Embed Size (px)

Citation preview

www.pwc.com/globalmoneytree

www.pwc.in

PricewaterhouseCoopers India Pvt Ltd

MoneyTreeTM India Report Q3 2016

Technology Institute

This special report provides summary results of Q3 ’15, Q2 ’16, and Q3 ’16.

Data provided by Venture Intelligence

PwC MoneyTree India – Q3 2016 2

Table of contents

1. Overview 3

2. Analysis of PE investments 4

Investments by industry 5

Investments by stage of development 7

Investments by region Q3 ’15, Q2 ’16 and Q3 ’16 8

Top 20 PE deals Q3 ’16 9

3. Analysis of PE exits 10

Exits by industry 11

Exits by type Q2 ’15, Q1 ’16 and Q2 ’16 12

Top five PE exits Q3 ’16 13

4. Active PE firms 14

5. Sector focus – IT & ITeS sector 15

Total PE investments 16

Investments by stage of development 18

Investments by region 19

Investments by subsector 20

PE exits in the sector 21

Definitions 22

PwC MoneyTree India – Q3 2016 3

1. Overview

The first nine months of 2016 witnessed 12.7 billion USD worth of private equity investments across 473 deals, as compared to 15.9 billion USD across 628 deals in the first nine months of 2015, indicating a 20% decline in deal value and a 25% decline in deal volume.

As compared to the second quarter of 2016, despite a slight decline in the number of deals, deal values were up by 4%, with investments worth 4.3 billion USD across 131 deals as compared to 4.2 billion USD across 156 deals in Q3. Late and Growth stage investments accounted for the majority of funding this quarter, contributing 84% in terms of value.

Investments in this quarter were dominated by the Banking, financial services & insurance (BFSI) sector which accounted for 45% of the total investment value, with 1.9 billion USD across 20 deals. The Information technology & IT-enabled services (IT & ITeS) sector was the second largest sector in terms of value with 1.2 billion USD invested across 68 deals. Healthcare & life sciences and Engineering & construction were other sectors that witnessed increased activity and could attract further investment in the last quarter of the year.

Exit activity picked up considerably as compared to the previous quarter, with 2.3 billion USD across 63 exits. Strategic sales accounted for 62% of the total exit value; an almost four-fold increase as compared to the previous quarter. This quarter also witnessed four private-equity-backed IPOs.

The IT & ITeS sector witnessed significant consolidation, with exits valued at 0.8 billion USD, the majority being strategic sales. This was closely followed by the Healthcare & life sciences sector with o.7 billion USD across 10 exits.

We expect some volatility in the near future as investors assess the implications of the recently concluded US Presidential elections, US Federal Bank stance on rates, and the possibility of the Trans Pacific Partnership being implemented. Having said so, private equity firms continue to express interest in India on account of government reforms and strong macroeconomic indicators. The long-term story for India remains strong with rapid reforms being introduced by the current government. There may be a pause created by the demonetisation scheme introduced by the government. Investors will be in wait-and-watch mode to digest the sectoral impact of the scheme and thereafter we expect capital inflows to be strong.

Sanjeev Krishan Leader, Private Equity and Transaction Services PwC India

PwC MoneyTree India – Q3 2016 4

2. Analysis of PE investments

Total equity investments in PE-backed companies

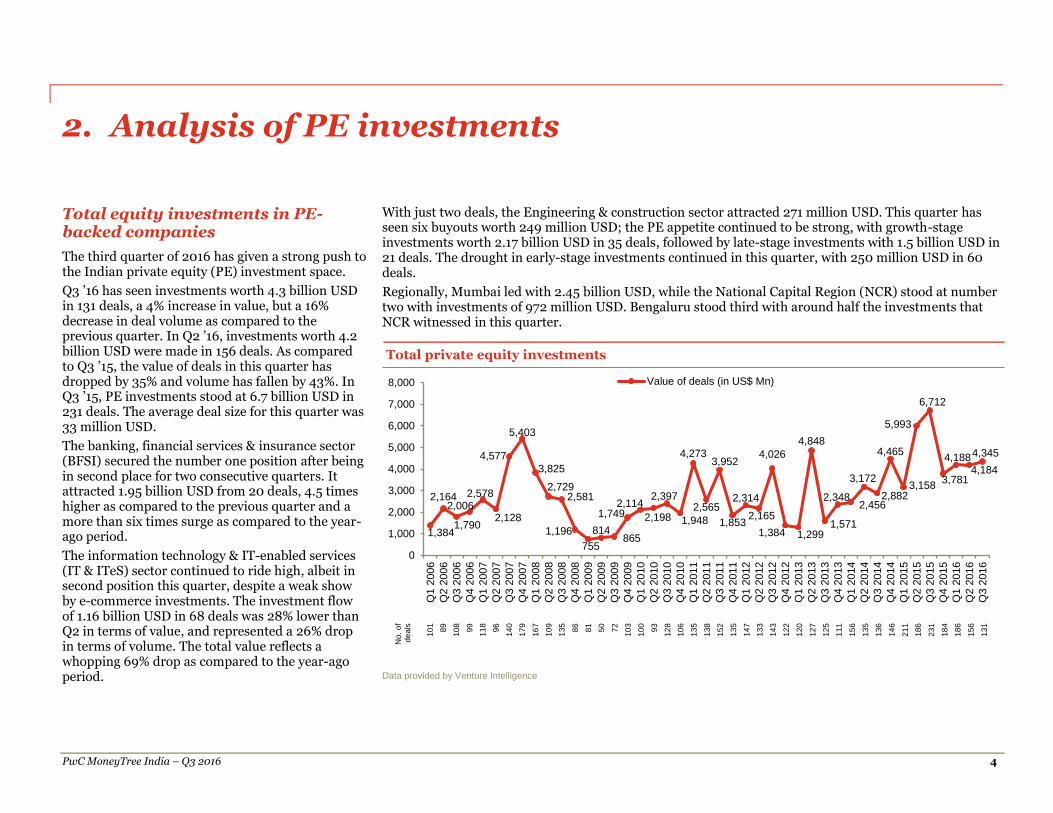

The third quarter of 2016 has given a strong push to the Indian private equity (PE) investment space.

Q3 ’16 has seen investments worth 4.3 billion USD in 131 deals, a 4% increase in value, but a 16% decrease in deal volume as compared to the previous quarter. In Q2 ’16, investments worth 4.2 billion USD were made in 156 deals. As compared to Q3 ’15, the value of deals in this quarter has dropped by 35% and volume has fallen by 43%. In Q3 ’15, PE investments stood at 6.7 billion USD in 231 deals. The average deal size for this quarter was 33 million USD.

The banking, financial services & insurance sector (BFSI) secured the number one position after being in second place for two consecutive quarters. It attracted 1.95 billion USD from 20 deals, 4.5 times higher as compared to the previous quarter and a more than six times surge as compared to the year-ago period.

The information technology & IT-enabled services (IT & ITeS) sector continued to ride high, albeit in second position this quarter, despite a weak show by e-commerce investments. The investment flow of 1.16 billion USD in 68 deals was 28% lower than Q2 in terms of value, and represented a 26% drop in terms of volume. The total value reflects a whopping 69% drop as compared to the year-ago period.

With just two deals, the Engineering & construction sector attracted 271 million USD. This quarter has seen six buyouts worth 249 million USD; the PE appetite continued to be strong, with growth-stage investments worth 2.17 billion USD in 35 deals, followed by late-stage investments with 1.5 billion USD in 21 deals. The drought in early-stage investments continued in this quarter, with 250 million USD in 60 deals.

Regionally, Mumbai led with 2.45 billion USD, while the National Capital Region (NCR) stood at number two with investments of 972 million USD. Bengaluru stood third with around half the investments that NCR witnessed in this quarter.

