Embed Size (px)

Citation preview

Presenting the Results of a DFA Study to Management

Casualty Actuarial Society

Seminar on Dynamic Financial Analysis

July 17-18, 2000

Gerald S. Kirschner, FCAS, MAAA

Liberty Mutual Group

LMN

2

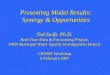

DFA Model Structure

(2)

Invested

Assets

Accounting

and

Cashflow

(1)

Economic

Scenarios

(4)

Underwriting

Cashflow

(8)

Financial

Statements

(9)

Report

Generator

(6)

Reinvest

Cashflow

(7)

Taxes

(5)

Miscellaneous

Cashflow

(3)

Underwriting

Scenarios

Loss

Expense

Other

Premiums

3

Framing the Question

“What actions can my organization take

to maximize our expected economic net

worth* five years from now?”

* Economic net worth = all assets at market

value, all liabilities at their present value.

Present value calculated using a risk-free rate

of return -- i.e. no risk loading included in

liability valuation.

4

Considerations

Look at influence caused by various possible

future states of the world:

Interest rates

Equity returns

Inflation

Volatility in underwriting and company operations

Influence of various portfolio mixes on expected

future net worth values and the associated

volatility of results

Projected statutory capital versus capital

required by NAIC’s Risk Based Capital formula

5

Impact of Stochastic Elements

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Pe

rce

nt

of

Ob

se

rva

tio

ns

in

Ra

ng

e

55 61 66 72 78 84 90 96 102

108

114

120

126

132

138

144

150

156

162

168

Year Five Economic Net Worth (in Units)

Distribution of Year Five Economic Net Worth

arising from the modeling of all sources of variability

Deterministic Base Case

Year 5 Economic Net Worth

6

Impact of Stochastic Elements - an Alternative Way to View Results

Impact on Year Five Economic Net Worth

Arising From All Modeled Sources of Variability

40 Units

60 Units

80 Units

100 Units

120 Units

140 Units

160 Units

1 50 100 150 200 250 300 350 400 450 500 550 600 650 700 750 800

Observation

Ec

on

om

ic N

et

Wo

rth

1927 - 1939 1940 - 1949 1950 - 1959 1960 - 1969 1970 - 1979 1980 - 1989 1990 - 1998

Fully Deterministic State Stochastic Base Case

7

Drivers of Volatility

Influence of Different Elements on Variation

from Base Case to Totally Variable State

Variable

Interest

Rates

10%

Time T1 - T5 Loss

Ratio Volatility

8%Time T0 Loss

Reserve Volatility

7%

Payout Pattern

Volatility

2%

Variable

Inflation

Rates

21%

Variable Stock

Market Returns

36%

Variation Not

Accounted For

16%

8

Reinvestment Alternatives

Government bonds

Corporate bonds

High yield bonds

Tax-exempt bonds

Cash

Common stocks

Status quo (= 6% government, 60%

corporate, 2% high yield, 14% tax exempt,

5% cash and 13% common stock)

9

Effect of Alternative Investment Strategies on Economic Net Worth

Base

StatusQuo

Alt. 1:

All Govt.Bonds

Alt 2:

All Corp.Bonds

Alt 3:

All HighYield

Bonds

Alt 4:

All TaxExemptBonds

Alt 5:

All Cash

Alt 6:

AllCommon

Stock

EconomicNet Worth

Mean Value

100.0 97.2 98.6 100.6 98.3 97.9 108.0

Percentincrease overStatus Quo

N/A -3% -1% 1% -2% -2% 8%

StandardDeviation 15.6 14.0 14.1 14.2 14.6 14.3 27.3

Percentincrease overStatus Quo

N/A -11% -10% -9% -7% -9% 75%

10

40 Units

60 Units

80 Units

100 Units

120 Units

140 Units

160 Units

180 Units

200 Units

220 Units

1 100 200 300 400 500 600 700 800

Observation

Ec

on

om

ic N

et

Wo

rth

Graphical View of the Effect of Alternative Investment Strategies

Status Quo 100% Comm. Stock 100% High Yield Bonds Fully Deterministic State

1927-1939 1940-1949 1950-1959 1960-1969 1970-1979 1980-1989 1990-1998

Variations in Economic Net Worth Caused by

Alternative Asset Reinvestment Strategies

11

Influence of Economic Variables on RBC Calculation

Examined relationships between the

calculated RBC ratios and:

average stock market returns

average long term interest rates

average overall inflation rates

Common stock strategy is most heavily

influenced by stock market movements,

less by interest rate or inflation rate

changes

12

Graphical View of Capital Adequacy Variations

0.00

0.50

1.00

1.50

2.00

2.50

3.00

1 100 200 300 400 500 600 700 800

Ra

tio

: A

ctu

al

Ca

pit

al

to N

ee

de

d C

ap

ita

l

Fully Deterministic StateStatus Quo 100% Comm Stock Target Minimum100% High Yield Bonds

