Embed Size (px)

Citation preview

presents

Federal Consolidated Return Regulations for Corporate Taxpayers

presents

Corporate Taxpayers Mastering Complex Rules and Guidance to Ensure Ongoing Compliance

A Live 110-Minute Teleconference/Webinar with Interactive Q&A

Today's panel features:Robert G. Lorndale, Jr., Tax Partner, Dewey & LeBoeuf, Washington, D.C.

Michelle Albert, Senior Manager, Transaction Advisory Services – Tax, Ernst & Young, Washington, D.C.D B d h P i i l W hi t N ti l T C t P ti KPMG W hi t D C

Q&

Devon Bodoh, Principal, Washington National Tax Corporate Practice, KPMG, , Washington, D.C.

Thursday, July 1, 2010

The conference begins at:The conference begins at:1 pm Eastern12 pm Central

11 am Mountain10 am Pacific10 am Pacific

You can access the audio portion of the conference on the telephone or by using your computer's speakers.Please refer to the dial in/ log in instructions emailed to registrations.

For Continuing Education purposes, gplease let us know how many people are listening at your location by g y y

• closing the notification box • and typing in the chat box your• and typing in the chat box your

company name and the number of attendeesattendees.

• Then click the blue icon beside the box to sendto send.

For live event only

• If the sound quality is not satisfactory• If the sound quality is not satisfactory and you are listening via your computer speakers please dial 1-866-871-8924speakers, please dial 1 866 871 8924 and enter your PIN when prompted. Otherwise, please send us a chat or e-, pmail [email protected] so we can address the problem.

• If you dialed in and have any difficulties during the call, press *0 for assistance.

Federal Consolidated Return Regulations For Corporate

Taxpayers Webinarp y

July 1, 2010July 1, 2010

Robert Lorndale, Dewey & LeBoeuf [email protected]

Michelle Albert, Ernst & Young [email protected]

Devon M. Bodoh, KPMG [email protected]

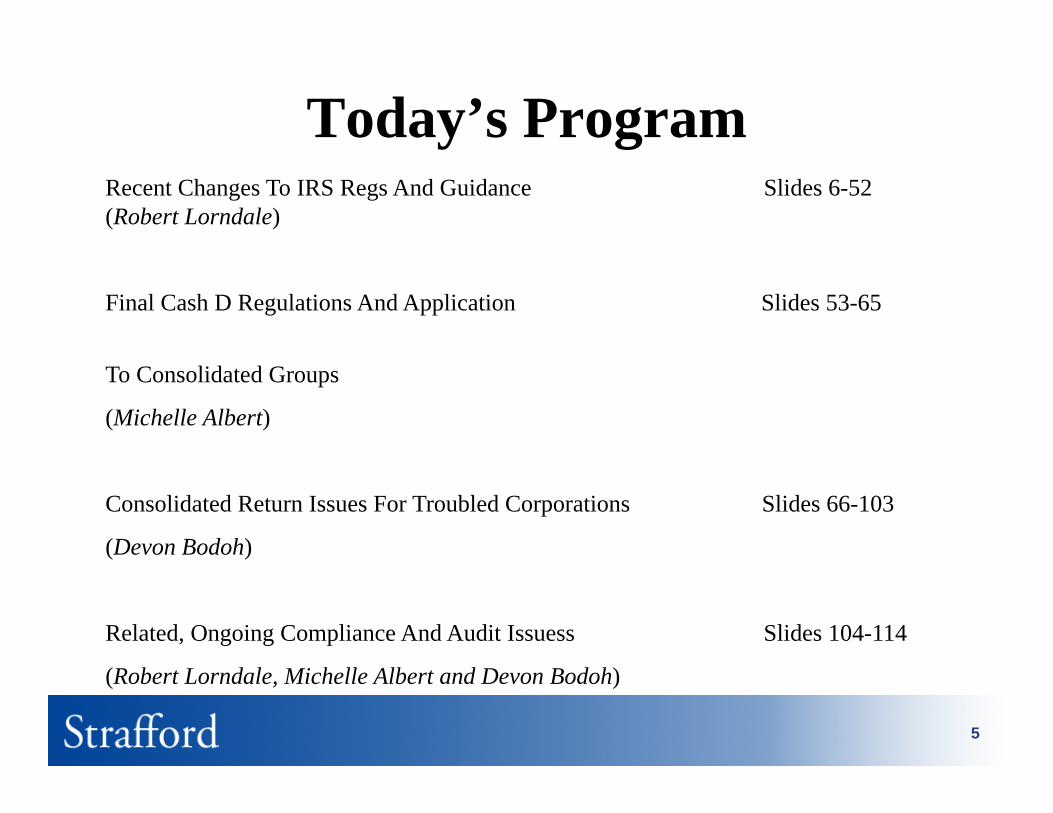

Today’s ProgramRecent Changes To IRS Regs And Guidance Slides 6-52 (Robert Lorndale)

Final Cash D Regulations And Application Slides 53-65

To Consolidated Groups

(Michelle Albert)

Consolidated Return Issues For Troubled Corporations Slides 66-103

(Devon Bodoh)

Related, Ongoing Compliance And Audit Issuess Slides 104-114

5

(Robert Lorndale, Michelle Albert and Devon Bodoh)

Recent Changes To IRS R A d G idRegs And Guidance

Robert Lorndale, Dewey & LeBoeuf LLPRobert Lorndale, Dewey & LeBoeuf LLP

Unified Loss Rule§1.1502-36

T.D. 9424 (9/10/2008)

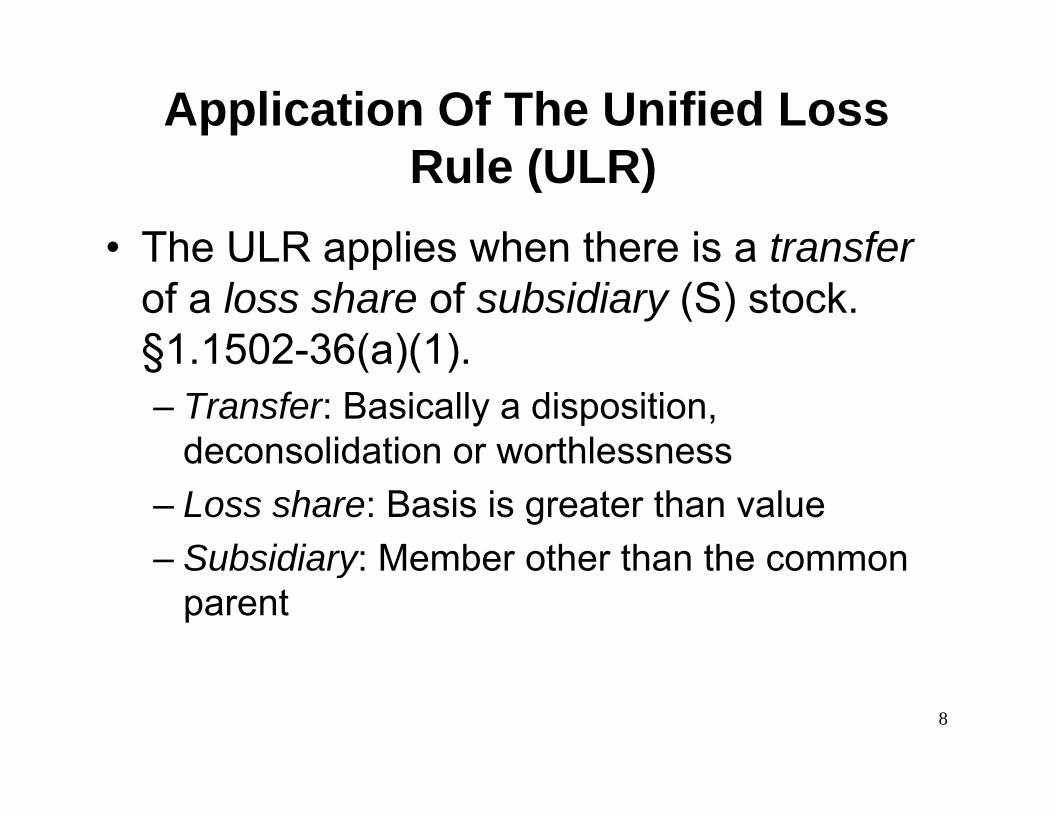

Application Of The Unified LossR l (ULR)Rule (ULR)

• The ULR applies when there is a transferThe ULR applies when there is a transferof a loss share of subsidiary (S) stock. §1 1502-36(a)(1)§1.1502 36(a)(1).– Transfer: Basically a disposition,

deconsolidation or worthlessnessdeconsolidation or worthlessness– Loss share: Basis is greater than value– Subsidiary: Member other than the common– Subsidiary: Member other than the common

parent

8

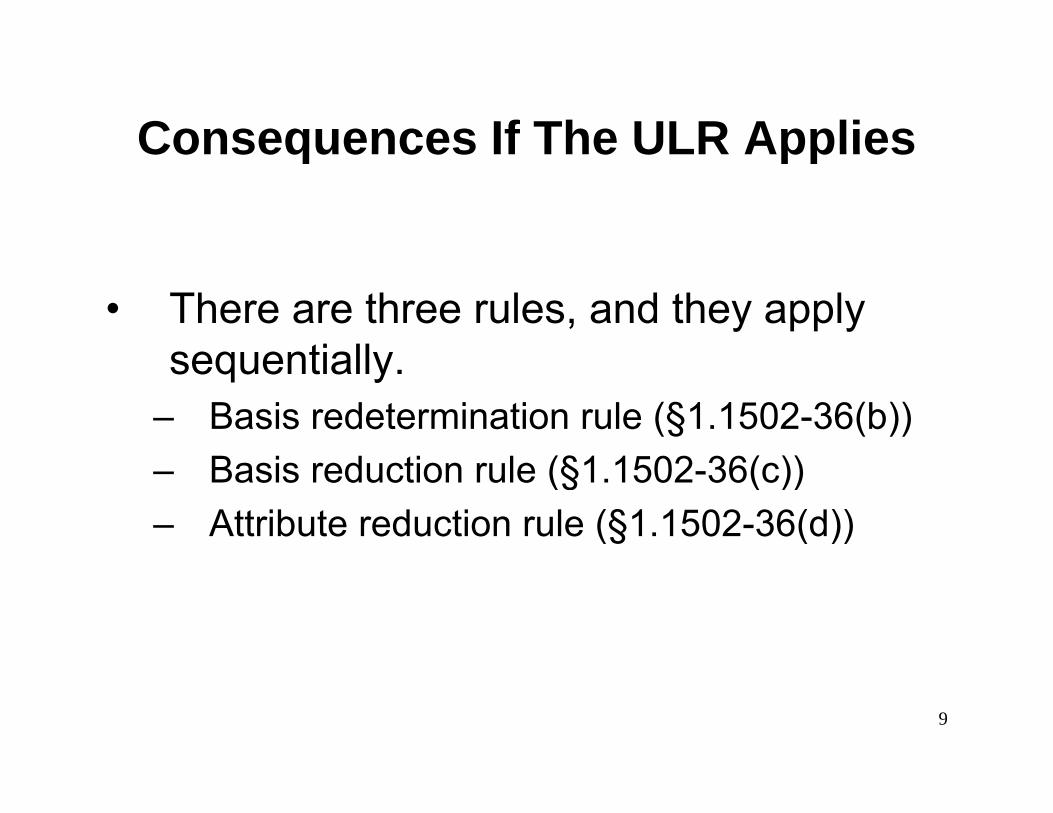

Consequences If The ULR AppliesConsequences If The ULR Applies

• There are three rules, and they apply sequentiallysequentially.

– Basis redetermination rule (§1.1502-36(b))B i d ti l (§1 1502 36( ))– Basis reduction rule (§1.1502-36(c))

– Attribute reduction rule (§1.1502-36(d))

9

Goal Of ULR• One integrated set of rules applies to all

transactions in which non economic and/ortransactions in which non-economic and/or duplicated stock loss is either recognized or preserved for later useor preserved for later use.– Basis redetermination rule of §1.1502-36(b)

addresses losses arising from non economicaddresses losses arising from non-economic allocations under §1.1502-32.Basis reduction rule of §1 1502 36(c)– Basis reduction rule of §1.1502-36(c) addresses non-economic “son of mirror” loss.

– Attribute reduction rule of §1 1502-36(d)10

Attribute reduction rule of §1.1502 36(d) addresses duplicated loss.

Basis Redetermination §1.1502-36(b)

Basis RedeterminationBasis Redetermination

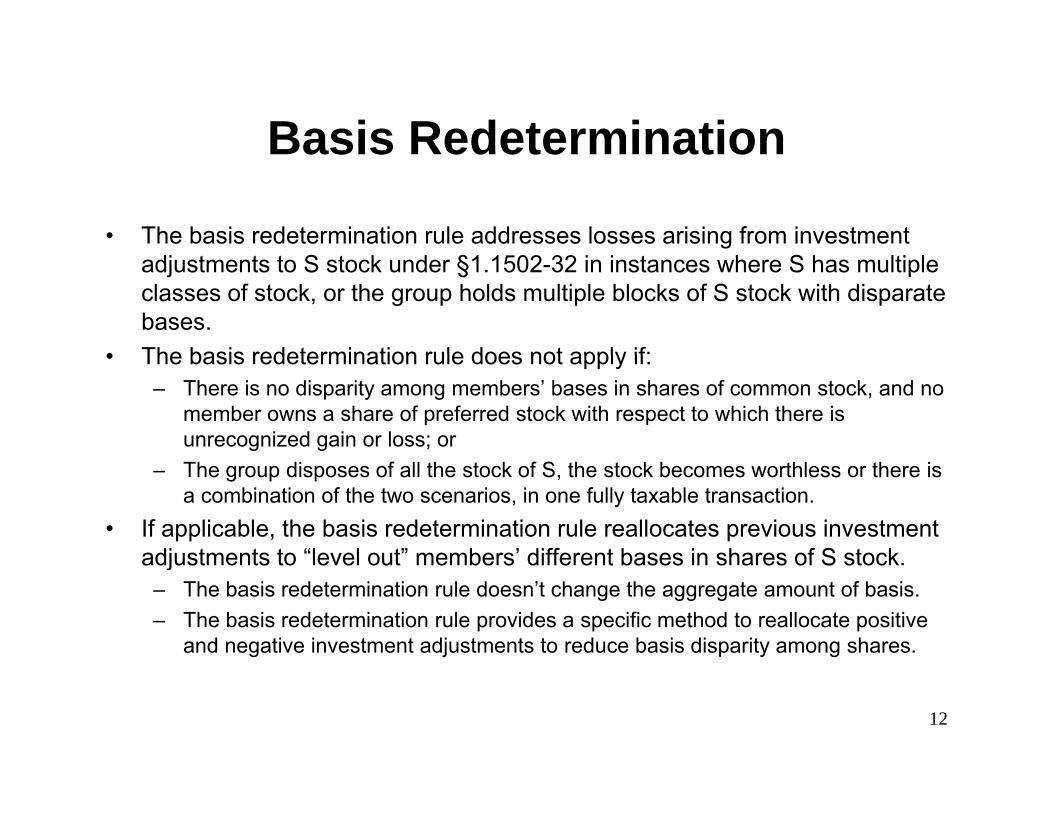

• The basis redetermination rule addresses losses arising from investment adjustments to S stock under §1.1502-32 in instances where S has multiple classes of stock, or the group holds multiple blocks of S stock with disparate bases.

