Embed Size (px)

Citation preview

Presenting a live 110‐minute teleconference with interactive Q&A

Executive Compensation Tax Issues in Mergers and AcquisitionsNavigating Tax Rules for Stock Options Deferred Navigating Tax Rules for Stock Options, Deferred and Equity Compensation, Golden Parachutes, and More

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, APRIL 11, 2013

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Stuart M Finkelstein Partner Skadden Arps Slate Meagher & Flom New YorkStuart M. Finkelstein, Partner, Skadden Arps Slate Meagher & Flom, New York

Regina Olshan, Partner, Skadden Arps Slate Meagher & Flom, New York

Attendees seeking CPE credit must listen to the audio over the telephone.

Please refer to the instructions emailed to registrants for dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Quality

S d Q litSound QualityFor this program, you must listen via the telephone by dialing 1-866-570-7602 and entering your PIN when prompted. There will be no sound over the web connection.

If you dialed in and have any difficulties during the call, press *0 for assistance. You may also send us a chat or e-mail [email protected] immediately so we can address the problemwe can address the problem.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE credits, please let us know how many people are listening online by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

For CPE credits, attendees must listen to the audio over the telephone. Attendees can still view the presentation slides online.

Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open. Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

EXECUTIVE COMPENSATION, EMPLOYEE BENEFITS AND TAX ISSUES IN CORPORATE M&A TRANSACTIONS

Regina OlshanSkadden Arps Slate

Presented byStuart M. FinkelsteinSkadden Arps Slate Skadden, Arps, Slate,

Meagher & Flom LLP, New York

Skadden, Arps, Slate, Meagher & Flom LLP, New York

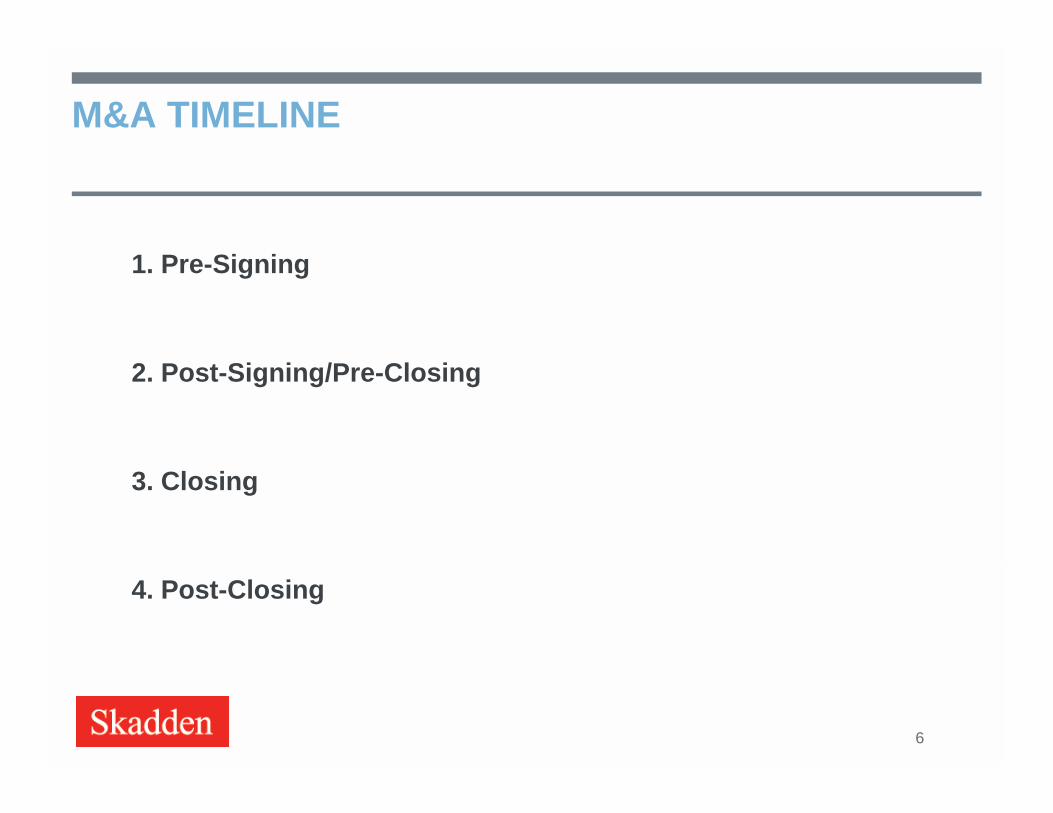

M&A TIMELINE

1. Pre-Signing

2. Post-Signing/Pre-Closing

3. Closing

4. Post-Closing

6

1. PRE-SIGNING

7

1. PRE-SIGNING

A. Structuring the Deal

B. Conducting Diligence

C. Negotiating the Transaction Document

D. Considering Retention/Employment Arrangements

8

A. Structuring the Deal

9

1. PRE-SIGNINGA St t i th D l

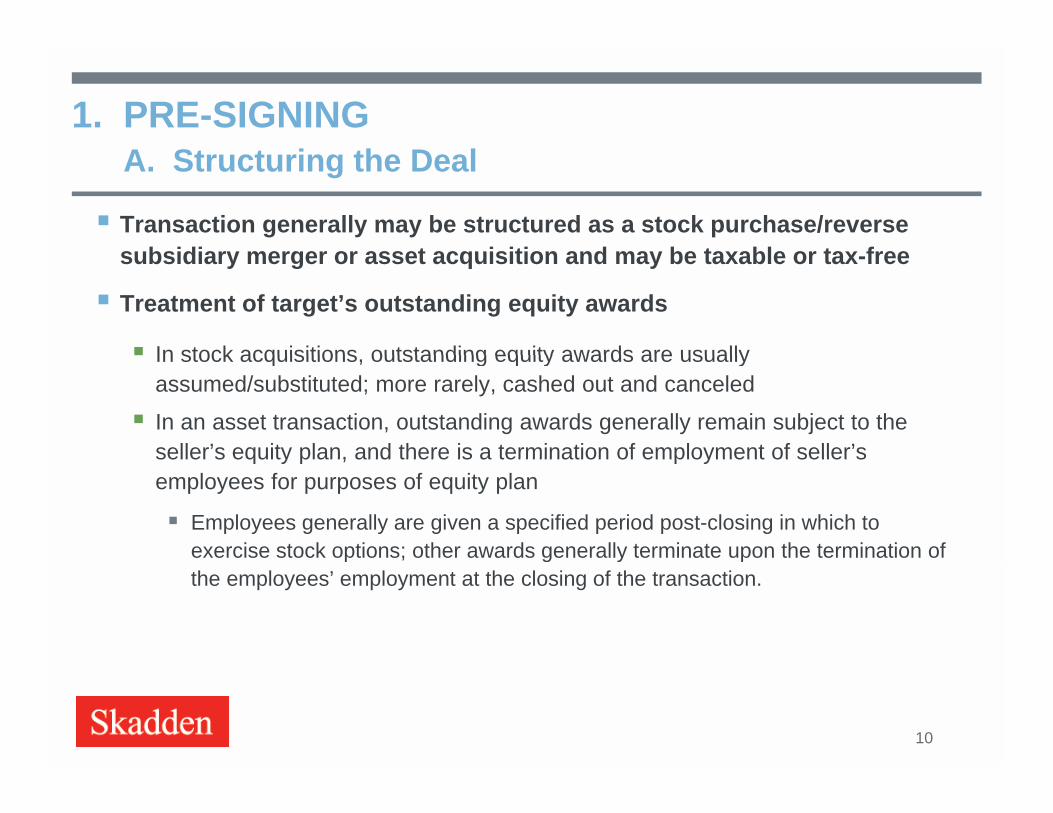

Transaction generally may be structured as a stock purchase/reverse subsidiary merger or asset acquisition and may be taxable or tax free

A. Structuring the Deal

subsidiary merger or asset acquisition and may be taxable or tax-free

Treatment of target’s outstanding equity awards

In stock acquisitions outstanding equity awards are usuallyIn stock acquisitions, outstanding equity awards are usually assumed/substituted; more rarely, cashed out and canceled

In an asset transaction, outstanding awards generally remain subject to the seller’s equity plan, and there is a termination of employment of seller’sseller s equity plan, and there is a termination of employment of seller s employees for purposes of equity plan

Employees generally are given a specified period post-closing in which to exercise stock options; other awards generally terminate upon the termination of p ; g y pthe employees’ employment at the closing of the transaction.

