Embed Size (px)

Citation preview

Presenting: Board Orientation

YourCredit Union

Date of OrientationLocation of Orientation

Section 1

Overview of theCredit Union Movement

Overview of the Credit Union Movement

Nonprofit Financial Institutions in a For-Profit Industry

Member-Owned• Financial cooperatives organized to help

members achieve their financial goals (not make a profit for shareholders)

A Proud Tradition• “Not for profit, not for charity, but for service”

Governance• Board of directors elected by members, not

shareholders

Overview of the Credit Union Movement

History of Credit Unions • Founded in Europe in 1800s as “people’s banks”

• First formed in North America as an alternative to loan sharks for working-class people

• Credit unions chartered to serve narrowly defined fields of membership (workplace, profession or trade, community, association, church)

• Federal Credit Union Act became law in 1934

• National Credit Union Administration created to 1970 to charter and supervise federal credit unions

Overview of the Credit Union Movement

History of Credit Unions (cont.)Credit unions were founded to “make the system

work better for more people. … The founders of credit unionism … stressed participation by all members. The goal, then, was economic democracy through self-help.”

--J. Carroll Moody and Gilbert C. Fite, The Credit Union Movement: Origins and Development, 1850-1970

Overview of the Credit Union Movement

Credit Unions Today• Many serve wider fields of membership through

select employer groups (SEGs) and community charters

• Consolidation means fewer, but financially stronger, credit unions

• Full-service financial institutions

• Committed to “people helping people” through financial education and member advocacy

• Heavily regulated to protect members’ assets and organizational safety and soundness

Section 2

About theCredit Union

About the Credit Union

MissionYour mission statement here.

About the Credit Union

VisionYour vision statement here.

About the Credit Union

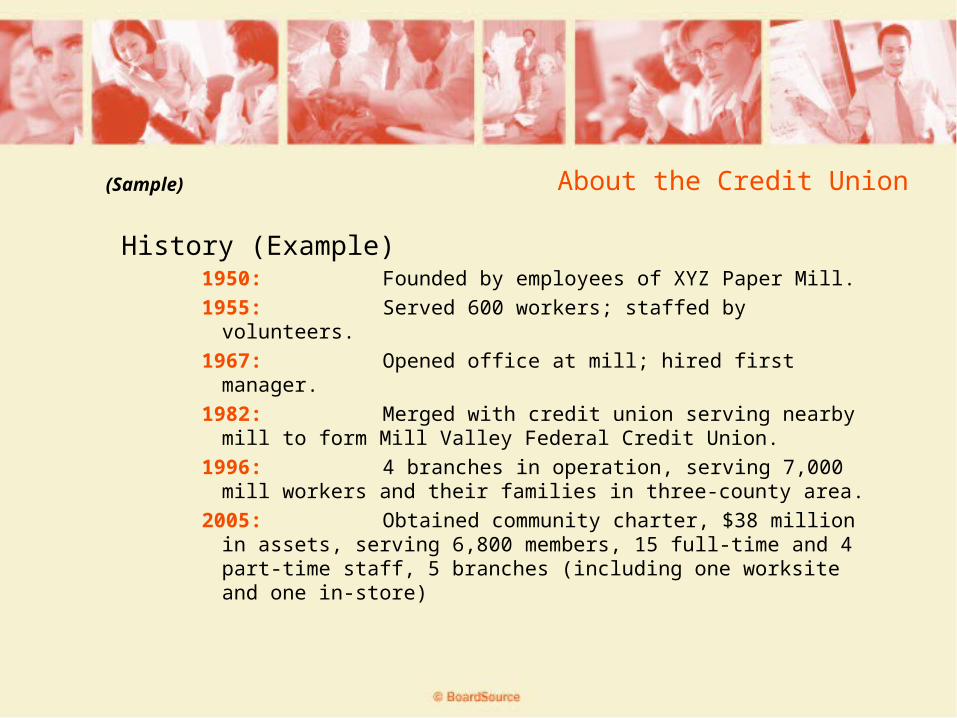

History (Example)1950: Founded by employees of XYZ Paper Mill.