Observation

Year Five Capital Adequacy

1927 - 1939 1940 - 1949 1950 - 1959 1960 - 1969 1970 - 1979 1980 - 1989 1990 - 1998

% Observations below the Target Minimum

0.0% - Status Quo

7.9% - Common Stock

0.0% - High Yield

13

Revisiting the Impact of Alternative Investment Strategies on Net Worth

Base

StatusQuo

Alt. 1:

All Govt.Bonds

Alt 2:

All Corp.Bonds

Alt 3:

All HighYield

Bonds

Alt 4:

All TaxExemptBonds

Alt 5:

All Cash

Alt 6:

AllCommon

Stock

EconomicNet Worth

Mean Value

100.0 97.2 98.6 100.6 98.3 97.9 108.0

Percentincrease overStatus Quo

N/A -3% -1% 1% -2% -2% 8%

StandardDeviation 15.6 14.0 14.1 14.2 14.6 14.3 27.3

Percentincrease overStatus Quo

N/A -11% -10% -9% -7% -9% 75%

14

Efficient Frontiers of Alternative Asset Mixes

Analyze the risk / return tradeoffs

associated with varying the % of assets

reinvested in:

Common stocks versus high yield bonds

Common stocks versus the relative

percentage invested in all other asset

classes

Examine each mix’s downside potential

15

“Efficient Frontier” of Common Stock / High Yield Bond mix options

Common Stock vs. High Yield Bond Efficient Frontier:

Economic Net Worth versus Ratio of Held Capital to Needed Capital

98 Units

100 Units

102 Units

104 Units

106 Units

108 Units

110 Units

1.350 1.400 1.450 1.500 1.550 1.600 1.650 1.700

Ratio: Actual Capital to Needed Capital

Ec

on

om

ic N

et

Wo

rth

Common Stock & High Yield Bond Mix Reinvestment Alternatives - Average of Stochastic Observations

Status Quo Reinvestment Alternatives - Average of Stochastic Observations

Higher Economic

Net Worth, using

more Capital:

Higher return with

more risk

Lower Economic Net Worth, using more Capital:

Lower return with more risk

Higher

Economic

Net Worth,

using less

Capital:

Higher

return

with

less risk

A

DC

EF

GH

J

I

B

K

Point A: 100% common stock

Point K: 100% high yield bonds

16

Varying Level of Common Stock Efficient Frontier:

Economic Net Worth versus Ratio of Held Capital to Needed Capital

98 Units

100 Units

102 Units

104 Units

106 Units

108 Units

110 Units

1.350 1.400 1.450 1.500 1.550 1.600 1.650 1.700

Ratio: Actual Capital to Needed Capital

Ec

on

om

ic N

et

Wo

rth

“Efficient Frontier” of Common Stock / Status Quo mix options

Varying % of Common Stock relative to rest of Status Quo portfolio - Average of Stochastic Observations

Status Quo Reinvestment Alternatives - Average of Stochastic Observations

Higher Economic

Net Worth, using

more Capital:

Higher return with

more risk

Lower Economic Net Worth, using more Capital:

Lower return with more risk

Higher

Economic

Net Worth,

using less

Capital:

Higher

return

with

less risk

A

D

C

E

F

G

H

J

I

B

K

Point A: 100% common stock

Point K: 0% common stock

17

Comparison of the Risk/Return Tradeoff Associated with Varying the

Reinvestment Mix of Cash and Common Stock

0% Comm. Stk.

10% Comm. Stk.

20% Comm. Stk.

30% Comm. Stk.

40% Comm. Stk.

50% Comm. Stk.

60% Comm. Stk.

70% Comm. Stk.

80% Comm. Stk.

90% Comm. Stk.

100% Comm. Stk.

98 Units

100 Units

102 Units

104 Units

106 Units

108 Units

110 Units

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

Ec

on

om

ic N

et

Wo

rth

“Downside Potential” of Common Stock / Status Quo mix options

Varying Common Stock Reinvestment Percentage - Average of Stochastic Observations

Status Quo Reinvestment Alternatives - Average of Stochastic Observations

% of Observations Falling Below Targeted Minimum Capital Threshold

Recommendation

to management