• The basis redetermination rule does not apply if:• The basis redetermination rule does not apply if:– There is no disparity among members’ bases in shares of common stock, and no

member owns a share of preferred stock with respect to which there is unrecognized gain or loss; or

– The group disposes of all the stock of S, the stock becomes worthless or there is a combination of the two scenarios, in one fully taxable transaction.

• If applicable, the basis redetermination rule reallocates previous investment adjustments to “level out” members’ different bases in shares of S stockadjustments to level out members different bases in shares of S stock.

– The basis redetermination rule doesn’t change the aggregate amount of basis.– The basis redetermination rule provides a specific method to reallocate positive

and negative investment adjustments to reduce basis disparity among shares.

12

Basis Reduction§1.1502-36(c)

Basis Reduction:Th P blThe Problem

P PP

AB $110

P

AB $210

SS sellsland for

$110

SP sells S stock for

$110$110LandAB $10FMV $110

$110

• Facts: P purchases the stock of S for $110. S’ sole asset is land with a value of $110 and basis of $10. S sells the land giving rise to a gain of $100 that the P group includes on its consolidated return. Under §1.1502-32, P increases its basis in the S t k b $100 t $210 L t P ll th S t k f $110

14

stock by $100 to $210. Later, P sells the S stock for $110.• Result: Without a basis reduction rule, P’s $100 non-economic loss on the sale of S

stock is allowed.

Basis Reduction (Cont.)Basis Reduction (Cont.)

• Based on “simplifying conventions”p y g• Tracing is not an option.• This rule:

– Reaches the correct economic result in the simple “son of mirror” case

– Can allow “son of mirror” losses that tracing would disallowg– Can disallow economic losses that tracing would allow

• This rule is “balanced” in the sense that some taxpayers have economic losses disallowed and others have nonhave economic losses disallowed and others have non-economic losses allowed.

15

Basis Reduction (Cont.)Basis Reduction (Cont.)

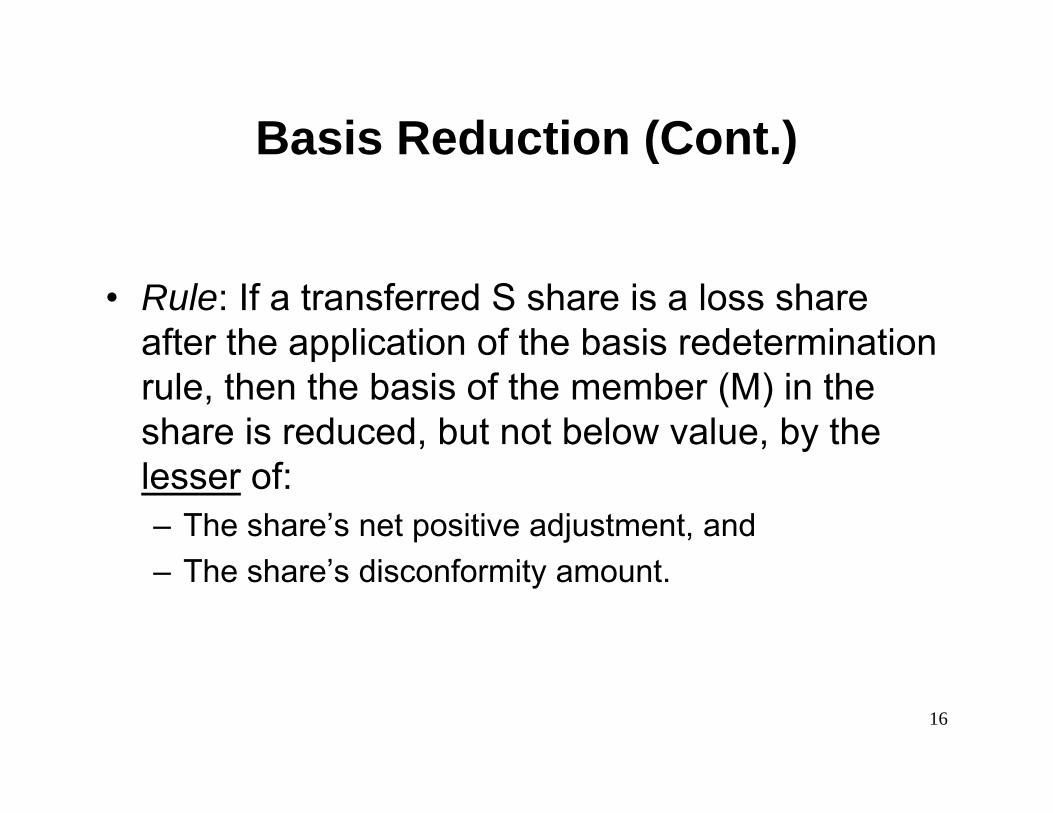

• Rule: If a transferred S share is a loss share after the application of the basis redetermination pprule, then the basis of the member (M) in the share is reduced, but not below value, by the lesser of:– The share’s net positive adjustment, and

Th h ’ di f it t– The share’s disconformity amount.

16

Basis Reduction (Cont.)Basis Reduction (Cont.)

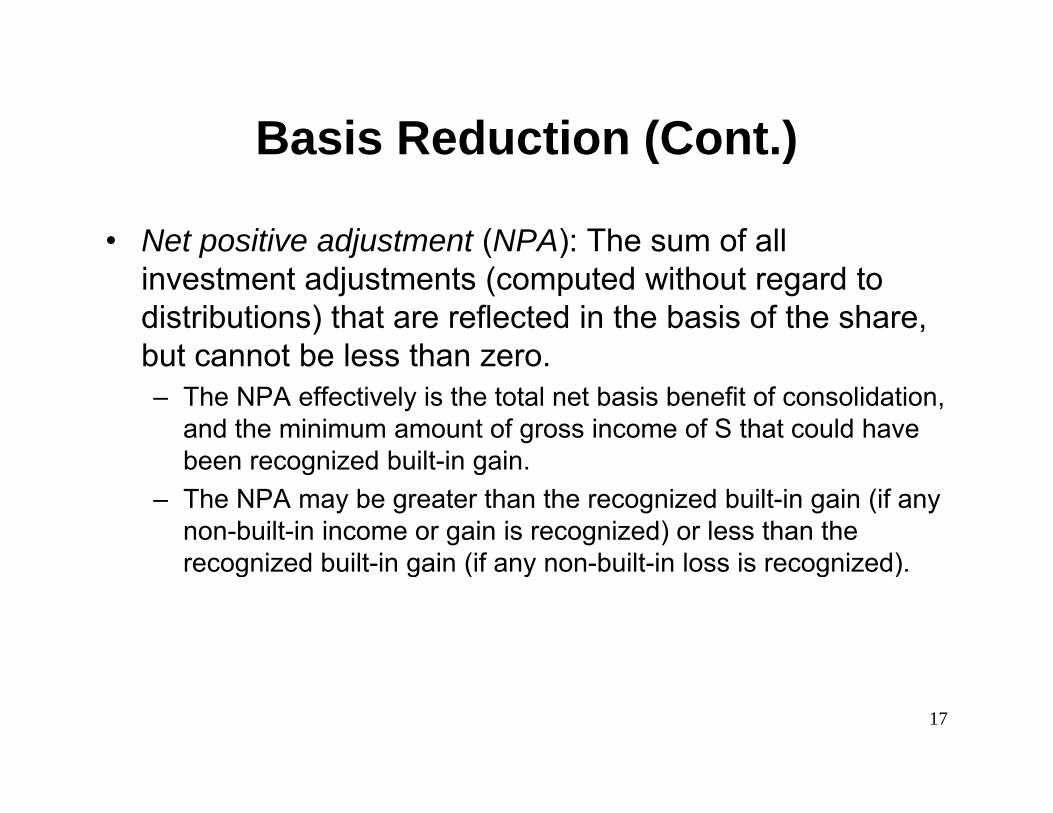

• Net positive adjustment (NPA): The sum of all p j ( )investment adjustments (computed without regard to distributions) that are reflected in the basis of the share, but cannot be less than zerobut cannot be less than zero.– The NPA effectively is the total net basis benefit of consolidation,

and the minimum amount of gross income of S that could have been recognized built in gainbeen recognized built-in gain.

– The NPA may be greater than the recognized built-in gain (if any non-built-in income or gain is recognized) or less than the recognized built in gain (if any non built in loss is recognized)recognized built-in gain (if any non-built-in loss is recognized).

17

Basis Reduction (Cont.)Basis Reduction (Cont.)

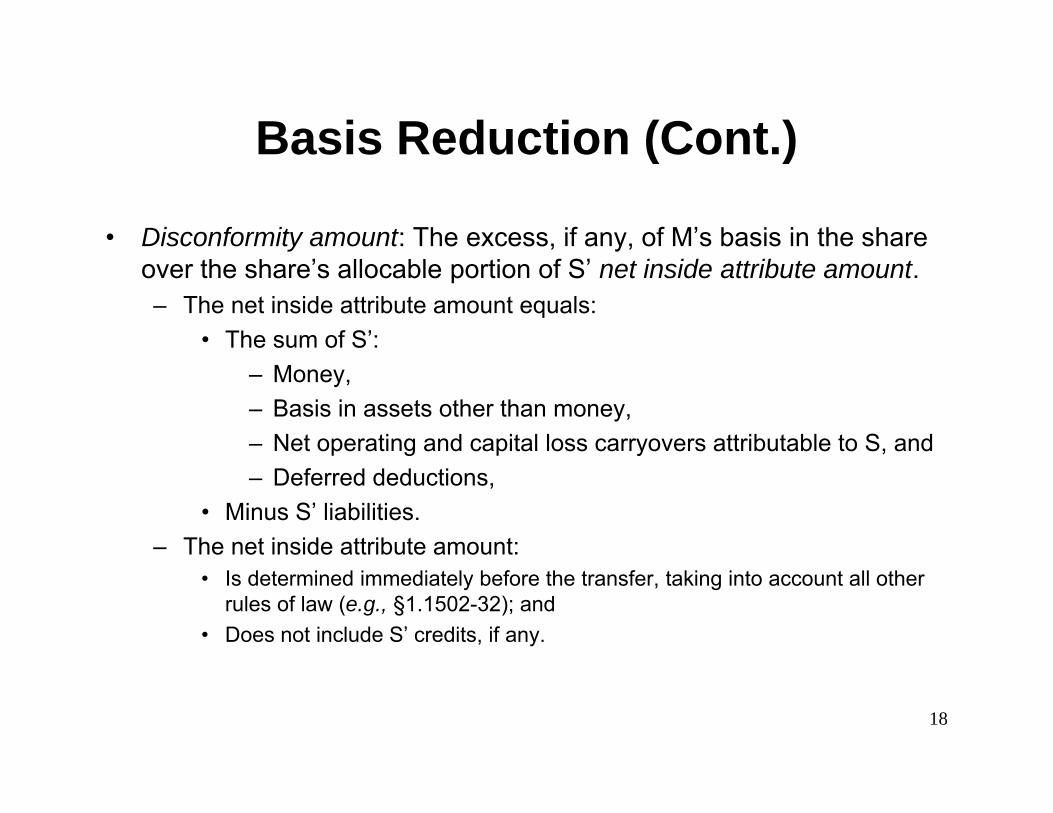

• Disconformity amount: The excess, if any, of M’s basis in the share over the share’s allocable portion of S’ net inside attribute amount.– The net inside attribute amount equals:

• The sum of S’:– Money,– Basis in assets other than money,– Net operating and capital loss carryovers attributable to S, and– Deferred deductions,

• Minus S’ liabilities.– The net inside attribute amount:

• Is determined immediately before the transfer, taking into account all other rules of law (e.g., §1.1502-32); and

• Does not include S’ credits, if any.

18

Attribute Reduction§1.1502-36(d)

Attribute Reduction:Th P blThe Problem

P PP AB $100FMV $100

P P

AB $100FMV $80

AB $100FMV $100 $80

S

AB $100

S S

AB $100 AB $100

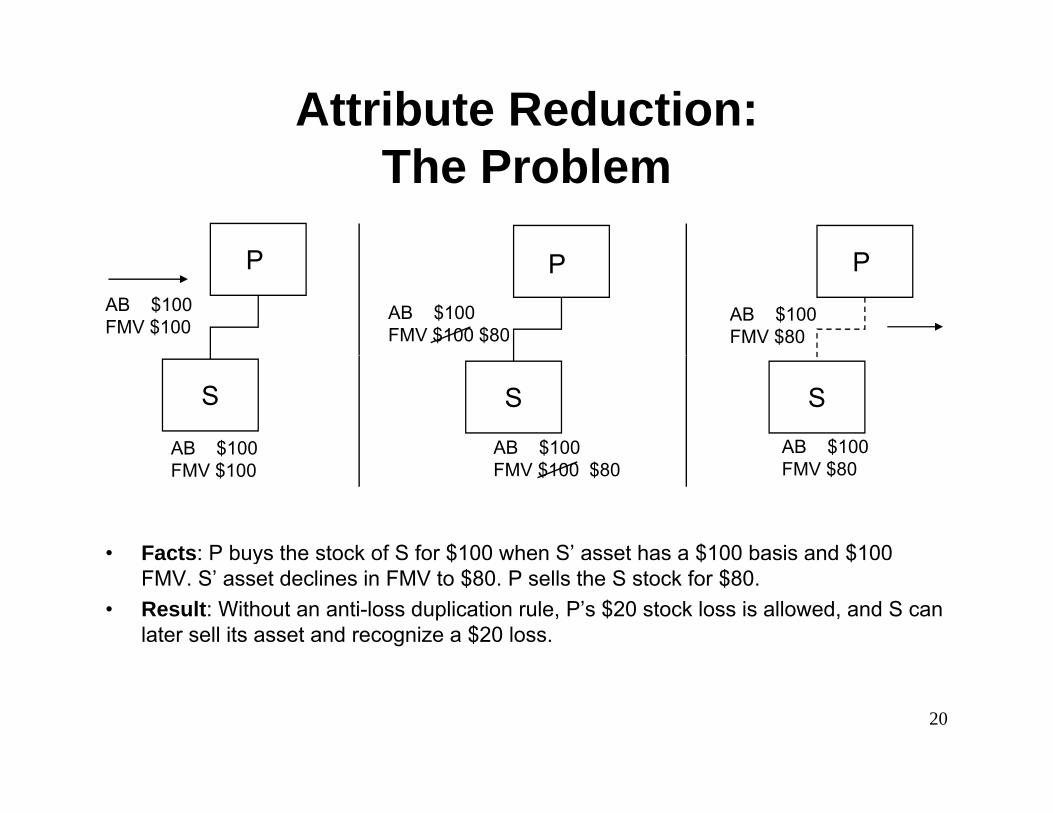

• Facts: P buys the stock of S for $100 when S’ asset has a $100 basis and $100

FMV $100 FMV $100 $80 FMV $80

y $ $ $FMV. S’ asset declines in FMV to $80. P sells the S stock for $80.

