Embed Size (px)

Citation preview

Presentation Title

© 2010 Fox Rothschild

How Much Does Your Retirement Plan Really Cost?

Presented byHarvey M. Katz, Esq.Fox Rothschild LLP

100 Park Ave. 15th FloorNew York, NY 10017

212-878-7976973-650-7656

Presentation Title

© 2010 Fox Rothschild

Overview

Hidden fees cost employers and participants money

Who is legally responsible? Department of Labor Regulations What’s an employer to do? Conclusion

Presentation Title

© 2010 Fox Rothschild

Explicit Fees Charged to Retirement Plans and Sponsors

Recordkeeping Fees Custodian Fees Third Party Administration Fees Plan document filing Set up, conversion costs Annual audit fees Trustee service costs Non-discriminatory testing fees Participant Education fees

Presentation Title

© 2010 Fox Rothschild

Hidden Fees – Brokerage Costs

Whenever the fund manager buys or sells a security, he pays for it which means you pay for it.

Even though fund may pay a lower commission rate, based upon volume trading,

These costs are not included in the Annual expense ratio or the prospectus.

Statement of Additional Information for the fund will contain statement

Presentation Title

© 2010 Fox Rothschild

Asset Management/Fund Expenses

Asset management fee is not the only cost a retirement plan will incur.

Plans must also pay funds expenses, and this is where you’ll find fixed expenses and variable expenses.

Every mutual fund and ETF charges the annual expense ratio. This pays for, the fund’s recurring operating costs, the fund manager’s salary.

Average expense ratio is about 1.5%, although many are more 2%,

The annual expense ratio is actually debited on a daily basis. Contained in the prospectus

Presentation Title

© 2010 Fox Rothschild

Revenue Sharing

Mutual Fund 12b-1 Fees Used to compensate brokers and sales

personnel Shared with recordkeepers, brokers,

consultants and administrators Sharing arrangements are generally

hidden from consumers

Presentation Title

© 2010 Fox Rothschild

Undisclosed and Partially Disclosed Fees

Asset management fee brokerage commission costs 12b-1 fees Investment transfer expenses Other asset based fees and charges Undisclosed/partially disclosed “revenue