1955: Served 600 workers; staffed by volunteers.

1967: Opened office at mill; hired first manager.

1982: Merged with credit union serving nearby mill to form Mill Valley Federal Credit Union.

1996: 4 branches in operation, serving 7,000 mill workers and their families in three-county area.

2005: Obtained community charter, $38 million in assets, serving 6,800 members, 15 full-time and 4 part-time staff, 5 branches (including one worksite and one in-store)

(Sample)

About the Credit Union

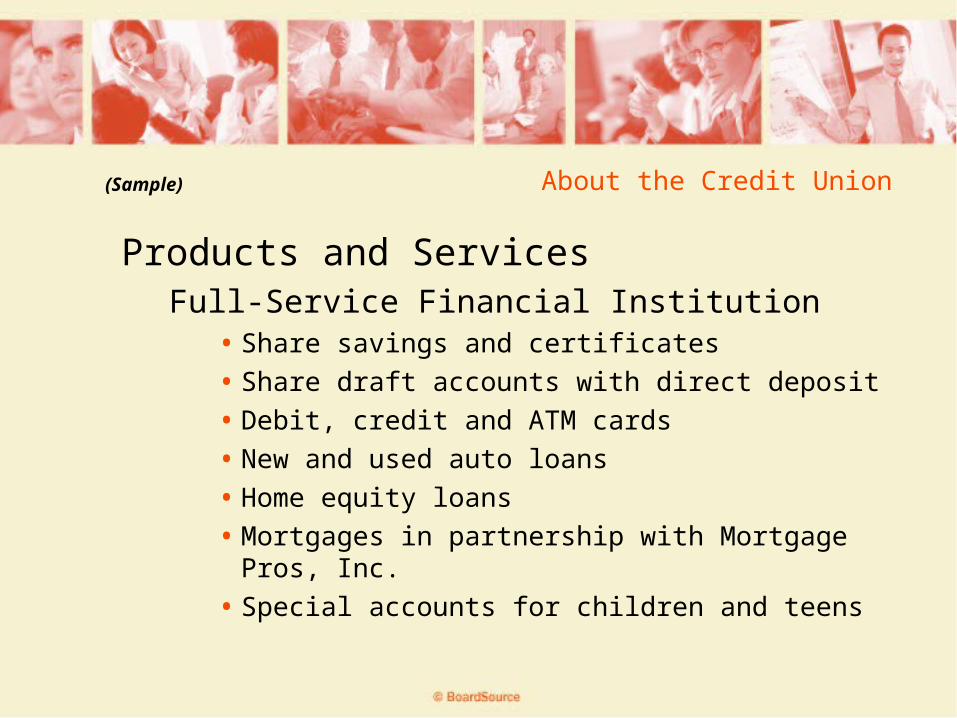

Products and ServicesFull-Service Financial Institution

• Share savings and certificates

• Share draft accounts with direct deposit

• Debit, credit and ATM cards

• New and used auto loans

• Home equity loans

• Mortgages in partnership with Mortgage Pros, Inc.

• Special accounts for children and teens

(Sample)

About the Organization(Sample)