• Result: Without an anti-loss duplication rule, P’s $20 stock loss is allowed, and S can later sell its asset and recognize a $20 loss.

20

Attribute Reduction (Cont.)Attribute Reduction (Cont.)

• If a transferred share is a loss share after the application of the basis d ti l S’ tt ib t d d b S’ tt ib t d tireduction rule, S’ attributes are reduced by S’ attribute reduction

amount (ARA), which is the lesser of:– Net stock loss: The excess, if any, of members’ aggregate bases in

transferred S shares over the aggregate value of those sharestransferred S shares over the aggregate value of those shares– S’ aggregate inside loss: The excess, if any, of S’ net inside attributes

(inside asset basis plus losses minus liabilities) over the value of all outstanding shares of S stockg

• Attribute reduction rule does NOT apply if the ARA is less than 5% of the value of the shares transferred.– However, the group may elect to apply the rule, e.g., in order toHowever, the group may elect to apply the rule, e.g., in order to

reattribute S’ losses.

21

ARA: The BasicsARA: The Basics

• S’ ARA is applied:pp– First, to reduce recognized losses:

• Capital loss carryovers,• Net operating loss carryovers and• Net operating loss carryovers, and• Deferred deductions

– Then, to reduce asset basis

• The selling group may specify the losses to which the ARA is applied. To the extent the group doesn’t specify, they are reduced in the following order:they are reduced in the following order:– Capital loss carryovers (oldest to newest),– Net operating loss carryovers (oldest to newest), and

D f d d d ti ( ti t l )22

– Deferred deductions (proportionately)

ARA: The Basics (Cont.)ARA: The Basics (Cont.)

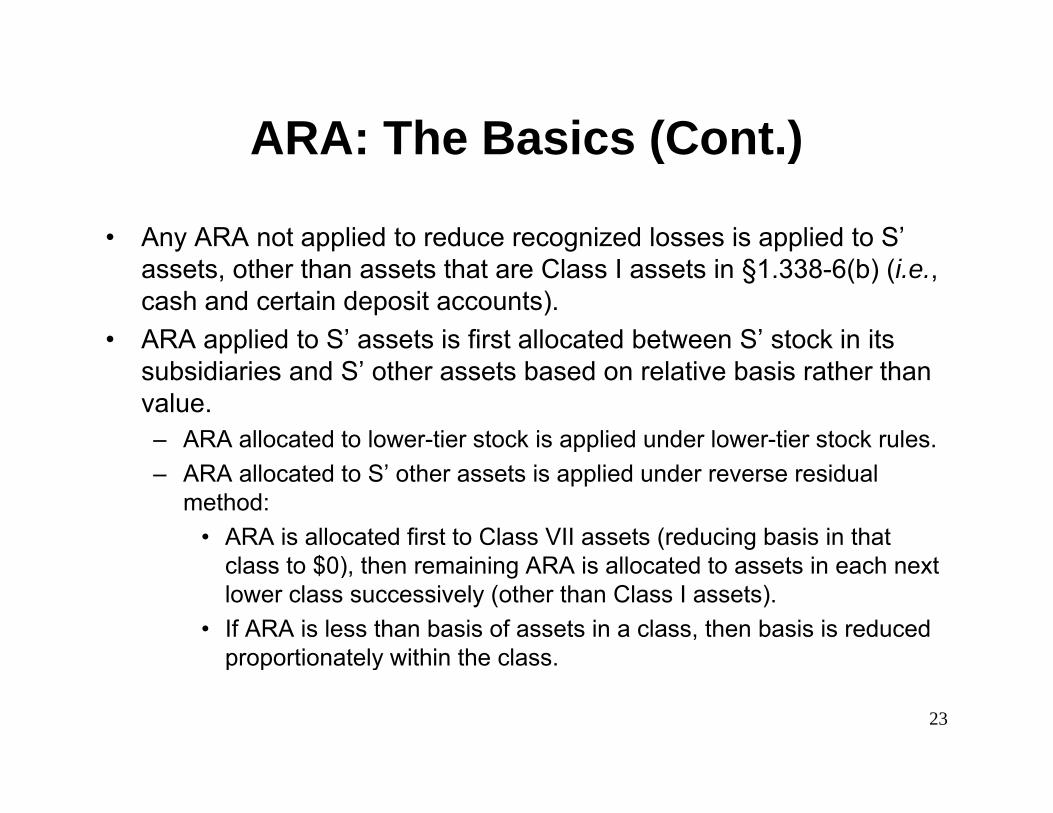

• Any ARA not applied to reduce recognized losses is applied to S’ assets, other than assets that are Class I assets in §1.338-6(b) (i.e., cash and certain deposit accounts).

• ARA applied to S’ assets is first allocated between S’ stock in its subsidiaries and S’ other assets based on relative basis rather than value.– ARA allocated to lower-tier stock is applied under lower-tier stock rules.– ARA allocated to S’ other assets is applied under reverse residual

method: • ARA is allocated first to Class VII assets (reducing basis in that

l t $0) th i i ARA i ll t d t t i h tclass to $0), then remaining ARA is allocated to assets in each next lower class successively (other than Class I assets).

• If ARA is less than basis of assets in a class, then basis is reduced proportionately within the class.

23

proportionately within the class.

ARA: The Basics (Cont.)ARA: The Basics (Cont.)

• If the ARA exceeds attributes, then it has no further ,effect unless S has contingent liabilities (in which case the excess ARA is suspended and applied as attributes attributable to those liabilities are taken into account)attributable to those liabilities are taken into account).

• Reductions are effective immediately before the transferReductions are effective immediately before the transfer of S shares.

• Attribute reduction is NOT treated as a non-capital, non-deductible expense so as to prevent duplicative stock basis reductions under §1.1502-32.

24

basis reductions under §1.1502 32.

§1.1502-36(d)(6) Election§1.1502 36(d)(6) Election• Selling group can avoid or reduce attribute reduction by electing to reduce

members’ bases in transferred loss shares reattribute S’ attributes to P (butmembers bases in transferred loss shares, reattribute S attributes to P (but only if S leaves the group), or both.

– Can specify amount elected (or not elected)– Can only reattribute up to ARA. No effect is given to election for any amount in

excess of ARA. However, P can make a protective election to reduce basis.– Can reattribute §382 limitation to which reattributed losses are subject– Stock basis reduction is deemed elected if the stock loss would be permanently

disallowed (e.g., under §311(a)).disallowed (e.g., under §311(a)).• P can specify the losses to be reattributed; otherwise, losses are

reattributed in the manner in which they would have been reduced under the default rule.

• In effect, through an election to reattribute S’ NOL, the parties can convert what would otherwise be a current capital loss for the seller on the S stock, or an NOL carryover subject to §382 for the buyer, to an NOL carryover not limited by §382 for the seller

25

limited by §382 for the seller.

Anti-Avoidance RulesAnti Avoidance Rules

• Anti-avoidance rules are intended to prevent (among p ( gother things) attempts to avoid the §1.1502-36(d) rules.

• Under §1.1502-36(g), if a taxpayer acts with a view to id th f §1 1502 36 t l §1 1502 36avoid the purposes of §1.1502-36 or to apply §1.1502-36

to avoid the purposes of any other rule of law, appropriate adjustments will be made to carry out the purposes of §1.1502-36 or such other rule of law.

• A separate anti-abuse rule in §1.1502-80(h)(2) applies when (1) §362(e)(2) would apply but for its nonwhen (1) §362(e)(2) would apply but for its non-application to consolidated group intercompany transactions, and (2) the taxpayer has a view to

26

inappropriately duplicate loss.

ULR: Seller IssuesULR: Seller Issues

• The common parent (P) should be thinking about:The common parent (P) should be thinking about:– Is there a loss in the S stock after applying all other rules of

law?• Consider the possible treatment of transaction costs as• Consider the possible treatment of transaction costs as

an offset to purchase price (and presumably amount realized), or potentially an increase to stock basis.

– Will any of the stock loss be eliminated as a result of the– Will any of the stock loss be eliminated as a result of the basis reduction rule (i.e., is any of the loss non-economic)?

– Do S (or any lower-tier subsidiaries) have any losses or deferred deductions that might be carried out of the group?deferred deductions that might be carried out of the group?

27

ULR: Seller Issues (Cont.)ULR: Seller Issues (Cont.)

• Are any of the S (or lower-tier subsidiary) losses or deductionsAre any of the S (or lower tier subsidiary) losses or deductions eligible for reattribution?– Would the losses otherwise be reduced?– If there are lower-tier subsidiaries is there sufficient stock– If there are lower-tier subsidiaries, is there sufficient stock

basis?– Character, quality (SRLY, §382 limited, etc.) and ability to

utilize vs value to buyer are factors to considerutilize vs. value to buyer are factors to consider.• What is the potential impact of the ULR on S’ (or any lower-tier

subsidiary’s) other attributes (i.e., what will buyer be getting)?

Note: It is essential for P to model the potential tax impact of the ULRto determine the available elections, impact and other planningopportunities

28

opportunities.

ULR: Buyer IssuesULR: Buyer Issues

• Buyer should be thinking about:– Will the selling group recognize a loss on the S stock after

applying the basis redetermination rule and the basis pp y greduction rule?

– Can P reattribute any losses or deferred deductions from S (or any lower-tier subsidiaries)?( y )

– What is the potential impact of the ULR on S’ (or any lower-tier subsidiary’s) other attributes (i.e., what will buyer be getting)?g g)

29

ULR: Buyer Issues (Cont.)ULR: Buyer Issues (Cont.)

• What is the potential financial statement impact if S (or anyWhat is the potential financial statement impact if S (or any lower-tier subsidiaries) experience a significant amount of attribute reduction?

• It is critical that the buyer be thinking up-front about negotiating P’s elections to reattribute losses or deductions, or to reduce stock basis.stock basis.

Note: It is essential for buyer to model the potential tax impact of theULR to determine what it is buying and the scope of potentialelections it might want to negotiate.

30

g g

Intercompany Obligations§1.1502-13(g)

Intercompany Obligation R l ti Hi tRegulations: History

• §1.1502-13(g) was originally issued in 1995.• In 1998 proposed regulations were issuedIn 1998, proposed regulations were issued.• In 2007, new proposed regulations were issued,

and the regulations proposed in 1998 wereand the regulations proposed in 1998 were withdrawn.

• Each version of the regulations employed a ac e s o o t e egu at o s e p oyed adeemed satisfaction and reissuance (DSR) model.

32

Intercompany Obligation R l ti C tRegulations: Current

• On Dec. 24, 2008, new final regulations (2008On Dec. 24, 2008, new final regulations (2008 final regulations) were issued regarding the treatment of certain transactions involving obligations between members of a consolidated group.

• The 2008 final regulations are effective for transactions involving intercompany obligations occurring in consolidated return years beginningoccurring in consolidated return years beginning on or after Dec. 24, 2008.

33

Intercompany ObligationIntercompany Obligation

• Obligation of member: Any obligationObligation of member: Any obligation constituting debt for federal income tax purposes or certain securities of a memberpurposes or certain securities of a member

I t bli ti A bli ti• Intercompany obligation: Any obligation between members of the same

lid t dconsolidated group

34

Application Of 2008 Final R l tiRegulations

• The 2008 final regulations generally apply toThe 2008 final regulations generally apply to three types of transactions:– Transactions in which an intercompany obligation

ceases to be an intercompany obligation,– Transactions in which an intercompany obligation is

assigned or extinguished within the consolidatedassigned or extinguished within the consolidated group, and

– Transactions in which a non-intercompany obligation p y gbecomes an intercompany obligation.

35

2008 Final Regulations:Intragroup And OutboundIntragroup And Outbound

Transactions• The DSR model is retained for transactions thatThe DSR model is retained for transactions that

are “triggering transactions,” but the DSR model does not apply in enumerated exceptions.– Exception to DSR may be subject to the tax benefit

rule.DSR i di t l b f d• DSR occurs immediately before, and independently of, the transaction giving rise to the DSRthe DSR.

• DSR is generally at fair market value.

36

2008 Final Regulations:Intragroup And OutboundIntragroup And Outbound

Transactions (Cont.)• DSR applies to triggering transactions• DSR applies to triggering transactions.• A triggering transaction includes an intercompany transaction in

which a member realizes an amount from the assignment or extinguishment of an intercompany obligation (“intragroupextinguishment of an intercompany obligation ( intragroup transactions”).– Examples of intragroup transactions include bad debt deductions and

mark-to-market transactions.mark to market transactions.– However, a creditor’s reduction of the basis of an intercompany

obligation under §1.1502-36(d) or §§108 and 1017 and §1.1502-28 (basis reductions upon the exclusion of COD income from gross income) is not an intragroup transaction.

• A triggering transaction also includes a transaction in which an intercompany obligation becomes a non-intercompany obligation (“ b d i ”)

37

(“outbound transactions”).

2008 Final Regulations:Intragroup And OutboundIntragroup And Outbound

Transactions (Cont.)• Deemed satisfaction under §1.1502-13(g)(3)Deemed satisfaction under §1.1502 13(g)(3)

– Intercompany obligation is deemed satisfied for all federal income tax purposes immediately before the triggering transaction

• Deemed satisfaction transaction is separate from actual transaction.p• Obligation is generally deemed satisfied for cash in an amount

equal to the obligation’s fair market value• However, if amount realized in actual transaction giving rise to DSR

is different from fair market value, generally use amount realized.• Deemed reissuance under §1.1502-13(g)(3)

– Intercompany obligation is deemed reissued for the cash used in the deemed satisfaction transaction

• Reissued obligation is not reexamined for debt-equity treatment• The parties are then treated as engaging in the actual transaction,

38

but with the new obligation.

