Embed Size (px)

Citation preview

Presented by: Evelyn Parra

December 2010

1

Managing Director, Energy Welfare Training Ltd, Scotland, UKHonorary Associate, Centre for Energy, Petroleum Mineral Law and Policy (CEPMLP) - University of Dundee, Scotland, UK

Energy Welfare Training Ltd - Evelyn Parra 2010 2

Experience sharing and analysis of Government Take for one of the former largest vertically integrated extra-heavy

oil projects of the Orinoco Belt in Venezuela:

Why crude oil is key to Venezuela?

Evolution of Venezuelan oil and gas industry

Types of oil opening contracts

First extra-heavy oil joint ventures

Comparison between general oil and gas taxation versus extra-heavy oil tax regulations

The creation of mixed companies: a new nationalization tool?

EHO Government /Company take statistics

Orinoco belt proven reserves certification activities

2008-2010 extra-heavy oil bidding processes: Carabobo project, results and analysis.

3Energy Welfare Training Ltd - Evelyn Parra 2010

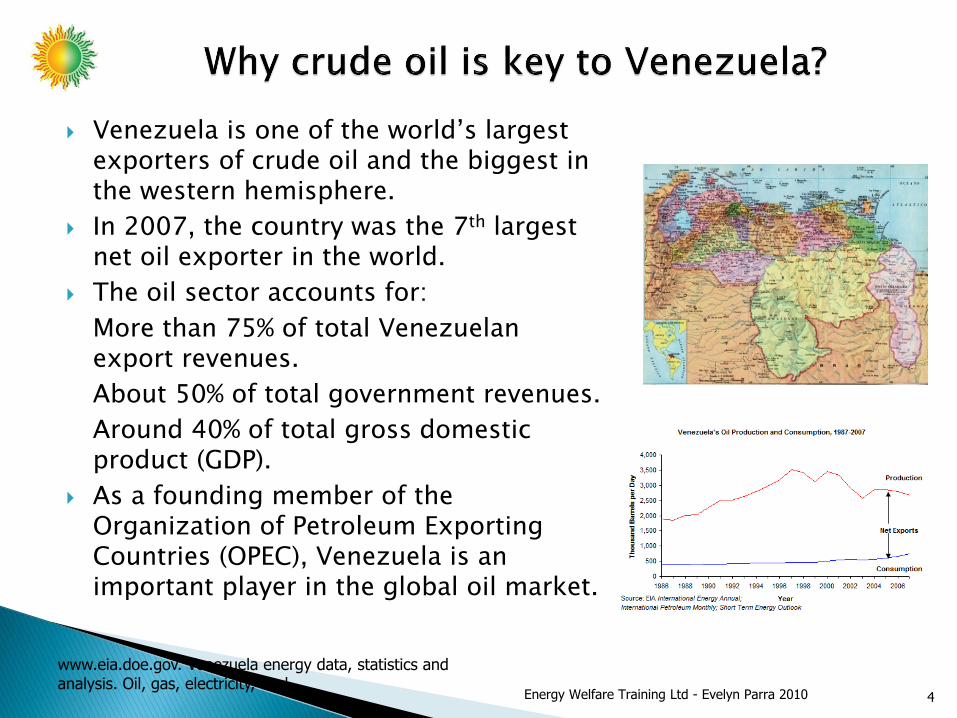

Venezuela is one of the world’s largest exporters of crude oil and the biggest in the western hemisphere.

In 2007, the country was the 7th largest net oil exporter in the world.

The oil sector accounts for:

More than 75% of total Venezuelan export revenues.

About 50% of total government revenues.

Around 40% of total gross domestic product (GDP).

As a founding member of the Organization of Petroleum Exporting Countries (OPEC), Venezuela is an important player in the global oil market.

4

www.eia.doe.gov. Venezuela energy data, statistics and analysis. Oil, gas, electricity, coal.

Energy Welfare Training Ltd - Evelyn Parra 2010

1870 first evidence of crude oil on land

1883 first concession contract

1886 first drilling activities

1899 first government contract dispute with an IOC

1943 first hydrocarbon law

1960 Venezuela promotes the foundation of the OPEC

1971 nationalization of gas activities

1975-1976 nationalization of the oil industry and creation of PDVSA

1990 decade: oil opening to foreign investments

2001 new hydrocarbon law

2002 PDVSA strike and consequent dismiss of 18,000- 20,000 (around 40% payroll).

2004 - 2008 modification of oil opening conditions

2008-2010 new extra-heavy oil bidding processes over the Orinoco belt areas

Sources:

o Montiel Ortega, L. 1984 and 1999. Guia para estudiantes sobre petroleo y gas.

o http://www.pdvsa.com/index.php?tpl=interface.sp/design/readmenuprinc.tpl.html&newsid_temas=88

o http://www.mem.gov.ve/repositorio/imagenes/secciones/pdf_pode/pode_2006/PODE2006.pdf