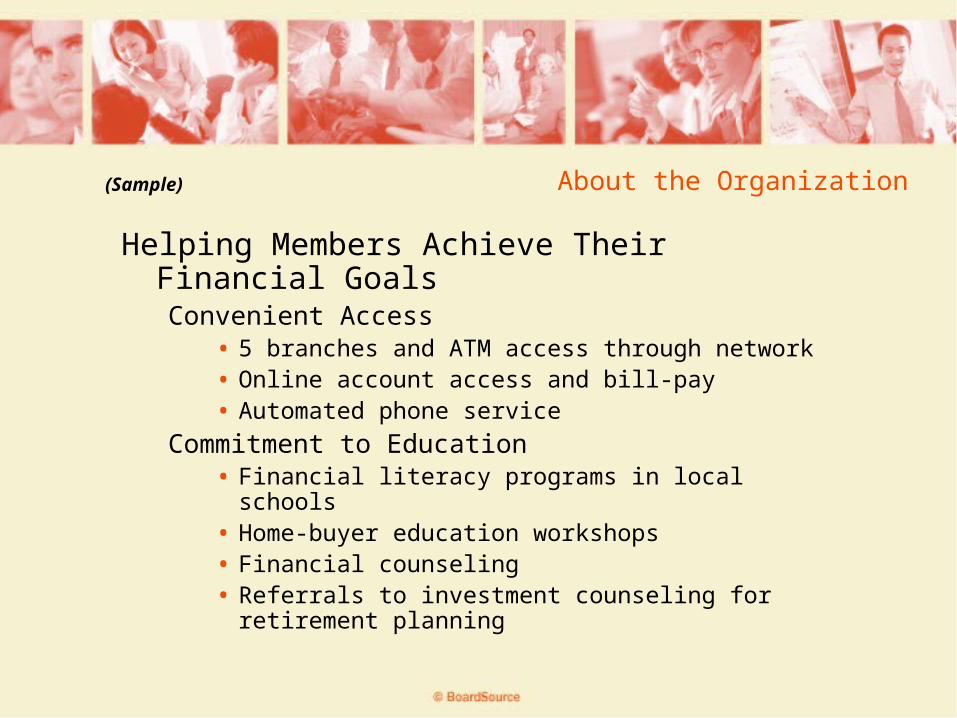

Helping Members Achieve Their Financial GoalsConvenient Access

• 5 branches and ATM access through network• Online account access and bill-pay• Automated phone service

Commitment to Education• Financial literacy programs in local schools• Home-buyer education workshops • Financial counseling • Referrals to investment counseling for retirement

planning

About the Credit Union

By the Numbers• Current number of members• Assets• Current number of employees• Key financial indicators, ratios and trends

(perhaps presented in comparison to industry average)

About the Credit Union

Strategic Goals Develop branch-based member recruitment.

• Train and incent branch managers to lead recruitment efforts of prospective members within a 5-mile radius

• Open 25 new share draft accounts per month at each branch

• Recruit five new SEGs within each branch territory

Position credit union as member-friendly mortgage alternative.

• Provide referral packets to area real estate offices • Offer home-buyer workshops to SEG groups• Partner with local community groups to promote affordable

mortgage to first-time home buyers

(Sample)

About the Organization

Strategic Goals, cont. Increase membership in 18-34 age group.

• Launch “noon-hour branches” at three high schools, staffed by students and offered in conjunction with financial literacy curriculum.

• Package free share draft accounts with debit cards and no-fee ATM access and low-cost computer/book loans to college students

• Introduce low-cost used car loans with low down payment requirements for first-time car buyers

Streamline operations to offer best possible rates. • Assess potential of check imaging to reduce processing costs. • Introduce incentives to steer members to e-statements and online

account access.

(Sample)