10

A St t i th D l1. PRE-SIGNING

A. Structuring the Deal

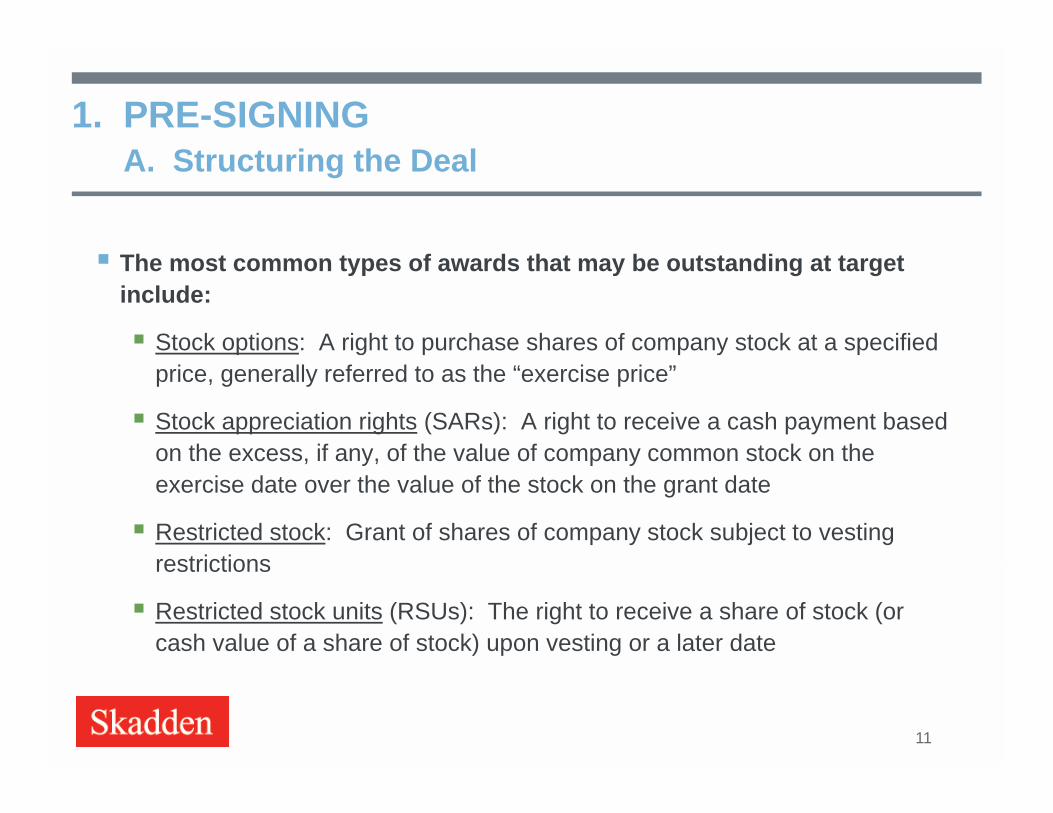

The most common types of awards that may be outstanding at target include:

Stock options: A right to purchase shares of company stock at a specified price, generally referred to as the “exercise price”

Stock appreciation rights (SARs): A right to receive a cash payment based on the excess if any of the value of company common stock on theon the excess, if any, of the value of company common stock on the exercise date over the value of the stock on the grant date

Restricted stock: Grant of shares of company stock subject to vesting restrictionsrestrictions

Restricted stock units (RSUs): The right to receive a share of stock (or cash value of a share of stock) upon vesting or a later date

11

1. PRE-SIGNINGA St t i th D l T t t f E it A d

Considerations for determining treatment of equity awards:

A. Structuring the Deal: Treatment of Equity Awards

g q y

business decisions/use of cash

dilution of acquiror’s shareholders

l f t f th ti prevalence of out-of-the-money options

ability to achieve retention benefits through continuation of awards

terms of the applicable equity compensation plans

legal compliance issues raised in diligence

legal limitations (e.g., consent requirements, substitution limitations)

Section 280G golden parachutes and potential gross-upsg p p g p

administrative burden considerations: equity tracking, employee communications, accounting, SEC registration

international compliance

12

1. PRE-SIGNINGA St t i th D l T t t f E it A d

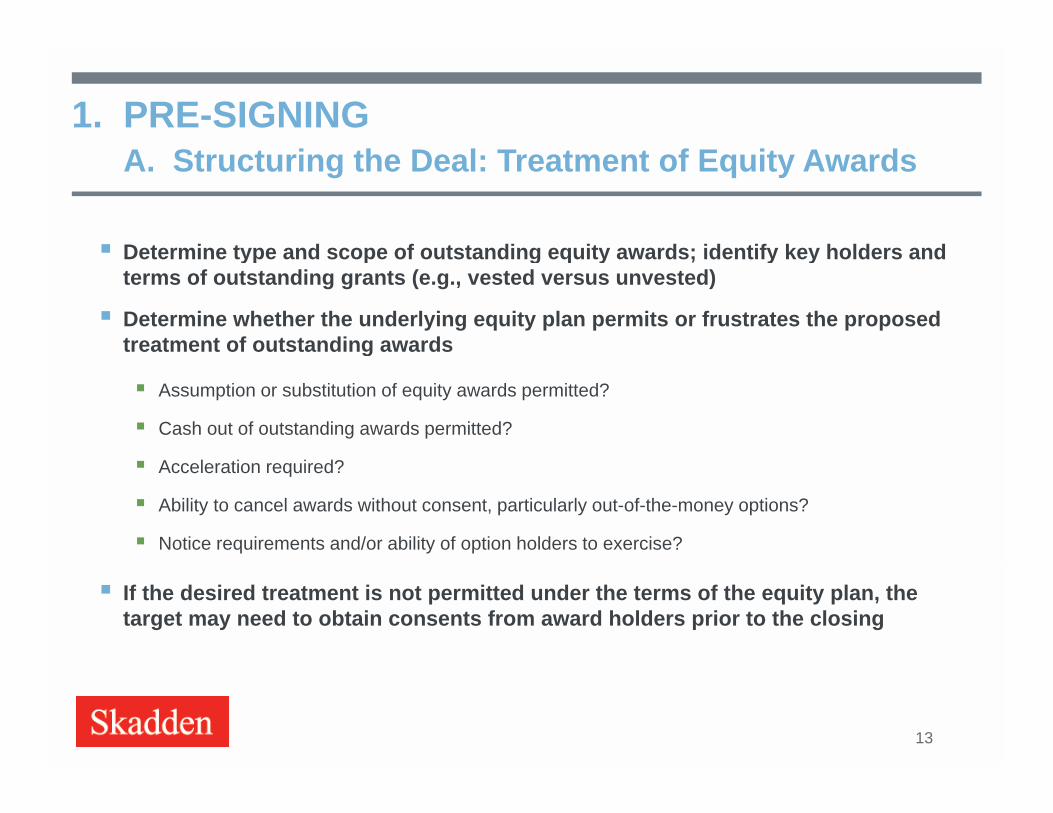

Determine type and scope of outstanding equity awards; identify key holders and

A. Structuring the Deal: Treatment of Equity Awards

Determine type and scope of outstanding equity awards; identify key holders and terms of outstanding grants (e.g., vested versus unvested)

Determine whether the underlying equity plan permits or frustrates the proposed treatment of outstanding awardsg

Assumption or substitution of equity awards permitted?

