Embed Size (px)

Citation preview

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 1/59

z

Pricing Structure of Petroleum

Products

The project has been mentored by Mr. Lokesh Chabbra, Head Finace, Delhi andguided by Mr. Prasun Garg, Manager Finance Delhi.

6/16/2011HPCLGautam Jain

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 2/59

DECLARATION

It is hereby declared that, this project is being submitted as a partial fulfillment

of the Post-Graduate Program in Masters of Business Administration (Full Time)

under Faculty of Management Studies, University of Delhi & has been

exclusively designed and prepared by me. It has not been submitted to any

other institute or organization except Hindustan Petroleum Corporation of

India, New Delhi. It has also not been published elsewhere.

Gautam Jain

FMS, Delhi

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 3/59

ACKNOWLEDGEMENT

Sometimes words fall short to show gratitude, the same happened with meduring this project. The immense help and support received from HPCL

overwhelmed me during the project.

It was a great opportunity for me to work with HPCL, pioneers in the field of Oil

and Gas. I am extremely grateful to the entire team of HPCL at Scope Minar,

New Delhi who have shared their expertise and knowledge with me and

without whom the completion of this project would have been virtually

impossible.

I would like to express my deepest gratitude and sincere thanks to all those

who have guided, encouraged or supported me in one way or another

throughout the whole course of my project.

I express my sincere thanks to my guide, Mr. Prasun Garg, Manager Finance,

for imparting their knowledge to me, and for his continuous and conscientious

guidance & attention. I would like to thank Mr. Lokesh Chabbra, Head

Finance, Northern region who gave me an opportunity to become a part of this

important and interesting project.

In the end, a sincere thanks to everyone else professionally involved in my

internship. I believe my eight weeks tenure at HPCL was a very vividexperience that gave me a feel of the corporate culture.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 4/59

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 5/59

Contents

Contents ........................................................................................................................ 5

RESEARCH METHODOLOGY:.......................................................................................... 6

PRIMARY OBJECTIVES:................................................................................................ 6

SCOPE OF THE STUDY: ................................................................................................ 7

DATA COLLECTION: ..................................................................................................... 7

LIMITATIONS: .............................................................................................................. 7

INTRODUCTION TO GLOBAL OIL AND GAS SECTOR ....................................................... 8

ENERGY SOURCES ......................................................................................................... 8

OIL & NATURAL GAS AS AN ENERGY SOURCE ................................................................ 9

Role of Oil & Gas in India's Energy Mix: .................................................................... 11

COMPANY OVERVIEW ................................................................................................... 14

MISSION AND VISION OF HPCL .................................................................................. 15

PERFORMANCE PROFILE OF HPCL ............................................................................. 16

Products & Services .................................................................................................. 17

JOINT VENTURES OF HPCL ........................................................................................ 18

REFINERIES OF HPCL ................................................................................................ 19

NEW PROJECTS ......................................................................................................... 19

Corporate Social Responsibility ................................................................................ 22

INDIAN PETROLEUM SECTOR ....................................................................................... 27

MAJOR PLAYERS IN MARKET ..................................................................................... 29

MAJOR UPSTREAM PLAYERS ..................................................................................... 29

KEY PLAYERS IN THE INDIAN OIL AND GAS SECTOR ................................................... 30

COMPANY OVERVIEW ................................................................................................... 34

PERFORMANCE PROFILE OF HPCL ................................................................................ 35

REFINERIES OF HPCL ................................................................................................ 38

CAPACITY OF REFINERIES ......................................................................................... 39

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 6/59

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 7/59

SCOPE OF THE STUDY:

.

DATA COLLECTION:

Primary Data: Primary data was collected through direct interaction with the

company’s finance and accounts department. If needed

schedule/questionnaires would be devised to get the information on all the

relevant areas of the study such as receivable management, inventory

management, management of cash etc.

Secondary Data: The secondary sources comprise Annual Reports of the firm,

other journals and periodicals. Also I have referred some websites, the list of

which is given in the bibliography.

LIMITATIONS:

Time is definitely the main constraint. Time was not sufficient enough to

assess all processes and policies of an organization of the stature of

HPCL.

Inadequacy of required data is another constraint.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 8/59

INTRODUCTION TO GLOBAL OIL AND GAS SECTOR

ENERGY SOURCES

Fossil Fuels: Fossil fuels such as Oil, Coal and Gas continue to dominate the

world energy scenario. However these resources are limited in nature and

significant uncertainty exists regarding their reserves. Political considerations

over the security of supplies, environmental concerns related to global

warming and sustainability will move the world's energy consumption away

from fossil fuels. The concept of peak oil shows that we have used about half

of the available petroleum resources, and predicts a decrease of production. Agovernment led move away from fossil fuels would most likely create

economic pressure through carbon emissions trading and green taxation.

Some countries are taking action as a result of the Kyoto Protocol, and further

steps in this direction are proposed.

Nuclear Power: Resources and technology do not constrain the capacity of

nuclear power to contribute to meeting the energy demand for the 21st

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 9/59

century. However, political and environmental concerns about nuclear safety

and radioactive waste do constraint it.

Renewable Energy Sources: These include energy derived from Solar, Wind,

Hydro, Wave and Tidal, Geothermal, Biomass sources. However, technologies

to harness these sources are only now being adapted and are yet to reach the

efficiency and effectiveness achieved by conventional fuel engines and cells.

OIL & NATURAL GAS AS AN ENERGY SOURCE

For hundreds of years, oil and natural gas has been known as a very useful

substance. The Chinese discovered a very long time ago that the energy in oil

and natural gas could be harnessed, and used to heat water. In the early days

of the oil and natural gas industry, the oil and gas was mainly used to light

streetlamps, and the occasional house. However, with much improvedrce: EIA Statisticsure 2

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 10/59

distribution channels and technological advancements, oil and natural gas is

being used in ways never thought possible. There are so many different

applications for this fossil fuel that it is hard to provide an exhaustive list of

everything it is used for. And no doubt, new uses are being discovered all the

time. Oil and natural gas has many applications, commercially, in your home,

in industry, and even in the transportation sector! While the uses described

here are not exhaustive, they may help to show just how many things oil and

natural gas can do.

Natural gas is used across all sectors, in varying amounts. The industrial sector

accounts for the greatest proportion of natural gas use in India, with the

residential sector consuming the second greatest quantity of natural gas. Oncebrought from underground, the oil and natural gas is refined to remove

impurities like water, other gases, sand and other compounds.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 11/59

GLOBAL ENERGY SCENARIO

PRIMARY ENERGY RESOURCES IN INDIA (%)

Role of Oil & Gas in India's Energy Mix:

The importance of oil in India can be gauged from the fact that it accounts for

36 percent of the Primary Energy Mix in India. Taken with natural gas, this

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 12/59

percentage rises to 45 percent. However, the proportion of natural gas is

approximately one-third that of the world average, once again indicating the

potential for rapid growth. It may be noted in this context, that a heavy

reliance on coal in India is not optimal, given that coal is a far more polluting

fossil fuel as compared to natural gas.

INDIA - ESTIMATED FUEL MIX BY 2020 (%) (Fig 3)

MARKET SEGMENTATION

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 13/59

Segmentation I

63.00%

21.40%

6.40%

6.00%3.10%

Refining and marketing

Exploration and production

Chemicals

Gas and power

Other

Segmentation II

45.30%

37.10%

11.00%

6.60%

Europe

United States

Rest of the World

Asia-Pacific

MARKET SHARE

Market Share

15.70%

15.50%

11.30%

8.60%

48.90%

Royal Dutch Shell plc

ExxonMobil Corp.

