Embed Size (px)

Citation preview

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

26

PRICE VOLATILITY TRANSMISSION BETWEEN OPEC AND

NON-OPEC OILS, A WAVELET BASED APPROACH.

¹MS. ALEXANDER SOUZA BLOCK¹, ²DR. MARCELO BRUTTI RIGHI, ³DR. DANIEL

ARRUDA CORONEL,

1Pampa Federal University

2Universidade Federal do Rio Grande do Sul

3Santa Maria Federal University

Email: ¹[email protected], ²[email protected], ³[email protected]

ABSTRACT

The importance of measuring volatility cannot be ignored. Equally important is to understand how

volatility is transmitted between markets and assets. Using the wavelets methodology, this study seeks to

analyze at different frequencies, the direction and magnitude of volatility transmission in the crude oil

produced by OPEC countries and other producing and exporting countries that are not part of this

organization (non-OPEC. This approach contributes to the literature identifying the crude oil volatility in

different frequencies and in its origin, the producing countries. This way is possible to provide information

for Energy Policy Makers, investors and researchers about the two groups of suppliers, helping them to

define strategies of purchase, trade, storage and hedging.

Key-words: Price volatility transmission, OPEC and non-OPEC crude oils behavio, Frequency analysis.

1. INTRODUCTION

Since the 1986 oil price shock, the behavior of

these prices has become a daily concern for

governments and investors. Trading in crude oil

also changed, attracting numerous types of market

participants, not just the parts with commercial

interests, but also those who treat oil as a form of

investment. In recent years the role negotiation

became even wider and accessible. At the same

time, there is a relatively easy access to several

markets, particularly European and North

American markets.

On the world stage of oil, OPEC (Organization of

Petroleum Exporting Countries) plays a central role

in discussions about pricing and supply global

demand. Founded in 1960 by Iran, Iraq, Kuwait,

Saudi Arabia and Venezuela, in 2013 has 14

members, all major world producers. Aiming to

coordinate and unify petroleum policies of member

countries, ensuring fair and stable prices for the

producing countries, an efficient and regular supply

of petroleum to consuming nations and a fair return

for those investing in the industry (OPEC, 2012).

Despite having approximately 78% of proven

world reserves of oil (OPEC Annual Statistical

Bulletin, 2012), all member countries are

considered underdeveloped and are located mostly

in the Middle East and North Africa, regions of

great political instability and social. In this context

one should note the five major shocks in oil prices

due to this instability: 1956 with the nationalization

of the Suez Canal, 1973 with the Yom Kippur War,

1979 due to the Iranian revolution and 1991 with

the Gulf War I.

The majority of OPEC members are located in

regions of great political instability, social and

economic. As it is known, the Gulf region is very

rich in oil resources, being responsible for about

60% of U.S. imports of crude oil. Successive wars,

terrorists attacks and every kind of instability is

directly reflected on crude oil price.

However it must be considered that seven of the 15

largest oil producers are outside of OPEC (EIA,

2012). In 2006 these countries were: Russia, USA,

China, Mexico, Canada, Norway and Brazil.

However many non-OPEC producers are faced

with wells that are rapidly depleting. Some major

producers such as the United States, Mexico and

Norway, have experienced a decline in production

in recent years. However, the overall figures for

non-OPEC producers are reinforced by significant

increases in production in Brazil, Canada, and

Russia.

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

27

The importance of measuring volatility cannot be

ignored. Equally important is to understand how

volatility is transmitted between markets and

assets. In oil markets, agents often have exposure

to a large number of different types of crude oil,

with different prices and volatilities and enabling

them to build portfolios consisting of different

varieties of this commodity.

Notable paper verified these questions about

international crude oil markets. Weiner (1991)

results suggested that the world oil market is far

from unified and crude oil prices do not move

together around the world. However, more studies

tend to support that oil markets behave like one

common market (Adelman (1992); Gulen (1999);

Ewing and Harter (2000); Engle and Granger;

(1987), Bachmeier and Griffin (2006))

From a different point of view Salisu and Fasanya

(2012) employed the tests developed by Liu and

Narayan (2010) to detect structural breaks in data

series. This evidence suggests that oil volatility is

not uniform in time presenting persistence and

leverage effects. This kind of evidence shows some

necessity of investigate crude oil volatility from a

time variable point of view since its behavior is

changed because of the considered time window.

Therefore, using the wavelets methodology, this

study seeks to analyze at different frequencies, the

price volatility relations in the crude oil produced

by OPEC countries and other producing and

exporting countries that are not part of this

organization (non-OPEC). This way you can

understand the functioning of this important market

and answer the following question: How volatility

behaves in relations between the different types of

oil and how it is transmitted between OPEC

members and non-OPEC producers?

This approach brings two main contributions to the

literature: (1) We present the OPEC and non-OPEC

volatilities correlations in different frequencies and

(2) present the price volatility transmission

between these producers. This way is possible to

provide information for Energy Policy Makers,

investors and researchers about the two groups of

suppliers, helping them to define strategies of

purchase, trade, storage and hedging.

This paper is structured as follows. Section 2

provides a review of the selected studies and aims

to demonstrate how the wavelets methodology can

bring a new perspective to this issue. In Section 3

we describe the data and period analyzed, and

present the econometric model developed in this

paper. The application, estimation and comparison

with previous studies are presented in Section 4

with some tables and figures. In Section 5 we draw

some important policy conclusions about the

volatility relations among crude oil producers’

countries.