sharing” arrangements Termination Charges/ Asset value

adjustments

Presentation Title

© 2010 Fox Rothschild

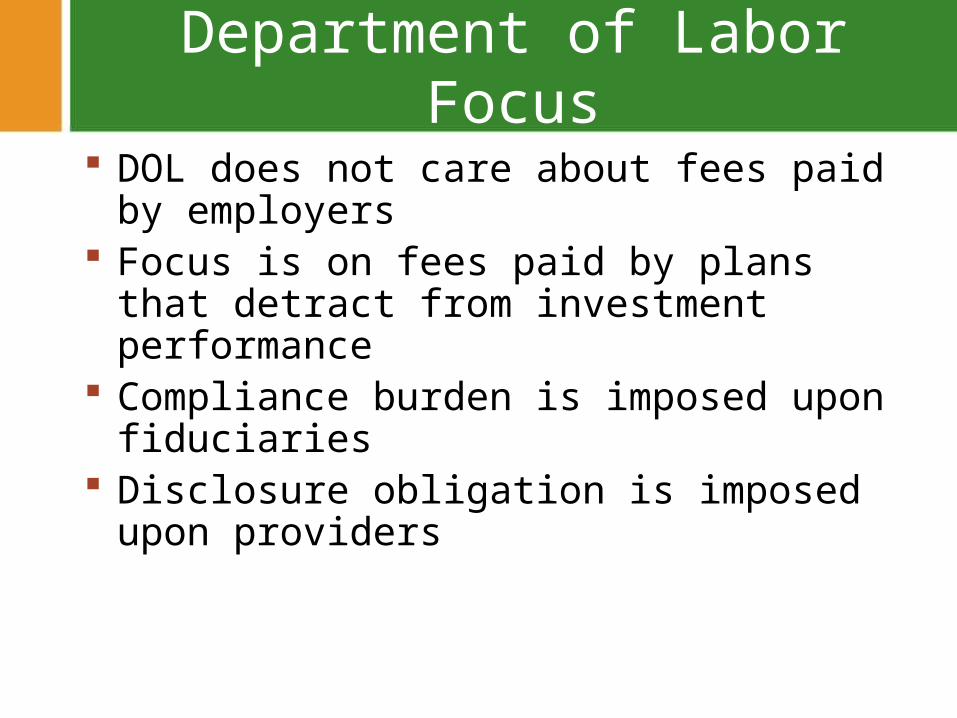

Department of Labor Focus

DOL does not care about fees paid by employers

Focus is on fees paid by plans that detract from investment performance

Compliance burden is imposed upon fiduciaries

Disclosure obligation is imposed upon providers

Presentation Title

© 2010 Fox Rothschild

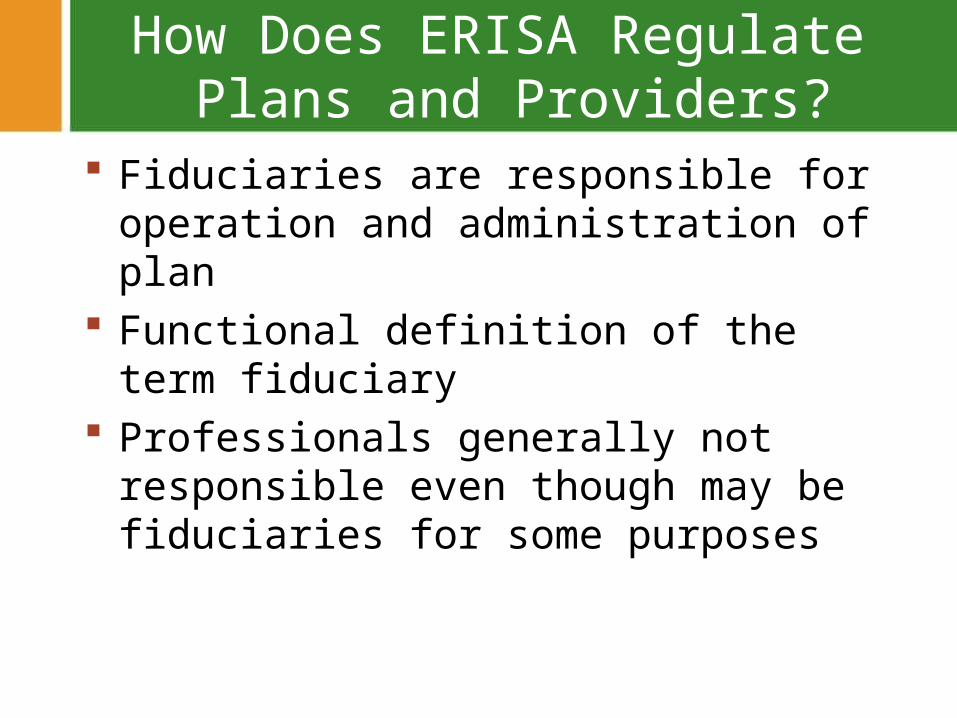

How Does ERISA Regulate Plans and Providers?

Fiduciaries are responsible for operation and administration of plan

Functional definition of the term fiduciary Professionals generally not responsible

even though may be fiduciaries for some purposes

Presentation Title

© 2010 Fox Rothschild

How Does ERISA Regulate Service Providers

ERISA §406(a)(1)(C) generally prohibits a plan fiduciary from engaging a “party in interest” to furnish goods or services to the plan (“Prohibited Transactions”)

A “fiduciary” is a person with discretionary authority or who provides investment advice for a fee

A “party in interest” includes persons providing services to the plan.