BP plc

Chevron Texaco

Corporation

Other

.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 14/59

COMPANY OVERVIEW

HPCL is a Fortune 500 company, with an annual turnover of Rs. 1,08,599 Crores

and sales/income from operations of Rs 1,14,889 Crores (US$ 25,306 Millions) during

FY 2009-10, having about 20% Marketing share in India and a strong market

infrastructure. HPCL operates 2 major refineries producing a wide variety of

petroleum fuels & specialties, one in Mumbai (West Coast) of 6.5 Million Metric

Tonnes Per Annum (MMTPA) capacity and the other in Vishakhapatnam, (East

Coast) with a capacity of 8.3 MMTPA. HPCL holds an equity stake of 16.95% in

Mangalore Refinery & Petrochemicals Limited, a state-of-the-art refinery at Mangalore

with a capacity of 9 MMTPA. In addition, HPCL is constructing a refinery at Bhatinda, in

the state of Punjab, as a Joint venture with Mittal Energy Investments Pte. Ltd.

o HPCL also owns and operates the largest Lube Refinery in the country

producing Lube Base Oils of international standards, with a capacity

of 335 TMT. This Lube Refinery accounts for over 40% of the India's

total Lube Base Oil production.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 15/59

o HPCL's vast marketing network consists of 13 Zonal offices in major cities

and 101 Regional Offices facilitated by a Supply & Distribution infrastructure

comprising Terminals, Pipeline networks, Aviation Service Stations, LPG Bottling

Plants, Inland Relay Depots & Retail Outlets, Lube and LPG Distributorships.

HPCL, over the years, has moved from strength to strength on all fronts. Therefining capacity steadily increased from 5.5 MMTPA in 1984/85 to 14.8

MMTPA presently. On the financial front, the turnover grew from Rs. 2687

Crores in 1984-85 to an impressive Rs 1, 16,428 Crores in FY 2008-09.

MISSION AND VISION OF HPCL

MISSION

"HPCL, along with its joint ventures, will be a fully integrated company in the

Hydrocarbons sector of exploration and production, refining and marketing;

Focusing on enhancement of productivity, quality and profitability; caring for

customers and employees; caring for environment protection and culturalheritage.

It will also attain scale dimensions by diversifying into other energy related

Fields and by taking up transnational operations."

VISION

To be a World Class Energy Company known for caring and delighting the

customers with high quality products and innovative services across domestic

and international markets with aggressive growth and delivering superior

financial performance. The Company will be a model of excellence in meeting

social commitment, environment, health and safety norms and in employee

welfare and relations

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 16/59

PERFORMANCE PROFILE OF HPCL

o FINANCIAL

2009-2010 2005-2006

SALES 114,888.63 76,920.26

GROSS PROFIT 4,193.18 1,151.21

DEPREICIATION 1,164.40 690.23

INTEREST 903.75 175.88

TAX (includingdiffered tax)

823.61 (131.91)

PROVISION FOR FBT 0.05 11.38

NET PROFIT 1,301.37 405.63

DIVIDEND 406.35 101.80

TAX ON DISTRIBUTED

PROFIT

67.49 14.28

RETAINED EARNINGS 827.53 289.55

SOURCE: 58 ANNUAL REPORT OF HPCL

o WHAT CORPORATION OWES

2009-2010 2005-2006

GROSS FIXED ASSETS 24,988.37 13,479.25

DEPRECIATION 9,681.70 6,141.85

NET FIXED ASSETS 15,306.67 7,337.40

CAPITAL WORK IN

PROGRESS

3,887.59 2,363.88

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 17/59

INVESTMENTS : JVC 2,623.83 825.76

OTHERS 8,763.39 3,201.88

NET CURRENT

ASSETS

4,086.83 3,055.09

DEFFERD TAX

LIABILITY

(1,807.97) (1,384.44)

TOTAL 32,860.34 15,399.57

2009-2010 2005-2006

NET WORTH 11,557.97 8,735.74

SHARE CAPITAL 339.71 338.94

SHARE FORFEITURE (0.70) -

RESERVES 11,218.96 8,396.80

BORROWINGS 21,302.37 6,663.83

TOTAL 32,860.34 15,399.57

SOURCE: 58 ANNUAL REPORT OF HPCL

This data shows that overall sales of the company are increased from Rs.

76,920.26 crores (2005-2006) to Rs. 114,888.63 (2009-2010), the gross profit

of the company increased from Rs. 1,151.21 crores (2005-2006) to Rs.

4,193.18 (2009-2010) and the overall net profit of the company is increased

from Rs. 405.63 (2005-2006) to Rs. 1,301.37 (2009-2010) so this shows that

there is a 220.8% of increase in net profit but the overall net worth of the

company is increased from Rs. 8,735.74 (2005-2006) to Rs. 11,557.97 (2009-

2010).

Products & Services

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 18/59

• Refineries

• Aviation

• Bulk Fuels & Specialities

• International trade

• LPG - HP GAS• Lubes - HP LUBES

• Retail

• Exploration & Production

• Joint Ventures

• Alternate Energy

JOINT VENTURES OF HPCL

In an effort to fulfill its vision and achieve its objectives, HPCL has formulated

plans for expansion, diversification and internal development

Crude Refining and Marketing of finished Petroleum products is the

core area of the Corporation. Opportunities are also being explored to access new

revenue streams, and augment downstream businesses. Accordingly, HPCL has

ventured in Upstream activities (Exploration and Production) and piped gas

distribution in major cities

1 HPCL-Mittal Energy Ltd. (HMEL)

2 Hindustan Colas (HINCOL)

3 Prize Petroleum Company Limited

4 South Asia LPG Co Pvt. Ltd. ( SALPG)

5 Bhagyanagar Gas Limited (BGL)

6 Aavantika Gas Limited

7 Petronet India Limited (PIL)

8 Petronet MHB Limited (PMHBL)

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 19/59

9 Mangalore Refineries and Petrochemicals Limited (MRPL)

10CREDA-HPCL Biofuel Limited (CHBL)

11Sushrut Hospital and Research Centre

REFINERIES OF HPCL

Without refining, the rich resources of crude petroleum of nature would remain

latent. Value-added products from crude petroleum like petrol, diesel,

kerosene, liquefied petroleum gas, naphtha and many more products would

not be available for growth and development of a nation.

HPCL refineries upgrade the crude petroleum into many value-added products

and over 300 grades of lubricants, specialties and greases. The Lubricating

Oils Refinery set up at Mumbai is largest lube refinery in India. It produces

superior quality lube base oils.

The offsite product handling facilities of refineries at Mumbai and

Vishakhapatnam has been automated. Projects have been implemented and

facilities upgraded to produce green fuels like unleaded petrol and low sulphur

diesel. and Euro III & Euro IV works are in progress . The refineries have been

benchmarked by an international agency for various performance parameters.

Numerous awards have been bestowed on both the refineries in recognition of

the efforts in the field of energy conservation, environment and safety.

CAPACITY OF REFINERIES

1 MUMBAI REFINERY : 6.5 million metric tons per annum (MMTPA) capacity

2 VISAKH REFINERY : 8.3 million metric tons per annum (MMTPA) capacity

NEW PROJECTS

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 20/59

Identification and implementation of projects

for process improvement, performance,

safety and environment related concerns are

ongoing processes. The following newprojects have been undertaken by Mumbai

and Visakh Refineries to upgrade the

facilities to meet the product demand :

Facilities for Euro-III & IV grade Gasoline: Both Refineries have

executed Green Fuels & Emission Control Project (GFECP) at

Mumbai Refinery and Clean Fuel Project at Visakh Refinery to

produce Euro-III/IV gasoline with capability to produce Euro-IV MS.Apart from meeting MS quality stipulations, the project also enabled

to upgrade Naphtha to Gasoline which is a value added product.

New FCCU project at Mumbai Refinery: In order to enhance the

production of value added products like LPG, MS and HSD, the

refinery is installing a new FCCU of 1.4 MMTPA capacity, which will

increase the FCCU processing capacity from the existing level of 1

MMTPA to 2.4 MMTPA. The project is expected to be completed by

the 2nd qtr of 2010-11.

Environmental facilities: Environmental facilities are being

upgraded in both the Refineries by installing Integrated Effluent

Treatment Plants to comply with air pollution limits set forth by

Pollution Control Board.