5Energy Welfare Training Ltd - Evelyn Parra 2010

6

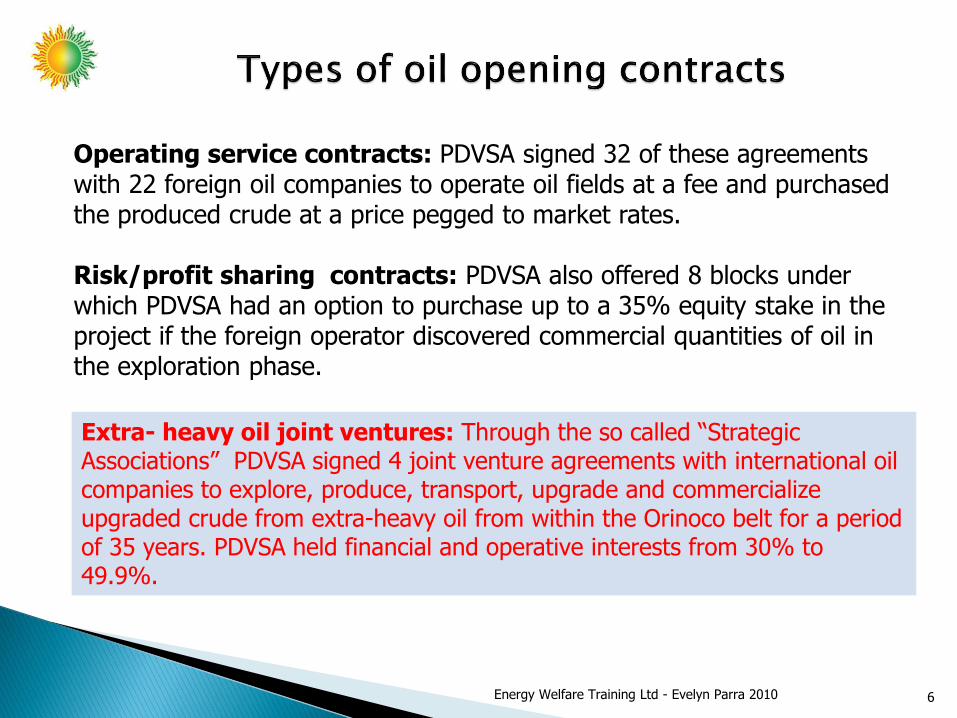

Operating service contracts: PDVSA signed 32 of these agreements with 22 foreign oil companies to operate oil fields at a fee and purchased the produced crude at a price pegged to market rates.

Risk/profit sharing contracts: PDVSA also offered 8 blocks under which PDVSA had an option to purchase up to a 35% equity stake in the project if the foreign operator discovered commercial quantities of oil in the exploration phase.

Extra- heavy oil joint ventures: Through the so called “Strategic Associations” PDVSA signed 4 joint venture agreements with international oil companies to explore, produce, transport, upgrade and commercialize upgraded crude from extra-heavy oil from within the Orinoco belt for a period of 35 years. PDVSA held financial and operative interests from 30% to 49.9%.