2. WAVELETS APPLICABILITY

The interaction of a variable with the changes of

the environment may result in a universe of

relationships, difficult to be observed and

understood In this sense, the filtering methods in

finance and economics are useful tools to identify

certain features and behavior of time series.

Decomposing the series is possible to extract

seasonality, trends and noise. Thus, Wavelets are

an interesting methodology to decompose time

series in different frequencies and reveal more

information.

The method uses a wavelet basic function called

mother wavelet, which is expanded and contracted

to capture local characteristics in time and

frequency. The wavelet filter is long in time when

capturing low frequency events, and short in time

when capturing events of high frequency. Through

combinations to expand and contract the "mother

wavelet", you can capture all the information

present in a time series (Gençay et al., 2002). Thus,

the wavelet fits through a range of frequencies, to

capture and locate features events that are local in

time. This makes this method an excellent tool for

time series analysis, especially non-stationary.

Capobianco (2003) investigated this potential for

decomposing financial volatility processes. The

results indicate that wavelets and derived

functional dictionaries may play an important role

in detecting hidden features and the dependence

structures.

Looking to demonstrate the contributions of

wavelet methodology to correlations analysis,

Razdan (2004) studied the correlations between

Bombay stock index (BSE) and National stock

index (NSE). As known the traditional correlation

coefficient between these indices is 99310.r ,

indicating that the BSE index is strongly correlated

with NSE index. However using the Wavelet

correlation coefficient he was capable to show that

this correlation changes as the time scale, including

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

28

being negative. This found highlights the

applicability of wavelets in reveal new information.

Souza and Silva (2010), employed wavelet analysis

to remove high frequency price movements of oil

price, then using hidden Markov model, they were

capable to forecast the probability distribution of

the price return accumulated over the next days and

infer future price trends.

Power and Turvey (2010) analyzed the long-range

dependence in the volatility of 14 commodities

futures prices including crude oil. Using wavelets

to decompose in time scales and Hurst coefficient,

was not possible to reject the null hypothesis that

the long memory parameter H has been constant

over the entire sample characterizing no long-range

dependence. Unlike the findings of Alvarez-

Ramirez et al (2008) were no evidences of the

existence of a trend in the time-varying Hurst

coefficient for any of the commodity futures.

Wavelets can be especially useful to investigate

reanalyze old questions with divergent results,

given its capacity to revel more time-series

information. Benhmad (2012) used a wavelet

approach to study the linear and nonlinear Granger

causality between the real oil price and the real

effective U.S. Dollar exchange rate. The series

decomposition reveled seven frequency bands with

different causality relations each. This approach

show that previous studies were capable to detect

only the relation present at the analyzed frequency,

and the wavelets decomposition expand the

researched universe.

Several papers had divergent results when analyzed

the relationship between crude oil price changes

and stock market returns. Combining wavelet

analysis and Markov Switching Vector

Autoregressive (MS-VAR) model to explore the

Impact of the crude oil shocks on the stock market

returns for UK, France and Japan, Jammaz & Aloui

(2010), shows the efficiency of wavelet to filtering

series and determining the behavior of the stock

market volatilities. Applying this technique, they

were able to extract the driving dynamics of crude

oil prices and to bring out past events that were not

originally visible.

Using wavelets methodology we are able to

identify the behavior of crude oil volatility in

different frequencies. This approach can be

especially meaningful to understand the

transmission direction; supplying market

participates with more precise information.

3. METHODOLOGY

3.1 Wavelets filtering methodology

According to Gençay et al. (2002) a wavelet ψ (t) is

a function of time (t) wich obeys two basic rules,

known as wavelet admissibility condition. The first

condition ensures that ψ (f) goes to zero quickly as

f→0. This first condition can be expressed by

,0)(

dtt (1)

The second condition imposed on a wavelet

function is unit energy, that is,

,1|)(| 2

dtt (2)

In order to quantify the function change at a

particular frequency and at a certain point in time

the mother-wavelet ψ (t) is dilated and translated,

s

ut

stsu

1)(, (3)

Where: u and s are, respectively, the time location

and scale parameters or frequency ranges. The

continuous wavelet transform (CWT) is a function

),( suW which is obtained by projecting the

original function x (t) in the mother wavelet

)(, tsu ,

.)()(),( , dtttxsuW su (4)

In order to assess variations in large-scale basis (ie

a low frequency), a large value for s must be

chosen, and vice versa. Applying CWT for a

continuous location and scale parameters of a

function, it is possible to extract a set of "basic"

components.

3.2 Transmission and Granger causality

The Granger causality test (1961) has

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

29

been applied in several economic and financial

studies, as an efficient methodology to detect the

direction of transmissions whether of prices,

currency exchange rates or volatilities. Wang

(2010) analyzed the volatility transmission between

U.S. industries. Using causality tests, the results

showed that the industrial base, producing

machinery, can be a source of risk that can affect

virtually all other sectors. Their results indicate that

traditional sectors like oil and automobile

apparently not seem to have great influence on

other major sectors. Bentzen (2007) used high

frequency data and causality tests to investigate the

relationship between WTI, Brent and Dubai. The

results demonstrate bidirectional transmissions,

which highlights the globalization of this market.

He et al. (2010) investigated the relationship

between economic activity and oil prices. They

found strong evidence of Granger causality

between these variables. Other applications of

Granger causality test can also be found in Hong

(2001), Bubak et. al (2011) Nishiyama (2011).