2008 Final Regulations:Intragroup And OutboundIntragroup And Outbound

Transactions (Cont.)

• The 2008 final regulations contain exceptions to DSR in certain limited situations that include:DSR in certain limited situations that include:– Intercompany nonrecognition transactions– Intercompany assumption transactionsIntercompany assumption transactions– Intercompany extinguishment transactions– Routine modification transactions– Outbound subgroup transactions

39

Intercompany Nonrecognition T tiTransactions

• The transaction is an intercompany exchange to which §361(a), §§332 and 337(a), or §351 l d§351 apply; and

• Neither the creditor nor the debtor recognizes income, gain, deduction or loss.• However, the exception to DSR for intercompany nonrecognition transactions does

not apply if the creditor assigns the intercompany obligation in a §351 exchange and:pp y g p y g § g– The transferor or transferee has a loss subject to a limitation, and the other member is not

subject to a comparable limitation;– The transferor or transferee has a special status (e.g., a bank) that the other member does

not also have;– A member of the group realizes COD income that is excluded from gross income under

§108(a), and the tax attributes of the transferor or transferee are reduced under §1.1502-28;– The transferee has a non-member shareholder;– The transferee issues preferred stock to the transferor in exchange for the assignment of the

intercompany obligation; or– The stock of the transferee is directly or indirectly disposed of within 12 months from the

assignment of the intercompany obligation.

40

Intercompany Assumption T tiTransactions

• All of the debtor’s obligations under an intercompanyAll of the debtor s obligations under an intercompany obligation are assumed in connection with the debtor’s sale or other disposition of property (other than solely money) in an intercompany transaction in which gain ormoney) in an intercompany transaction in which gain or loss is recognized under §1001

41

Intercompany Extinguishment T tiTransactions

• All or part of the rights and obligations under the intercompany obligation are extinguished in anintercompany obligation are extinguished in an intercompany transaction, the adjusted issue price of the obligation is equal to the creditor’s basis in the obligation and the debtor’s corresponding item offsets inobligation, and the debtor’s corresponding item offsets in amount the creditor’s intercompany item

42

Routine Modification TransactionsRoutine Modification Transactions

• All of the rights and obligations under the intercompany obligation are extinguished in an intercompany t ti th t i h ( d d h )transaction that is an exchange (or deemed exchange) for a newly issued intercompany obligation, and the issue price of the newly issued obligation equals both the adjusted issue price of the extinguished obligation and the creditor’s basis in the extinguished obligation

43

Outbound Subgroup TransactionsOutbound Subgroup Transactions

• The intercompany obligation becomes an obligation that is not an intercompany obligation in a transaction in which the members of an intercompany obligationwhich the members of an intercompany obligation subgroup cease to be members of a consolidated group; neither the creditor nor the debtor recognizes any i i d d i l i h hincome, gain, deduction or loss with respect to the intercompany obligation; and such members constitute an intercompany obligation subgroup of another p y g g pconsolidated group immediately after the transaction

44

2008 Final Regulations:A ti A id R lAnti-Avoidance Rules

• Tax benefit ruleTax benefit rule– The tax benefit rule applies if an intercompany assignment or

extinguishment transaction is:Otherwise excepted from DSR and• Otherwise excepted from DSR, and

• Engaged in with a view to secure a tax benefit that would not otherwise be enjoyed in a consolidated or separate return yearyear.

– If the tax benefit rule applies, then the assignment or extinguishment transaction triggers DSR.

f f f– A tax benefit is a net reduction, for federal income tax purposes, in income or gain; or a net increase in loss, deduction, credit or allowance.

45

2008 Final Regulations:A ti A id R l (C t )Anti-Avoidance Rules (Cont.)

• Off-market issuance rule– If an intercompany obligation is issued at a rate of interest that is

materially off-market (off-market obligation) with a view to shift items of built-in gain, loss, income or deduction from the g , ,obligation from one member to another member in order to secure a tax benefit; then the intercompany obligation will be treated, for all federal income tax purposes, as originally issued for its fair market value, and any difference between the amount loaned and the fair market value of the obligation will be treated as transferred between the creditor and the debtor at the time th bli ti i i dthe obligation is issued.

46

2008 Final Regulations:Intragroup And OutboundIntragroup And Outbound

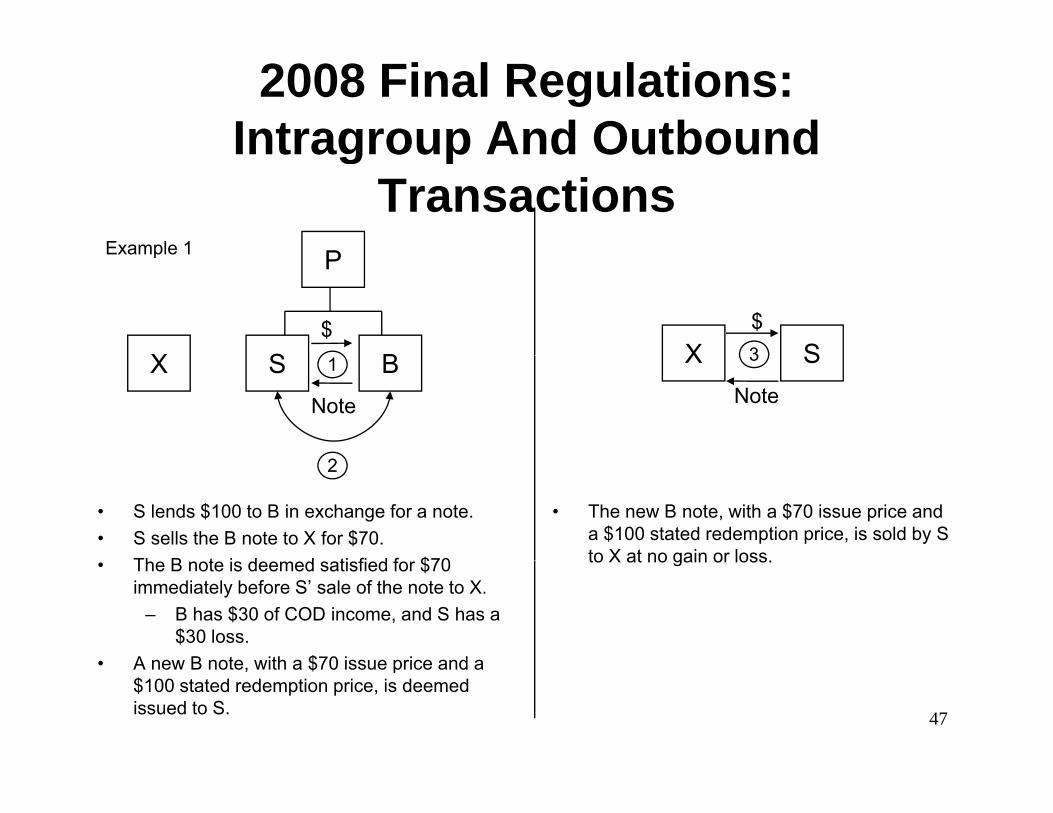

TransactionsPExample 1

X$

P

BS X S$3

Example 1

Note

X BS 1 X SNote

3

2

• S lends $100 to B in exchange for a note.• S sells the B note to X for $70.

Th B t i d d ti fi d f $70

• The new B note, with a $70 issue price and a $100 stated redemption price, is sold by S to X at no gain or loss.• The B note is deemed satisfied for $70

immediately before S’ sale of the note to X.– B has $30 of COD income, and S has a

$30 loss.• A new B note with a $70 issue price and a

to X at no gain or loss.

47

• A new B note, with a $70 issue price and a $100 stated redemption price, is deemed issued to S.

2008 Final Regulations:Intragroup And OutboundIntragroup And Outbound

Transactions (Cont.)Example 2 PExample 2

$

BS

Note 12

S $ S f

S1

• S1 lends $100 to S in exchange for a note.• S1 merges with and into S in a §332 liquidation when the S note is worth $90.• The S note is not subject to DSR if neither S nor S1 recognize gain or loss in the

transaction.

48

a sac o

2008 Final RegulationsIntragroup And OutboundIntragroup And Outbound

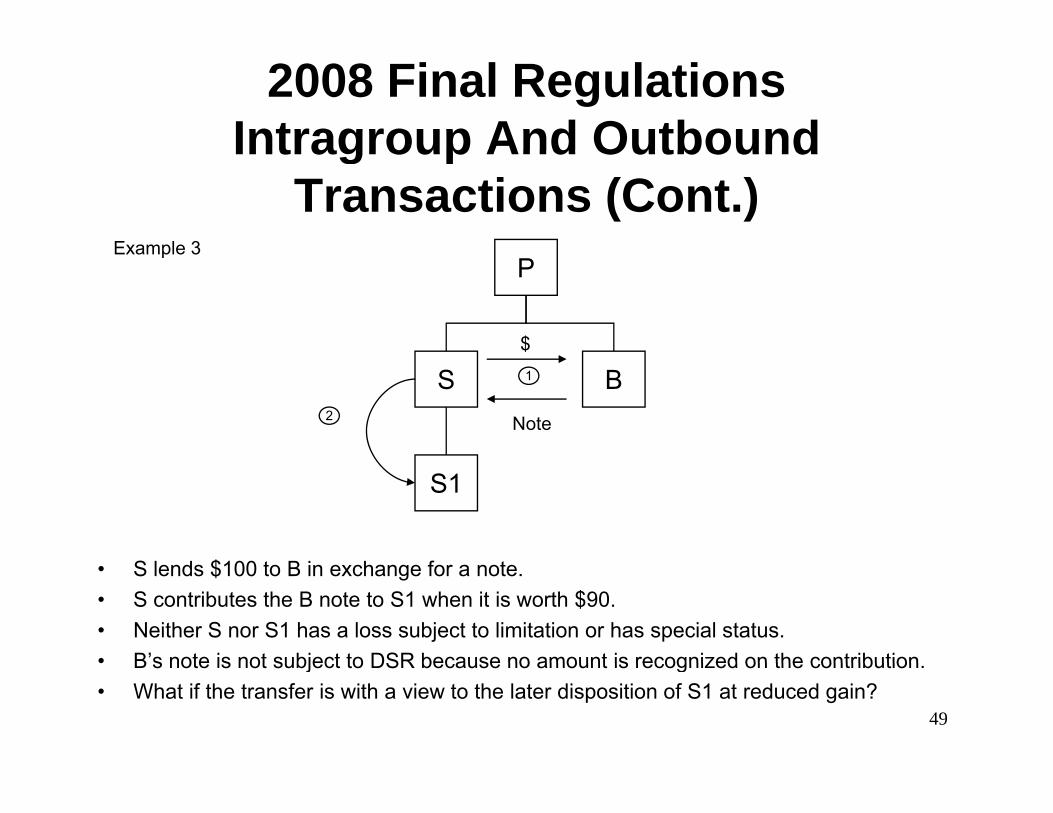

Transactions (Cont.)Example 3

$

PExample 3

BSNote

1

2

S $ f

S1

• S lends $100 to B in exchange for a note.• S contributes the B note to S1 when it is worth $90.• Neither S nor S1 has a loss subject to limitation or has special status.• B’s note is not subject to DSR because no amount is recognized on the contribution

49

• B s note is not subject to DSR because no amount is recognized on the contribution.• What if the transfer is with a view to the later disposition of S1 at reduced gain?

2008 Final RegulationsIntragroup And OutboundIntragroup And Outbound

Transactions (Cont.)Example 4 PExample 4

$

S

Note 12

Note

S1stock

S $ S f

S1

• S lends $100 to S1 in exchange for a note.• When the S1 note is worth $90, S transfers the S1 note to S1 in exchange for S1

stock, and the S1 note is extinguished.• The extinguishment of the S1 note is not subject to DSR, because the adjusted issue

50

e e gu s e o e S o e s o subjec o S , because e adjus ed ssueprice of the S1 note ($100) is equal to S’ basis in the note ($100), and S1’s corresponding item ($10) and S’ intercompany item ($10) offset in amount.

2008 Final RegulationsI b d T tiInbound Transactions

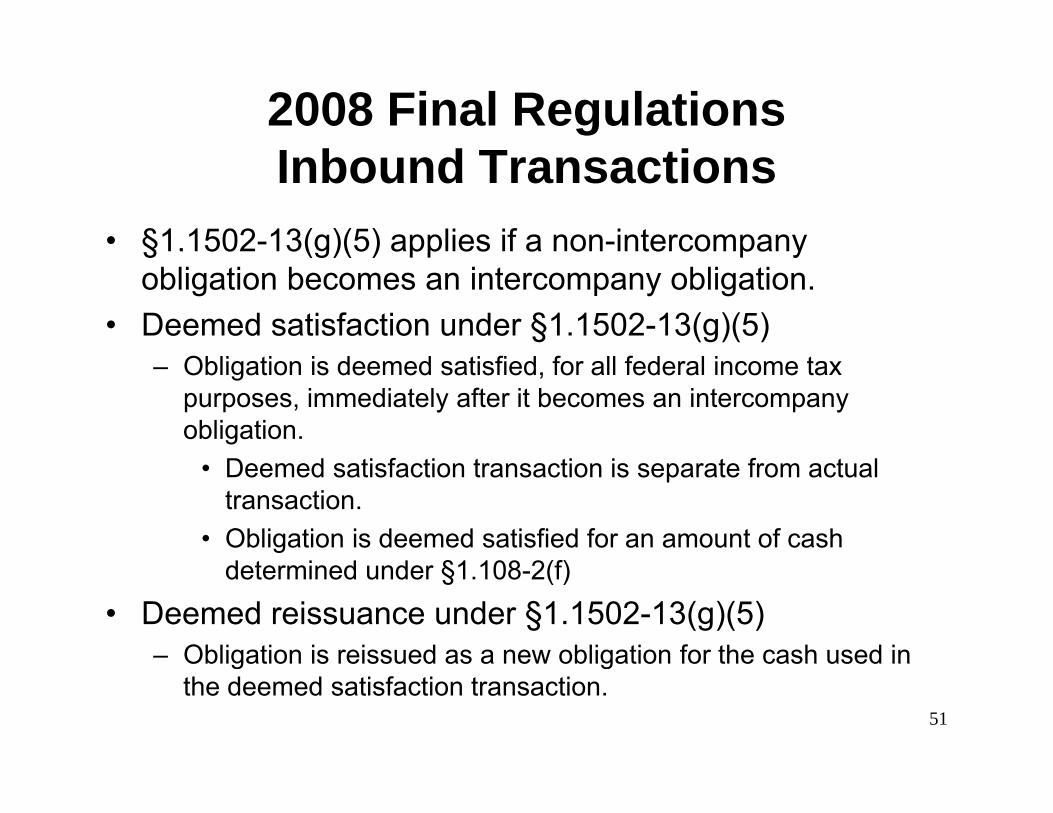

• §1.1502-13(g)(5) applies if a non-intercompany § (g)( ) pp p yobligation becomes an intercompany obligation.