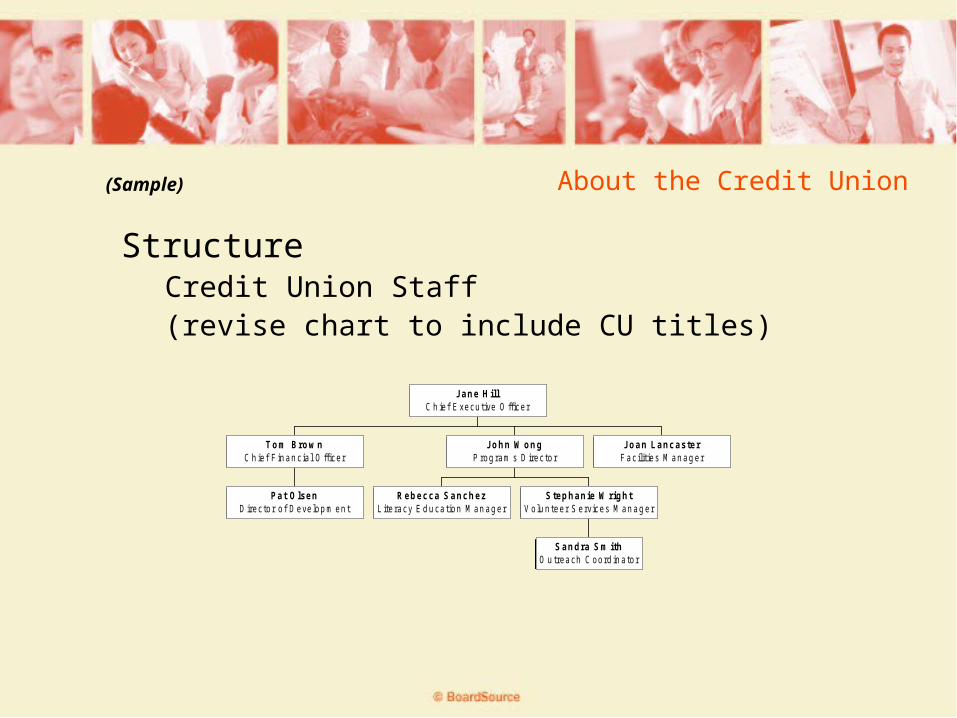

About the Credit Union

StructureCredit Union Staff(revise chart to include CU titles)

(Sample)

Pat OlsenD irec to r o f D eve lop m en t

Tom Brow nC h ie f F in an c ia l O ffice r

Rebecca SanchezL ite racy E d u ca tion M an ag er

Sandra Sm ithO u treach C oord in a to r

Stephanie W rightV olu n teer S ervices M an ag er

John W ongP rog ram s D irec to r

Joan LancasterF ac ilit ies M an ag er

Jane HillC h ie f E xecu tive O ffice r

About the Credit Union

Community PartnershipsSponsors, SEGs

• 75 SEGs and counting• Branch on XYZ campus• Homebuyer education program offered through

Mill Valley Community Association

Support for Local Schools and Community Groups

• Sponsor financial literacy programs in local schools

• Cosponsor annual Run to Save the River

(Sample)

Section 3

Aboutthe Board

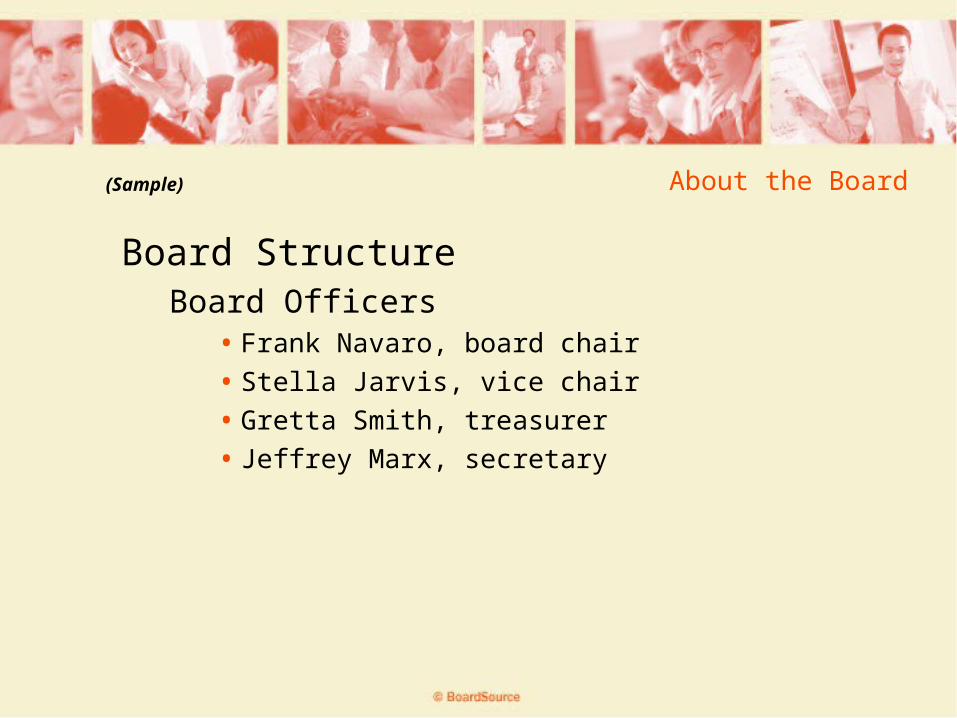

About the Board

Board StructureBoard Officers

• Frank Navaro, board chair

• Stella Jarvis, vice chair

• Gretta Smith, treasurer

• Jeffrey Marx, secretary

(Sample)