According Tsay (2008), the Granger causality test

is based on the assumption that the future cannot

cause the past nor the present . Thus, if Y

comes after X, then Y cannot cause X. Likewise if

X precedes Y, that does not mean that X causes Y.

Thus the test looks for an evidence of any of the

following events: i) X causing Y (X → Y), ii) Y

cause X (Y → X), iii) bi causality (Y → X and X

→ Y).

Thus, the test Granger causality checks whether

information contained in a time series explain the

occurrence of variations in the other series.

Formally, in the current study, the causality test is

represented as follow,

k

i

k

i

txitiyitixlt yxx1 1

,,,, (5)

k

i

k

i

tyitiyitixlt yxy1 1

,,,, (6)

where ltx , and

lty , represent the volatility,

squared return, of the OPEC and non-OPEC crude

oil price, in time t and in the frequency l, tx, and

ty , are white noise. Do not reject the null

hypothesis 0... ,2,1,0 kxyyH ,

in the regression equation (5) implies that the

volatility of OPEC crude oil prices do not Granger

cause the volatility of the price of non-OPEC crude

oil. Similarly, do not reject the null hypothesis,

0... ,2,1,0 kxxxH , in the

regression equation (6) implies that the volatility of

non-OPEC do not Granger cause the OPEP crude

oil volatility.

To perform this study we analyzed weekly average

prices ($ / barrel) weighted by the volume exported

by OPEC member countries and other producing

and exporting countries not members of the

organization these indices are released by the U.S.

Energy Information Administration (EIA)

considering the following countries and varieties of

crude oil (Table 1). The sample period extends

from January 3, 1997 to September 30, 2011,

totaling 768 observations.

OPEC non-OPEC

Abu Dhabi Murban Spot

Price FOB

Australia Gippsland

Spot Price FOB

Algeria Saharan Blend

Spot Price FOB

Brunei Seria Light Spot

Price FOB

Angola Cabinda Spot

Price FOB

Cameroon Kole Spot

Price FOB

Asia Dubai Fateh Spot

Price FOB

Canadian Par Spot Price

FOB

Ecuador Oriente Spot

Price FOB

Canada Heavy Hardisty

Spot Price FOB

Mediterranean Sidi

Kerir Iran Heavy Spot

Price FOB

Canada Lloyd Blend

Spot Price FOB

Mediterranean Sidi

Kerir Iran Light Spot

Price FOB

China Daqing Spot

Price FOB

Iraq Kirkuk Netback

Price FOB

Colombia Cano Limon

Spot Price FOB

Kuwait Blend Spot

Price FOB

Egypt Suez Blend Spot

Price FOB

Libya Es Sider FOB

Spot Price

Gabon Mandji Spot

Price FOB

Neutral Zone Khajji

Spot Price FOB

Indonesia Minas Spot

Price FOB

Nigeria Bonny Light

Spot Price FOB

Malaysia Tapis Blend

Spot Price FOB

Europe (Forcados,

Nigeria) Spot Price FOB

Mexico Isthmus Spot

Price FOB

Qatar Dukhan Spot

Price FOB

Mexico Maya Spot

Price FOB

Saudi Arabia Heavy

Spot Price FOB

Europe (Ekofisk,

Norway) Blend Spot

Price FOB

Saudi Arabia Light Spot

Price FOB

Oman Blend Spot Price

FOB

Saudi Arabia Medium

Spot Price FOB Mediterranean (Russia,

Urals) Spot Price FOB Venezuela Bachaquero

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

30

OPEC non-OPEC

17 Spot Price FOB

Venezuela Bachaquero

24 Spot Price FOB Europe (UK) Brent

Blend Spot Price FOB Venezuela Tia Juana

Light Spot Price FOB Table 1: Crude oil used in the composition of OPEC and

non-OPEC averages

Note: FOB denotes Free on Board, price without

additional costs as insurance or taxes.

In this work the squared log-return are chosen to

represent the volatility once it can be considered an

efficient measure of dispersion behavior, been

calculated according to equation (7): 22

1 )())/(log( ttt rpp (7)

Where pt and pt-1 are the crude oil prices indexes

in time t. According to Gençay et al. (2002) this

is an efficient proxy for volatility, once its

represent the price fluctuations in time, respecting

the main characteristics of volatility. Furthermore,

how it is not an estimation, does not

present estimation error, being ideal to be

decomposed by Wavelets.

4. RESULTS

As known, stationary is an important assumption

when using methods of time series analysis as

Granger causality tests. Thus, we applied

Aumented Dickey-Fuller with GLS constant

(ADF-GLS) and KPSS tests in the square of the

logarithm of the price return series.

Augmented Dickey-Fuller (GLS) test KPSS test

Variable Test Statistic p-value: Z(t) Test Statistic Critical value 5%

OPEC -3.8171 0.0001 0.1173 0.462

Non-OPEC -3.5656 0.0003 0.1171 0.462

Table 2: ADF-GLS and KPSS stationary tests.

The ADF-GLS and KPSS confirm the absence of

unit root, allowing its statistical modeling.

