Embed Size (px)

Citation preview

SESSION TITLE

1

Employee Ownership Conference 2017

Presented by:

Anthony DolanPrairie Capital [email protected]

William Stewart, [email protected]

• Market Update

• Circumstances about Selling an ESOP Owned Company

• Board of Director Responsibilities

• Trustee Responsibilities

• M&A Process

• ESOP Transaction Issues and Considerations

• Select Case Study

• Q&A

2

SESSION TITLE

2

Employee Ownership Conference 2017

• The S&P 500 is at an all time high, growing 15%+ in last twelve months

• Public market valuations are strong

• Interest rates are low

• Lender appetite remains robust

• Supply and demand imbalance in the middle market M&A environment in 2016 and YTD 2017

• Broad based tax reform issues for 2017 and beyond

3

4

Total U.S. M&A Deal Volume and Value <$300M Transaction ValueQ1-2013 to Q2-2017

Source: Capital IQ

SESSION TITLE

3

Employee Ownership Conference 2017

5

U.S. Private Equity ExitsQ1-2013 to Q2-2017

Source: Pitchbook

6

Total Enterprise Value / EBITDA by Deal Size ($ Millions)2013 to Q1-2017

Source: GF Data

SESSION TITLE

4

Employee Ownership Conference 2017

7

TEV/EBITDA Multiple by Buyer Type ($10-250M of TEV)2013 to Q1-2017

Source 1: Financial Buyers: GF Data ($10-250M TEV)Source 2: Strategic Buyers: Capital IQ ($10-250M TEV; Excluding outliers defined as transactions with TEV/EBITDA of less than 3.0x and more than 14.0x)

8

Equity and Debt Capitalization2013 to Q1-2017

Source: GF Data

SESSION TITLE

5

Employee Ownership Conference 2017

9

Loan Issuance for the Middle Market <$100M2009 to May 2017

Source: Thomson Reuters

• Unsolicited offer

• Non-ESOP majority shareholder

• Market conditions and industry dynamics

• Board of Directors conclude best way to maximize shareholder value

• Company-specific issues:

– Management succession issues

– Performance

– Repurchase obligation

– Excessive debt leverage (cash flow issues)

10

SESSION TITLE

6

Employee Ownership Conference 2017

11

• High potential value

• Gain liquidity, fund retirement accounts

• Diversification from the risk of a single employer security

• Reduce holding risk

• Strategic partnership opportunity, may help grow the business

• Other

Positives Negatives

• Change in governance

• Potential loss of culture

• Potential loss of jobs/consolidation

• Potential loss of long-term equity upside

• M&A closing risk –exposure to competitors

• Other

• Solicitation/offer types:

• Inquiry

• Indication of interest

• Letter of intent

• Definitive agreement

• Each type of solicitation/offer deserves a certain level of response

• Bona fide offer

• Proposed consideration is nominally adequate

• Other proposed deal terms are fair and reasonable and treat all shareholders equitably

• Potential buyer has the financial ability to pay the proposed purchase price

• Management should treat “real” offers seriously but no duty to inform the Board/ESOP trustee if offer is not bona fide

• Is ESOP minority or majority shareholder?

12

SESSION TITLE

7

Employee Ownership Conference 2017

• Very common for ESOP held companies

• Determine legitimacy

• Who made the offer?

• Industry competitor/participant

• Financial buyer/private equity

• Related party, management/former owner

• Where was it first received?

• Company management

• Director/Board of Directors

• ESOP Trustee

13

14

Corporate Team (Seller)

Shareholders

Board of directors

Senior management

Investment banker

ESOP Team

(Seller)

ESOP trustee/transaction

fiduciary

Financial advisor

Legal counsel

Plan participants

(maybe)

Buyer Team

(Buyer)

Owner/board of directors

Senior management

Legal counsel

Financing sources

Legal counsel

Tax advisors/accountants

Environmental/other

consultants

ESOP AdministrationQuality of earnings

consultants

Environmental

Real estate and equipment

appraisal firms

SESSION TITLE

8

Employee Ownership Conference 2017

• Duty of Loyalty

• Director must act in good faith and not place personal interests above corporation’s interests

• Duty of Care

• A director must carry out his corporate duties with such care as an ordinarily reasonable prudent man in a like position would carry out his corporate duties under similar circumstances

• Business Judgment Standard

• A director who makes a business decision (i.e., a decision made on behalf of the corporation) in good faith fulfills the “Duty of Care” if the director: (i) is not interested in the subject of his business decision; (ii) is informed with respect to the subject of the business decision to the extent the director reasonably believes to be appropriate under the circumstances; and (iii) rationally believes that the business decision is in the best interest of the corporation

15

• Board of Director policies and procedures regarding the sale of an ESOP company

• Policies on how to handle unsolicited offers or an auction process

• Document reasons for sale

• Strategic alternatives analysis

• Does future value exceed the bona fide offer?

