Embed Size (px)

Citation preview

Presentation to the Standing Presentation to the Standing Committee on FinanceCommittee on Finance

Annual Report Annual Report 20092009Bank Supervision DepartmentBank Supervision Department

Presentation to the Standing Presentation to the Standing Committee on FinanceCommittee on Finance

Annual Report Annual Report 20092009Bank Supervision DepartmentBank Supervision Department

Errol Kruger Errol Kruger

Registrar of BanksRegistrar of Banks

1 September 20101 September 2010

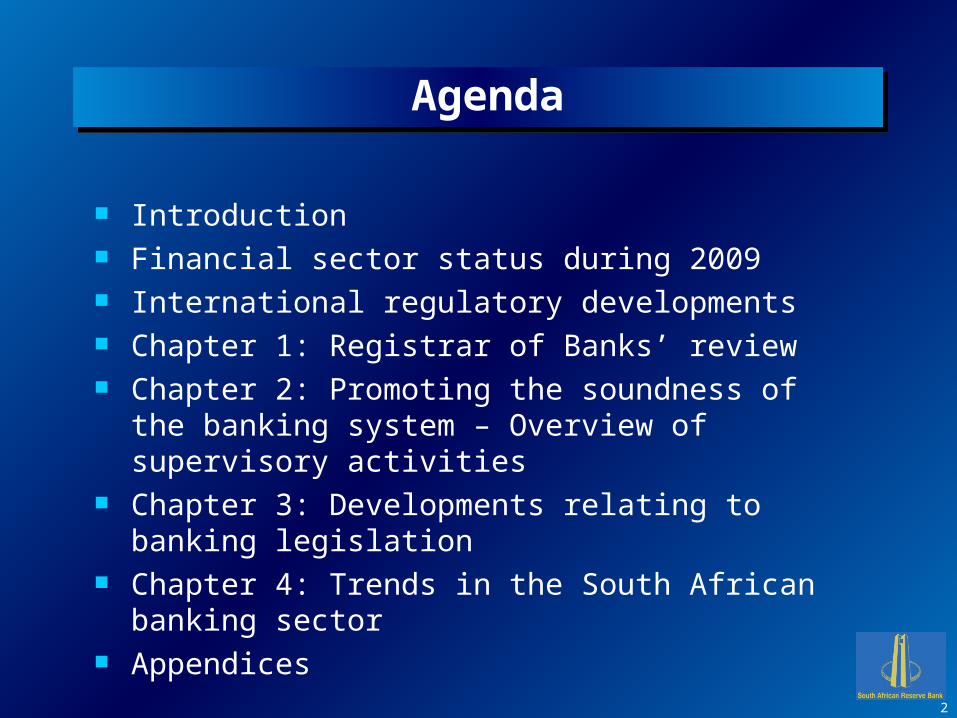

AgendaAgenda

Introduction Financial sector status during 2009 International regulatory developments Chapter 1: Registrar of Banks’ review Chapter 2: Promoting the soundness of the banking

system – Overview of supervisory activities Chapter 3: Developments relating to banking

legislation Chapter 4: Trends in the South African banking

sector Appendices

2

IntroductionIntroduction

The Bank Supervision Department (BSD) executes the functions assigned to the Registrar of Banks in terms of the Banks Act, 1990 and its mission is:

“To promote the soundness of the banking system through the effective and efficient application of international regulatory and

supervisory standards.”

3

4

BSD’s business philosophy :

– Market principles underlie all our activities and decisions

– We strive to act with professionalism, integrity, credibility and impartiality at all times

– Single point of entry – relationship manager, assisted by a team with diverse competencies

– Risk-based supervisory approach – objective is to add value

– Emphasis on empowering staff, professional service delivery and ethical behaviour

– Mutual trust between the Department and all other key players – regular open communication

Introduction (cont.)Introduction (cont.)

5

BSD’s supervisory framework:

– Revised supervisory framework, incorporating Basel II, implemented w.e.f. 1 January 2008

– Revised framework, formally known as the ‘supervisory review and evaluation process’ (SREP), based on:

• Risk-based supervision

• Matrix structure: relationship team assisted by specialist teams with diverse competencies

– Legal framework for regulation and supervision of banks comprise three tiers:

• Banks Act, 1990 (Act No. 94 of 1990)

• Regulations relating to Banks

• Directives, Banks Act circulars and guidance notes

Introduction (cont.)Introduction (cont.)

6

SREP consists of the following steps:

Introduction (cont.)Introduction (cont.)

7

Introduction (cont.)Introduction (cont.) BSD’s organisational structure:

BSD’s Annual Report 2009

– Annual Report for the calendar year ended 31 December 2009 issued in terms of section 10 of the Banks Act, 1990 (Act No. 94 of 1990) and section 8 of the Mutual Banks Act, 1993 (Act No. 124 of 1993).

– The report presents an overview of the objectives and activities of BSD, with particular reference to the period 1 January 2009 to 31 December 2009.

8

Introduction (cont.)Introduction (cont.)

Financial sector status during 2009Financial sector status during 2009

During 2009 the banking sector continued to experience a challenging operating environment:

– Cyclical downturn in domestic economic conditions.

– Aftermath of the 2007/08 international financial market crisis.

– Consumer spending remained subdued.

– Level of impaired advances in existing asset portfolios of banks continued to increase.

However, notwithstanding these difficult circumstances, the banking system remained stable and profitable, and capital levels were adequate throughout 2009.

9

International regulatory developmentsInternational regulatory developments

International regulatory/supervisory standard-setting bodies (e.g.: the Financial Stability Board & the Basel Committee on Banking Supervision), continued their respective processes of developing/issuing guidance and standards to strengthen the resilience of the financial sector in general and the banking sector in particular.

Key Basel Committee press releases:– 13 July 2009 re. (1) enhancements to the Basel II framework; (2)

revisions to the Basel II market risk framework; and (3) guidelines for computing capital for incremental risk in the trading book.

– 7 September 2009 re. comprehensive response to the global banking crisis.

– 17 December 2009 re. consultative proposals to strengthen the resilience of the banking sector and introducing minimum liquidity ratios.

