Embed Size (px)

Citation preview

Presentationon the Greek Real Estate

Investment Market

New York

Monday 30th October 2000

Agenda

• Greece in a European Economy

• Greece in European Property Market

• Greek Real Estate Market Overview

• Why invest in Greece?

Greece in a European Economy

GDP Growth

-5 0 5 10 15 20 25 30

Ireland

Poland

Finland

Hungary

Spain

N'lands

Greece

Portugal

Belgium

Sweden

Norway

UK

France

Denmark

Austria

Turkey

Swit'land

Germany

Italy

Russia

Czech Republic

Total Growth (%) over 1997-1999Source: Consensus Forecasts

European inflation

0

5

10

15

20

25

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Greece Italy Portugal Spain France UK

%

Source : OECD (1990-9), Consensus Forecasts (2000-1)

European interest rates

0

5

10

15

20

25

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Greece Italy Portugal Spain France UK

%

Source : OECD

Greek GDP growth and inflation

GDP growth (%)

Sources: OECD, Consensus Forecasts

-2

-1

0

1

2

3

4

5

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0

5

10

15

20

25

GDP Inflation

Inflation (%)

Greece in European Property Market

European Cross-BorderDirect Investment in Real Estate - by Origin

0 €2 €4 €6 €8 €

10 €12 €14 €16 €18 €20 €

Billions Euro

1997 1998 1999 2000

Ireland

Other

UK

Scandinavia

Far East

Netherlands

MiddleEast

Germany

N.America

Source DTZ Research

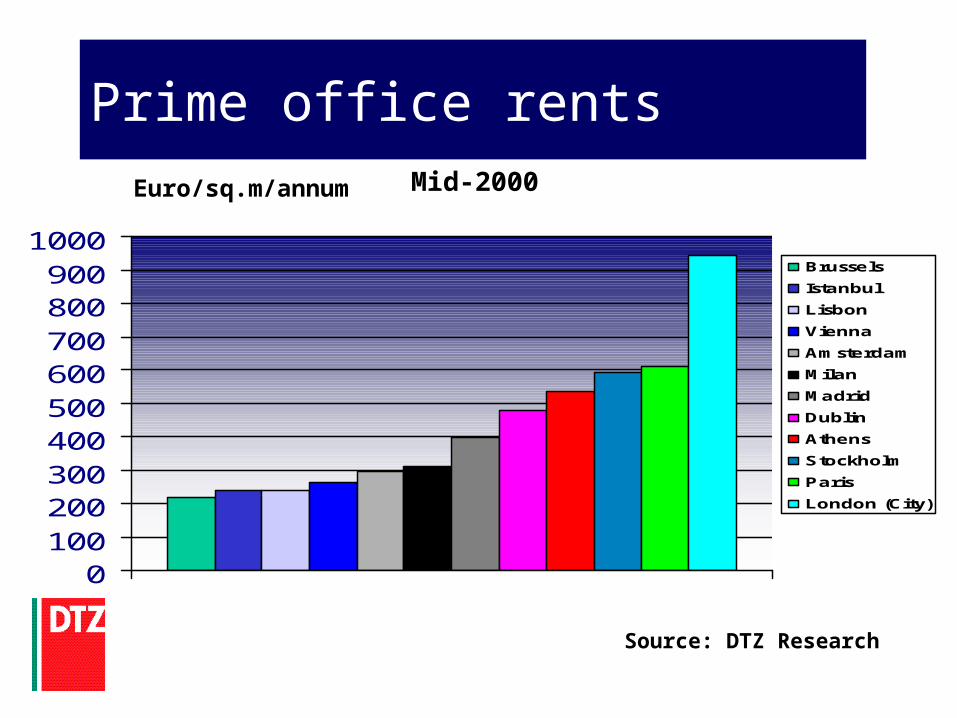

Prime office rents

0100200300400500600700800900

1000Brussels

Istanbul

Lisbon

Vienna

Amsterdam

Milan

Madrid

Dublin

Athens

Stockholm

Paris

London (City)

Mid-2000

Source: DTZ Research

Euro/sq.m/annum

European prime office yields (current)

0

12

34

5

67

89

10

%

Dublin

Madrid

Paris

Stockholm

Frankfurt

Milan

London (city)

Vienna

Amsterdam

Brussels

Lisbon

Athens

Mid-2000

Source: DTZ Research

European office yield trends

0

2

4

6

8

10

12

14

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 mid-2000

%

Paris

Athens

Milan

Rome

Barcelona

Madrid

Lisbon

London

Source: DTZ Research

0 50 100 150 200 250 300 350

Greece

Belgium

Italy

Germany

Portugal

Switzerland

Spain

EU AVERAGE

Austria

Eire

UK

France

N'lands

Sweden

Source : Various

Gross Lettable Area (sq.m) per 1,000 inhabitants

European shopping centre density 1999

Greece Real Estate Market Overview

A Changing Market

• Entry to Euro-Zone – Jan 2001

• Lowering of interest rates

• Infrastructure Projects

– New Airport

– Greater Athens Ring Road and other road projects

– Expansion of Metro System

• 2004 Olympic Games and associated projects

• Legal Framework and securitisation through mutual funds

Characteristics

• Traditionally owner-occupied• High State ownership – although increasing

disposals through privatisations • Immature Investment Market• Historical lack of transparency and information• Currently increasing interest from domestic and

international investors.

The Attica market

Development opportunities

• Central Athens undersupplied with quality product• Urban regeneration in Central Athens and Pireaus.• Demand for large spaces cannot be satisfied • Development activity continues in prime locations.• New Airport - Mesoghia Valley• Olympic Games in 2004 and associated infrastructure

projects• Interest from major foreign players: Chelverton, Lend

Lease, Sonae, TrizecHahn, Rodamco, Hindes• East Coast of Attica – expansion of ports

Source: DTZ Research

Why Invest in Greece?

International Real Estate Cycle

Source: Deutsche Bank Real Estate Private Equity

Why invest in Greece ?

• Entry into the Euro in Jan 2001• High rate of economic growth• Reducing interest rate• Widening yield gap between bonds and real estate returns• Major EU Investment Program• Olympic Games 2004• Substantial Infrastructure Improvements• Positive rental growth prospects• Legal framework becoming more ‘investor friendly’ • Indirect property investment vehicles emerging in mutualisation• Sale and leaseback opportunities• Emerging market performance within the EU

Source: DTZ Research