Total private equity investments

No.

of

de

als

10

1

89

10

8

99

11

8

96

14

0

17

9

16

7

10

9

13

5

86

81

50

72

10

3

10

0

93

12

8

10

6

13

5

13

8

15

2

13

5

14

7

13

3

14

3

12

2

12

0

12

7

12

5

11

1

15

6

13

5

13

6

14

6

21

1

18

6

23

1

18

4

18

6

15

6

13

1

Data provided by Venture Intelligence

1,384

2,164

1,790

2,0062,578

2,128

4,577

5,403

3,825

2,7292,581

1,196

755

814865

1,7492,114

2,198

2,397

1,948

4,273

2,565

3,952

1,853

2,314

2,165

4,026

1,384 1,299

4,848

1,571

2,3482,456

3,172

2,882

4,465

3,158

5,993

6,712

3,781

4,1884,184

4,345

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Q3 2

016

Value of deals (in US$ Mn)

Analysis of private equity investments

PwC MoneyTree India – Q3 2016 5

Investments by industry Q3 ’15, Q2 ’16 and Q3 ’16

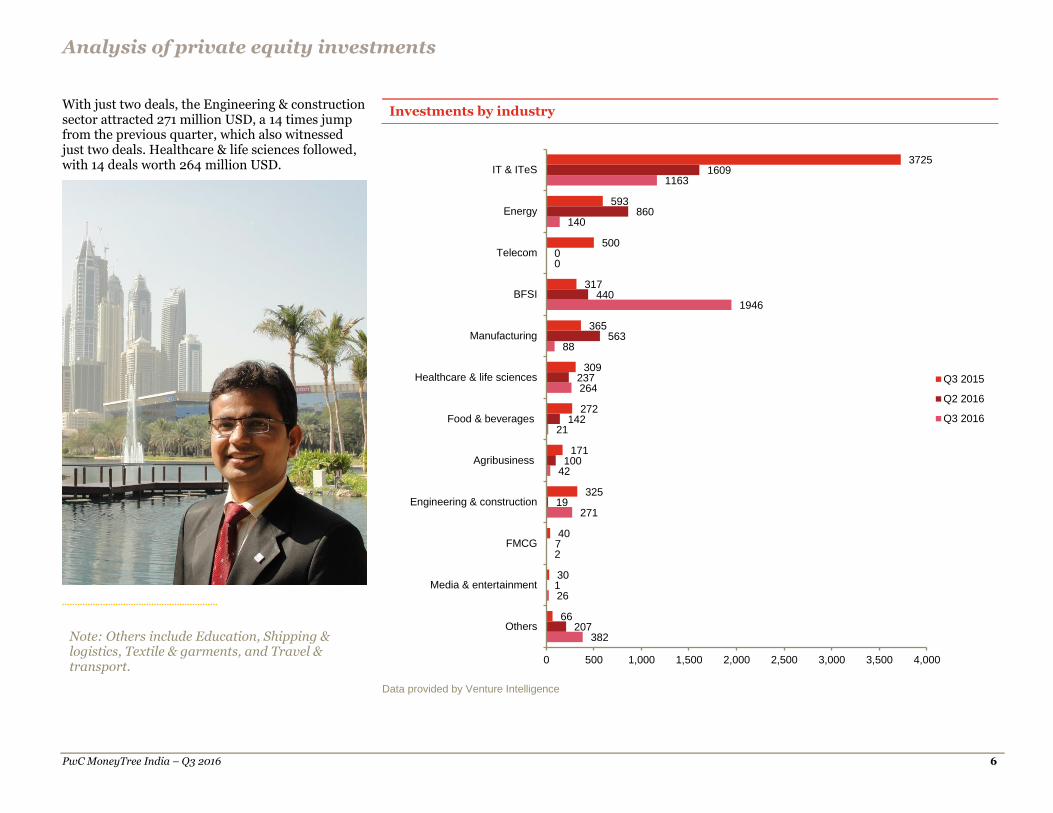

The BFSI sector dominated this quarter, a change from the dominance of the IT & ITeS sector in the second quarter of the year. In just 20 deals, this sector attracted 1.94 billion USD, which is 4.5 times higher than the 440 million USD in 13 deals it attracted in the previous quarter and more than six times higher than the 317 million USD in nine deals it received in Q3 ’15.

The IT & ITeS sector occupied the number two position and witnessed a reasonably good deal flow in this quarter, with 68 deals worth 1.16 billion USD compared to 92 deals worth 1.6 billion USD in the previous quarter, but much lower than the 3.72 billion USD in 135 deals seen in Q3 '15.

“BFSI has seen significantly higher investment quarter on quarter even as overall investment flow is lower. We expect that distressed asset players, fintechs, real estate funds and even non-banking financial companies (NBFCs) may see continuing investment despite global and domestic head winds for Indian deals in the next few quarters.”

Bharti Gupta Ramola Leader, Financial Services PwC India

“This quarter saw two major developments, the US Elections and the demonetisation scheme by the Indian government, which might have significant long-term impact on the Technology and eCommerce industry. In terms of activity in the IT & ITeS space, deals continue to happen, albeit at a slower pace. This year has seen the startup market undergoing a valuation correction, and several startups have begun controlling their burn rate and are focusing on strong unit economics. The Fintech space saw several marquee investments this quarter and we saw the addition of another Indian company in the list of Unicorn startups, when Hike Messenger raised USD 175 million, at a valuation of 1.4 billion USD.”

Sandeep Ladda Leader, Technology PwC India

Analysis of private equity investments

PwC MoneyTree India – Q3 2016 6

With just two deals, the Engineering & construction sector attracted 271 million USD, a 14 times jump from the previous quarter, which also witnessed just two deals. Healthcare & life sciences followed, with 14 deals worth 264 million USD.

Investments by industry

Data provided by Venture Intelligence

382

26

2

271

42

21

264

88

1946

0

140

1163

207

1

7

19

100

142

237

563

440

0

860

1609

66

30

40

325

171

272

309

365

317

500

593

3725

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Others

Media & entertainment

FMCG

Engineering & construction

Agribusiness

Food & beverages

Healthcare & life sciences

Manufacturing

BFSI

Telecom

Energy

IT & ITeS

Q3 2015

Q2 2016

Q3 2016

Note: Others include Education, Shipping & logistics, Textile & garments, and Travel & transport.

Analysis of private equity investments

PwC MoneyTree India – Q3 2016 7

Investments by stage of development Q3 ’15, Q2 ’16 and Q3 ’16

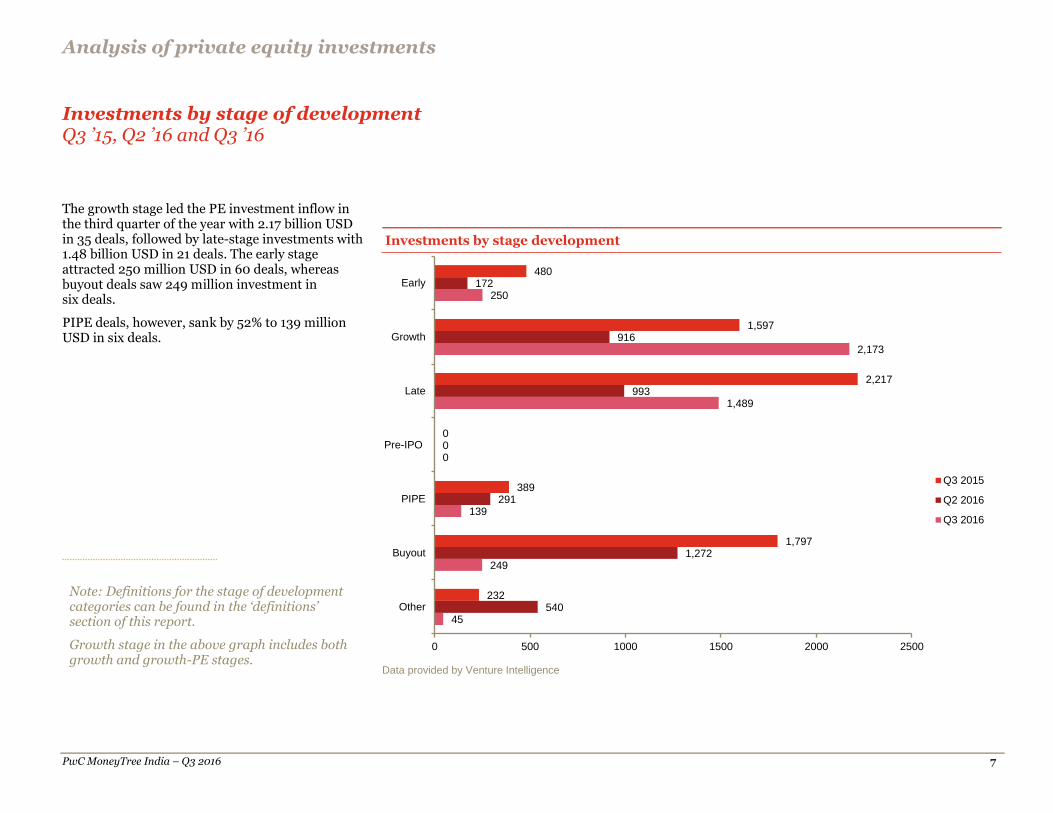

The growth stage led the PE investment inflow in the third quarter of the year with 2.17 billion USD in 35 deals, followed by late-stage investments with 1.48 billion USD in 21 deals. The early stage attracted 250 million USD in 60 deals, whereas buyout deals saw 249 million investment in six deals.