Energy Welfare Training Ltd - Evelyn Parra 2010

7Energy Welfare Training Ltd - Evelyn Parra 2010

8

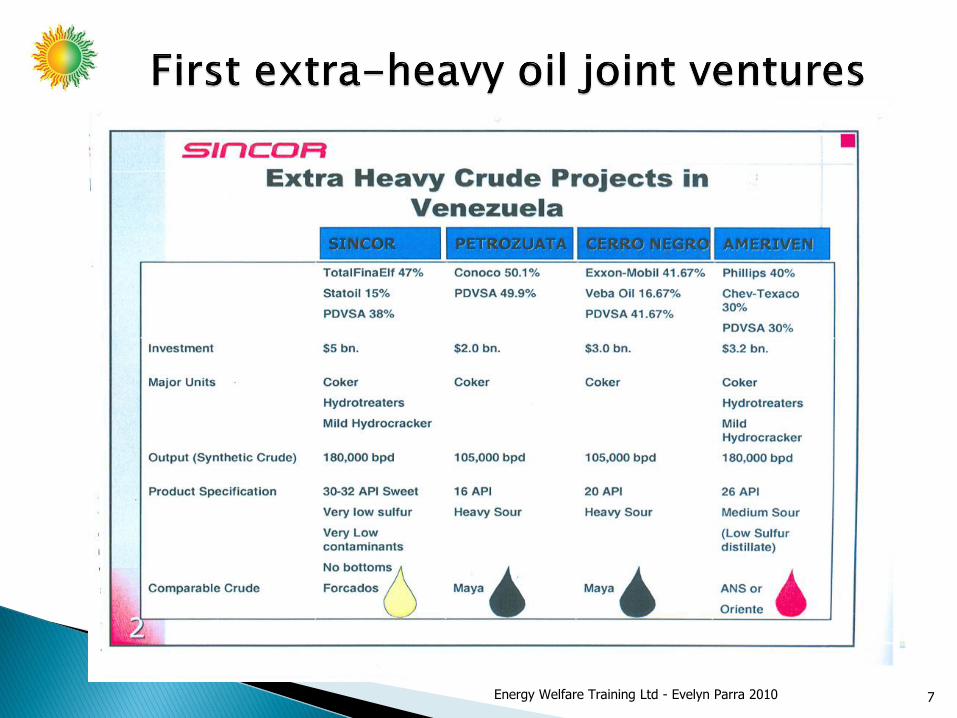

CERRO NEGRO

Energy Welfare Training Ltd - Evelyn Parra 2010

9

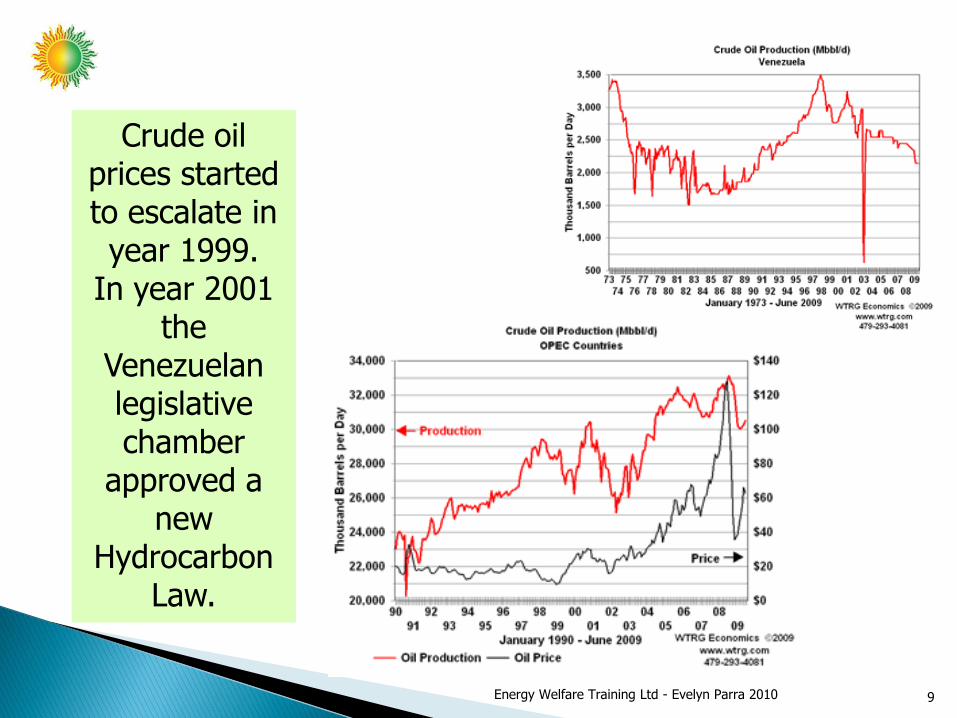

Crude oil prices started to escalate in year 1999.

In year 2001 the

Venezuelan legislative chamber

approved a new

Hydrocarbon Law.

Energy Welfare Training Ltd - Evelyn Parra 2010

In October 2004, the government announced a new oil policy called: Petroleum Full Sovereignty.

Several months later, during a National Assembly’s session held on 25/05/05 the Minister of Energy and Petroleum and President of PDVSA, asked to investigate the oil opening in the understanding that such process harmed the economic conditions of the nation. Being necessary to take proper measures to restore the control of the hydrocarbon industry as per the terms of the 2001 Organic Hydrocarbon Law.

10Energy Welfare Training Ltd - Evelyn Parra 2010

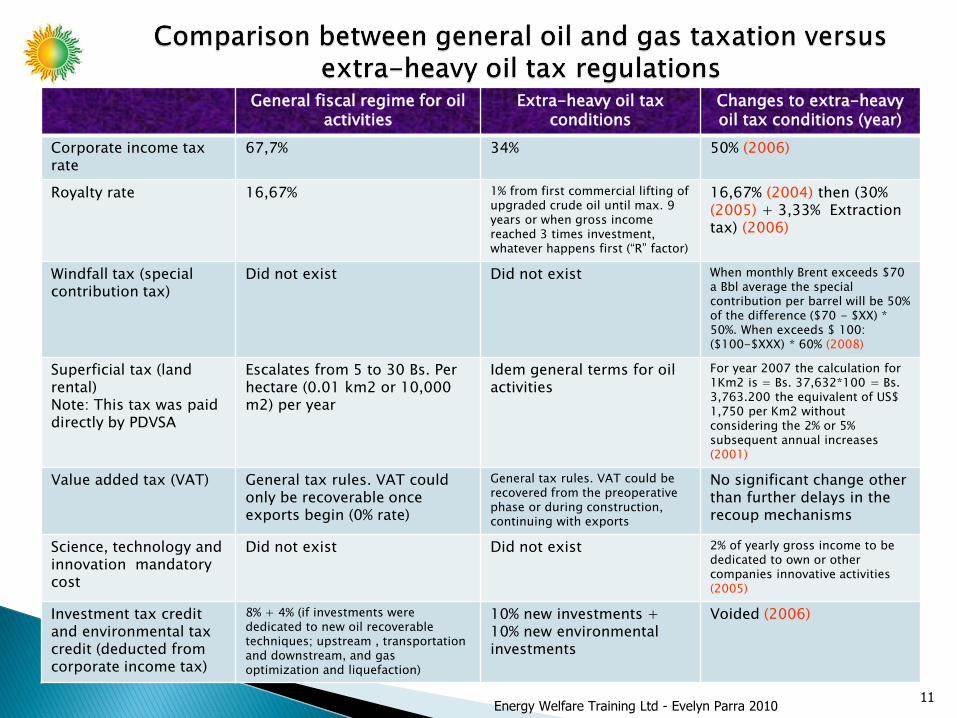

General fiscal regime for oil activities

Extra-heavy oil tax conditions

Changes to extra-heavy oil tax conditions (year)

Corporate income tax rate

67,7% 34% 50% (2006)

Royalty rate 16,67% 1% from first commercial lifting of upgraded crude oil until max. 9 years or when gross income reached 3 times investment, whatever happens first (“R” factor)

16,67% (2004) then (30% (2005) + 3,33% Extraction tax) (2006)

Windfall tax (specialcontribution tax)

Did not exist Did not exist When monthly Brent exceeds $70 a Bbl average the special contribution per barrel will be 50% of the difference ($70 - $XX) * 50%. When exceeds $ 100: ($100-$XXX) * 60% (2008)