Bottom Up-gradation Projects: Mumbai Refinery has undertaken

Feasibility Study of “Solvent Deasphlating Unit (SDA)” by using the

proprietary technology “Residuum Oil Supercritical Extraction

(ROSE)”. Setting up of this plant is expected to enhance the

recovery of valuable oil from the heavier fraction of the crude (VTB).

Similarly Visakh Refinery has also planned to implement the

Delayed Coker Unit (DCU) Projects for bottom up gradation.

LOBS Project: Mumbai refinery produces various grades of LOBS

with sulphur above 300 ppm and saturates below 90%, which fall

under API Gr-I category. To meet the increased demand of the same

LOBS quality in the domestic market including the API Gr-II/III

category the capacity is being uplifted. The project will help HPCL to

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 21/59

keep its market share of LOBS intact. The project is expected to be

completed by June 2010.

MR/VR DHT: Both Refineries are setting up DHT projects to

upgrade / produce the Euro-III / IV HSD and projects are expected to

be completed mechanically by Sept 2011. The Environmental

Clearance for DHT Projects for both the refineries, Mumbai

Refinery and Visakh Refinery has been obtained.

The Environmental Statement for the FY 2009-10 has been

submitted to Andhra Pradesh Pollution Control Board (APPCB). View

the Compliance Status of Environmental Clearance Stipulations for

DHT VR Project.

Single Point Mooring (SPM) Project at Visakh

Refinery: Visakh Refinery putting up SPM project to facilitate

unloading of large crude parcels of the size of around 300,000

Metric Tonnes from Very Large Crude Carriers (VLCCs). The VLCCs

cannot be berthed in the existing crude receiving jetties due to

draught restrictions. The installation of SPM will reduce the freight

cost and wharf age charges and thus will improve the economics of

the Refinery. The Environmental Clearance for this project has been

obtained. View status of Compliance of Stipulated EC Conditions.

The offshore and onshore installation work of the project has been

completed. The Environmental Statement for the financial year

(FY2009-10) has also been submitted to the Andhra Pradesh

Pollution Control Board (APPCB) .

Modernization Project for Mounded Storage System for

LPG /Propylene at Visakh Refinery: Visakh Refinery is executing

the Mounded storage system for LPG and Propylene in place of

existing LPG /Propylene Horton spheres. This is a risk mitigation

project and undertaken following the recommendations by theexternal safety agencies, viz., High Power steering Committee

August, 1998, 4th Round ESA - September, 1999 etc. The Mounded

storage of LPG has proved to be safer compared to above ground

storage vessels since it provides intrinsically passive and safe

environment and eliminates the possibility of Boiling Liquid

Expanding Vapor Explosion (BLEVE) phenomenon. The approved

project cost is Rs. 124 Crores.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 22/59

Corporate Social Responsibility

Environment

Mission & SHE policy

Mission

To have safe, healthy and pollution free environment in and around all our refineries,

plants, facilities and other premises at all times; instill awareness in these areas,

including relevant laws, in all employees, families and the communities in which they

carry out the activities.

Environment Policy

The Corporation is committed to conduct its operation in such a manner as

compatible with environment and economic development of the community. Its aim is

to create an awareness and respect for the environment, stressing on every

employee’s involvement in environmental improvement by ensuring healthy

operating practices, philosophy and training.

Health Policy

To provide a structured program to look after and promote the health of vital “Human

Resource”, essential for productivity and effectiveness of the Corporation.

Safety Policy

As an integral part of its business, HPCL believes that no work or service or activity is

so important or urgent that safety be overlooked or compromised. Safety of the

employees and public, protection of their as well as Corporation’s assets shall be

paramount. Corporation considers that safety is one of the important tools to enhance

productivity and to reduce national losses. The Corporation will constantly Endeavour

to achieve and maintain high standards of Safety in its operations.

BEYOND BUSINESS CORPORATE SOCIAL

RESPONSIBILITY

Promising whatever it takes to make a difference:

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 23/59

HPCL is committed to create a positive impact on the society and contribute to

socio economic development including measures for improving the quality of

life of underprivileged classes of the society. Since its inception, HPCL has tried

to follow Corporate Social Responsibility in the true sense. This sense of responsibility comes from a feeling that not every achievement of the

company is reflected in its balance sheets. The relevance that a company

achieves by virtue of its socio-economic participation surpasses the profit and

loss measurements by far. In this respect HPCL has proceeded in the truly

corporate manner, planning investments in social causes methodically,

executing the various steps with utmost care and securing distinctive

developments for the poor and the downtrodden masses. HPCL has provided

sustained value for the above mentioned investments all the time and has

contributed to the living standards of underprivileged masses.

A compact booklet: "Bringing Smiles (2008-09)" provides details of HPCL's

various CSR activities during FY 2008-09. "Bringing Smiles (2009-10)" contains

details of CSR activities undertaken by HPCL during the FY-2009-10.

When it comes to social contribution our country never lacked goodwill among

corporate citizens but competent contributors were never in good numbers as

far as management and execution skills are concerned. HPCL has surely paved

the way in the right direction with exemplary contributions. HPCL's initiatives

have created value in the following diverse ways –

1. HPCL's initiatives have made notable differences in fields as diverse aseducation, infrastructure, welfare measures, health and hygiene,vocational training & employment generation, training in self-reliance,amenities for the sufferers of natural disasters and environmentalprotection. The most commendable feature of the support is that HPCLhas taken innovative measures to infuse self reliance in masses to

secure long lasting improvements.

2. HPCL has categorized different projects of social relevance according tonational and regional significance. The investment has been madeaccording to solid result oriented plans with every detail of the prospecttaken into consideration.

3. The funds for different CSR projects have been consistently allocated ina transparent manner. HPCL follows an allocation process based on

complete evaluation and benchmark standardization.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 24/59

4. A Foundation has been established to take up projects of Nationalsignificance. This initiative has helped to identify the impacts of projectskeeping national interest in mind.

5. HPCL has set exemplary organizational competency in carrying outcomplex and demanding projects. The implementation process issupported by adequate checks and balances including reporting,assessment and appraisal by world class professionals.

HPCL took its first step in this direction during the year 1985-86 with a modest

budget allocation of Rs.18 Lakhs for undertaking various welfare activities for

the benefit of SC/STs and other weaker sections of the Society under the

Special Component Plan/Tribal Sub-Plan and Welfare Plan for Weaker Sections.Later the corporation expanded the scope and allotment of such projects in

manifolds to uphold its "Socially Responsible Corporate citizen" Image and to

address the huge welfare expectation which the society was increasingly

resting on the corporation. Budget for the CSR projects subsequently rose

every year and larger portions of underprivileged masses were gradually

incorporated into the schemes. The corporation went beyond the parameters

of the SC/ST Component Plan to extend support. The fund has been arranged

by virtue of a policy decision to allocate certain percentage of the net profit for

each financial year to Component Plan and CSR activities and to operate the

CSR policy on Triple Bottom Line principle i.e. Economic, Social & Environment.

The Expenditure for the year 2005-06 stands at a whopping Rs.7 crores for SCP

projects and Rs. 8 crores for other CSR projects.

An "HPCL Foundation" is being set up to finance the CSR projects and also

monitor implementation of distinct schemes like AIDS prevention, vocational

training for unemployed youth, education of rural children, computer training,

healthcare facilities, etc.

Corporate Social Responsibility Initiatives touching lives :

The following CSR Initiatives have placed HPCL in a league of its own.

Swavalamban:

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 25/59

The objective of this programme is to provide free Vocational Training to

beneficiaries from low income group households. HPCL and CII have joined

hands along with M/s City & Guilds to impart training to youths and change

them into able professionals.

Navjyot:

This project aims at increasing the health index of children who have been

unfortunately displaced from slums. The project currently accommodates 3100

slum children from Bawana Resettlement Colony and imparts health care

services. Navjyot India Foundation is the official partner in the project.

Unnati:

The objective of this initiative is to provide Computer training to 3000 students

at Visakhapatnam through NIIT Limited.

