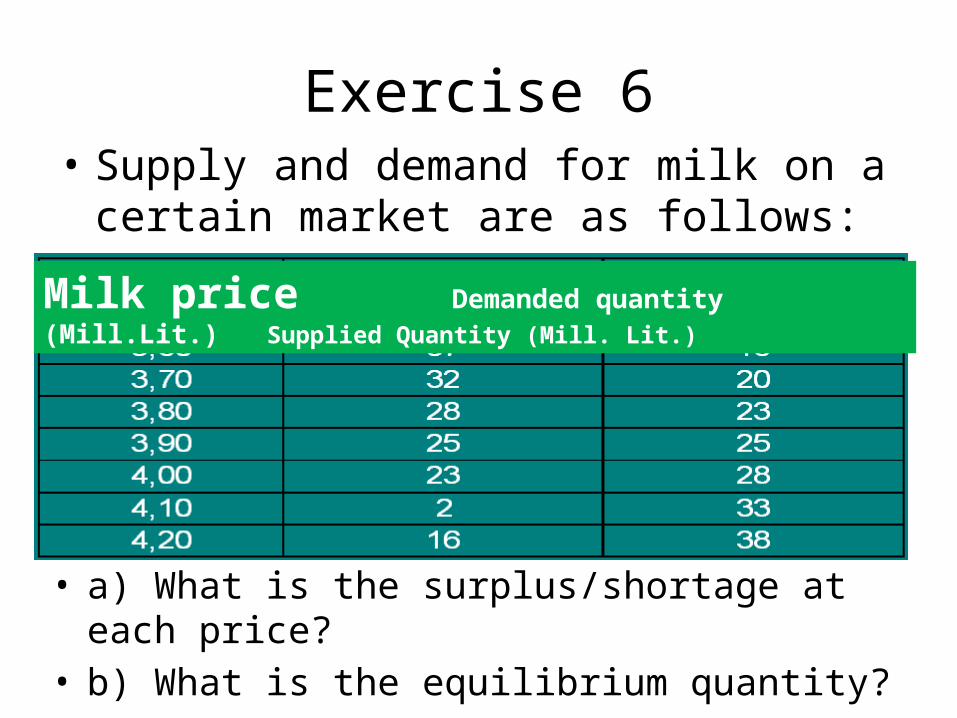

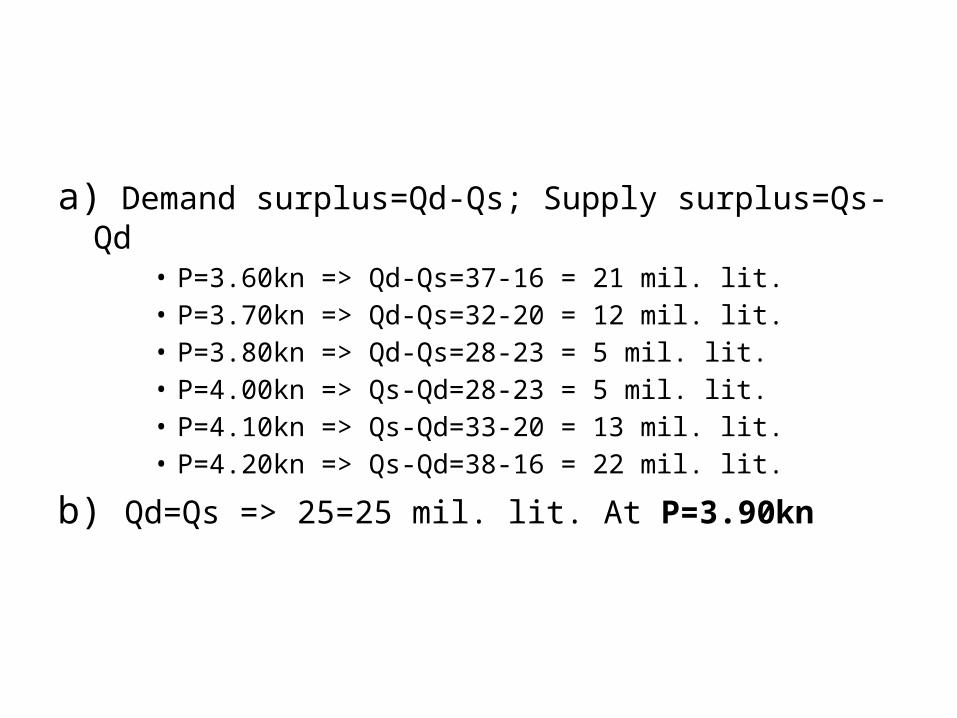

Exercise 6• Supply and demand for milk on a certain

market are as follows:

Milk price Demanded quantity (Mill.Lit.) Supplied Quantity (Mill. Lit.)

• a) What is the surplus/shortage at each price? • b) What is the equilibrium quantity?

a) Demand surplus=Qd-Qs; Supply surplus=Qs-Qd • P=3.60kn => Qd-Qs=37-16 = 21 mil. lit. • P=3.70kn => Qd-Qs=32-20 = 12 mil. lit.