Embed Size (px)

Citation preview

Presentation to:

Virginia Government Finance Officers’ Association

“Virginia College Savings Plan – Program Overview and a CFO’s Viewof Surviving Recent Market Challenges”

Gary Ometer, CPA, Chief Financial OfficerJune 8, 2011

Presented by:

VGFOA – June 8, 2011 2

Presentation Goals

State of Saving for College

529 Plans

Virginia College Savings Plan

Regulatory Challenges

VGFOA – June 8, 2011 3

State of Saving for College

VGFOA – June 8, 2011 4

Tuition and Fee Increases

Source: The College Board, Trends in College Pricing 2010

VGFOA – June 8, 2011 5

Cost of College

Source: The College Board, Trends in College Pricing 2010

VGFOA – June 8, 2011 6

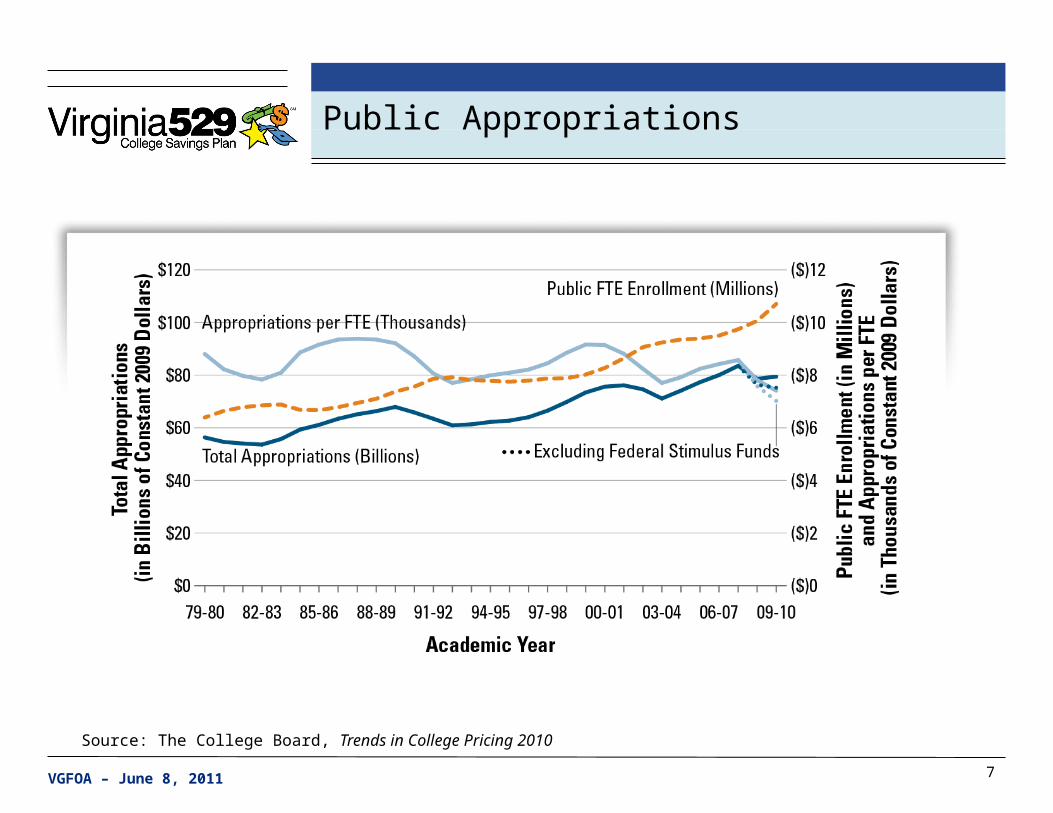

Public Appropriations

Source: The College Board, Trends in College Pricing 2010

Annual Percentage Changes in State Appropriations for Higher Education per Full-Time Equivalent (FTE) Student and in Tuition and Fees at Public Four-Year Institutions in Constant 2009 Dollars, 1979-80 to 2009-10

VGFOA – June 8, 2011 7

Public Appropriations

Source: The College Board, Trends in College Pricing 2010

VGFOA – June 8, 2011 8

Saving For Funding College

Funding Sources

Savings (529 Plans and other savings vehicles)

Scholarships (academic and need-based)

Grants (federal and state)

Loans (federal, state, school)

Cash-on-hand (parents, students)

Scholarships (athletic)

VGFOA – June 8, 2011 9

How Much Have You Saved for College?