Superficial tax (land rental)Note: This tax was paid directly by PDVSA

Escalates from 5 to 30 Bs. Per hectare (0.01 km2 or 10,000 m2) per year

Idem general terms for oil activities

For year 2007 the calculation for 1Km2 is = Bs. 37,632*100 = Bs. 3,763.200 the equivalent of US$ 1,750 per Km2 without considering the 2% or 5% subsequent annual increases (2001)

Value added tax (VAT) General tax rules. VAT could only be recoverable onceexports begin (0% rate)

General tax rules. VAT could be recovered from the preoperative phase or during construction, continuing with exports

No significant change other than further delays in the recoup mechanisms

Science, technology and innovation mandatory cost

Did not exist Did not exist 2% of yearly gross income to be dedicated to own or other companies innovative activities (2005)

Investment tax credit and environmental tax credit (deducted from corporate income tax)

8% + 4% (if investments were dedicated to new oil recoverable techniques; upstream , transportation and downstream, and gas optimization and liquefaction)

10% new investments + 10% new environmental investments

Voided (2006)

11Energy Welfare Training Ltd - Evelyn Parra 2010

12

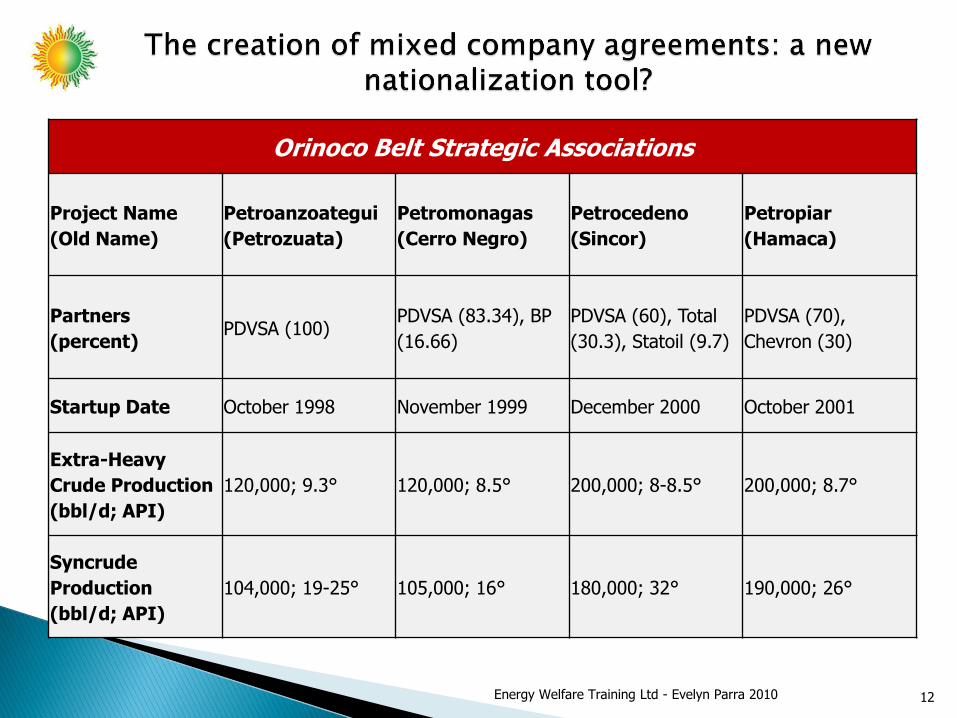

Orinoco Belt Strategic Associations

Project Name

(Old Name)

Petroanzoategui

(Petrozuata)

Petromonagas

(Cerro Negro)

Petrocedeno

(Sincor)

Petropiar

(Hamaca)

Partners

(percent)PDVSA (100)

PDVSA (83.34), BP

(16.66)

PDVSA (60), Total

(30.3), Statoil (9.7)

PDVSA (70),

Chevron (30)

Startup Date October 1998 November 1999 December 2000 October 2001

Extra-Heavy

Crude Production

(bbl/d; API)

120,000; 9.3° 120,000; 8.5° 200,000; 8-8.5° 200,000; 8.7°

Syncrude

Production

(bbl/d; API)