Presentation Title

© 2010 Fox Rothschild

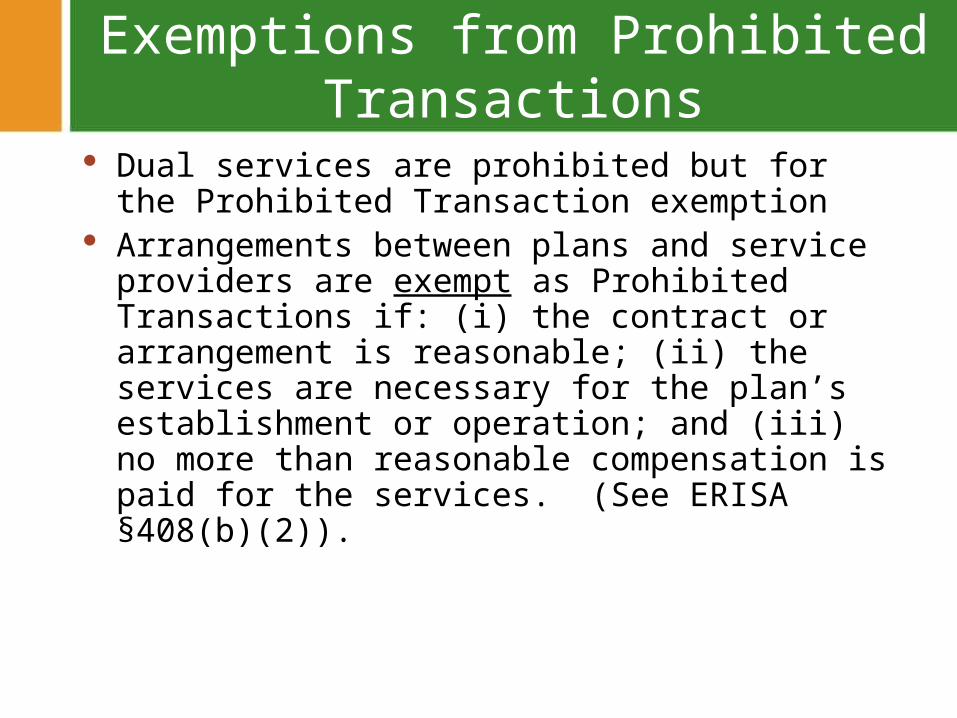

Exemptions from Prohibited Transactions

Dual services are prohibited but for the Prohibited Transaction exemption

Arrangements between plans and service providers are exempt as Prohibited Transactions if: (i) the contract or arrangement is reasonable; (ii) the services are necessary for the plan’s establishment or operation; and (iii) no more than reasonable compensation is paid for the services. (See ERISA §408(b)(2)).