• Board is subject to “Business Judgment Rule” and should take into account:

• Value to shareholders/Revlon

• Company culture and independence

• Employees, employment, motivation and productivity

• Alternative buyers/strategies (if unsolicited offer)

• Continuity of business

• Whether purchase price is no less than fair cash value

• Makes the decision to analyze and negotiate the offer

• Is an auction process required?

16

SESSION TITLE

9

Employee Ownership Conference 2017

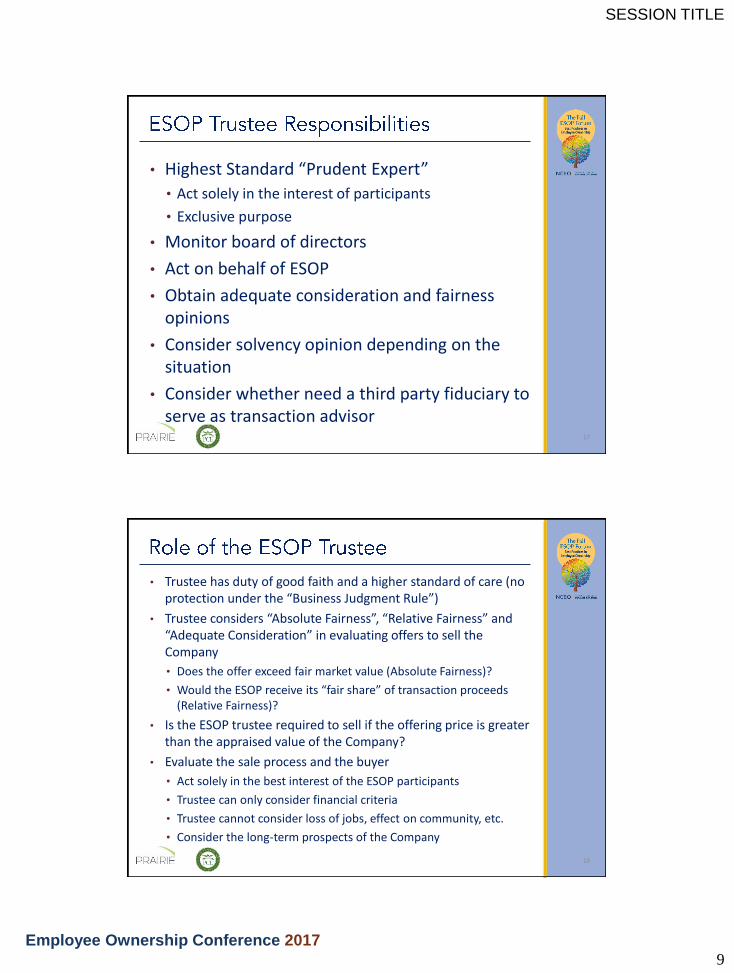

• Highest Standard “Prudent Expert”

• Act solely in the interest of participants

• Exclusive purpose

• Monitor board of directors

• Act on behalf of ESOP

• Obtain adequate consideration and fairness opinions

• Consider solvency opinion depending on the situation

• Consider whether need a third party fiduciary to serve as transaction advisor

17

• Trustee has duty of good faith and a higher standard of care (no protection under the “Business Judgment Rule”)

• Trustee considers “Absolute Fairness”, “Relative Fairness” and “Adequate Consideration” in evaluating offers to sell the Company

• Does the offer exceed fair market value (Absolute Fairness)?

• Would the ESOP receive its “fair share” of transaction proceeds (Relative Fairness)?

• Is the ESOP trustee required to sell if the offering price is greater than the appraised value of the Company?