• P=3.80kn => Qd-Qs=28-23 = 5 mil. lit. • P=4.00kn => Qs-Qd=28-23 = 5 mil. lit. • P=4.10kn => Qs-Qd=33-20 = 13 mil. lit. • P=4.20kn => Qs-Qd=38-16 = 22 mil. lit.

b) Qd=Qs => 25=25 mil. lit. At P=3.90kn

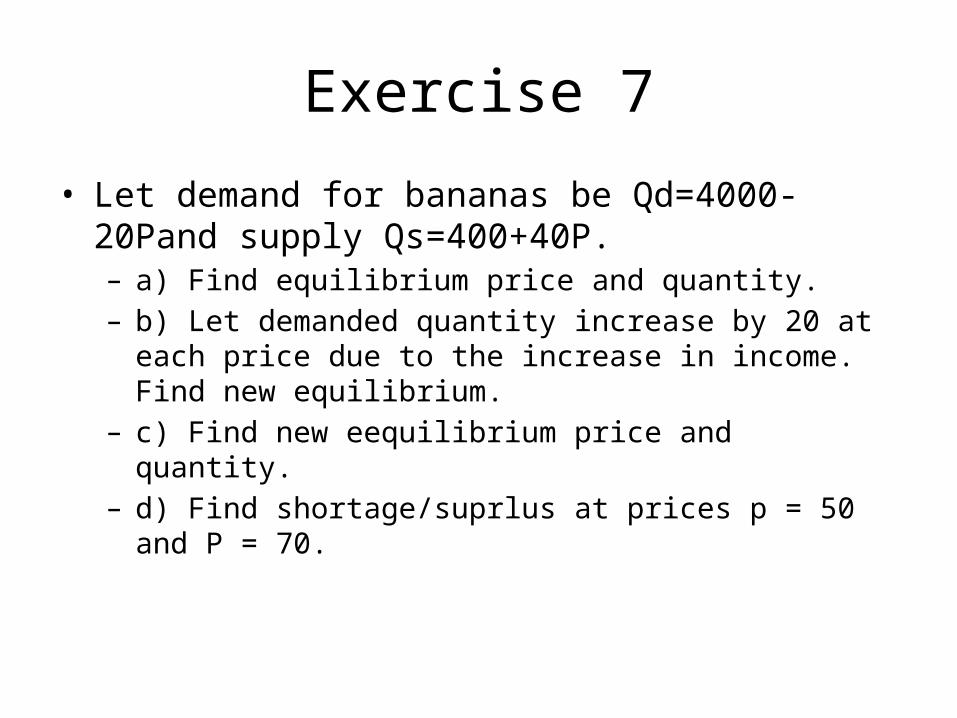

Exercise 7

• Let demand for bananas be Qd=4000-20Pand supply Qs=400+40P. – a) Find equilibrium price and quantity.– b) Let demanded quantity increase by 20 at each price due to

the increase in income. Find new equilibrium.– c) Find new eequilibrium price and quantity.– d) Find shortage/suprlus at prices p = 50 and P = 70.