Nanhi Kali:

The project is an initiative towards Supporting the Girl Child. Corporation has

provided Sponsorship of the quality school education of 498 renewals of Nanhi

Kalis and additional 1400 Nanhi Kalis from various Govt. Schools from

Mehboobnagar Dist. and Paderu region in Andhra Pradesh in collaboration withM/s KC Mahindra Education Trust.

Muskan:

This project ponders into the welfare of 100 underprivileged children, many of

them living in footpaths by providing shelter at Tuglakabad and Jahangipuri in

Delhi. Education, meals, clothing, health care, vocational training etc. are

provided for them through HPCL's operating partner M/s Prayas Juvenile Aid

Centre (JAC) Society.

Suraksha:

This is an initiative towards prevention of HIV/AIDS through training/lectures

and distribution of condoms to truckers at Highway Retail Outlets. The project

operating partner is Organization for Socially Economic and Rural Development

(OSERD).

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 26/59

Global Warming:

Under this project, approximately 20000 school children are being educated on

causes of Global Warming at Delhi, Goa and Mumbai through our operatingpartner CSRL (Centre for Social Responsibility & Leadership).

A Corporate approach towards development:

The current projects bear the mark of a well thought of corporate mindset .To

summarise HPCL's approach towards social welfare we have to mention the

following points-

1. Strategic approach to every issue is the key to HPCL's success.

2. HPCL has meticulously secured the input-output-outcomebalance.

3. HPCL has underlined the social problems accurately and hastaken result oriented initiatives.

4. The advanced planning regarding allocation of resource andcorrect evaluation of performance against benchmark haverepresented organizational competence.

The success of HPCL lies in the maintenance of social responsibilities amid profit

driven and competitive business environment. Apart from directly contributing to the

betterment of weaker sections of the society, HPCL has been associated with

healthcare, education, environmental protection, agricultural development, rural

reconstruction, water supply development etc. It can be said that the corporation hastouched lives qualitatively acting as a corporate social ambassador. HPCL has always

seen itself as a contributing participant in India's overall development. The

corporation has stood the test of time being true to citizen's expectations.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 27/59

INDIAN PETROLEUM SECTOR

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 28/59

Natural gas

distribution

Downstream Sector

Upstream Sector

Oil & Gas

Exploration

ONGC, OIL, RIL

Indian Petroleum Sector

IOC, BPCL, HPCL, ONGC, RIL,

CPCL, BRPL, KRL, NRL, MRPL

GAIL

Refining &

Marketing

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 29/59

MAJOR PLAYERS IN MARKET

MAJOR UPSTREAM PLAYERS

GSPC RIL

OILHOEC

ONGC

Cairn

British

Gas

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 30/59

KEY PLAYERS IN THE INDIAN OIL AND GAS SECTOR

Company

Fortun

e 500Rank

Profile

105

• India’s largest company by sales (Turnover

: USD 37bn)

• India’s flagship Downstream company –

Along with subsidiaries accounts for 47%

of Petroleum market share among Public

Sector Oil Companies, 41% of National

refining capacity and 51% downstream

pipeline capacity

• Operates the largest and widest network of

petrol and diesel stations in the country

264

• India’s largest private sector company on

all major financial parameters

• Presence in Upstream, midstream and

downstream segment

287

• PSU engaged in refining and marketing of

petroleum products

• Have two subsidiary companies – Kochi

Refineries Ltd. And Numaligarh RefineriesLimited

• Refining Capacity – 24.5 MT (16.25% of

India’s refining capacity)

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 31/59

311

• Another mega Public sector company with

focus on refining and marketing

• Turnover of about US$ 17 Billion

• Accounts for about 10% of India’s total

refining capacity

335

• India’s Flagship E & P Company

• Accounts for 77% of crude oil and 81% of

natural gas produced in India

• Venturing into downstream refining and

marketing

OPPORTUNITIES FOR INDIA

1. Strategic location

• Nearness to the premier crude oil and gas supply market (Middle East)

• Geographical Proximity to the major petroleum product importers – China

and

Japan

2. Well Developed Maritime infrastructure

3. Government policies conducive to the growth of the sector – tax holidays,

Special Economic

Zones for Petroleum products

4. Availability of experienced manpower at lesser costs –Cost advantage

5. Existence of hi-tech indigenous EPC Companies – lower construction periods

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 32/59

6. Large domestic market

• Anchor customer of the various petroleum products

• Possibility of achieving economies of scale

Significant Business Opportunities for foreign players

Upstrea

m

• NELP rounds and Open acreage system

(Opportunities for providers of services –

platforms, rigs, Offshore vessels etc.)

• Redevelopment of existing fields to improve

recovery factor

• Offer of CBM blocks through Competitive bidding

route.

• Natural gas hydrate programme

• Underground coal gasification

• Coal to oil conversion

Midstrea

m/

Downstre

am

• Refining – Expansion of existing capacities, setting

up of new refineries, acquiring stakes in these

refineries

• Ethanol and Biodiesel production – cultivation of

Sugarcane and Jatropha

• Petroleum marketing – setting up of retail outlets,

new product pipelines.

• LNG imports

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 33/59

• Setting up of LNG Regasification terminals.

• Offshore Transshipment (Single Buoy Mooring)

•

Laying of cross country gas grid and transnationalgas pipelines

• City Gas Distribution including laying of CGD and

CNG networks

Initiatives to attract Foreign Direct Investment

Exploration

& Production

• Up to 100% FDI through automatic route

• Through incorporated/ unincorporated

• Joint ventures or directly

Refining

• Up to 100% FDI if set up as a private

Indian company

• Up to 26% in case of state owned

companies

Marketing • Up to 100% FDI through automatic route

Product Pipelines • Up to 100% FDI through automatic route

Natural Gas/ LNG

pipelines

• Up to 100% FDI allowed

• Approval required from Foreign Investment

Promotion Board

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 34/59

COMPANY OVERVIEW

HPCL is a Fortune 500 company, with an annual turnover of Rs. 1,08,599 Crores

and sales/income from operations of Rs 1,14,889 Crores (US$ 25,306 Millions) during

FY 2009-10, having about 20% Marketing share in India and a strong market

infrastructure. HPCL operates 2 major refineries producing a wide variety of

petroleum fuels & specialties, one in Mumbai (West Coast) of 6.5 Million Metric

Tonnes Per Annum (MMTPA) capacity and the other in Vishakhapatnam, (East

Coast) with a capacity of 8.3 MMTPA. HPCL holds an equity stake of 16.95% inMangalore Refinery & Petrochemicals Limited, a state-of-the-art refinery at Mangalore

with a capacity of 9 MMTPA. In addition, HPCL is constructing a refinery at Bhatinda, in

the state of Punjab, as a Joint venture with Mittal Energy Investments Pte. Ltd.

o HPCL also owns and operates the largest Lube Refinery in the country

producing Lube Base Oils of international standards, with a capacity

of 335 TMT. This Lube Refinery accounts for over 40% of the India's

total Lube Base Oil production.

o HPCL's vast marketing network consists of 13 Zonal offices in major cities

and 101 Regional Offices facilitated by a Supply & Distribution infrastructure

comprising Terminals, Pipeline networks, Aviation Service Stations, LPG Bottling

Plants, Inland Relay Depots & Retail Outlets, Lube and LPG Distributorships.

HPCL, over the years, has moved from strength to strength on all fronts. The

refining capacity steadily increased from 5.5 MMTPA in 1984/85 to 14.8

MMTPA presently. On the financial front, the turnover grew from Rs. 2687

Crores in 1984-85 to an impressive Rs 1, 16,428 Crores in FY 2008-09.

MISSION AND VISION OF HPCL

MISSION

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 35/59

"HPCL, along with its joint ventures, will be a fully integrated company in the

Hydrocarbons sector of exploration and production, refining and marketing;

Focusing on enhancement of productivity, quality and profitability; caring for

customers and employees; caring for environment protection and cultural

heritage.

It will also attain scale dimensions by diversifying into other energy related

Fields and by taking up transnational operations."