10

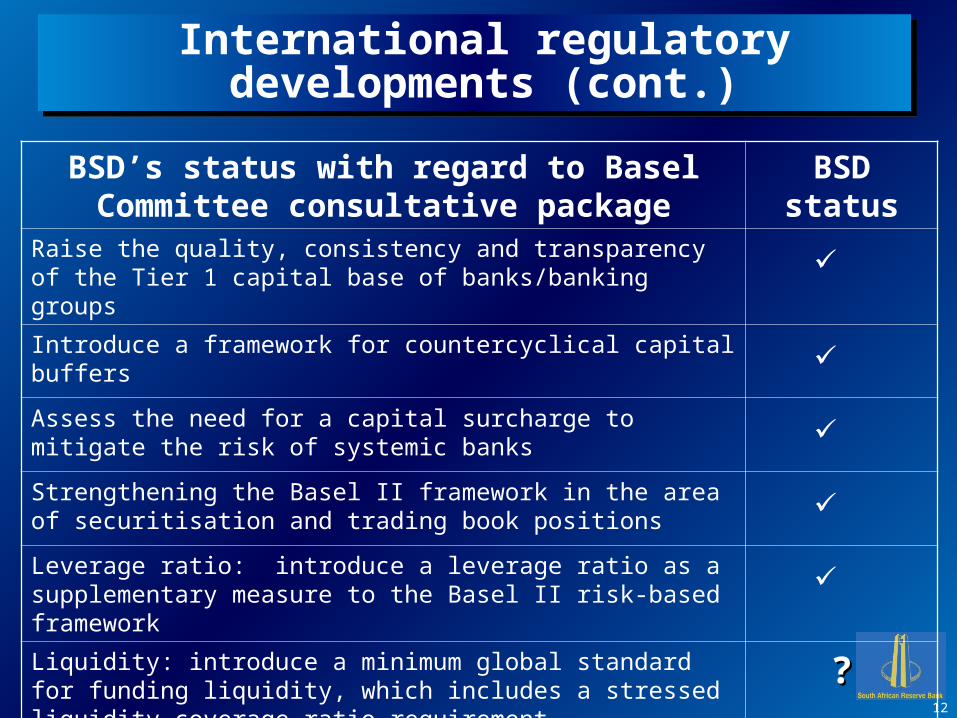

17 December 2009 announcement covered the following areas:

– Raising the quality, consistency and transparency of banks’ Tier 1 capital base

– Introducing a series of measures to promote the build-up of capital buffers in good times (i.e. a countercyclical capital framework)

– Strengthening the risk coverage of the capital framework (e.g. capital requirements for counterparty credit risk arising from derivatives)

– Introducing a leverage ratio as a supplementary measure to the Basel II risk-based framework

– Introduce a minimum liquidity standard for internationally active banks (e.g. liquidity coverage ratio and a longer-term structural liquidity ratio)

BSD, as always, closely monitored and considered developments on the international regulatory/supervisory fronts in an ongoing effort to promote the soundness of the domestic banking sector through the effective and efficient application of international regulatory and supervisory standards.

11

International regulatory developments (cont.)

International regulatory developments (cont.)

12

BSD’s status with regard to Basel Committee consultative package

BSD status

Raise the quality, consistency and transparency of the Tier 1 capital base of banks/banking groups

Introduce a framework for countercyclical capital buffers Assess the need for a capital surcharge to mitigate the risk of systemic banks

Strengthening the Basel II framework in the area of securitisation and trading book positions

Leverage ratio: introduce a leverage ratio as a supplementary measure to the Basel II risk-based framework

Liquidity: introduce a minimum global standard for funding liquidity, which includes a stressed liquidity coverage ratio requirement

??

International regulatory developments (cont.)

International regulatory developments (cont.)

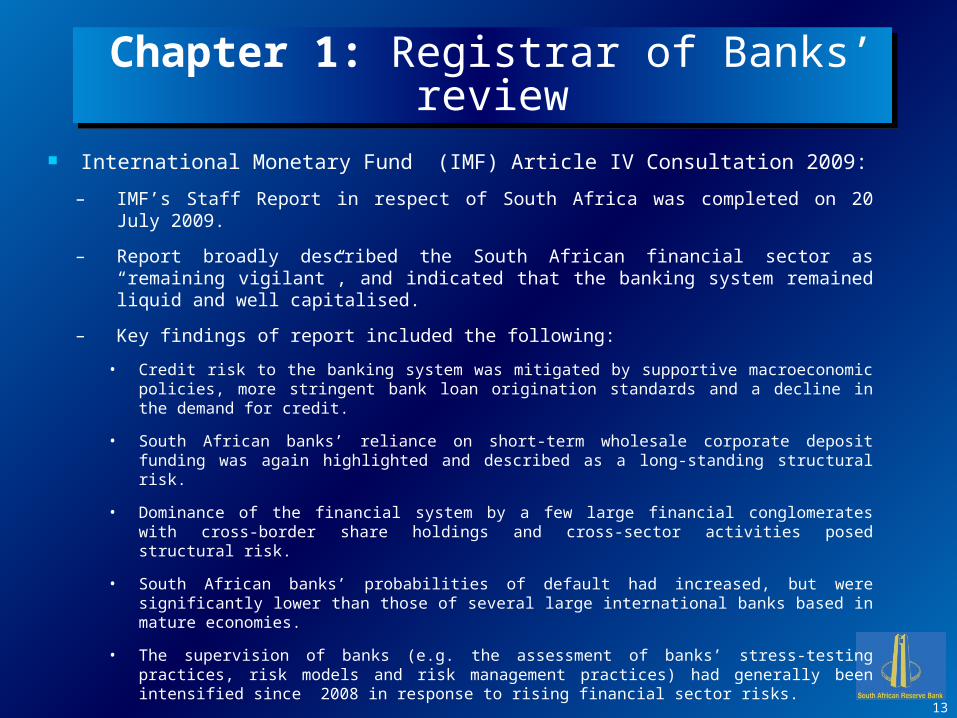

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

International Monetary Fund (IMF) Article IV Consultation 2009:

– IMF’s Staff Report in respect of South Africa was completed on 20 July 2009.

– Report broadly described the South African financial sector as “remaining vigilant”, and indicated that the banking system remained liquid and well capitalised.

– Key findings of report included the following:

• Credit risk to the banking system was mitigated by supportive macroeconomic policies, more stringent bank loan origination standards and a decline in the demand for credit.

• South African banks’ reliance on short-term wholesale corporate deposit funding was again highlighted and described as a long-standing structural risk.

• Dominance of the financial system by a few large financial conglomerates with cross-border share holdings and cross-sector activities posed structural risk.

• South African banks’ probabilities of default had increased, but were significantly lower than those of several large international banks based in mature economies.

• The supervision of banks (e.g. the assessment of banks’ stress-testing practices, risk models and risk management practices) had generally been intensified since 2008 in response to rising financial sector risks.

13

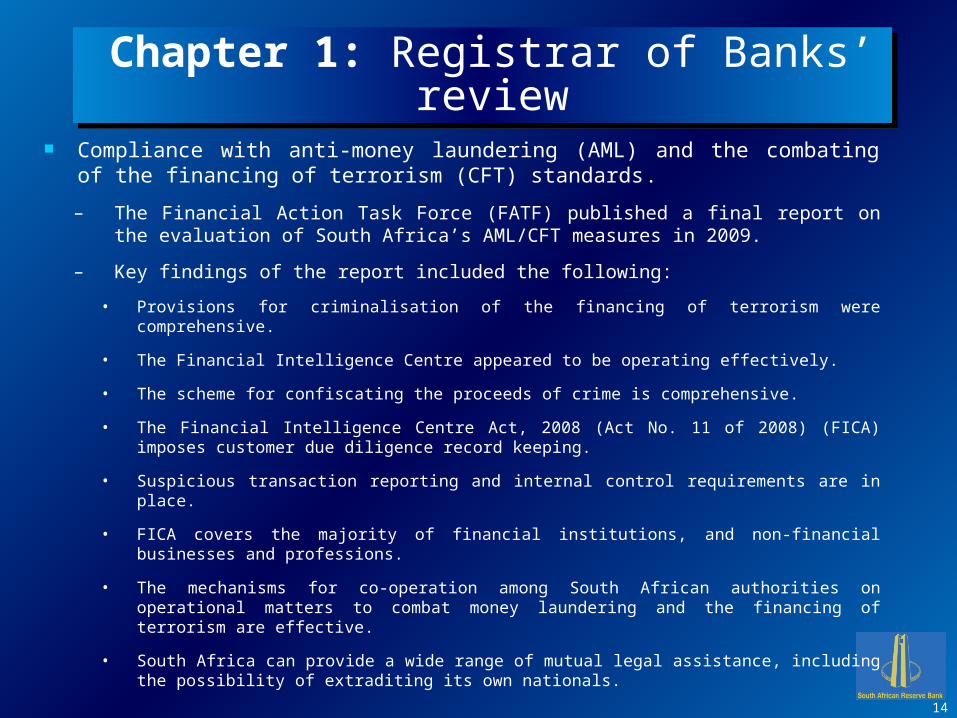

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Compliance with anti-money laundering (AML) and the combating of the financing of terrorism (CFT) standards.