PIPE deals, however, sank by 52% to 139 million USD in six deals.

Data provided by Venture Intelligence

45

249

139

0

1,489

2,173

250

540

1,272

291

0

993

916

172

232

1,797

389

0

2,217

1,597

480

0 500 1000 1500 2000 2500

Other

Buyout

PIPE

Pre-IPO

Late

Growth

Early

Q3 2015

Q2 2016

Q3 2016

Investments by stage development

Note: Definitions for the stage of development categories can be found in the ‘definitions’ section of this report.

Growth stage in the above graph includes both growth and growth-PE stages.

Analysis of private equity investments

PwC MoneyTree India – Q3 2016 8

Investments by region Q3 ’15, Q2 ’16 and Q3 ’16

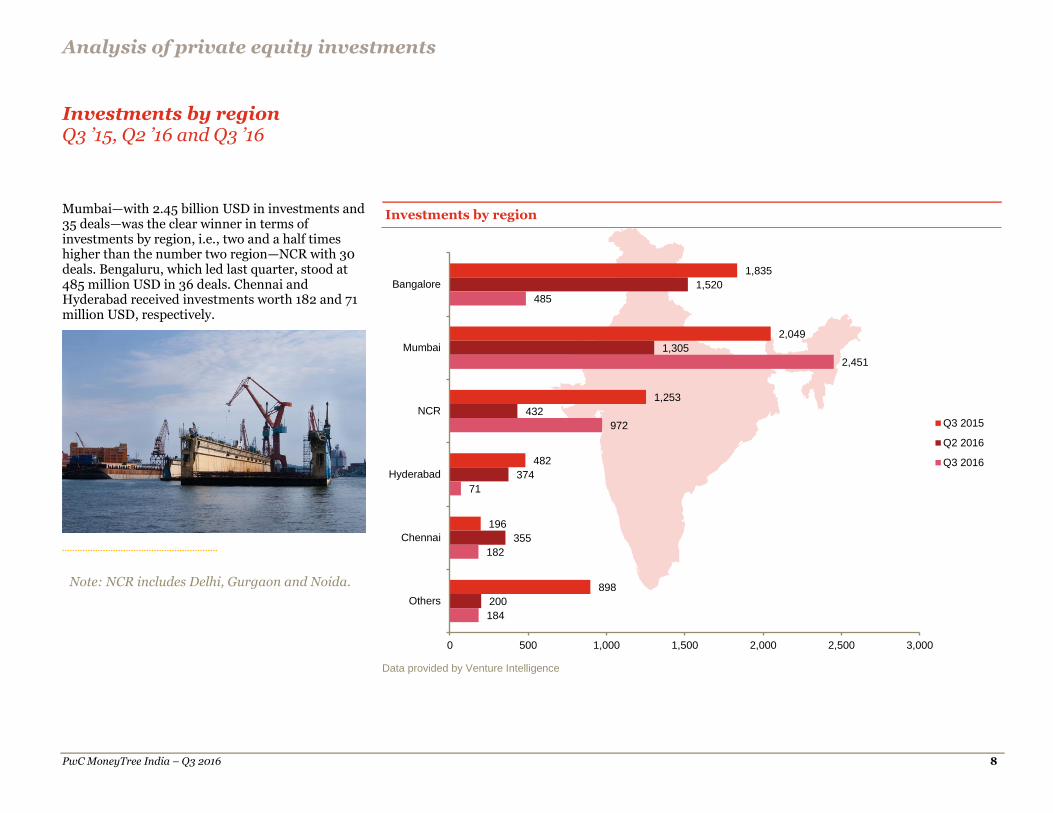

Mumbai—with 2.45 billion USD in investments and 35 deals—was the clear winner in terms of investments by region, i.e., two and a half times higher than the number two region—NCR with 30 deals. Bengaluru, which led last quarter, stood at 485 million USD in 36 deals. Chennai and Hyderabad received investments worth 182 and 71 million USD, respectively.

Data provided by Venture Intelligence

1,835

2,049

1,253

482

196

898

1,520

1,305

432

374

355

200

485

2,451

972

71

182

184

0 500 1,000 1,500 2,000 2,500 3,000

Bangalore

Mumbai

NCR

Hyderabad

Chennai

Others

Q3 2015

Q2 2016

Q3 2016

Investments by region

Note: NCR includes Delhi, Gurgaon and Noida.

Analysis of private equity investments

PwC MoneyTree India – Q3 2016 9

Top 20 PE deals Q3 ’16

The top 20 deals comprised 72% of the total deal value in Q3 ’16. The top five deals together accounted for 44% of the total deal value. The average deal value for this quarter was 33 million USD.

Top 20 PE deals in Q3 2016

Company

Industry

Investors

Amount

(US$M)

SBI ARC* BFSI Brookfield 1045

One97 Communications IT & ITeS SAIF, Alibaba, MediaTek 300

Essel Highways Engg. & construction Goldman Sachs 250

Hike IT & ITeS Tiger Global, Tencent, Foxconn 175

India Infoline Finance BFSI CDC Group 149

TCNS Clothing Company Textiles & garments TA Associates 140

National Stock Exchange BFSI ChrysCapital 135

Hero Future Energies Energy IFC 125

Stellar Value Chain Shipping & logistics Warburg Pincus 125

Hero FinCorp BFSI ChrysCapital, Credit Suisse 105

Indecomm Global Services IT & ITeS Capital Square Partners 90

Bookmyshow IT & ITeS SAIF, Accel India, Capital18, Accel USA, Stripes Group 82

InCred Finance BFSI IDFC PE, Alpha Capital, Others 75

Privi Organics Manufacturing Fairbridge Capital 55

Ratnakar Bank BFSI ChrysCapital, Others 54

Druva Software IT & ITeS Sequoia Capital India, Nexus Venture Partners, Tenaya Capital, Others

51

Mobikwik IT & ITeS Sequoia Capital India, Tree Line Asia Master Fund, MediaTek, GMO Venture Partners, Others

50

Byjus Classes Education Sequoia Capital India, Lightspeed Ventures, Sofina, Others

50

Star Health and Allied Insurance Company

BFSI ICICI Venture, Apis Partners 47

Encube Ethicals Healthcare & life sciences Multiples PE 45

*SBI and Brookfield Asset Management Inc. propose to launch a joint venture fund to which Brookfield has agreed to commit 1

billion USD to purchase distressed assets.