Source: College Savings Foundation – 2010 Survey of Parents

VGFOA – June 8, 2011 10

How Do Parents Plan on Funding College?

Source: College Savings Foundation - 2010 Survey of Parents

VGFOA – June 8, 2011 11

Primary Savings Vehicle

Source: College Savings Foundation - 2008 Parents Survey

VGFOA – June 8, 2011 12

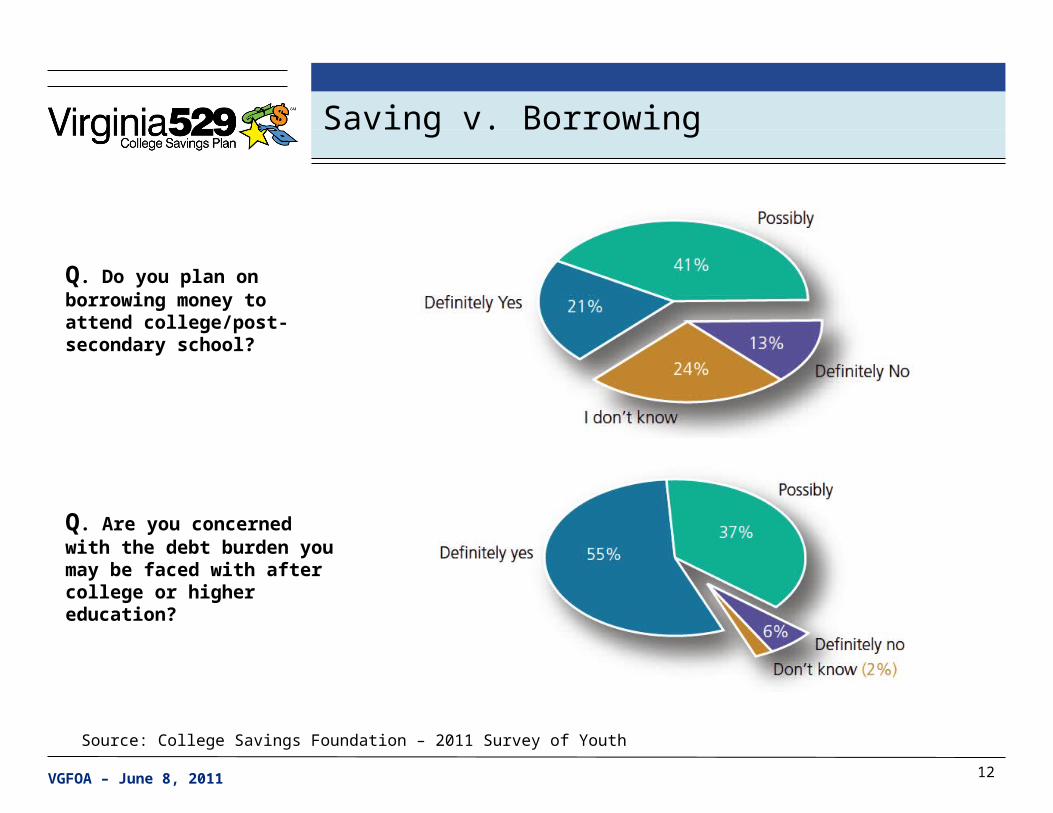

Saving v. Borrowing

Q. Do you plan on borrowing money to attend college/post-secondary school?

Q. Are you concerned with the debt burden you may be faced with after college or higher education?

Source: College Savings Foundation – 2011 Survey of Youth

VGFOA – June 8, 2011 13

Saving v. Borrowing (cont.)

Source: College Savings Foundation – 2010 Survey of Parents

VGFOA – June 8, 2011 14

529 Plans

VGFOA – June 8, 2011 15

What is a 529 Plan?