– The Financial Action Task Force (FATF) published a final report on the evaluation of South Africa’s AML/CFT measures in 2009.

– Key findings of the report included the following:

• Provisions for criminalisation of the financing of terrorism were comprehensive.

• The Financial Intelligence Centre appeared to be operating effectively.

• The scheme for confiscating the proceeds of crime is comprehensive.

• The Financial Intelligence Centre Act, 2008 (Act No. 11 of 2008) (FICA) imposes customer due diligence record keeping.

• Suspicious transaction reporting and internal control requirements are in place.

• FICA covers the majority of financial institutions, and non-financial businesses and professions.

• The mechanisms for co-operation among South African authorities on operational matters to combat money laundering and the financing of terrorism are effective.

• South Africa can provide a wide range of mutual legal assistance, including the possibility of extraditing its own nationals.

14

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Financial Stability Institute: High-level Meeting on Recent Developments in Financial Markets and Supervisory Responses.

– The FSI, jointly with BSD hosted a high-level meeting in January 2009 focused on developments in financial markets and supervisory responses thereto.

– The meeting was attended by the heads of supervisory authorities from various Africa countries and representatives of Basel Committee member countries and the private sector.

– Topics covered at the meeting included, inter alia:

• A high-level synopsis of the United States (US) Federal Reserve System’s response to the financial market crisis.

• A high-level overview of key strategic responses of the Basel Committee to developments in financial markets subsequent to the international financial market crisis.

• The role of credit-rating agencies (CRAs) and the regulatory approach towards CRAs.

• The similarities and differences between International Financial Reporting Standards and prudential regulation.

• Challenges for supervisors with regard to the implementation of Basel II.

• The impact of the financial market crisis from a South African perspective.

15

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Incentive schemes of banking institutions.

– BSD conducted a thematic review of all South African banks’ incentive schemes during 2008 and found that banking organisations generally had sound principles embedded in their incentive schemes, including:

• Alignment with the objectives of the organisation as a whole.

• Business unit bonus pools determined by overall performance of the organisation.

• Consideration of risk management in the performance assessment process.

• Incorporation of team and business unit performance in individual assessments.

– In April 2009 the FSB issued FSB Principles for Sound Compensation Practices (the Compensation Principles) which should be implemented by banking institutions and be reinforced through the supervisory process at national level.

– In September 2009 the FSB published FSB Principles for Sound Compensation Practices: Implementation Standards (the Compensation Standards) in addition to its Compensation Principles.

– BSD commenced participation in a thematic review conducted by the FSB on the implementation of the Compensation Principles and Compensation Standards, which will form part of the areas of focus during 2010. 16

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

The international financial market turmoil: Responses by standard-setting bodies.

– Fundamental weaknesses in international financial markets were revealed by the international financial market crisis that started in 2007.

– In response, international standard-setting bodies such as the Group of Twenty Finance Ministers and Central Bank Governors (G-20), the FSB and the Basel Committee announced various initiatives, strategies, and new or amended requirements and standards covering a wide range of areas.

– Key aims of the broader programme are to introduce new standards to, among other things:

• Promote the build-up of capital buffers that can be drawn down in periods of stress.

• Strengthen the quality of bank capital.

• Introduce a leverage ratio as a backstop to the Basel II risk-sensitive measures.

• Introduce measures to mitigate any excess cyclicality of the minimum capital requirement.

• Promote a more forward-looking approach to provisioning.

17

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

The international financial market turmoil: Responses by standard-setting bodies (cont.).

– On 25 September 2009, following the Pittsburgh Summit, the G-20 issued a leaders’ statement in which they agreed to, among other things:

• Act together to raise capital standards, implement international compensation standards and create tools to hold large global institutions to account for the risks they took.

• Strengthen prudential oversight, improving risk management, strengthening transparency, promoting market integrity, establishing supervisory colleges and reinforcing international co-operation.

• Enhance and expand the scope of regulation and oversight, with tougher regulation of OTC derivatives, securitisation markets, CRAs and hedge funds.

• Raise standards together so that national authorities implement global standards consistently.

• Conduct robust and transparent stress tests as needed.

• Strike an adequate balance between macroprudential and microprudential regulation to control risks.

18

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

The international financial market turmoil: Responses by standard-setting bodies (cont.).

– In December 2009 the Basel Committee issued for consultation, a package of proposals to further strengthen global capital and liquidity regulations.

– These proposals along with the measures taken by the Basel Committee in July 2009 to strengthen the Basel II framework, form part of the Basel Committee’s comprehensive response to address the lessons learnt from the crisis related to the regulation, supervision and risk management of global banks.

– The Basel Committee initiated a comprehensive impact assessment of the capital and liquidity standards proposed in the consultative documents to determine the final proposals and their calibration.

– It is expected that the fully calibrated set of standards will be developed by the end of 2010 to be phased in as financial conditions improve and the economic recovery is assured, with a view to implementation by the end of 2012

19

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Participation in international regulatory or supervisory forums.

– BSD is represented on, and contributes to, various international regulatory and supervisory forums, including the following:

• The Southern African Development Community (SADC) Subcommittee of Banking Supervisors (SSBS), a subcommittee of the Committee of Central Bank Governors (CCBG) in SADC.

• The Validation Subgroup (SIGV) of the Standards Implementation Group (SIG), an expert subcommittee of the Basel Committee.

• The Standards Implementation Group Operational Risk, a permanent working group of the SIG.

• The Trading Book Group, an expert subcommittee of the Basel Committee.

• A work stream of the Basel Committee focusing on microfinance .

• The Basel II Capital Monitoring Group.

20

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Skills development.

– During 2009 BSD spent R887 000 on the training of approximately 107 employees.

– Various training interventions were arranged, such as technical and managerial courses, risk management seminars and supervisory workshops.

– The main purpose of the training was to:

• Assist staff in implementing sound supervisory standards and practices.

• Keep staff abreast of the latest information on market products, practices and techniques.

• Keep staff abreast of the latest developments in international financial markets and supervisory responses to the financial market crisis.

• Ensure that staff were equipped with the necessary tools and techniques in order to meet their everyday supervisory tasks.

21

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Regional co-operation.

– BSD continued to be involved at a regional level in providing input and training to regulatory counterparts in neighbouring Africa countries.

– These interactions included the following:

• August 2009 – BSD met with senior banking supervision representatives of the Bank of Namibia to share the Department’s experience with regard to various supervisory matters.

• September 2009 – BSD provided training/lectured at a workshop on risk-based supervision under the auspices of the Macroeconomic and Financial Management Institute of Eastern and Southern Africa (MEFMI) in Tanzania.