Data provided by Venture Intelligence

PwC MoneyTree India – Q3 2016 10

3. Analysis of PE exits

Total PE exits Q3 ’16

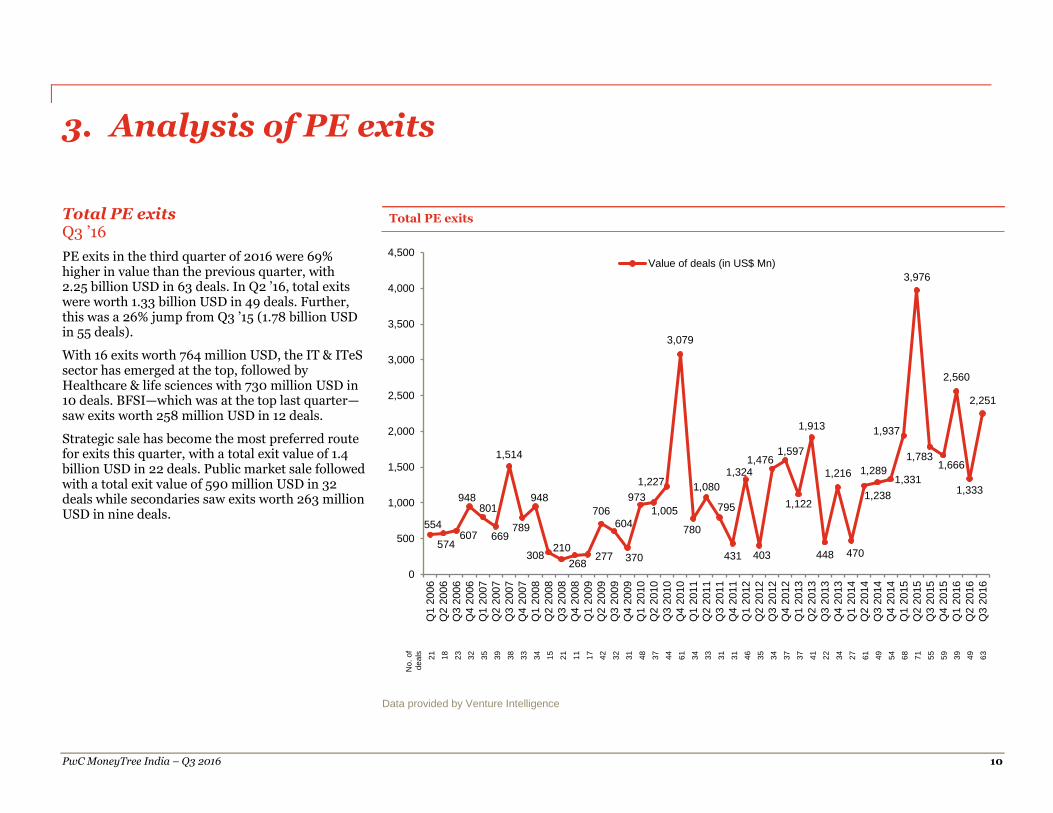

PE exits in the third quarter of 2016 were 69% higher in value than the previous quarter, with 2.25 billion USD in 63 deals. In Q2 ’16, total exits were worth 1.33 billion USD in 49 deals. Further, this was a 26% jump from Q3 ’15 (1.78 billion USD in 55 deals).

With 16 exits worth 764 million USD, the IT & ITeS sector has emerged at the top, followed by Healthcare & life sciences with 730 million USD in 10 deals. BFSI—which was at the top last quarter—saw exits worth 258 million USD in 12 deals.

Strategic sale has become the most preferred route for exits this quarter, with a total exit value of 1.4 billion USD in 22 deals. Public market sale followed with a total exit value of 590 million USD in 32 deals while secondaries saw exits worth 263 million USD in nine deals.

Total PE exits

No.

of

de

als

21

18

23

32

35

39

38

33

34

15

21

11

17

42

32

31

48

37

44

61

34

33

31

31

46

35

34

37

37

41

22

34

27

61

49

54

68

71

55

59

39

49

63

Data provided by Venture Intelligence

554

574607

948801

669

1,514

789

948

308210

268277

706

604

370

973

1,005

1,227

3,079

780

1,080

795

431

1,324

403

1,4761,597

1,122

1,913

448

1,216

470

1,238

1,2891,331

1,937

3,976

1,7831,666

2,560

1,333

2,251

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Q3 2

016

Value of deals (in US$ Mn)

Analysis of PE exits

PwC MoneyTree India – Q3 2016 11

Exits by industry Q3 ’15, Q2 ’16 and Q3 ’16

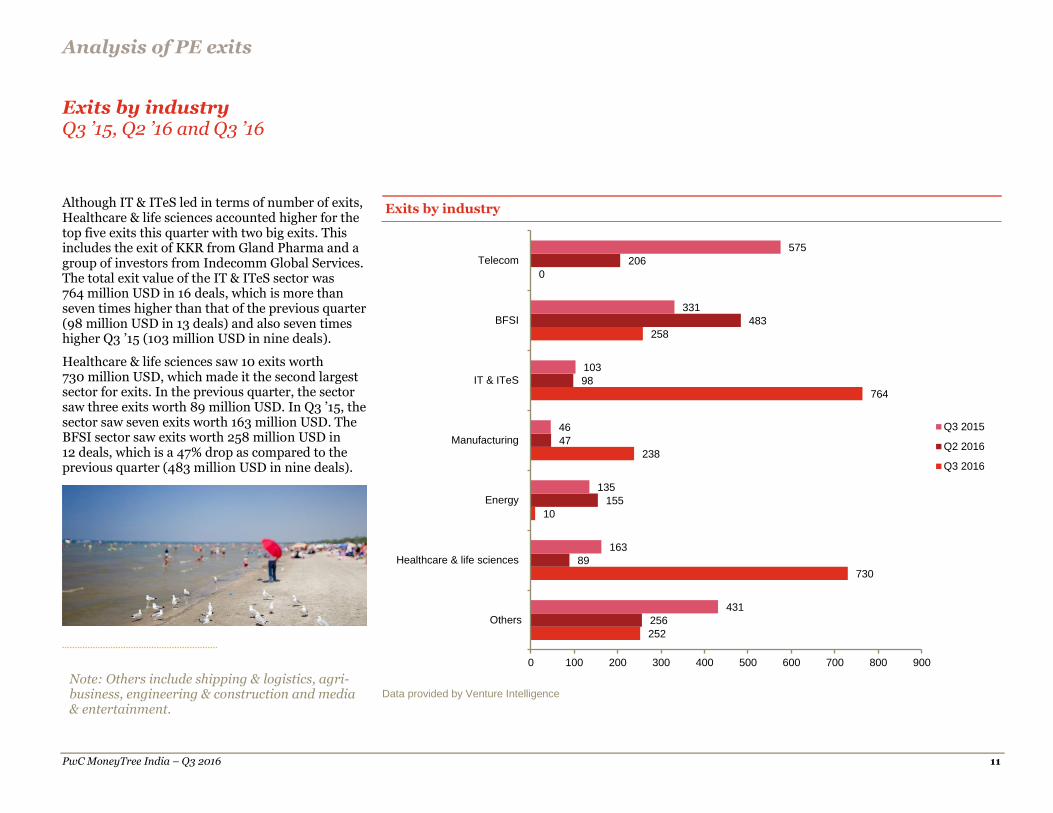

Although IT & ITeS led in terms of number of exits, Healthcare & life sciences accounted higher for the top five exits this quarter with two big exits. This includes the exit of KKR from Gland Pharma and a group of investors from Indecomm Global Services. The total exit value of the IT & ITeS sector was 764 million USD in 16 deals, which is more than seven times higher than that of the previous quarter (98 million USD in 13 deals) and also seven times higher Q3 ’15 (103 million USD in nine deals).

Healthcare & life sciences saw 10 exits worth 730 million USD, which made it the second largest sector for exits. In the previous quarter, the sector saw three exits worth 89 million USD. In Q3 ’15, the sector saw seven exits worth 163 million USD. The BFSI sector saw exits worth 258 million USD in 12 deals, which is a 47% drop as compared to the previous quarter (483 million USD in nine deals).

Data provided by Venture Intelligence

252

730

10

238

764

258

0

256

89

155

47

98

483

206

431

163

135

46

103

331

575

0 100 200 300 400 500 600 700 800 900

Others

Healthcare & life sciences

Energy

Manufacturing

IT & ITeS

BFSI

Telecom

Q3 2015

Q2 2016

Q3 2016

Exits by industry

Note: Others include shipping & logistics, agri-business, engineering & construction and media & entertainment.