Education savings plan operated by a state or educational institution designed to help families set aside funds for future college costs

Section 529 Internal Revenue Code, enacted in 1996

Plans can be used to meet qualified higher education expenses at eligible educational institutions

Tax advantaged

Two types:

• Prepaid plans

• Savings plans

VGFOA – June 8, 2011 16

Growth of the National 529 Market – January 2000 - June 2010

• Beginning in 2001, participation in savings plans far outpaced prepaid plans

• Savings plan assets decreased more dramatically than prepaid assets in 2008 with similar increases in 2009

• Asset and account growth across remained relatively unchanged between year-end 2009 and mid-year 2010

Source: College Savings Plan Network (“CSPN”); data as of June 30, 2010

YE 2000

YE 2001

YE 2002

YE 2003

YE 2004

YE 2005

YE 2006

YE 2007

YE 2008

YE 2009

Q2 2010

$0

$35,000,000,000

$70,000,000,000

$105,000,000,000

$140,000,000,000National 529 Assets 2000 - June 2010

Prepaid Savings

($ B

illio

ns)

YE 2000

YE 2001

YE 2002

YE 2003

YE 2004

YE 2005

YE 2006

YE 2007

YE 2008

YE 2009

Q2 2010

0

3,000,000

6,000,000

9,000,000

12,000,000

National 529 Accounts 2000 - June 2010

Prepaid Savings

Acc

ount

s (0

00s)

VGFOA – June 8, 2011 17

Benefits of 529 Plans

Federal tax benefits – earnings grow free from federal tax, and withdrawals for qualified higher education expenses are likewise free from federal tax

State tax benefits – Virginia 529 plan account owners with Virginia taxable income are eligible for up to a $4,000 tax deduction per contract or account with an unlimited carryforward – other states’ plans may also provide state tax benefits

No income limits – no calculations required to determine whether you may contribute

Virginia has a $350,000 aggregate limit per beneficiary

Donor retains control of funds – account owner rather than beneficiary retains control of account assets and determines amount and timing of distributions (VPEP distributions paid directly to college)

VGFOA – June 8, 2011 18

Benefits of 529 Plans (cont.)

You may open an account for your child, grandchild, spouse, friend or yourself

Plan assets may be used to pay qualified higher education expenses at any eligible educational institution in the world – expenses include tuition, room and board, books, supplies and certain fees (VPEP covers tuition and mandatory fees only)

Flexible – account owners may change beneficiaries without penalty provided the new beneficiary is a member of the previous beneficiary’s immediate family

Rollovers – Can roll from one program to another

Low maintenance – Virginia accounts may be set up with a variety of payment plans (depending on VPEP, VEST, etc.) and Virginia savings plans offer a number of investment options