VISION

To be a World Class Energy Company known for caring and delighting the

customers with high quality products and innovative services across domestic

and international markets with aggressive growth and delivering superior

financial performance. The Company will be a model of excellence in meeting

social commitment, environment, health and safety norms and in employee

welfare and relations

PERFORMANCE PROFILE OF HPCL

o FINANCIAL

2009-2010 2005-2006

SALES 114,888.63 76,920.26

GROSS PROFIT 4,193.18 1,151.21

DEPREICIATION 1,164.40 690.23

INTEREST 903.75 175.88

TAX (including

differed tax)

823.61 (131.91)

PROVISION FOR FBT 0.05 11.38

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 36/59

NET PROFIT 1,301.37 405.63

DIVIDEND 406.35 101.80

TAX ON DISTRIBUTED

PROFIT

67.49 14.28

RETAINED EARNINGS 827.53 289.55

SOURCE: 58 ANNUAL REPORT OF HPCL

o WHAT CORPORATION OWES

2009-2010 2005-2006

GROSS FIXED ASSETS 24,988.37 13,479.25

DEPRECIATION 9,681.70 6,141.85

NET FIXED ASSETS 15,306.67 7,337.40

CAPITAL WORK IN

PROGRESS

3,887.59 2,363.88

INVESTMENTS : JVC 2,623.83 825.76

OTHERS 8,763.39 3,201.88

NET CURRENT

ASSETS

4,086.83 3,055.09

DEFFERD TAX

LIABILITY

(1,807.97) (1,384.44)

TOTAL 32,860.34 15,399.57

2009-2010 2005-2006

NET WORTH 11,557.97 8,735.74

SHARE CAPITAL 339.71 338.94

SHARE FORFEITURE (0.70) -

RESERVES 11,218.96 8,396.80

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 37/59

BORROWINGS 21,302.37 6,663.83

TOTAL 32,860.34 15,399.57

SOURCE: 58 ANNUAL REPORT OF HPCL

This data shows that overall sales of the company are increased from Rs.

76,920.26 crores (2005-2006) to Rs. 114,888.63 (2009-2010), the gross profit

of the company increased from Rs. 1,151.21 crores (2005-2006) to Rs.

4,193.18 (2009-2010) and the overall net profit of the company is increased

from Rs. 405.63 (2005-2006) to Rs. 1,301.37 (2009-2010) so this shows that

there is a 220.8% of increase in net profit but the overall net worth of the

company is increased from Rs. 8,735.74 (2005-2006) to Rs. 11,557.97 (2009-

2010).

Products & Services

• Refineries

• Aviation

• Bulk Fuels & Specialities

• International trade

• LPG - HP GAS

• Lubes - HP LUBES

• Retail

• Exploration & Production

• Joint Ventures

• Alternate Energy

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 38/59

JOINT VENTURES OF HPCL

In an effort to fulfill its vision and achieve its objectives, HPCL has formulated

plans for expansion, diversification and internal development

Crude Refining and Marketing of finished Petroleum products is the

core area of the Corporation. Opportunities are also being explored to access new

revenue streams, and augment downstream businesses. Accordingly, HPCL has

ventured in Upstream activities (Exploration and Production) and piped gas

distribution in major cities

12HPCL-Mittal Energy Ltd. (HMEL)

13Hindustan Colas (HINCOL)

14Prize Petroleum Company Limited

15South Asia LPG Co Pvt. Ltd. ( SALPG)

16Bhagyanagar Gas Limited (BGL)

17Aavantika Gas Limited

18Petronet India Limited (PIL)

19Petronet MHB Limited (PMHBL)

20Mangalore Refineries and Petrochemicals Limited (MRPL)

21CREDA-HPCL Biofuel Limited (CHBL)

22Sushrut Hospital and Research Centre

REFINERIES OF HPCL

Without refining, the rich resources of crude petroleum of nature would remain

latent. Value-added products from crude petroleum like petrol, diesel,

kerosene, liquefied petroleum gas, naphtha and many more products would

not be available for growth and development of a nation.

HPCL refineries upgrade the crude petroleum into many value-added products

and over 300 grades of lubricants, specialties and greases. The Lubricating

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 39/59

Oils Refinery set up at Mumbai is largest lube refinery in India. It produces

superior quality lube base oils.

The offsite product handling facilities of refineries at Mumbai andVishakhapatnam has been automated. Projects have been implemented and

facilities upgraded to produce green fuels like unleaded petrol and low sulphur

diesel. and Euro III & Euro IV works are in progress . The refineries have been

benchmarked by an international agency for various performance parameters.

Numerous awards have been bestowed on both the refineries in recognition of

the efforts in the field of energy conservation, environment and safety.

CAPACITY OF REFINERIES

3 MUMBAI REFINERY : 6.5 million metric tons per annum (MMTPA) capacity

4 VISAKH REFINERY : 8.3 million metric tons per annum (MMTPA) capacity

NEW PROJECTS

Identification and implementation of projects

for process improvement, performance,

safety and environment related concerns are

ongoing processes. The following new

projects have been undertaken by Mumbai

and Visakh Refineries to upgrade the

facilities to meet the product demand :

Facilities for Euro-III & IV grade Gasoline: Both Refineries have

executed Green Fuels & Emission Control Project (GFECP) at

Mumbai Refinery and Clean Fuel Project at Visakh Refinery to

produce Euro-III/IV gasoline with capability to produce Euro-IV MS.

Apart from meeting MS quality stipulations, the project also enabled

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 40/59

to upgrade Naphtha to Gasoline which is a value added product.

New FCCU project at Mumbai Refinery: In order to enhance the

production of value added products like LPG, MS and HSD, the

refinery is installing a new FCCU of 1.4 MMTPA capacity, which will

increase the FCCU processing capacity from the existing level of 1

MMTPA to 2.4 MMTPA. The project is expected to be completed by

the 2nd qtr of 2010-11.

Environmental facilities: Environmental facilities are being

upgraded in both the Refineries by installing Integrated Effluent

Treatment Plants to comply with air pollution limits set forth by

Pollution Control Board.

Bottom Up-gradation Projects: Mumbai Refinery has undertakenFeasibility Study of “Solvent Deasphlating Unit (SDA)” by using the

proprietary technology “Residuum Oil Supercritical Extraction

(ROSE)”. Setting up of this plant is expected to enhance the

recovery of valuable oil from the heavier fraction of the crude (VTB).

Similarly Visakh Refinery has also planned to implement the

Delayed Coker Unit (DCU) Projects for bottom up gradation.

LOBS Project: Mumbai refinery produces various grades of LOBS

with sulphur above 300 ppm and saturates below 90%, which fallunder API Gr-I category. To meet the increased demand of the same

LOBS quality in the domestic market including the API Gr-II/III

category the capacity is being uplifted. The project will help HPCL to

keep its market share of LOBS intact. The project is expected to be

completed by June 2010.

MR/VR DHT: Both Refineries are setting up DHT projects to

upgrade / produce the Euro-III / IV HSD and projects are expected to

be completed mechanically by Sept 2011. The Environmental

Clearance for DHT Projects for both the refineries, Mumbai

Refinery and Visakh Refinery has been obtained.

The Environmental Statement for the FY 2009-10 has been

submitted to Andhra Pradesh Pollution Control Board (APPCB). View

the Compliance Status of Environmental Clearance Stipulations for

DHT VR Project.

Single Point Mooring (SPM) Project at Visakh

Refinery: Visakh Refinery putting up SPM project to facilitate

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 41/59

unloading of large crude parcels of the size of around 300,000

Metric Tonnes from Very Large Crude Carriers (VLCCs). The VLCCs

cannot be berthed in the existing crude receiving jetties due to

draught restrictions. The installation of SPM will reduce the freight

cost and wharf age charges and thus will improve the economics of

the Refinery. The Environmental Clearance for this project has been

obtained. View status of Compliance of Stipulated EC Conditions.

The offshore and onshore installation work of the project has been

completed. The Environmental Statement for the financial year

(FY2009-10) has also been submitted to the Andhra Pradesh

Pollution Control Board (APPCB) .