104,000; 19-25° 105,000; 16° 180,000; 32° 190,000; 26°

Energy Welfare Training Ltd - Evelyn Parra 2010

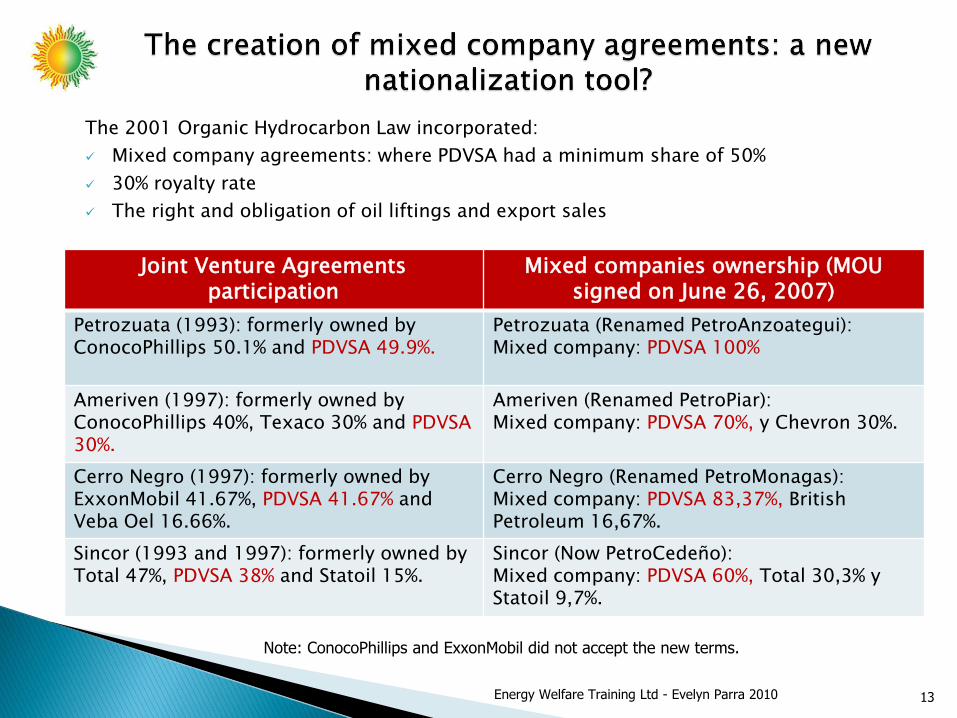

The 2001 Organic Hydrocarbon Law incorporated:

Mixed company agreements: where PDVSA had a minimum share of 50%

30% royalty rate

The right and obligation of oil liftings and export sales

13

Joint Venture Agreements participation

Mixed companies ownership (MOU signed on June 26, 2007)

Petrozuata (1993): formerly owned by ConocoPhillips 50.1% and PDVSA 49.9%.

Petrozuata (Renamed PetroAnzoategui): Mixed company: PDVSA 100%

Ameriven (1997): formerly owned by ConocoPhillips 40%, Texaco 30% and PDVSA 30%.

Ameriven (Renamed PetroPiar):Mixed company: PDVSA 70%, y Chevron 30%.

Cerro Negro (1997): formerly owned by ExxonMobil 41.67%, PDVSA 41.67% and Veba Oel 16.66%.

Cerro Negro (Renamed PetroMonagas):Mixed company: PDVSA 83,37%, British Petroleum 16,67%.

Sincor (1993 and 1997): formerly owned by Total 47%, PDVSA 38% and Statoil 15%.

Sincor (Now PetroCedeño):Mixed company: PDVSA 60%, Total 30,3% y Statoil 9,7%.

Note: ConocoPhillips and ExxonMobil did not accept the new terms.

Energy Welfare Training Ltd - Evelyn Parra 2010

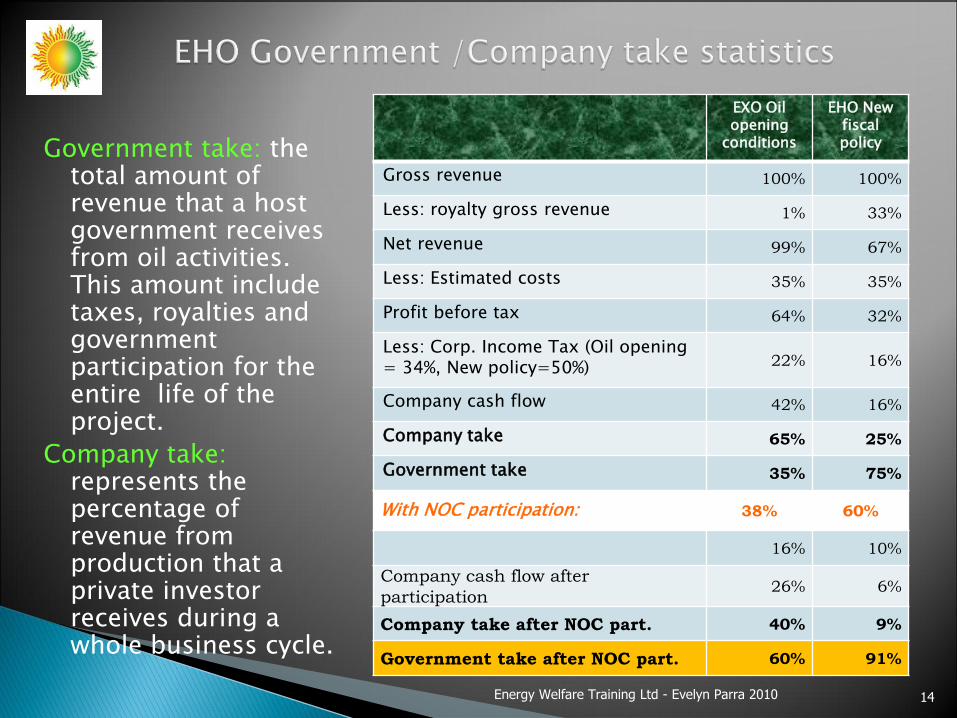

Government take: the total amount of revenue that a host government receives from oil activities. This amount include taxes, royalties and government participation for the entire life of the project.

Company take: represents the percentage of revenue from production that a private investor receives during a whole business cycle.