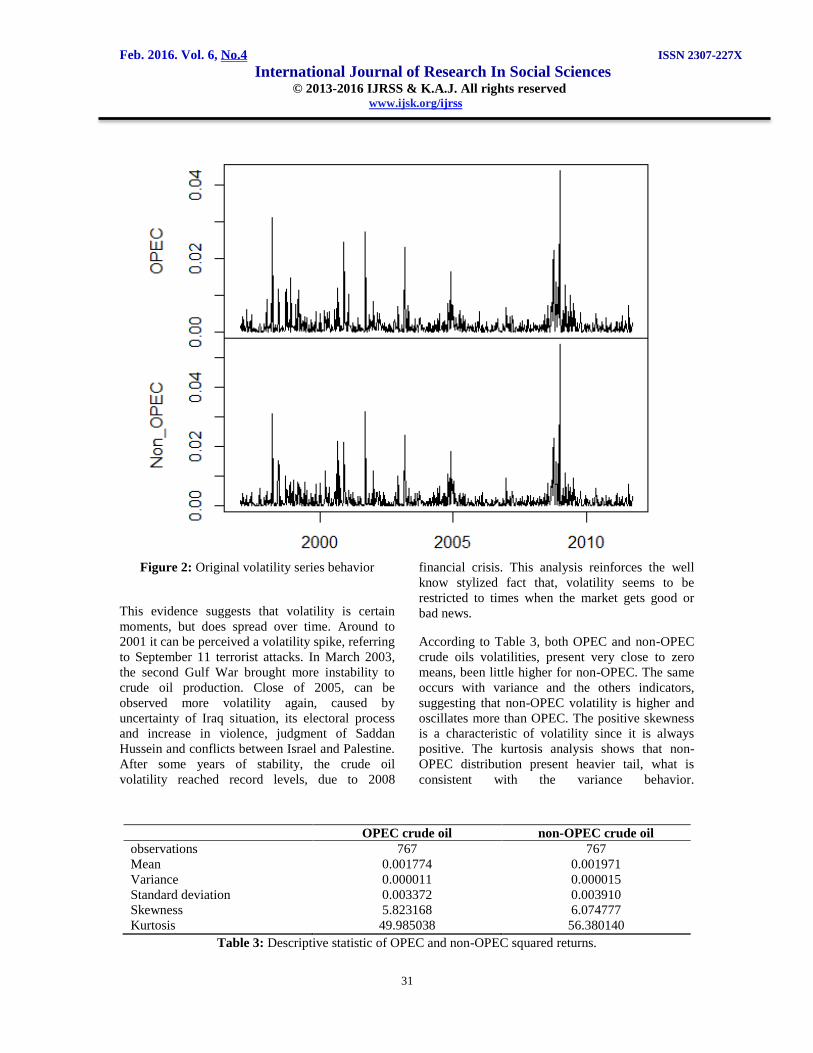

Figure 1 show the original volatility series

behavior. It is possible to verify that volatility is

not constant in time, besides there are strong

volatilities clusters

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

31

Figure 2: Original volatility series behavior

This evidence suggests that volatility is certain

moments, but does spread over time. Around to

2001 it can be perceived a volatility spike, referring

to September 11 terrorist attacks. In March 2003,

the second Gulf War brought more instability to

crude oil production. Close of 2005, can be

observed more volatility again, caused by

uncertainty of Iraq situation, its electoral process

and increase in violence, judgment of Saddan

Hussein and conflicts between Israel and Palestine.

After some years of stability, the crude oil

volatility reached record levels, due to 2008

financial crisis. This analysis reinforces the well

know stylized fact that, volatility seems to be

restricted to times when the market gets good or

bad news.

According to Table 3, both OPEC and non-OPEC

crude oils volatilities, present very close to zero

means, been little higher for non-OPEC. The same

occurs with variance and the others indicators,

suggesting that non-OPEC volatility is higher and

oscillates more than OPEC. The positive skewness

is a characteristic of volatility since it is always

positive. The kurtosis analysis shows that non-

OPEC distribution present heavier tail, what is

consistent with the variance behavior.

OPEC crude oil non-OPEC crude oil

observations 767 767

Mean 0.001774 0.001971

Variance 0.000011 0.000015

Standard deviation 0.003372 0.003910

Skewness 5.823168 6.074777

Kurtosis 49.985038 56.380140

Table 3: Descriptive statistic of OPEC and non-OPEC squared returns.

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

32

As know the OPEC is responsible for most crude

oil production, and how it is an Organization, all

members take decisions together, unlike what

occurs for non-OPEC countries, which do not have

a coordinated policy. This regulation from OPEC

side can offers some stability to the market. This

supply regulation is perceived for market agents

and it has a little reflex in the descriptive statistics.

Besides, OPEP countries are more traditional

producers and exporters and their reserves capacity

is already know, while non-OPEP countries has

most part of their reserves discovered during the

last few years, and the annual extracted volume is

not stable yet (a good example is Brazil, with huge

reserves in the pre-salt layer, but due to technical

complexity and high costs, they remain

unexplored). Despite of seven of the 15 largest oil

producers do not belong to OPEC, non-OPEP

countries are not big exporters, they consume the

most part of this production, and maybe that's can

be one of reason why their prices are more volatile.