• Evaluate the sale process and the buyer

• Act solely in the best interest of the ESOP participants

• Trustee can only consider financial criteria

• Trustee cannot consider loss of jobs, effect on community, etc.

• Consider the long-term prospects of the Company

18

SESSION TITLE

10

Employee Ownership Conference 2017

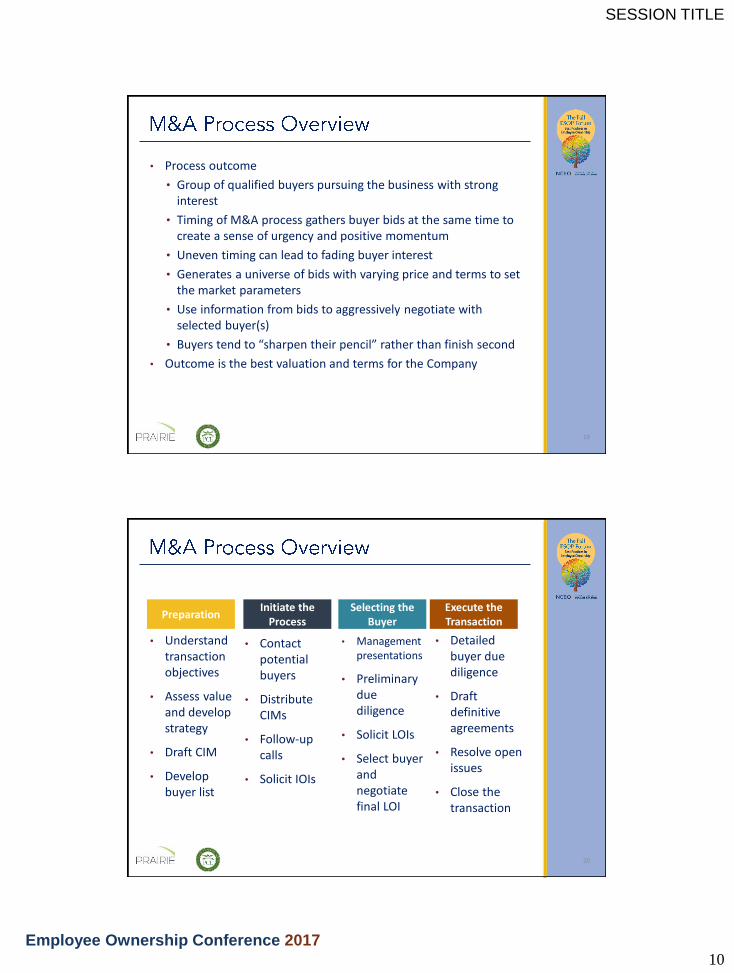

• Process outcome

• Group of qualified buyers pursuing the business with strong interest

• Timing of M&A process gathers buyer bids at the same time to create a sense of urgency and positive momentum

• Uneven timing can lead to fading buyer interest

• Generates a universe of bids with varying price and terms to set the market parameters

• Use information from bids to aggressively negotiate with selected buyer(s)

• Buyers tend to “sharpen their pencil” rather than finish second

• Outcome is the best valuation and terms for the Company

19

20

• Understand transaction objectives

• Assess value and develop strategy

• Draft CIM

• Develop buyer list

Preparation

• Contact potential buyers

• Distribute CIMs

• Follow-up calls

• Solicit IOIs

Initiate the Process

• Management presentations

• Preliminary due diligence

• Solicit LOIs

• Select buyer and negotiate final LOI

Selecting the Buyer

• Detailed buyer due diligence

• Draft definitive agreements

• Resolve open issues

• Close the transaction

Execute the Transaction

SESSION TITLE

11

Employee Ownership Conference 2017

• Buyer needs to be educated as to the peculiarities of ESOP-owned companies

• Divergence from what is customary in non-ESOP M&A transactions and what is “allowable” under ERISA and customary in ESOP M&A transactions

• Buyers need to conduct more extensive due diligence – recourse typically limited to an escrow

• Valuation, fiduciary and administrative issues relating to the ESOP will need to be explained

• Need for pass-through voting (maybe)

• Additional parties means additional deal risk for the buyer

• What is the proposed transaction structure?

• Asset purchase

• Stock purchase

• Merger

• What is the consideration to be paid?