VGFOA – June 8, 2011 19

Virginia College Savings Plan

VGFOA – June 8, 2011 20

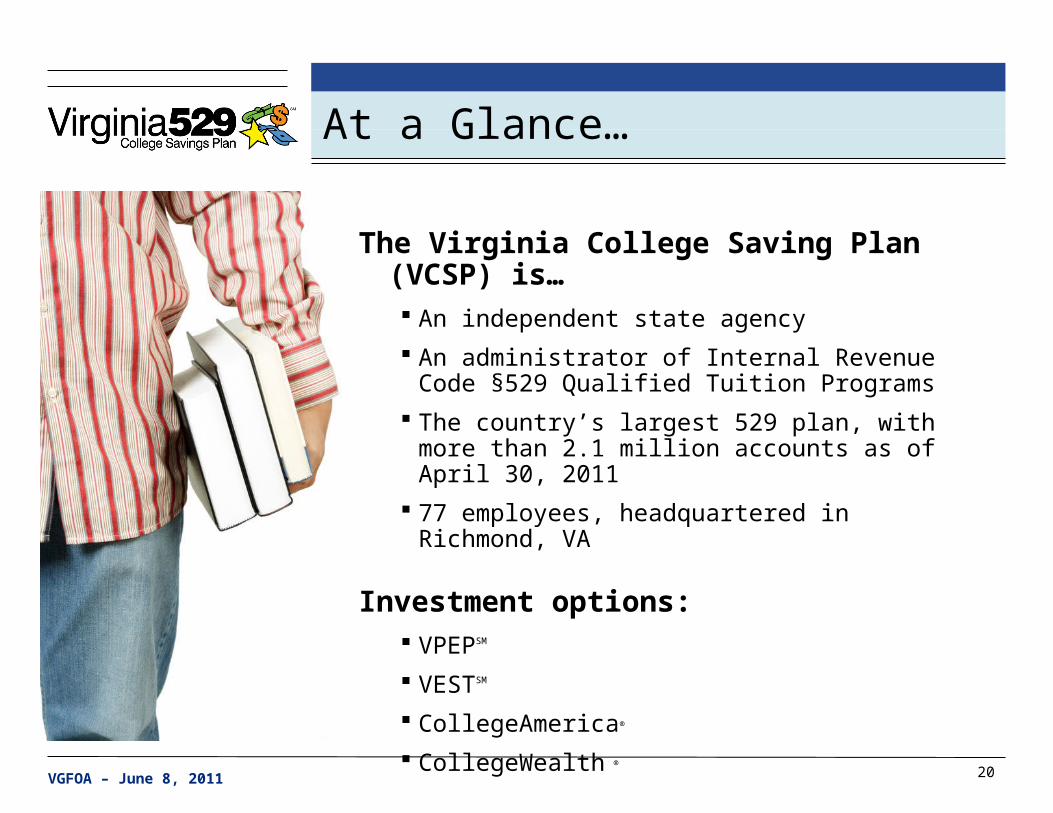

At a Glance…

The Virginia College Saving Plan (VCSP) is… An independent state agency

An administrator of Internal Revenue Code §529 Qualified Tuition Programs

The country’s largest 529 plan, with more than 2.1 million accounts as of April 30, 2011

77 employees, headquartered in Richmond, VA

Investment options: VPEPSM

VESTSM

CollegeAmerica®

CollegeWealth ®

VGFOA – June 8, 2011 21

Our Programs

Virginia Prepaid Education Program (VPEP) - allows families to purchase contracts for future tuition and mandatory fees at Virginia public colleges and universities. Opened in 1996.

Virginia Education Savings Trust (VEST) - a direct-sold savings program offering age-based evolving portfolios and static investment portfolios featuring Vanguard and other mutual funds. Opened in 1999.

CollegeAmerica - a broker-sold savings program offering a wide selection of the American Funds portfolios, one of the largest mutual fund families in the country. Opened in 2002.

CollegeWealth - FDIC-insured 529 savings accounts offered through participating banks including Union First Market Bank and BB&T. Opened in 2007.

VGFOA – June 8, 2011 22

VPEP Assets and Account Growth

FYE 19

97

FYE 19

98

FYE 19

99

FYE 20

00

FYE 20

01

FYE 20

02

FYE 20

03

FYE 20

04

FYE 20

05

FYE 20

06

FYE 20

07

FYE 20

08

FYE 20

09

FYE 20

10

3/31

/201

1

$0

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

$1,600,000,000

$1,800,000,000

$2,000,000,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

VPEP Assets Under Management and Total Accounts

Balances

Accounts

VGFOA – June 8, 2011 23

VEST Assets and Account Growth

FYE 20

00

FYE 20

01

FYE 20

02

FYE 20

03

FYE 20

04

FYE 20

05

FYE 20

06

FYE 20

07

FYE 20

08

FYE 20

09

FYE 20

10

3/31

/201

1

$0

$200,000,000

$400,000,000

$600,000,000

$800,000,000

$1,000,000,000

$1,200,000,000

$1,400,000,000

$1,600,000,000

$1,800,000,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

VEST Assets Under Management and Total Accounts

Balances

Accounts

VGFOA – June 8, 2011 24

Program Statistics

Distributions began in 2000

Over $681 million distributed through 6/30/10 (VPEP and VEST)

VPEP Student Attendance – 2010 Fall Semester

• 67% in-state public four-year institutions*

• 13% community college

• 6% in-state private

• 14% at more than 460 out-of-state schools

* 64% of students (43% overall) attending in-state public institutions attend University of Virginia, Virginia Tech, William & Mary, James Madison and Virginia Commonwealth University