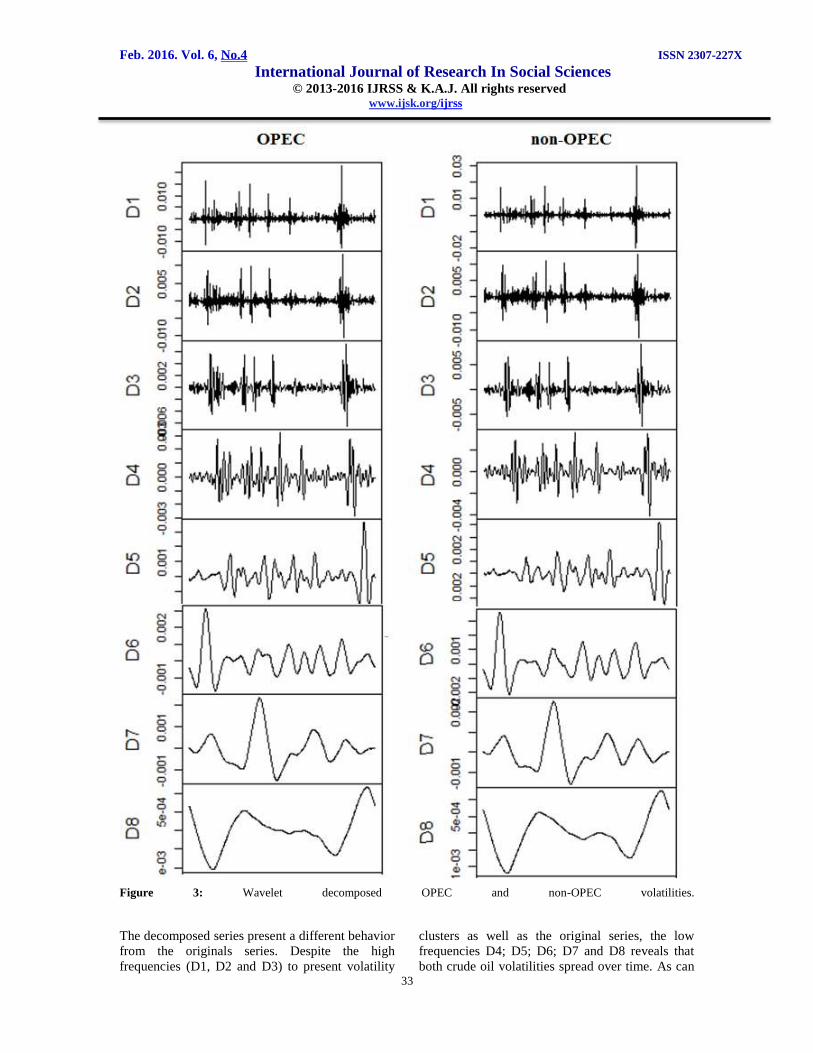

In order to capture more information,

OPEC and non-OPEC volatility series were

decomposed using the Daubechies Wavelet LA(8).

According to Gençay (2002) the LA(8) present the

better fit to financial series behavior, especially

when one works with volatility. By applying this

formula, we decomposed in eight frequencies, D1

to D8, due to series lenght, considering frequencies

of 1, 2, 4, 8, 16, 32, 64 and 128 weeks respectively.

Figure 3 shows the behavior of the wavelet

decomposed series.

The frequencies descriptive statistics for

OPEC and non-OPEC are presented in Table 4 and

Table 5 respectively. The decreasing standard

deviation of OPEC and non-OPEC shows that in

low frequency the series oscillates less, being more

constant.

D1 D2 D3 D4 D5 D6 D7 D8

Mean 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Variance 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

St.dev. 0.0021 0.0015 0.0012 0.0007 0.0007 0.0008 0.0007 0.0005

Skewness 2.3582 1.2937 0.7972 0.4710 1.0023 0.9296 0.9124 0.1532

Kurtosis 29.081 15.653 7.8281 2.4630 4.4679 2.5996 0.9124 -0.109

Table 4: OPEC frequencies descriptive statistics.

D1 D2 D3 D4 D5 D6 D7 D8

Mean 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Variance 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

St.dev. 0.0025 0.0017 0.0014 0.0009 0.0008 0.0009 0.0008 0.0005

Skewness 1.9878 1.0145 1.0059 0.0901 1.1811 0.9228 0.9122 0.0882

Kurtosis 37.332 14.457 9.6055 3.0776 5.9191 2.3422 1.3087 -0.279

Table 5: non-OPEC frequencies descriptive statistics.

As occurs in the original data, skewness is

always positive and decrease from D1 to D8, the

same occurs with kurtosis, due to long term of low-

frequencies, decrease the presence of outliers and

the series become smoother. The variance is 0.000

in all frequencies which according to Fan and

Gençay (2010) is due to the unit energy property

and indicates that the series are stationary after the

decomposition. Figure 3 shows the behavior of the

wavelet decomposed series.

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

33

Figure 3: Wavelet decomposed OPEC and non-OPEC volatilities.

The decomposed series present a different behavior

from the originals series. Despite the high

frequencies (D1, D2 and D3) to present volatility

clusters as well as the original series, the low

frequencies D4; D5; D6; D7 and D8 reveals that

both crude oil volatilities spread over time. As can

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

34

be observed, wavelet decomposition reveals that

crude oil volatility does not keep isolated in one

single event, it is capable to contaminate the

following periods. This means that considering

longer periods of observation

,

once the series are strike by bad or god news,

volatility does not come back to the level before

keeping their effects on the market. From a

different point of view Jin et al. (2012) conclude

that only large shocks will increase expected

conditional volatilities. This can be confirmed

for wavelet decomposition, once the volatility

seems to be embodied in futures periods.

This result can bring new information to oil market

agents. Long-term investors can be subject to

volatility effects for long periods, while short-term

investors are subject only to volatility. That does

not mean that short-term investors are less exposed

to risk, but means that long-term investors must to

monitor events for longer periods.