• Deemed satisfaction under §1.1502-13(g)(5)– Obligation is deemed satisfied, for all federal income tax

purposes, immediately after it becomes an intercompany obligation.

f f• Deemed satisfaction transaction is separate from actual transaction.

• Obligation is deemed satisfied for an amount of cash d i d d §1 108 2(f)determined under §1.108-2(f)

• Deemed reissuance under §1.1502-13(g)(5)– Obligation is reissued as a new obligation for the cash used in

51

Obligation is reissued as a new obligation for the cash used in the deemed satisfaction transaction.

2008 Final RegulationsI b d T ti (C t )Inbound Transactions (Cont.)

$

P

$

TX stock

2

$

P

X B

Note

1

Note

$

3 XB

• X lends $100 to B in exchange for a note.

• P purchases all the X stock when the B

• A new B note, with a $70 issue price and a $100 stated redemption price, is deemed issued to X.pu c ases a e s oc e e

note is worth $70.• B is deemed to satisfy the B note for

$70 immediately after the purchase of the X stock

52

the X stock.• B has $30 of COD income and X has a

$30 loss.

Fi l C h D R l tiFinal Cash D Regulations And Application To pp

Consolidated Groups

Michelle Albert, Ernst & YoungMichelle Albert, Ernst & Young

Background - D Reorganizations Generally

► Sect. 368(a)(1)(D) defines the term “reorganization” as:

► “A transfer by a corporation of all or a part of its assets to another corporation ifimmediately after the transfer the transferor, or one or more of its shareholders (including

h h h ld i di t l b f th t f ) bi tipersons who were shareholders immediately before the transfer), or any combinationthereof, is in control of the corporation to which the assets are transferred; but only if, inpursuance of the plan, stock or securities of the corporation to which the assets aretransferred are distributed in a transaction which qualifies under section 354, 355,or 356” (emphasis added)or 356 (emphasis added)

► Sect. 354(a)(1) generally provides that no gain or loss is recognized if stock orsecurities in a corporation a party to a reorganization are, in pursuance of the plan ofreorganization, exchanged solely for stock or securities in such corporation or inanother corporation a party to the reorganization.

► Sect. 354(b)(1) further provides that for D reorganizations, the stock, securities andother properties received by the transferor must be distributed pursuant to theplan of reorganization (emphasis added).p g ( p )

► Sect. 356 generally provides that if Sect. 354 would apply to an exchange but for thefact that the property received in the exchange consists not only of property permittedby Sect. 354, but also of other property or money, then gain (if any) will be recognizedbut not in an amount greater than the sum of such money and the FMV of such other

Page 54

but not in an amount greater than the sum of such money and the FMV of such otherproperty.

Background – D Reorganizations And Meaningless Gesture

► Notwithstanding the distribution requirement required bysections 368(a)(1)(D) and 354(b), the IRS and the courts have( )( )( ) ( )not required the actual issuance and distribution of stock and/orsecurities of the acquiring corporation when the same personor persons own all the stock and/or securities of the transferorpcorporation and acquiring corporation.

► In these circumstances, the IRS and the courts have viewedthe issuance of stock to be a “meaningless gesture” notmandated by sections 368(a)(1)(D) and 354(b).► See e.g., Rev. Rul. 70-240, 1970-1 C.B. 81; James Armour, Inc. v.g , , ; ,

Comm’r, 43 TC 295 (1964); Wilson v. Comm’r, 46 TC 334 (1966).Compare Warsaw Photographic Associates, Inc. v. Comm’r, 84 TC 21(1985)

Page 55

2006 Proposed And Temporary All-Cash D Regulations

► Issued in December 2006 and were scheduled to sunset onDec. 19, 2009► See T.D. 9303 and REG-125632-06

► Essentially provide that the distribution requirement in sections368(a)(1)(D) and 354(b) will be satisfied even though no stock( )( )( ) ( ) gis actually issued in the transaction, if the same person orpersons own, directly or indirectly, all of the stock of thetransferor and acquiring corporations in identical proportionsq g p p p► In such cases, the acquiring corporation is deemed to issue a nominal

share of stock to the transferor in addition to the actual considerationexchanged for the transferor corporation’s assets.

► Nominal share is then deemed distributed by the transferor to itsshareholders and, when appropriate, further transferred through theownership chains to the extent necessary to reflect the actual post-transaction ownership structure

Page 56

transaction ownership structure.

Final All Cash D Regulations – T.D. 9475

► Finalize, with modifications, the 2006 proposed andtemporary regulations► Reg. §1.368-2(l)

► Significant comments to the 2006 proposed andg p ptemporary regulations were received primarily withrespect to the following categories:► Meaningless gesture doctrine► Meaningless gesture doctrine► Issuance of nominal share► Basis allocation► Application to consolidated groups

► Applicable to transactions occurring on or after Dec. 18,

Page 57

2009

General Explanation Of Final All-Cash D Regulations – Reg. §1.368-2(l)

► Meaningless gesture doctrine► If no consideration is received, or the value of the consideration received in the

transaction is less than the FMV of the transferor’s assets:

► Acquiring corporation is treated as issuing stock with a value equal to the excess ofthe FMV of the transferor’s assets over the value of the consideration actuallyreceived in the transaction

► If the value of the consideration received is equal to the FMV of the transferor’sassets:

► Acquiring corporation is deemed to issue a nominal share

► Nominal share► Nominal share approach retained; has significance beyond satisfying the

distribution requirement of Sections 368(a)(1)(D) and 354(b)

► Provides a useful mechanism with respect to stock basis consequences to theexchanging shareholder and should be treated as non-recognition property underSection 358(a) (i.e., substituted basis property)

► Nominal share preserves remaining basis if any and facilitates future stock gain or

Page 58

► Nominal share preserves remaining basis, if any, and facilitates future stock gain orloss recognition by the appropriate shareholder.

General Explanation Of Final All-Cash D Regulations – Reg. §1.368-2(l) (Cont.)

► Basis allocation► Reg. §1.358-2(a)(2)(iii) was amended to provide that in the case of a reorganization

in which the property received consists solely of non-qualifying property equal top p y y q y g p p y qthe value of the assets transferred (including the nominal share), the shareholdermay designate the share of stock of the acquiring corporation to which the basis, ifany, of the stock surrendered will attach.

► Approach is most consistent with current law regarding basis determination if stock► Approach is most consistent with current law regarding basis determination if stockwas actually issued in the transaction

► Application to consolidation groups► In all-cash D reorganizations occurring between members of a consolidated group:

► Selling member (S) is treated as receiving the nominal share and additional stock of thebuying member (B) under Reg. §1.1502-13(f)(3), which it will distribute to its shareholdermember (M) in liquidation;

► Immediately after the sale, the B stock (with the exception of the nominal share which isstill held by M) received by M is treated as redeemed, and the redemption is treated underSect. 302(d) as a Sect. 301 distribution; and

► M’s basis in the B stock is reduced under Reg §1 1502-32(b)(3)(v) with any remaining

Page 59

► M s basis in the B stock is reduced under Reg. §1.1502-32(b)(3)(v), with any remainingbasis attaching to the nominal share under Reg. §1.302-2(c)

Boot In Intercompany Reorganizations Under Reg. §1.1502-13(f)(3) - Generally

► Non qualifying property received as part of a transaction► Non-qualifying property received as part of a transactiondescribed in Reg. §1.1502-13(f)(3) is treated as received bythe member shareholder in a separate transaction.► Sections 302 and 311 apply rather than sections 356 and 361.

► Nonqualifying property is treated as taken into accountimmediately after the transaction if Sect. 354 would apply butfor the fact that non-qualifying property is received.q y g p p y► Applies for all federal income tax purposes

Page 60

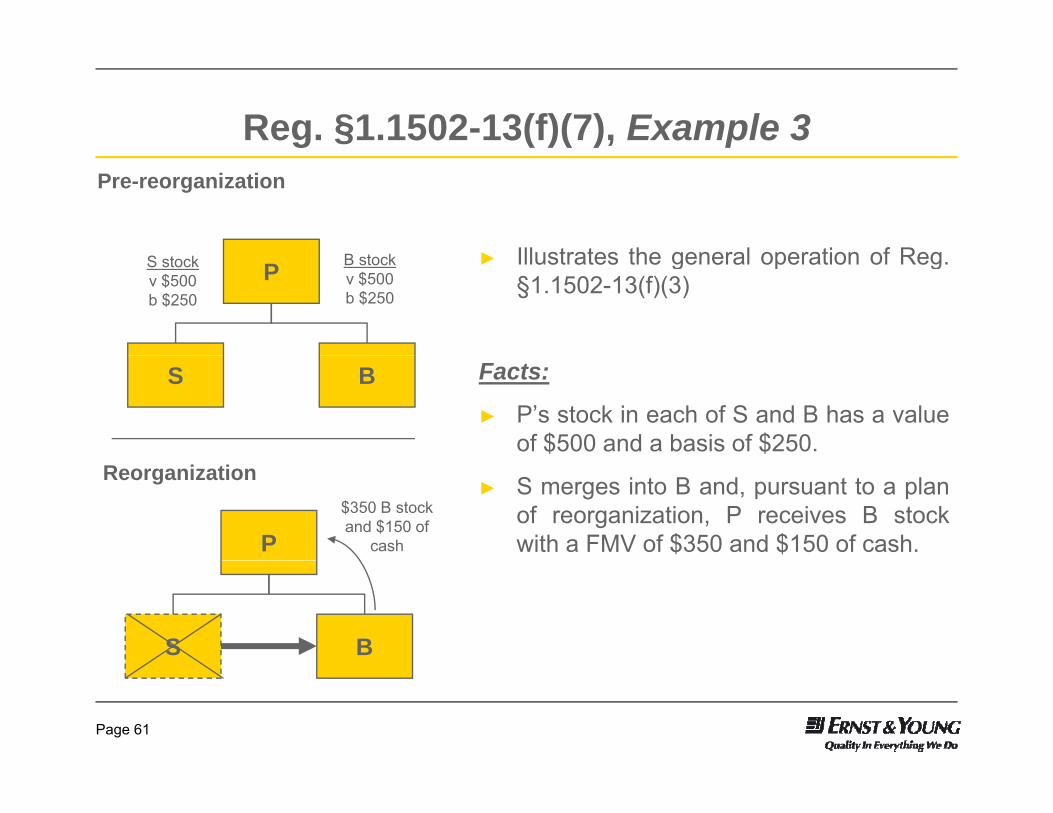

Reg. §1.1502-13(f)(7), Example 3

► Illustrates the general operation of Reg

Pre-reorganization

► Illustrates the general operation of Reg.§1.1502-13(f)(3)

S stockv $500b $250

P B stockv $500b $250

Facts:

► P’s stock in each of S and B has a valueof $500 and a basis of $250.

S B

► S merges into B and, pursuant to a planof reorganization, P receives B stockwith a FMV of $350 and $150 of cash.

Reorganization

P$350 B stock and $150 of

cash

S B

Page 61

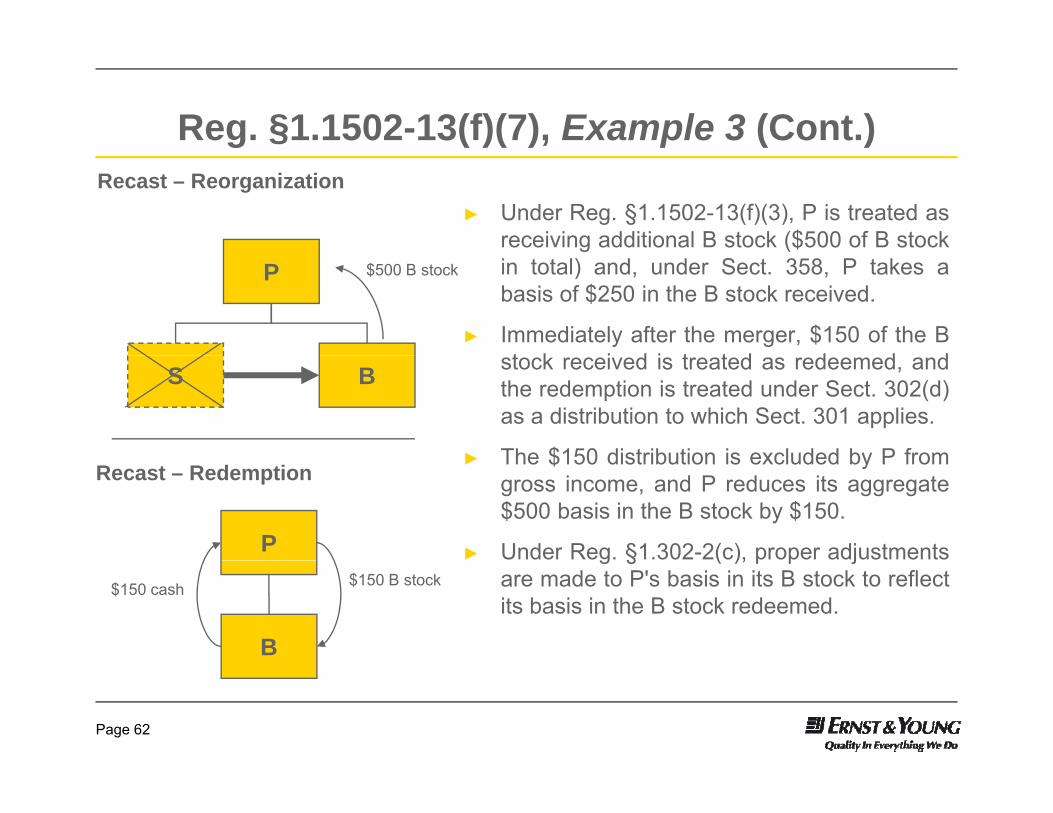

Reg. §1.1502-13(f)(7), Example 3 (Cont.)

► Under Reg. §1.1502-13(f)(3), P is treated asreceiving additional B stock ($500 of B stock

Recast – Reorganization

in total) and, under Sect. 358, P takes abasis of $250 in the B stock received.