VGFOA – June 8, 2011 25

Assets Under Management

Number of Accounts Assets Under Management

Program June 30, 2009 June 30, 2010 April 30, 2011 June 30, 2009 June 30, 2010 April 30, 2011

VPEP 71,847 71,373 71,415 $1,335,093,400 $1,613,149,325 $1,952,551,463

VEST 115,957 129,415 141,402 $1,056,274,799 $1,346,385,956 $1,768,049,095

CollegeAmerica 1,807,211 1,893,271 1,921,918 $21,115,858,233 $25,021,126,526 $32,671,015,902

CollegeWealth 601 2,760 5,034 $4,986,631 $13,911,187 $23,282,280

Total 1,995,616 2,096,819 2,139,769 $23,512,213,064 $27,994,572,994 $36,414,898,741

VGFOA – June 8, 2011 26

VPEP Assets Under Management

Market Value by Asset Class as of April 30, 2011

Domestic Equity17.7%

International Equity18.6%

Alternatives13.0%

Core Fixed Income23.3%

Non-Core Fixed Income24.5%

Cash2.8%

VGFOA – June 8, 2011 27

2007-2009 Financial Meltdown

Causes Domestically:

Poor lending decisions

Poor borrowing decisions

Excessive leverage (individual / corporate / government)

Lax risk management

Misaligned incentives

Antiquated and dysfunctional regulatory framework

Predatory rather than productive bankers

VGFOA – June 8, 2011 28

VPEP – New Target Asset Allocation

In 2008 recognized that the VPEP portfolio volatility (risk) was not generating returns commensurate with volatility

Desire to review VPEP’s long-term expected liabilities and cash flows versus the assets invested under VPEP

Asset Liability Modeling study in 2009 with goal of finding optimal balance between investment risk and long-term cost

Report completed and presented by VCSP’s investment consultant and actuary in June 2009

Investment Advisory Committee and Board approved new target asset allocation

Decreased: Domestic equity and core fixed income

Increased: Emerging market equity and high yield fixed income

Added: Emerging market debt and alternatives

VGFOA – June 8, 2011 29

VPEP – New Target Asset Allocation (cont.)