EXO Oil opening

conditions

EHO New fiscal policy

Gross revenue 100% 100%

Less: royalty gross revenue 1% 33%

Net revenue 99% 67%

Less: Estimated costs 35% 35%

Profit before tax 64% 32%

Less: Corp. Income Tax (Oil opening = 34%, New policy=50%) 22% 16%

Company cash flow 42% 16%

Company take 65% 25%

Government take 35% 75%

With NOC participation: 38% 60%

16% 10%

Company cash flow after

participation26% 6%

Company take after NOC part. 40% 9%

Government take after NOC part. 60% 91%

14Energy Welfare Training Ltd - Evelyn Parra 2010

EXO Oil opening conditions

EHO New fiscal policy

Sensitivity # 1 17% Royalty

Sensitivity # 230% Royalty

Gross revenue 100% 100% 100% 100%

Less: royalty gross revenue 1% 33% 17% 33%

Net revenue 99% 67% 83% 67%

Less: Estimated costs 35% 35% 35% 35%

Profit before tax 64% 32% 48% 32%

Less: Corp. Income Tax (Oil opening = 34%, New policy=50%)

22% 16%16% 11%

Company cash flow 42% 16% 32% 21%

Company take 65% 25% 49% 32%

Government take 35% 75% 51% 68%

With NOC participation: 38% 60% 38% 38%

16% 10% 12% 8%

Company cash flow after

participation26% 6% 20% 13%

Company take after NOC part. 40% 9% 31% 20%

Government take after NOC part. 60% 91% 69% 80%

15

Compounded Gvt for original project fiscal conditions: ((60%*9 years)+(69%*26 years))/35 years = 67%

Energy Welfare Training Ltd - Evelyn Parra 2010

Johnston, D. J World Energy Law Bus 2008 1:31-54; doi:10.1093/jwelb/jwn006

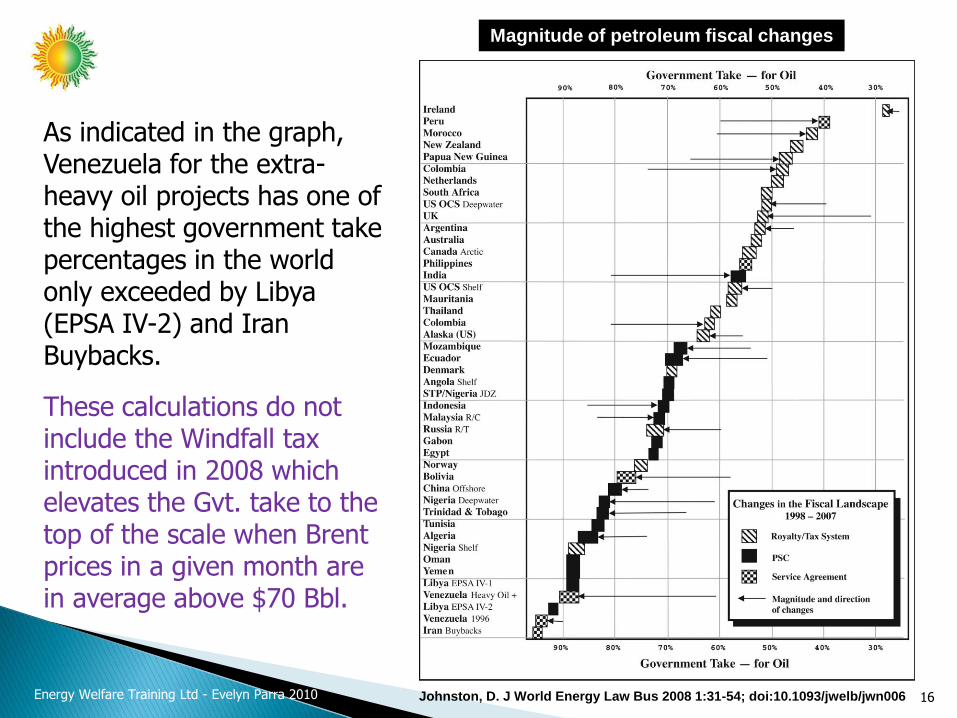

Magnitude of petroleum fiscal changes

As indicated in the graph, Venezuela for the extra-heavy oil projects has one of the highest government take percentages in the world only exceeded by Libya (EPSA IV-2) and Iran Buybacks.

These calculations do not include the Windfall tax introduced in 2008 which elevates the Gvt. take to the top of the scale when Brent prices in a given month are in average above $70 Bbl.