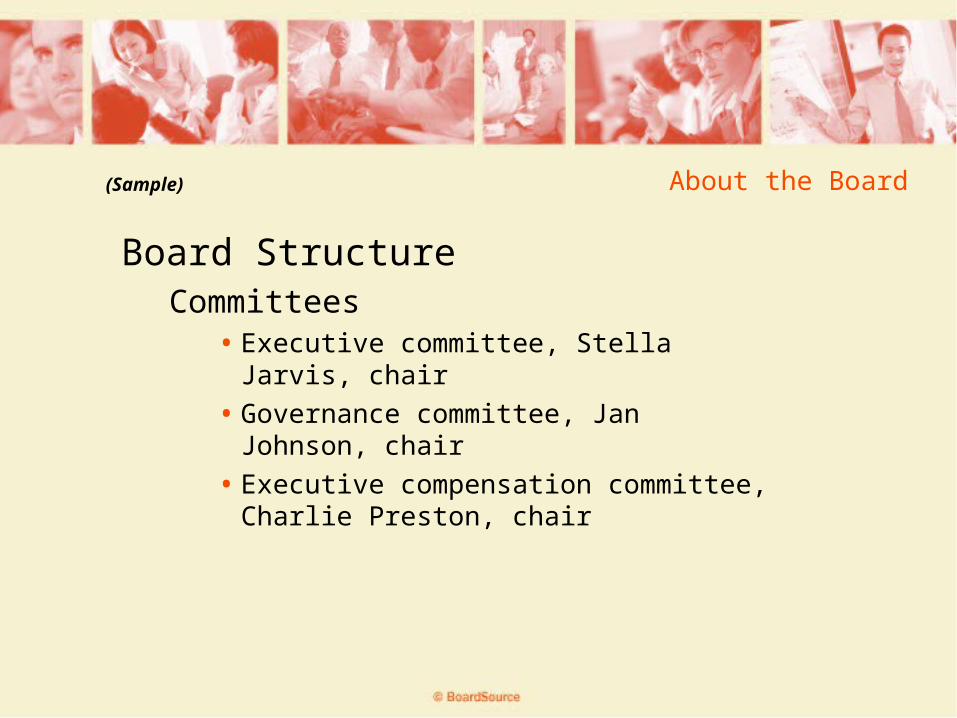

About the Board

Board StructureCommittees

• Executive committee, Stella Jarvis, chair

• Governance committee, Jan Johnson, chair

• Executive compensation committee, Charlie Preston, chair

(Sample)