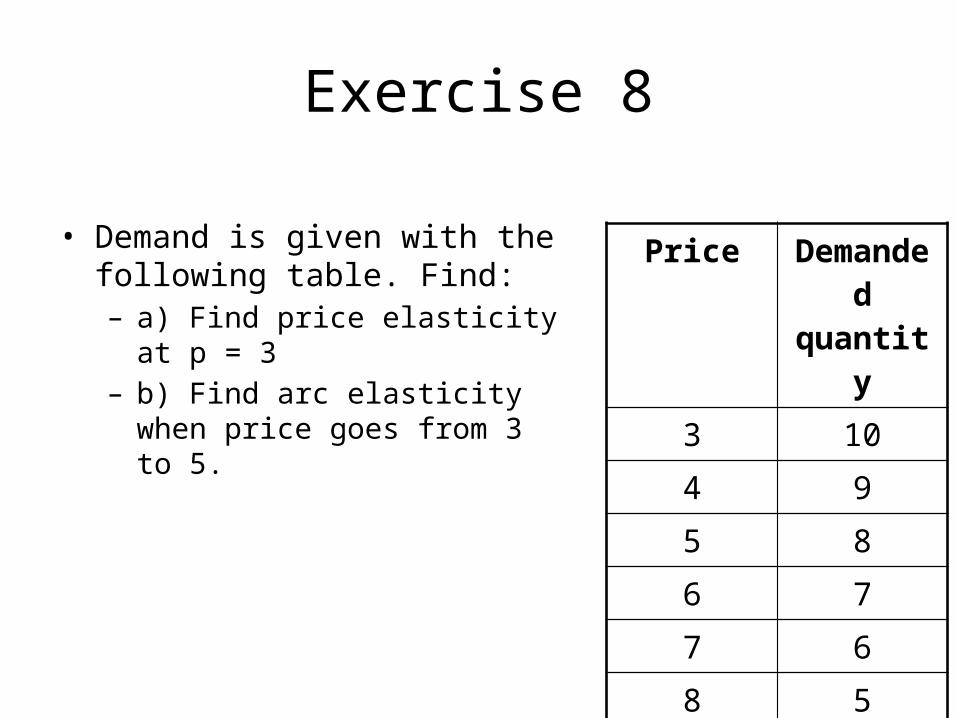

Exercise 8

• Demand is given with the following table. Find:– a) Find price elasticity at p = 3– b) Find arc elasticity when price

goes from 3 to 5.