• October 2009 – BSD provided training/lectured at a regional seminar on consolidated supervision, jointly hosted by the FSI and the MEFMI, in Lusaka, Zambia.

• October 2009 – BSD was requested by the IMF, through its support for the development of appropriate regulatory practices, to assist with the implementation of regulations for market risk in Kenya.

22

Chapter 1: Registrar of Banks’ reviewChapter 1: Registrar of Banks’ review

Issues to receive particular attention during 2010 include, inter alia:

– Ongoing review and amendment of the banking legislative/regulatory framework in South Africa.

– Continued refinement of BSD’s supervisory review & evaluation processes.

– Continued participation in the various international forums to formulate further internationally agreed requirements to strengthen the resilience of the banking sector.

– Further development and implementation of BSD’s common scenario stress-testing methodology and process in respect of banks’ capital adequacy and liquidity.

– Continued performance of thematic reviews focusing on backtesting of credit risk models.

– Ongoing focused reviews of banks making use of advanced approaches to calculate credit risk, market risk and operational risk capital requirements.

– Continued monitoring of banks’ compliance with AML/CFT legislation.

– Continued investigation of illegal deposit-taking by unregistered institutions and persons, and participation in consumer education initiatives.

23

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Credit risk.

– The credit risk-related work carried out by BSD during 2009 covered the following:

• Quantitative analysis – including a credit risk survey and an assessment of the impact of an economic down-turn on banks’ capital relative to their level of credit risk exposure.

• Review of IRB self-assessment templates submitted by banks to assess their compliance with the minimum IRB requirements as prescribed in the Regulations relating to Banks.

• Focused reviews of standardised approach (SA) requirements for credit risk to assess the degree of compliance by each bank with the SA requirements prescribed in the Regulations relating to Banks.

• Processing of applications by banks to implement new or revised models and rating systems.

• Reassessment of eligible external credit assessment institutions (credit rating agencies).

24

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Market risk.

– The market risk-related work carried out by BSD during 2009 covered the following:

• Market risk reviews, specifically on banks with approval to use the internal models approach (IMA) for regulatory reporting.

• A review of the trading activities of one bank was conducted.

• Liquidity risk management formed the basis of BSD’s annual meeting with the boards of directors of banks during 2009.

• BSD initiated a thematic review of the asset and liability management process at banks, examining the durability of liquidity risk management in the current turbulent financial climate and in the future under increasingly stressed circumstances.

– No new applications for using the IMA were received or processed during 2009.

25

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Operational risk.

– The operational risk-related work carried out by BSD during 2009 covered the following:

• Operational risk reviews that focused on changes in the business environment and Operational risk reviews that focused on changes in the business environment and banks’ response to it from an operational risk perspective.banks’ response to it from an operational risk perspective.

• A detailed review of the management information reports or “dashboards” used for A detailed review of the management information reports or “dashboards” used for operational risk management. operational risk management.

• A detailed review of the scenario approval, governance process and specific A detailed review of the scenario approval, governance process and specific scenarios used by banks in their application of the advanced measurement scenarios used by banks in their application of the advanced measurement approach (AMA).approach (AMA).

• Processing of a new application received from one of the registered banks to use AMA.

• Based on the results of an international operational loss data collection exercise that was performed, BSD provided participating South African banks with a customised analysis comparing their data with industry data at both the international, and where possible, regional or national levels.

26

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Internal capital adequacy assessment process (ICAAP).

– The adequacy of a bank’s and banking group’s capital needs to be assessed by both the particular bank and the Department.

– Various thematic ICAAP reviews of larger banks and some smaller banks were performed during 2009

– The process followed to assess a bank’s ICAAP can be illustrated as follows:

27

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Developments in respect of Pillar 3 Disclosure.

– During 2009 BSD determined and performed an analysis of the level of disclosure by banks in South Africa.

– Banks that were found not to be disclosing appropriately and where the frequency of disclosure was not in accordance with the provisions of regulation 43 of the Regulations relating to Banks were identified and formally informed.

– A template was developed in order to analyse banks’ Pillar 3 disclosures, i.e., to benchmark the Pillar 3 disclosure requirements of banks against the requirements of the Regulations relating to Banks and best practice applied by the industry.

– The benchmarking process will be a focus area in 2010.

28

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Stress testing.

– Stress testing is defined by the Basel Committee as “a risk management technique that is used to evaluate the potential effects of a specific event and/or movement in a set of financial variables on an institution’s financial condition”.

– Stress testing is a key tool used by the regulator in understanding the appropriate level of regulatory capital to ensure that banks remain solvent during difficult times.

– Stress testing is an important input to the capital-adequacy process and decisions concerning the adequacy of capital buffer requirements.

– BSD’s stress-testing framework consists primarily of two main work streams:

• The first focusing on the stress-testing frameworks of banks; and

• The second on common scenario stress testing performed by BSD (using the information obtained from the first work stream).

– BSD performed various thematic stress-testing reviews during 2009 and findings were communicated to the relevant banks.

29

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Chapter 2: Promoting the soundness of the banking system: Overview of supervisory activities

Developments in consolidated supervision.

– BSD proactively took the following actions to further improve the consolidated supervision of banking groups :

• Regular supervisory meetings between the Department and the Financial Services Board.

• A policy decision was taken to allow only the acquisition or establishment of cross-border banking operations (inwards and outwards) in instances where a memorandum of understanding with the cross-border banking supervisor had been concluded.

• BSD is planning to host a supervisory college in 2010 with those African supervisors in whose countries South African banking groups have a presence.

• To improve the supervision of banking groups on a consolidated basis, BSD recommended to one of the large banking groups to undergo a restructure.

30

Chapter 3: Developments relating to banking legislation

Chapter 3: Developments relating to banking legislation

The Banks Act, 1990 and the Regulations relating to Banks.

– A key responsibility of BSD is to ensure that the legal framework for the regulation and supervision of banks and banking groups in South Africa remains relevant and current.

Initiatives monitored and developments considered by BSD include the following:

– International developments relating to the global financial crises (e.g. the G-20 discussions and publications and directives issued by the Basel Committee and the FSB).

– The New Companies Act, 2008.

– Board of review findings.

– King III.

– Flowing from these initiatives and developments, extensive proposed amendments to the banking legislative and regulatory framework have been issued for public comment.

31

Chapter 3: Developments relating to banking legislation

Chapter 3: Developments relating to banking legislation

Illegal deposit-taking.

– One of the auxiliary functions of BSD is to inspect and investigate persons and institutions suspected of taking deposits from the general public in contravention of the provisions of the Banks Act, 1990.

– The following graph depicts the investigations performed relating to illegal deposit taking during the past five years:

32

Chapter 3: Developments relating to banking legislation

Chapter 3: Developments relating to banking legislation

Update regarding co-operative banks.

– Co-operative Banks Act, 2007 (Act No. 40 of 2007) (CBA) was assented to by the President on 18 February 2008 and published as Government Notice No. 737 in Government Gazette No. 30802 on 22 February 2008.

– The CBA seeks to create a development strategy and a regulatory environment for deposit-taking financial co-operative institutions.

33

Chapter 3: Developments relating to banking legislation

Chapter 3: Developments relating to banking legislation

Developments regarding Postbank.

– Operates under an exclusion provided for in section 2(vii) of the Banks Act, 1990.

