Embed Size (px)

Citation preview

Presented byEnoch Ch’ng

Date8 October 2004

ASEANPay – What’s the story?

Whose big idea? Look who is talking Ambitious, ambitious Hurdle #1 Not that unexpected Where do we go from here? Still peddling snake oil?

Presentation Outline

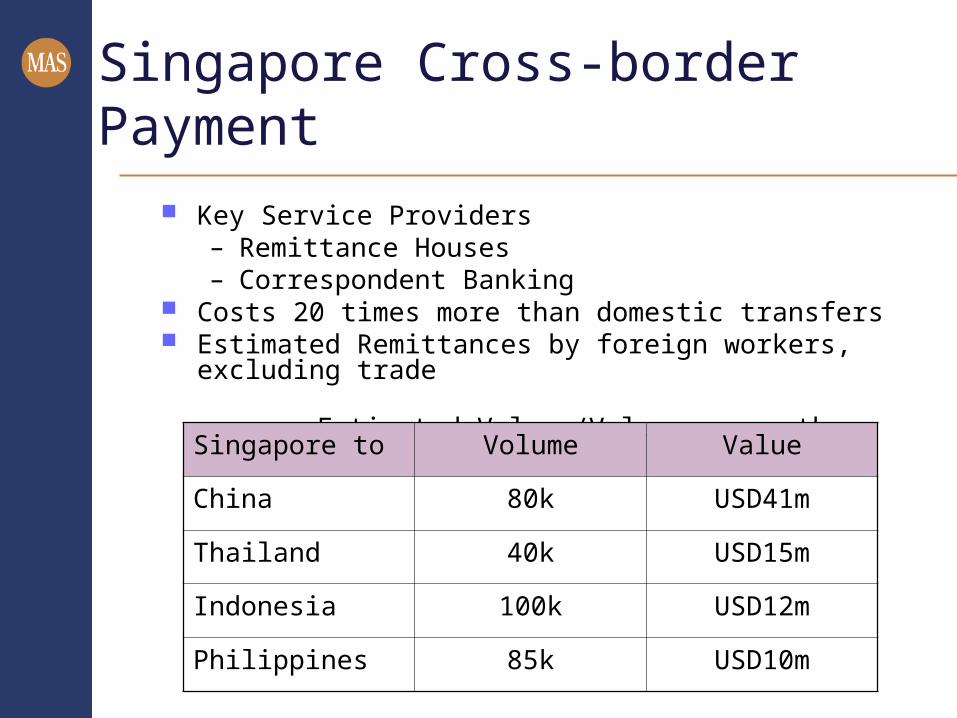

Singapore Cross-border Payment

Key Service Providers– Remittance Houses– Correspondent Banking

Costs 20 times more than domestic transfers Estimated Remittances by foreign workers, excluding trade

Estimated Volume/Value per month

Singapore to Volume Value

China 80k USD41m

Thailand 40k USD15m

Indonesia 100k USD12m

Philippines 85k USD10m

US$BillionMalaysia China Thailand US

Export2003 22.8 10.1 6.1 19.22002 21.8 6.9 5.7 18.4

Import2003 21.5 11.1 5.5 17.82002 21.2 8.9 5.4 16.5

In 2003, Singapore’s largest trade partner was Malaysia, followed by US

In 2003, Singapore was 13th largest trade partner of US*

* Source: International Trade Administration, US Department of Commerce

Singapore Trade Statistics

What’s in it for Central Bank?

Secure and efficient regional electronics transactions, payments and settlement.

Facilitate regulation, supervision & monitoring of cross-border payments.

Level playing field. Benefit smaller banks with no cross-border capability.

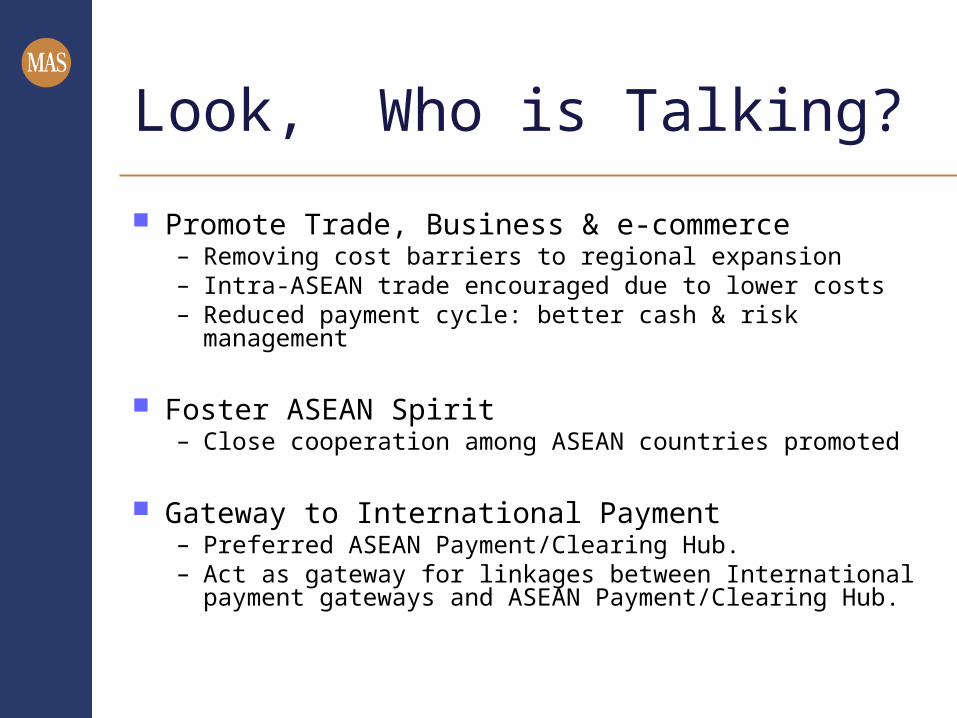

Look, Who is Talking?