• Cash, stock, other

• Is the transaction nominally “adequate” to the ESOP?

21

22

Price and terms

Non-equity allocations

Reps and warranties

Indemnification

Adequate Consideration

▪ Cash (non-contingent)

▪ Indemnity escrow (contingent)

▪ Earn-out (contingent)

▪ Treatment of unallocated shares

▪ Are there solutions to these deal

sticking points?

SESSION TITLE

12

Employee Ownership Conference 2017

23

Non-equity

allocations

Price and terms

Reps and warranties

Indemnification

Relative Fairness

▪ Employment agreements

▪ Non-compete payments

▪ Transaction and stay bonuses

▪ Deferred compensation

▪ Golden parachutes

▪ Leases between company and

related parties

▪ Company guarantees of related

party debts and lease payments

24

Reps and

warranties

Price and terms

Non-equity

allocations

Indemnification

Considerations

▪ ESOP trustee typically wants to limit

reps and warranties to

appointment, authority and

ownership

▪ The Company typically will make all

the reps and warranties

▪ Will the escrow be the only source

of the indemnity?

▪ Survival period

SESSION TITLE

13

Employee Ownership Conference 2017

25

Indemnification

Price and terms

Non-equity

allocations

Reps and warranties

Considerations

▪ Indemnity for breach of agreement

and reps and warranties will be

limited to escrowed funds

▪ Duration of escrow

▪ Survival period (trustee and

company)

• Pass-Through vote required?• Compliance with voting instructions requirements and applicable

fiduciary rules

• 1042 – Is the ESOP less than 3 years old?• Excise tax

• Is the ESOP still leveraged?• Use of proceeds from sale of unallocated shares

• Repay ESOP debt• Comply with prohibited transaction rules

• Fiduciary concerns

• Alternatives to using proceeds to repay ESOP debt

• Code Section 415

• Equity allocation negotiation

26

SESSION TITLE

14

Employee Ownership Conference 2017

• Options for ESOP post-transaction

• Merge ESOP into buyer’s plan

• Amend to profit sharing

• Terminate ESOP and distribute assets to participants

• ESOP plan termination

• Prepare board resolution to terminate plan

• IRS favorable determination letter

• Amendments to ESOP document (if needed)

• Establish procedures for making final allocations

27

• Distribution of plan assets

• Changes to timing, method or form?

• Stock vs. cash distributions

• Wait for favorable IRS determination letter

• Transferring assets to a buyer’s plan – plan amendment

• Current distributions in process will need special attention – most recent valuation vs. sale price

• What should be done after a possible sale is known and before a transaction is closed?

• How are earned escrow funds treated?

28

SESSION TITLE

15

Employee Ownership Conference 2017

29

Background

Challenge

Action

Results

▪ Company is a leading processor and distributor of specialty enameling

and electrical steel with significant steel toll processing, storage, and

transportation capabilities

▪ The Company became 66.7% ESOP-owned in 1990 and 100% ESOP-

owned in 2003

▪ The Company maintained a redemption policy which began to

concentrate ownership

▪ Alternatives were explored to overcome this issue, however, given the

robust M&A activity level in the market, the Company explored a

strategic sale

▪ The deal team not only needed to understood the M&A markets and the

steel industry, but also needed experience with ESOPs as a selling

shareholder

▪ Marketing materials and buyers lists were developed and a targeted

group of strategic buyers were approached in a highly structured auction

environment

▪ Multiple indications of interest were received and ultimately one party

(buyer) was chosen in a highly competitive process

▪ Communication was key between all parties involved

▪ Successful transaction which was highly beneficial to ESOP participants

▪ The competitive nature of the transaction led not only to premium

pricing, but above-average terms and structure

▪ Long-term strategic fit for the buyer from a business perspective

▪ Time will tell if it ends up being a long-term cultural fit

30

Anthony DolanPrairie Capital Advisors

William Stewart, CFAPCE

![NOTE - Stetson University · 1995] Dolan 217 19. John T. Dolan, husband of the Petitioner, Florence Dolan, initially joined with his wife in bringing suit. However, Mr. Dolan died](https://img.pdfslide.us/doc/110x75/5f8376d34c77f5385d0a54c2/note-stetson-university-1995-dolan-217-19-john-t-dolan-husband-of-the-petitioner.jpg)