– It’s the Government’s intention to restructure its banking interest in Postbank in a three-phased process:

• Phase I – Postbank would operate as a profit centre providing greater autonomy within the existing divisional structure.

• Phase II – Postbank would operate as a fully owned subsidiary of the SA Post Office or Government, providing a complete range of payment and funds transfer services, and an expanded deposit service range.

• Phase III – Postbank would operate as a savings bank that is an autonomous company owned by the SA Post Office or government and operate as a fully fledged savings bank extending lending facilities.

34

Chapter 3: Developments relating to banking legislation

Chapter 3: Developments relating to banking legislation

Decision of the Board of Review in the review of the decision of the Registrar in respect of an application for authorisation to establish a bank.

– In 2006 BSD received an application for authorisation to establish a bank which was refused on the grounds that the Applicant could not satisfy many of the prescribed requirements.

– In February 2008 the decision was taken on review to the Board of Review (established in terms of section 9 of the Banks Act, 1990) which the Board dismissed.

– In August 2009 the Applicant brought an application in the High Court (Pretoria) for the review of both the Registrar’s and the Board’s decisions.

– The Applicant’s application to the High Court to have the Registrar’s decision set aside by the Board was also dismissed with costs.

35

Chapter 4: Trends in the South African banking sector

Chapter 4: Trends in the South African banking sector

The following slides present some of the key trends in the South African banking sector that are predicated on risk-based information submitted by banks during 2009 and updated for the first six months of 2010.

36

Overview of the banking sector Overview of the banking sector

June 2010 June 2010

Overview of the banking sector Overview of the banking sector

June 2010 June 2010

37

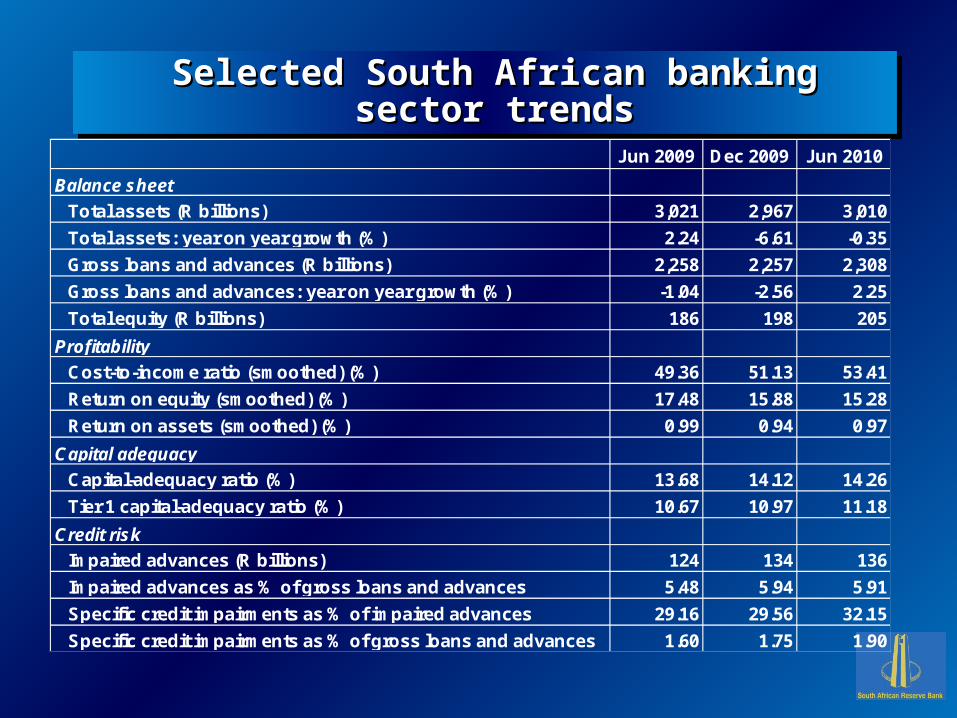

Selected South African banking sector trendsSelected South African banking sector trendsSelected South African banking sector trendsSelected South African banking sector trends

Jun 2009 Dec 2009 Jun 2010

Balance sheet

Total assets (R billions) 3,021 2,967 3,010

Total assets: year on year growth (%) 2.24 -6.61 -0.35

Gross loans and advances (R billions) 2,258 2,257 2,308

Gross loans and advances: year on year growth (%) -1.04 -2.56 2.25

Total equity (R billions) 186 198 205

Profitability

Cost-to-income ratio (smoothed) (%) 49.36 51.13 53.41

Return on equity (smoothed) (%) 17.48 15.88 15.28

Return on assets (smoothed) (%) 0.99 0.94 0.97

Capital adequacy

Capital-adequacy ratio (%) 13.68 14.12 14.26

Tier 1 capital-adequacy ratio (%) 10.67 10.97 11.18

Credit risk

Impaired advances (R billions) 124 134 136

Impaired advances as % of gross loans and advances 5.48 5.94 5.91

Specific credit impairments as % of impaired advances 29.16 29.56 32.15

Specific credit impairments as % of gross loans and advances 1.60 1.75 1.90

Distribution of banking-sector assetsDistribution of banking-sector assetsDistribution of banking-sector assetsDistribution of banking-sector assets

Jun 2008 Jun 2009 Jun 2010Jun 2010

Year on year growth

(Rbn) (Rbn) (Rbn) (%)

5 largest banks 2,647 2,735 2,724 -0.40

Standard Bank 752 808 767 -5.03

Absa 673 692 659 -4.86

FirstRand Bank 567 561 571 1.86

Nedbank 485 500 533 6.65

Investec 170 174 194 11.35

Other 307 285 286 0.10

Total banks 2,955 3,021 3,010 -0.35

Balance-sheetBalance-sheetBalance-sheetBalance-sheet

-10

-5

0

5

10

15

20

25

30

35

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Total assets Gross loans and advances

Growth in total assets (rhs) Growth in gross loans and advances (rhs)

Total assets, gross loans and advances and Total assets, gross loans and advances and respective growth ratesrespective growth rates

Total assets, gross loans and advances and Total assets, gross loans and advances and respective growth ratesrespective growth rates

Per cent R billions

2,2%

R3 010 bn

R2 308 bn

-1,0%

2,3%

-0,4%

28,0%

17,9%

0

10

20

30

40

50

60

70

80

90

100

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Loans and advances (net of impairments) Derivatives

Investment and trading securities Short-term negotiable securities

Other Cash and balances with the central bank

Composition of total assetsComposition of total assets (R3 010 bn)(R3 010 bn)Composition of total assetsComposition of total assets (R3 010 bn)(R3 010 bn)