Cash out of outstanding awards permitted?

Acceleration required?

Ability to cancel awards without consent, particularly out-of-the-money options?

Notice requirements and/or ability of option holders to exercise?

If the desired treatment is not permitted under the terms of the equity plan, the target may need to obtain consents from award holders prior to the closing

13

1. PRE-SIGNINGA St t i th D l T t t f E it A d

Determine whether treatment of equity awards should vary by type of equity award

A. Structuring the Deal: Treatment of Equity Awards

Determine whether treatment of equity awards should vary by type of equity award, holder or based on vested status or exercise price (compared to per share price applicable in the transaction)

Should options, SARs, restricted stock and RSUs be treated differently (e.g., one or more types of the target’s outstanding equity awards may be inconsistent with acquiror’s employee equity program)?

Should employee-held equity awards be treated differently from awards held by non-employee p y q y y y p ydirectors/consultants?

Should certain key employee equity awards be treated differently than equity awards held by employees generally? Does the plan allow for such disparate treatment?

Should vested and unvested stock options be treated differently?

If permitted by the terms of the applicable target plan, should in-the-money stock options be treated differently from out-of-the-money options?

14

1. PRE-SIGNINGA St t i th D l E it /409A C id ti

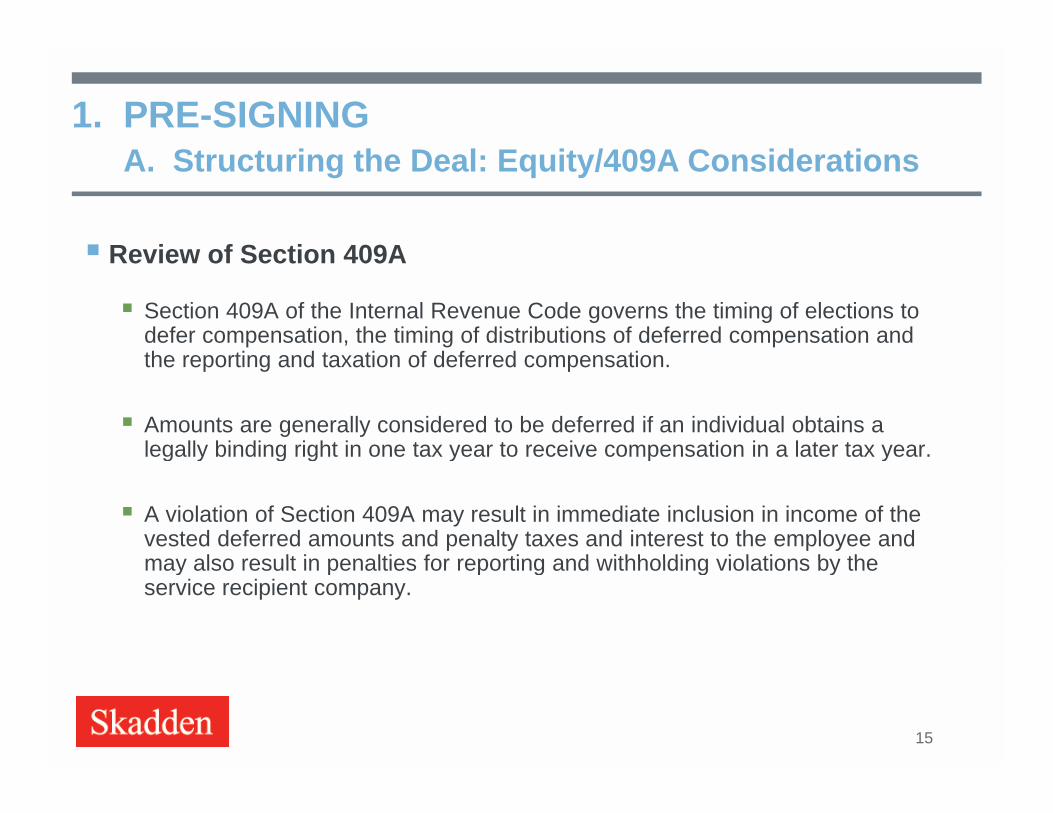

Review of Section 409A

A. Structuring the Deal: Equity/409A Considerations

Review of Section 409A

Section 409A of the Internal Revenue Code governs the timing of elections to defer compensation, the timing of distributions of deferred compensation and the reporting and taxation of deferred compensationthe reporting and taxation of deferred compensation.

Amounts are generally considered to be deferred if an individual obtains a legally binding right in one tax year to receive compensation in a later tax year. g y g g y p y

A violation of Section 409A may result in immediate inclusion in income of the vested deferred amounts and penalty taxes and interest to the employee and may also result in penalties for reporting and withholding violations by themay also result in penalties for reporting and withholding violations by the service recipient company.

15

1. PRE-SIGNINGA St t i th D l E it /409A C id ti

Cash out of options and SARs generally do not violate Section 409A

A. Structuring the Deal: Equity/409A Considerations

Canceling stock options and SARs in exchange for an immediate cash payment that is equal to the excess of the per share transaction price over the applicable exercise price should not violate Section 409A

Earnouts and escrows should be structured to comply with Section 409A

Section 409A provides an exemption for “earnout” payments or payments otherwise held back from payment upon closing, so long as the earn-out is paid on the same schedule and on the same terms and conditions as payments are made to target shareholders generally and thesame terms and conditions as payments are made to target shareholders generally and the amount is paid out fully within five years after the change of control

Practitioners take view that cashing out out-of-the-money stock options for a specified price is also permitted under the rules of Section 409A

Cashing out unvested options and paying proceeds out over time (e.g., in accordance with the original vesting schedule) raises issues under Section 409A. Converting options into restricted stock units likewise raises issues under Section 409A