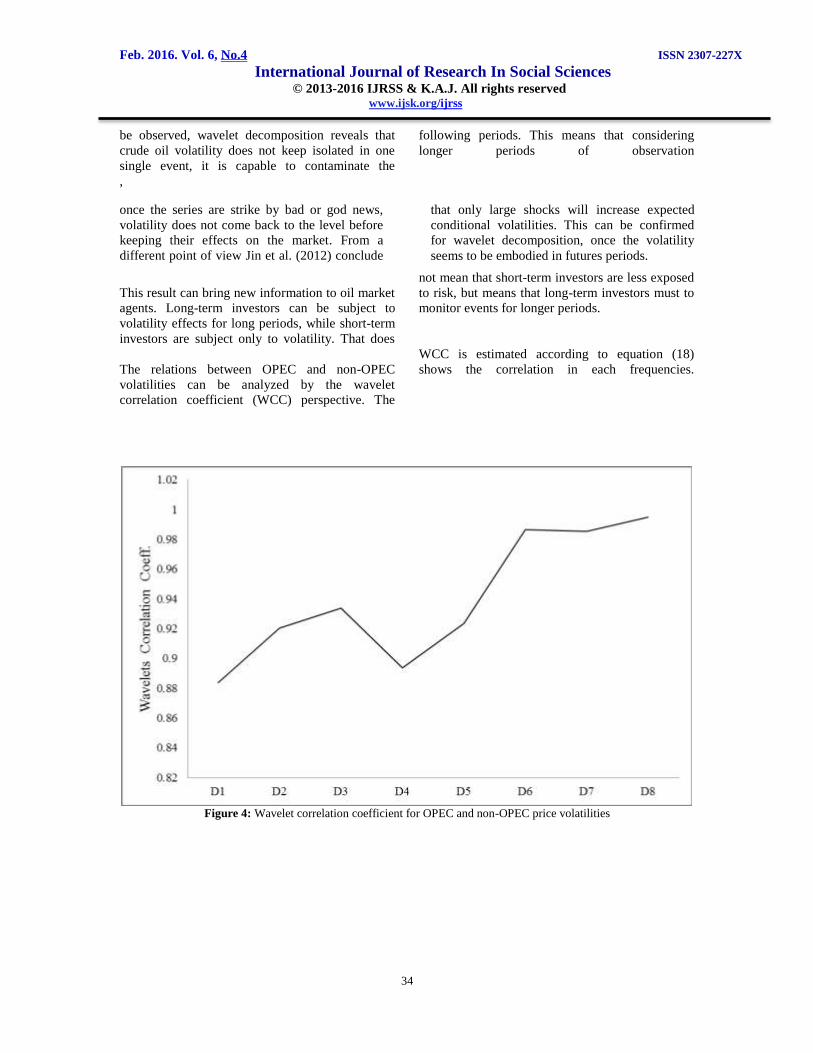

The relations between OPEC and non-OPEC

volatilities can be analyzed by the wavelet

correlation coefficient (WCC) perspective. The

WCC is estimated according to equation (18)

shows the correlation in each frequencies.

Figure 4: Wavelet correlation coefficient for OPEC and non-OPEC price volatilities