Presentation Title

© 2010 Fox Rothschild

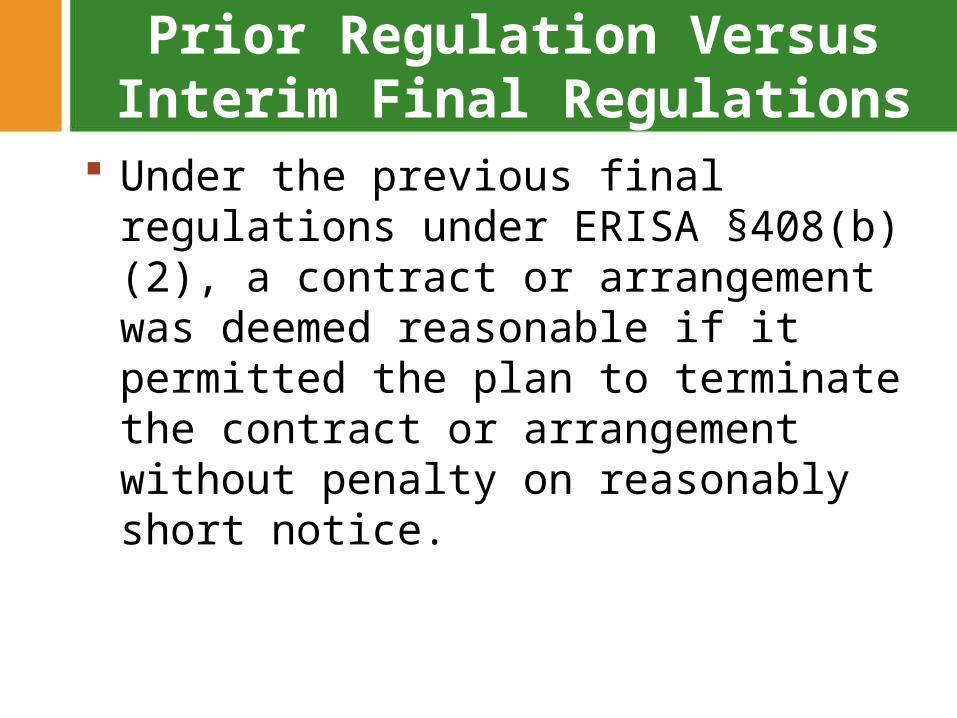

Prior Regulation Versus Interim Final Regulations

Under the previous final regulations under ERISA §408(b)(2), a contract or arrangement was deemed reasonable if it permitted the plan to terminate the contract or arrangement without penalty on reasonably short notice.

Presentation Title

© 2010 Fox Rothschild

Department of Labor Regulations

The Department of Labor’s Employee Benefits Security Administration recently issued interim final regulations (Labor Reg. §2250.408b-2(c)) that require information disclosures by certain ERISA plan service providers

Presentation Title

© 2010 Fox Rothschild

Purpose of Final Regulations

The purpose of the final regulations is to assist plan fiduciaries in assessing the reasonableness of contracts or arrangements, compensation, and any potential conflicts of interest.

Using power as an advisor/fiduciary to increase/maintain compensation

Presentation Title

© 2010 Fox Rothschild

More Stringent Provider Requirements

The new interim final regulations impose more stringent information disclosure requirements on covered service providers to provide specified information to a “responsible plan fiduciary” for certain contracts and arrangements. If such disclosures are not made, the contracts or arrangement will fail to be reasonable and thus, will not be exempt as a Prohibited Transaction.

Presentation Title

© 2010 Fox Rothschild

INTERIM FINAL REGULATION REQUIREMENTS

Covered Plan: The final regulations apply only to “covered plans” which include most employer–sponsored plans,

Not SEPs, SIMPLE plans, or IRAs (or Welfare Plans)

Presentation Title

© 2010 Fox Rothschild

Covered Service Provider

Covered Service Provider: A “covered service provider” is a service provider that enters into a contract or arrangement with the covered plan and reasonably expects to receive $1,000 or more in compensation, directly or indirectly, from the Plan.