Per cent

74,873,1

7,311,8

6,95.2

76,1

10,7

4.4

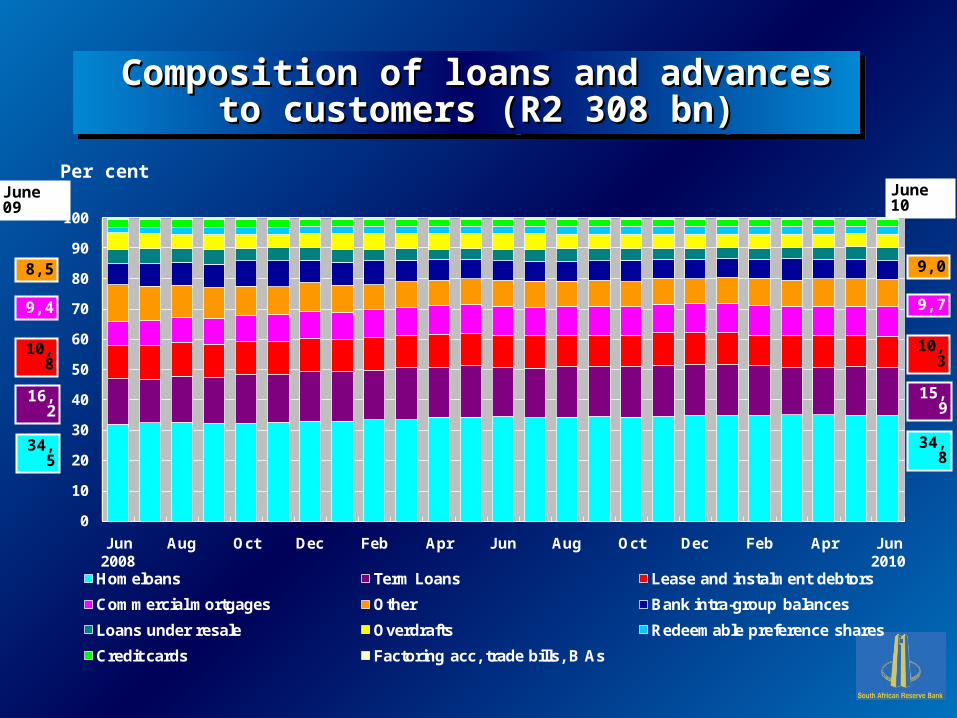

Composition of loans and advances to Composition of loans and advances to customers (R2 308 bn)customers (R2 308 bn)

Composition of loans and advances to Composition of loans and advances to customers (R2 308 bn)customers (R2 308 bn)

Per cent June 09 June 10

34,8

10,3

15,9

9,7

9,0

34,5

10,8

16,2

9,4

8,5

0

10

20

30

40

50

60

70

80

90

100

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Homeloans Term Loans Lease and instalment debtors

Commercial mortgages Other Bank intra-group balances

Loans under resale Overdrafts Redeemable preference shares

Credit cards Factoring acc, trade bills, B As

0

10

20

30

40

50

60

70

80

90

100

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Deposits Derivative and other trading liabilities Term debt instruments Other

Composition of liabilities (R2 805 bn)Composition of liabilities (R2 805 bn)Composition of liabilities (R2 805 bn)Composition of liabilities (R2 805 bn)

Per cent

83,1

12,5

87,582,2

12,7 7,7

0

10

20

30

40

50

60

70

80

90

100

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Fixed and notice deposits Call deposits

Current accounts Negotiable certificates of deposit

Other deposits and loan accounts Savings deposits

Repos

Composition of deposits Composition of deposits (R2 454 bn)(R2 454 bn)Composition of deposits Composition of deposits (R2 454 bn)(R2 454 bn)

Per cent

24,0

22,6

17,4

17,1

28,2

17,2

18,2

16,4

23,9

22,0

14,7

18,4

0

10

20

30

40

50

60

70

80

90

100

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Corporate Customers Retail Customers

Banks Security Firms

Public sector and local authorities Other

Sovereigns

Sources of deposits (as a percentage of total Sources of deposits (as a percentage of total deposits) deposits) (R2 454 bn)(R2 454 bn)

Sources of deposits (as a percentage of total Sources of deposits (as a percentage of total deposits) deposits) (R2 454 bn)(R2 454 bn)

Per cent

42,0

13,4

22,0

13,5

21,1

42,341,4

13,7

20,9

ProfitabilityProfitabilityProfitabilityProfitability

0.0

0.5

1.0

1.5

2.0

2.5

0

5

10

15

20

25

Jun 2009

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2010

Return on equity Return on assets (rhs)

Profitability ratios (smoothed)Profitability ratios (smoothed)

17,5%

0,99%

15,3%

0,97%

Per cent Per cent

0

10

20

30

40

50

60

Jun 2009

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 2010

Cost-to-income ratio (smoothed)Cost-to-income ratio (smoothed)

Per cent

53,4%49,4%

Capital adequacyCapital adequacyCapital adequacyCapital adequacy

0

50

100

150

200

250

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Share capital Retained earnings

Other reserves Minority ordinary shareholders' equity

Preference shareholders' equity

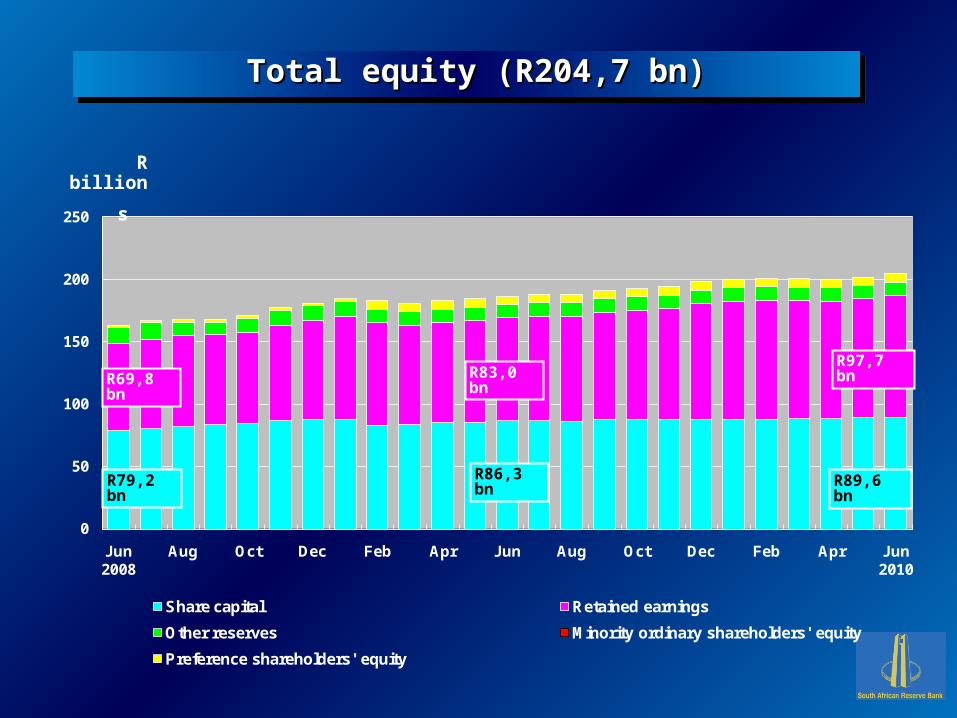

Total equityTotal equity (R204,7 bn)(R204,7 bn)Total equityTotal equity (R204,7 bn)(R204,7 bn)

R billions

R86,3 bn R89,6 bn

R83,0 bnR97,7 bn

R79,2 bn

R69,8 bn

0

5

10

15

20

25

30

35

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Financial leverage multiple

Financial leverage multipleFinancial leverage multipleFinancial leverage multipleFinancial leverage multiple

Times

17,0

15,4

18,4

0

2

4

6

8

10

12

14

16

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Capital-adequacy ratio Tier 1 capital-adequacy ratio