16

1. PRE-SIGNINGA St t i th D l E it /T /409A C id ti

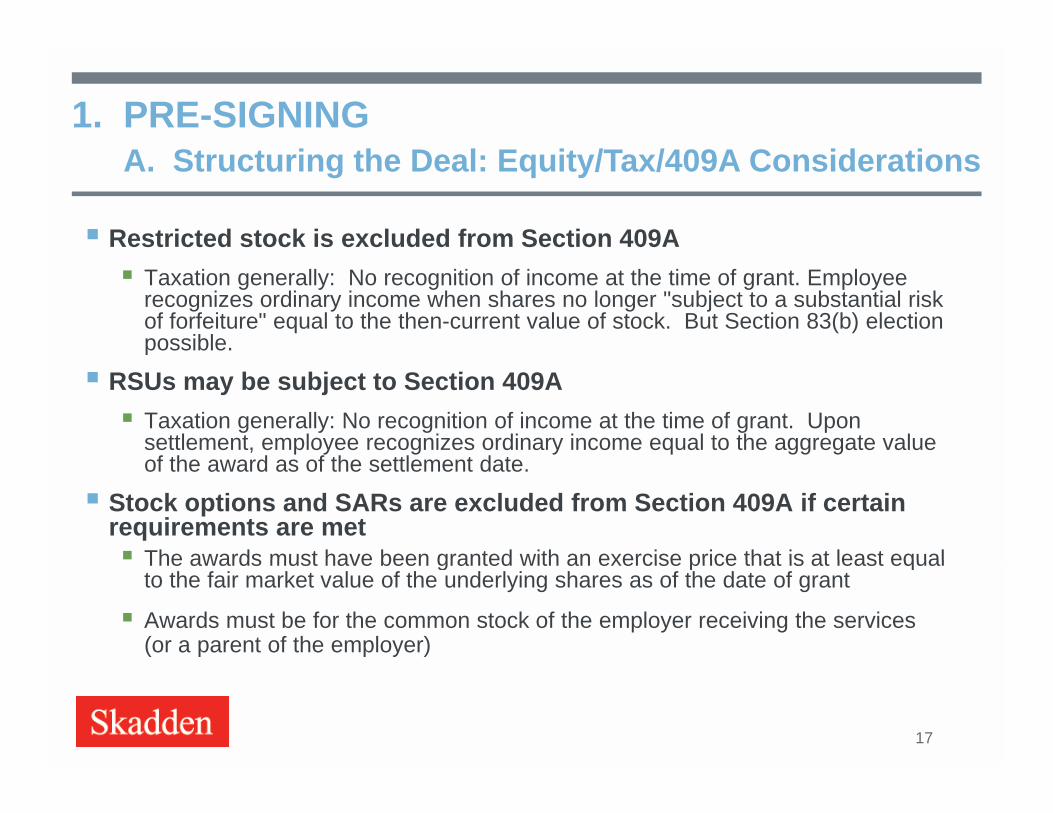

Restricted stock is excluded from Section 409A

A. Structuring the Deal: Equity/Tax/409A Considerations

Taxation generally: No recognition of income at the time of grant. Employee recognizes ordinary income when shares no longer "subject to a substantial risk of forfeiture" equal to the then-current value of stock. But Section 83(b) election possible.

RSUs may be subject to Section 409A Taxation generally: No recognition of income at the time of grant. Upon

settlement, employee recognizes ordinary income equal to the aggregate value f th d f th ttl t d tof the award as of the settlement date.

Stock options and SARs are excluded from Section 409A if certain requirements are met The awards must have been granted with an exercise price that is at least equalThe awards must have been granted with an exercise price that is at least equal

to the fair market value of the underlying shares as of the date of grant

Awards must be for the common stock of the employer receiving the services (or a parent of the employer)

17

1. PRE-SIGNINGA St t i th D l E it /T /409A C id ti

Taxation of non-qualified stock options and SARsN iti f i t th ti f t ti

A. Structuring the Deal: Equity/Tax/409A Considerations

No recognition of income at the time of grant or vesting. Upon exercise, employee recognizes ordinary income equal to the excess of the

fair market value of the shares received over the exercise price (or in the case of SARs, the excess of the fair market value of the shares at the time of grant over the fair market value at the time of exercise).

Taxation of incentive stock options (ISOs) No recognition of income at the time of grant vesting or exerciseNo recognition of income at the time of grant, vesting or exercise. If shares acquired upon exercise are held for at least two years from the date of

grant and at least one year from the date of exercise, employee recognizes capital gain or loss upon a subsequent sale of the shares.If h di d f i t i ti f ith h i d ( "di lif i If shares disposed of prior to expiration of either such period (a "disqualifying disposition"), employee recognizes ordinary income at the time of such disposition equal to the excess of (A) the lesser of (i) the fair market value of the shares of stock acquired on the date of exercise or (ii) the amount realized upon the disposition over (B) the exercise pricedisposition over (B) the exercise price.

18

1. PRE-SIGNINGA St t i th D l ISO

Incentive stock options

A. Structuring the Deal: ISOs

p

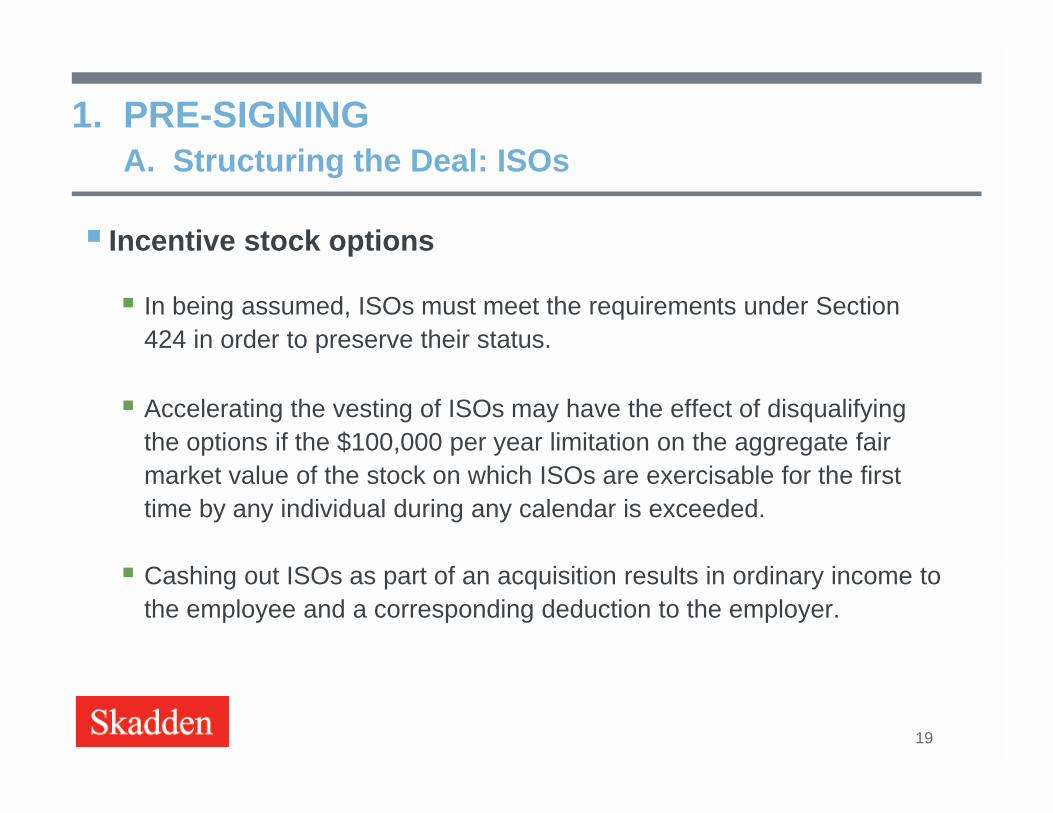

In being assumed, ISOs must meet the requirements under Section 424 in order to preserve their status.

Accelerating the vesting of ISOs may have the effect of disqualifying the options if the $100,000 per year limitation on the aggregate fair market value of the stock on which ISOs are exercisable for the first time by any individual during any calendar is exceeded.

Cashing out ISOs as part of an acquisition results in ordinary income to the employee and a corresponding deduction to the employer.

19

1. PRE-SIGNINGA. Structuring the Deal: Option Assumption

Assumption of options and SARs must be structured to preserve the aggregate spread in order to comply with Section 409A

Assumed awards are usually not exchanged on a 1:1 basis in shares of the Assumed awards are usually not exchanged on a 1:1 basis in shares of the acquiror; rather, an exchange ratio is used to adjust the awards.