► Immediately after the merger, $150 of the Bt k i d i t t d d d d

$500 B stock P

stock received is treated as redeemed, andthe redemption is treated under Sect. 302(d)as a distribution to which Sect. 301 applies.

► The $150 distribution is excluded by P from

S B

► The $150 distribution is excluded by P fromgross income, and P reduces its aggregate$500 basis in the B stock by $150.

► Under Reg. §1.302-2(c), proper adjustments

Recast – Redemption

P g § ( ), p p jare made to P's basis in its B stock to reflectits basis in the B stock redeemed.

B

$150 cash $150 B stock

Page 62

Reg. §1.1502-13(f)(7), Example 4 Added By All-Cash D Regulations

ReorganizationP

RecastP

M $100 cash B M

S stock

$100 cash B$100 B stock and nominal

$100 Cash

S stockb $25 Assets

S

S stockb $25

Assets

S

nominal share

► S sells all of its assets to B for $100 and liquidates.

► The transaction qualifies as a D reorganization.

► Pursuant to Reg §1 368 2(l) B will be deemed to issue a nominal share of B stock to S in addition► Pursuant to Reg. §1.368-2(l), B will be deemed to issue a nominal share of B stock to S in additionto the $100 of cash actually exchanged for the S assets, and S will be deemed to distribute all ofthe consideration to M. M will then be deemed to distribute the nominal share of B stock to P.

► Under Reg. §1.1502-13(f)(3), S is treated as receiving, in addition to the nominal share issued by Bto S under Reg §1 368-2(l) additional B stock with a FMV of $100 (in lieu of the cash) which S

Page 63

to S under Reg.§1.368-2(l), additional B stock with a FMV of $100 (in lieu of the cash), which Sdistributes to M in liquidation.

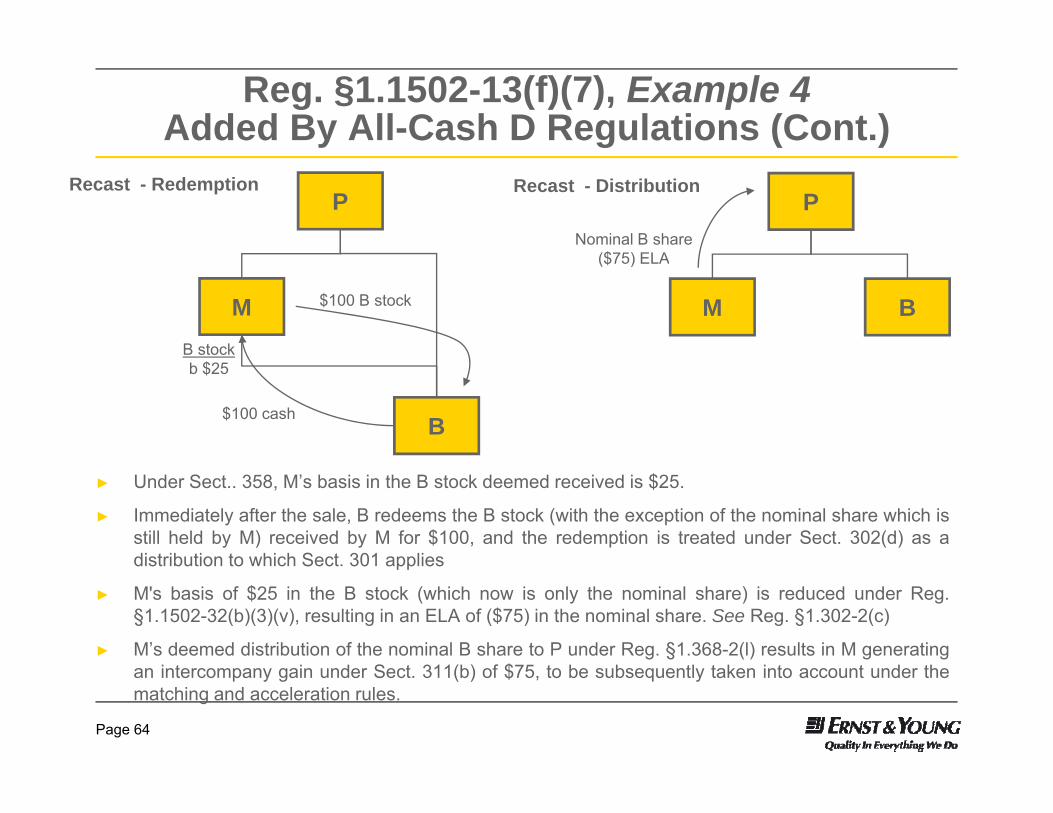

Reg. §1.1502-13(f)(7), Example 4 Added By All-Cash D Regulations (Cont.)

Recast - Redemption Recast - DistributionP

Nominal B share($75) ELA

P

M

($75) ELA

BMB stock

$100 B stock

b $25

B$100 cash

► Under Sect.. 358, M’s basis in the B stock deemed received is $25.

► Immediately after the sale, B redeems the B stock (with the exception of the nominal share which isstill held by M) received by M for $100, and the redemption is treated under Sect. 302(d) as adistribution to which Sect 301 appliesdistribution to which Sect. 301 applies

► M's basis of $25 in the B stock (which now is only the nominal share) is reduced under Reg.§1.1502-32(b)(3)(v), resulting in an ELA of ($75) in the nominal share. See Reg. §1.302-2(c)

► M’s deemed distribution of the nominal B share to P under Reg. §1.368-2(l) results in M generating

Page 64

an intercompany gain under Sect. 311(b) of $75, to be subsequently taken into account under thematching and acceleration rules.

Questions – Final All-Cash D Regulations

► No effective date for Example 4, in Reg. §1.1502-13(f)(7)► Is the approach taken a clarification of the 2006 proposed and

temporary all Cash D regulations? Retroactive to the effective datetemporary all-Cash D regulations? Retroactive to the effective dateof the 2006 proposed and temporary all-Cash D regulations?

► What if M owned B shares prior to the D reorganization ofS?S?► Should the ELA in the B shares be deemed issued and then

redeemed post-reorganization transfer to the existing B sharesthat M continues to own?

► Can the results be avoided if B actually transfers oneshare of its stock as consideration?share of its stock as consideration?

Page 65

C lid t d R tConsolidated Return Issues For Troubled

Corporations

Devon M. Bodoh, KPMG LLPDevon M. Bodoh, KPMG LLP

Cancellation of Indebtedness Income In Consolidation

Cancellation Of Indebtedness In lid iConsolidation

• A taxpayer may be able to exclude otherwise taxable cancellation of indebtedness (“COD”) income from gross income in certain circumstances including among others (i) where theincome from gross income in certain circumstances including, among others, (i) where the debt is cancelled in a Title 11 bankruptcy case, and (ii) where the taxpayer is insolvent immediately before the cancellation (in which case, the COD income is excluded only to the extent that the taxpayer is insolvent). §§108(a)(1)(A),(B); 108(a)(3).

• Generally any COD income that is excluded from gross income will reduce certain tax• Generally, any COD income that is excluded from gross income will reduce certain tax attributes of the taxpayer. §108(b).

• Treasury Regulations Sect. 1.1502‐28 provides rules regarding the application of Sect. 108(a) and the reduction of tax attributes pursuant to Sect. 108(b) when a member of a

l d d l h l d d fconsolidated group realizes COD income that is excluded from gross income.

• For purposes of determining whether COD income is excluded from gross income, the regulations state that sections 108(a)(1)(A) and (B) are applied separately to each member that realizes excluded COD income.

– For example, the limitation on the amount of COD income that is excluded from gross income when the debtor is insolvent is determined based on the assets (including stock and securities of other members) and liabilities (including liabilities to other members) of only the member that realizes excluded COD income. §§108(a)(3);108(d)(3); Treas. Reg. §1.1502‐28(a)(1)

68

Attribute Reduction In ConsolidationAttribute Reduction In Consolidation

• With respect to a member that realizes excluded COD income in a taxable year, the tax ib ib bl h b ( d i di d i di b idi i hattributes attributable to that member (and its direct and indirect subsidiaries to the extent

required by Sect. 1017(b)(3)(D) and Treasury Regulations Sect. 1.1502‐28), including basis of assets and losses and credits arising in separate return limitation years, are reduced as provided in sections 108 and 1017 and Treasury Regulations Sect. 1.1502‐28.

• Generally, the attributes of a member that realizes excluded COD income are reduced in the following manner:

– First, tax attributes attributable to the debtor are reduced under the “debtor first rule”. Treas. Reg. §1.1502‐28(a)(2) g ( )( )

• The basis of subsidiary stock is not reduced below zero. Treas. Reg. §1.1502‐28(a)(2)(i)

– Next, the “look through rule” is applied to reduce certain tax attributes of the debtor’s subsidiaries Treas Reg §1 1502 28(a)(3)subsidiaries. Treas. Reg. §1.1502‐28(a)(3)

– Finally, certain remaining attributes of all members are reduced pursuant to the “fan out rule”. Treas. Reg. §1.1502‐28(a)(4)

69

Attribute Reduction In Consolidation: i d iBasis Reduction

• Sect. 1017 contains rules for applying excluded COD income of a taxpayer to reduce the basis of depreciable property held by the taxpayer.

– A taxpayer may elect to first apply its excluded COD income to reduce the basis of its depreciable property. §108(b)(5)

• Generally, to the extent that excluded COD income of a taxpayer is applied to reduce the y, p y ppbasis of property, it will reduce the basis of property held by the taxpayer at the beginning of the taxable year following the taxable year in which the cancellation occurs. §1017(a)

• With respect to an exclusion of COD income pursuant to Sect. 108(a)(1)(A) (cancellation of debt in a Chap 11 bankruptcy) or Sect 108(a)(1)(B) (taxpayer is insolvent when thedebt in a Chap. 11 bankruptcy) or Sect. 108(a)(1)(B) (taxpayer is insolvent when the cancellation occurs), the amount of the basis reduction under Sect. 1017 will not exceed the excess of the aggregate basis of the property held by the taxpayer over the aggregate liabilities of the taxpayer (the “liability floor”) in both instances, immediately after the cancellation of indebtedness. §1017(b)(2)cancellation of indebtedness. §1017(b)(2)

• For purposes of Sect. 1017, if a taxpayer and its subsidiary are both members of the same consolidated group for the taxable year in which the taxpayer has indebtedness cancelled, then the subsidiary stock held by the taxpayer will be treated as depreciable property to the extent that the subsidiary consents to a corresponding reduction in the basis of itsextent that the subsidiary consents to a corresponding reduction in the basis of its depreciable property. §1017(b)(3)(D)

70

Attribute Reduction In Consolidation: Timing• Treasury Regulations Sect. 1.1502‐28(b) provides, among other things, special rules for the timing

of attribute reduction in consolidation where the member that realizes excluded COD income departs the group, is succeeded by another member of the group, or becomes the new common parent of the group.

Intra group reorganizations: If the taxable year of a member during which such member realizes excluded COD– Intra‐group reorganizations: If the taxable year of a member during which such member realizes excluded COD income ends prior to the last day of the consolidated return year and, on the first day that follows the taxable year of such member during which such member realized excluded COD income, such member has a successor member (determined by reference to Sect. 381), the successor member is treated as if had realized the excluded COD income. Thus, all attributes of the successor member listed in Sect. 108(b)(2) (including attributes that were attributable to the successor member prior to the fate such member became a successor member) are subject to reduction prior to the attributes attributable to other members of the group See Treas Reg §§1 1502 28(b)(9)(i) 1 1502 28(b)(10)attributes attributable to other members of the group. See Treas. Reg. §§1.1502‐28(b)(9)(i); 1.1502‐28(b)(10)

– Group structure change: If a member that realizes excluded COD income acquires the assets of the common parent of the group in a transaction to which Sect. 381(a) applies (and succeeds such common parent under Treasury Regulations Sect. 1.1502‐75(d)(2)), the members attributes that remain after determination of tax for the group for the consolidated return year during which the excluded COD income is realized (including attributes that were attributable to the former common parent prior to the date of the acquisition) are subject to reduction prior to the attributes attributable to other members of the group. See Treas. Reg. §1.1502‐28(b)(9)(ii).

– Departure of member: If the taxable year of a member during which such member realizes excluded COD income ends on or prior to the last day of the consolidated return year and, on the first day of the taxable year of such member that follows the taxable year during which such member realizes excluded COD income, such member is not a member of the group (and does not have a successor), then all Sect. 1098(b)(2) attributes that remain after determination of the tax imposed that belong to members of the group (including the departing member and p g g p ( g p gsubsidiaries of the departing member) are subject to reduction. See Treas. Reg. §1.1502‐28(b)(8)

• The basis of property is subject to reduction under the rules of sections 108 and 1017 and Treasury Regulations Sect. 1.1502‐28 after the determination of tax for the year during which the member realized excluded COD income (and any prior years) and coincident with the reduction of other attributes pursuant to Sect 108 and Treasury Regulations Sect 1 1502‐28 See Treas Reg §1 1502‐attributes pursuant to Sect. 108 and Treasury Regulations Sect. 1.1502 28. See Treas. Reg. §1.150228(b)(3)(i)

71

Attribute Reduction In Consolidation: h “ k h h l ”The “Look‐Through Rule”

• If the debtor member reduces its basis in a subsidiary’s stock, then the subsidiary will beIf the debtor member reduces its basis in a subsidiary s stock, then the subsidiary will be treated as realizing excluded COD income on the last day of the taxable year of the debtor member that includes the date on which the debtor member realized the excluded COD income (i.e., a “look‐through rule”). Treas. Reg. §1.1502‐28(a)(3)(ii)

– If the look‐through rule applies then the subsidiary must reduce an equal amount of its own taxIf the look through rule applies, then the subsidiary must reduce an equal amount of its own tax attributes, including asset basis, under general attribute ordering rules.