Analysis of PE exits

PwC MoneyTree India – Q3 2016 12

Exits by type Q2 ’15, Q1 ’16 and Q2 ’16

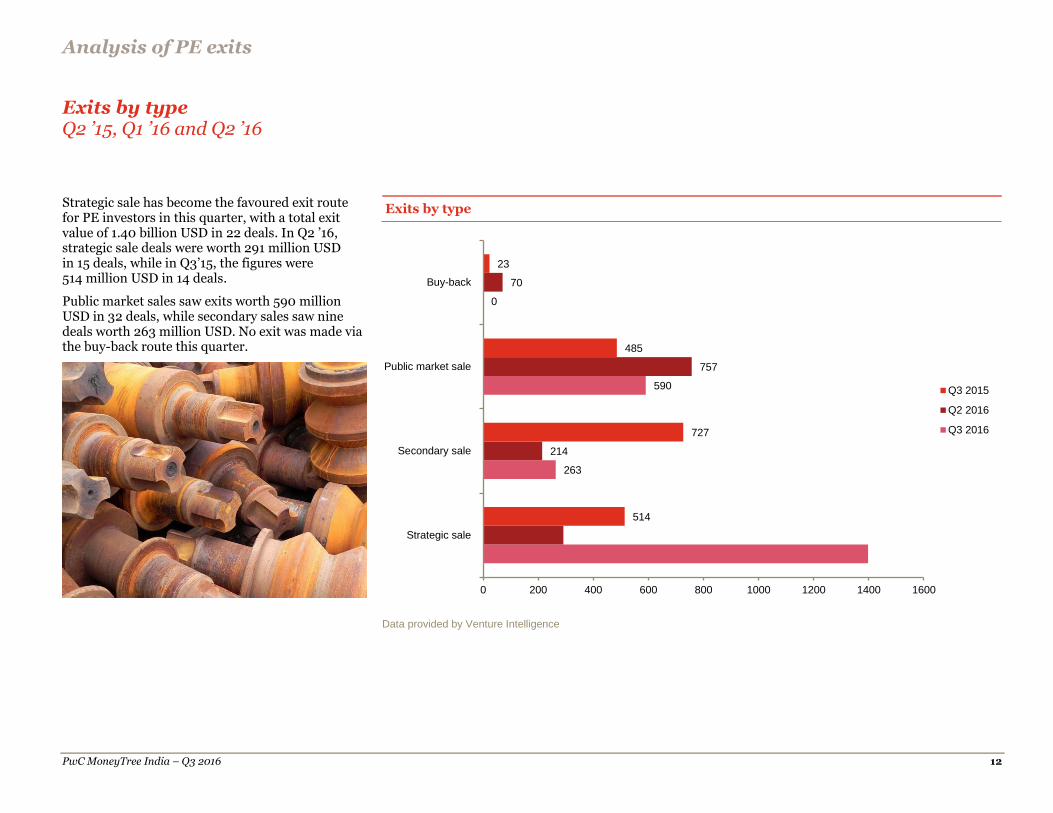

Strategic sale has become the favoured exit route for PE investors in this quarter, with a total exit value of 1.40 billion USD in 22 deals. In Q2 ’16, strategic sale deals were worth 291 million USD in 15 deals, while in Q3’15, the figures were 514 million USD in 14 deals.

Public market sales saw exits worth 590 million USD in 32 deals, while secondary sales saw nine deals worth 263 million USD. No exit was made via the buy-back route this quarter.

Data provided by Venture Intelligence

263

590

0

214

757

70

514

727

485

23

0 200 400 600 800 1000 1200 1400 1600

Strategic sale

Secondary sale

Public market sale

Buy-back

Q3 2015

Q2 2016

Q3 2016

Exits by type

Analysis of PE exits

PwC MoneyTree India – Q3 2016 13

Top five PE exits Q3 ’16

The top five exits comprised 54% of the total exit value in Q3 ’16.

Top 5 PE exits in Q3 2016

Company Industry Investor Deal amount

(US$ M)

Gland Pharma Healthcare & life sciences KKR 556

Minacs BPO IT & ITeS CX Partners, Capital Square Partners

420

Indecomm Global Services

Healthcare & life sciences IFC, Tiger Global, Acer Technology Ventures, WestBridge

90

Hero MotoCorp Manufacturing GIC 83

Jabong.com IT & ITeS CDC Group, Rocket Internet 70

Data provided by Venture Intelligence

PwC MoneyTree India – Q3 2016 14

4. Active PE firms

Sequoia Capital India and Accel India have entered into 11 and nine deals, respectively in this quarter.

The most active PE investors in Q3 ’16 are listed at right.

Data provided by Venture Intelligence

* Number of deals includes both single and co-investments by PE firms. Cases where two or more firms have invested in a single deal are accounted for as one deal for each firm.

Most active PE investors – Q3 2016

Investors No of deals

Sequoia Capital India 11

Accel India 9

Kalaari Capital 6

IDG Ventures India 5

SAIF 5

ChrysCapital 4

IFC 4

Nexus Venture Partners 4

Norwest 4

RB Investments 4

Bertelsmann India Investments 3

Goldman Sachs 3

Helion Ventures 3

India Quotient 3

Jungle Ventures 3

Omidyar Network 3

Qualcomm Ventures 3

WestBridge 3

PwC MoneyTree India – Q3 2016 15

5. Sector focus – IT & ITeS sector

The technology sector in India is undergoing a significant change driven by movements in demand and supply equations, and technological disruption as well as socioeconomic and geopolitical factors. Recently, Nasscom lowered its IT export growth target to 8-10% for 2016-17; at the beginning of the year Nasscom had projected a 10-12% growth rate for the Indian IT & ITeS market.* The change in business environment is being influenced by the forces of global macroeconomic headwinds, e.g., the US election, Brexit, oil price fluctuations and volatility in currency and financial markets, whereas the demand-supply equation is being impacted by trends like IT outsourcing and vendor consolidation. In terms of trends, business-driven technology spending has been growing at a faster rate than traditional spending. Digitalisation is transforming business models as companies look to reinvent themselves while traditional outsourcing is inching towards next-gen IT outsourcing, where the focus is on integrated services delivery, artificial intelligence, automation and cloud. The technological breakthrough megatrends are manifesting themselves in a proliferation of technologies. PwC’s Essential Eight, a shortlist of emerging technologies to watch out for, have the potential to transform business models across all industries and drive significant organisational change. These emerging technologies are directly impacting businesses and are changing buyer behavior, making it business-centric. Buying decisions are now being strongly influenced by business leaders, in addition to the IT leaders in an organisation, as companies realise the impact of technologies like 3D printing, robotics and the Internet of Things on their organisations. To remain relevant and to succeed, an emerging technology strategy will have to be a part of every company’s corporate strategy. Another important business development this quarter has been the Indian government’s demonetisation scheme which banned notes of higher denominations in order to curb the flow of black money and corruption. The scheme is likely to help build a cash-less economy, thereby helping businesses to pursue higher growth in digital driven areas. Along with the upcoming Goods and Services Tax (GST) launch, these initiatives are likely to help strengthen the economy and improve the ease of doing business in India. An important growth area in terms of deals activity this quarter has been the Mobile Wallets subsector and recent government initiatives have triggered the strong adoption of electronic payments. We have seen explosive growth for digital transactions and usage of mobile wallets by consumers and mobile in point of sale (PoS) by merchants. Mobile wallets are being used for a variety of purposes from bill payments to food delivery and travel. Further, the launch of a unified payment interface (UPI) will make transactions easier and aid in overall growth. Mobile Wallet companies will have to focus on customer retention and building customer loyalty as well as challenges around cyber security. Achieving scale with positive unit economics and acquiring greater wallet share of the target customer segment will also be important for the growth of the subsector. Sandeep Ladda Leader, Technology PwC India *http://economictimes.indiatimes.com/tech/ites/nasscom-cuts-it-export-growth-forecast-to-8-10-for-2016-17/articleshow/55457227.cms