Modernization Project for Mounded Storage System for

LPG /Propylene at Visakh Refinery: Visakh Refinery is executingthe Mounded storage system for LPG and Propylene in place of

existing LPG /Propylene Horton spheres. This is a risk mitigation

project and undertaken following the recommendations by the

external safety agencies, viz., High Power steering Committee

August, 1998, 4th Round ESA - September, 1999 etc. The Mounded

storage of LPG has proved to be safer compared to above ground

storage vessels since it provides intrinsically passive and safe

environment and eliminates the possibility of Boiling Liquid

Expanding Vapor Explosion (BLEVE) phenomenon. The approved

project cost is Rs. 124 Crores.

Corporate Social Responsibility

Environment

Mission & SHE policy

Mission

To have safe, healthy and pollution free environment in and around all our refineries,

plants, facilities and other premises at all times; instill awareness in these areas,

including relevant laws, in all employees, families and the communities in which they

carry out the activities.

Environment Policy

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 42/59

The Corporation is committed to conduct its operation in such a manner as

compatible with environment and economic development of the community. Its aim is

to create an awareness and respect for the environment, stressing on every

employee’s involvement in environmental improvement by ensuring healthy

operating practices, philosophy and training.

Health Policy

To provide a structured program to look after and promote the health of vital “Human

Resource”, essential for productivity and effectiveness of the Corporation.

Safety Policy

As an integral part of its business, HPCL believes that no work or service or activity is

so important or urgent that safety be overlooked or compromised. Safety of the

employees and public, protection of their as well as Corporation’s assets shall be

paramount. Corporation considers that safety is one of the important tools to enhance

productivity and to reduce national losses. The Corporation will constantly Endeavour

to achieve and maintain high standards of Safety in its operations.

BEYOND BUSINESS CORPORATE SOCIAL

RESPONSIBILITY

Promising whatever it takes to make a difference:

HPCL is committed to create a positive impact on the society and contribute to

socio economic development including measures for improving the quality of

life of underprivileged classes of the society. Since its inception, HPCL has tried

to follow Corporate Social Responsibility in the true sense. This sense of responsibility comes from a feeling that not every achievement of the

company is reflected in its balance sheets. The relevance that a company

achieves by virtue of its socio-economic participation surpasses the profit and

loss measurements by far. In this respect HPCL has proceeded in the truly

corporate manner, planning investments in social causes methodically,

executing the various steps with utmost care and securing distinctive

developments for the poor and the downtrodden masses. HPCL has provided

sustained value for the above mentioned investments all the time and has

contributed to the living standards of underprivileged masses.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 43/59

A compact booklet: "Bringing Smiles (2008-09)" provides details of HPCL's

various CSR activities during FY 2008-09. "Bringing Smiles (2009-10)" contains

details of CSR activities undertaken by HPCL during the FY-2009-10.

When it comes to social contribution our country never lacked goodwill among

corporate citizens but competent contributors were never in good numbers as

far as management and execution skills are concerned. HPCL has surely paved

the way in the right direction with exemplary contributions. HPCL's initiatives

have created value in the following diverse ways –

6. HPCL's initiatives have made notable differences in fields as diverse aseducation, infrastructure, welfare measures, health and hygiene,

vocational training & employment generation, training in self-reliance,amenities for the sufferers of natural disasters and environmentalprotection. The most commendable feature of the support is that HPCLhas taken innovative measures to infuse self reliance in masses tosecure long lasting improvements.

7. HPCL has categorized different projects of social relevance according tonational and regional significance. The investment has been madeaccording to solid result oriented plans with every detail of the prospecttaken into consideration.

8. The funds for different CSR projects have been consistently allocated ina transparent manner. HPCL follows an allocation process based oncomplete evaluation and benchmark standardization.

9. A Foundation has been established to take up projects of Nationalsignificance. This initiative has helped to identify the impacts of projectskeeping national interest in mind.

10. HPCL has set exemplary organizational competency in carrying outcomplex and demanding projects. The implementation process issupported by adequate checks and balances including reporting,assessment and appraisal by world class professionals.

HPCL took its first step in this direction during the year 1985-86 with a modest

budget allocation of Rs.18 Lakhs for undertaking various welfare activities for

the benefit of SC/STs and other weaker sections of the Society under the

Special Component Plan/Tribal Sub-Plan and Welfare Plan for Weaker Sections.

Later the corporation expanded the scope and allotment of such projects in

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 44/59

manifolds to uphold its "Socially Responsible Corporate citizen" Image and to

address the huge welfare expectation which the society was increasingly

resting on the corporation. Budget for the CSR projects subsequently rose

every year and larger portions of underprivileged masses were gradually

incorporated into the schemes. The corporation went beyond the parameters

of the SC/ST Component Plan to extend support. The fund has been arranged

by virtue of a policy decision to allocate certain percentage of the net profit for

each financial year to Component Plan and CSR activities and to operate the

CSR policy on Triple Bottom Line principle i.e. Economic, Social & Environment.

The Expenditure for the year 2005-06 stands at a whopping Rs.7 crores for SCP

projects and Rs. 8 crores for other CSR projects.

An "HPCL Foundation" is being set up to finance the CSR projects and also

monitor implementation of distinct schemes like AIDS prevention, vocationaltraining for unemployed youth, education of rural children, computer training,

healthcare facilities, etc.

Corporate Social Responsibility Initiatives touching lives :

The following CSR Initiatives have placed HPCL in a league of its own.

Swavalamban:

The objective of this programme is to provide free Vocational Training to

beneficiaries from low income group households. HPCL and CII have joined

hands along with M/s City & Guilds to impart training to youths and change

them into able professionals.

Navjyot:

This project aims at increasing the health index of children who have been

unfortunately displaced from slums. The project currently accommodates 3100

slum children from Bawana Resettlement Colony and imparts health care

services. Navjyot India Foundation is the official partner in the project.

Unnati:

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 45/59

The objective of this initiative is to provide Computer training to 3000 students

at Visakhapatnam through NIIT Limited.

Nanhi Kali:

The project is an initiative towards Supporting the Girl Child. Corporation hasprovided Sponsorship of the quality school education of 498 renewals of Nanhi

Kalis and additional 1400 Nanhi Kalis from various Govt. Schools from

Mehboobnagar Dist. and Paderu region in Andhra Pradesh in collaboration with

M/s KC Mahindra Education Trust.

Muskan:

This project ponders into the welfare of 100 underprivileged children, many of

them living in footpaths by providing shelter at Tuglakabad and Jahangipuri inDelhi. Education, meals, clothing, health care, vocational training etc. are

provided for them through HPCL's operating partner M/s Prayas Juvenile Aid

Centre (JAC) Society.

Suraksha:

This is an initiative towards prevention of HIV/AIDS through training/lectures

and distribution of condoms to truckers at Highway Retail Outlets. The project

operating partner is Organization for Socially Economic and Rural Development

(OSERD).

Global Warming:

Under this project, approximately 20000 school children are being educated on

causes of Global Warming at Delhi, Goa and Mumbai through our operating

partner CSRL (Centre for Social Responsibility & Leadership).

A Corporate approach towards development:

The current projects bear the mark of a well thought of corporate mindset .To

summarise HPCL's approach towards social welfare we have to mention the

following points-

5. Strategic approach to every issue is the key to HPCL's success.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 46/59

6. HPCL has meticulously secured the input-output-outcomebalance.

7. HPCL has underlined the social problems accurately and has

taken result oriented initiatives.

8. The advanced planning regarding allocation of resource andcorrect evaluation of performance against benchmark haverepresented organizational competence.

The success of HPCL lies in the maintenance of social responsibilities amid profit

driven and competitive business environment. Apart from directly contributing to the

betterment of weaker sections of the society, HPCL has been associated with

healthcare, education, environmental protection, agricultural development, ruralreconstruction, water supply development etc. It can be said that the corporation has

touched lives qualitatively acting as a corporate social ambassador. HPCL has always

seen itself as a contributing participant in India's overall development. The

corporation has stood the test of time being true to citizen's expectations.