– If the subsidiary’s outside stock basis reduction exceeds its available inside tax attributes, then the excess is “black hole” COD that does not reduce attributes of any other member. Treas. Reg. §1.1502‐28(a)(3)(i)

• If a member treats stock of a subsidiary as depreciable property pursuant to Sect. 1017(b)(3)(D), then the basis of the depreciable property of such subsidiary will be reduced prior to the application of the look‐through rule. Treas. Reg. §1.1502‐28(a)(3)(ii)

• The look‐through rule will apply only if the debtor member and the subsidiary are membersThe look through rule will apply only if the debtor member and the subsidiary are members of the same consolidated group on (a) the last day of the debtor member’s taxable year that includes the date on which the excluded COD is realized, or (b) the first day of the debtor member’s taxable year that follows the taxable year that includes the date on which the excluded COD income is realized. Treas. Reg. §1.1502‐28(a)(3)(ii)excluded COD income is realized. Treas. Reg. §1.1502 28(a)(3)(ii)

72

PLR 200934001 (Aug. 21, 2009)PLR 200934001 (Aug. 21, 2009)

FP

Pre‐TransactionStructure (Simplified)

FP

Post‐TransactionStructure (Simplified)

FP

P

3rd Party

FP

P

HoldCo

FinCo S

Intercompany Debt

Creditors FinCo

NewcoNewCoLLC

Facts (simplified transaction structure):

● FP, a foreign corporation, owns all of the stock of P, a U.S. corporation that is the common parent of a U.S. consolidated group (the “P Group”) that includes FinCo, HoldCo and HoldCo Subs 1 through 43 (collectively, “S”).S ).

● Prior to the transaction, various members of the P Group (including FinCo) had outstanding third‐party indebtedness. In addition, there is various intercompany indebtedness among the members of the P Group including, among others, an intercompany indebtedness between FinCo (as the creditor) and HoldCo (as the debtor).

● In order to simplify its corporate structure the P Group undertook a restructuring in bankruptcy that● In order to simplify its corporate structure, the P Group undertook a restructuring in bankruptcy that resulted in FinCo becoming a first‐tier subsidiary of P and the elimination of certain members of the P Group. In addition, as part of this restructuring, the P Group restructured its third‐party indebtedness (the “external debt restructuring”) and its intercompany indebtedness (the “internal debt restructuring”), which resulted in various members of the P Group realizing COD income. 73

PLR 200934001 (Cont.)PLR 200934001 (Cont.)

The PLR’s findings – COD Income:

• With respect to actual COD income realized and excluded under Sect. 108(a), the Service ruled that the liability floor of Sect. 1017(b)(2) will be determined at the surviving entity level by taking into account the basis of the surviving entity’s assets and the amount of itsby taking into account the basis of the surviving entity s assets and the amount of its liabilities immediately after all of the proposed transactions. Solely for purposes of applying the liability floor of Sect. 1017(b)(2) at the surviving entity level, the external debt restructuring will be deemed to occur immediately after all of the proposed transactions (citing Treasury Regulations Sect 1 1502‐28(b)(9))(citing Treasury Regulations Sect. 1.1502 28(b)(9)).

• With respect to any deemed COD realized pursuant to Treasury Regulations Sect. 1.1502‐28(a)(3)(ii), the liability floor of Sect. 1017(b)(2) will be determined at the surviving entity level by taking into account the basis of the surviving entity’s assets and the amount of the surviving entity’s liabilities on the last day of the taxable year of the higher tier member thatsurviving entity s liabilities on the last day of the taxable year of the higher‐tier member that includes the date the higher‐tier member realized the COD income giving rise to the look‐through COD income at the surviving entity level.

74

Sect. 108(i)Legislative change

• Sect. 1231 of the American Recovery and Reinvestment Act of 2009 added subsection (i) to Sect. 108.

Deferral of COD incomeDeferral of COD income

• A taxpayer may elect under Sect. 108(i) to include COD income from the reacquisition of an “applicable debt instrument” in gross income ratably over a five‐year period (rather than including the entire COD income in the year of the reacquisition).

• The five‐year period for recognition of COD income begins with the fifth tax year following the tax year in which the reacquisition occurs if the reacquisition occurs in 2009.

– If the reacquisition occurs in 2010, the five‐year period begins with the fourth tax year following the tax year in which the reacquisition occurs.

– Thus, for calendar‐year taxpayers, the five years of inclusion would be 2014‐2018 regardless of whether COD income is realized in 2009 or 2010 (assuming no short‐period returns).

– Sect. 108(i) does not apply to a reacquisition occurring after 2010.

Sect. 163(e)(5)(F)

• Sect. 163(e)(5)(F) was added in connection with Sect. 108(i) to prevent Sect. 163(e)(5) from deferring or disallowing original issue discount (“OID”) that is deductible by issuers of applicable high‐yield discount obligations.g y g

75

Sect. 108(i) (Cont.)Interaction with Sect. 108(a)

A l ti d S t 108(i) l d th t f l di th COD i d S t• An election under Sect. 108(i) precludes the taxpayer from excluding the COD income under Sect. 108(a) (with a potential reduction of attributes under Sect. 108(b)) for the year of reacquisition as well as any subsequent year. §108(i)(5)(C)

– Thus, a taxpayer cannot exclude the COD income under Sect. 108(a) after deferring l ( h d )recognition until 2014 (assuming no short‐period returns).

Election to defer COD income

• A taxpayer makes an election to defer COD income under Sect. 108(i) by including a statement that clearly identifies the instrument, includes the amount of deferred COD income, and any other y , , yinformation prescribed by the secretary.

– Rev. Proc. 2009‐37, 2009‐36 I.R.B. 309, provides guidance on a number of items including how to make the election, reporting after election years, reporting for flow‐through entities and other specialized procedures.

Th l ti t t t i d ith th t ’ ti l fil d (i l di t i ) i i l f d l i t• The election statement is due with the taxpayer’s timely filed (including extensions) original federal income tax return for the taxable year of the acquisition. Automatic extension of 12 months.

• The election statement is made on an instrument‐by‐instrument basis.

• The election can be made to defer all or any portion of the COD income realized on an instrument.

• Protective elections may be made but are subject to similar reporting and limitations.

• The Sect. 108(i) election is irrevocable. §108(i)(5)(B)(ii)

• Note that the election is made by the entity for partnerships, S corporations or other pass‐through entities rather than the partners, shareholders or members. §108(i)(5)(B)(iii)

• Annual information statements are required for every tax year after the election year and include• Annual information statements are required for every tax year after the election year and include the amount of COD income deferred/included/accelerated, OID deferred/deducted/accelerated, etc.

76

Definitions Of TermsApplicable debt instruments

• Sect. 108(i) applies to reacquisitions of “applicable debt instruments.”

• An “applicable debt instrument” is defined as any debt instrument that was issued by:

– A C corporation, or

– Any other person in connection with the conduct of a trade or business by that person.

• A “debt instrument” is defined broadly to include:

A bond– A bond,

– A debenture,

– A note,

– A certificate, or

– Any other instrument or contractual arrangement constituting indebtedness within the meaning of Sect. 1275(a)(1).

• A taxpayer may treat two or more applicable debt instruments that are part of the same issue and that are reacquired during the same taxable year as one applicable debt instrument, for purposes of Rev. Proc 2009 37Proc. 2009‐37.

– Pass‐through entity may do the same, but only if the owners and their ownership interests in the pass‐through entity immediately prior to the reacquisition of each applicable debt instrument are identical.

77

Definitions Of Terms (Cont.)Acquisitions and reacquisitions

• A “reacquisition” is defined as any acquisition of an applicable debt instrument by the debtor that issued the debt instrument, or is otherwise the obligor or a person related to that debtor.

– A “related person” is defined by reference to Sect. 108(e)(4).

• An “acquisition” is defined to include:

– A “debt‐for‐cash” exchange,

– A “debt‐for‐debt” exchange (including an exchange resulting from a modification of a debt instrument),

– A “debt‐for‐stock” exchange (including debt exchanged for a partnership interest),

The contribution of debt to capital or– The contribution of debt to capital, or

– The complete forgiveness of the indebtedness by the holder of the debt instrument.

• The term “acquisition” also includes an indirect acquisition within the meaning of Treasury Regulations Sect. 1.108‐2(c), if a direct acquisition of the debt instrument would qualify for an election under Sect. 108(i). See Rev. Proc. 2009‐37

• The conference report provides that the enumerated acquisitions apply “without limitation.”

– A government official has confirmed that the term “acquisition” should not be limited to the specified acquisitionsspecified acquisitions.

78

OID Deferral Rule: Debt‐For‐Debt Exchanges

• Sect. 108(i)(2) defers deductions related to OID in debt‐to‐debt exchanges (including exchanges resulting from significant modifications) to match the deferral of income when a debtor makes a Sect. 108(i) election.

OID b t i f l h i ti d bt i t t d t d f th t– OID may be at issue, for example, where existing debt is restructured to defer the payment of interest on the new debt or to increase the interest rate on the new debt instrument.

– The related party rules of Sect. 108(e)(4) apply (i.e., issuance of debt for related party debt covered by Sect. 108(i)(2)).

• If the taxpayer elects to defer COD income under Sect 108(i) and the new debt instrument has• If the taxpayer elects to defer COD income under Sect. 108(i), and the new debt instrument has OID, then the issuer of the debt instrument cannot deduct the portion of the OID that:

– Accrues before the first tax year in the five‐taxable‐year period in which the COD income attributable to the reacquisition of the debt instrument is includible, and

Does not exceed the COD income from the debt instrument being reacquired– Does not exceed the COD income from the debt instrument being reacquired.

• The aggregate amount of these disallowed deductions is allowed as a deduction ratably over the five‐year period to match the inclusion of COD income under Sect. 108(i).

– If the amount of OID accruing before the first tax year in the five‐year period exceeds the amount of deferred COD income then the deductions are disallowed in the order in whichamount of deferred COD income, then the deductions are disallowed in the order in which the OID accrued.

• Note that there is no requirement to defer OID income accruals on the new debt instrument

79

OID Deferral Rule: Deemed Debt‐For‐Debt ExchangesExchanges

• Pursuant to Sect. 108(i)(2)(B), an OID deferral rule applies to deemed debt‐for‐debt exchanges where the issuer of a new debt instrument uses the proceeds directly or indirectly to reacquire an applicable debtthe proceeds directly or indirectly to reacquire an applicable debt instrument.

• The debt instrument that was issued is treated as issued for the debt• The debt instrument that was issued is treated as issued for the debt instrument being reacquired.

h d f l l l f h l d d b h• The OID deferral rule applies if the newly issued debt instrument has OID.

– If only a portion of the proceeds are used to reacquire an applicable debt instrument of the issuer, then the OID deferral rule applies to the portion of any OID on the newly issued debt instrument that is equalportion of any OID on the newly issued debt instrument that is equal to the portion of the proceeds from that instrument used to reacquire the outstanding instrument.

80

Sect. 108(i) – Other RulesAcceleration of deferred items

• Any item of income or deduction deferred under Sect. 108(i) must be taken into account at the time the taxpayer dies, liquidates or sells substantially all of its assets (including in a Title 11 or similar case). §108(i)(5)(D)(i)

– The deferred items will not be accelerated if the taxpayer reorganizes and emerges from the Title 11 case See conference report H R Report 111 16 (2009)Title 11 case. See conference report, H.R. Report 111‐16 (2009)

• The acceleration rule applies to the sale or exchange or redemption of an interest in a partnership, S corporation or other pass‐through entity by a partner, shareholder or other person holding an ownership interest in the entity. §108(i)(5)(D)(i)

• The IRS has been granted authority to extend the application of the acceleration rules “to otherThe IRS has been granted authority to extend the application of the acceleration rules to other circumstances where appropriate.” §108(i)(7)

Earnings and profits (“E&P”)

• Regulations regarding the computation of E&P will be issued and will generally provide that:

– Deferred COD income under Sect. 108(i) increases E&P when realized (i.e., not when includible in gross income).

– Deferred OID deductions under Sect. 108(i) decrease E&P when the deduction would be allowed without regard to Sect 108(i)allowed without regard to Sect. 108(i).

– In the case of RICs and REITs, COD income and OID deductions that are deferred adjust E&P in the tax year(s) such income/deduction is includible/deductible in determining taxable income.

• COD income and OID deductions that are deferred increase or decrease ACE under Sect. 56(g)(4) in the taxable year or years that the income/deduction is includible/deductible in determining taxablethe taxable year or years that the income/deduction is includible/deductible in determining taxable income.

• See Rev. Proc. 2009‐37.81

Sect. 108(i) – Other Rules (Cont.)Sect. 108(i) Other Rules (Cont.)Partnership allocations

• In the case of a partnership any deferred COD income is allocated to the partners• In the case of a partnership, any deferred COD income is allocated to the partners immediately before the discharge in the manner those amounts would have been included in the distributive shares of the partners under Sect. 704 if the income were recognized at that time.

• Any decrease in a partner’s share of partnership liabilities as a result of the discharge is notAny decrease in a partner s share of partnership liabilities as a result of the discharge is not taken into account for purposes of Sect. 752 partnership liability rules to the extent it would cause the partner to recognize gain under Sect. 731.

– Thus, the deemed distribution under Sect. 752 is deferred for a partner to the extent it exceeds the partner’s basis.

• Any decrease in partnership liabilities that is deferred under Sect. 108(i) will be taken into account by the partner at the same time, and to the same extent, as the deferred income is recognized.

• A partnership electing to defer less than all of the COD income realized from its reacquisition p p g qmay determine, in any manner, the portion, if any, of a partner’s COD income amount that is deferred and the portion, if any, of a partner’s COD income that is not deferred.

– A partner can exclude from income its COD income that is not deferred under Sect. 108(a), if applicable.

– These provisions apply only for purposes of Sect. 108(i) and are not intended as an interpretation of or change to existing law under Sect. 704. See Rev. Proc. 2009‐37

82

Sect. 108(i) – ConsolidationIssues in consolidation

• Elections under Sect. 108(i)

• Stock basis adjustments under Treasury Regulations Sect. 1.1502‐32

• Treatment of E&P

• Transactions resulting in the acceleration of deferred Sect. 108(i) amountsamounts

• Application of the matching rule and acceleration rule in Treasury Regulations Sect. 1.1502‐13Regulations Sect. 1.1502 13

• Application of the deemed satisfaction/reissuance approach (the “DSR” approach) of Treasury Regulations Sect. 1.1502‐13(g)

83

Worthless Stock Losses In Consolidation

Worthless Stock Loss:R i t F C it l L U d S t 165( )(1)Requirements For Capital Loss Under Sect. 165(g)(1)

• A corporation (“taxpayer”) may claim a capital loss with respect to the stock of a subsidiary corporation (“Loss Co”) under Sect. 165(g)(1) if Loss Co’s stock is “worthless” in the tax year that the loss is claimed.in the tax year that the loss is claimed.

• To establish worthlessness, Loss Co must:

• Have had value (liquidating or potential) at some point during the tax year, but by year‐end have no liquidating value (i.e., liabilities > FMV of assets) and no potential value (with the lack of potential value generally indicated by an “identifiable event” such as a liquidation); and,

• If Loss Co is a consolidated subsidiary, meet the consolidated return timing standards under Treasury Regulations Sect. 1.1502‐80(c).