Sector focus – IT & ITeS sector

PwC MoneyTree India – Q3 2016 16

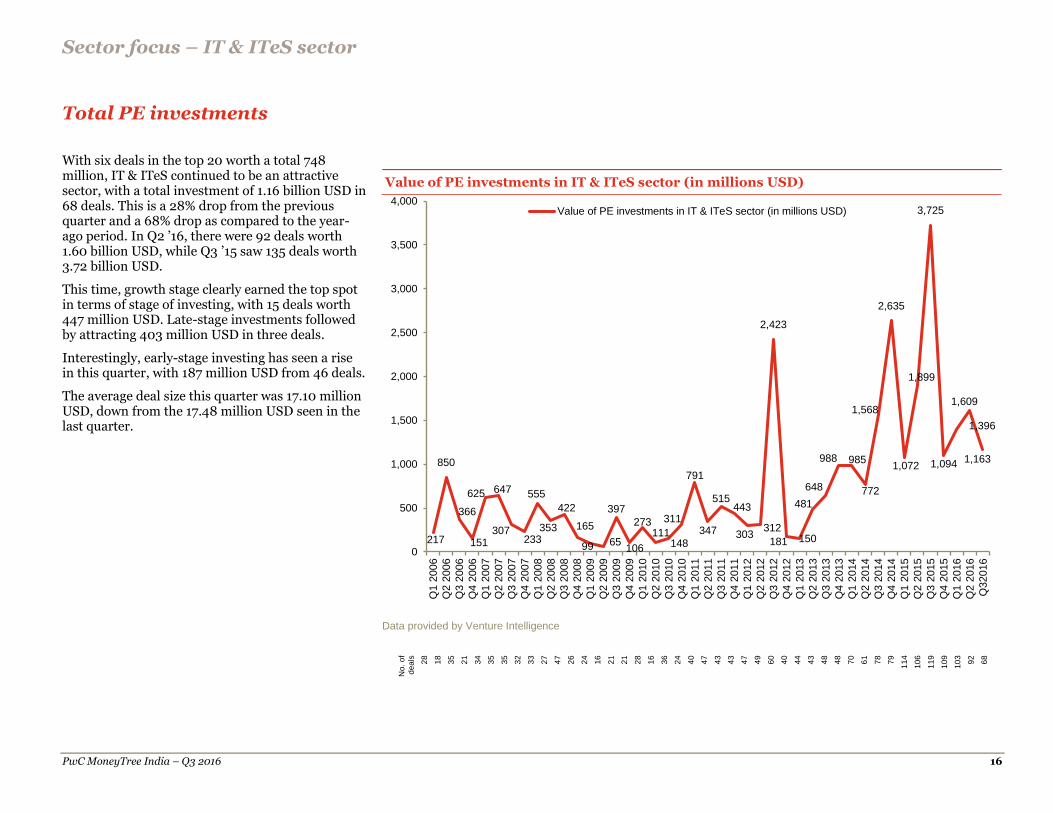

Total PE investments

With six deals in the top 20 worth a total 748 million, IT & ITeS continued to be an attractive sector, with a total investment of 1.16 billion USD in 68 deals. This is a 28% drop from the previous quarter and a 68% drop as compared to the year-ago period. In Q2 ’16, there were 92 deals worth 1.60 billion USD, while Q3 ’15 saw 135 deals worth 3.72 billion USD.

This time, growth stage clearly earned the top spot in terms of stage of investing, with 15 deals worth 447 million USD. Late-stage investments followed by attracting 403 million USD in three deals.

Interestingly, early-stage investing has seen a rise in this quarter, with 187 million USD from 46 deals.

The average deal size this quarter was 17.10 million USD, down from the 17.48 million USD seen in the last quarter.

Data provided by Venture Intelligence

No.

of

de

als

28

18

35

21

34

35

35

32

33

27

47

26

24

16

21

21

28

16

36

24

40

47

43

43

47

49

60

40

44

43

48

48

70

61

78

79

11

4

10

6

11

9

10

9

10

3

92

68

217

850

366

151

625 647

307233

555

353

422

165

99 65

397

106

273111

148

311

791

347

515443

303312

2,423

181 150

481

648

988 985

772

1,568

2,635

1,072

1,899

3,725

1,094

1,396

1,609

1,163

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Q32016

Value of PE investments in IT & ITeS sector (in millions USD)

Value of PE investments in IT & ITeS sector (in millions USD)

Sector focus – IT & ITeS sector

PwC MoneyTree India – Q3 2016 17

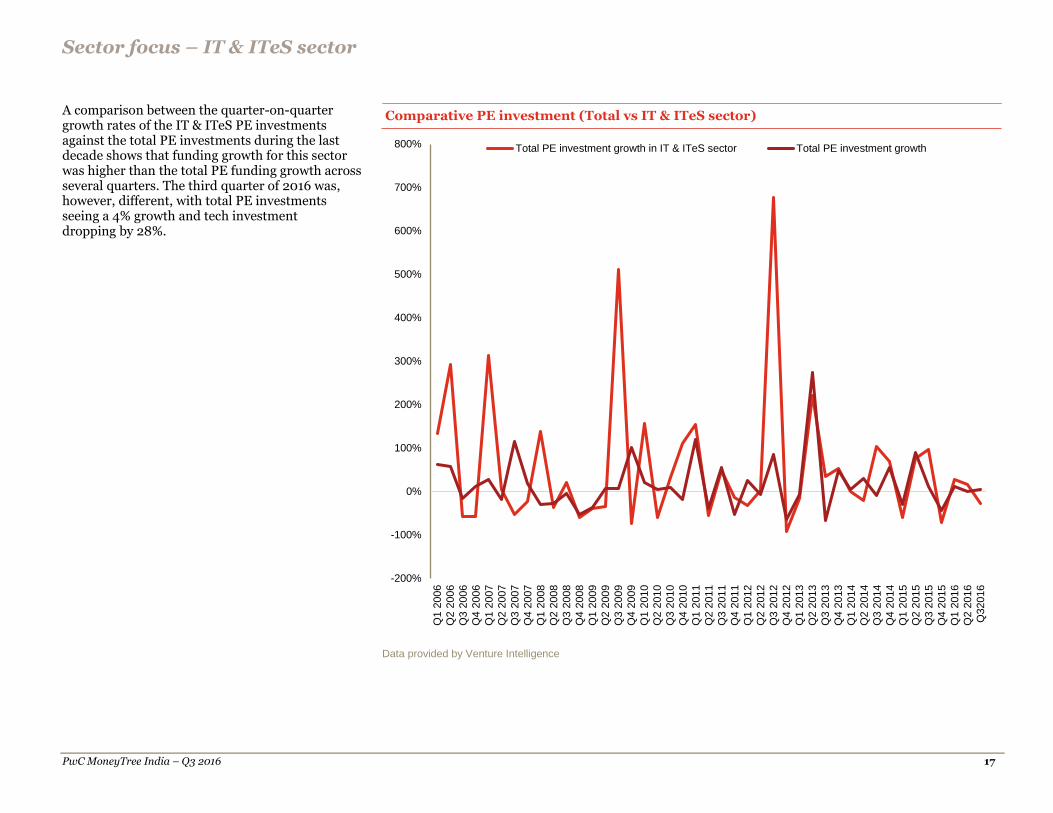

A comparison between the quarter-on-quarter growth rates of the IT & ITeS PE investments against the total PE investments during the last decade shows that funding growth for this sector was higher than the total PE funding growth across several quarters. The third quarter of 2016 was, however, different, with total PE investments seeing a 4% growth and tech investment dropping by 28%.

Data provided by Venture Intelligence

-200%

-100%

0%

100%

200%

300%

400%

500%

600%

700%

800%

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

Q4 2

013

Q1 2

014

Q2 2

014

Q3 2

014

Q4 2

014

Q1 2

015

Q2 2

015

Q3 2

015

Q4 2

015

Q1 2

016

Q2 2

016

Q32016

Total PE investment growth in IT & ITeS sector Total PE investment growth

Comparative PE investment (Total vs IT & ITeS sector)

Sector focus – IT & ITeS sector

PwC MoneyTree India – Q3 2016 18

Investments by stage of development Q3 ’15, Q2 ’16 and Q3 ’16

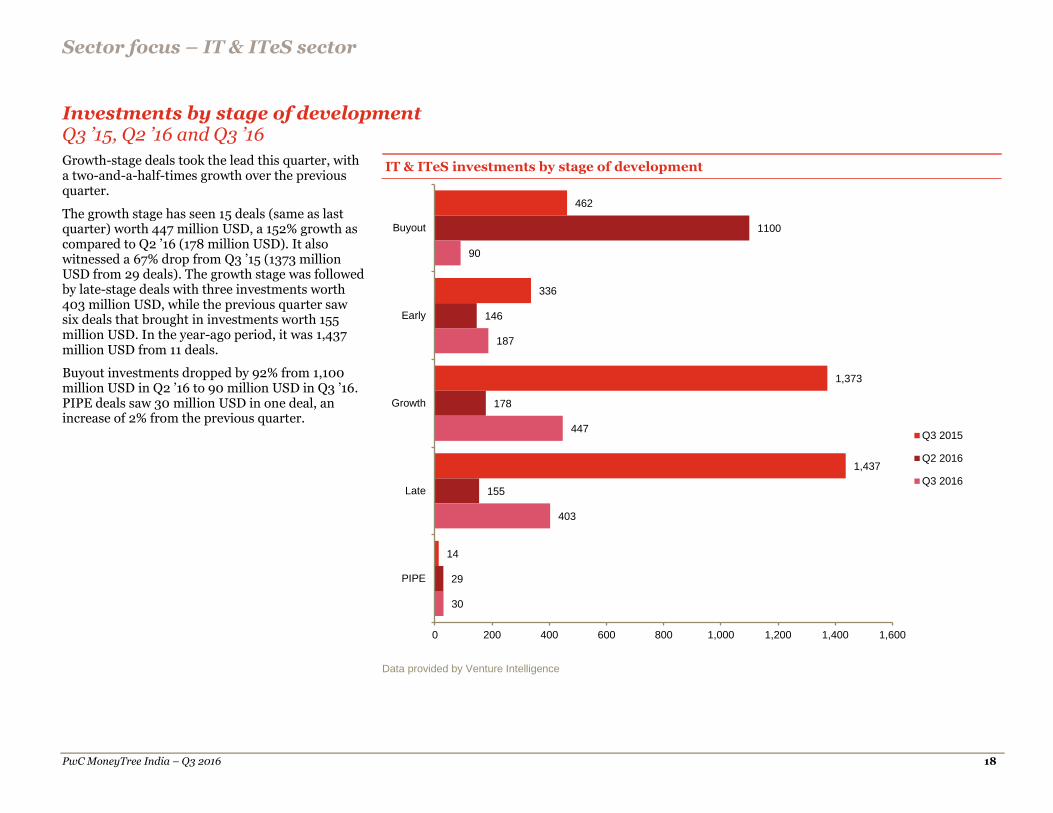

Growth-stage deals took the lead this quarter, with a two-and-a-half-times growth over the previous quarter.