Options and SARs may generally be exchanged and adjusted forOptions and SARs may generally be exchanged and adjusted for equivalent rights in a transaction and will not violate Section 409A so long as the aggregate spread on the options or SARs is preserved.

Exchanging options or SARs for another form of compensation or the use of escrows and earnouts requires additional analysis and considerations.

20

1. PRE-SIGNINGS O

“Rollover” of options/SARs

A. Structuring the Deal: Option Assumption

Consider both ISO and 409A rules, which are very similar Options may be “in the money” immediately after closing and exempt from

Section 409A and comply with the ISO rules if the rollover would comply with Section 424 (i.e., no increase in the aggregate value of the spread or the per share ratio of exercise price to share price) Transaction must be a “corporate transaction” (as defined in Reg. § 1.424-

1(a)(3))1(a)(3)) A corporate merger, consolidation, acquisition of property or stock, separation,

reorganization or liquidation A distribution (excluding ordinary dividends) or change in terms in number of ( g y ) g

outstanding shares Conversion is permitted in a spin-off but not a carve-out IPO

21

1. PRE-SIGNINGA St t i th D l O ti A ti

The Section 409A exchange ratio test is similar to the ISO rules but

A. Structuring the Deal: Option Assumption

The Section 409A exchange ratio test is similar to the ISO rules but more permissive

The Section 409A test is satisfied if the ratio of the exercise price to the fair market value of a share subject to the option immediately after thefair market value of a share subject to the option immediately after the assumption or substitution is not greater than the ratio of the exercise price to the fair market value of a share subject to the option immediately before the assumption or substitution Like the ISO rules, the Section 409A rules require that the aggregate

spread value not be increased But Section 409A allows an acquiror to “de-leverage” the equity position of

employees by lowering the ratio of exercise price to stock value and thusemployees by lowering the ratio of exercise price to stock value and thus rollover with respect to fewer shares This may be helpful to address limitations under the NYSE or NASDAQ

20% shareholder approval rule

22

1. PRE-SIGNINGA St t i th D l E /E t

Escrows and earn-outs may raise special concerns as to the value

A. Structuring the Deal: Escrows/Earnouts

Escrows and earn-outs may raise special concerns as to the value on which the rollover occurs

Example: Target is being acquired for $10 per share in cash 20% of the purchase price is being placed in an escrow as security for

Acquiror’s claims for any breaches of target representations and q y g pwarranties Acquiror’s stock is trading at $20 per share Acquiror is assuming outstanding target options and substituting Acquiror is assuming outstanding target options and substituting

Acquiror’s stock for target stock

23

1. PRE-SIGNINGS /A. Structuring the Deal: Escrows/Earnouts

To comply with Reg. § 1.409A-1(b)(5)(v)(D), the option exchange ratio must not increase the aggregate spread in the option being assumed

For purposes of applying this test should target stock be valued at: For purposes of applying this test, should target stock be valued at: $10 per share?

$8 per share?

Somewhere in between?

24

1. PRE-SIGNING

There are at least 3 schools of thought on how to answer this question:

A. Structuring the Deal: Escrows/Earnouts

The traditionalist school – we never had to worry about escrows for ISO purposes under Section 424(a), why start now? -- use $10 per share

The worrywart school – Section 409A is a whole new ballgame so better safe than sorry –use $8 per share This could be coupled with a cash payment and/or reload option when and if the escrow is

paid But…reload options must have a fair market exercise price when granted

The pragmatist school – it is a question of fact not law – get an appraisalThe pragmatist school it is a question of fact not law get an appraisal Appraisal would not necessarily be a typical valuation exercise; rather it would involve risk

analysis as to likelihood of indemnities being triggered

This should be an issue only with private target companies In addition, remember that any payments from the escrow/earn-out payments

made to former holders of options, restricted stock, RSUs, SARs, etc. will be taxed as ordinary income (and not as capital gain) upon receipt and will also be subject to withholding taxeswithholding taxes

25

1. PRE-SIGNINGA. Structuring the Deal: Equity/Section 409A Considerations

RSUs and Section 409A RSUs are subject to Section 409A unless there is an applicable exemption

(e.g., short-term deferral where the RSUs are settled at, or within a limited ( g , ,period following, vesting)

Typically, where unvested RSUs are being assumed pursuant to the same vesting terms or cashed out in a transaction, such treatment does notvesting terms or cashed out in a transaction, such treatment does not violate Section 409A However, additional analysis is required if the target’s RSUs are subject to

Section 409A and the target’s equity plan permits the exercise of discretion over the treatment of RSUs

26

1. PRE-SIGNING

Cash-out of Options

A. Structuring the Deal: Who gets the deduction?

Generally Section 83 and 162 rules govern timing of deduction of cash-out of options except for ISOs

Under these rules, deduction would be taken by target at closing, y g g

But Next-Day Rule: Reg. § 1.1502-76(b)(i)(ii) may move deduction to acquiror return

Spin off Spin-off Revenue Ruling 2002-1

In spin-off context, deduction “relates back” to when the compensation plan entered into Who was employer at grant?

27

1. PRE-SIGNING

If t t t th d d ti it ll b d t ff t th

A. Structuring the Deal: Who gets the deduction?

If target gets the deduction, it can generally be used to offset the current year's income, then carried back 2 years, and any balance can be used to offset future income (subject to Section 382 and other limitations) Can the parties agree in the acquisition agreement whether target or

acquiror will claim the deductions?

Can the parties allocate the tax benefits from the deductions between target and acquiror (i.e., the deductions create a net operating loss (NOL) carry forward and acquiror must pay the target shareholders all or a portion of theforward and acquiror must pay the target shareholders all or a portion of the tax refund attributable to the use of the NOL when received)

28

B. Conducting Diligence

29

1. PRE-SIGNINGB. Conducting Diligence

General Transaction Principles and Section 409A

Section 457A

Types of Employee Arrangements

Change in Control and Employment Agreements; Severance Plans Equity Compensation Plans Cash Incentive Plans Nonqualified Deferred Compensation Plans Retirement Health and Welfare and Retiree Medical Plans Retirement, Health and Welfare, and Retiree Medical Plans

Considerations Under Section 280G

30

1. PRE-SIGNINGC

General Transaction Principles and Section 409A

B. Conducting Diligence

p In a stock purchase/merger transaction, an acquiror generally assumes (directly or

indirectly through the surviving entity) employee plans and agreements automatically by operation of law. Generally, plans are not assumed in an asset purchase transaction but it is not uncommon for certain specified employment agreements to betransaction but it is not uncommon for certain specified employment agreements to be assumed by the acquiror or for assets and liabilities relating to transferred employees under certain plans to be assumed.

Benefits may become payable accelerate or become enhanced by reason of anBenefits may become payable, accelerate or become enhanced by reason of an acquisition. Single Trigger: a payment that is triggered upon only the occurrence of a change in control Double Trigger: a payment that is triggered by a change in control and a subsequent qualifying

t i ti f l t h t i ti b th ith t C btermination of employment, such as a termination by the company without Cause or by an individual for Good Reason

Has the target violated Section 409A?