Domestic Equity44.1%

International Equity11.0%

Core Fixed Income35.2%

Non Core Fixed In-

come5.2%

Cash4.6%

Asset Allocation as of June 30, 2008

Domestic Equity17.7%

Interna-tional Equity18.6%

Alterna-tives

13.0%

Core Fixed Income23.3%

Non-Core Fixed In-

come24.5%

Cash2.8%

Asset Allocation as of April 30, 2011

VGFOA – June 8, 2011 30

VPEP – Transition to Target Asset Allocation

Domestic Equity15.0%

International Equity17.5%

Alternatives15.0%

Core Fixed Income25.0%

Non Core Fixed Income

27.5%

Target Asset Allocation

Domestic Equity17.7%

Interna-tional Equity18.6%

Alterna-tives

13.0%

Core Fixed Income23.3%

Non-Core Fixed In-

come24.5%

Cash2.8%

Asset Allocation as of April 30, 2011

VGFOA – June 8, 2011 31

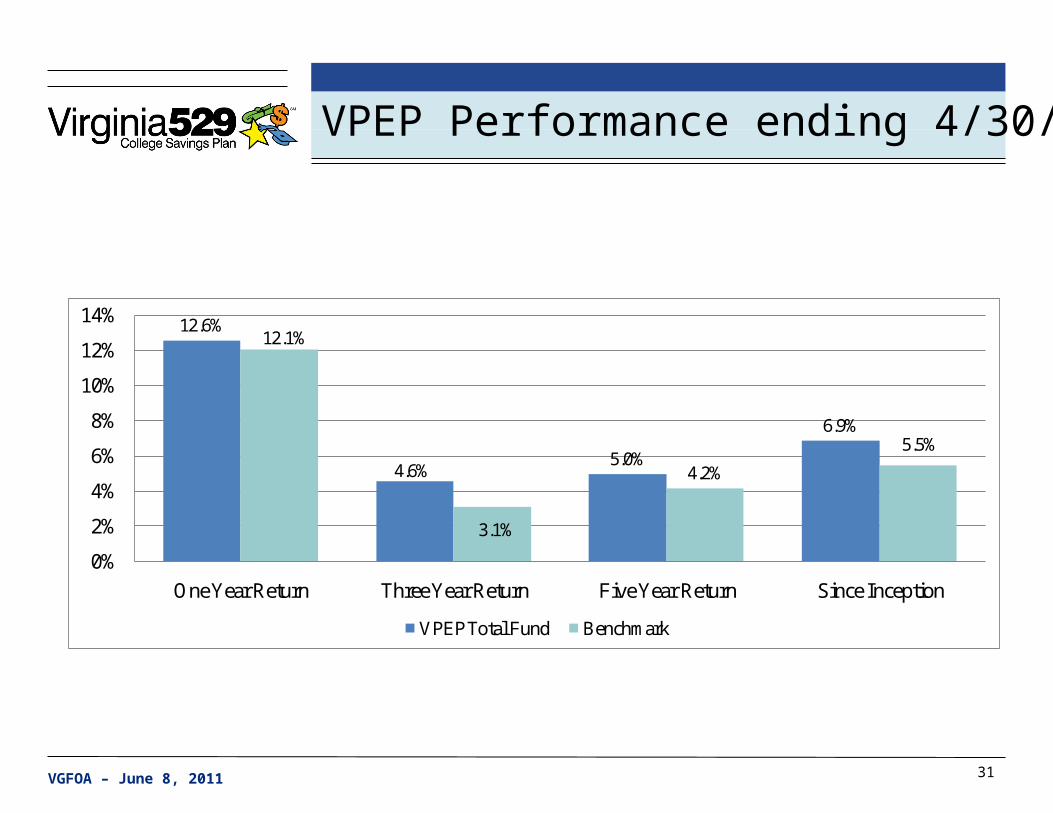

12.6%

4.6%5.0%

6.9%

12.1%

3.1%

4.2%

5.5%

0%

2%

4%

6%

8%

10%

12%

14%

One Year Return Three Year Return Five Year Return Since Inception

VPEP Total Fund Benchmark

VPEP Performance ending 4/30/2011

VGFOA – June 8, 2011 32

VPEP Annual Returns Since Inception

10.4%7.6% 7.6%

1.4%

-1.4%

5.6%

14.9%

10.1% 9.8%

14.6%

-4.3%

-16.3%

18.7% 20.1%

-20%-15%-10%

-5%0%5%

10%15%20%25%

One Year Returns by Fiscal Year

*2011 performance through 4/30/2011

VGFOA – June 8, 2011 33

Investment Return Assumptions

Year Return

1996 – 2000 8.0%

2001 7.5%

2002 7.0%

2003 6.75%

2004 - 2010 7.0%

VGFOA – June 8, 2011 34

VPEP Actuarial Tuition Increase Assumptions*

Universities Community Colleges

Academic YearJune 30, 2010

assumptionPrior

assumptionJune 30, 2010

assumptionPrior

assumption

Fall 2011 10.00% 8.50% 9.50% 7.50%

Fall 2012 10.00% 7.50% 8.50% 7.50%

Fall 2013 forward 7.50% 7.50% 7.50% 7.50%

*Assumption includes tuition and all mandatory fees (both education and general fees and non-education and general fees)