The growth stage has seen 15 deals (same as last quarter) worth 447 million USD, a 152% growth as compared to Q2 ’16 (178 million USD). It also witnessed a 67% drop from Q3 ’15 (1373 million USD from 29 deals). The growth stage was followed by late-stage deals with three investments worth 403 million USD, while the previous quarter saw six deals that brought in investments worth 155 million USD. In the year-ago period, it was 1,437 million USD from 11 deals.

Buyout investments dropped by 92% from 1,100 million USD in Q2 ’16 to 90 million USD in Q3 ’16. PIPE deals saw 30 million USD in one deal, an increase of 2% from the previous quarter.

Data provided by Venture Intelligence

462

336

1,373

1,437

14

1100

146

178

155

29

90

187

447

403

30

0 200 400 600 800 1,000 1,200 1,400 1,600

Buyout

Early

Growth

Late

PIPE

Q3 2015

Q2 2016

Q3 2016

IT & ITeS investments by stage of development

Sector focus – IT & ITeS sector

PwC MoneyTree India – Q3 2016 19

Investments by region Q3 ’15, Q2 ’16 and Q3 ’16

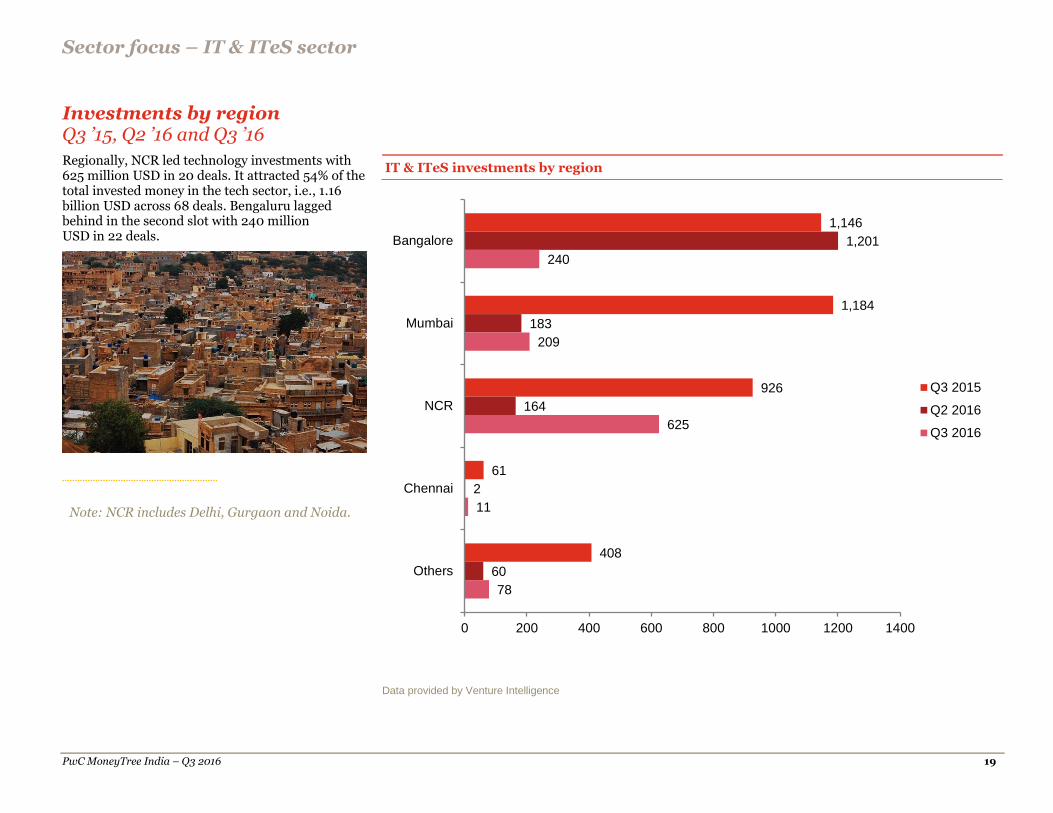

Regionally, NCR led technology investments with 625 million USD in 20 deals. It attracted 54% of the total invested money in the tech sector, i.e., 1.16 billion USD across 68 deals. Bengaluru lagged behind in the second slot with 240 million USD in 22 deals.

IT & ITeS investments by region

Data provided by Venture Intelligence

1,146

1,184

926

61

408

1,201

183

164

2

60

240

209

625

11

78

0 200 400 600 800 1000 1200 1400

Bangalore

Mumbai

NCR

Chennai

Others

Q3 2015

Q2 2016

Q3 2016

Note: NCR includes Delhi, Gurgaon and Noida.

Sector focus – IT & ITeS sector

PwC MoneyTree India – Q3 2016 20

Investments by subsector Q3 ’15, Q2 ’16 and Q3 ’16

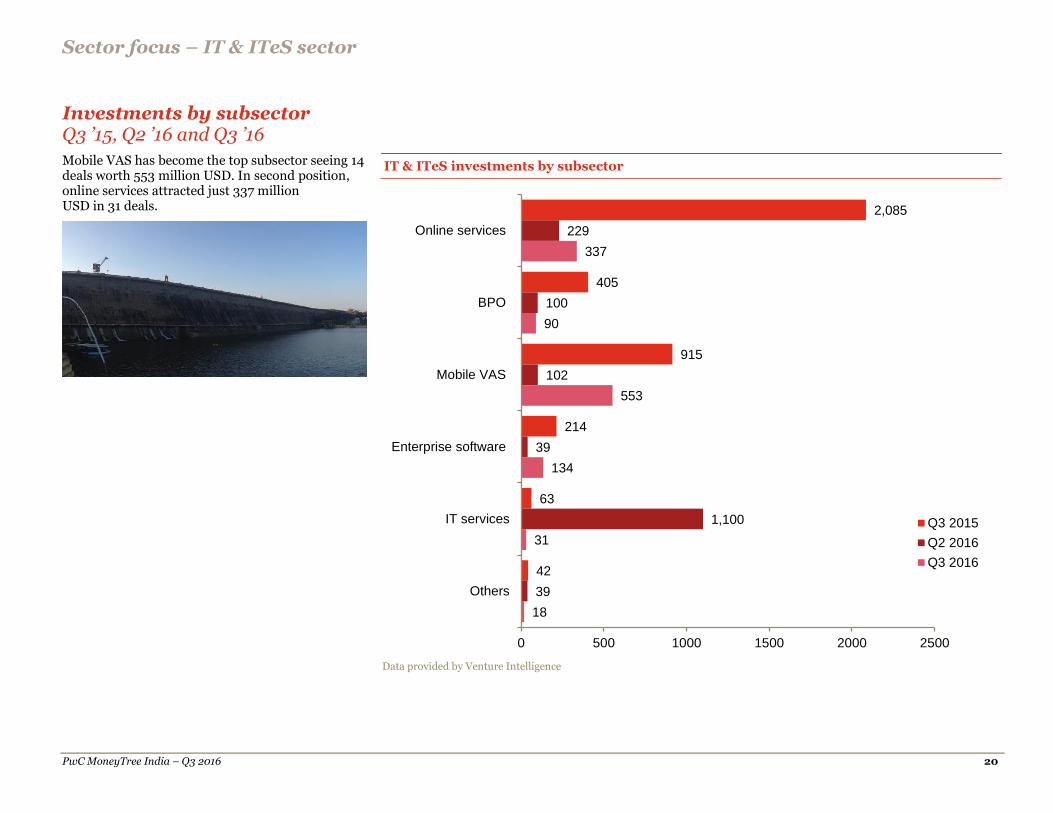

Mobile VAS has become the top subsector seeing 14 deals worth 553 million USD. In second position, online services attracted just 337 million USD in 31 deals.