No formal contract is required

Presentation Title

© 2010 Fox Rothschild

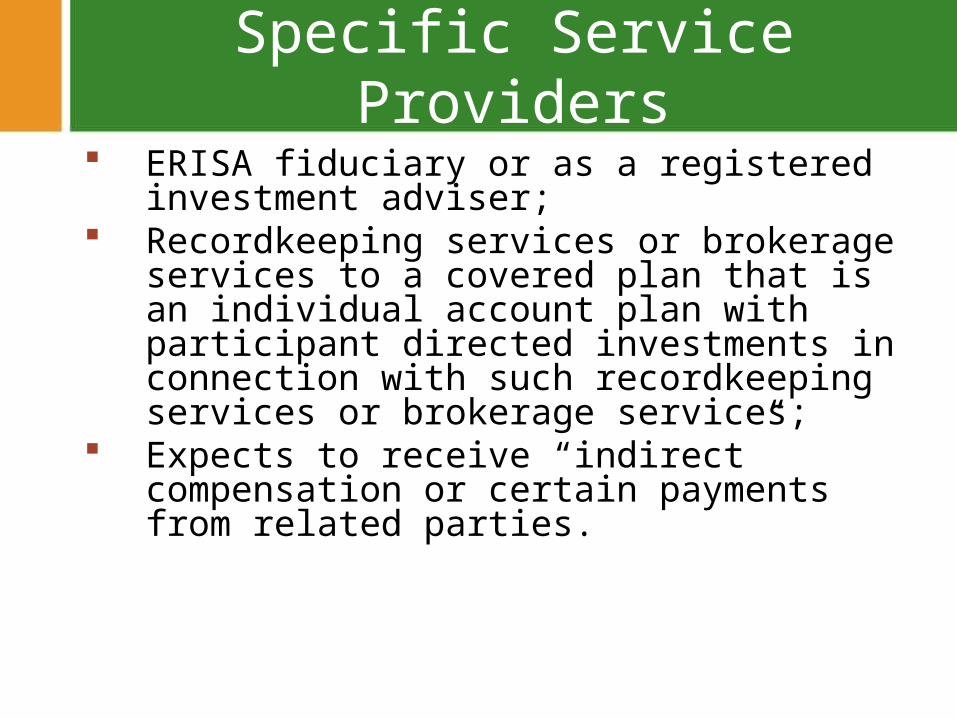

Specific Service Providers

ERISA fiduciary or as a registered investment adviser;

Recordkeeping services or brokerage services to a covered plan that is an individual account plan with participant directed investments in connection with such recordkeeping services or brokerage services;

Expects to receive “indirect” compensation or certain payments from related parties.

Presentation Title

© 2010 Fox Rothschild

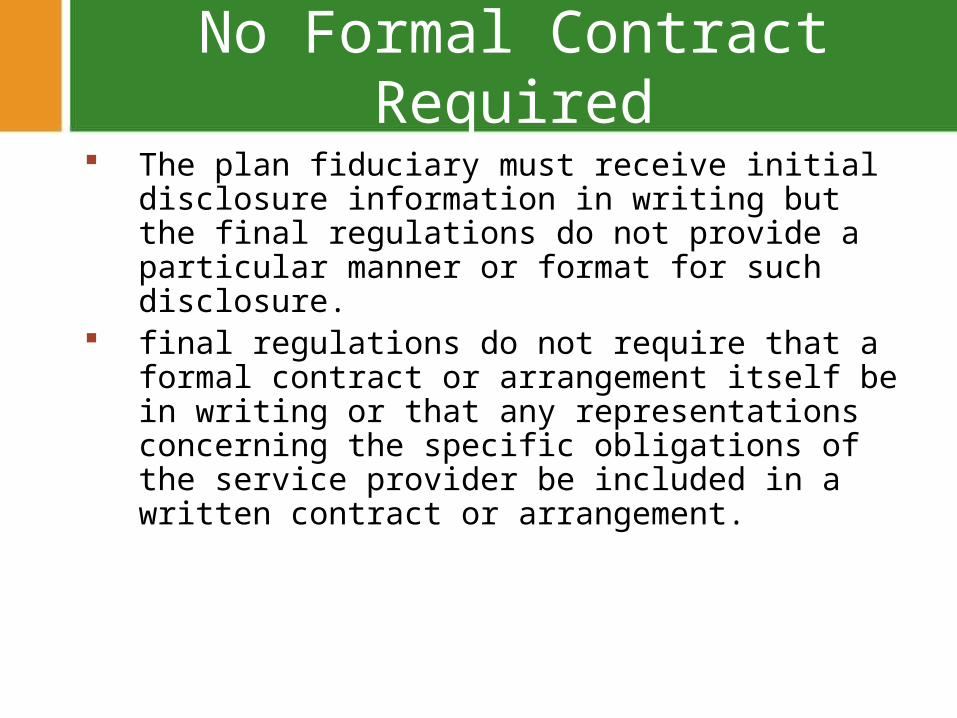

No Formal Contract Required

The plan fiduciary must receive initial disclosure information in writing but the final regulations do not provide a particular manner or format for such disclosure.

final regulations do not require that a formal contract or arrangement itself be in writing or that any representations concerning the specific obligations of the service provider be included in a written contract or arrangement.