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

35

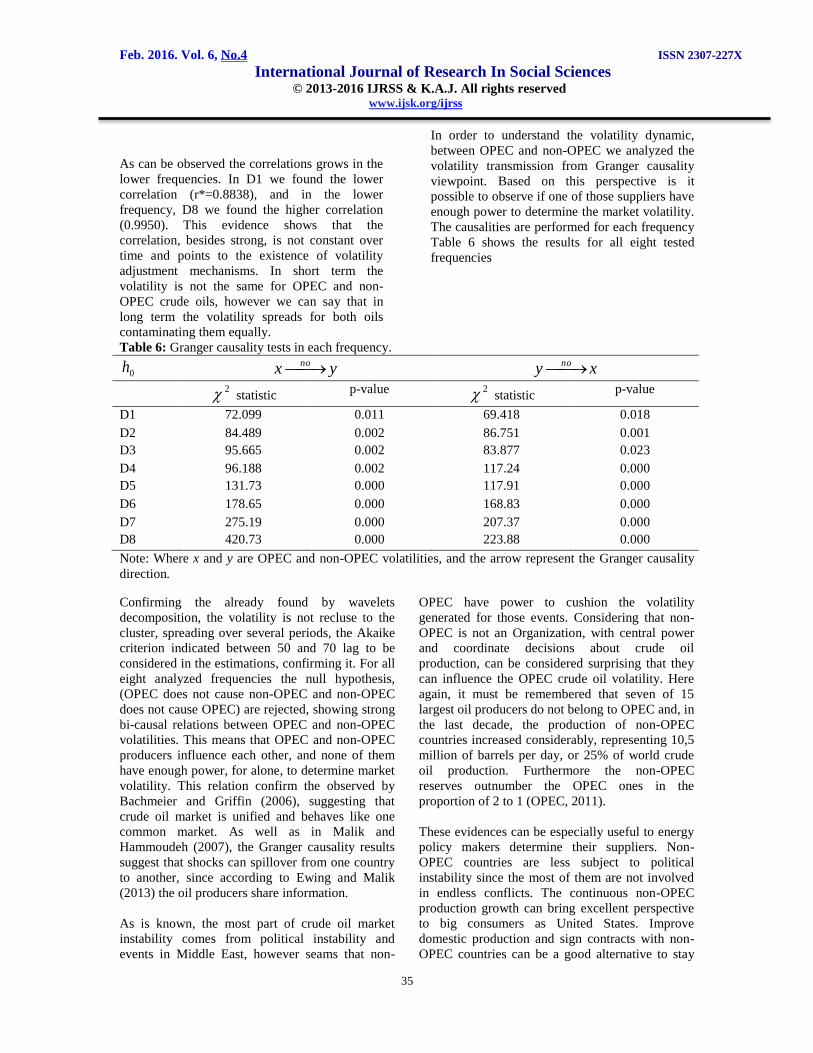

As can be observed the correlations grows in the

lower frequencies. In D1 we found the lower

correlation (r*=0.8838), and in the lower

frequency, D8 we found the higher correlation

(0.9950). This evidence shows that the

correlation, besides strong, is not constant over

time and points to the existence of volatility

adjustment mechanisms. In short term the

volatility is not the same for OPEC and non-

OPEC crude oils, however we can say that in

long term the volatility spreads for both oils

contaminating them equally.

In order to understand the volatility dynamic,

between OPEC and non-OPEC we analyzed the

volatility transmission from Granger causality

viewpoint. Based on this perspective is it

possible to observe if one of those suppliers have

enough power to determine the market volatility.

The causalities are performed for each frequency

Table 6 shows the results for all eight tested

frequencies

Table 6: Granger causality tests in each frequency.

0h yx no xy no

2 statistic p-value 2 statistic

p-value

D1 72.099 0.011 69.418 0.018

D2 84.489 0.002 86.751 0.001

D3 95.665 0.002 83.877 0.023

D4 96.188 0.002 117.24 0.000

D5 131.73 0.000 117.91 0.000

D6 178.65 0.000 168.83 0.000

D7 275.19 0.000 207.37 0.000

D8 420.73 0.000 223.88 0.000

Note: Where x and y are OPEC and non-OPEC volatilities, and the arrow represent the Granger causality

direction.

Confirming the already found by wavelets

decomposition, the volatility is not recluse to the

cluster, spreading over several periods, the Akaike

criterion indicated between 50 and 70 lag to be

considered in the estimations, confirming it. For all

eight analyzed frequencies the null hypothesis,

(OPEC does not cause non-OPEC and non-OPEC

does not cause OPEC) are rejected, showing strong

bi-causal relations between OPEC and non-OPEC

volatilities. This means that OPEC and non-OPEC

producers influence each other, and none of them

have enough power, for alone, to determine market

volatility. This relation confirm the observed by

Bachmeier and Griffin (2006), suggesting that

crude oil market is unified and behaves like one

common market. As well as in Malik and

Hammoudeh (2007), the Granger causality results

suggest that shocks can spillover from one country

to another, since according to Ewing and Malik

(2013) the oil producers share information.

As is known, the most part of crude oil market

instability comes from political instability and

events in Middle East, however seams that non-

OPEC have power to cushion the volatility

generated for those events. Considering that non-

OPEC is not an Organization, with central power

and coordinate decisions about crude oil

production, can be considered surprising that they

can influence the OPEC crude oil volatility. Here

again, it must be remembered that seven of 15

largest oil producers do not belong to OPEC and, in

the last decade, the production of non-OPEC

countries increased considerably, representing 10,5

million of barrels per day, or 25% of world crude

oil production. Furthermore the non-OPEC

reserves outnumber the OPEC ones in the

proportion of 2 to 1 (OPEC, 2011).

These evidences can be especially useful to energy

policy makers determine their suppliers. Non-

OPEC countries are less subject to political

instability since the most of them are not involved

in endless conflicts. The continuous non-OPEC

production growth can bring excellent perspective

to big consumers as United States. Improve

domestic production and sign contracts with non-

OPEC countries can be a good alternative to stay

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

36

less subject to crude oil volatility, cushioning bad

news.

Another important political and economic

conclusion comes from the fact that non-OPEC

even not being an Organization and still be able to

influence the crude oil volatility. If important non-

OPEC producers and consumers as United States,

Canada, Norway, Brazil, Russia, Mexico and China

have coordinate oil policy this influence could be

stronger.

CONCLUSIONS

Since its foundation, OPEC is in the center of crude

oil supply, its decisions and policy has determined

the market volatility. Especially in the last three

decades, crude oil market has gone through many

turbulent periods. Conflict, terrorist attacks and

financial crises have increased the market

volatility. At the same time, new reserves have

been discovered, and new countries have gained

important roles in this scenario, and now seven of

the 15 largest oil producers do not belong to this

organization.

To understand the role of OPEC and non-OPEC

crude oil in the market volatility, this study

employed the Wavelets methodology to decompose

the series and realize a detailed frequency analysis

of volatility transmission in this market. It’s

possible to observe that crude oil volatility is not

restrict clusters, the frequency analysis reveal that

it spreads over time contaminating futures periods.

The correlation between OPEC and non-OPEC

price volatilities is not constant, changing in each

frequency. It is possible to observe that the wavelet

correlation coefficient grows in the lower

frequencies pointing to the existence of volatility

adjustment mechanisms, which are confirmed by

the volatility transmission analysis.

The strong bi-causal relation between OPEC and

non-OPEC crude oil volatilities confirms the found

by Bachmeier and Griffin (2006), and show

evidences that non-OPEC has e has as much force

as OPEC to influence the market volatility,

suggesting volatility spillovers between both.