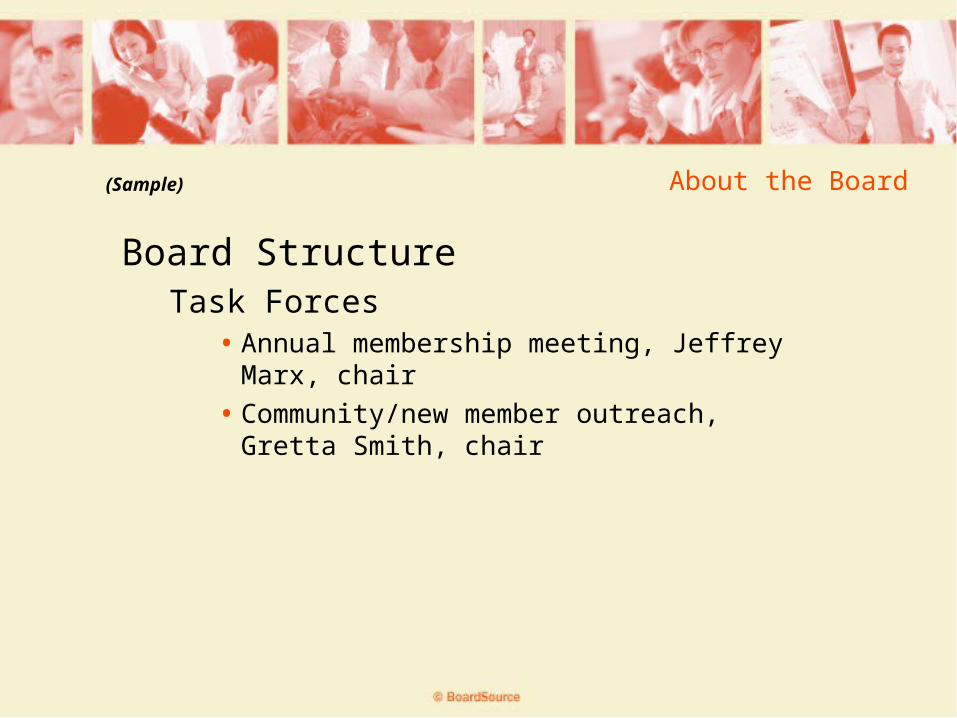

About the Board

Board StructureTask Forces

• Annual membership meeting, Jeffrey Marx, chair

• Community/new member outreach, Gretta Smith, chair

(Sample)

About the Board

Board OperationsBoard Composition and Recruitment

• 9 directors

• Three-year terms

• Three consecutive term maximum service

• Governance committee leads recruitment and nominating process

(Sample)

About the Board

Board Consultants• Legal counsel, Peter Nunez, Esq.

• Auditor, Valerie Lourdes, CPA

• Strategic planning facilitator, Sylvia Grant

(Sample)

About the Board

Reading List• Bylaws

• Board policies

• Board biographies

• Prior year’s annual audit

• Budget

• Annual report

• Strategic plan

(Sample)

About the Board

Board Calendar• Board meetings / dates

• Annual membership meeting / dates

• Chief executive performance evaluation / date

• Annual strategic planning retreat / date

• Annual audit / date

(Sample)

Section 4

BoardRoles andResponsibilities

Board Roles and Responsibilities

Board FunctionOrganizational Governance

• Authority

• Accountability

Board Roles and Responsibilities

Key Roles of the BoardSet Organizational DirectionProvide OversightEnsure Safety and Soundness

Board Roles and Responsibilities

Board RoleSet Organizational Direction

Responsibilities:▪ Participate in regular strategic planning

▪ Determine organization’s mission

▪ Set the vision for the future

▪ Establish organizational values

▪ Set major goals and develop strategies

▪ Approve operational or annual plans

Board Roles and Responsibilities

Board RoleEnsure Necessary Resources

Responsibilities:▪ Hire capable executive leadership

▪ Ensure adequate financial resources

▪ Promote positive public image

▪ Ensure the presence of a capable and responsible board

Board Roles and Responsibilities

Board RoleProvide Oversight

Responsibilities:▪ Oversee financial management

▪ Minimize exposure to risk

▪ Measure progress on strategic plan

▪ Monitor and evaluate programs and services

▪ Provide legal and moral oversight

▪ Evaluate the chief executive (annually)

▪ Evaluate itself (every two to three years)

Board Roles and Responsibilities

Individual DirectorResponsibilities

Act in Accordance with Legal StandardsDuty of Care

▪ Stay informed and ask questions

Duty of Loyalty▪ Show undivided allegiance to credit union’s welfare

Duty of Obedience▪ Stay faithful to the credit union’s mission

Board Roles and Responsibilities

Individual DirectorResponsibilities

• Participate in the governance of the organization

• Work on committees and task forces

• Volunteer services to the credit union outside of board work

• Serve as ambassador to the member community

![INDEX [] · Semester 1 Semester 2 Year 1 • Vision & policy • Introduction to Tourism • Cultural Orientation • English, Training reporting & presenting, Excel Year 1 • Successful](https://img.pdfslide.us/doc/110x75/60455d3cf5e6cf4df5105674/index-semester-1-semester-2-year-1-a-vision-policy-a-introduction.jpg)