Presentation Title

© 2010 Fox Rothschild

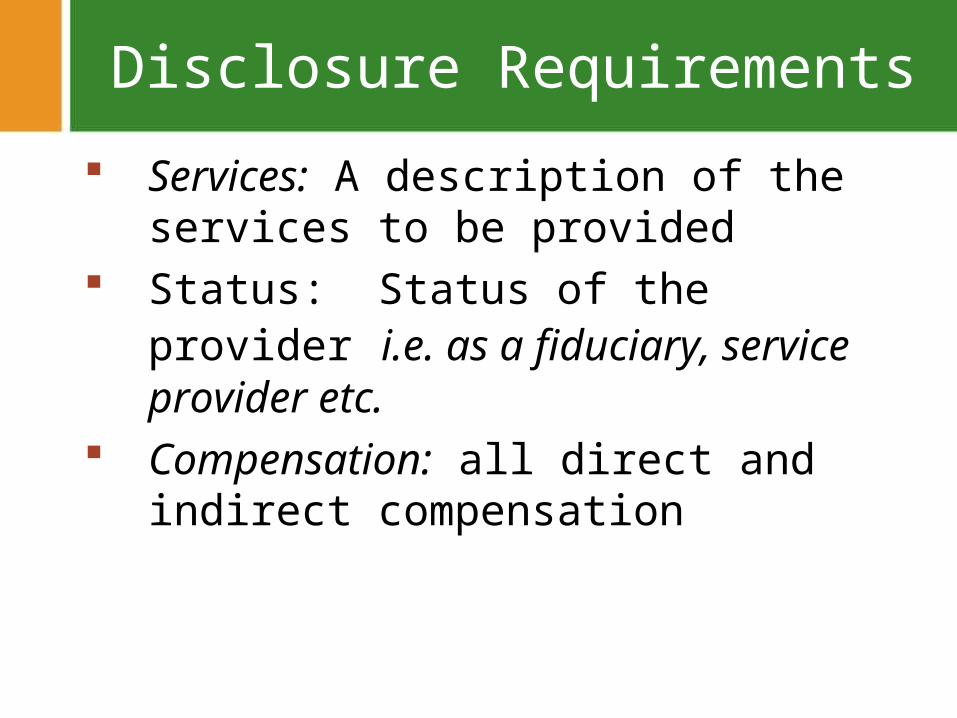

Disclosure Requirements

Services: A description of the services to be provided

Status: Status of the provider i.e. as a fiduciary, service provider etc.