31

1. PRE-SIGNINGB. Conducting Diligence

General Transaction Principles and Section 409A (cont’d)

The Section 409A definition of change in control must be used where:g

A change in control is a payment trigger for deferred compensation, or

A change in control is used to toggle a different form of payment (e.g., lump sum v. installments) upon a “separation from service” within a specified amount of time following a change in control

32

1. PRE-SIGNING

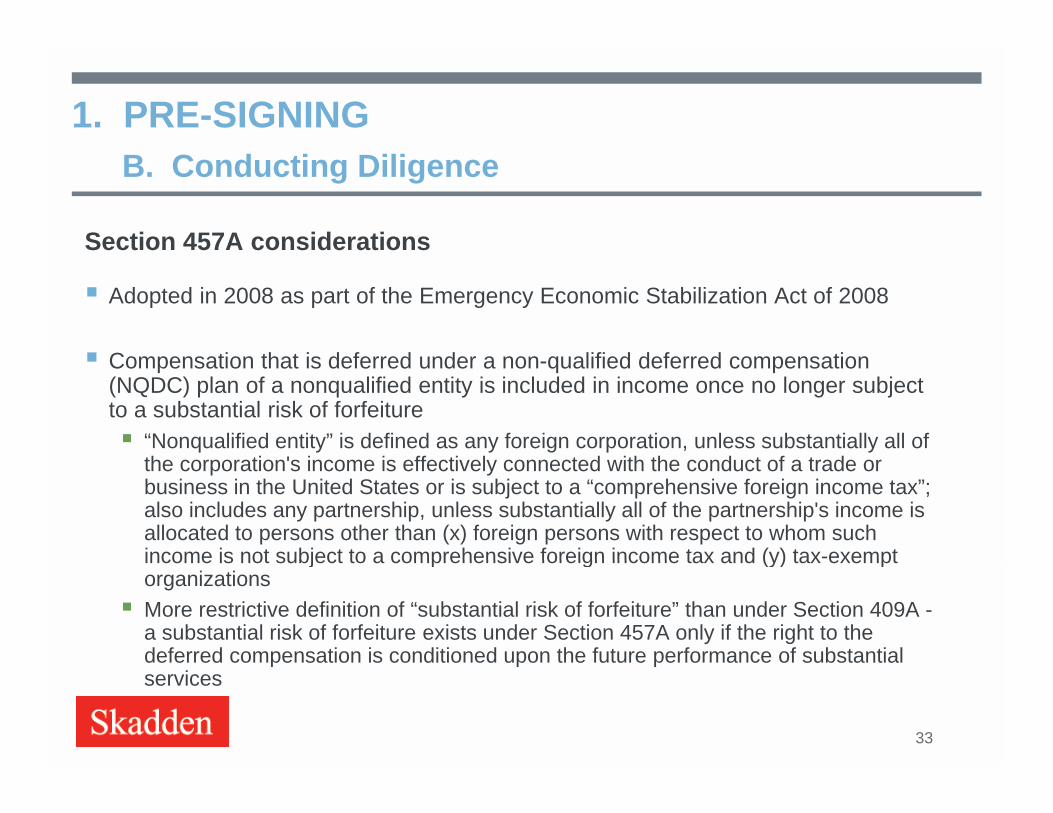

Section 457A considerations

B. Conducting Diligence

Adopted in 2008 as part of the Emergency Economic Stabilization Act of 2008

C ti th t i d f d d lifi d d f d ti Compensation that is deferred under a non-qualified deferred compensation (NQDC) plan of a nonqualified entity is included in income once no longer subject to a substantial risk of forfeiture “Nonqualified entity” is defined as any foreign corporation, unless substantially all of

th ti ' i i ff ti l t d ith th d t f t dthe corporation's income is effectively connected with the conduct of a trade or business in the United States or is subject to a “comprehensive foreign income tax”; also includes any partnership, unless substantially all of the partnership's income is allocated to persons other than (x) foreign persons with respect to whom such income is not subject to a comprehensive foreign income tax and (y) tax-exemptincome is not subject to a comprehensive foreign income tax and (y) tax exempt organizations More restrictive definition of “substantial risk of forfeiture” than under Section 409A -

a substantial risk of forfeiture exists under Section 457A only if the right to the deferred compensation is conditioned upon the future performance of substantial p p pservices

33

1. PRE-SIGNINGB. Conducting Diligence

Section 457A considerations (cont’d)

For purposes of Section 457A, NQDC generally has the same meaning as under Section 409A, but also includes any arrangement under which compensation is based on the , y g pincrease in value of a specified number of equity units of the service recipient, including cash-settled SARs, regardless of the exercise price of the SARs, but excluding stock options or share-settled SARs, so long as those awards are issued at no less than fair market value with no other deferral featuremarket value with no other deferral feature

Short-term deferral exception is available if compensation is paid by the end of the taxable year following the taxable year in which it is no longer subject to a substantialtaxable year following the taxable year in which it is no longer subject to a substantial risk of forfeiture (as defined under Section 457A)

34

1. PRE-SIGNING

Types of Employee Arrangements:

B. Conducting Diligence

yp p y g

Change in Control (“CIC”) and Employment Agreements; Severance Plans

D i if (i l di i b ) ill b i d Determine if any payments (including any transaction bonuses) will be triggered on a change in control (single trigger)

Determine the severance protections to be triggered on a change in control andsubsequent termination and the timeframe of such protectionssubsequent termination and the timeframe of such protections

Determine whether the change in control triggers a walk away right or otherwise gives significant flexibility under a Good Reason definition

A Good Reason definition that gives the individual too much flexibility to determine the timing of triggering severance may subject the agreement to Section 409A

Examine any restrictive covenants

35

1. PRE-SIGNING

Types of Employee Arrangements (cont.):

B. Conducting Diligence

Equity Compensation Plans Determine whether the plans require or permit accelerated vesting of unvested equity or

accelerate the payment of equity awards in a change in control D t i if it d bj t t S ti 409A Determine if any equity awards are subject to Section 409A As previously discussed, determine whether the plans permit assumption or cash out, and

whether consent of the individual equity award holders will be required As previously discussed, the assumption of equity awards must be structured to comply

with plan terms, Section 409A and ISO rules, if applicable

Cash Bonus Plans Transaction bonus, annual cash incentive and commission-based plans Review bonus/incentive plans for purposes of determining whether, based on transaction

structure, such plans will remain in place after the transaction or will need to be modified or replaced

Determine whether the plans provide for accelerated vesting or payment of awards, in whole or in part, in connection with a change in control

36

1. PRE-SIGNING

Types of Employee Arrangements (cont.):

B. Conducting Diligence

Nonqualified Deferred Compensation Plans Include supplemental retirement plans or excess benefit plans

Determine whether the plans provide for accelerated vesting or distribution in Determine whether the plans provide for accelerated vesting or distribution in connection with a change in control If the plans provide that amounts will be paid upon a change in control, the definition

must comply with Section 409A

Determine whether there has been a trust established in connection with the plan and whether a change in control triggers the funding of these benefits

Section 409A permits the distribution of amounts under a plan in connection with the termination of the plan within the 30 days preceding or the 12 monthswith the termination of the plan within the 30 days preceding or the 12 months following a change in control, but only if all arrangements of the same plan aggregation type are terminated with respect to all participants who experienced a change in control, and distributions are made within 12 months of such terminationof such termination.