Evolution of Pricing in Petroleum Industry

Historical Perspective

The development of petrol-retail sector in India has witnessed three distinct

phases:

• Period of dominance of multinational companies

• Advent of public sector, its growth in co-existence with these

transnational companies

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 47/59

• Marketing by the wholly government-owned companies and the

fulfillment of socio-economic objectives

At the time of the independence, the marketing and retailing of petroleum

products was in the hands of the private companies like Catlex, Esso, Shell etc.

Later the government gradually exercised control through public sector

companies. The second phase started with actions taken in pursuance of the

Industrial Policy Resolution, 1956 to promote growth of the vital petroleum

sector under the state control. Eventually, IOC was formed in 1959, IBP was

acquired in 1970 and HPC came into existence in 1974 and BPC in 1976.

In the third phase, the experience gained by the government during thesecond phase and the socio- economic factors encouraged it to go ahead for

acquiring the assets of all multinational companies operating in the country. In

1981, the entire oil industry was truly in the government fold.

A new era of planned development in consonance with national priorities under

the overall direction of the government thus began in the oil sector. From the

state of the cutthroat competition in marketing and distribution, the PSUs had

to quickly adapt to the changed scenario. The assets of the oil company interms of infrastructure facilities were now the national assets. The important

area of concern was their optimum utilization.

Administered Price Mechanism

The country has traditionally operated under an Administered Pricing

Mechanism for petroleum products. This system is based on the retention price

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 48/59

concept under which the oil refineries, oil marketing companies and the

pipelines are compensated for operating costs and are assured a return of 12%

post-tax on networth. Under this concept, a fixed level of profitability for the oil

companies is ensured subject to their achieving their specified capacity

utilisation. Upstream companies, namely ONGC,oil and GAIL, are also under

retention price concept and are assured a fixed return.

The administered pricing pilicy of petroleum products ensures that products

used by the vulnerable sections of the society, like kerosene, or products used

as feedstocks for production of fertilizer, like naphtha, may be sold at

subsidized prices.

Gradually, the Government of India is moving away from the administered

pricing regime to market-determined, tariff-based pricing. Free imports are

permitted for almost all petroleum products except petrol and diesel. Free

imports are permitted for almost all petroleum products except petrol and

diesel. Free marketing of imported kerosene, LPG and lubricants by private

parties is permitted. It is contemplated that in a phased manner, all

administered price products will be taken out of the administered pricing

regime and the system will be replaced by a progressive tariff regime in order

to provide a level playing field for new investments in a free and competitive

market

Up to 1939, there were no controls whatsoever on the pricing of the petroleum

products. Between 1939 and 1948, the oil companies themselves maintained

pool accounts for major products without any intervention by the government.

In 1948, an attempt was made to regulate prices through Valued Stock

account procedure. Under this procedure realization of oil companies was

restricted to the import parity price of finished goods, plus excise duties/local

taxes/ dealer margins and agreed marketing margins of each of the refineries.

Any excess realization was surrendered to the Government.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 49/59

Administered Pricing Policy for Petroleum products

The pricing of petroleum products in India is governed by the administered

pricing mechanism based on accepted recommendations of oil pricingcommittee appointed from time to time.

Principles followed to carry out pricing through APM: Fixation of selling price of

petroleum products is done under the APM of government of India \. The

criteria followed for fixation are:

• Products which are essential for common man are priced under APM

• High volume products should be administered under the pricing system

in overall public interest

• Petroleum products are divided into the following categories for the

purpose of APM:

The categories are :-

1. Formula Products (viz. MS, HSD, SKO, etc) are the products whose

basic ceiling selling prices are fixed.

2. Other products (Benzene, toluene, lubes, etc) whose prices are

determined by market forces or through negotiations between oil

companies and bulk industry consumers.

• Each refinery/pipeline/marketing function is considered separate pricing

centre

• The administered pricing concept is based on the retention concept

which ensures a return on capital employed. Capital employed,

comprising of net worth and borrowings. Return is allowed at 12% net of

tax on net worth at actual interest rates on borrowings.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 50/59

• Operating cost is allowed on normative basis. Variations for major factors

like long term settlement with employees (LTS). Government levies, etc

are compensated separately.

• Returns at the prescribed levels are available to the oil companies if they

achieve the prescribed parameters, viz.

1. Production pattern

2. Sales

3. Fuel and Loss

4. Normative working capital

5. Operating Cost

• The crude oil cost forms a bulk of total cost is insulated from the

fluctuations of international prices by means of a pool accounts

mechanism so that the net cost to the refinery is independent of whether

it is processing imported or indigenous crudes.

Primary Pricing Point

For the purpose of uniformity in consumer pricing (excluding freight and local

levies), pricing points have been fixed for petroleum products. Each pricing

point has an assingned pricing zone. The producer’s location (refinery) is fixedat primary point. The price of petroleum products (controlled) at all primary

points will be uniform. The price at locations within the pricing zone assigned

to a pricing point will be the ex-storage point price plus cost of transportation

to that location. Currently all the refineries are primary pricing points for

controlled products.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 51/59

Secondary Pricing Point

While ex-storage will be the price at a primary point, the price at secondary

pricing point will be arrived at the element of transportation cost there on a

predetermined basis. Secondary pricing points are the depots attached to

particular refinery.

Import Parity System

The APM continued through 1970s, 1980s and 1990s. But the explosive growth

in the late 1990s required the government to call for funds from private and

international investors. The ability of oil companies to generate investable

surpluses was reduced considerably by the APM which allowed returns on the

depreciated net fixed assets. Accordingly, the Government, in 1995, set up an

industry study group to prepare the blue print of the deregulation and tariff

reforms required in the oil sector. The report of this Study Group formed the

main input for the strategic Planning Group on Restructuring of Indian oil

Industry otherwise known as the “R” group headed by the , then Secretary

P&NG, Dr. Vijay Kellar. The “R” group submitted its report in September, 1996,

recommending dismantling of the APM for the following reasons:-

• Cost Plus compensation did not provide strong incentive for cost

reduction thereby breeding inefficiencies.

• Absence of internationally competitive petroleum sector in the context of global economy.

• With the entry of private sector, gold plating of the costs would be

encouraged.

• Wide distortion in consumer prices due to subsidies/ cross subsidies.

• Adverse impact on oil companies due to huge deficits in Oil Pool

Accounts as price revision was not timely.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 52/59

The Group’s recommendations were approved by the Government in principle

in September, 1997 and further action was started. The Government appointed

an “Expert Technical Group (ETG)” to study the phasing and tariff structure of

the oil sector. The recommendations of this group were notified in November,

1997. The ETG headed by Mr. Nirmal Singh, Joint Secretary Refineries,

MOP&NG recommended the following:-

• There should be a phased deregulation of the sector spread over a

period of four to five year, culminating in total deregulation by 1.4.2002

•

The first phase should encompass full deregulation of upstream/refineries and partial deregulation of marketing sectors,

• The customs tariff, structure, which provided for a negative duty

protection needs to be amended so as to attract investments to the

sector.

• Changes in tariff structure may be done over the transition phase,

keeping in mind the equilibrium to be maintained between the

Governments’ revenue needs, necessity to keep consumers prices low

and the need to increase the profitability of the companies.

• Subsidies should be phases out gradually to within acceptable limits

which will be provided through budget.

• In the end, on deregulation, the duties should be so positioned that the

tariff protection becomes 25% of the value addition while the

Government revenue is maintained.

Accordingly in the first phase, effective 1.4.1998, the APM was dismantled for

the upstream and refining sector and a partial deregulation took place for the

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 53/59

marketing sector. Subsequently, effective 1.4.2002, the Government

announced complete dismantling of APM.

The dismantling of APM gave rise to establishment of import parity mechanism

for calculation of petroleum prices.