Compensation: all direct and indirect compensation

Presentation Title

© 2010 Fox Rothschild

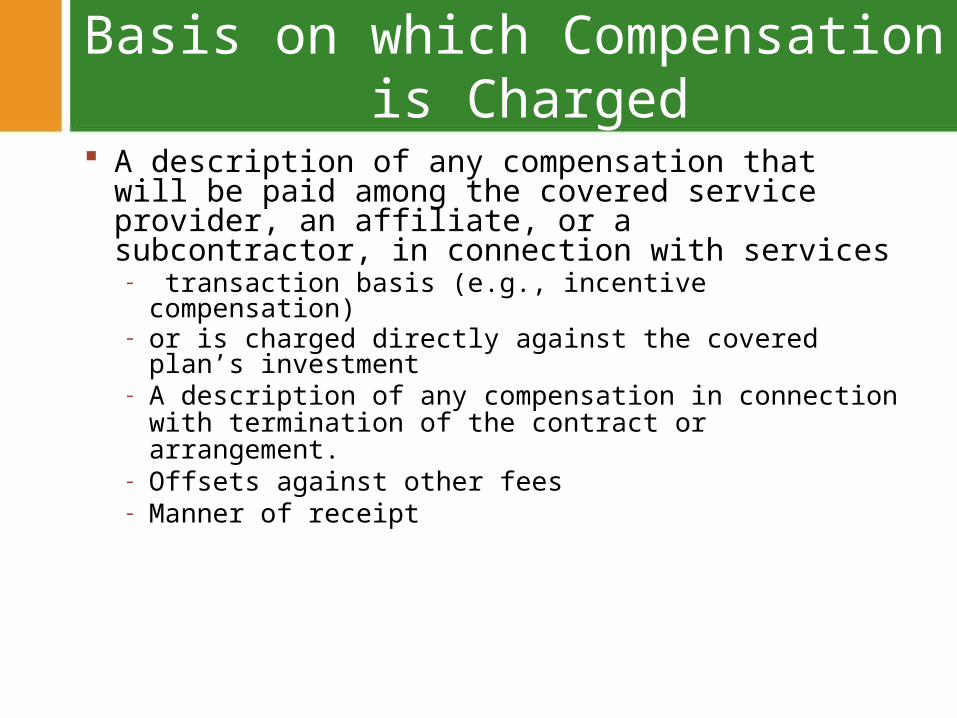

Basis on which Compensation is Charged

A description of any compensation that will be paid among the covered service provider, an affiliate, or a subcontractor, in connection with services - transaction basis (e.g., incentive compensation) - or is charged directly against the covered plan’s

investment- A description of any compensation in connection

with termination of the contract or arrangement. - Offsets against other fees- Manner of receipt

Presentation Title

© 2010 Fox Rothschild

Example – Fiduciary Investment Services

Fiduciaries for investment vehicles holding plan assets must provide additional information :

- any compensation charged directly against the amount invested in connection with the acquisition, sale, transfer or withdrawal from the investment contract, etc.;

- the annual operating expenses if the return is not fixed; and

- any ongoing expenses in addition to annual operating expenses.

Presentation Title

© 2010 Fox Rothschild

Disclosure - Timing The initial disclosure information must be provided

reasonably in advance of the date the contract is entered into and extended or renewed.

Any changes to the initial disclosure information must be provided as soon as practicable but no later 60 days from the date the service provider is informed of such changes.

Service providers are required to provide, upon request any other information that is required for the covered plan to comply with the reporting and disclosure requirements of Title I of ERISA and its regulations.

Presentation Title

© 2010 Fox Rothschild

Fiduciary Burdens

New Regulations will become effective 2012

Plan Fiduciaries now will have information concerning fee arrangements and how fees are computed and imposed

No excuse for failure to negotiate appropriate fees

Participant disclosure required

Presentation Title

© 2010 Fox Rothschild

Fiduciary Risk – Participant Litigation

Hecker vs. Deere. Participants charged Deere violated its fiduciary duty by providing investment options that charged excessive fees and failed to adequately disclose the fee structure to participants.

Wal-mart sued by their participants in 2008, which has gained the support of the DOL And most recently the case against

Caterpillar which agreed to pay $16.5 million to settle charges that the company violated its fiduciary duty by offering options with “excessive fees’ and concealed administration costs.

Presentation Title

© 2010 Fox Rothschild

Conclusion – New Burden

No easy answers – burden on plan fiduciaries

Look for providers whose fees are transparent

Review fees and expenses carefully No one size fits all

Presentation Title

© 2010 Fox Rothschild

Contact Information

Harvey m. Katz, Esq.

212.878.7976

![Presentation copy[2] - Fox Rothschild · 2017-01-23 · " Bath Salts" Prescription Psycho- stimulants: Amphetamine Methylphenadate Cylert Dexadrine Diet pills Mood Altering Drugs](https://img.pdfslide.us/doc/110x75/5eca876b04448f469b1edf38/presentation-copy2-fox-rothschild-2017-01-23-bath-salts-prescription.jpg)