85

Worthless Stock Loss:R i t F O di L U d S t 165( )(3)Requirements For Ordinary Loss Under Sect. 165(g)(3)

• A domestic taxpayer may claim an ordinary loss with respect to the stock of Loss Co under Sect. 165(g)(3) if:

– Worthlessness is established for Loss Co’s stock (i.e., the same test as under Section 165(g)(1));

– Loss Co is “affiliated” with taxpayer (i.e., taxpayer must directly own Loss Co stock that has at least 80% of the total voting power and at least 80% of the total value of Loss Co); AND

– More than 90% of Loss Co’s aggregate “gross receipts” for all taxable years are from sources other than royalties, rents, dividends, interest, annuities and gains from the disposition of stocks or securities (i.e., passive income).

• Note that the amount of the worthless stock loss is subject to the unified loss rule under Treasury Regulations Sect. 1.1502‐36.

86

Worthless Stock Loss:E l ti Of G R i t T t I C lid tiEvolution Of Gross Receipts Test In Consolidation

• PLR 200710004 (Mar 9 2007) broke new ground with two of its rulingsPLR 200710004 (Mar. 9, 2007) broke new ground with two of its rulings.

• First:

– Gross receipts are an item under Sect 381(c)Gross receipts are an item under Sect. 381(c).

• Thus, gross receipts of subsidiaries of Loss Co that liquidated or merged into Loss Co in a Sect. 381(a) transaction are included in Loss Co’s gross receipts as if Loss Co had directly earned such receipts (a “step into the shoes” approach).if oss Co had directly earned such receipts (a step into the shoes approach).

• Prior intercompany distributions from such lower‐tier subsidiaries to Loss Co are eliminated, “as appropriate, to prevent duplication.”

– A subsequent ruling confirmed that the Sect. 381 approach applies regardless of whether the lower‐tier subsidiaries are domestic or foreign (e.g., PLR 201006003 (discussed subsequently).

• Sect. 381 approach appears conceptually correct but may be administratively difficult to apply.

87

Worthless Stock Loss:Evolution Of Gross Receipts Test In Consolidation –p

PLR 200710004• Second:

– Dividends from lower‐tier consolidated subsidiaries of Loss Co (that are not covered by the Sect. 381 ruling) are treated as gross receipts from passive sources to the extent they are attributable to the distributing member’s gross receipts from passive sources (a “look through” or single‐entity approach for intercompany p ( g g y pp p ydistributions)

• In applying the look through approach, “dividends will be attributed pro rata to the gross receipts that gave rise to the E&P from which the dividend was d b d ”distributed.”

– Subsequent PLRs depart from the approach of looking to E&P.

• Compare TAM 200727016 (July 6, 2007), denying a look through approach for dividends received by Loss Co from foreign subsidiaries.

• See also PLR 200932018 (Aug. 7, 2009), which is generally consistent with PLR 200710004 i l i th S t 381 h d th l k th h h200710004 in applying the Sect. 381 approach and the look through approach for intercompany dividends.

88

Worthless Stock Loss:Evolution Of Gross Receipts Test In Consolidation –p

PLR 201006003 (Feb. 12, 2010)

• Continues the Sect. 381 approach (and reiterates that prior “intercompany distributions” are eliminated to prevent duplication).

• Clarifies the look through approach by denying the approach for intercompany distributions made out of E&P and received by Loss Co in a tax year beginning prior to July 12, 1995 (i.e., under the prior version of the intercompany transaction regulations).

89

Worthless Stock Loss:Evolution Of Gross Receipts Test In Consolidation –p

PLR 201011003 (March 19, 2010)• An accelerated movement toward single‐entity treatment

• Expands look through approach to ALL intercompany transactions

– Loss Co includes in its gross receipts all amounts from “intercompany g p p ytransactions” (as described in the current regulations under Treasury Regulations Sect. 1.1502‐13), and such amounts are treated as gross receipts from passive sources to the extent they are attributable to the counterparty’s gross receipts from passive sources.

– Look through is required until a source of income from outside the group is reached (i.e., the counterparty member applies the same methodology for its gross receipts from other members until the ultimate counterparty that transacts with outside parties is reached)that transacts with outside parties is reached).

• Continues the Sect. 381 approach

Loss Co must eliminate gross receipts from all intercompany transactions– Loss Co must eliminate gross receipts from all intercompany transactions with the transferor, “as appropriate, to prevent duplication.”

90

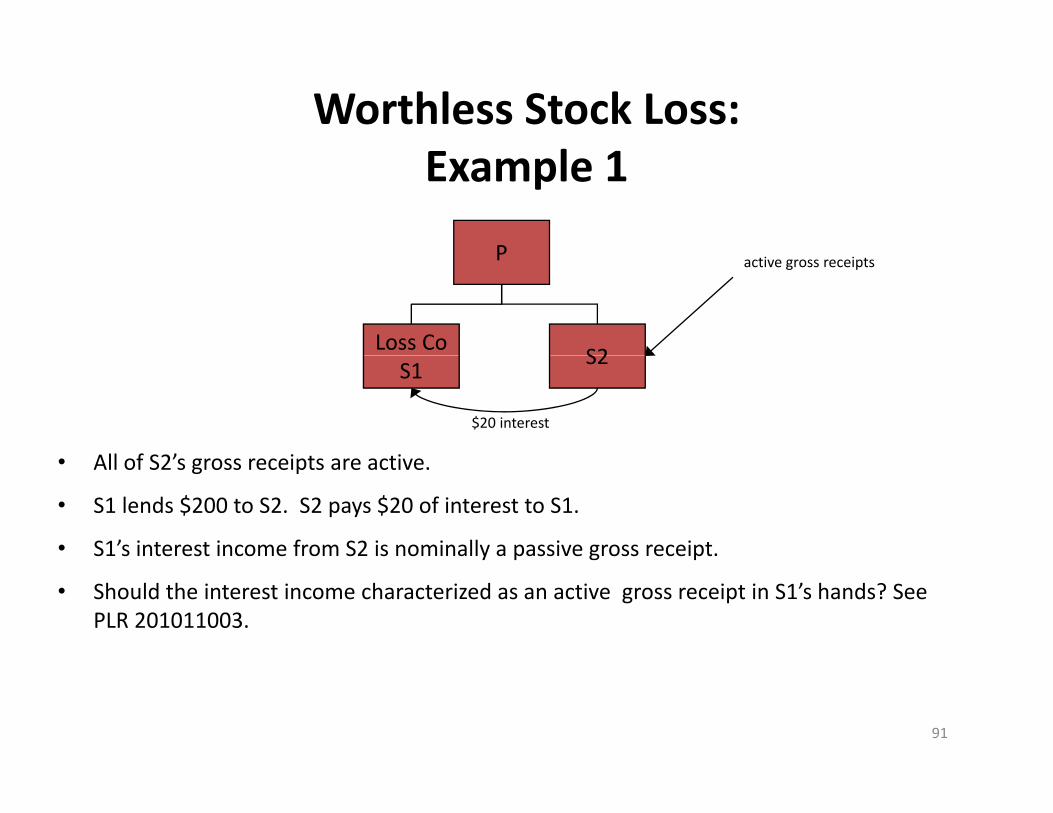

Worthless Stock Loss:lExample 1

P

S2

P

Loss Co

active gross receipts

S2S1

All f S2’ i t ti

$20 interest

• All of S2’s gross receipts are active.

• S1 lends $200 to S2. S2 pays $20 of interest to S1.

• S1’s interest income from S2 is nominally a passive gross receipt.

• Should the interest income characterized as an active gross receipt in S1’s hands? See PLR 201011003.

91

Worthless Stock Loss:lExample 2

P

S2

P

Loss Co

passive gross receipts

S2S1

All f S2’ i t i

$200 purchase price

• All of S2’s gross receipts are passive.

• S1 sells a truck to S2 in the course of S1’s business for $200.

• S1’s proceeds for the sale are active gross receipts.

• Should the sales proceeds characterized as passive gross receipts in S1’s hands? See PLR 201011003.

92

Worthless Stock Loss:Evolution Of Gross Receipts Test In Consolidation –p

PLR 201011003

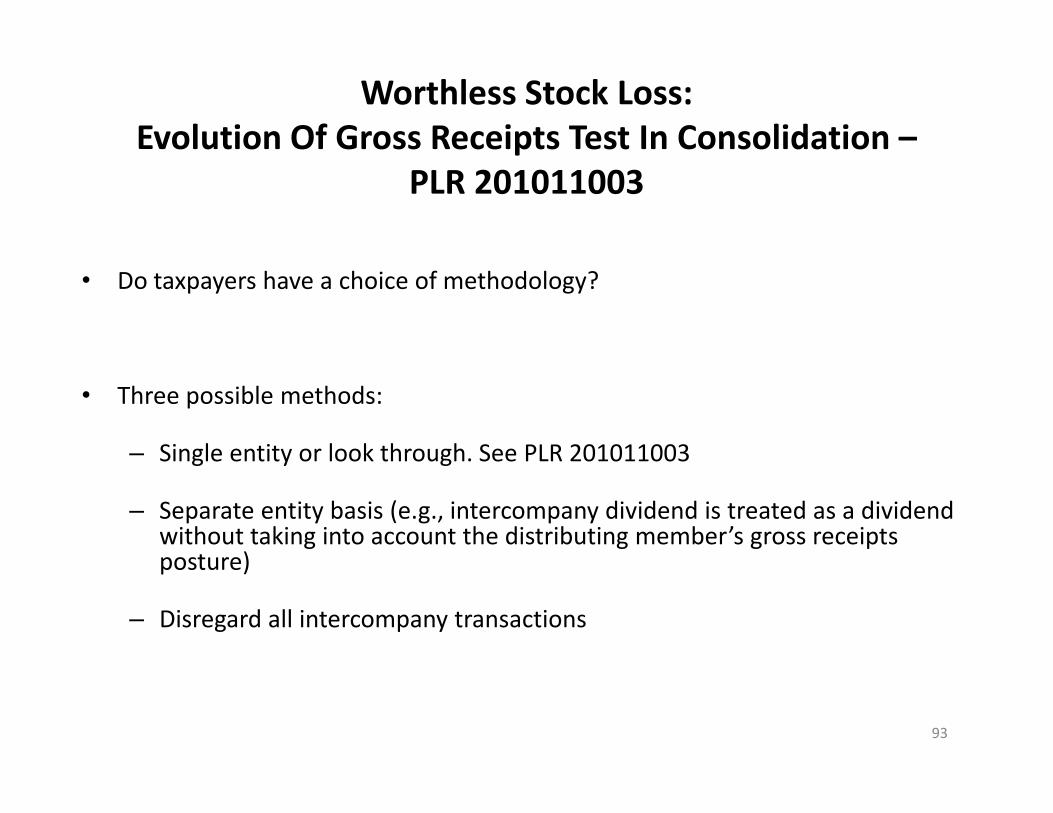

• Do taxpayers have a choice of methodology?

• Three possible methods:

– Single entity or look through See PLR 201011003Single entity or look through. See PLR 201011003

– Separate entity basis (e.g., intercompany dividend is treated as a dividend without taking into account the distributing member’s gross receipts posture)posture)

– Disregard all intercompany transactions

93

NOL Carryback ChangesNOL Carryback Changes

94

Overview Of New Five‐Year Extended NOL C b k El tiCarryback Election

• The Worker, Homeownership, and Business Assistance Act of 2009 (the “Act”), signed into law on Nov. 6, 2009, allows most taxpayers an extended carryback period of up to five years for net operating losses (NOLs) incurred in a tax year beginning or ending in 2008 or 2009.

• Key provisions:

– Ability to elect extended carryback period for 2008 or 2009 NOL

– 50% limitation for NOL carried back to fifth year– Removal of 90% limitation for AMT NOL carryback– Special rules for small businesses, life insurance companies and Troubled

A t R li f P (TARP) i i tAsset Relief Program (TARP) recipients– Modification of corporate equity reduction transaction (CERT) rules to

conform with the extended carryback provision

95

Election To Extend Carryback From 2008 Or 2009

• The five‐year extended carryback period is available for any NOL incurred in a tax year beginning or ending in 2008 or 2009.

• The election to extend the carryback period, however, can only be made for an NOL from one tax year.

• Guidance issued in Rev. Proc. 2009‐52, 2009‐49 I.R.B. 744 (discussed subsequently)

96

Exception For TARP RecipientsException For TARP Recipients

• The extended carryback election is not available for “TARP recipients,” as d fi d i hdefined in the Act.

– If the federal government acquired before the date of enactment an equity interest in the taxpayer or any warrant (or other right) to acquire any equity interest with respect to the taxpayertaxpayer,

– If the taxpayer receives after the date of enactment funds from the federal government in exchange for such an equity interest or warrant, and

– Fannie Mae and Freddie Mac– Fannie Mae and Freddie Mac.

• These rules apply to “any taxpayer” which at any time in 2008 or 2009 was or is a member of the same affiliated group determined without regard to Sect 1504(b) as a taxpayer described aboveSect. 1504(b) as a taxpayer described above .

• If a taxpayer becomes a TARP recipient after making the NOL carryback election, then it is retroactively rendered ineligible for the extended

b k d b i d t fil d d tcarryback and may be required to file amended returns.

97

Statutory LanguageStatutory Language

• In general, Sect. 172(b)(1)(H) allows a taxpayer to elect to carry back an “applicable net operating loss” for between three and five years, rather than the two‐year period otherwise allowed.

– “The term ‘applicable net operating loss’ means the taxpayer’s net operating loss for a taxable year ending after December 31 2007 and beginning before January 1 2010”taxable year ending after December 31, 2007, and beginning before January 1, 2010 .

– JCT Explanation (JCX‐44‐09): “For all elections under this provision, the common parent of a group of corporations filing a consolidated return makes the election, which is binding on all such corporations”.

• The election “shall be made by the due date (including extension of time) for filing the return for the taxpayer’s last taxable year beginning in 2009.”

• Once made, the election is irrevocable.

• Statute authorizes the issuance of anti‐abuse regulations.

98

Rev. Proc. 2009‐52

• Provides “basic” guidance to allow taxpayers to elect to carry back an applicable net operating loss for a period of three four or five years toapplicable net operating loss for a period of three, four or five years, to offset taxable income in those preceding taxable years.

– For taxpayers that have not claimed a deduction for an applicable NOL

– For taxpayers that previously claimed a deduction for an applicable NOLFor taxpayers that previously claimed a deduction for an applicable NOL

– For taxpayers that previously filed an election under section 172(b)(3) to forgo the NOL carryback period