37

1. PRE-SIGNING

Types of Employee Arrangements (cont.):

B. Conducting Diligence

Types of Employee Arrangements (cont.):

Retirement, Health and Welfare, and Retiree Medical Plans

Determine the type of retirement plans in place at target (i.e., defined contribution or d fi d b fit) d th t ll l t d t ti h b id d ith t tdefined benefit) and that all relevant documentation has been provided with respect to each

Determine whether there are any potential liabilities associated with the retirement plans, such as underfunding of a pension plan or withdrawal liabilities in connection with a multiemployer plan

Determine the health and welfare plans that are maintained by the target and confirm compliance with applicable laws (e.g., the Patient Protection and Affordable Care Act)

Determine whether the target self-insures its medical coverage and associated liabilities Determine whether the target self-insures its medical coverage and associated liabilities, as well as whether it maintains stop loss coverage

Determine whether the target provides retiree medical benefits or has ongoing life insurance obligations to individuals

38

1. PRE-SIGNINGC 280G

C id ti d S ti 280G

B. Conducting Diligence: 280G

Considerations under Section 280G

Applies to payments made to “disqualified individuals” that are contingent on a change in ownership or control of a corporation, a change in the effective

t l f ti h i th hi f b t ti l ticontrol of a corporation or a change in the ownership of a substantial portion (generally 1/3) of a corporation’s assets. Note that these rules generally don’t apply to partnerships and LLCs

Any payment made pursuant to an agreement entered into within one year before a change in control is presumed to be contingent on that change in control, i.e., parachute payments.

“Disqualified individuals” include officers, certain shareholders or a group of highly-compensated individuals determined pursuant to a formula.

39

1. PRE-SIGNINGB. Conducting Diligence: 280G

Calculating excess parachute payments as a function of base compensation

An excess parachute payment is the amount by which the parachute payments exceed the average taxable compensation received by an executive from the company during the g p y p y g5 preceding years, which is the individual’s base compensation

Lost tax deduction to corporation and excise tax on individual (subject to required withholding by corporation) in the event excess parachute paymentsrequired withholding by corporation) in the event excess parachute payments equal or exceed three times base compensation

If the parachute payments equal or exceed 3x the individual’s base compensation, Section 280G provides that no deduction is allowed to a corporation for excess parachuteSection 280G provides that no deduction is allowed to a corporation for excess parachute payments (i.e., everything in excess of 1x base compensation) and Section 4999 imposes an excise tax on the recipient of any excess parachute payments, equal to 20% of such amount

40

1. PRE-SIGNING

E l i l d f h f ll i f

B. Conducting Diligence: 280G

Employment arrangements may include one of the following types of provisions relating to Section 280G:

Haircut provision: payments must be reduced to a level that would not trigger p p y ggthe excise tax

Better-of provision: payments are cut back to a level that would not trigger the excise tax unless the individual would be in a better economic position (on an after-tax basis) in receiving all amounts and simply paying the excise tax

G i i dditi l t t th i di id l t k th Gross-up provision: an additional payment to the individual to make the individual whole for any excise tax triggered by excess parachute payments

41

1. PRE-SIGNING

E l f h t t

B. Conducting Diligence: 280G

Examples of parachute payments:

Severance payments and the value of health benefits to be paid or provided under an employment, change in control or severance arrangementunder an employment, change in control or severance arrangement

Transaction bonuses or accelerated annual bonuses

Value of accelerating the vesting of equity awards or the cash out of unvested awards

Additional benefits under nonqualified deferred compensation plans

42

1. PRE-SIGNINGB C d ti Dili 280G

Examples of payments that are generally exempt from being

B. Conducting Diligence: 280G

Examples of payments that are generally exempt from being parachute payments:

Payments that are not in the nature of compensation (e.g., payments in respect of vested shares held by the individual)of vested shares held by the individual)

Payments to be paid with respect to stock options already vested at the time of the change in control Any portion of a parachute payment that is attributable to the performance ofAny portion of a parachute payment that is attributable to the performance of

services before the change in control

Reasonable compensation for personal services to be rendered after the change in control or payments made pursuant to an agreement entered into g p y p gafter the change in control (as compared to pre-change in control compensation for services)

43

1. PRE-SIGNINGB C d ti Dili 280G

Private company shareholder approval exemption – a change in control-

B. Conducting Diligence: 280G

Private company shareholder approval exemption a change in controlrelated payment will not be a parachute payment if shareholder approval of the payment is obtained in accordance with the rules

Sh h ld b ti h t i bj t t th t t t Shares held by executives whose payment is subject to the vote may not vote their shares 75% of the shares entitled to vote (on a date within six months before the

change in control) must approve the paymentg ) y Adequate disclosure of all material facts concerning all parachute payments

must be made to all shareholders (include individual quantification) The vote must determine the right of the individual to receive or retain the

t ( t t )payment (no agreement to pay anyway) The vote must be separate from the shareholder vote to approve the

transaction

44

1. PRE-SIGNINGB C d ti Dili 280G A h

Common technique

B. Conducting Diligence: 280G Approaches

q Employees waive their rights under existing agreement and enter into new

agreements, which are effective only if shareholder approval is obtained

Can target arrangements be converted into “reasonableCan target arrangements be converted into reasonable compensation”?

Allocation to non-compete

Reasonable compensation conversion and non-compete allocation approaches became more challenging post-2003 Final 280G regulations 8/4/03 Square D case (Tax Court 2003) – discredited Pearl Meyer testimony

relating to characterization of executives’ compensation

Section 409A challenges?

45

C. Negotiating the Transaction Document

46

1. PRE-SIGNINGC N ti ti th T ti D t

Compensation and benefits provisions include:

C. Negotiating the Transaction Document

Compensation and benefits provisions include:

Mechanics surrounding the treatment of outstanding equity awards

Representations and Warranties Representations and Warranties Copies of all employee benefit plans have been provided

Employee benefit plans are and have been operated in compliance with their terms, ERISA the Internal Revenue Code and other applicable lawsERISA, the Internal Revenue Code and other applicable laws

No claims or suits against any employee benefit plan

No plans provide for any payments or for the acceleration of vesting/payment, trigger golden parach te e cise ta es or are req ired to be f nded on acco nt of the dealgolden parachute excise taxes or are required to be funded, on account of the deal or in tandem with another event

Foreign benefit plan representations and compliance

47

1. PRE-SIGNING

Compensation and benefits provisions include (cont’d):

C. Negotiating the Transaction Document

Interim Operating Covenants Without the consent of the acquiror, target may not increase compensation or benefits,

grant bonuses, severance pay or equity awards, establish/amend/terminate benefit plans, etc.etc.

Post-Closing Covenants Common covenants include that acquiror agrees to: maintain comparable compensation

and benefits for a specified period, provide service credit to target employees and maintain severance arrangements for a specified period, etc. Consider whether any carve-outs from comparable benefits continuation are warranted (e.g.,

equity compensation, defined benefit pension benefits)

Di l S h d l Disclosure Schedules Review and update seller’s exceptions and qualifications to the terms of the transaction

document. Careful attention is warranted.

48

D. Considering Retention/Employment Arrangements

49

1. PRE-SIGNINGD C id i R t ti /E l t A t

Identify key employees critical to retain and the length of retention period

D. Considering Retention/Employment Arrangements

y y p y g pneeded for each Review adequacy of, and issues with, existing employment and retention

arrangements Unique treatment of key employee equity awards Determine whether to negotiate new retention awards or offer letters with key

employees, including modifications to existing arrangements (and the timing for such arrangements)

Section 409A issues with modifications/conversion into new arrangements

Determine whether any employees should be terminated in connection with the Determine whether any employees should be terminated in connection with the closing and the terms of any termination arrangement

* Identification of key employees and effective communication to affected employees is critical

50

1. PRE-SIGNING

Section 409A may limit the ability convert severance arrangements into

D. Considering Retention/Employment Arrangements

Section 409A may limit the ability convert severance arrangements into new consulting, retention or non-competition arrangements

Conversion was way of converting the imminently payable compensation (b f h i t l ti ) i t ti th t i(because of change in control or separation) into compensation that is subject to a substantial risk of forfeiture Section 409A does not recognize non-compete payments as being subject

to a substantial risk of forfeitureto a substantial risk of forfeiture

Substitution rules – Any amount, or entitlement to any amount that acts as a substitute for, or replacement of, NQDC amount constitutes a , p ,payment of NQDC under Section 409A

51

1. PRE-SIGNING

Th till b t d thi

D. Considering Retention/Employment Arrangements

There still may be ways to do this Severance agreements which fit into the short-term deferral exemption

under Section 409A can be convertedb t b f t ith l G d R d fi iti … but beware of agreements with loose Good Reason definitions

However, payments that vest on a change in control may be modified , p y g yto extend vesting beyond the change in control, if the extended vesting condition would constitute a substantial risk of forfeiture

Asset sales may permit distribution as separation from service

52

1. PRE-SIGNING

If Company has Section 409A subject deferred compensation, can you pay out

D. Considering Retention/Employment Arrangements

at the CIC if not provided for in the document?