VGFOA – June 8, 2011 35

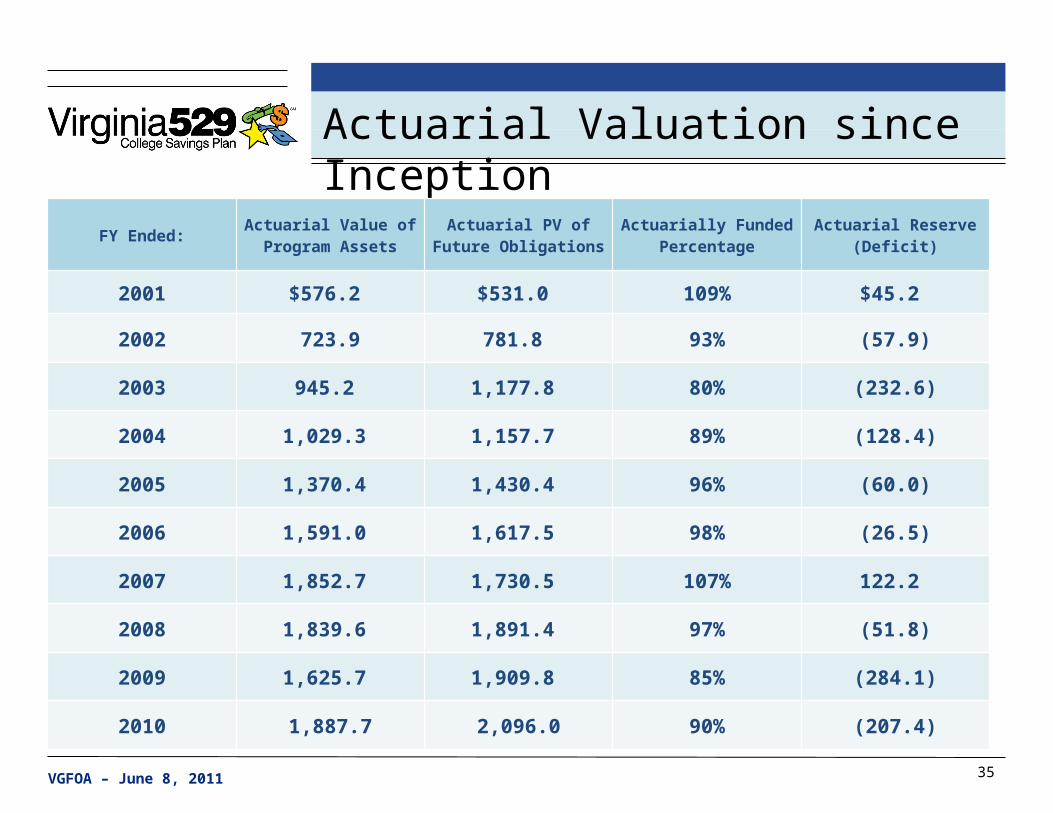

Actuarial Valuation since Inception

FY Ended:Actuarial Value of

Program AssetsActuarial PV of Future

ObligationsActuarially Funded

PercentageActuarial Reserve (Deficit)

2001 $576.2 $531.0 109% $45.2

2002 723.9 781.8 93% (57.9)

2003 945.2 1,177.8 80% (232.6)

2004 1,029.3 1,157.7 89% (128.4)

2005 1,370.4 1,430.4 96% (60.0)

2006 1,591.0 1,617.5 98% (26.5)

2007 1,852.7 1,730.5 107% 122.2

2008 1,839.6 1,891.4 97% (51.8)

2009 1,625.7 1,909.8 85% (284.1)

2010 1,887.7 2,096.0 90% (207.4)

VGFOA – June 8, 2011 36

Historical Funded Status and Actuarial Reserve

Fun

ded

Per

cent

age

Act

uari

al R

eser

ve

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

0%

20%

40%

60%

80%

100%

120%

140%

($300)

($200)

($100)

$0

$100

$200

$300

Funded Percentage Actuarial Reserve

VGFOA – June 8, 2011 37

Regulatory Challenges

VGFOA – June 8, 2011 38

Government Employees

“You give 100 percent in the first half of the game, and if that isn’t enough in the second half you give what’s left.”

Yogi Berra

VGFOA – June 8, 2011 39

Recent Regulatory Changes / Announcements

•Federal Trade Commission Red Flags Rule

•Dodd-Frank Wall Street Reform and Consumer Protection Act

•Municipal Securities Rulemaking Board (MSRB)

•Securities and Exchange Commission (SEC)

•HR 529

VGFOA – June 8, 2011 40

9001 Arboretum ParkwayRichmond, Virginia 23236Toll Free:1-888-567-0540On the web:Virginia529.com