Promote Trade, Business & e-commerce– Removing cost barriers to regional expansion– Intra-ASEAN trade encouraged due to lower costs– Reduced payment cycle: better cash & risk management

Foster ASEAN Spirit– Close cooperation among ASEAN countries promoted

Gateway to International Payment– Preferred ASEAN Payment/Clearing Hub.– Act as gateway for linkages between International payment

gateways and ASEAN Payment/Clearing Hub.

Ambitious, ambitious

Secure, efficient and cost effective Avoid re-inventing the wheel

– Leverage on existing ACH infrastructure – Use of national &/or international standards for

submission & receipt of payments to ASEANPay Stakeholders reliant

– Product responsibility lies with Financial Institutions (FIs)

– Foreign exchange conversion carried out by originating / remitting FIs

Regional PaymentRegional PaymentGatewayGateway

eACHVietnam

eACHBrunei

eACHCambodia

eACHIndonesia

eACHLaos

eACHMalaysia

eACHMyanmar

eACHPhilippines

eACHThailand

eACHSingapore

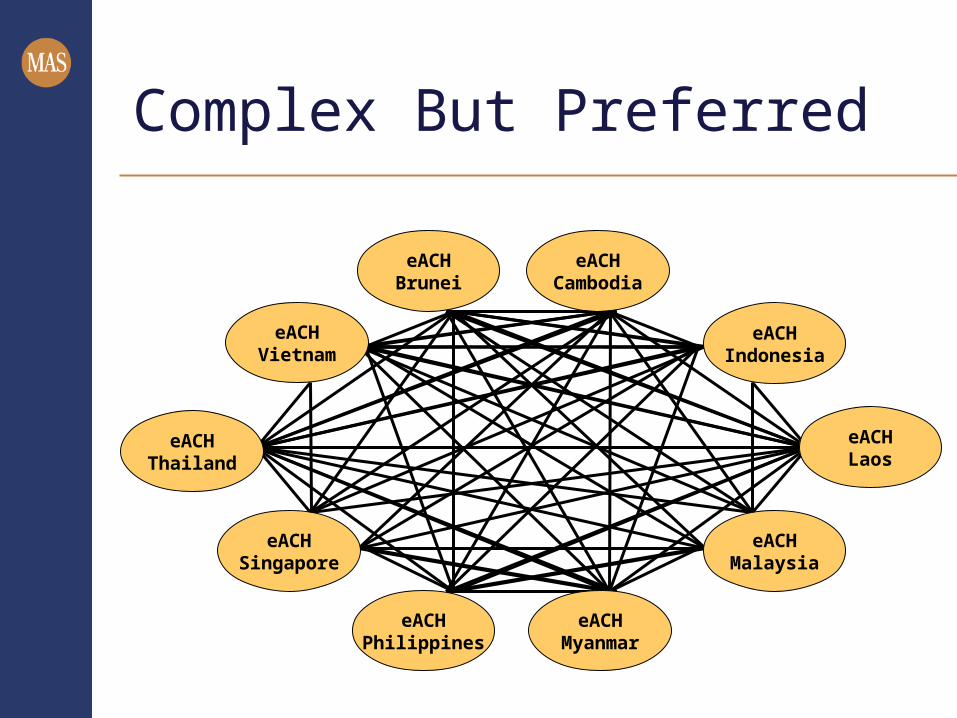

Viable But Rejected

Complex But Preferred

eACHVietnam

eACHBrunei

eACHCambodia

eACHIndonesia

eACHLaos

eACHMalaysia

eACHMyanmar

eACHPhilippines

eACHThailand

eACHSingapore

Buyer

Buyer’s Bank

Seller

Seller’s Bank

Country A

Country B

eACH A1 2

56

3Regional Regional PaymentPaymentGatewayGateway

eACH B

Settlement Agent Settlement Agent

4

Regional Payment Gateway

Not That Unexpected

Central Banks and ACH operators were keen. Difficult to get banks’ buy-in.

Uneven country readiness Currency exchange control for some countries

Money always matters.– Coverage and convenience of Remittance Houses– Transaction volume low, cost per transaction high– Low costs in SWIFT messaging

Borders still matters.

Where do we go from here?

Revalidate requirements Assessment of countries’ readiness Formulation of Business and Technical

Model Pilot Development in 2005?

Establish efficient, cost-effective & secure ASEAN cross-border payment infrastructure

Improve efficiency for cross border payments. Currently, predominantly correspondent banking. High costs, long payment cycle

Operate by Trusted Financial Institutions (Central banks, In-country National ACH)

Address consumers' need for faster, cheaper & secure payment service supported by a trusted financial community

Provide a complementary payment service to FIs

Still Selling Snake Oil?

Thank You