Price Demanded quantity

3 10

4 9

5 8

6 7

7 6

8 5

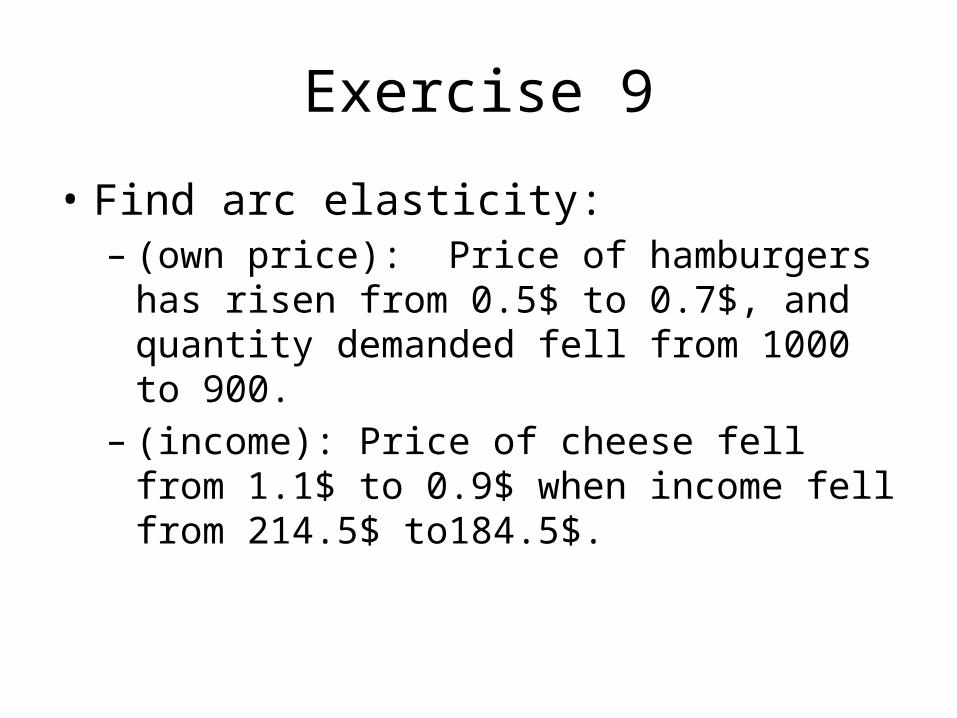

Exercise 9

• Find arc elasticity:– (own price): Price of hamburgers has risen from

0.5$ to 0.7$, and quantity demanded fell from 1000 to 900.

– (income): Price of cheese fell from 1.1$ to 0.9$ when income fell from 214.5$ to184.5$.

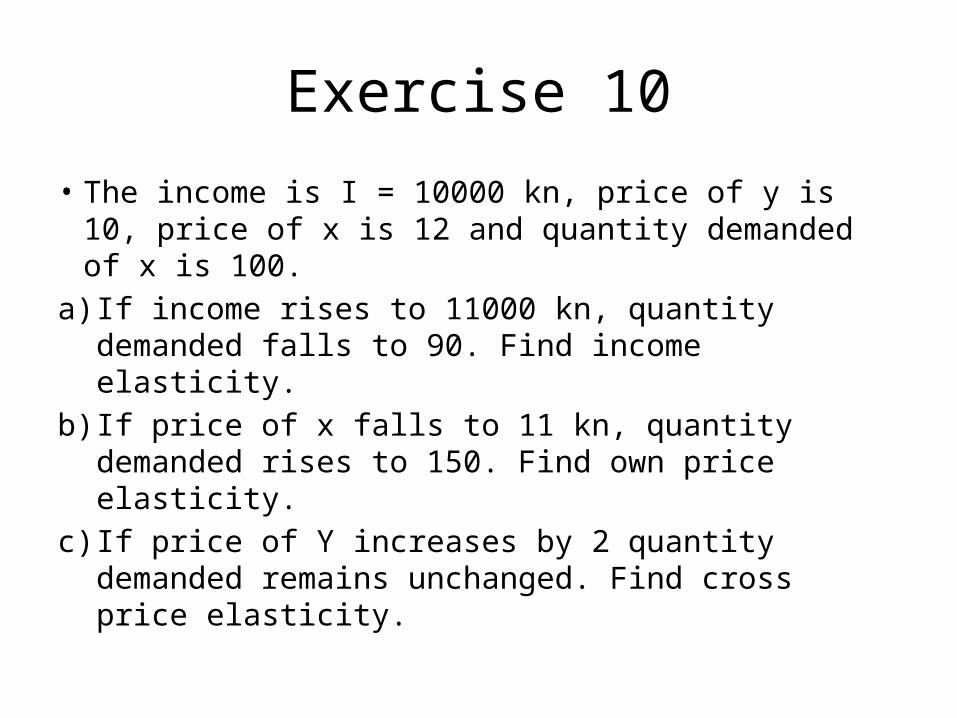

Exercise 10

• The income is I = 10000 kn, price of y is 10, price of x is 12 and quantity demanded of x is 100.

a) If income rises to 11000 kn, quantity demanded falls to 90. Find income elasticity.

b) If price of x falls to 11 kn, quantity demanded rises to 150. Find own price elasticity.

c) If price of Y increases by 2 quantity demanded remains unchanged. Find cross price elasticity.