Considering that non-OPEC is not an Organization,

with central power and coordinate decisions about

crude oil production, can be considered surprising

that they can influence the OPEC crude oil

volatility. If important non-OPEC producers and

consumers have coordinate oil policy this influence

could be stronger.

The increasing participation of non-OPEC

countries in the oil production can be the reason

behind this behavior. Those evidences can be

especially useful to energy policy makers

determine their suppliers, since Non-OPEC

countries are less subject to political instability

since the most of them are not involved in endless

conflicts.

To improve this research, we suggest the use of

structural breaks and copula function to model the

volatility. The absence of longer series, with

previous periods is a limitation of this study, since

was not possible to verify if this behavior was the

same before 1997.

References:

1. Adelman, M.A., 1992. Is the world oil

market ‘one great pool’? – Comment.

Energy J. 13 (1), 157–158.

2. Alvarez-Ramirez, J. Alvarez, E.

Rodriguez, G. Fernandez-Anaya, 2008.

Time-varying Hurst exponent for US

stock markets, Physica A 387 6159-6169.

3. Bachmeier, L.J., Griffin, J.M., 2006.

Testing for market integration crude, oil,

coal, and natural gas. Energy J. 27 (2),

55–71.

4. Benhmad, F. (2012). Modeling nonlinear

Granger causality between the oil price

and .U.S. dollar: A wavelet based

approach. Economic Modelling, 29,

1505–1514.

5. Bentzem, J. 2007. Does OPEC influence

crude oil prices? Testing for co-

movements and causality between

regional crude oil prices. Applied

Economics. v. 39, Issue 11.

6. Capobianco, E. 2003. Empirical volatility

analysis: feature detection and signal

extraction with function dictionaries.

Physica A, A319 495 – 518.

7. Cheung, C.S., Kwan, C., 1992. A note on

the transmission of public information

across international stock markets. J.

Bank. Finance 16, 831–837.

Feb. 2016. Vol. 6, No.4 ISSN 2307-227X

International Journal of Research In Social Sciences © 2013-2016 IJRSS & K.A.J. All rights reserved www.ijsk.org/ijrss

37

8. de Souza e Silva, E.G., Legeya, L., de

Souza e Silva E. A., 2010, Forecasting oil

price trends using wavelets and hidden

Markov models Energy Economics 32,

1507–1519.

9. Engle, R.F., Granger, C.W.J., 1987. Co-

integration and error correction:

representation, estimation and testing.

Econometrica 55, 251–276.

10. Ewing, B.T., Harter, C.L., 2000. Co-

movements of Alaskan North Slope and

UK Brent crude oil prices. Applied.

Economic. Letters. 7, 553–558.

11. Granger, C. W. J., 1961. Invetigating

causal relations by econometric models.

Econometrica, 37, 424 - 438.

12. Gulen, S.G., 1999. Regionalization in the

world crude oil market: further evidence.

Energy J. 20 (1), 125–139.

13. Hong Y. A. Test for volatility spillover

with application to exchange rates.

Journal of Econometrics, 103), pp. 183–

224, 2001.

14. Jammazi, R., Aloui, C. Wavelet

decomposition and regime shifts:

Assessing the effects of crude oil shocks

on stock market returns. Energy Policy 38,

1415–1435.

15. Jin, X., Lin S. X.; Tamvakis, M.; JIN, X.

et al. Volatility transmission and volatility

impulse response functions in crude oil

markets. Energy Economics, 34 (2012)

2125–2134.

16. Malik, F.; Hammoudeh, S. Shock and

volatility transmission in the oil, US and

Gulf equity markets International Review

of Economics and Finance 16, 357–368.

17. Narayan, P.K.,Popp,S., 2010. A new unit

root test with two structural breaks in

level and slope at unknown time. Journal

of Applied Statistics 37 (9), 1425–1438.

18. Ng, V.K., Chang, R.P., Chou, R.Y., 1991.

An examination of the behavior of Pacific

basin stock market volatility. In: Rhee,

S.G., Chang, R. (Eds.), Pacific Basin

Capital Markets Research, vol. II. Elsevier

Science Publishers, Amsterdam,.

19. Nishiyama Y., The term structure of CD

rates and monetary policy transmission.

Journal of Banking & Finance, 35, 82–94,

2011.

20. Organization of Oil Exporting Countries,

2011. OPEC Annuary,. Avaiable at

http://www.opec.org. Accessed at

2/13/2013.

21. Power, G.J. and Turvey C.G. (2010).

Long-range dependence in the volatility of

commodity futures prices: Wavelet-based

evidence. Physica A, 389, 79-90.

22. Razdan, A., 2004. Wavelet correlation

coefficient of ‘strongly correlated’ time

series. Physica A, 333, 335 – 342.

23. Salisu, A. A., Fasanya, I.O., 2013.

Modelling oil price volatility with

structural breaks. Energy Policy 52, 554–

562.

24. Souza e Silva, E. G., Legey, L. F., Souza e

Silva, E. A. (2010). Forecasting oil price

trends using wavelets and hidden Markov

models Energy Economics 32 1507–1519.

25. Tsay, R., S. 2008.. Analysis of Financial

Time Series. 3 ed. New Jersey.John Wiley

& Sons,

26. Wang, Z., 2010. Dynamics and causality

in industry-specific volatility. Journal of

Banking & Finance 34, 1688–1699.

27. Weiner, N., Extrapolation, Interpolation,

and Smoothing of Stationary Time Series.

Wiley, New York. 1949.