Data provided by Venture Intelligence

2,085

405

915

214

63

42

229

100

102

39

1,100

39

337

90

553

134

31

18

0 500 1000 1500 2000 2500

Online services

BPO

Mobile VAS

Enterprise software

IT services

Others

Q3 2015

Q2 2016

Q3 2016

IT & ITeS investments by subsector

Sector focus – IT & ITeS sector

PwC MoneyTree India – Q3 2016 21

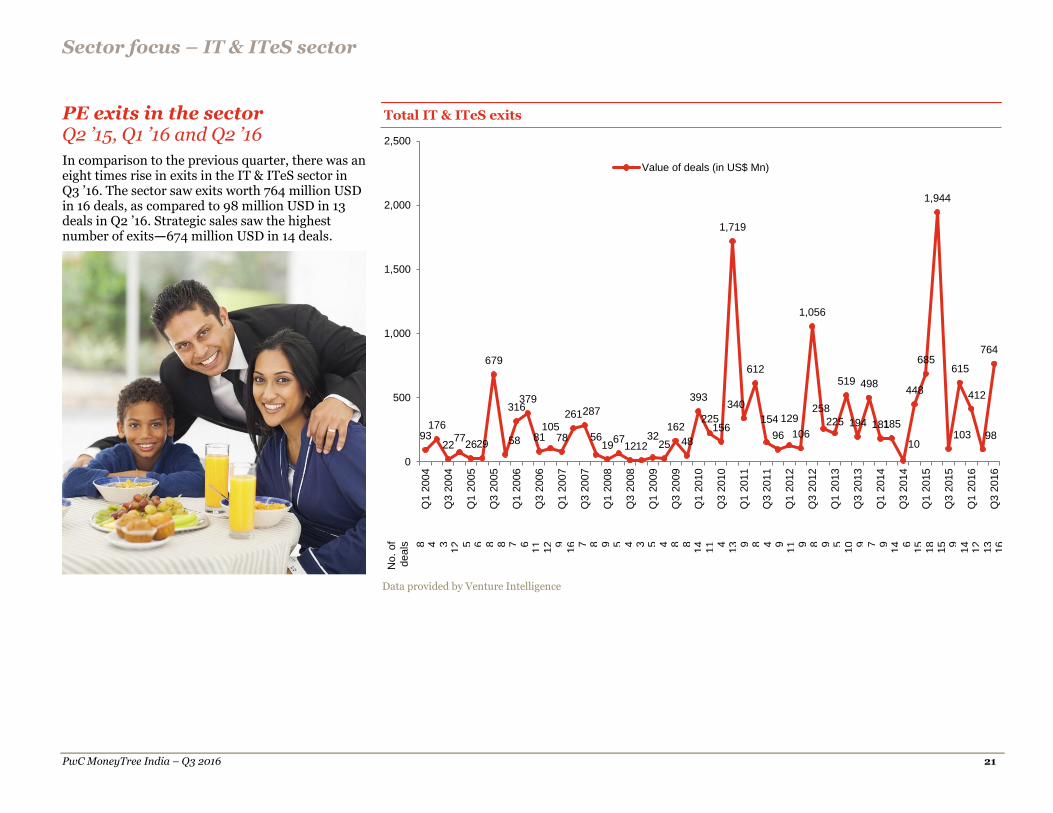

PE exits in the sector Q2 ’15, Q1 ’16 and Q2 ’16

In comparison to the previous quarter, there was an eight times rise in exits in the IT & ITeS sector in Q3 ’16. The sector saw exits worth 764 million USD in 16 deals, as compared to 98 million USD in 13 deals in Q2 ’16. Strategic sales saw the highest number of exits—674 million USD in 14 deals.

No.

of

deals

8

4

3

12

5

6

8

8

7

6

11

12

9

16

7

8

9

5

4

3

5

4

8

8

14

11

4

13

9

8

4

9

11

9

8

9

5

10

9

7

9

14

6

15

18

15

9

14

12

13

16

Data provided by Venture Intelligence

93176

2277

2629

679

58

316379

81105

78

261287

5619

671212

3225

162

48

393

225156

1,719

340

612

154

96

129

106

1,056

258

225

519

194

498

181185

10

448

685

1,944

103

615

412

98

764

0

500

1,000

1,500

2,000

2,500

Q1 2

004

Q3 2

004

Q1 2

005

Q3 2

005

Q1 2

006

Q3 2

006

Q1 2

007

Q3 2

007

Q1 2

008

Q3 2

008

Q1 2

009

Q3 2

009

Q1 2

010

Q3 2

010

Q1 2

011

Q3 2

011

Q1 2

012

Q3 2

012

Q1 2

013

Q3 2

013

Q1 2

014

Q3 2

014

Q1 2

015

Q3 2

015

Q1 2

016

Q3 2

016

Value of deals (in US$ Mn)

Total IT & ITeS exits

PwC MoneyTree India – Q3 2016 22

Definitions

Stages of development

Early stage – This refers to the first or second round of institutional investments in companies that adhere to the following:

Less than five years old

Not part of a larger business group

Investment is less than 20 million USD

Growth stage – This refers to investments of less than 20 million USD. Also, investments meeting the following criteria are considered to be in the growth stage:

Third or fourth round funding of institutional investments

First or second round of institutional investments in companies that are more than 5 years old and less than 10 years old or spin-outs from larger businesses

Growth stage PE: This includes the following:

First or second round of investments worth 20 million USD or more

Third or fourth round funding in companies that are more than 5 years old and less than 10 years old, or subsidiaries or spin-outs from larger businesses

Fifth or sixth round of institutional investments

Late stage – This comprises the following:

Investment in companies that are a decade old

Seventh or later round of institutional investments

PIPEs – The following constitute PIPEs:

PE investments in publicly listed companies via preferential allotments or private placements

Acquisition of shares by PE firms via the secondary market

Buyout – This is an acquisition of controlling stake via purchase of stakes of existing shareholders.

Buyout–large – This includes buyout deals of 100 million USD or more in value.

Other – This includes PE investments in special purpose vehicle (SPV) or project-level investments.

Types of PE exits

Buyback – This includes the purchase of PE or VC investors’ equity stakes by either the investee company or its founders or promoters.

Strategic sale – This includes the sale of PE or VC investors’ equity stakes (or the entire investee company itself) to a third-party company (which is typically a larger company in the same sector).

Secondary sale – Any purchase of PE or VC investors’ equity stakes by another PE or VC investors constitutes secondary sale.

Public market sale – This includes the sale of PE or VC investors’ equity stakes in a listed company through the public market.

Initial public offering (IPO) – This includes the sale of PE or VC investors’ equity stake in an unlisted company through its first public offering of stock.

www.pwc.com/globalmoneytree www.pwc.in

Contacts

Sandeep Ladda Leader, Technology PwC India [email protected]

Sanjeev Krishan Leader, Private Equity PwC India [email protected]

This report was researched and written by the following:

Pradyumna Sahu Executive Director, Markets & Industries PwC India [email protected]

Jitesh Bijlani Sector Driver, Technology PwC India [email protected]

About PwC’s Technology Institute

The Technology Institute is PwC’s global research network that studies the business of technology and the technology of business with the purpose of creating thought leadership that offers both fact-based analysis and experience-based perspectives. Technology Institute insights and viewpoints originate from active collaboration between our professionals across the globe and their first-hand experiences working in and with the technology industry.

About PwC

At PwC, our purpose is to build trust in society and solve important problems. We’re a network of firms in 157 countries with more than 223,000 people who are committed to delivering quality in assurance, advisory and tax services. Find out more and tell us what matters to you by visiting us at www.pwc.com.

www.pwc.com

PricewaterhouseCoopers and Venture Intelligence have taken responsible steps to ensure that the information contained in the MoneyTreeTM report has been obtained from reliable sources. However, neither of the parties can warrant the ultimate validity of the data obtained. Results are updated periodically. Therefore, all data is subject to change at any time. Before making any decision or taking any action, you should consult a competent professional adviser.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

©2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see pwc.com/structure for further details.