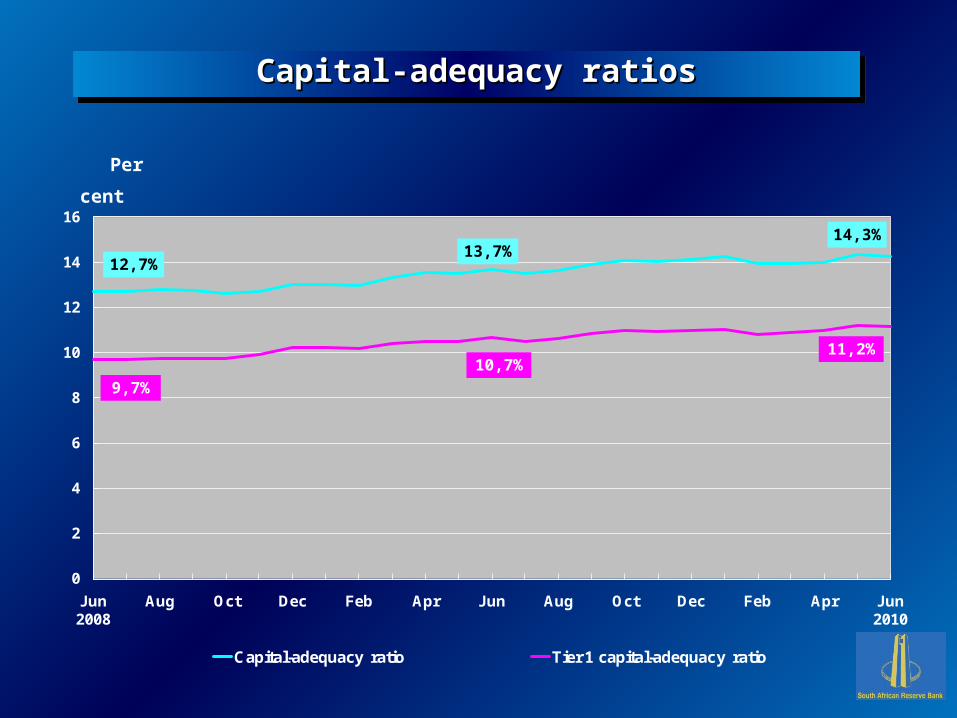

Capital-adequacy ratiosCapital-adequacy ratiosCapital-adequacy ratiosCapital-adequacy ratios

Per cent

13,7%14,3%

11,2%

12,7%

9,7%

10,7%

0

50

100

150

200

250

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Total Primary capital and reserves Secondary capital and reserves Tertiary capital

Composition of qualifying regulatory capital and Composition of qualifying regulatory capital and reserve funds (R225,6 bn)reserve funds (R225,6 bn)

Composition of qualifying regulatory capital and Composition of qualifying regulatory capital and reserve funds (R225,6 bn)reserve funds (R225,6 bn)

R billions

R211,6 bn

R165,0 bn

R147,6 bn

R225,6 bn

R193,5 bn

R176,9 bn

R46,3 bnR45,3 bn R48,4 bn

0

10

20

30

40

50

60

70

80

90

100

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

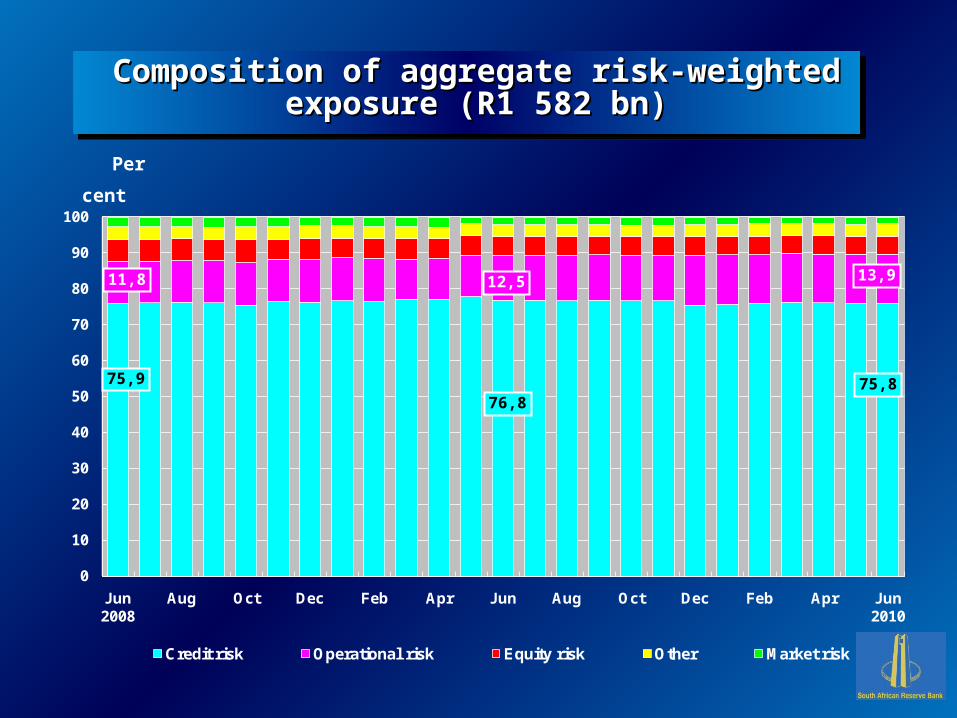

Credit risk Operational risk Equity risk Other Market risk

Composition of aggregate risk-weighted Composition of aggregate risk-weighted exposure (R1 582 bn)exposure (R1 582 bn)

Composition of aggregate risk-weighted Composition of aggregate risk-weighted exposure (R1 582 bn)exposure (R1 582 bn)

Per cent

75,8

13,9

76,8

12,5

75,9

11,8

Liquidity riskLiquidity riskLiquidity riskLiquidity risk

0

25

50

75

100

125

150

175

200

225

250

0

25

50

75

100

125

150

175

200

225

250

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Liquid assets required to be held

Liquid assets held

Liquid assets held to liquid asset requirement (rhs)

Statutory liquid assets (actual versus required)Statutory liquid assets (actual versus required)Statutory liquid assets (actual versus required)Statutory liquid assets (actual versus required)