16Energy Welfare Training Ltd - Evelyn Parra 2010

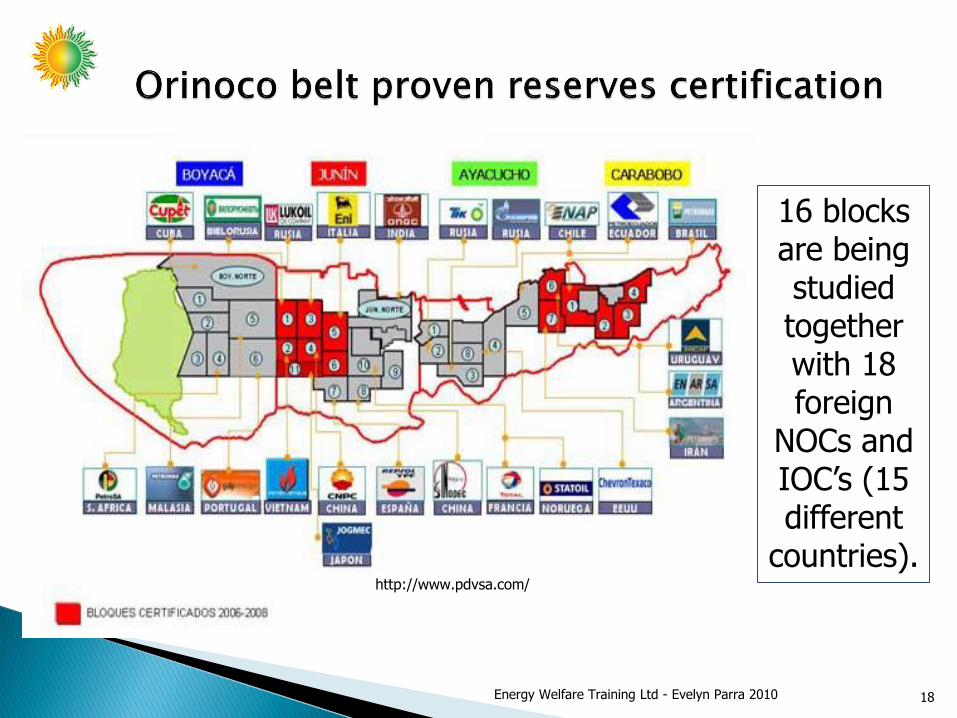

17

http://www.pdvsa.com/

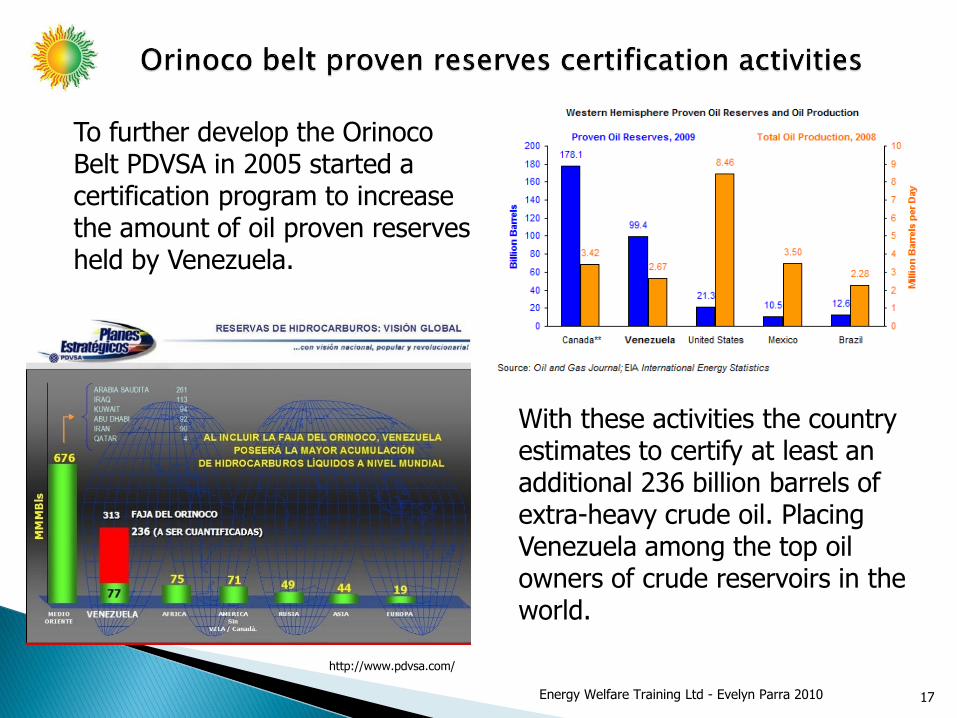

To further develop the Orinoco Belt PDVSA in 2005 started a certification program to increase the amount of oil proven reserves held by Venezuela.

Energy Welfare Training Ltd - Evelyn Parra 2010

With these activities the country estimates to certify at least an additional 236 billion barrels of extra-heavy crude oil. Placing Venezuela among the top oil owners of crude reservoirs in the world.

18

16 blocks are being studied together with 18 foreign

NOCs and IOC’s (15 different

countries).http://www.pdvsa.com/

Energy Welfare Training Ltd - Evelyn Parra 2010

19

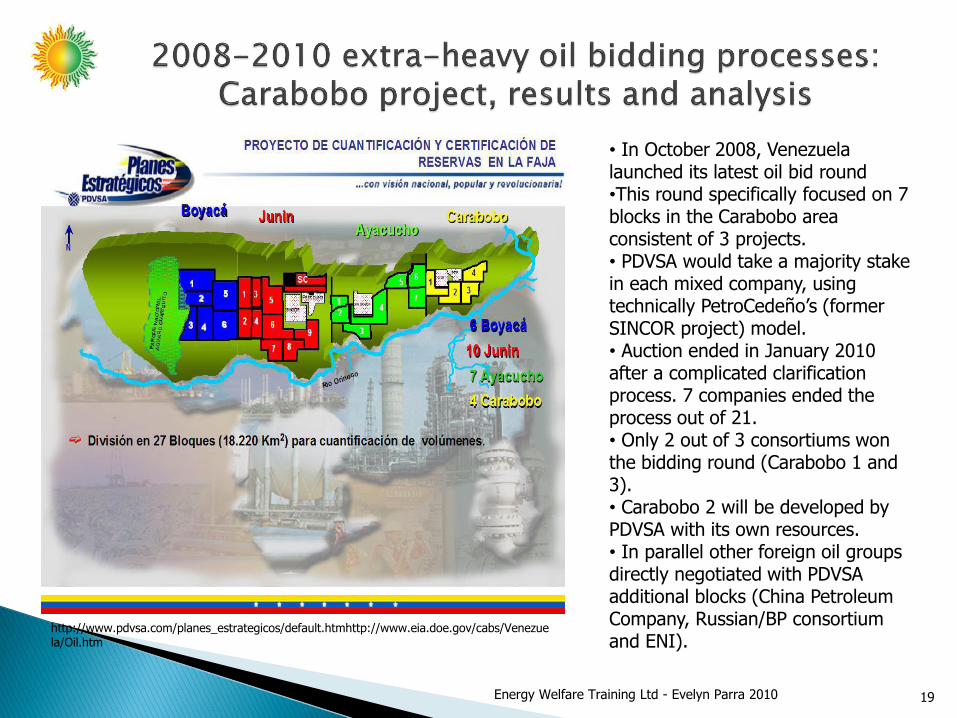

• In October 2008, Venezuela launched its latest oil bid round•This round specifically focused on 7 blocks in the Carabobo area consistent of 3 projects. • PDVSA would take a majority stake in each mixed company, using technically PetroCedeño’s (former SINCOR project) model.• Auction ended in January 2010 after a complicated clarification process. 7 companies ended the process out of 21.• Only 2 out of 3 consortiums won the bidding round (Carabobo 1 and 3). • Carabobo 2 will be developed by PDVSA with its own resources.• In parallel other foreign oil groups directly negotiated with PDVSA additional blocks (China Petroleum Company, Russian/BP consortium and ENI).