Section 409A permits the termination of an NQDC plan within the 30 days preceding or the 12 months following a change in control event but only if all g g g yaggregated plans, agreements, etc. sponsored by the company immediately after the change in control event that apply to each participant experiencing the change in control event are terminated Action to be taken by the service recipient that is primarily liable immediately after

the transaction for the payment of the NQDC

Balances must be paid under all aggregated plans within 12 months of the date the i i i t t k th ti t t i t th lservice recipient takes the action to terminate the plan

For aggregation, these types of plans are generally “account balance” or “non-account balance” plans for purposes of Section 409A

53

2. POST-SIGNING/PRE-CLOSING

54

2. POST-SIGNING/PRE-CLOSING

P St t t I f ti St t t d b S ll f it Proxy Statement or Information Statement prepared by Seller for its shareholders to vote on the proposed deal; relevant provisions: Interest of Certain Persons section

Golden Parachute Compensation disclosure relating to Seller’s named executive officers as part of any disclosure required by Item 401(t) of Regulation S-K under the Securities Exchange Act of 1934.

For private targets, reviewing any Section 280G-related materials prepared by Seller in connection with Seller shareholder vote

Finalizing any employment arrangements to be executed at or prior Finalizing any employment arrangements to be executed at or prior to, but contingent upon, the closing of the transaction

55

2. POST-SIGNING/PRE-CLOSING

NASDAQ and NYSE listing rules may require shareholder g y qapproval in connection with the assumption of equity plans

If an acquiror assumes a target’s plan for purposes of granting future awards under the plan the acquiror may need to obtain approval by itsawards under the plan, the acquiror may need to obtain approval by its shareholders for such assumption.

Such shareholder approval would not generally be required if awards under the assumed plan would not be granted to individuals who were employedthe assumed plan would not be granted to individuals who were employed by the acquiror at the time of transaction.

Looking ahead to necessary regulatory filings Form 3/Form 4 filings Form S-8 filing for assumed equity awards

56

3. CLOSING

57

3. CLOSING

Execution of employment agreements (if not executed pre-closing)

E l it d h d t d Employee equity awards are cashed-out or assumed Employee communications regarding equity award treatment and specific

award conversions

Looking ahead to post-closing matters Employee transition Maintenance or termination or target benefit plans Employee reductions and communications relating to such reductions

58

4. POST-CLOSING

59

4. POST-CLOSING

Ongoing compliance with post-closing covenants in the transaction agreement

Form 3 and Form 4 filings by Section 16 officers of the Seller

Section 16 officers of the Seller to make Form 3 and/or Form 4 filings regarding their changes in beneficial ownership of securities in connection with either an assumption or cash out of equity awards in the transaction.

To be filed within two days after the closing of the transaction

60

4. POST-CLOSING

Form S-8 Requirements in Connection with the Assumption of Equity q p q yAwards Acquiror must register the shares underlying assumed equity awards on Form S-8

(but no registration of shares required for substituted awards)R i t f dit ( ) Requires consent from auditor(s)

Legal and registration fees will be incurred

Timing of filing depends on assumed equity awards (e.g., if only unvested options g g p q y ( g y pare assumed, the Form S-8 must be filed prior to the time that an assumed option is exercised)

Employees of the target could be anxious if required to wait for a Form S-8 to be effective in order to exercise optionsin order to exercise options

Acquiror must distribute to holders of assumed awards a prospectus pursuant to Section 10(a) of the Securities Act of 1933, which summarizes the terms of the applicable plan and certain tax implicationsapplicable plan and certain tax implications.

61

Stuart M Finkelstein

62

Stuart M. FinkelsteinSkadden, Arps, Slate, Meagher & Flom LLPNew York, NY212.735.2841 | [email protected]

Stuart Finkelstein, head of the firm’s New York Tax Group, represents clients on a wide range of tax matters, with particular emphasis on mergers, acquisitions and divestitures, including spin-offs, debt and equity offerings, corporate and partnership restructurings, and joint ventures. He also provides tax guidance regarding executive compensation and tax controversy matterscompensation and tax controversy matters.

Mr. Finkelstein has been involved in a number of significant transactions in the financial services industry. He is regularly consulted on tax matters related to corporate restructurings and also counsels clients on matters relating to financially troubled businesses, both in and out of bankruptcy proceedings. Mr. Finkelstein also has advised clients in the telecommunications industry and has represented various private equity funds in a variety of transactions.

Mr. Finkelstein repeatedly has been named among the nation’s top tax practitioners by Chambers USA: America’s Leading Lawyers for Business, Legal 500, Tax Directors Handbook, Who’s Who in American Law, g y , g , , ,Who’s Who in America, Who’s Who in the East and Turnarounds and Workouts’ list of Top Bankruptcy Tax Specialists in the Nation’s Major Law Firms. He has spoken around the country and published several articles on various corporate tax planning matters.

Regina Olshan

63

Regina OlshanSkadden, Arps, Slate, Meagher & Flom LLPNew York, NY212.735.3963 | [email protected]

Regina Olshan is the global head of Skadden’s Executive Compensation and Benefits Group. Her practice focuses on advising companies, executives and boards on navigating the regulatory complexities of executive compensation and benefits. This includes tax laws (including laws governing deferred compensation, golden parachute arrangements and deduction limitation rules) and securities laws (including reporting and disclosure p g ) ( g p grequirements and registration issues).

In addition, Ms. Olshan regularly advises public companies, boards, private equity clients and members of management on executive compensation and benefits issues arising in the context of mergers, acquisitions, spin offs initial public offerings restructurings and other extraordinary corporate events including private equityspin-offs, initial public offerings, restructurings and other extraordinary corporate events, including private equity and leveraged buyout transactions. She also regularly advises large public companies and individual senior executives on the adoption, revision, and negotiation of executive employment and severance agreements.

Ms. Olshan is the author and editor of the Section 409A Handbook. She speaks and writes frequently on executive compensation issues and co-chairs “Hot Issues in Executive Compensation,” an annual seminar presented by PLI. She also has been quoted in various major publications on significant executive compensation issues of the day. Ms. Olshan was ranked in Band 1 in Chambers USA: America’s Leading Lawyers for Business for New York employee benefits and executive compensation. She also is listed in The Best Lawyers in America and The Legal 500 U SBest Lawyers in America and The Legal 500 U.S.

U.S. Treasury Department Circular 230 Notice

To ensure compliance with Treasury Department regulations, you are advised that unless otherwise expressly indicated anyyou are advised that, unless otherwise expressly indicated, any federal tax advice contained in this presentation was not intended or written to be used, and cannot be used, for the purpose of avoiding tax related penalties under the Internalpurpose of avoiding tax-related penalties under the Internal Revenue Code or promoting, marketing or recommending to another party any tax-related matters addressed herein.

64