R billions Per cent

175,7%

119,2%

R225,2 bn

109,2%

R159,1 bn

R133,0 bn

0

10

20

30

40

50

60

70

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

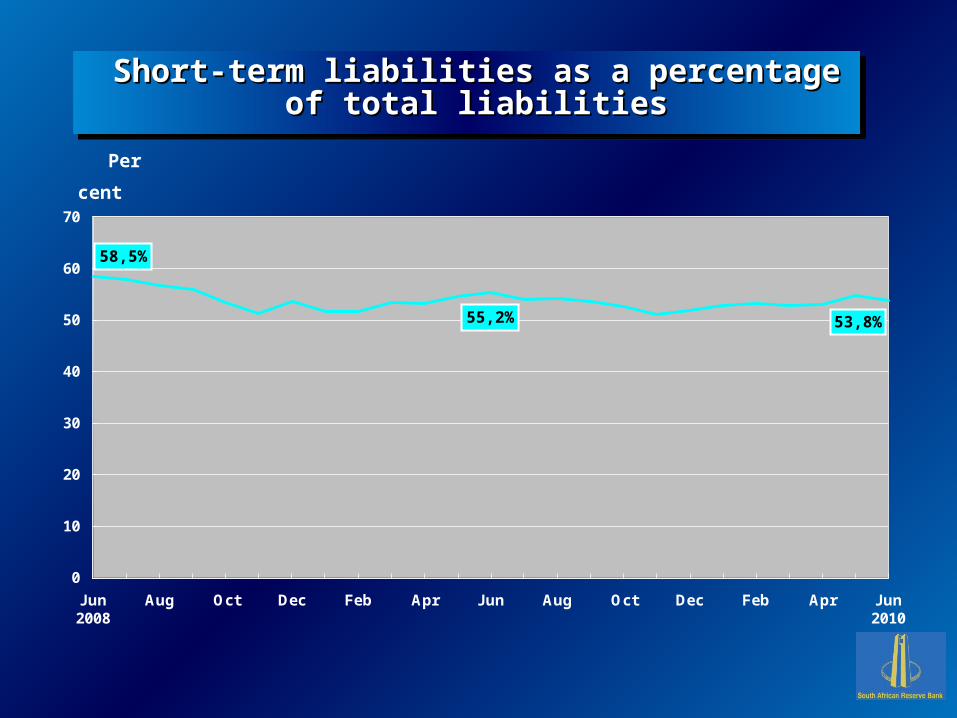

Short-term liabilities as a percentage of total Short-term liabilities as a percentage of total liabilitiesliabilities

Short-term liabilities as a percentage of total Short-term liabilities as a percentage of total liabilitiesliabilities

Per cent

53,8%55,2%

58,5%

Credit riskCredit riskCredit riskCredit risk

0

1

2

3

4

5

6

7

8

0

20

40

60

80

100

120

140

160

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Impaired advances Impaired advances to gross loans and advances (rhs)

Impaired advances to gross loans and advances Impaired advances to gross loans and advances (R136,4 bn)(R136,4 bn)

Impaired advances to gross loans and advances Impaired advances to gross loans and advances (R136,4 bn)(R136,4 bn)

Per cent R billions

5,91%

R136,4 bn

5,48%

R123,8 bn

2,72%

R62,0 bn

0

5

10

15

20

25

30

35

40

45

50

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Specific credit impairments Portfolio credit impairments

Specific and portfolio credit impairmentsSpecific and portfolio credit impairmentsSpecific and portfolio credit impairmentsSpecific and portfolio credit impairments

R billions

R43,9 bn

R12,1 bn

R21,8 bn

R9,9 bn

R36,1 bn

R12,1 bn

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

5

10

15

20

25

30

35

40

Jun 2008

Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun 2010

Specific credit impairments to impaired advances

Specific credit impairments to gross loans and advances (rhs)

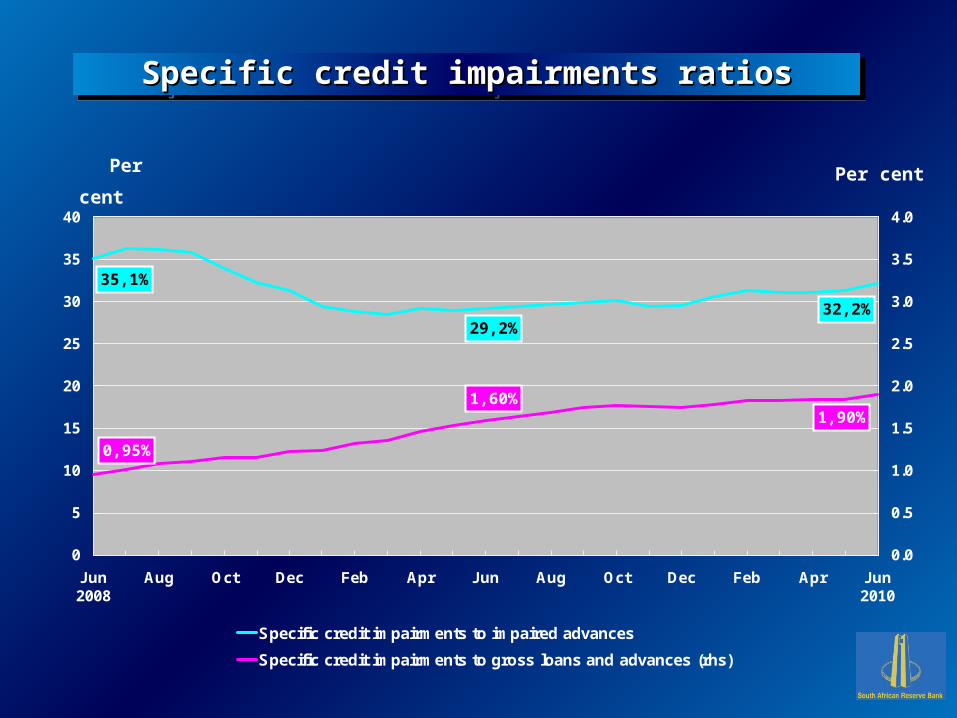

Specific credit impairments ratiosSpecific credit impairments ratios Specific credit impairments ratiosSpecific credit impairments ratios

Per cent Per cent

32,2%

1,90%

35,1%

0,95%

29,2%

1,60%

Summary – June 2010Summary – June 2010Summary – June 2010Summary – June 2010

• Year on year asset growth improved during the second quarter of 2010, but still remained negative, amounting to -0,4% at the end of June 2010 (June 2009: 2,2% and December 2009: -6,6%).

• Growth in retail portfolios still weak and lacking consistency.

• Profitability ratios still compressed, as reflected in ROE and ROA - slight improvement at the end of 1st quarter of 2010. Deteriorating cost-to-income ratio.

• Improved capital adequacy and leverage ratios – compliant with international proposed reforms.

• Ratio of impaired advances to gross loans and advances is not improving , amounting to 5,9% at the end of June 2010 (June 2009: 5,5% and December 2009: 5,9%).

• Overall ….. low growth, particularly on the retail side, lower profitability levels together with sticky impaired advances. In general, activity in banking sector remains subdued.

AppendicesAppendices

Appendices 1 to 5 and 7 to 10 contain useful administrative information pertaining to the banking sector, such as the following:

– Names and details of the registered banks, mutual banks and local branches of foreign banks.

– Details of name changes and cancellation of registration of banks and branches of foreign banks.

– Names of the registered controlling companies.

– Details of foreign banks with approved local representative offices.

– Directives sent to banks.

– Exemptions and exclusions from the application of the Banks Act, 1990.

– Approval of the acquisition or establishment of foreign banking interests in terms of section 52 of the Banks Act, 1990.

– Memorandums of understanding concluded between BSD and foreign supervisors.

Appendix 6 contains 24 tables detailing extensive financial data predicated on risk-based information submitted by banks over a 24-month period ending December 2009).

64

Thank you.Thank you.

65

![JOLES EIENDOM (PTY) LIMITED JOHAN BLOEM KRUGER First ... · 2]and JOHAN BLOEM KRUGER First Respondent REGISTRAR OF DEEDS Second Respondent 3] JUDGMENT: DELIVERED 1 MARCH 2007 4] 5]GRIESEL](https://img.pdfslide.us/doc/110x75/601c8f2ed16cd135284d54dd/joles-eiendom-pty-limited-johan-bloem-kruger-first-2and-johan-bloem-kruger.jpg)