http://www.pdvsa.com/planes_estrategicos/default.htmhttp://www.eia.doe.gov/cabs/Venezuela/Oil.htm

Energy Welfare Training Ltd - Evelyn Parra 2010

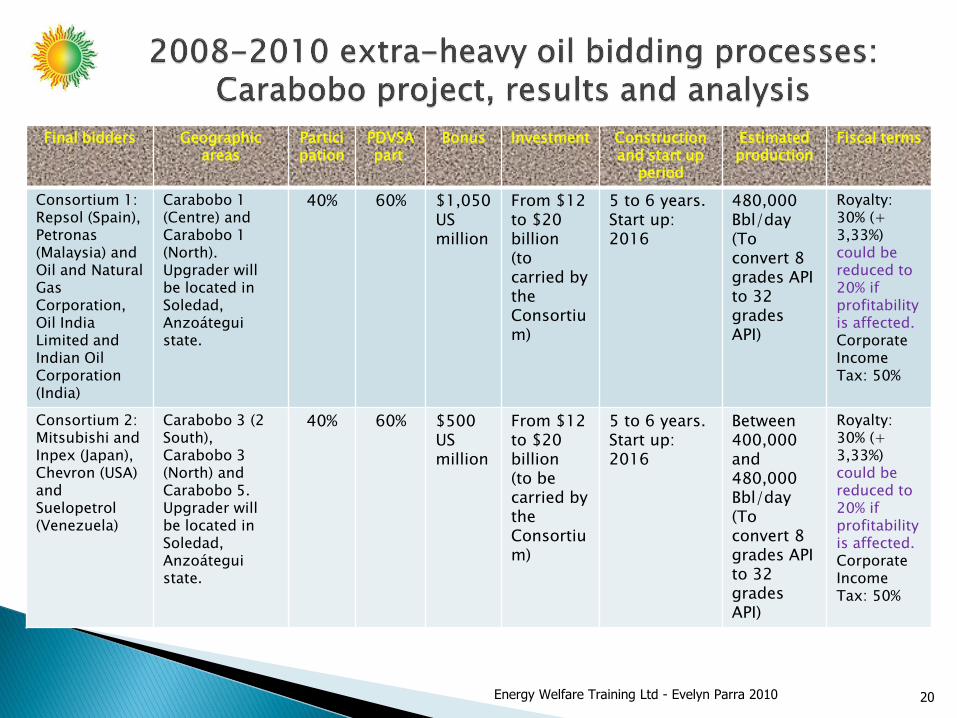

Final bidders Geographic areas

Participation

PDVSA part.

Bonus Investment Construction and start up

period

Estimated production

Fiscal terms

Consortium 1:Repsol (Spain), Petronas(Malaysia) and Oil and Natural Gas Corporation, Oil India Limited and Indian Oil Corporation (India)

Carabobo 1 (Centre) and Carabobo 1 (North). Upgrader will be located in Soledad, Anzoátegui state.

40% 60% $1,050US million

From $12 to $20billion (to carried by the Consortium)

5 to 6 years.Start up: 2016

480,000Bbl/day(To convert 8 grades API to 32 grades API)

Royalty: 30% (+ 3,33%) could be reduced to 20% if profitability is affected.Corporate Income Tax: 50%

Consortium 2: Mitsubishi and Inpex (Japan), Chevron (USA) and Suelopetrol(Venezuela)

Carabobo 3 (2 South), Carabobo 3 (North) and Carabobo 5.Upgrader will be located in Soledad, Anzoátegui state.

40% 60% $500 US million

From $12 to $20billion (to be carried by the Consortium)

5 to 6 years.Start up: 2016

Between 400,000 and 480,000 Bbl/day(To convert 8 grades API to 32 grades API)

Royalty: 30% (+ 3,33%) could be reduced to 20% if profitability is affected.Corporate Income Tax: 50%

20Energy Welfare Training Ltd - Evelyn Parra 2010

Key questions:

1) Do excessively high fiscal terms stopped foreign investment in

Venezuela?

2) How negotiable were tax conditions in the Carabobo project round?

3) Did political risk, contract and fiscal instability halt foreign investments

even for projects that require from 2 to 3 times higher costs in

Venezuela?

4) Were the recent Orinoco oil bidding activities 100% successful?

5) What are the main drivers of economic investment decisions for oil

projects with high government take?

21Energy Welfare Training Ltd - Evelyn Parra 2010

How countries use fiscal policy reforms acknowledging capacity strengths and weaknesses as well as consequences for all parties determine success or failure in subsequent oil and gas project developments.

22Energy Welfare Training Ltd - Evelyn Parra 2010

THANK YOU !

23Energy Welfare Training Ltd - Evelyn Parra 2010