Import Parity is a pricing policy adopted by suppliers of a good for their sales

to domestic customers; according to which price is set at the opportunity cost

of a unit of an imported substituted good. As such, price is set equal to the

world price converted into exchange rated plus any transport, tariff and other

costs the customer would bear if importing.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 54/59

A VIABLE AND SUSTAINABLE SYSTEM OF PRICING OF

PETROLEUM PRODUCTS

PETROL

Petrol is largely an item of final consumption. Its price, therefore, has a

very small impact on inflation due to forward linkages. The average

annual use of petrol per vehicle is given in the following table

Average Annual Consumption of Fuel by Class of Vehicles

Type

of

Average

DistanceCovered

Fuel

Efficiency

Litres/Vehicle/ Year

MonthlyFuel

Cost atprice on

Two Wheelers

(Petrol)

6300

(10000)

73.0 86 320

ThreeWheelers

35000

(40000)

34.0 1,029 3835

Cars 8000 13.5 593 2210

Cars 8000 14.0 571 1566

MPV 7800 8.7 897 2461

Bus 55000 4.1 13,415 36,802

Heavy Trucks 55000 3.6 15,278 41,913

Light Trucks 20000 4.5 4,415 12,112

.

Source: ’Residential and Transport Energy use in India: Past Trend and Future Outlook’ by Ernest

Orlando Lawrence Berkeley National Laboratory, USA, January 2009

Figures in parentheses are estimates for Delhi, taken from the report of CPCB (2000)

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 55/59

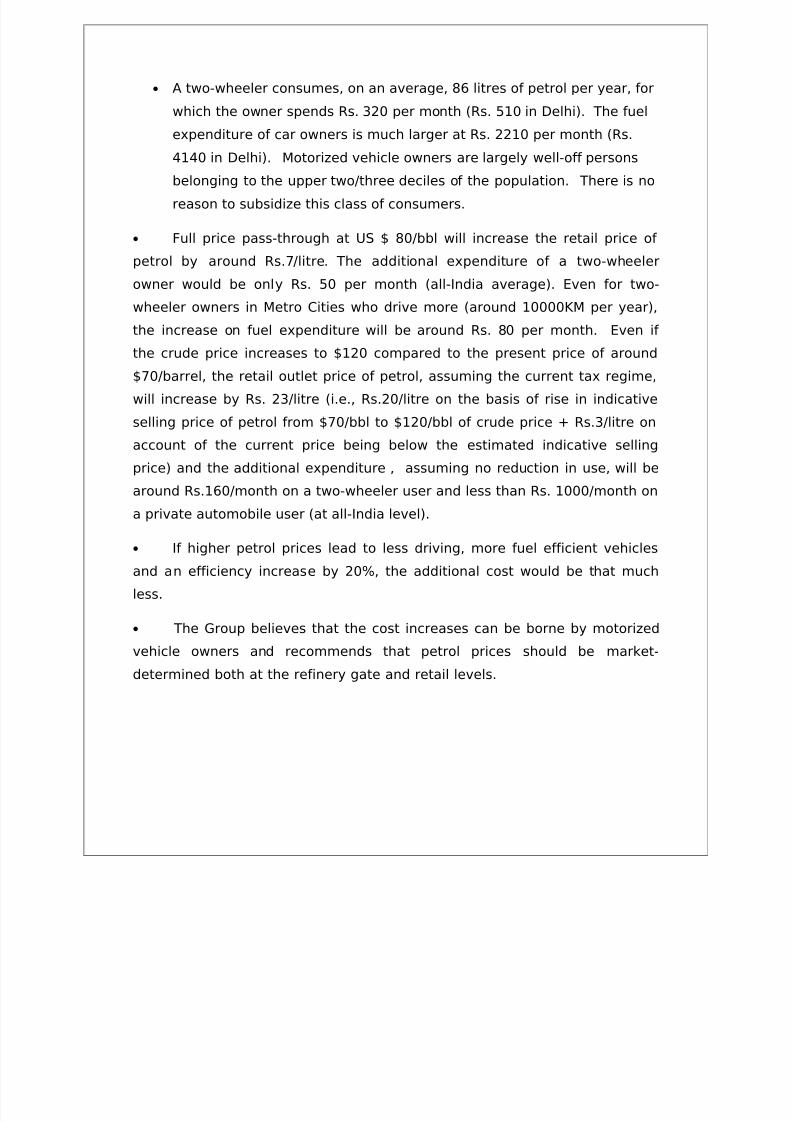

• A two-wheeler consumes, on an average, 86 litres of petrol per year, for

which the owner spends Rs. 320 per month (Rs. 510 in Delhi). The fuel

expenditure of car owners is much larger at Rs. 2210 per month (Rs.

4140 in Delhi). Motorized vehicle owners are largely well-off persons

belonging to the upper two/three deciles of the population. There is no

reason to subsidize this class of consumers.

• Full price pass-through at US $ 80/bbl will increase the retail price of

petrol by around Rs.7/litre. The additional expenditure of a two-wheeler

owner would be only Rs. 50 per month (all-India average). Even for two-

wheeler owners in Metro Cities who drive more (around 10000KM per year),

the increase on fuel expenditure will be around Rs. 80 per month. Even if the crude price increases to $120 compared to the present price of around

$70/barrel, the retail outlet price of petrol, assuming the current tax regime,

will increase by Rs. 23/litre (i.e., Rs.20/litre on the basis of rise in indicative

selling price of petrol from $70/bbl to $120/bbl of crude price + Rs.3/litre on

account of the current price being below the estimated indicative selling

price) and the additional expenditure , assuming no reduction in use, will be

around Rs.160/month on a two-wheeler user and less than Rs. 1000/month on

a private automobile user (at all-India level).

• If higher petrol prices lead to less driving, more fuel efficient vehicles

and an efficiency increase by 20%, the additional cost would be that much

less.

• The Group believes that the cost increases can be borne by motorized

vehicle owners and recommends that petrol prices should be market-

determined both at the refinery gate and retail levels.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 56/59

TAXATION

At present there is zero custom duty on crude oil, domestic LPG and PDS

kerosene; 2.5 percent custom duty on Motor Spirit and diesel and 5 percent

custom duty on other petroleum products. The excise duty on domestic LPG

and PDS kerosene has already been reduced to zero. The basic excise duty on

Motor Spirit and Diesel (other than branded) has also been reduced to Rs.13.35 per litre on Motor Spirit and Rs. 3.60 per litre on diesel. The Group has

already recommended an additional excise duty on diesel-driven vehicle

corresponding to the differential tax in the form of higher excise on petrol

consumed by average petrol-driven car, which will act as the equaliser. There

is also the cascading impact of taxes such as entry tax/octroi imposed by

State Governments on crude oil, petrol and diesel. Almost 20 percent of the

price build up of petroleum products is attributed to state taxes. This needs

to be rationalised in order to achieve faster adaptation of domestic price of

petrol and diesel to international crude price.

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 57/59

RECOMMENDATIONS:•

India’s imports of oil are increasing. Our import dependence hasreached 80 per cent and is likely to keep growing. At the same time 2008 saw

an unprecedented rise in oil price on the world market. Oil price volatility has

also increased. Though future oil prices are difficult to predict, they are

generally expected to rise. Given our increasing dependence on imports,

domestic prices of petroleum products have to reflect the international prices.

• The Government has not permitted public sector oil marketing

companies to pass global prices to domestic consumers. We have examinedthe impact of the formula-based prescriptive pricing of major petroleum

products devised by the Government from time to time, particularly since

2002. The present system of price control on petrol and diesel in particular

has resulted in major imbalances in the consumption pattern of petroleum

products in the country, and has put undue stress on finances of the PSU oil

marketing companies as well as of the Government. It has also led to

8/3/2019 Pricing Structure

http://slidepdf.com/reader/full/pricing-structure 58/59

withdrawal of private sector oil marketing companies from the market. This

has affected competition in the domestic petroleum product market.

• The petrol is largely an item of final consumption. An analysis of the

trend of petrol consumption by the automobile owners reveals that increase

in prices of petrol

8/3/2019 Pricing Structure